By Ovi

All of the Crude plus Condensate (C + C) production data for the US state charts comes from the EIAʼs Petroleum Supply monthly PSM which provides updated production information up to March 2025.

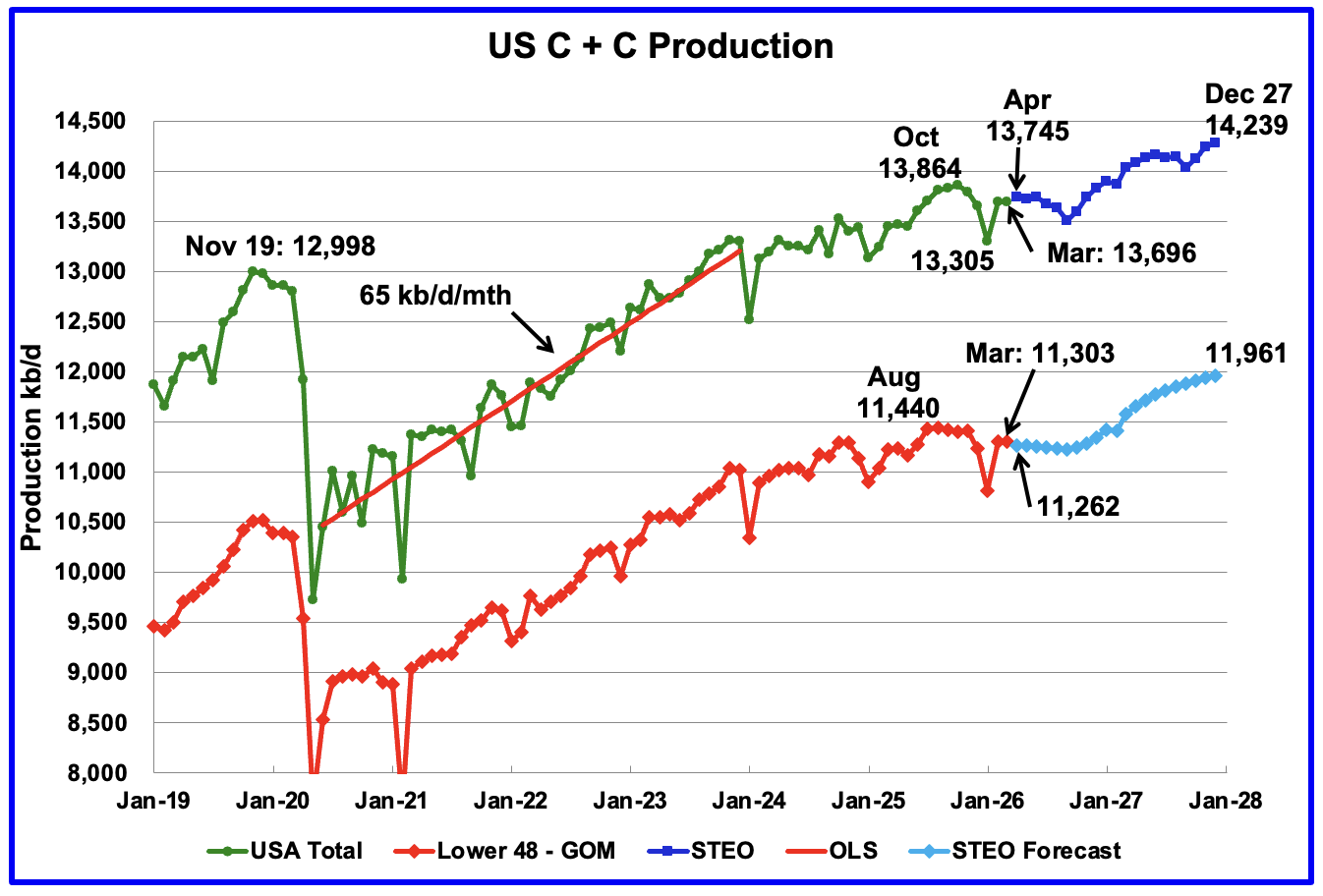

U.S. March oil production decreased by 1 kb/d to 13,696 kb/d and is down by 168 kb/d from October 2025. The largest decrease came from TX. April production is expected to rise by 49 kb/d to 13,745 kb/d according to the May STEO. Peak US oil production occurred in October 2025 at 13,864 kb/d but may be exceeded in early 2027, according to the STEO forecast.

The dark blue graph, taken from the May 2026 STEO, is the U.S. oil production forecast from April 2026 to December 2027. Output for December 2027 is expected to rise to 14,239 kb/d, upwardly revised by 82 kb/d from last month. From April 2026 to December 2027 U.S. oil production is expected to increase by 494 kb/d.

The light blue graph is the STEO’s forecast for the Onshore L48 output to December 2027. March Onshore L48 production increased by 2 kb/d to 11,303 kb/d. From March 2026 to December 2027 production is expected to increase by 658 kb/d to 11,961 kb/d, upwardly revised by 69 kb/d. The rising production starting in Octoberber 2026, according to the EIA, is due to expected higher prices for WTI and more NG pipelines being built. Note how production is essentially flat out to November 2026.

U.S. Oil Production Ranked by State

Listed above are the 10 US states with the largest oil production along with production from the Gulf of Mexico.

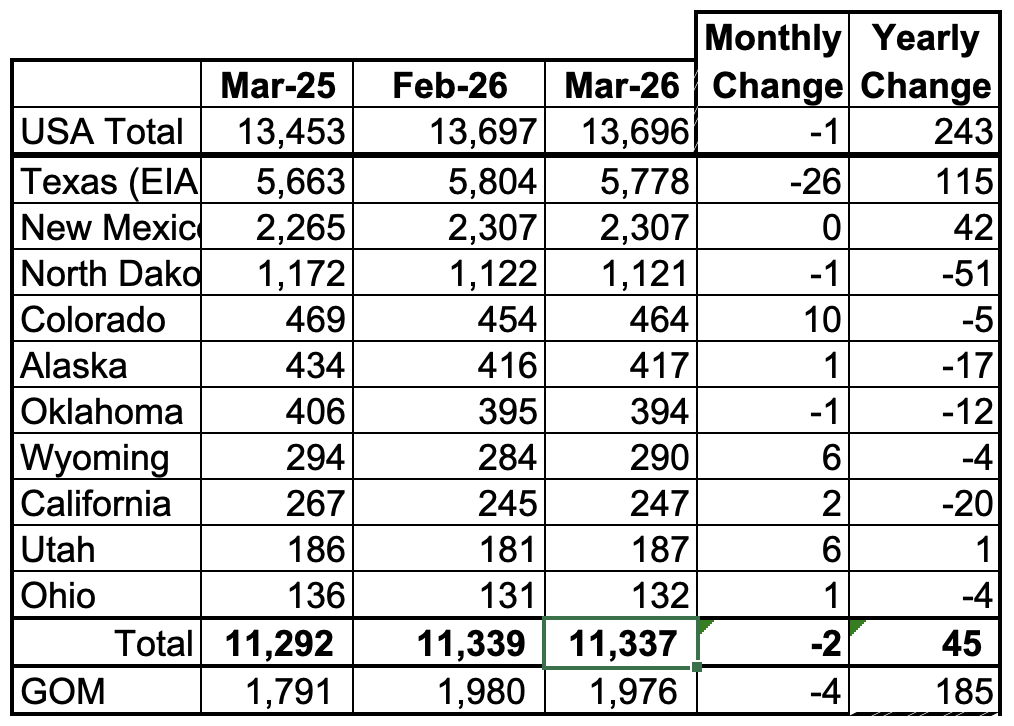

These 10 states accounted for 82.8% of all U.S. oil production out of a total production of 13,696 kb/d in March 2026. On a MoM basis, March oil production in these 10 states dropped by 2 kb/d. On a YoY basis, US overall production increased by 243 kb/d with the largest contributors being Texas and New Mexico and the largest decliner being North Dakota.

State Oil Production Charts

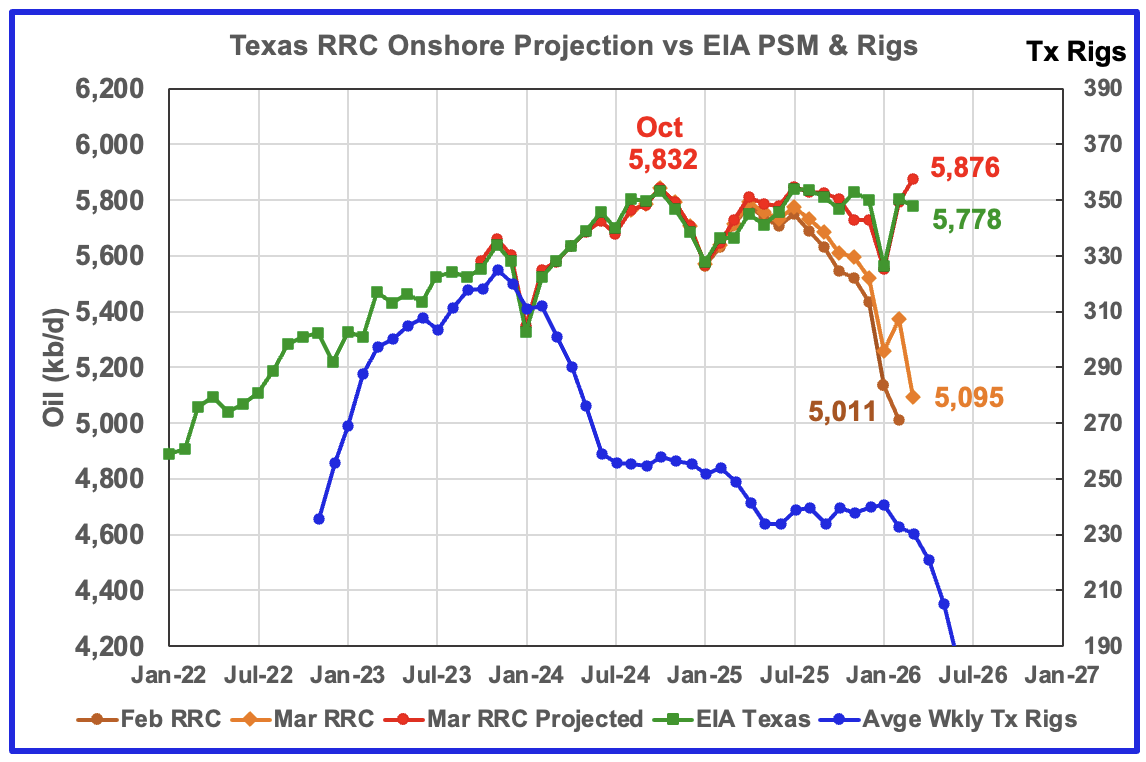

Texas’ March oil production decreased by 26 kb/d to 5,778 kb/d according to the EIA. YoY production rose by 115 kb/d.

The Texas’ RRC initial production for March dropped by 279 kb/d from February to 5,095 kb/d. The projection added 781 kb/d to raise March projected production to 5,876 kb/d. While the projection is very close for January and February, the March projection is showing an increase. The divergence is due to large upward revisions to February production in the March report which results in an optimistic projection.

The red graph is a production projection using the preliminary February and March Texas RRC data.

The blue graph shows the average number of weekly rigs reported for each month shifted forward by 10 months. So the 276 rigs operating in July 2023 have been shifted forward to May 2024. From February 2024 to July 2024, the rig count dropped from 312 in time shifted February 2024 to 256 in July 2024. That drop of 56 rigs had little impact on production up to July 2025. August 2025 appears to be the first month when the impact of the start of the flat rig count results in essentially flat production. Will the dropping rig count starting in time shifted February/March 2026 result in dropping Texas production going forward?

According to the EIA, New Mexico’s March production was unchanged at 2,307 kb/d. YoY production rose by 42 kb/d, second only to Texas.

The red graph shows the projected output up to March and is calculated using the preliminary February and March NM OCD data. March’s projected production decreased by 8 kb/d from February to 2,249 kb/d and is 58 kb/d or 2.5 % lower than the EIA’s reported March production. While the EIA and projection numbers are slightly different, the trend is the same.

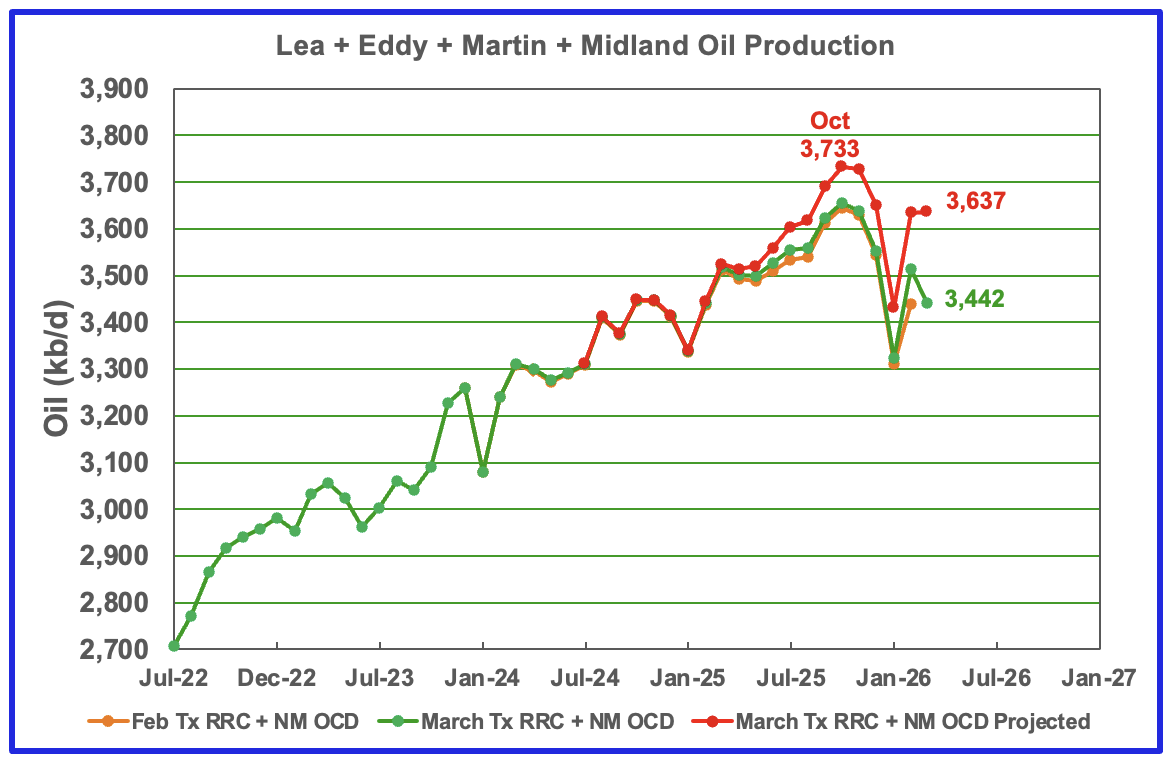

Production in Lea County and Eddy County offset each other with Lea rising and Eddy dropping. See Permian section further down.

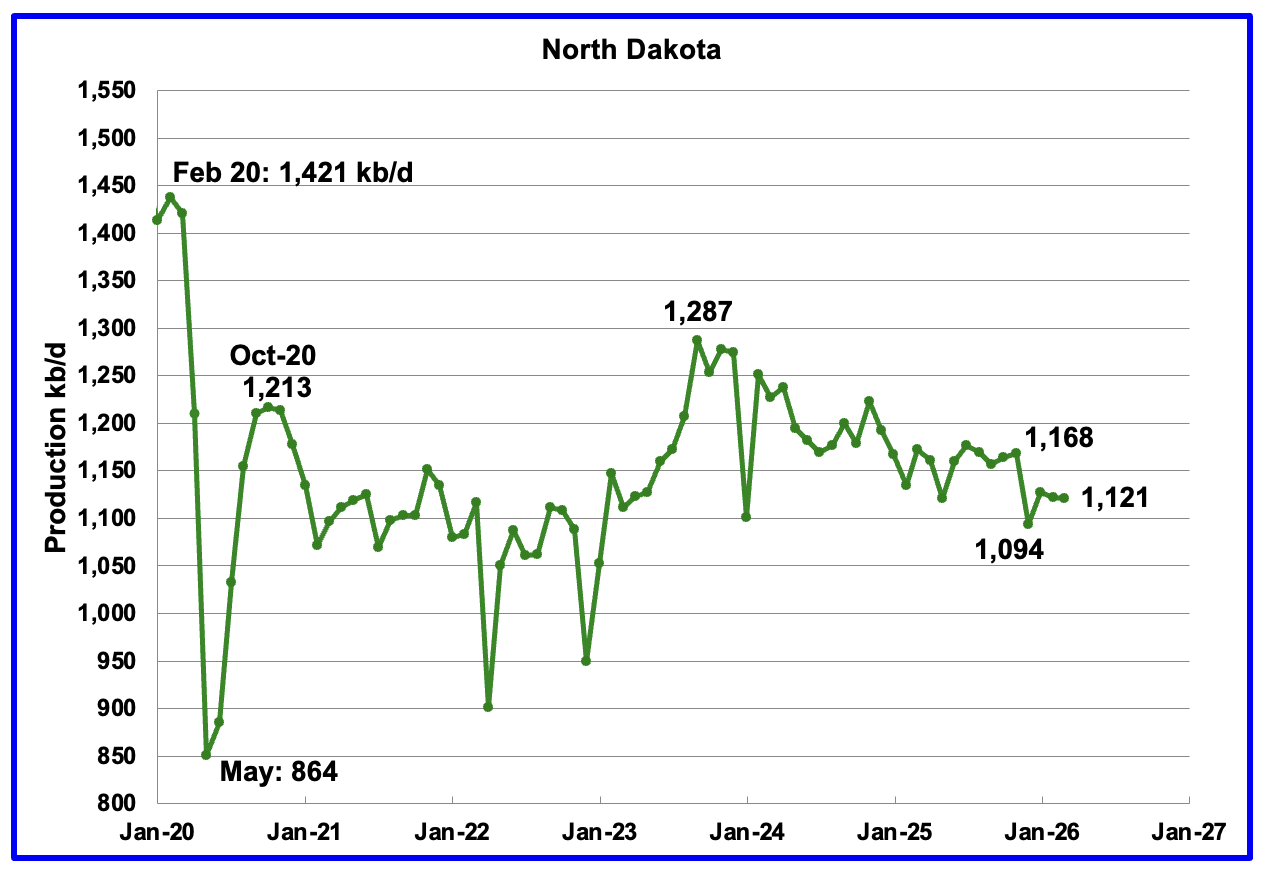

Production in North Dakota dropped by 1 kb/d in March to 1,121 kb/d, according to the EIA. March 2026 production is 51 kb/d lower than last March.

The North Dakota Department of Mineral resources reported March production increased by 9 kb/d to 1,143 kb/d, which is 22 kb/d higher than the EIA’s estimate.

According to this Article, U.S. oil operators in North Dakota are moving cautiously on ramping up drilling despite a sharp rise in oil prices.

“U.S. oil operators in North Dakota are moving cautiously on ramping up drilling despite a sharp rise in oil prices driven by the Iran war, as companies wait to see if higher prices will last long enough to justify new investment, the state’s regulator said on Friday.

While elevated prices have improved near-term fundamentals, most producers are sticking to budgets set at the end of last year, limiting any immediate jump in drilling activity, Mark Bohrer, assistant director of the Oil and Gas Division at the state’s Industrial Commission, said. However, output could edge higher in the near term as more wells are completed and some drilling activity picks up.

Harold Hamm, chief executive of Continental Resources, which helped pioneer fracking in North Dakota’s Bakken basin, plans to put drilling crews back to work after a temporary pause announced in January, local media reported. ConocoPhillips COP.N, EOG Resources EOG.N and Diamondback Energy FANG.O are also diverting resources to drill new wells or expand existing ones, mainly in the Permian basin, to take advantage of the price environment.”

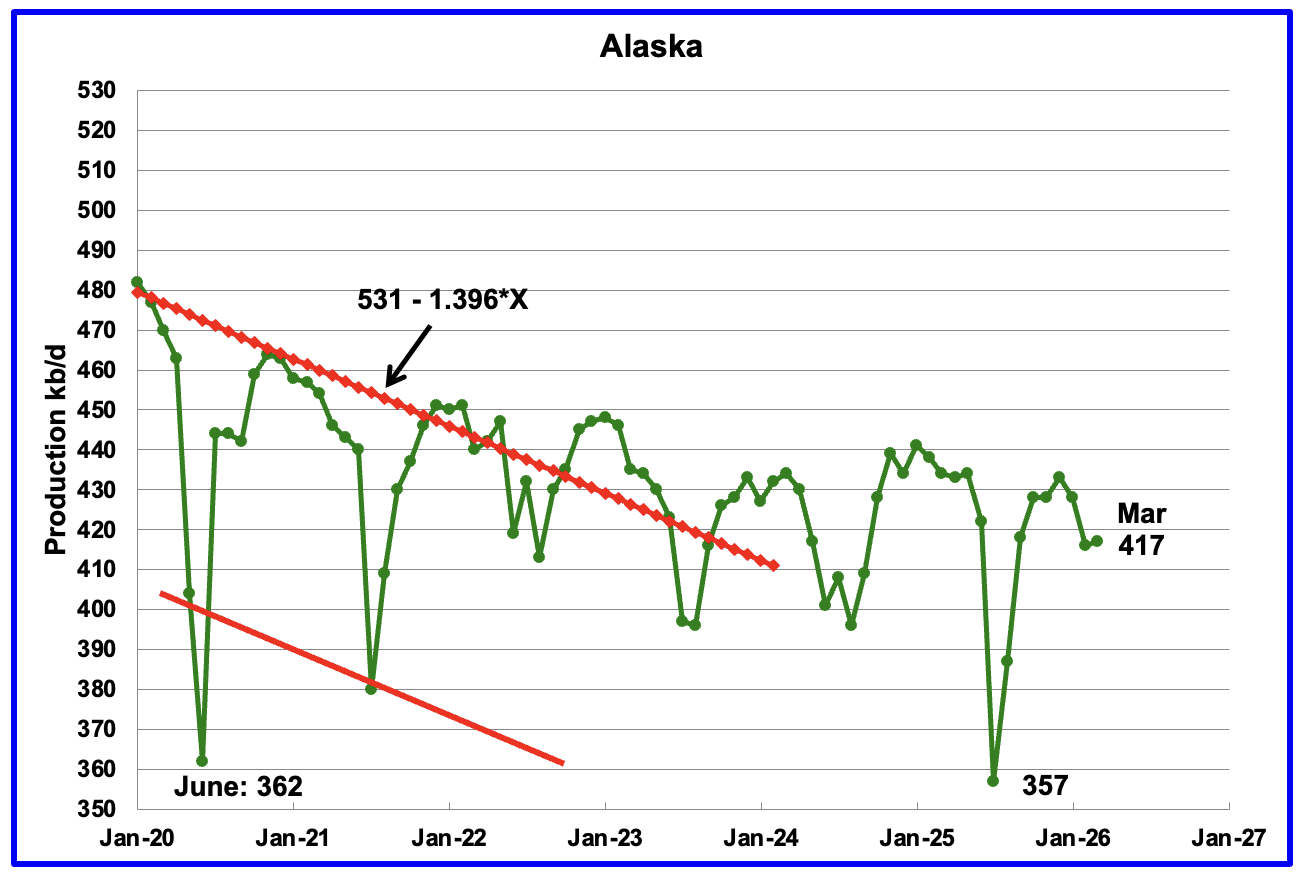

Alaskaʼs March output rose by 1 kb/d to 417 kb/d while YoY production decreased by 17 kb/d. The EIA’s weekly report for March indicated that March production would average close to 420 kb/d.

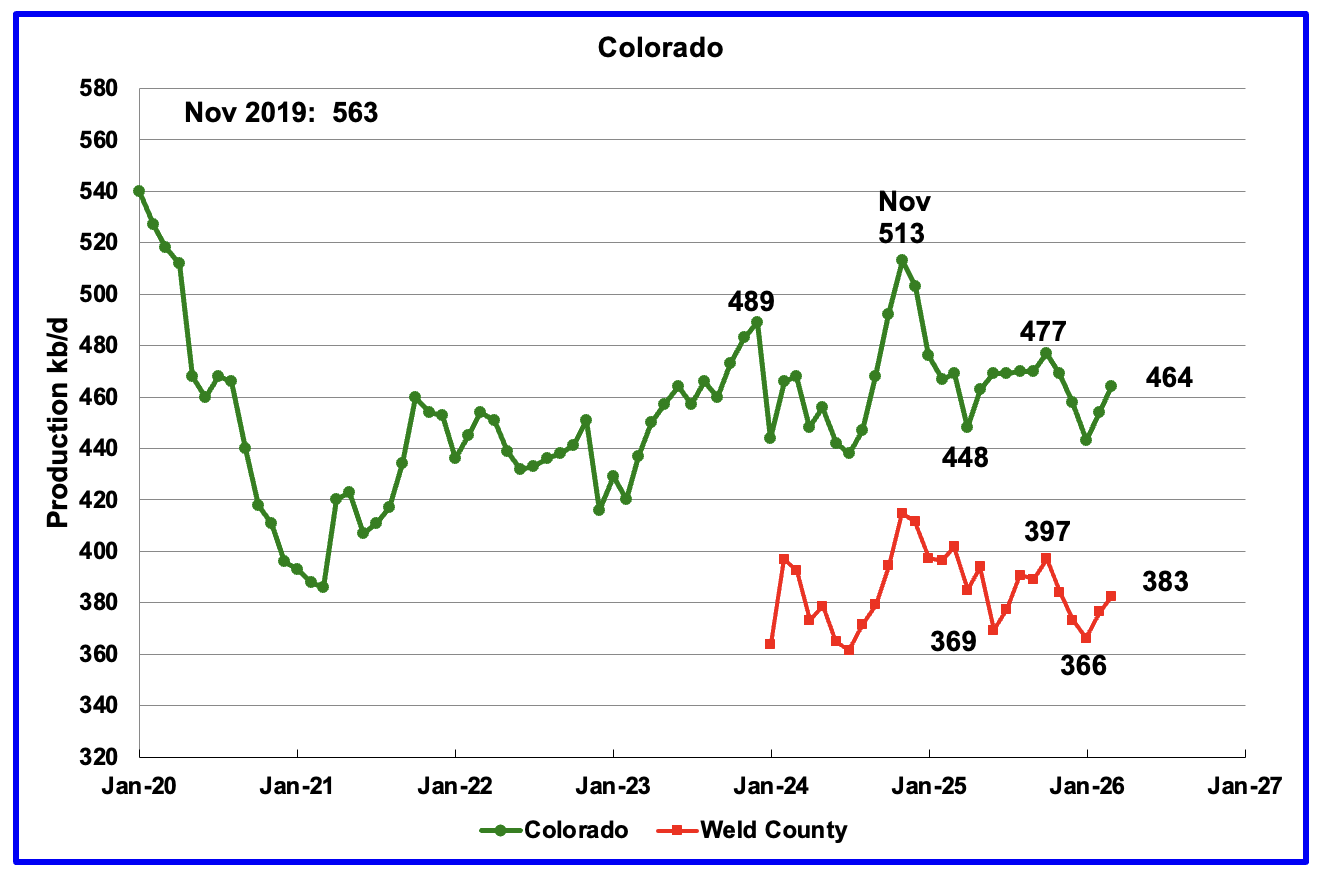

Coloradoʼs March oil production rose by 10 kb/d to 464 kb/d.

The biggest oil producing county in Colorado is Weld County and its production has been added to the chart. The two graphs have almost been parallel over the last six months. Weld’s production rose by 6 kb/d in March to 383 kb/d.

Colorado began 2026 with 7 rigs in January and they rose to 8 rigs in late May. Of the 8 rigs, 6 were stationed in Weld county.

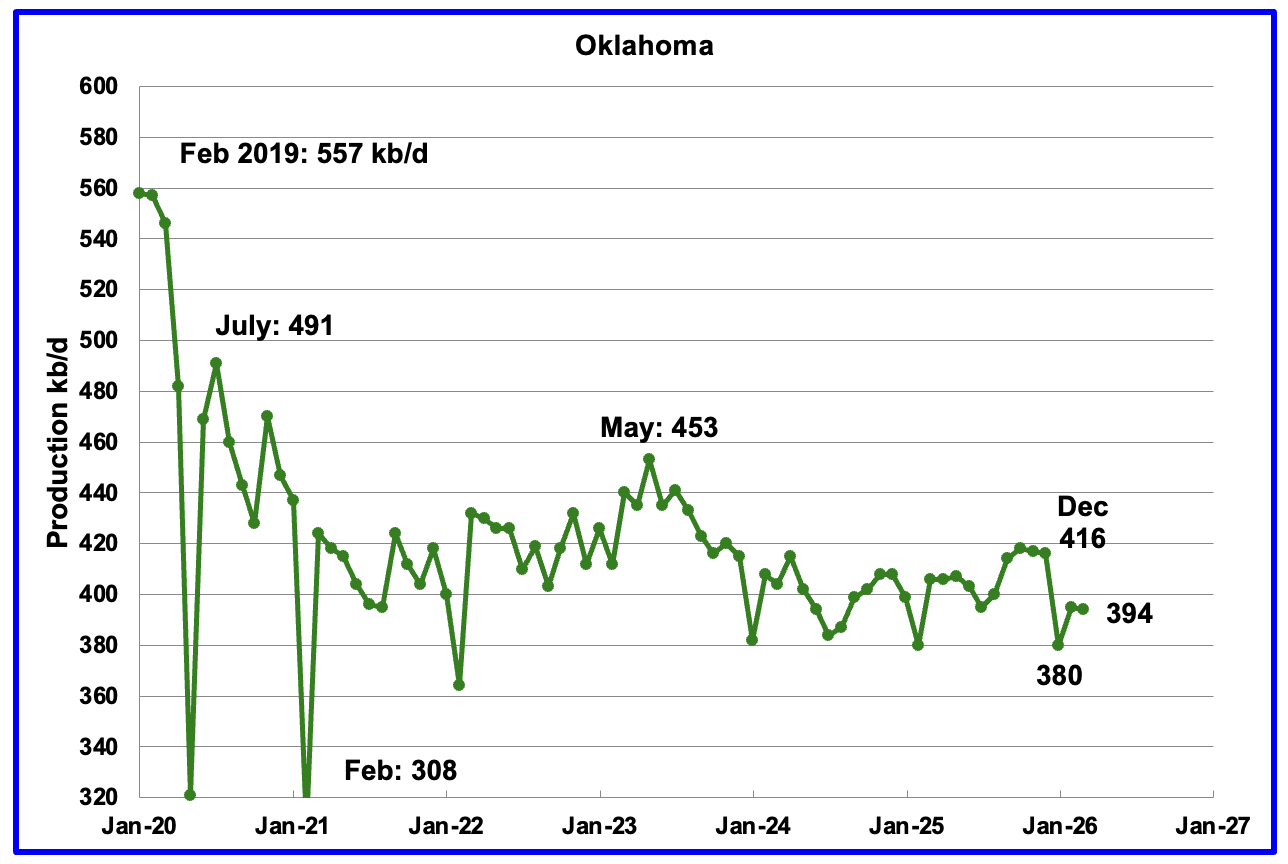

March oil production dropped by 1 kb/d from February to 394 kb/d.

Oklahoma’s January output dropped by 36 kb/d to 380 kb/d. Production remains below the post pandemic July 2020 high of 491 kb/d and is down by 59 kb/d since May 2023. The large drop out of the 400 kb/d ± 20 kb/d range may be due to the late January extreme weather.

Oklahoma had 51 operational rigs in May 2025 which slowly dropped to 41 rigs in July 2025. The rig count has been fairly steady around 41 from July 2025 to May 2026. The steady rig count since July 2025 may be showing up in the steady oil production around 400 kb/d.

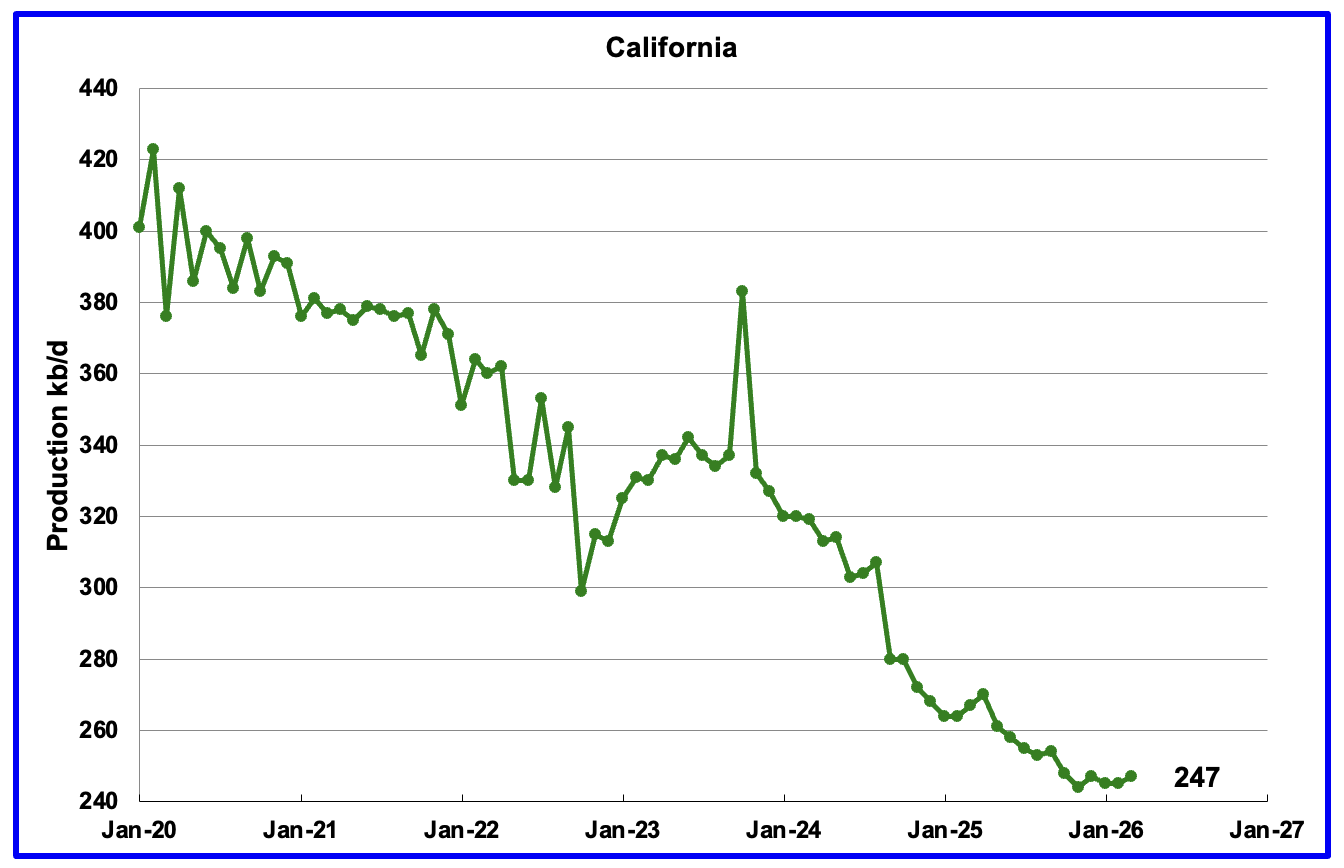

California’s overall declining production trend continues. However March production rose by 2 kb/d to 247 kb/d. YoY production dropped by 20 kb/d.

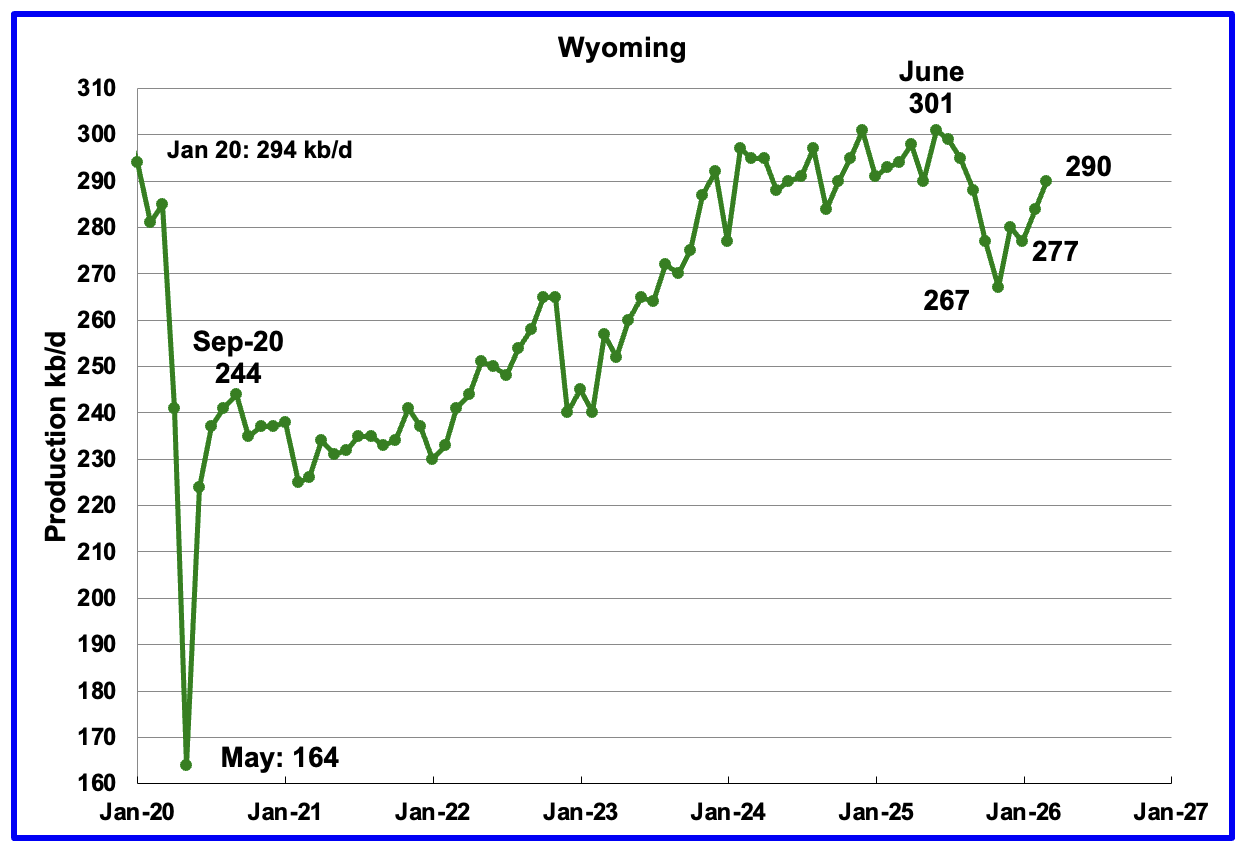

Wyoming’s oil production reached a post pandemic high in June 2025 of 301 kb/d. Production dropped in each of the subsequent 5 months before rebounding in December. March production rose by 6 kb/d to 290 kb/d.

Wyoming started the year with 13 rigs and in May also had 13 operational rigs.

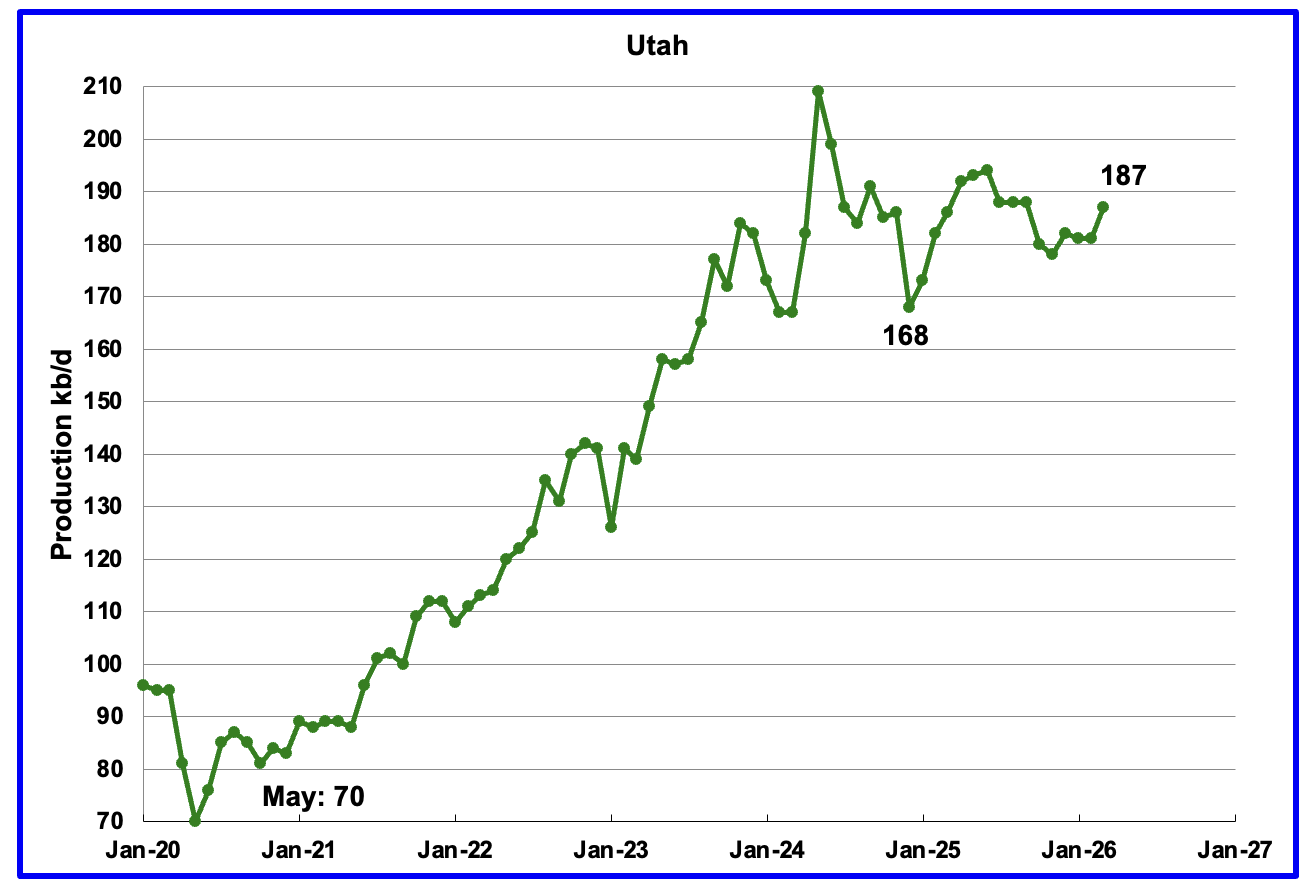

March production rose by 6 kb/d to 187 kb/d. Utah had 11 rigs operating in late January. In May, the number of operational rigs had dropped to 8.

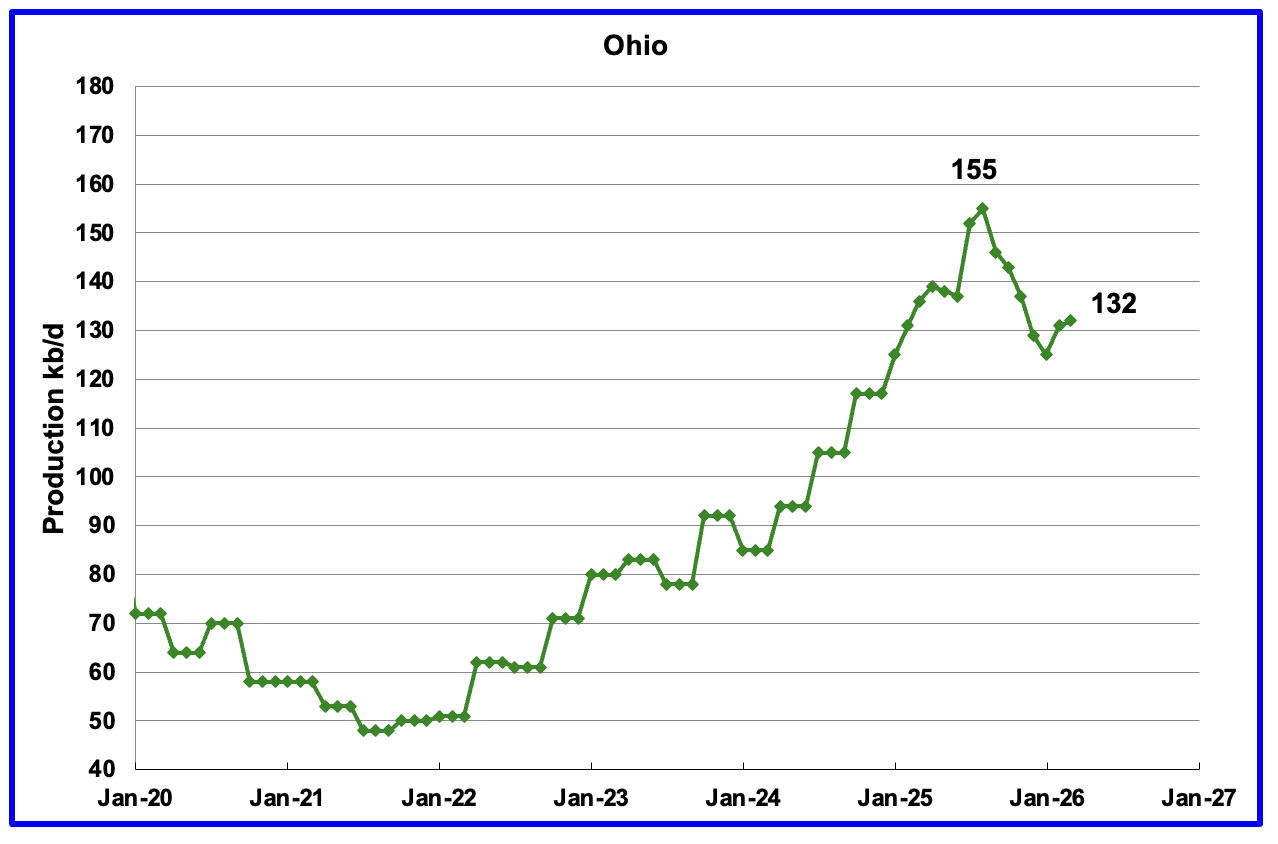

Ohio’s March oil production increased by 1 kb/d to 132 kb/d and was 23 kb/d lower than the August peak of 155 kb/d. In January 2026 Ohio had 12 NG rigs operating. At the end of May, nine NG rigs were operational along with one oil rig.

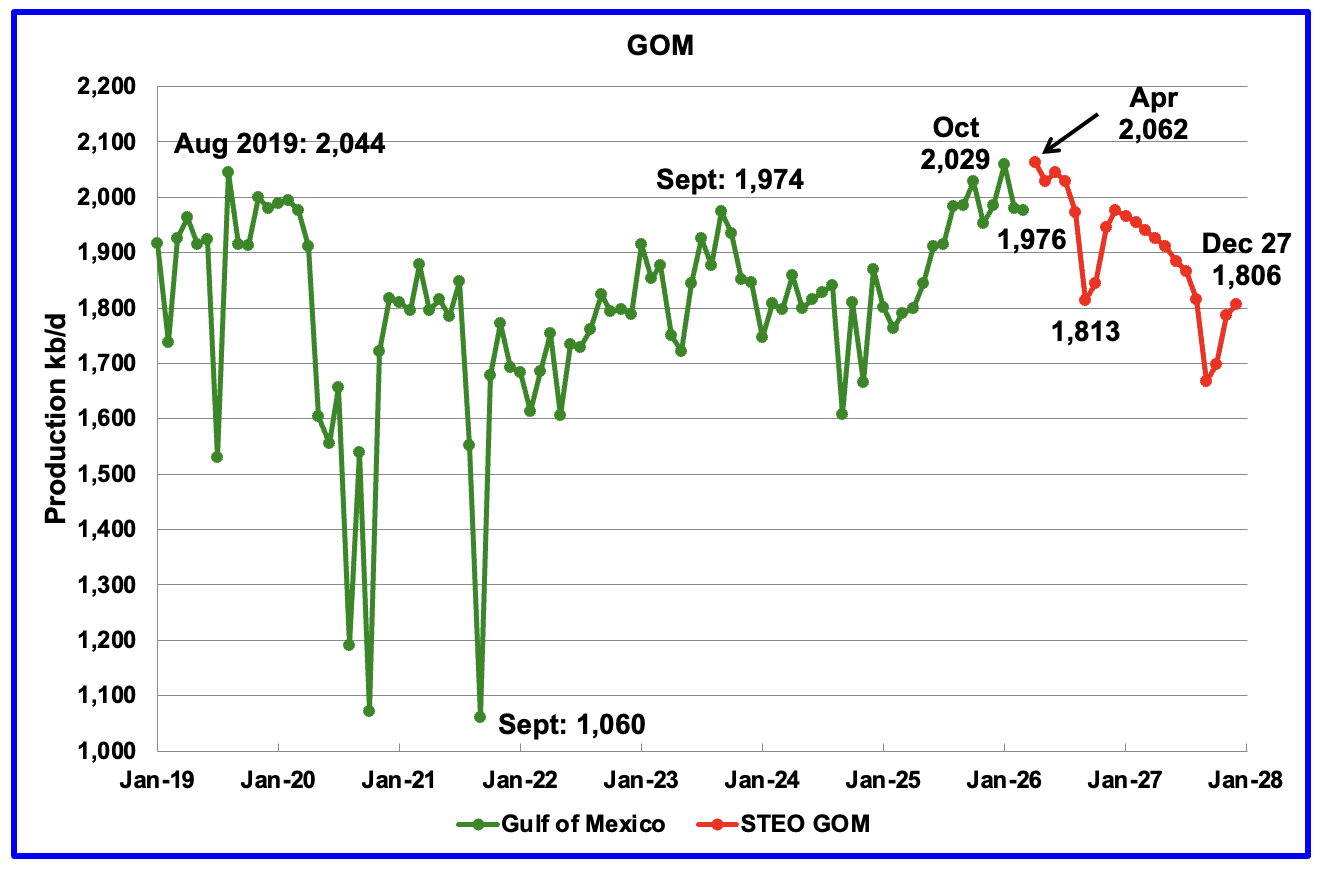

GOM production dropped by 4 kb/d in March to 1,976 kb/d. It is up by 185 kb/d YoY.

The May 2026 STEO GOM projection has been added to this chart. For April production is projected to increase to 2,062 kb/d. If the projection is correct, April production will be a new high, exceeding the August 2,019 high by 18 kb/d. It also projects production in December 2027 will be 256 kb/d lower than April 2026 at 1,806 kb/d.

A Different Perspective on US Oil Production

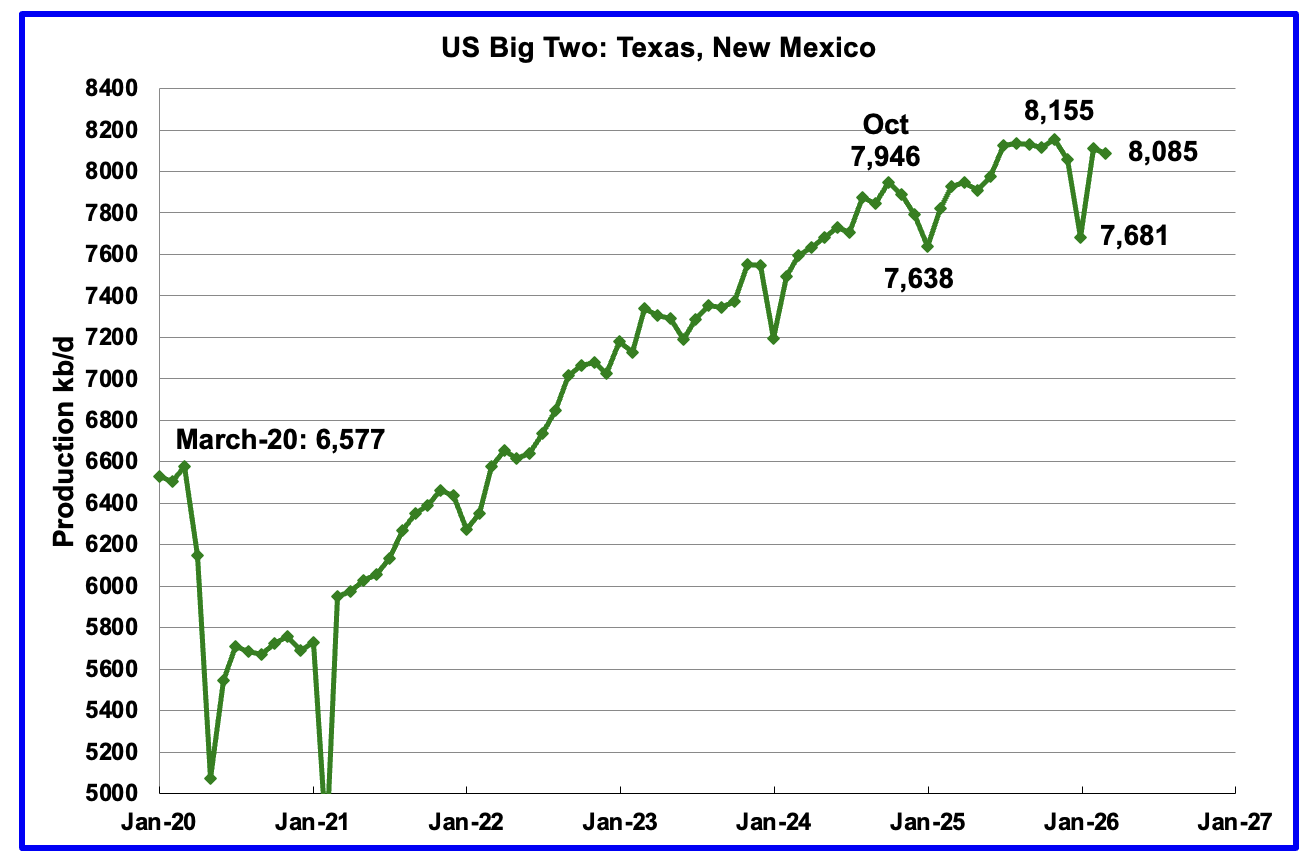

Combined Oil output for the Big Two states Texas and New Mexico.

March production in the Big Two states decreased by a combined 26 kb/d to 8,085 kb/d. The decrease was all due to a production drop in Texas while New Mexico production was flat. Clearly these two states were the drivers of US oil production growth up to July 2025. The essentially flat production starting in August 2025 was the first sign that production in these two states was close to peaking. The next few months will determine whether these two states have reached peak production.

Oil Production by The Rest

March oil production by The Rest rose by 28 kb/d to 3,218 kb/d and is 268 kb/d lower than November 2023. The remaining states may have entered a slowly decline phase.

Permian Basin Report for Main Counties and a District

This special monthly Permian section was added to the US report because of a range of views on whether Permian production will continue to grow or will peak over the next year or two. The issue was brought into focus many months back by two Goehring and Rozencwajg Reports and Report2 which indicated that a few of the biggest Permian oil producing counties were close to peaking or past peak.

A more recent report was issued and can be reviewed Here. In this report they state:

“For years now, we have outlined with what we hoped was clarity, and what we now submit was prescience, the view that U.S. shale oil, that great source of modern supply, could not grow forever. It would mature, crest, and begin its long descent. That moment, by our models and measures, has arrived: shale has plateaued, and 2024 appears to be its high-water mark. And yet, investor sentiment has scarcely been more downbeat.”

This section will focus on the four largest oil producing counties in the Permian, Lea, Eddy, Midland and Martin. It will track the oil and natural gas production and the associated Gas Oil Ratio (GOR) on a monthly basis. The data is taken from the state’s government agencies for Texas and New Mexico. Typically the data for the latest two or three months is not complete and is revised upward as companies submit their updated information. Note the natural gas production shown in the charts that is used to calculate the GOR is the gas coming from both the gas and oil wells.

Of particular interest will be the charts which plot oil production vs GOR for a county to see if a particular characteristic develops that indicates the field is close to entering or in the bubble point phase. While the GOR metric is best suited for characterizing individual wells, counties with closely spaced horizontal wells may display a behaviour similar to individual wells due to pressure cross talking . For further information on the bubble point and GOR, there are a few good thoughts on the intricacies of the GOR in an earlier POB comment and here. Also check this EIA topic on GOR.

New Mexico Permian

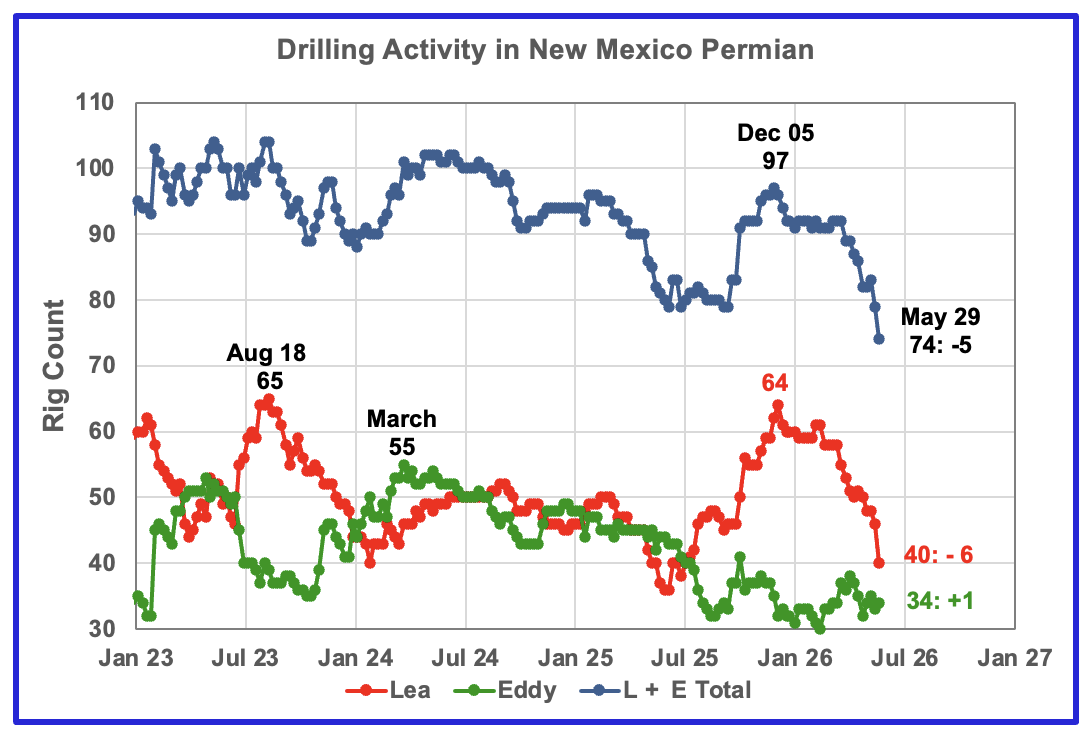

The rig counts in both Lea and Eddy counties have started to decline over the last 8 weeks. Over the past five months Lea County dropped 24 rigs to 40 while Eddy dropped 4 rigs from 38 in April to 34 in May. Overall NM dropped 23 rigs to 74 from December 2025 to late May 2026. Will the dropping rig counts show up in dropping production in a few months?

Oil Production in New Mexico’s Primary Permian Counties

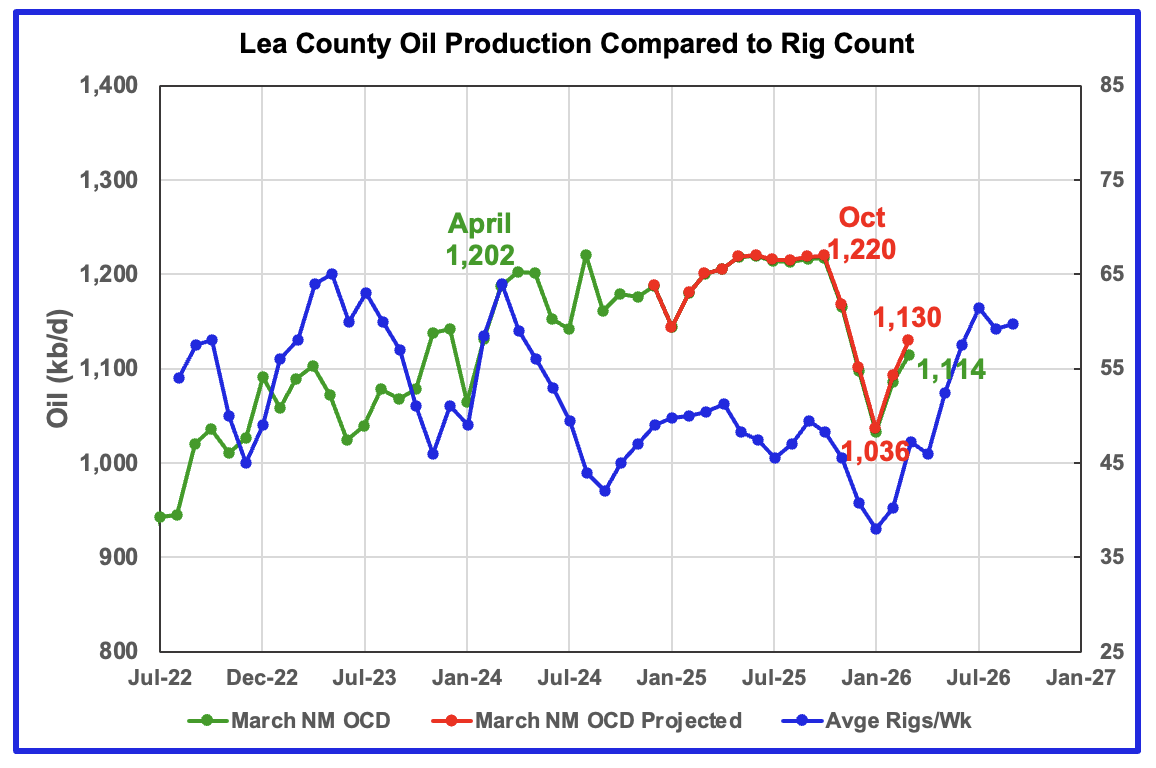

Lea County’s oil production started its plateau phase in April 2024 at 1,202 kb/d and it continued to October 2025. November 2025 to January 2026 have seen steady production drops in both the projected and NM OCD’s preliminary production. However the majority of January’s projected production drop of 65 kb/d was due to the severe January weather. February projected production rebounded and came in at 1,093 kb/d, revised down from 1,123 kb/d in the previous post.

March projected production increased by 37 kb/d to 1,130 kb/d. It now appears more likely that the projected production increase in February and March are related to the time shifted increasing rig count and to some storm related recovery. The question/issue here is whether production will exceed the October 2025 peak of 1,220 kb/d or peak at a new lower level?

Preliminary March data from New Mexico’s Oil Conservation Division (OCD) indicates Lea County’s March oil production rose by 28 kb/d to 1,114 kb/d, green graph.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly rig data. The rig graph has been shifted forward by 7 months. So the 64 Rigs/wk operating in August 2023 have been time shifted forward to March 2024 to show the possible correlation and time delay between rig count, completion and oil production.

Note that rig counts are being used to project production as opposed to completions because state completion data is not available. Completion data from the Drilling Productivity report below indicates that the number of completed DUCs slightly exceeds newly drilled wells in the Permian basin.

According to this Article, Devon Energy has recently acquired land in Lea and Eddy counties. The acquisition cost $2.6B or $161,500 per net acre and adds approximately 400 net locations normalized to 2-mile laterals, with expected strong well economics and low breakevens.

The cost for each of the 400 wells is $6.5M. Is this a good deal? According to this Article: “The price is “eye watering compared to historical M&A in the Permian,” RBC Capital Markets analyst Scott Hanold said in a note. The leases are mainly in three sections of the basin that have no existing development, and one is near Devon’s best-performing asset, Hanold said.

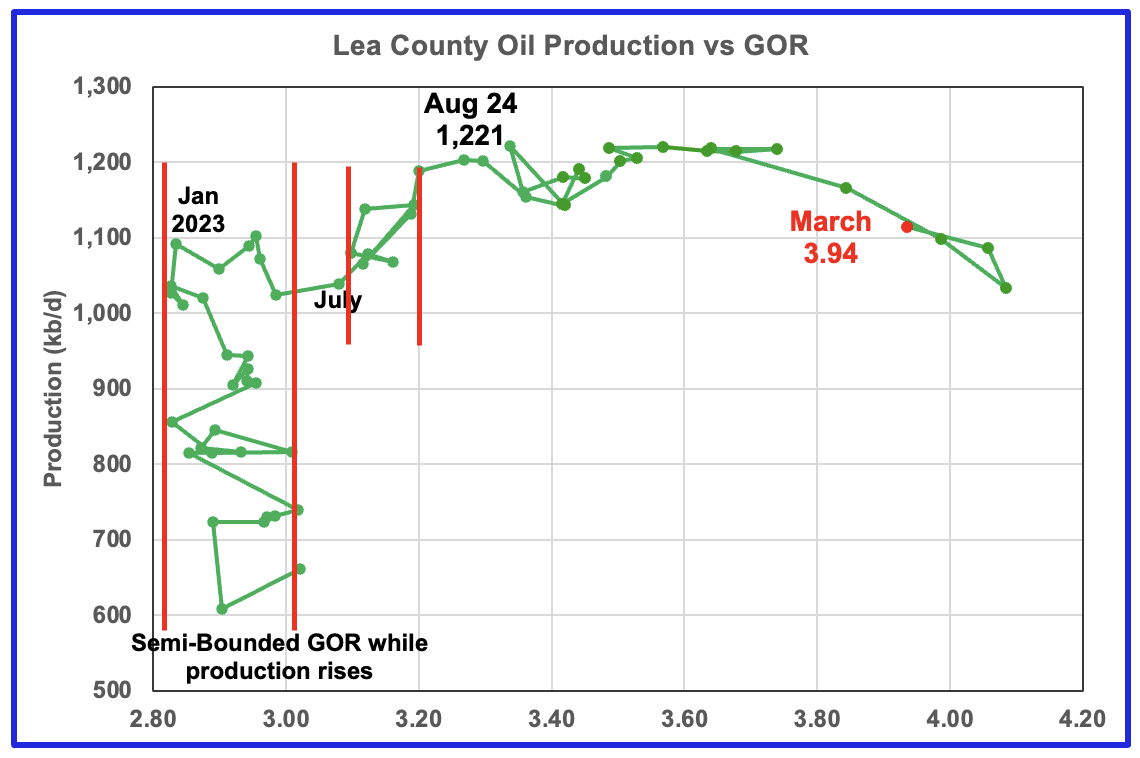

After much zigging and zagging, oil production in Lea county stabilized just below 1,100 kb/d in early 2023. Once production reached a new high in January 2023, production appeared to be on a plateau while the GOR started to increase rapidly to the right and first entered the bubble point phase in July 2023.

Since July 2023 Lea County’s production continued to increase as the GOR remained within a second semi-bounded region. This may indicate that additional production was coming from an oilier part of a layer since the GOR’s behaviour since August 2023 to March 2024 time frame appears once again to be in a second semi bounded GOR phase accompanied with rising production.

The GOR moved out of the second semi-bounded GOR region in April 2024 and production hit a new high of 1,221 kb/d in August 2024. From August 2024 to February 2025 the GOR was range bound between 3.34 and 3.53 but starting in June 2025 the GOR started to rise every month, except for one, to hit new highs. February and March saw a double change in direction, both a production increase and a GOR decrease to 3.94, which may be consistent with rising production.

This zigging and zagging GOR pattern within a semi-bounded GOR while oil production increases to some stable level and then moves out to a higher GOR to the right has shown up in a number of counties. See a few additional cases below. The rising GOR to new highs and dropping oil production in Lea county is an early indicator that production may be entering a declining phase.

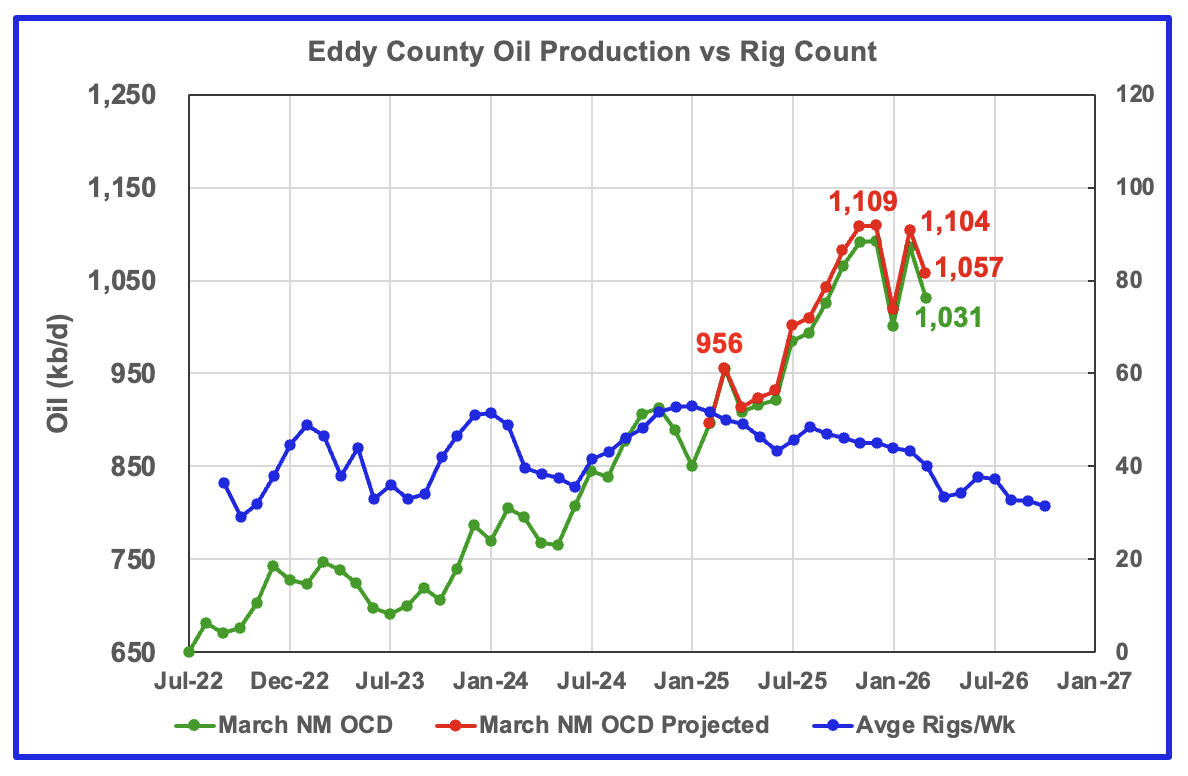

Eddy’s March projected oil production decreased by 47 kb/d to 1,057 kb/d while preliminary production from the NM OCD decreased by 55 kb/d to 1,031 kb/d. Most of the February production rise was due to a rebound from the severe January weather. If the storm had not occurred, January production would have been closer to 1,100 kb/d.

March production along with upward revisions to previous months indicates that Eddy county may have peaked in December 2025. The dropping rig count starting in time shifted September 2025 may have finally shown up in falling production in March. November, December and February projected production formed a plateau. The March production drop by 47 kb/d to 1,079 kb/d may have ended the plateau.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the above weekly drilling chart. The rig graph has been shifted forward by 8 months to roughly coincide with the increase in the production graph starting in October/November 2023.

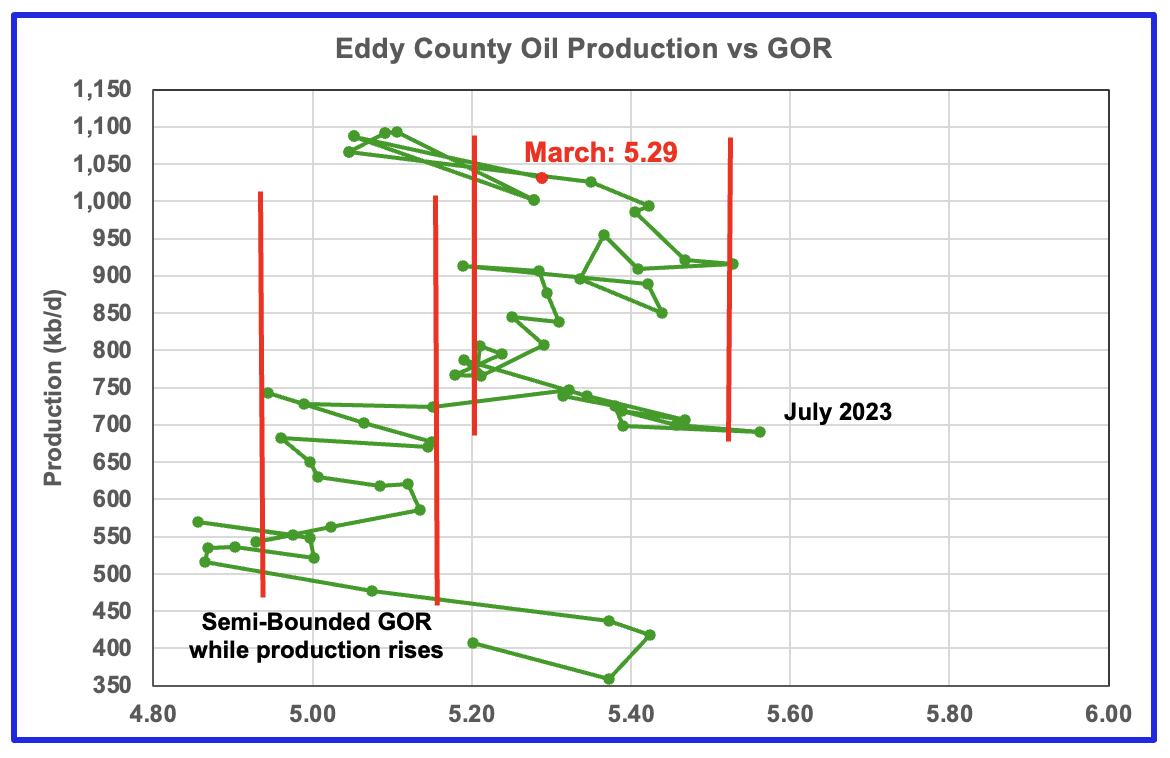

The Eddy county GOR pattern is similar to Lea county except that Eddy broke out from the first semi bounded range earlier and then added a second wider semi-bounded GOR phase.

For March New Mexico’s Oil Conservation Division (OCD) reported preliminary oil production decreased by 55 kb/d to 1,031 kb/d while the GOR rose to 5.29 and moved back into the second Semi-Bounded GOR range.

Texas Permian

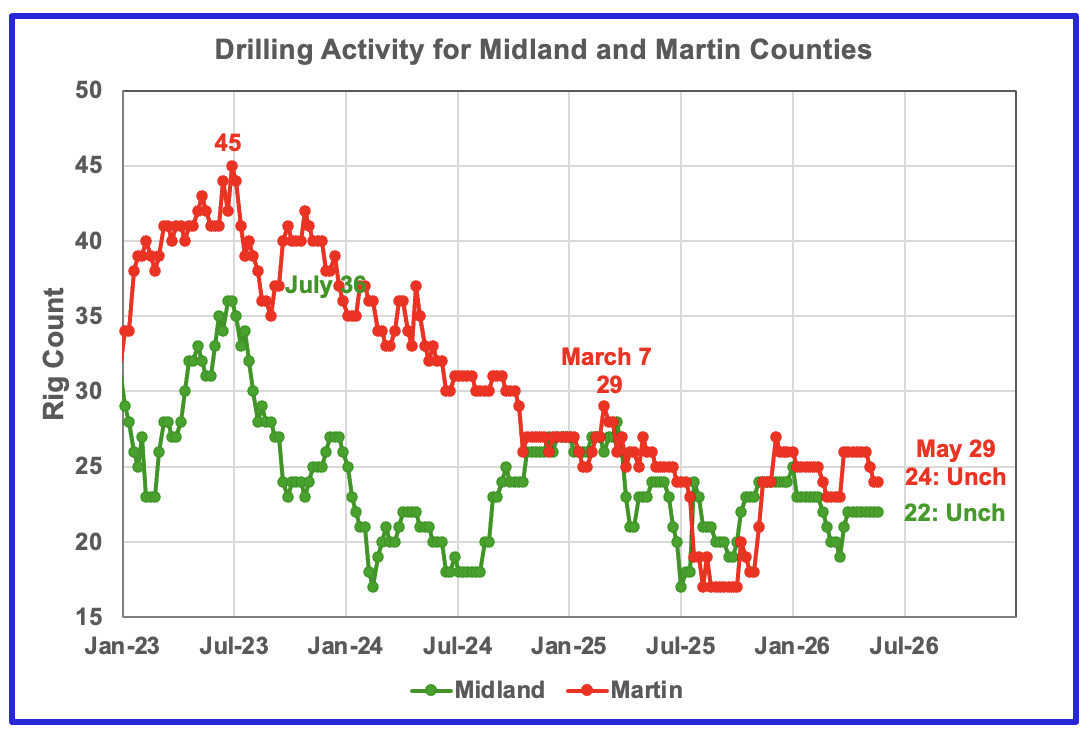

The rig count in Midland county has remained unchanged for the last seven weeks while Martin county reduced its rig count from 26 to 24 over the last few weeks in May.

Oil Production in the Two Primary Texas Permian Counties

Comparison Chart from previous post.

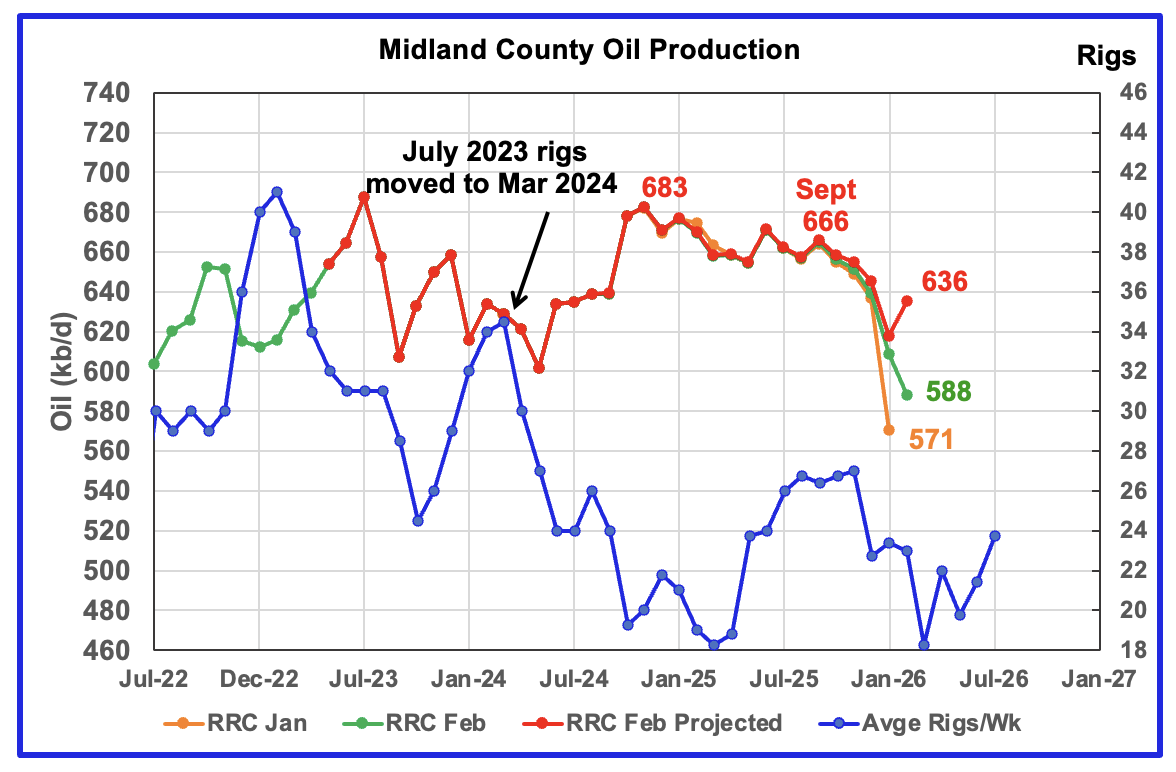

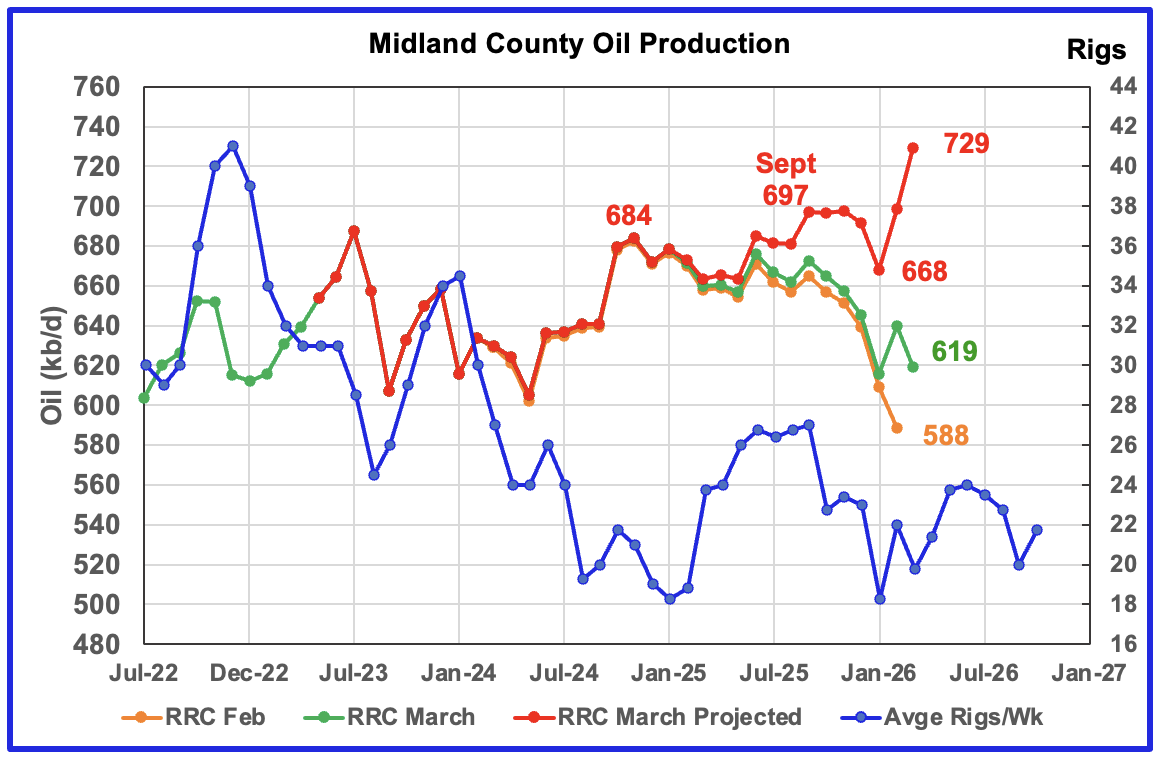

March projected production rose by 30 kb/d to 729 b/d. The February rise is due to the production rebound from the severe Texas winter storm in late January. With the rig count rising in time shifted February and March from the January low, the February and March increases may be directionally correct. However combining the sharp drop in the time shifted October 2025 to January 2026 rig count along with the dropping preliminary RRC March production along with the large February gap between the orange and green graphs makes me think that Midland’s March oil production is Overly Optimistic.

Compare the projected production for September 2025 in the preceding comparison chart with the current one. Production has increased by 31 kb/d from 666 kb/d to 697 kb/d. The increase is due to the atypical large upward revisions to the February production in the March RRC report. Hopefully April will clarify Midland’s production trend going forward.

The orange and green graphs show preliminary oil production for Midland County as reported by the Texas RRC for February and March, respectively. The red graph uses February and March data to project production as it would look after being updated over many months.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly drilling chart. The rig graph has been shifted forward by 6 months to better align with the latest production.

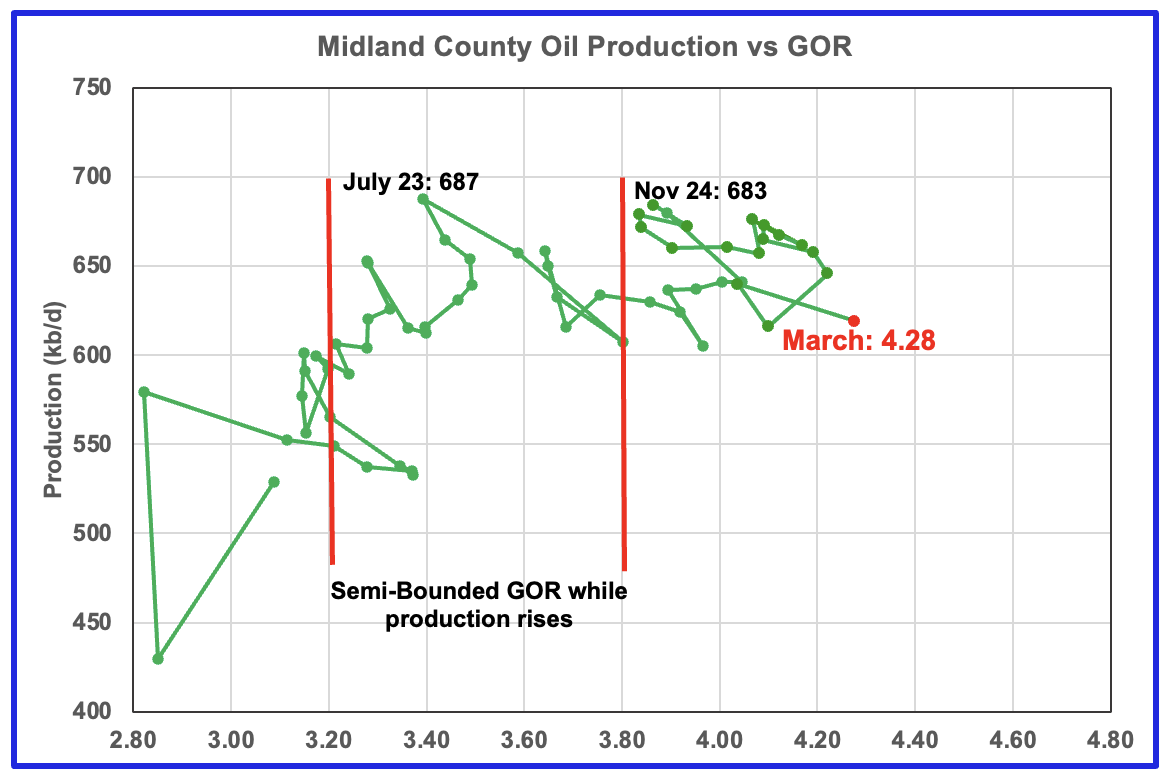

For March the Midland GOR ratio rose to a new high of 4.28 while the reported preliminary oil production dropped by 21 kb/d to 619 kb/d.

When the Midland county GOR initially moved into the bubble point phase, oil production and the GOR stayed within a narrow GOR range of 3.8 to 4.2 outside of the initial Semi-Bounded GOR region from March 2024 to November 2025. For March GOR rose to a new high of 4.28, which is an indicator of dropping production.

The oil production and GOR data shown in this chart are based on the RRC’s March preliminary production report.

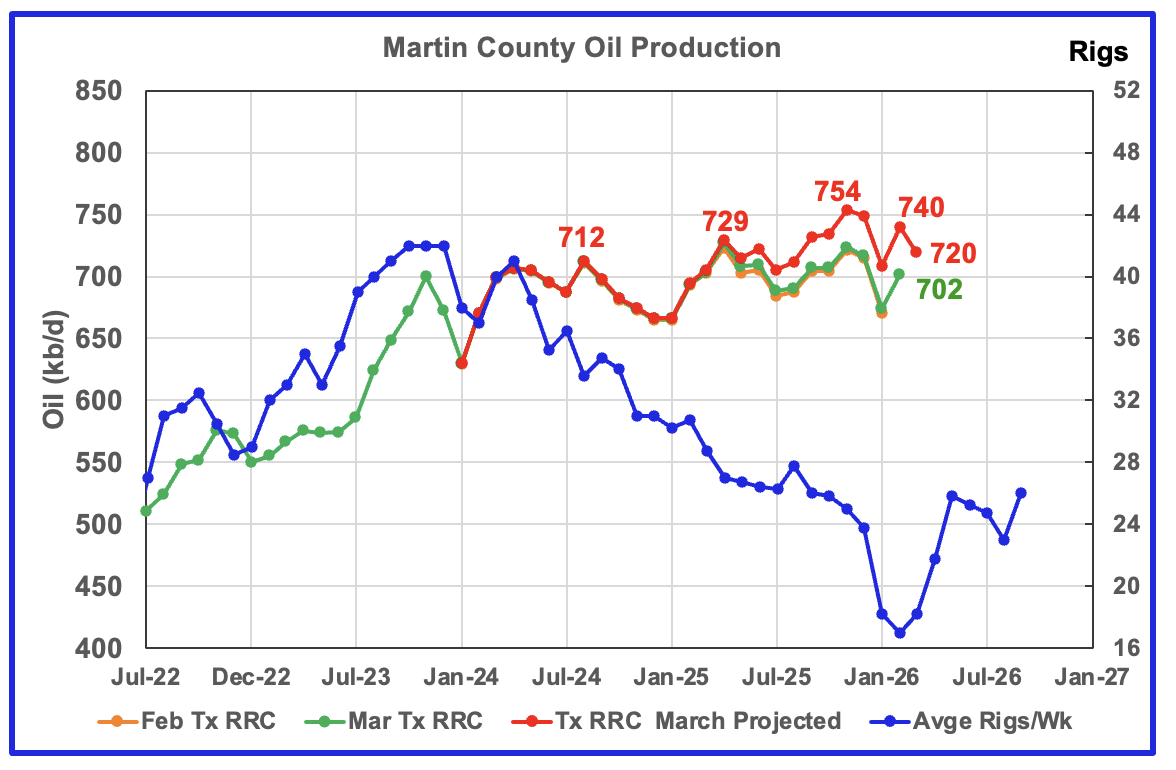

Martin county’s projected March oil production dropped by 20 kb/d to 720 kb/d. Production has been essentially flat since August 2024 even though the rig count has been in a steady decline. Will the rising rig count starting in time shifted April affect production?

The red graph is a projection for oil production as it would look after being updated over many months. This projection is based on a methodology that uses preliminary February and March oil production data.

The orange and green graphs show production for Martin County as reported by the Texas RRC for February and March. The blue rig graph time shifts the rig count forward by 5 months.

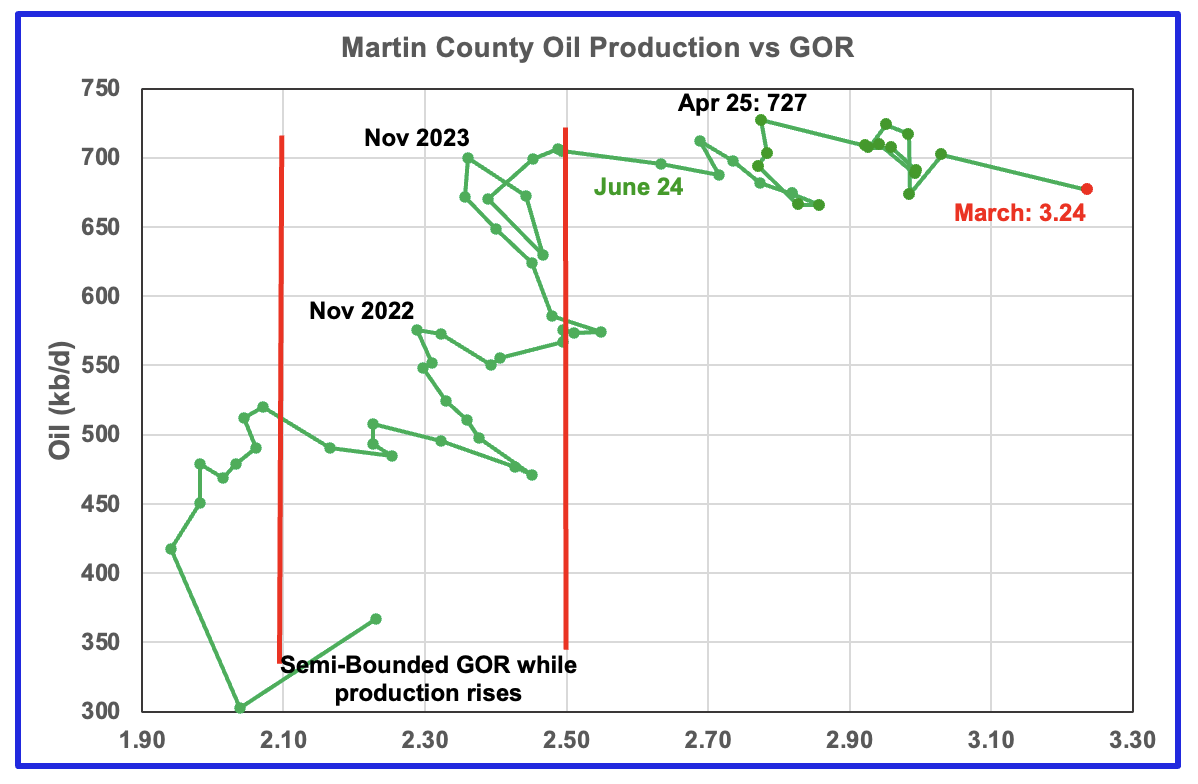

Martin county’s oil production after November 2022 increased and at the same time drifted to slightly higher GORs within the semi bounded range. However the June 2024 GOR saw its first move out of the semi bounded region.

The RRC’s preliminary March 2026 production for Martin County shows a 25 kb/d decrease to 677 kb/d accompanied by an increase in the GOR to a record 3.24.

Martin county has the lowest semi-bounded GOR boundary of the four counties at a GOR of close to 2.50. The March GOR is now clearly out of the semi-bounded region. Martin County has now entered the bubble point phase that should result in a plateau phase that should shortly turn into a slowly dropping oil production phase.

This chart shows the total oil production from the four largest Permian counties. Assuming the total current Permian production is close to 6,600 kb/d, these four counties account for 55% of the total.

March projected production increased by 2 kb/d to 3,637 kb/d. Increases in Lea and Midland were offset by drops in Eddy and Martin. February and March production being flat and lower than October 2025 is an early indicator that the Permian is in either a plateau phase or in its initial declining phase.

The February and March initial production data are shown in the orange and green graphs respectively. The red graph uses the February and March production data to project a final updated production for March.

Findings

– March projected production increases for the Texas counties are possibly a bit optimistic. The optimistic projections are mainly due to atypically large updates to February production in the updated March production data. Need to wait for April production to clarify February/March production and the trend going forward.

– Lea county entered its plateau phase in May 2024. While oil production is not following the rig count graph directly, the dropping rig count has resulted in Lea County production being in a steady flat plateau phase up to October 2025. However the November to January production drops may indicate Lea County has entered a declining phase. February and March production has risen and is currently tracking the time shifted rig count. It is not clear whether the current rising production could enter a lower level plateau phase in 2026 as the time shifted post January rig count begins to increase.

– July to December production in Eddy County saw a steady increase to 1,109 kb/d. February projected production fell to 1,104 kb/d and March dropped further. The March production drop along with upward revisions to previous months indicates that Eddy county may have peaked in December 2025. The dropping rig count starting in September 2025 may have finally shown up in falling production in March.

– Midland’s March oil production is overly optimistic due to atypical upward revisions to February production in the March report. Midland county may actually be in its declining phase.

– Martin’s projected production has been essentially flat since August 2024. Martin’s March projected production decrease indicates that its oil production is still in its plateau phase of approximately 725 kb/d and may be close to entering its declining phase.

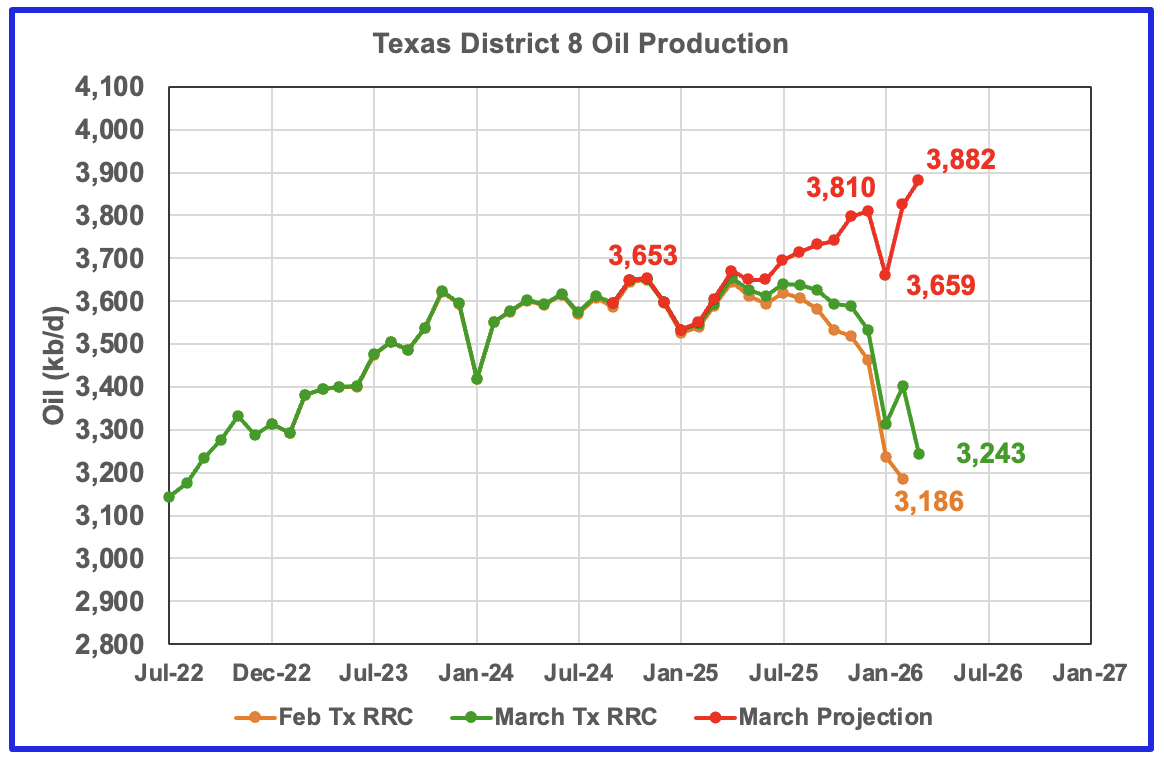

Texas District 8

District’s 8 projected production rose by 57 Kb/d in March. This is an overly optimistic projection that is being affected by a number of atypical upward revisions to many counties in District 8.

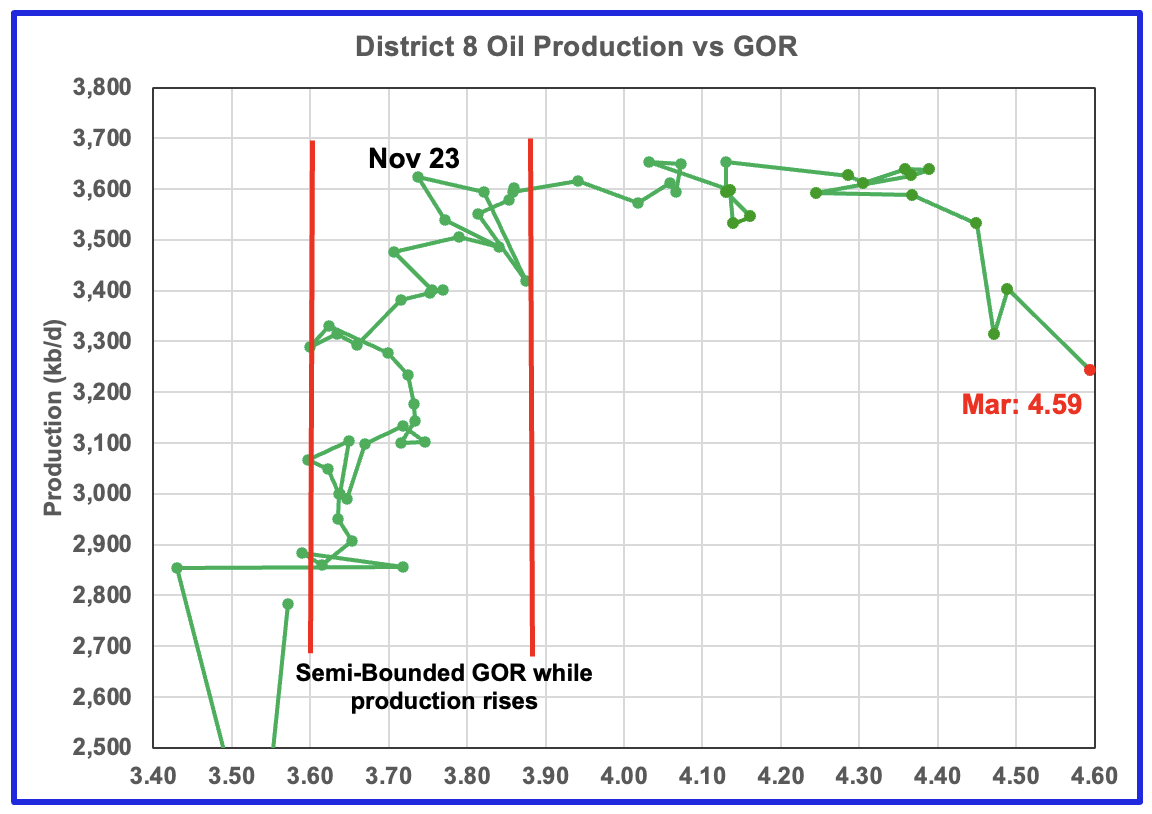

Plotting an oil production vs GOR graph for a district may be a bit of a stretch. Regardless here it is and it seems to indicate many District 8 counties may well be into the bubble point phase. The March GOR increased to 4.59, a new high, as preliminary production continued to drop.

Oil Production and GOR Charts for Four of the Next Larger Texas Oil Counties

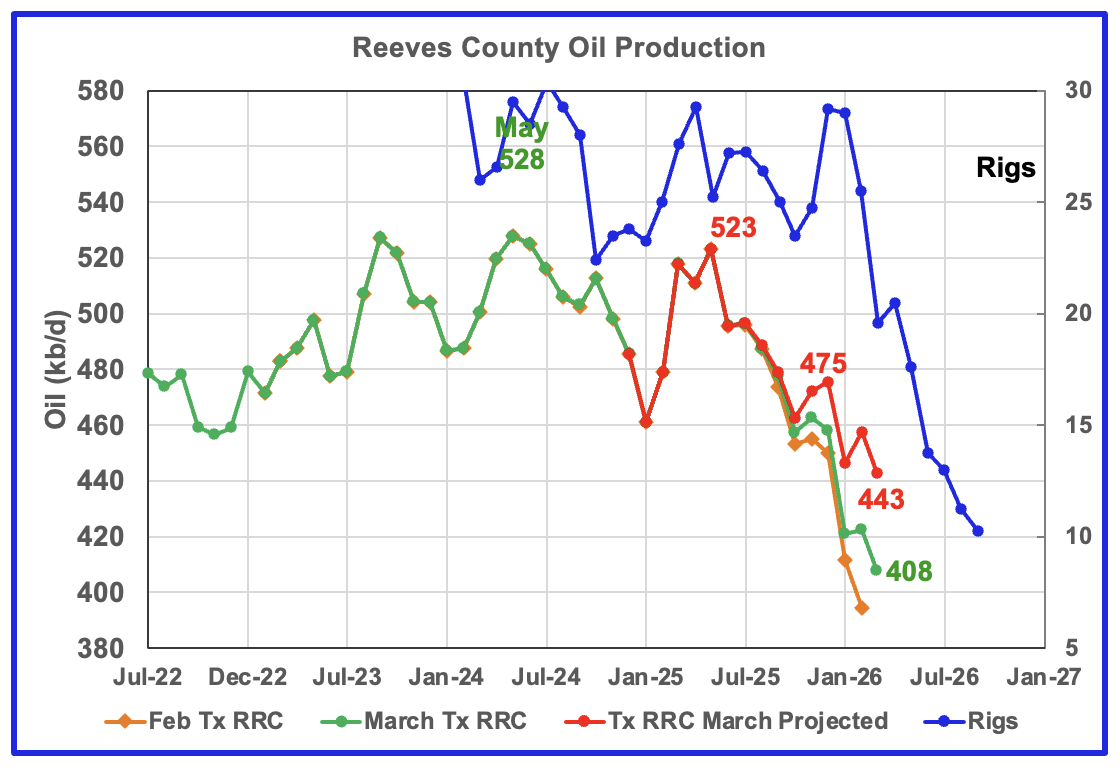

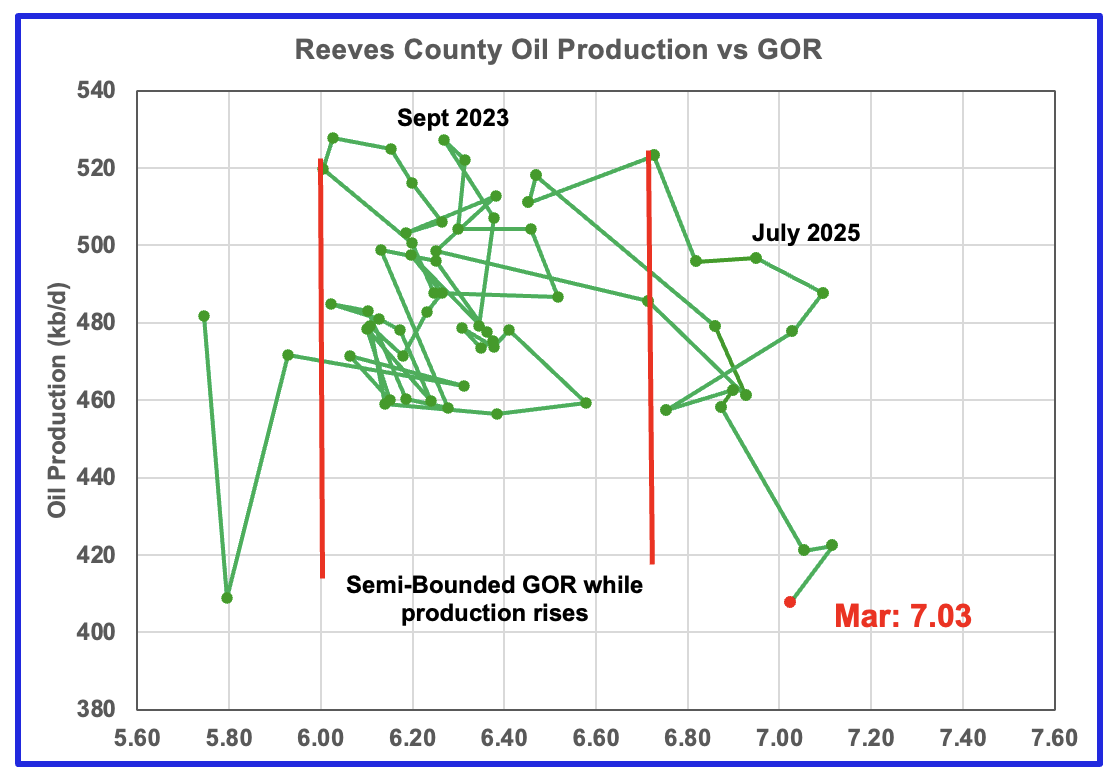

Reeves County GOR is high because it is the number one Texas county ranked by gas production. The current C + C production is almost evenly split between crude and condensate, with condensate about 17% higher than crude.

Reeves County GOR first moved out of the Semi-Bounded region in June 2025 and in March 2026 fell to 7.03 while initial production dropped to a new low of 408 kb/d. Reeves county is in its declining phase.

The rig count is time shifted forward by 7 months.

In real June 2025, 29 rigs were operational in Reeves county. By late May 2026 the rig count had risen to 16 from a February low of 10. Regardless of the current increase, 29 rigs to 17 rigs is a large drop in 11 months. The large drop shows up starting in time shifted Febuary 2026

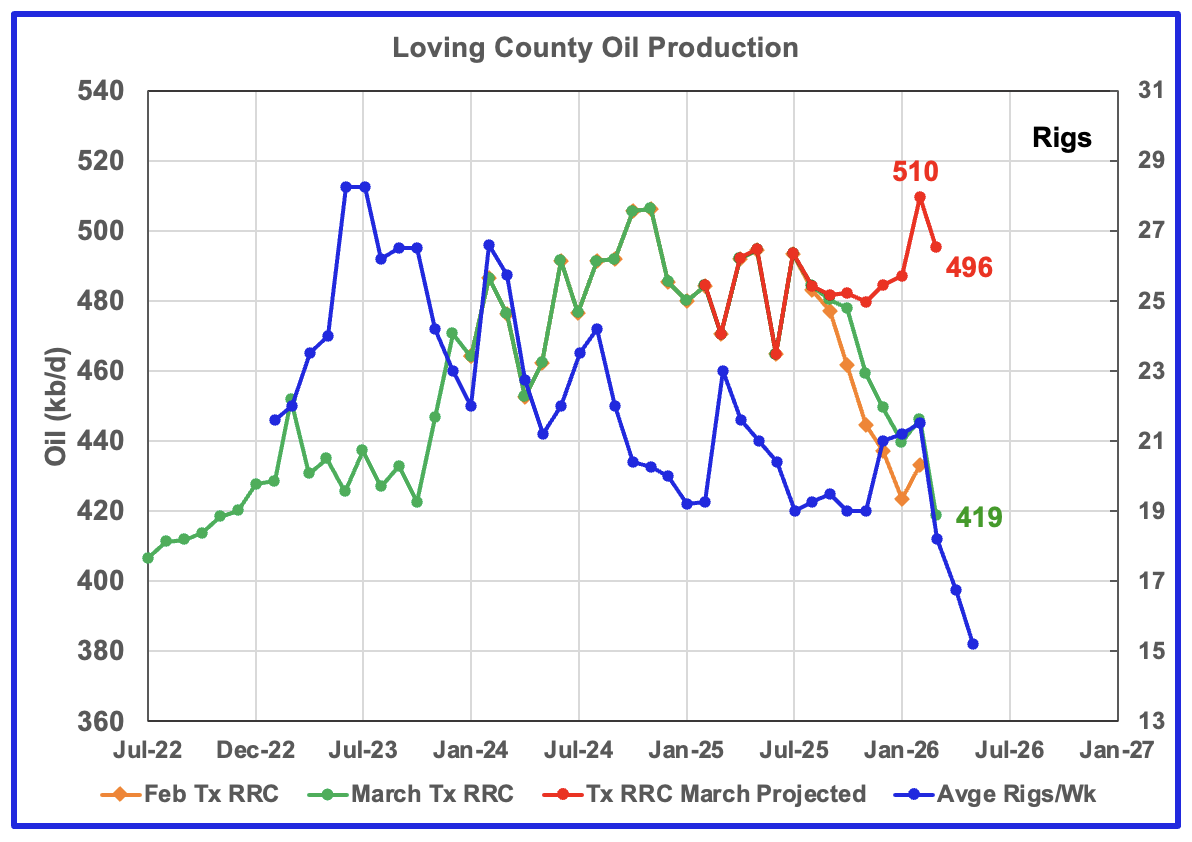

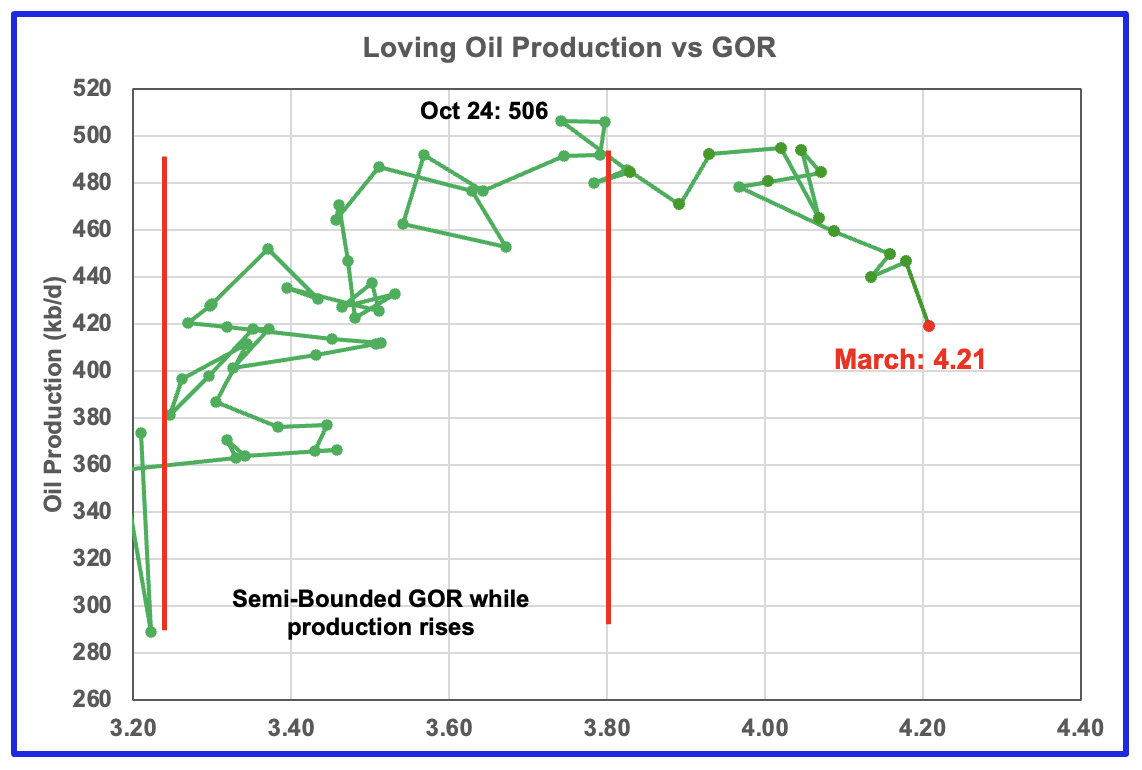

Loving’s projected production dropped by 14 kb/d to 496 kb/d in March. For March, the GOR increased to 4.21, a new high, while preliminary production dropped to 419 kb/d. Loving’s February and March projected production is a bit optimistic due to overly upwardly revised February oil production. It will be interesting to see if production continues to fall in April as it follows the dropping rig count.

Loving’s rig graph is time shifted forward by 5 months.

Loving had 17 operational rigs in late May 2026.

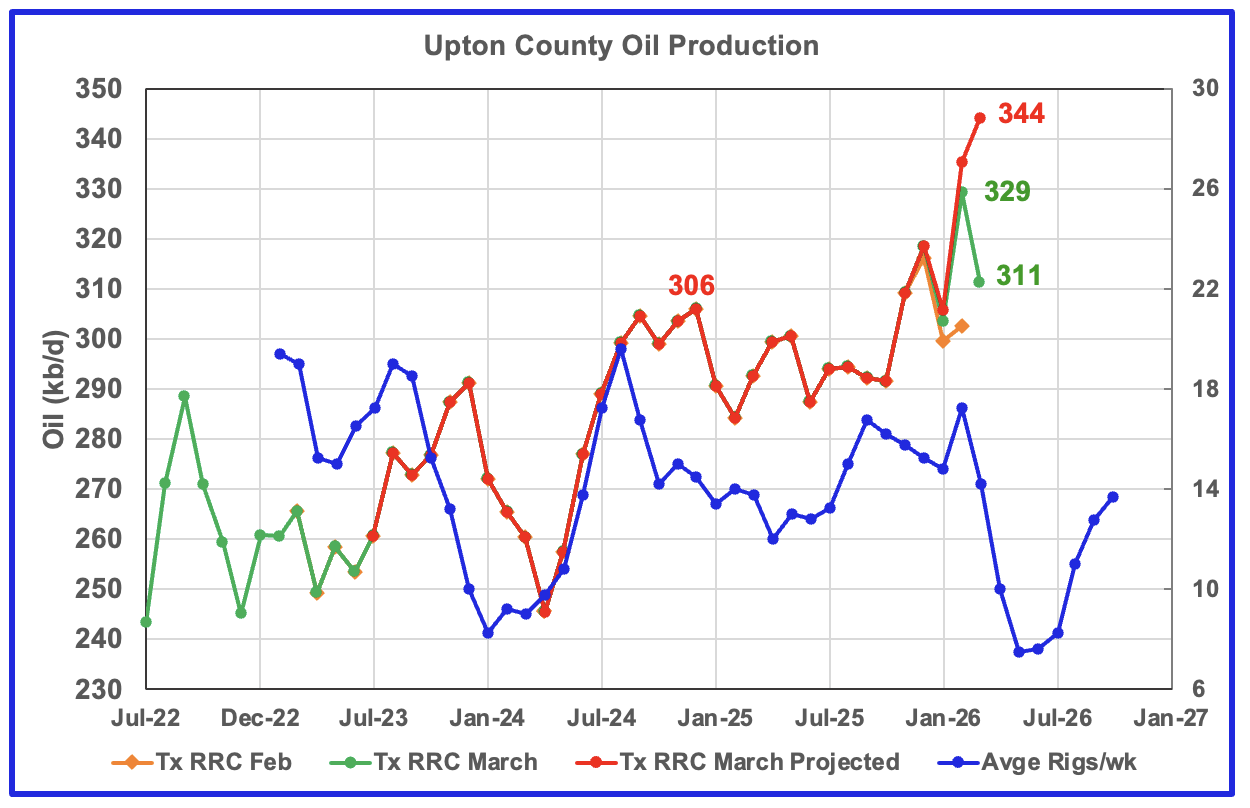

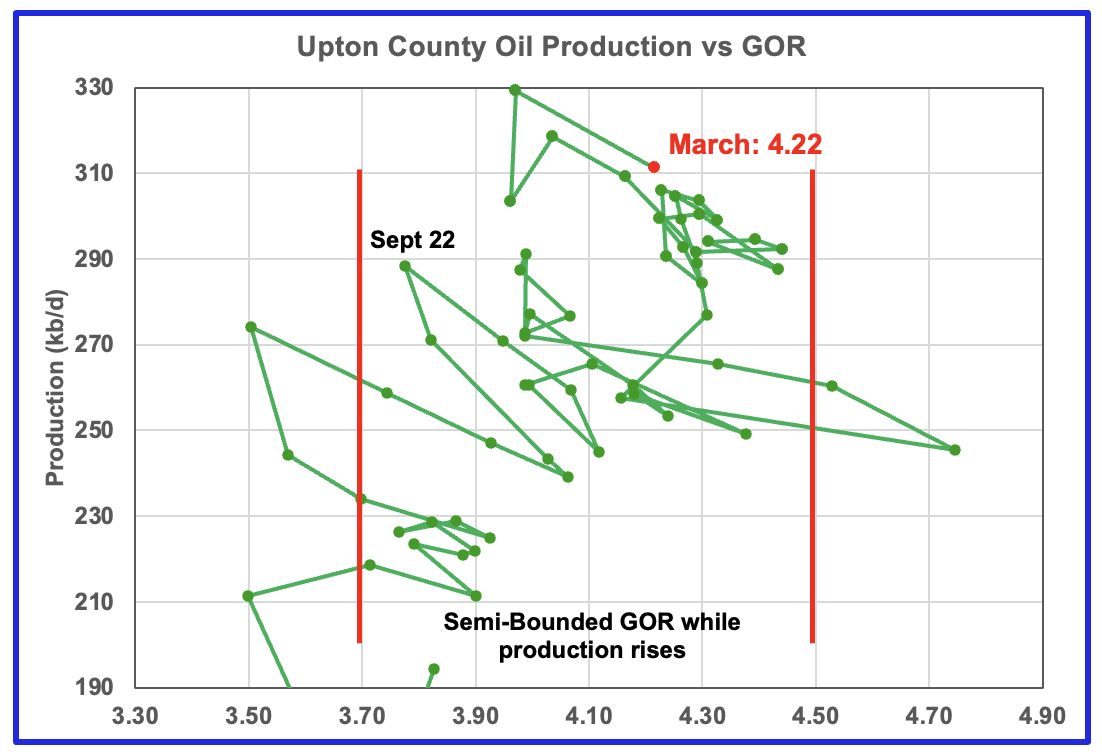

Upton’s projected March production rose by 9 kb/d to 344 kb/d.

For the next few months Upton County may see a production decrease associated with the dropping rig count which started in time shifted March 2026. The March increase is due to the large revision in the February production, the large gap between the orange and green graphs in February, and is a bit optimistic.

Upton’s GOR continues to stay within the Semi-Bounded region but rose to 4.22 in March.

Upton’s rig chart has been time shifted forward by five months. Upton began 2026 with 7.6 rigs, time shifted to May 2026. In real May 2026, the rig count had risen to 14.

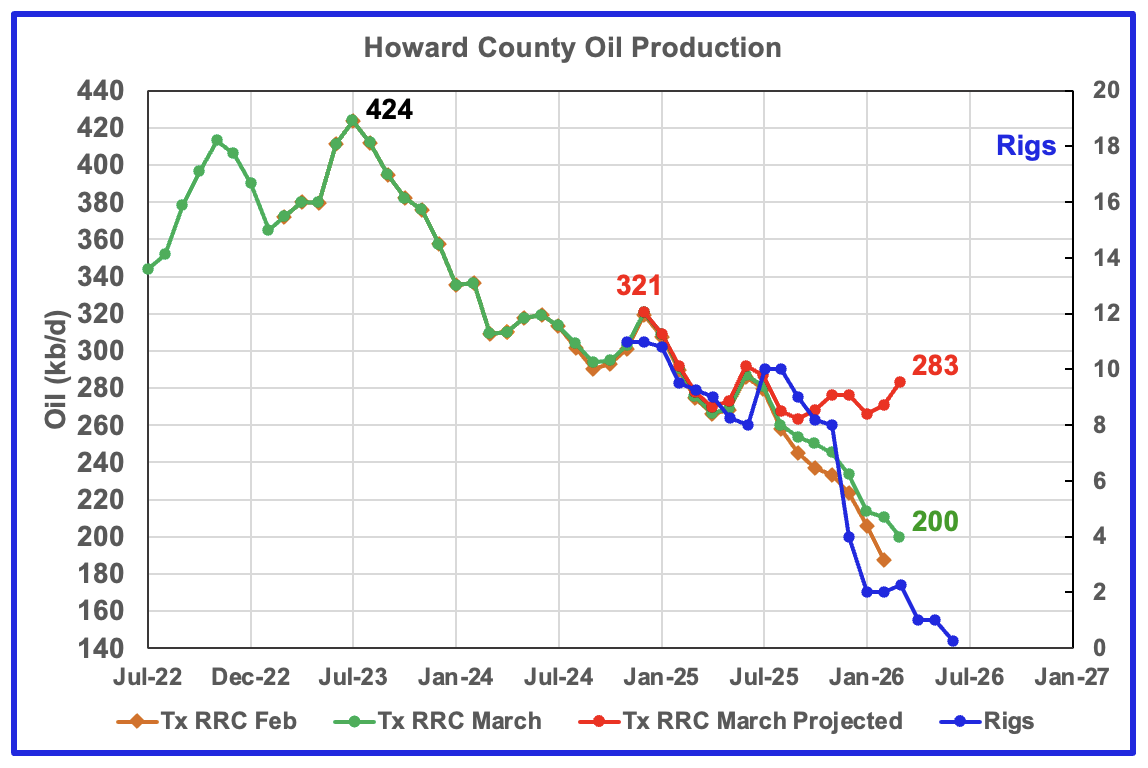

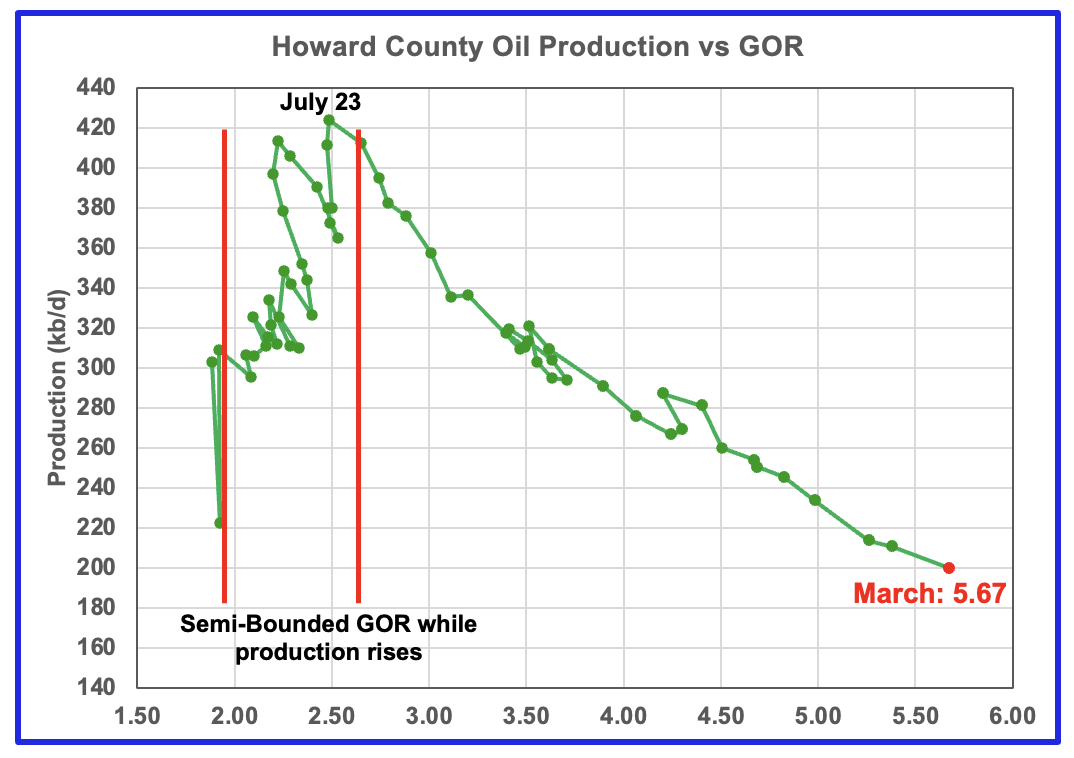

Howard County oil production peaked in July 2023 and has been in a slow decline ever since.

March’s projected production rose by 12 kb/d to 283 kb/d. This may be an optimistic projection due to the atypical upward revisions to February production.

Note the rig count in time shifted June 2026 is 0.25, i.e. 1 rig for one week in real January 2026. The rig graph is time shifted forward by 5 months. In real April 2026, Howard added one rig for a total of one operational rig.

For March the GOR rose to a new high of 5.67 as the initial production dropped to 200 kb/d.

Drilling Productivity Report

The Drilling Productivity Report (DPR) uses recent data on the total number of drilling rigs in operation along with estimates of drilling productivity and estimated changes in production from existing oil wells to provide estimated changes in oil production for the principal tight oil regions. The new DPR report in the STEO provides production up to March 2026. The report also projects output to December 2027 for a number of basins. The DUC charts and Drilled Wells charts are also updated to April 2026.

The DPR has made been significant upward changes to the oil production forecasts for the three tight oil basins, Permian, Eagle Ford and Bakken reported here. It is not clear if the increases are related to the sudden rise in the WTI oil price from $65/barrel in February 2026 to over $100/b in March 2026. While production starts to rise in October 2026 all the way to December 2027, the price of WTI slowly drops back to $64/b in December 2027.

The forecast seems be model driven whereby increases in the oil price brings on new drilling and the associated increase in oil production. Also interestingly there appears to be the typical six to seven month delay from February 2026 before production begins to rise. The only flaw in this possibility is that oil prices fall steadily from March 2026 to December 2027. Also there has been no reported significant increase in drilling rigs in March and April 2026.

For the Permian, production was expected to increase in October 2026 because there was an expectation that new gas pipelines were being built that would permit more high GOR oil wells to be drilled. However the projected increase has been increased further.

So at this time, it is not clear if the sudden production increase starting in the September/October time frame is simply a partially driven model forecast or related to pure Hopium.

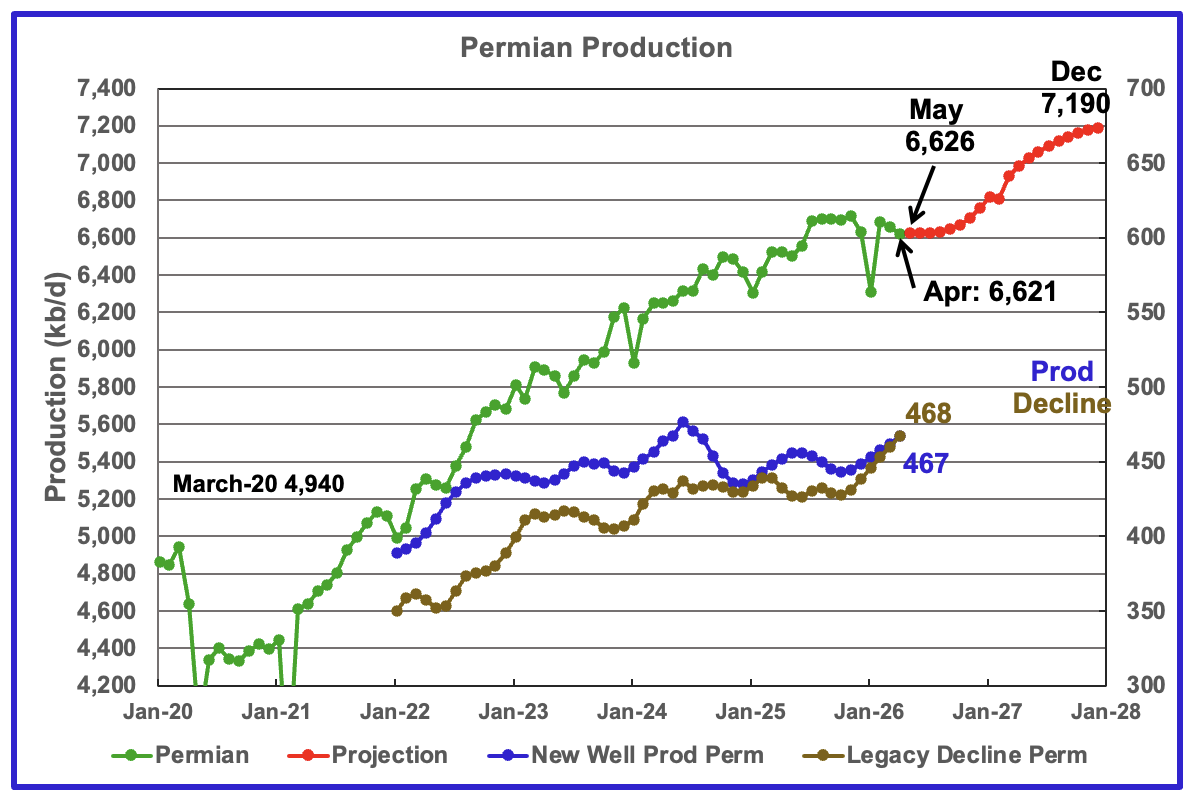

The EIA’s May STEO/DPR report shows Permian April output dropped by 36 kb/d to 6,621 kb/d. May production is expected to increase by 5 kb/d to 6,626 kb/d. From April 2026 to December 2027 output is expected to increase by 569 kb/d to 7,190 kb/d. December 2027 production has been revised up by 69 kb/d from the previous report.

Note that production begins to rise steadily from September 2026 to December 2027. According to the EIA, this is due to higher prices for WTI and more NG pipelines being built. The gas pipelines are needed to capture the associated flared gas coming from new oil wells.

Production from new wells and legacy decline, right scale, have been added to this chart to show the difference between new production and legacy decline.

These numbers reflect a one year production trend and provide the production contribution from new wells over a rolling 12-month period to determine if the rate of new production is increasing or decreasing compared to previous periods. The averaging process approximately adds a six month delay.

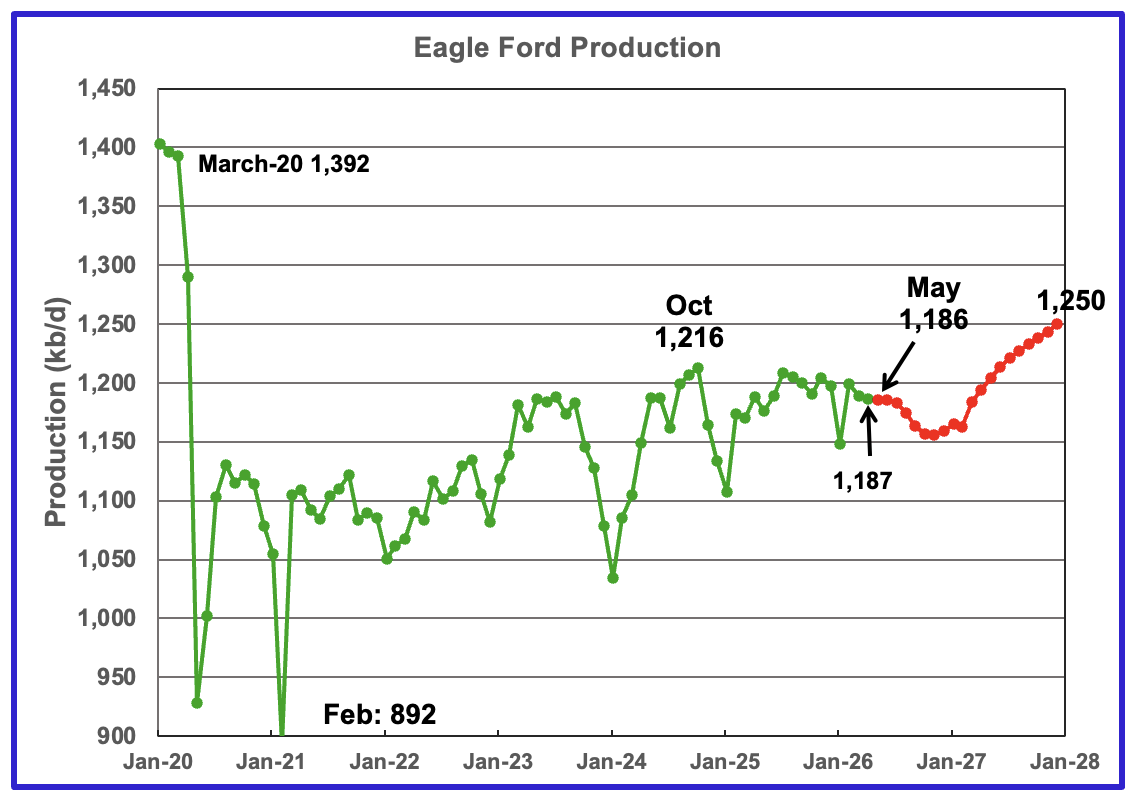

April output in the Eagle Ford basin decreased by 2 kb/d to 1,187 kb/d. May 2026 production is forecast to drop by 1 kb/d to 1,186 kb/d.

Output in December 2027 is expected to be 1,250 kb/d, revised up by 9 kb/d from the previous report.

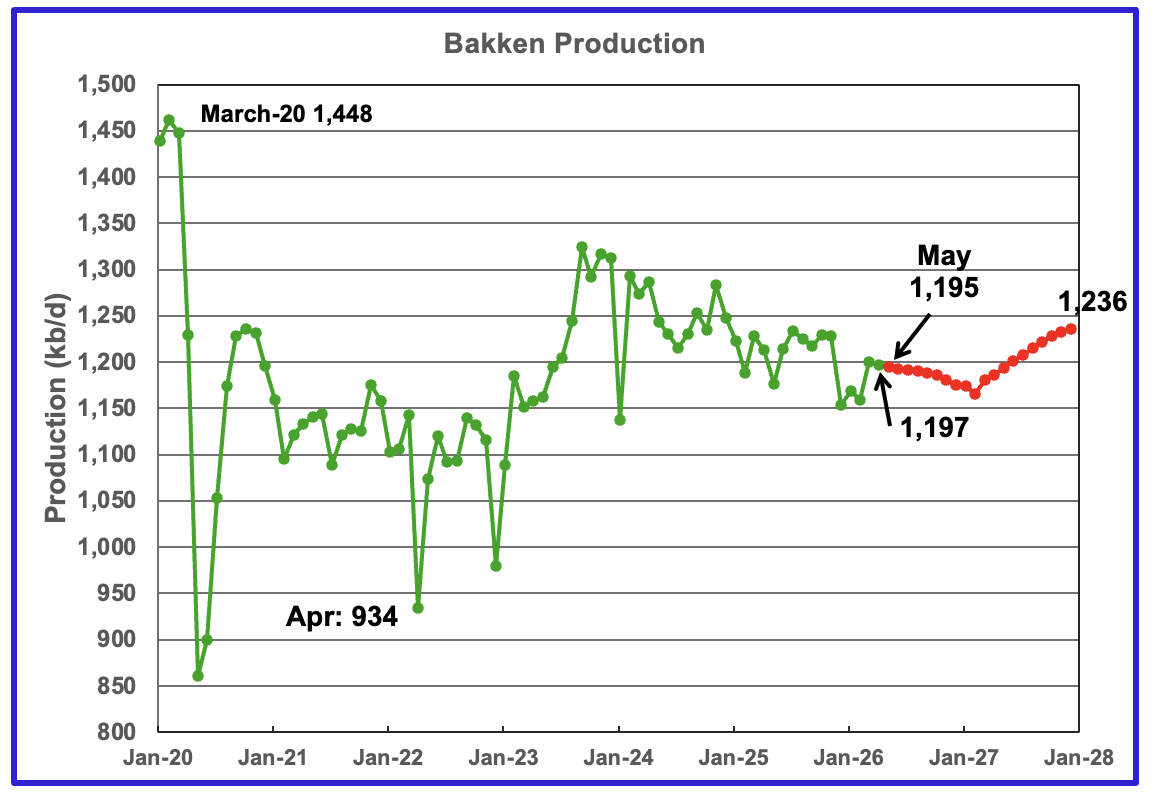

The DPR/STEO reported the Bakken’s April output dropped by 3 kb/d to 1,197 kb/d. May 2026 production is expected to decrease by 2 kb/d to 1,195 kb/d. The STEO/DPR projection, red markers, shows output rising to 1,236 kb/d in December 2027.

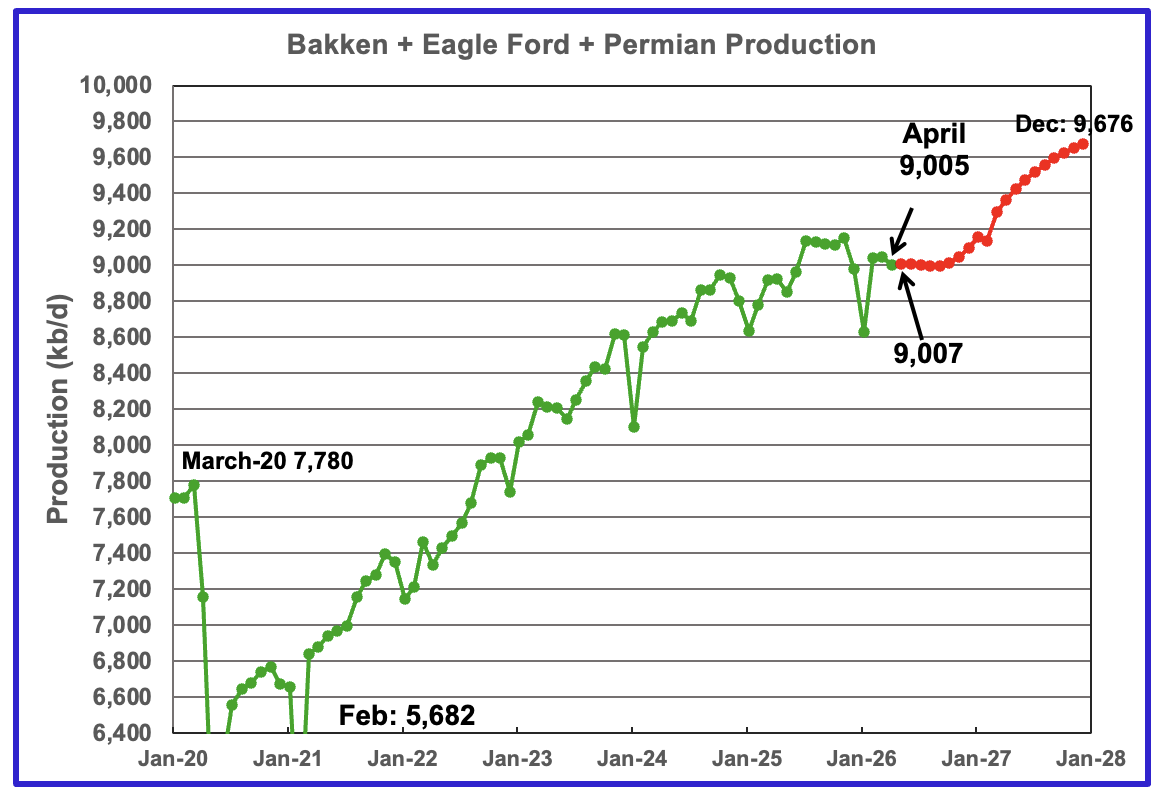

This chart plots the combined production from the three main LTO regions. April output decreased by 41 kb/d to 9,005 kb/d. May is expected to add 2 kb/d to 9,007 kb/d. Production for December 2027 is forecast to be 9,676 kb/d.

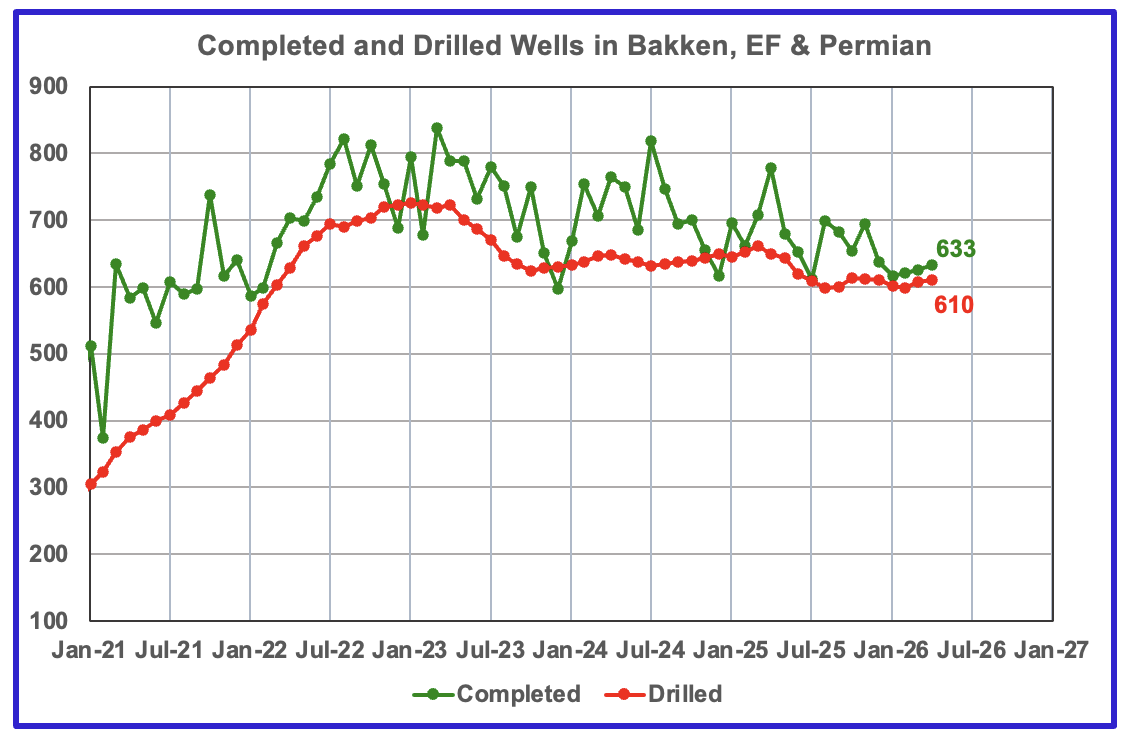

DUCs and Drilled Wells

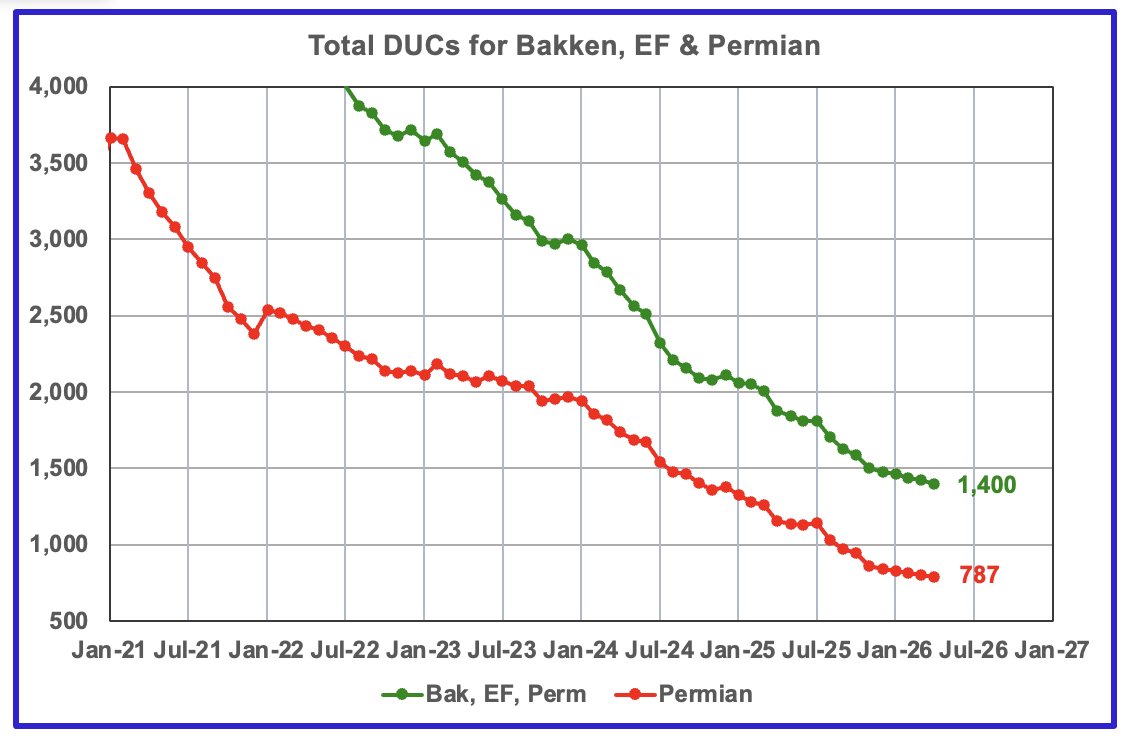

The number of DUCs available for completion in the Permian and the three major DPR regions continues its dropping trend. The April DUC count for the three basins dropped by 21 to 1,400. In the Permian the DUC count dropped by 13 to 787.

In the three primary regions, a total of 633 wells were completed in April, 8 more than in March. There were 610 wells drilled in April 2026, up 2 from March 2026.

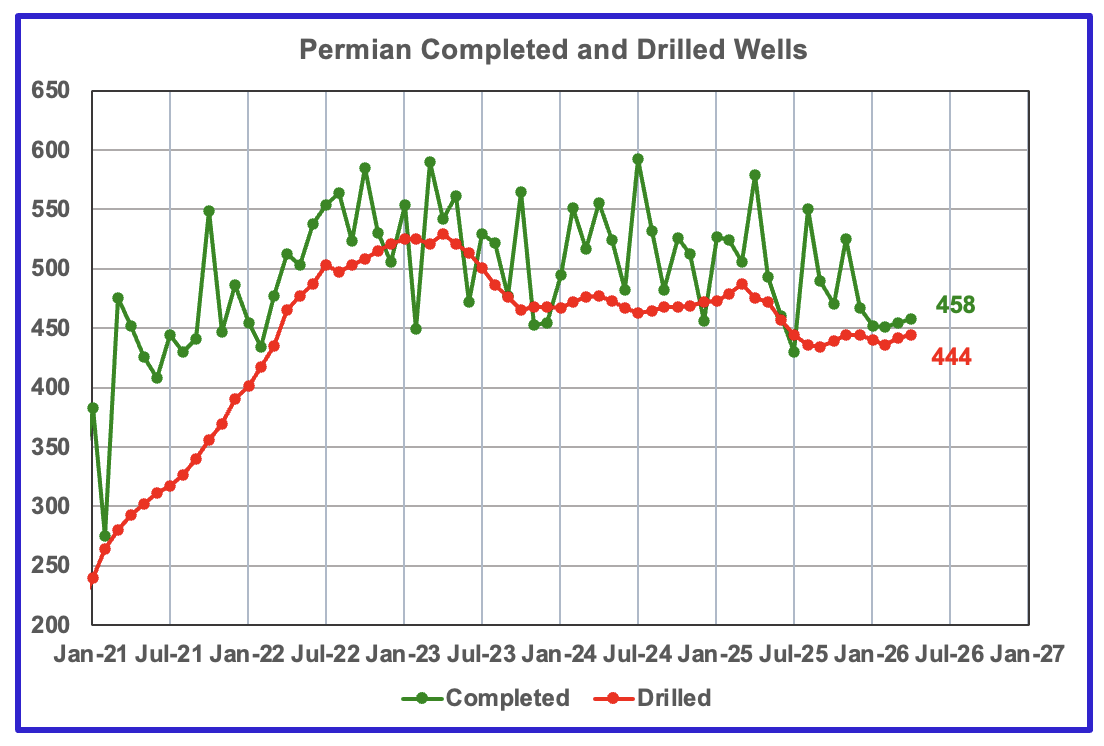

In the Permian, 458 wells were completed in April and 444 were drilled.

166 responses to “US March Oil Production Flat”

So can we all agree that Permian has entered a plateau phase? Appears to be nearly 12 months since peak Permian…

Kengeo,

In April 2026, Permian tight oil output was 6.13 Mb/d and in April 2025 Permian tight oil output was 5.91 Mb/d, so the peak is April 2026, might be a plateau going forward. Depends in part on the price of oil, at $180/bo we might see output rise. For US tight oil data see

https://www.eia.gov/outlooks/steo/xls/Fig42.xlsx

Kangeo

The only fly in the ointment is the DPR projection for the Permian in the DPR section above. Is that projection based on a model that says higher prices bring higher production or is just plain Hopium?

US tight oil output trailing 12 month average (TTMA). In past 12 months the TTMA for US tight oil output increased by 100 kb/d (from 9.23 Mb/d to 9.33 Mb/d), in the past 6 months the TTMA has increased by only 10 kb/d (from 9.32 Mb/d to 9.33 Mb/d). The DPR forecast is likely optimistic from May 2026 to December 2027. See chart linked below.

tight ttm 2606

why they dont drill in Upper and Lower Bakken shale to make “shale oil real shale oil”?

https://oilprice.com/Energy/Crude-Oil/North-Dakota-Chases-A-Second-Bakken-Boom-Through-Enhanced-Recovery.html

Sheng Wu,

Probably because those formations are more difficult to frac and the results of wells that have been drilled in Upper or lower Bakken have had very low productivity.

EOR is expensive, and would result in even lower profits, tight oil EOR is a pipe dream.

From the piece you linked:

North Dakota oil producers have yet to determine the most efficient and cost-effective EOR technology to deploy in the Bakken. Additionally, oil and gas executives have warned that EOR is far from a silver bullet due to the many unknowns.

Ovi,

Great job, thank you.

Permian DUC count is about 1.72 months of supply at the most recent month’s completion rate. For the Bakken and Eagle Ford the DUCs are equivalent to 3.5 months of supply at the most recent month’s completion rate. At some point the DUCs run dry unless the drilling rate increases or the completion rate decreases.

Dennis

Thanks. Much appreciated.

Do you have any idea or way of cross checking the sudden addition of 11 directional rigs to Eddy county. I wonder if it could be related to the article under the Lea oil chart that reports that Devon Energy has recently acquired land in Lea and Eddy counties.

In a way I am assuming that Devon would use a directional rig to drill a 4 mile U well.

Ovi,

My knowledge on the actual practices in the oil field are limited, your guess sounds reasonable. Chart below considers HOR for the US compared to horizontal plus directional rigs (H+DOR). Since March 6 a big jump in the number of directional oil rigs operating. (see link at endof post for chart.)

As far as the Devon aquisition, when we look at the total cost of these wells when this lease aquisition cost is added, the wells are likely to need $180/b oil prices sustained over 5 years in order for the well to pay out.

See

https://www.oilystuff.com/group/gassy-stuff/discussion/8358eb16-210d-4945-b411-83c889e31baf

This expert says the following about this lease aquisition:

Devon yesterday paid $161,500 per acre to the government. On a standard 10-11,000 foot lateral layout Devon will be able to drill 400 locations/benches on this new acreage, theoretically…that works out to $6.5 MM per location, or roughly $ $17 MM per well. I promise you, however, you will never hear about these actual full cycle well costs nor will you ever get the corresponding truth whether this lease acquisition worked economically.

It won’t. Not based on liquids and gas EUR’s in Lea and Eddy Counties and not unless oil prices go to $150 a barrel and stay there.

Mr. Trump I believe whacked RI on BLM tracts from 3/16ths back to 1/8th but you can just about be assured they’ll go back to 3/16ths, or more, in 2029. What oil prices will be in just six months is anybody’s guess.

oil rigs 2606

Rig Report for the Week Ending June 5

The dropping rig count that started in early April 2025 when 450 rigs were operating dropped this week. Drilling continues at a steady rate of 368 ± 6 rigs per week since August 2025 while WTI closed at $90.54/b, up from $87.36 from last Friday.

– US Hz oil rigs rose by 2 to 373, down 77 since April 2025 when it was 450. It was also up 11 rigs from the low of 362 first reached in the week ending August 1, 2025. The rig count is down 17% since April 2025.

– The New Mexico Permian Hz rig count dropped by 1 rig to 73. Eddy dropped by 1 to 33 while Lea was unchanged at 40. As noted last week, the Rig report showed that 11 directional rigs were added to Eddy county for a total of 14. The same number 14 is being reported this week. Will this show up as increasing production seven months from now.

– Texas added 4 to 196. Midland and Martin were both unchanged at 22 and 24 respectively. The biggest change occurred in Reeves county where 3 rigs were added.

– Eagle Ford added 1 to 33.

– NG Hz rigs dropped by 1 to 105.

A Rig

Frac Spread Report for the Week Ending June 5

The frac spread count dropped by 2 to 190. From one year ago, it is up by 4 spreads but is still down by 25 since March 21, 2025. This is the first drop since the rise started 6 weeks ago.

A frac

Hi Ovi,

Thank you for the update!

Hey, I haven’t verified this data, but if it is correct the fuel oil situation is getting rather dire.

https://x.com/HFI_Research/status/2062988811735560219?s=20

Japan stopped reporting around week 11/12, which is probably not a good sign.

Brent futures chart from

https://oilprice.com/futures/brent/

also see link below (chart snipped from site at link above)

brent futures 2606

At post linked below there is a great chart showing the decrease in Permian productivity per foot of lateral length. Click on the second chart for a larger view, great stuff. Thank you sir.

https://www.oilystuff.com/group/operational-stuff/discussion/af141534-8e4c-480e-8f19-71f7ee66f29b

yes, DC and Mike,

because they drill longer laterals, and larger fracs, the IP for each lateral barely drop, or might even increase, operators/investors are not that pessimistic.

but decline is certainly faster, but only obvious after 1-2 years, and that is too late, and the final statistics bite them badly.

Sheng Wu,

It is the cumulative well profile that is important. When normalized for lateral length average new well productivity in the Permian Basin has been decreasing since 2017. They are not creating any new tight oil formations, if there are a potential 100,000 wells with lateral lengths of 10,000 feet, increasing the lateral length to 20,000 feet simply reduces the potential number of wells to 50,000. Note however that as the lateral length increases, the productivity per 1000 feet of lateral decreases, so actual basinwide URR tends to decrease as average lateral length increases to more than 10 kft for newer wells.

INTERVIEW: Mercuria shipping head says fuel shortages could **idle 10% of global fleet**

https://www.spglobal.com/energy/en/news-research/latest-news/refined-products/060326-interview-mercuria-shipping-head-says-fuel-shortages-could-idle-10-of-global-fleet

“The shipping sector is fast approaching a fuel crisis that could paralyze a tenth of the global fleet, Larry Johnson, global head of freight at commodities trading house Mercuria, said in an interview.

Since the Middle East war erupted, markets have been preoccupied with potential shortfalls in the diesel and jet fuel traditionally exported in large quantities from the Persian Gulf.

However, as refiners strain to capture soaring clean product cracks, residual fuels have suffered. Increasingly, feedstocks have been held back from the marine fuel market to kept for further processing, leaving the shipping sector at risk of crippling shortages, Johnson said.

“My view on marine fuel oil is there will be regional stock-outs by July and that there are potentially outages in the major hubs by August, September, at the latest,” Johnson said.”

It sounds to me like marine fuel oil is low price, low profit, so it’s being de-emphasized in favor of more expensive “clean” products. If the shipping sector is afraid of shortages, they probably need to be willing to pay more for their fuel. If they’re not willing to pay more, than it’s not really a shortage, it’s more that they’re being out-competed by people who need it more than they do and are willing to out-bid them.

It reminds me of the trucking sector complaining about not enough drivers. If they’re not willing to pay enough to attract drivers, then it’s not really a shortage of drivers, it’s a shortage of shippers willing to pay what it takes to run their business.

The good news is that the ships that used to sail through the Straits of Hormuz aren’t burning a lot of fuel these days.

Hi Nick,

Yes, given that the Hormuz has been closed so long and is unlikely to normalize, users will have to start bidding up to access available supplies/refining capacity.

From the article:

“Singapore, the world’s largest bunker hub, saw residual fuel supplies near one-year lows in April, but has pulled additional stock from Europe and Russia to slow losses. Inventories in Northwest Europe have continued to slide, however, and stocks in the UAE’s Fujairah have launguished at record lows.

“For marine fuel oil, there’s no buffer. There’s nothing. So once you’re out, you’re out. And then ships will have to try to buy diesel fuel, for example,” Johnson said.

The sector would then be forced to compete with other end-markets for limited gasoil supplies, which already command a premium to conventional fuel oil.”

“Should trade disruptions last another month, Johnson says mass fuel shortages could trigger trade congestion on the scale of the Covid-19 pandemic – shutting down as much as 10% of marine traffic.

As vessels jostle for limited supply, lower-margin segments like dry bulk are most likely to be caught short, he said, potentially exacerbating challenges for agricultural sectors relying on fertilizers for next year’s crops.”

Yes. The highlights:

“ once you’re out, you’re out. And then ships will have to try to buy diesel fuel, for example,” Johnson said. The sector would then be forced to compete with other end-markets for limited gasoil supplies, which already command a premium to conventional fuel oil.”

Commercial/industrial consumers will become more efficient – water shippers will slow down* – and then bid supplies away from low-value uses like single passenger SUVs and pickups.

—————————-

*Ship fuel consumption is the cube of speed – reducing speed by 10% can reduce fuel consumption by 1/3.

https://www.opec.org/pr-detail/604-16-june-2026.html

Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman adjust production and reaffirm commitment to market stability

The seven OPEC+ countries, which previously announced additional voluntary adjustments in April and November 2023, namely Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman met virtually on 7 June 2026, to review global market conditions and outlook.

In their collective commitment to support oil market stability, the seven participating countries decided to implement a production adjustment of 188 thousand barrels per day from the additional voluntary adjustments announced in April 2023. This adjustment will be implemented in July 2026 as detailed in the table below. The additional voluntary adjustments announced in April 2023 may be returned in part or in full subject to evolving market conditions and in a gradual manner. The countries will continue to closely monitor and assess market conditions, and in their continuous efforts to support market stability, they reaffirmed the importance of adopting a cautious approach and retaining full flexibility to increase, pause or reverse the phase out of the voluntary production adjustments, including reversing the previously implemented voluntary adjustments announced in November 2023.

Just as Iran can shut down imports and exports from the other Gulf nations, those nations in turn can shut down Iranian shipping if they decide to retaliate in kind. Iran can shut down the pipelines and ports that are/can serve as alternative oil export, by targeting the pipelines, pumping stations, and port facilities.

So either there will eventually be some uneasy accommodation between these parties, or a long term period of disruption, or an imposed settled period. China could play a big role in this, but I don’t think they want involvement the problem. Rather they will more likely take the stance of ‘whoever wants the income (in yuan) send me the oil’.

Can the US impose a renewed settled period (regarding oil flows) from the Gulf, as it has done for many decades? I don’t see it, unless Iran has a wholesale shift in stance at some point. No one can impose that shift from the outside, as we are now fully aware.

https://www.youtube.com/results?search_query=young+turks

Trump to integrate US Military and Israel.

Israel will have access to US Military data and designs.

US found lots of 3He in Minnesota, no need to get it from moon

https://www.youtube.com/watch?v=NoxHubOdxIk

The YouTube says $30 million per kg of Helium. So a semi-trailer full weighing 5000 kg would be worth $150 billion.

YouTube also shows the bugs out in force in northern Minnesota — gnats, mosquitos, black flies, deer flies, horse flies, moose flies.

Gulf of Mexico: little to no hurricane activity last 4 years.

As a result, 2025 was a record year for GOM oil production at 1.94 mmbopd. The previous high was right at 1.9 mmbopd in 2019, another pretty quiet year. If 2026 is a quiet year, it should exceed 2025.

I only learnt this past week that the ultra-deep sub-salt GOA has not only black oil with low GOR, but also heavy oil like bitumen or Venezuela heavy.

A USD 100 Million “Rock”: Bitumen in the Deepwater Gulf of Mexico SPE Drilling & Completion,

2010 https://sci-hub.st/10.2118/138228-PA

Only the drillers care about it because such heavy oil is causing trouble for drilling for the low GOR black oil below in the sand reservoirs.

No geologists seem to care how much & where such bitument come from?

during drilling, such bitumen could get to the wellhead with mud like they hit a lake of bitumen/tar, tons of it for weeks, and Chevron’s Big Foot had couple of drilling wells stalled and even abandoned due to this heavy oil deposit at the bottom of the salt, and just above the sand.

In my experience, this tar/bitumen came in 2 forms – mobile and immobile. The mobile version was more likely to be encountered right below salt, while the immobile version was encountered deeper in the subsalt section. The mobile version could enter the wellbore and completely mess up the entire system. The geologists spent alot of time in the planning process trying to predict if this material might be encountered because it was always a big headache. It often resulted in having to sidetrack the well.

Anyone care to speculate about what happens when Cushing commercial inventories drop below 20 million barrels?

05/29: 22.4 million barrels

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=W_EPC0_SAX_YCUOK_MBBL&f=W

And……Cushing now down another 1.4 million bbls according to Kpler’s drone data

https://x.com/HFI_Research/status/2063773153999061256?s=20

Cushing is not SPR

Cushing June 5: 21,640,000 barrels

Hi SW,

Not sure what you are referring to, could you clarify?

Data from EIA is “Weekly Cushing, OK Ending Stocks excluding SPR of Crude Oil (Thousand Barrels)”

Currently: 23,024,000 barrels

If I had a commodity hedge fund with capabilities to store/deliver/transport/market WTI in Cushing, I would probably consider ways to play the long side of it, including taking (forcing) delivery from the shorts who are increasingly unlikely to be able to deliver what they have sold.

“Inverse Covid”

US tight oil scenario in chart linked at bottom, tight oil output decreases at an average annual rate of 8.5% per year from 2029 to 2035 for this scenario, which may be on the optimistic side.

us tight 2606b

That is a dramatic decline. What price assumption does that projection use?

Does it assume decrease demand, or simply decline in production capability?

Thanks DC

Hickory,

It assumes the futures curve is correct. See chart below for recent Brent Oil Futures curve.

brent futures 260610

Thanks DC. I don’t give much credence to the long term futures market as being a legit predictor of Permian oil pricing/output.

But the two graphs combined does point out that lower price will lead to lower output.

Good morning,

I just took a peek at the WTI COT report:

https://www.barchart.com/futures/commitment-of-traders/interactive-charts/CL*0

In the disaggregated report (=more accurate representation of physical commercial players), the commercials are long 358,016 contracts.

If you click on the “max” button, you can see the historical data, and this appears to be the biggest long position the commercials have ever held.

In contrast, the swap dealers (the big banks and financial institutions like Goldman or JPM) are hugely short.

I wonder who is shorting via the banks?

The big banks and financial institutions (more likely their clients) are net short 546,125,000 barrels of oil……….

These paper barrels explain a lot about how the market price has stayed so comfortably low during the biggest disruption to supplies in history.

Dennis, Ovi,

Might a fairly simple model of our current Hormuz situation be helpful? Here’s a very rough draft:

Hormuz Estimates (MBPD)

World C&C prior to closure – 86 Source: “January World Oil Production Drops”

Shut in: 9 source: OPEC May 26 report per POB post

Net: 79

Current sources of reolacement for 9M shut in:

China reserves: 5

US SPR: .6?

Other reserves 1.4?

Consumption reductions: 2?

Estimated reserves duration:

China reserves: 1B

Daily output: 5M per day

1B/5M = 200 days (MOL?)

200 days from 2/28/26 would be roughly middle of September.

SPR starting reserves: 415M

Output: .6M per day?

MOL?

——————————

I’d think that there would be several tranches of reserves, whose life would be helpful to identify. As each reserve is exhausted we’d see a new level of scarcity.

HI Nick,

That’s a nice, practical way to follow the ongoing oil saga.

Seems like Cushing may be the first to breach the MOU (20 million barrels).

I looked at Nymex oil deliveries this year.

https://www.cmegroup.com/solutions/clearing/operations-and-deliveries/nymex-delivery-notices.html

The numbers have been low since the Iran war began. Largest delivery month since the war begain was 1.889 million barrels (1889 contracts) in May, and the lowest delivery month was 1.005 million barrels in June (1005 contracts).

According to AI, “Historically, in an ordinary, healthy market month, between 5,000 and 15,000 WTI contracts stand for physical delivery at Cushing.”

That would be 5 to 15 million barrels delivered per month.

All it would take is traders standing for an ordinary amount of deliveries to place Cushing commerical inventories WAY below MOL.

BUT conveniently delivery against Nymex futures have dropped about 80% since the war began.

I wonder if someone has warned oil traders NOT to take delivery of Nymex WTI?

Cushing is storing mainly domestically produced crude, not import?

The amazing mainstream media biased facts are:

1. US refineries could “only” refine “import light crude”. They keep on saying US (gulf coast) refineries can not process/refine domestic light tight/shale oil, and only process foreign import crude.

Art mentioned specifically these refineries are tailored to refine Venezuela and Mexico heavy, but only occasionally; and therefore let mainstream medias to bash Trump’s take-over of Venezuela. In China, this biased fact is becoming mainstream media — they claim that Trump has to beg/force India and China to buy Venezuela crude, because US can not process it (only China&India have the refinery capability and bear the pollution). This biased fact is even reaching quite a portion of US, and even some field oil roughnecks and oil refinery chemists/engineers believe so, and not to mention all the left-extremists.

2. The Venezuela heavy is the same as Canadian Heavy, hard/expensive to produce and hard to refine, and needs Billions $$$ and years to restart. This is created by US majors as well as China oil importers preying Venezuela crude at huge discount. They are ignoring the great heavy reserves in Venezuela and Canada have huge difference and shades across a large board.

The facts are that US refineries are tuned up for the Venezuela Orinoco heavy shortly after they developed it quickly in just over 5 years in late 1990s to early 2000s. The technologies were not there in China and India at that time. US majors still has Vz import all the time even small portion, and always dreaming of getting back their bounties. Once the Chinese importer started scaling up oil operations in Vz, they got mad and unleased fury accumulated over 20 years— who would not!?!?

Venezuela certainly added 0.8~1 MBOPD,

starting at 0.5MBOPD, right now close to 1.3MBOPD

Weekly U.S. Ending Stocks of Distillate Fuel Oil

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WDISTUS1&f=W

05/29 102 million barrels

MOL = 85 million and 90 million barrels?

Sheng Wu,

Average Venezuela crude output was 937 kb/d in 2025 and in April 2026 output was 1031 kb/d according to May MOMR from OPEC using secondary sources. Venezuela itself reports 2025 average crude output was 1081 kb/d and in April 2026 crude output was 1136 kb/d, an increase of only 55 kb/d.

In 2019 Venezuela produced about the same as in April 2025 and disd fall to as low as 500 kb/d in early 2021 under sanctions by the US under Trump (in 2018) and continued by Biden through 2021. In 2015 Venezuelan output was about 2400 kb/d. It is unlikely we see a quick return to 2400 kb/b due to a deteriorated oil infrastructure in Venezuela, but perhaps by 2036.

Since April 2021 Venezuela has added about 530 kb/d to crude output.

Where are you getting your data?

Here is the latest data on Venezuela and other OPEC producers from the June MOMR. Venezuela at 1072 kb/d in May 2026 vs 943 k/d for 4Q25. OPEC output is down about 9.67 Mb/d in May 2026 from the 4Q25 level. The 5 main OPEC nations using SOH (Saudi Arabia, UAE, Iraq, Kuwait and Iran) produced 23280 kb/d in 4Q25 and in May 2026 output was 13406 kb/d, 9874 kb/d less due to Hormuz being closed.

opec2606

Venezuela’s C+C data from EIA at link below

https://www.eia.gov/international/data/world/petroleum-and-other-liquids/monthly-petroleum-and-other-liquids-production?pd=5&p=00000000000000000000000000000000002&u=0&f=M&v=line&a=-&i=none&vo=value&vb=173&t=C&g=none&l=249–243&s=94694400000&e=1769904000000&ev=true

Venezuela C+C data from EIA in chart linked below, last data point is Feb 2026.

venezuela 2606

DC,

Looks like this author agrees with your sentiments:

https://oilprice.com/Energy/Energy-General/The-Countdown-to-a-Major-Oil-Price-Surge-Has-Begun.html

Thanks, excellent piece.

WTI under $90 this morning, as it slowly keeps falling in price.

The investment world does not believe in any short-term or long-term oil shortage.

Asklepias,

Prices are low because the market believes Trump’s bullshit that an agreement will happen in 2 or 3 days, he has been saying this for weeks, at some point the market loses faith in Trump and then prices increase. In a month things will look very different if no deal with Iran is reached. It does not look like Iran is in any hurry and Trump doesn’t want to admit how weak his position has become so this could continue for months. Maybe when Brent spot prices climb back to $138/b, Trump will make a deal, in the mean time he will try to talk down oil prices by saying it will only be another few days until an agreement is reached. It will stop being effective very soon.

Also keep in mind that there can be a very large disparity between the futures price and the spot price for WTI.

We will have to wait and see what happens.

Read the piece linked above by Kurt Cobb, it is well written and explains quite clearly and concisely why the “investment world” has its collective head in the sand.

Wild times!

Perhaps once they load the public’s stock accounts and retirement funds with SpaceX (June 12?) the market’s price finding mechanism will be allowed to function.

In the past, about 4 years ago, I was chided here when I suggested that the situation for world petrol demand had changed over the last decade. After peak we at least now had a viable alternative to ICE transport, I had indicated.

Consider that

-“Every one of the top sixteen cars sold in China was an EV in May according to China Passenger Car Association data, as gasoline-powered cars continue their structural decline in the world’s largest auto market.”

-“Amazon hit a massive milestone, deploying over 50,000 electric delivery vans globally. This puts the company exactly halfway toward its goal of 100,000 zero-emission vehicles on the road by 2030.”

The capability to deploy a wide range of EV’s seriously blunts the dire repercussions of global oil production decline. Especially for those who get with the program.

IIRC, peak ICE was about 2018, caused almost entirely by China. Chinese domestic EV sales have grown to 62% of the market, and Chinese EV exports more than doubled year over year in May, spurred by Hormuz Nuz.

Hickory

China looked at the economic facts at the turn of the century and realized that their Achilles heal was the need to import more and more oil to support their economic expansion and as a side bar possible military expansion. They came up with a simple plan, let’s pivot to EVs and power them with coal powered electricity plants. They started by funding EV research and then Tesla and Chinese companies started producing serious EVs in the mid 2000 teen years and the rest is history.

Unfortunately that thinking has escaped another major power.

“ They came up with a simple plan, let’s pivot to EVs and power them with coal powered electricity plants.”

Well, by the time EVs became a big deal China had already started to deprioritize coal. They officially recognized air quality problems in 2006, and started really doing something about it in 2013 by closing old inefficient plants and reducing coal in central cities. Since then coal has become lowest priority and wind and solar are definitively replacing them as the primary source of new generation. Renewables have even started actually reducing total coal consumption.

Yes, China is probably better diversified than most nations.

And, if people want to follow their lead, they will find that china owns all of the major markets in this area:

*Solar panels

*Silicon wafers for solar panels

*Wind turbines

*EV batteries (incl. materials)

*EVs

*Rare earths

It’s way too late to turn this around.

Dagnnabit, China also owns coal-to-liquids now.

According to AI:

“Coal-to-Liquids (CTL): The Global Gold Standard

China possesses the most advanced, largest-scale, and commercially operational CTL infrastructure in the world, having largely surpassed South Africa (Sasol), the historical pioneer of the technology.”

“China has world-class technology and the world’s largest operating capacity. It uses CTL as a strategic defense mechanism to ensure its military and transport sectors can run on domestic coal if maritime oil imports are ever cut off.”

“China utilizes both primary chemical pathways for CTL at an unprecedented industrial scale:

Direct Coal Liquefaction (DCL): This highly complex process grinds coal and reacts it directly with hydrogen under extreme pressure and temperature to create synthetic oil. China Energy Investment Corporation (CHN Energy) operates the world’s premier commercial DCL plant in Ordos, Inner Mongolia. It remains a massive feat of chemical engineering that **few other nations have successfully replicated at scale**.”

“Indirect Coal Liquefaction (ICL): This process gasifies coal into synthesis gas (syngas) first, then converts it to liquid fuels via the Fischer-Tropsch (FT) process. China has optimized high-temperature and low-temperature FT catalysts to maximize the output of ultra-clean diesel, gasoline, and jet fuel.”

THC,

Your point is well taken – China has a big lead. OTOH, the rest of the world can certainly catch up, if they decide to. Will they decide to? FF billionaires seem to have enough political power at the moment to make it hard. They can’t stop the transition, but they can protect their home markets for a while…

The rest of the world still produces a lot of “electro tech”. Tesla still sells the most popular EV (the Model Y). European wind turbines are still doing well. The US actually has a good battery industry.

As for CTL – it’s very expensive and dirty. China is understandably interested in having it as an emergency backup, but it will never be a primary industry.

Ovi, Many years back you indicated (correctly in my eyes) that a plug-in hybrid electric/ICE vehicle that was well optimized (got plenty of electric miles prior to shifting to the ICE) would be important for wider deployment.

Well, there are now lots of good vehicles like that currently out, or shortly so.

I’ve got an early spot reservation for the Scout Traveler PHEV. Not sure if I’ll pull the trigger on the purchase, but I’m watching carefully. Projected to get 150 electric miles. In this vehicle the ICE will act as a generator for the electric drivetrain, once the batteries are depleted.

https://www.scoutmotors.com/traveler

note that Coal to liquid with F-T process can not deliver good yield in jet fuel.

Venezuela heavy has good yield in jet fuel.

One reason the Waffen SS lost the air in WWII in deep winter was due to lack of aviation fuel with lower freezing point. Germany FT process could even make butter from coal, but not high % of cyclic hydrocarbons.

Koch sold the process to refine aviation and other fuels to Stalin for 3 tons of gold.

One other important technology in electrification is the ultra-high-voltage transmission technology. China deployed 800kV DC and 1100KV AC lines, while rest world limited to 750kV AC at the best.

You hook a thorium reactor to a CTL Plant.

This is what China is trying to do.

There is thorium in the coal.

You get your electricity and liquid fuels.

Oak Ridge Labs built a working Thorium reactor and abandoned it.

China has built a very small one.

Germany FT process could even make butter from coal ー>

Hmm, butter from coal! Was it tasty??

Hehe.

Most of China’s electrical energy comes from coal, so while EVs will reduce their oil consumption somewhat, the cost is a very dirty energy. It’s not that CO2 coal produces, oil does that as well, but it is the particulates, which are dangerous to human health.

Note that only 18% of China’s primary energy comes from oil.

Hickory

Yes I recall I did say that. My thought at the time was its a good transition vehicle to full BEVs and it was cheaper to buy because of the smaller battery.

A friend a few years back bought a RAV 4 plain hybrid. She use 6.5 litres per 100 km while I use 10.5 litres per 100 km in my Mazda CX-5. Her driving and mine are almost 100 percent city driving. Can’t believe the savings with just a plain hybrid.

The Scout you are looking at must be a serial drive system. It would not be as efficient as a parallel drive system but possibly simpler mechanically. I assume the engine must operate over a very narrow RPM range near its most efficient operating condition.

Mazda had a similar serial system but it used a rotary engine to power the MX 30. Not sure how successful it was. I think it was a trial horse. They are now working on an upgrade.

https://www.youtube.com/watch?v=7VCRimXqxx8

True Ovi. The manufacturers are calling this serial setup Range Extended EV [EREV].

16 Range-Extender (EREV) vehicles expected in the U.S. (2026-2029)

https://topelectricsuv.com/hybrid-trucks/range-extender-models-upcoming/

Sheng Wu

Go back to your history books. The ‘Luftwaffe’ was the aerial arm of the Nazi German military.

Since peak conventional oil (2015), we’ve now witnessed the 10 year plateau provided mainly by U.S. unconventional.

We are now locked into 6-7% decline rate which will increase each year as production decline accelerates.

In the worst case scenario, worldwide oil production approaches zero in 2040s, with the unconventional supply gone in next 10 or so years.

This would match the 1P reserves scenario that Rystad has been publishing for over a decade.

While I consider it unlikely, it represents a significant hurdle for worldwide supply and demand.

U.S. Crude Inventories Drop 9 Million Barrels in Surprise Draw

(Suprising to who?)

The American Petroleum Institute reported a 9.119 million barrel decline in U.S. crude inventories for the week ending June 5, far exceeding the anticipated 3.4 million drop. Combined with a 7.9 million barrel release from the Strategic Petroleum Reserve, the total crude draw reached about 17 million barrels, while Cushing hub stocks fell 1.125 million to 22.4 million amid high refinery runs and strong exports. Traders highlighted the bullish signal amid Middle East tensions, though prices dipped slightly to $88.70 per barrel for West Texas Intermediate, with attention now on Wednesday’s official EIA report.

This story is a summary of posts on X and may evolve over time

Hmm. So in one week:

commercial inventories dropped 9.1M (1.3M per day),

SPR dropped 7.9M (1.1M/day), and

Cushing dropped 1.1M (.16M/day)?

And the US just launched a 3rd wave of strikes on Iran:

BREAKING:

*US launches a third wave of strikes on Iran, with a massive fleet of US fighter jets now airborne across western Iran, per N12.

*Iran launches 3 ballistic missiles from Isfahan towards US bases in the Gulf.

*US strikes now in Ahvaz, Iran’s main oil region, and in Zahedan, southeastern Iran near the Pakistan border.

And yet WTI front month still below $90 — guess we’ll have to wait for real shortages to see what price discovery looks like.

Maybe this SOH crisis revealed that CHina’s crude consumption has seriously dropped significantly, 3~5MBOPD.

If China SPR is really 1G BO, and CHina has stockpiled for 2 years, then each day China demand is 1.5MBOPD less. With China refined fuel export at 2MBOPD ramped up recent 2 years, China domestic demand is 3~5MBOPD less.

With the other 1.5~2MBOPD reduction comes from alternative switching due to higher oil prices.

China’s crude import % drops from 60+% to less than 50%.

That’s an interesting thought: whatever China was putting into it’s reserves up until the Iran war was counted as consumption when it really was not.

So if, for instance, China was putting 1M per day into reserves, that should be subtracted from pre-attack consumption estimates, and it reduces the shortage accordingly.

Hi Sheng Wu,

Is the relative weakness of oil prices, given the circumstances, caused by demand destruction or other factors?

We’ve seen the financial institutions drop 250 million barrels of paper oil (net shorts) in addition to their existing positions since the beginning of the year.

And we have governments committing to 400 million barrels of SPR releases.

Combined, that’s 650 million barrels. Divide by 100 days, and that’s 6.5 million barrels a day.

Then throw on top of that China’s use of inventories (a speculation) and inventory reduction elsewhere, and I don’t see why we need to argue for demand destruction.

But as an intellectual exercise, let’s look at your suggestion that China may be consuming as much as 5 mbd less of oil now.

According to AI, in 2025 China consumed the following amounts of oil:

Petrochemicals & Plastics 4.35 mbd

Commercial Transport & Logistics Diesel 4.15 mbd

Consumer & Passenger Travel Gasoline 3.61 mbd

Maritime Shipping & Heavy Industry Fuel Oil / Marine Lubricants 1.56 mbd

Aviation & Civil Aerospace Jet Fuel 0.87 mbd

TOTAL CONSUMED BY ECONOMY All Sectors 14.54 mbd

Out of these sectors, where do you think 5 mbd might have been removed from demand in 2026?

THC,

I think that it is possible to affect futures prices temporarily, but placing of contracts doesn’t replace physical barrels (in this case, we’re talking about a contractual promise to deliver something that doesn’t exist). If consumption is greater than production, at some point there is going to be a reckoning that manipulation of derivatives can’t prevent or even delay.

Hi Nick,

Yes, I agree, paper contracts cannot replace physical commodities, and *eventually* the market will sort that out. But in the short term (as in the 100 days of the Iran war), it can have a serious impact, especially when we are talking about that many barrels.

Remember, many of the barrels sold by the banks were bought by physical users/producers, who have the right, per the Nymex specifications, to take delivery should they decide to do so.

If they wait until real shortages start to appear to try to close their shorts, they make be in trouble…..probably some vassal state of the US (like Japan) was talked into managing “temporary” oil price volatility by shorting the futures as an alternative to sending troops to “help open the Hormuz.”

China increase refined fuel export significantly in the past 3 years, and especially diesel and especially aviation fuel. Aviation fuel production from CHina used to be less than Korea or Singapore, and just 20% of US ,and now already close or even surpass US this year — all with import from Venezuela and China’s Bohai bay, S China Sea, all with higher cyclic saturated compositions, or “rare earth crude”.

https://www.linkedin.com/pulse/orinoco-oil-rare-earth-crude-sheng-wu-eta1c

I did some search on “China SPR” and many claim that China SPR is ranging from 1.3 G to over 2 G BO.

In the months just before SOH crisis, China was stockpiling over 2MBOPD.

So it seems that China’s real domestic demand has caved in dramatically in the past 3 years.

https://gulfnews.com/world/americas/37-times-trump-claimed-an-iran-deal-was-near-what-s-going-on-1.500568358

“38 times Trump claimed an Iran deal was near. ”

At some point the investment world stops believing Trump’s lies.

I feel like we’ve reached that point, but with the insane volatility and the 500 million paper barrels they dumped on the market, people are hesistant to hold long positions.

Eventually it will sort out, but it’s been a tiring journey so far.

And just what ‘deal’ would be acceptable to both [Iran/Houti/Hezbollah/Hamas] and

the [USA, UAE, Saudi, Qatar,Bahrain,Oman, Kuwait, Iraq, Israel] governments.

I think back often to ‘Imagine’ by John Lennon…’no country to live and die for…no religion too’

https://www.youtube.com/watch?v=iOs9Osz3UFQ

Trump as

“The Boy who cried Deal”

Hickory,

Finding a compromise will be difficult and may not be possible, thus the Strait of Hormuz may remain closed for many more months.

Only a Fool Would Say That

https://www.youtube.com/watch?v=Hvz0TOm0zgI

The song is widely interpreted as a cynical critique of 1960s utopian ideals and, more specifically, a direct musical jab at John Lennon and his 1971 hit song “Imagine”.

The Meaning Behind the Song: Critique of “Imagine”: Steely Dan’s founders, Donald Fagen and Walter Becker, mocked Lennon’s peace-forward, “no possessions” utopian lyrics, viewing them as out-of-touch and hypocritical coming from a wealthy celebrity while working-class people struggled in the real world.

Lennon References: The lyrics target a “natural man wearing a white Stetson hat” who is “talking about a world where all is free,” a reference to Lennon’s signature fashion and the themes of his music.

The Everyman’s View: The song contrasts the dreamer on television with the “man in the street” who works a 9-to-5 job and has to live through the harsh realities of everyday life.

Hickory- Trump on the other hand, may have done more to advance the world away from oil transportation than the green revolution has ever accomplished. Who would have guessed.

Personally, I’m rooting for $12 gasoline and a U.S. depression to send a message to MAGA’s cult of Trump and his authorian ways are a lose lose situation. Just ask Putin how well his evil has done for his country. If you can find him in his bunker(ballroom). Slava Ukraine

“Imagine there’s no oversized pickup trucks with a bumper flag.

It isn’t hard to do

Nothing to kill or die for

And no religion, too”

Gary. I get that. Wake me up when religion and country are no longer things to fight over.

Gary,

One of my favorite Steely Dan songs! Never made the connection to Imagine, also a favorite.

Thanks.

According to Drop-Site News airlines spent 78% more on jet fuel in April 2026 than in April 2025 despite using less of it in 2026. It seems like the heavy transportation fuels: bunker fuel, diesel, and jet fuel are in shorter supply than the lighter (less dense) products.

An example of the geopolitcal ramifications of this conflict-

https://oilprice.com/Energy/Crude-Oil/The-Clock-Is-Ticking-Down-To-Iraqs-Economic-Disaster-On-27-July.html

Keep in mind that an unstable Iraq risks falling even further into Irans sphere of influence. About 2/3rds of Iraqi are Shia.

It is war. An economic war that diminishes American prospects.

“The US Department of War has declared that BYD, Nio, CATL, Baidu,..” on the Chinese Military list

There are now 188 companies on the list, including many premier companies that are leaders in their industry. Modern industrial industries.

‘The newly added companies include prominent names across several sectors. In addition to Alibaba, Baidu, BYD, and NIO, the list incorporates semiconductor firms such as CXMT and YMTC, robotics company Unitree, biopharmaceutical firm WuXi AppTec, lidar specialists Hesai and RoboSense, solar manufacturers JA Solar and Trina Solar, and networking equipment maker TP-Link Technologies Co.’

If you keep up with technology innovation industries you will recognize all/most of these names, and realize what a hobbling affect this will have on the US. When you don’t compete with cutting edge products you fall further behind, and you pay more that privilege.

https://www.yahoo.com/news/politics/articles/188-chinese-military-companies-now-110001042.html

Hickory,

Spot on!!!

abduction of Venezuela “rare earth” crude is to slow down China’s insatiable growth in aviation fuel production, which is a strategic war fuel supply; and ensure US dominance in aviation fuel production distribution and risk prevention.

China Unveils Nuclear-Powered Floating Hub for Zero-Emission Shipping-

‘Jiangnan Shipyard — a subsidiary of state-owned China State Shipbuilding Corporation — unveiled a nuclear-powered floating logistics hub at the Posidonia International Shipping Exhibition in Greece, designed to serve as a container transshipment terminal, energy production centre, and vessel charging station.

The platform’s core power source is a molten salt reactor, supplemented by solar and wind, capable of producing hydrogen, ammonia, and synthetic green fuels for both terminal operations and support vessels.’

https://oilprice.com/Energy/Energy-General/China-Unveils-Nuclear-Powered-Floating-Hub-for-Zero-Emission-Shipping.html

Hickory,

Like almost all nuclear news these days, it’s a concept, not a real product. Maybe in 10 years. Maybe.

————————-

Nuclear has 2 major problems: weapons proliferation and cost competitiveness with the moving target presented by renewables & batteries. I don’t see any sign that either is likely to be solved.

Another piece on World Stock draws

https://oilprice.com/Energy/Crude-Oil/Disconnected-Oil-Futures-Market-Could-See-Price-Spike-within-Weeks.html

By the end of June 2026, I predict daily Brent spot prices above $150/bo, if the impasse between the US and Iran continues to the end of July I expect Brent daily spot price will rise above $180/b. By the end of August perhaps $250/b unless demand destruction is rapid.

Dennis,

This article suggests that the supply loss is 12.8M. What do you think?

Any thoughts on whether the price spike might be more extreme in WTI or Brent?

From a conversation with AI:

“In an extreme product shortage, WTI is structurally primed for a violent, localized price explosion because short-sellers will pay virtually any price to avoid failing physical delivery at landlocked Cushing. Brent will rise sharply based on true global supply and demand, but its cash-settlement structure eliminates the risk of an artificial, panic-induced price squeeze.”

Nick G,

I have often heard estimates like 13 Mb/d for supply loss, but believe that includes crude plus products which often includes NGL. I focus on C+C and believe that supply loss to be on the order of 9 to 10 Mb/d due to the closure of SOH. If we use crude only as reported in the June MOMR and focus on the DOC, the output loss is 9842 kb/d from the 4Q25 average to May 2026 based on secondary sources used by OPEC. If that supply loss was maintained for 90 days, that would be about 886 million barrels of supply loss. If it continues another 90 days we are up to 1772 million barrels by the end of August. At some point crude oil stocks reach MOL and then all the jawboning in the World won’t keep oil prices down.

Looks like things might be kicking off again in the Hormuz area.

WTI futures up this morning.

Some unverified news headlines (ironically Iranian news is probably more reliable in terms of ongoing events than Trump’s tweets):

1. ” The IRGC Navy has released a new statement saying that approaching the Strait of Hormuz will be considered cooperation with the enemy:

Following repeated violations of the ceasefire by the American enemy, the Strait of Hormuz will be closed until further notice.

We warn that no vessel should leave its anchorage in the Persian Gulf and the Sea of Oman. Approaching the Strait of Hormuz will be considered cooperation with the enemy.”

2. “The IRGC Navy has announced that two vessels attempting to transit the Strait of Hormuz were struck by Iranian projectiles”

3. “Mehr News Agency reports that the U.S. has struck 7 coastal areas so far.”

https://t.me/GeoPWatch

(Re this source, according to AI: Like many prominent Open-Source Intelligence (OSINT) and military-tracking channels on Telegram, the Geopolitics Watch (@GeoPWatch) channel operates anonymously. Their raw information regarding the actions of Iran and Russia is often highly accurate and incredibly fast, but their interpretations, framing, and context are heavily biased.)

“But can U.S. citizens truly stop the madness their own empire imposes on them and on the rest of the world?”

hightrekker!

hightrekker,

“But can U.S. citizens truly stop the madness their own empire imposes on them and on the rest of the world?”

Good question — currently the answer appears to be “no.”

~~~~~

Trump: Iran deal reached

Tehran: no “final decision”

~~~~~

“They lie to us, we know they’re lying, they know we know they’re lying but they keep lying anyway, and we keep pretending to believe them.”

https://youtu.be/GbkTEpjtGwE?si=PCdQADH8vay094u3&t=261

now, Art constantly use “beer” and “whisky” to tell that US is not energy independent.