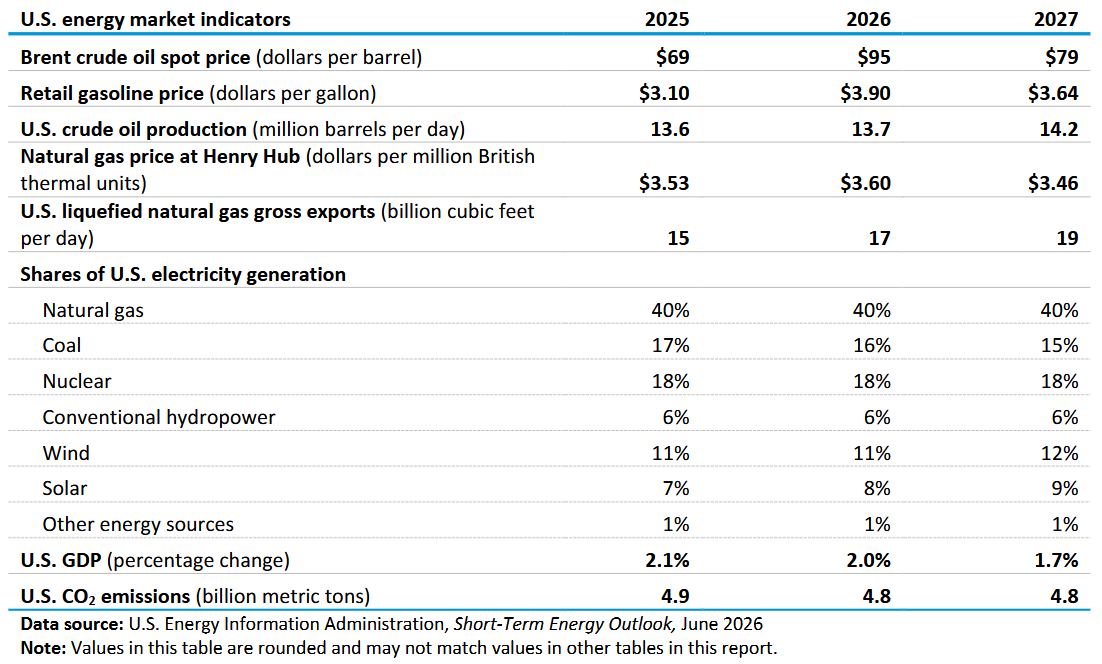

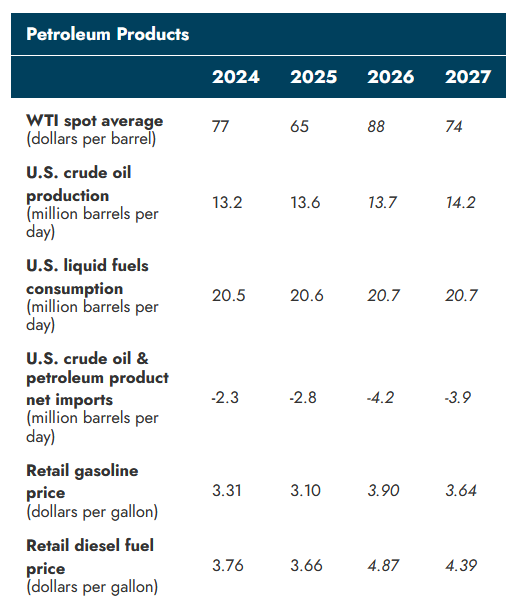

The EIA Short Term Energy Outlook (STEO) was published recently. A summary in chart form.

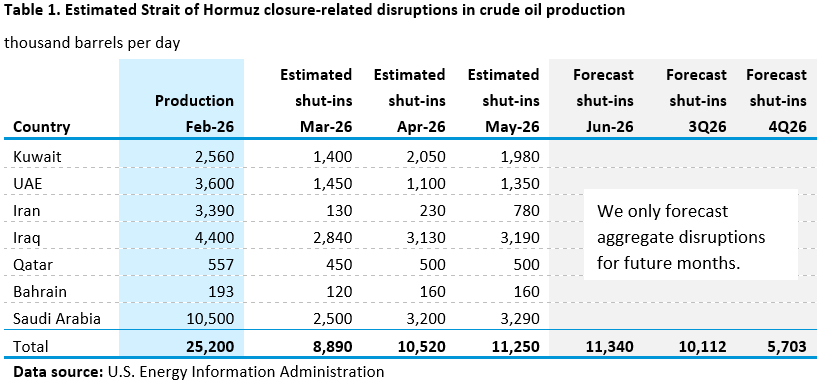

The EIA expects disruptions from the closure of the Strait of Hormuz will be reduced by 5547 kb/d from June 2026 to 4Q2026. Probably this is an optimistic assumption by the EIA.

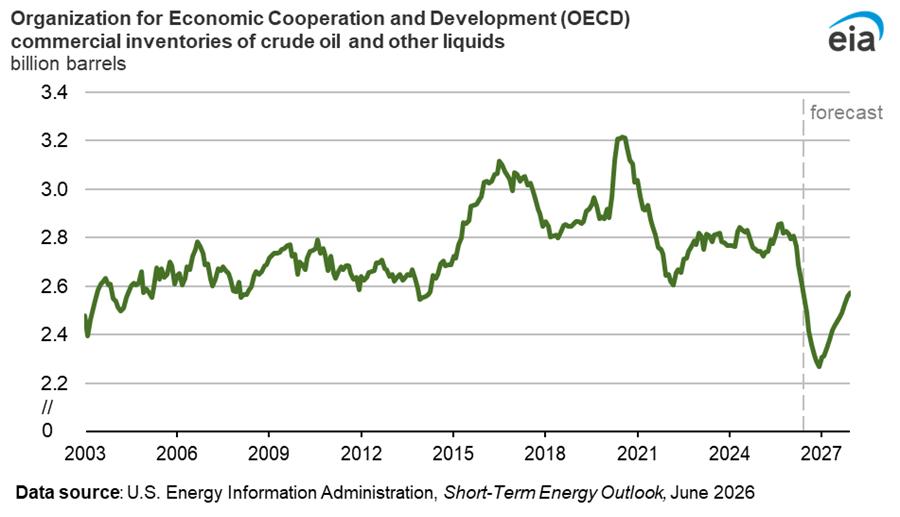

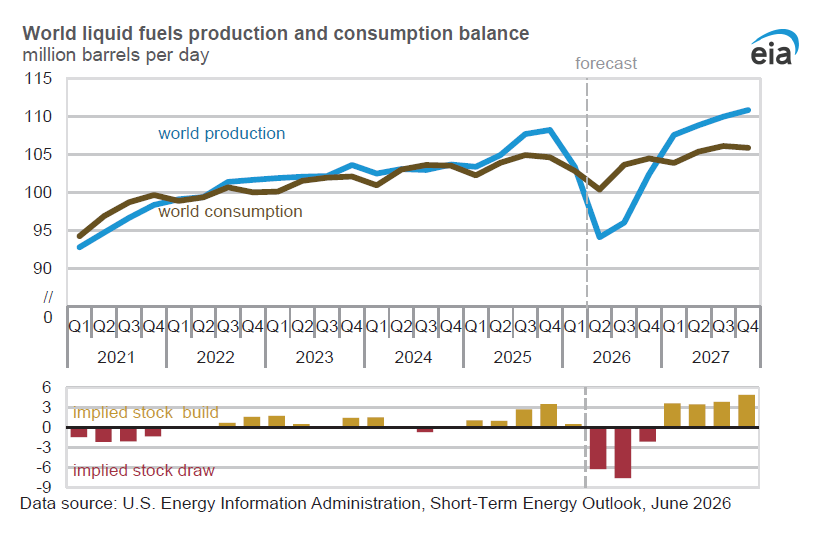

OECD commerical oil stocks are expected to rebound in 2027, but stocks will remain below the avergae level from 2022 to 2025.

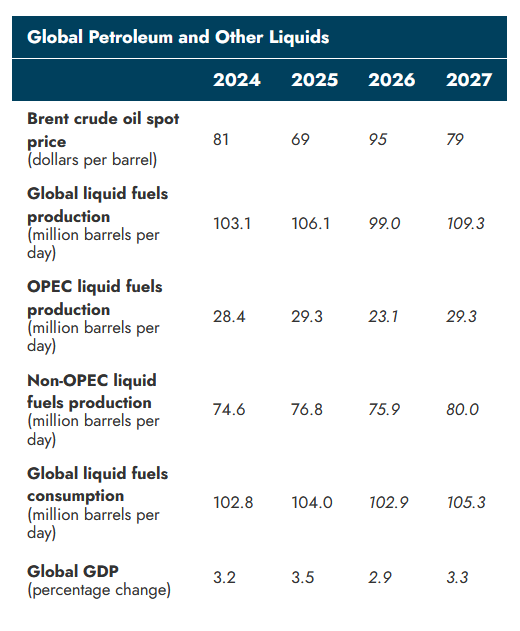

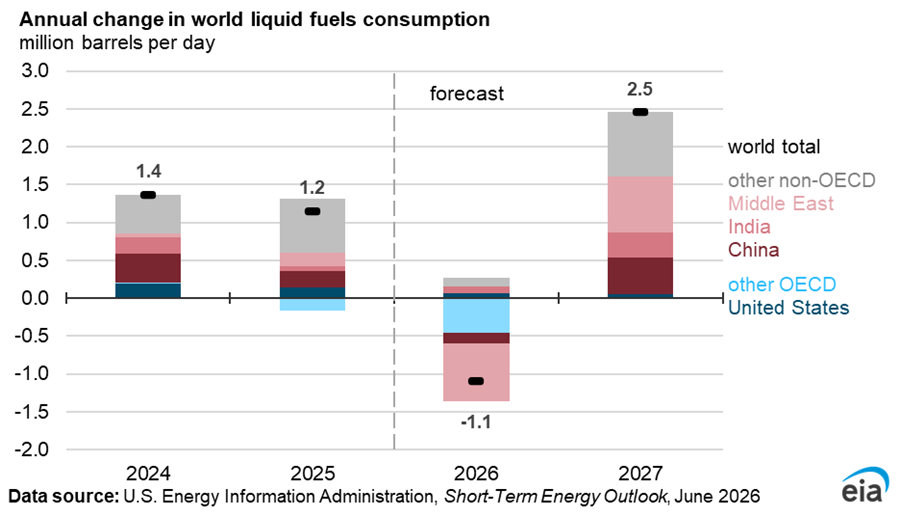

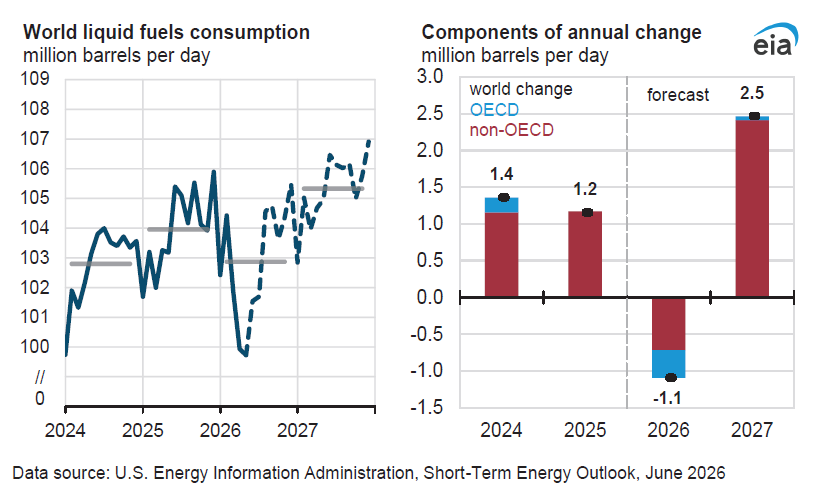

Consumption of liquid petroleum rebounds strongly in 2027 after a fall in 2026 due to higher oil prices in the June 2026 STEO.

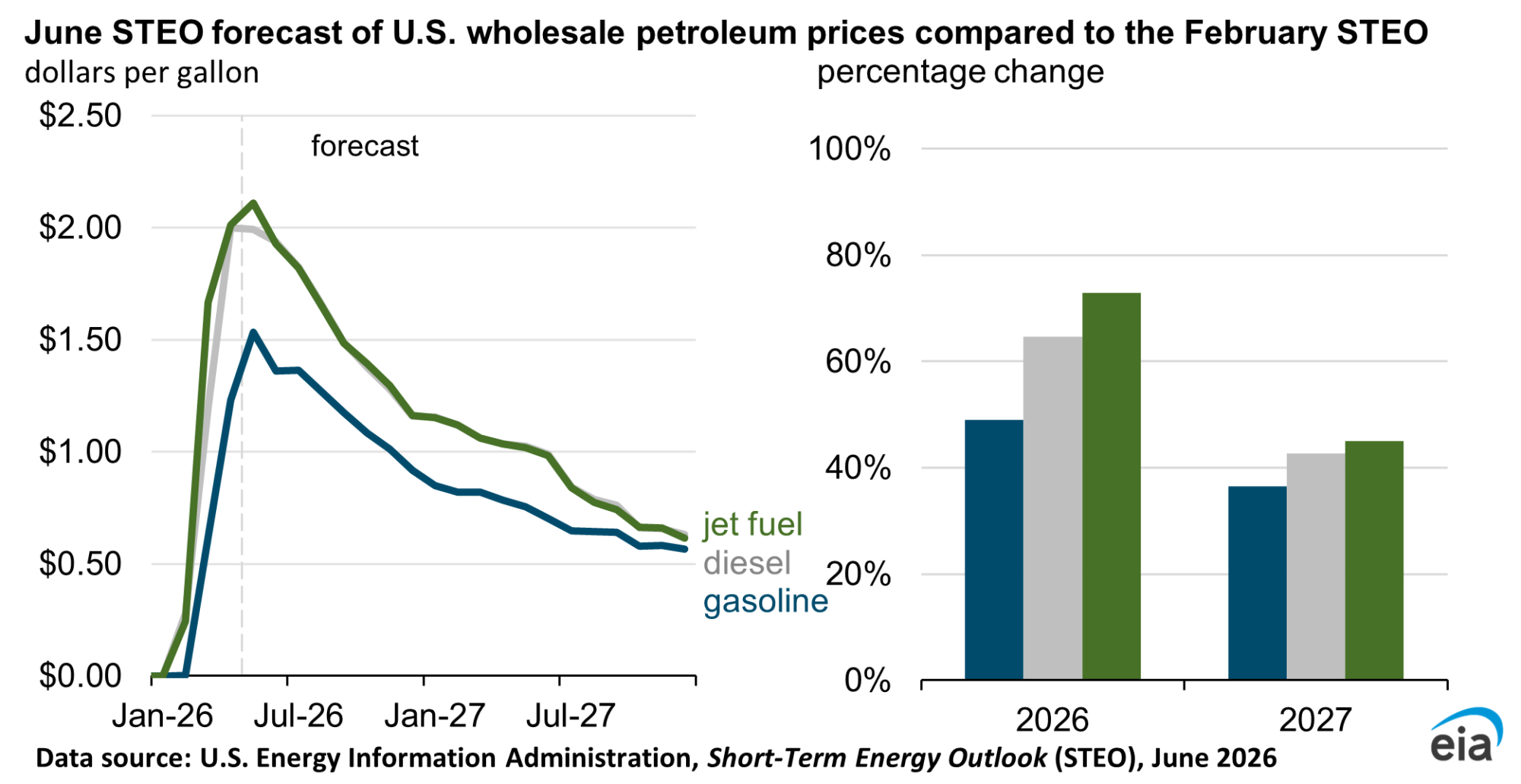

Wholesale fuel prices are expected to be much higher than forecast in the February 2026 STEO, about $1.50/gallon higher for gasoline at the peak and about $2/gallon higher for jet and diesel fuel.

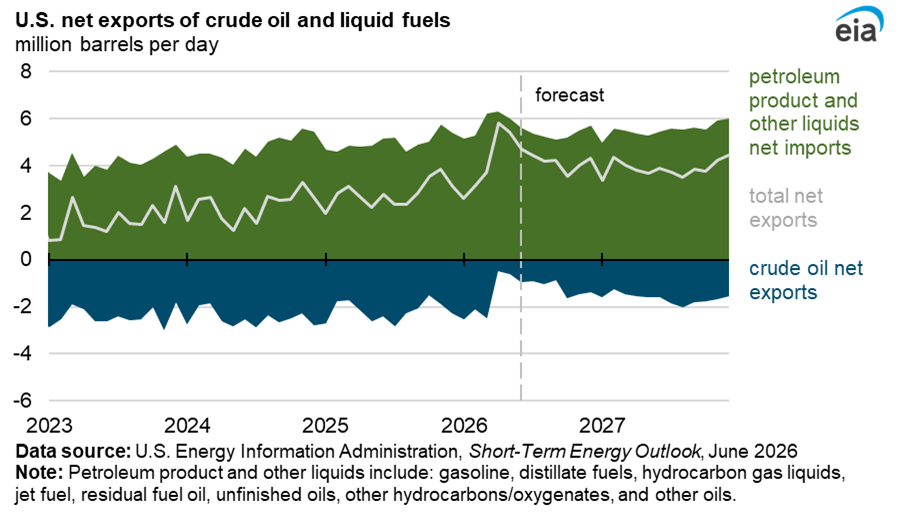

Net exports of crude and petroleum products are forecast to be higher, much of this is from the US SPR.

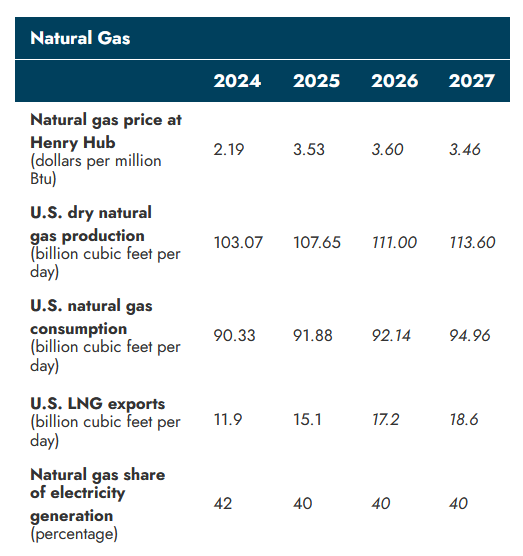

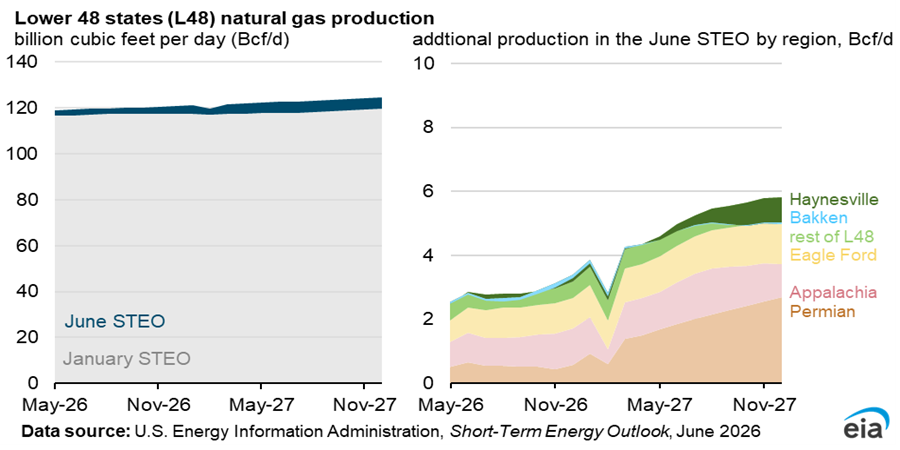

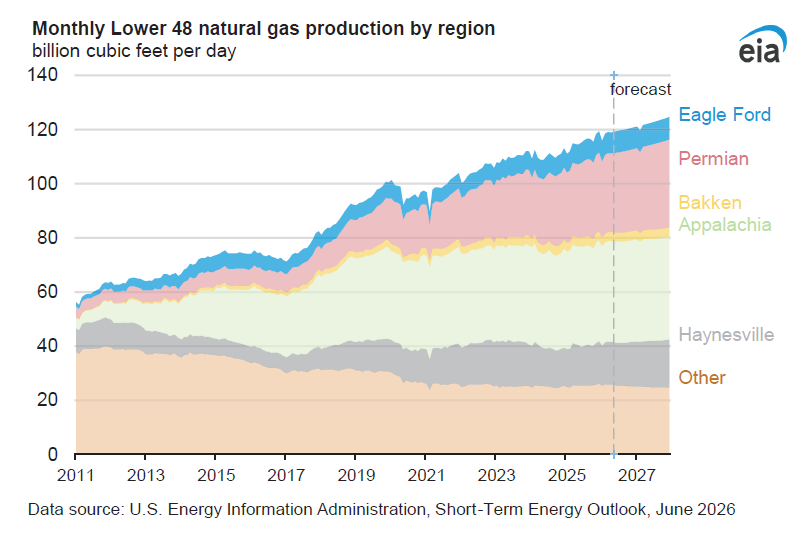

US natural gas output increases by about 6 BCF/d from 2025 to 2027 in this forecast with about half being consumed in the US and the rest being exported.

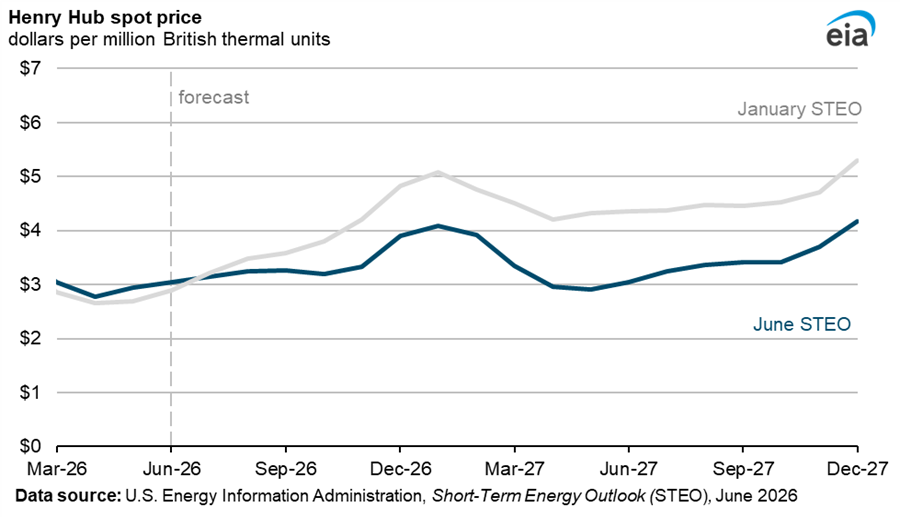

The STEO forecast for natural gas production has increased compared to the January 2026 STEO and this results in lower natural gas prices in the June STEO compared to January.

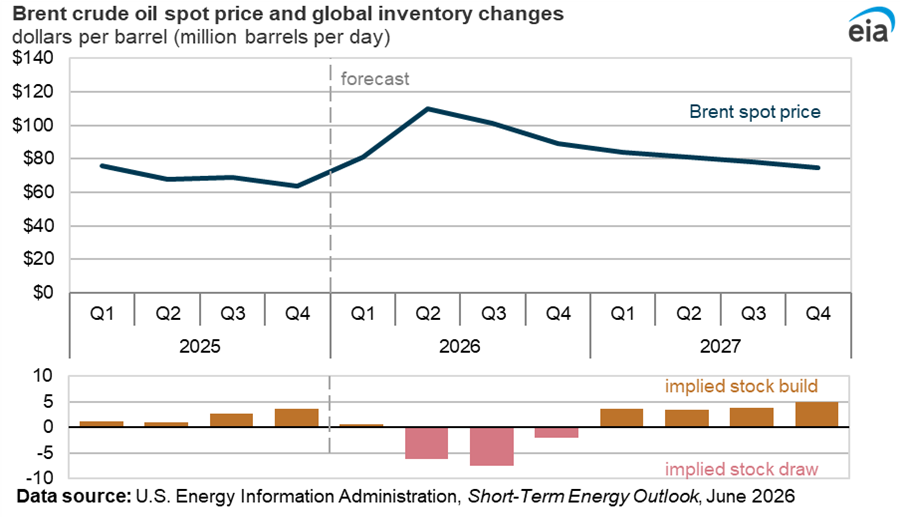

The EIA expects a stock build in 2027, we will see, again seems optimistic.

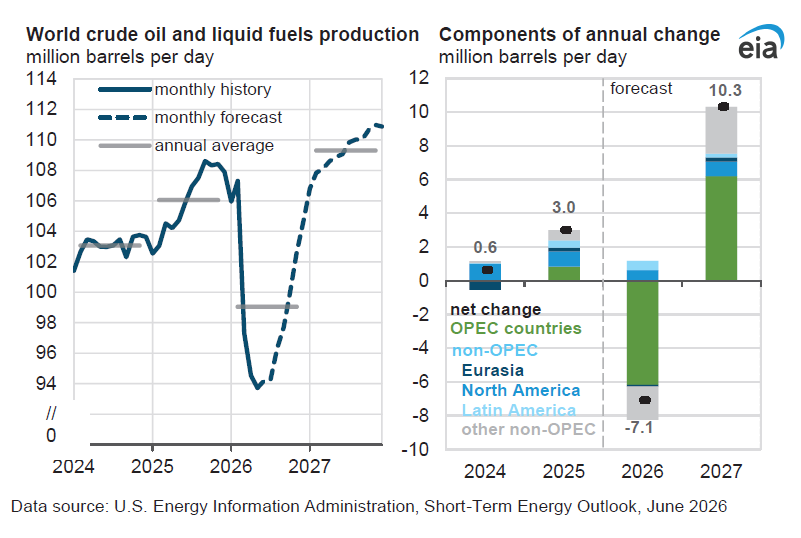

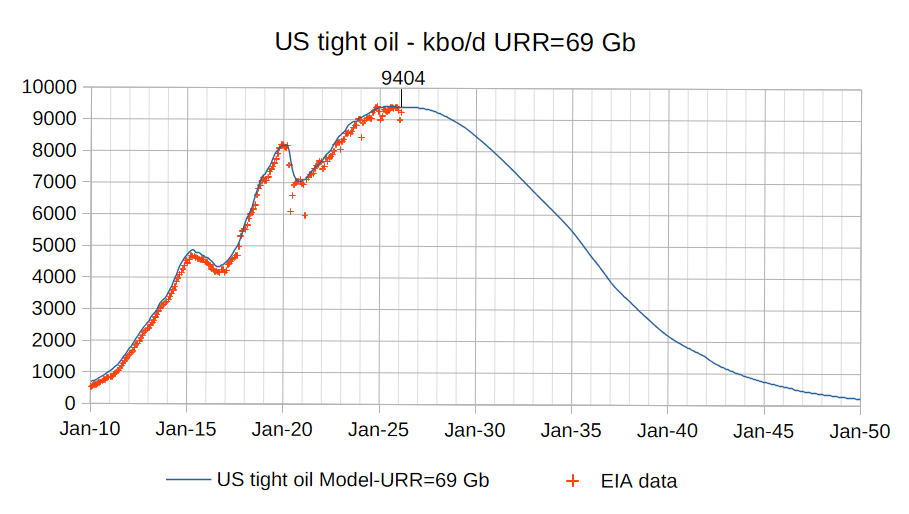

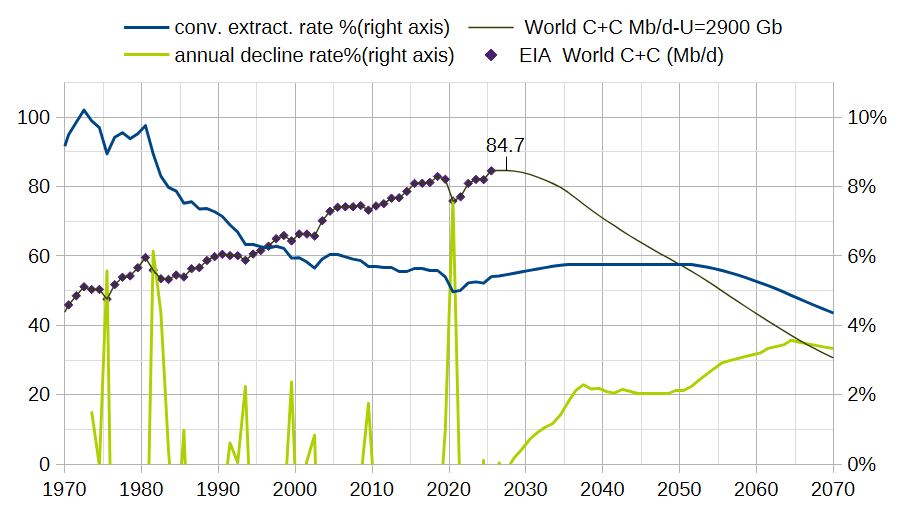

The scenario above uses the US tight oil scenario from previous chart. URR=2900 Gb for World C+C, peak is 2027 at 84.7 million barrels per day.

152 responses to “Short Term Energy Outlook, June 2026”

THC, I think you will appreciate this link

IRAN STRIKES TANKER IN HORMUZ DESPITE U.S.-IRAN PEACE DEAL – w/ Energy Expert Anas Alhajji

Anas talks about where and how the oil has been flowing during the war in the second half of the link.

https://www.youtube.com/watch?v=y_0lb8b5P3g

Hi Gary,

Thank you for the link to Abas’ interview.

I’ll give it a listen.

I listened to him a month or two back, and he had some unusual takes. He suggested that despite the claims of the Hormuz being closed, some were getting out by paying bribes to corrupt Iranian officials.

Side note:

I’ve been listening to some of the Mario Nawfal’s content, and I have to wonder how he manages to lign up so many interviewees and put out a new polished long-form interview seemingly every few hours.

I also get the feeling that he is now positioned as some form of promotional platform for influencers and narrative creation.

I also notice he appears to be flashing a Masonic hand symbol in his youtube profile photo (not evidence of anything, but perhaps he belongs to a “club”).

HI again Gary,

Thanks again for the Anas interview. I got about halfway through, and found it interesting.

minimal damage to oil production in Venezuela, probably Orinoco is distant from epic center and suffers much less; while the old conventional Macaibo field was close to epic centers.

https://www.reuters.com/business/energy/petrochemical-complex-venezuela-restarting-following-quake-firefighters-say-2026-06-25/

Thanks for the post D C, informative work as usual. The EIA seems to be treating the Hormuz closing as a short term blip. It would be interesting to have a timeline of how much oil they assume will exit the Persian Gulf to make this forecast.

Shinzy,

See

https://www.eia.gov/outlooks/steo/data/browser/#/?v=30&f=M&s=0&start=202401&end=202712&linechart=~COPR_OPEC&maptype=0&ctype=linechart&map=

For OPEC crude oil forecast (most of the change is Hormuz). And link below.

chart(128)

For World Oil Production and Consumption estimates by the EIA in the June STEO see

https://www.eia.gov/outlooks/steo/data/browser/#/?v=6&f=A&s=0&start=2022&end=2027&linechart=PAPR_WORLD~PATC_WORLD&id=&ctype=linechart&maptype=0&map=

Thanks DC. So the EIA thinks production will start to recover in July. Not sure this will be true as it seems that the U.S. and Iran are back to shooting at each other.

Still can’t figure out the price of oil. It seems we are heading for shortages of diesel and jet fuel and yet Brent is less than $75 / barrel.

Seems to assume oil consumption will recover very quickly to where it would have been before the events of the last 3 months. That seems unlikely, even if production recovered completely (which also seems unlikely).

Nick G,

I agree the STEO forecast seems quite optimistic about both future oil production and consumption.

Chart below (at link) compares EIA’s International Energy Outlook (IEO) 2023 with my Oil Shock Model. There is a tendency for the EIA to be optimistic about future oil output, the IEA scenarios tend to be a bit more realistic.

shock and ieo 2023

What if we exclude NGLs, condensate, tight oil, oil sands/bitumen, biofuels, refinery gains, etc? Do you think it has declined since 2008?

P5 2 Tb

P25~2.25 Tb

(Low but plausible)

P50 / median ~2.4 Tb

(best guess)

P75 ~2.55 Tb

Strong plateau / reserve-growth case

P95~2.8 Tb

Using 2005 to 2010 as conventional peak:

The narrowest defensible estimate for cheap conventional crude URR is ~2.28 Tb, with a tight working band of ~2.22–2.34 Tb.

Why exclude those other forms of liquid fuels, other than for a bookkeeping exercise?

Does it change how many people can live, or perhaps where the money (and bombs) flows?

Thanks.

Kengeo,

We would not exclude condensate as C+C is the standard for “oil” since at least 1970 and probably long before that. The US does not even track crude only production in its data sets at the EIA. So any sensible analysis includes condensate. Excluding NGL makes sense and I do that in many cases (STEO mostly has all liquids and crude at the World level). My shock model presented in the post has 2700 Gb for World conventional C+C, that is my best guess for a mean URR (F50) for conventional C+C.

I can see a mean URR for conventional oil (excludes tight oil and extra heavy oil) of 2400 Gb based on Hubbert linearization using years from 1994 to 2025, but would note that such an analysis often underestimates the URR. An HL using years 1984 to 2000 results in a URR of about 1700 for conventional oil which is clearly too low with about 1523 Gb produced through 2025.

“Using 2005 to 2010 as conventional peak:

The narrowest defensible estimate for cheap conventional crude URR is ~2.28 Tb”

Cheap meaning less than $200/b in 2015 dollars?

C+C is just a reporting category and condensate should not simply be ignored. But separating crude, condensate, and NGLs is not just a bookkeeping exercise; it matters because these barrels are not economically or functionally equivalent.

A barrel of conventional crude, especially middle-grade refinery feedstock, is not the same as a barrel of ultra-light condensate or an NGL barrel. They differ in refinery value, product yield, energy density, transport/handling, and end-use flexibility. Condensate can be valuable, but often as diluent, splitter feedstock, or petrochemical/naphtha-linked material rather than a direct substitute for balanced crude oil. NGLs are even more distinct and trade into different markets.

For total liquids supply, C+C or all-liquids makes sense. But for questions about cheap conventional crude, refinery-compatible transport fuels, geopolitical leverage, and how much high-value liquid fuel the system can actually rely on, it is useful to separate these components.

That doesn’t mean condensate has no value, it means counting it together with conventional crude can hide degradation in barrel quality. A 2.7 Tb conventional C+C URR and a 2.3–2.4 Tb conventional crude estimate may both be reasonable depending on the definition. The key is not to treat every liquid barrel as equal just because it appears in the same statistical category.

On “cheap,” I would define it less as a single fixed price like <$100-200/b in 2015 dollars, and more as crude that can be developed and supplied without requiring structurally high prices, extreme fiscal stress, or major unconventional/extra-heavy upgrading. In that sense, the 2005–2010 conventional plateau is informative because it occurred despite very strong price signals and still did not produce a durable new conventional crude growth cycle.

The core conclusion is that “cheap oil” should not be measured only by posted Brent or WTI prices. Cheap oil means a system where large volumes of high-quality crude can be produced with low decline rates, low capital intensity, and broad refinery compatibility. That system likely peaked or plateaued around 2005–2010. What followed was not a return to old cheap oil, but a substitution: tight oil, condensate, NGLs, deepwater, oil sands, and more complex barrels filled the gap.

By 2035, the world may still have plenty of liquid hydrocarbons, but the average barrel will likely be more differentiated: more condensate and NGLs in some regions, more heavy/sour or ultra-light mismatch issues, more dependence on a few low-decline supergiant regions, and more vulnerability to drilling slowdowns in tight oil. The “End of Cheap Oil” was therefore not best understood as an immediate end of liquid fuel supply. It was the beginning of a new regime where total liquids can be sustained, but only with more complexity, higher reinvestment needs, lower average barrel quality, and greater sensitivity to both geology and demand transition.

Kengeo,

We don’t have good data on the historical split between crude and condensate so it is difficult to guess on URR. I agree NGL should be considered separately. Perhaps conventional crude only is 2400 Gb, difficult to say, my bust guess for conventional C+C IS 2700 Gb.

Without proactive solutions, FF or ICE might have died 50 years ago

in 1970s, three shocks happened,

1. lead gasoline was uncovered to kill civil society like lead pipes did to Roman empire

2. smog from gasoline was uncovered to kill civil society like smog chambers

3. OPEC embargo

Then, the industries came with 3 positive inventions,

1. non-leaded gasoline

2. catalytic converters

3. along with more efficient engines, the ICE numbers added a zero instead of removing a zero.

same for the source of FF, when we ran out of medium and light sweet crude, new refineries are able to process heavy and sour. THen, North sea, GOA, ALASKA, shale oil and more gas are utilized, and added 100% to total consumption.

Even the old all forgotten coal got a 2nd life when China more than doubled total coal consumption.

Now, situation is much different — the western industries totally got lost. We have to blame the IPCC and EU doomsday policy.

Like Bill Gates also recently admitted, the biggest threat is not climate change itself,

https://www.cnn.com/2025/10/28/business/bill-gates-climate-change

Although the mainstream likes to laugh “drill baby drill”, they are even more laughable if they don’t have a solution and only ready for doomsday.

If China could use coal as the major step stone to the next level of energy for civilization, then the west has to admit their doomsday policy failure.

In the 1980s, there was already a failed doomsday “greenpeace” terrorists, and they were not successful as this time fighting to slow down any industrialization — nuclear to Brazil’s rainforest development.

DC – The BP/Energy Institute dataset is actually quite useful because it separately reports NGLs, so the crude/condensate stream can be analyzed apart from NGLs. Then the main adjustment is separating conventional C+C from unconventional barrels which are primarily U.S. tight oil and Canadian oil sands, with smaller caveats for places like Argentina tight oil and Venezuela extra-heavy oil.

There are estimates of global condensate production, but not a clean free annual public series in the BP/EI dataset. JODI and EIA generally report crude oil including lease condensate, while NGLs are separated. IEA has published condensate estimates, and those suggest global condensate rose from roughly 6 mb/d in the mid-2000s to about 9 mb/d by 2020 — roughly 0.2 mb/d per year of growth over that period. So condensate growth is material enough that C+C growth after 2005 can overstate growth in crude-only production.

Kengeo,

EIA has crude only data in STEO, using that and EIA C+C data from 2003 to 2025 we can find the percentage of condensate to C+C at the World level, from 1998 to 2003 condensate was less than 1%, no data for crude only prior to 1998 at EIA. Chart at link below

condensate to C+C ratio

Thanks, Dennis — this is very useful, and sobering.

It implies that conventional crude may have peaked as far back as 2002. It also suggests that remaining 1P conventional reserves are quite limited — perhaps only ~300 Gb or so, depending on definitions and reserve quality.

The biggest takeaway for me is that, over the last decade, global conventional oil decline rates appear to have been fairly steady in the 4–5% range, with a gradual upward drift. But the forecast now appears to roll into a much steeper, accelerating decline profile:

2024: ~6%

2026: ~7%

2027: ~8%

2029: ~9%

2031: ~10%

2033: ~13%

2034: ~15%

2035: ~18%

That suggests we may be approaching the exponential decline phase — where the long tail remains, but the annual loss rate becomes increasingly difficult to offset with new supply.

Kengeo,

Note that this data includes conventional and unconventional oil, the rise in the percentage of condensate is likely due to the increase in tight oil output, if we exclude tight oil the numbers might be quite different, but we do not have such a data set for crude oil only. So I believe your assumptions are incorrect. Conventional crude which I define as World C+C minus tight oil output minus extra heavy oil output peaked in 2014. World crude output will not decrease at more than 2 to 3% per year in my view.

URR for World Crude will be at least 2900 Gb and perhaps more if oil prices rise.

**Events after Friday close of US financial market trading**

*U.S. aircraft struck Iranian missile and drone storage locations and coastal radar sites

https://x.com/CENTCOM/status/2070607101207232829?s=20

*Iran struck multiple high value US Army positions in the region

https://x.com/HormuzLetter/status/2070646987813159266?s=20

~~~~~~~~

This also kicked off:

Lebanese army depoyed against protestors upset with puppet gov’t agreeing to allow Israeli army to stay in Lebanon.

https://x.com/maxosintintel/status/2070629173488505093?s=20

Israel is publicly discussing how they could manipulate Lebanon into a state of civil war:

Ravi Drucker, host of a popular program on Israel’s Channel 13:

“The Israeli plan in Lebanon is to divide the country and plunge it into a civil war to force the Lebanese government into a military confrontation with Hezbullah!”

https://t.me/Middle_East_Spectator/33926

~~~~~~

It does not look like these peace negotiations are anything more than a distraction for the public while the chess pieces are moved around for round 2.

“Distraction”

Again, that suggests a master plan. It seems pretty clear that the US, Israel, Iran, and the Gulf states are all uncoordinated. Not to mention that there are competing players in the White House, and apparently a number of different voices in the president’s head.

Hi Nick,

““Distraction”

Again, that suggests a master plan.”

It suggests that there is deception going on, which is a common element of warfare.

Whether the deception is coordinated between multiple parties, and if so which parties, is hard to verify for an outsider.

However, it would be naive to exclude the possibility of US/Israel collusion against Iran and Lebanon (and Iran/Lebanon against US/Israel).

On January 15, the Pentagon reported a change in the Unified Command Plan shifting Israel from U.S. European Command (EUCOM) to U.S. Central Command (CENTCOM).

https://www.washingtoninstitute.org/policy-analysis/moving-israel-centcom-another-step-light

Hmmm. That article about CENTCOM is 5 years old. If the move was intended to improve collaboration between the US and Israel, it appears to have failed.

The problem here is that there is no evidence of good planning – the Iran war was a complete failure. At the moment the only deception that is clear is the president trying to portray the MOU as a success.

BREAKING: Iran likely struck another tanker vessel with drones/missiles with damage to the ship’s bridge.

The vessel was transiting through the US-approved Omani alternative route, which the IRGC did not agree with.

THC- on Israel/Lebanon it is very simple.

Israel is extremely motivated to survive and so will go to any extreme measure to disarm and or disable those attempting to eradicate it- Hezbollah, Hamas, Islamic Republic of Iran.

Thats it.

And I’m not all that sure that they will survive. Looks like Iran will come out of this greatly enabled, over the next 5 years.

Problem is- no place to go. And you better believe that they know it in their deepest core.

Hi Hickory,

Apologies if I came out souding as “for” or “against” one or more of the countries involved with the Hormuz/ME conflict.

My primary interest right now is to understand current oil flows, inventory levels, and whether the Hormuz is going to return to normal, or if the recent semi-closure is a “new normal.”

When I read the MOU, it does not look anywhere close to something that the US, Israel, and Iran could all be serious about implementing.

Lebanon is one area where there is a major disagreement.

And of course the strikes and counter strikes this weekend……..are we still in a ceasefire?

If I owned a fleet of oil tankers I doubt I would want my ships to go back in through the Hormuz once they had left.

Agree. Imagine how this is all going down if you happen to be one of Gulf countries not named Iran.

Rig Report for the Week Ending June 26

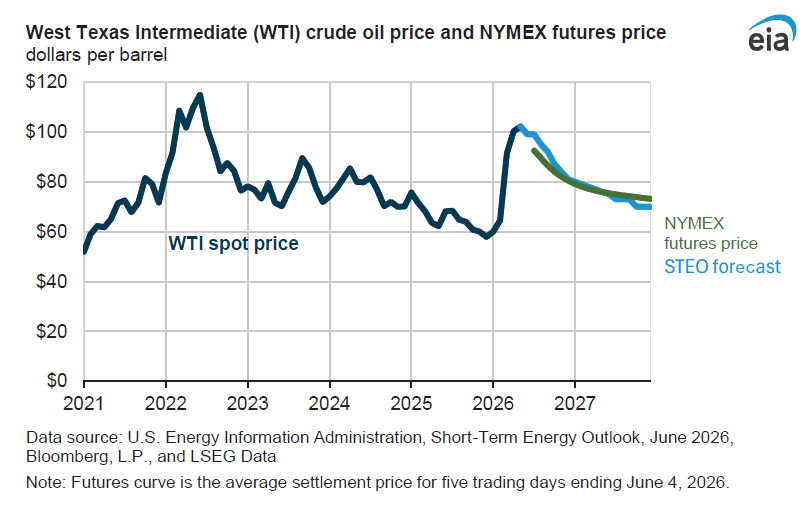

The dropping rig count that started in early April 2025 when 450 rigs were operating had a big increase this week. The Rig count broke above the previous steady rate of 367 ± 5 rigs per week since August 2025. Today WTI closed at $70.24/b, down from $77.54 last Friday.

– A big question here is whether the decision to deploy these extra rigs was take a month back when crude was over $90/b. At $70/b, will these rigs make any payback today?

– US Hz oil rigs rose by 7 to 379, down 71 since April 2025 when it was 450. It was also up 17 rigs from the low of 362 first reached in the week ending August 1, 2025. Regardless of the increase, the rig count is still down 16% since April 2025.

– The New Mexico Permian Hz rig count was unchanged at 70. Both Eddy and Lea were unchanged at 37 and 33 respectively.

– Texas added 3 to 198. Midland added 1 to 22 while Martin was unchanged at 23. The biggest change was in Reeves where 2 rigs were added.

– Eagle Ford was unchanged at 34.

– NG Hz rigs added 1 to 105.

– Directional rigs (Drigs) rose by 1 to 56. While Eddy county was unchanged at 20, Texas Drigs were also unchanged at 15 for this week.

A Rig

Thanks Ovi,

Everyone should keep in mind that rig count increases today takes about 8 months to impact tight oil output, so the 7 rig increase at the end of June might lead to some minor increase in tight oil output at the end of February 2027 assuming no change in average well productivity due to technological improvements (increasing productivity) or due to pressure depletion (which will decrease average well productivity per foot of lateral).

My guess is that any technological improvements will be overwhelmed by accelerating decreases in average well productivity as sweet spot areas become very crowded. A 17 rig increase over a 10 month period (roughly 2 per month on average) is unlikely to be enough to increase tight oil output and may lead to gradually falling tight oil output.

it is like all bubble industry, need some sizable catalysts.

Like shale oil become real shale oil, i.e. Bakken high Shales are now producible!

There is an analysis of the AI bubble, that the difference of AI bubble and previous .com bubble is that AI bubble built way too many data centers.

Dennis

I am wondering if the blip up in Permian production which you show in this chart from above is future production from those extra 14 Drigs that have been added to Eddy county.

Could this affect your model?

A Perm

Ovi,

Not clear the extra directional rigs will have much of an effect, since week ending May 8 the directional plus horizontal oil rigs in the Permian increased by about 7%, so we might see an increase in output 8 months after May 8 (Jan 2027). A modified model for Permian at link below which accounts for the horizontal and directional rig count and the possible affect of the increasing rig count we have seen since the end of May for horizontal plus directional rigs in the Permian Basin. Output increases by about 130 kb/d from May 2026 to Dec 2027 for the Model, note that higher rig counts might just replenish the dwindling DUC inventory and falling oil prices might lead to a lower completion rate than this scenario (leading to lower output.)

The Permian region forecast from the STEO has Permian output increasing by 730 kb/d from May 2026 to December 2027, it will be 230 kb/d at most using optimistic assumptions that ignore ongoing pressure depletion in the Permian Basin and lack of profitability of tight oil plays under $80/b at current natural gas prices in West Texas and New Mexico.

permian260629

Frac Spread Report for the Week Ending June 26

The frac spread count rose by 8 to 200. From one year ago, it is up by 21 spreads but is still down by 15 since March 21, 2025.

A Frac

Suggest we recall a few things here:

1. Public media reports that EIA has lost 30%-40% of staff under current administration. Probably aren’t too many or any independently wealthy among the remaining staff.

2. Current administration has gleefully gutted technical expertise across federal agencies.

3. Current administration has quite clearly indicated what the ‘right’ answer is with respect to fossil fuels and the disruption caused by the war with Iran.

The EIA is part of the DOE, led by Wright. He’s the boss. A few excerpts from Wikipedia of the complete and intentional disconnect from reality:

-The Union of Concerned Scientists said Wright “deliberately misrepresents climate data and research.”

-In September 2025, Wright wrote on social media platform X that “Even if you wrapped the entire planet in a solar panel, you would only be producing 20% of global energy.

Points to bigger phenomena. Over my life I have generally thought that knowledge, literacy and fact were gradually gaining ground on ‘belief’, ignorance or misguided thinking.

Are we now backsliding on this, or is it just the USA?

Trump has been the greatest force in a hundred years against truth telling, science, honest debate, and rules based order.

And yet the country seems to have some serious hunger for this. We drew the joker card and many are so cloudy minded they think they are seeing a king.

I am not at all confident that a pendulum swing fixes this deeply embarrassing and degraded condition of ours.

At least US are able to turn on ACs at full throttles, while EU left with only climate change.

There is a video of how Chris Wright tried to kiss ass of boss and his MIT heritage, and got embarrassed.

https://www.youtube.com/watch?v=p3ydgAAM4_k

Hey Hickory

I haven’t seen any good global metrics on this, but the story for the US is clear as noted in a recent Pew Research report.

https://www.pewresearch.org/science/2026/01/15/americans-confidence-in-scientists/

It is incredible to see how the split by party affiliation is much larger than the other variables they consider. I can’t help but think about an aunt that was paralyzed by polio as a child and then look at all the anti-vax, anti-science people in my rural area. Tribe over fact. It does seem like the rise of social media and various right wing media outlets are also very effective with their propaganda on topics like climate change.

I agree that a pendulum swing won’t be enough. This administration has done and continues to do permanent harm to the US and the world. The oil exports that some (rightly) complain about on this site due to strategic reasons are certainly part of this foolishness, but a pretty small part.

The mainstream climate doomsday scientists have fooled and doomed the western civilization, now EU need an AC revolution to completely reverse the mainstream climate scientists.

IPCC and EU should be charged with civilization disruption and inhumane crimes.

Sheng Wu- have you considered that your viewpoint on this issue might be heavily swayed by you having a personal vested interest?

In the past, people in relatively cool summer zones have done just fine without AC. Those places are frequently experiencing hotter and hotter summer days. This includes where I live in Seattle the area where AC has gone from rare to now over 50%.

Actually very funny to see you blame the need for AC on ‘climate doomsday scientists’, as if the temperatures would be cooler if they just would stop talking about it.

Don’t look up!

“We lost the last fight over the means of production, and then the winners gave it away. We should not let them do it twice.”

I suppose there are those who think of thermometers as a science doomer plot-

June 28th- Paris France

“Paris, the capital of France, has recorded more days above 40°C [104F] this week than during the 147-year period spanning from 1872 to 2019 combined”.

https://www.dailymail.com/news/article-15934661/Astonishing-moment-South-Korea-blasts-drone-swarm-sky-military-drill-finishing-laser-cannon.html

South Korea demonstrates ability to blast drone swarm out of the sky.

GOSH GOLLY? I wonder what they think is coming …………………

with love,

Nostrodamus the Giant

Nice guns!

But it looks like they shot down maybe 20 or so drones all grouped together.

I wonder how they would do against hundreds or thousands of drones approaching from different angles and directions:

https://www.youtube.com/watch?v=LpaSXwpKzGk

Next generation drones land in trees and wait.

NG drones will have Starlink communication and AIG processing

“Next generation drones land in trees and wait.”

Whoa, that is nuts…….

I’m just making things up but it seems that loitering on a branch or somewhere undisturbed would be a useful capability.

A year ago, there was talk of drones that could land on a power pole to recharge.

haha, IPCC and EU will require drones to have solar/renewable and USB C

LeeG — Drones that wait on the side of the road are already common.

Sooooo……..

**Friday June 26**

30 minutes after WTI futures and stock market trading closed, the US attacked several Iranian targets, setting off a round or two of attacks on targets by both Iran and the US.

**Monday June 28**

30 minutes prior to the beginning of the WTI and stock indice futures trading overnight session, Trump mouthpiece Axios announces “U.S. and Iran agree to halt strikes and meet this week (in Qatar)”.

If this is true, Iran appears to be actively participating in the US’ manipulation of the oil and stock markets.

But manipulating oil to the downside is ostensibly against the interests of Iran (as the oil price is part of their leverage).

This whole thing may involve more kayfabe than most can imagine.

This is getting tiresome:

#BREAKING 🚨: Iran’s Deputy Foreign Minister Kazem Gharibabadi says there are currently no intentions of holding meetings with US officials from the “technical teams” in Qatar this week.

And another reverse course. Can’t trust either side’s statements.

~~~~~

Iran confirms technical negotiations in Doha

The country’s deputy foreign minister stated that the expert delegation is in Qatar solely to monitor the implementation of the memorandum of understanding through the Qatari mediator, and not to meet with the US counterparts.

Key points of Kazem Gharibabadi’s statement:

🔶 Experts will work on blocked funds in Doha

🔶 Working groups will only start talks if “necessary conditions” are met

https://t.me/SputnikInt/106302

Dennis

Did you see my question just above the Frac Spread report?

Ovi,

Just replied a few minutes ago.

Dennis

Thanks.

Eddy is not doing well now, I will continue to track it in the US posts and see if production picks in in late 2026,

ww ii Iran invasion, UK US collaborated with USSR

https://www.youtube.com/shorts/yKhMWpgqNeE

The Energy Institute has published it’s annual report.

https://www.energyinst.org/statistical-review?utm_source=Master+Mailing+List&utm_campaign=8935f907c2-EMAIL_CAMPAIGN_2025_08_26_10_19_COPY_01&utm_medium=email&utm_term=0_-320c1b4f51-454004622

Ron’s claim that Peak Oil was in 2018 has been clearly dispelled.

Dennis’s made and assertion several years ago, that global coal consumption peaked in 2018. 2021 saw the 2018 high broken and After 4 years of consumption increasing each year since, we can sadly say Dennis was wrong.

Claims by certain people here in the past, that solar and wind growth would ensure that gas consumption along with coal would decline each and every year. Where is island boy now?

A prediction he made in 2016 I do believe.

Sad to say global CO2 emissions are higher than ever and increasing global heatwaves, floods and storms are baked into this broth we have cooked

TYS,

In 2018 I might have claimed that peak consumption of coal was in 2014 as that was what the data showed at the time, I often say future consumption is not known, which is always a correct statement, true with 100% probability. Anyone who claims something different will be incorrect 100% of the time.

Do you have prediction of when oil and coal consumption will peak? If so you will no doubt be incorrect.

The analysis I did in 2016 is at link below

https://peakoilbarrel.com/coal-shock-model/

An excerpt:

The peak for world coal output will be sooner than most people think, the range is 2013 to 2045, my estimate is 2025 to 2030 with peak output between 4 and 5 Gtoe/year (2014 output was about 4 Gtoe/year).

1 Gtoe is roughly 42 EJ, so my best guess in 2016 for peak coal output in Exajoules was 168 to 210 EJ between 2025 and 2030.

In my Coal Shock model post in 2016, I suggested a best guess URR of 570 Gtoe for World Coal, the chart below uses my high and medium coal scenarios from that post with URRs of 510 Gtoe and 630 Gtoe and averages them, those scenarios are compared with Energy Institute data just released. The peak for this scenario is 191 EJ in 2032, note that this scenario is certain to be incorrect as the future is unknown.

coal shock 2607

Never forget the 3 largest oil exporters all are facing significant risks:

1) USA – Permian basin decline and other issues (water, etc)

2) Saudi Arabia – In the Middle East; Strait of Hormuz

3) Russia – Inching towards war with NATO, Ukraine is hammering their oil infrastructure.

If the dice turn up a certain way, oil importers could be hurting in a big way.

DC

Peak Oil was considered by yourself and other as the most pressing issue facing humanity. The geological decline of oil would gravely impact billions of people.

Today there are just a few people who think a geological oil peak is important. Global electric vehicle sales are set to hit 23 million, that’s one in four vehicles.

LNG powered ships are becoming more popular and could completely replace oil demand.

https://sea-lng.org/why-lng/global-fleet/

Today geological peak oil has become almost irrelevant.

You wrongly believed that wind and solar would reduce coal consumption, what you failed to study is exactly how much energy would be required to power all those electric cars, vans and other machinery.

Electricity demand has increased from 24 thousand Terawatt hours to 32 thousand in just 10 years.

God alone knows how much electricity would be required to power 1.8 billion cars and lorries.

Have you seen global sales of air conditioning units.

The number of units in existence has risen from 1.2 billion to 2.5 billion in 15 years.

https://www.statista.com/chart/22703/air-conditioning-by-region-country/

And with global warming, billions more people will want this luxury enjoyed by many Americans.

To meet that demand we will burn everything we can get our hands on.

Peak Oil has been replaced by a far worse threat. Relentless heat waves and droughts and there is no technology that will fix it.

https://climateandeconomy.com/2026/07/02/2nd-july-2026-todays-round-up-of-climate-news/

The number of countries where fresh water availability is reaching crisis point has only got worse. Europe is one bad year away from extreme water rationing.

TYS

I never thought peak oil would be a big problem, except for China’s rapid expansion of cod consumption in the 2000 to 2010 period, growth in coal output has been relatively gradual, it will take time to replace fossil fuel for energy use, solar output has been growing at 30% per year, in time fossil fuel demand will likely fall.

Also natural gas will also peak as will coal, resources deplete and as they do they become more expensive to produce.

Average annual growth rate for coal in my URR=570 Gtoe scenario from 2014 to 2033 is roughly 0.73% per year.

DC

Again not studying the data properly.

https://www.energyinst.org/__data/assets/file/0004/1827616/Statistical-Review-of-World-Energy-PDF-Report.pdf

Renewables increased from 32.2 exajoules to 35.4. That’s about 10%.

Many people don’t want to think about the consequences of global warming, the increasing droughts, floods and fires devastating infrastructure and the natural world that we need to survive.

Soil erosion running at 75 billion tonnes, add to that desertification and soil salinity. We have now hit peak affordable food.

Food cost which had been declining for decades since the 1930s thanks to tractors, combined harvesters. Pesticides and herbicides. Most importantly farmers all over the world draining the fresh water reserves that would take a century of rest to refill.

https://unu.edu/inweh/news/world-enters-era-of-global-water-bankruptcy

Many people are utterly uninformed of the water crises, how much is used and what it would take to store, clean and desalinate enough to ensure not just enough water for people. Relatively doable. But to ensure enough water to irrigate the crops where aquifers are depleted.

Fact is not much is done because those in power have ensured they and their powerful friends will survive. They know the global population is far too high and is destroying the planet.

A reduction of 3 to 4 billion is required to balance natures ability to regenerate.

Watch food prices go through the roof!

I know there are Canadians who read here so maybe you can help on this.

I received a report by email that stated Canadian oil inventories are at minimum operating levels, which are 30 million barrels.

Canada apparently doesn’t have an SPR.

This seems very low to me, given per EIA the US is importing between 3.5 million and 4 million BOPD of crude oil from Canada.

If anyone has insights on Canadian crude inventories I’d appreciate it.

SS

Canada does not have a strategic reserve.

Canada has commercial/private reserves owned by private companies. Companies like Suncor, Cdn Natural Resources and Imperial Oil would have tanks of Synthetic Crude or Western Canada Select in for example Calgary.

If the oil is heading for the US, it is mostly transferred to Hardisty Alberta where it is transferred into pipelines heading into the US and across Canada.

Out of curiosity I asked Google how much storage capacity is in Hardisty. This is the answer I got and may explain your 30 M barrels.

Hardisty, Alberta is Canada’s premier crude oil storage hub, featuring a total storage capacity of over 20 million barrels. The site consists of approximately 100 massive, dome-capped storage tanks operated by major midstream companies.

Key operators at the hub include:

– Gibson Energy: Operates approximately 14 million barrels of storage across four separate terminal locations, handling roughly one out of every four barrels exported from Western Canada.

– Enbridge Inc.: Operates approximately 10.5 million barrels of storage, which includes 7.5 million barrels of above-ground contract storage and 3 million barrels of salt cavern storage.

– Husky Midstream: Manages about 5.9 million barrels of commercial storage capacity at the hub.

I hope this helps

Hi Ovi,

If Canada’s premier crude oil storage hub only has a capacity of 20 mmbbls, Cushing really is a beast of a tank farm!

THC

Add up the tank volumes

14 + 10.5 + 5.9 = 30.4 Mbs.

Regardless Cushing is a big beast

Thanks Ovi!

Yes, duly noted.

US April Production: Another Record High

A US

Wow, didn’t expect that.

Neither did I?

Thanks Ovi,

US increase in April was 216 kb/d with 119 kb/d increase in Gulf of Mexico output and a 36 kb/d increase in Texas output and a 65 kb/d increase from New Mexico, the 3 area combination increased by 220 kb/d accounting for more than 100% of the US increase.

From Energy Aspects:

“China has not stopped buying crude. It has stopped buying crude for now.

What our proprietary data shows:

→ The 3–4 mb/d import drop combines halted strategic purchases and run cuts. Both are reversible.

→ Petrochemical stocks are tight and margins are strengthening. Runs will recover.

→ EA estimates a floor for Chinese runs at around 12.5 mb/d.

→ The moment China returns to spot purchases, the prompt market tightens. The buffers to absorb that move are largely gone.

The glut story is premature. The data tells a different one.”

https://x.com/EnergyAspects/status/2070451229478547878?s=20

On reaching new highs in production:

Quite a few conventional wells (and the rare unconventional) are choked back for longevity. When oil goes over $90 you’re going to loosen the choke and try to catch up with what has been a very long span of time during which the U.S. government has done its best to ruin the domestic oil industry. It’s actually pretty amazing how profitable some of those wells are when prices reach a level where they should be.

The rationale for “ckoking back” is to prevent the reservoir’s natural pressure from declining too rapidly, which would leave significant oil unrecoverable, So sure, if prices get high and profits too tempting, the flow might get opened up, but then depletion will hasten.

And don’t forget a major process in oil flow is dispersion — the harder you drive it the deeper some of it goes as you really can’t herd all the oil molecules like you can sheep,

It is criminal to keep releasing oil from the SPR if we are heading into a major oil glut, as the big banks are now forecasting.

I’m glad to see even our conservative oil producers now understand that President Trump wants nothing more than to see us suffer.

Nothing in moderation when it comes to him.

He also doesn’t give a damn about the US farmer, he just sends bandaids out for farmers now and then. Corn below $4 and beans below $11 cash at our elevators.

Yeah, it’s nuts.

Recent SPR loan tenders had barely any takers.

Perhaps going forward those who borrowed from the SPR will be happy to buy back at $69 what they borrowed at $110 or so?

Where do those returning SPR oil loans need to park their oil to return it? Does anyone know the details of how this is done and the rate at which SPR loans can be returned in mmbbld?

WTI $67 / barrel

Gasoline $123/barrel

Heating oil $134 / barrel

Insanely good profit margins for refiners.

Do any of Trump’s kids or cronies own oil refineries?

the energy industry is not as profit/price driven as tourism, fast food or entertainment.

The shale oil industry should not thrive or even survive after 2014 if it is following profit driven.

Same for alternatives, like China solar & battery industries drained approximately similar amount as US shale oil industry?

But, both are now the strategic pillars for China and US energy supplies.

EU initiated the SAF program for aviation fuel, and now CHina finally approved the merger of China Aviation Oil Company and SINOPEC, aiming to dominate the SAF

https://www.yicaiglobal.com/news/sinopec-cnaf-merger-could-boost-aviations-green-transition-lead-to-fuel-price-cuts-analysts-say

all the renewables initiated by EU led extremists are coming back to bite them.

In 2008, when China was mired in smog caused by coal and one geologist leading CHina academy of science in IPCC laughed at the clowns at the IPCC Parisian and asserted that in 2 decades the west will completely give up IPCC and reverse the cause.

Sheng Wu,

Those last 2 paragraphs don’t make any sense. Please put more time into writing carefully.

Without proactive solutions, FF or ICE might have died 50 years ago

in 1970s, three shocks happened,

1. lead gasoline was uncovered to kill civil society like lead pipes did to Roman empire

2. smog from gasoline was uncovered to kill civil society like smog chambers

3. OPEC embargo

Then, the industries came with 3 positive inventions,

1. non-leaded gasoline

2. catalytic converters

3. along with more efficient engines, the ICE numbers added a zero instead of removing a zero.

same for the source of FF, when we ran out of medium and light sweet crude, new refineries are able to process heavy and sour. THen, North sea, GOA, ALASKA, shale oil and more gas are utilized, and added 100% to total consumption.

Even the old all forgotten coal got a 2nd life when China more than doubled total coal consumption.

Now, situation is much different — the western industries totally got lost. We have to blame the IPCC and EU doomsday policy.

Like Bill Gates also recently admitted, the biggest threat is not climate change itself,

https://www.cnn.com/2025/10/28/business/bill-gates-climate-change

Although the mainstream likes to laugh “drill baby drill”, they are even more laughable if they don’t have a solution and only ready for doomsday.

If China could use coal as the major step stone to the next level of energy for civilization, then the west has to admit their doomsday policy failure.

In the 1980s, there was already the failed doomsday “greenpeace” terrorists, and they were not as successful as this time IPCC+EU to disrupt civilization/industrialization — nuclear to Brazil’s rainforest development.

Sheng Wu,

Recent quote from mayor of Paris regarding use of air conditioners …

“… makes the problem worse by heating the city even more”.

Meanwhile, the IEA predicts that 85% of Chinese households will have A/C by 2030.

Over half of Chinese electricity comes from coal plants.

1.4 billion Chinese are benefitting from modern conveniences while ~70 million French are sweltering.

C’est la vie.

Cushing below MOL, SPR lowest since 1983, traffic through hormuz still not back to normal, but no one is panicking… WTF?

https://www.zerohedge.com/energy/wti-holds-losses-spr-drain-slows-cushing-just-tank-bottoms

That one guy,

Breathtaking isn’t it?

But as they say,

“The cure for low prices is low prices”

Hopefully this drop will not cause too much damage before the invisible hand of the marketplace sorts things out.

They are writing of a 3-4 mbpd surplus next year, even after SPR refill buys. That’s enough to bring the prices down (it’s all paper in future trade anyway).

Iran and Venezuela will increase production, Shale increases anyway. 2$ gas prices incoming, please vote Trump.

Let’s see if the prices will stay deep after the midterms…

Hi Eulenspiegel,

Does that 3-4 mbpd surplus exist in addition to satisfying the refill demand for the 1 billion barrels or so of production that was lost this year? (with SPR loans repayed at +10 ~20% in barrels).

It’s counted as surplus after refill demand already satisfied. A kind of oil cornopia, with low prices and abundant supply.

For example this one: https://thebull.com.au/news/oil-forecast-is-a-multi-million-barrel-surplus-approaching-in-2027/

That’s enough to move the paper market – for example they account the strong reduced chinese demand where other sources say China simply taps their good filled storage tanks instead of paying high prices.

“2$ gas prices incoming, please vote Trump.”

Damn Yankees is about a middle-aged, long-suffering fan who sells his soul to the Devil so his beloved baseball team can finally defeat the dominant New York Yankees.

THC,

TRUMP PAUSED WAR TO MANIPULATE OIL PRICES – w/ Philip Pilkington

https://www.youtube.com/watch?v=4QRpMjgE-pw

Why Oil Prices Are Diverging from Fundamentals

https://www.youtube.com/watch?v=OakeC8zQzJM

Hi Gary,

Thanks for the links!!!

It’s so hard to figure what is really going on in the Middle East right now.

The EU is now saying the fees might be unavoidable (= acceptable and semi-permanent?):

~~~~

Some European countries now accept that ships transiting the vital Strait of Hormuz will have to pay fees to Iran and Oman

https://x.com/business/status/2072687507754393760?s=20

WTI Futures curve at link below from

https://oilprice.com/futures/wti/

The price of WTI oil is expected to fall to $55/b by August 2036. No new tight oil wells will be drilled in the US at that price which would be about $43/b in 2025$ assuming an average inflation rate of 2.5% per year for the next 10 years.

WTI futures 2607

And we know official inflation data wildly underestimates inflation:

https://www.shadowstats.com/

THC,

For an alternative perspective search on billion prices project. Bottom line is that cpi data is pretty good, shadow stats is bunk.

Hi DC,

Thanks for sharing that.

This may not be the right forum to do in depth on this and we both probably don’t have the time, but I would guess one could probably pick, choose and adjust one’s metrics to arrive at the desired outcome.

Super simple example — if you want to argue for inflation, just compare how much a dollar can buy in gold, if you want to show low inflation, compare how much corn or oil one could buy.

It feels to me like fiat currency is being inflated to high heaven, but that’s a subjective/anecdotal observation.

Oil & gas have never done well under a Republican president. The same is true for farmers. I couldn’t tell you why that is, even under torture.

But the president is doing pretty doggoned well, according to the newspapers. I knew I should have moved into bitcoin.

My impression from a brief reading about the president and crypto is that he didn’t do bitcoin (which has dropped by a third since January 2025), it was another cryptocurrency, and that he did well while a lot of other investors did quite badly…

https://www.youtube.com/watch?v=iNvwpbbZTPc

Trump created his own coin. The UAE invested heavily in it.

Only an idiot or a foreign government looking to bribe would put money into a Trump created financial instrument.

Most of the 2.2 billion he earned came from his version of “Bit-Coin”

We did pretty well under George W Bush.

2005 and 2006 were good years for us. We even drilled some good wells those years.

They admittedly weren’t fun for our men and women in the military

Andre is correct, trump invented $trump out of thin air that’s what a meme coin is: air. On the announcement (around his inauguration) the total value was bid up to billions with him holding 80% of it. Crypto is great for criminals, the perfect method of payment. The $trump meme even makes you sign a waiver that you won’t sue him when you lose, what a racket. This will be seen as far bigger than Teapot Dome, Agnew’s bags of money and Nixon’s slush fund put together. Wanna pardon? I’ve got some biggly crypto to sell you…

https://en.wikipedia.org/wiki/%24Trump

https://finance.yahoo.com/news/trump-reports-2-2-billion-232324833.html

Trump made 2.2 billion in his second term first year.

Don Jr and Eric were awarded a “No-Bid” contract from the government to develop/produce drones.

https://www.telegraph.co.uk/us/news/2026/05/28/trump-drones-don-jr-invest/

What do these two know about drones?

I wish the Pentagon would offer me a multi-billion dollar contract to start a business I know nothing about, that no other company is allowed to bid against.

These guys are brilliant businessmen /sarc

I looked at Ember’s data for Chinese coal burning. They provide electricity produced by coal, and CO2 emissions. I suspect CO2 is a better measure, because the Chinese have been working hard on increasing the electricity produced per unit of coal, so CO2 emissions will track actual tons of coal burned better than electricity produced. It looks like 10/23 was their peak in coal consumption.

I don’t seem to be able to upload a chart, either PNG or JPG, about half a MB, from a folder or from an iOS photo album.

Nick,

The chart has to be downsized to under 55 kilobytes to be uploaded. Often changing to a gif format is smaller, usually I do this in Excel though there are many different ways to do this. Also you can put the image on Google Drive and simply share a link to the file here.

Canadian governments (federal and provincial) has agreed to a new major pipeline to bring Alberta oil to the west coast (Vancouver area) to serve the export market. 1 Mbpd additional export capacity.

https://oilprice.com/Latest-Energy-News/World-News/Alberta-and-Ottawa-Greenlight-New-Pacific-Pipeline.html

“Canada’s oil production has been growing robustly despite environmentalist opposition and federal government policies. This year, it is expected to hit 5.3 million barrels daily. The only export corridor to markets other than the United States, however, is the Trans Mountain pipeline, already running at capacity due to the surge in demand for Canadian crude amid the Middle Eastern war.”

Hickory

This was a political announcement but also a very real one.

I don’t think that Canada can add 1 Mb/d of export capacity without a significant expenditure of capital to increase production which won’t be there at $60/b WTI down the road. Maybe a 500 kb/d pipeline might make more sense,

I think the idea is to divert more oil from the US to try to reduce the $12 to $15 discount between WTI and WCS. I also think the US may try to squeeze Canada by importing more from Venezuela.

Note that Maduro was removed but the regime is the same and somehow the sale of Venezuelan oil is funnelled through the US. Why does that make sense?

“Why does that make sense?”

I suppose its about the bully exerting control. Its a big theme in the ways of man.

Canada will assert the WCS discount to be less than $5/bbl, otherwise the oil will be diverted to Pacific.

With the Venezuela crude now controlled by Trump, WCS discount will be over $20 if Canada did not build the pipeline.

I am reading a number of reports by analysts expecting an oil glut and very low oil prices by 2027 on the order of $60/b. If correct we can expect a crash is US tight oil output as new wells are not profitable to drill and complete under $80/b and with declining new well productivity this number will continue to fall. It is also not clear that many deep water offshore or Arctic oil projects would be profitable at an oil price deck at $60/b or less.

Any projected supply glut is likely to be very short lived as production will fall until oil prices reach a level where profits return. This is very basic Econ 101. The oil business is not a charity, the idea is to make money for shareholders. At $60/b in 2026$ this will be a challenge in many oil basins.

Or…this president will find another way to subsidize oil producers: the intangibles accelerated writeoff has been there for a long time, and this president added expensing of “tangibles”, and also reduced royalties paid on publicly owned land.

Dennis what you say makes sense. However the rig count and frac Spread count continue to rise.

Ovi,

We will see what happens if oil pricey remain low. Frac spread data includes both oil an natural gas focused spreads so is less useful.

Most of the tight oil is from the Permian and the sum of horizontal and directional oil rigs in the Permian shows a small increase since early March which may reverse. The important number is C+C output in US, I expect we will see this stagnate if oil price remains low.

All right, here’s the chart of monthly Chinese coal consumption (based on CO2 emissions) – we see a peak at October 2023, followed by a plateau:

China Coal CO2

Nick G,

That peak in China’s coal demand is now likely tied to the massive Deflation hitting China. While this has been happening for several years, it is picking up speed.

https://www.youtube.com/watch?v=-ngXh2f1P8c

steve

Nick G,

That peak in China’s coal production is likely linked to the massive Deflation hitting the country. While this started after the Pandemic, it picked up even more speed since the collapse of the domestic real estate market.

This could spread to the rest of the world…. can you imagine… a Deflationary Depression, vs Inflation?

https://www.youtube.com/watch?v=-ngXh2f1P8c

steve

meanwhile-

“China’s nominal GDP is projected to reach roughly $20.85 trillion in 2026, with annual economic growth tracking between 4.5% and 5.0%. The current trend shows a two-speed recovery: robust, tech-driven export growth and industrial output are keeping the economy afloat, while domestic consumption and the real estate market remain sluggish”

China population peaked in 2021-22.

MIT news- “Research on consumption-based carbon footprints indicates that roughly 20% to 30% of China’s overall fossil fuel emissions are attributed to the production of goods for international export. Because coal drives over 50% of China’s energy footprint, a similar proportion of its total coal consumption is tied to global supply chains [export to support other countries demand].”

Hickory,

Just watch that video…

steve

Rig Report for the Week Ending July 3

My initial look at the numbers was a bit of a shock. Hz oil rigs up 33. NM +20 and Tx +14. After slowly sifting through the numbers it appears that most of the directional rigs have been re-classified to Hz rigs. The one number that makes the most sense for the week is the sum of Hz + Drigs is up by 5.

The biggest change occurred in Eddy county. Eddy went from 37 Hz rigs to 56 while the Drigs went from 18 to zero.

In Texas Midland and Martin were unchanged at 22 and 23 respectively. Reeves went from 20 to 24 Hz rigs while the Drigs dropped by 3. A number of counties dropped 1 Drig.

A rig

Frac Spread Report for the Week Ending July 3

The frac spread count rose by 5 to 205. From one year ago, it is up by 29 spreads but is still down by 10 since March 21, 2025.

A Frac

This guy sounds like the talking heads I’d expect — he cites others calling for Brent at $130-140 right now, but prices are lower than before the war, with the largest crack spread in history. The big thing: China’s lowered imports aren’t demand destruction, and our demand sure hasn’t dropped either. It’s the same as our overall consumption pattern — we’re not actually using less, we’re drawing down commercial stocks and the SPR to paper over the gap and calling it stability. Same move as the household running the credit card instead of cutting spending. Makes me wonder how bad the unwinding is going to be when the tab comes due.

youtu.be/rnAgMMP1hu8

Zactly.

100% Pops!

https://x.com/MarioNawfal/status/2073474423810637859?s=20

“The “oil glut” has a math problem: 1.3 BILLION barrels VANISHED from the market this year, and nobody is refilling the reserves…

Philip Pilkington came back armed with the numbers everyone’s talking around.

His question cuts through the noise: if crude is really slopping around cheap and unwanted, why is the Strategic Petroleum Reserve still being emptied instead of restocked?”

The tab may never come due. The Saudis shipped a lot of oil during the blockade from their Sanju port on the shores of the Red Sea, coming in via the east-west pipeline. The pipes were built for 7-million bopd but the loading was limited to five; that has been addressed. They are not laying more pipe but the UAE is doubling their pipeline capacity from Abu Dhabi to Fujairah, on the Oman side, well past the chokepoint. That will put them at 3-million bopd from the Abu Dhabi fields, and that is mostly Murban which is prized as a feedstock for aviation fuel. Iraq has turned into a big producer and they’re enlarging their export capacity. Since they’re up in the far recess of the Persian Gulf, they’re going the other way, into Turkey with most of theirs. Bahrain already had a network of pipes laid out before this debacle began, and they’re following through in high gear. Qatar hasn’t done much, but you get the drift: the Arab states are not only piping around the Strait of Hormuz but they’re increasing production. I’m not making accusations I can’t back up, but there have been a number of large deals in the UAE and KSA regarding real estate transactions.

Right now the United States is producing more oil than OPEC, especially with the UAE out of the OPEC alliance. Ukraine is putting Russian refineries and tankers out of commission. Soon the pendulum will swing, as the OPEC and the UAE will try to make up for lost time. This war between Ukraine and Russia can’t go on forever, as Russia is running out of men to throw into the meatgrinder. So if the Iran “deal” goes through, every country will be able to fill their strategic reserves using inexpensive oil. Even if it doesn’t go through, the sanctions are off for Iranian oil and the rest of the neighboring countries have figured out a way to get oil to export links. Venezuela can’t get up to huge levels without a lot of time and money, but they can produce enough to significantly quell new oil production from Canada.

This all has the stench of quid pro quo, and it leaves the American producer in a bad situation if WTI goes down to $50, where the president says he wants it. Drilling a big well used to be a head-scratcher: investors would talk about the seismics and proven wells that had been drilled into similar fault blocks, ancient sand channels running into shallow oceans, then an earthquake a few million years ago that created a facies shift, forming a stratigraphic trap. Amplitudes were examined, and all the great new ways of looking for oil were discussed ad nauseum. And you’d place your bet and go for it, knowing there was a chance you’d lose your whole nut. Not so these days: this shale basin development is like a factory line. At every point there is some nuance but unless you’re a rank amateur you,re going to hit enough light tight oil to pretty much get your investment back, and if you get lucky you’ll drill smack into one of these special sweet spots with an EUR of 650-700 barrels. There are enough guys wearing Luchesse aligator boots to keep this going until it’s as empty as a longneck beer bottle on Saturday night in Midland.

So the big price boom may have already happened. In fact, I’m betting it has. This administration wants cheap gasoline and diesel at the pump, low-priced aviation fuel, another “miracle” in the Middle East, and bragging rights to the lowest price at the pump of any modern president. This conundrum, as they say, is not your father’s Pontiac. The UAE wants Dubai to become the Las Vegas of the world, so glitsy and full of excess that every nutcase with the price of a trip will show up. They can’t do that without some additional help. The KSA wants Noem to become a rival, and it is faltering. These countries are so rich and eager to join in as fleshpots that they will put the pedal to the metal on oil production, even at a $50 price tag. Venezuela has no option. If Mr. Trump sets the price tag, nobody will have an option. Including the American shale oil guy losing his ass.

Gerry,

We will see how much gets produced at low prices. My guess is that over the longer term not very much.

OPEC is likely to cut back output if the cartel survives. If it doesn’t oil prices might go very low due to competition for market share. US and Canadian production might fall like a rock if oil prices fall to under $50/b.

At prices that low profits will be minimal and future oil investment may cease so that supply falls to match demand.

Steve suggested above that China’s peaking of coal consumption was probably linked to a severe deflation. I think the logic would be that deflation means less economic growth, and less growth means less electricity, and less electricity means less coal.

But…Chinese overall electrical generation grew by 19% from May 2023 to May 2026.

Coal consumption dropped by -1%.

Coal’s share of generation dropped from 60% to 50%. In just 3 years.

Here’s the data:

China Coal

..…….. CO2…… %…… Total TWH

5/23 422.05 60.11 726.04

5/26 417.89 50.38 862.72

% growth -1.0% -16.2% 18.8%

https://ember-energy.org/data/electricity-data-explorer/

It is correct to say that in China-

coal consumption and population have peaked, whereas

total electricity production and GDP are still growing rather briskly.

If you believe that AI capabilities in the next decade or two will be limited by electricity supply/cost,

then China is set to have a big edge. I also think it is likely they will deploy more practical and efficient models/agents than those generated in the US. They also will a big edge on mass robotics (vehicles, drones, etc) manufacture. Got batteries?

look at the electricity of Germany and UK — truly suicidal civilizations

Hickory,

Yeah, this president is working hard to shut down our cheapest and fastest forms of energy – not good for AI.

FWIW, the US does have a fair amount of domestic battery production – not quite as technically advanced as China’s but pretty good.

A new design in AI computing has emerged, UMA, and will render large data centers obsolete as “large super computers” decades ago. The AI computing will be back to personal computers.

Windows OS will be replaced by AI chatbot OS

How big can a nuclear reactor be before it is no longer a SMR?

Small and modular.

The term is being thrown around in the press very inaccurately.

For example- “Canada’s first grid-scale Small Modular Reactor (SMR) is currently under construction at the Darlington New Nuclear Project in Clarington, Ontario. The project features a 300-megawatt GE Vernova BWRX-300 reactor. Targeted for operation by 2030, this deployment marks the first grid-scale SMR in any Western country.” [Actually 4 of these on one site.]

Those 300 MW reactors will have some components produced in a factory, but most of the project is built on-site (including the reactors themselves). These are just 1/3rd size power plants, and are certainty not modular.

It remains to be seen if there is any cost advantage for smaller or modular reactors to be realized by the industry, compared with the full size versions. Very doubtful if any lower cost/kWh units can be deployed at scale in the US within 10-20 years, if ever.

I’m not saying that there is no role for the effort… that is a different question.

Rather I’m saying that people shouldn’t get their hopes up that any of this production will be inexpensive (or even cost competitive), or can be achieved in a timely manner.

The US percent electricity generation from nuclear production has been 19% for a long time, now drifting toward 18%. I’ll pay for a round of drinks if it reaches 20% in some far future day. Perhaps it can happen if/when nat gas supply tanks.

To the above, that’s what I tried to address. Yes, a lot of crude oil that had been projected by the virtually worthless IEA did not hit the market. But quite a few Arab countries have storage. During the conflict for example, Iran kept shipping through the SOH for much of it and then when the blockade was complete, stored an awful lot of oil (to full capacity I am told). Now that the sanctions have been lifted, they are exporting all of that stored oil as quickly as they can get tankers in there–and they of course have preferential treatment at Kharg Island. The UAE and KSA mostly piped around the chokepoint. All the Arab countries are recovering more quickly than was predicted, because it’s their lifeblood. Even little Kuwait is going gangbusters. And during whis whole thing, the United States sold into this market like it was a Filene’s basement sale. This doesn’t even address the overshadowing issue: some massive entity almost certainly had to have shorted oil during this thing, as you don’t usually see oil futures peak out at $118 when this much disruption occurs.

So now OOW is abundant, almost flooding the market, it happened that quick. Dennis makes the point that the cure for low oil prices has always been low oil prices, and that’s true, but we are no longer in that sort of world. The shale basins are giant assembly lines, with the most promising sweet spots marked for drilling and fracking next. This is so well marked off that nascent minerals buyers have paid outrageously in front of the wave, for the quick yield and then five years of annuity. These productions companies all carry massive debt, some more than others, and to stop is to, well, declare bankruptcy, because many companies don’t have, in this tumultuous market, a balance sheet that will pass muster when put against virgin assets (potential targets). They realize that they can make a cluster of wells from a pad and each one will produce enough to move on to the next spot. And yes, they will indeed keep producing and selling into a $50-60 market, because the production of oil and gas is their only business plan. In other words, they can’t get off the merry-go-round.

The SPR is very likely in sad shape. These sixty some caverns are over 50 years old and were built to be kept full, at a pressure of 800 psi. They have been partly emptied so many times for political gain that salt growth has become a problem. One thing is for damn sure: they are not going to be refilled unless light tight oil goes to exceptionally low prices, and I imagine that’s where we’re going. I am not privy to talks between the president’s people and the UAE and Bahrain and KSA but I imagine it goes along the lines of produce at full capacity and take the cheap prices because we saved your bacon and you owe it to us. Notice that I have left out any mention of building golf courses and resorts in those countries, because I only know what I read, and I doubt most of it.

Therefore, with all intentions of remaining forever a good patriot, I think the oil industry in the U.S. has been used, more or less, as a pawn. I’m not sure what entity but probably large banks have, with some degree of reassurance, been keeping the price of oil artificially depressed. And going forward, we are much more likely to see $50 oil than $90 WTI. The true experts on this, such as Art Berman, are likely to have egg on their faces, because we’re well into July and prices are about where they were pre-war, and I haven’t seen gas lines at the pump; nor has air travel slowed down. I like Mr. Berman and think he is genuinely serious and prepared, but he has been hoodwinked, as have we all, by forces totally unlike any we’ve ever experienced. As a consequence, we’re going to sell American oil for much less than it’s worth, and even, in some cases, for less than it cost to produce. The aftermath of that will fall to another administration.

When you think about resource management at a national level, especially for something like oil which is a critical factor in economic function and is a finite resource, it sure looks like the US political and economic system has done a very poor job at paving a path for steady and long duration production.

Rather we have been operated in a free-for-all, boom and bust manner. I don’t trust governments to make good/fair/wise decisions but it sure seems like it wouldn’t be too hard to have a system that does better than we have done. Perhaps by having managing commissions that have a well designed mandate, isolated from short term political/partisan/financial pressures. I think such a system would be useful for managing federal budgets and expenditures, for example things like Medicare, SS, and debt levels.

Not holding my breathe, as we watch very poor management undermine our foundations.

‘Management’ doesn’t have to equate with communism, as some may be prone to counter. Warren Buffet was a good manager, and he weren’t no communist.

Hi Gerry,

An interesting take, thanks. In the short term perhaps tight oil producers keep going, if it were my money I would slow down the completion rate to a minimum and hope that oil prices increase. Otherwise I would not be able to get out of the hole being dug using a shovel (drilling more wells), a ladder (reducing the number of completions) would work much better.

For large oil companies they will see their prices tank as the price of oil falls as profits per share will be in the crapper.

What do you think happens at less than $50/b? I do not see tight oil production continuing at a long term oil price under $50/b and if OPEC falls apart and Middle East producers are competing for market share we may see very low oil prices.

UAE left OPEC, Iraq is threatening an exit.

Hickory,

It’s worth keeping in mind that “energy” is critical, but not oil/FF. FF has been a convenient and scalable resource, but really it’s just another source of hydrocarbons (H & C). Hydrocarbons can come from biomass; they can be synthesized from renewable electricity, water (H from H2O) and air* (C from CO2); and they can be replaced for most functions by cheaper direct electrification, which is now even more convenient, scalable, clean, quiet, and powerful.

On the subject of commission management: that has been the job of the TRRC and OPEC. Sadly, that kind of industry “management” almost always maximizes industry revenue and consumer costs. They always claim they’re pro-consumer, and that they just want to minimize destructive instability, but…not so much. In a traditional decentralized free market, prices are at the point of marginal costs: that means that there are always sellers who are losing money and going out of business.

Agriculture is a good example: consumers have benefited from ever cheaper food, and farmers have continually gone out of business: 90% of Americans lived on the farm 200 years ago, now it’s less than 1%. Manufacturing is going through the same process, though rather more slowly due to more concentration and oligopoly: output rises and employment falls. This is a painful process for sellers – that’s not what they want!

————————————————

*That sounds like air, fire and water from the Ancient Greeks! And the fourth classical element was wind, which also fits.

‘Every day brings more news of Trump’s greed, incompetence, cruelty, and criminality. Raking in $2.2 billion in his first year in office, much of it siphoned off from taxpayers and gullible followers.’

The gullible followers must be getting something- but what?.

They’re getting membership in a social group.

Sadly, many people are unlucky, and they grow up with unfortunate intellectual capital. They’re trained to obey authority, from parents and pastor, and go along to get along. And they have a large set of ideas about the world that are unrealistic.

hightrekker

I live and work in a rural area that voted 70%+ for Trump in 2024. Poverty rate is about twice the US average. I think I can speak to your question anecdotally based on a couple of hundred of my neighbors, coworkers and community members. Also based on polling I’ve read.

The one item on their list that is most pertinent to this site is inexpensive fuel. They drive long distances in this area and are convinced that democrats and their regulations are holding back a flood of oil that would help their wallets. They’ve swallowed big oil’s copy of big tobacco’s disinformation playbook on the environment and climate.

Aside from that, racism remains pervasive. A great many want the US to remain white and to get all of those ‘foreigners’ out. They are just fine with the administration’s approach and believe that they haven’t gone far enough. Guns are also a hot button topic with a great many.

The wealthy have gotten quite a bit.

As for the others, for many years, decades even, Ds have been browbeating Rs over all manner of perceived moral transgressions and character flaws. Think Meathead berating Archie for his language, perceptions, religion, humor. Add to it that for many, education and meritocratic individualism were a way up the ladder while the older means of getting by, manual work and skilled labor, were off-shored and automated. So “traditionalists” clung to their guns and bibles because their ways are indeed endangered.

[The educated may not realize but their ways are just as endangered by the coming wave of AI tools, but that’s a different backlash]

None of the damage to the blue collar middle class can be changed, least of all by Rs on the Citizens United payroll or Ds at the very same trough. BUT, trump makes them feel like he is going to hurt the people that hurt them. Burn it down? Why not? What has the government ever done for me?

Ds & Rs are both equally to blame in my book. They both would rather play uni-sex bathroom bingo culture games rather than address runaway plutocracy, wealth inequality and the fraying US social fabric.

Pops,

What did you think of Reagan’s reductions of taxes for the highest incomes from 70% to 28%?

Nick, since Reagan our economy has seen lower growth and higher debt overall. Demographics is also a factor but in general “Trickle Down” has proven to be every bit the lie the left made it out to be. As Buffet said, “it’s class war and my side won.” Many modern economies have both higher taxes and higher perceived quality of life, health outcomes and social mobility, just fewer billionaires. We pay about 27% of GDP in total tax, EU and Scandinavia pay around 40%. Of course it isn’t just income tax, not many of the 1% get a W2, which is convenient. The ownership was afraid of a socialist overthrow in the 30s and so they laid low for a few years until they could fracture the labor coalition, meritocracy did that, Citizens United did the rest.

EQT just announced the world’s longest drilled ‘shale’ well at 37,610 feet TMD (Total Measured Depth) with a 29,070′ lateral.

Thatsa over 7 mile long/5.5 mile lateral well.

100% in target zone.

It is these ongoing operational and technical advances that will continue to expand long, longity long time the productive footprint of natgas basins (worldwide).

Kinda miss ol’ Nony’s irreverent postings.

Agree or disagree, he regularly offered up accurate and relevant hydrocarbon data.

the SWPA and WV, and even SE OH Marcellus are super shallow, only 6Kft TVD, and could be drilled and completed at a fraction cost as the Permian, Eagle Ford and Bakken, and yet they are very prolific and even more and more liquid as TVD gets shallower.

For EQT longest shale well at 1.5mil TVD, the Marcellus has GOR around 2~3:2, similar to the Barnett in Permian, or EagleFord at 11~14K ft TVD.

Sheng Wu,

There is an incremental expansion of Ohio drilling into its more northerly counties.

EOG had a couple of wells in Columbiana county (Kitzmiller pad) produce 318,000 and 376,000 bbls of earl in 2025.

Not too shabby.

About 1/3 of the Buckeye state is sitting atop oil from various formations.

Should the lifting technology improve so that this shallow oil becomes economically recoverable, a massive amount of hydrocarbons could become marketable.

yes, Coffeeguyzz,

The Utica part in OH also has shallow shale TVD, and easy to drill ultra-long laterals.

Years ago, they were already drilling close to 5mile long ?

https://www.wvnews.com/news/wvnews/report-expand-energy-drills-record-5-6-mile-lateral-in-west-virginias-utica-shale-in/article_790241b6-ff69-11ef-b72c-a7c5a8680b9c.html

this thread says it is 5.6miles long and landing in the WV Utica Dry gas window — usually it is 10K~12Kft deep, unbelievable!!! They might also set a record in unit shale gas well IP and EUR!

https://altitude-ep.com/wp-content/uploads/2026/02/U-Shaped-Architectures-Deliver-More-Reservoir-Exposure-Access-to-Multiple-Benches.pdf

Sheng Wu,

Yeah, your second link may only be of interest to us operational wonks.

Shame, that, as the included factoid of 550 rigs drilling in 2014 produced 1/3 the fluids that the same number is producing in 2026 is emphatically explained by much of the progress described in that article.

Taking a different perspective, those of us who are wary of ‘model’ driven prognostications re oil production have been – over and OVER again – shown to be validated by actual production numbers.

Used to be derided as ‘Cornicopians’ (proudly raises cyber hand here. Curious … along with ‘Red Queen’, Cornicopian is a never used term anymo’), we hydrocarbon-abundance advocates have been consistently shown as correct to this very day.

… and that’s the way it is.

Cuba just made all solar EV a reality,

https://www.youtube.com/watch?v=eeg0CthbzTE

An update to US Oil Production has been posted.