By Ovi

The focus of this post is an overview of World oil production along with a more detailed review of the top 10 Non-OPEC oil producing countries. OPEC oil production is covered in a separate post.

Below are a number of Crude plus Condensate (C + C) production charts, usually shortened to “oil”, for the oil producing countries. The charts are created from data provided by the EIA’s International Energy Statistics and are updated to March 2026. This is the latest and most detailed/complete World oil production information available. Information from other sources such as OPEC, IEA, STEO and country specific sites such as Brazil, Norway, Mexico, Argentina and China is reported to provide an extra one or two months production preview beyond the EIA’s latest report.

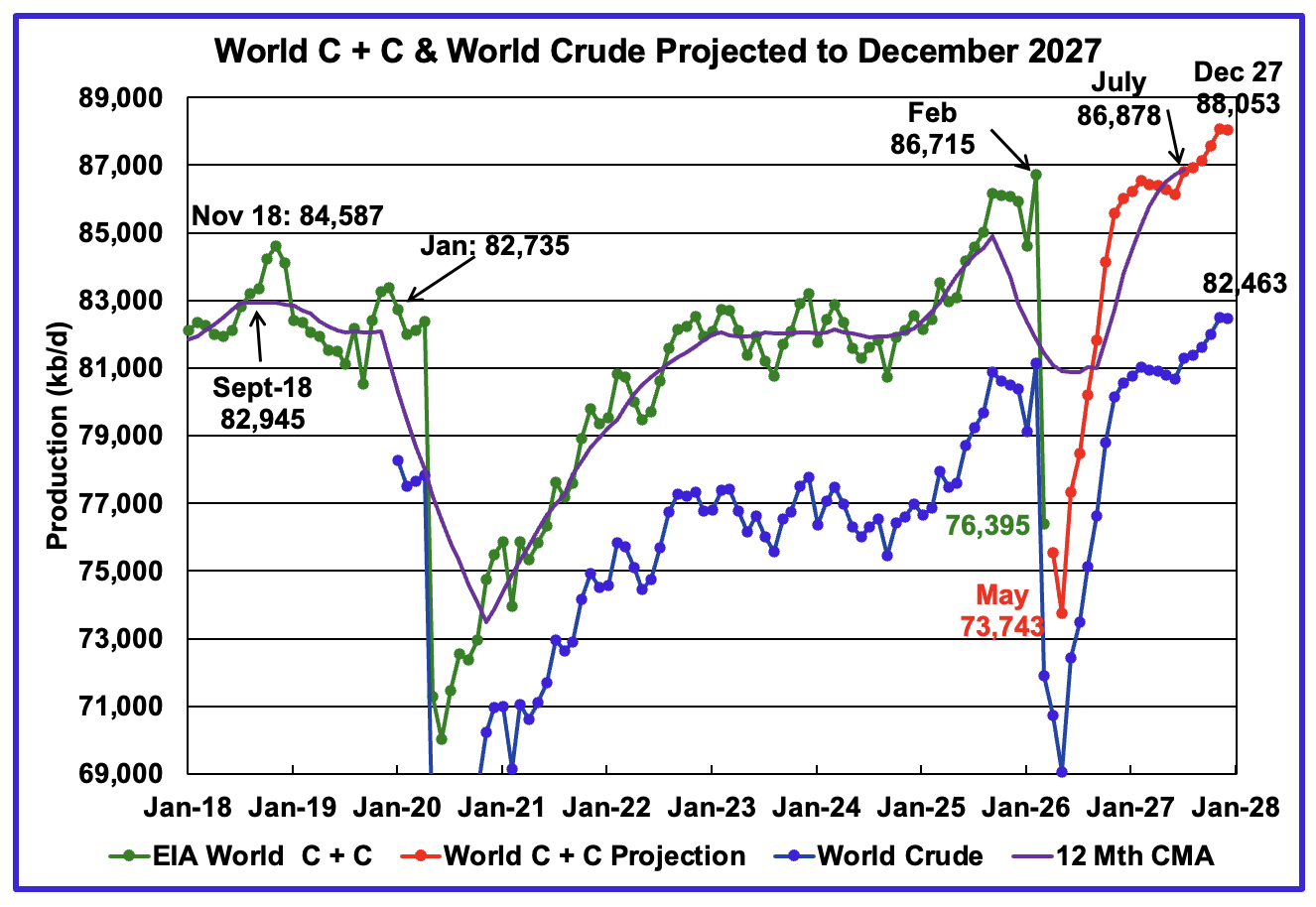

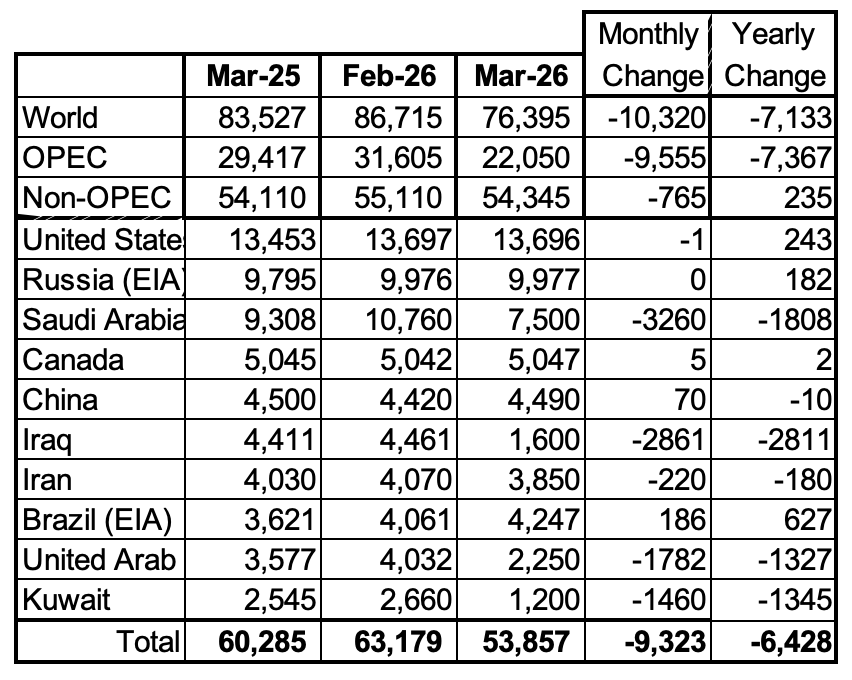

The World’s March oil production dropped by 10,320 kb/d to 76,395 kb/d due to the closing of the Hormuz Straits. The largest contributors to the drop were Saudi Arabia, Iraq, Kuwait and the UAE.

The EIA’s July STEO report continues to make significant and major revisions to the World’s projected oil production after March 2026 due to the US/Iranian war.

This chart has been updated using the July 2026 STEO to project World C + C production out to December 2027. It uses the STEO report along with the International Energy Statistics to make the projection. Production in May 2026 is projected to fall to 73,743 kb/d and is forecast to be the bottom.

The 12 month Centred Moving Average shown at July 2027 is 86,878 kb/d.

For December 2027, production is projected to be 88,053 kb/d, a new projected high and is an upward revision of 257 kb/d over the previous post. The increase comes from a number of Non-OPEC countries.

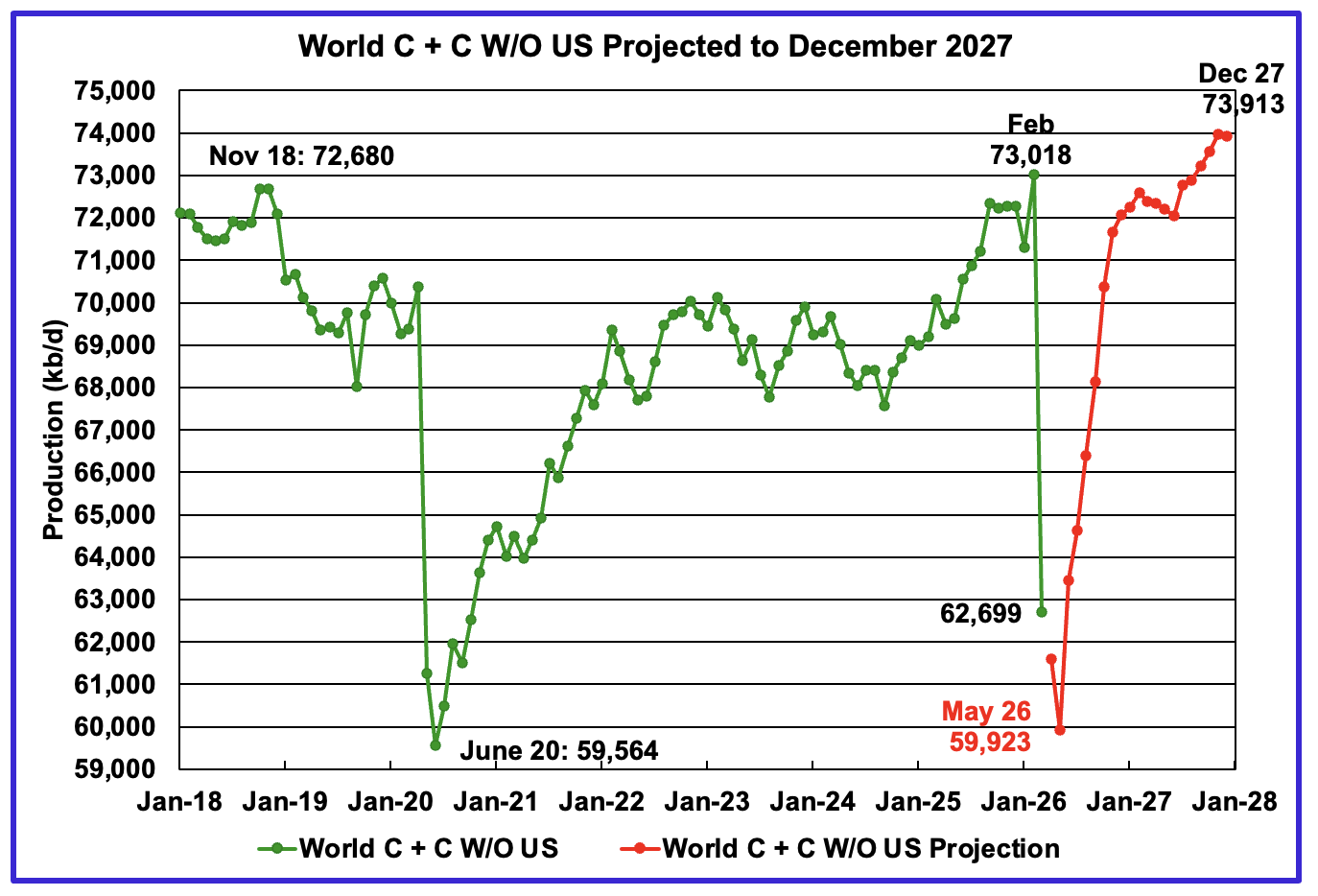

March World oil output W/O the US decreased by 10,319 kb/d to 62,699 kb/d. May production is expected to be the low point at 59,923 kb/d.

The projection is forecasting that December 2027 World W/O US oil production will rebound to 73,913 kb/d. This is 895 kb/d higher than the previous February projection of 73,018 kb/d.

From February 2026 to December 2027, production is expected to grow by 895 kb/d. This small increase may be more than welcome to offset the demand destruction associated with higher oil prices.

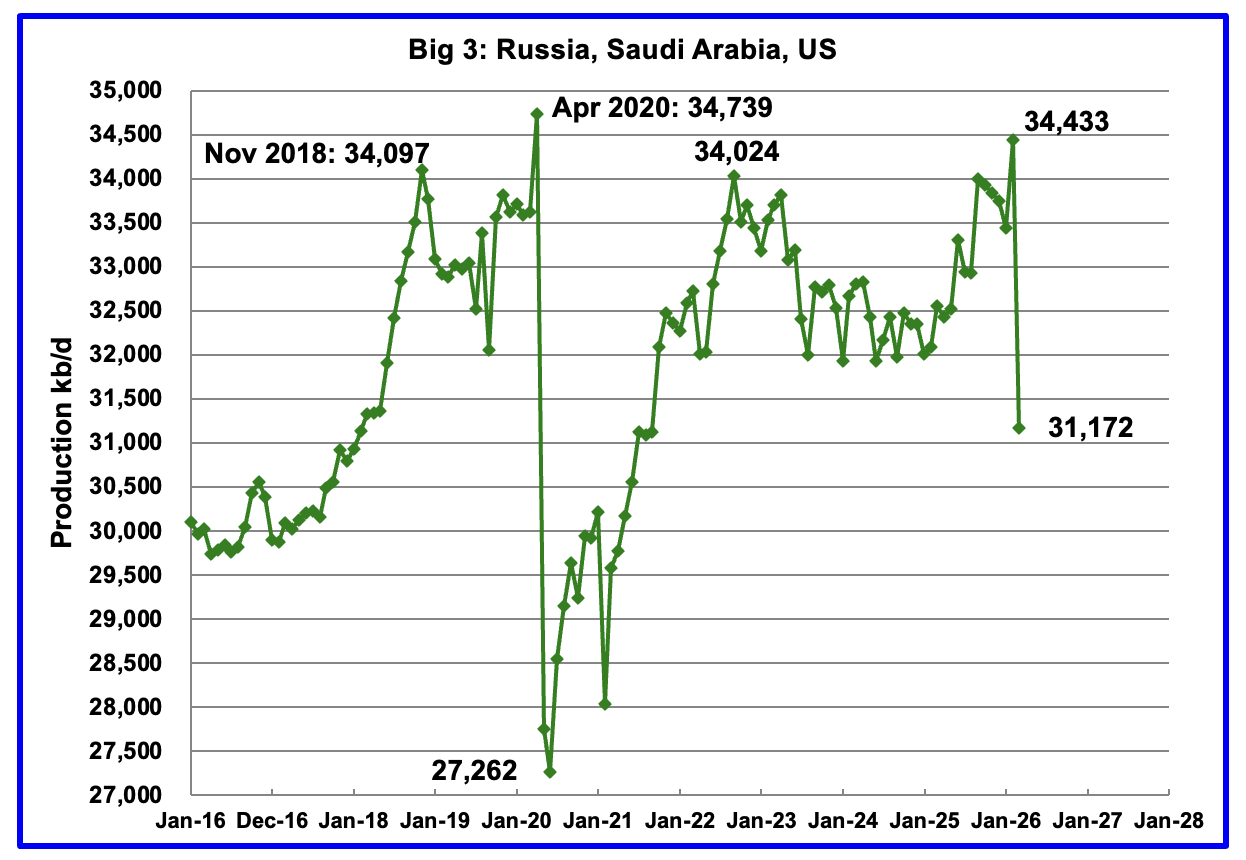

A Different Perspective on World Oil Production

March Big 3 oil production decreased by 3,261 kb/d to 31,172 kb/d. Of the 3,261 kb/d drop, 3,260 kb/d came from Saudi Arabia.

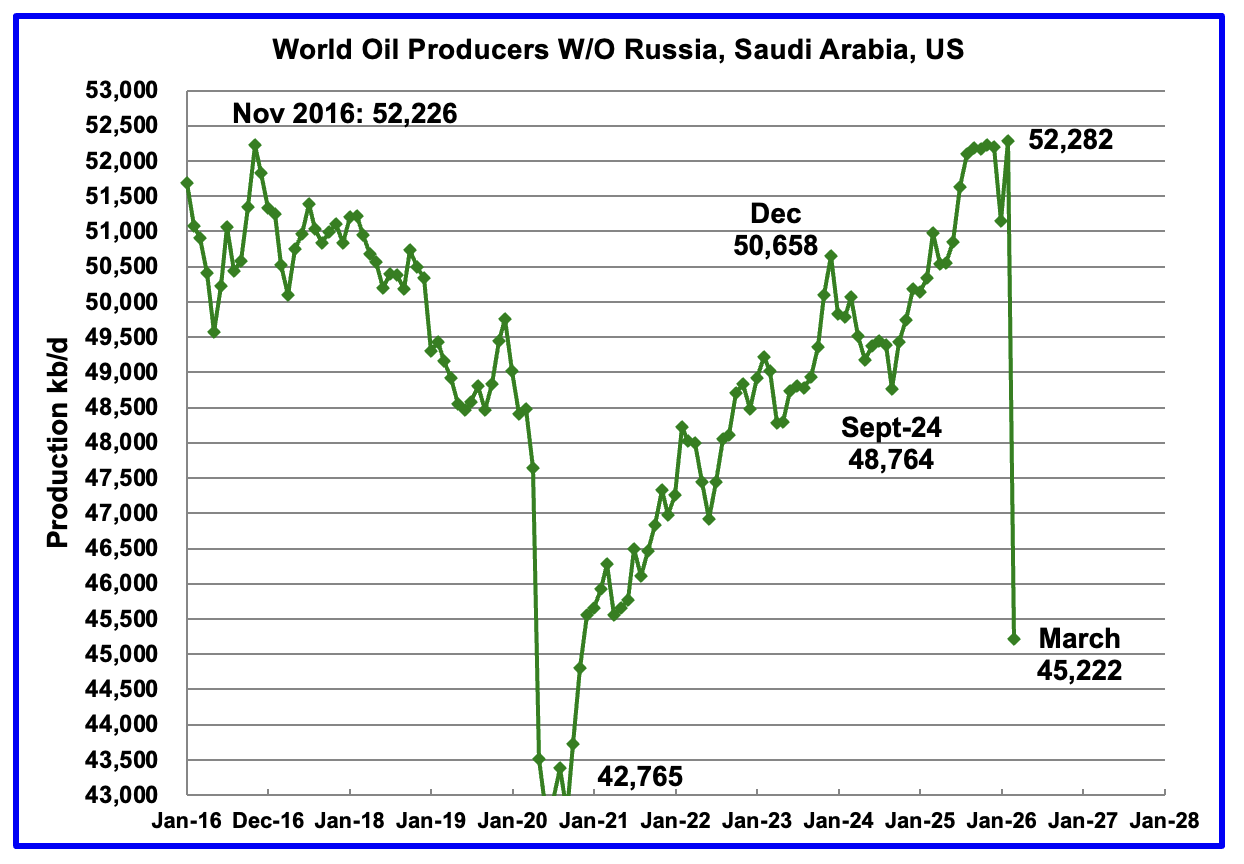

Production in the remaining countries also dropped due to the closing of the Straits of Hormuz. March 2026 production dropped by 7,060 kb/d to 45,222 kb/d. The biggest contributors to the drop were Iraq, UAE and Kuwait.

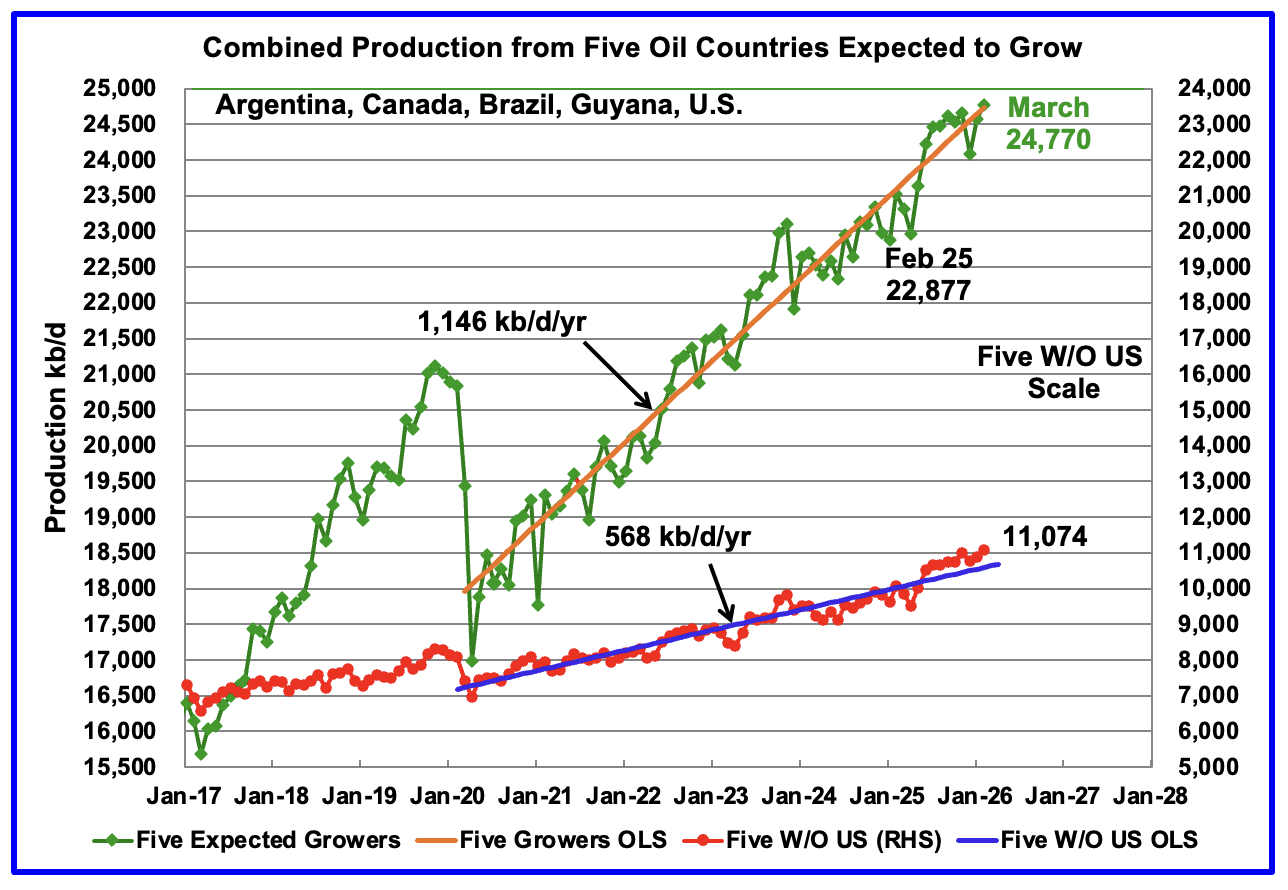

Countries Expected to Grow Oil Production

This chart shows the combined growing oil production from five Non-OPEC countries, Argentina, Brazil, Canada, Guyana and the U.S., whose oil production is expected to grow in coming years. These five countries are often cited by OPEC and the IEA for being capable of meeting the increasing World oil demand for next few years. Production from these five countries from April 2020 to February 2026 rose at an average rate of 1,146 kb/d/year as shown by the orange OLS line. This is an updated OLS to February 2026 and the growth rate rose slightly from the previous rate of 1,130 kb/d/yr to 1,146 kb/d/yr. From March 2025 to March 2026, production rose by 1,252 kb/d.

To show the impact of US growth over the past 5 years, U.S. production was removed from the five countries and that graph is shown in red. The production growth slope for the remaining four countries has been reduced by 578 kb/d/yr to 568 kb/d/yr.

March production has been added to the five growers W/O US chart and it rose by 196 kb/d to 11,074 kb/d.

World Oil Countries Ranked by Production

Above are listed the World’s 10th largest oil producing countries. In March 2026 these 10 countries produced 70.5% of the World’s oil. On a MoM basis, production decreased by 9,323 kb/d in these 10 countries while on a YOY basis production dropped by 6,428 kb/d. Due to the ongoing US/Iran war, the countries are ranked using March 2025 production.

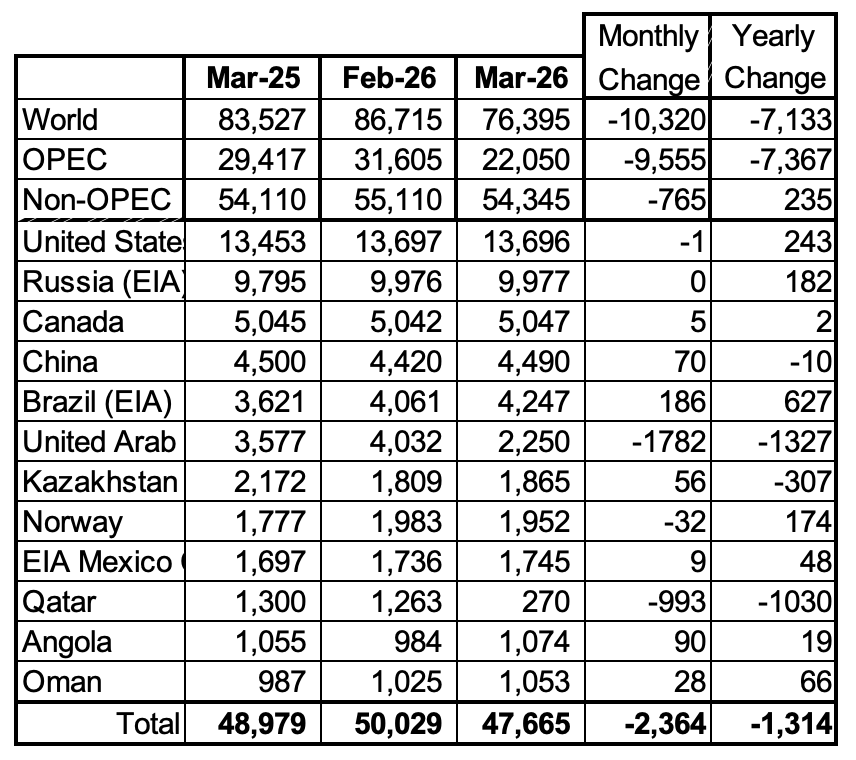

Non-OPEC Oil Countries Ranked by Production

Listed above are the World’s 10 largest Non-OPEC producers. The original criteria for inclusion in the table was that all of the countries produced more than 1,000 kb/d. The UAE has been added since they have left OPEC.

March MoM production decreased by 2,364 kb/d to 47,665 kb/d for these 10 Non-OPEC countries while as a whole the Non-OPEC countries saw a yearly production increase of 235 kb/d to 54,345 kb/d. The large monthly drops for the UAE and Qatar are due to the Iran US war.

In March 2026, these 10 countries produced 87.7% of all Non-OPEC oil.

Non-OPEC Country Oil Production Charts

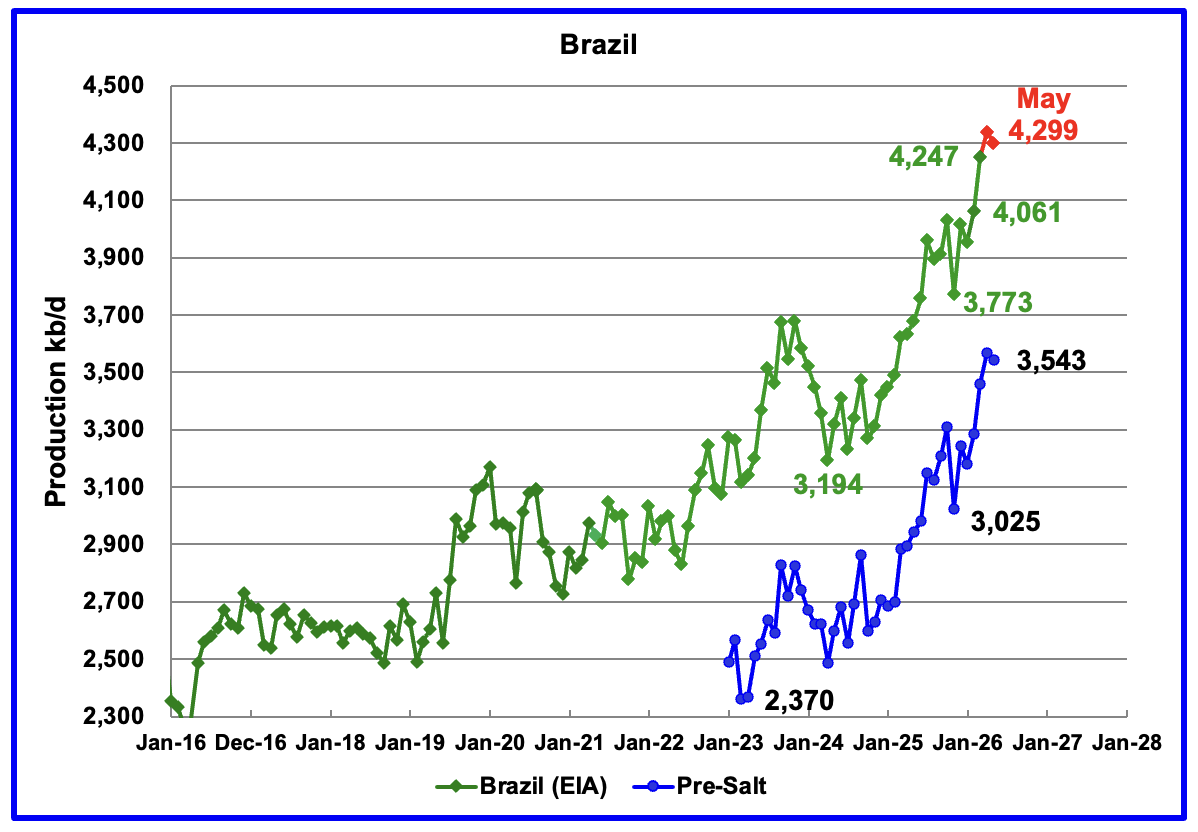

The EIA reported that Brazil’s March production rose by 186 kb/d to 4,247 kb/d, a new record high. According to this Article, the pre-salt reservoirs remained the backbone of national production, accounting for nearly 80 per cent of total oil and gas output.

Brazil’s National Petroleum Association (BNPA) reported that production rose in April to 4,337 kb/d, a new high, and then dropped in May to 4,299 kb/d.

Pre-Salt production was a major contributor to the March increase.

According to the July OPEC MOMR: “In 2027, Brazil’s liquids supply, including biofuels, is forecast to increase by about 110 tb/d, y-o-y, to average 4.8 mb/d.“

“Despite promising start-up plans in offshore Brazil, rising development costs and sustained inflation could tighten offshore project economics, leading to delays in final investment decisions and tempering near-term growth.“

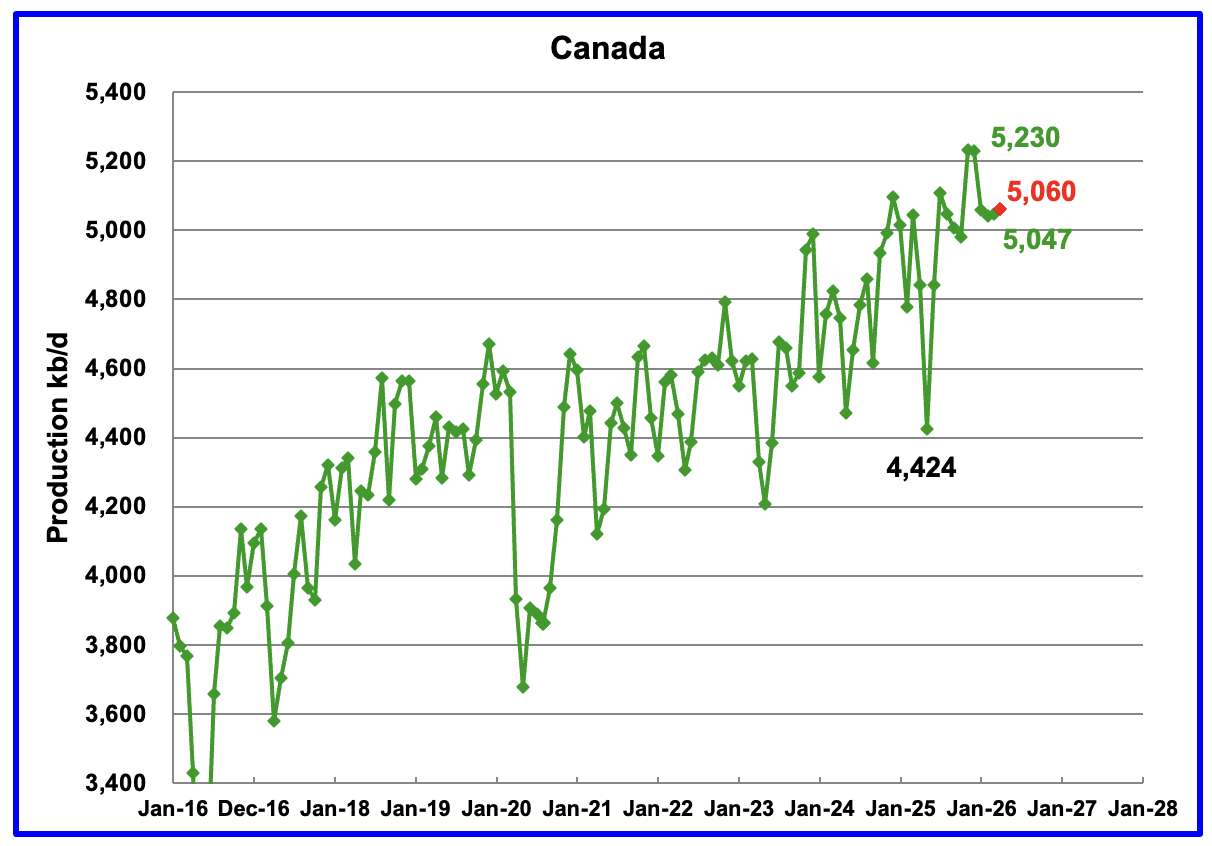

Canada’s oil production increased by 5 kb/d in March to 5,047 kb/d according to the EIA.

Canada’s January and February production was down due to unexpected downtime at a few oil sands companies. April production is expected to grow by 13 kb/d to 5,060 kb/d, red marker.

According to the IEA’s May OMR: “May is expected to see further losses as both the Syncrude and Suncor Base Plant upgraders have scheduled maintenance. Annual production is forecast to increase by 90 kb/d to 6.5 mb/d on average.”

According to this Article, President Trump signed an executive order to build a smaller version of the Keystone XL pipeline.

The pipeline, proposed by Canadian pipeline company South Bow (SOBO.TO) and its U.S. partner Bridger Pipeline, could increase Canada’s crude exports to the U.S. by more than 12% if it goes ahead. A presidential permit was required for the project to proceed.

According to this Article, Canada and Alberta have agreed to build a 1 Mb/d pipeline from Alberta to the BC coast.

“Prime Minister Mark Carney and Alberta Premier Danielle Smith have announced plans to build a new pipeline from Alberta to the British Columbia coast as a private public partnership.

The plan also calls for the new pipeline to be built following the corridor of the existing Trans Mountain pipeline, which is federally owned and runs from Edmonton to a terminal in Burnaby, B.C.”

While this pipeline will be welcomed by Alberta, it will not be clear sailing.

According to this Article: Environmental organizations are questioning why this pipeline should be built as the world is transitioning to renewable energy sources.

“Energy and environmental organizations are reacting with alarm to the recent Canada-Alberta deal to build a new oil pipeline to the West Coast, questioning whether overseas buyers can be found for the oil that may eventually flow through the pipeline.

The Alberta government’s proposal estimates the pipeline would cost $35.2 to $43.7 billion, with the federal and Alberta governments remaining majority owners in the project. That’s despite an earlier promise from Prime Minister Mark Carney — enshrined in his government’s memorandum of understanding with Alberta — that the pipeline would be privately financed.

“What we’re seeing here is that we’ve got a pipeline that is being built for political reasons rather than economic reasons. And that’s tremendously concerning,” said Chris Severson-Baker, executive director of Pembina Institute, the energy think-tank which has been working for decades on decarbonization in Canada’s oil industry.“

The EIA reported China’s March oil output rose by 70 kb/d to 4,490 kb/d. On a YoY basis, China’s March production down by 10 kb/d. For May, China reported average production of 4,373 kb/d, red markers.

For the last two years, March has proven to be a record production month. Again this year March showed a large gain but it did not exceed the March 2025 peak of 4,500 kb/d. Does this hint at an upcoming peak in China’s oil production?

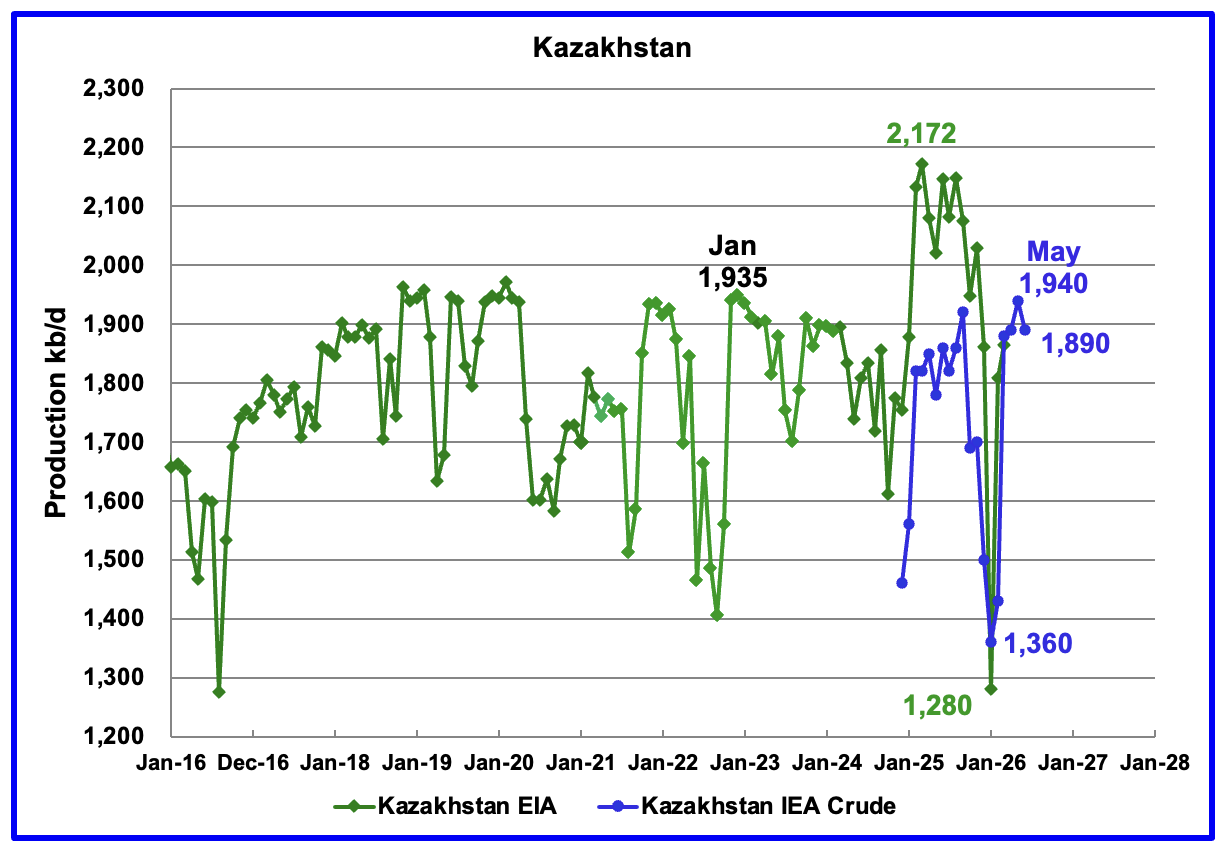

According to the EIA, Kazakhstan’s March oil output increased by 56 kb/d to 1,865 kb/d after the fire damage to the Tengiz oil field power generating plant was repaired. Production hit a low of 1,280 kb/d in January 2026.

Since Argus no longer reports OPEC + crude production, production data for Kazakhstan will now be taken from the monthly IEA reports. April production rose by 10 kb/d to 1,890 kb/d even though Kazakhstan was supposed to reduce production in April. The July IEA OMR reported that crude production in May rose to 1,940 kb/d and then dropped by 50 kb/d to 1,890 kb in June.

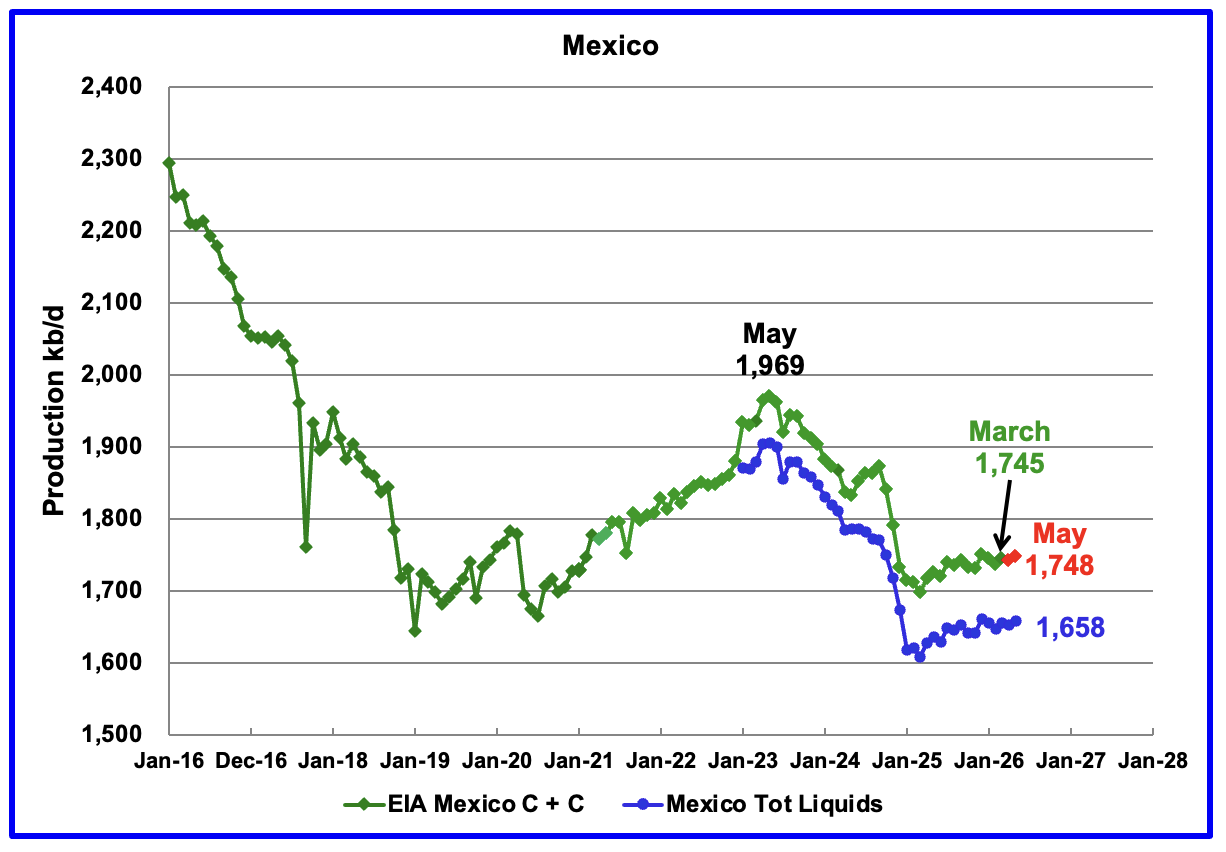

According to the EIA, Mexico’s March output rose by 9 kb/d to 1,745 kb/d.

In June 2024, Pemex issued a new and modified oil production report for Heavy, Light and Extra Light oil. It is shown in blue in the chart and it appears that Mexico is not reporting condensate production when compared to the EIA report.

In earlier EIA reports, they would add close to 55 kb/d of condensate to the Pemex’s “Total Liquids” report. More recently the EIA has been adding 90 kb/d of condensate to Mexican production. For April and May production, 90 kb/d have been added to the Pemex report. May production is estimated to be close to 1,748 kb/d, red markers. Note that Mexico’s production, as reported by Pemex for the last eight months has stabilized around 1,650 kb/d, blue graph.

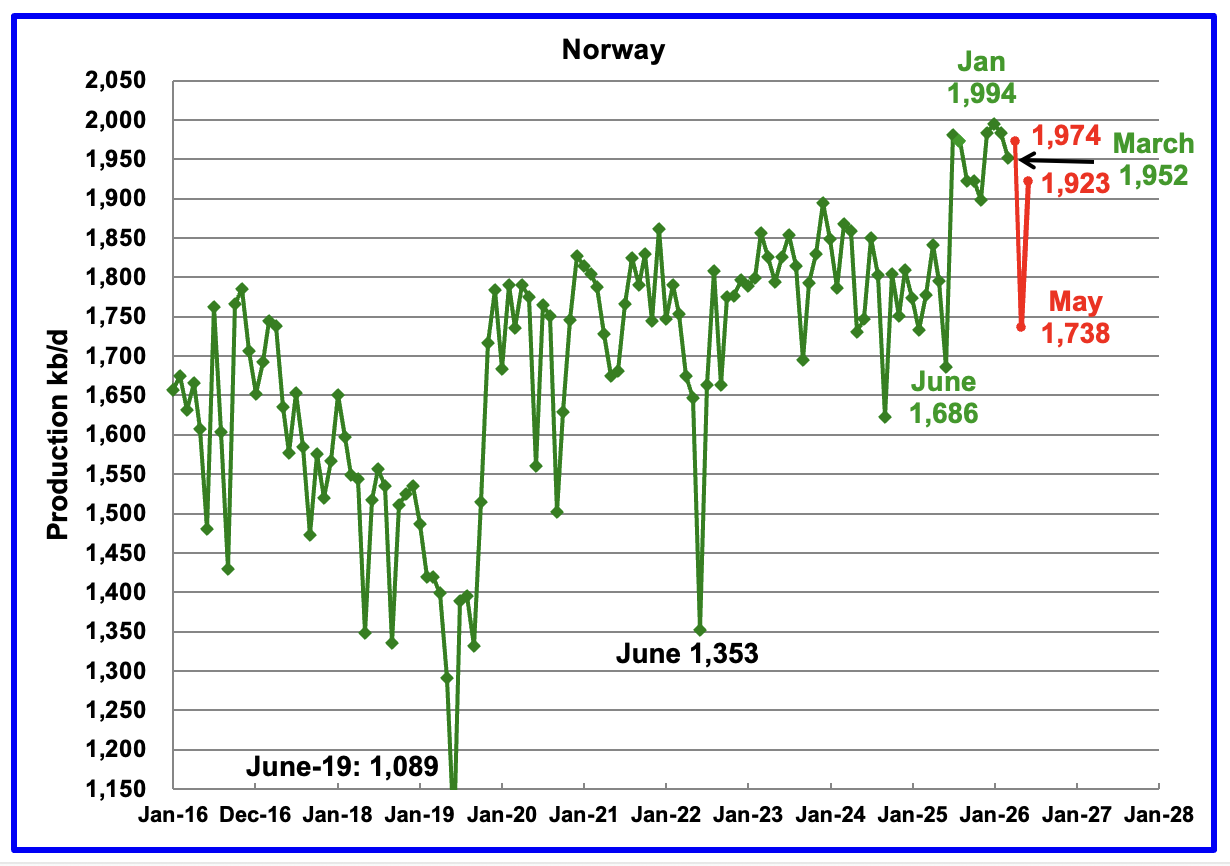

The EIA reported Norway’s March production dropped by 32 kb/d to 1,952 kb/d.

Separately, the Norway Petroleum Directorship projected that oil production in April will rise to 1,974 kb/d. It will then will drop to 1,738 kb/d in May before rebounding to 1,923 kb/d in June. The red markers are the NPD’s production forecast.

According to OPEC’s July MOMR: “In 2027, Norwegian liquids production is forecast to drop by around 70 tb/d to average 2.0 mb/d.”

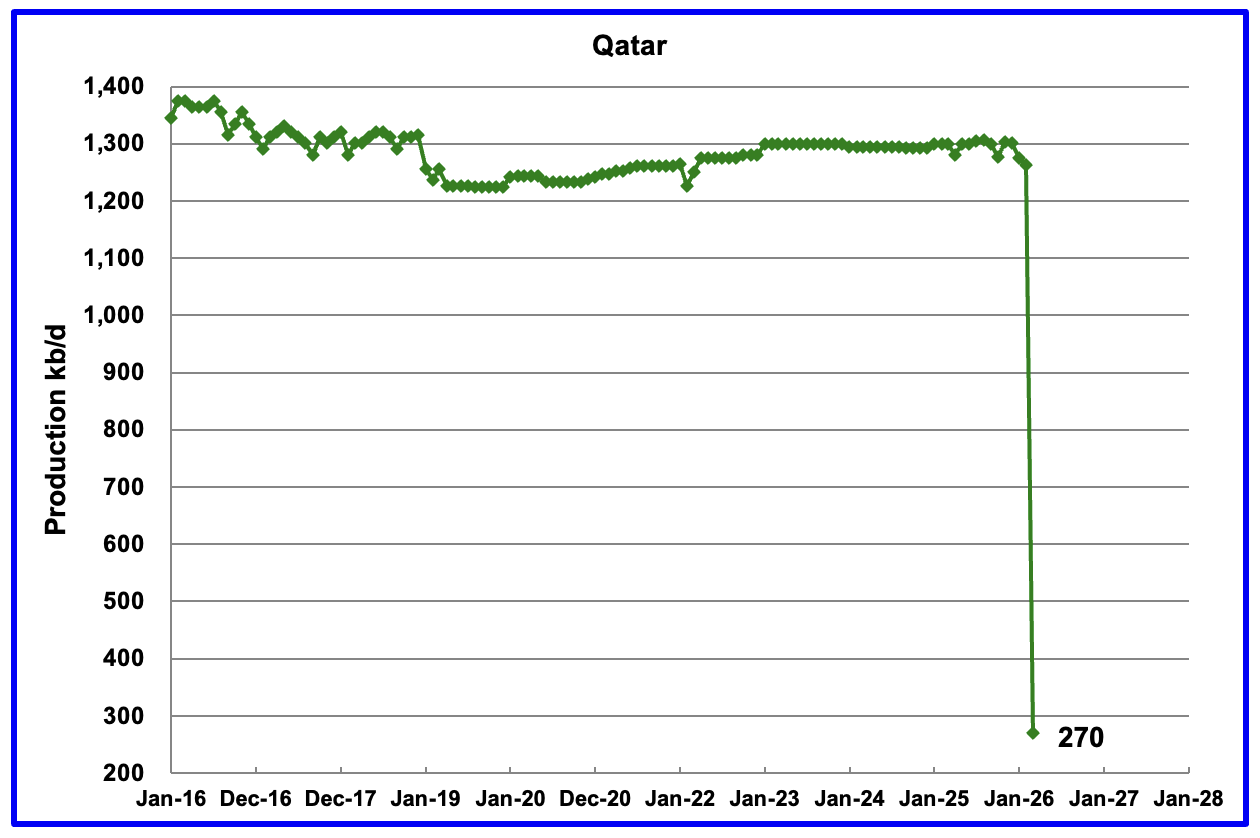

Qatar has restarted providing the EIA with monthly updated oil production. Qatar’s March output dropped to 270 kb/d due to the Iran/US war.

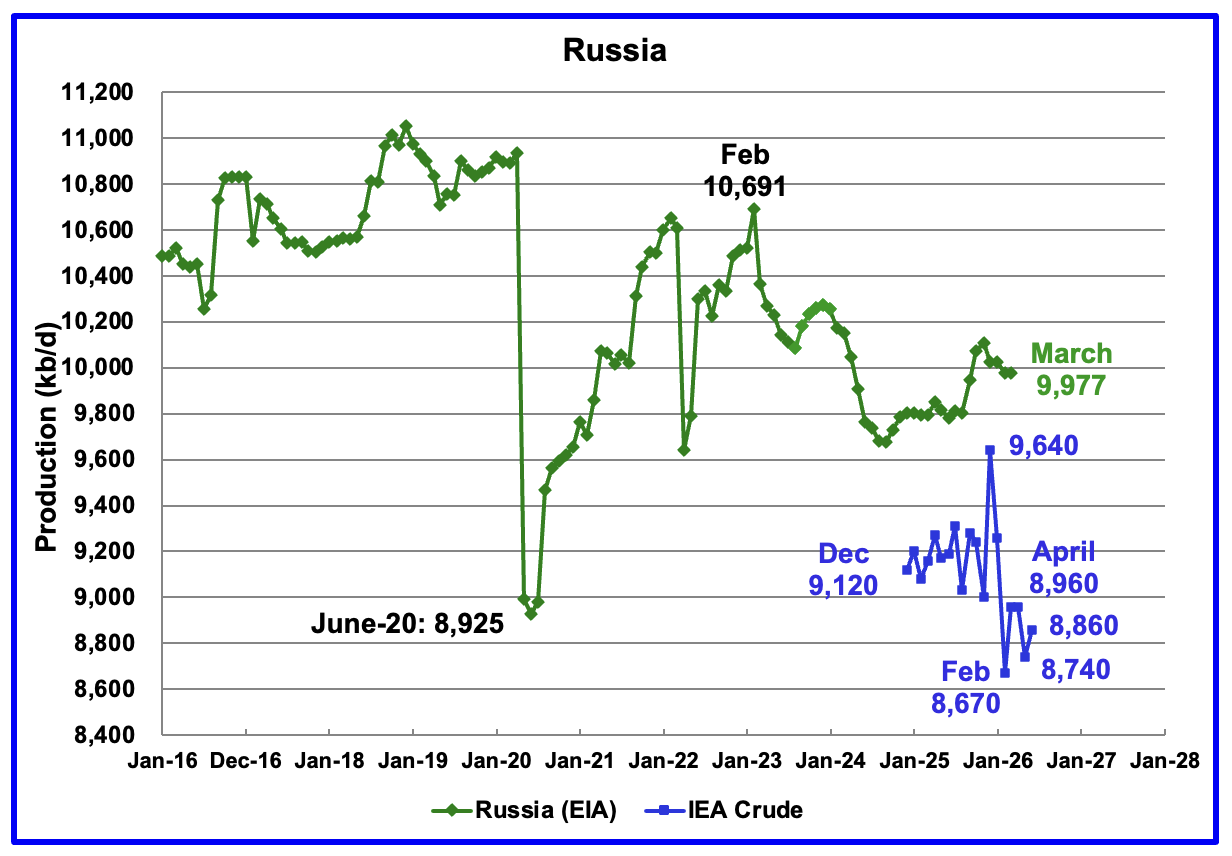

The EIA reported Russia’s March C + C production was unchanged at 9,977 kb/d and was up by 182 kb/d from March 2025.

The above chart also shows Russian production as reported by the IEA. It is difficult to assess the accuracy of the IEA report since in the past the IEA’s Russian production had been around 100 kb/d to 150 kb/d higher than Argus’ Media. The best that can be done at this time will be to compare the production trends between the EIA and the IEA. I think that Russian oil production continues to be a major state secret at this time because of the damage being caused by the heavy bombing to its related crude oil processing facilities.

The IEA’s July OMR reported that Russia’s May crude production was 8,740 kb/d and then rebounded in June to 8,860 kb/d. It is difficult to comprehend how Russian production is increasing in light of the reported intense bombing of Russian refineries.

The OPEC July MOMR is reporting Russian Crude production in May and June was 8,989 kb/d and 8,928 kb/d, respectively. For June, OPEC’s Russian crude production is 68 kb/d higher than reported in the IEA’s report. Clearly current crude production is down from the December 2025 high of 9,640 kb/d.

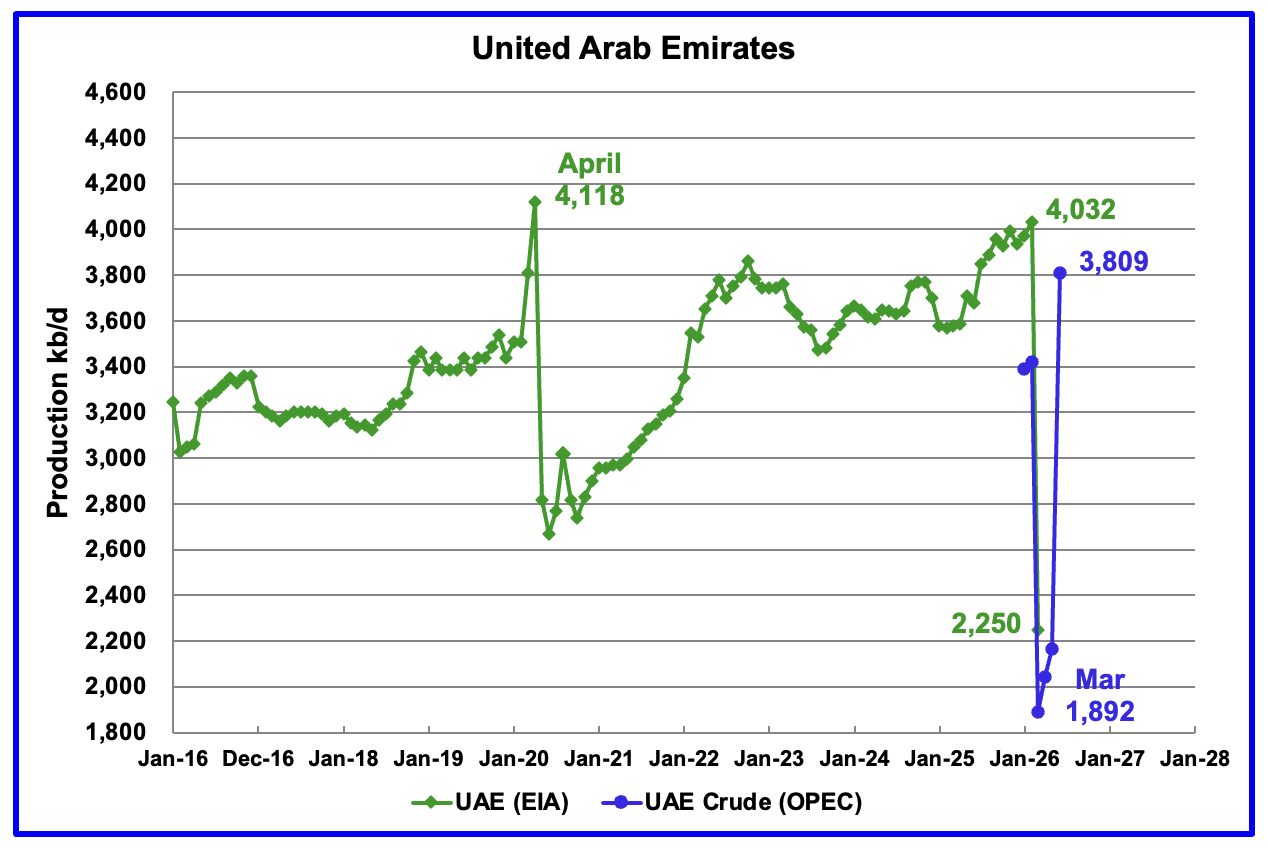

The above UAE chart is being added to the Non-OPEC charts since the UAE has left OPEC. The green graph is C + C production as reported by the EIA. The blue graph is crude production as estimated by OPEC.

The UAE left OPEC because it wanted to produce more oil now. It does raise the question of whether the UAE’s strategic thinkers are looking ahead to when oil demand will begin to fall and are concerned with being left with Stranded Oil Assets.

For March the EIA is reporting that production was 2,250 kb/d. OPEC reported that crude production bottomed in March at 1,892 kb/d. June crude production rebounded to 3,809 kb/d.

Comparing Crude production with C+C production for January and February, it appears that Condensate production is close to 600 kb/d. Potentially UAE C + C production could be in the neighbourhood of 4,400 kb/d in June, a new record.

This Article shows new pipelines being built to bypass the Straits of Hormuz.

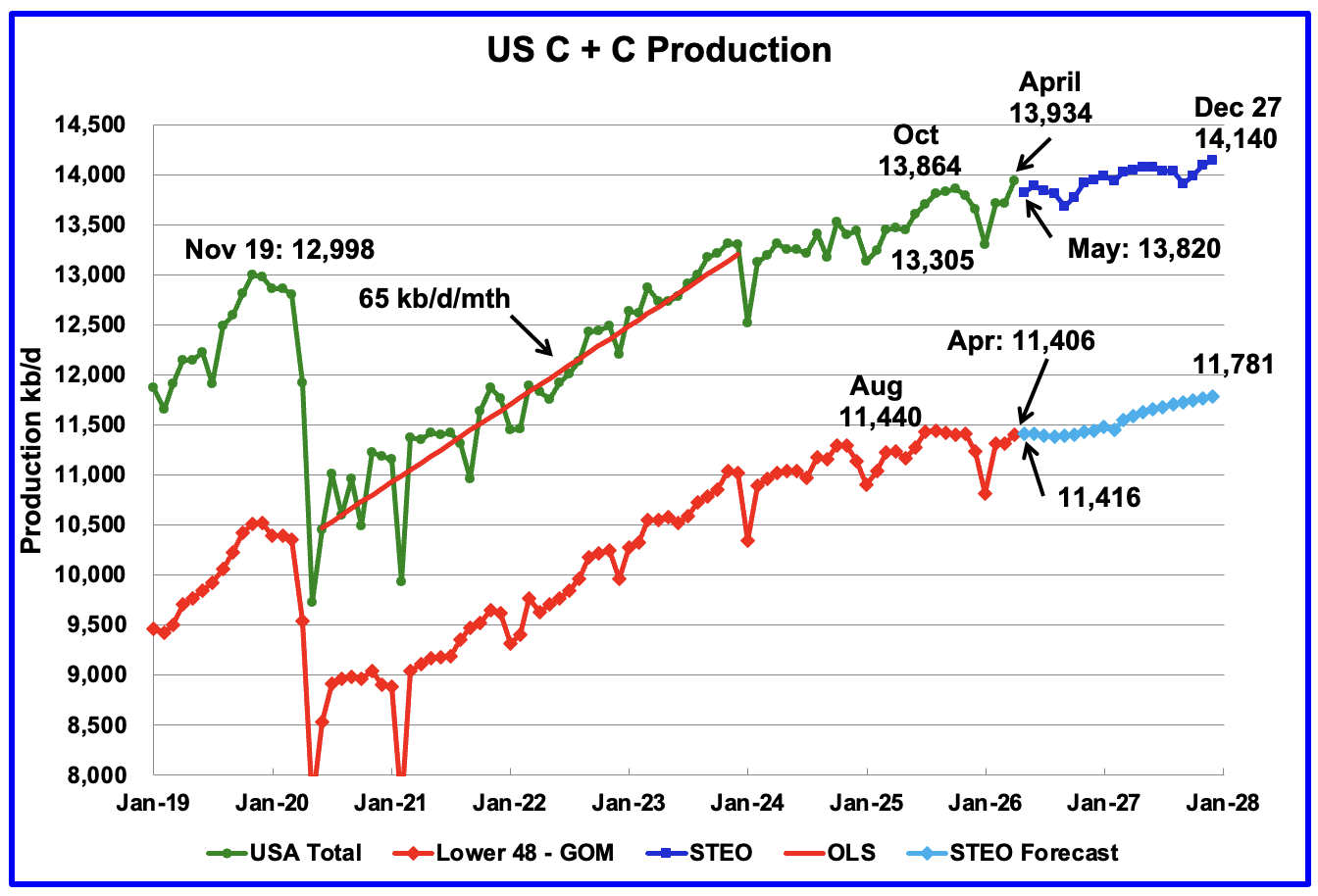

This US production chart showing output up to April 2026 is the same as the one published last week in the US Update.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply