By Ovi

All of the Crude plus Condensate (C + C) production data for the US state charts comes from the EIAʼs Petroleum Supply monthly PSM which provides updated production up to April 2025.

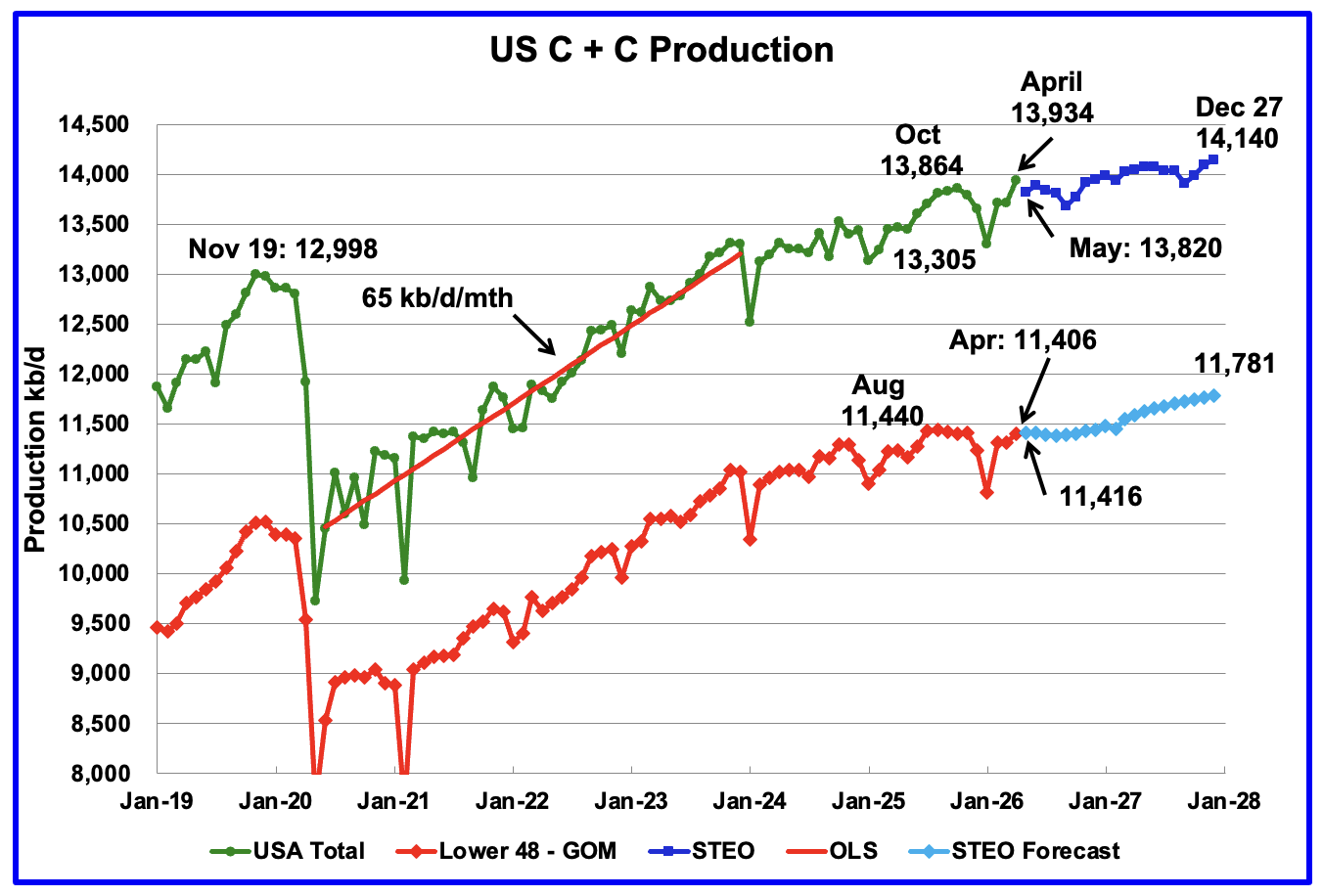

U.S. April oil production increased by 216 kb/d to 13,934 kb/d and is another record high. The largest increases came from TX and NM. May production is expected to drop by 114 kb/d to 13,820 kb/d according to the July STEO. The previous Peak US oil production occurred in October 2025 at 13,864 kb/d but now going forward will be in new high territory after January 2027 according to the STEO forecast.

The dark blue graph, taken from the June 2026 STEO, is the U.S. oil production forecast from May 2026 to December 2027. Output for December 2027 is expected to rise to 14,140 kb/d, downwardly revised by 270 kb/d from the US chart posted in the June World update. The new forecast may be reflecting lower WTI prices. From April 2026 to December 2027 U.S. oil production is expected to increase by 206 kb/d.

The light blue graph is the STEO’s forecast for the Onshore L48 output to December 2027. April Onshore L48 production increased by 93 kb/d to 11,406 kb/d. From April 2026 to December 2027 production is expected to increase by 375 kb/d to 11,781 kb/d. Note how production is essentially flat out to January 2027. The 2027 production increase may be due to the recent addition of 20 Hz rigs in Eddy county. Check Eddy county further down.

U.S. Oil Production Ranked by State

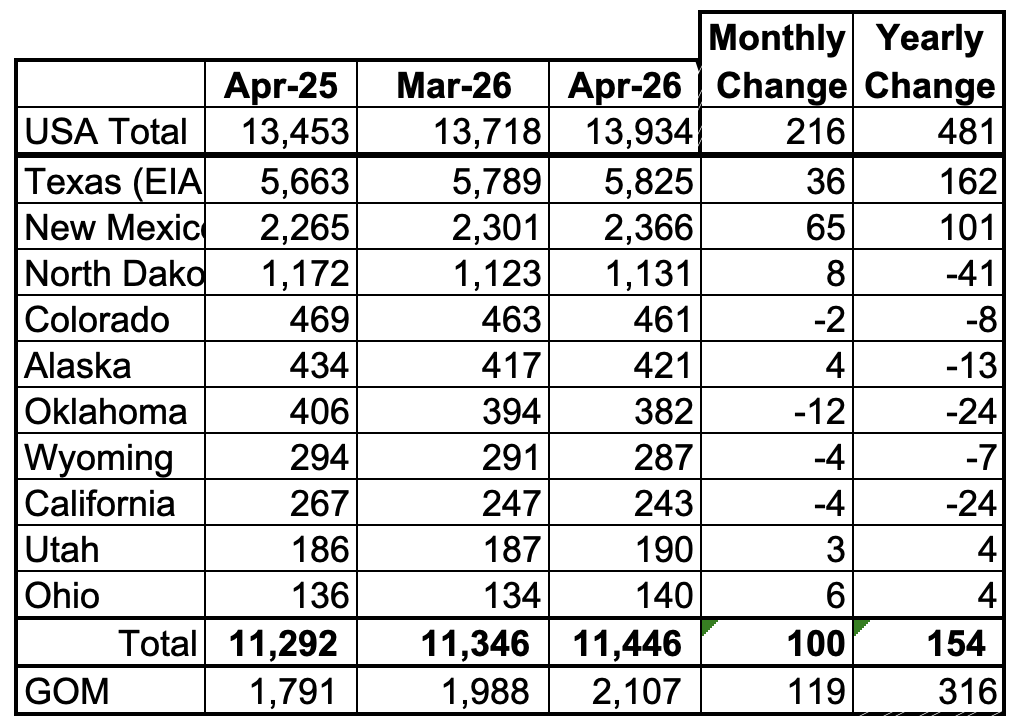

Listed above are the 10 US states with the largest oil production along with production from the Gulf of Mexico.

These 10 states accounted for 82.1% of all U.S. oil production out of a total production of 13,934 kb/d in April 2026. On a MoM basis, April oil production in these 10 states rose by 119 kb/d. On a YoY basis, US overall production increased by 481 kb/d with the largest contributors being Texas and New Mexico and the largest decliner being North Dakota.

State Oil Production Charts

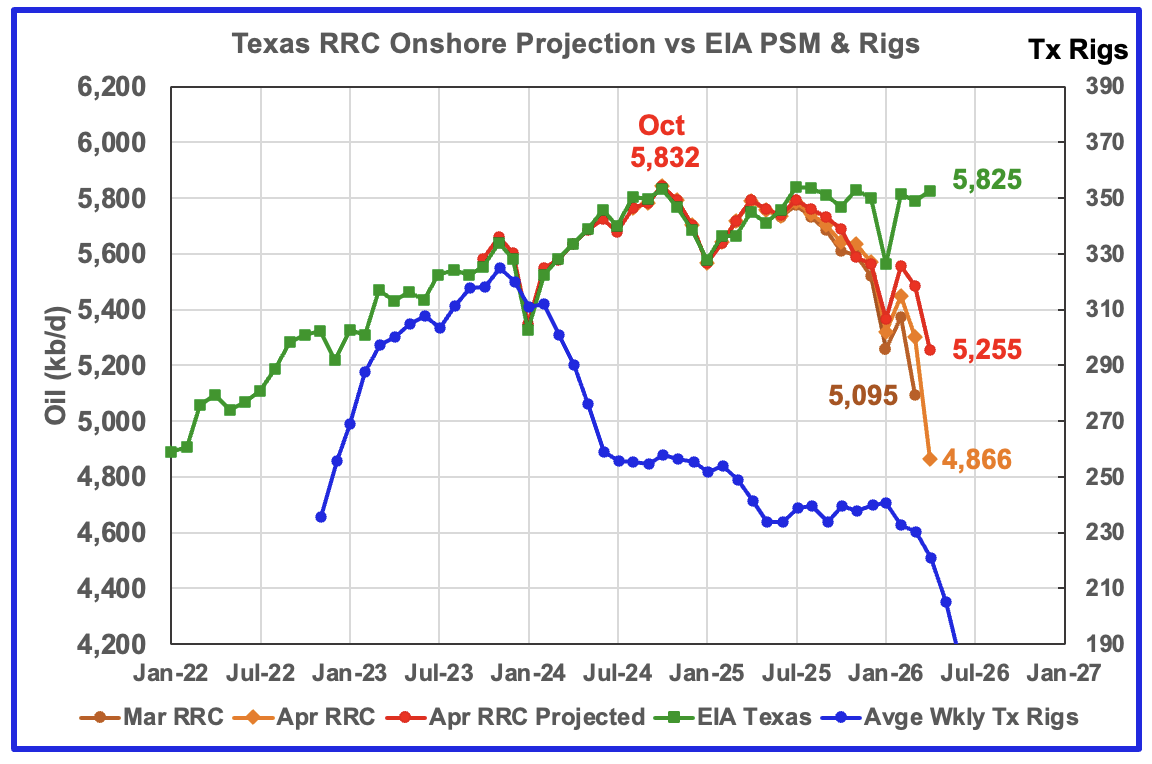

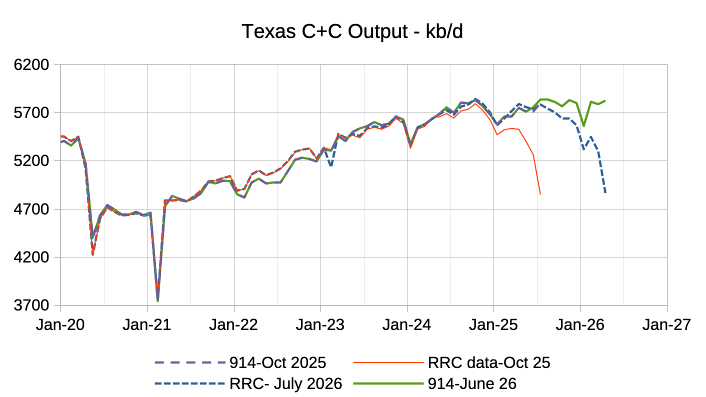

Texas’ April oil production increased by 66 kb/d to 5,825 kb/d according to the EIA. YoY production rose by 162 kb/d.

The Texas’ RRC initial production for April, orange graph, dropped by a significantly large 439 kb/d from March to 4,866 kb/d. The projection only added 514 kb/d to the April initial production to raise it 5,255 kb/d. The divergence between the EIA and the projection is due to much smaller upward revisions to March production in the April report, brown graph, which results in the very large discrepancy of 570 kb/d between the EIA and the projection

The red graph is a production projection using the preliminary March and April Texas RRC data.

The blue graph shows the average number of weekly rigs reported for each month shifted forward by 10 months. So the 276 rigs operating in July 2023 have been shifted forward to May 2024. From February 2024 to July 2024, the rig count dropped from 312 in time shifted February 2024 to 256 in July 2024. That drop of 56 rigs had little impact on production up to July 2025. August 2025 appears to be the first month when the impact of the start of the flat rig count results in essentially flat production. Will the dropping rig count starting in time shifted February/March 2026 result in dropping Texas production going forward?

According to the EIA, New Mexico’s April production rose by 65 kb/d to 2,366 kb/d. YoY production rose by 101 kb/d, second only to Texas.

The red graph shows NM’s projected output up to April and is calculated using the preliminary March and April NM OCD data. April projected production increased by 48 kb/d from March to 2,287 kb/d and is 79 kb/d or 3.3 % lower than the EIA’s reported April production. While the EIA and projection numbers are slightly different, the trend is the same.

Production in both Lea County and Eddy County rose. See Permian section further down.

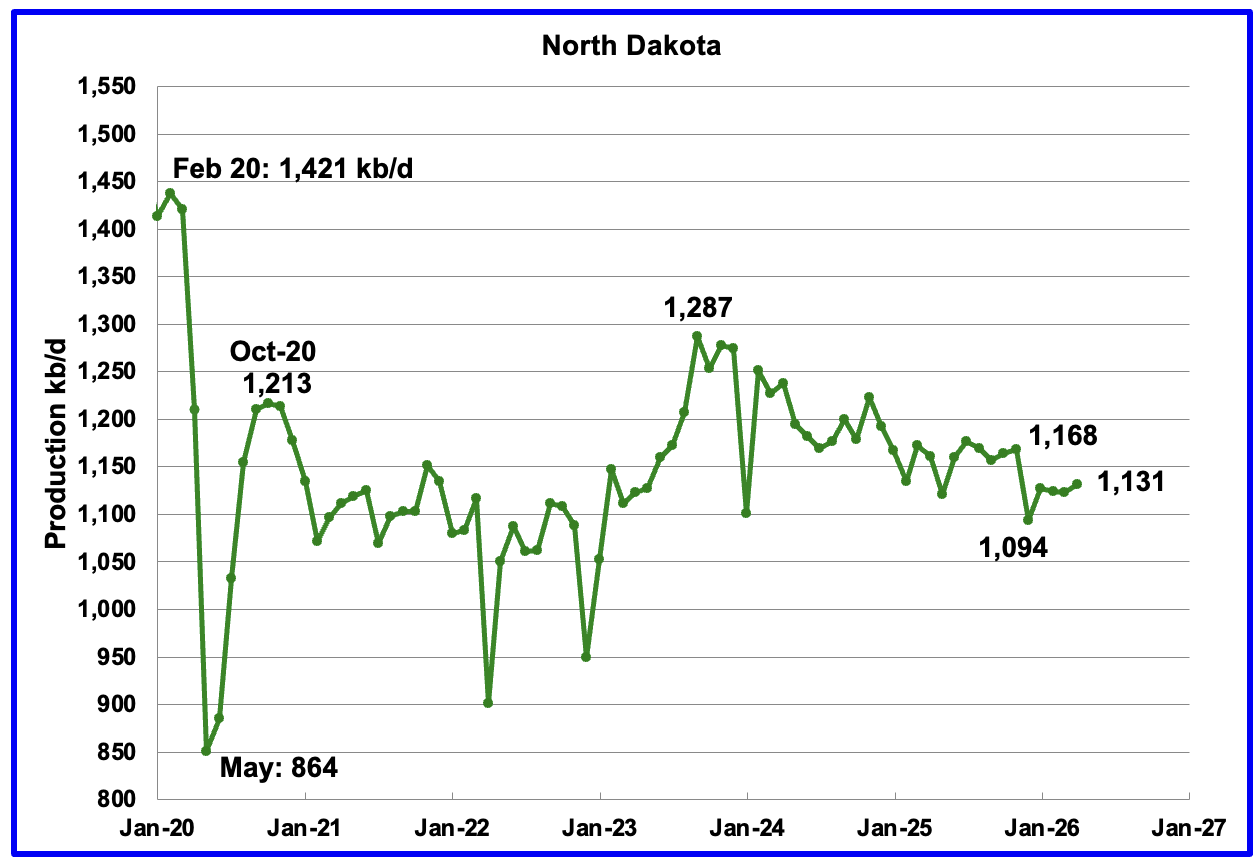

Production in North Dakota rose by 8 kb/d in April to 1,131 kb/d, according to the EIA. April 2026 production is 41 kb/d lower than last April..

The North Dakota Department of Mineral resources reported April production decreased by 6 kb/d to 1,137 kb/d, which is 6 kb/d higher than the EIA’s estimate.

According to this Article, North Dakota oil production came in below forecast.

“Nathan Anderson, director of the North Dakota Department of Mineral Resources, who released the most recent oil and natural gas production numbers Thursday, June 18, said the oil production number for April was 1.12% below the revenue forecast of 1.15 million barrels per day. He said it is a 0.48% decrease or 5,500 barrels per day from March to April.

Anderson said Bakken-Three Forks Formation production continues to dominate the production in North Dakota at about 97.4%, and 2.6% is from non-Bakken-Three Forks production.

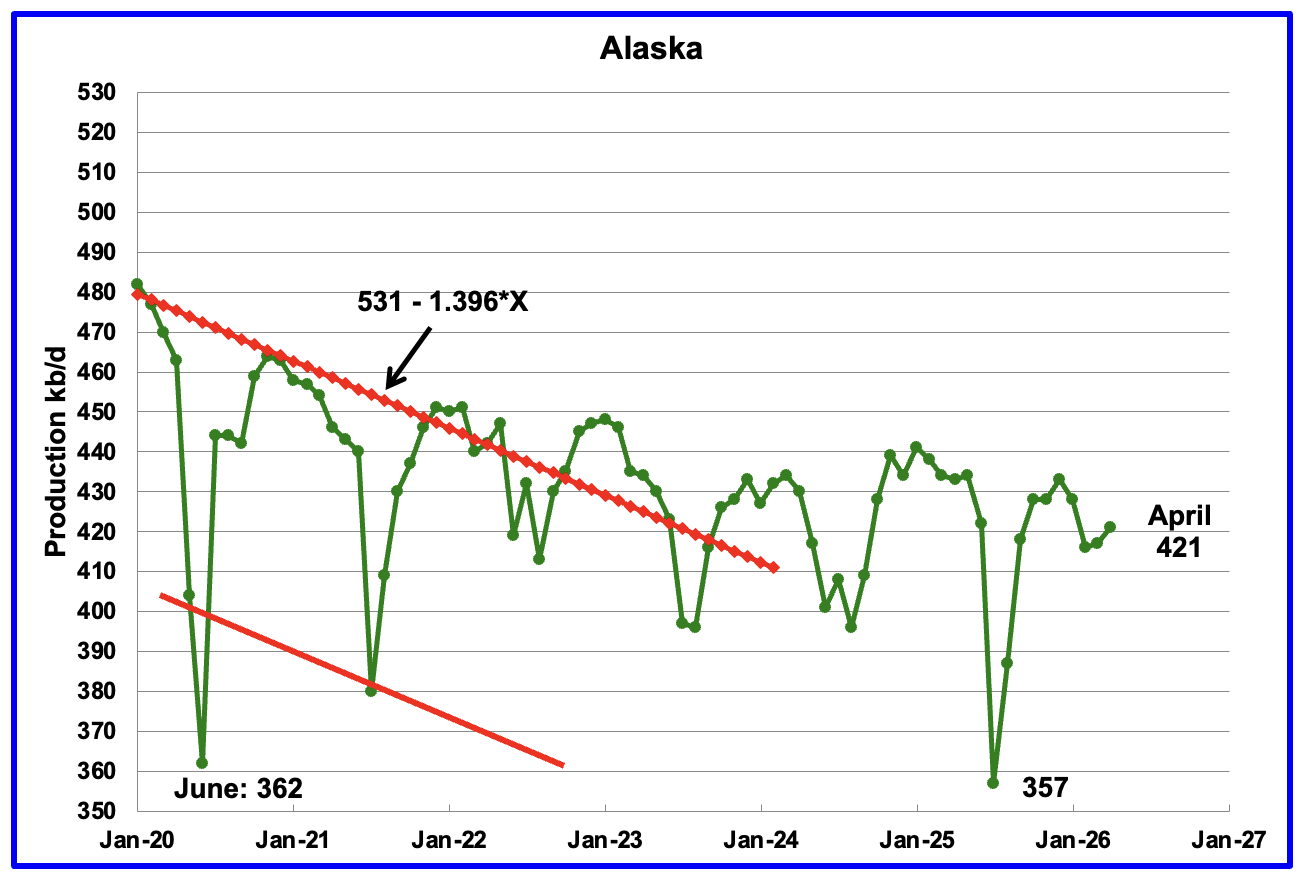

Alaskaʼs April output rose by 4 kb/d to 421 kb/d while YoY production decreased by 13 kb/d. The EIA’s weekly report for April indicated that April production would average close to 423 kb/d.

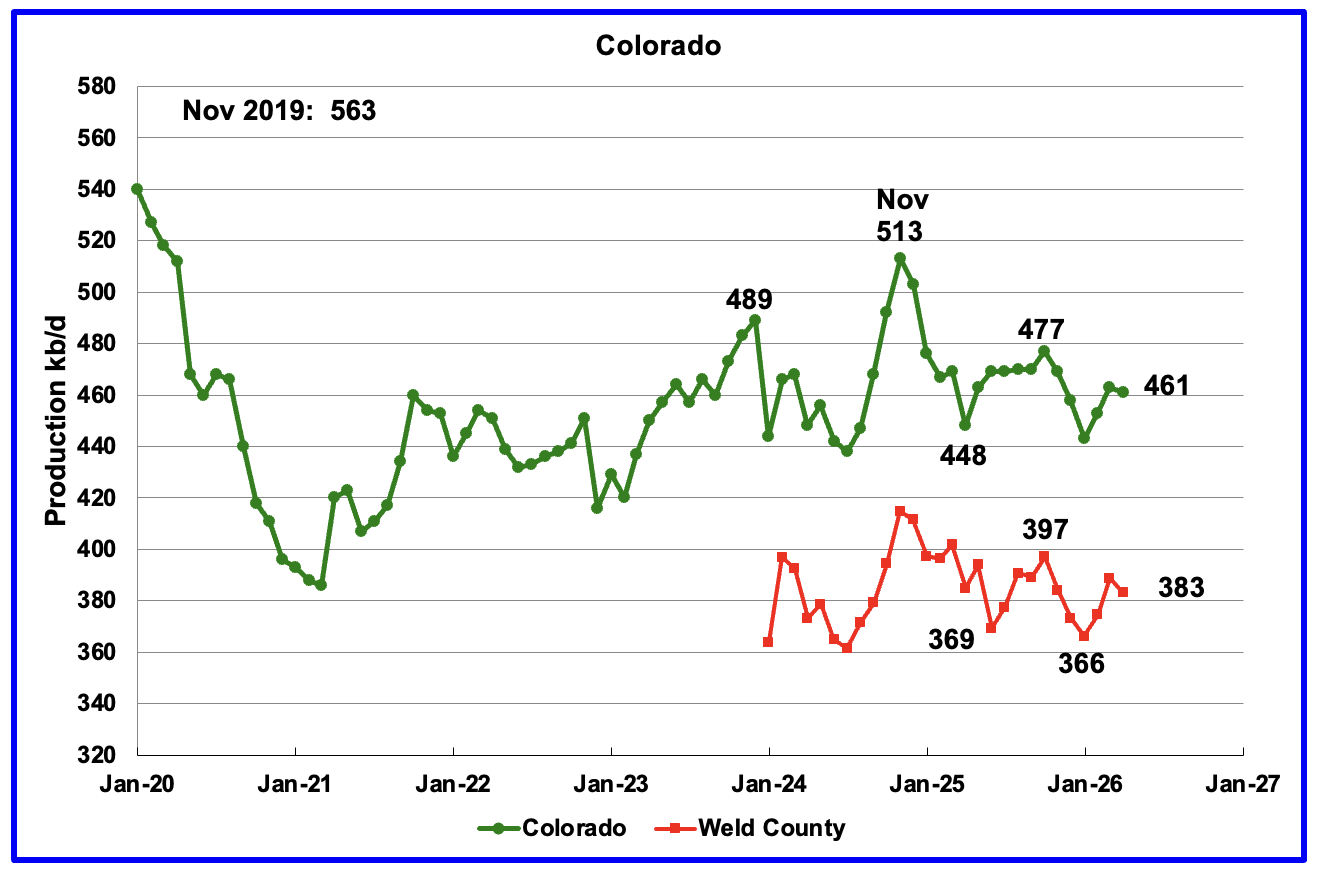

Coloradoʼs April oil production dropped by 2 kb/d to 461 kb/d.

The biggest oil producing county in Colorado is Weld County and its production has been added to the chart. The two graphs have almost been parallel over the last six months. Weld’s production dropped by 6 kb/d in April to 383 kb/d.

Colorado began 2026 with 7 rigs in January and they rose to 9 rigs in late June. Of the 9 rigs, 7 were stationed in Weld county.

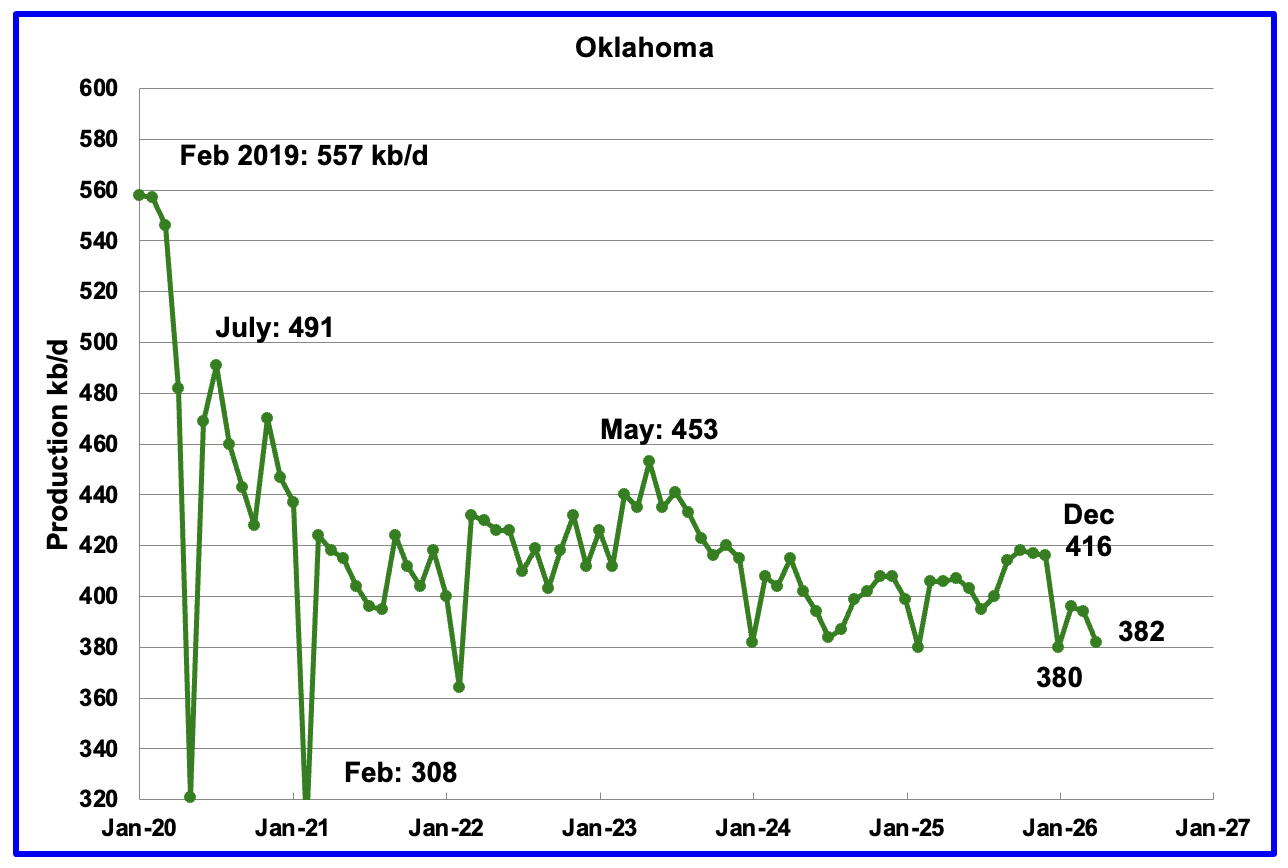

April oil production dropped by 12 kb/d from March to 382 kb/d.

Oklahoma’s January output dropped by 36 kb/d to 380 kb/d due to severe weather. Production remains below the post pandemic July 2020 high of 491 kb/d and is down by 71 kb/d since May 2023. Oklahoma’s production continues to stay within the 400 kb/d ± 20 kb/d range.

Oklahoma had 40 operational rigs in January 2026 and they have slowly increased to 45 in late June.

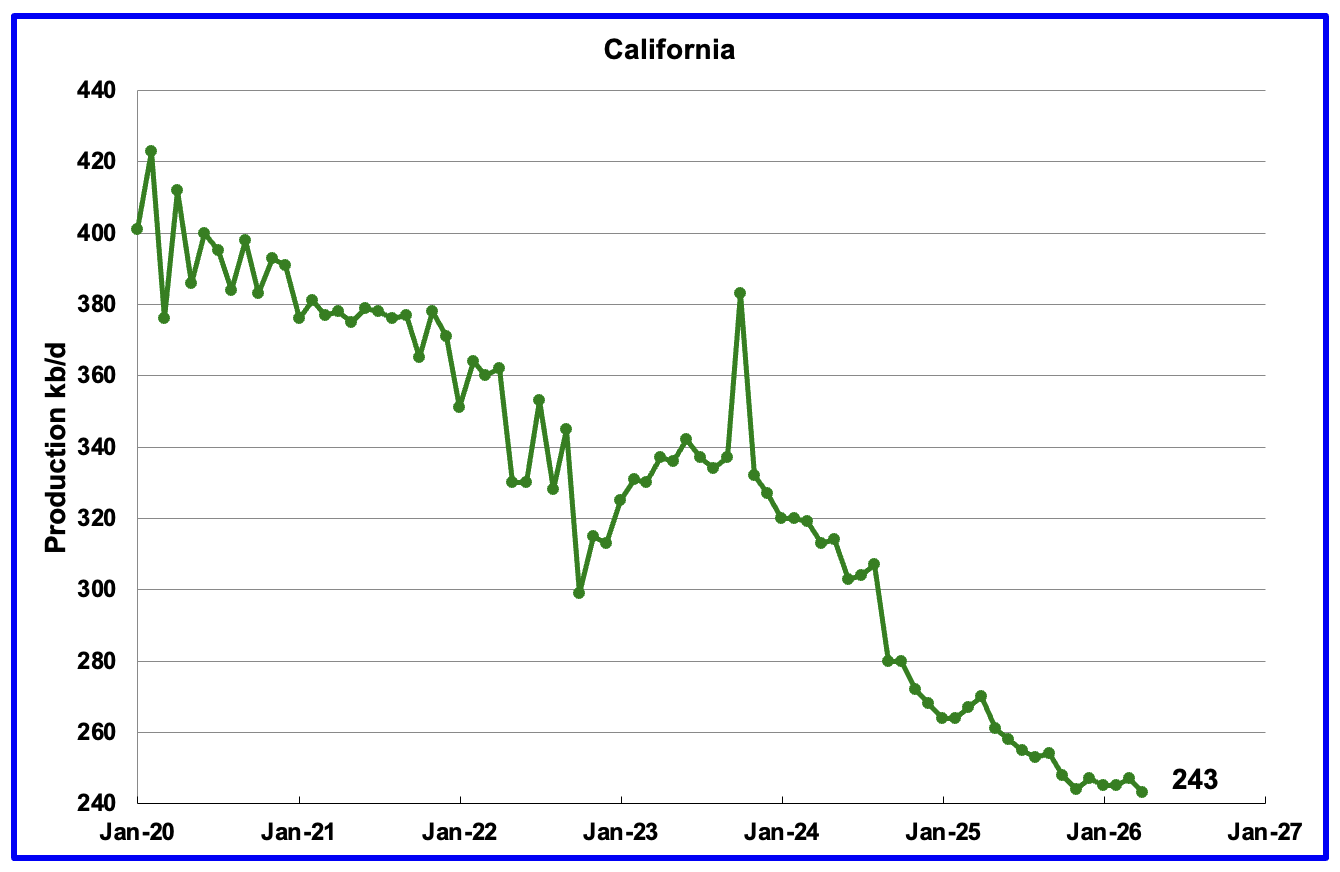

California’s overall declining production trend continues. April dropped by 4 kb/d to 243 kb/d. YoY production dropped by 24 kb/d.

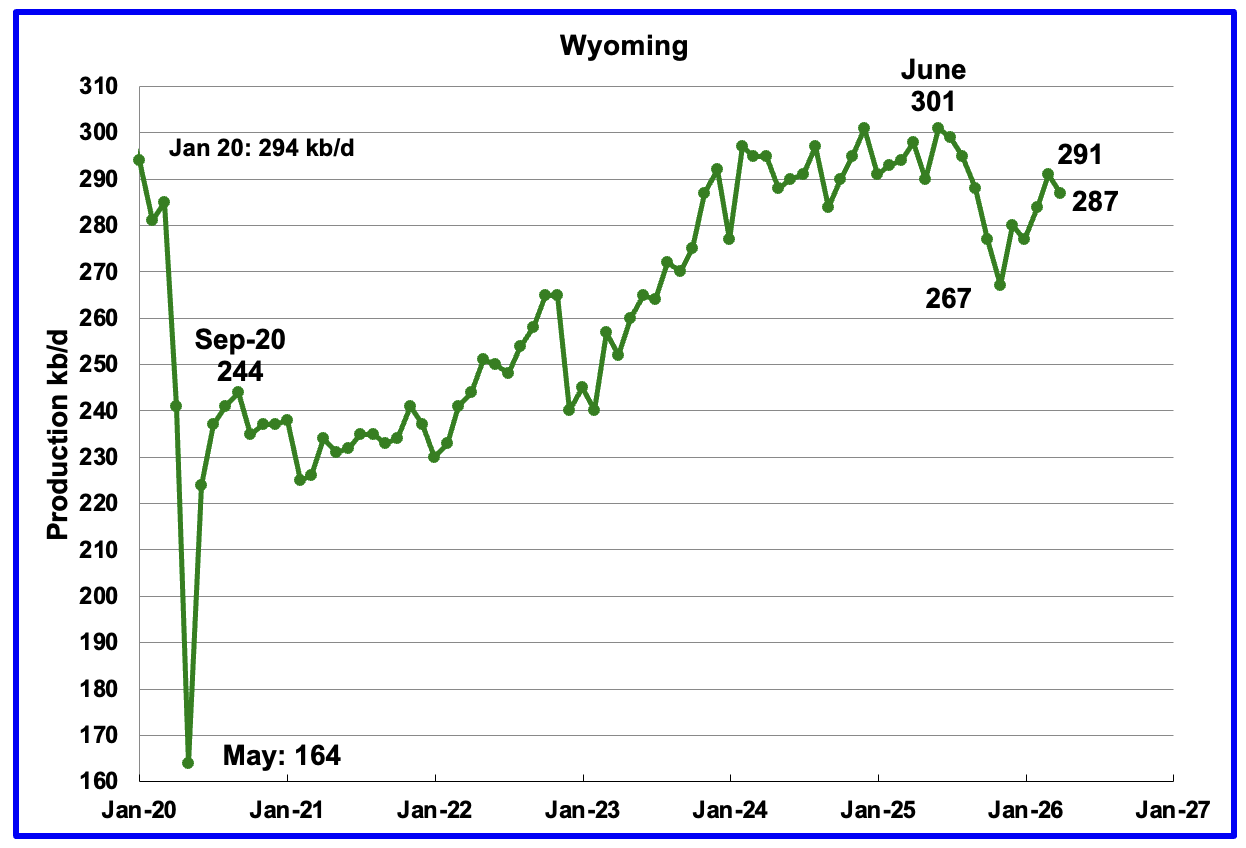

Wyoming’s oil production reached a post pandemic high in June 2025 of 301 kb/d. Production dropped in each of the subsequent 5 months before rebounding in December. April production dropped by 4 kb/d to 287 kb/d.

Wyoming started the year with 13 rigs and in late June added 1 to 14 operational rigs.

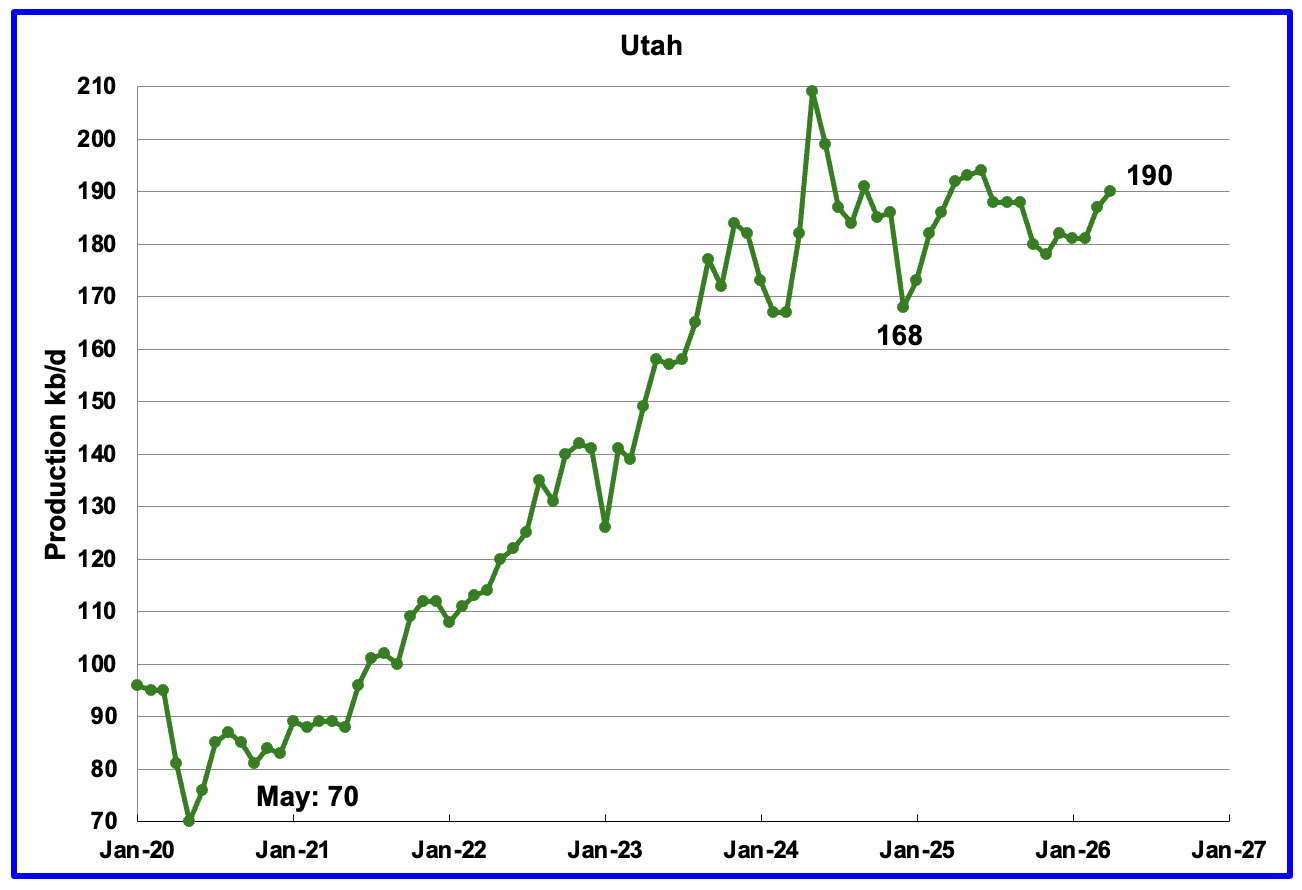

April production rose by 3 kb/d to 190 kb/d. Utah had 11 rigs operating in late January. In June, the number of operational rigs had dropped to 8.

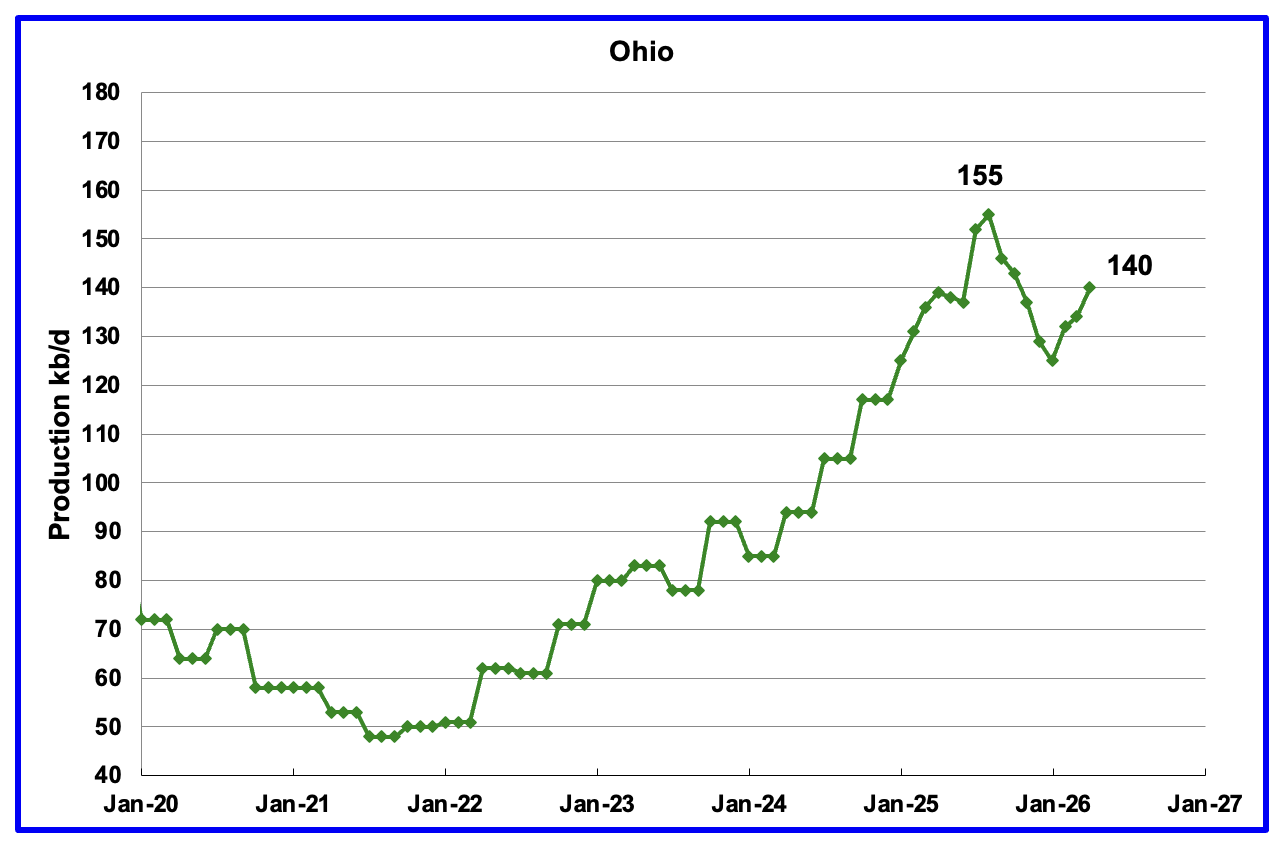

Ohio’s April oil production increased by 6 kb/d to 140 kb/d and was 15 kb/d lower than the August peak of 155 kb/d. In January 2026 Ohio had 12 NG rigs operating. At the end of June, nine NG rigs were operational along with one oil rig.

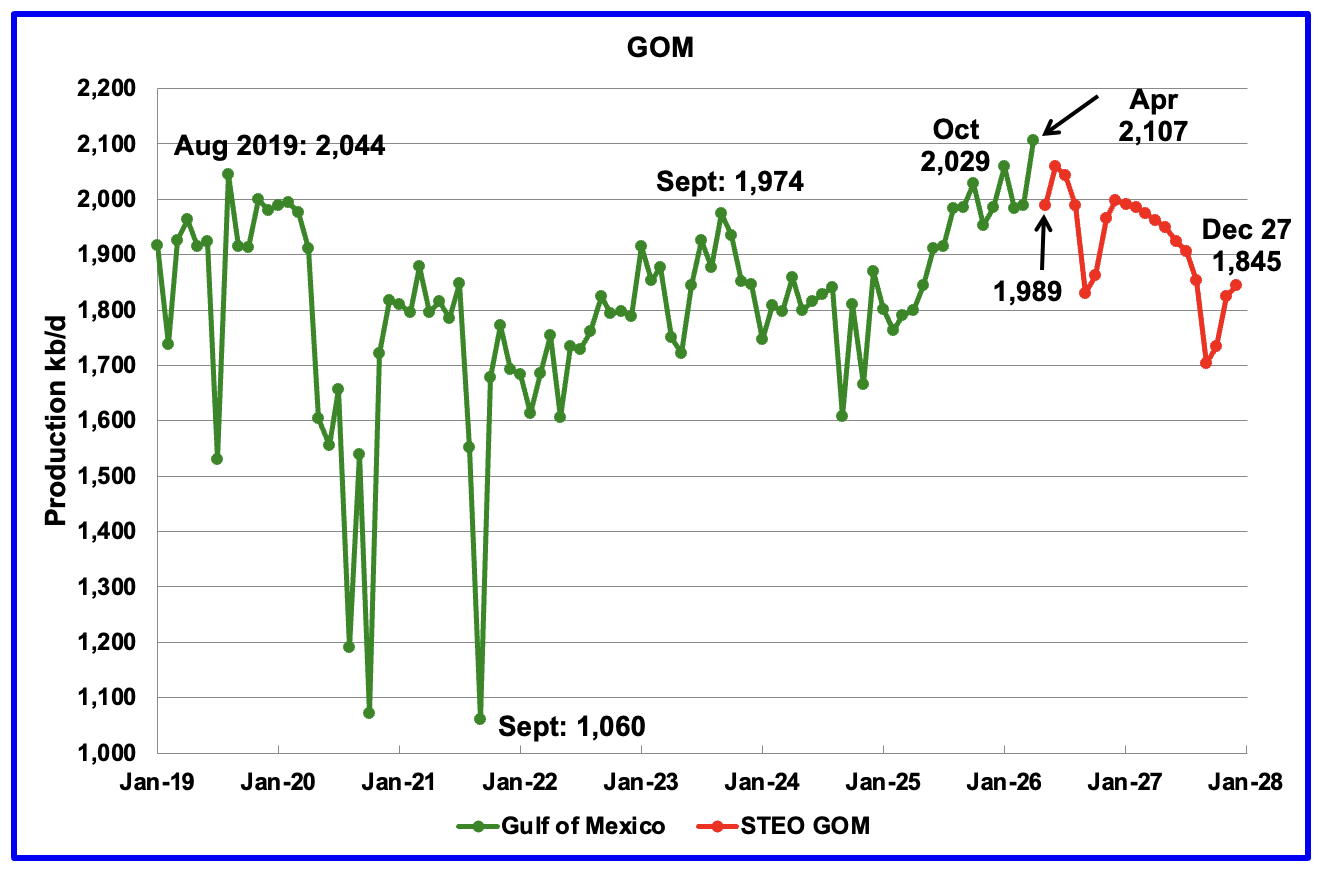

GOM production rose by 119 kb/d in April to 2,107 kb/d a new record high. It is up by 316 kb/d YoY.

The July 2026 STEO GOM projection has been added to this chart. For May production is projected to decrease by 118 kb/d to 1,989 kb/d. It also projects production in December 2027 will be lower at 1,8445 kb/d.

A Different Perspective on US Oil Production

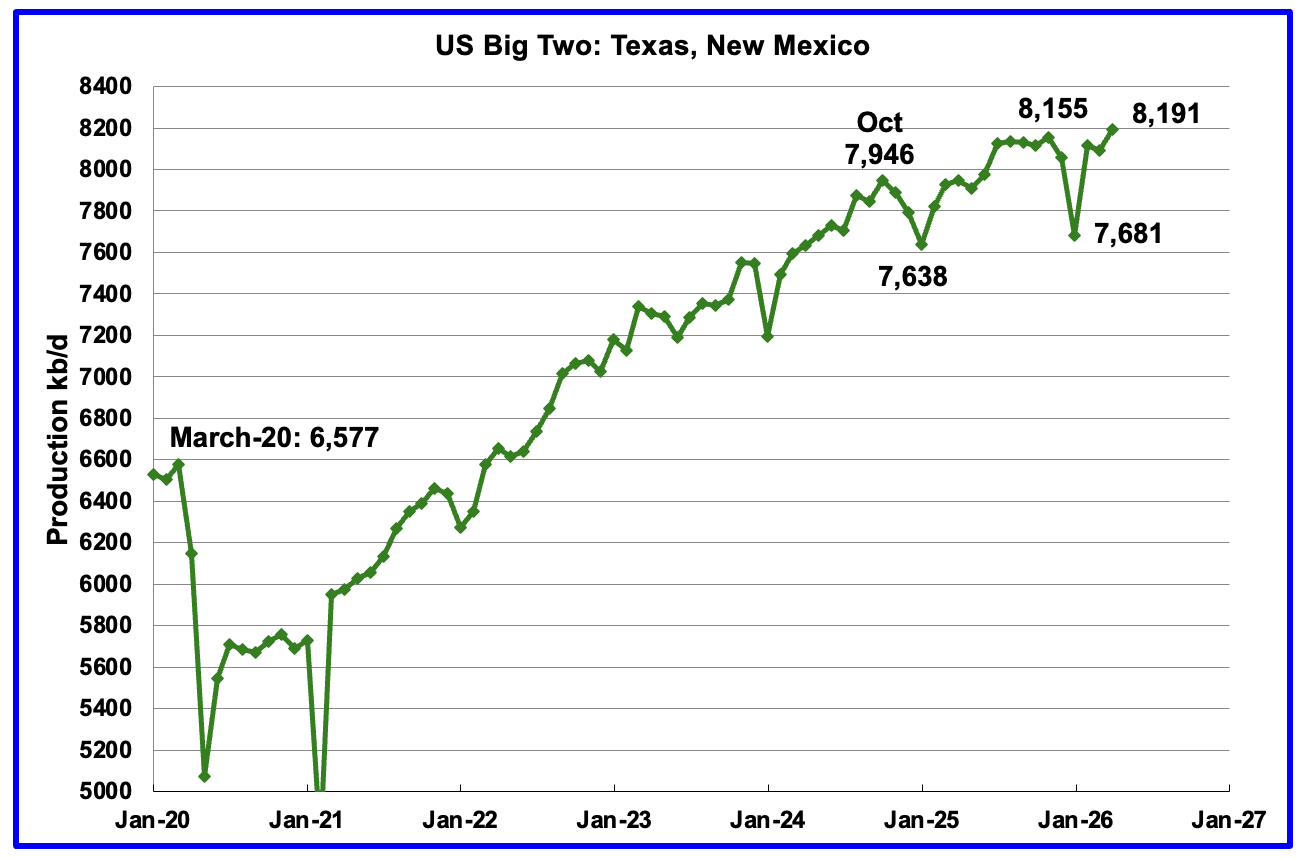

Combined Oil output for the Big Two states Texas and New Mexico.

April production in the Big Two states increased by a combined 101 kb/d to 8,191 kb/d, another new record high. The increase was due to a production rise in both Texas and NM, 36 kb/d and 65 kb/d, respectfully. Clearly these two states were the drivers of US oil production growth up to July 2025. The essentially flat production starting in August 2025 was the first sign that production in these two states was close to peaking. The next few months will determine whether these two states are in their plateau phase.

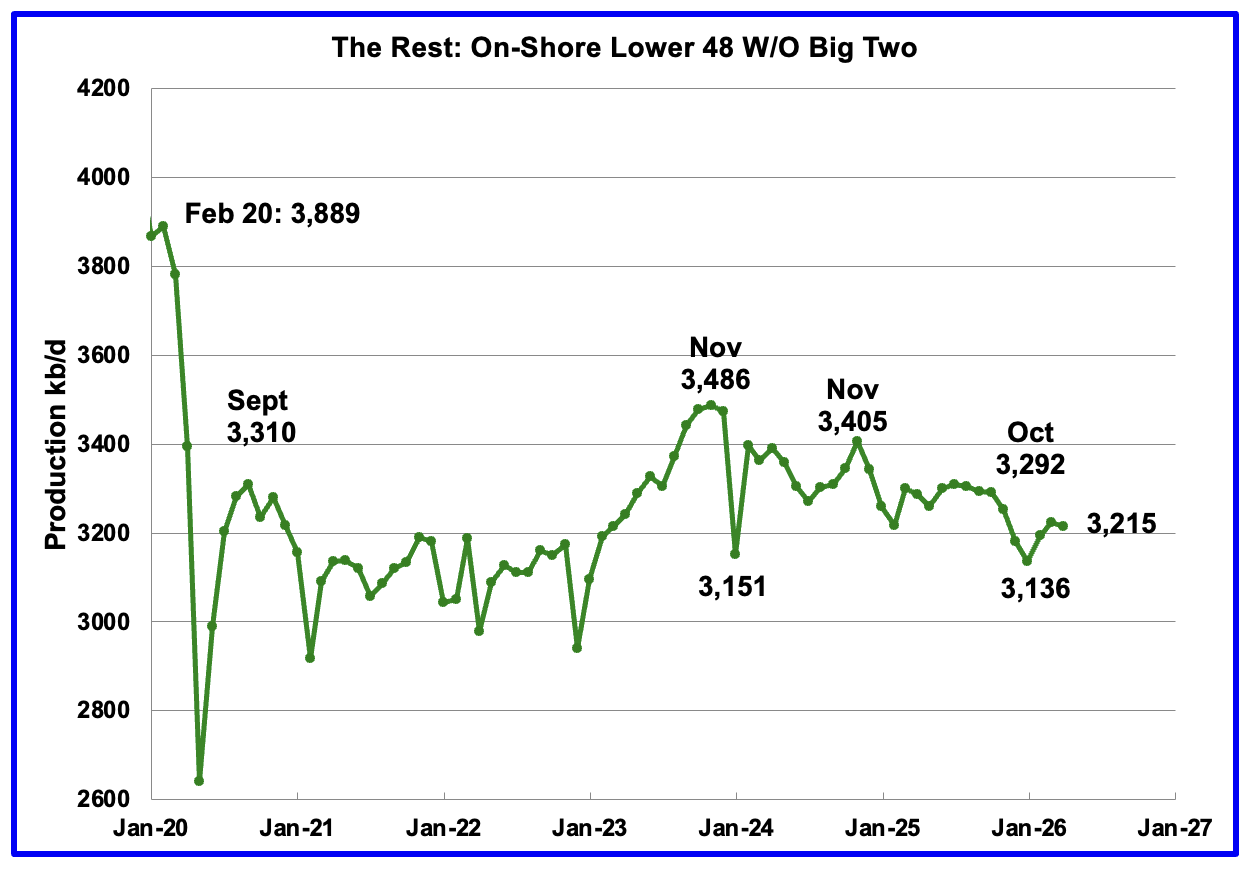

Oil Production by The Rest

April oil production by The Rest dropped by 8 kb/d to 3,215 kb/d and is 271 kb/d lower than November 2023. The remaining states may have entered a slowly declining phase.

Permian Basin Report for Main Counties and a District

This special monthly Permian section was added to the US report because of a range of views on whether Permian production will continue to grow or will peak over the next year or two. The issue was brought into focus many months back by two Goehring and Rozencwajg Reports and Report2 which indicated that a few of the biggest Permian oil producing counties were close to peaking or past peak.

A more recent report was issued and can be reviewed Here. In this report they state:

“For years now, we have outlined with what we hoped was clarity, and what we now submit was prescience, the view that U.S. shale oil, that great source of modern supply, could not grow forever. It would mature, crest, and begin its long descent. That moment, by our models and measures, has arrived: shale has plateaued, and 2024 appears to be its high-water mark. And yet, investor sentiment has scarcely been more downbeat.”

This section will focus on the four largest oil producing counties in the Permian, Lea, Eddy, Midland and Martin. It will track the oil production and the associated Gas Oil Ratio (GOR) on a monthly basis. The data is taken from the state’s government agencies for Texas and New Mexico. Typically the data for the latest two or three months is not complete and is revised upward as companies submit their updated information. Note the GOR shown in the charts uses the gas coming from both the gas and oil wells.

Of particular interest will be the charts which plot oil production vs GOR for a county to see if a particular characteristic develops that indicates the field is close to entering or in the bubble point phase. While the GOR metric is best suited for characterizing individual wells, counties with closely spaced horizontal wells may display a behaviour similar to individual wells due to pressure cross talking . For further information on the bubble point and GOR, there are a few good thoughts on the intricacies of the GOR in an earlier POB comment and here. Also check this EIA topic on GOR.

New Mexico Permian

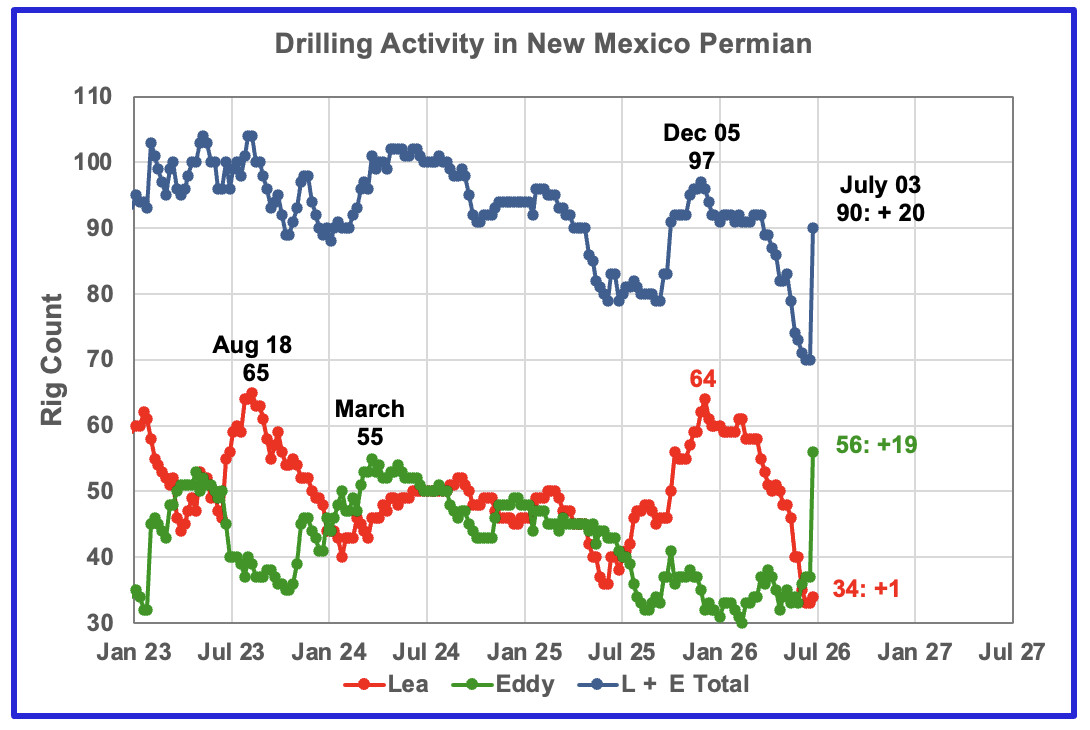

The rig count in Lea County has continued to decline over the last 8 weeks. Over the past six months Lea County dropped 30 rigs to 34 while Eddy added 19 Hz and Directional rigs last week. Actually the 19 Drigs operating in Eddy county were re-classified as Hz rig.

Eddy County added 14 Directional rigs between May 21, 2026 and June 11, 2025 for a total of 20. This is a significant addition to drilling capacity regardless of whether they were Hz or Drigs

Oil Production in New Mexico’s Primary Permian Counties

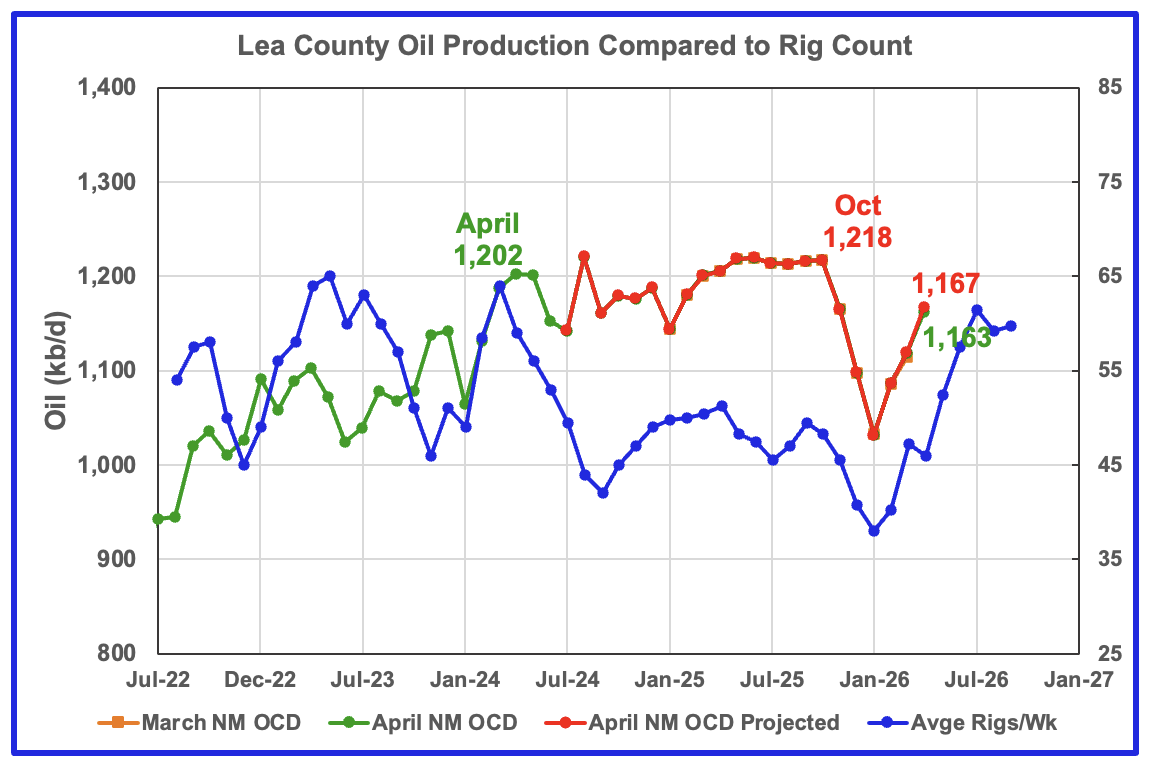

Lea County’s oil production started its plateau phase in April 2024 at 1,202 kb/d and it continued to October 2025. November 2025 to January 2026 has seen steady production drops in both the projected and NM OCD’s preliminary production. However the majority of January’s projected production drop of 66 kb/d was due to the severe January weather. February projected production rebounded and came in at 1,087 kb/d, revised down from 1,093 kb/d in the previous post.

April projected production increased by 48 kb/d to 1,167 kb/d. It now appears more likely that the projected production increases in March and April are related to the time shifted increasing rig count. The question/issue here is whether production will exceed the October 2025 peak of 1,218 kb/d or peak at a new lower level? Note that from time shifted April 2026 to July 2026 the rig count increases from 46 to 61.

Preliminary April data from New Mexico’s Oil Conservation Division (OCD) indicates Lea County’s April oil production rose by 44 kb/d to 1,163 kb/d, green graph.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly rig data. The rig graph has been time shifted forward by 7 months. So the 64 Rigs/wk operating in August 2023 have been time shifted forward to March 2024 to show the possible correlation and time delay between rig count, completion and oil production.

Note that rig counts are being used to project production as opposed to completions because state completion data is not available. Completion data from the Drilling Productivity report below indicates that the number of completed DUCs slightly exceeds newly drilled wells in the Permian basin.

According to this Article, Devon Energy has recently acquired land in Lea and Eddy counties. The acquisition cost $2.6B or $161,500 per net acre and adds approximately 400 net locations normalized to 2-mile laterals, with expected strong well economics and low breakevens.

According to this Article: Wolfcamp Y currently delivers the strongest overall performance among the primary target.

“Type curve analysis of nearby wells reveals that Wolfcamp Y currently delivers the strongest overall performance among the primary target benches in the area (Figure 2). Wells turned to production since 2024 average approximately 10,000-foot laterals, roughly 2,300 pounds of proppant per lateral foot, and the average Estimated Ultimate Recovery (EUR) is roughly 75 barrels of oil equivalent (BOE) per lateral foot. These are some of the strongest development metrics currently being observed in the northern Delaware Basin and help explain why operators are aggressively competing for undeveloped acreage capable of supporting similar future development programs.

This Article states there are 10 to 20 years of Tier 1 drilling inventory remaining in the Permian.

Prieto said the company has been watching the development of new zones, including the Woodford and Barnett, Avalon and Harkey Sand and Wolfcamp C and D benches. Technology is lowering drilling and completion costs, improving efficiency and lowering breakeven costs, making those new zones competitive, he said.

“The Permian Basin is evolving as the best play through technology and innovation,” he said.

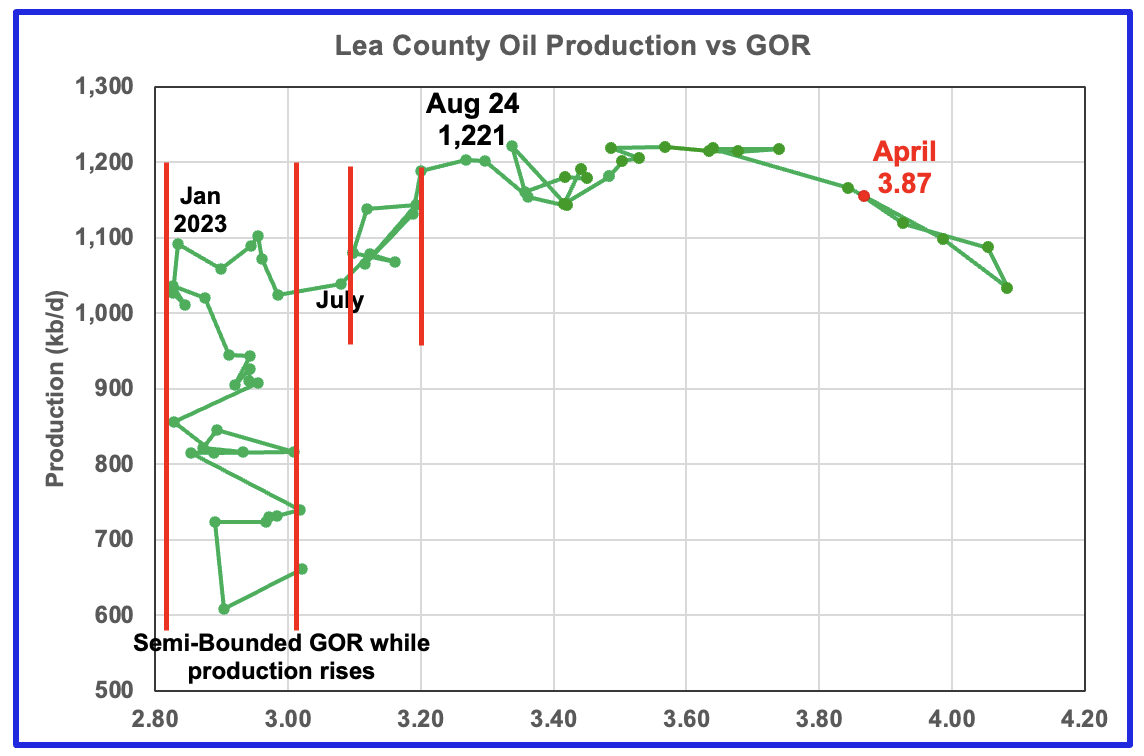

After much zigging and zagging, oil production in Lea county stabilized just below 1,100 kb/d in early 2023. Once production reached a new high in January 2023, production appeared to be on a plateau while the GOR started to increase rapidly to the right and first entered the bubble point phase in July 2023.

Since July 2023 Lea County’s production continued to increase as the GOR remained within a second semi-bounded region. This may indicate that additional production was coming from an oilier part of a layer since the GOR’s behaviour since August 2023 to March 2024 time frame appears once again to be in a second semi bounded GOR phase accompanied with rising production.

The GOR moved out of the second semi-bounded GOR region in April 2024 and production hit a new high of 1,221 kb/d in August 2024. From August 2024 to February 2025 the GOR was range bound between 3.34 and 3.53 but starting in June 2025 the GOR started to rise every month, except for one, to hit new highs. February through April saw a double change in direction, both a production increase and a GOR decrease to 3.87, which may be consistent with rising production.

This zigging and zagging GOR pattern within a semi-bounded GOR while oil production increases to some stable level and then moves out to a higher GOR to the right has shown up in a number of counties. See a few additional cases below.

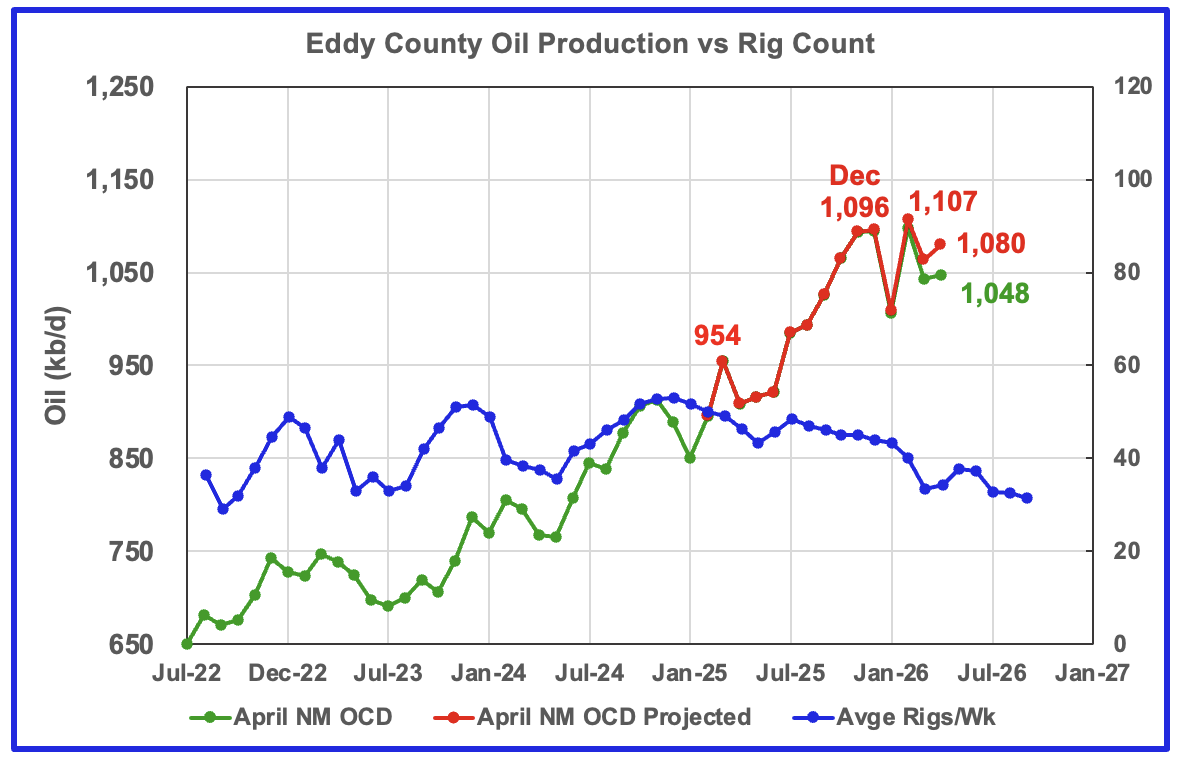

Eddy’s April projected oil production increased by 16 kb/d to 1,080 kb/d while preliminary production from the NM OCD increased by 5 kb/d to 1,048 kb/d. Most of the February production rise was due to a rebound from the severe January weather. If the storm had not occurred, January production would have been closer to 1,100 kb/d.

The dropping rig count starting in time shifted January 2026 may have finally shown up in falling production in real March followed by both a small production and rig count rise. November/December 2025 and February 2026 projected production formed a plateau. The April production rise of 16 kb/d may be the beginning of an upcoming small production increase.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the above weekly drilling chart. The rig graph has been shifted forward by 7 months to roughly coincide with the increase in the production graph starting in September/October 2023.

Between May 21, 2026 and June 11, 2025, 14 Directional Rigs were added to Eddy County. This is a significant addition of drilling capacity.

Assuming, these rigs are being use for drilling Paper Clip or U wells, this will provide a significant boost to Eddy oil production by year end. According to AI, it generally takes about 15 to 25 days (from spud to rig release) to drill a U-shaped lateral (U-turn or horseshoe well) in the Delaware Basin of Eddy County, NM. This is slightly longer than the 10-15 days it takes for a standard extended-reach single-lateral well in the Permian, due to the complex geometry of the drill path.

Assuming an average of 20 days to drill these wells, that implies 28 new wells being drilled each month. Assuming an IP of 1,500 b/d, that translates into an additional 42 kb/d of oil production starting in late 2026 or early 2027. Need to reduce this increase due to depletion but this could result in a new peak for Eddy county.

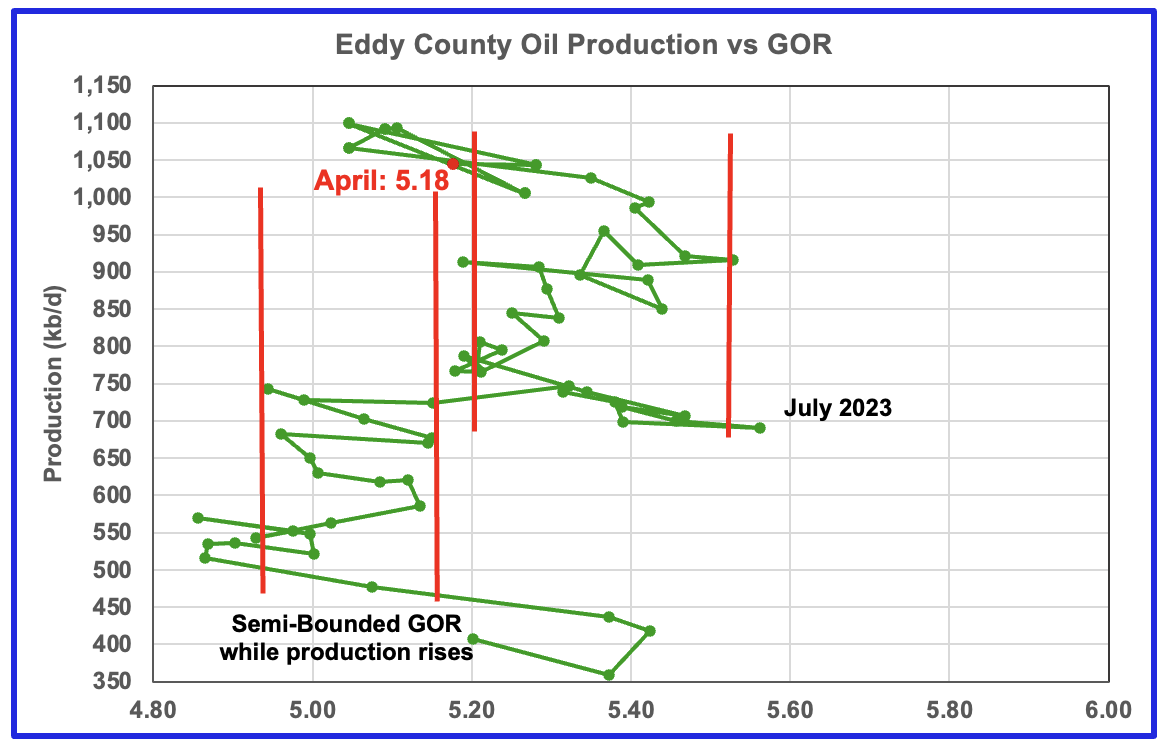

The Eddy county GOR pattern is similar to Lea county except that Eddy broke out from the first semi bounded range earlier and then added a second wider semi-bounded GOR phase.

For April New Mexico’s Oil Conservation Division (OCD) reported preliminary oil production increased by 1 kb/d to 1,044 kb/d while the GOR dropped to 5.18 and almost moved back into the first Semi-Bounded GOR range.

Texas Permian

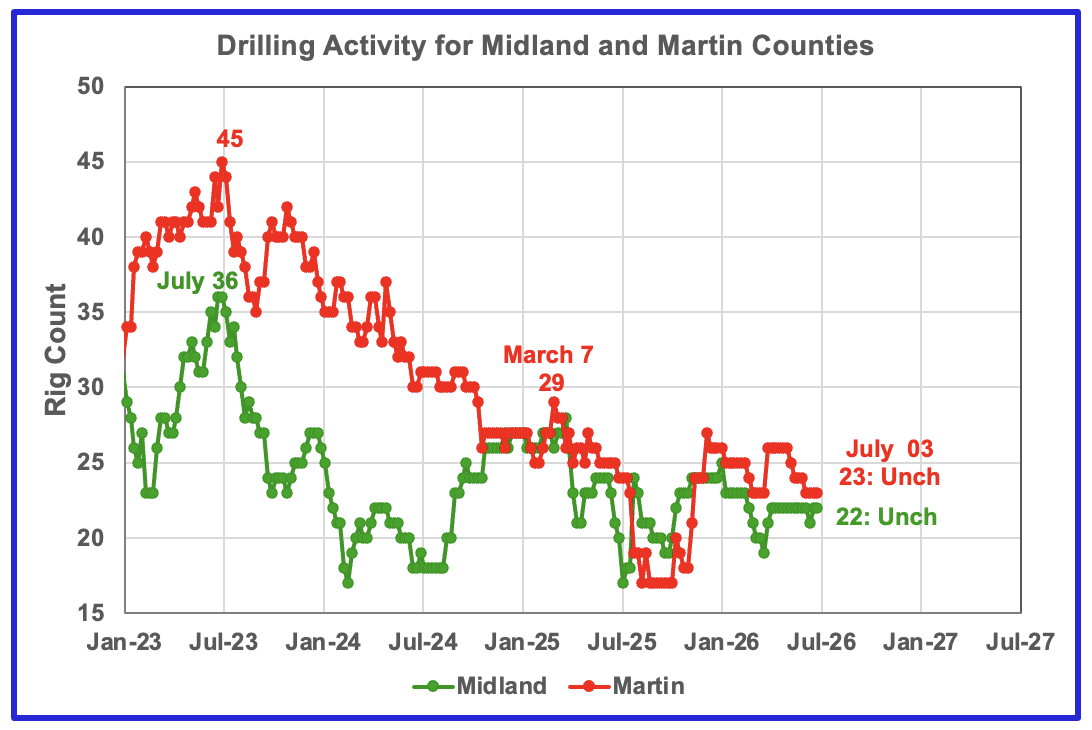

The rig count in Midland county has remained essentially unchanged for the last twelve weeks at 22 while Martin county reduced its rig count from 26 to 23 from May into early July..

Oil Production in the Two Primary Texas Permian Counties

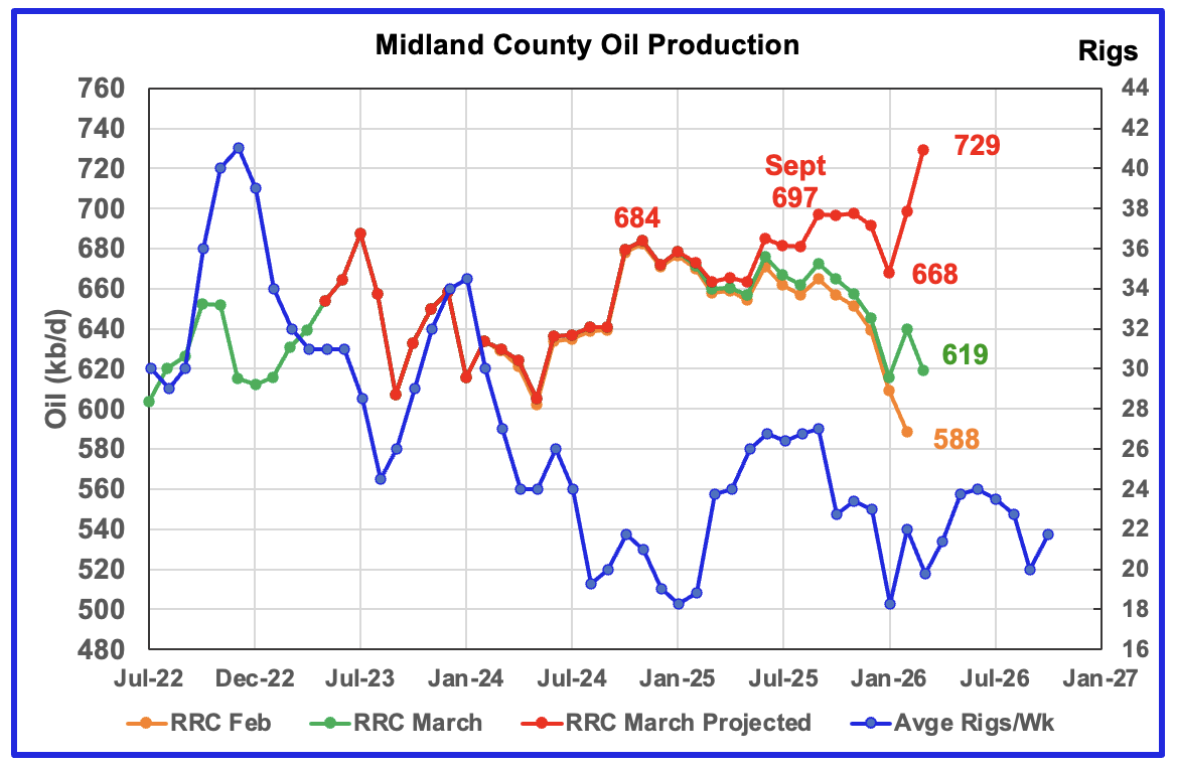

Comparison Chart from the previous post.

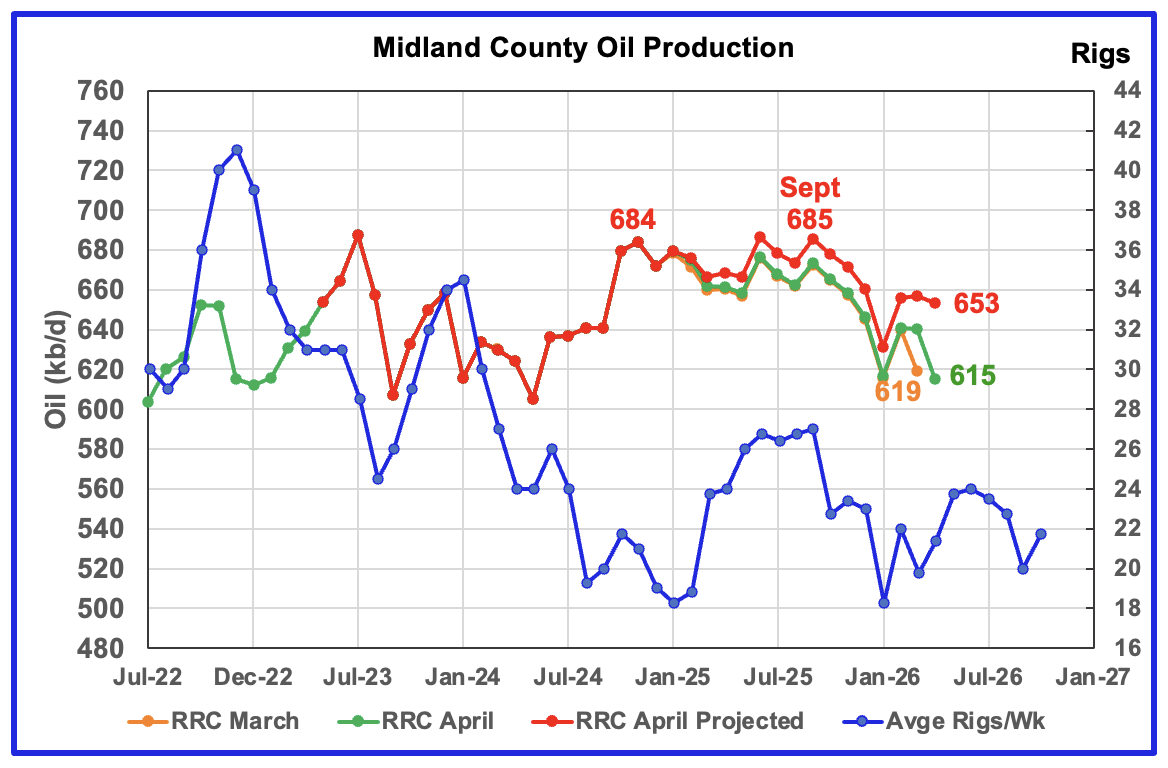

April projected production dropped by 4 kb/d to 653 b/d. The February rise is due to the production rebound from the severe Texas winter storm in late January. In the last report it was noted that “With the rig count rising in time shifted February and March from the January low, the February and March increases may be directionally correct”. It was also noted that the February and March Midland projection were too optimistic but directionally correct.

Compare the projected production for September 2025 in the preceding comparison chart with the current one. Production has dropped by 12 kb/d from 697 kb/d to 685 kb/d. The biggest change is for March. March projected production has dropped from 729 kb/d to 657 kb/d. The main reason for the large drop is the more up to date reporting of oil production for March and April.

The orange and green graphs show preliminary oil production for Midland County as reported by the Texas RRC for March and April, respectively. The red graph uses March and April data to project production as it would look after being updated over many months.

The blue graph shows the average number of weekly rigs operating during a given month as taken from the weekly drilling chart. The rig graph has been shifted forward by 6 months to better align with the latest production.

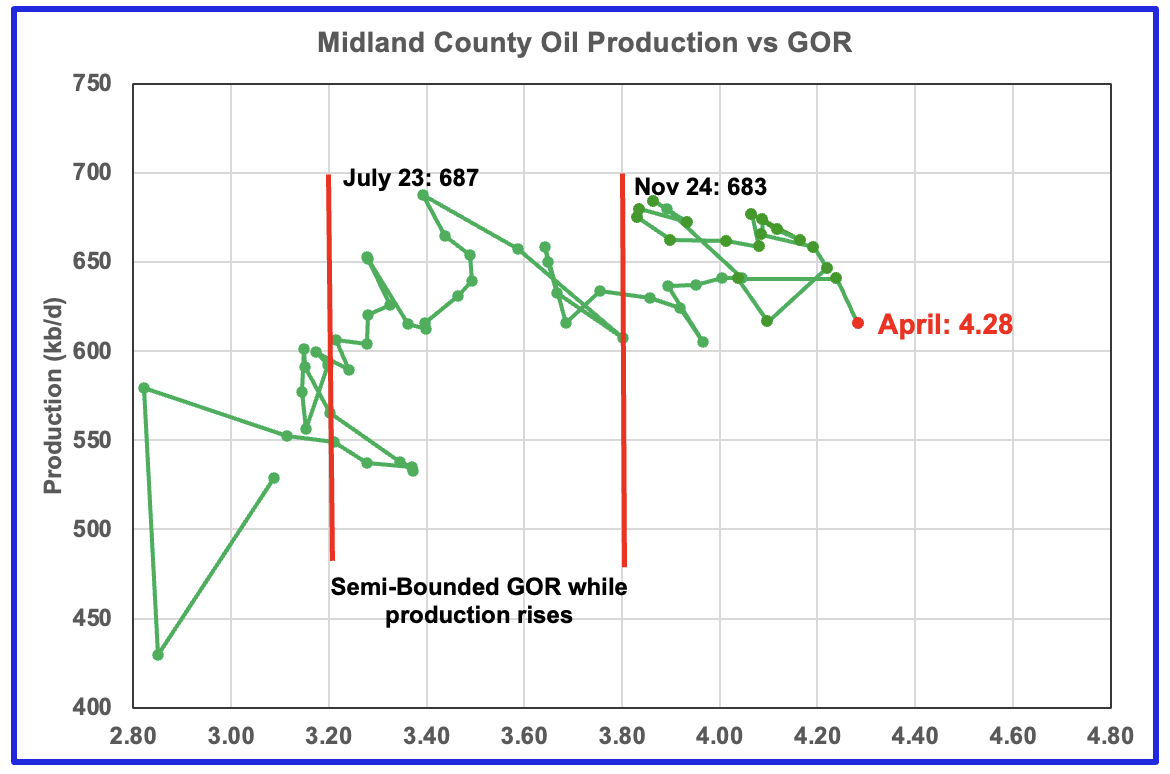

For April the Midland GOR ratio rose to a new high of 4.28 while the reported preliminary oil production dropped by 25 kb/d to 615 kb/d.

When the Midland county GOR initially moved into the bubble point phase, oil production and the GOR stayed within a narrow GOR range of 3.8 to 4.2 outside of the initial Semi-Bounded GOR region from March 2024 to November 2025. For April the GOR rose to a new high of 4.28, which is another indicator of dropping production.

The oil production and GOR shown in this chart are based on the RRC’s April preliminary production report.

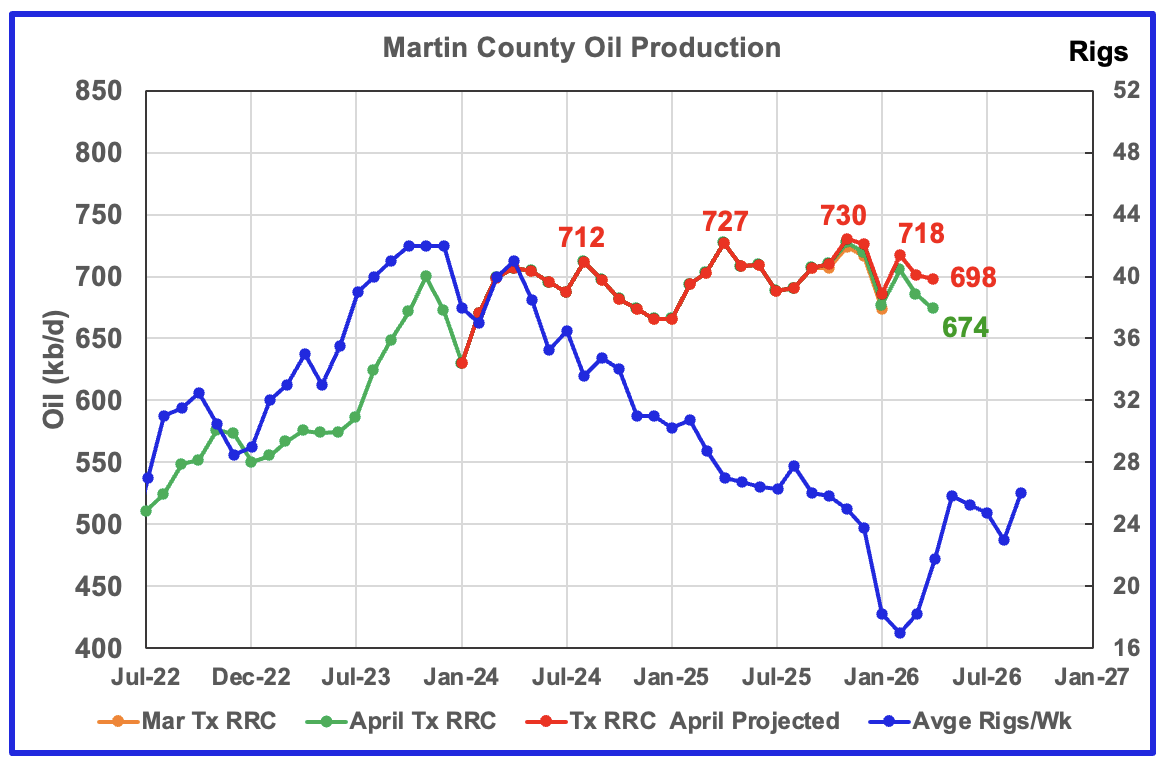

Martin’s projected April oil production dropped by 3 kb/d to 698 kb/d. Production has been essentially flat since August 2024 at close to 712 kb/d even though the rig count has been in a steady decline. Will the rising rig count starting in time shifted April 2026 affect production?

The red graph is a projection for oil production as it would look after being updated over many months. This projection is based on a methodology that uses preliminary March and April oil production data.

The orange and green graphs show production for Martin County as reported by the Texas RRC for March and April. The blue rig graph time shifts the rig count forward by 5 months.

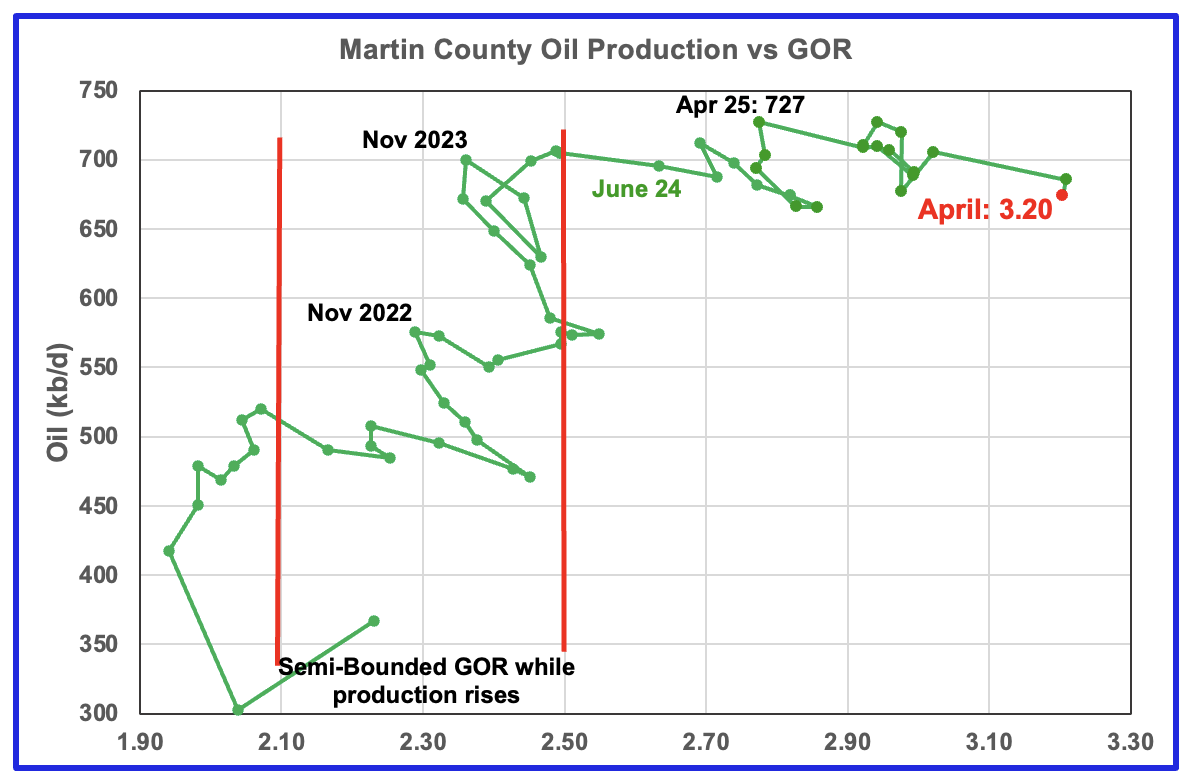

Martin county’s oil production after November 2022 increased and at the same time drifted to slightly higher GORs within the semi bounded range. However the June 2024 GOR saw its first move out of the semi bounded region.

The RRC’s preliminary April 2026 production for Martin County shows a 12 kb/d decrease to 674 kb/d accompanied by a very small decrease in the GOR to a record 3.20.

Martin county has the lowest semi-bounded GOR boundary of the four counties at a GOR of close to 2.50. The March GOR is now clearly out of the semi-bounded region. Martin County has now entered the bubble point phase that should result in a plateau phase that should shortly turn into a slowly dropping oil production phase.

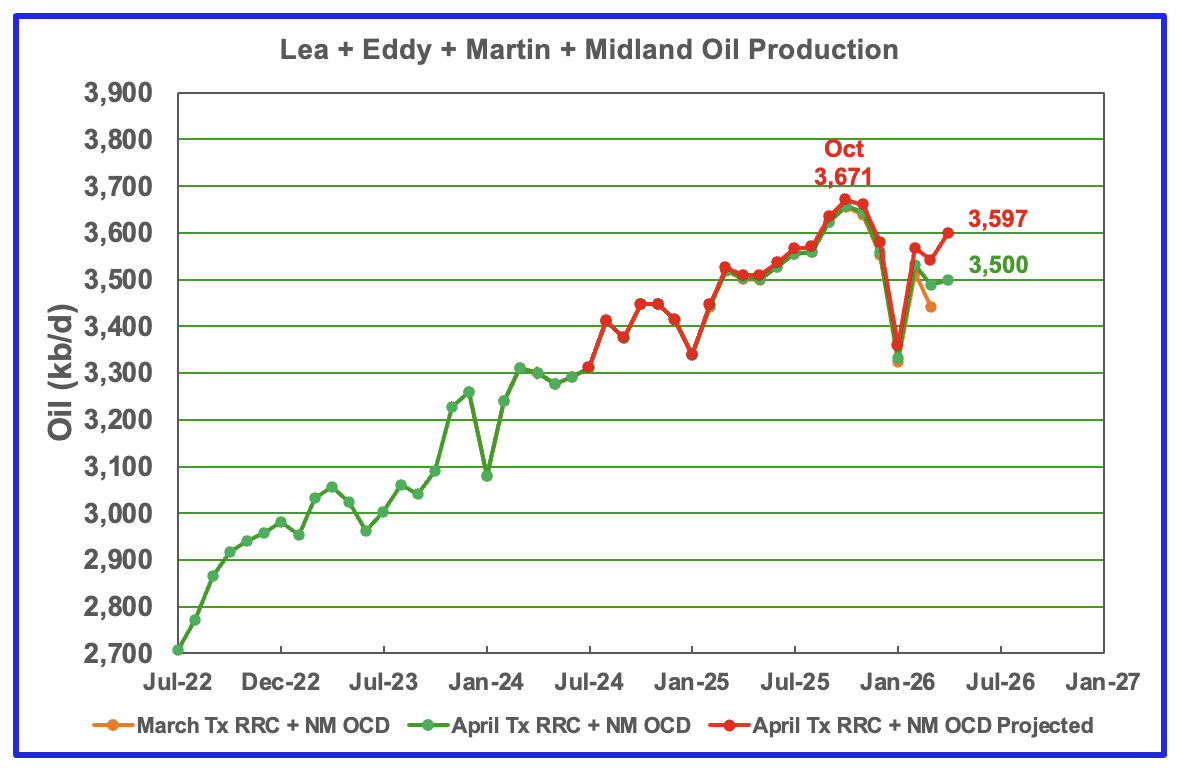

This chart shows the total oil production from the four largest Permian counties. Assuming the total current Permian production is close to 6,600 kb/d, these four counties account for 55% of the total.

April projected production increased by 58 kb/d to 3,597 kb/d. The combined increase in Lea and Eddy was 64 kb/d, offset by small drops in Midland and Martin.

The March and April initial production are shown in the orange and green graphs respectively. The red graph uses the March and April production to project a final updated production for April.

Findings

– In general the projected production charts for the Texas and New Mexico counties are very reasonable.

– Lea county entered its plateau phase in May 2024. While oil production is not following the rig count graph directly, the dropping rig count has resulted in Lea County production being in a steady flat plateau phase up to October 2025. However the November to January production drops appeared to indicate that Lea County had entered a declining phase. Rising production from February to April which is currently tracking the time shifted rig count has changed the outlook.. It is not clear whether the current rising production could enter a lower level plateau phase in 2026 as the time shifted post January rig count begins to increase.

– From July 2025 to December 2025 production in Eddy County saw a steady increase to 1,093 kb/d. February projected production rose to 1,103 kb/d. Between May 21, 2026 and June 11, 2025, 14 Directional Rigs were added to Eddy County. This is a significant addition to drilling capacity. If these rigs are used to drill Paper Clip or U wells they could add up to 42 kb/d of oil production in late 2026 early 2027.

– Midland’s April oil production indicates that Midland may have entered is declining phase as its production follows the time shifted rig count.

– Martin’s projected production has been essentially flat since August 2024. Martin’s April small projected production decrease indicates that its oil production is still in its plateau phase of approximately 715 kb/d and may be close to entering its declining phase. The next few months may show a production increase as the April and May time shifted rig count begins to rise.

Texas District 8

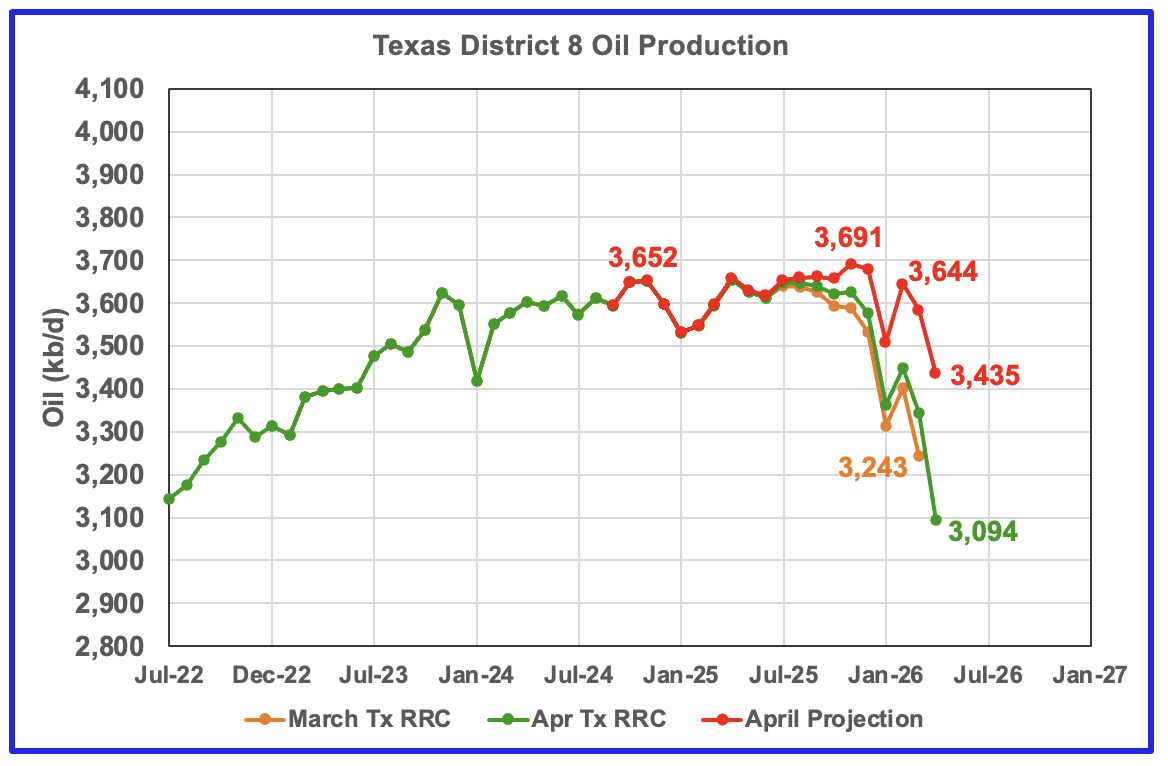

District 8’s projected production dropped by 149 Kb/d to 3,435 kb/d in April. District 8 appears to be entering its declining phase.

It was noted in the previous post that the District 8’s projected production was too optimistic due to an atypical number upward revisions to many counties in District 8. April data looks much better.

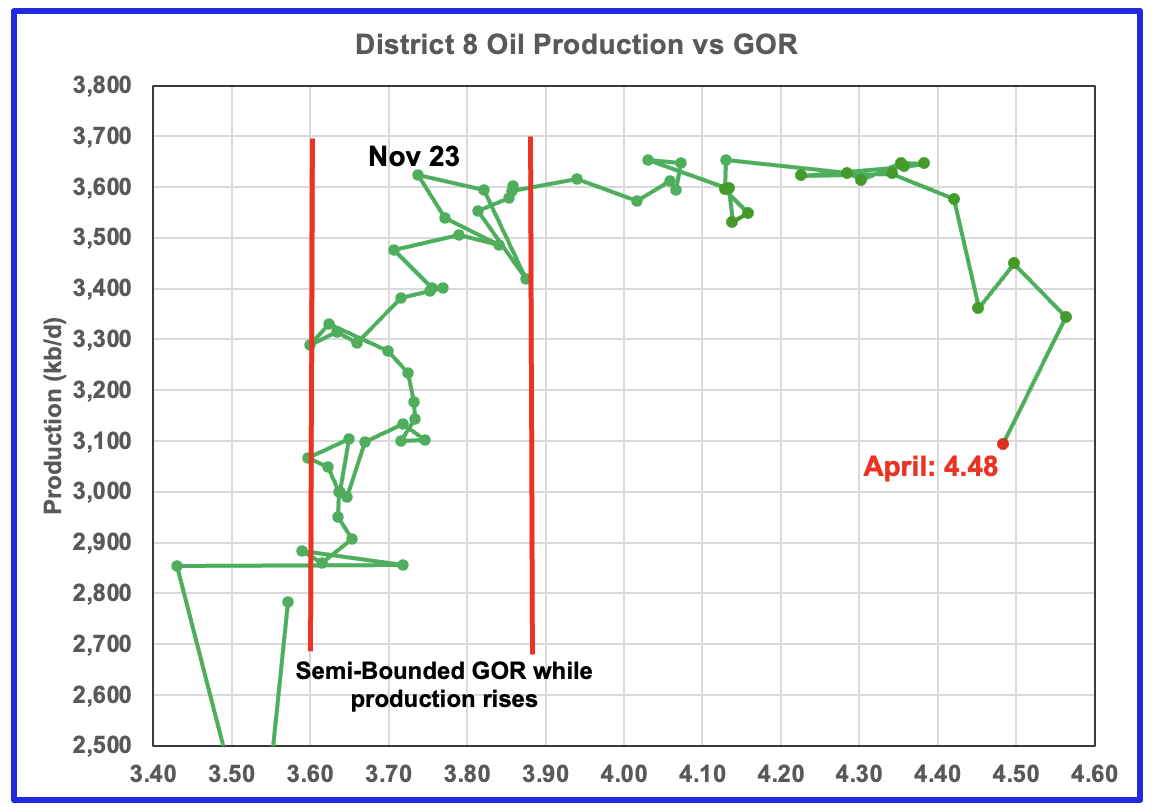

Plotting an oil production vs GOR graph for a district may be a bit of a stretch. Regardless here it is and it seems to indicate many District 8 counties may well be into the bubble point phase. The April GOR decreased to 4.48 as preliminary production continued to drop.

Oil Production and GOR Charts for Three of the Next Larger Texas Oil Producing Counties

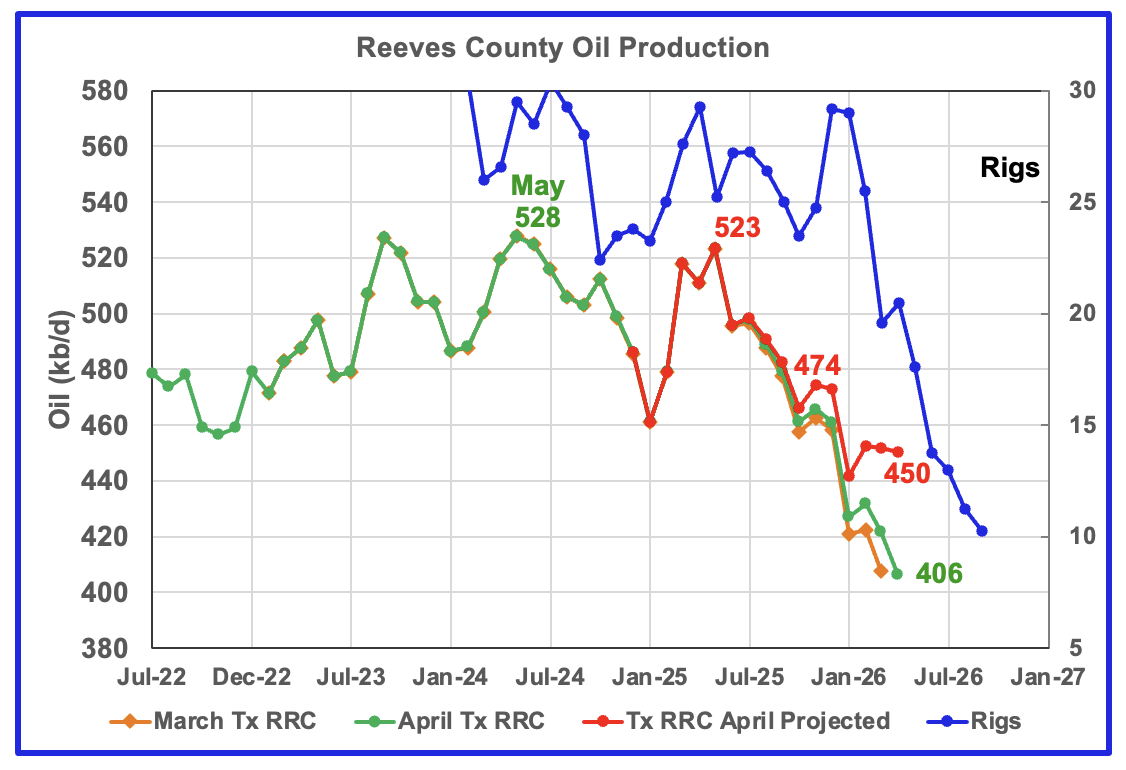

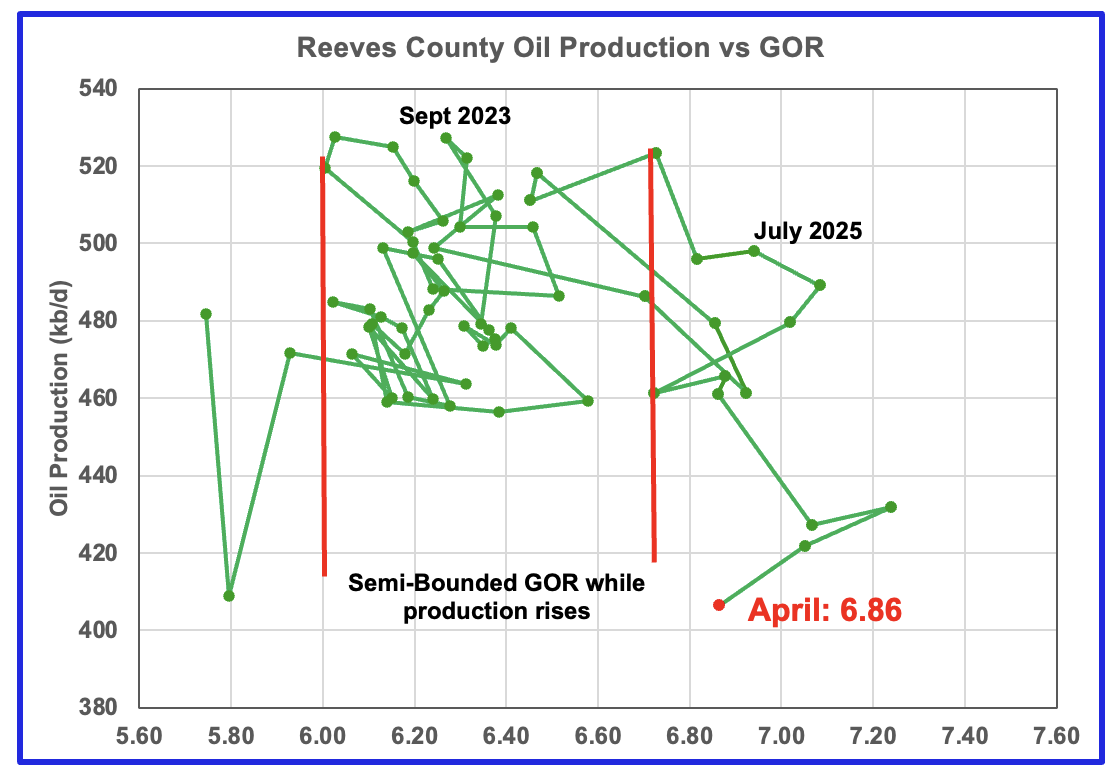

Reeves County GOR is high because it is the number one Texas county ranked by gas production. The current C + C production is almost evenly split between crude and condensate, with condensate compromising 54% of the total output.

Reeves County GOR first moved out of the Semi-Bounded region in June 2025 and in April 2026 fell to 6.86 while initial production dropped to a new low of 406 kb/d. Reeves county is in its declining phase.

The rig count is time shifted forward by 7 months.

In real June 2025, 29 rigs were operational in Reeves county. By late May 2026 the rig count had risen to 16 from a February low of 10. Regardless of the current increase, 29 rigs to 17 rigs is a large drop in 11 months. The large drop shows up starting in time shifted February 2026.

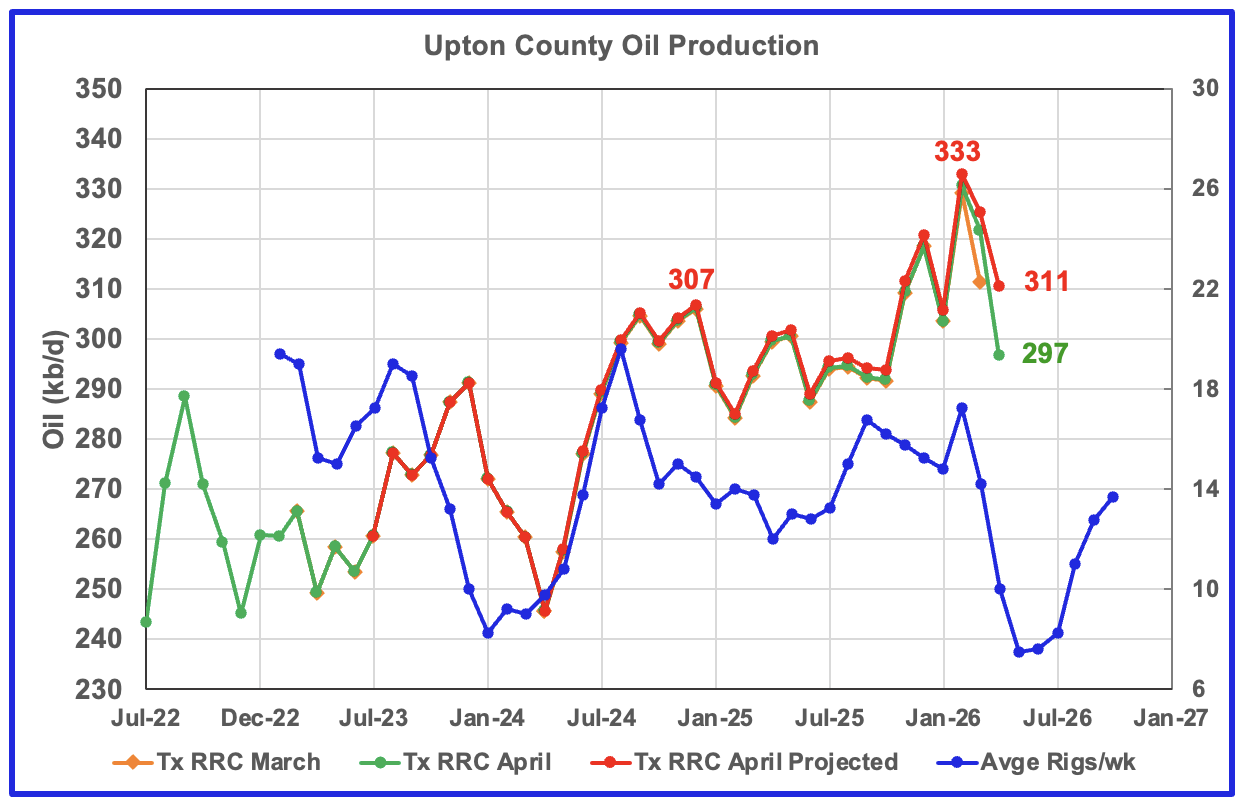

Upton’s projected April production dropped by 14 kb/d to 311 kb/d.

For the next few months Upton County may see a production decrease associated with the dropping rig count which started in time shifted March 2026.

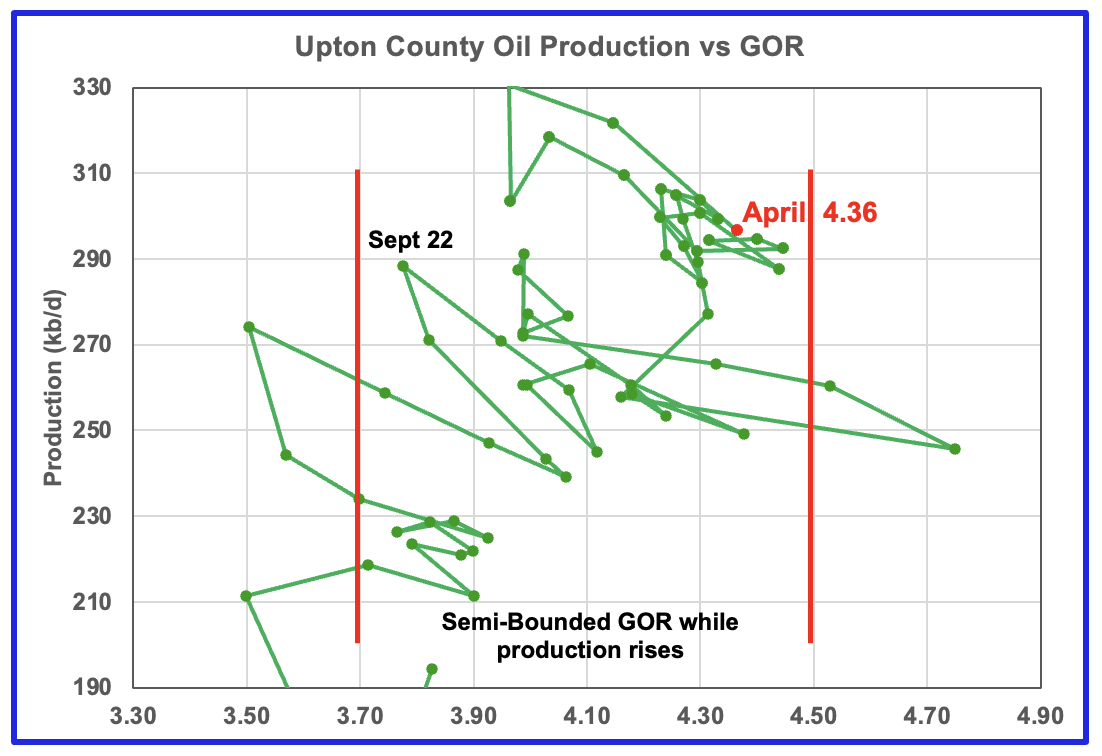

Upton’s GOR continues to stay within the Semi-Bounded region but rose to 4.36 in April.

Upton’s rig chart has been time shifted forward by five months. Upton began 2026 with 7.6 rigs, time shifted to May 2026. In real May 2026, the rig count had risen to 14.

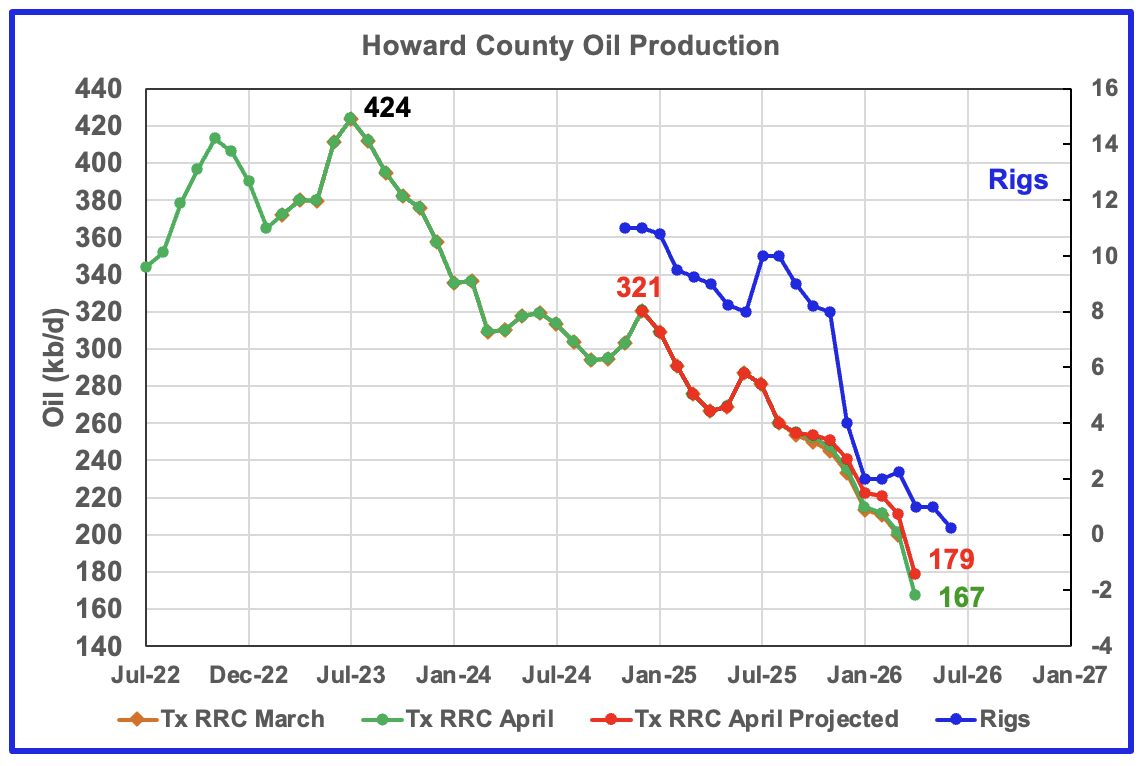

Howard County oil production peaked in July 2023 and has been in a slow decline ever since. April projected production dropped by 32 kb/d to 179 kb/d while preliminary production was 167 kb/d.

Note the rig count in time shifted June 2026 is 0.25, i.e. 1 rig for one week in real January 2026. The rig graph is time shifted forward by 5 months. In real April 2026, Howard added one rig for a total of one operational rig.

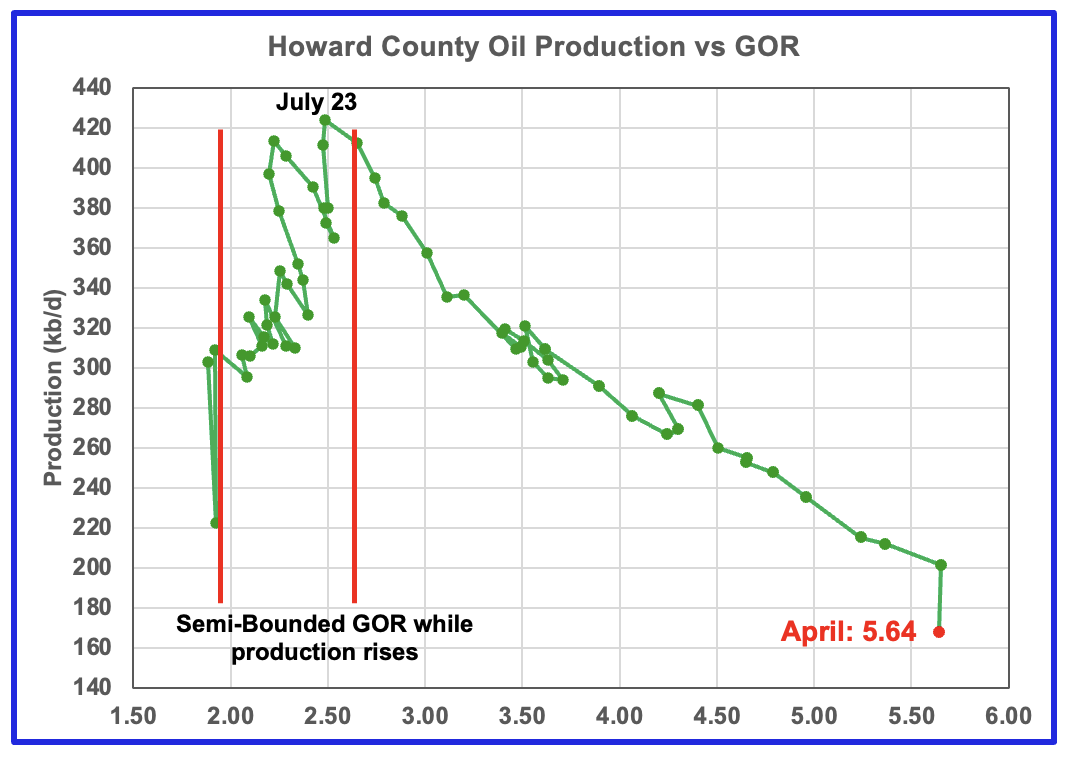

For April the GOR dropped slightly to 5.64 as the initial production dropped to 167 kb/d.

Drilling Productivity Report

The Drilling Productivity Report (DPR) uses recent data on the total number of drilling rigs in operation along with estimates of drilling productivity and estimated changes in production from existing oil wells to provide estimated changes in oil production for the principal tight oil regions. The new DPR report in the STEO provides production up to March 2026. The report also projects output to December 2027 for a number of basins. The DUC charts and Drilled Wells charts are also updated to April 2026.

The DPR has made been significant upward changes to the oil production forecasts for the three tight oil basins, Permian, Eagle Ford and Bakken reported here. It is not clear if the increases are related to the sudden rise in the WTI oil price from $65/barrel in February 2026 to over $100/b in March 2026. While production starts to rise in October 2026 all the way to December 2027, the price of WTI slowly drops back to $64/b in December 2027.

The forecast seems be model driven whereby increases in the oil price brings on new drilling and the associated increase in oil production. Also interestingly there appears to be the typical six to seven month delay from February 2026 before production begins to rise. The only flaw in this possibility is that oil prices fall steadily from March 2026 to December 2027. Also there has been no reported significant increase in drilling rigs in March and April 2026.

For the Permian, production was expected to increase in October 2026 because there was an expectation that new gas pipelines were being built that would permit more high GOR oil wells to be drilled. However the projected increase has been increased further.

So at this time, it is not clear if the sudden production increase starting in the September/October time frame is simply a partially driven model forecast or related to pure Hopium.

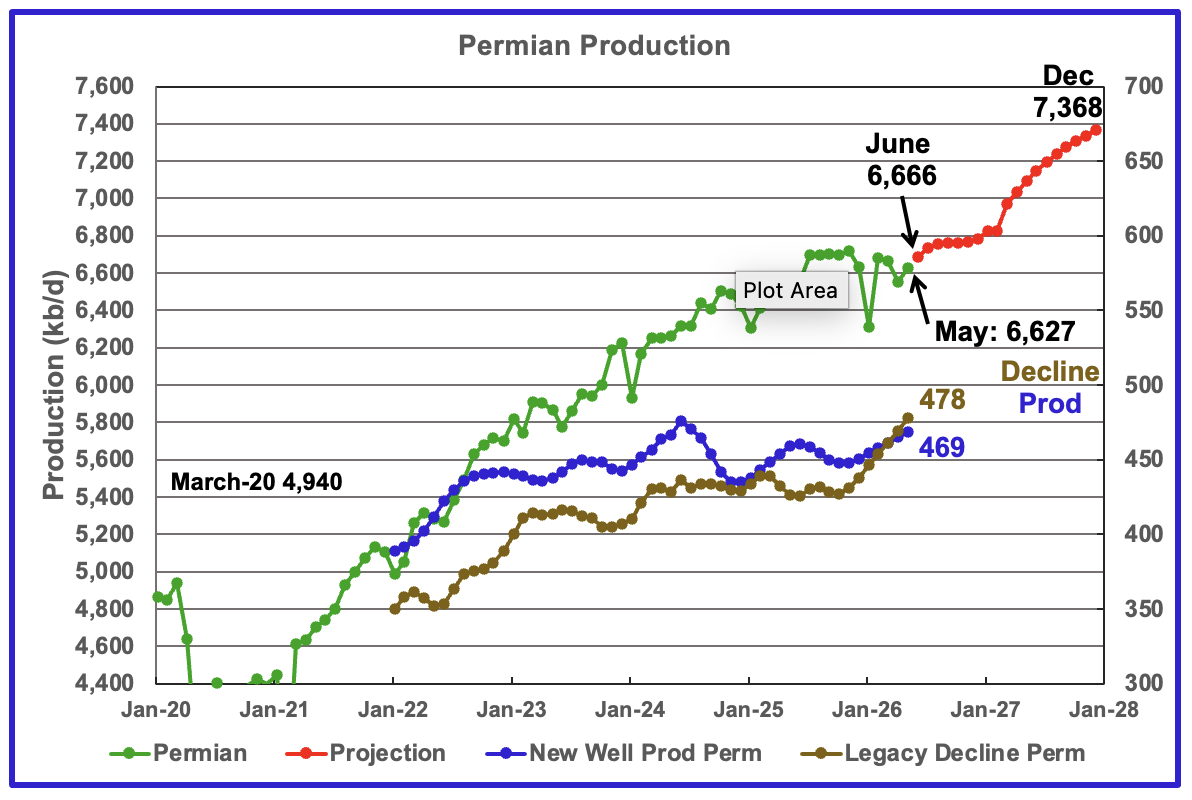

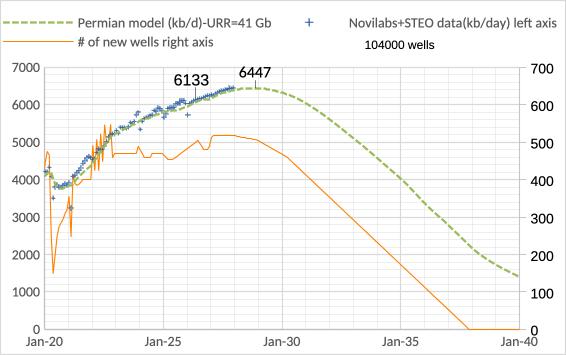

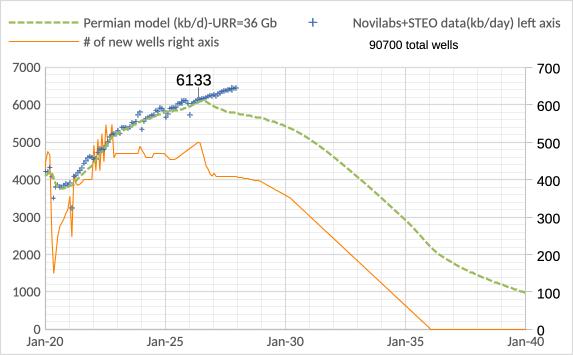

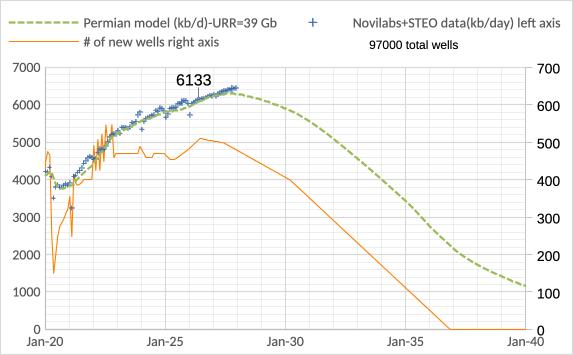

The EIA’s June STEO/DPR report shows Permian May output rose by 77 kb/d to 6,627 kb/d. June production is expected to increase by 39 kb/d to 6,666 kb/d. From June 2026 to December 2027 output is expected to increase by 702 kb/d to 7,368 kb/d. December 2027 production has been revised up by 178 kb/d from the previous report.

Note that production begins to rise steadily from March 2027 to December 2027. According to the EIA, this is due to higher prices for WTI and more NG pipelines being built. The gas pipelines are needed to capture the associated flared gas coming from new oil wells.

Production from new wells and legacy decline, right scale, have been added to this chart to show the difference between new production and legacy decline.

These numbers reflect a one year production trend and provide the production contribution from new wells over a rolling 12-month period to determine if the rate of new production is increasing or decreasing compared to previous periods. The averaging process approximately adds a six month delay.

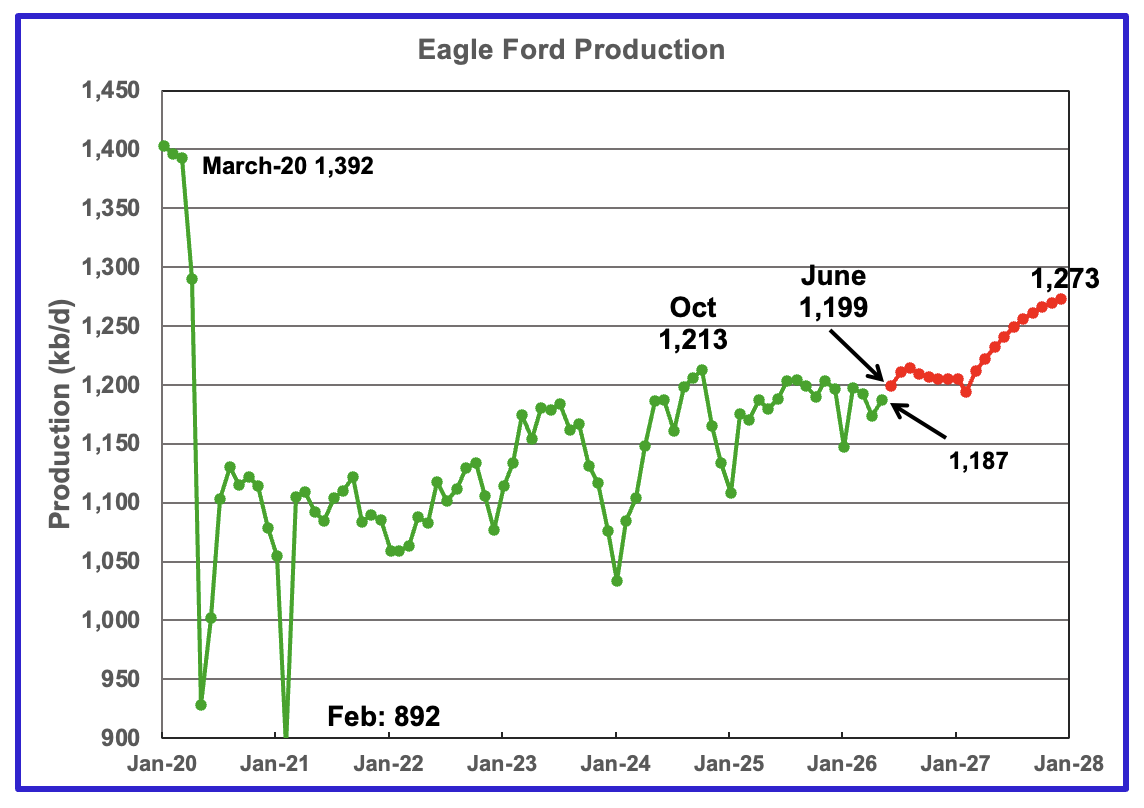

May output in the Eagle Ford basin increased by 13 kb/d to 1,187 kb/d. June 2026 production is forecast to rise by 12 kb/d to 1,199 kb/d.

Output in December 2027 is expected to be 1,273 kb/d, revised up by 23 kb/d from the previous report.

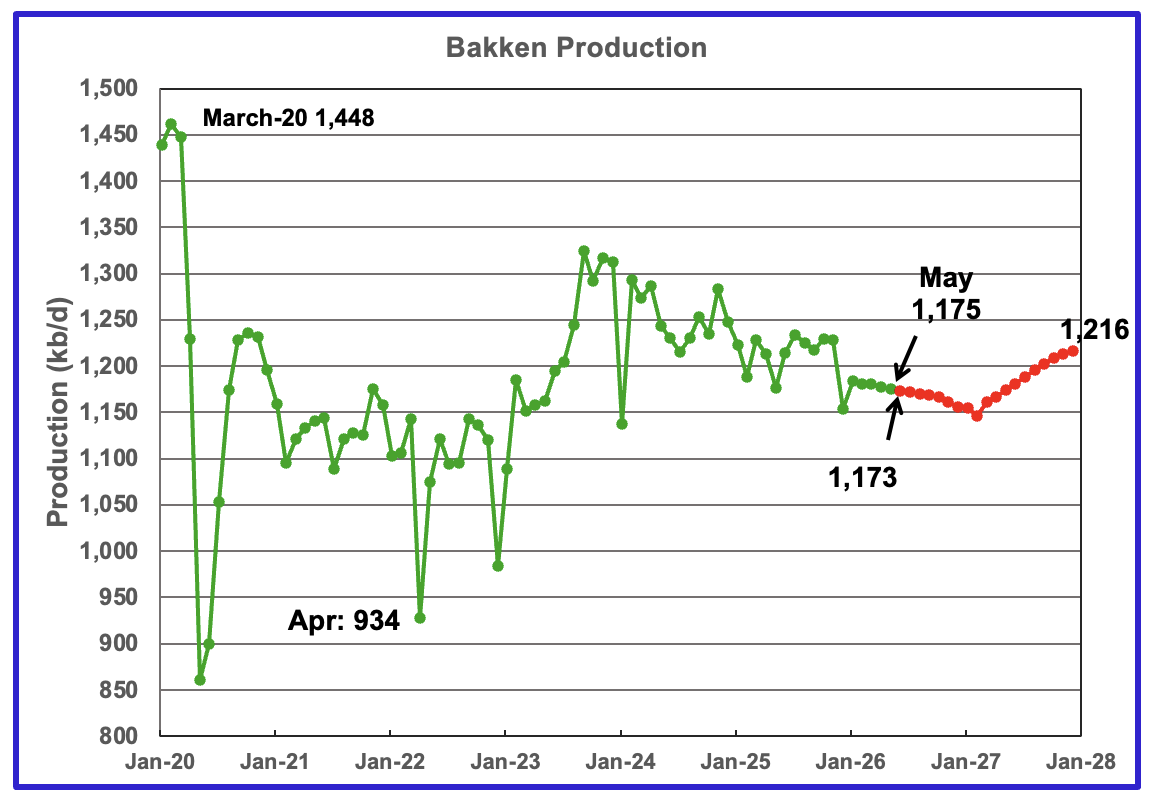

The DPR/STEO reported the Bakken’s May output dropped by 2 kb/d to 1,175 kb/d. June 2026 production is expected to decrease by 2 kb/d to 1,173 kb/d. The STEO/DPR projection, red markers, shows output rising to 1,216 kb/d in December 2027, revised down by 20 kb/d from the previous report.

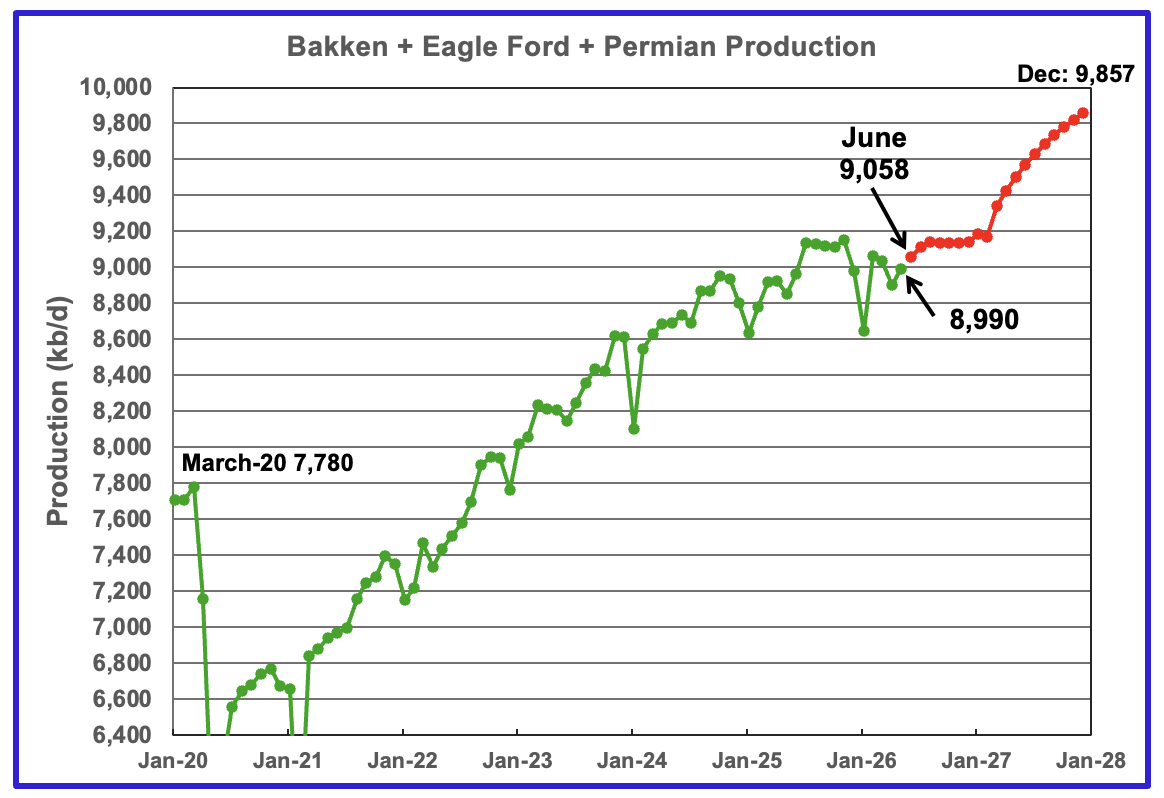

This chart plots the combined production from the three main LTO regions. May output increased by 88 kb/d to 8,990 kb/d. June is expected to add 68 kb/d to 9,058 kb/d. Production for December 2027 is forecast to be 9,857 kb/d, revised up by 181 kb/d from the previous report.

DUCs and Drilled Wells

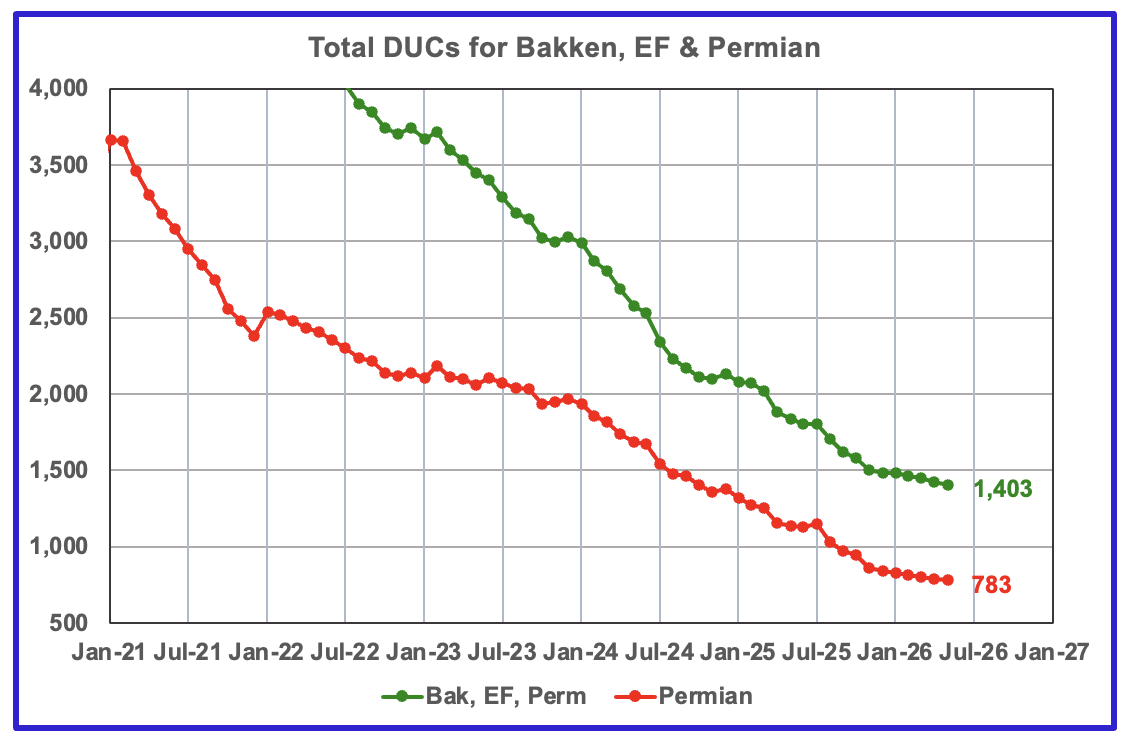

The number of DUCs available for completion in the Permian and the three major DPR regions continues its dropping trend. The May DUC count for the three basins dropped by 18 to 1,403. In the Permian the DUC count dropped by 5 to 783.

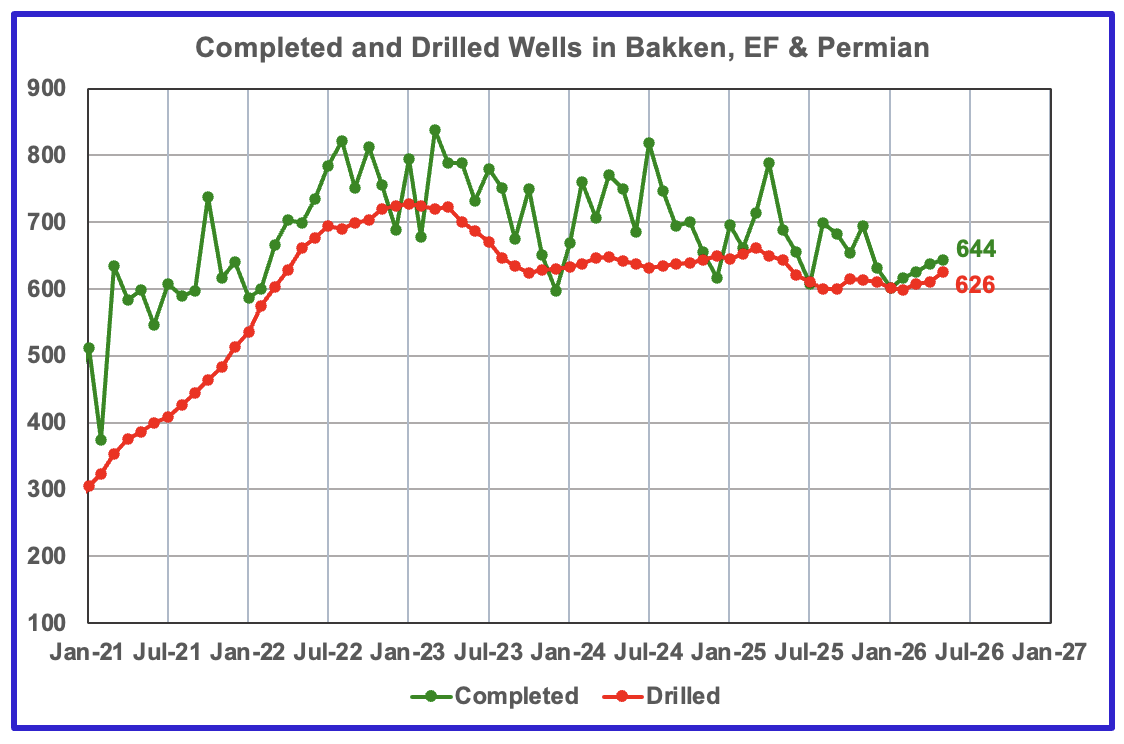

In the three primary regions, a total of 644 wells were completed in May, 6 more than in April. There were 626 wells drilled in May 2026, up 16 from April 2026.

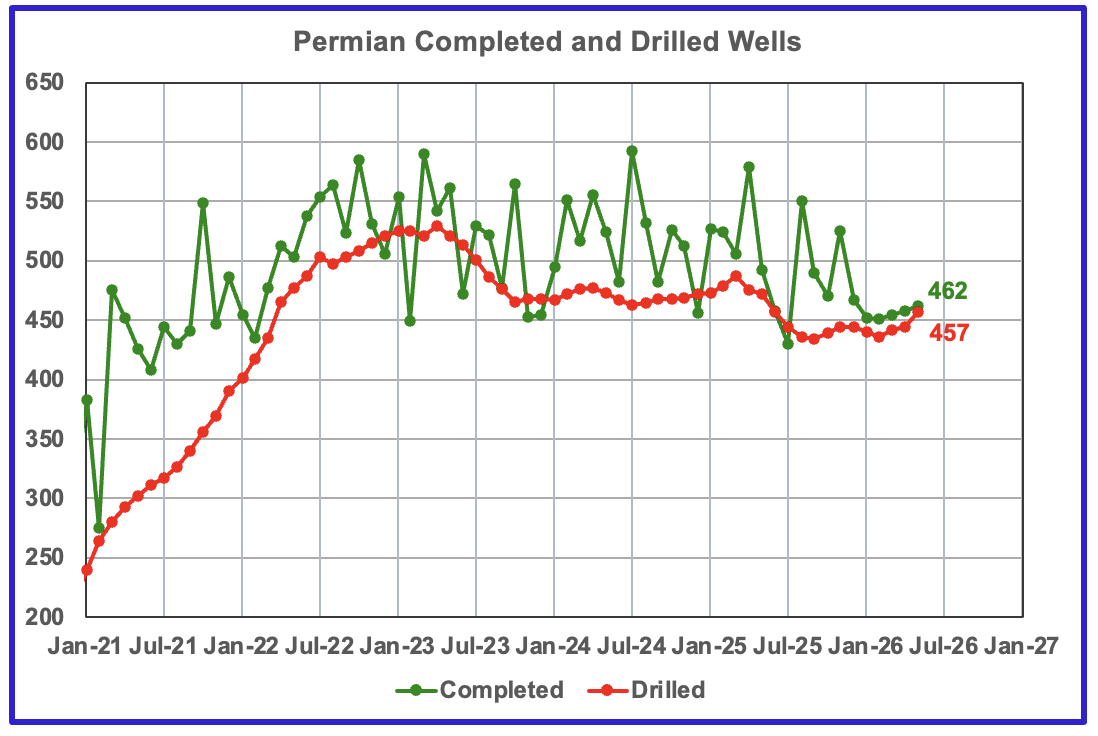

In the Permian, 462 wells were completed in May and 457 were drilled. Drilling and completions have been increasing since March.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply