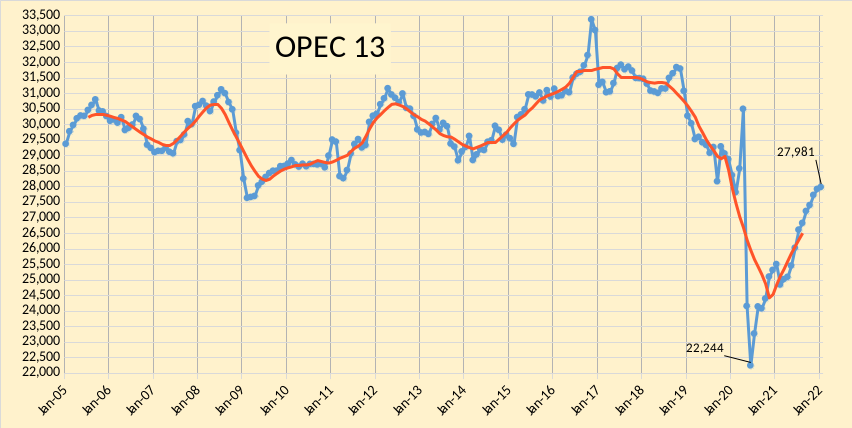

The OPEC Monthly Oil Market Report (MOMR) for February 2022 was published last week. The last month reported in each of the charts that follow is January 2022 and output reported for OPEC nations is crude oil output in thousands of barrels per day (kb/d). In most of the charts that follow the blue line is monthly output and the red line is the centered twelve month average (CTMA) output.

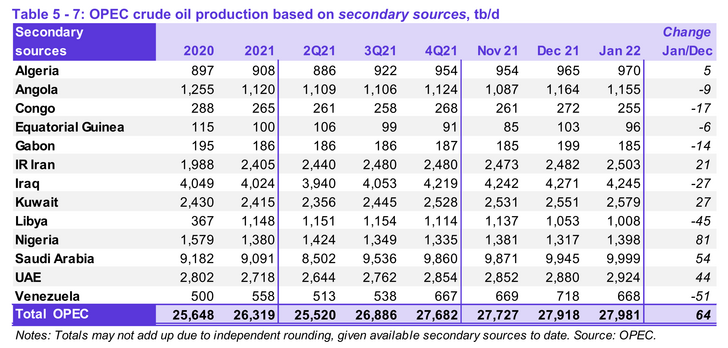

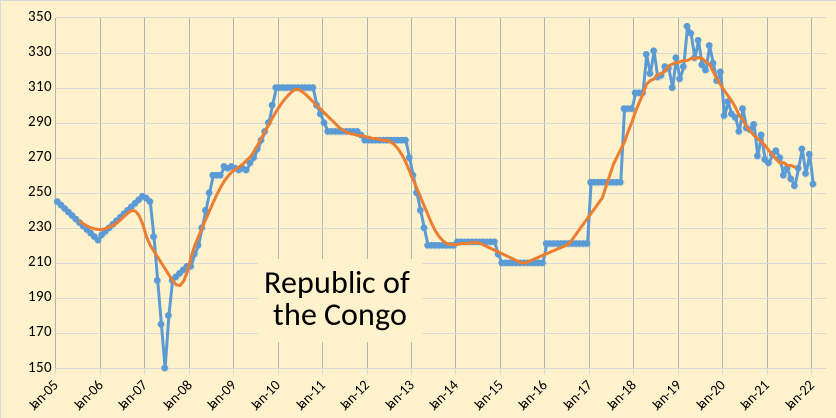

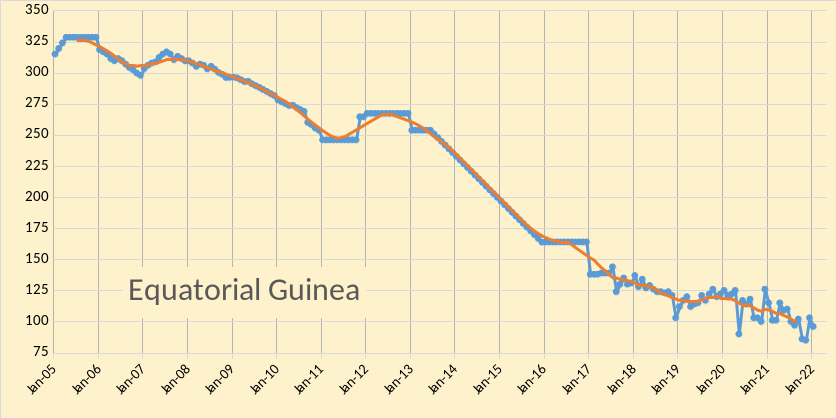

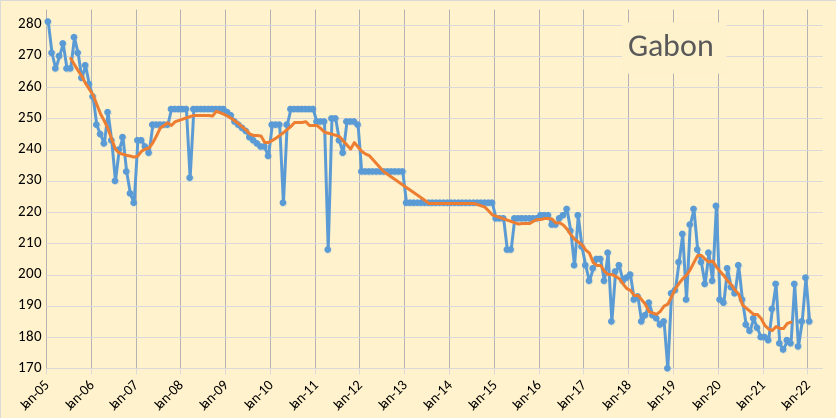

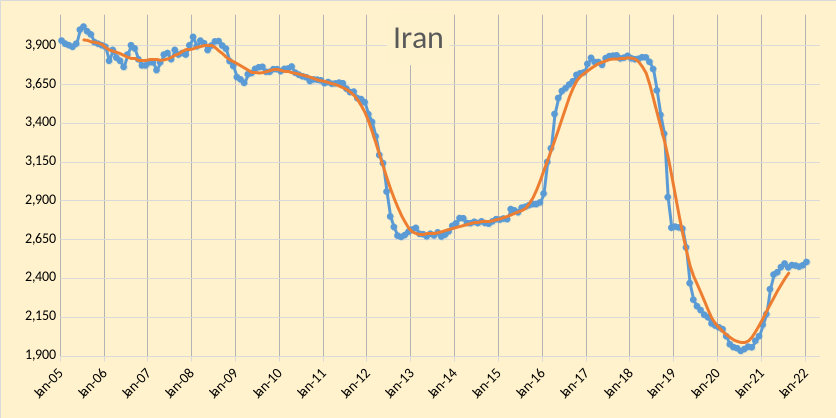

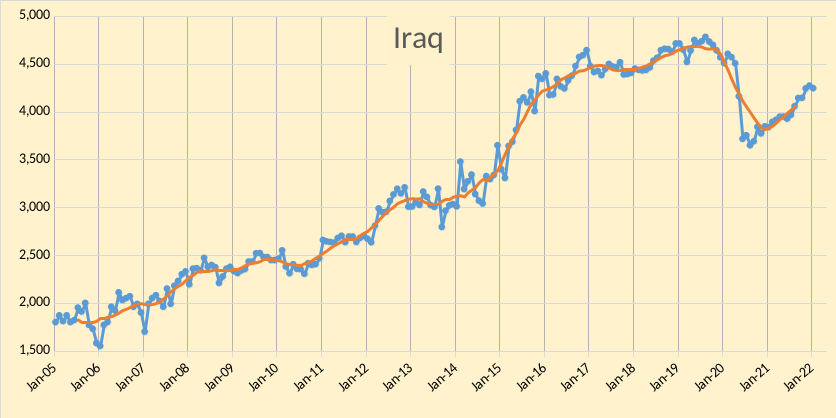

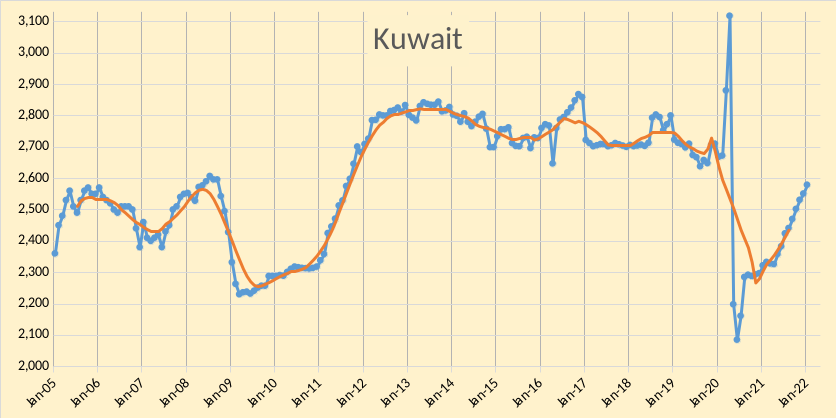

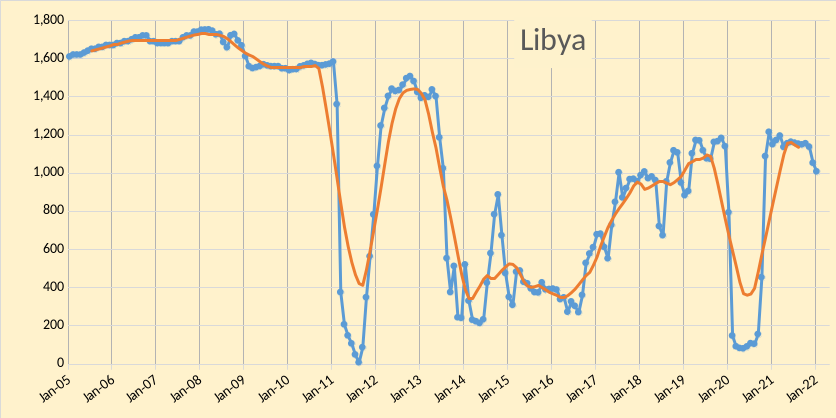

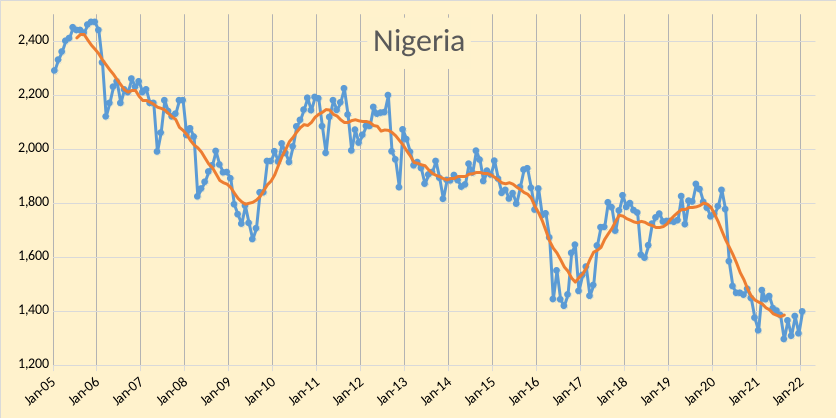

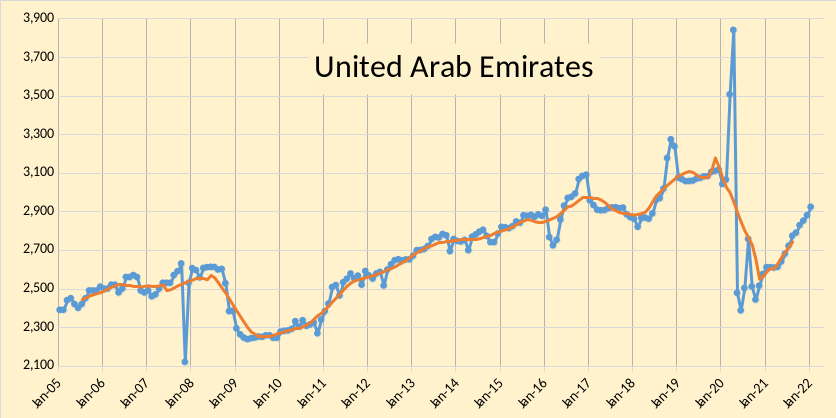

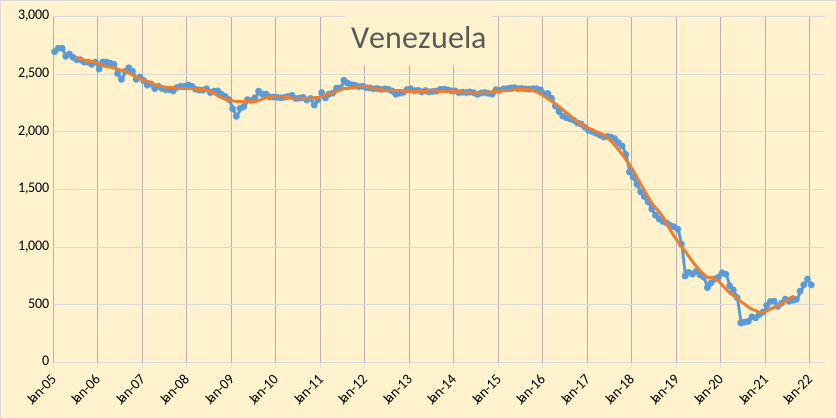

OPEC produced 27981 kb/d of crude oil in January 2022 based on secondary sources, an increase of 64 kb/d from December 2021. November 2021 output was revised higher by 12 kb/d from what was reported last month and December 2021 output was revised up by 99 kb/d compared to the January 2022 MOMR. Most of the increase in OPEC output was from Nigeria(81 kb/d) and Saudi Arabia(54 kb/d) followed by UAE (44 kb/d), Kuwait (27 kb/d), and Iran (21 kb/d). Five OPEC members saw decreases, Venezuela (-51 kb/d), Libya (-45 kb/d), and Iraq (-27 kb/d) with others having decrease of less than 15 kb/d.

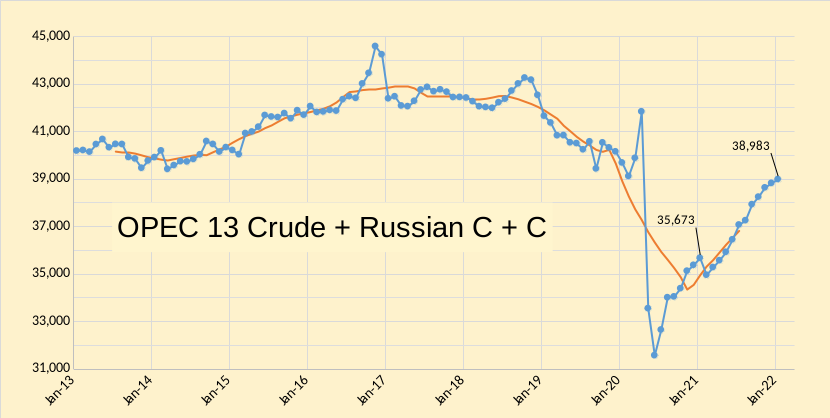

In the chart below OPEC 13 crude and Russian C+C are shown, I expect that OPEC 13 crude plus Russian C + C will likely top out at about 40280 kb/d, where I assume there will be no near term sanctions relief for Iran and Venezuela (together they might add 1800 kb/d in the medium term, if sanctions were removed.) Over the next 6 months we might see 1300 kb/d added from Russia and OPEC 13. Sanctions relief for Iran might add 1300 kb/d over the 12 months following that relief and for Venezuela we might see a 500 kb/d increase over 12 months following a removal of US sanctions. Without the US sanctions on Iran and Venezuela OPEC 13 and Russian output might reach 42080 kb/d in the near term.

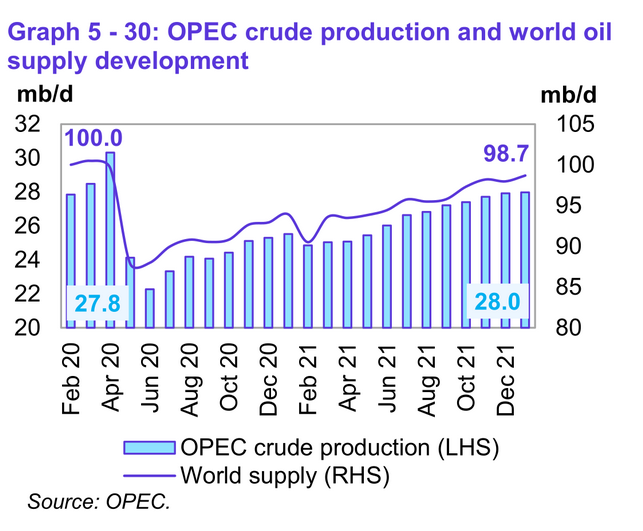

World supply was about 1.3 Mb/d below the Feb 2020 level in Jan 2022 based on OPEC estimates.

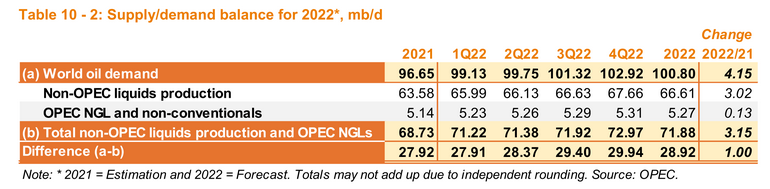

By the third quarter of 2022 the World Oil Market is likely to be short on supply if the optimistic supply estimates of OPEC prove correct. It is unlikely that OPEC will be able to meet the call on OPEC of over 29 Mb/d in the last half of 2022 unless there is sanctions relief for Iran and/or Venezuela. Note also the big jump in non-OPEC output from 2021Q4 (figure 5) to 2022Q1 (figure 6) of 850 kb/d forecast by OPEC, this jump seems unlikely.

What is OPEC spare capacity?

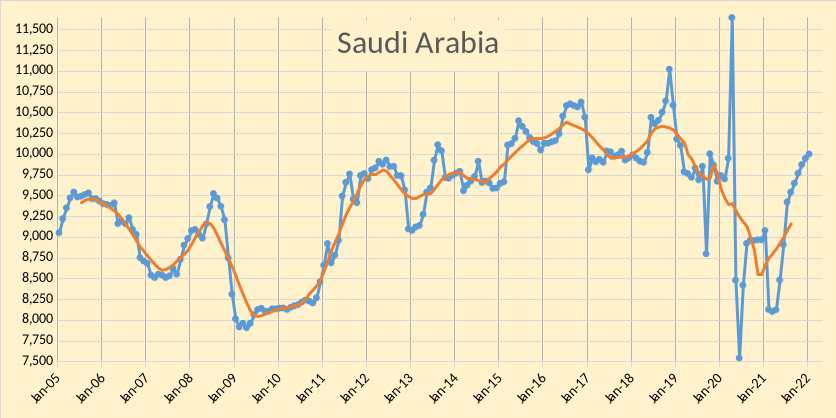

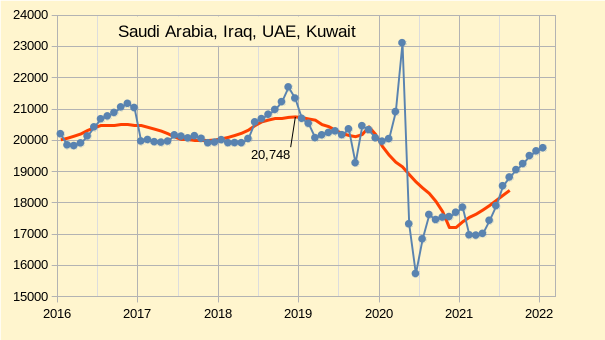

One way to answer this question is to look at the peak 12 month average output of the Big 4 OPEC producers (Saudi Arabia, Iraq, UAE, and Kuwait). This is 20748 kb/d as shown in the chart above. Jan 2022 output for these four nations was 19747 kb/d, all other OPEC nations were producing all the oil they could as they were either not subject to quotas (Iran, Libya, and Venezuela) or were producing below their Jan 2022 quotas. This suggests current OPEC spare capacity of about 1 Mb/d, far lower than the 3 to 5 Mb/d of spare capacity often claimed in media reports. Russia’s 12 month average peak for C+C was about 11300 kb/d so they might be able to increase output by about 300 kb/d from the Jan 2022 level of about 11002 kb/d.

OECD Commercial stocks have continued to trend lower, in December 2021 they were at 2725 million barrels which is 210 million barrels below the most recent 5 year average. The trend might flatten a bit over the next 2 quarters and then may continue lower in the last half of 2022. For this reason I expect oil prices may remain above $90/bo over the next 12 months.

210 responses to “OPEC Update, February 2022”

Good YT interview with Josh Young.

https://www.youtube.com/watch?app=desktop&v=GAkupcU1G7I&t=4065s

It’s long but there are a number of interesting bits:

-Capital has no interest in financing 1.5bn offshore rigs with a 30 payback period because they won’t be needed by then.

– Some interesting on the ground comments from a guy running a rig about various bottlenecks at 58.50

There is nothing earth shattering for those who have been following PO but it’s obvious that people in the financial sector are also on top of it. That makes me wonder why it is not a more prominent issue in the main stream press.

Rgds

WP

The chart below, in blue, is OPEC total liquids production, and the EIA’s projection. They slightly missed January but they are predicting a big jump of 620,000 barrels per day in February, (arrow). But then are predicting OPEC to peak in production, at least for the next two years. They are saying OPEC will peak out at just over 29 million barrels per day then start to slowly decline. Their previous monthly peak was just over 32 million bp/d back in 2017.

But the absurd part of the chart below is what the EIA says about OPEC’s spare capacity. They are saying that even after they peak, they will still have a spare capacity of just under 4 million barrels per day. I think that is absurd.

Ron.

The EIA model’s OPEC production as filling the gap between demand and non-OPEC output, my guess is that the EIA expects high levels of non-OPEC output, but often they are too optimistic. In any case 29 Mb/d is the likely limit for OPEC and as George Kaplan suggests it will be less over time as many OPEC nations are likely to to decline, unless Iranian and Venezuelan sanctions are removed, that would bump capacity up by 1800 kb/d minus any decline from other OPEC producers.

Hello Ron,

You said: ” They are saying that even after they peak, they will still have a spare capacity of just under 4 million barrels per day.”

This might have some basis in the 2004 debate between Matt Simmons and Saudi Aramco at the Center for Strategic and International Studies. Mr. Simmons postulated that the Saudi numbers were a mirage and they didn’t have reserves of 256(?) billion barrels of oil; more like 157 BB. The Saudis countered and said that they could produce at 10 and 12 million barrels of oil a day until 2042(?) and 2034(?) respectively. My numbers may be off. But the “surprise” was that “in an emergency, Aramco could produce at 16 million barrels of oil a day.” **They didn’t say for how long** but the difference between 12 and 16 million barrels of oil per day is 4 million. The EIA number registered the thought that might be where their 4 MBOD is coming from. I’m no expert in this so take it with a grain of Saudi sand.

but the difference between 12 and 16 million barrels of oil per day is 4 million. The EIA number registered the thought that might be where their 4 MBOD is coming from.

Sorry Peter, but that is nonsense. Saudi is not now, and has never, produced 12 million barrels per day. They came close in April 2020, but that was when they were emptying their storage tanks and delaying all maintenance to get a higher quota for production cuts due to the covid collapse. They are now producing about 10 million barrels per day and showing definite signs of peaking. Getting from 10 million barrels per day to 16 million barrels per day is only possible in one’s imagination. But we all have to live in the real world.

The Saudis never quite said how they would get from 12 to 16 MBOD. The assumption at the debate was that they could trade production increases for a shorter time to peak from 2042 to 2034 if I remember the numbers correctly. The obvious question was why should they if it meant flooding the market with oil and driving down the price per barrel. Therefore 12 MBOD was not going to happen but it was a possibility. The Saudi preference was to produce at 10 MBOD but 12 was doable and 16 was possible in an emergency.

Simmons argument was that the reserves were not there and the use of maximum contact wells was creating the illusion of being able to up production. Simmons, looking at the Saudi data was concerned that the water cut would hamper production dramatically when the water cut reached the pipes. I’m not sure if it was complete nonsense as it was more like bravado.

Thanks for the work Dennis, always appreciated.

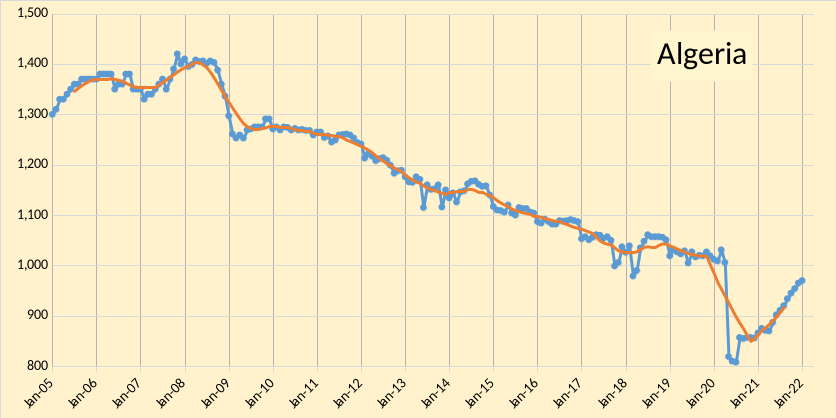

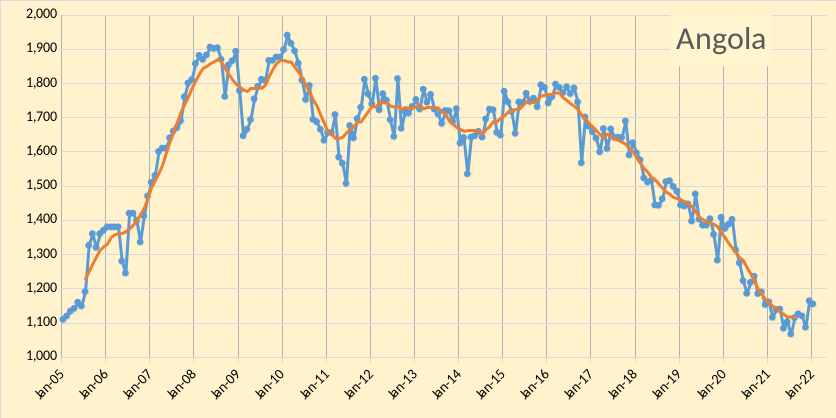

Libya might lose 200 kbpd (https://oilprice.com/Energy/Energy-General/Workers-Threaten-To-Close-200000-Bpd-Libyan-Oil-Export-Terminal.html) but even if it doesn’t this time it’s production is always going to be fragile. Angola looks likely to resume declining now it has just about caught up to where it would have been, but with fewer rigs now. Angola had a small lift because a new tie-in from Eni and will now likely go back to steady decline until the next start ups, which I think will be a small Chevron gas/condensate platform and then a new Total FPSO that has just passed FID and will be four to five years away. I haven’t seen anything to indicate that Iraq wouldn’t continue decline from mid 2019 (maybe Chinese input will have an effect but from rig numbers would suggest not yet).

The first Angola was supposed to be Algeria.

Dennis

Attached is a table which compares the January crude output of the OPEC 10 countries with their required January commitment. The overall deficit is 748 kb/d, 119 kb/d higher/worse than the December deficit of 629 kb/d.

As can be seen, the biggest January deficiencies are in Angola, Nigeria and Saudi Arabia. Also noted at the bottom for SA is their January output according to the “official communications” that shows they are above target.

OPEC+ is suppose to be increasing 400K/d per month until this summer. That is just not going to happen, obviously. Maybe the Saudis will go back to their fave excuse: “the markets are balanced but speculators and driving up prices!” LOL

Adding the asterisk to SA output converted it to text and the sum changed, which I just noticed. The correct sum for January is 23,806 kb/d.

Ovi,

Yes they are below target, based on secondary sources. Most of the deficit is from Nigeria and Angola.

Dennis

Saudi Arabia is missing one whole month since they add close to 105 kb/d each month. January is short by 123 kb/d. So right now they are more than one month behind according to secondary sources.

Also if you compare secondary sources with direct contact, you will see how the gap gets bigger from Q4 to January. My recollection is that they were never that far apart.

Q2 —— Q3 —. Q4 —- Nov—- Dec. — Jan

8,502, 9,536, 9,860, 9,871, 9,945, 9,999

8,535, 9,565, 9,905, 9,912, 10,022, 10,145

GAP: 33, — 29 — 45, . 51, —- 77, —-146

This, to me, hints of inventory use in the direct communication table from SA. The next couple of months will begin to demonstrate SA’s pumping capability.

Tks Ovi for the KSA inventory info . They disguise their incapacity to pump more .

Ovi,

Note that we do not have stock data for Saudi Arabia from secondary sources, JODI data comes directly from the nations that report to JODI. So if we are going to use JODI oil stock data, for consistency we should use the direct communication data in the MOMR in order to compare apples with apples.

The production data is separate from stock data from my perspective. The production is likely what the Saudis report, consumption (both within KSA and oil that is exported) reduces stock levels and production adds to stock levels. Any change in stock levels over a period will be equal to production minus consumption over that period.

Dennis

For SA, the direct communication production in the OPEC report is the same as reported to JODI. My main point in the post is that there is a widening gap between for SA between secondary sources and direct communications.

I am keeping track of inventory separately to see if inventory data will be able to explain the widening gap. Jodi only has data up to November. The first chance to compare Inventory change with production will be for December.

Compare SA production data from OPEC Direct and Jodi

Aug Sept Oct Nov

JODI 9,562 9,662 9,780 9,912

OPEC Direct: 9,562 9,662 9,780 9,903

Ovi,

It is not clear that there is indeed a widening gap, the most recent few month’s data gets revised over time and note that the direct commumication number from KSA also gets revised as the November 2021 data point did in the most recent MOMR, currently it is the same as the JODI number you give above.

If we are not going to trust the Saudi data, then we can’t trust either the stock data or the production data, seems being consistent makes sense, rather than picking the data that matches our preconceived ideas.

Trust, but verify! : )

Edit: Hih below, my point exactly, but might have put a small sarc, or not, note on it.

But I thought it was obvious…

(Out of scotch, but a few beers left)

Laplander , verify what ? EIA , IEA , USGS all a bunch of liars . Now let us verify Ukraine invasion . CNN , MSNBC , ABC , CNBC .? Verify this ? My take . Evolution gave us a thing called the ” brain ” . Use this . Funny , evolution put the brain between the ears . Why ? So that it could be a filter between the BS what the MSM spouts and reality . Hey , who am I to argue about Darwin ?

Dennis

On occasion it gets revised but not often and for November it is a small adjustment. Attached is a picture that shows August for the first time for SA in the Sept report and the final one in the November report. Didn’t change.

Ovi,

The gap is based on two different reports, secondary sources and direct communication.

You have shown that direct communication estimates don’t change often, that may be the case most of the time, I do not really pay much attention to the direct communication numbers. If you did something similar for the secondary sources you will find that there are often revisions, especially for the most recent two months, for prior months is is difficult to say, because we would need to calculate the quarterly data based on previous reports to see if it matches, too much work for me.

Dennis

Yes the OPEC secondary sources are revised.

I will start to monitor JODI stocks monthly change and see if some correlation develops with secondary sources.

Sometime one needs to try different approaches to unravel deep info.

Ovi,

I think the idea that increases in Saudi output is coming from stocks is a myth.

When Saudi Arabia ramps up output temporarily for higher quotas or whatever, that production is real, but it cannot be sustained, that is why I focus on peak twelve month average output which is about 10.3 million barrels per day. That is a better measure of Saudi Arabia’s sustainable output capacity.

Dennis

I will collect the info and let it speak for itself.

We will need to see a steady drop in inventory over let’s say the next six months before coming to any conclusion.

“but it cannot be sustained”

Could you add a little color to that Dennis ?

When Saudi Arabia ramps up output temporarily for higher quotas or whatever, that production is real, but it cannot be sustained,..

Of course this is true. Saudi could easily produce from stocks for one month or even two. And there are always other ways. Wells and GOSPs are often shut doen for maintenance. They rotate this maintenance so that a certain percentage of wells and GOSPs are shut down every month. They could simply delay maintenance for a month or two to ramp up production. Yes, it is that simple.

They can also overproduce from fields while ignoring the need to balance water injection, the pressure declines a bit but with such big fields there is a lot of leeway. Later they can make up the difference by reducing production and overinjecting for a time.

Thanks, but isn’t there a list of future projects of new areas that can be drilled that haven’t been tapped and could be moved forward in time ?

Example- There are areas of the Permian that haven’t been drilled.

California Resources(CRC) works 100 year old fields in the LA basin but has untouched properties in other parts of the state.

The Gulf of Mexico which still has undrilled areas.

“January 5, 2022, by Nermina Kulovic

U.S. oil and gas giant ExxonMobil has made two oil discoveries at Fangtooth-1 and Lau Lau-1 wells located in the prolific Stabroek block offshore Guyana.”

Back in 2014 before the collapse of the price of oil. There were small projects being worked. CRC was increasing conventional production with additional capex.

Huntington Beach,

The fact is the maximum 12 month average output of Saudi Arabia has been 10.3 Mbpd. If they have had any major new fields developed lately there would have been news of it.

Their claimed 12 Mbpd capacity is temporary capacity which might produce for 1 to 3 months, it is not clear it really exists. I will believe it does when I see 3 month average output of 12 Mbpd, in the mean time I remain a skeptic.

I will keep my mouth shut . I know it is ZH and they are a Russia mouthpiece as per CIA . 🙂

https://www.zerohedge.com/commodities/pioneer-ceo-warns-us-shale-cant-increase-supply-even-if-biden-asks

Whether ZH is a Russian mouthpiece is up for debate but Sheffield’s most important statement that the smaller independents will run out of inventory is spot on if they grow at 20%. His view of 5% growth rate is a smart approach. He wants to have some inventory that will last longer than 3 years.

LTO Survivor,

If tight oil producers as a group in the Permian basin increas annual output by 7% per year we get the following scenario. In a high oil price scenario ($95/bo in 2020 $ at well head or higher) this scenario may prove quite realistic.

Dennis, you are really saying that the Permian producing 10M/d in 2033 is realistic? That’s straight up crazy. This is why the oil folks on this board find your comments insulting. Because they spend so much time trying to explain the on the ground situation in places like the Permian and then you revert to this pie in the sky nonsense.

Stephen Hren,

If the USGS mean TRR estimate is correct and oil prices rise to $100/bo in 2020$ and remain there up to 2035, yes I think this is possible. The mean estimate for Permian net acres to be developed was about 50.4 million acres in 2017. That is the basis for my estimate. If the average well completed was about 300 acres, that would be over 166 thousand wells.

There is much that changes at $100/bo, lower prices would reduce output.

Note that the oil pros do not think EVs will reduce demand much, if that occurs prior to 2033 and oil prices fall then this scenario is not realistic, this scenario assumes oil supply is short through 2035.

Stephen Hren,

Note that this scenario was based on LTO Surviovor’s comment that 5% growth seemed reasonable, I increased it to 7% growth because I have created optimistic scenarios that have the Permian reaching 10 Mb/d by 2032. In the chart below I compare a 5% annual growth scenario with a 7% annual growth scenario. Perhaps the growth stops sooner, I believe Reservegrowthrulz might think either of these scenarios is too pessimistic for the $95/bo wellhead oil price I have assumed (also natural gas price is assumed to be $3.50/ MCF at wellhead and NGL sells for $33/b).

What has been discussed frequently is that inventory for many companies is in the 3-6 year range (implied even in LTO’s comment above). You do not take multiple sources of information into account and your projection lacks nuance. Instead you rely only on the source of information you want to believe in. That means you are almost certain to be wrong even with high oil prices.

Stephen Hren,

LTO Survivor said

His view of 5% growth rate is a smart approach. He wants to have some inventory that will last longer than 3 years.

To me the implication was that 20% growth would cause inventory to run out in 3 years. LTO survivor has said his company had 3 to 4 years of inventory, there are a lot of sources that say something different. If oil prices remain high the oil is likely to be profitable to produce. LTO survivor has also mentioned that the oil is there, he is skeptical that it can be produced profitably. He has also said that 5% growth is reasonable, I agree, but think that is on the conservative side. World oil output grew at about 7% annually from 1935 to 1975, as long as there is enough demand to keep oil prices at levels where a profit can be made 7% growth is not that hard to accomplish.

We know why , but still for the record .

https://oilprice.com/Energy/Energy-General/Why-Isnt-US-Shale-Production-Soaring.html?fbclid=IwAR32R7wJHYlnAqzArmXkGgScYwm08w_14EgVF0GxJLXMRJ-lfl6ZZ9WQyhE

Not Even $200 a Barrel: Shale Giants Swear They Won’t Drill More

(Bloomberg) — The Texas wildcatters that ushered in America’s shale revolution are resisting the temptation to pump more oil as the market rallies, signaling higher gasoline prices for consumers already battered by the worst inflation in a generation.

“Whether it’s $150 oil, $200 oil, or $100 oil, we’re not going to change our growth plans,’’ Pioneer Chief Executive Officer Scott Sheffield said during a Bloomberg Television interview. “If the president wants us to grow, I just don’t think the industry can grow anyway.’’

To be sure, U.S. oil output will rise substantially this year and is forecast to return to pre-pandemic levels by 2023. But it probably won’t be enough to knock oil prices off their upward trajectory any time soon.

“We’ve had enough head fakes that we’re going to be very thoughtful in ramping activity up,” Rick Muncrief, CEO of Devon Energy Corp., said during a phone interview. “Let’s face it: we all are recovering in one way or another from this pandemic. We’re just slowly getting healthier and healthier over time, but you don’t get there overnight.”

Such comments are a world away from the free-wheeling “drill, baby, drill’’ heyday earlier this century when shale upended global oil markets with year after year of record-high production. Seasoned CEOs like Muncrief, Sheffield and Hamm have seen too many bust cycles to get carried away again.

https://finance.yahoo.com/news/shale-wildcatters-send-bullish-oil-002829906.html

I registred this article, to me it seems for some months now the shale producers have spent more of their profit due to surge in oil prices to increased drilling activity and I guess some riggs are needed to increase levels of Ducks.

The production each well increase as now it is 3 mile latherales and also cost each foot is reduced. From what I have read long latherals have also some negative impact as more oil will remain in the shale formation. Would be good to see a courve, diagram that show how many riggs US need to add to keep production from decreasing as more and more wells are drilled. I believe at some point they will both runs out off acre and pepole/equipment even there is a profit. That is normal what happens and the oil Companies all time need to invest in new fields to keep up for decline.

Ovi,

From the yahoo finance article you linked above:

Exxon Mobil Corp. and Chevron Corp., for example, are targeting 25% and 10% shale growth, respectively, this year.

So between privately held companies and the Oil majors which have plans to grow at higher rates than 5% per year, we might see overall Permian growth at something higher than 5% per year, especially if oil prices remain at current levels ($91.77/bo for WTI crude front month futures as I write this.)

Dennis

The problem with these growth estimates is that they are BOEPD. Not BOPD.

It is rare for companies in the shale space to differentiate.

A cynical person would state that is because of ever rising GOR.

If I am incorrect, I apologize. But seems when I have dug into the forecasts, they have almost always been BOEPD forecasts.

Shallow sand,

You are probably correct, companies do tend to report things in BOEPD. If we look at US tight oil output from Pioneer from April 2021 to Sept 2021 (data from http://www.shaleprofile.com) the average annual rate of increase was about 8%. So at least for the largest operator in the Permian basin the 7% guess might be pretty good. For all of the Permian basin from April 2021 to Sept 2021 the increase in tight oil output using shaleprofile oil data was at an annual rate of about 12.8%, on that basis my projection is somewhat conservative. I expect high growth (15% or so from 2023 to 2027) and then slower growth as the ramp up in completion rate levels off in the Permian basin in a world where oil prices remain at $90 plus per barrel of oil. As you know, I tend to get future oil prices wrong.

Today’s Rig Report

Inspite of what the article above says, Hz Rigs are being beeing added at a record pace. Last week 17 rigs were added and this week an additional 8 Hz rigs were added for a total of 474.

In the Permian, 7 were added last week and 5 this week.

Must be the allure of $90 WTI.💰💰

For Permian at a rig efficiency of 1.3 wells drilled per month per rig the 284 rigs could drill 369 wells per month, for 400 horizontal oil wells per month about 308 horizontal oil rigs would need to turn at a rig effiency of 1.3, so an additional 24 rigs or four weeks at the rate of increase of the past two weeks( average of 6 rigs per week).

Dennis

What is the delay time from rig increase to output increase. Or put another way, how many weeks (average) after a rig arrives at a site does the first well drilled by that rig start producing oil. I keep reading that the delay time is about 6 months. Doesn’t sound right to me but as I have pointed out many times, I know nothing about drilling.

Ovi,

I have also heard about 6 months, but 3 to 6 is likely the correct range. I also know little about the details of the drilling process. EIA suggests about 60 days for drilling on average, and anywhere from 90 days to a year for drilled wells to be completed. So perhaps 5 to 7 months from first spud to production , if a producer is in a hurry, but in many cases wells remain in the DUC stage for many months. At present, the DUC count is getting pretty low so the average time may be at the 6 month stage.

For the Permian basin I am thonking in terms of a 400 well per month completion rate and the drilling rate catching up to that rate to stabilize the DUC count, then any further increases in the rig count can either allow thre completion rate to increase (with a stable DUC count) or allow the DUC inventory to increase (if the completion rate remains stable).

See

https://www.eia.gov/todayinenergy/detail.php?id=41253

Nowadays I think all the horizontal rigs are walking rigs so several wells will be drilled from a single pad. The rig would be assembled and then drill each well, maybe up to ten per pad but with things so crowded maybe fewer now. In the main basins a rig can drill about two wells a month so it may take up to six months but for an average pad less. Once finished the rig is removed, at this point the wells are DUCs. Sometime afterwards, not immediately, but depending on logistics and how contracts have been placed, the fracking spread will move in and complete each well in turn. The well would be hooked up to separation equipment and gas pipeline and started up. I don’t now what clean-up and testing requirements there are but I’d have thought they’d be ramped to full flow very quickly. The fracking completions are faster than the drilling so there are fewer frac spreads than rigs but overall there might be three to six months between spudding and completion. With capital controls tight companies might try to minimise the time as much as possible.

Thank you George Kaplan for the clear explanation.

Ovi , terrific ( not the data , but you ) . This confirms the ” Red Queen ” is causing the runner to breakdown . Some who still believe in the shale miracle are going to have a nervous breakdown . Get some help .

Apache is being hit with a class action suit for bilking its investors out of billions of dollars. I have only posted the first two charges here. There a total of eight of them. Bold theirs.

CONSOLIDATED CLASS ACTION COMPLAINT

FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS

INTRODUCTION

1. Apache is an oil exploration and production company whose single most important

asset during the Class Period was an oil and gas field in the Texas panhandle called “Alpine High.”

For three years, Defendants touted Alpine High as a “transformational discovery” and “world

class resource play” with immense production capabilities, including “conservative” estimates of

over three billion barrels of oil and significant amounts of “really rich gas.”1

Defendants supported

their claims by highlighting examples of “strong well results” and “successful oil tests” that were

purportedly representative of Alpine High’s “2,000 to more than 3,000 future drilling locations,”

which would “deliver incredible value to Apache and its shareholders for many, many years to

come.” Analysts and industry media lauded this “massive shale discovery,”Fless than emphasizing that

Alpine High’s “compelling economics” represented Apache’s “largest catalyst opportunity” for

the coming years and put Apache “back in the game” after a “rough time keeping up with

competitors.” Fueled by Defendants’ assurances, Apache’s stock price soared, reaching a Class

Period high of $69.00 on December 12, 2016. The Individual Defendants took full advantage,

reaping more than $75 million in Alpine High-linked compensation during the Class Period.

2. Unbeknownst to investors, Defendants’ statements were false. In reality, Apache’s

own production data and analyses of the Alpine High play never supported Defendants’ public

representations. As Apache was ultimately forced to admit, Alpine High was virtually barren.

Indeed, after three years of relentlessly touting Alpine High to investors, the “world class resource

play” that was supposedly going to “transform” Apache produced less than 1% of the oil and gas

that Defendants had represented to investors was recoverable. Alpine High was so devoid of oil

and gas that Apache was forced to cease all drilling at the field in 2020, take a $3 billion write

down, and slash its dividend by a staggering 90%. When the truth regarding Defendants’ fraud

emerged, analysts and the nation’s leading financial publications excoriated Defendants, noting

that the revelations “were in stark contrast to [Defendants’] past defense of Alpine High,” and

Apache’s stock price was decimated, closing at a mere $4.46 on March 17, 2020—an astonishing

decline of 93% from its high during the Class Period.

Just goes to show that technically recoverable and technology improvements, lower costs and higher product prices don’t mean a damn thing when you are lied to by management.

I knew some folks at Apache. They knew Alpine High was a bust. The entire industry in the know referred to it lovingly as “Alpo High” because it was Dog meat. They were not allowed to say anything negative about the project and quickly shut it down when they were bailed out by Guyana. However at today’s prices Alpine High could be economic. It’s just deep and gassy.

Isn’t the primary issue that APA led investors to think there was more oil there than there actually is?

Peak Oil Dynamics at work .

https://www.bangkokpost.com/world/2266499/sri-lankan-energy-crisis-worsens

Sri Lanka, like other nations that subsidize fuel, are always at the risk of shortages. And this type of policy is difficult to undo as eliminating subsides often causes civil unrest. In my opinion, the whole subsidies idea is a trap to be avoided.

Frugal , let us start with the USA and see how fast it will collapses or maybe with KSA and we can watch the beheading of MBS on CNN , Fox etc . Would be entertaining and what better when the public only wants ” bread and circus ” .

Between Covid tourism drop-off and Peak Oil to think “subsidies” is the issue sounds like Libertarian mumbo-jumbo. Most of the globe has been one giant revolving bubble and subsidy monetary circle jerk as the diminishing returns of capital gets ever smaller, especially since 2008. But don’t worry – the Metaverse will save us.

The second largest producer of OPEC is having some domestic problems .

https://www.al-monitor.com/originals/2022/02/iraqis-queue-petrol-mosul-amid-shortages

Will the adoption of EV’s be able to offset the depletion of oil?

No.

Too late to get the job done without the world experiencing shortage oil for transport, with high prices and shortages.

At some point the decline in petrol fueled transport will be met by a rising EV transport trend, but it will be not be any time soon.

“A report from IHS Markit shows that in 2020, light plug-in and fuel-cell vehicles, as well as electric city buses and two-wheelers, collectively displaced about 370,000 barrels per day of global oil consumption, a figure that is projected to grow to 1.5 million barrels per day by 2025, equal to about 1.4% of the projected level of total world oil demand.”

“Bloomberg New Energy Finance estimates that road fuel oil demand will peak in 2027, but it will take another decade for the impact of advancements to be materially felt.”

[remember that peak does imply anything about the rate of decline thereafter. A peak in oil demand will likely be followed by a very very slow post-peak demand decline rate]

“That said, the EV sector could end up hurting the oil sector in the long run, with BNEF predicting that electric and fuel cell vehicles will displace 21 million barrels per day in oil demand by 2050.”

[this statement has odd wording- the 21 million barrels won’t be ‘displaced’, since you can’t displace something that is already gone. The depletion of oil will exceed 21 Mbpd long before 2050]

On a related topic, with the Russian oil and gas geopolitical situation in mind-

Renewable energy is potentially the greatest peace plan in history, U.S. Energy Secretary Jennifer Granholm said in her opening remarks at a U.S.-EU Energy Council Ministerial this week.

“No country has been held hostage to access to the sun,” Granholm said, quoting her Irish counterpart Eamon Ryan. “No country has been hostage to the wind. This is not just an energy and climate issue; it is also potentially the greatest peace plan that ever existed, to be able to build energy independence from clean energy,”

I think it is wishful thinking, but has a strong aspect of truth to it.

My lithium carbonate prices come from a great website, tradingeconomics.com.

In early January 2020 the price in China was $3.94/lb, with 135 lbs in a 70kw Tesla battery the cost to purchase the needed lithium was $530. At yesterdays price lithium carbonate is now costing $33.58/lb. Ok now let’s do the math. $33.58 X 135 lbs = $4533 per battery just for the required lithium. Obviously this huge increase hasn’t found it’s way to the show rooms but just don’t see how an EV can be practical when it does.

Ervin , cool . Great info which very few are aware of . Any other flies in the ointment ? Keep us informed .

Ervin- for some reason HinH thinks price inflation or supply shortages are cool. Everyone has different that they think are cool I suppose (cheerleaders for economic hardship club?)

Regardless, I suspect that going forward everything related to energy cost is going to be on an upward trend. Humanity has been exceedingly fortunate with energy costs in the last 100 years. Cheap energy party’s winding down.

But the recent sharp lithium carbonate price spike is a temporary deal. That resource is huge.

Since the price spike is a reflection of an imbalance in supply and demand one has to ask themselves, how will the balance be restored? World wide the auto industry is hell bent to go electric and governments are throwing money in every direction to get the masses to go to EV,s. Other than price there aren’t any pressures to reduce demand. And on the supply side I agree it’s a plentiful element but only incremental increases in supply are occurring. I see only that price will be the the driving force for the future.

Ervin,

The high price of lithium carbonate will result in more supply as the high profits will lead to more investment in the production of lithium carbonate. I agree price will be a big factor, it always is a big part of the story.

That”s not as easy as you are imagining this. The current problem doesn’t come from the abundance of lithium carbonate as ore but from the fact that the industrial-grade lithium carbonate is in shortage. This is coming from the scarceness of the industrial plants necessary to refine lithium carbonate ore. These industrial facilities are outrageously long to build ; for example, Lithium Americas has been built in 10 years. it doesn’t matter if there are dollars or not. What is important are the industrial construction times.

https://www.morningbrew.com/emerging-tech/stories/2021/12/13/a-lithium-shortage-is-coming-and-automakers-might-be-unprepared

I don’t imagine any of this will ‘be easy’.

Rather it will be a struggle, just like it will be for many other aspects of energy supply.

Nobody knows what the biggest or first large scale choke points will be.

Japan didn’t realize that nuclear would fail them (or vice versa), and the next big shortfall or stumbling block could be one of many possibilities.

Ghawar, failed states, lithium, copper, war- take your pick but it will just be a guess.

One big thing is for certain- oil supply depletion.

Regarding the spot price of lithium- the big battery manufacturers like CATL, Panasonic etc, and users like Tesla, BYD etc have long term contracts for lithium supply. They aren’t rookies.

Jean Francois,

Humans learn by doing. As the production of lithium carbonate ramps up we will become better at building the necessary industrial facilities and it will take less time to build them. The profit motive tends to move things along and those who do it best will establish themselves as industry leaders and stand to make a lot of money in the process. High prices tend to increase the supply of a good in a free market capitalist system.

Dennis,

In the previous FF thread I had a question for Eulenspiegel, but he didn’t answer. Can you, or someone else, elaborate a little more on the possible future for sodium batteries compared with lithium batteries ?

EULENSPIEGEL

02/13/2022 at 3:18 am

Its not sodium sulfur. Google CATL sodium battery. It works until -20 degrees without heating needed.

REPLY

HAN NEUMANN

02/14/2022 at 2:15 pm

Eulenspiegel,

So the mentioned issues with Lithium are not relevant ?

Han,

I don’t have an answer. Research it and report back.

From the end of the article Jean Francois linked:

You’ve got to ride out the volatility. Long term, it will be fine. The price will be fine. There’s no geological shortage. Lithium-ion battery powered EVs will dominate the world.

The author goes through some of the potential problems and thinks they will be addressed, my take home message from this article is that this space (companies that mine and refine lithium) is an excellent investment opportunity.

A good example of the dynamics Dennis proposes, regarding lithium production industry. High demand and prices will stimulate new production, with certainty-

“The Salton Sea geothermal field in California potentially holds enough lithium to meet all of America’s domestic battery needs, with even enough left over to export some of it. But how much of that lithium can be extracted in a sustainable and environmentally friendly way? And how long will the resource last? These are just a few of the questions that researchers hope to answer in a new project sponsored by the U.S. Department of Energy (DOE)….”

https://cleantechnica.com/2022/02/18/the-salton-sea-geothermal-field-in-california-quantifying-californias-lithium-valley-can-it-power-our-ev-revolution/

For anyone interested in geography/history, the Salton Sea is a fascinating story

https://allthatsinteresting.com/salton-sea-history

https://en.wikipedia.org/wiki/Salton_Sea

Dennis,

An educated guess is that sodium batteries take up (much) more space.

Maybe Eulenspiegel didn’t answer my question because he is shareholder of the company

Anyhow, the oil addiction is a dangerous one, like a Lithium addiction

Han,

Perhaps the sodium batteries will work well in stationary applications (say for grid backup). I am not familiar with the technology in this case.

If anyone is interested in the issue of energy related mining constraint there is an excellent recent report on this issue (as has been presented and discussed a bit on the other thread)-

“The Role of Critical Minerals in Clean Energy Transitions” IEA

Its a hard look at the issue and I highly recommend it. There is a lot to digest. Clear your slate.

Here is the link to the executive summary, with an embedded link to the full report-

https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions/executive-summary

Teaser-

“The types of mineral resources used vary by technology. Lithium, nickel, cobalt, manganese and graphite are crucial to battery performance, longevity and energy density. Rare earth elements are essential for permanent magnets that are vital for wind turbines and EV motors. Electricity networks need a huge amount of copper and aluminium, with copper being a cornerstone for all electricity-related technologies.

The shift to a clean energy system is set to drive a huge increase in the requirements for these minerals, meaning that the energy sector is emerging as a major force in mineral markets.”

Hickory —

Rare earth elements are essential for permanent magnets that are vital for wind turbines

Not true. Wind turbines almost always use induction motors, which have no permanent magnets. The EIA is simply wrong, for whatever reason.

Alim-

you’ve said this previously yet there are many sources that discuss the use of REE’s in the wind industry.

I’d appreciate any good source of information you have that clarifies the actual situation.

I know there is an aspiration to do without REE’s in wind turbines, but what is actually the state of the industry?

Hickory – see the third link I posted as a reply to one of your other cmments, which I prbably meant to post here.

Thanks George.

And there is good coverage of the REE’s use in various wind turbines in the full version of IEA report pages 65-68

https://iea.blob.core.windows.net/assets/24d5dfbb-a77a-4647-abcc-667867207f74/TheRoleofCriticalMineralsinCleanEnergyTransitions.pdf

The REE requirement varies with type of turbine to large degree, and there is some wiggle room.

Nonetheless, it will likely be a big problem, especially if China restricts the market.

It takes a long time to get new production sources up and running. Check out the history of Lynas company from Australia to get a sense of that.

Hickory —

The advantage of permanent magnets in wind turbines is that they work at low rotation speed. To deal with that wind turbines have increasingly huge gearboxes, which are a weight and maintenance problem. The advantage is a much cheaper generator, which is why most turbine manufacturers use them.

It’s interesting that people talk so much about magnets in connection with renewables. All electricity generation requires magnets whether permanent or not, and whether fueled by fossil fuels or not. There is a lot of electricity generation around, but nobody seemed to notice before wind started threatening fossil fuels.

That is why I suspect it is probably bullshit. It sounds like a desperate attempt to project the problems of the extractive fossil fuel industry on the circular economy. Nobody has the numbers though, so who knows?

One of the things to remember is that this is looking at current technologies and projecting forward. One of the dark horses are perovskite solar cells. They are based on lead and current maximum efficiencies are around 30% but their longevity is much shorter than silicon based solar cells.

If they do solve the longevity problems, they are projected to be much cheaper to manufacture than silicon solar cells. This could then change the graphs and adoption of perovskite cells over their silicon brethren.

Also, with EV batteries, there is a push to go back to LiFePO batteries to avoid use of Cobalt. The energy density is not as great but the cost is less.

In the IEA report with respect to the element graphs, I love the way that when you run a cursor over the element, the other elements in the bar graphs fade and the element of interest brightens up.

Chile has by far the world’s largest known lithium reserves. At 8 million tons. Australia 2.7 million tons, Argentina 2 million tons and China 1 million tons.

Chile imports 68% of the energy it consumes. 98% of it’s oil, 73% of its natural gas and 88% of its coal.

Chile also uses the above fossil fuels for 73% of its total energy use. They have to import energy just to mine lithium.

What happens to the lithium when fossil fuels are no longer available to Chile for imports?

HHH- “What happens to the lithium when fossil fuels are no longer available to Chile for imports?”

When oil becomes expensive, and eventually in restricted supply, everything that is solely or heavily dependent on it will be hit hard and possibly extinguished. Lithium included.

But lets remember that the down slope from peak oil is not going to happen all on one day.

There is going to be a period of rough plateau (I think we are already there) followed by decline.

Prices will rise and rise, and some places may lose access to physical supply regardless of price willing to be paid.

Less important uses of oil (like light vehicle transport which is the big majority of consumption)

will get weeded out first by either higher pricing or by outright restriction by governments.

They call it rationing. Read up about WWII policies to get a inkling of what happens.

http://abacus.bates.edu/muskie-archives/ajcr/1973/Gas and Fuel Oil Rationing.shtml

Oil will get shunted away from routine citizen use and towards more critical and irreplaceable uses such as the petrochemical industry, the heavy mining and ore processing industries, bunker fuel, etc., either by market forces and/or government intervention.

It won’t be smooth or seamless or pretty.

These things will be a big part of the story over the next 2-3 decades, for starters.

Maybe at some point the collective human consciousness will realize it is time to downsize population and economy, or the downsizing will just commence without any realization-

It will be forced by the circumstances.

If anyone really wants to get in the weeds there are other reports from the European Joint Research Council, some are a bit old but they are detailed and specific:

https://setis.ec.europa.eu/jrc-report-critical-metals-energy-sector_en

https://setis.ec.europa.eu/critical-metals-strategic-energy-technologies_en?wt-search=yes

https://publications.jrc.ec.europa.eu/repository/bitstream/JRC122671/jrc122671_the_role_of_rare_earth_elements_in_wind_energy_and_electric_mobility_2.pdf

A search OECD library shows a load of hits too but I haven’t been through them yet:

https://www.oecd.org/dev/Session-4_Investing-in-Green-Supply-Chains_World%20Bank.pdf

https://www.oecd.org/env/global-material-resources-outlook-to-2060-9789264307452-en.htm

https://www.oecd.org/greengrowth/greening-energy/greengrowthandenergy.htm

Adding to what George has linked . Short video about 12 minutes. Mining and LTG .

https://www.youtube.com/watch?v=JRGVqBScBRE&t=297s&ab_channel=SimonP.Michaux

A podcast of about 45 minutes but good bringing EROEI etc into the discussion .

https://www.youtube.com/watch?v=gpPRZNF1Pso&ab_channel=PhilDobbie

Here Is a video, who has combed through the weeds and summarized her findings in two books.

https://www.youtube.com/watch?v=k-gyAp3GO3k

Chile is ideal for solar energy, because so much of the country is at high altitude. Northern Chile has the highest solar irradiance of any region in the world.

Mining companies like Anglo American and Biliton that operate in Chile have been investing heavily in in renewables for years. This has mostly been for copper mining, but solar is also growing in the Atacama desert now as well.

In general, mining in remote locations is well ahead of the rest of the world in terms of electrification, because transporting fossil fuels is more expensive than transporting electricity. On site renewables are even cheaper, so they are enjoying rapid uptake.

Oil drillers buy diesel and flare gas, but other industries are better at pinching pennies. Renewables cut costs at remote locations by making maximum use of local resources.

Yes, the mining industry is deploying more and more electrical machinery along the chain of production.

However, at some point we will find ourselves in a situation where petrol for transport is in restricted supply or very expensive. And electric transport may not be available for purchase due to battery manufacturing capacity constraint or high cost of component materials.

The ease at which people have been able to get ‘a new ride’ may evaporate.

Everyone who hopes to keep traveling beyond walking range better get used to a much tougher, less convenient and more expensive future deal. Pick a location that you really like to live, and get used to it.

An exception to this exists- if you get an EV before possible supply constraints limits availability, and you have a dozen solar panels and a half sunny location then you will have (relatively) very inexpensive miles at your disposal. I bet such a person will be in high demand as a people or cargo mover.

Mrs. Granholm’s comment about renewables representing the “greatest peace plan that ever existed” is naive beyond comprehension. As the price rises for “Unobtainium”–rare earth elements (REE’s) over which China now holds a virtual monopoly (China Rare Earth Group)–and the price for increasingly scarce oil & gas rises in lockstep, there is going to be a mad quest for energy, especially electricity. China refines 95% of all REE’s. The largest known cache was in Helmand Province Afghanistan. The USGS obtained the data, but the whole enchilada is now being offered to China for mining/refining. In effect, if we don’t watch it, the transition from fossil fuels to renewables could represent the most treacherous time for global civilizations since WWII.

Gerry we agree on this

“the transition from fossil fuels to renewables could represent the most treacherous time for global civilizations since WWII”

Where we part thinking is on a pretty simple distinction-

It is the running out of oil and then the other fossils that is the both the wood and the spark that will light the bonfire of war, both internal and external.

The renewables and electrification of industry and travel are a sideshow to that. Countries that deploy these alternatives to oil/ICE at mass scale are going to have a buffer to fall back on- either a lot or just a little depending on how proactive (and fortunate with resource) they are.

I don’t disagree. But part of me does wonder why we are building wind turbines with rare earth magnet alternators in them? Why not just a hydraulic pump in each turbine with dozens of turbines powering a single large electrical generator on the ground? And for smaller power output, local applications, i.e ~100kW, wind turbines could be built using compressive stone towers and wooden blades, close to the applications they are powering. Lower embodied energy materials. The towers should last for centuries. The blades get replaced every 20 years. Some applications could even make use of direct mechanical drives, without need for electricity production at all.

Intermittent power generation can be dealt with either by adjusting working patterns to when energy is available, or by overbuilding generation, storing excess power as heat and backing up baseload with a gas turbine. I cannot escape the thought that somewhere along the line society is failing due to a lack of lateral thinking. With wind energy, we appear to be building complexity into something whose advantage lies in its simplicity.

Thank you gentlemen .

https://oilprice.com/Latest-Energy-News/World-News/The-US-Will-Be-A-Net-Oil-Importer-In-2022.amp.html

I have never understood this. Why is this news?

From what I gather, the US, over at least the last two decades, has always consumed over 18 million barrels of oil-based products per day.

When has the US ever produced anything near 18 million barrels per day? US Oil Consumption.

Isn’t that what “net importer/net exporter means,” the difference between production and consumption?

Or am I thoroughly confused?

The US produces a large amount of natural gas liquids from the shale gas fields especially (ethanes to pentanes) so overall, as pure barrels of anything hydrocarbon, it was a net exporter, but it doesn’t keep all the prduction to itself. It tends to import heavier hydrocarbons and export lighter ones and (I think still) it has more refining capacity than for domestic needs alone, so as a net result it imports crude and exports product.

Thanks. So what you’re saying is, “It depends upon what your definition of oil is”?

A significant part of the definition is that exportable crude oil includes that oil that is imported for refining purposes. So once the USA refines the imported oil, it becomes labelled USA crude and then can be used for accounting purposes as exported oil.

That’s the only way that the USA can claim to be an oil exporter if it only extracts 12 million barrels of oil per day but is consuming over 18 million.

Seems than Opec need to increase production to cover the worlds oil demand, but that spare capacity aint not much perhaps 1 mbpd. mainly SA.

Will the increased riggs in US shale change much of this in 2023 and onwards…?

Seems like high oil price will be the new reality..

Freddy,

I will have some more on this later this week with a post on the Permian basin. At the current oil price level, Permian basin output may increase significantly. So the short anwer to your question is yes, US tight oil output might be significant from 2023 onwards to 2030 if oil prices remain at current levels (I expect they will increase to over $100/bo). A significant supply response from OPEC plus and others to higher oil prices and some demand destruction due to high oil prices might reduce oil prices to under $100/bo, but if they remain above $75/bo then tight oil output will remain significant.

Dennis

What about availability of experienced crews to operate the frac spreads and rigs. Also one of our participants keeps saying steel rods are in short supply.

Ovi,

Prices and wages will rise, the pandemic fears will subside and market dislocations are likely to be resolved as markets respond to price signals. Shortages happen in market economies, prices increase, profits go up, more investment occurs in industries where supply is tight and supply increases bringing prices back to “normal levels” where the price is equal to marginal cost in competitive industries. If this does not occur then oil prices will rise to levels that are high enough to balance the market.

” … If this does not occur then oil prices will rise to levels that are high enough to balance the market.” – Dennis

As you know oil is not just a “market”, it’s the precursor to every market, everywhere, including yours. I know you know that but you appear to treat PO like a cold snap in Florida, “well, a shortage simply means the price of orange juice goes up.”

Your point is factually correct, but it stops where most everyone else’s’ concern starts, which is why you get the grief.

Pops,

I agree peak oil may be a problem. My guess is that prices will rise to the point that people find alternatives, whether more fuel efficient ICEVs that use less oil, or plugin hybrids that use even less, or BEVs that use none at all. Heavy land transport can move to electrified rail with BEV heavy duty trucks used for rail to warehouse, also natural gas could be used for heavy duty transport. While this transition occurs oil prices may be very high and the transition may be difficult, much depends on relative prices and how fast battery production (and the raw material production that is needed to support this) can be ramped up. Once peak oil is finally taken seriously by the mainstream political power brokers we could see a WW2 like effort to make the needed transition.

We will see. Some government intervention might be needed.

Pops —

As you know oil is not just a “market”, it’s the precursor to every market, everywhere, including yours.

Although there is some truth to this claim, most oil is flagrantly wasted. For example, long distance trucking would be a good example of your argument, but long distance trucking is ridiculous and only exists thanks to massive subsidies. If oil prices get too high, the market will find workarounds.

Yes , we can get back to using mules , donkeys and horses . Oil is the master resource and there is no workaround it . Read this .

https://energyskeptic.com/2016/when-trucks-stop-running-so-does-civilization/

Alimbiquated – market will definitely find a reach around. keep telling yourself that as you take it up the wahoo. That’s the funniest shit I’ve heard today, and today was a humdinger for a doomer like me.

Twocats

take it up the wahoo.

If there is one thing the pandemic has taught me, it’s that many people are just whiners and are so stuck in their habits that even minor lifestyle adjustments get compared to genocide. The sky won’t fall if we can’t get fresh flowers from Kenya delivered to your door or another load of stamped plastic crap from East Asia trucked across the continent.

I think a big misunderstanding about economics is that people think “demand” means “what people have to have or they will die” instead of “what people are willing to pay for”. If shipping gets expensive it will just stop, and people will buy local, or simply less.

Another problem I see is a stunning faith in modern technology coupled with an inability to imagine anything better. Voltaire lampooned this “best of all possible worlds” thinking in the 18th century, but people still haven’t gotten over it.

In fact modern society is rife with inefficiency, and America is particularly inefficient when it comes to energy consumption. There are many easy solutions to the problem, both technical and non-technical. Notice for example that the US consumes about three times as much oil per capita as Germany does, and Germany isn’t particularly efficient. You don’t have to look far for solutions.

ALIMBIQUATED: “most oil is flagrantly wasted”

No doubt oil is wasted, hunter/gatherers didn’t need any. But every drop of oil in modern society is tied to someone’s income.

So the question is: whose income is “wasted”?

Pops , correct . Our system is designed like that . My waste is your income . Somebody wrote a book ” The landfill economy ” . Describes exactly this phenomenon .

Pops- “No doubt oil is wasted…But every drop of oil in modern society is tied to someone’s income.”

It is certain that as oil supplies deplete that whole industries that are now seen as a normal part of life will fade out. And the income and jobs in those sectors will fade with it. There would be some wisdom to understand and come to grips with this.

In some places and sectors this may be abrupt and severe, and others much more gradual.

It comes with the territory of peak oil.

Examples of the vulnerable sectors- internal combustion engine component manufacturing, leisure travel by land sea and air…

Example of most vulnerable places- I’m curious to hear others peoples take on this

And yes- most oil is wasted. It is 2022 and something like 60% of oil is used for light transport with an energy efficiency of only around 30% (70% energy content wasted as friction/heat/partial combustion). Much of that oil consumption could be replaced with electric transport. And eventually it will- it appears that humanity will wait to be forced into the transition rather than being out in front of the crises. And I ask- what other issue stares humanity so clearly in the face as oil depletion? [Ok, overpopulation is the base problem]

Very slow to react to the reality. Even though we like to think of humanity as smart. Even many people here who may consider themselves savvy to energy issues don’t seem to have digested the realities beyond what was going on last year..

Dennis

This is old news from last week. Thought I should remind you what Pioneer said.

“Whether it’s $150 oil, $200 oil, or $100 oil, we’re not going to change our growth plans,” Pioneer Natural Resources’ chief executive Scott Sheffield told Bloomberg Television in an interview. “If the president wants us to grow, I just don’t think the industry can grow anyway,” Sheffield added.

Ovi,

Pioneer is one of many producers of tight oil, other companies may choose to grow faster than Pioneer and they will lose market share, that is their choice.

Dennis.

The companies at present have pretty much defined their remaining well locations. They mostly have HBP acreage.

Recent articles have explained that the faster they use those locations up, the quicker their companies will run out. None seem to have exploration plans past US shale.

I have thought about that quite a bit before now. All of these pure shale plays, what is the long term plan?

I also think they finally figured out that they can affect oil prices. US producers had zero affect on them from 1973-2013. They didn’t realize they did until 2019, when they started taking their foot off the pedal.

Shallow sand,

Wouldn’t you guess that the drillable locations that are profitable would be different at $100/bo compared to $50/bo, what about $150/bo?

Am I missing something here.

The USGS mean estimate for net acres (acres times expected success rate) for the Permian basin is about 50.5 million acres as of mid 2017. Let’s assume 300 acres per well on average (9500′ by 1320′ is about 290 acres), that would be roughly 168 thousand wells. The most productive benches assessed have net acres of about 31 million acres, if we assume only those benches have future completed wells at 300 acres per well that would be about 103 thousand wells.

I have not gone through the work of looking at all publicly traded companies 10ks and 10qs to try to determine the number of drillable locations, but I imagine this changes as the price of oil changes.

Bottom up analysis is definitely better, but more work than I have time for.

He is correct.

Thanks Coyne, that would be interesting.

What I remember for some years ago was the CEO of Continential Resorces Mark Papa told they would not add more riggs if the oil price WTI was below 75 usd each barrel WTI. Since that I believe the Capex have increased even with 3 miles latheral.

I am exspected to see a significant increase of US oil production from L48 2-3 months from now as the rig count is increasing a lot. If we not could see that it might be a combined reason of constraints on the ground related to Earth quake, increase child well problems, contacts between wells because of tighter spacing as more wells are drilled on a limited Area. From what I have read a long 3 mile lateral will have higher production each well but lower production trough life time each foot wich mean more oil will be left in the ground. As the field gets more utelized there is also lots of other factors that will impact production like water cut, pressure drop. I guess the old fields line Eagel Ford have some challanges we also will see in Permian during time.

Freddy,

It may be that output per acre will decrease with the longer laterals, that is up to each individual business to decide on the most profitable approach. My model simply takes the basinwide average of about 9500 foot laterals and assumes spacing of 1320 feet between laterals (based on comments by LTO survivor) which is 288 acres per well, as Mike Shellman has pointed out most leases are only two sections (2 square miles of area) and allow for only 10,000 foot laterals at most (the leases are 2 miles by one mile in many cases). So there may not be a big move to 3 mile laterals. I assume new well productivity will decrease starting in Jan 2021 in my scenarios, I use actual production through 2021 based on http://www.shaleprofile.com data from the blog posts there to develop individual well profiles for the average 2010-2012 well, then 2013, 2014, 2015, 2016, 2017, 2018, 2019, and 2020. The newer wells have less data (only 12 months for the 2020 well profile) so the estimate will be less accurate. I then assume output decreases dependent in part on the well completion rate (if more wells are completed in a given month the decrease in new well productivity is higher than it would be if the completion rate was lower). I take the net acres based on the USGS mean TRR estimate and divide by 300 acres to estimate total wells and then adjust the rate of decrease so that the TRR is 75 Gb (USGS mean estimate for Permian basin). Then economic assumptions are applied for a future oil price scenario using a discounted cash flow analysis to determine if a completed well will be profitable. This reduces the number of completed wells and reduces the cumulative output to the ERR which will always be less than the TRR (though in a high oil price scenario sometimes the ERR is equal to the TRR).

Here is an article from 2015, this is now 7 year since…

https://uk.finance.yahoo.com/news/u-shale-oil-needs-80-114040277.html

Here mark Papa tells 80 usd WTI is needed to further grow shale oil production.

What have happened since this?

Longer latherals to decrease some drilling cost.

Ducks reduced to very low level

Inflation growing and increase capex

Labour cost increase

Earth quake gives challanges with produced water

Thiere 1 /hot spots are used, now Thiere 2, 3 with lower output of oil each foot latheral.

There is also higher costs due to Methane and CO2 emisions, that add cost.

What happens if there will be a oil glut again in 2025 with oil price WTI hits 75 usd. Would the producer still earn money trough hedging contracts..?

Freddy,

Since 2015 well productivity has increased and breakeven costs have fallen. For the average 2020 Permian well the well breaks even at a nominal annual discount rate of 25% and a natural gas price of 3.50 per MCF, NGL price at $18.20/b, and crude oil price of $52/bo at well head assuming well cost of $10.8 million (full cycle) and OPEX per barrel of $14.37 over the life of the well with royalties and taxes assumed to be 28.5% of wellhead revenue, and transport cost to refinery assumed to be $5/bo.

You are not confused Mike. A lot of effort has gone into creating numbers to hide the fact that America is a massive net consumer of oil, and has been since WWII.

I guess it’s a “feel good” thing, like a fat girl telling everybody she’s on a diet and eating tiny portions at meals but still gobbling sweets in private.

Was anyone here aware that Alice Friedemann called Peak oil? What do you think about it? Look here for yourself:

https://energyskeptic.com/2022/failing-oil-and-gas-companies-a-sign-of-peak-oil/

No, I was not aware of this publication. It is dated very recent, February 1st, 2022. It will take me some time to digest this. She agrees with what I have been saying for over two years. However she explains it better than I ever could. She also digs deep into every detail of peak oil. Thanks a million for posting it.

A complimentary article from the same site-

“Is there a long emergency plan for peak oil?”

https://energyskeptic.com/2022/is-there-a-long-emergency-plan-for-peak-oil/#comment-58661

[don’t look here to find a national energy policy that has developed over the past 4 decades or has made it through a hyperpartisan and short sighted congress- you won’t find it]

LUKASCH —

From your excellent Alice Friedemann article.

“Nor will we ever reach “peak oil demand” because heavy-duty transportation (trucks, locomotives, ships), manufacturing, the 500,000 products made out of petroleum, and natural gas fertilizer that keeps 4 billion of us are utterly dependent on fossil fuels. Even the electric grid depends on fossil fuels to provide two-thirds of electricity, and nearly all of the energy to construct wind and solar contraptions (they are ReBuildable, NOT renewable). This is explained in great detail in my latest book “Life After Fossil Fuels: A Reality Check on Alternative Energy” and previous book” When Trucks Stop Running: Energy and the Future of Transportation””

According to this article by Michael Kern, oil companies are prevented from increasing production due to supply chain bottlenecks and the soaring cost of drilling.

https://oilprice.com/Energy/Energy-General/The-Cure-For-High-Oil-Prices-Might-Just-Be-Higher-Oil-Prices.html

Gail Tverberg has been predicting something similar for years. As time goes forward, a greater proportion of reserves consists of unconventional deposits or deep offshore. So production cost of each incremental barrel is increasing. But the price that refiners are able and prepared to pay is limited.

Tony H , bullseye . I have long argued that EcOE ( Economic Cost Of Energy ) is too high for our current lifestyle . Further I have espoused ” If you can’t afford it then you can’t have it ” . Affordability is the key .

Ask Sri Lanka and Turkey . The next Lebanon’s ? Only time will tell but Sri Lanka is in line . I have posted a link on this earlier . Europe would be no better but for the Ponzi being carried out by the ECB . All ponzi’s collapse , the question is not ” if ” but ”when” . ECB is the biggest ” bad ” bank in the history of finance . It is loaded with BS bonds of the PIIGS and zombie corporations . Get a parachute .

I coincidentally just put a link above to her discussion of the various ways peak oil leads to insurmountable troubles. I met Alice Friedeman at ASPO Pisa conference in 2006. She is a tireless worker and interestingly her grandfather knew Hubbert when both were at University of Chicago. I am reading now her book, life after fossil fuels.

Dennis

This is a first look at the “production/stock change” discussion started above. JODI updated their data to December 2021.

The first chart shows that stocks went up by 2,284 kb or 74 kb/d in December.

The second chart looks at four pieces of info. Two are direct info from the OPEC reports.

The red graph shows production according to secondary sources. The number shown is the three-month revised final number shown in the OPEC report.

The green graph is production according to direct communication. Note that Direct communication output is always higher.

The remaining two graphs present two ways of looking at the OPEC data.

The blue line assumes that the secondary sources numbers are too low and missing some info since those numbers have been lower than direct communications for the last six months.

For December 2021, secondary sources estimate production to be 9,945 kb/d. (Note this is from the February OPEC report). Since stocks increased by 74 kb/d in December, that would imply actual production of 10,019 kb/d. By fluke OPEC direct communication is 10,022 kb/d. On the other hand in January, output from secondary sources was 9,077 kb/d, but stocks went down by 91 kb/d so real production would be 8,986 as opposed to direct which claimed 9,103.

The orange graph assumes that direct communication info is correct. The graph then shows how much oil Saudi Arabia exported and used internally. For January 2021, direct communications says 9,103 kb/d were produced. At the same time stocks dropped by 91 kb/d. That implies that SA’s exports and internal use of crude amounted to 9,194 kb/d in December.

The data collected is shown in a table below. Only six months of data is used in the chart because an expanded Y scale was required to show the small differences.

Ovi,

Current oil stocks of oil are equal to stocks in the previous period plus revisions, minus internal oil consumption within the nation minus exports of oil plus imports of oil plus oil produced. So there are several pieces of missing information which your chart assumes are unchanged, this may be correct, I don’t have enough information to say.

Table

Two weeks in a row 10year US bond yields have been rejected as they try to climb over 2%.

Is the inflation and growth story getting rejected here? I still believe when they actually start hiking rates the yield curve inverts as long term bond yields fall while short term rise.

I wonder how much margin debt has been used to bid up price of oil? Don’t be surprised if the price of oil heads other direction as the rate hikes cycle takes place.

Wall Street thinks the Fed is too chickenshit to actually raise rates.

Wall Street darling Cathie Wood has once again gone rogue against the common consensus on rising price pressures, and reassuring the investment community that inflation is anything but a problem.

During her latest monthly market webinar which aired this week, Wood took aim at the financial market’s obsession with accelerating prices, instead insisting that inflation is not a growing threat. To illustrate her firmly-held conviction, the Ark Invest CEO pointed to the influence of labour productivity gains, citing a slight 0.3% increase in unit labour costs in the fourth quarter of last year.

Wood insisted that financial markets have a tendency to overlook the effect of productivity improvements on long-term inflation prospects. She took aim at recent US wage data showing that average hourly earnings rose 5% from the year before, instead contending that the figure is probably closer to 3% in real terms due to an increase in worker productivity. “I think not taking into account productivity is going to cause a serious miscalculation in terms of what’s going to happen to inflation,” she added.

The Ark Invest CEO also pointed to the oil market, which has recently been a substantial source of rising consumer inflation. According to her, the sudden appreciation in oil prices to above $90 per barrel will eventually correct itself, as an increase in supply will be attracted back into the oil market, ultimately equalizing the inflation equation. Wood cited 2019 oil production data, which showed that output peaked at 12.3 million barrels per day, making the US one of the largest producers of energy.

According to Wood, such levels will be reached once again, because “it appears in 2022 we will be going up to roughly 12 million barrels per day and in 2023 up 12.6M barrels per day.”

https://thedeepdive.ca/cathie-wood-criticizes-financial-markets-for-focusing-on-inflation/

HuntingtonBeach

I saw her on CNBC the other day and she looked pretty rattled. She seemed to be trashing around, like a rudderless ship. Her big holdings of TSLA, ZM, ROKU and COIN have all taken a big hits recently.

As for oil production, the peak in 2019 was 12,966 kb/d. For her, like many economists, it’s all about more investing and innovation. Geology has no place in their thinking.

I suppose if you don’t like ARKK, you can invest in SARK, which is a fund which seeks to be -1x ARKK.

I remember the dot com crash and the Munder net net fund.

I am sure some of her choices will be big long term winners and some won’t.

But saying oil will never be higher than a certain price (or lower) is the sign of someone who doesn’t follow the oil market closely enough.

Wonder if she has ever studied shaleprofile? I doubt it.

Ovi,

Many point to average annual output rather than a single month’s peak output. In 2019 average annual US crude plus condensate output was 12289 kbpd according to EIA data as of today. The most recent STEO has US average annual crude plus condensate output at 12598kbpd in 2023. Seems her data is based on average annual output and is correct.

Dennis

Note what Cathy said: “Wood cited 2019 oil production data, which showed that output peaked at 12.3 million barrels per day, making the US one of the largest producers of energy.”

Peaked not Average.

Ovi,

I interpret 2019 oil production data as the average for the year 2019 and for the US that was the peak year of oil production.

As in chart below

Ovi,

“Also last week, Devon Energy’s Rick Muncrief told the Financial Times, “In the back of everyone’s minds is, ‘When is it going to be [production] growth? . . . We have investors saying ‘My gosh, if not now, when?’ But for everyone saying that there’s at least one other if not two others waiting to say, ‘Gotcha! We knew that discipline would be shortlived.’ We have learned our lesson.”

Speaking to Bloomberg in a separate interview, Muncrief also said, “We’ve had enough head fakes that we’re going to be very thoughtful in ramping activity up. Let’s face it: we all are recovering in one way or another from this pandemic. We’re just slowly getting healthier and healthier over time, but you don’t get there overnight.””

https://oilprice.com/Energy/Crude-Oil/Are-US-Shale-Firms-Spending-Enough-On-New-Oil-Projects.html

I believe Fed Fund Futures for 2022 is still pricing in for over 5 rate hikes, which is insane. So yes, Wall Street is absolutely convinced the Fed is going to make due on its bat-shit hawkishness.

Okay so funds rate will be only about six percentage points below the rate of inflation at that point? Meaning only a -6% actual return rate. Not a number generally associated with hawkishness. Typically this funds rate has been ABOVE the rate of inflation, not six points below.