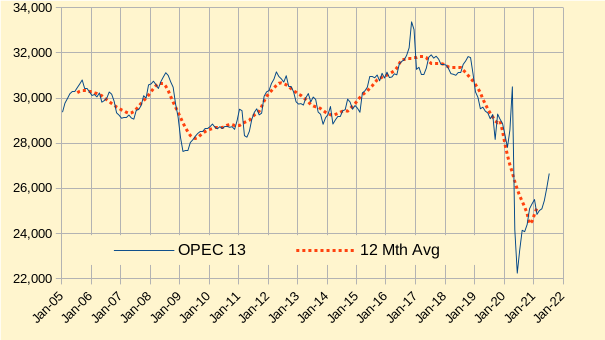

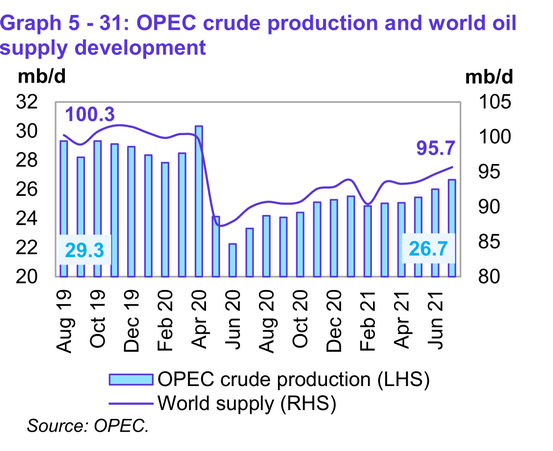

The OPEC Monthly Oil Market Report for August 2021 was published this past week. The last month reported in each of the charts that follow is July 2021 and output reported for OPEC nations is crude oil output in thousands of barrels per day (kb/d). In the charts that follow the blue line is monthly output and the red line is the centered twelve month average (CTMA) output.

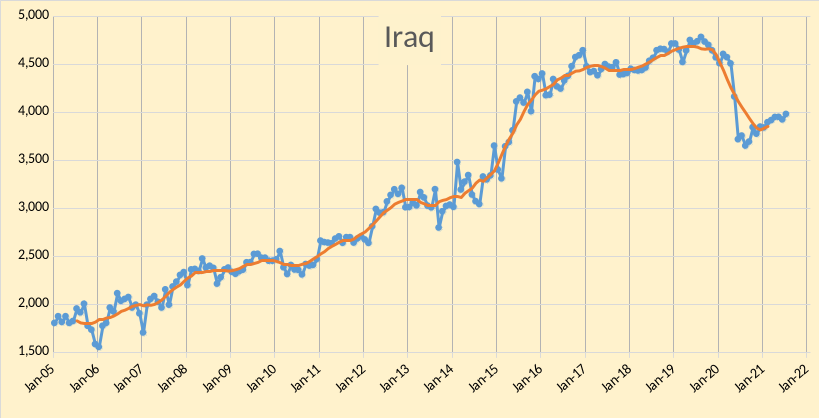

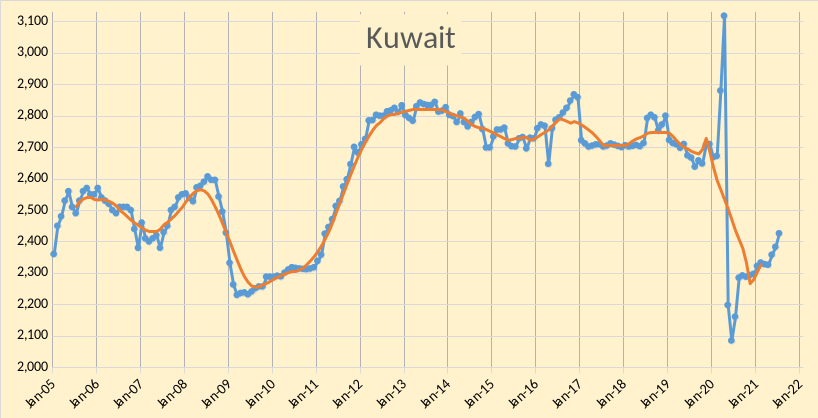

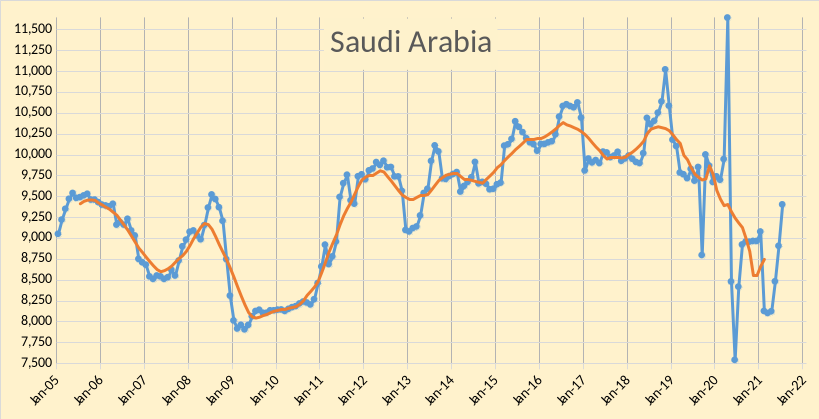

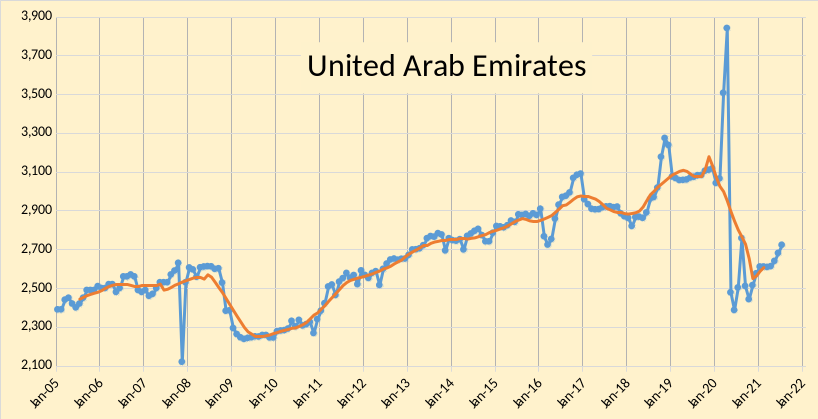

OPEC produced 26657 kb/d of crude oil in July 2021 based on secondary sources, an increase of 637 kb/d from June. June output was revised down by 14 kb/d from what was reported last month and May output was revised up by 6 kb/d. Most of the increase in OPEC output was from Saudi Arabia (497 kb/d) followed by Iraq (56 kb/d), Nigeria (45 kb/d), UAE (42 kb/d), and Kuwait (42 kb/d).

World liquids output was 95.7 Mb/d in July 2021 about 4.6% below the August 2019 level of 100.3 Mb/d. OPEC crude oil output in July 2021 was 2.6 Mb/d (about 9%) below the August 2019 level of 29.3 Mb/d.

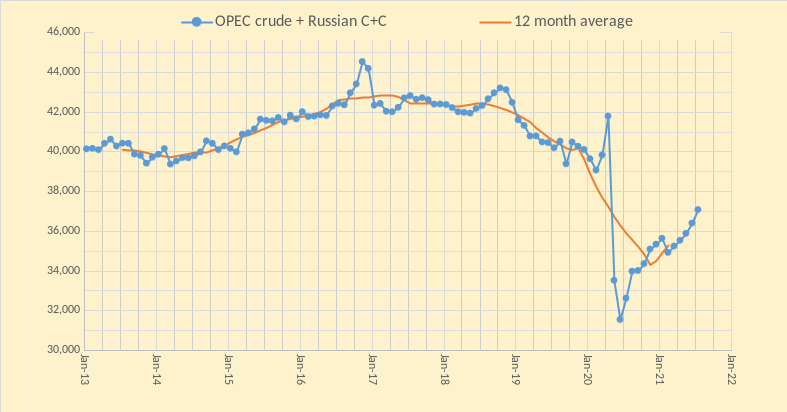

The chart above uses data from the Russian Energy Ministry and converts from metric tonnes to barrels at 7.3 barrels per tonne, the combination is OPEC crude plus Russian C+C output. Russian output increased by 42 kb/d in July 2021 to 10418 kb/d. OPEC13 crude + Russian C+C output increased by 679 kb/d in July 2021 to 37075 kb/d. The centered 12 month average OPEC crude plus Russian C+C output in Feb 2021 (most recent data point) was 35283 kb/d an increase of 372 kb/d from the Jan 2021 level.

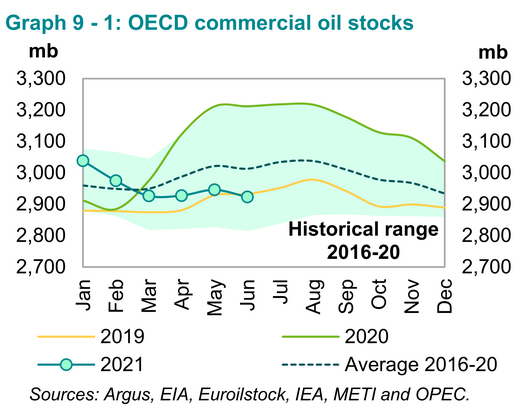

OECD commercial oil stocks are 90 million barrels below the 5 year average (2016-2020) and have been below the 5 year average for the March to June 2021 period (4 months). OECD oil stocks have now have fallen below the level of June 2019, see figure 18 above. Typically we see oil prices rise as commercial OECD stocks fall below their recent 5 year average.

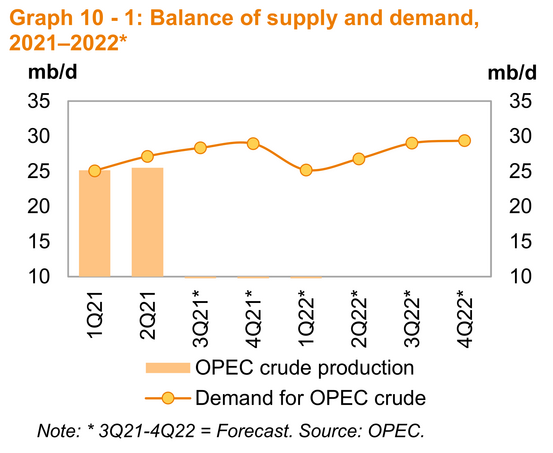

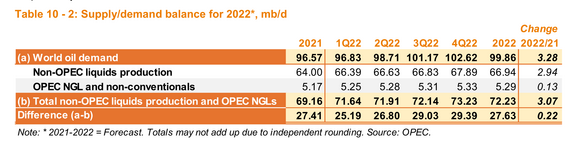

Figures 19 to 21 cover the difference between World demand and non-OPEC liquids production and OPEC NGL and non-conventional oil production shown in the last line in figure 20 and 21. This difference is also referred to as the “call on OPEC” for crude oil production. Based on the trends in OPEC output it seems unlikely OPEC will be able to meet this level of output of roughly 29 Mb/d for the fourth quarter of 2021 and the 3rd and 4th quarters of 2022, without sanctions being lifted on Iran, at current levels of Iranian output OPEC is likely to come up short by at least 500 kb/d in the last quarter of 2021. This assumes OPEC projections for non-OPEC output and World demand are correct. I believe the “call on OPEC” estimates are conservative and that actual demand for OPEC crude is likely to be higher than OPEC has estimated due to higher World demand and lower non-OPEC output than OPEC is forecasting.

It looks like oil prices will continue to rise until at least 2023, by that time the high prices might lead to higher World output and lower demand growth and potentially a more balanced oil market.

233 responses to “OPEC Update, August 2021”

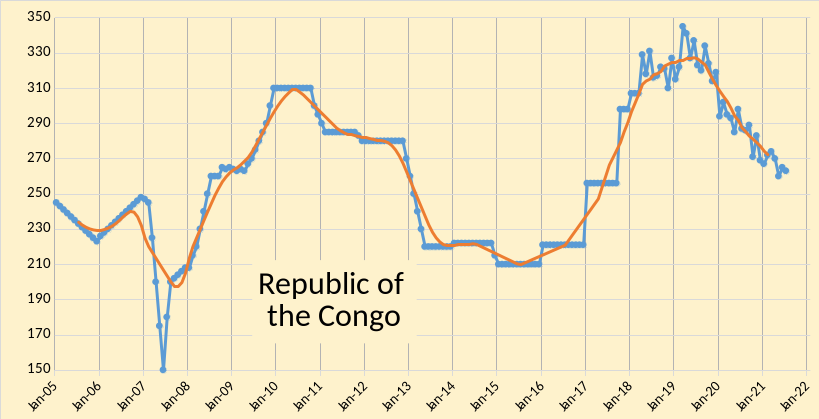

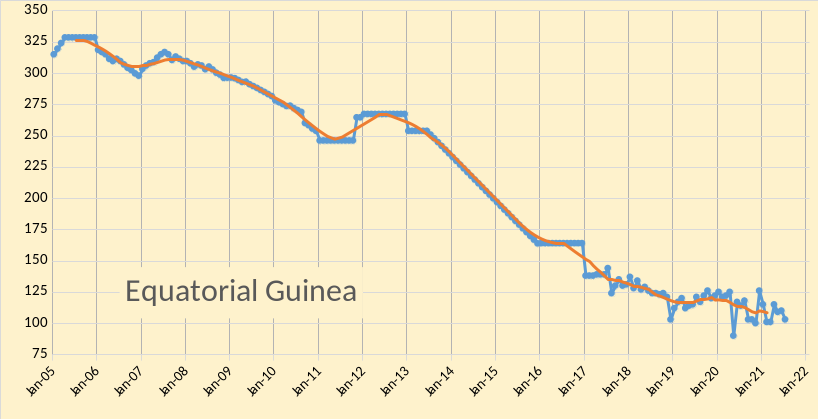

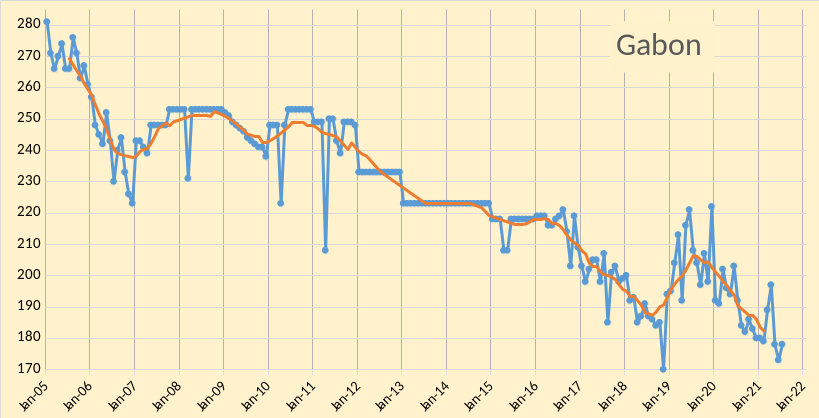

OPEC is now basically five nations, Saudi Arabia, the UAE, Iran, Iraq, and Kuwait. They produce about 80% of OPEC production. The other eight are Algeria, Angola, Congo, Equatorial Guinea, Gabon, Nigeria, Libya, and Venezuela. The combined production of these eight OPEC nations has been declining since 2008.

While the big five have been ramping up production, with plans to reach their pre-covid level in a few months, the other eight have done nothing for the last 9 months. In fact, since February of this year, the big 5 have increased production by 1,886,000 barrels per day. Since February, the other eight’s production has declined by 70,000 barrels per day.

The other eight have recovered by about 1.14 million barrels per day from their post-covid lows. But it looks like that is about as far as they are going to go. In fact, their current level of production matches their decline trajectory perfectly. Here is the important point: They are down just over 1 million barrels per day from their pre-covid level. And they are down about 2.25 million barrels per day from the OPEC 2017 12 month average peak.

This all means that OPEC’s Big Five, in order to get back to their pre-covid level would have to increase their production by 1 million barrels per day, over and above what they produced pre-covid. And if they were to ever surpass their 2017 peak, the Big Five would have to increase their combined production by 2.25 million barrels per day over and above what their average production was in 2017. I seriously doubt they can do it. (Their monthly peak was Nov. 2016.)

The moral of this story is: In the rest of the world, as in OPEC, the declining nations are a very serious headwind in any attempt to increase world oil production. Every year, some producing nations are going from being increasing nations to declining nations. Russia just recently entered this group. So unless your prognostications take into consideration this declining nation headwind, it is destined to be in error.

Ron,

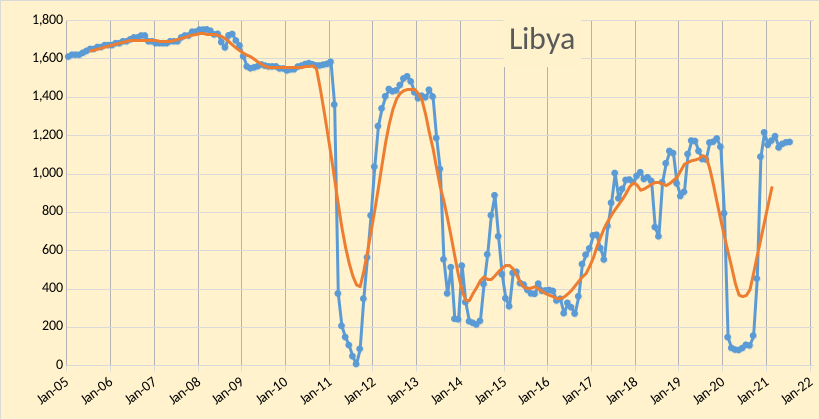

Much of the decrease in the other 8 is due to decreases from Libya and Venezuela, a better chart would be the other 6 (excluding Libya and Venezuela). Venezuela cannot decline by more than another 512 kb/d. Libya might stabilize or resume its civil war, lately things seem to have stabilized there (1160 kb/d is average for past 9 months for Libya).

Dennis, Libya is already back to producing at her pre-covid level. Most likely, Libya is currently producing flat out. So no, none of the decreases is due to Libya.

Venezuela is another story.

Venezuela’s Oil Reserves Doomed To Become The World’s Largest Stranded Asset

The aggressive push to decarbonize the world economy is forcing big oil to examine how the carbon emissions of its operations can be reduced with a goal of becoming carbon neutral. That coupled with the threat of peak oil demand has seen oil supermajors reevaluate their business strategy, with many now choosing to eschew high-cost carbon-intensive petroleum projects. This poses a major threat to Venezuela and the crisis-torn petrostate’s economic recovery. The OPEC member possesses the world’s largest oil reserves, estimated to be around 304 billion barrels or enough crude oil to meet global consumption for roughly 8 years. Most of Venezuela’s petroleum reserves, as much as 77% or possibly more, are composed of the extra-heavy and heavy crude oil found in the Orinoco Belt in the East Venezuela Basin. That heavy and extra-heavy crude oil, most of which is very sour and has an API gravity of 10 degrees or less, is highly carbon-intensive to extract and refine. For those reasons, there is a growing likelihood that a significant portion of Venezuela’s vast petroleum reserves could become a costly stranded asset.

Venezuela is gone forever. Or at least gone for the remainder of our lifetimes. So its decline is a legitimate decline. Not something temporary.

Game over Dennis. But my prognosis remains as it is, including Libya and Venezuela. There is no need to revise my charts or estimate.

Ron,

I have assumed Venezuela will not recover, but future decline from Venezuela can be no more than the July 2021 level of about 500 kb/d. Or Venezuela might stabilize at 500 kb/d.

The decline from Venezuela going forward will be considerably less, so using the decline of the other 8 based on decline from Libya and Venezuela which is inlikely to continue gives a false impression. The 6 countries of interest which are likely to continue to decline, did so at a rate of 120 kb/d per year over the period before OPEC cut back on output (Jan 2019). Much less than increases from other OPEC nations.

Ron , thanks for your analysis . The ” savior 5″ could very soon become 3 . Climate change is drying up the rivers and creating electricity problems . Hydro power is as good as dead in this part of the world . A good read .

https://oilprice.com/Latest-Energy-News/World-News/Baghdad-Says-Iran-Halted-Electricity-Exports-To-Iraq.html

Tks Dennis . Proficient as always .

Thanks Dennis,

I am actually surprised by the resilience of Saudi production in the face of declining rig counts. Didn’t expect them to be able to continue up by 1/2 mbd. In fact world supply is higher than I expected it to be at current investment levels also.

A big reason for OPEC decline after 2017 was decreases in Iranian and Venezuelan crude output. Venezuelan output is unlikely to recover near term, Iranian output will only recover with a removal of US sanctions and might add 1.4 Mbpd to OPEC output. That might allow OPEC output of close to 30 Mbpd. Note that the absolute level of decline from the declining group of OPEC nations has been much less than the increase from Ron’s big 5 minus Iran over the 2013 to 2018 period. I exclude Iran because sanctions were imposed in 2017 driving down Iranian output by 1800 kb/d through mid 2020 with some recovery since the low point.

Dennis , the water problems in Iran and Iraq are unfathomable . While Iran is an Islamic republic are you aware that the “Sikh” community(religion) is the only one allowed temples in Iran . Fortunately when I was in India my immediate neighbor was a “Sikh” whose inlaws were in Tehran and I still keep in touch with him . According to his report the sanctions have had a terrible effect on the economy . Hyperinflation ( $ 1 for a doughnut )shortages are the order of the day . The only thing keeping the cohesion is the hatred for the US regime which is pinned for all problems due to sanctions . Iran survives because of smuggling of every item ( rice to spare parts ) via Dubai . They print and devalue their currency but unfortunately they cannot print water . They have no coal ,nuclear only hydro and gas for electricity production . The choice now is water for drinking or electricity .

Iraq is even worse . Saddam diverted the waters of the Tigris and Euphrates . Constructed a dam near Mosul but on unstable ground and soil . It needs 24/7 cement gritting to keep it stable . Drinking water problems are just as bad as in Iran . The choice is now between water for drinking or electricity here also .

Your assessment based on the situation 2013-2018 is invalid , just as invalid would be the situation in Afghanistan in July and August . There are tipping points and one ignores them at peril. . Had to edit because Biden is crazy .

https://news.antiwar.com/2021/08/13/us-sanctions-companies-for-transporting-iranian-oil/

Only sanctions aren’t going to be removed. And prices are likely going lower not higher. Vaccines aren’t sterilizing vaccines. They don’t stop the spread of the virus and likely lead to more variants. Because they don’t stop the spread of the virus. Only matter of time before a variant comes along that is truly deadly. 10% or greater death rate.

Herd immunity isn’t possible without a sterilizing vaccine. Which nobody has.

Beirut is experiencing an energy collapse currently. Seems when the oil, the diesel stop flowing. The lights go out soon after.

HHH , I agree . Every nation has its reasons . UK would rather have continued lockdowns or partial lockdowns and subsidise salaries . If it ends with the stimulus program it is going to face a wave of bankruptcies and will destabilise the banks . Commercial real estate is the biggest threat and that is where the municipalities and pension funds have parked their funds .

UK imports coal from Russia. Natural gas from Norway and uranium from Kazakhstan. If Russia has a large drop in oil production. It likely won’t be mining as much coal. You could see coal exports from Russia go to Zero. How much uranium comes out of Kazakhstan if oil is not as plentiful there?

Apparently, the world coal production is flat since 2010. Don’t have hope with coal.

https://ourworldindata.org/grapher/coal-production-by-country

My point was when the oil supply starts to shrink so will coal, natural gas and nuclear. If your a place like the UK that has to import energy. You will look like Beirut currently is looking today. No central bank can save the UK. The rich in the UK will likely try to move their money out. Watch for currency movement GBP/USD will go to below parity. Ditto with the EUR/USD because Europe is largely in same boat as UK is in.

And Putin is an idiot for accepting Euro’s as payment for energy resources. Accepting Euro’s is a long term bet the Eurozone stays together when energy resources are in decline.

If the US Navy ever just ups and leaves 80% of China’s oil just doesn’t make it to China. China’s coal production goes off a cliff. As so does their carbon emissions.

Europe is China’s number 2 customer for exports behind the US. Lack of energy in Europe takes China down anyway.

China is also completely 100% dollarized. They can’t do anything without US dollars because nobody will accept their currency as payment except maybe Iran. And maybe Russia on some gas deals. Which Russia again will be left holding the bag of worthless currency for it’s resources.

When the writing is on the wall clearly for everyone to see. Energy exports basically go to zero over night. Unless you have something of value besides currency as payment.

The graph is incomplete. I found an other one from the same website. For coal, the world is producing flat. https://ourworldindata.org/grapher/coal-production-by-region

Yeah, it looks like coal has been more or less flat outside of a little variation up and down in a range since 2010.

And yes, the UK is in for some massive shocks. We already have our bills going up a lot because of the wholesale cost of gas and oil. The North Sea is basically a giant liability at this point, not an asset, and we’ve gone from exporting gas and oil to importing vast swathes of the stuff in the last 15 years.

The pandemic is less of a thing here, with most people vaccinated now and Delta being less harmful than expected. But the winding down of the furlough scheme among other relief efforts by the BoE and Treasury for stopping job losses will lead to… job losses. Next month. And this at a time when we have many positions, like HGV drivers and retail, being unfilled.

Hell, KFC is having supply shortages! Again.

So, if the energy prices go up much more, the population will be massively pinched (fuel poverty is already a major concern, even with that pathetic price cap that isn’t a cap). I know people who commute with diesel cars, and they’re now having to reconsider doing a bit of overtime at their workplace since just going in for a couple of hours means they don’t breakeven on the cost of fuel to get to work.

All this, and the Tories with a clueless idea about levelling up the devastated Northern cities which would cost something on the order of £2tn. The same amount pissed up a wall in a certain Asian nation that’s currently in the news.

HHH-

you paint a picture of complete collapse of the international oil market as soon as the oil starts to decline- that being the most extreme case.

It would interesting to hear your thoughts on a much more likely scenario (in my view anyway) where oil supply available for export declines after peak something like 20% in the first ten years. Thats about 2% a year, or take 3% if you think I’m far too optimistic about the incentive that higher oil prices will have on oil production.

What happens in that kind of scenario, which is still a very disruptive one? What happens before any wars of desperation.

I don’t have a clear idea of how things will play out, but clearly there will a reshuffling of the global order, with a new set of losers and some who lose less than others.

I suppose Russia could demand payment for oil, gas and coal in whatever currency they choose to since they will be the driver seat, for example.

Hickory,

We might have a handful of years that seem ok. Russia will have a choice. Do they use a shrinking oil supply to continue getting coal out the ground just to export it to UK. Or do they produce just enough coal for their own use saving oil. If your Russia at some point you cut everybody off. And it really depends on how fast their oil production goes down as to how soon that will be.

Putin might take Europe’s gold in those handful of year where things seem ok. But in the end he cuts everybody off. Including China

Russia has been creaming those old oil fields for awhile now. There is a seneca cliff somewhere ahead we just don’t know exact timing of it.

HHH,

US oil fields are older than Russia’s and no Seneca cliff (even after subtacting unconventional oil). US oil will see steep decline after 2035 or so as tight oil declines much more rapidly than conventional oil. I doubt this occurs in Russia, decline will be 2 to 3% unless demand falls faster than this.

As to oil prices decreasing, doubtful. Oil supply will be short and prices will go up. Changes in dollar valuation in foreign currency will be countered by actions by other central banks.

Dennis,

Maybe US conventional oil falls of a cliff too. Same method are being used to limit natural decline here in US as in over in Russia. Just because it hasn’t happened yet don’t mean it won’t.

To believe that the decline rate won’t accelerate and accelerate drastically at some point is foolish.

To believe that a 2%-3% decline can be maintain through out the remaining life of an oil field is idiotic. Cliff is coming Dennis.

HHH,

We will see, US fields are older than Russia’s, conventional onshore in L48 started in 1970, so 50 years, no Seneca cliff so far, perhaps it will come, I did not say it would not. I don’t know when it will occur or if it will. You assume it will and you may well be wrong.

Just because you think it is so, does not make it so. Check the data for US L48 onshore C plus C output for the US, you will see that I am correct on the historical data. The future is unknown. I think I have said this before.

Coal producing can be much less oil needed than you think.

The DDR had this problem already solved in the 80s – they got their cheap oil deliveries cut up from the UDSSR.

I visited a museum at a brown coal site. All big machines have been electric – even the moveable one. These had flexible power lines. They spend round about 10% of the power plant output (which was fed from this pit mine) to power them.

So they could use their spare oil for chemical, agriculture and a bit for cars (it was hard to get a car for normal people).

The biggest piece of equipment there:

https://www.f60.de/en/

Ron the Original Seneca cliff idea was from Ugo Bardi.

See

https://cassandralegacy.blogspot.com/2011/08/seneca-effect-origins-of-collapse.html

He is actually talking about World output. I think the only thing that brings on such a cliff is lack of demand. Perhaps we see a demand cliff as the World moves to EVs in the 2035 to 2040 period, though it seems unlikely we can produce enough cars to create such a cliff, though robo taxis might cause this, but that may not arrive until 2040 at the earliest.

Bardi’s figure for the Seneca cliff looks like a literal cliff, probably a 70% decline rate, I doubt this occurs without a nuclear war or large asteroid strike, or some unknown unknown of similar magnitude.

US oil fields are older than Russia’s and no Seneca cliff (even after subtacting unconventional oil).

Good gravy Dennis, you know that is not so. Prudhoe bay is far younger than Russia’s old fields, and Prudhoe bay definitely underwent a Seneca cliff. But the oldest and largest field in the USA, and once the largest field in the world, definitely underway a Seneca cliff, the great East Texas oil field. It is now almost nothing. That is what happens to all oil fields eventually.

THE HISTORY

OF THE

EAST TEXAS

OIL FIELD

Eulenspiegel,

I understand the excavators are electric. You still have to transport all that coal out of a mine and to market. Coal production takes a massive amount of oil to get to market.

Ok say you go all electric, Electric trucks, trains and even ships. That is a lot of damn electricity getting that coal to market. You’d have to export less way less to just get it to markets.

When oil goes down it takes coal and natural gas and nuclear production with it. Yet we think we are going to be able to build out a massive amount of EV’s powered by wind and solar during this to continue BAU

Ron,

Talking about regional output, for a region to experience a Seneca Cliff all fiels would need to hit their steep decline phase simultaneously, I also exluded Alaska, that is what lower 48 onshore conventional C plus C means (no tight, offshore or Alaskan production).

From 1970 to 2017 this is what the decline looked like for US L48 onshore conventional C+C, that is the metric most comparable to Russian output which is mostly onshore conventional oil.

See chart below, click on chart for larger view, annual decline rate averaged about 3.18% over the 1970 to 2017 period.

HHH,

Natural gas output won’t be affected much by a decline in oil output. If we are short on natural gas prices will rise and rate of resource development will increase. Probably little affect on nuclear or coal as well. Prices will rise if supply is short of demand, as long as it is profitable to produce, it will be produced.

You are right Dennis, my mistake. A Seneca cliff is caused when the natural decline of a field is not allowed. Like when a field has a natural decline rate of say 8%. But infill drilling brings that decline rate down to say… almost 2%. So depletion is greatly increased while decline is decreased.

That is exactly what they have been doing in Saudi Arabia. That is exactly what they have been doing in Russia.

So a Seneca cliff is brought about by massive infill drilling with horizontal wells. We did not do that with Prudhoe bay or East Texas.

It is inevitable that if you pull the oil out a lot faster while disguising the natural decline rate the decline rate must eventually catch up, with avengence. That process is called a Seneca Cliff.

@HHH

In the local market here, main transport is by (electric) train, under the earth and to the customer. Street transport is not cheap enough. A typical coal train here has 100 wagons, pure coal not mixed up with other goods and drives directly to the customer. If you need 1000 tons coal a day, you’ll build a local rail access.

Only the international market is by ship, and therefore by oil. Theoretical you could power them by coal, too, as in the 19th century. I hope not.

The coal economy was invented before oil – and therefore it has little oil components.

We may not have oil here in Germany, but a coal past. And coal was a mostly rail centered business, or on ships. On the road there was only transport until the 60s for home heating, from the station to a home. But most coal was consumed for power plants and factories / iron production.

You have always to spend energy to transport things to the market. That was why old heavy industrial centers have been cluttered around the coal – cheaper not to transport it wide before using.

You’ll see the effect again when solar is the solution – heavy industry will move to the sun belt states.

From Russia I know it’s mostly by rail and some by ship, too – and all russian main lines are already electric.

It looks like this:

https://jamestown.org/wp-content/uploads/2018/04/Russian-Coal-Train-EDM-April-3-2018.jpg?x44080

Coal is so old industry – I hope we can phase it out some time. It’s always dirty, no matter how much you do.

Ron,

We will see, the US has developed its oil resource more aggressively than any other nation on the planet, if there was going to be a Seneca cliff, we would have seen it in the US. If we are going to claim a 3.2% decline in output is a Seneca cliff, then yes there will be a “cliff”, but this strikes me as more of a wheelchair ramp than a cliff.

Dennis , USA peaked for onshore production in 1970 . 52 years ago was there horizontal drilling ? I don’t think so . In that case it followed the Hubbert curve(cliff) . Now all that is left from onshore is 3.5mbpd from L48 and 0.4 –0.5 mbpd from Alaska . L48 is mostly stripper wells . They don’t have a cliff because they are the tail . This is my understanding of the situation . There will be no Seneca Cliff because the conditions for this are long past .

We will see, the US has developed its oil resource more aggressively than any other nation on the planet, if there was going to be a Seneca cliff, we would have seen it in the US.

I am sorry Dennis but you just don’t seem to understand the whole horizontal well infill drilling process. You cannot do it in shale because each well has its own tiny reservoir. It’s source rock, not a sandstone or limestone reservoir. Also, such infill drilling does not lend itself to deep offshore.

What they are doing in Saudi Arabia, Russia, and other nations, especially the Middle East is creaming the top of the reservoir, pulling the oil right off the top of the reservoir instead of lower where the water cut is much higher. But eventually, the water hits the top of the reservoir, then you have your Seneca Cliff.

This is a process that is necessary only in giant and supergiant fields. We just don’t have any of those in the USA anymore.

Ron,

Note that horizontal wells have been used in the US since the 1980s, and I agree that for most of the history of the US oil industry they were not a factor.

Your theory sound reasonable, can you cite any onshore regions where we have seen a Seneca cliff in output that have not been the result of a war or political turmoil that has disrupted most new investment in the oil industry in that region?

Off shore is a bit different because the expensive nature of the projects results in a sharper end of life (there are no stripper wells for deep water off shore oil production), for off shore production a Seneca cliff like production profile is entirely possible. Note that Mexico is sometimes though of as a good example of a Seneca cliff type output profile with the crash of Canterell. For Mexico as a whole from 2005 to 2019 average annual decline in output was about 4.4% (using least squares fit to annual data for that 15 year period). Doesn’t seem very cliff like to me.

United Kingdom is a better example where average annual production fell by 8.2% from 1999 to 2014. That is pretty steep, though if it were a ski slope, I would call it a beginner slope and not really a cliff.

can you cite any onshore regions where we have seen a Seneca cliff in output that have not been the result of a war or political turmoil that has disrupted most new investment in the oil industry in that region?

No, not yet. The point is, it is about to happen in Western Siberia. And… Ghawar… and perhaps is a few of Saudi’s other super giant fields.

Ron,

I will wait for evidence, I do not doubt there will be decline, I doubt a “cliff like” decline profile. Can you define a Seneca cliff in terms of average annual decline rate? Maybe 30%?

The gradual shift of discussion from date of peak oil to decline rates of oil supply is an indication of the time in history.

The Seneca cliff would be applied to a field, not a nation. And no, it would not be 30%. 10% would be a pretty stiff decline, as opposed to the 2% they reached by infill drilling.

Dennis

This tracking company (I do not subscribe) has repeatedly claimed that Iran is exporting much larger volumes than reported and has evidence of cargoes arriving in China with false origin documentation.

https://tankertrackers.com/

Lights out,

Are they saying how much more? If they are correct then World output is higher than claimed, I just assume reported World output by the US EIA is roughly correct (though they seem to under report Russian and Canadian output due to differences in how pentanes plus [C5 plus] from natural gas processing is accounted for, the EIA excludes this from C plus C and most other national agencies correctly include this in total C plus C produced). EIA data is far from perfect, but is the best monthly World output data that is readily accessible.

https://www.eia.gov/international/data/world/petroleum-and-other-liquids/monthly-petroleum-and-other-liquids-production

I have oft commented that Iran is producing all it can and shipping all it can . They are masters of deception . A country does not survive 42 years of sanctions without knowing and learning new tricks daily . Just this year they sent 3 tankers of gasoline and diesel to Venezuela right under the nose of Washington . Washington plays blink, blink because the alternatives are closure of the Strait of Hormuz , war against US proxies KSA and Israel .

The same goes for Iraq . They pump all they can but from 2020 electricity is becoming a constraint to raising production . The oil produced in Kirkuk ( Iraqi Kurdistan ) is underreported and smuggled to Turkey big time . Erdogan and his family run the show .

And talking about Kirkuk ,

https://oilprice.com/Geopolitics/Middle-East/Islamic-State-Attacks-Iraqi-Oil-Field.html

Dennis

In my previous US post, I wrote the following.

From April to June, OPEC added 1,100 kb/d. Using an approximate 85 – 15 split for OPEC and the remaining members, of the 2,100 kb/d, OPEC would add 1,800 kb/d and the members 300 kb/d. So for July we should expect OPEC to add close to 700 kb/d since they have already added 1,100 from April. This will bring their output in July close to 26,700 kb/d.

Below is my best guess for which OPEC countries will supply the expected 700 kb/d.

Guesstimate. ——————— July Actual Increase

Saudi Arabia 300 kb/d ——— 497 kb/d

Kuwait 150 kb/d. —————- 42 kb/d

UAE 150 kb/d. ——————— 42 kb/d

Iraq 100 kb/d. ———————- 56 kb/d

Another article I saw later indicated that the actual July increase could have been 760 kb/d. So OPEC under produced by 100 kb/d in July, since their increase was only 637 kb/d.

Looking at the above numbers, we can see which countries are not meeting their targets. Clearly SA raised their target as part of the UAE compromise and I think they will get their output back to more than 10,000 kb/d.

Why are Kuwait, UAE and Iraq so far below their potential. Not sure about Kuwait and UAE. However, I recall reading that BP and EXXON were trying to get out of their Iraq contracts. They may be holding production back or maybe the fields aren’t as productive as they originally thought. Other issues could be pressing.

Going forward, we will see how OPEC meets its 400 kb/d increase from August to December. This could provide a clue as to where the spare capacity is in OPEC.

If we look at “big 4” OPEC producers from 2013-2018 (before they cut output in 2019 and 2020) we can see the trend in their output over that period by applying least squares linear regression on the Jan 2013 to December 2018 data, the CTMA (centered twelve month average) is shown simply for reference it is not part of the regression. The trendline is projected to 2025 which would lead to about 24000 kb/d in 2025, the pandemic interruption likely reduces this growth by 1500 kb/d so I would expect perhaps 22500 kb/d in 2025 from these 4 OPEC producers, if the 2013-2018 trend continues. No doubt there are differences, the important one being oil prices in 2022-2025 that are considerably higher than 2015 to 2018. Note also that the peak 12 month centered average output for these 4 nations was 20483 kb/d in Sept 2016.

Annual average increase in crude output for the big 4 was 517 kb/d each year on average over the 2013 to 2018 period (6 years or 72 months). See chart below.

Dennis

Are you seriously expecting the “big 4” trend line to continue with only a small blip attributed to Covid?

Lightsout,

No, I do not know the future. Note that many show evidence of declining output in the past as suggesting future decline, showing the 6 year trend of increasing output is no different. I do not think that I said that I expect the trend to continue, I said that if it were to continue, this is what output might be. When there is less demand and output decreases, rig counts decrease. Also note people claim the increase in rigs indicates a problem, now it is the decrease in rigs indicating a problem. Seems many are predisposed to citing any evidence (even if it contradicts previous claims) as indicating a problem. I am not buying it, rigs simply reflect operating companies capital spending plans based on current and expected future market conditions.

Ovi,

Why would we expect that nations producing 3 times less than Saudi Arabia would see increases that are half as large?

June output

Saudi 8906

UAE 2681

Kuwait 2383

Iraq 3921

% increase July increase/June output

saudi 5.6%

UAE 1.6%

Kuwait 1.8%

Iraq 1.4%

Saudi increase is larger because they cut an extra 1000 kb/d of output below their quota.

Your estimate had Saudi increases of 3.37% above June output, if the other big producers were to have increased by a similar percentage UAE would be up by 90 kb/d, Kuwait by 80 kb/d, and Iraq by 132 kb/d.

My reading of the media was to expect all OPEC to increase by about 400 kb/d each month or about 1.2 Mb/d per quarter. That would get them to about 28 Mb/d by the end of the year and to 30 Mb/d by the middle of 2022, they are being careful to ramp up output slowly and not tank oil prices. I doubt they will be able to reach 30 Mb/d by mid-2022, unless they are able to increase capacity more quickly than I have assumed.

Dennis

The 400 kb/d OPEC plus monthly increase starts in August. July was the last month of the first agreement and OPEC was 760 kb/d short of their first agreement target. I had estimated 700 kb/d. Actually they could have added 760 kb/d in July and be in complaince. They ended up 100 kb/d short of their target, possibly more.

“Moving to supply, and we are starting to get preliminary OPEC production estimates for July. According to a Reuters survey, OPEC output increased by 610 Mbbls/d MoM to 26.72 MMbbls/d, which is the highest output from the group seen since April last year. The increase was still below the 760Mbbls/d they could have increased by (including the return of voluntary cut volumes from Saudi Arabia). Unsurprisingly, Saudi Arabia saw the largest increase over the month, with output growing by 460 Mbbls/d.”

https://think.ing.com/snaps/the-commodities-feed-opec-supply-grows-in-july

(An aside. Parsing the statement above, I am wondering if OPEC could have produced more. The base for the early 26.72 Mb/d estimate was for adding 0.610 Mb/d to 26.11 Mb/d to get 26.72 Mb/d. So if the increase could have been 0.76 Mb/d, then OPEC’s July output could have been 26.87 Mb/d, [26.11 plus 0.76] instead of the reported 26.66 Mb/d, 200 kb/d short of target.)

Since all of these countries have spare capacity they could all increase to their agreed limit. This is not a question of percentage, it is a question of their shut in spare capacity since they are all below their pre-pandemic levels.

That is the basis for my question. Why was their output increase so small. For instance the UAE complained that they should be allotted more, yet they only produced an extra 42 kb/d. Similarly for Iraq and Kuwait. Only SA completed their return of their earlier unexpected 1.0 Mb/d cut to the market.

Ovi,

Some OPEC and OPEC plus producers were supposed to produce less to bring their overall cumulative production in compliance with the past quota agreement by September 2020. I cannot find the details of the quota agreements, but perhaps that is the reason output was less. Also note the NY Times on June 1 said total OPEC plus output would increase by 840 kb/d in July, but that is all OPEC plus. The June increase was supposed to be 700 kb/d. Unfortunately we don’t have the data for the “plus” part of the equation so this is difficult to track. Reportedly OPEC plus raided output by 750 kb/d in July, so 90 kb/d short of expectations in early June. Also as a group, OPEC plus produced 106% of their target, so some members are still over producing, Libya, Iran and Venezuela are exempt from quotas.

Ovi,

I have this backwards, compliance was 106% do they held back 6% more than the agreed quota levels, but this may be nations making up for overproducing early in the quota agreement to bring their overall cumulative output in compliance with the original quota agreement. Unfortunately, OPEC is not very transparent about the specific targets.

Article below details OPEC plus overproduction above quotas (cumulative totals) through March 2021.

I found quotas at link below

https://www.opec.org/opec_web/static_files_project/media/downloads/15th%20ONOMM%20-%20Production%20adjustments%20table.pdf

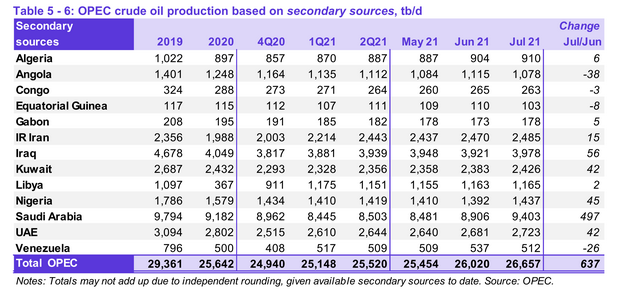

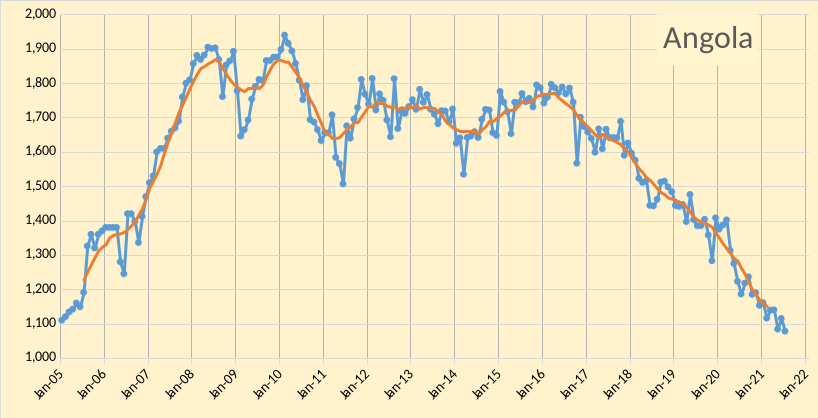

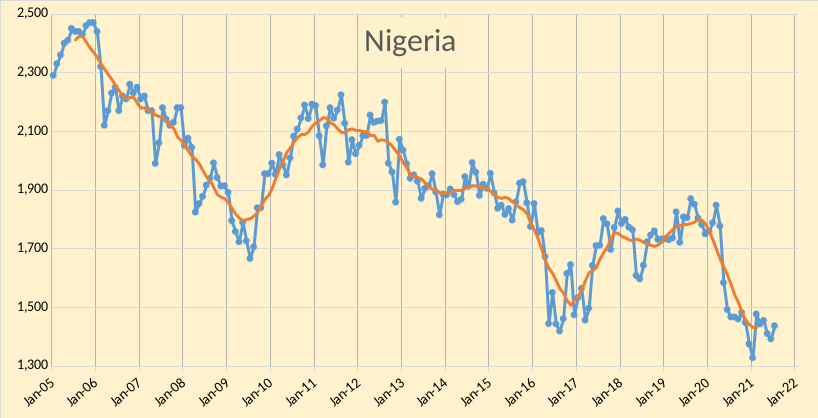

Overall OPEC 10 (excludes Iran, Venezuela, and Libya) output in July was 22495 kb/d and the quota target was 23033, so output was short of quota by 538 kb/d. Of this total Angola was short by 241 kb/d and Nigeria was short by 142 kb/d, for a total of 383 kb/d. the other 155 kb/d is probably individual nations reducing their output below quota to bring overall cumulative output in compliance with the quota agreements.

Much of the shortfall is Angola and Nigeria where perhaps output is in permanent decline (I expected as much from Angola, but thought Nigeria might recover, though there are political struggles in Nigeria and a lack of new investment as a result).

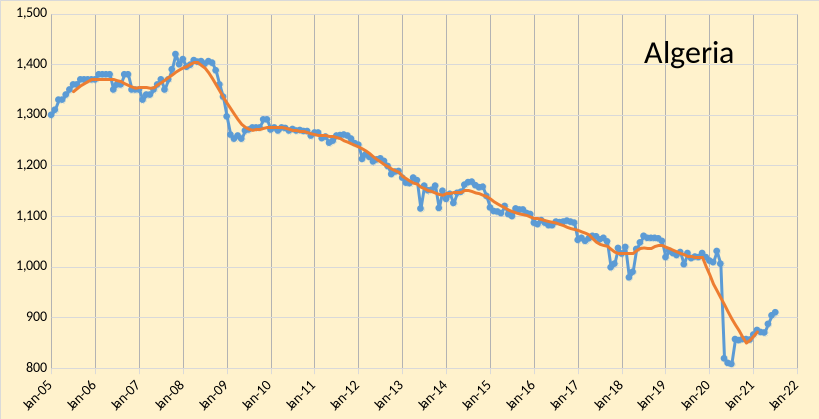

The group of declining OPEC nations without sanctions or civil war over the 2013 to 2018 period are 6 in number. They are Algeria, Angola, Republic of Congo, E. Guinea, Gabon, and Nigeria. Over the Jan 2013 to December 2018 period these nations saw an average annual decrease in crude output of 123 kb/d per year over the 6 year period. The least squares linear regression on the 72 months of data is projected forward to 2025. Output would be about 4100 kb/d at the start of 2025 if the 2013 to 2018 trend had continued. The pandemic dropped output of these 6 nations below that level to about 4000 kb/d and we may see output stablize at that level as some nations (Algeria and Nigeria) increase their output as quotas allow while the other 4 nations may see continued decline offsetting the increases from Algeria and Nigeria.

Do you think really that Nigeria and Algeria will be able to produce more than they do currently?

Jean-Francois,

Yes, mostly Nigeria, Algeria will probably be up another 100 kb/d and Nigeria about 300 kb/d, both have reduced output due to OPEC cuts since early 2020 when OPEC got more serious about output cuts in response to the pandemic.

Revised my thinking on Nigeria, they have been producing significantly under their quota for past 2 months, so it looks like they are struggling to increase output, this may be due to lack of investment due to political turmoil there.

Dennis ,places like Libya , Nigeria will always be in turmoil so to expect anything from these is wishful thinking . Also regarding Algeria it is mostly NGL ( I think 80%) . Algeria is like Qatar , mainly gas very little oil .

Well, the gas production is also decreasing.

Hole in Head,

The OPEC monthly oil market report reports crude output from the OPEC nations, it includes neither NGL (C4, C3, and C2) or condensate (C5). In July Algeria produced 910 kb/d of crude oil according to secondary sources, see figure 2 in the post. Also in the comment above I was talking about Angola, if you meant Angola, they produced 1078 kb/d of crude oil in July, also in fugure 2 of the post. Algerian output has increased from 808 kb/d in July 2020 to 910 kb/d in July 2021 and they are producing almost exactly what their quota allows. So Algeria may indeed return to their previous level befor the pandemic and Libya has already done so, but I agree they will remain unstable and Nigeria probably will also. I don’t really expect big increases from the group of decliners, Algeria may return to pre-pandemic levels, and it looks like Nigeria will not, difficult to foresee.

Nigeria may bump along at current level for a while or may continue to decrease as they did from 2013 to 2018.

As to significance of hydro power in Iran and Iraq, in 2020 for Iran 21.2 TWh of hydropower wer produced and for Iraq, 2.5 Twh of hydro power electricity were produced. Total generation of electricity in Iran in 2020 was 331.6 TWh and for Iraq in 2020 131.3 TWh of electricity was generated. Hydro provided about 6% of Iranian electricity in 2020 and about 2% of Iraq’s electricity in 2020.

The hydro power could be replaced with oil or natural gas fired electricity, or with solar or nuclear power.

Dennis , your comment was about Algeria and Nigeria , so I posted accordingly . Angola is not in the picture . Regarding Algeria IIRC a comment(lament) by a top man of Total ( they own and run the fields) that they were getting low prices because their output out of Algeria was not crude oil but NGL’s .

As to % of hydro in Iran and Iraq , the % is immaterial . For countries that are in deficit of a critical resource additional shortfall has a compounding effect . Anyway if the Iraqis say that Iranians are not supplying them electricity and the Iranians say they themselves are short because of drying rivers that feed their dams ,then I am the last one to argue . It is from the horse’s mouth .

Regarding mitigation , the solution are known but ” easier said then done ” especially in the political and economic conditions that prevail in both the countries .

Hole in head,

The US sanctions on Iran are a bad idea, lack of hydropower is a problem, but it is a minor source of electricity, especially in Iraq, perhaps in Iran where it is a larger source, it has reduced the ability to export electricity to Iraq.

Algeria probably produces a significant amount of NGL, but the numbers I focus on is the crude output reported by OPEC.

According to BP in 2020 Algeria produced 233 kb/d of NGL and 1098 kb/d of C plus C. I ignore the NGL and focus on crude reported by OPEC or C plus C reported by the US EIA. You are correct that Algeria does produce a lot of natural gas, but in 2020 they were the 17th largest producer of C plus C in the World. They are somewhat similar to Qatar in that they produce about the same amount of crude plus condensate (over 2011 to 2020 Qatar produced about 7% more crude than Algeria), but Qatar produced more than double the natural gas that Algeria produced over the 2011 to 2020 period.

Tks , Dennis .

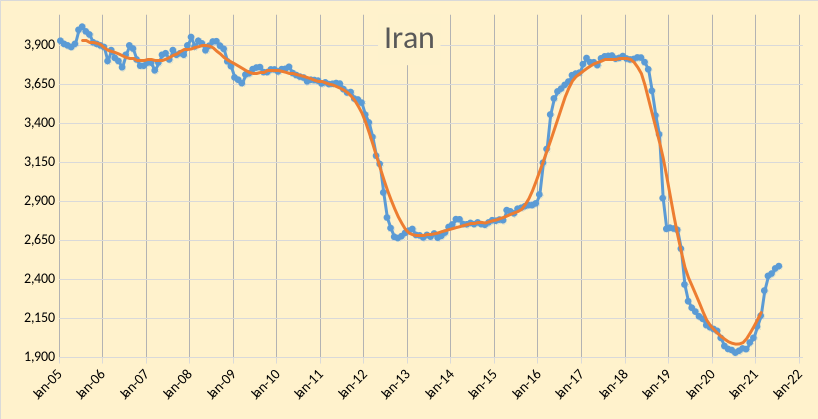

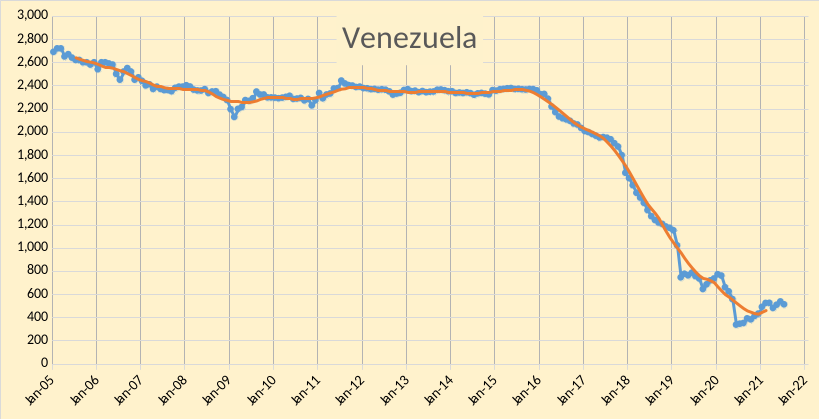

A final group of 3 OPEC nations have been affected by political turmoil, civil, war, and sanctions (none have experienced all 3 problems, but all have been victim to 2 of these three problems). Output has fluctuated quite a bit in Iran and Libya, Venezuela has mostly seen a steady decline in crude output from 2016 to 2020 from 2400 kb/d to about 600 kb/d (Jan 2020). For the period from July 2017 to July 2021 Venezuelan output fell by about 1401 kb/d.

The peak for these three nations was in July 2017 when centered 12 month output was 6541 kb/d, if we subtract the Venezuelan fall in output from July 2017 we get a potential increase in these three nations of 5140 kb/d (this does not include the 350 kb/d increase in Libyan output from July 2017 to July 2021, but assumes Iranian sanctions are lifted.

For all of OPEC we would have 22500 kb/d from big 4, 4000 kb/d from 6 declining OPEC nations, and 5140 kb/d from the troubled 3 OPEC nations for a total of 31640 kb/d by Jan 2025, if Iranian sanctions were lifted. Without sanctions relief fro Iran the 5140 kb/d estimate becomes 4162 kb/d (output of these 3 nations in July 2021) for a total OPEC output of 30662 by Jan 2025 and assuming the trends from 2013 to 2018 in the big 4 and declining 6, continue from July 2021 to Jan 2025. Higher oil prices would make these estimates conservative.

A final note is that the OPEC decrease in output after 2017 is largely explained by the steep drop in output from this group of 3 nations from Sept 2017 to July 2019.

Chart below for troubled 3.

Looks to me like a long plateau at 6 mb/d for these three countries, IF they get more stable. Not even enough to offset the decline of other countries that are in decline.

West Texas Fan club,

I think for these 3 it will be more like a plateau at 5400 kb/d due to a drop in Venezuelan output. Note that the big 4 (Saudi Arabia, Iraq, UAE, and Kuwait) will easily be able to offset the small decline from the 6 declining nations (Algeria, Angola, Congo, E.Guinea, Gabon, and Nigeria). The big 4 increased output on average by 500 kb/d from 2013 to 2018 while the declining 6 had their output fall by about 125 kb/d, note that if Iran never has sanctions removed then the 3 “troubled” OPEC members will see a plateau at about 4000 kb/d.

Iranian output could increase by 1400 kb/d with an end to sanctions. At some point this may happen if oil prices reach $100/bo or more.

Environmentalists Slam Biden For OPEC Plea

Environmentalists have lashed out at President Biden after he called on OPEC to boost oil production in a bid to arrest the price climb at the pump.

“If Biden’s going to urge OPEC to increase oil production one day after the UN’s ‘code red’ climate report, he may as well come to California and personally light more wildfires,” the director of the Center for Biological Diversity’s Climate Law Institute, Kassie Siegel, told The Independent.

Yeah right, when I want to know what environmentalists are thinking oil price dot com is my go to place.

Quo Vadis ? Now what ?

https://www.zerohedge.com/markets/bidens-abysmal-day-just-got-worse-opec-snubs-plea-more-oil-says-wont-pump-more

Zero Hedge is a Russian propaganda outlet. They intentionally spread misinformation, so take their output with a grain of salt.

https://www.rand.org/content/dam/rand/pubs/research_reports/RR2200/RR2237/RAND_RR2237.pdf

@Ali

No, it’s just a right wing site, not one of the zillion left wing or liberal sites.

A russian propaganda site won’t fight critical race theory – Putins loves critical race theory in the USA, dividing the country instead of uniting it.

Years ago when the term was “in”, it was called a teabag site. That describes it best. They’re conservative, but not 100% pro Trump, too. I think they would like a president like Bush at best.

Yeah, not sure how citing a well known US DoD funded think tank works with pointing out Russian propaganda. We’re okay with American propaganda now?

As the Russians say: trust, but verify. Zero Hedge has a lot (LOT) of bullshit, but now and then it does find that diamond in the rough before the MSM outlets get to it.

And

And

And

Thanks for these Lightsout. The NOCs and the large public oil companies seem to be taking the same path: endgame. Invest little in future production with low CAPEX, large dividends and share buybacks, and act like everything is hunky dory. They’ll be others to blame when prices spike through the roof in a year or two, especially the greens.

It makes sense to me that all oil producers would be cautious. COVID is a huge unknown regarding future demand. Electric vehicles are a huge unknown regarding future demand. Major consumers can’t borrow trillions forever, can they? Also uncertain regarding demand.

We have not drilled a well since September, 2014. I question if we ever will again. Our production has declined, but it hasn’t made sense oil price wise to drill. Now, with all of the uncertainty, our goal is to downsize and ultimately get out.

Has been a very demoralizing 7 years for oil producers. 2018 was decent. Keep in mind our average price for 2021 is still just $52, even though currently our price is $64. That is a big difference. The volatility has been brutal.

I am still surprised Biden asked OPEC for more oil. Besides his policy to transition the USA from oil, it is never a good look for a US President to make such a request from the Middle East and Russia.

“I am still surprised Biden asked OPEC for more oil”

Agree, and much the same with other public statements on this issue by previous presidents.

It seems that these kind of public statements do nothing for bargaining, diplomacy, or market influence.

What Biden wants to communicate is: “Covid is under control, the economy is recovering and we’re returning to pre-pandemic conditions.”

Thats probably complete BS, but that’s how politics work.

Shallow, just for my curiosity:

Are there still spots in such an old field as yours to drill a new well? I would think everything viable is already drilled and the only thing thinking about would be some enhanced recovery stuff.

We have many locations. We drilled 2-4 per year from 2005-2014, except for 2009. Also have drilled a few injection wells.

Logic, due to the numerous geopolitical problem they faced, they have still half of their reserves still intact.

Iran Oil Output Falls To 40-year Low In 2020

Iran’s crude oil production fell to the lowest in 40 years, according to an updated analysis by the U.S. Energy Information Administration.

At less than 2 million bpd, the EIA said, the country’s oil output was affected by both the pandemic, which decimated demand for oil, and U.S. sanctions targeting specifically the Iranian oil industry.

Frugal , from your link ,

“Before the U.S. withdrawal from the Iran nuclear deal and the snap-back of sanctions, Iran was pumping around 2.6 million barrels daily and exporting some 2.5 million bpd, the EIA also said.”

Doesn’t make sense . Iran’s domestic consumption is not 2.6-2.5 = 0.1 mbpd (100000 barrels ) . Doesn’t add up .

Yes there must be a typo in this report unless Iran is importing oil.

They import gasoline and diesel.

Before the US pulled out of the Iran nuclear deal (May 2018) Iran was producing about 3822 kb/d, that was the centered 12 month average crude output in December 2017 (includes average output from June 2017 to May 2018). The low point for centered twelve month average crude output was 1988 kb/d for July 2020 (January 2020 to December 2020). Output has recovered to 2485 kb/d in July 2021 and the most recent centered 12 month average was 2190 kb/d (Feb 2021). The peak monthly output since the nuclear deal was agreed was 3835 kb/d in Sept 2017. If Iran can return to 3800 kb/d with a removal of sanctions (I don’t know if this is possible) that would add roughly 1300 kb/d to OPEC output. If Biden wants more output from OPEC, this is a simple solution, return to the Iran agreement. Of course nothing is simple in international diplomacy.

Dennis , does that infer that they have little to export as of today ? You said that they produced

2.45 mbpd in July 2021 and they have a refining capacity of 2.3mbpd locally OR it could be as Lightsout and I have said that they are producing and selling all they can ? The second argument is difficult to prove since it is all ” off the books” but if the first one is correct then it is a problem also . As a matter of fact if the first is correct then Iran should not be a part of OPEC . What is your opinion ?

Hole in head,

It is possible they are producing more than the secondary sources are reporting, I won’t speculate. I think the secondary sources are probably correct and Iran is exporting very little oil currently, the US sanctions are likely to be hurting the Iranians, I think this was a dumb move by Trump, unfortunately undoing the damage is not easy to accomplish.

It is unlikely that Iran is producing anywhere near capacity, but we won’t really know until sanctions are removed.

Note that I don’t know what actual production of oil is anywhere, I only have the numbers printed in reports, they could be right or they could be wrong, I am just reporting what I read in the Monthly Oil market report from OPEC.

Hole in head,

Iran was pumping about 3.8 Mb/d of crude oil before US left the JPCOA. In 2017 Iran consumed 1677 kb/d of C C NGL and in 2018 they consumed 1717 kb/d of C C NGL (BP data), so roughly consumed 1.7 kb/d before US left nuclear deal, leaving at least 2.1 Mb/d for exports. Actually BP has C plus C for Iran over these two years (2017 to 2018) at about 4300 kb/d and NGL at about 366 kb/d for a total output of 4660 kb/d for C C NGL, that would leave about 2940 kb/d for export according to BP data.

Obviously a typo, see

https://www.eia.gov/todayinenergy/detail.php?id=49116

Great post & comments. Thanks everybody.

Up above there was talk about rapid collapse of the oil industry after peak.

As I indicated, I think that rapid collapse is a very unlikely scenario on a global basis.

But what may be extremely rapid is the change in mentality/psychology, especially as it pertains to security issues and financial behavior [examples- collapse of the Afghanistan 300Kstrong security force, or the 2009 financial crises].

These kind of human mob immediate shifts in mentality can cause extreme instability in the global economy when applied to an issue like peak oil supply. When the times arrives where the global mainstream understanding is that oil has peaked, and especially when oil first becomes harder to for countries to purchase, there may be a rapid panic reaction.

In fact I would very surprised if there wasn’t such a reaction.

What will countries/populations do when they first realize that the oil spigot is starting to close?

Reactions will vary depending on how dependent a country is on imports, and it varies tremendously.

There will a very rapid scramble to arrange priority customer relationship with oil suppliers on a much bigger and desperate scale than we now see (ex China-Iran). All previous alliances will be up for re-shuffle. There will be closed door deals for food supply, essential materials, and security, in return for oil supply guarantees. This will include big promises and big threats, as international ‘diplomacy’ always does.

Governments that are seen as slow to react will be removed- like we have seen in the middle east over the last decade. A big opportunity for authoritarians, nationalists, fundamentalists, and anarchy or civil war. Think Iran in 1979, or Iraq and Syria more recently.

There will be a massive scramble for all thing electric, for example battery manufacturing capacity/material supply . What is now a trickle will become an industrial tsunami. Shortages of solar components and electrical vehicles will likely be severe in most countries. Much worse than we see with semi-conductors this past year.

Countries may have to take drastic financial steps to shore up accounts. All mechanisms will be up for consideration- competitive currency devaluation, pension/social spending rollback, asset seizure. special taxes are some of the things that have happened in past episodes of instability. These kind of things will all be on the table.

I emphasize that some countries are much more vulnerable to these kinds of disruption than others, but the ripple effect on all countries will be very, very large.

While the global oil supply may not fall of a cliff anytime soon. the global mentality may change extremely rapidly.

Hickory,

There are a lot of different ways that things could play out, but keep in mind that the main stream media will not be convinced of peak oil until well after it has occurred (perhaps 5 or 10 years later). In the interrim oil prices will be high and a transition to electric land transport will accelerate as a result, governments may start to digest the realities of the IPCC AR6 report and create policies that accelerate the transition away from fossil fuel. These two forces may lead to demand for oil falling faster than the supply of oil. How does OPEC plus react to such a circumstance? My guess is the cartel falls apart and we see large producers start to develop their resources more agressively in an all out war for market share in the shrinking oil market. Oil prices could fall very steeply in such a scenario driving high cost producers (tight oil, deep water oil, newly developed oil sands projects, and Arctic oil) from the market with most oil production coming from the middle east former OPEC producers and Russia. We might see oil prices stabilize at $25/bo in 2021$ by 2045 under such a scenario.

Bottom line, we see very different futures for the oil market.

Agreed- there are lot of ways things could play out. I was describing some of the possible ramifications of a sudden change in global sentiment after peak oil is felt. Global sentiment is not rooted in facts and reality all that well.

Regarding “main stream media will not be convinced of peak oil until well after it has occurred (perhaps 5 or 10 years later)’

I see it differently- The global perception of the arrival of peak oil could happen very quickly, maybe well before it even has occurred. I acknowledge that it will take 5-10 years for the charting to clearly depict an irreversible drop in the monthly trailing averages. But human reactions to the perception could be extremely rapid.

Regarding messaging- there may come a time when large producing companies or countries decide it is in their best economic interests to proclaim peak oil supply, as a way to boost their bargaining power. That message will have a big effect on sentiment. Ron has been often repeating the message that the Russians have proclaimed their peak, for example.

When other big players start saying the same thing loudly in the media- it won’t matter whether or not the charts agree. It will be perceived as true, or at least imminent.

5-10 years after peak is 2023-2028 so really any time now. Unless of course Dennis gets his 30 trifectas in a row and we squeak out a new peak in 2023-24.

Stephen,

You are way off on your odds. I would say it is less than one in 4 that there will not be a new centered twelve month average (CTMA) peak in World C plus C output. You seem to believe a transition to EVs will occur much more rapidly than is likely. We don’t produce that many EVs now Worldwide and don’t have the battery manufacturing capacity to produce a lot more at present.

It will take time for the transition to occur and demand for oil will quickly rebound to the 2019 level, probably by 2023 at the latest.

High oil prices are likely to create a resurgence in capital spending in the oil industry and the increased demand will be met with increased supply of crude plus condensate. The main unknown is at what oil price will supply and demand match in 2028. Will it be $100/bo for Brent in 2021$ or will it be $150/bo? My guess is the middle of this range at about $125/bo in 2021$.

There are many that argue for an undulating plateau, even if Ron is correct that 2018 is the final peak, if we see World oil output approach that peak then we might be on a plateau that can be maintained many years or might see a new peak in any future year. I think the peak will fall in 2025 to 2030 and until we see steady decline for 5 to 10 years beyond that we won’t have much consensus on a final peak being reached.

If my guess is correct that puts us at 2030 to 2040, with a best guess at around 2035 for this realization. It is likely (perhaps 60% probability) that by 2035 there will have been enough EVs and plugin hybrids sold that demand for oil begins to fall more quickly than the supply of oil is falling and drives oil prices lower to reach a market clearing price. This will make OPEC fall apart and may well lead to a price war and supply glut.

It will be all about peak demand rather than peak supply at this point and the oil industry will become a shell of its former self within 5 to 10 years (so 2040 to 2050 or so).

It is all speculation of course, but that is how I see it playing out at this moment in time.

Dennis , the key is exportable surplus oil . The world is depending on OPEC 5 + Russia (Total 6 countries ) to save their butt . Out of 6 we have 2 (Iran and Iraq ) on crutches and all are past peak . Skating on extremely thin ice . The collapse of Kabul is well defined as ” Nothing happened for 20 years and then 20 years happened in 20 hours ” . Downhill momentum catches speed real fast .

Hole in head,

Doubtful that as a group these nations are past their peak. Time will tell who is correct on this question. Either of us claiming that our claim is correct is silly, trends can change, direction unknown.

Also exportable surplus is less important than total output. You take US out of your calculus, but more output from US means less net imports to the US leaving more oil for other nations.

So US, OPEC big 5, Russia, Canada, Brazil, Norway, and China, in fact the top 20 World producers will be important. They have produced about 87% of cumulative World output of C plus C from 2011 to 2020.

See comment at end of thread for chart.

I do see EV adoption adding great uncertainty, like Shallow Sand started above, in addition to the Covid picture, the debt bubbles in consuming nations, the civil wars in producing nations, the unknowns about how much oil is left underground in KSA, Russia, the Permian, etc. You believe in a stable world that I do not think exists any longer and won’t again in our lifetimes. If oil prices are high and then they are low the next year, CAPEX will not increase like you expect it to. Your assumptions are widely optimistic. There’s only a 10-20% chance everything holds together long enough to reach a new peak imho. Oil prices that are high enough for long enough to induce significantly higher investment will be highly destabilizing economically, while simultaneously inducing a much more rapid effort to transition to EVs, which will immediately dampen investment sentiment. There’s just no way your oil price scenario is possible, and without that, the CAPEX won’t be there.

Stephen Hren,

The problems you suggest have been with us a long time 50 years or more, you think the future will be much different than the past (much worse), I think it will be much the same (progress, backslide, etc) there will be problems, some of them will be new (unknown unknowns), I cannot predict unknown unknowns, some of them may help and others will hurt and there will likely be some of each.

An assumption that only bad things will happen is just as bad as an assumption that only good things will happen, my guess is that there will be some of both as has been true for all of history. Perhaps the future will be completely different from the past and every event will only have negative consequences, this seems statistically unlikely in my view. I will wait and see what happens.

I generally don’t think of reality as a 3 sigma event, your perspective may be different.

Oh and your assumption that I believe in a stable world is incorrect. A model is a simplified expression of the World where stable assumptions are made to make the math easy as well as the model easy to understand.

Oil prices have been unstable since 2004, has capital investment stopped? Generally we have seen reduced capital investment in response to low oil prices.

As to high oil prices resulting in instability, Brent oil prices were over $120/bo in 2020 US$ for most of the period from early 2011 to mid 2014. Today the World GDP is much higher than that period so we could likely afford $130/bo in 2020 $ with little problem. World real GDP growth over that high oil price period was around 3% per year.

Will we see stable oil prices at $130/bo, of course not. I use stable oil prices as a model simplification to represent average oil prices over a period. So when I use an $80/bo maximum oil price, one could easily add a random fluctuation in oil price up and down by 20% or more and little would change in the model. I expect there will be oil price volatility, though I expect it will be in the range of $80 to $120/b for 3 month average oil prices. I use the $80/bo maximum oil price as a very conservative assumption for real oil prices that are likely to be a minimum of $80/bo in 2020$ from 2022 to 2033 for any 12 month average. I would say $100/bo for average Brent oil prices for the period from 2022 to 2033 with fluctuations from 80 to 120 per barrel would be a more realistic model.

Hickory,

Yes sentiment can change very quickly, I agree. I just disagree on when that is likely to occur. My expectation is 2035 or so about the time when the peak will be seen as due to a lack of demand rather than a lack of supply. It may not be a big problem for the economy in general, but it will be a bad time to be invested in the oil industry. Those with foresight will sell out at the peak in 2028 or so when oil prices may be close to their maximum, maybe 2030 at the latest. Those who wait may be left with stranded assets.

Ovi , I know they had a Rupee payment agreement with India for crude before the Trump sanctions . Their main buyer was Reliance but they stopped . They have a lot of refining capacity . They shipped gasoline and diesel to Venezuela against their gold .

https://www.tehrantimes.com/news/440117/Iran-s-refining-capacity-reaches-2-3m-bpd

I think WTI is heading back to $60 ish where there is support from buyers but if that gives way it is back to the low 50’s

50$ will finally collapse shale. All giants will speed their exit – they are already leaving, and production will decline a few mbpd.

Big offshore will slow down, too, and the result will be a supply crisis.

Cool. Let’s see if WTI hits $60 before it hits $70. Currently $66. If it hits $60 first I might take your US$ predictions more seriously…

Frac spread count through Aug 13, 2021, frac spread count is 238 up 3 wow but down 5 from 3 weeks earlier. Up 168 from one year ago when count was 70.

Frac spread count was 245 on March 27, 2020 and it was 319 on Feb 14, 2020 (highest value on chart below. On Jan 17, 2020 the count was 359 (highest in 2020). The peak frac spread count in 2019 was Jan 26 at 463, and for 2018 the peak was June 22 at 503, the 2017 peak was 437, 2016 peak was 239, and 2015 peak was 405 in January. No data before 2015.

Blue hydrogen, (hydrogen from natural gas), far worse than just burning the gas.

Blue Hydrogen Worse Than Natural Gas: Study Bold mine

Blue hydrogen, the kind that involves fossil fuels combined with carbon capture, could be worse for the environment than natural gas or even coal, a new study has suggested.

The study, conducted by researchers from Cornell University and Stanford, also suggested that the carbon footprint of blue hydrogen is as much as 60 percent higher than that of burning diesel for heating, Energy Live News reports.

“Politicians around the world, from the UK and Canada to Australia and Japan, are placing expensive bets on blue hydrogen as a leading solution in the energy transition,” one of the authors, ecology and environmental biology professor Robert Howarth from Cornell University, said in a statement.

“Our research is the first in a peer-reviewed journal to lay out the significant lifecycle emissions intensity of blue hydrogen. This is a warning signal to governments that the only ‘clean’ hydrogen they should invest public funds in is truly net zero, green hydrogen made from wind and solar energy,” Howarth also said.

The study’s authors have suggested that because of the enormous amounts of natural gas that blue hydrogen requires, its emission footprint is bigger than gray hydrogen, which does not use carbon capture at all. The emission footprint also does not depend on the specific carbon capture and storage technology used.

Ron,

Makes sense. If you are going to burn natural gas and capture the carbon, better to not waste energy converting to hydrogen. That is pretty obvious.

The use of hydrogen as a storage medium is to utilize excess capacity from wind and solar when more is being produced than can be utilized. The “free” electricity which would just be dumped to ground in the absence of some storage method would be used to produce hydrogen which could be stored and burned later, other possibilities are large stationary batteries (these do not need to be lithium ion for stationary storage). Whichever method is cheapest and does the least amount of envoronmental damage should be encouraged with proper policy measures, or just let the market decide and have good regulation of the industry.

I wonder if you meant to put this in the Open thread perhaps?

Feel free to move it, I don’t care if my comment gets deleted.

No, I thought hydrogen and natural gas should be part of the energy discussion.

Ron,

I have read several of your comments in this thread and agree with your sentiments about peak oil. I do believe we are heading more towards a SENECA CLIFF.

In researching the collapse of the Late Bronze Age, Ancient Roman Empire, and the Mayan Civilization, what I found quite fascinating is the COLLAPSE PERIOD in all three was quite similar… 10% of the overall period. Thus, the Collapse of Major Empires & Civilizations occurs quickly, not over a slow period of time.

While the PEAK of the Empire may have been for 100 years, the collapse occurs suddenly.

If we assume the same fate to the Modern High-Tech Global SemiConductor Economy which depends upon a massive amount of fossil fuels to sustain itself, the collapse will occur in roughly 25 years.

If we throw a DART at the wall and say the Modern Industrial Revoluation started in 1800 and the peak of Global Oil Production (High & Low EROIs) occurs in 2025, then by 2050… most the global economy will be in ruins.

Lastly, the idea we are going to transition to SMART ENERGY like Wind, Solar, Blue Gas, Green Algae or whatever, will not happen because all those energy sources need OIL-NATGAS-COAL to be possible.

GOD HATH A SENSE OF HUMOR…

Steve

I think China get’s it right. They are working on energy independence, and getting rid of oil and later coal.

No need to maintain a global military presence to protect the oil ways then. Normal trade doesn’t need the same protection than this oil business.

Since China has it’s own chip industry, they can build anything else they need. They can persist even when the west collapses.

You do realize China imports something like 80% of their energy needs right? Normal trade doesn’t need protection because US Navy is still providing that protection. If the US wanted to see China collapse all they’d have to do is go home.

China’s neighbors all of who hate them would see to it that China collapses. Only reason China exists as it currently does is because of US led order. US led order allows anybody to buy and sell whatever they want to whomever they want. Anywhere in the world. World goes back to pre Bretton Woods. Imperialistic world if US ever decides just to go home.

China has never in it’s history been able to breakthrough what they call the first island chain. They can’t even interface with rest of the world without US led order.

China is nowhere near energy independence. And they, like everyone else, are reliant on Taiwan for semiconductors en masse. Good luck invading that place so long as the 7th Fleet and Taiwan’s SDF have anything to say about it.

Top 20 producers of C plus C in the World (lest axis) and World C plus C minus top 20 (rest of world or ROW) on right axis. I do not think trend higher will continue at same slope, but I do expect output will rebound from pandemic eventually and then continue higher at a lower rate of increase (perhaps 300 kb/d on average from 2023 to 2028, rather than the almost 1000 kb/d average rate from 2011 to 2020).

Data from

https://www.eia.gov/international/data/world/petroleum-and-other-liquids/annual-petroleum-and-other-liquids-production?pd=5&p=00000000000000000000000000000000002&u=0&f=A&v=mapbubble&a=-&i=none&vo=value&&t=C&g=00000000000000000000000000000000000000000000000001&l=249-ruvvvvvfvtvnvv1vrvvvvfvvvvvvfvvvou20evvvvvvvvvvnvvvs0008&s=94694400000&e=1609459200000

Dennis, why do I get totally different numbers from you, especially for the “Rest of the World”.

In 2019 before any covid decline set in, the Top 20 declined 47,000 barrels per day from 2018. However “The Rest of the World” declined 671,000 barrels per day from 2018 to 2019.

That was of course a total decline of 718,000 BPD or almost a 3/4 of a million barrels per day the year before the Covid 19 decline.

Interesting to note, that in that same year, 2018 to 2019, the USA increased production by 1,284,000 barrels per day while Iran declined by 1,283,000 barrels per day. Of course, both are in the top 20.

Note: On the chart below the Top 20 is left axis while the Rest of the World is right axis.

Ron,

Are you using crude plus condensate from the EIA international energy statistics?

Perhaps we defined top 20 differently. I used cumulative production from 2011 to 2020 for all nations in EIA database and then sorted high to low.

My top 20 are:

Russia

Saudi Arabia

United States

China

Iraq

Canada

Iran

United Arab Emirates

Kuwait

Brazil

Mexico

Nigeria

Venezuela

Kazakhstan

Angola

Norway

Qatar

Algeria

Oman

United Kingdom

Rest of World is World total minis top 20 listed above (using C plus C only from EIA).

Maybe we used different data sets?

Yes, I am using C+C. But I am using production data for 2019, the last year before the Covid demand hit. Here are my top 20 in order of the highest production.

United States

Russia

Saudi Arabia

Iraq

Canada

China

United Arab Emirates

Iran

Kuwait

Brazil

Nigeria

Kazakhstan

Mexico

Angola

Norway

Qatar

Algeria

Libya

United Kingdom

Oman

That explains it, our top 20 producers are different, ranking on the basis of a single year didn’t seem like the best idea to me.

Yeah, that explains it. My top 20 are the current top 20. And my “rest of the world” includes many nations that have gone into decline in the last decade. And that part, the “rest of the world” is where my chart so radically differs from yours.

Ron,

The difference between the two lists is Venezuela is in my top 20, but not in yours and Libya is in yours but not in mine. Over the period you focus on the difference is significant. Note that the number you quote for rest of world decline from 2018 to 2019 of 671 kb/d is mostly from Venezuela which saw output plummet by 608 kb/d that year. So for rest of World minus Venezuela we saw only a decrease of 63 kb/d. For top 20 we saw a drop in output from 2018 to 2019 because OPEC cut back output in 2019 (this is true even if we exclude Iran and Venezuela which both dropped a lot in 2019).

If Venezuelan output dropped another 608 kb/d they would be producing negative 82 kb/d for average output in 2021, so that is pretty unlikely, they cannot produce less than zero.

Also for your rest of world drop in output of about 3300 kb/d from 2015 to 2020, 1962 kb/d or 59.4% of the drop was from Venezuela.

When we look at your “rest of world” without Venezuela, the average annual decrease from 2015 to 2019 was about 176 kb/d.

For your top 20 the average annual increase in output from 2015 to 2019 was 990 kb/d.

I am confident the top 20 producers will be able to increase their output by more than the rest of the World will see their production drop over the next 5 to 10 years.

Dennis, the Venezuelan decline can be considered permanent. If you have Venezuela in your top 20 producers then it is obviously in error.

I am confident the top 20 producers will be able to increase their output by more than the rest of the World will see their production drop over the next 5 to 10 years.

Well hell, that may very well be the case. But both, the top 20 and the rest of the world have declined a combined 7 million barrels per day since 2018. 1.65 million barrels of that were from the rest of the world. That 1.65 million barrels, plus further decline from them, will not be coming back. So the top 20 will have to increase by 7 million bpd, plus all further decline from the rest of the world, just to break to their 2018 level.

So even if your confidence is well-founded, that will still not be nearly enough Dennis. 2018 was the peak year for world oil production. Get used to it Dennis.

Ron,

I agree the Venezuelan output will not increase and this is the second time I have said it. Should I repeat it yet again?

Most of the “rest of World” decline was from Venezuela as I showed.

Do you think Venezuelan output will decrease by more than the 2020 level of output in the future?

Including Venezuela in your “rest of World” category is silly, a few years ago in 2015 Venezuela was in the top 10 World oil producers.

Of the 1.654 million decline in output for your “rest of world” group, 58% was Venezuela (959 of 1654 kb/d). In 2020 Venezuela’s output was 527 kb/d, so it cannot fall by more than this. After output falls to zero (if it does) it will fall no further.

For your rest of world group output in 2015 was 12368 kb/d and for Venezuela in 2015 output was 2489 kb/d. In 2020 rest of world was 9067 kb/d and for Venezuela in 2020 output was 527 kb/d.

So for rest of world output fell by 12368 minus 9067 or by 3301 kb/d and Venezuela fell by 1962 kb/d, so 59% of the decrease was from Venezuela. Obviously World output fell a lot during the pandemic and it is likely to rebound in 2022, if we only look at 2015 to 2019 rest of world fell by 2318 and Venezuela from 2015 to 2019 fell by 1613 kb/d, so Venezuela was about 70% of the fall in rest of world output over that period.

Rest of world minus Venezuela fell by 705 kb/d (2318 minus 1613), then divide by 4 years to find annual average decline of 176 kb/d. No increase in Venezuelan output needs to be assumed, simply that Venezuelan output remains at 527 kb/d in the future. Or if it continues at the 2015 to 2019 decline rate of 1613/4 or 404 kb/d each year, then Venezuela would be at zero output by 2023 and could not decline any further.

That is the reason it makes sense to exclude Venezuela from “rest of World” decline estimates.