The data for the charts below are from the EIA’s Monthly Energy Review. I will update this post Friday, May 31st with March data for the USA and charts for several states when the EIA’s Petroleum Supply Monthly is published. All data is through February 2019 and is thousand barrels per day.

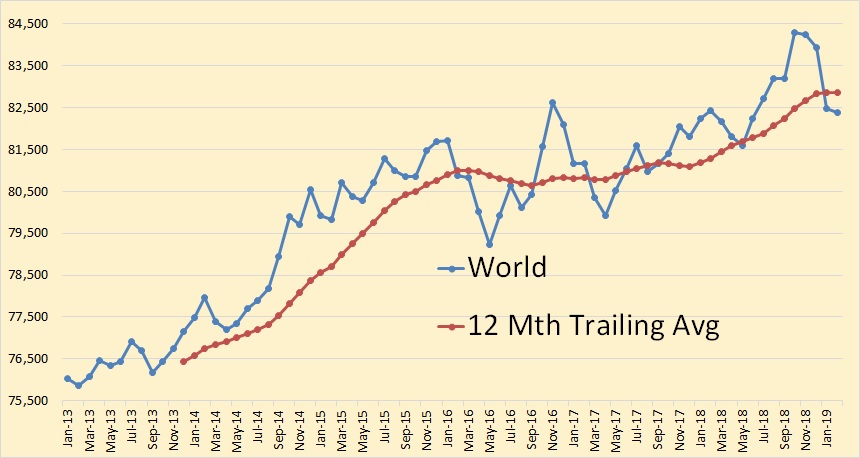

World C+C production was down only slightly in February, dropping only 87,000 barrels per day to 82,389,000 bpd.

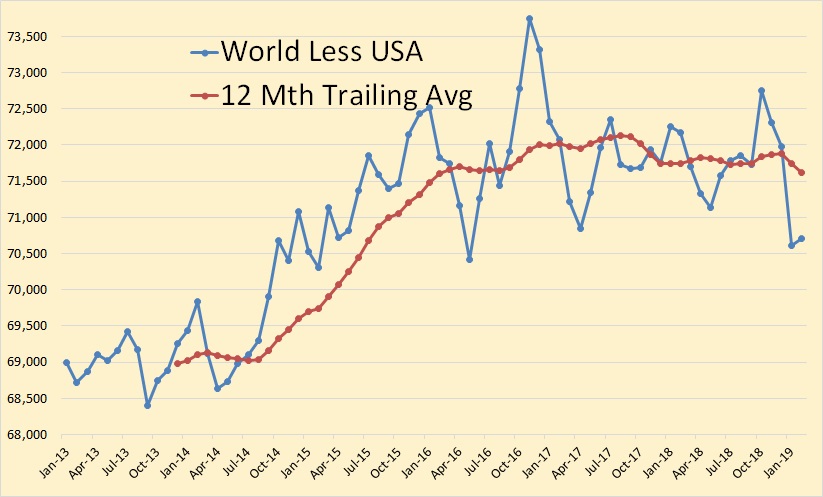

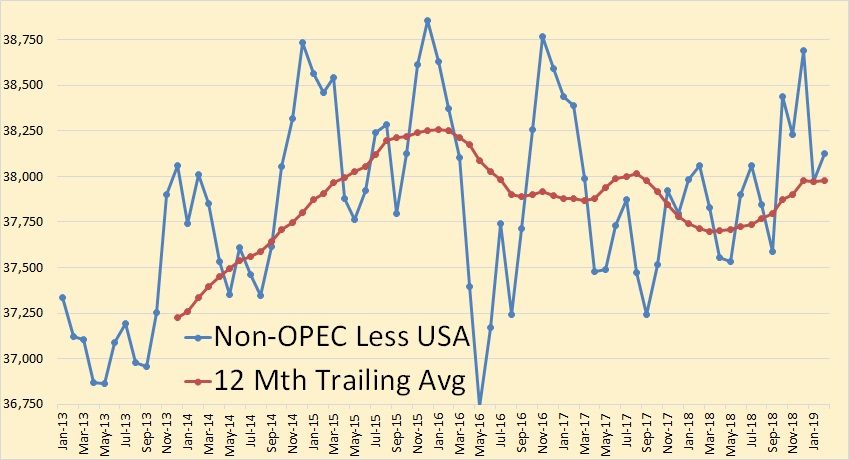

It is my contention that World, less USA peaked in November 2016 with the 12 month average peaking in 2017.

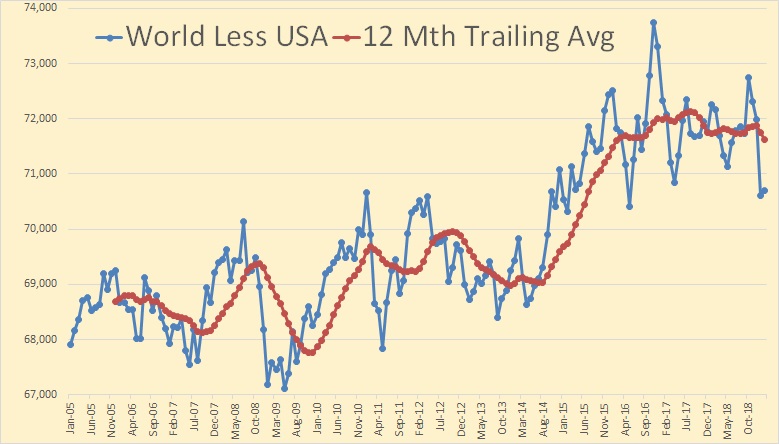

A longer view of things. I am thinking of creating a “World less US Tight Oil” graph. Perhaps I will do that next month.

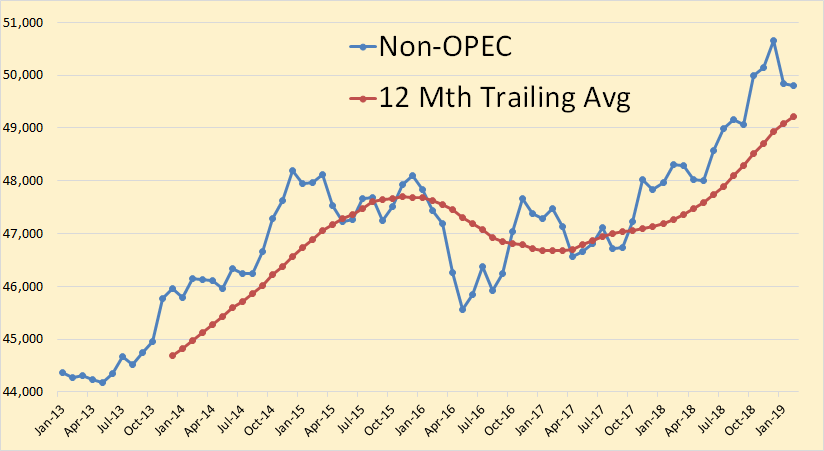

Non-OPEC production was down 36,000 bpd in February.

Non-OPEC less USA peaked in December 2015. The 12-month trailing average peaked one month later.

OPEC is not, and will not, be our savior from Peak oil. It is the Non-OPEC big three.

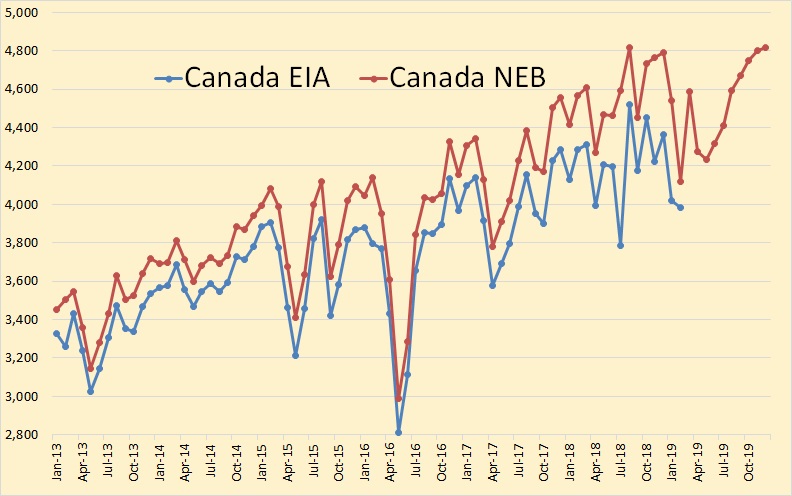

Canada was down only slightly in February according to the EIA. The Canadian Energy Board has them recovering in March but dropping big again in April.

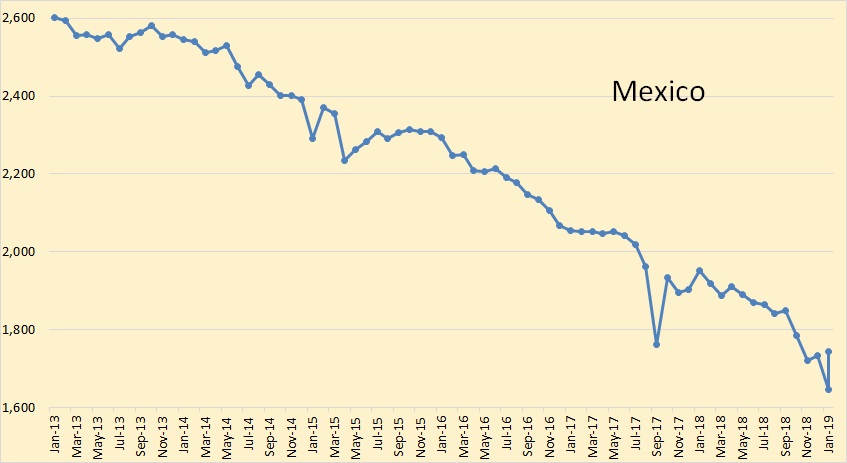

Mexico recovered slightly in February.

China seems to be holding steady after the big decline in 2016.

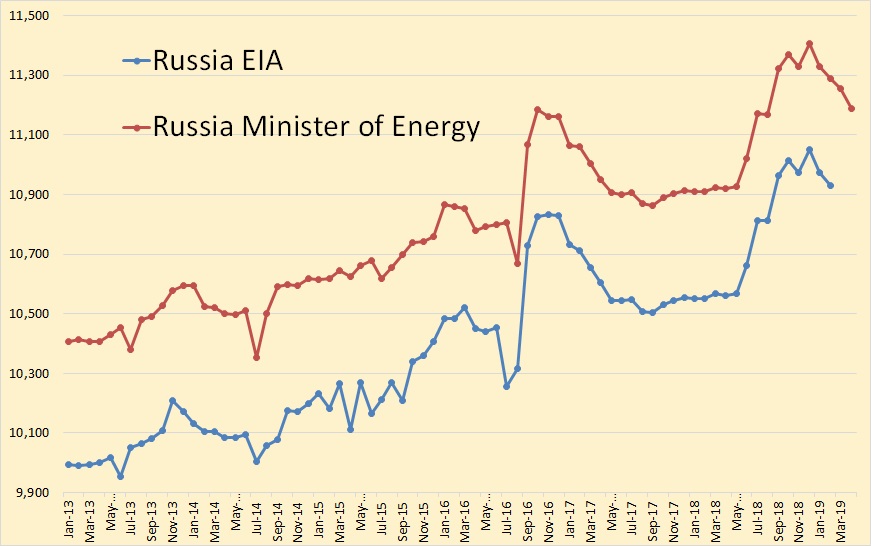

Russian oil according to the Minister of Energy through April. I converted tonnes to barrels using 7.33 barrels per ton. The EIA data is through February.

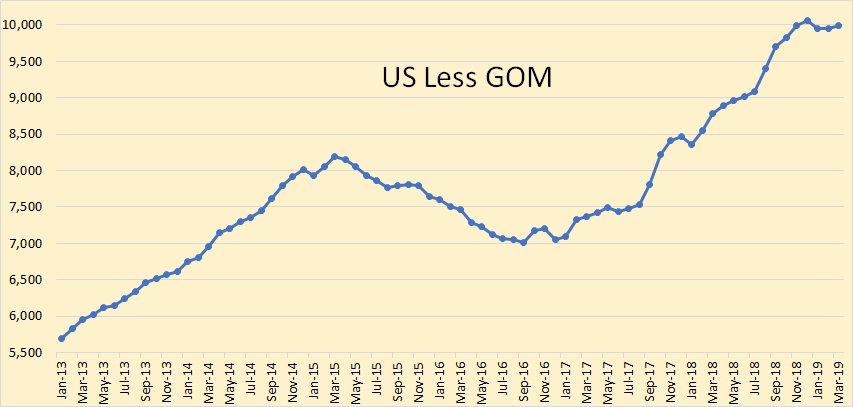

All the USA data below is through March 2019.

The above chart is through March 2019. US production was up 241,000 barrels per day to 11,905,000 bpd. That was after February production was revised down by 19,000 bpd. Production is still below November and December however.

The EIA’s Monthly Energy Review had estimated March production to be 12,110,000 bpd. They were 205,000 bpd too high.

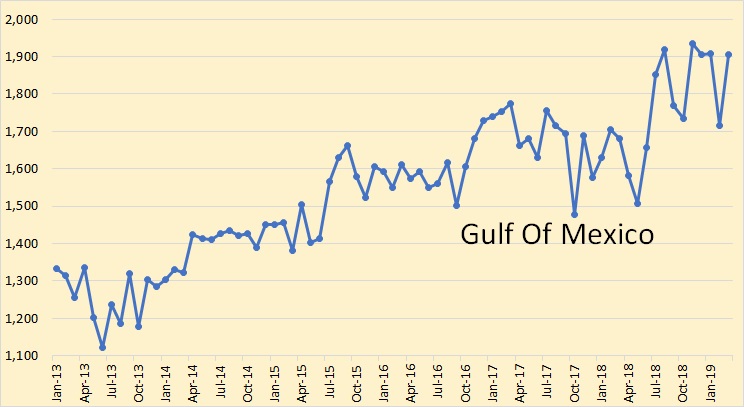

The lions share of the March increase came from the Gulf of Mexico which was up 191,000 barrels per day. USA less the GOM has been flat for 5 months. Does this mean anything?

Ahhh, there’s the problem. The Permian is petering out. Either that of Eagle Ford is pulling things down.

And the Bakken is not doing all that well either.

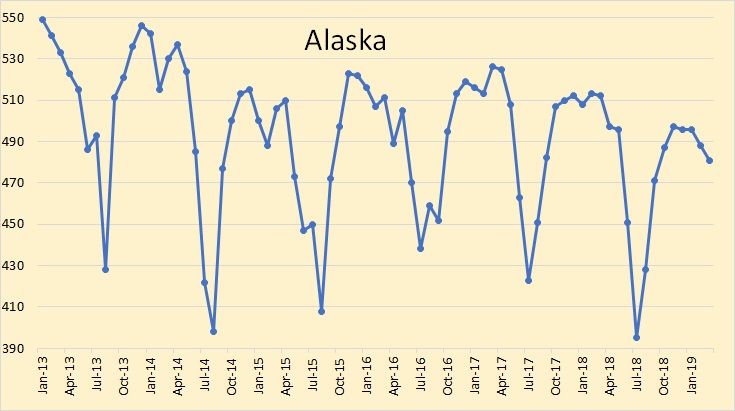

Alaska continues its slow decline. This is the first time in decades that they failed to reach half a million bpd this past winter. They got to 497,000 bpd in November.

The GOM seems to be doing okay however.

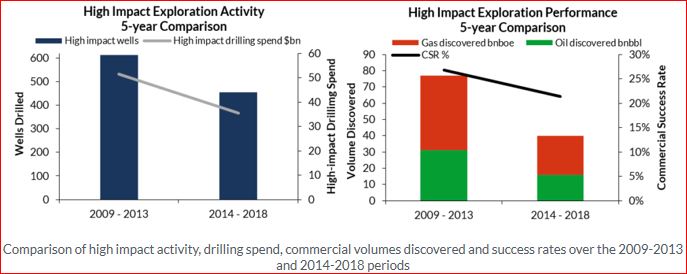

Discovered volumes from high impact drilling fell overall by 50% in the 2014-2018 period compared to the previous five years. Only a little over half of the decline can be accounted for by a lower well count which fell by 28%; falling success rates and average discovery sizes accounted for the rest. Portfolio renewal has become a critical issue for the industry and larger companies have responded by trying harder to open new plays through increased frontier drilling.

So they drilled 28% fewer wells and found 50% less oil. No wonder they are drilling fewer wells, apparently they are just not that profitable.

401 responses to “World Oil Production, February 2019 Data.”

The great inventory drain for 2019 and 2020 is coming soon. It will not be very visual in the beginning. Because, every on is concentrating on what the US reports. Yeah, US will go down, just not to the extent of all other countries. Heck, we still have close to 3 million a day we are exporting. I changed my mind on lower expectations of WTI due to over production. It ain’t gonna happen. I’m going back into 2021 leaps for USO 2021 tomorrow morning.

Heck, we still have close to 3 million a day we are exporting.

Well no, we don’t. First, the government does not export oil, oil companies do. And while oil companies do export oil produced in the USA, they import more than they export. In April, net imports were just over one and one half million barrels per day. The table below was taken from this month’s Monthly Energy Review and is in thousand barrels per day.

Petroleum Overview

Ron,

I think GuyM’s point is that we are exporting some of the oil that is produced in the US, we have done this for a long time with Canada and Mexico, but some people think exporting oil is a bad idea. I think oil companies should be free to sell their oil where they wish, if they get a better price by exporting the oil they produce, then export it.

The approximate annual net revenue to the US LTO industry from its 3MM BOPD of exports just about covers its approximate annual interest expense on $300bn of long term debt. That export revenue cannot be used to deleverage debt, replace reserves, or grow production rates. In fact, the LTO industry is still outspending revenue to be able to export that 3MM BOPD: https://www.rystadenergy.com/newsevents/news/press-releases/Just-10-percent-of-shale-oil-companies-are-cash-flow-positive/

As most of these exports come from the Permian we should not discount the approximate 1 BCF of associated gas getting pissed up a flare stack, wasted forever, nor the 1 billion barrels of fresh water being used to frac those wells, whose oil production then gets exported.

The United States is the largest oil consumer in the world. Granted, the shale oil phenomena the past decade has proven that “reserves” no longer need to be economical to recover. Still, wild ass guesses of 50,60,70G BO of recoverable reserves in the US are nuts. 302,000 more shale oil wells, for instance, will cost somebody, the American tax payer most likely, well over $3t. The 1975 Energy Policy and Conservation Act banning exports was signed into law for a reason. Those same reasons for prohibiting exports then, exist today…x 100.

Exporting America’s last remaining oil resources away, extracted on credit, is not free enterprise, nor capitalism, nor smart long term energy policy. Its stupid.

Yup.

Mike,

Why was it ok to export oil before 1975, but not after? Besides the law passed by fearful legislators.

The reasons were not good then, and they are not good now.

see

https://en.wikipedia.org/wiki/Comparative_advantage

I agree flaring the natural gas is not smart, that is up to state regulators to stop.

As far as running a business poorly, that is allowed in a free capitalist society. Eventually lenders will smarten up and stop lending money to poorly run enterprises.

At the end of 2017 US C+C proved reserves were about 42 Gb according to the EIA. My low oil price ($70/bo Brent in 2017$) scenario has about 53 Gb total tight oil produced, with about 14 Gb produced to date.

For my low oil price scenario at total of 256000 wells are drilled with 143300 completed through Feb 2019 and 112000 left to complete. The cost for those wells will be about 815 billion 2017$. With about 39 Gb left to produce at $70/b and net of about $37/b (assuming $5/bo of natural gas revenue used to offset part of LOE and transport cost of $5/b), we have about 1443 B in 2017$ which can be used to pay for the wells.

The tight oil plays can be run properly, perhaps some of the better independents and the oil majors will get to it.

We can even restrict exports, but my guess is the majority of oil producers don’t want the government telling them what to do, this is a pretty standard conservative principle.

@Mike

Your last paragraph is a little wordy for a bumper sticker…but I wouldn’t mind quoting that to a few people.

Your LTO jeremiads are hair-raising.

Keep at it.

I know we are a net importer. All I was saying was some of that now exported could be used to refine here, thus reducing potential decreases in inventory. I should have been clearer.

I think the overview of US oil import and exsport will be very interesting to follow in the years to come. There is now information stated that trade war will reduce world growth and oil demand by 50% , they now exspext demand will grow by 0,7% or approximately 700 k barrels in 2019. WTI soon reach 55 usd / bbl. I believe it will be the lower 50 range or even upper 40 usd range rest of 2019 and depending of Trumph how long it will stay there.

There is now information stated that trade war will reduce world growth and oil demand by 50% ,…

I think you meant the trade war will reduce World growth in oil demand by 50%. If so, then I agree.

When looking at imports and exports, we are exporting very light oil and importing heavy oil. The refineries in the U.S. Are set up to process heavy oil. Processing heavy oil gives them the highest margins.

This year’s Bible release is scheduled for 11/12 June. Heads up.

If the economy holds up, we might be looking at four dollar gasoline nationwide within a year.

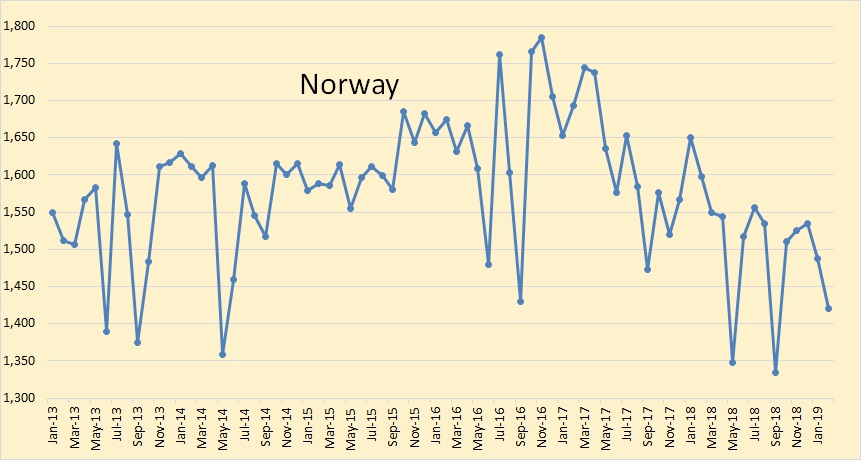

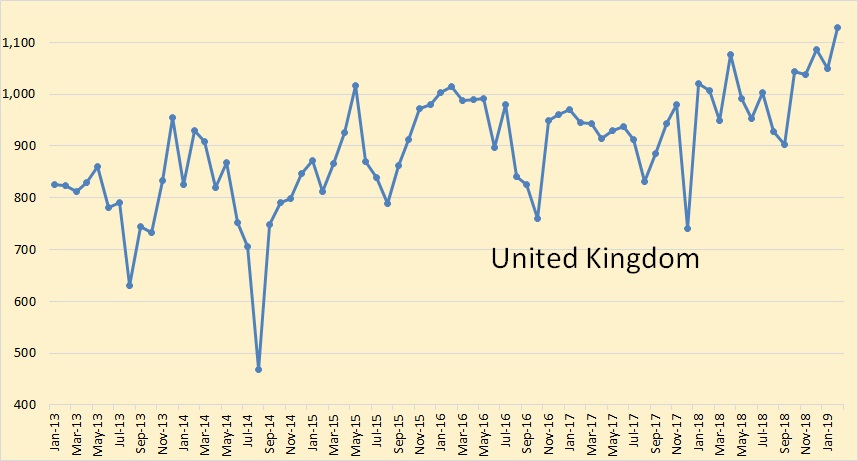

Amazing that with the lack of investment in offshore, the UK is rocketing upward.

Came across a blurb concerning the contaminated Russian oil. The dilution of the contaminant is the solution selected by apparently everyone, including China.

China seems to have enough storage to buy quite a lot of the contaminated Russian oil, at a discounted price, with the intention of doing their own dilution at a later date with clean oil that they will obtain from wherever.

I have taken a look at trailing twelve month averages (TTMA) for World C+C minus tight oil output and World C+C minus tight oil minus bitumen (Canadian oil sands). The sharp rise in output from 2015 to 2017 was due to OPEC’s surge in output from Jan 2015 to Jan 2017 (about 2250 kb/d increased output over those 24 months for TTMA). Over past 13 years the average annual rate of increase for World minus tight minus bitumen has only been 124 kb/d each year.

OPEC TTMA chart below the average annual rate of increase in OPEC output from Jan 2005 to Jan 2019 (using TTMA) from linear trend is 202 kb/d each year.

When we consider the TTMA (trailing twelve month average) of non-OPEC C+C output minus tight oil minus bitumen , we find an average annual rate of decrease of 77 kb/d each year.

TTMA for US tight oil plus Canadian bitumen (oil sands) from 2010 to 2019 with linear trend line slope is 816 kb/d.

Dennis, drawing trendlines from 2005 is really misleading. It implies that this trendline will continue into the future. Many countries have peaked and gone into decline since 2005. And many other countries are at their peak right now.

Many people believed 2005 would be the year World oil production would peak. They were off by almost 15 years… so far. Do you think your trendlines will continue? Will oil production never peak? If not, then why draw the trendline from 2005? How about 2016?

Hi Ron,

No I am simply looking at the long term trend in OPEC output, it has been fairly flat. Looking at the month to month ups and downs is of little interest to me.

I chose the longer period because the slope was smaller than using the 2013- 2019 period you choose for your charts. Below is what we get when we choose 2014 to 2019 for the trailing twelve month average, the slope is 614 kb/d over that period.

I have never said what I expect about future OPEC output, I don’t really know, we have very little good information except past output.

The trend line shows what has happened over a given historical period, full stop. You are reading things that are not in the chart and imagining what I think will happen in the future. Hard to know what the Chump will do next, maybe sanctions on Canada and Mexico? 🙂

My best guess is that OPEC output will be relatively flat from 2019 to 2030 maybe up a bit or down a bit (+/-100 kb/d) from the Jan 2019 TTMA.

Ron,

You asked if I thought oil will never peak. I think you know the answer, hint below.

URRs are also deceptive Dennis. Easy oil comes up fast but hard and expensive oil comes up very slowly. URRs just don’t take that into consideration.

One of your URRs above may be correct, but that does not imply that your production curve is correct. My best guess is, and let’s admit it, we are both just guessing, that we will see a sharp decline soon after peak oil, then a very long tail that may go out for a century. So the URR could be 2800 to 3400 GB. But it will take many decades to get those last few GBs to the surface.

Ron,

The main point is you asked if I expect that oil production will peak.

I have endlessly posted charts with a peak in oil production, the point is not whether the production curve is precisely correct, it is why would you ask such a question? Have you not been paying attention. 🙂

Of course nobody knows future output, these are scenarios, a set of assumptions are proposed and the model follows from those. This is a basic material flow model, oil is discovered, then moves through fallow, build and maturation stages of development and is finally produced. The model is calibrated to actual output given discovery data, The future is a guess based on what we have seen in the past.

Of course the production curve will not be precisely correct, if the assumptions of the model are correct, the model will be correct. There are an infinite number of different assumptions that could be made resulting an infinite number of possible production curves for any single URR (of course the same applies to the URR).

So the chances that my model will be correct are roughly 1 divided by infinity or approximately zero.

The same can be said of every prediction of the future, they all have about the same chance of being correct, that is no chance at all. 🙂

So we agree future production cannot be predicted.

Ron what causes the very steep decline after the peak, all the wells in the World water out simultaneously? 🙂

Ron what causes the very steep decline after the peak, all the wells in the World water out simultaneously?

When there is plenty of other, easier oil to find, it makes sense to let an old well gradually decline and move on to better fields. When all the oil in the world is becoming more expensive, and scarcer, then every effort will be made to maintain production till the very end.

This means that historical well production and decline curves cannot be a basis for predicting the total world decline after peak. Decline will be steeper as efforts to maintain production fail “all at once” so to speak.

Further, economies do not decline gracefully. For those of us who believe that oil is an essential “ingredient” of the global economy, we expect the economy to decline, spasmodically and rapidly. For an idea what this looks like, one only needs to observe Venezuela’s oil production over the last decade.

Niko,

Statistically it is highly unlikely that the failures will occur “all at once”. The oil fields all over the world are each unique and the “steep decline” that you expect is unlikely to occur all at once. The most mature producing nation is the US. If you look at lower 48 (excludes Alaska) onshore (excludes Gulf of Mexico) conventional (excludes tight oil) C+C production from 2000 to 2010 the annual rate of decline is about 2% per year.

It is possible that oil production will be pushed to very extreme limits and then crash, there are many different possibilities for future extraction rates from conventional (excludes extra heavy oil sands and Orinoco output and tight oil) producing reserves.

The scenario below assumes extraction rates are pushed up to the 1973 level (10.8%) before levelling off and then declining back to 2018 levels. The possible number of future extraction rate paths is infinite, so this is one of many possible outcomes. We do not know how it will play out, only guesses are possible.

Clicking on chart will make it more readable (larger).

An alternative model below.

Click on chart for larger view.

Natural log of US lower 48 C+C output excluding tight oil and Gulf of Mexico output.

Average rate of decline was 3.5% from 1985 to 2010 (output increased over 2010 to 2015 period). Note that the 2000 to 2010 period has a lower decline rate, about 1.8%.

Niko,

Oil has become less and less important as an economic input. Oil prices will increase and oil will be used for the most important economic uses and substitutes will gradually replace oil. Oil production does not stop overnight and all fields do not fail to produce at the same moment. Decline rates are likely to slowly increase at the World level. Venezuela is a failed state and that is the reason oil output has decreased, you have the causation arrow reversed there. It is unlikely that all nations become failed states, a few will, most will not.

Dennis Wrote:

“Oil has become less and less important as an economic input. ”

If that was true, then demand of Oil would have leveled off or declined. I think jevon’s paradox is in play. Even if Transportion and other devices that use Oil have become more efficient, it just enabled more vehicles on the road.

To provide some prospect, in 2001 China had about 18 million cars & trucks registered. In 2019 it has about 310M cars & trucks, adding about 23M new vehicles per year. I recall pictures of China in the 1990’s when everyone was driving bicycles. Today you can see jammed back roads & highways full of vehicles.

Dennis Wrote:

“Oil production does not stop overnight and all fields do not fail to produce at the same moment. ”

Issue is that advance oil production technology was used to maintain production output for extended period, but at the cost of steeper production declines in the future. At some point. the oil column floating on top of the water column is going to be too thin to maintain production rates. Thus when horizontal drilling methods can no longer effectively manage water cuts, production declines will accelerate. My guess is that one this happens Oil production decline rate will be around 7%.

Yes, not all fields will simultaneous experience steep declines, but one by one they will slip into deeper declines until most of the big, oil field are all experience high production declines.

Consider that most of the Oil majors abandon reserve replacement project around 2013-2016. The need much higher oil prices but the global economy cannot support it. When prices do eventuall climb up to make these replacement project feastible, its going to take a long time for them to be completed & which the new supply is unlikely to offset years of declines.

Why is the the USA gov’t is bent on taking control of most of the ME oil fields? If ME oil wasn’t important that why has the US spent Trillions on ME wars?

Hi Techguy,

Can you explain why we have not seen the 7% decline rates for overall US L48 on shore C+C production excluding tight oil. From 1985-2010 was about 3.5 %, from 2010 to 2015 the rate slowed to about 2%.

Output declines very steeply for tight oil wells, but the rate changes over time, this will also be the case for fields with high water cuts, many wells will stop producing but the timing is different for every well.

When they all get added up worldwide, it will probably look more like the US L48 excluding GOM and LTO.

As to oil being less important, it is less important as an economic input, measured in dollars. About 2.1 trillion for a World economy of 80 trillion so about 2.6%.

As to oil being less important, it is less important as an economic input, measured in dollars. About 2.1 trillion for a World economy of 80 trillion so about 2.6%.

Oh my goodness, Dennis, are you serious? Oil is only 2.6% of the world economy? So by that reasoning, if all oil disappeared tomorrow the World economy would suffer a 2.6% decline. It would still be 77.4 trillion?

No, no, I know you know better than that Dennis. You are a very smart guy and only an idiot would believe that. Nevertheless, that is what your post leaves hanging. It leaves hanging nonsense that you obviously know better.

Right now there is nothing more critical to our economy, and our well being as 7.6 billion people on this planet, than liquid energy production. If it were to collapse tomorrow, we would all be dead within a few months.

But of course, we both know it will not collapse tomorrow. It may start it’s slow decline tomorrow but that is another story. If it does it will not be a catastrophe. But that does not diminish from the very important fact that liquid energy, along with all the other products made possible by oil, is what is driving our economy.

No, we will not all die quickly from the demise of fossil fuel. Our demise will be a long slow drawn out process.

Hi Ron,

We disagree on the importance of liquid fuel.

The point is that we do agree that oil output will not collapse overnight.

In part, the value of a commodity is measured in dollars. So it is a question of the relative importance of oil as an economic input, so in 1980 oil output was about 7.9% for total World GDP relative to 2.6% in 2018, so one third the importance as an economic input into the World economy. Oil will continue to fall in relative importance as output falls and as it becomes scarce and prices increase this will spur further substitution.

The fact that oil output will not collapse overnight will allow this substitution to occur to the point that oil prices will start to fall after 2040 after rising over the 2020 to 2030 period. Prices may be flat from 2030 to 2040 as the World substitutes other sources of energy for oil.

Dennis Asked:

“Can you explain why we have not seen the 7% decline rates for overall US L48 on shore C+C production excluding tight oil. ”

Yes I can. Largely because Tech. Advances in Oil extraction have significantly improved. the US 48 saw decline rates as high as above 5%. before they applied extensive in-fill drilling. This has enabled older fields to reduce declines, but at a cost in the future of steeper declines.

https://www.woodmac.com/news/opinion/can-conventional-oil-projects-compete-with-l48-oil/

“In our insight on decline rates, we calculated that non-OPEC conventional onstream declines stabilised at around 5% in 2016. We believe they’ll stay at this level through 2020 before increasing to historic norms of 6%.”

https://www.woodmac.com/news/feature/non-opec-decline-rates-remain-stable-until-2020/?contentId=7018&source=13

“After peaking at nearly 7% during the last decade (2.4 million barrels per day (b/d) a year), decline rates for conventional fields reached record lows in 2014 — just 1.2 million b/d per year, or 3.6%. The price collapse accelerated these rates back up to 1.9 million b/d (5.1%), due to the extent of immediate spending cuts, but we believe this level is sustainable until 2020.”

— Realistically, a 7% decline rate by the mid 2020s is pretty optimistic, considering its about 5% today. The only way likely to prevent production declines is to spend another $500B to $1T to drill the expensive oil (arctic, Deepwater, etc). But with Oil prices still bouncing between $45 and $65, there is little chance an Oil major is going to start. By the time they eventually complete new oil projects they won’t be able to offset years of high decline rates. Higher energy prices will also start impacting the global economy.

Bottom line, the World should have started a massive transition away from Oil started back in 2005 when trouble began. It was a warning that something import is wrong. It was ignored.

Tech guy,

We are talking past each other here, you are talking about individual wells or possibly fields in the absence of any new investment.

I am talking about large regions such as the US or the World and the rate that total production declines. Just look at the data, I used the data from the EIA. Prior to 1970 output in the US was rising and for the World output has risen most years through 2018.

The US decline rate for US L48 onshore conventional oil was about 3.5%. Note that we only have data from 1981 and from 1981-1985 US L48 onshore conventional output was flat.

Individual fields that have no more investment may indeed decline at 5%, bit it is not likely this happens for al fields everywhere in the World at the same time.

Decline rates will gradually increase from 0% to about 3.5% from 2025 to 2050.

Hi Dennis,

“The US decline rate for US L48 onshore conventional oil was about 3.5%. Note that we only have data from 1981 and from 1981-1985 US L48 onshore conventional output was flat.

Individual fields that have no more investment may indeed decline at 5%, bit it is not likely this happens for al fields everywhere in the World at the same time.

Decline rates will gradually increase from 0% to about 3.5% from 2025 to 2050.”

This last part “Decline rates will gradually increase from 0% to about 3.5% from 2025 to 2050.” Can you explain to me what you mean by that one? Decline rate 0%?

Im not sure if i have the wrong terminology here but you always have a decline rate right except on initial plateau? If for an area production dont decrease as in your example above US 81-85 it is simply new drilling hiding the effect of decline for production already on stream, but you still have a decline rate in those already producing assets right?

Also i think perhaps using history of the us conventional onshore to predict decline rates of future world might be a bit flawed. Im with you on the “it wont happen at the same time” logic, but i think there might be potential for a slightly different story since we globally have the potential of old super giants running dry abruptly on main producers rather than slowly fading out. If that happens we probably are looking at higher decline rates than historical ones.

I mean we have more or less just moved production forward in time with technology right, at some point geology should set the limit and we will have high decline rates left and not much to do about it except transition into something new and i hope you are right on that part but i find myself being a bit more pessimistic about it myself.

Hi Baggen,

I am looking at the output curve for the US L48 excluding Gulf of Mexico and excluding tight oil output. The US is a very large very mature producing region and has a number of giant oil fields. There were surely individual fields that may have declined at 5% or perhaps even higher decline rates, but for the data we have from 1981-2015 the decline rate of total output was 3.5% or less.

There are a number of supergiant fields in the World, they will decline at different rates (and the rate is unlikely to be constant) and the decline of each field will start at different times. Even for any individual field (and these fields are enormous in many cases) individual wells will water out at different times and in many cases these are maximum reservoir contact (MRC) wells with multiple legs which will water out one leg at a time.

There were about 85,000 wells drilled by OPEC from 1980 to 2018 (not sure how many of these are still producing), statistically these wells will be shut in one well at a time and just as in a tight oil play the field decline will be less than the rate of decline of an individual well, this will also be the case for the World where we may have between 450,000 and one million individual producing wells (my guess is perhaps 600k to 700k (in 2017 there were 450k producing oil wells in the US alone, I am guessing 150k to 250k for the rest of the World). Note also that investment in new oil wells and maintenance of existing wells is unlikely to cease before 2050. If at some point oil prices drop due to lack of demand investment may cease and in that case the decline rate in World C+C production will steepen to perhaps 5% or more.

This only occurs when there is a lack of demand for oil and oil prices become very low (perhaps $30/b in 2017$ or less). I don’t anticipate this will be the case until a Great Depression 2 (perhaps in 2030) or until 2050 when BEVs and/or AVs have replaced most ICEVs. It is possible increased air and water transport and petrochemical use may lead to continued demand for oil so that oil prices never fall to low levels, in that case we never see the steep decline rates. Difficult to predict how it will play out over the next 100 years.

Dennis Wrote:

“The US decline rate for US L48 onshore conventional oil was about 3.5%. Note that we only have data from 1981 and from 1981-1985 US L48 onshore conventional output was flat”

L48 is decline rate for onshore conventional fields is running at about 5%, and will start increasing in 2020. Not individual wells, but entire legacy fields.

Not sure why you think Conventional, On Shore decline rates is only at 3.5% when it is not. Its running at 5% with investment into the legacy fields to prevent much steeper declines. ie Red Queen to hold declines at 5%.

I think you’re including the GOM, offshore (non-conventional) fields to get your 3.5%, but considering that Oil Majors have shelved Deep Water GOM projects, the GOM is not going to help offset declines.

Currently there are about 19 Rigs Drilling for Oil in the GOM, down from 60+ in 2014. I believe most of the GOM rigs are adding horizontal wells on already existing drilled fields. All the growth in US Oil production is from LTO.

Techguy,

No I use US data for C+C and deduct Alaskan output, GOM output and tight oil output.

From 1985 to 2010 the rate of decline averaged about 3.5 %, after that is slowed down further.

Just go to the EIA website and do the analysis, it is not very hard to do, took me about 10 minutes or less.

https://www.eia.gov/dnav/pet/pet_crd_crpdn_adc_mbbl_m.htm

My point is trendlines are not just useless but also deceptive. Your OPEC trendline above is a perfect example. It suggests that OPEC production will continue along that line. Yet your best guess is that OPEC production will be flat for the next 11 years. Then why the trendline? What does your trendline suggest? Really? Then why draw it?

Ron,

I was considering how World C+C output had grown and where that growth came from. I chose 2005 as a starting point because that was the start of a relatively long plateau in output.

So a trendline is used to give the general trend over the period covered, no more, no less. In fact it is no different than the reason you like to post charts, to see what the past trends have been. Does that mean you expect the future will look like the past? I would say mostly no.

On the steep decline that you expect consider that there are not many wells that decline more steeply than tight oil wells. The tight oil output for the nation will not decline steeply until producers stop drilling new wells or change the average rate of well completion very steeply.

For conventional output the oil can be produced at the usual rate the main difference for untapped resources is that they are expensive to produce, if oil prices are high enough to produce it profitably it can be produced. I model extra heavy oil and tight oil separately. The extra heavy oil model is based in part on the projections of the Canadian Association of Petroleum Producers (CAPP), I assume Venezuela starts to ramp up output about 15 years after Canada and then follows a similar trajectory (a WAG) but 15 years behind Canada. Only 200 Gb of extra heavu oil output is assumed, following Jean Laherrere.

Consider chart of shock model below and note the Mr. Laherrere usually focuses on C+C-XH, where XH=extra heavy oil. This model uses a high US tight oil scenario with peak LTO of 10.7 Mb/d in 2025, so it is on the optimistic side assuming high oil prices. The shape of my model and that of Mr. Laherrere is not very different.

I typically show the chart on a different scale, the URR of my “medium model” is about 3100 Gb. If extra heavy oil was added to Mr. Laherrere’s 3000 Gb model it would be 3200 Gb, my model is just a bit lower than the 3000 Gb model at 2900 Gb for C+C-XH.

Chart from Laherrere 35 nation oil forecast paper, page 19

https://aspofrance.org/2018/10/03/updated-extrapolation-of-oil-past-production-to-forecast-future-production/

Ron I will try one last time.

A trendline shows the trend over the period covered by the data.

It does not imply that trend should be extrapolated into the future.

It is shown to show the trend explicitly over the period considered.

I guess it may be deceptive to those that do not know what an ordinary least squares regression is. I assume people know the basics.

No problem Dennis. You continue to draw trendlines and I will continue not to do so.

Fair enough, but keep in mind most people just look at it as the trend over the period where there is data.

Extrapolation of a historical trend requires a solid theoretical justification.

And if Bubba takes over shale, what is the theoretical extrapolation? Not easy to figure, because no one knows how many independents will be still standing. Bubba will proably not export. We will always have imports, because other than Canadian, we have little heavy oil.

GuyM,

In that case the peak occurs earlier because tight oil production will not peak as high, but it will remain on plateau longer so declines will be less steep. So this suggests a long plateau in World C+C output from 2021 to 2030 or so or possibly slightly rising output if high oil prices spur more rapid development of oil resources as well as more exploration that might lead to some deep water discoveries.

Chart below shows a variety of US lto scenarios, your bubba scenario might look like the lower of these scenarios (or perhaps even lower).

Clicking on chart will make it bigger.

Dennis, your brilliant!

GuyM,

Thanks. The low scenario was developed in response to brilliant comments by you.

A group effort.

As to oil being less important, it is less important as an economic input, measured in dollars. About 2.1 trillion for a World economy of 80 trillion so about 2.6%.

Denise you are way out on this . The heart does not even weigh a kilo but once it is out then all your 80 kilo are headed directly six feet under . Remember the poem “the battle was lost for the horse shoe nail” .

Holeinhead,

In economics importance is measured in dollars. In 1980 oil output was about 8% of World economy, in 2018 about 2.6%. The relative importance of oil decreased from 1980 to 2018. The relative value of a good is in part a reflection of abundance. Water is very important but its abundance in the World makes its value from an economic perspective much lower than oil even though we can live without oil, but not without water.

Dennis Wrote:

” In 1980 oil output was about 8% of World economy, in 2018 about 2.6%. The relative importance of oil decreased from 1980 to 2018. ”

Oil is just as important today, as it was in 1980. Oil is probably more important today since a lot of developing world starting consuming a lot of it. Recall China in 1990s: everyone drove bicycles. China 2019, most people use cars & buses to get around.

Something does not seem right with your estimate that Oil decreases from 8% to 2.6% since 1980. For one in the 1980’s Oil was expensive (about $115/bbl adjusted for inflation, world was in a recession, and US interest rates were about 15% (topping out at about 20% during that year).

Bottom line: When Oil global production starts declining it will have a significant impact on the global economy. Consider that High Oil prices kill economic growth. (2011-2014 was an exception due to QE Money printing). If Oil prices did not impact the global economy, it would stall economic growth.

Dear Dennis, you are way off. In 1980 the world economy was very different from today’s world economy. The correct answer beeing China. Oil is super important. Actually, fossil fuels are super important. Every level of our society depends on them, their multiple utilizations and deployment. Without them there is no economy as we now have it. World economy needs energy and a lot of it. Without energy there is no economic growth. All the hype about degrowth, green, blabla, as much as I want that to happen…it will not happen. Thus, oil industry, as oil is the backbone of modern life, had, is having and for some time will have a disproportionate importance to our survival as a specie as to its size in the world economy.

USA did not spend trillions of dollars on wars and Drill, baby, drill just for the sake of spending.

It spend those money and got a lot of ppl killed in the process to maintain access to the MOST important mineral resource ever. Not even th shale boom has not stop America from bombing, invading and killing.

Linear extrapolation has never been a good technique to find out about the future, whether it is extrapolating oil production, oil price, Arctic sea-ice, or global surface temperature. The future remains unknowable and those that expect that trends will continue into the future are bound to be surprised when those trends inevitably change.

Javier,

I agree, it was not intended that the trend should be extrapolated, it was shown to illustrate the trend over the period of the regression, no more no less. There have been long periods (1982-2018) where the increase in C+C output has followed a linear trend, I do not expect that will continue.

Please keep the climate references in the Electric Power Monthly thread.

Thank you.

Most on the oil side are not interested and you brought it up, not me.

Oil production trend has generally decreased over time, as Gail Tverberg has shown repeatedly. See for example:

https://transitionferndale.files.wordpress.com/2011/04/world-oil-production-with-trend-lines.png

from

https://transitionferndale.wordpress.com/2011/04/25/oil-supply-trends/

As we all know the trend that was nearly flat 2005-2010, partly recovered with the fracking boom, yet it has gone back to less than 1% since 2016. It doesn’t look good for the future despite more people trusting that if more oil is needed more oil will be produced, because that is what has happened in the past.

But it amazes me that people well aware that linear trends in their field of expertise mean nothing for the future, totally buy that for other fields they do.

Javier,

What part of “the trend applies to the period of historical data included in the regression” do you not understand?

Nobody has suggested, except you and Ron that the trend should be extrapolated to the future.

This is so obvious to anybody that has taken a course in statistics that it does not need to be stated.

Chart below shows the linear trend from Jan 1982 to Jan 2019.

Just to make it plain, I do not expect the trend will continue beyond Jan 2019. To show that there has been a change in trend requires more than putting lines on a chart, there are statistical tests to determine the statistical significance of any changes in trend.

Ok, that seems logical. We point the driver where we think it will go, based upon what we know of the course (which we have never played before), but quien sabe?

What your trend hides is how the slope of the trend in oil production has been changing over time. Your linear trend just gives you an average for the whole period.

The annual rate of change in oil production has been consistently declining. As it is noisy data it is better looked as a 10-year average in the rate of change. It shows oil production grows more slowly over time, something your graph doesn’t show. Shale oil has not changed the declining trend in oil production growth, but without it it is obvious that rate of change would have become negative.

https://i.imgur.com/aDEPfia.png

The graph shows Peak Oil is inevitable if the decline in growth continues and while I can think of many things that could accelerate the decline leading to Peak Oil in the short term, I can’t think of anything that would make this 35 year negative trend become flat or positive.

So the linear trend is deceiving. The trend is getting flatter over time.

Javier,

If you mean that the rate of growth has slowed, then yes for a linear trend in output that is quite obvious. And of course it shows the average rate of increase, as that would be the definition of an OLS regression.

I agree the 1945-1972 rate was very different (about 7.7% annual rate of increase in C+C output over that period) and roughly 6.6% per year from 1920 to 1973.

From 1983 to 2018 the rate of increase was much slower about 1.2% per year on average. There are “flat” periods in 1990-1993 and 2005-2010 which followed periods of faster growth. 2011 to 2018 has followed the trend fairly closely.

I do agree at some point output will flatten, my expectation is between 2021 and 2024.

Both you and I could be incorrect, the peak date will be known about a year or maybe even 5 years after it has occurred.

Click on chart for larger view.

Javier,

I thought you said we should not assume trends will continue into the future.

The trends that fit your narrative will continue, no doubt. 🙂

I agree there will be a peak and I agree the trend will change, probably to a slower rate of growth reaching zero by 2022-2030, then growth will become negative at some unknown future rate, likely it will gradually decrease from 0% to around -3.5% over several decades. Though much will depend on unknown future extraction rates from producing reserves as well at the rate that resources are developed from discovery to producing reserves.

Exactly. The existence of a trend does not provide information about the future as you have pointed out. Information about the future can be obtained from a good knowledge of the system, though. To a certain extent we can predict what will happen to an object falling from a height from physical laws and material resistance studies. There is always uncertainty about the future. Election polls provide knowledge that sometimes, but not always, allows good predictions on the outcome. The more we know about a system the better we are at projecting what might happen. That’s the idea behind this site, I guess.

I don’t think that getting the opposite result for 15 years can be construed in any way other than failure. Don’t lower your standards so much.

Javier,

People knew the 2005 prediction was wrong by 2011, over the 2005 to 2010 period there was an undulating plateau, most did not see the tight oil coming in 2011 (tight oil output was about 1.7 Mb/d at the time). Most people at the time were only aware of Bakken output (about 500 Kb/d) and perhaps Eagle Ford output about 360 kb/d at the end of 2011, but the data was not tracked very well by the EIA at the time so mostly the Bakken got the headlines.

Here are my thoughts from 2012

https://oilpeakclimate.blogspot.com/2012/07/an-early-scenario-for-world-crude-oil.html

https://oilpeakclimate.blogspot.com/2012/07/further-modeling-for-world-crude-plus.html

https://oilpeakclimate.blogspot.com/2012/08/i-noticed-that-compared-to-model-by.html

The last of these 3 posts was the best I could do in 2012 and note that I had not yet accounted for the rapid rise in tight oil that would occur from May 2012 to April 2019 (about an increase of 5.4 Mb/d over that period in tight oil output). So the low peak output in these scenarios reflects this unknown future.

A physics problem such as dropping an object from a given height is a fairly easy study that is easy to reproduce.

We have very limited information publicly available for the oil industry, predicting future discoveries, resource development and consumption is not possible.

So I set realistic standards, as only a single prediction (best guess) can be made and the possible future scenarios are infinite.

A simple math exercise suggests the probability of a correct prediction is zero.

The linear trendline of this true stress vs. true strain chart for AISI 4140 steel looks very reliable from 0ksi to about 175ksi. While on the linear portion of this curve, it appears that the material will continue to behave predictably for ever increasing loading. However, if you keep pulling to the point where 175ksi is reached, the curve takes a serious departure to nearly horizontal until the tensile limit is achieved. The catastrophic rupture of material ends with a jarring bang when you hear it on a materials testing machine. It is always unnerving even when you know it’s coming, as your eyes follow the pen plotter across the graph paper past the yield point.

Fracture mechanics is largely the study of crack propagation in metal alloys. Strain energy drives crack propagation dramatically from the yield point to the plastic limit; ultimately, both the density and extent of crystalline dislocation at the crack fronts within the material becomes so severe that failure occurs all at once.

Based on Ron’s graphs, I submit to you, that it is possible we are still on the linear portion of the hydrocarbon production curve and have just reached the yield point in 2019.

I edited the above comment and it appears the AISI 4140 graph disappeared. Here it is again.

Mike, when you edit a post, any attachment only appears to disappear. It is still there, just not in the edit. If you refresh the page it will appear again, just like magic. 😉

Hi Mike Sutherland,

Interesting analogy. In this case for the World, it would be more like testing some new metal that had never been discovered. Based on my own experience as a mechanical engineering student the point where the curve becomes nonlinear is not predictable. I would submit the hypothesis that the curve might become non-linear at any point from 2018 to 2025 with my best guess around 2020 or 2021, with the peak in output arriving in 2022 to 2030, depending upon actual resources (2800 to 3600 Gb), the state of the World economy, and the price of oil.

This is far more complex than a simple repeatable controlled lab experiment and far less predictable.

Javier, You seem not not realize that much of the discovery data is from the past, so the extrapolation also uses data from the past. Next time remember that current production comes from discoveries that may have been made years ago.

Javier said: ” The future remains unknowable”

Yet the past is known.

Sure, sure. That’s why the Peak Oil prediction for 2004 came out wrong. Because the past was known. But some people never learn that it is difficult to make predictions, especially about the future.

Javier,

The 2004 or 2005 prediction depended on a flawed Hubbert Linearization approach. That’s not how we approach this.

See

https://www.amazon.com/Mathematical-Geoenergy-Discovery-Depletion-Geophysical/dp/1119434297

If you suck fluid out of a cup through a straw, the production rate of fluid appears to be consistent as long as there is fluid to be drawn. There is no smooth transition of flow rate from minimum to maximum to minimum. It simply goes from 0 to maximum, perhaps holds there for a while, and then stops completely. Likewise, I believe that most oil reservoirs will behave in this fashion.

Mr Sutherland.

For a single well you are correct. For a reservoir we have a non-homogeneous rock matrix with random fractures in many cases as well as multiple straws inserted at random intervals as well as thousands of unique reservoirs each with different behaviors and permeability. The oil shock model uses a maximum entropy model to capture the statistical uncertainty in the rate of development in oil resources, then assumes a constant annual rate of extraction from the average producing reserves (the average extraction rate from producing conventional reserves). Historical production is matched by setting the extraction rate so modelled production matches actual production. Future production assumes the rate of resource development remains similar to the past and assumes either constant extraction rates, increasing extraction rates or decreasing extraction rates after 2018.

We can only guess which it will be. From 1982 to 2010 extraction rates were decreasing and from 2011 to 2018 the trend was gradually increasing extraction rates as the pool of producing reserves reached its maximum in 2011 (for low URR case of 2800 Gb). Seems more likely in my view that the extraction rate will gradually increase over time after 2018, but the correct assumption will only be known after the fact.

Javier said:

“That’s why the Peak Oil prediction for 2004 came out wrong”

In the greater scheme of things, it came out reasonably correct. What is being off by a few years when one realizes that we are now relying on fracked oil and tar sands and all kinds of non-conventional oil.

That’s so funny. Specially coming from someone that claims to apply the scientific method. If you are into predictions the timing is everything. If the timing is wrong your hypothesis is wrong. If you predicted a La Niña for 2019 and it doesn’t take place your hypothesis is wrong. It doesn’t matter that eventually there is a La Niña sometime later as it is bound to happen. It has been 15 years since 2004. The Peak Oil prediction was wrong because nobody in the Peak Oil camp thought that fracking could be expanded so much, providing the missing oil from conventional sources. Peak Oil is inevitable but the timing is everything. Even some cornucopians like David Middleton accept that Peak Oil is inevitable, they just think it will be irrelevant because it will take place when we have solved the problem of substituting it.

Javier,

In a highly complex system prediction is probabilistic, precise predictions are not possible in nature where controlled experiments are not possible. Surely you can see this. Don’t hold others to impossible standards, not only is data imcomplete but predicting future choices by 7.7 humans is beyond impossible.

We are not doing simple lab experiments in microbiology here.

Dennis,

Javier does not realize that Peak Oil timing is a stochastic analysis and any date has a probabilistic interpretation.

I can talk El Nino but that needs to go on another thread.

Venezuela production was probably ~ 800k per day in April. EIA estimate is 830k; OPEC secondary sources are 750k.

https://www.eia.gov/todayinenergy/detail.php?id=39532&src=email

https://oilprice.com/Latest-Energy-News/World-News/Tanker-Sabotage-Venezuelas-Crisis-Worsens.html

The chart below was taken from the EIA’s latest Monthly Energy Review. March and April are obviously projections. Are they a tad overly optimistic?

The data is in thousand barrels per day.

Jan-19 11,870

Feb-19 11,683

Mar-19 12,110

Apr-19 12,200

Yeah, probably over current by over 200 bbs per day.

GuyM,

Possibly a typo? I think you might have meant 200 kb/d?

If so, I agree, though the GOM is the wild card. I think there was news that some new field just came online, these types of startups (if I am remembering correctly) can lead to a bump in output. My guess for March is about 233 kb/d less than the estimate from the MER, nearly equal to your estimate.

Ron I agree the EIA is too optimistic, I think their tight oil estimates need to be adjusted lower for March and April.

https://www.reuters.com/article/us-shell-appomattox/shell-starts-production-at-giant-appomattox-field-in-gulf-of-mexico-idUSKCN1ST1R4

It is about 175 kboe/d, but probably will not affect April’s output as it was reported in May.

Another report suggests several wells will come online in 2019, no specific dates were given.

https://www.offshore-mag.com/drilling-completion/article/16790570/llog-expects-three-field-startups-in-2019

https://oilprice.com/Energy/Energy-General/BP-Unlocks-One-Billion-Barrels-In-Gulf-Of-Mexico-With-New-Tech.html

Lots of activity, not a lot of firm dates. SouthLaGeo could you up date us on GOM?

Yeah, not a typo, just typing ahead of rational thought. Yes, and they may eventually be reduced even further than that, if Dean’s estimates are correct. It looks like one or more companies have over reported since mid year 2018. I don’t pick it up on my calculations, as the corrections could be made after a three month look back.

Hi Guy,

Here is a slight modification of Dean’s chart using the last 12 months of vintage data rather than all vintage data. The 12 month line is pretty close to the EIA estimate in Feb 2019 only about 70 kb/d under the EIA estimate for Feb 2019.

Yes, I did not say it was substantial, only noticeable.

From August 2018 to Jan 2019 the difference between Dean’s estimate and that of the EIA for Texas output is indeed substantial, but by February they seem to be converging. It will be interesting to see how the EIA march estimate compares with Dean’s 12 month vintage estimate which is 4939 kb/d for March 2019 Texas C+C output.

GuyM,

Your guess was nearly perfect, off by about 3 kb/d. Amazing!

US inventories week/week change (1000 barrels)

Crude Oil -282

7 oil products -4,003

Total (crude oil + 7 products) -4,285 (shown on chart)

Propane & Natural Gas Plant Liquids: +3,659

SPR no change

Line 13 Adjustment +6,167

Seasonal: Total (crude oil + 7 products) +48,588 year/year

Chart with dates of highs and lows

https://pbs.twimg.com/media/D72C1cjXkAYs7ze.png

Inventories: the sum of the USA + Fujairah + Japan (million barrels)

Total (Crude + Distillates) -4.0 week/week

Total (Crude + Distillates) +53.6 year/year

Total https://pbs.twimg.com/media/D72DrOVXkAIK_F_.png

Split https://pbs.twimg.com/media/D72EApFXsAALJCq.png

https://oilprice.com/Energy/Crude-Oil/Why-Oil-Majors-Are-Going-All-In-On-US-Shale.html

Morgan Stanley sees a 1.1 million a day deficit by the third quarter. Umm, yep, or more. That’s global, not what the EIA reports.

1.2 million a day from OPEC, and add in net Venezuela and Iran drop, Russia’s half million makes OPEC plus a wash, at least 600k a day from demand increase, and I could count far more than 1.1 million, as US is at a standstill. But, I discount my computations, as they never work out.

GuyM.

Hey at least we had some ok prices for April and May. Here we go back down again.

I’m using the time to shop for options. Calm before the hurricane. Not sure exactly when, but it’s coming.

GuyM.

Maybe.

Or maybe the Smoot-Hawley like tariffs will crash the US (and world) economy.

Some sections of the US and China economy are damaged. But China, overall, is NOT dependent on what the US buys. Farmers are damaged in the US. Not good! But, overall, the US economy will chug along. But, that would be dependent on how much chicken little convinces everyone the sky is falling. We should have adopted a VAT many years ago. Tarrifs are too hokey.

Hi Guym,

Any advice on the best place to buy options appreciated.

Sean

Sign up for etrade, or any comparable site, deposit money, and buy.

There is certainly a deficit in the market, question is how much and who is covering it short and medium term.

Interesting to note that OPEC has it that Iran has decreased production in May (Reuters survey) with 400k b/d from 2.6 m b/d to 2.2 m b/d. Which begs the question where about 800k/d are going since domestic use is a bit more than 1 m b/d and exports are less than 200k b/d at the moment. Most of it is inventory building, some can be some sort of smuggling of crude or utilising extra refining capacity and move products abroad one way or another. Anyway probably at least 0.5 m b/d gone from the market in the form of inventory. This has the potential to be released later though, when waivers may be given once again.

Russia with 1 m b/d disruption, from June 10th pipelines should be up again. Nobody knows what the rate will be after that.

No matter how you put it, it is safe to estimate that we would be at least 2 m b/d short in 2019, with about 1 m b/d being demand increase, 0.5-1 mill b/d Venezuela, 0.5 mill b/d decrease due to decline mostly offshore (North Sea, Mexico, Angola, Asia) and 0.5 mill b/d Iran (although countries like that has a tendency to look at all other options before actually reducing production – a bit sceptical). Assuming US production being flat, I bet the deficit will more than 3 m b/d going forward, especially because 2H of the year is always high demand season for crude. The assumption of flat US production becomes even stronger when we know there is a trend towards more condensate/less normal oil coming from the shale patch. It takes a stable genius to sort this situation out, and I don’t think lower oil prices for a period of time is the medicine.

https://uk.reuters.com/article/oil-opec-survey/table-opec-oil-output-falls-by-60000-bpd-in-may-survey-idUKL8N2355XJ

Posted an article earlier that said the Russian pipeline will operate at half speed for about six months.

Ok ,thanks. Not sure what information is realiable anymore in this market, but we will see what happens.

Yeah, you got that right.

Regarding the Russian contamination issue, it doesn’t seem all that trivial after looking at this chart (from twitter).

So how long was China’s (and other countries) trade surplus with the US to be tolerated? The largely anti Trump media will devote most text to how Trump states are hurt, and never point out that none of his predecessors sought a fix of any kind.

So . . . how long? Don’t hand wave and talk about how this fix cannot work. Just answer how long? Why did everyone else decide not now?

I’d say everyone else didn’t tariff because they had studied both history and economics.

Don’t disagree there are issues with both China and Mexico, but not sure tariffs plus insults will get the desired result.

Trade war is a major gamble. Is there a plan here or are we totally shooting from the hip?

Yes, agree. I have studied economics and it says that a country should produce what it is best at producing (lowest cost) and trade it with other countries exporting what they are best at. And maximise volumes, and all will benefit. Growth everywhere. Tariffs do not solve anything really. It just adds to the cost of the products a country is best at producing.

If the history part is included, what happend in the 1930’s? Trade barriers lowering world trade substantially and lack of stimulus to get out of a deflationary cyclus. Beacuse a lot of people have studied this time period, I think the main solution to the debt/lack of growth problem this time around is to print money (or give credit) and ensure governement deficit spending (by getting loans from the central bank? seems likely). So inflation out of control on the horizon could be what is coming; at least this would be the most likely scenario if oil prices spiral out of control.

The best solution? Maybe to increase money (QE) of all the the major currencies at the same rate at the same time because of the stimulus needed and the stable exchange rates, encourage and ensure stable trade relations (bin the tariffs) and also have a realistic policy in the energy sector (state governed if needed).

Shallow sands,

“We’ll see what happens…”

-President Chump

How long?

Why does the talk turn into hand waving and questioning mechanism?

It’s a simple question. How long was the trade deficit to be tolerated?

The yuan Peg is the target IMO. I don’t think there will be any agreement. Until china free floats their currency. This is going to end badly for the majority and a few minority will benefit greatly from it.

With all the currency Japan has created. Watch the Yen end up at an all time high against every other currency including the dollar as that carry unwinds. Which is a problem in itself because of the debt load they have.

The US official position on China is US wants China to allow their currency to strengthen. They going to get the exact opposite if that Peg is broken.

QE or currency depreciation to lesson the burden of debt isn’t working. Nobody gets to keep their gains long enough to lesson the burden. Trade wars are just an end product of not being able to print away the debt burden.

I guess it would go against human nature if all countries lived within their means and didn’t spend money they didn’t actually have. World would be a totally different place if you couldn’t borrow from the future and then print money when you realize the future just isn’t enough.

Interesting. I have noticed that every time trade war is on the agenda the US dollar seems to show strength against Euro and other asian currencies. An overvalued currency is not exactly the way to ensure a better trade balance, so I can see how currency can be used as a weapon.

No country has to submit its currency to FX trading. Hasn’t China proven that?

Hell, even if you do trade it, behold the Japanese yen. No one can print more than they have. It generated no inflation and it generated no currency collapse.

Money is a substance created by whim from nothingness. No such thing has to make any sense.

I kind of see your point with the “money is created through nothingness”. Low inflation would however not last if there is scarcely not enough energy around though. Your argument is counterintuitive; a lot of money easily available and scarce resources. Would you not get what you need if you have the money? Imagine the scenario: Pressure builds up, nobody wants to stand in lane for petrol and all kind of companies would claim they need the diesel to make the economy go around. Airlines screaming for more kerosine. Price would go to a certain point, then it would be all state control maybe. Or if not, way too high. Price, rationing and incentives to produce more would be in danger of being regulated (oil, natural gas or even better renewables if competitive).

You don’t win a ‘trade war’ by installing artificial barriers or punitive measures.

You must compete. Develop your strengths. Be disciplined.

That is why China is doing better.

They are focused, hungry, and much more disciplined.

We are easy prey, and Trump is pursuing a lose-lose policy.

Secondly, at some point in the next year there is a real possibility that the republican party will decide that it is time to dump trump [what took so long?], or the voters will. He will not go quietly I fear. Major tantrum. He is the kind who would burn down the house rather than admit to himself that he is loathed- narcissist nightmare.

No one else did ANYTHING. He has taken action. How long was the trade differential to be tolerated? Concentrate on that last sentence and ignore all media.

Watcher.

Maybe do some reading on the subject of trade deficits.

Pretty telling this morning when Trump supporter Rick Santelli agreed that we will only know in hindsight if the tariffs were a good idea.

Santelli also admitted if they don’t work by 2020 elections the R’s will be swept out of office.

Shallow Sand,

Hey tariffs worked great in the 1930s, what could possibly go wrong? 🙂

I recently participated in the restoration of the computer and electronics system of a flooded late model Cadillac. If you look at the different sensors and control modules you will find parts manufactured and assembled in various countries such as Canada, Mexico, Hungary, etc, etc… If you look inside those modules you will find computer chips and components from all corners of the globe, such as Malaysia, Philippines, Taiwan, Vietnam, etc… Where do you suppose the minerals and rare earths come from?

Do you even understand how interconnected the global supply chain actually is…

.

Trade deficits have nothing to do with “fair” trade or tariffs.

If a country exports more than it imports it is a net saver — it produces more than it consumes and squirrels away the extra income.

If a country imports more than it exports it a net consumer — it consumes more than it produces and spends its savings or borrows from foreigners to cover its consumption.

America has had a trade deficit for decades because consumers borrow and spend instead of saving. The country wastes immense amounts of oil on a ridiculous transportation system, and that oil (which the country does not have) has to be imported. But instead of offsetting this by cutting spending in other areas, we simply print and export dollars.

The solution to the trade deficit issue is to simply tax the bejesus out of oil consumption.

Holding off on USO options for 2021. It has been said to never try to catch a falling knife. Makes no sense that Dow and oil are attached for awhile, but history tells us it does attach.

Ok, did anyway. 127 calls at 16 jan 21 at .62.

Backwardation has started… !

This could get really ugly.

Brent was in backwardation at $70. And ugly is in the eyes of the beholder. Right now, they are dumping paper barrels to cover. USO performs best in backwardation. We will have a long run on backwardation.

Things are interesting—

https://www.bloomberg.com/news/videos/2019-05-28/oil-analyst-sen-sees-demand-perception-as-main-driver-of-prices-video

From a few days ago….

Here is a good interview with Amrita Sen from Energy Aspects. I think she does a good job with summing up the situation.

One of the conundrums in the oil market lately has been why are we seeing the physical market tight and also we are seeing global oil inventories much higher(about 90 million barrels) than a year ago. If we dig into where inventories have increased it has all come from the U.S. and China. Partly driven by more refinery maintenance than usual because the changeover in fuel standards from bunker fuel for ships at the beginning of next year, refiners are taking extra maintenance now so they can run harder at the end of the year and partly because China has built out a lot of storage. Everywhere else stocks are much lower. Oil on water has plummeted which indicates exports are declining and that tells us that inventories are about to start coming down substantially.

Yeah, that’s what I was guessing.

Or suppose none of that data is reliable. Then what?

Then I guessed wrong, not the first time?

https://www.eia.gov/petroleum/production/

Pretty flat through March.

Yes most of the increase is due to the GoM rather than LTO

US crude oil production in March at 11,905 kb/day up +241 in March

February at 11,664 kb/day, was revised from 11,683 kb/day

Federal Offshore Gulf of Mexico, March at 1,907 up +191 from February 1,716

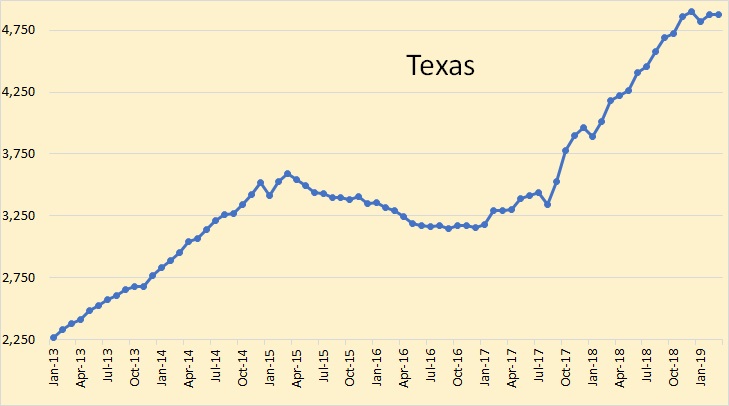

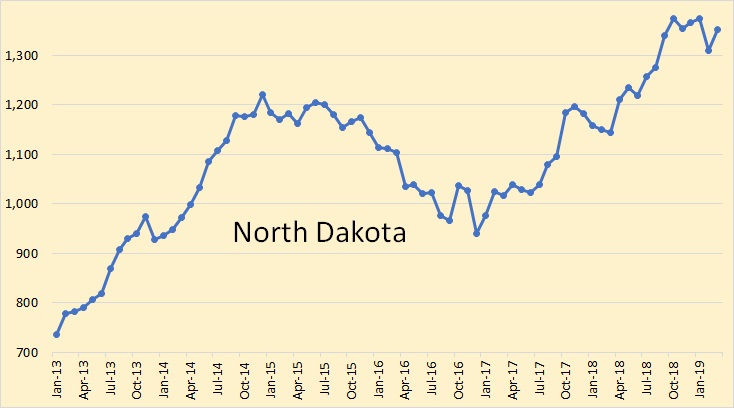

North Dakota +42 kb/day

New Mexico +23 kb/day

Texas down -6 kb/day

Yeah, it was slightly higher Nov 18, so flat the past 5 months for total US. And not higher (except maybe GOM) to current. And no plans for an increase per the RRC permits. Minimum five months from permit to production. Shale can’t stay flat for long at this rate.

GuyM,

Pretty sure if the completion rate stays around the April 2019 level for the Permian that will be enough to keep output either flat or slightly increasing. Once the market wakes up to the impending oil shortage, oil prices will increase and the completion rate might increase a bit. The permit numbers are for new permits I think, I imagine producers have enough permits filed that they can drill what they need, the completion numbers are where the rubber meets the road as it were. Permits suggest intention, completions are real.

The March average of the weeklies was 12,106

And the IEA had 11,948

And the EIA STEO (date May 7th) was 12,005

Yeah, and the latest EIA weekly had 12.3. The May RRC permits will most likely be the predictor for the rest of this year.

Above comments all very interesting. As a Canadian with a son working in the Alberta Patch, plus as a long time Oil Drum/Ron reader, I would like to comment about the often denigrated Oil Sands product. At least you know what you have with Oil Sands and can forecast an accurate production and decline rate. Lay out your grids, sample and drill for cores…do it all over again. Development costs are known as are extraction costs. The only changing factor is wage contracts and interest rates and even those are visible and easier to forecast than guessing at sesmic, dry holes, declining flows, etc. It’s mining. Every shovel scoops this much this fast, every truck takes this long to haul X distance and as the distance increases add trucks. Heavy haulers are now autonomous. Maint is done by contract, rebuilds are forecasted ahead of time and scheduled for, and equipment can even be leased at set rates without production fears. Obviously, the crunch is in price per bbl vrs set production costs, but what isn’t?

These are good 200K per year jobs and are of vital interest to the Canadian economy. I predict the KM Trans Mtn will be started this summer before the next election in October. When it is completed 900K bbl/day will be going on the World market, (most likely to Asia) and not to the US. This will really disrupt a lot of complacency about supplies and current US exports, plus what to do with all the light shale products now able to be blended in US refineries thanks to available heavy Cdn product at a discounted price.

regards Paul S

That’s a powerful pipeline, but there is powerful secretive funding of the First Nations groups opposing it. You’ll need to buy some judges to make this happen, and I think they are already bought.

They just want a piece of the pie, and will, most likely, eventually get it.

Hi Paul,

What is your estimate for URR for the Canadian oil sands? Do the CAPP forecasts seem reasonable to you? Jean Laherrere only estimates a 115 Gb URR for Canadian oil sands. Also what oil price is needed for the more expensive areas (less prospective) to be extracted profitably?

Thanks. Figured you may have done some research, or you sound very knowledgeable in any case.

Hi Paulo. It’s good to hear from you.

Added to the TransMountain expansion, if Enbridge gets to finish the Line 3 replacement that will add 760 000 barrels of crude a day to the US, and the Keystone XL would contribute at least 700 000 bpd for a total of 1 460 000 bpd. It appears that Canada would be in the catbird seat as regards getting its oil to market, finally.

Historically, oil-sands crude has been refined mostly by the Midwest refineries, if memory serves. I’d expect that their source of diluent would be LTO from the Bakken/Permian/Eagle Ford/etc. as long as they pay more than the shippers from the Gulf Coast would.

It will be fun to watch all this play out.

Baker Hughes U.S. Rig Count

Oil: up +3 to 800

Natural Gas: down -2 at 184

BH-> https://bakerhughesrigcount.gcs-web.com/na-rig-count?c=79687&p=irol-reportsother

I have updated the USA graph in the post with the March data. I have also added several states and a few comments.

Thanks Ron,

Even though Texas output is flat, that might be due to a slowdown in conventional output.

What does the flat output in the US mean? Possibly that the crash in oil prices affected the completion rate for new wells, fewer completions means lower output growth (perhaps none). When oil prices rise, the completion rate will rise and output will increase up to about 2025, then falling new well EUR will lead to a short plateau and then decline as fewer wells are completed as profitability falls for new tight oil wells.

Chart below has Permian plus Eagle Ford output, though some of the Permian output is from New Mexico so this doesn’t match up with Texas production exactly. According to the EIA the Eagle Ford has not declined since Jan 2019, output has been flat there, the Permian and Eagle Ford combined saw a 100 kb/d drop in output in January, but by March output was about 50 kb/d above the Dec 2018 output level. For all US tight oil the March 2019 level was only 8 kb/d higher than December 2018, essentially flat.

Yes, there are a lot of other plays other than the horizontal drilling in the EF and Permian. Drops are probably in the Permian conventional, and less drilling in the Austin Chalk which had some monster wells for awhile from EOG efforts. And, I really doubt that EF is maintaining.

GuyM,

I am with you on the Eagle Ford. The EIA seems to be punting on that one, they have the same estimate for Jan, Feb, Mar, and April 2019 for Eagle Ford output, seems doubtful at best. Though when I look at the numbers in greater detail there is a bit of change from month to month.

EF in kb/d, Jan to April 2019

1212.056

1212.139

1212.223

1212.307

I think they may be making this stuff up. 🙂

Yeah, those numbers do NOT seem real.

Even though Texas output is flat, that might be due to a slowdown in conventional output.

So you are suggesting that conventional oil is now declining about the same speed is tight oil is accelerating. I am not surprised. I agree wholeheartedly. It’s just a matter of months now until the decline in tight oil starts to decline. Then both conventional oil and tight oil will be in decline.

Do you agree? Or do you disagree? Interesting? I would love to know.

The May EIA drilling report says:

Bakken: + 16 kb/d, legacy: -67, new wells 83

EF: -1, L: -119, new wells 118

Permian: +56, L -259, New wells +315

The Red Queen is doing a US shale tour. Rystad Energy, who usually claims US shale will continue to grow, says: only 4 of 40 studied shale oil companies had a positive cash flow first quarter.

https://www.oilandgasmiddleeast.com/drilling-production/34061-just-10-of-shale-oil-companies-are-cash-flow-positive-rystad-energy

US shale oil will soon hit a peak. The question is will it be permanent?

Tom,

Unless Brent oil prices remain at $70/bo in 2017$ or lower from now until 2030 (52 week average Brent oil price) US tight oil is unlikely to peak before 2023, my best guess is 2025, and it might be as late as 2027 with low completion rates and oil prices close to the EIA AEO 2018 reference oil price case.

Hi Ron.

My guess is that Texas output will be up slightly over the course of April to Dec 2019, probably 200 to 500 kb/d over that 8 month period.

WTI is down 6.01% as I write this. Wow. Is that a record? Interesting days 🙂

I know this is not an investment website but back in early January I made a bet on oil prices going up. Well that was a good bet, until now when it is nearly even anyway. I just could not decide to sell before some “actors” decided to crash the market. And I am not really a gambling guy or anything, but how much money are made by the guys having inside information? Fortunes, I for sure don’t have it. I hope it all comes crashing down, because the last thing I want to see is the smug faces of the ones cheating in the market place (Btw don’t worry about me, more than 80% of my assets are relatively safe – if energy related could ever be safe).

I wouldn’t sell now!!!!

Inside information?

What information could there be that would tell you anything?

This has to be the most illogical and insane day I have seen in the price of oil. No connection to reality, or even perceived reality.

Is this not temporary Trump tariff tomfoolery?

Problem is most of Trump’s tariff tomfoolery will have a long-lasting effect, not all that temporary. We elected an idiot for a president.

I think countries are looking for ways to reduce dependence on the US. And it doesn’t help that we have now proven that we will abandon agreements as it suits us.

I think Trump is permanently shifting the US in the world. I don’t think the Chinese model is preferable to what we might have offered, but the country is bigger, thinks in terms of longer range plans, and appears to have a smarter leader.

Plus I think they have a better grasp of defense spending. They better understand how to undercut us without the need for conventional warfare.

Neither the Chinese model nor the US model looks particularly appealing right now, but I think Trump is incapable of mobilizing the world against China. And I don’t necessarily want that anyway.

I think Trump is permanently shifting the US in the world.

Trump is like a bull in a china shop. He has no idea what he is doing. He is just willy-nilly putting tariffs on everything. He thinks he is fixing things when he is really screwing everything up. Trump is an idiot. We elected an idiot for our president.

Will we survive this stupid idiot of a president? I have no idea but it will be difficult.

“He has no idea what he is doing”

Wrong, he knows exactly what he is doing. It’s just not in most Americans interest. That’s the plan. Our democracy has been and is under attack by a welcome trojan horse. Pelosi is waiting for Americans to wake up and care. But The Bachelorette is starting a new season, the Angry Bird app downloads for free and understanding politics isn’t fun.

Wrong, he knows exactly what he is doing.

Not so sure.

He is a 6 times bankrupt scammer from Queens.

No one would touch him, as he had ripped so many people (except the Russians and Deutsche Bank- for some pretty interesting reasons).

Being a scammer, he has those instincts, but not that smart.

You may be right, but the morally challenging behavior has me questioning.

He may be what late stage capitalism needs in a “leader”.

Your belief in late stage capitalism is a scam perpetrated on the electorate to accept failure as the powerful concentrate power. Don’t help wheel the horse(a stacked court, deregulation, tax cuts) inside the gate.

Don’t be a victim, salud

Really?

Some political literacy is needed.

Hmmm! I wonder what would happen if the Russians are forced to take a loss on their investment in Trump (IOW it turns out he has scammed them) and start to think that DJT is a liability to them?

I don’t believe your wondering, you know better.

Trump is a wrecking ball to American democracy. The Russian gift that just keeps on giving. Putin is going to double down for 2020.

https://www.patheos.com/blogs/dispatches/2019/05/31/is-trump-the-worlds-most-petty-man-ever/

Whatever you think of John Mccain politically, he was a POW at the Hanoi Hilton.

Trump is a draft dodger because of a “bone spur” in his foot. But he can’t remember which foot.

Forcing the US Navy to move a ship with John Mccains name on it is a disgrace.

Without the US Navy, the strait of hormuz would be controlled by rapscallions.

Woot Woot!

McCain has been tainted for a very long time, since the S&L Crisis in the 1980. More recently he’s been in several photos with confirmed terrorists that were fighting in Syria. McCain is not a nice guy.