This post reviews my method for estimating output from tight oil and shale gas plays. The basic method involves convolution which sounds complicated (pr perhaps convoluted) but is fairly simple to accomplish using a spreadsheet. It may be helpful to review my post on this from over 11 years ago at this link.

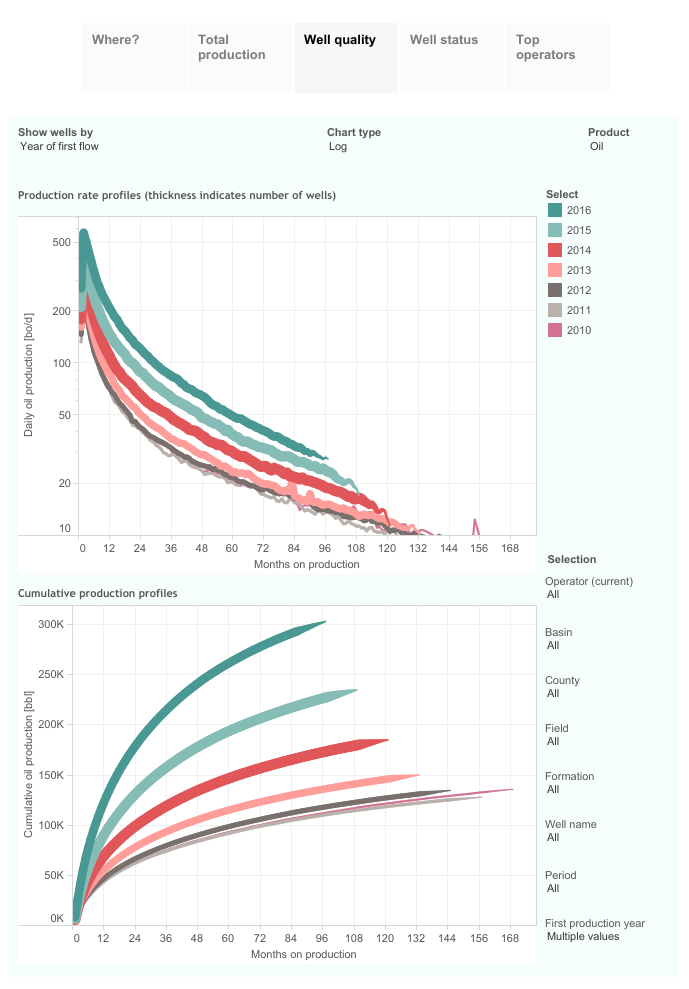

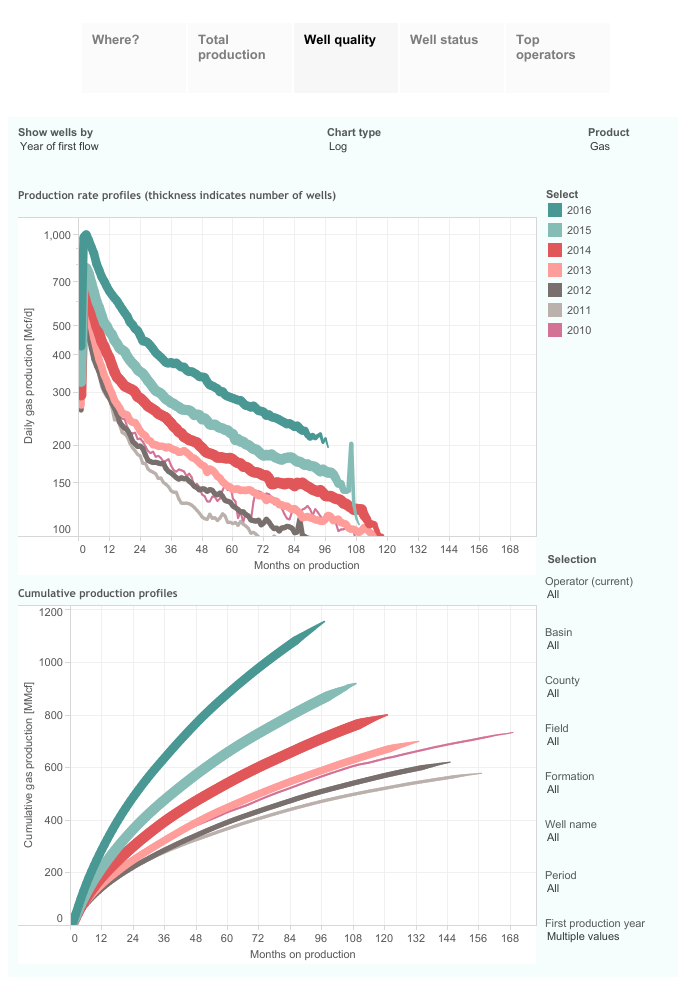

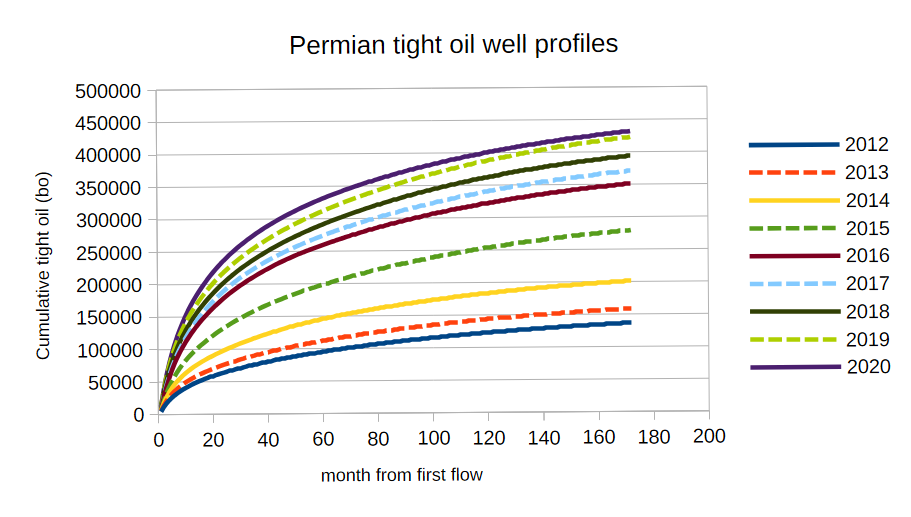

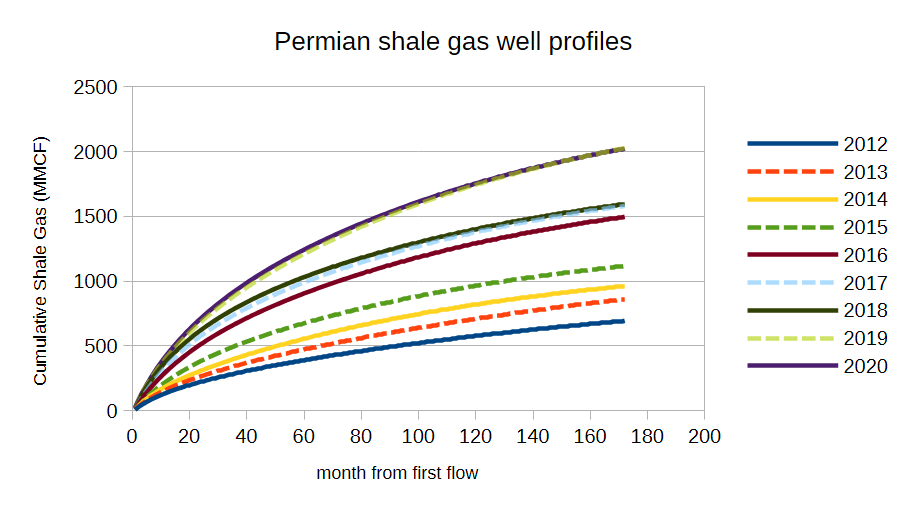

The two charts above show the average Permian Basin wells by year of first flow from 2010 to 2016 for both tight oil and shale gas for all horizontal wells completed in the Permian Basin, I used the well quality tab in a post by Enno Peters linked here to grab these charts. Links directly to these charts are here for first chart and here for second chart. At each of these links the data can be explored in greater detail.

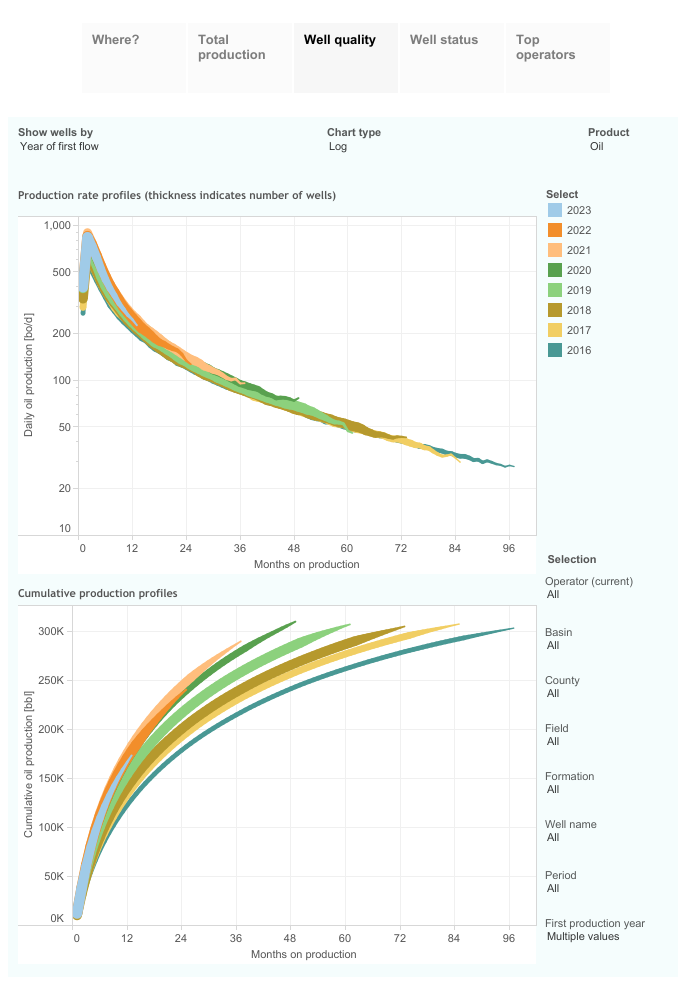

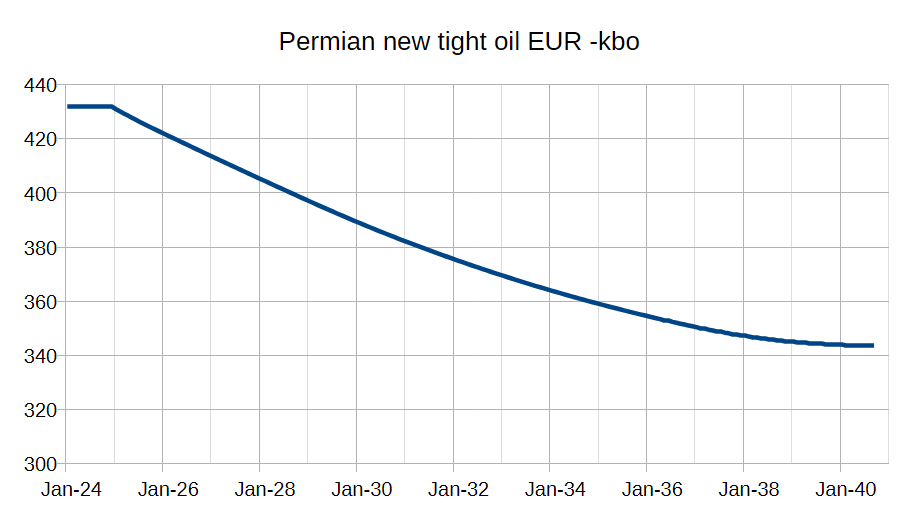

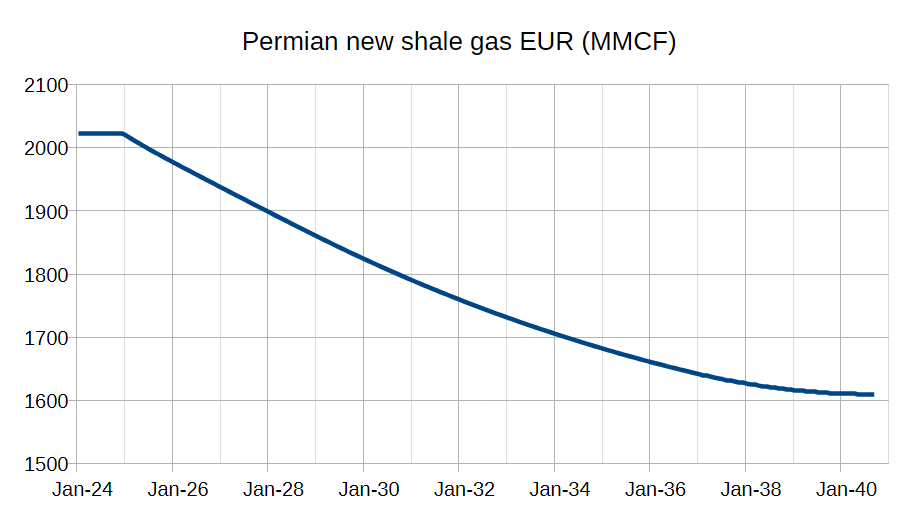

The second pair of charts shows average Permian Basin well profiles by year of first flow from 2016 to 2023 for both tight oil and shale gas. Links to the charts are here for tight oil and here for shale gas. Note that after 2020 for tight oil and 2021 for shale gas the well profiles stop increasing and in the case of tight oil decrease after 2022. These charts are not normalized for lateral length. The average lateral length has been increasing from 2010 to 2023, after 2016 the EUR of tight oil for the average Permian tight oil well when normalized to 10 thousand lateral feet has been decreasing since 2016 at roughly 2% per year.

Convolution

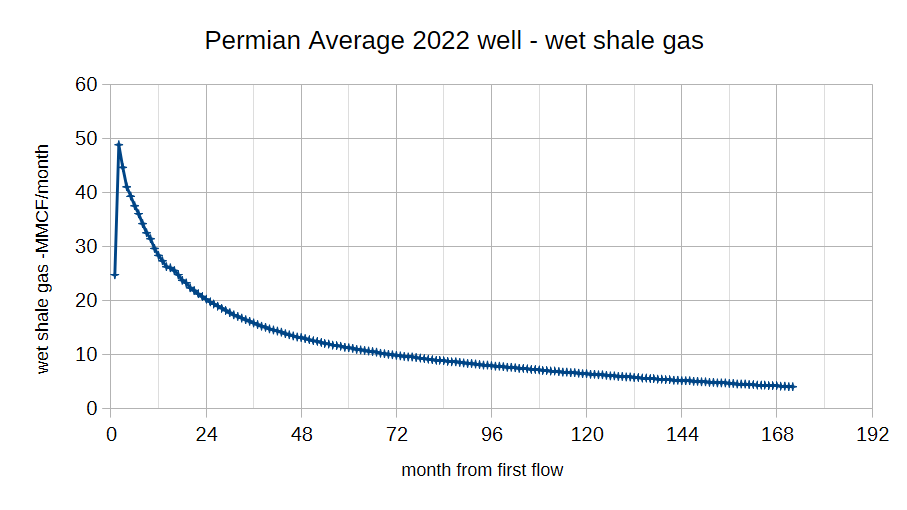

We start with an average well profile in our simple model, this is the average 2022 Permian Basin tight oil well profile.

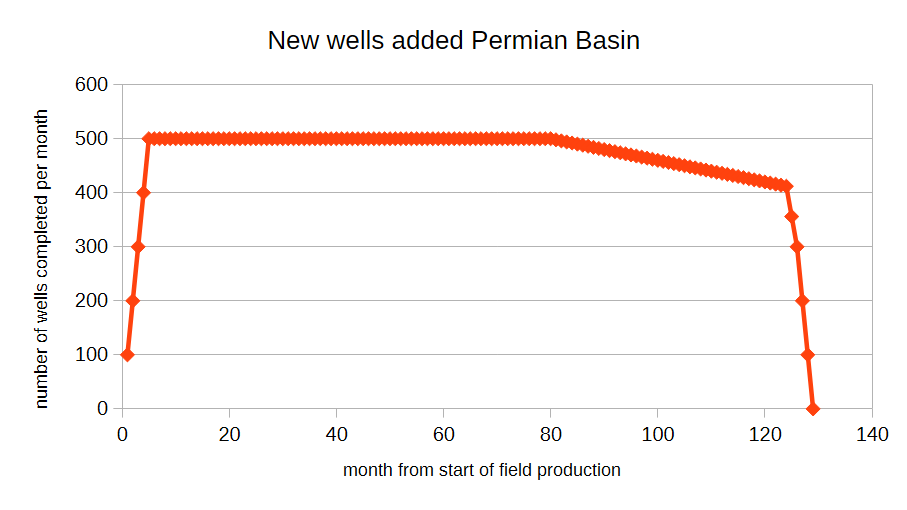

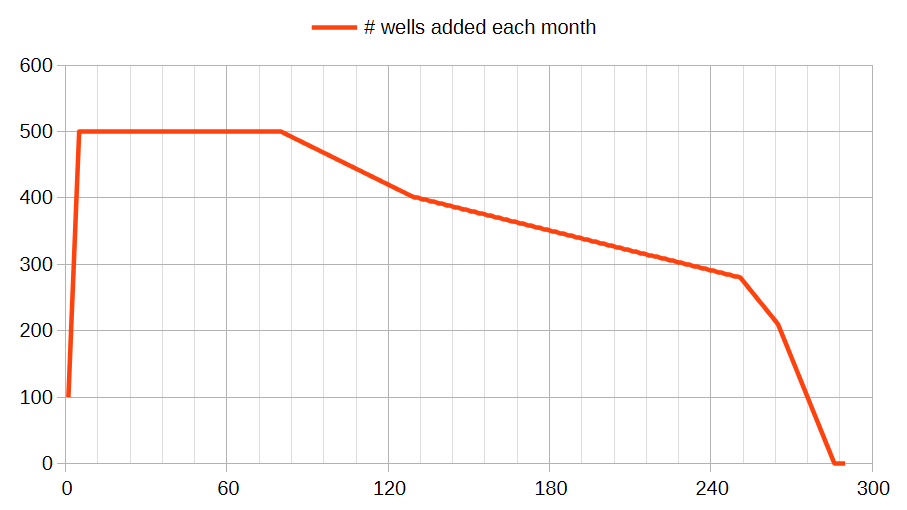

Then we have a chart representing the number of new wells added each month.

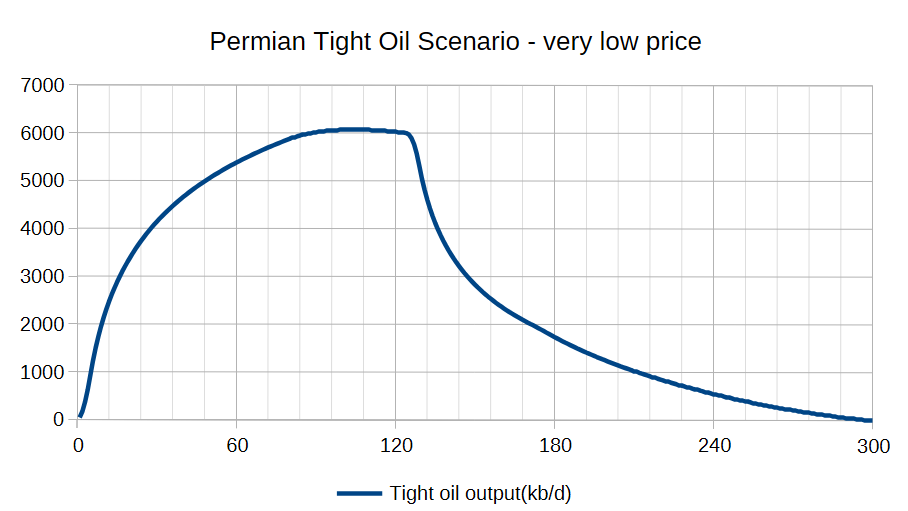

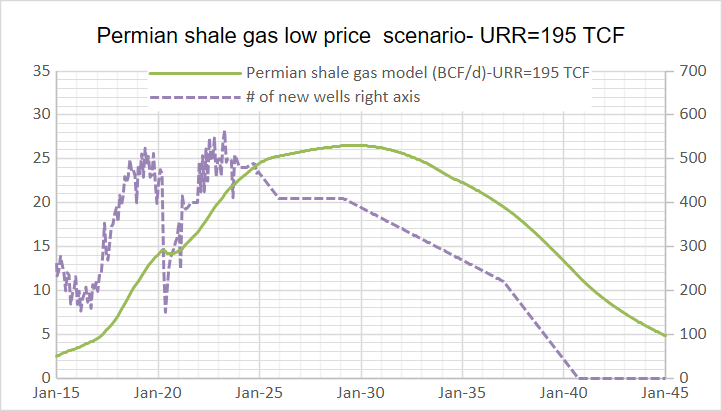

Wells are added from month 1 to month 129 in this scenario, the spreadsheet with the scenario can be downloaded here. This represents a very low price scenario, WTI under $45/b in 2025$.

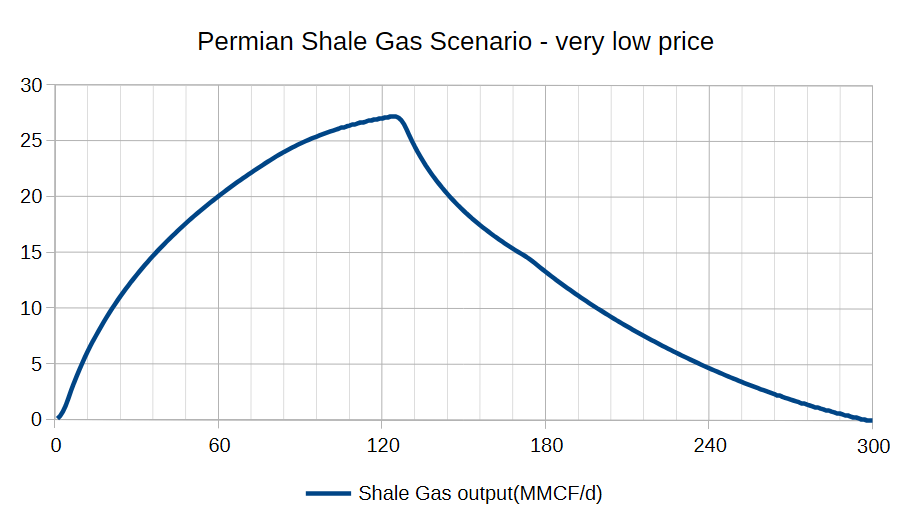

For the shale gas output for the scenario above we use the same chart for new wells added as presented earlier, but use the shale gas well profile below.

The spreadsheet is here for this shale gas scenario.

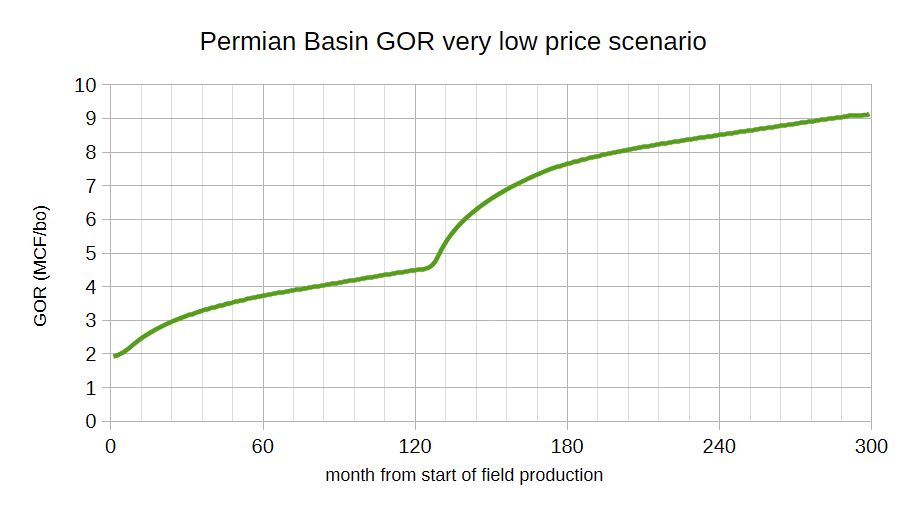

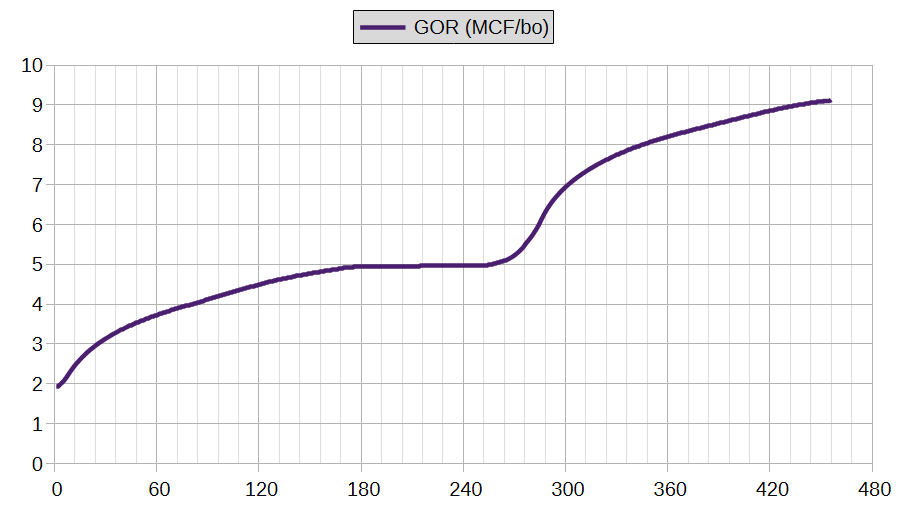

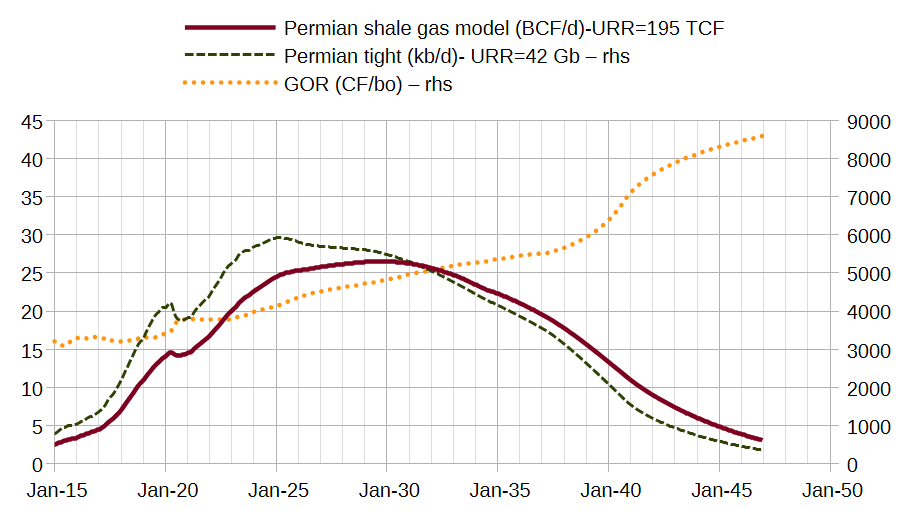

The GOR for this scenario (in second spreadsheet) is below.

To create a more realistic scenario we can use three scenarios and stitch them together as we need about 300 months or more to create a realistic scenario with about 108 thousand completed wells for a low oil price scenario (WTI is $65/b or less). For tight oil the results of the three spreadsheets are combined in the first here, the second spreadsheet (convolution 2) is here, and the third spreadsheet (convolution 3) is here. For the shale gas scenario there are also three spreadsheets, one, two, and three.

This is the number of new wells added per month for the scenario, note that the tight oil and shale gas well profile is unchanged from the short 129 month scenario (very low price scenario). The convolution spreadsheets result in the following output for tight oil and shale gas, see chart below.

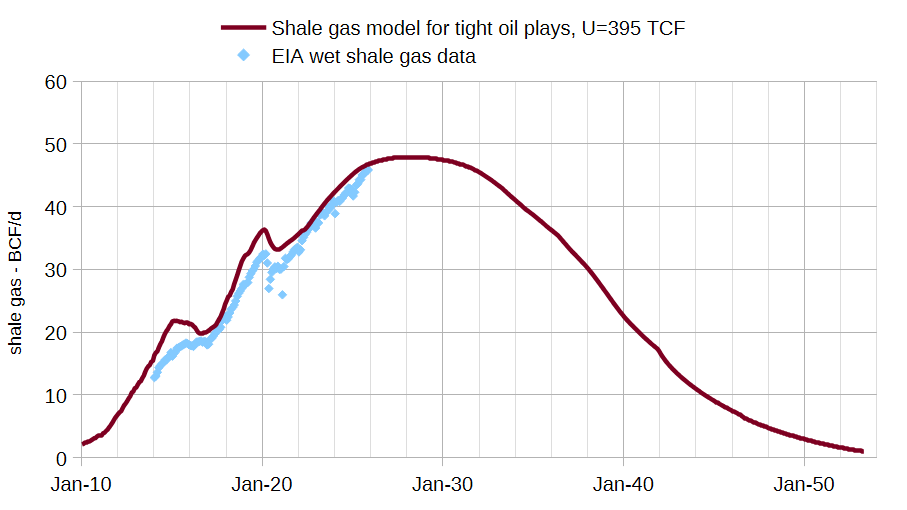

The tight oil scenario has a URR of 47 Gb and the shale gas scenario has a URR of 219 TCF.

The Chart above shows the GOR for the low price scenario presented in the previous chart, total wells completed for the scenario is 108 thousand wells. The URR for this scenario is optimistic because no degradation of new well EUR is assumed after 2021, pressure depletion has been evident since at least 2022 and probably started in 2017 (but is hidden by increasing lateral length), when we account for this by normalizing for lateral length the degradation in new well EUR begins in 2017.

The two previous charts show how the Average Permian well profile changed from 2012 to 2020. The tight oil well profiles for 2022 and 2023 were very similar to 2020, with 2021 about 4% higher, I assume that the 2024 average new well was similar to 2022 and 2023. For shale gas the average 2021 well has an EUR about 3.37% higher than 2020 and the 2022 and 2023 wells look very similar to 2021. I assume the 2024 well is also the same EUR as 2021-2023 average wells.

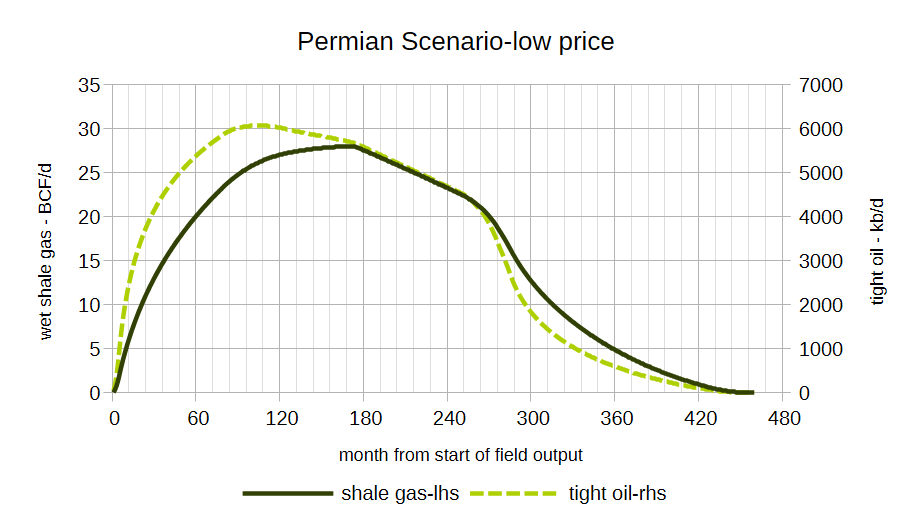

I assume the average Permian well suffers pressure depletion which reduces new well EUR as shown in the two charts above for the low oil and natural gas price scenario presented below. This scenario also assumes about 108 thousand wells are completed from Jan 2010 to August 2040. About 55 thousand horizontal Permian wells have been completed through September 2025. Analyses by Jorge Garzon of Novilabs of the Midland and Delaware sub-basins of the Permian (click links for details) suggest about 52 thousand locations with tier one or tier two economics remain in the Permian. For the low prices that I have assumed (consistent with current futures curves for oil and natural gas) I believe only locations with tier one or tier two economics will be viable.

Spreadsheet with tight oil scenario above can be downloaded here (about 5 Megabytes).

Spreadsheet for shale gas output for Permian low price scenario shown above is here.

Tight oil, shale gas and GOR for Permian low price scenario in chart above.

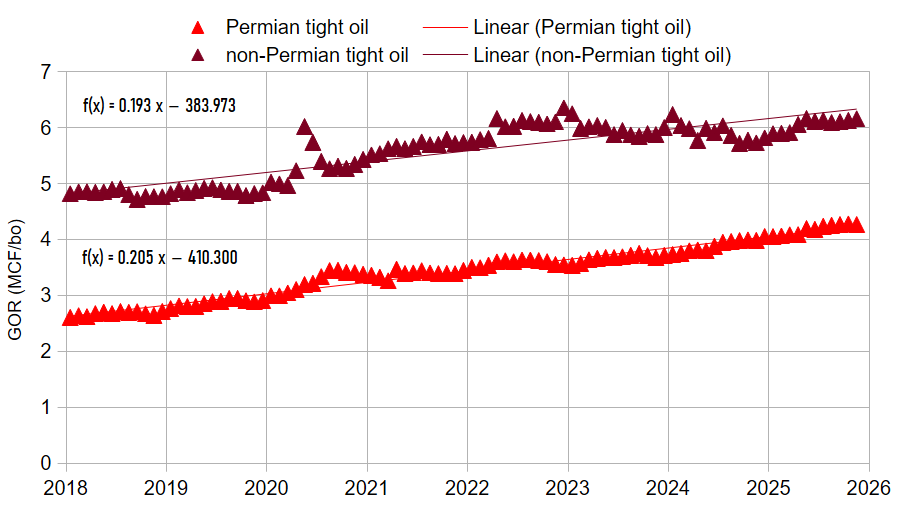

Using EIA data for shale gas and tight oil for the Permian and non-Permian tight oil plays we find that from 2018 to 2025 the trend in GOR has a similar slope (an increase of about 0.2 MCF/bo per year). The average difference in GOR is about 2 MCF/bo over this period with non-Permian tight oil having a higher GOR average than the Permian basin.

To get a rough estimate of US Shale Gas from tight oil plays in a low price scenario I use the Permian GOR shown in the chart before previous chart (second chart up) and add 2 MCF/bo to approximate GOR for non-Permian tight oil.

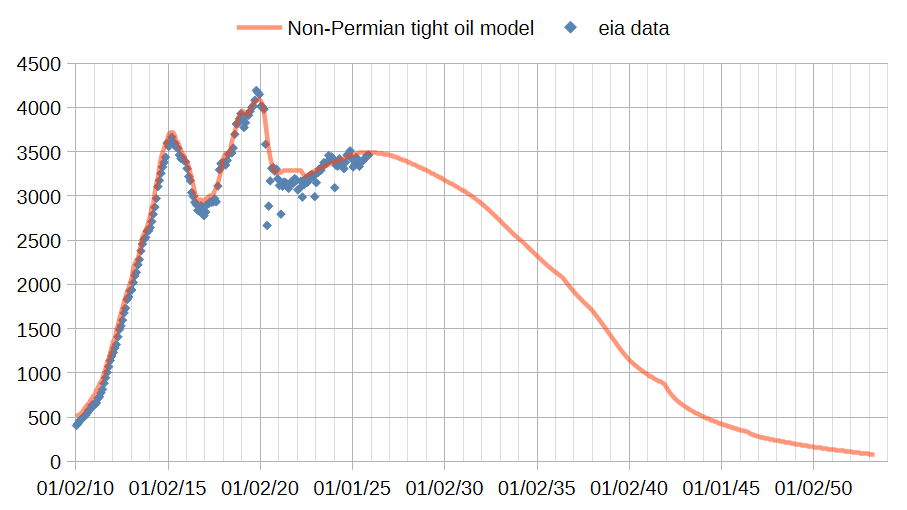

The chart above has a non-Permian US tight oil scenario for a medium price scenario for oil and natural gas (oil=75/b and gas $4/MCF), this is multiplied by the GOR scenario I referenced earlier (2 MCF/bo added to Permian scenario over the Jan 2010 to April 2053 period.)

The scenario above adds the Permian shale gas to the non -Permian tight oil associated shale gas, the model is very approximate with the GOR used as a short cut to approximate shale gas output from several distinct tight oil plays (Bakken, Eagle Ford, Niobrara, Woodford, Mississippian, Uinta, and Powder River. Note that over the 12 year period from Jan 2014 to November 2025, the model mostly over estimates shale gas output, so the model might be on the optimistic side. In addition the medium price tight oil scenario probably overestimates non-Permian tight oil for a low price scenario by 25% or so which would also tend to make the scenario above too optimistic. In any case the future is always unknown. Scenario in spreadsheet here.

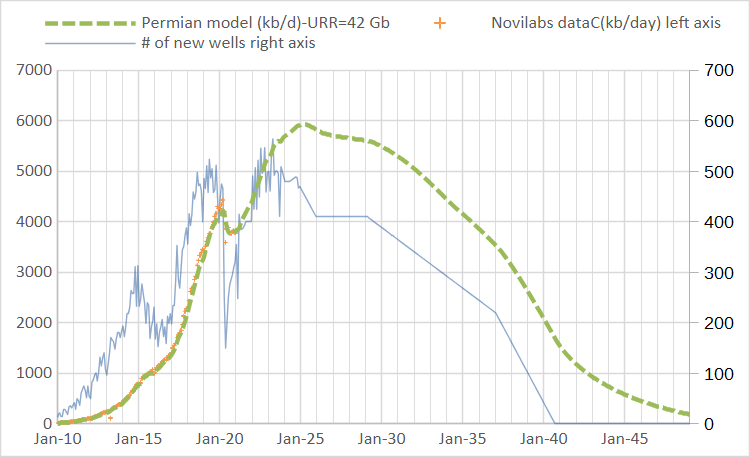

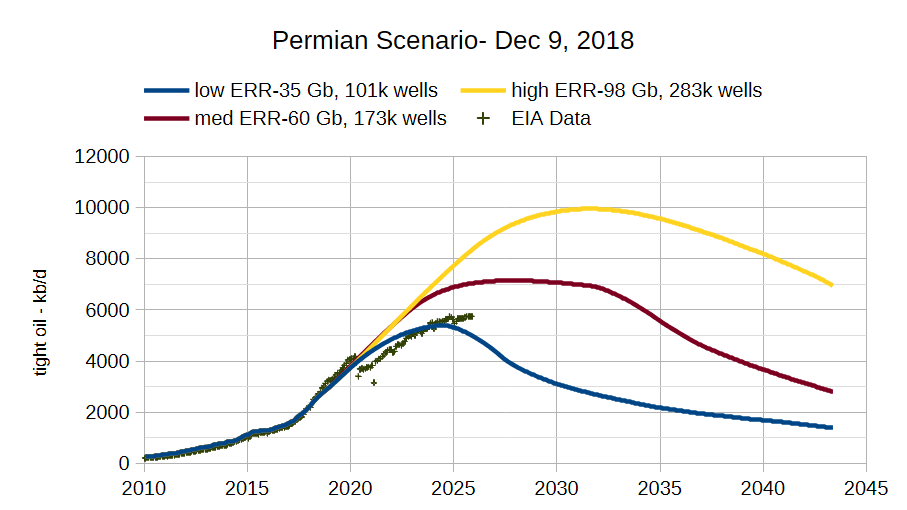

Above is a model I did in December 2018, my current best estimate for low, medium and high oil price scenario cases have a URR of 42 Gb, 52 Gb and 62 Gb respectively, roughly between my low and medium cases from 2018. The high case from the 2018 model would probably require an oil price of $250/b in 2025$ and natural gas at $10/MCF.

206 responses to “Permian Basin Shale Gas and Tight Oil and Shale Gas from US Tight Oil Plays”

Thanks for putting it down. Will read through. May have several questions, comments. Not just to peck critically…but that is what is needed to process complex article. Again, thanks.

Quick note on the simple low price scenario which used a single well profile for all 108 thousand wells and had a URR of 47 Gb compared to the more realistic scenario (with different well profiles over the 2010 to 2020 period followed by decreasing EUR after 2025 with a URR of 42 Gb. If we assume no decrease in EUR after Dec 2024, with no other changes to the scenario, the URR increases to 44 Gb. The other 3 Gb is due to the higher EUR of the first 27 thousand wells of the “simple scenario” with the single well profile used compared to the more reaslistic scenario with varying well profiles from Jan 2010 to Dec 2019. Clearly we do not know the future rate of decrease of new well EUR. I used the 1.5% annual decrease of normalized EUR over the 2017 to 2022 period as a guide and chose a 2% annual decrease in new well EUR at 6000 wells completed per year, the rate of decrease depends on average completion rate so if the rate of well completion were cut in half to 3000 wells per year the rate of decrease in new well EUR would also be cut in half to 1% per year. Obviously this will not be correct, it is a guess. The optimistic assumption of no decrease in new well EUR increases URR by 4.7%.

Nice work DC

https://www.youtube.com/watch?v=FwU4cGWDAAA

5 minutes

The end of Venezuela is here.

80% of food in Venezuela is bought from oil export revenue; Trump and Hegseth just cut that off

Venezuelan oil would go off the market for years.

This might have cascading effects around the world, leading to a wild ride in 2026

Says the chap in the video

Andre,

Thanks.

It is difficult to stop all oil tanker traffic, this may be Trump full of sound and fury, signifying nothing (from MacBeth). We will see, seems this will not be good for the people of Venezuela.

Venezuela has 3 ports that export oil.

That is nothing for the US Navy to stop.

I want low prices for consumers. Let the oil flow. Iran too. Russia too. I want Mike and Shallow crying. 😉

Don’t dick around with Vz. I hate this war crap, whether from Ds or Rs. Both a bunch of chicken hawks. I only want to fight if it is in America’s interest. And no…drug smuggling is not sufficient for going to war.

Only 40% of the Venezuelan oiltankers is sanctioned by the U.S.

Andre

Let me make several points.

Please look to Guyana to see want oil wealth can do for a country when the leaders have its citizens welfare as their top priority.

Ever since Hugo took power, the people of Venezuela has been the last priority. Gaining and maintaining power is all that matters for the leading elite.

Weather you like it or not Trump and Hegseth have the welfare of the people of the US as a priority and working to stop the 1000,s of drug deaths and ruined lives is what matters to them.

So the Venezuelans are starving but can buy $20,000 of outboard motors to put on a “fishing” boat loaded with a thousand gallons of fuel to race across the ocean.

And don’t forget the millions of dollars of oil given to Cuba so the elites can learn how to set up and run a proper terror and control apparatus so as to maintain their power.

Ervin,

When a nation blows up small boats in international waters with no due process, who is the terrorist? The US was once a nation where the rule of law meant something, now we have war criminals ( and convicted felons) running the show.

I agree Chavez and Maduro have done a poor job leading Venezuela, but also believe regime change often results in very poor results based on the historical record. It is up to the people of Venezuela to do something about Maduro.

Venezuela has mostly suffered as revenue from oil exports decreased both due to lower oil prices and sanctions imposed by the US, especially those on the petroleum industry starting in August 2017. The EU and Canada are also applying sanctions pressure on Venezuela in concert with the US. This has led Venezuela to become closer to Russia and China (Venezuela has been close to Cuba since Chavez came to power in 1997) in order to avoid sanctions.

Not clear there are any easy answers, doubtful a war will improve the lot of the people of Venezuela, but that should be up to them and not the US government.

Not an oil related comment.

Irvin, the few boats from Venezuela aren’t carrying fentanyl for the US as stated by Pete and Donald, it’s most likely cocaine getting transhipped to Africa and Europe. This is less of an example of Pete and Donald acting on America’s best interests than tariffs on Canada to stop fentanyl from Canada where more guns and fentanyl go north to Canada than south from Canada. The majority of fentanyl comes across the border from Mexico in vehicles. If drugs were a real concern for Donald he’d be funding the social system that treats addicts and reduces demand. But he doesn’t and he isn’t.

“ If drugs were a real concern for Donald he’d be funding the social system that treats addicts and reduces demand.”

True. He also wouldn’t be pardoning drug kingpins.

An AI summary(!):

President Donald Trump has pardoned multiple individuals described as “drug kingpins” and high-level drug traffickers during his time in office, a decision that has drawn significant controversy.

The most notable pardons include:

Juan Orlando Hernández: The former President of Honduras was convicted in March 2024 of conspiring to import over 400 tons of cocaine into the U.S. and related weapons offenses, and sentenced to 45 years in prison. Trump granted him a full pardon in December 2025, leading to his release from prison. Trump defended the decision by claiming the case was a “politically motivated” setup by the Biden administration.

Ross Ulbricht: The founder of the “Silk Road” dark web marketplace, which facilitated the anonymous sale of over $200 million in illegal drugs and other illicit goods, received a full pardon in January 2025. He was serving a life sentence without parole, but his case had become a cause célèbre among some in the tech and libertarian communities who viewed his sentence as excessive.

Larry Hoover: The former leader of the Chicago-based Gangster Disciples street gang, described as running one of the largest and most violent drug syndicates in the U.S., had his federal sentence commuted by Trump in May 2025. He was serving multiple life sentences for murder and continuing a criminal enterprise from behind bars.

Garnett Gilbert Smith: A Baltimore drug trafficker who ran a multimillion-dollar cocaine ring and was described by the DEA as “one of the largest cocaine and heroin dealers to be arrested… in recent history” was pardoned by Trump in May 2025.

These actions have been widely criticized as inconsistent with Trump’s “tough on crime” and anti-drug war rhetoric, with critics suggesting they undermine U.S. counter-narcotics efforts and the rule of law.

Always Trump, always Trump, always Trump! AWW…that was a yellow.

https://www.youtube.com/watch?v=ElJe5M54brI

Seems to me that some guy named Jefferson sent our ships to kill pirates in Tripoli. That set the standard for what the US was all about. Monroe issued the Monroe doctrine. Almost 100 years later, the ship Maine’s boiler blew up and we sent troops and invaded Cuba. We wanted a way to get from the Atlantic to the Pacific, so we “took” some land and built a canal. They made it pretty clear how the US would be run. So, here we are, over 100 years later – and everyone is perfectly free to leave. Have a nice day.

“everyone is perfectly free to leave”

Well, sure. The thing is, the US is a democracy. That means that the government operates with the permission of the citizens. The citizens are in charge, and they’re not only free to criticize the government, they’re obligated to. That’s the way it’s supposed to work.

So, if you like living in a country where you’re not allowed to criticize the government, you should really move to Russia or China.

America’s Biggest Oil Field Is Turning Into a Pressure Cooker

Drillers’ injection of wastewater is creating mayhem across the Permian Basin, raising concern about the future of fossil-fuel production there

https://www.wsj.com/business/energy-oil/americas-biggest-oil-field-is-turning-into-a-pressure-cooker-8a1bfe4e?reflink=desktopwebshare_permalink

I am posting this here as it came to the end of OPEC thread

Thanks Professor Korpela,

For me that article is behind a paywall.

https://mishtalk.com/economics/toxic-wastewater-turns-us-largest-oil-field-into-a-pressure-cooker/

Issues with WW disposal are serious but far (very far) from new. This is about the gazillionth article on this….and we should be astuted enough not to react to articlers that pose it as a new concern. A more grown up reaction would be to compare to previous warnings (issues going back 10+ years!) and see what is new.

thanks for the epic reviews and forecasts for Permian!

I would guess when investor realized that the EUR seems to be an invariable no matter how much they put into fracing, so-called magic coke proppant 10%ish increase is just marginal. Under the low price scenario, your off-the-cliff falling is quite possible.

Thanks Sheng Wu.

I am also a skeptic of coke proppant. But “no matter what” is a bridge too far. Go look at the Haynesville renaissance, for example. Remember when that was a post peak, old man play? Yeah…Pepperidge Farms remembers.

ANonymous,

You mentioned Haynesville renaissance, and I want to detail that renaissance.

In the Barnett revolution, they started with conventional text-book fracking, i.e. Massive Hydraulic Fracking (MHF), and it is totally different from todays’ massive slick-water fracking.

They have to use gua gel as proppant carrier, and in many cases, ceramic proppant, both are super expensive. Then, the frac fleet only charge by gel and proppant amount, not the water added.

Then, Nick Steinsberger bravely copied the success at tight sand gas in Union Resources, when he only applied slickwater and very small amount of sand, and this reduces the cost by 50~80%, and IP up 3~20X and EUR up 2~10X.

So, to qualify as revolution, you need some cost-down and production improvements close to what happened in Barnett.

But, when the E&P companies tried to copy the success in Barnett to Haynesville, they revert to text-book MHF, and used gua gel and ceramic proppant, citing the ultra-high pressure much higher than Barnett. This did not change until Haynesville had its first death sentence in 2013, and see off-the-cliff production drop. Then, in 2015, slick water and high strength white sand (from Michigan) were used, and see the IP up 2~5X, and EUR up 2~3X, and even some refrac with water and sand had super stellar wells. This basically repeated the revolution in Barnett more than 10 years ago. Now, they are starting to use local sand?

My impression is that it is more than just cheaper proppants and less gum. That they upped the solids loading and horsepower. CHK’s “Propageddon” was the starter.

There was a good overview on the overall change (I think on HGS, I think by William Demis, while he was at Goldman), but it seems to have disappeared or gone behind a paywall, or I just can’t find it, now.

There are many article overviews. Here is one:

https://archives.datapages.com/data/HGS/vol61/061005/21_hgs610021.htm

See also:

https://www.aapg.org/news-and-media/details/explorer/articleid/44930/new-methods-drive-haynesville-renaissance

Anonymous,

I agree that the larger frac size helps, but the mainstream always only mention the proppant volume, ignoring the slick water amount.

Imaging how ludicrous this logic is against textbook fracking design:

the principle is to use proppant with strength high enough to prop under the formation pressures.

If it over 7Kpsi, we already have to use ceramic to survive, and for Haynesville at over 12Kpsi to over 20Kpsi, using sand is like pumping mud.

Sheng Wu,

I only know the popular version. If there are some subtleties, I just don’t have the basis for them. Something had to be going on though. Look at the incredible rebound of the whole play…even after it peaked. And even at worse prices.

I always sort of wonder about the whole fetishization of “slickwater”. Is that a cost savings or a performance improvement? If cost were not an object and I just wanted performance, would guar be better?

Anonymous,

You could chatbot and easily find out the cost reduction switching from gua-gel to “slickwater”. For slickwater, the concentration is only 1~2% of the water and it is cheap chemical; for gua-gel, the concentration is like 20~30% and is much more expensive to pump the same volume.

The gua-gel is to increase the proppant carrying capability according to textbook, and one should avoid leaking water to the rock volume; and the slickwater only reduce friction and barely have 1/100th of the proppant carrying capability of proppant. So, the proppant to fluid ratio is like 3~5:1 when switching from gua-gel to slick watre, and to pump 10X more proppant, one need to actually pump 100s more liquid volume — but it is so ashamed for experts to say it is water they pumped.

In terms of performance or the key to revolution, it is really the water that did the X3~X>10 magic.

But for any people with normal petroleum production training — they have an inherent resistance to such magic story. You could read my story here,

https://www.linkedin.com/pulse/shale-revolution-arent-when-you-judge-conventional-wisdom-sheng-wu

The fact that a small mainstream “hard core” geologists refuse to admit oil could be produced from shale is based on the fact that they refuse such concept of “volume stimulation” — by which the rock volume permeability is changed by the magic water. Because the textbook of conventional fracking is only increase the contact at the production hole, not the volume, and water is actually harmful to the volume. If the volume permeability is not changed, then oil could not be produced as its viscosity is orders higher than gas. With this logic, they also coined that only “light tight oil” could be produced, i.e. API 35 is the lower limit. But, in the past 5 years facts have proven them wrong, not only API 25 shale oil could be produced, they could actually produce more efficiently than API 45.

Thank you very much for the donated brainpower and explanation DC.

A good chart of the Nat Gas output from the various US basins is attached, from

https://www.eia.gov/todayinenergy/detail.php?id=62283

nat gas

Thanks Hickory,

One problem with those EIA numbers is that shale gas and conventional gas are combined in each region, most of the output is probably shale gas, but it is difficult to get a good read on what is happening.

It’s probably not that big a deal. All of PA was 1 BCF/d, before the shale boom. Presumably that has gone through decline, also. So, it’s a small fraction.

For the Permian, it might be more. Per the DPR, the region was doing 6 BCF/d in 2014. Hard to say if that grew or declined. I would guess declined. There was some vertical drilling over last 10 years. But also even that 2014 number probably includes a fair amount of gas from hz wells.

For that matter, sort of, who cares. I mean…it’s in the region. It’s in the pipes. Would a gas molecule (rose) by any other name smell as sweet? For the customer it’s all production. And same for the midstreamers.

From earlier in the fall a good visual update on the balance of Asia Pacific basin oil production/consumption broken down by country, courtesy of Matt from down under.

For the combined country balance look to figure 9

https://crudeoilpeak.info/peak-oil-in-asia-2024-update

I read it. He does good stuff. Wish he would do more “so what” (the story). Even if wrong, I want some insight/import. Not just graphs. But still….good work.

I really hated the one chart with 3D columns. Such an awful format. and I could not read it either. Better off in a table.

Dennis

I would love to call you names, ridicule you and question the ability of your little gray cells but I won’t. The fact that the best you say “ a poor job leading” speaks volumes about your judgement of what’s right or wrong. Sure capture them and send them to court in the Eastern District of New York. Un*****ing believable. Please explain to me, using all the intelligence you have, why there are open boats cruising at 60 mph powered by $20,000 worth of Honda engines on the open ocean.

Sometimes Dennis you are bewildering.

What is it we celebrate about being American? What are the American freedoms that we honor soldiers for defending?

A big part of it is civil liberties: innocent until proven guilty, a court process with a jury of one’s peers, etc. Police aren’t allowed to just kill people because they’re confident that they’re guilty.

Even worse, soldiers aren’t police: they shouldn’t be used to do police work. Soldiers are supposed to fight wars, not smugglers. And killing civilian smugglers is against military law, and should offend our conscience: it’s absolutely considered a war crime for a reason.

Thank you Nick G!!!!

Thank you Dennis!!!

People like Dennis have a broken moral compass.

Nit picking of every tiny thing in America. Yet strangely silent about real brutality and murder committed by other governments especially those with so called left credentials.

https://www.hrw.org/world-report/2025/country-chapters/venezuela

These people are too stupid to realise that many of the world wars could have been avoided if the brutal dictators were stopped early on. Before they were allowed to build up huge armies.

Iver,

Either one follows the law or does not. I don’t support criminal activity either by the US Government or other governments. The UK can act as policeman of the World if you think that is the proper course. See to it.

I do not support Maduro, it is up to the people of Venezuela to remove him from office, this is what national sovereignty is all about. Try reading and comprehending what is written, it is not difficult.

Ervin,

It is not against the law to travel fast in a small boat. They can be sent to a court in Florida or Texas.

Do you believe in the rule of law?

Keep in mind that rule by executive order can cut both ways. The Trump administration is acting lawlessly, maybe after 2026 Trump will be impeached and removed from office due to his lawless behavior. Senators will no longer be able to make the argument that McConnell made in 2020 that no person is above the law. The Supreme Court has ruled that is not the case for Presidents and it seems the only recourse for a president that does not abide by normal rules of behavior is removal by the Senate after being impeached by the House.

It is doubtful there will be enough Republican Senators with the spine to convict Trump, which is unfortunate.

Keep in mind this will lead to no check on presidential power, a slippery slope to dictatorship.

Dennis

What you are talking about is not the law.

When a person kills somebody they get arrested and put in prison. Maduro, Putin, Chinese mass murderers would never be subject to the law thanks to people like you.

This is why the world is in such chaos.

https://globalinitiative.net/analysis/the-politics-of-murder-criminal-governance-and-targeted-killings-in-south-africa/

When America and other fought to stop North Korea invading the rest of the country they ensured millions of people and their children grew up in a free country.

You just don’t want to contemplate what freedom costs.

Iver,

On occasion interventions work, note that in the case of Korea one side invaded the other. Not the case for Venezuela, Iraq in 2001, Afghanistan, or Syria.

It is not the responsibility of the US to right every wrong in the World. In fact US action in Iraq and Afghanistan may have done more harm than good. Often US regime change as occurred in Iran and Chile put brutal dictators in power.

In any case if you think this is the right thing to do petition your government to do so.

Ervin, I would be very pleased if we could exclude political discussions, especially about such complex topics like Venezuela and Cuba. Peak Oil itself is a very complicated issue and its imminent political and economical consequences are highly demanding in themselves.

Peak Oil: Why the world can’t break its fossil fuel habit bold theirs

Climate change shifted the oil production debate from scarcity to demand. If countries do not deliver on ambitious green pledges, one expert predicts that production may peak within two years, forcing a chaotic decline.

Peak Oil once struck fear into policymakers, businesses and consumers as a looming moment when the world might suck the last drops of black gold from the ground, like a straw reaching the bottom of a milkshake.

The idea was popularized in the 1950s by geologist M. King Hubbert, who warned that US oil production would follow a bell‑shaped curve and eventually hit an unavoidable peak as fields matured and declined.

Climate change has flipped the narrative in recent years. Instead of the fear of scarcity, the debate now centers on when demand will finally peak as the shift to electric vehicles (EV) and other cleaner energy gathers pace.

At the same time, political pushback, from delays to combustion‑engine car bans to rollbacks of EV subsidies, is casting doubt on how fast that transition from fossil fuels will actually happen.

Experts divided on when demand will peak

Opposing views have emerged about when global oil demand will start to decline.

The International Energy Agency (IEA), a Paris-based body representing major oil-consuming nations, projects that demand will flatten to around 102 million barrels per day (bpd) by 2030. In its World Energy Outlook 2025, published last month, the IEA’s main Stated Policies Scenario assumes governments follow through on ambitious energy and climate goals.

OPEC, the Organization of the Petroleum Exporting Countries, takes the opposite view. In its latest long‑term outlook, the oil producer group forecasts that demand will continue to rise for decades and sees no peak before 2050, projecting consumption will reach nearly 123 million bpd by mid‑century.

The organizations share one underlying concern: Supply is becoming harder to sustain. OPEC believes that robust demand growth will justify steady investment to ensure ample reserves from its members for decades to come. The IEA, by contrast, offers a more restrained outlook.

Ron, in my humble opinion, climate change has always been to a certain extent a spin to make peak oil look manageable. This does not mean that ecological aspects of energy use and production have to be ignored. But everything has to be put in its real proportion and has to be related to the interests of strong economic and financial groups.

Westexasfanclub wrote: Ron, in my humble opinion, climate change has always been to a certain extent a spin to make peak oil look manageable.

Really now! Just spin to make peak oil look manageable? No, I don’t think so. I believe it is a real threat to millions of people and animals living in low-lying coastal areas. If anything, it is being denied by right-wing politicians who think it is just a conspiracy of the liberals. However, they have not explained why they would create such a conspiracy.

And that Antarctic glacier is a real threat. That alone could cause sea level rise on half a meter in the next 50 years, or as much as two meters if it should break loose and start sliding much faster.

It’s the Peak Demand concept. Not news. And I look side-eyes at articles that treat it as a new concept. It definitely matters and may in fact happen. (The whole “Stone Age didn’t end for lack of stones” quote from Saudi oil minister.) But an article (or commenters here) who treat it as an aha are way, way, way too simplistic.

You wrote: “Really now! Just spin to make peak oil look manageable? No, I don’t think so. I believe it is a real threat to millions of people and animals living in low-lying coastal areas. If anything, it is being denied by right-wing politicians who think it is just a conspiracy of the liberals. However, they have not explained why they would create such a conspiracy.

And that Antarctic glacier is a real threat. That alone could cause sea level rise on half a meter in the next 50 years, or as much as two meters if it should break loose and start sliding much faster.”

I am not discussing the fact of climate change Ron. But in this civilizational clusterfuck (rising sea levels or peak oil) we obviously have on both sides almost identical timelines and a very similar shape of the projected oil consumption.

So what would I prefer if I were in a powerful position? Tell everybody that we are screwed and that our way of life will end soon due to a lack of energy – or raise carbon taxes and promote renewables with the goal to save the planet? I obviously would chose the latter ( as a consequence there would surge the concept of peak demand). I would do so even if I knew that there were unsurmountable problems on that path – the convenience of a positive, proactive position is simply too tempting. It’s so obvious, you don’t even need a conspiracy to achieve the spin. Everybody simply takes his position out in the open and gradually climate change is weightiing out peak oil. And exactly that is what has happened IMO.

I have heard this argument long ago, maybe on TOD. Peak oil was cast as a more immediate existential threat to a comfortable way of life, while climate change was posed as a challenge that could be mitigated by gradually adopting alternative energy strategies. It’s obvious that the latter is less threatening to the status quo, so that’s why climate change pulls more weight.

But go ahead and make PO your main political platform and see how it works.

We are approaching the point where you may begin to hear more and more talk about geoengineering to counteract combustion related global warming. I suspect that by 2030 this talk will be widespread.

Forced migrations, flood and drought disasters, and escalating property insurance costs around the world will provide lots of motivation.

There are two mechanisms that seem to be worth studying, and perhaps even testing on a small scale.

One is sulfur aerosol dispersal in the high atmosphere (blocks some sunlight, like a volcano)-

https://en.wikipedia.org/wiki/Stratospheric_aerosol_injection

The other is Fe fertilization of ocean phytoplankton (takes carbon to ocean floor)-

https://www.whoi.edu/ocean-learning-hub/ocean-topics/climate-weather/ocean-based-climate-solutions/iron-fertilization/

I am deeply skeptical of any attempts to fix what we are breaking.

But I suspect some nations or corporations will try, at large scale, with or without anyone’s permission.

For example, OPEC could easily fund such an effort so that their products remain readily accepted for combustion and so that their water reservoirs, groundwater and rivers don’t continue to shrink.

Other big entities will have their own motivations…perhaps similar.

Paul Pukite wrote:

But go ahead and make PO your main political platform and see how it works.

Do you really think PO is a political platform? No, it is not, and neither is climate change. Hard facts of nature are not political, even though politicians argue about their validity. That is because politicians see denial as a political advantage and make it a political platform.

I am not arguing for action, one way or the other. That is because my argument would have no effect whatsoever. But I will tell you what the outcome will be. Some will attempt to soften the effects of both the decline of natural resources and climate change, but in the long run, all attempts will be futile. We will keep on doing what we have always done and behaving as we have always behaved. We will continue to take resources and territory from all other species until they have no territory left. Then they will simply die.

We evolved as hunter-gatherers, and we still have all those survival genes. So, doing what we are doing is just in our nature. Every species lives to the limit of its existence. One great ape, Homo sapiens, evolved a trait that gave it a huge and unfair advantage over all other species: intelligence. So once we developed the resources to wipe them out and take over their every niche, we did so.

Again, every species lives to the limit of existence. And, since we can create food supply for many billions, we will continue to do so. But once that food supply starts to dwindle because we have used up all, or most, of our natural resources, it will drop like a rock. And so will our population.

That will happen! It will happen because it is in our nature to continue to behave as we have always behaved. We cannot alter human nature.

It’s hard to say…especially when. To date the alarmist predictions have been too early. TOD and ASPO went bust after all.

I would also consider things like how fertility rate declines with wealth (starting to happen in more and more countries).

And maybe NickG, DennisC, and ElonM will invent some magic unicorn/rainbow clean energy device. 😉

It definitely seems like peak oilers are peaking well before peak oil. Deffeyes and Campbell and Staniford all gone. Meanwhile the world just hit another production record…and you got another failed peak call.

That is revisionist history. The conventional wisdom as determined by deep learning from available sources may be 2005. You may want to come up with a different measure to convince the historians otherwise.

deepseek-po

Record World Oil Production, 11DEC2025 article on this site.

But you go enjoy your deep learning. Along with closed for business ASPO and TOD.

You apparently don’t know how to specify a query. “When did peak oil occur for crude oil?” is a query. Here is another response from a different learning model :

gemini-po

Oh…wow…a query, for a large language model. Kissing cousin to a Google search. I prefer to use my brain, but here:

AI Overview

No, global peak oil (the point of maximum oil extraction before decline) hasn’t definitively happened yet, but experts disagree on when it will, with some predicting it within this decade due to slowing demand (EVs, China’s economy) and others seeing continued supply, though many large fields are past their peak production, and a supply peak might occur before a demand peak, with some forecasting strong annual declines post-2030.

Anonymous,

You claim peak oil too:

anon

Dennis

Nice job.

I am wondering in the chart below is this just tight oil and is it missing conventional oil or some condensate. I note the DPR Permian model shows peak production in December/January, the same as your model, close to 6,750 kb/d. Wondering what oil is missing. Is it the condensate from the NG wells,

Screenshot

Ovi,

This is a model of tight oil from horizontal wells.

See tight oil data in STEO rather than DPR data.

For 2025 Q3 they have Permian tight oil peak at 5.73 Mbpd.

https://www.eia.gov/outlooks/steo/tables/pdf/10btab.pdf

The missing oil is mostly conventional oil that is included in the Permian regional estimates. STEO has Permian regional output at 6.63 Mbpd for 2025 Q3, so about 900 kbpd of that is conventional C+C.

Regardless of who governs or further destroys Venezuela, I wonder

-What percent of their #1 global oil reserves are comprised of Orinoco Tar?

-Is there enough condensate/diluent domestically to get that tar to flow?

-What is the breakeven price for turning that tar into usable liquid fuel?

-What percent of the eventual Orinoco earnings will stay within the boundaries of the country?

-How pissed off will China be when the US renders their investments worthless, what will be the price to pay for that expropriation?

-Will the US escalation result in eventual palatable (for the average Venezuelan) stability, or a persistent long term chaotic state?

-Does Brazil and Colombia end up more or less cooperative/aligned with US?

-Does Marco Rubio end up being seen as a villain, or resolute and wise, by Latin America?

Hickory

Maybe not much of it will go into trucks but very useful anyway

https://en.wikipedia.org/wiki/Bitumen

Most importantly all people deserve to be free and have democracy. People like Dennis have no idea what a dictatorship is like.

Hickory

The big supplier of diluent to Venezuela has been Iran. They have a large condensate component in their C + C I think because of their large NG production.

https://www.argusmedia.com/en/news-and-insights/latest-market-news/2381419-iranian-diluent-boosts-venezuela-s-oil-output

https://www.vortexa.com/insights/mid-august-exports-snapshot

Iver,

I would love to see a democracy in Venezuela, this is up to the people of Venezuela, not me.

Iver.

Do you suppose the US will impose a democracy like ours,

where the leader pardons hundreds of extremists who were convicted for attack on the capital in attempt to disrupt the presidential election?

where gerrymandering prevents fair representation of the population in congress?

where a tiny state (Rhode Island or Wyoming) have as much power in congress as large states (Texas or California)?

Who are we to impose our dysfunction and severe wealth inequality on others?

Don’t fool yourself- this is not about proper governance. We generally tolerate authoritarians just fine, especially those with theocratic and fascist leanings.

Even in our own country.

Dennis

Thankfully most Americans in WW2 were not self justifying cowards and many died in order to get rid evil regimes in Japan and Europe.

You obviously would not have done so, from your own words.

https://www.dailymail.co.uk/sciencetech/article-15412467/Pentagon-report-WWIII-fears-China-missiles.html

“How pissed off will China be when the US renders their investments worthless, what will be the price to pay for that expropriation?”

How bout arming 100 Nuclear ICBMs capable of hitting the US?

First of all, the US doesn’t have the power for an invasion. Feet on the ground would be something too crazy to even consinder it. They can only establish a sea blockade and do some airstrikes. The response to these actions against Venezuela will be asymmetrical, think about Iran and that they control the strait of Hormuz for example.. Over all, these politics will fail, because such pressure is only hardening the Venezuelan government. Rubio and Trump will go down in history as unsuccessful politicians if they don’t get things straight. And for that, I perceive a lack of realism in their politics. From a Latin American point of view I would even say people generally reject any imposition from the north. And when it’s mixed with failure, there won’t be no sympathy at all for the US government.

The US has a lot of light oil, lease condensate, and plant condensate (pentanes plus) and even butane. All useful as diluent. We also need heavy oil for blending.

Howzabout we stop bombing and start trading? They got stuff we want. We got stuff they want.

We are natural partners. Send me a Vz hottie as payment for this brain storm.

Strong comment Hickory!!!

Annoying, eres un cerdo. Pendejo.

WestTexasFanClub said: “I perceive a lack of realism in their politics.”

I agree from the point of view of dealing with Venezuela. The best way to help a dictator is to create an outside enemy which unites a country under it’s existing leadership, and this president fits the role of imperialistic bogeyman perfectly.*

OTOH, I don’t think they really care about Venezuela. I strongly suspect that this is entirely theatre aimed at their voter base in the US. This president thinks in terms of perception, viewer ratings, and keeping a loyal followership. That informs most of his policies. No matter how destructive his policies are, if they keep his followers engaged they’re a success.

Fooling his followers isn’t’ his only goal. This president has a balancing act: he needs to keep his followers fooled and loyal, while he serves his true constituencies: his investments, the wealthy and the FF industry. It’s a balancing act because these constituencies have very different goals and needs. For instance, the true aim of his tariffs is to reduce or eliminate progressive income taxes. That, of course, harms his low income followers, so he has to pretend that he’s trying to protect or grow manufacturing jobs. In reality his tariffs have created enormous uncertainty and therefore only harmed both domestic and foreign investment in US manufacturing, but that doesn’t matter – only perception matters.

Similarly, his attack on wind and solar serves the FF industry but harms consumers (especially AI computing) and the country. And his attack on EVs helps FF but harms the domestic car industry and helps China.

————————————

*The value of bogeymen is something this president understands and values greatly. It’s the entire basis for his destructive foreign policy, including Venezuela, China, Iran and immigration.

Ovi, as far as can find there is very little of the Orinoco Tar being produced currently.

Dennis,

1. A minor comment to start. Mea culpa. The “convolution” gave me pause. What you are doing is (I think) a a many well summation. Generations of wells, by birth month, I guess.

Probably these are mathematically equivalent, but I will stick to thinking of it as a summation as it is more intuitive to me. And that is how I would code it.

“And that is how I would code it.”

waiting ….

I’m looking at the sheet now. He coded it as an addition of wells (or actually month-generation of wells, but each generation is a sum of wells within that generation and then the generations are summed).

It is better to have an intuitive physical understanding, not use fancy words/concepts, when not needed. This is the case in fluid dynamics, economics, wide bandgap semiconductors, market analysis or whatever.

Total production (time) = Sigma well production (time), from 1 to n, over all n wells. (Even the ones that have not started producing or have ceased producing, since the well function is just a “zero” at these parts of the domain.)

That’s more intuitive than star operator and box on box Wiki drawing.

I would also add that the idea of adding all the future wells is very similar to what is actually done for the production from the historic wells. That is just a summary of production from each well to give the field production. Not a fancy schmancy “convolution”. Appropriately named, I might add. 😉

Anonymous,

Any professional AI data scientist understands what convolution means. It’s at the heart of combining neural net layers. Condescending to call it “fancy schmancy” considering it’s importance in data analysis.

2. The 2010 to 2016 charts are interesting. I remember several years ago (c. 2017 or 2018, but I can’t find the thread), Mike saying something about Permian or perhaps PXD) wells getting worse. And I went and looked at Enno’s portal and it showed a very similar story to what you just showed. A story of massive getting better, at that time.

This is not to say that wells always get better as we can see them getting worse (not as dramatically as the got better, but still). But there definitely was a tendency to predict (or even claim observation) of wells getting worse, by peak oilers back in the day, that was a little bit jumping the gun. I think some of your 10+ year old Bakken analyses had a similar tendency, always expecting in the near future for those well to get worse, but they were not…the opposite.

Annoying, I have said numerous times you have the oil and natural gas literacy of an 8th grader; I don’t fault you for wanting to get even with me by lying.

From 2015 to 2022 when shaleprofile.com was bought from Novi Labs, Enno and I were close and we worked together on TRRC regulatory matters. He came to a well location of mine and to supper one night in my home. I had cursory subscriptions to SPC, then Novi, until 2023. I still have access to Novi data as current as November of 2025.

I would never had said that Pioneer wells were getting worse in 2017 because I had something to do with how the production profiles were created at SPC. The same images you saw, I helped create. You can’t find the comment, because I never made it. I have 3,000 SPC and Novi charts indexed; for me to have said that I would have provided proof. There was no proof of that; productivity was, indeed, improving.

Nice try, DH. I am not a peak oiler, just a real oil man.

You’re not.

One cannot project past performance to future results in the oil and gas business unless they live in the numbers matrix and are on an anti-oil agenda. New wells (in the Permian) are getting progressively worse, old wells are declining more rapidly, water is getting to be the single most factor affecting the future of American oil production…I don’t know what you will do with yourself after all these years, Nony.

I could actually care less.

https://www.oilystuff.com/group/oily-stuff/discussion/021eb38d-3fd3-4abe-bc48-124f59ce0a71

For Dennis:

This is an example of your Bakken expectations:

https://oilpeakclimate.blogspot.com/2015/06/eagle-ford-permian-basin-and-bakken-and.html?showComment=1436132391702#c7329748871877860722

“EUR decrease starts in June 2016 and takes 3 years to reach the maximum annual rate of decrease of 7%, wells are added at the rate of 200 wells per month starting in July 2013 and continuing for 250 months, 56,000 wells total.”

—

Back around that time, this seemed like a pretty consistent part of your modeling that soon wells would start getting worse. (Maybe even goalpost moved back as time marched on.) In fact, the Bakken wells got a lot better from 2015 to 2020, not worse.

Nony,

Yes I was wrong, Now they are getting worse, note that I expected an optimum lateral length would be established sooner. If I had been correct and lateral length had not continued to increase, EUR per well would have decreased. EUR per lateral foot has been decreasing for years in the Bakken. Also note that I was expecting about 9 to 11 Gb for Bakken/TF URR back in 2014, still looks about right, probably closer to 9 Gb if prices remain at current level.

Bakken lateral length was pretty stable in 2015-2019.

It’s not just neener, neener “you were wrong”. But why were you wrong? What basis or motivation drove you to make that -7%/yr prediction (a pretty bold one). IOW what did you learn?

Nony,

I made a guess based on logic, my expectation was that technological progress would slow down and that room in the sweet spots would run out and reduce EUR. Note that overall basin URR estimate was about 8.1 Gb in 2015 due to underestimating how many future wells would be drilled and underestimating what would happen to future new well EUR. How quickly EUR would decrease and when was unknown in 2015.

What I have learned is that predicting the future is difficult. Note that I explored different assumptions about decreasing future EUR in post linked below

http://oilpeakclimate.blogspot.com/2013/10/exploring-future-bakken-decrease-in.html

The scenarios ranges from 5 Gb to 17 Gb for TRR for scenarios with 50 thousand total wells, my best guess coincided with the USGS mean TRR estimate of 8.5 Gb for North Dakota Bakken/Three Forks.

Note that number of future wells and the rate that they would be completed was also unknown. I overestimated future completion rate and under estimated future new well EUR.

One of the middle cases from the October 2013 post at link below.

bakken 2013

3. The last 5 years wells Novi chart is excellent also. I agree that they are getting worse last few years.

Thanks especially for showing gas as well. Kudos. I had the idea (hope?) that natty might even be increasing while oil got worse. After all, drilling has been moving to the Delaware, which has higher GORs, for individual wells. So even if oil got worse, didn’t mean gas would. But I agree it has also.

It is interesting that the worsening for gas is less than the worsening for oil. So, perhaps this is some amount of the “moving to the Delaware”, but not enough to flip the switch to better gas.

4. The analysis (for gas, my interest) seems to have an implicit assumption that the price of gas does not matter. E.g. the very low price scenario is a very low OIL price scenario.

Now…I do think the Permian is oily and that this is extremely important to look at oil price, and then associated gas. But it is a complex basin with deep layers and areas that have high gas, low oil. So, looking at gas price also (or at least addressing in discussion) would be useful. Right now, at ~$0 HH, nobody is drilling for dry gas or for mixed wells supported by both fluids. But at $3-4, it is possible they will.

Again, the Permian is extremely rich and complex and does have gassy layers further down. In particular the Barnett.

4. Are you penalizing the new wells, with the expected 2%/yr EUR degradation or not? Like it seems like before you were, but now perhaps not? Did the analysis change versus previous recent graphs?

I just wasn’t even clear from your discussion. (Not even arguing, yet. For now, just asking.)

Nony,

New wells have decreasing EUR at about 1.8% oer year (at 410 new wells per month) starting in Jan 2025. See well profile spreadsheet (left hand column).

On prices I assume low oil, NGL and natural gas prices based on futures curve, I assume at some point soon Permian producers will get closer to Henry Hub prices minus transport cost from Permian by pipeline as more pipelines get built. NGL price is assumed to be 30% of WTI price.

I agree natural gas prices matter.

For a medium price scenario (WTI=$75/b, HH=$4/MCF) cash flow for average 2022 well becomes negative at about 204 months rather than 172 months for low price scenario. Also I assume about 50% of Tier one to tier 3 wells that do not have tier one or tier 2 economics are completed at the medium price scenario and 25% of tier 4 locations get completed, this results in about 140k total wells completed in the Perman for Medium price scenario. See chart below

permian medium price

A. When I look at the spreadsheet logic, I don’t see EUR changing by generation. (Or is it and I am missing the coding.)

B. Is the 1.8% per year the GAS decrease or the OIL decrease? You have a tendency to think of gas as oil. But we know (looking at the charts you provided) that oil has degraded faster than gas.

Nony,

It is both gas and oil with EUR decrease at 1.8% per year, see well profile sheet left column starting in Jan 2025.

5. Also, for gas (my interest), the degradation/yr has been less than oil (after all, we have the “moving to Delaware” trend masking things. So, instead of a 2%/yr, you would want to apply whatever holds for gas.

Nony,

When we look at EUR normalized for lateral length from 2019 to 2022, for tight oil the annual rate of decrease is about 1.7% per year and for shale gas well profiles the annual rate of decrease is about 3.3% per year, roughly 2 times higher. So adjusting for this would make shale gas less plentiful.

Looking at your charts, unnormalized, the charts look closer *(lower degredation) on the gas side than on the oil side. (2021 to 2023). Is that effect different than the 2019 to 2021 one? If you normalize, it ought to affect both of them the same (2021 to 2023), so comparing gas to oil, I saw less of a dropoff.

In any case, even if it IS -3.5%, then THAT is the number to cite. The gas number. Not the oil number. (when we discuss gas.)

I also don’t see in your model how you incorporate any -2% or -3% or whatever per year for any of the EURs. These feels like discussion, but is not a part of the model. Correct?

Nony,

In the first spreadsheets presented the model was “simplified” by assuming no change in well profile. For the “realistic” Permian models towards the end of the post look at the well profile sheet, there is a multiplier in the left column which reduces EUR starting in January 2025 in the well profile sheet. The multiplier is proportional to the number of wells, so if with 400 wells the decrease was 1%, at 800 wells it would be 2% and at 200 wells 0.5%.

6. It seems like there’s an implicit confounding of the normalized degradation to the per well degradation. Your model is in wells, not in lateral feet. If anything, you should put a thumb on the number of wells instead, not the well profile.

Nony,

Either number of wells could change or well profile (doesn’t really matter which we could assume well profile decreases by 10% or wells completed are reduced by 10%, output would be the same in either case.) We do not have lateral length information after 2022, so I assume lateral length is unchanged at 2022 average level in the absence of information. I assume Novi uses average lateral length in 2025 when assessing locations, they do not give us more information on this, so any adjustment would be a guess. Could perhaps be 10% more wells (an extra 5000 wells) if lateral length of assumed wells is at the 2025 level vs the 2023 level (average lateral length increased at about 500 feet per year from 2016 to 2022).

The assumptions on lateral length are not unreasonable. I just wanted to remind of the implicit assumption embedded.

Also, I am probably living in the past where lengths had not yet even gotten to 2 mile, 10,000 ft nominal average yet.

7. With respect to (6), this also brings up the question of what the “locations” in Novi catalog are in terms of average length. If they average X ft and the 2022 reference well averaged Y feet, you would want to compensate for that.

8. I like the idea of looking at the Novi location count. It’s novel and at least not one more USGS usage. This is irrespective of if the number works or looks good or whatever. Just kudos for trying something different.

Could you give a little more detail on what your source was? They have had several articles. And then also have used the tier 1/2 term in different contexts (e.g. ideal geology only, or after accounting for pressure depletion from nearby prior drilling).

[Edit: Just reread and saw the links, will read through. May still have questions, but will look.]

9. Not sure how I feel about T1/2 only. In principle seems reasonable, especially for the $45 WTI case.

Right now there is some drilling of the other tiers going on. So, not sure that none will be drilled at strip prices. E.g. for HBP. But also there is some T1 and 2 that won’t get drilled either because of landowner issues.

Also, it does raise the question of if the 2022 well profile (that so much of the analysis hinges on) is the same as a T1/2 average. Do we know how much T1/2/3/4 was done in 2022?

Nony,

I don’t have information on well profiles by tier, just basin wide averages by year. Most wells completed are probably tier 1 and tier 2 currently. Scenario below assumes EUR decrease starts in June 2029 when wells completed reaches 75k, which is when wells with Tier one economics run out, then the annual rate of decrease is assumed to be 4% per year when the annual completion rate is 4920 per year. Well profile from Jan 2022 to June 2029 assumed constant (no decrease). Title should say URR=259 TCF.

permian gas 2601

Novi had some post or article a while ago that showed depletion of the stock of tiers over time. It can be hard to find stuff from before. But not as hard as searching for old comments here. 😉 I kid.

I did find this presentation, see minute 14:46 and 17:46.

https://novilabs.com/resources/webinar-permian-staying-power-inventory-now-and-through-the-2040s/

It looks like about a third of 2022 was “geologic” lower tiers (even higher, factoring in pressure depletion, maybe to adjust to economic tiers). In any case eliminating all T3 and T4 would be high grading.

10. I think an ultralow price environment will not show continued worse wells. The opposite probably (similar to last note in para 9). We should expect high grading versus recent past. The impact would be more on the number of wells drilled. So, yes…minimal T3 or 4 at $45 WTI. But then the wells might actually have stronger average EURs than 2022. After all…we are cutting the worse ones from the average.

11.

I don’t understand the explication in the para “To create a more realistic scenario we can use three scenarios and stitch them together as we need about 300 months or more to create a realistic scenario with about 108 thousand completed wells for a low oil price scenario (WTI is $65/b or less).”

Like, you showed me that $45 scenario. Can’t you show me a separate strip scenario? 60ish, I guess. And then one that is high (e.g. $75). Perhaps there is some simple location math (low is T1, medium is T1 and 2, high is T1-3…or something analagous.)

Like, I get having 3 separate price scenarios to look at. but why show low (you call it very low) and then some sort of “stitching”.

I’m not even complaining about peakerism. I just don’t track what you are doing.

Nony,

The simple spreadsheet (first one with link) has only 129 rows (just the way I set it up years ago, didn’t want to create a new spreadsheet), so any scenario that lasts longer than 129 months needs a new spreadsheet that covers month 130-258 and another for months 259 to end of scenario. I have links to the three different spreadsheets, the output rows from the second and third spreadsheets are added to the bottom of the first spreadsheet (rows labelled convolution 2 and convolution 3).

The realistic spreadsheet is much larger with 543 rows, but that has a second spreadsheet with well profiles that I thought would create confusion.

The question about fast rampup is due to so few rows in the 129 row spreadsheet, couldn’t get close to current Permian output without fast ramp to 500 wells per month.

12. In chart “new wells added each month”, why does it have that big jump from zero to 500? Shouldn’t it just start at 500?

Similarly for the “# well added each month” chart further down. What is the explanation of the initial ramp?

“US shale oil production has turned negative [year-over-year] for the first time in history[.] That matters. Oil bull markets are born when depletion overwhelms new supply. Once new production can’t offset decline rates, prices do the work. …”

Link.

Not sure what/how exactly he is plotting. The latest 914 showed YOY growth of ~650,000 bopd. I wouldn’t be surprised if we see production turn soon. but it hasn’t been in the 914.

Maybe he is lumping in STEO (and considering it history) or looking at weeklies, which are STEO based. Often see those types of errors. But those aren’t historical data…are modeling/predictive trending.

13. Typical well profile:

a. How are you extending the 2022 Permian gas shale well through later life? (Not disagreeing, just would be nice to see it stated, the hyperbolic or exponential or whatever formula that is used.) Obviously, the historical only gives us 3-4 years, so there must be some extension.

b. And what are you capping end of life at (a X flow rate or Y time?) Obviously this affects EUR. Again, even before critiquing, like to just have stated how the model works.

Nony,

I use an Arps hyperbolic until annual decline rate reaches 12.5%, after that it is exponential decline at 12.5% per year. The Arps is fit to data using solver in excel, minimizing least squares, the 2020 well is used so about 36 months of data, the 2022 well looks very similar to the 2020 well over the period we have data. I use a discounted cash flow analysis looking at 3 stream output (crude, NGL, and gas). Cash flow becomes negative at around 171 months for the low price scenario. See first spreadsheet for well profile output in Barrels per month, output is about 15 b/d when cash flow becomes negative (oil at $60/b, gas at $3/MCF and NGL at $18/b.

a. I am looking at the first gas model, the “very low” price one, I think. Called “convolution-permiangasa”. I can see the typical well stopping production after month 172. That’s a little over a 14 year lifetime. (matches your comments)

b. At what month does the transition from Arps to exponential occur? I tried fiddling with your sheet and back-calculating, and it looks like ~5 year mark. [Not sure exactly as there is a small amount of noise in the reference well profile.]

c. 12.5% seems aggressive (in the peaker favor). I remember the arguments about 10% peakers versus 5% cornies. But we are espousing 12.5% now?

d. Also my understanding is that gas declines slower than oil. (GOR for an individual well increases over time, right?). So the 12.5% terminal decline for GAS seems especially aggressive. Is the oil terminal declining at 15%?

e. I don’t know the details of your cost model, but I have a hard time believing 15 bpd wells are cash negative and get shut in. Especially at the prices you noted. Do we see that in the Bakken? Does Shallow (a stripper well operator) think 15 bpd wells (even hzes, even in the Permian with more water) will get shut in. I wonder if you have some sunk costs (drilling/completion, bonds, land) mixed into your model (those are not cash costs). 15 bpd just seems very early to shut in wells. I guess if there is ton of water maybe. Otherwise, not making sense. I suggest to triple check your cost model.

f. [Edit] Doing the backcalculation, I’ seeing more like ~10% for the last couple years of life. Not 12.5%. Are you sure you put in a 12.5% annual decline?

Nony,

Sorry my explanation was incomplete, I use 12.5% per year for tight oil well profile, starting at month 98, note that first 21 months is Novi data, months 22 to 97 is based on Arps hyperbolic fit to the data and exponential decline after month 97 at 12.5% per year.

For the shale gas well I use a 10% annual decline rate starting at month 83. These decline rates match with the data from older wells and in fact may be optimistic because newer wells have been declining at faster rates and their tails might also show steeper decline.

Nony,

The low price model assumes long term oil prices of about $60/b with natural gas at $3/MCF no sunk costs are part of the net revenue calculation, I assume $18/bo (C+C barrels only) varialble costs and a fixed monthly cost of $25000 per month per well to cover future downhole maintenance. I was told by Fernando Leanme this was standard practice at major oil and gas companies (the fixed plus variable cost model). There are also royalties plus taxes of about 28.5% per barrel on average, I assume transport cost from wellhead to refinery gate averages $5/bo. Company overhead is included as a part of OPEX (often this is G&A in a 10k).

Note that operators often look at well payout when net revenue pays for the D&C for the well, for current Permian wells that cost about 12 million per well this would occur at about 134 months. cash flow becomes negative at month 172 under these assumptions. Total net revenue (not discounted) is $12.194 million at month 172.

10% (gas) doesn’t sound as unreasonable.

I found a paper on old conventional gas wells (30+ years old!) that said the average yearly decline was 6.5% (80-20 was covered by 2.5% to 9.5%). So, I get where people come with a 7% thumbrule. But then again these shale wells are still younger and declining faster, probably, not really in full terminal decline yet. So 10% (gas) not unreasonable for a 6-15 year old well.

I still don’t know about the EOL. Maybe they can cycle the wells? Do you still have to account 25,000/month maintenance for a well when it is idle half the year? (Donno, asking.) I realize these are a little more complicated, given the lateral. And the Permian is waterier than the Bakken.

Somehow, intuitively 15 bpd seems harsh for shutting the well down. I just think the history of U.S. stripper operation argues against it. Maybe the wells get sold to people with lower cost structures than the big guys.

Nony,

The 15 bopd cutoff seemed a bit high when Mr. Shellman first suggested this. The breakeven analysis confirms this at $60/b oil, $18/b NGL and $3/MCF natural gas, higher prices would increase the well life. I have long assumed higher oil prices and have been wrong since about 2015 on this. Maybe prices rise in the future, but I don’t see it in the futures strips, in fact when we account for inflation real prices actually fall, so in that respect my price assumptions are very optimistic relative to the futures strip. So the scenarios would be optimistic if anything. Prices are likely to be lower than my low price scenario in the future. For my medium price scenario (prices about 25% higher than low price scenario) well life is about 204 months (17 years) with cutoff for C+C production at about 10 bo/d.

Interesting article Explaining why OPEC’s Over Production is not Crashing the Price of Oil

China overtakes OPEC+ to become the primary oil price maker

The conventional wisdom on the crude oil markets is that producers like OPEC+ largely control the price of crude oil by changing output levels in order to achieve a desired result.

This shibboleth has been challenged by China in 2025, who used its position as the largest oil importer of the world to set an effective floor and ceiling for prices by increasing or decreasing how much crude was sent into storage tanks.

Prices were stabilized by the production cuts by OPEC+ in 2022. OPEC+ is a grouping of the Organization of Petroleum Exporting Countries (OPEC) and its allies, led by Russia. These gains faded once the organization began to reverse its cuts in April of this year. Faced with a looming glut of oil, OPEC+ decided to hold production steady for the first quarter next year.

China is left to clean up the surplus.

The biggest unknown on the crude market is what China will do in 2026. Beijing’s actions will likely influence the strategies of other participants.

https://www.marinelink.com/blogs/blog/russell-china-overtakes-opec-to-become-the-primary-oil-price-103879

Ovi

that is not a new strategy for China – I observed the same strategy decades ago in their purchasing strategy for pulp and paper products.

Not buying it. OPEC has been watching market response and adjusting its speed in coming off quota. Yeah…China matters, but much more short term than OPEC. It’s not like China can fill storage forever. Net, net: article is midwit.

Interregnum:

I’m going through the spreadsheet now. It’s pretty sweet actually. Still a bit of work for an outsider to parse (not heavily formatted, commented…but also very intuitive.) I am making a list of comments/questions so you don’t have as much of a stream of consciousness to respond to.

I do see where some of my questions from article are answered (like end of life criteria). But not all…and I don’t feel guilty for asking. 😉

The other major piece of work remaining is to look at the Novi analysis (itself) and then see how it was translated into your work. Even as mechanical as checking how many locations Novi cited and then how many wells you have. Haven’t started on that yet.

https://www.msn.com/en-us/news/world/russia-says-ukraine-tried-to-attack-putins-residence/ar-AA1Tegp0

Ukraine bombs Putin

Sheng Wu:

Was looking for the DeMis talk (it may have been at AAPG), and I found this:

https://www.aapg.org/video/articleid/59516/ursula-hammes-gas-giant-the-haynesville-shale-of-east-texas-and-northwest-louisiana

Pretty much a geology overview, not production, but there is a little bit on the renaissance at about minute 29.

There is also some very portentious talk at minutes 9 to 15 and at minute 27, saying people should look at the Waynesville. And this was a 2021 talk! So that term didn’t exist. She talks about the Pinnacle Reef instead.

I would say there is another 3rd life/renaissance for East Haynesville, given the facts:

1. Haynesville has the highest porosity, highest pressure

2. EUR is just on par with Marcellus core or lower, and seems that the pore throat closed earlier or not fully water fracked as Marcellus which has higher sand/quartz content

14. How are you accounting for the gas flow from existing wells? They will have a big impact on the eventual Permian peak and on midstream needs. It seems like your spreadsheet only shows the new well production. How are you estimating existing well production and adding it in for the basin total?

Nony,

Look at the last spreadsheets, Model starts in 2008. There were not that many existing wells at that point and output from any wells that existed in at the end of 2008 would be relatively negligible by now. Here is the medium price scenario 140k total wells for shale gas from Jan 2008 to Jan 2049.

permian med price2512

OK, I found it here:

“Spreadsheet for shale gas output for Permian low price scenario shown above is here.”

This kind of is what would be good for an in depth discussion. There is enough to fill a headpost, no need to pad out with oil or other plays. I’m sure the sheet works logic wise, but is a little hard to read (not a lot of row/column name markers, not clear where transition from historical to predicted occurs, etc.) so fulsome supporting discussion would be useful. I do see how there are differing well profiles by vintage now, I think.

15. On the spreadsheet (gasa), I don’t have much to ask or criticize. It seems to make sense in logic and layout. Doesn’t mean it’s right, if the assumptions are too conserative. But the sheet itself looks good.

I prefer a little more formatting for totals and headers. And showing multiple sheets for inputs (like the well profile) versus hard coding a cut and paste. And prefer to have the outputs on separate worksheets of the Excel, not floating graphs. But…the basic logic of the well count, typical well, generations, addition…the math guts of the thing…that all looks very sweet.

I guess I still need to look at the other two gas sheets. See how they differ.

Also, still need to look into the location math.

The global effort to survive without as much petrol for transport is going to get a boost soon courtesy of Contemporary Amperex Technology Co., Ltd.- CATL, which is the world’s leading designer, manufacturer, and seller of electric vehicle (EV) batteries and energy storage systems (ESS). The low cost and volume leader in the world, by a large margin.

They are on the verge of commercial production of a strong competitor to Lithium by a much less expensive alternative- Sodium. Their lead in the battery race will increase further.

https://cleantechnica.com/2025/12/29/catl-makes-big-announcement-on-sodium-batteries-for-2026/

Seems to me the critical application for electricity storage is in the power grid to complement intermittent solar/wind supply. While more money is available to continue the 5000lb personal vehicle lifestyle it’s that lifestyle that’s sucking up fossil fuels.

OK, I looked at all three spreedsheets, now.

a. They seem to differ mostly in the total number of wells added. I see “gasa” has a little under 60,000 wells added. “gas2” has a little over 43,000 wells added. And then “gas3” has only 3,675 total wells added. I don’t know how to understand this in terms of three different price scenarios. Especially since “gasa” I thought to be your lowest price scenario.

b. There are some differences in the shape of the well addition for each scenario. Not sure why we have to play with that also…but probably the total well count is the major feature, so…oh well. But I sort of would prefer one variable changed at a time. Or if there is some reason for the shape of the well addition curve to differ by price, some explanation/description to explain it.

c. I think the rest of the scenarios (sheets) are just the same in terms of well profile, no difference in well quality. This seems unrealistic. The highest price scenario should have the most wells added, but also a lower average quality well. And visa versa.

d. I think the basic logic/layout of each sheet is the same. (Fine.)

Nony,

The first spreadsheet is months 1 to 129 and second is month 130 to 258 and the third is months 259 to end of scenario. Price scenario is the same for all three of these spreadsheets.

Also output of each of these is included at the bottom of convolutionpermian1 spreadsheet for appropriate months.

OK, Dennis.

Kinda pooping out now. 😉

Probably the bigger spreadsheet would have made more sense to me. I am used to multisheet models for M&A and capex decisions (like a factory consolidation).

But…I’m tired now.

All…cool.

I looked at the two Novi LI posts that you linked to. I don’t see where you are getting the 52,000 Tier 1 and 2 well counts. Suspect there is a different source you are using. (They have had a lot of different posts on the Permian tiering concept.) I sort of want to check the number versus your scenario.

Also, trying to understand if you are using the before or after pressure depletion tier numbers. They have had posts where they said X Tier 1 in terms of geology. But then they did later posts moving some of the wells down because of parent-child. I.e. the effective Tier 1 count was lower.

Also, 52,000 (from your post’s text) is a lower number than your spreadsheet, which has just under 60,000 wells added. Although these are close….just not sure why the difference.

Hi Nony,

The two posts I linked to by Jorge Garzon have for Midland Tier1 economics 6154 wells, and 10065 wells with Tier 2 economics, a total of 16219 wells in Midland with Tier 1 and Tier 2 economics after accounting for pressure depletion.

For Delaware there are 14093 wells with Tier 1 economics and 21884 wells with tier 2 economics for a total of 35977 wells with Tier one or Tier 2 economics in Delaware. Total for Permian is 52196 wells with Tier 1 or Tier 2 economics in Permian Basin. As of July 2025 about 55000 wells had already been completed so total would be 107196 wells if no wells with tier 3 or lower economics were completed.

OK, I looked at the “eye charts” a little closer. 😉

I think I’m done fussing at it. Can’t really comment more until some of my comments/questions are addressed.

I didn’t get into the Permian oil or overall tight oil stuff. Trying to keep my focus on the Permian gas.

Actually I think there’s enough content, you could have just done a headpost on that. Would still be plenty long, especially if you had done some things like explain the typical well profile extension/EUR. But whatever…didn’t hurt me…I just kept my focus on first half of the post.