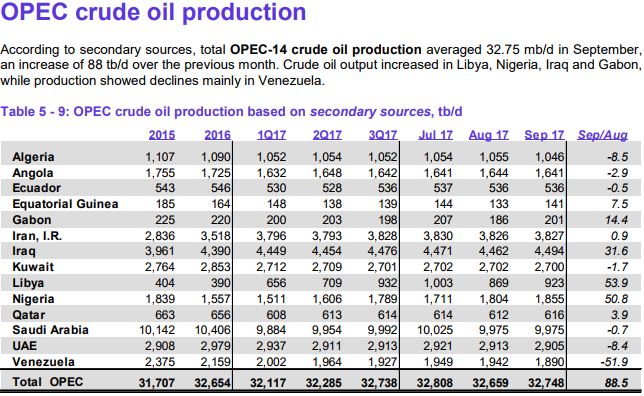

All data below is based on the latest OPEC Monthly Oil Market Report.

All data is through September 2017 and is in thousand barrels per day.

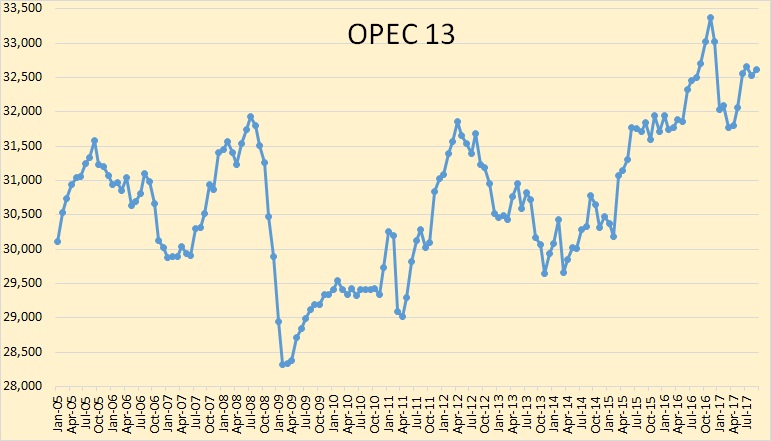

The above chart does not include the 14th member of OPEC that was recently added, Equatorial Guinea. I do not have historical data for Equatorial Guinea so I may not add them at all. OPEC production has held steady for the past four months. Equatorial Guinea production is tiny, 141,000 bpd so their monthly change in production can be ignored without much effect. OPEC 14 production was up 88,000 barrels per day in September. But that was after their August production had been revised downward by 82,000 bpd.

The OPEC 13, (not including Equatorial Guinea), peaked in 2016 at 32,385 kbpd and are down 150 kbpd for the first 9 months of 2017. Please note that when I say “peaked” I mean “peaked so far“. I am well aware of the fact that OPEC, or some OPEC nations may have further peaks in the future.

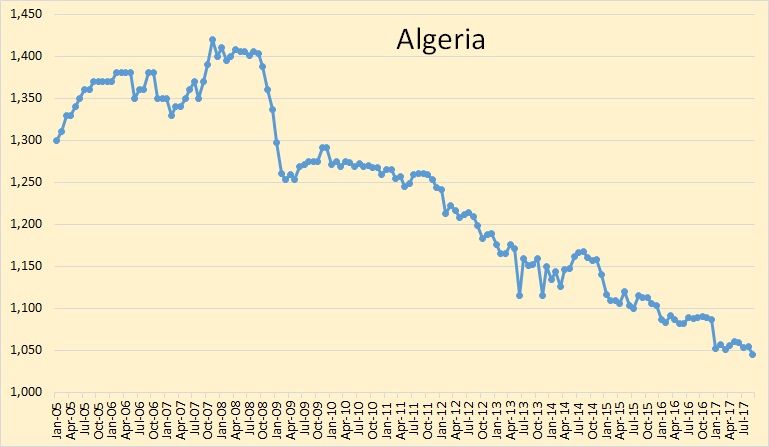

Not much is happening in Algeria. They peaked in 2008 at 1,393 kbpd and their annual average is down 338 kbpd since then.

Note: Here and below the annual average being down from the peak, I am referring to the average of the first 9 months of 2017. And, of course, I am aware that there may be further peaks down the road although that is highly unlikely for all but a couple of OPEC nations. That is because every OPEC nation is currently producing every barrel they possibly can and that includes Saudi Arabia.

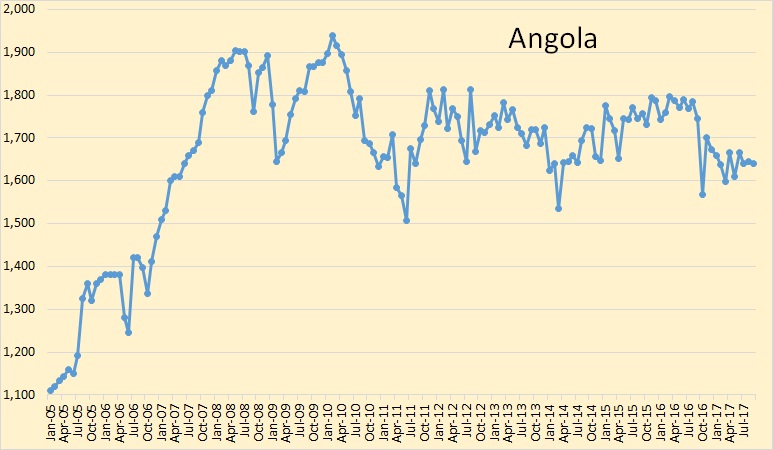

Angola peaked in 2008 at 1,870 kbpd and are down 229 kbpd since then.

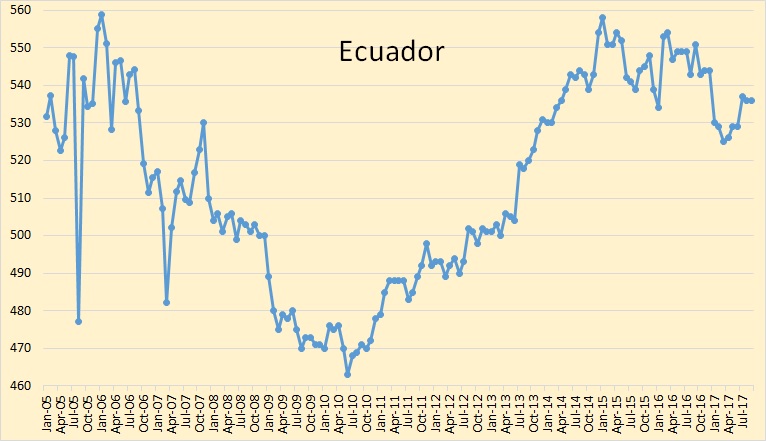

Ecuador peaked in 2015 at 547 kbpd and they are down 16 kbpd since then.

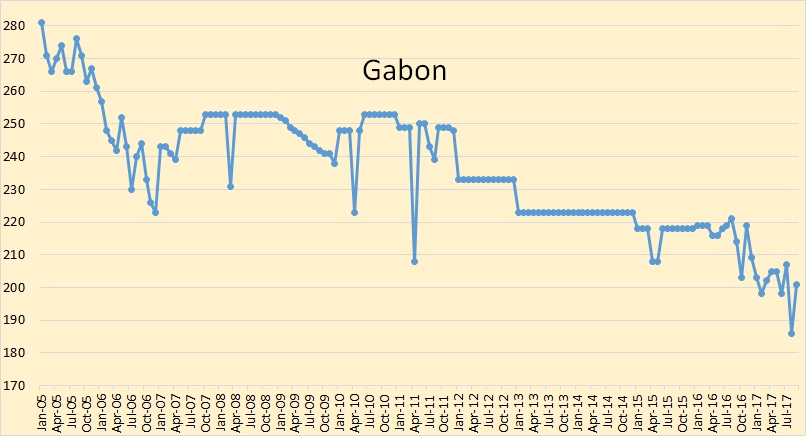

Gabon peaked in 1997 at 230 kbpd and they are down 29 kbpd since then. Note: My annual data only goes back to 1997 so their production could have been higher prior to 1997.

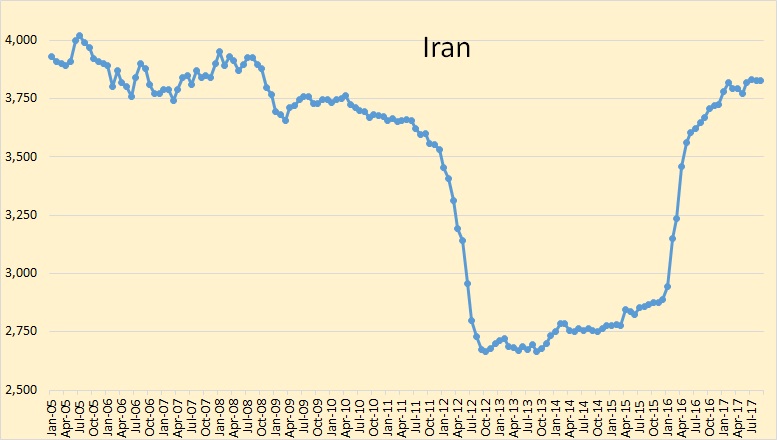

Iran peaked in 2005 at 3,938 kbpd in 2005 and they are down 131 kbpd since then.

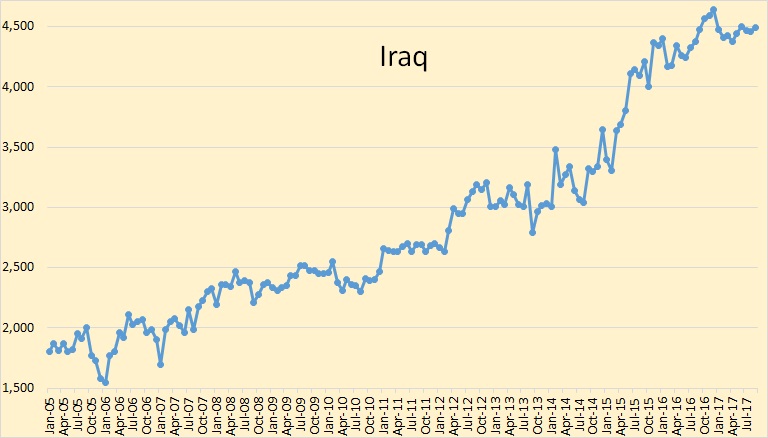

Iraq’s average production, this year, is 4,452 kbpd and that is a new high for them. Iraq is the only OPEC nation to reach an average yearly peak this year.

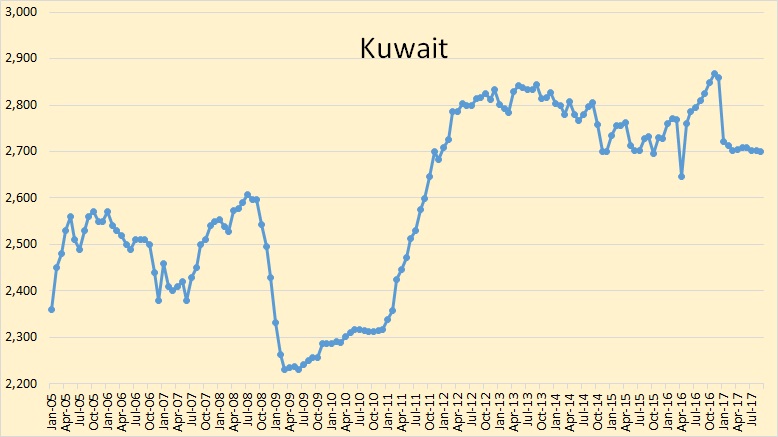

Kuwait peaked in 2012 at 2,794 kbpd and their annual production, this year, is down 87 kbpd since then.

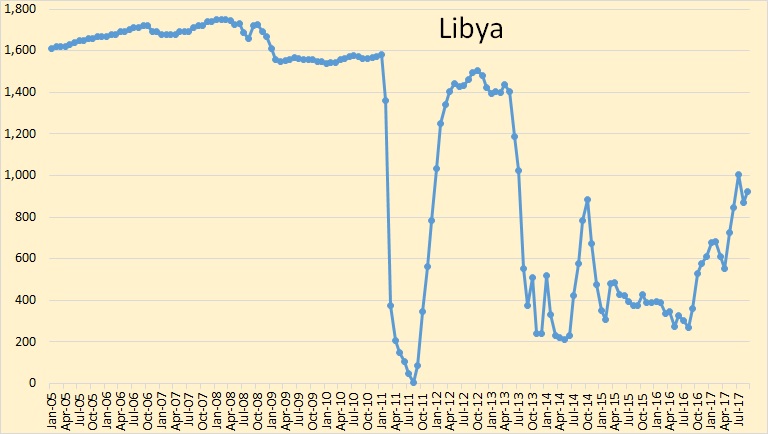

Libya’s production peaked in 2008 at 1,717 kbpd and their annual production is down 951 kbpd since then.

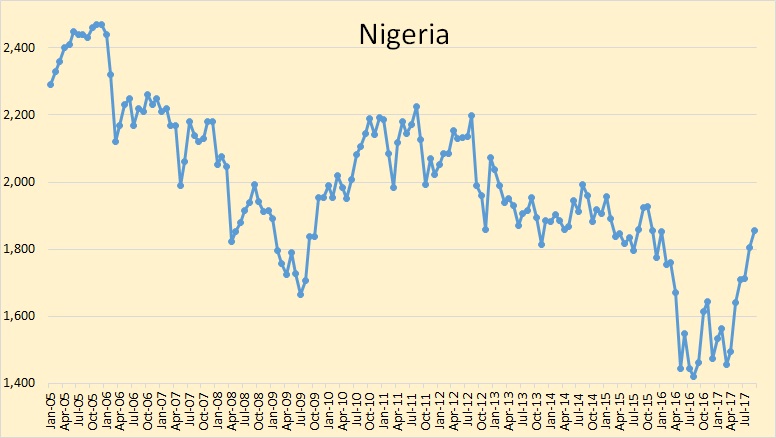

Nigeria’s production peaked in 2005 at 2,413 kbpd and their annual average production is down 717 kbpd since then. Nigeria seems to have solved some of their political problems however. Their annual production should increase further this year and in 2018. But I don’t expect it to reach levels they reached in 2010 and 2011.

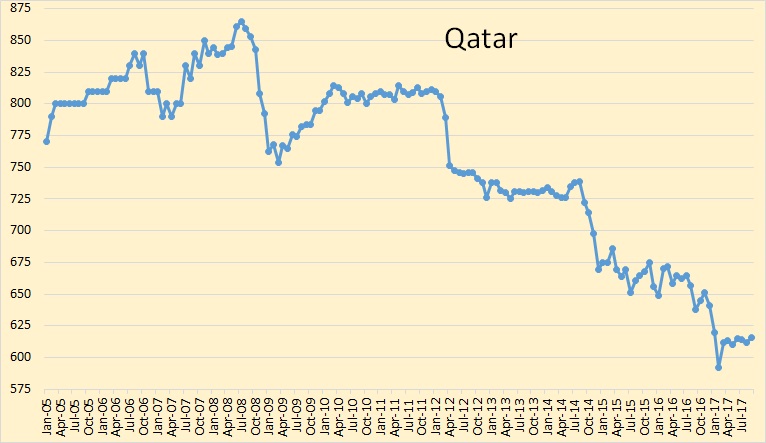

Qatar’s oil production peaked in 2008 at 841 kbpd and they are down 230 kbpd since then. Qatar has the largest percentage, non-political decline of any OPEC nation. That is their very large decline is due entirely to depletion of their reserves.

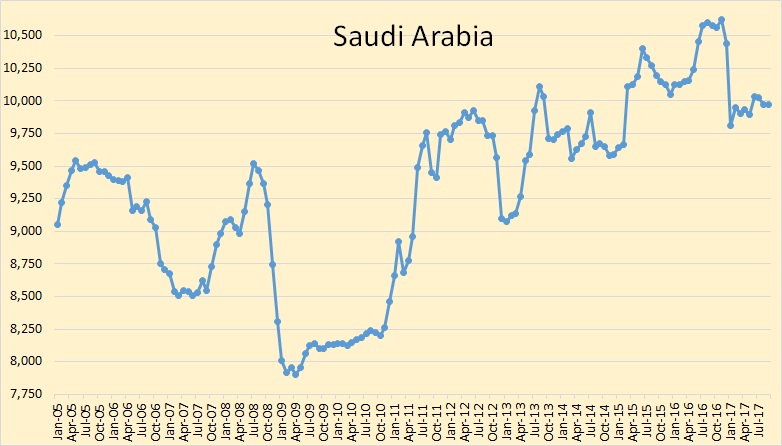

Saudi production peaked in 2016 at 10,338 kbpd and their average production for 2017 is down 443 kbpd so far.

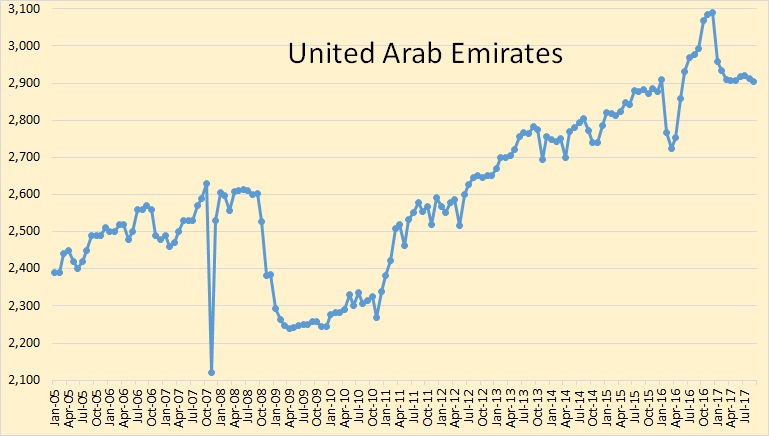

UAE production also peaked in 2016 at 2,927 kbpd and their average production is down only 8 kbpd this year.

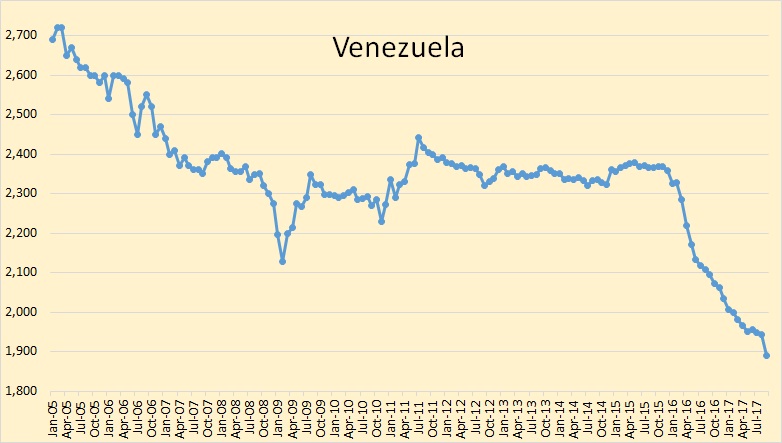

Again, my annual data only goes back to 1997 and that is when I have Venezuela peaking at 3,240 kbpd and their average annual production is down 1,280 kbpd since then. It is unclear as to how much the decline in Venezuela’s production is due to politics. Much of it is no doubt but the political situation there is so desperate that it will likely take decades for them to recover even a small percentage of their decline.

Of Non-OPEC news I need to add Russia’s latest production chart.

Russia’s average for the first 9 months of 2017 is 10,947 kbpd. That is the peak so far.

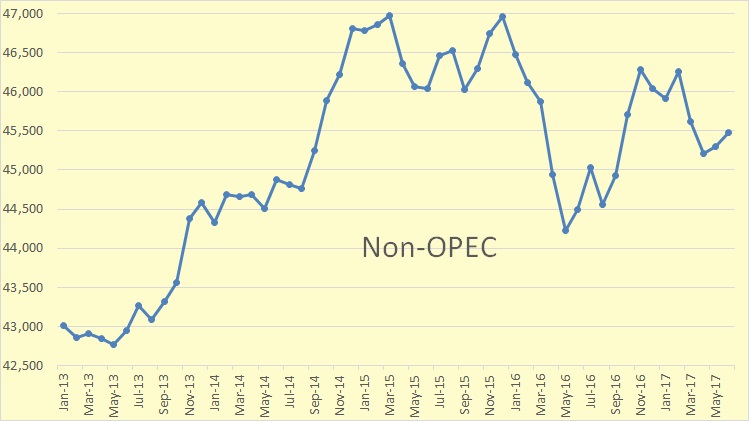

The above Non-OPEC data is from the EIA is through June only. Non-OPEC peaked in 2015 at 46,509 kbpd and the average for the first six months of 2017 is down 879 kbpd to 45,629 kbpd.

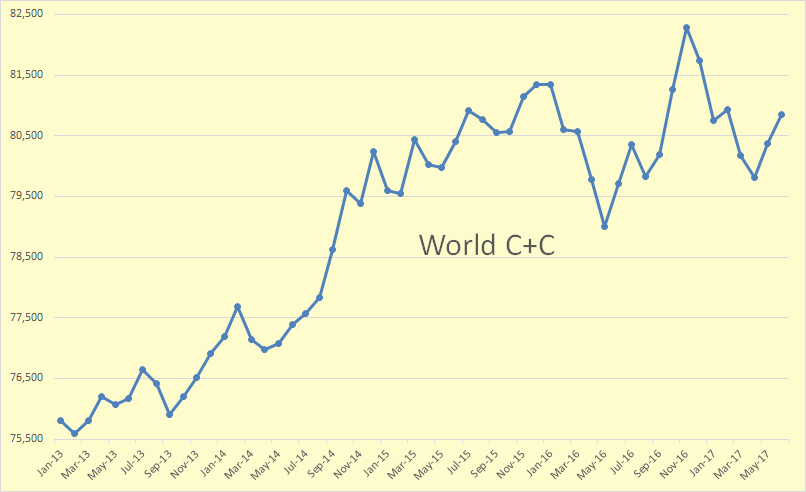

World C+C through June 2017. Peak 12 month average was 2016 at 80,556 kbpd. The first 6 months of 2017 was 80,480 kbpd. That is, so far, 77 kbpd below last year.

316 responses to “OPEC September Oil Production”

You could add world monthly c+c by EIA.

Good idea. I just did that.

Thanks.

So, we have now 2 years without supply growth.

Hi all,

Using the latest EIA World C+C data the trailing twelve month (TTM) average World C+C output reached a new peak in June 2017 at 80,713 kb/d only a bit above the previous TTM avg in Feb 2016 at 80,673 kb/d.

Chart with World C+C TTM avg from EIA below.

Data from https://www.eia.gov/totalenergy/data/browser/index.php?tbl=T11.01B#/?f=M&start=200001

Chart below

from the perspective of the 12 month World C+C avg, no supply growth for past 18 months.

For those that like zero based charts. 2005-2017.

On the chart above it does indeed appear to be roughly 2 years with no supply growth.

I really think suggesting that Saudi and a few others are pumping every last barrel is very inaccurate.

No one has said they are pumping every last barrel. What the hell do you mean by “last barrel” anyway? I am saying they are pumping every barrel they can. They are all drilling more wells, drilling more injection wells and doing everything they possibly can to increase production. Or to be more correct they are trying, as best they can to keep new production ahead of decline.

That is not to say that they cannot, or will not, increase production in the future. They are all engaged in massive infill drilling in an attempt to keep ahead of decline and, in some cases, increase production. But infill drilling just sucks the oil out a lot faster. It does not create new oil in the reservoir.

Yes Ron, adding here my little opinion, I think you’re right. The world, over the last decade, has implemented production “improvements” at a big scale and is now facing the limits of that method. Still, if hurricanes, wars, earthquakes and revolutions work hand in hand (or rather cease to do so), we could see some significant increase, but on the other hand an abrupt decline for the same reasons also could be possible. But I think we’ve reached more or less the final plateau now, which could last for half a decade before starting to decline significantly. Maybe it holds long enough and declines sufficiently slow to make a smooth transition possible. I’m still optimistic.

No need to be rude. I simply think you’re wrong. I think the very graphs you are posting show pretty clearly that Saudi and a few others have deliberately cut back on what they can produce. We will agree to disagree.

I think the saudi production spike before the lately flat production was result of a red hot and therefore unsustainable production and price battle, while the actual production, at least for a while, seems to be very well sustainable.

Dood, you gotta be precise with terminology. It matters.

Deliberately cut back on what they can produce . . . what does that mean? That means nothing.

What you meant to say was Deliberately cut back on what they are producing.

This is an industry with as much terminology obfuscation as finance. If you don’t understand the specifics, you’re helpless.

I don’t think I was rude at all. I still don’t know what you meant by “last barrel”. No one is anywhere near producing their last barrel.

We discussed this months ago. Several OPEC nations, as well as Russia and some other non-OPEC nations, made heroic attempts to increase production just before they announced “cuts”. This was not all that difficult. Wells are shut down, sometimes annually, for maintenance. All they would need to do is not shut down any wells for several months. That way they could artificially increase production in order to “cut production” according to their agreement. Also, they could empty their storage tanks.

The charts, in many cases, show a sudden increase then a decline from that increase, right back to where they were producing before.

Ron,

Is there any question that the US is drilling much more aggressively than most of the world?

Think of how many rigs are drilling in the US, and compare that to the number in Saudi Arabia – KSA’s drilling level is really tiny in comparison. The same applies to other large producers. We had one very credible contributor (I forget his name, he seems to have dropped out) who argued that Russia had enormous untapped potential at this point – more than enough to sustain current production levels for quite some time. It seems likely they could raise production substantially if they really wanted to.

It seems unlikely that KSA, and some other similar countries, are really reaching their limits of production, should they choose to invest more.

Hi Nick,

We really don’t know what will happen. It is possible that Russia and some OPEC nations may be able to maintain output or possibly even increase output a bit for another 10 years or so.

Higher drilling rates do not increase URR, it leads to faster depletion and a temporary boost in output with faster decline rates after the peak.

Also there will be a fall in output from many nations, so just to maintain World output the increases from OPEC and elsewhere must more than offset declining output elsewhere.

Output of C+C is unlikely to rise to more than 85 Mb/d, maybe around 2025-2027, if it occurs. Another possibility is a plateau between 80 and 81 Mb/d until 2030, higher output will lead to higher decline rates.

Ron, our studies show infill drilling increases recovery factor by a small amount in very continuous and homogeneous rocks, and can increase it by a large amount in discontinuous heterogeneous rocks. Even very homogeneous rocks can yield more oil in some cases (for example where an aquifer moves with an uneven front).

In general we can see the infill well helps due to a bit of improved recovery and rate acceleration effects.

Yes, I realize infill drilling helps some. There would be gaps where oil would be left in the reservoir if no infill drilling was done. However, all the oil that is recovered via infill drilling is not oil that would not be recovered otherwise.

That is most of the oil is simply creaming the top of the reservoir. They drill horizontal wells that skim the top of the reservoir as the water rises up from below. This keeps the production decline rate of the reservoir to almost nothing and in some cases actually, increases production from the field. But while the decline rate is decreased the depletion rate is increased.

As a result, all those old supergiant fields in the Middle East and Russia are still producing at near their peak levels. If you looked at their production curve it would have a flat top, only slightly declining. Then…. then…. the water finally hits those horizontal wells and…

It is going to happen. The only question is when?

Hi Ron

It is probably already happening one well at a time.

The process is likely to be gradual, unless most wells arrive at their shut down point at the same time.

I do not think there is a physical reason to expect that to occur.

Dennis, there are reasons to believe that many of the wells in giant Saudi fields will decline quickly and at around the same time.

An example is the development of the Shabayh field. Shabayh was discovered in 1968 and developed in the mid 1990’s using over 60 one km single lateral wells. N. G. Saleri and others published an SPE paper in August 2004 discussing how they redeveloped the field using MRC (Maximum Reservoir Contact) wells.

In Saleri’s paper on the Shaybah-220 they describe how they redeveloped Shaybah with MRC wells with target depths 60 feet above the oil/water contact and 150 feet below the gas/oil contact. The SPE papers show Aramco systematically drilled their fields using geosteering to place well bores exactly where they wanted them, then they used advanced completion technology including intelligent completions which reduce the effects of coning.

The SPE papers show similar projects using these MRC wells to redevelop Abqaiq and other fields.

Because they have systematically developed and redeveloped their fields, it is likely that many of their MRC wells in each field are of similar age, are similarly placed in relation to oil/water/and gas contacts, and have been produced in a similar and efficient manner. While they certainly won’t all go at once, it is very likely that wells in each field will go close together.

Some reservoirs benefit from natural gas liquid injection. The Saudis could use ethane/propane slugs to recover more oil, but this implies shutting down petrochemicals.

Hi dc longhorn,

The point is that there are many fields around the World, perhaps every well will be shut in at a large field over a short time.

A claim that this is likely in every field all over the world seems incorrect.

Even a claim that this would occur in most KSA fields over a short period is doubtful in my opinion.

Hi Dennis,

I agree with you that it is not likely that every well in most KSA fields will be shut in within a short time. That was not my assertion.

My view is that because of the manner and timing of their redevelopment, as well as the advanced technology used to redevelop these fields, these fields will not show a normal decline. Instead, they will produce at a high level, with a relatively low decline. Then they will suddenly water out with many (not all) of the wells in each field declining rapidly.

This will lead to a very steep field decline once production comes off the plateau. I believe that Ron was also expecting this type of production in his comments above with which you also disagreed.

I suppose we won’t know for sure how this turns out until KSA releases more production data. But if you will read some of their papers, the Aramco scientists make a good argument that they are accessing more oil from their giant fields. Of course the downside is that once their technology has run its course, there won’t be much left.

Hi Long Timber,

I agree with you at the field level, though my guess is that large fields may have been redeveloped in stages so that each development stage might have most wells water out at around the same time.

At the level of the nation state the timing may be such that decline remains gradual (2 to 3% per year). In any case we can only guess because we don’t have much data for KSA except nationwide output.

From what I have read, World 2P reserves based on proprietary databases is pretty close to BP reported proved reserves.

See section 3(b) of report linked below (published Dec 2013)

http://rsta.royalsocietypublishing.org/content/372/2006/20130179

Sorry the reply above should have been addressed to dclonghorn.

Question: Why did the last two points on the world-graph go up about 1 million bpd while OPEC stayed rather flat and the non-OPEC countries went up just about 1/2 million barrels? There seem to be 1/2 million of unreported barrels.

The answer to your question is rather simple. The non-OPEC graphs end with the June data while the OPEC graphs end in September. So let’s just look at the months of May and June, the two months in question. World production went up 1,018,000 bpd during those two months. OPEC production went up 757,000 bpd during May and June while non-OPEC nations increased by 261,000 bpd during May and June. Adding the two we get 1,018,000 bpd.

Thank you Ron, I missed that important detail while scrolling between the charts through the whole article.

Oil Production Vital Statistics September 2017

Fleshing out consumption numbers from the only place that matters — China.

Chinese July consumption up 690K bpd over 2016’s July. That’s about 6%

Chinese total consumption 11.67 mbpd July. YTD the average monthly increase has been 550K bpd, which compares with 210K bpd for the same period 2016.

This is not all liquids as BP tracks. That number will be headed towards 13 mbpd this year. Chinese consumption growth last year was 3+%. It’s on track for over 6% this year (amid the silliness of EV hype). This is a somewhat typical number for them.

Here’s what EIA has monthly for US consumption:

Avg of month to month consumption numbers 2016 Jan – July

19.561 mbpd

Same thing for this year

19.822 mbpd

The triumph of EVs.

According to the Monthly Plug-In Sales Scorecard over at insideevs.com, US plug in sales up to the end of September were 142, 514. Someone named Mark Larsen has a page on The State of United States’ Plug-In Vehicles where he tracks the sales of plug in vehicles in the US with lots of colorful graphs and pie charts. Larsen tags the cumulative sales of 100% electric vehicles at 374,463 with plug hybrids at 331,514 for a total of 705,977 plug in vehicles sold on the US up to the end of September 2017. Thats about 563,463 at the end of 2016 rising by 142, 514 as at the end of September, out of a fleet size of about 250 million. At 0.28% of the fleet, not quite at the point where we can expect them to “move the needle”…… yet.

Maybe that includes Walmart carts.

Jeff linked this on the previous post, just before the new one, and it’s worth a look – in French but Google translate gives the general gist (not that great though, I don’t know if Lahererre uses a lot of slang).

I don’t know who Sister Anne is, maybe some particular French meme, also a great old song by the MC5, but I don’t think that’s who he means.

(Note he is a climate change denier, and doesn’t make as much sense when going on about that as for oil reserves. I think he hangs his hat on ice core dating without considering all the research around it for bubble migration, permafrost melt etc.)

https://aspofrance.files.wordpress.com/2017/10/jmj-jr7271.pdf

Personally I think Nigeria is at their limit. They hinted that they’d be prepared to limit production at 1850, which is what they are at and if you extend the decline curve from 2012 it would be about there now. They don’t have much new this year, maybe a bit of ramp-up, or next until Egina. Their main offshore production comes from a set of FPSOs of a similar age, so they could start declining quickly at about the same time.

I also don’t follow how Ecuador maintains production. They have heavy oil, which usually needs a lot of wells continually coming on line. But they only have 5 rigs. Their new fields are funded by China, who also gets first option on the production, so maybe there are operating rigs that Baker Hughes don’t have access to.

I wouldn’t say Ecuador’s oil is heavy. Some older fields are in the 20’s API, and they have infill potential. The reservoir has oil over water, a large acquifer, and this is suitable for infills. The wells are easy to drill, can be completed with a workover rig.

This posted by Longtimber on previous oil and gas thread also worth repeating

“Art believes falling inventory will result in price support.”

http://www.artberman.com/higher-oil-prices-likely-early-2018/

Thanks George and Longtimber,

I agree with Art Berman’s assessment, hard to know about the timing, but the summer driving season from May to Sept 2018 seems a likely time that oil prices might rise, assuming no major recession or war in the interim.

TFP = T H E * F I N A L * P L A T E A U

THE Movie or reality? more or less is more or less

Like this flick-Gotta Ask-Where the hell are we?

https://en.wikipedia.org/wiki/The_Final_Countdown_(film)

http://www.ed.ac.uk/news/2017/uk-oil-and-gas-reserves-may-last-only-a-decade

The Scottish and UK oil industries are entering their final decade of production, research suggests.

A study of output from offshore fields estimates that close to 10 per cent of the UK’s original recoverable oil and gas remains – about 11 per cent of oil and nine per cent of gas resources.

The analysis also finds that fracking will be barely economically feasible in the UK, especially in Scotland, because of a lack of sites with suitable geology.

If the study’s predictions are correct, the UK will soon have to import all the oil and gas it needs, researchers warn.

Instead, they recommend a move towards greater use of renewable energy sources, particularly offshore wind and advanced solar energy technologies.

Survivalist,

Didn’t Scotland just ban fracking outright? (from failing memory)

They did,

https://www.theguardian.com/uk-news/2017/oct/03/scottish-government-bans-fracking-scotland-paul-wheelhouse

I suppose that Dr. Roy Thompson’s point is that fracking wouldn’t do much good in Scotland, even if it were to be permitted.

when faced by such hefty economic disparities an appeal to an increase in oil prices does not provide a way out. Remember there are many developmental possibilities, if oil prices rise, for virgin giant fields around the globe, especially subsalt and deep-water. As a consequence expensive Scottish hydrocarbon is not going to suddenly become in demand.

http://edinburghgeolsoc.org/eg_pdfs/edinburgh-geologist-62.pdf

The author doesn’t give his price assumption, and his assumption that prices will not rise seems to not be supported by the consensus on POB.

Thanks for the post, Ron. The site is very informative, and I have come to the conclusion that I need to read more, and comment less. But, you are right. Couldn’t help it.

2017-10-11 BSEEgov: From operator reports, it is estimated that approximately 32.68 percent of the current oil production in the Gulf of Mexico remains shut-in, which equates to 571,854 barrels of oil per day. It is also estimated that approximately 20.51 percent of the natural gas production, or 660.55 million cubic feet per day in the Gulf of Mexico is shut-in.

https://www.bsee.gov/newsroom/latest-news/statements-and-releases/press-releases/bsee-tropical-storm-nate-activity-4

Estimate of “Lost” Gulf of Mexico crude production due to Hurricane Nate is 7.82 million barrels of oil.

Also, Genscape GoM production chart: https://pbs.twimg.com/media/DL4r7v6UEAA75uK.jpg

You never fail to find good info. Thanks. Didn’t know Genscape tracked GOM.

Ron, Your statement on Gabon is not consistent with the graph. It might contain a typo, I think. What was the peak production level?

Yeah, the high was 370k a day in 1997. Pretty immaterial to the total, but a country I’d like to see.

Not much to see. The beaches can have worms, there’s a really nice beach at Sogara, but the view can be ruined a bit by the French refinery. Libreville public bathrooms are dirty.

Verwimp.

How is your Bakken model? I haven’t seen you update it, although maybe I missed it.

Hi Shallow Sand, Thanks for asking! I’ve reported some times during the last months that the gap between the model and the data is growing.

Or the extended version of the graph below. So you can see there was a huge correlation between the model and the data, and also between the first derivative of the model and the changes in the data for more then 3 years until january 2017. From that moment all correlation is lost. Data show that the increase in production was not only related to the increase in number of wells, but also in the amount of oil per well (on average). That is ‘weird’. I mean, that is absolutely not in line with what I expected to happen, and not in line with what was actually happening until the end of 2016. So, you know: we can all be very happy: Peak Oil is for some reason postponed again, and we can all keep going speculating about The Moment When It Will Happen! 🙂

What I see is that they are getting some good response out of drilling sweet spots, for sure. I think the stated demise of Bakken and the Eagle Ford is premature. Just needs a better oil price. Plus, it needs a long lead time to allow completion crews to gear up.

Or maybe it is company-saving choke release.

Verwimp,

Great to see you posting an update. I can honestly tell you that the “WEIRD” rise in production per well in the Bakken may not be as high as the data shows. Unfortunately, I can’t publicly state the reason I know this. If you contact me via my email address: [email protected], I can provide a few more clues.

However, the SHITE is going to hit the fan in the U.S. Shale Oil Industry once this news gets out… which will likely be made public shortly.

steve

Email from Jean Laherrere:

dear Ron

in your last post George Kaplan quotes my last paper in french but with graphs in english and wrote y that he does not know about Sister Anne who cannot see anything coming

you could tell him that it is from Bluebeard

https://en.wikipedia.org/wiki/Bluebeard

“Bluebeard” (French: Barbe bleue) is a French folktale, the most famous surviving version of which was written by Charles Perrault and first published by Barbin in Paris in 1697 in Histoires ou contes du temps passé.[1][2] The tale tells the story of a wealthy violent man in the habit of murdering his wives and the attempts of one wife to avoid the fate of her predecessors. “The White Dove”, “The Robber Bridegroom” and “Fitcher’s Bird” (also called “Fowler’s Fowl”) are tales similar to “Bluebeard ».

Bluebeard announces that he must leave for the country and gives the keys of the château (castle) to his wife. She is able to open any door in the house with them, each of which contain some of his riches, except for an underground chamber that he strictly forbids her to enter lest she suffer his wrath. He then goes away and leaves the house and the keys in her hands. She invites her sister, Anne, and her friends and cousins over for a party. However, she is eventually overcome with the desire to see what the forbidden room holds; and she sneaks away from the party and ventures into the room.

She immediately discovers the room is filled with blood and the murdered corpses of Bluebeard’s former wives hung on hooks from the walls. Horrified, she drops the key in the blood and flees the room. She tries to wash the blood from the key, but the key is magical and the blood cannot be removed. Fearing for her life, she reveals her husband’s secret to her visiting sister, and they plan to both flee the next morning, but Bluebeard unexpectedly comes back and finds the bloody key. In a blind rage, he threatens to kill her on the spot, but she asks for one last prayer with her sister Anne. At the last moment, as Bluebeard is about to deliver the fatal blow, the brothers of the wife and her sister Anne arrive and kill Bluebeard. The wife inherits his fortune and castle, and has the dead wives buried. She uses the fortune to have her other siblings married, and eventually remarries herself, to a man she loves, and moves on from her horrible experience with Bluebeard.

best regards

jean

So, not to be confused with Blackbeard. Blackbeard was the pirate, and Bluebeard was the ultimate misogynist.

Alice and Looking Glass is likely not required reading in all languages so Red Queen references may mean nothing to non English types. Significant lesson.

Thanks, always good to learn new stuff like that. I remember the film, though not for particularly good reasons, I don’t think Richard Burton at his best.

This link doesn’t have much to do with petroleum, but I’m hoping WHUT or Dennis or Schinzy will see it here and answer it, considering the call for review thread is now stale.

https://www.nytimes.com/2017/10/10/science/yellowstone-volcano-eruption.html

I take it that the new book will lay out a framework for estimating the likelihood of such an event as a super volcano eruption more accurately than has been possible in the past, and do this by tying together messy noisy data from various separate scientific fields that are not usually taken into simultaneous account by people who make such predictions.

No matter how you go about modeling a possible future scenario, any scenario, there will likely always be more data that might be relevant than is used in doing the modeling. I’m thinking the book will be , in part, about ways to take such previously known but unusable data and incorporate it into improved models.

I’m ready to venture a guess that it will be VERY useful to people who are wondering about the future of the oil industry, if they happen to be technically competent to make proper use of it.

SO….. Will the book be useful in that it will help refine existing estimates of volcanic super eruptions, or so called black swan economic events, or war breaking out unexpectedly ?

IEA monthly oil market report (OMR) is out:

https://www.iea.org/oilmarketreport/omrpublic/

“Meanwhile, detailed analysis of the global balance shows that in 2017 each quarter will show a deficit, other than a tiny build in 1Q17, and, for the year as a whole, stocks will fall by 0.3 mb/d. This assumes OPEC crude oil production remaining at 32.7 mb/d. Data is of course subject to revision, but we can now clearly see a major reduction in floating storage, oil in transit, and stocks held in some independent areas. In the OECD, the five-year average stock overhang is now down to 170 mb from 318 mb at the end of January and stocks have fallen in months when they normally increase, offsetting net builds in China. In the case of China, there is always a margin for error in data that is often derived rather than reported, but crude imports have fallen every month since June and the implied net build for China’s stocks in September was relatively small at 100 kb/d.”

IEA expects a balanced market in 2018 but their assumption on US production is probably a bit too high. They release the public report 2 weeks from now so will have to wait and check their numbers but I think that previous reports assumed US LTO and offshore to grow quite significantly in 2018. Also, I don’t think they have included KSA November cut which should affect stocks in Q1 2018.

The Castro dictatorship’s foreign relations minister smirked at a recent meeting that USA could forget about Venezuela, because Maduro could hold power until oil prices recover. The ongoing decline of production is hitting the Castro Mafia pretty hard, but they think they’ll retain their nearly colonial hold on Venezuela. Whatt they may not be factoring in is the continuous decline.

About a week ago I read that PDVSA is running low on natural gas to generate electricity, which in turn slows down oil production, which leads to lower natural gas production. Hopefully they’ve entered a death spiral from which they can’t recover and Maduro will fall.

I had a look at the report from last month. More than half of the global growth next year is expected to come from US. Not much offshore (GoM) but quite a lot of LTO (TX, ND), NGLs and “other”.

From OMR Sept ed.: “Producers even cut seven oil rigs in August following oil’s decline to around $42/bbl at the end of June. Since then, WTI has recovered to around $49/bbl, a level likely to prevent further declines. US crude oil production is forecast to grow by an average 360 kb/d this year and 850 kb/d in 2018. Additional NGLs output takes total supplies 470 kb/d and 1.1 mb/d higher, respectively.”

EIA STEO has GoM increase for next year at about 70 kbpd, down from 160 kbpd in January. They still have production rising to 1820 in May and then 1850 in December (but coming down with each new release now); that is only possible with no decline in any mature fields and instantaneous start up to nameplate of both Stampede and Big Foot.

Question for someone who knows more about cracking than I do. If we continue to try to produce more distillates to better the distillate inventory, won’t we wind up with more of an increase in gasoline inventories?

About thirty years ago I had a period doing a bit of work on refineries, and I’ve forgotten most of it, so not an expert and treat this accordingly. Cracking usually takes fuel oil which has a high C to H ratio and either takes out some of the C (that’s fluid cat cracking) or adds some H (that’s hydrocracking); the added H often ultimately comes from natural gas (that is partly why there is refinery gain – natural gas is being added to the mix and, actually ends up getting counted twice in hydrocarbon production numbers. Distillates boil a bit higher than fuel oil (has a bit lower C to H ratio) and gasoline a bit higher still (i.e. more H again). There’s is a bit of flexibility in what product you get (but not unlimited) so it’s possible to adjust the mix to some extent. Note that the world in general is getting heavier, even if the USA is getting lighter, so more gasoline with the distillate isn’t necessarily a bad thing overall, and with the USA now able to export balancing the mix is easier (the recent increase in USA exports might reflect this). Also the split between gasoline and distillate demand is much more elastic than the overall oil demand – small price differences from diesel to gasoline can quickly change the usage (not so long ago the UK had relatively cheaper diesel, but now it’s pretty much parity on an energy basis as demand and supply balance has changed). The bigger question might be if there will be sufficient cracking capacity as the oil gets heavier, but I think generally there will be as a lot of the producer nations have been developing their own refining capacity tailored to their particular oil.

I think it depends on what you mean. For example, if refiners absolutely need more diesel, so instead of refining 16 million bbl/day, they ramp up to 17 million bbl/day, then they will get more diesel and more gasoline.

I do know that the refiners used to tweak the refineries to produce a higher gasoline/diesel ratio during the summer and a lower gasoline/diesel ratio during the winter [especially when more heating oil (diesel) was being used out east, but now, a lot of that heating oil has been converted to natural gas]. So, if they have already tweaked their refineries, running more crude thru the refinery is about all they can do.

I do not know for sure what the tweak was, but it was not huge. If I had to take a WAG, I would say maybe 68%/32% during the summer, and 64%/36% during the winter [using WTI as opposed to heavier Venezuelan crude].

Looking at today’s report from the EIA, we are importing a trivial amount of diesel. Maybe someone here knows, but I do not know – Is that because there is very little diesel available on the world market, or is that because the US refiners are confident that with their heavier crude input, they can produce enough diesel domestically? Because total diesel inventories are somewhat below average, I would guess the former.

That helps. Thank you George and Clueless!

Ron,

The guys at Core Labs had an investor presentation a couple of weeks ago where they talked about Russia. Most analysts over the last five years have been wrong on Russia. Most thought they would never get that much above 10 mbpd. As you know most of these fields are old/mature. Russia was able to use short term low tech solution to enhance production. Frack the field and put in an electrical submersible pump. It worked very well, better than most had thought it would work. Core Labs thinks that these types of work overs sets them up for a hard decline. They see a possibility for a net decline rate for Russia at 7% a year and half out.

https://cc.talkpoint.com/wolf001/092817a_as/?entity=2_DQQGOH4

At the 3:25 mark they talk about Russia

Does this additional help to increase the total recovery rate?

Link didn’t work, demanded registration.

Fracking is low tech now? I thought it was a yankee know-how uber techno miracle.

OTOH, maybe this was meant:

http://www.businessinsider.com/russia-claims-to-have-invented-an-alternative-to-fracking-2017-8

that Russian replacement of fracking by chemical reaction that produces gas is interesting. Any of the technical people here care to comment at all?

The Rockman on TOD used to say fire flood was something that worked if you could get it right, which he said was impossible. but the expanding gasses were powerful

Fire flooding produces acid gases, they eat the producing wells’ steel casing and tubing. There are other problems as well, and this is why the industry leans towards polymers, CO2, and natural gas liquid injection.

Russian fields can’t be lumped together in one single group. Simple low tech hydraulic fracturing works well in fields with low permeability sandstones.

Russia has large unexploited condensate/NGL resources in the Jurassic which lies under the large Cretaceous gas fields, but that requires high prices. I see they are fiddling around a bit with these reservoirs, but they haven’t invested in full development. I suppose those will be developed in the 20’s and 30’s.

https://seekingalpha.com/amp/article/4112973-last-great-secular-oil-bull-market-begun

Quotes Ron.

Food for thought: if OPEC and Russia see the eventual demise of the oil industry, would they not want the highest possible price while it lasts? Manipulating the market has a negative connotation with the US, but it is their modus operandi.

No, it actually quotes Dennis. They still refer to all posts from PeakOilBarrel as being from me when they are actually from Dennis or a guest poster. Here is the article they refer to:

U.S. Shale Could Peak Before 2025 By Ron Patterson – Mar 25, 2017, 10:00 AM CDT

And that article was written by Dennis Coyne, not Ron Patterson. If I had written the article, I would have had shale peaking long before 2025.

So, they used your name in vain,?.

Hi GuyM,

In that post I assume that oil prices rise to about $75/b (65-85) by Jan 2022.

Clearly nobody knows the future price of oil. Based on USGS TRR estimates for US LTO and the oil price assumptions, US LTO may peak (if the assumptions are correct) between 2019 (low oil price scenario) and 2022 (high price scenario).

Both of these dates are before 2025, my best guess in March 2017 was about 2021, with the peak for US LTO at about 6.5 Mb/d. Output in Aug 2017 (at an oil price under $55/b) was about 4.75 Mb/d. I think higher oil prices (above $75/b) will increase US LTO output by another 1.75 Mb/d over the 2017 to 2021 period, followed by decline.

I believe it has another significant peak to it. It’s will take a lot more time, because EIA and Goldman Sucks won’t quit creating imaginary numbers. September will be worse, because of Harvey, and a very low completion count for Texas, with a lot of completions being vertical. Don’t expect much more activity, as it is the end of the year. Completions, at this point, won’t add much to year end figures.

Don’t think I’ve seen this linked here – may be relevant, I tend not to take much notice of these finance only type predictions that don’t even give a nod to possible geological influences and seem to take as read some kind of deterministic, technical and therefore predictable price forecast. Sometimes they come out correct but I’d bet no more than random chance.

WORLD’S NO.1 OIL TRADER: U.S. TO SEE FINAL OIL OUTPUT SPIKE IN 2018

http://oilprice.com/Energy/Oil-Prices/Worlds-No1-Oil-Trader-US-To-See-Final-Oil-Output-Spike-In-2018.html

Hi Ron,

When would you have it peaking? My low oil price scenario was 2019 for the peak. All scenarios are too low in Aug 2017 by about 500 kb/d. (4.25 Mb/d vs 4.75 Mb/d actual output). The current US LTO peak is Aug 2017, until next month 🙂

Peak, so far, was in May. EIA July numbers are more than suspect, August and September had Harvey, and completions in Texas were very low for August and September.

Hi GuyM,

The peak for US LTO was Aug 2017 according to EIA tight oil production estimates.

9 months will prove that wrong. Common sense should. Completions in Texas were down, and Eagle Ford was largely shut in for awhile, and production is up? Initial Texas production should be out in about four days. I’ll update then. July 2017 initial production was less than July 2016 initial production, but EIA still put it about 300k over what is currently reported for July of 2016 even by their count. They can play this game for about a year, and then they don’t have to explain anything later, because by that point, nobody cares.

The initial reported production by the RRC is usually 550 kb/d too low.

The initial EIA estimate is far better than reported RRC output. Not perfect but within 3% rather than low by 15% or more.

It was that way for 2016, also. Eia adjusted it up to close to actual. Both EIA numbers for July 2016 and current posting for RRC are about the same now. They are 300k barrels below what EIA is estimating for July 2017. Even though the initial reporting for July 2016 is higher than the initial reporting of 2017. Quite obviously one is wrong. As 2016 is now historical data, I would think that one is more correct.

http://www.rrc.state.tx.us/all-news/092517a/

Condensate for July 2017 was 8,641,731. I did not write down the condensate for July 2016, but it was running over 9 million barrels through most of 2016. So, let’s just say they ere equal. EIA has Texas production at 3,161,000 for July 2016, which is their CURRENT figure. They have July 2017 at 3,474,000. Actual RRC data shows 3,110,000, which is not that different from EIA’s number. But 2017 is 300k more, because? Sorry, Dennis, I edited my post while you were replying, and answered your objections in this post.

The EIA estimate does not change very much usually 2 to 3% at most.

The RRC initial estimate gets revised up for 12 to 18 months. In the end it ends up being within 2 or 3% of the initial EIA estimate.

Hi GuyM,

When you say the initial reporting for July 2016, do you mean the data initially reported on Sept 2016?

Hi Guym

That report does not give condensate output.

EIA reports C+C the Texas report you link to reports crude only.

Apples to oranges comparison.

The initial July 2016 estimate by the RRC has been revised up 12 %

Hi GuyM,

The RRC data bounces around quite a lot and the data for the most recent month especially, tells us very little.

In Sept 2016 the EIA reported Texas output for July 2016 (the most recent estimate at that time) as 3161 kb/d. Currently the July 2016 for TX C+C by the EIA is 3161 kb/d. This estimate is a bit higher than the currently reported RRC estimate for July 2016 C+C (3110 kb/d), but the RRC estimate for July 2016 may increase a bit more over time.

In any case, we will see how US LTO output will change over the next 9 months.

I get my tight oil output estimates from the link below:

https://www.eia.gov/energyexplained/data/U.S.%20tight%20oil%20production.xlsx

In Texas, the wells that were being completed in July 2017 may have been more productive on average than wells completed in July 2016. If completions drop by 10%, but average well productivity of newly completed wells increased by 15%, then output might increase by roughly 5%.

In any case, we will find out in the future what has occurred with US and Texas C+C output. In the past EIA estimates have been pretty good.

Occasionally the EIA estimates are a much too high, in June 2015, the April 2015 EIA Texas C+C estimate was about 6% too high (compared to the current April 2015 EIA TX C+C estimate). By contrast the initial RRC estimate for April 2015 was about 25% to low.

Hi Guy M,

In Sept 2016 the initial RRC estimate for July 2016 was 2753 kb/d.

In Sept 2017, the RRC estimated July 2017 C+C output at 2708 kb/d.

So the estimates are indeed very close.

The “correction factor” varies month to month it is not fixed because the percent of production reported in a timely manner by Texas oil producers is not fixed, it varies month to month.

Hi Guy M,

I took a look back at some of the data that Dean Fantazzini collects and you are correct that since April 2017 the EIA data for Texas has probably been too high. There was a noticeable shift in the difference between the initial EIA estimate and the RRC initial estimate over the past 3 months from about 450 kb/d to 700 kb/d, so it is quite possible the most recent EIA TX C+C estimate is too high by about 300 kb/d as you suggest.

Chart below has correction by Dean Fantazzini using last 3 months of Texas RRC initial estimates and using past 13 months of Texas RRC initial estimates (in each case using most recent 24 months of data reported in each of the past 3 or 13 months by the RRC). I prefer the most recent 13 months, there was a change in the correction factors (a shift to lower values, about 16 months ago(April 2016).

The Chart below is based on data provided by Dean Fantazzini.

Clicking on chart gives a larger view.

I already picked the peak, 2015. So I was slightly off, but not by all that much as you can clearly see by the chart. I think we are on the peak plateau right now. The actual 12-month peak could be anywhere from 2017 to 2019 but no later than that. Well, in my humble opinion anyway.

Hi Ron,

The question was about US LTO, you have picked the World C+C peak, but as far as I remember you have not said anything recently about US LTO except that it will be before 2025.

So far the 12 month centered average for US LTO peaked in June 2015.

If US LTO output continues at the August output level (4750 kb/d) for 5 months, then a new 12 month centered average peak will be reached by Aug 2017 (average output from Feb 2017 to Jan 2018). US LTO output has risen about 600 kb/d over the past 12 months so an assumption of no further US LTO output increases over the next 5 months is a conservative estimate in my view.

Hi Ron,

I agree that Peak Oil was reached in 2015. Looking at yearly production using EIA data for world C+C production, production remains at ~ 80.5 million barrels per day, including the first 6 months of 2017. Until production can go to 81.0 million barrels per day, we remain in Peak Oil. An undulating plateau is still Peak Oil.

Most people think production will go up and Peak Oil won’t take place for decades. After all the 30-year trend is clearly positive and some people only look at that. I don’t. Even though the capability to produce more oil remains, I think economic factors, production limitations, and depletion will determine this constituting the Peak Oil. The real test will take place when oil prices rise significantly in the future. I anticipate the decrease in demand resulting from higher prices will prevent oil production from increasing significantly on a yearly basis.

Data in the graph good to Sept 2017 EIA MoER (table 11.1b).

We still have a projected oil growth of about 1.5 million barrel a year the next few years – mostly driven by China and India. Even with China promoting electric cars aggressivly it will take a few years until you see the dent in chinese demand.

There are still reserves sitting in oil tanks and floting storage – but production has to climb or we have 100$+ oil already in 2019.

Times will get interesting.

Every period of 3 years or longer without an increase in oil production has been accompanied or followed by global slow economic growth, and economic crisis in large regions. Whether cause or consequence, if in 2018 there’s no increase in oil production we might have another serious economic situation developing.

Hi Javier,

Possibly there will be a slowdown in economic growth, the Global Financial Crisis of 2008-2009 was a particularly severe crisis, the most severe since the Great Depression.

From 1990 to 1994 the trailing 12 month average of World C+C output was relatively flat with low economic growth rates from 1990-1993, but no economic crisis. The relationship is far from simple, there may be slower growth or the transition may present new opportunities that enhance growth, slower growth seems more likely to me and eventually there may be a severe recession, this is uncharted territory has World Oil output has never peaked before, though we did see a severe decline from 1980 to 1982 with relatively little increase until 1986 (63 Mb/d down to 53 Mb/d in 1982 and only 54 Mb/d at the end of 1985). Over this period real economic growth fell from 4% in 1978 to 0.4% in 1982, but rose to 5% by 1984.

Unless there is another major war in the middle east (or a Great Depression) a fall in World C+C output like 1980-1982 (18% decline in output over 2.5 years) is unlikely before 2040.

We have not studied the same economic history. The early 90’s were characterized by poor economic performance in most of the Western World. Australia and New Zealand entered recession. Finland and Sweden had their worst recession in over 60 years. Germany had a very tough period with high interest rates and poor performance after reunification. The UK didn’t grow between 1990-93, and in 1992 the UK sterling pound was forced out of the exchange rate mechanism. Other European countries also had recession at this time. Even in the USA George H. W. Bush failed his reelection due to the poor economy, despite winning the Gulf War. This is known as Early 1990s recession

Your exception is not such.

Hi Javier,

World Real GDP increased at about 2% per year on average over that period. It was a slow growth period and the slow GDP growth may have been the reason for slow growth in oil output. It was followed by an increase in GDP growth.

You may have cause and effect reversed. In any case in the past GDP/barrel increased at higher rates than would be needed for a slow growth in GDP of 2 to 2.5% per year.

Hi Javier,

For climate 30 year trends are appropriate as we do not understand the reasons for the internal variability of the climate system very well.

So if 12 month average output reaches 81 Mb/d, then it is a new peak?

What is special about 81 Mb/d?

If there was a “peak plateau” from 2015-2020, the sensible place to call the peak would be 2017-2018, if we are going to arbitrarily define the plateau as 12 month average output between 80 and 81 Mb/d. From your chart it is clear we are on a plateau at present (as was also the case from 2005-2010). Perhaps we will remain on this plateau for a few years and output will decrease and perhaps output will increase further when/if oil prices rise.

I think it likely that if oil prices increase above $80/b (likely by Oct 2018) that World C+C output will increase above 82 Mb/d and possibly increase to as much as 85 Mb/d by 2025 unless a severe World recession occurs between now and 2025. After that output is likely to decline. A plateau scenario with output between 80 and 82 Mb/d (defined arbitrarily) might be extended to 2030 (that is the centered 12 month average World C+C output falls to less than 80 Mb/d by 2031). Both the plateau to 2030 and peak at 85 Mb/d are optimistic in my view, a peak at 83 Mb/d (between 2022 and 2024) or a plateau (80-82 Mb/d) to 2027 would be my best guess.

Hi Dennis,

There’s no accepted definition, but to me if production reaches a plateau and doesn’t increase further, the peak date is the year the plateau is reached, not its center or end. Significant oil production increase ended in 2015 so far. Small incremental temporary increases don’t change that.

While a few hundred thousand barrels per day aren’t going to change the picture, if production goes above 81 Mb/d then it is clear that the peak wasn’t reached at 80 in 2015. Production has been increasing at ~ 1 Mb/d per year, so 1 Mb/d difference is significant enough.

Oil models are almost as bad as climate models, and nobody knows what oil prices are going to do or if oil production is going up or not. I’ll remain convinced that the 2015 Peak Oil call is good until the data proves otherwise. I’ve seen a lot of people predicting oil production increases since 2015, but they haven’t taken place.

The problem with your model is that a prolonged plateau in oil production is so far incompatible with economic performance, so the severe world recession that invalidates your model is already baked in your model. You require a new economy that hasn’t been demonstrated yet.

Hi Javier,

The economy is not well understood, but during the 1978-1987 period, the World real GDP per barrel of World oil that was produced increased at a rate of 3.9% per year on average over those years.

If World oil output is flat at the 2016 level until 2029 and World real GDP grows at about 2.4% per year in 2017 and gradually falls to 2% per year by 2029, then real GDP per barrel of oil produced would increase at 2.2% per year (far lower than the 1978-1987 rate of growth). The rate of growth of real GDP per barrel of oil produced has increased at a rate of 1.8% per year from 1988 to 2014. From 2004 to 2008 the rate of increase was 3.3% per year.

So there is past economic data that suggests a plateau to 2029 might be possible. There is also a more likely possibility that World oil output will increase to 82 Mb/d between 2020 and 2023 and then gradually decline from 2025 to 2030 (1% per year decline on average, starting slowly with a gradual increase in decline rate).

I agree that like predictions of future Global Temperature, oil output and/or price predictions are likely to be imprecise.

As far as a recession invalidating the model, that is silly. A model makes some underlying assumptions. As most people understand that future economic rates of growth are difficult to predict, I make the simplifying assumption that the forecasts of international agencies such as the IMF or World Bank are roughly correct, but assume growth rates will be somewhat less than they predict because their past predictions for real GDP growth have usually been high by about 0.5%.

If their is a major recession that occurs, demand will be lower, prices will fall and output will be lower. Provide me with the correct date for a future recession and the growth rate in real GDP and a scenario can easily be devised that approximates future output.

My crystal ball is in the shop, maybe yours is working 🙂

Dennis, a recession is not the only scenario that invalidates your model. Recession is both cause and consequence of oil consumption reduction. A recession can be brought by an oil price shock, while at the same time it reduces oil consumption regardless of price. So strong oil price increases, non-oil related poor economic performance, or simply inability to increase oil production at a given price point, all lead to a different scenario to your model.

If I remember your model correctly, it predicts that in ~ 12 years oil production should be similar to now, either through a plateau or through modest increase followed by modest decrease, depending on oil price. In my modest opinion such a model requires fair economic performance under oil production circumstances that have been associated to poor economic performance in the past.

You claim that our economy is going to decouple from oil use enough to allow it. Perhaps, but I am not convinced. The decrease in oil intensity has taken place mostly while using more oil, not less. A big part of it is a transition to a more mature economy more dependent on services, while production was being shifted to other countries, and increased, not decreased. An actual stagnation or decrease of oil-dependent production might not be compatible with an increase in services, and prevent a continuation of the decoupling.

Hi Javier,

I have not made any decoupling claim, so please do not make things up.

Most of the scenarios have assumed no recession as I have difficulty predicting the date.

Recessions are variable in their intensity. The 1990 to 1994 recession was relatively mild on average for the World. A recession like that would simply help to keep oil prices low.

Less oil has been used over time per constant dollar of GDP produced, other forms of energy have been substituted for oil and energy in general is being used more efficiently.

There will never be a decoupling of the economy from energy that is absurd.

Energy will continue to be used more efficiently unless a ramp up in solar power makes it relatively abundent 100 years from now as population declines due to a lower TFR of 1.7.

On oil use increasing, this was not the case from 2005 to 2010 but Real GDP per barrel of oil continued to increase. This is mostly driven by real oil prices. During periods when oil prices have been high the rate of growth of GDP per barrel is usually higher. Rising oil prices if oil output remains on plateau is likely to lead to faster growth in GDP per barrel. Real oil prices above $100/b caused few problems from 2011 to 2014 World Real GDP grew 2 to 3%. Oil prices decreased due to oversupply which I do not think will occur again prior to 2030. A severe recession prior to 2030 would be one possible cause for oversupply due to lack of demand.

Hi Javier,

There were three main scenarios presented in my July 2015 post, and 3 other scenarios based on the medium scenario (from

pessimistic to optimistic with a “realistic” middle case).

Post at

http://peakoilbarrel.com/oil-shock-models-with-different-ultimately-recoverable-resources-of-crude-plus-condensate-3100-gb-to-3700-gb/

Spreadsheets with the scenarios are linked in the post.

Reality might fall anywhere between the low and high scenarios if the low to high URR estimates are roughly correct. Note however that I underestimated future extraction rates at least through 2016 so potentially peak output could be above the 80 Mb/d level shown in the chart below, perhaps as high as 85 Mb/d, but 83 Mb/d seems a more reasonable guess to me (probably between 2021 and 2024). An undulating plateau between 2015 and 2029 is also a possibility, but if we define the upper limit as 81.5 Mb/d, then I doubt this scenario will be followed, I think a new peak above 82 Mb/d some time after 2019 is likely. So the scenarios presented in 2015 were too pessimistic.

The other scenarios based on the medium (3400 Gb URR) scenario in chart below.

Hi Dennis,

Thank you for posting your model again. You know I am not too fond of trying to model very complex, multi-variable phenomena when there is very limited knowledge of some of the variables.

A very serious alternative to your Hubbert-type approach is the Seneca cliff collapse observed in some overshooting systems.

So how can you say where reality might fall if you can’t possibly know if decline is going to be Hubbert-like or Seneca-like? The answer is by making assumptions. Your model, any complex model, rests on a bunch of unstated assumptions. the probability that one of them will not be true is extremely high, and the moment one is not true, the scenario becomes completely different and the model is worthless.

I rather stick to the data and the evidence and make limited predictions that rest on as few assumptions as possible. The downward slope of Peak Oil is something we can’t possibly imagine, much less model.

In late 2014 it became clear to me that Oil had entered endgame. The LTO scheme was not a solution but a dilatory maneuver. Cheap-to-extract oil has reached a limit and is declining, and expensive-to-extract oil won’t do. It doesn’t matter how much oil is left. It doesn’t matter that we could extract a lot more than we do. The more we extract the less economic output we have left for other things, so we will extract as little as we can and still function, while we try to do with less oil. But as there are no cheap alternatives to cheap-to-extract oil for transportation we will reach a point when the economic world will awake to the end of growth, and the end of interest rates. There will be a huge run out of paper wealth into solid wealth, with the mother of all inflations and the end of financing, and that will be the end of civilization as we know it. Try to model that.

That’s why I predicted 2015 as Peak Oil. Perhaps I am wrong and a higher production can be reached, as you say. The capacity is there, but I don’t see the conditions as favorable. We have already seen the return of Iran production, and significant recovery from Libya and Nigeria, without a global increase. The downward potential is big and depletion is likely to accelerate.

And even if I am wrong with a 2015 Peak Oil, I don’t think it will matter much, as it would be just a temporary delay.

Javier said:

People aren’t usually fond of things that they can’t do well. This includes when they do not understand how to reason with limited knowledge avaailable (the discipline of probability) .

Hi Ron,

How would you define “peak plateau”? Would it be a 12 month output average of 80-81 Mb/d? Or maybe 79-82 Mb/d?

Another reality disconnect on the EIA weekly. Shows production down during Nate, but only 87k.

BSEE numbers are going to be over 300 kbpd so I don’t know where they get that number from, maybe they just counted the first day of outages in their weekly numbers.

Chinese September crude oil imports back above 9 million b/day

Reuters chart in tonnes: https://pbs.twimg.com/media/DL_WFnIVoAExIEl.jpg

EIA twip has total crude and products down 1.7 mmbbls or 0.2%, which is quite a bit less than the trend (crude down 2.7 – -0.8%, gasoline up 2.5 – 1.1%, distillate down 1.5 – -1.1%).

With USA crude export in full swing now I wonder if these numbers are quite as important to traders for setting prices, or to the media for headlines. There don’t seem to be quite as many Thursday stories saying “oil rises/slides on unexpected/expected stock build/decline”

https://www.eia.gov/petroleum/weekly/

Most probably know the numbers are total BS by now, its the press who still treat it as gospel, and, of course, Goldman Sucks.

Weekly numbers are not very good.

The monthly data is pretty good.

Ron

I appreciate these posts but I always feel the graphs are misleading at first glance because the production axis does not show zero. It seems to me like this is done to sensationalise the results.

For example at first glance it looks like Algeria production has totally collapsed but it is only actually down about 30% or so.

Sorry but as an Engineer in a different field this graphical misrepresentation is an issue that always bothers me.

Another common area I see this is when business magazines try to show explosive share price growth.

Gordon

Sorry Gordon, but as I stated when I started this site four years ago I stressed that my charts would never be zero-based unless the data actually went to near zero. I stated then that my intent was to emphasize the change in production. As an engineer, you should always be aware of where the vertical axis starts. After all, I am not the only one to not use zero-based charts. It is really the norm in this area of reporting.

I always thought that the whole “zero based” thing was a bit silly. First of all people tend to only look at one axis – the Y axis when zero based charts are discussed. If one wanted to be pure and be truly zero based the X axis would have to be zero based also – but to what? JC’s birthday? the start of mankind? When the earth first got formed? When the universe started? In any scenario the chart would be just a dot which is useless.

Somewhat similar with the Y axis. Why not plot sea levels starting from zero – just to be “pure”? Again, the chart would be a straight line or a dot, depending on how you’d chose your X-axis.

I think clear formatting and indications of scale, and preferably charts of the same data over different timeframes, are much more useful (and not sensational).

rgds

WP

Bit of a kick up in north Dakota. Highest daily oil since March 2016. And two charts on Lynn Helms report for the first time. Snazzy. Not near the old peak though.

There was an increase in activity in May and June. That’s when the new pipeline started and so it might be due to that?

http://www.zerohedge.com/news/2017-10-13/saudi-aramco-reportedly-shelves-ipo-face-saving-move

“The FT notes that talks about a private sale to foreign governments – including China – and other investors have gathered pace in recent weeks, according to five people familiar with the IPO preparations, amid growing concerns about the feasibility of an international listing.”

The absurdity of reporter thinking is just silly. This is civilization’s lifeblood of which they have most — and money is created from nothingness. They have the first. The second is only a matter of convenience.

haha there is no face at risk here.

And btw, in the article it’s clear that sale to “governments” means sale to Sovereign Wealth Funds. The largest of those is Norway’s — funded by oil. Oh and I’ll have to recheck but I do believe the 2nd largest belongs to . . . hahahahahaha KSA.

No not quite.

2nd is UAE, from oil

3rd China, which is an investment fund and not really an SWF, but it listed as non commodity based and 3rd place

4th is Kuwait, from oil

and 5th is KSA, from oil

Oil is pretty much paying for oil — because that’s the only way to be independent of QE whimsy. This excludes the China entry. Somewhat hilarious. One is reminded of poker saying about looking around the table to figure out who the sucker is and can’t. China should think about that.

They could try an auction, 0.5 % of Aramco auctioned every 6 months for 10 years.

US Baker Hughes Rig Count (Oct 13)

Oil rigs fall by -5 to 743 and gas rigs fall by -2 to 185 also miscellaneous -1

Regions: GoM -2, Permian +1, Wiliston +1, Eagle Ford -6, Niobrara -1, Barnett -4

http://phx.corporate-ir.net/phoenix.zhtml?c=79687&p=irol-reportsother

Yeah, it will probably keep going down til the end of the year.

Hi GuyM,

Depends on oil prices, my WAG over the next 12 months the oil rig count in the US will be between 730 and 760, roughly a plateau around 745+/-15 oil rigs. This is based on an expectation of gradually rising (10%/year) oil prices starting in May 2018 and $45/b to $60/b from Sept 2017 to May 2018.

http://oilprice.com/Energy/Oil-Prices/Mass-EV-Adoption-Could-Lead-To-10-Oil.html

Oil at $10 a barrel by 2022, according to this genius. Of course, the government can always outlaw ICEs, like they are doing in other countries. Good luck with that.

I agree 2022 is not a good estimate, maybe 2045-2050.

I try to live in today, I will be pushing up daisies long before then.

Hi Guy M,

Long before then, the oil peak will be clear (by at least 2030 it should be obvious, probably 5 to 10 years in the rear view mirror). Oil prices will rise and EV sales will increase fairly rapidly over the 2020-2030 period. I doubt it will be enough to bring down oil prices to $10/b, though possibly oil prices may fall from $120/b in 2024 to $80/b in 2030, if EVs ramp up as quickly as I foresee (25%/year increase in EV sales for 10 to 15 years).

Funny that you should post that! In a response to watcher up-thread I was thinking of including a link to something similar but I was in a hurry to go out and didn’t bother. There’s another “genius” responsible for the following headline (video embedded at link):

$25 oil is coming, and a new world order along with it, think tanks says

The world as we know it, will be no longer. The balance of power on a global scale will shift. All in the next decade.

Sounds dramatic right? But independent think tank RethinkX says it’s be true because of rapid advances in technology, and specifically the advent of self-drive or autonomous cars.

First and foremost, RethinkX co-founder and Stanford University economist and professor Tony Seba told CNBC’s “Street Signs” that the rise of self-driving cars will see oil demand plummet, the price of that commodity drop to $25 a barrel, and oil producers left without the political or financial capital they have today.

“Oil demand will peak 2021-2020 and will go down by 100 million barrels, and will go down to 70 million barrels within 10 years. And essentially what that means is that the new equilibrium price in the oil markets is going to be $25. So if you produce oil and you can’t compete at $25, essentially you are holding stranded assets,” Seba said.

“At $25 that means deep-water, sands and shale oil fields, most of them are going to be stranded. And also, all the refineries and the pipelines associated with these expensive oil are going to be also stranded. And that is going to reshape, of course, worldwide oil geopolitics and so on.”

It’s a big call, but if you look at what’s behind Seba’s premise, it comes down to money.

He said the world will not stop driving altogether, people will just switch to self-driving electric vehicles, which will become a much larger part of the sharing economy. And these electric vehicles are going to cost less to both buy and run.

“The day that autonomous vehicles are approved, the combination of ride hailing, electric and autonomous means that it’s going to be 10 times cheaper, up to 10 times cheaper, to use a robo-taxi, a transport as a service car, than it is to own a car,” he said.

Essentially, he is saying that the active US car fleet will shrink to 10% of current levels by 2030, in that a sizable chunk of VMT will be shared cars (Transport as a Service -TaaS) many of which will be electric. The quote on “oil demand ” figures is strange in that it says “Oil demand will peak 2021-2020 and will go down by 100 million barrels, and will go down to 70 million barrels within 10 years. ” Examination of the Report Rethinking Transportation 2020-2030 from RethinkX on page 40 it says

U.S. oil demand from passenger road transport drops by 90% by 2030

Using the EIA’s BAU forecasts as the baseline, the results of our analysis indicate that oil consumption from U.S. passenger vehicles will decline from over 8 million bpd in 2020 to under 1 million bpd in 2030. Over 7 million bpd of oil demand will be eliminated by the TaaS disruption. The implication is that around 90% of the U.S. passenger vehicle market demand for oil will evaporate within a decade.

and on page 41

Global oil demand peaks in 2020 at 100 million bpd and plunges to around 70 million bpd by 2030

For our global oil demand scenario, we applied the annual rate of change in light-, medium- and heavy-duty transport oil demand in the U.S. to the oil demand forecasts in China and Europe in the same year, and to the rest of the world with a four-year delay. Figure 11 shows the outcome of this analysis: global oil demand will drop from 100 million bpd in 2020 to 70 million bpd in 2030. That is, total global oil demand will decrease by about 30% in a decade.

Maybe it’s all just crazy talk. Maybe not.

Could be possible for me. Just have to ditch my self employment and find some menial, less paying job. Sell my vacation place. Then I can ride share with someone who may even be more irritable than myself (if that’s possible). Yeah, ride sharing will be here next month, at least.

I don’t think he’s talking about car-pooling. Carpooling is significant at about 11% of commuting, but I don’t really see it expanding.

He’s talking about car-sharing, which is Uber/Lyft and taxis, but with autonomous EVs that operate with much, much higher VMT per vehicle.

Thanks. Still sounds pretty complicated for rush hour traffic.

Hi GuyM,

I test drove a Tesla in rush hour traffic in Boston (weekday between 5:30 and 6:30 PM, Mass Pike westbound for those who know Boston). The Autopilot mode worked surprisingly well.

Try it blindfolded and let us know how it went.

This kind of consumption drop is actually likely.

Price goes lower, oil doesn’t flow. People kill each other for oil (food) by the billions.

The reduced population doesn’t burn as much oil.

Makes more sense.

Let’s revisit this in another five years. By then the trends should be indicative of what’s possible or likely. I’ve lived through enough transitions and disruptions in my 55 plus years to not write this sort of stuff off. Remember Polaroid, Kodak, Bell & Howell (16 mm movies), VHS, 8 tracks, cassettes, Cathode Ray Tube TVs, vinyl records and turntables, typewriters, mechanical cash registers, rotary dial telephones, vacuum tube electronics and probably lots more? That’s just during my living memory. I never experienced steam ships or steam trains except for a ride on The Bluebell Railway that my British mother took my siblings and I on, during a one year stay in the UK back in the late sixties. Can’t think of any other reason why I would remember anything called “The Bluebell Railway”. I cannot recall ever seeing and have never flown in a large passenger airliner that wasn’t a jet.

“Over and out”.

“vinyl records and turntables”

Hell, at this point I think you can add CD’s and DVD’s to your list

Actually vinyl is making a huge comeback.

Audio aficionados like the analog richness.

Contemporary cruise missiles are accurate by comparison. Still, precision weapons never do seem capable of assassinating specific individuals (Saddam, Osama, Qaddafi), even when hundreds are dropped. And ray guns have not materialized—surely not for lack of trying. We can assume the Pentagon has spent billions on death ray research, but the closest they’ve come so far are lasers that might, if aimed correctly, blind an enemy gunner looking directly at the beam. Aside from being unsporting, this is pathetic: lasers are a fifties technology. Phasers that can be set to stun do not appear to be on the drawing boards; and when it comes to infantry combat, the preferred weapon almost everywhere remains the AK-47, a Soviet design named for the year it was introduced: 1947.

Have you looked around at all the SSTs still flying?

And how many manned moon landings there have been since the 1970s?

Of Flying Cars and the Declining Rate of Profit

https://thebaffler.com/salvos/of-flying-cars-and-the-declining-rate-of-profit

It was right around 1970 when the increase in the number of scientific papers published in the world—a figure that had doubled every fifteen years since, roughly, 1685—began leveling off. The same was true of books and patents.

Toffler’s use of acceleration was particularly unfortunate. For most of human history, the top speed at which human beings could travel had been around 25 miles per hour. By 1900 it had increased to 100 miles per hour, and for the next seventy years it did seem to be increasing exponentially. By the time Toffler was writing, in 1970, the record for the fastest speed at which any human had traveled stood at roughly 25,000 mph, achieved by the crew of Apollo 10 in 1969, just one year before. At such an exponential rate, it must have seemed reasonable to assume that within a matter of decades, humanity would be exploring other solar systems.

Hi Hightrekker,

Perhaps a levelling in the rate of growth in publishing has to do with a slowing in the rate of population growth. We will have to wait for the warp drive to see another big jump in travel speed.

For now we should focus on sustainability on this planet, though research on interstellar travel could continue.

Maybe Einstein was wrong, though so far observational evidence confirms his theories (as far as I know, I am not an expert).

I agree, survival is what is important now.

Population overshoot, runaway climate change, ecological collapse, resource constraints, superstition based economic systems, etc. are first priority.

Hi Hightrekker,

Superstition based economic systems?

Political Economics is a complex subject and experimentation is difficult and an understanding of political economics affects the behavior of people making theories (even those that are accurate) obsolete over time.

Being a forward thinker but not being the genius Tony Seba is, I think he is pushing the time line by a few years. Not to say this could not happen in specific countries or happen in regions to a large degree by 2030. The key here is his assertion that the number of cars will fall, making the transistion quite possible.

I don’t quite understand how the number of cars could fall that far but I don’t have detailed access to his methods. Maybe rush hour will be more distributed over time or people will just not go to work.

I do agree to the high potential of major changes in transport and energy the next 12 years.

His claim that oil will drop to 70 million barrels per day production by 2030 is better than some peak oil predictions and might just be in line with depletion anyway. When there is less demand for it, the pricey oil will not be pumped. Every time the price of oil goes up, further transistion away will occur. A self defeating situation.

His ideas on using relatively small storage batteries to disrupt the grid system are quite astute.

Fair amount of detail available in the 77 page report from RethinkX.

Hi islandboy,

I have read it. It is a matter of assuming high growth rates will continue, I think there will be growth, but believe the rate of growth will decelerate.

Hi islandboy,

Tony Seba’s vision may be correct, but it is a World market and I think the transiltion will be slower than he envisions. I hope I am wrong and Seba is correct.

Hope is nice, but policy solutions should not be based on hope alone.

I’d be a little surprised if things moved as quickly as Seba is projecting. On the other hand….

Isn’t China moving faster to EVs than we expected?

Hi Nick,

Yes much of the World is moving faster than the US and China is moving faster than I would have guessed 3 years ago.

As I said, I hope I am incorrect, but Seba seems overly optimistic to me.

Seba is a techo narcissist.

But the more EV’s the better.

Hi Islandboy,

It is unclear when autonomous vehicles will be approved. I agree that EVs may rapidly take market share, but the takeoff of TAAS depends critically on self driving cars.

It is unclear when autonomous vehicles will be approved for general use. I doubt 2020, but possibly by 2025. Lyft and Uber might allow for easy car pooling (ride sharing) and this might take off in urban areas cutting the need for passenger vehicles by half. Many families with several vehicles may be able to cut the number of cars owned to one or even to zero (vacations could be done in a rental vehicle.)

I find the subject of car sharing/TaaS intriguing due to the fact that we already have something that vaguely resembles that in Jamaica. Public transport is being taken over by cars. In the capital city there are four main public transport options: