All data below is based on the latest OPEC Monthly Oil Market Report.

All data is through July 2017 and is in thousand barrels per day.

The above chart does not include the 14th member of OPEC that was just added, Equatorial Guinea. I do not have historical data for Equatorial Guinea so I may not add them at all. It doesn’t really matter since they are only a very minor producer. Also they are in steep decline, dropping at about 10% per year.

The huge June OPEC production increased was due to a revision, explained below.

May OPEC production was revised upward by 18,000 bpd and June OPEC production was revised upward by 109,000 bpd. Counting the June revision July production was up about 280,000 barrels per day over what was reported last month.

Not much is happening in Algeria. They peaked almost 10 years ago and have been in slow decline ever since.

Angola peaked in 2010 but have been holding pretty steady since.

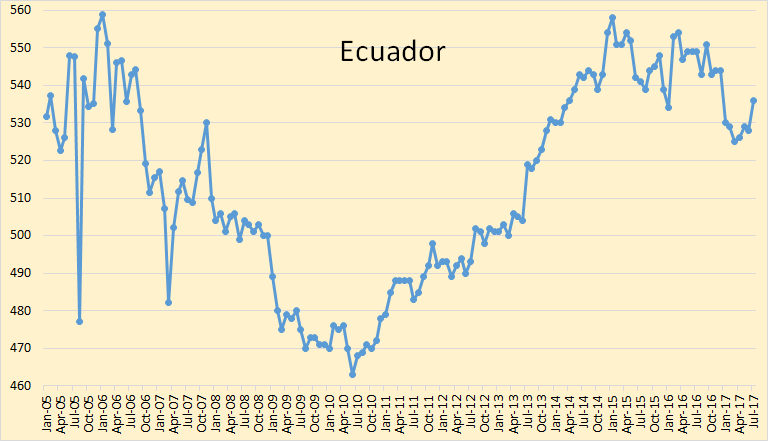

Ecuador peaked in 2015.

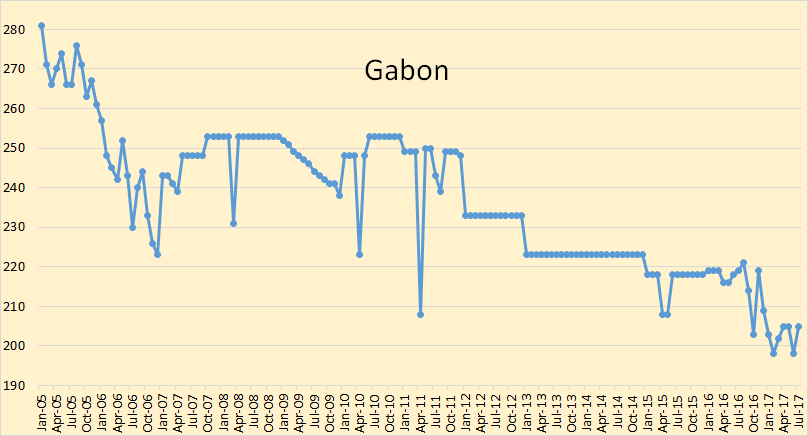

Any change in Gabon crude oil production is too small to make much difference.

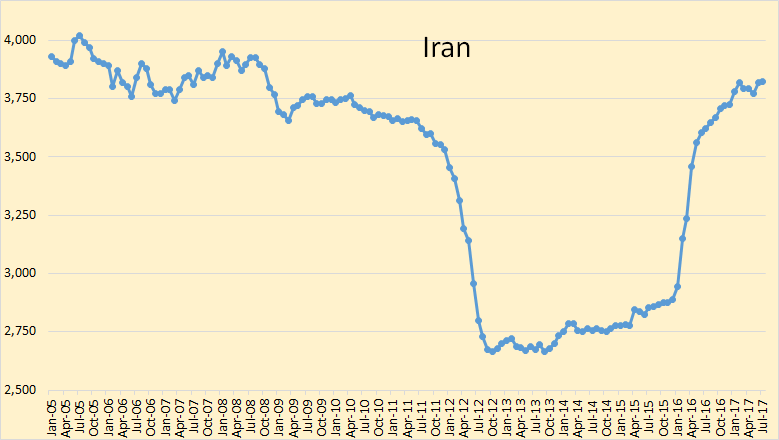

Iran’s June production was revised upward by 27,000 barrels per day.

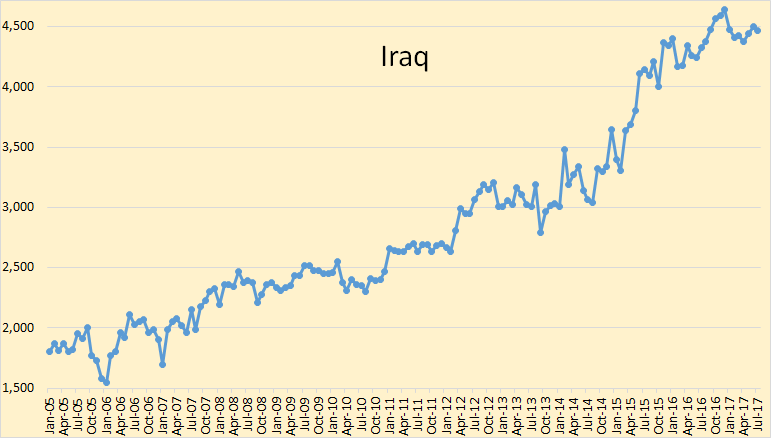

Iraq is holding steady since their December peak.

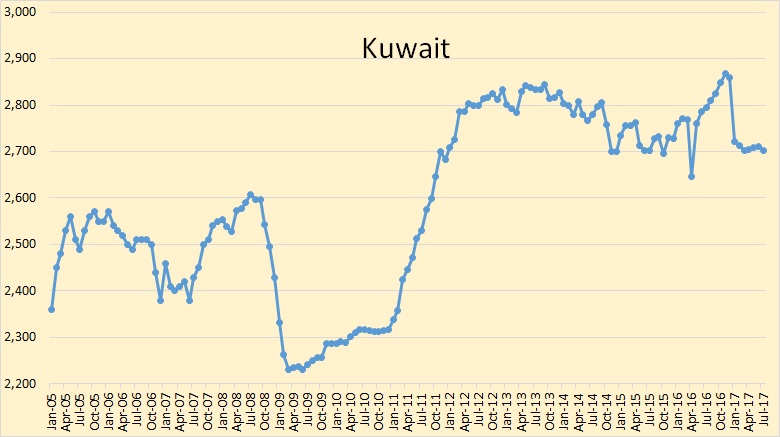

Kuwait is down 165,000 bpd from their November peak. That is about 5.75%.

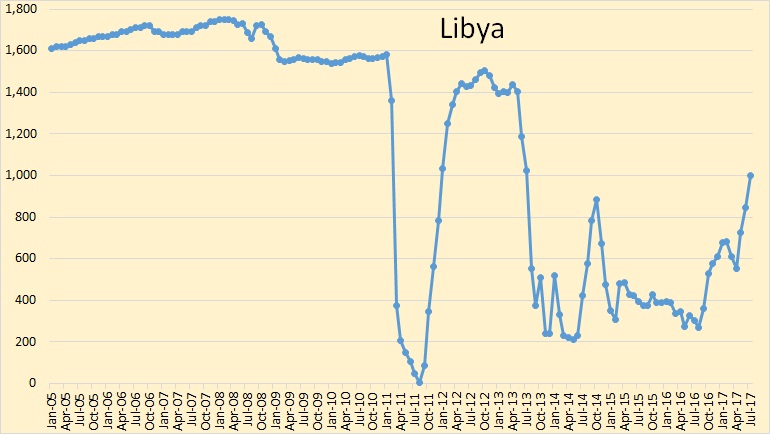

Libya is now producing just over 1,000,000 barrels per day. If this trend continues, and it just might, then they should be at their maximum possible production of about 1,400,000 barrels per day by the end of the year.

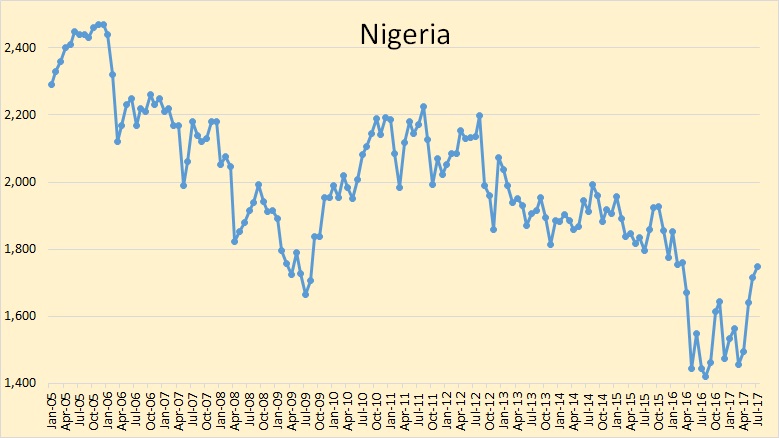

Peace seems to be breaking out in Nigeria as well as Libya. This is the worst possible scenario for oil prices.

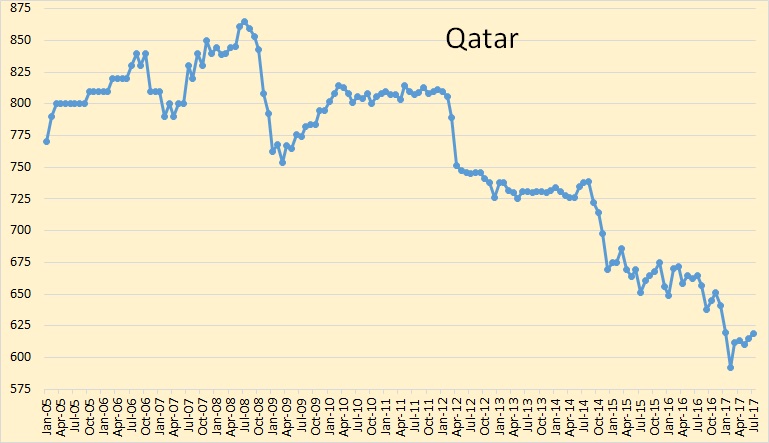

Qatar has been in decline since 2008. Her decline will continue albeit at a very slow pace.

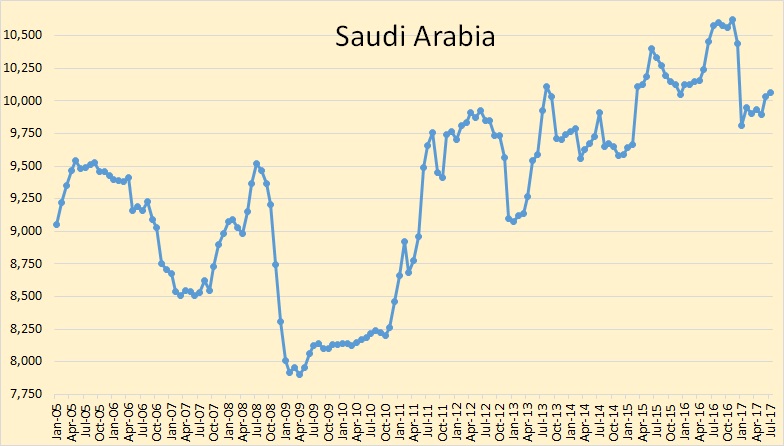

Saudi June production was revised upward by 85,000 barrels per day. That means they have increased production by 169,000 barrels per day over the last two months.

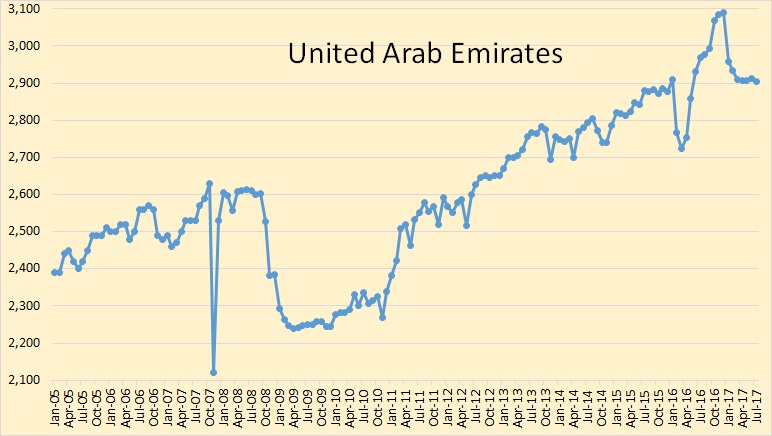

The UAE is down almost 185,000 bpd since December. This is the largest percentage cut in OPEC. I don’t think it is all voluntary.

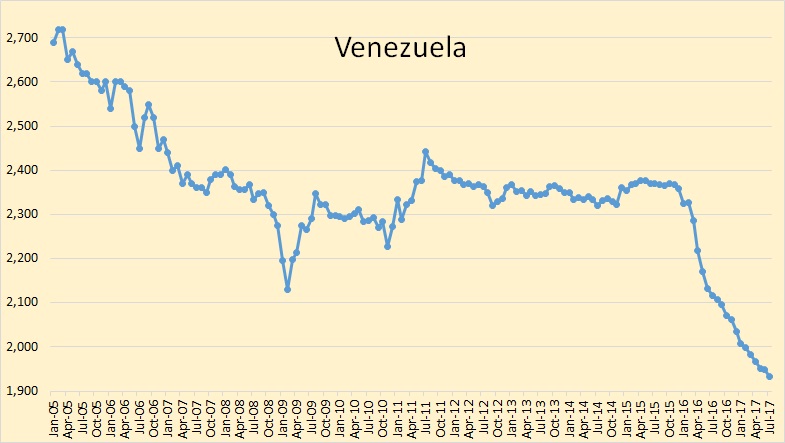

The production trend in Venezuela is obvious. It could get a lot worse as Venezuela is now on the cusp of becoming a failed state. If that happens it’s anyone’s guess as to what will happen to their oil production.

This chart has an error in the Y axis. It has Jun 17 twice. The last one should be Jul 17. At any rate World total liquids continues to rise. Yet oil prices continue to rise also. WTI is near $50 and Brent is just over $53. I have no idea what is happening here but something is just not right.

282 responses to “OPEC July Production Data”

I thought it was the case that oil prices correlate better with inventory data than with production data. That’s what Art Berman shows:

http://www.artberman.com/u-s-inventory-reductions-probably-not-sustainable/

Not too happy with perpetual demonization of pretty much anywhere by the western media. OTOH Ron reports the numbers as they exist (from OPEC), and odds are those numbers are pretty damn close to right.

But other things don’t make sense for Venezuela, specifically:

http://www.countrymeters.info/en/Venezuela/

https://en.wikipedia.org/wiki/Demographics_of_Venezuela

Relentless population growth doesn’t really mesh well with starvation stories and life is horrible this and that.

Update on their Sino-Russo-Goldman funded Puerto La Cruz heavy oil refinery and money flow in general:

Lemme first offer up a truth: If someone doesn’t borrow from US banks, it denies the prospective US lender business. Think about that for a moment. Loans are how the bank is supposed to make money (when the Fed doesn’t just give them return on excess reserves). Refuse to borrow from them and it comes right off banking executives’ bonuses.

Ven’s sovereign debt/gdp ratio is https://tradingeconomics.com/venezuela/government-debt-to-gdp FALLING. And that’s even with the denominator falling (contrast with US debt/GDP). US banks have zero reason to like this, and plenty of reason to want regime change and a govt that will borrow and fund the populace (who might also borrow).

A few weeks old: https://www.forbes.com/sites/kenrapoza/2017/06/13/venezuela-defaults-on-russia-is-goldman-sachs-next/#2f6ff9602bae

Operative phrase in the article:

Some bondholders in London immediately questioned whether or not the missed Russia payment constituted a default, the Financial Times reported. The International Swaps and Derivatives Association said it did not.

Don’t let your eyes glaze over, because this next part is critical to oil.

The ISDA, sportsfans, is the organization (comprised of and funded by . . . banks) who are given legal right to declare “credit events”. A credit event is a default. When there’s a default of one bond by a borrower, instantly all the borrower’s bonds are declared in default with repayment immediately required in full for them all. ISDA are the bozos that “carefully examined” the Troika’s loan arrangements for Greece (forced conversion of loans outstanding to much longer maturity and a different interest rate) and declared them to be right and pure and NO WAY IN HELL a total default (because of global systemic risk that would extrapolate). This was after an initial declaration of default for appearances sake. It got undone. And so we see now ISDA decided missing a payment on a Russia bond was not a default by Venezuela (likely because their bank members had some outstanding bonds from Ven).

Rosneft and Goldman are essentially the funding sources for Ven. Useful to understand that Forbes and others call these loans . . . “money for Venezuela”, but they are actually money for the state owned oil company, and a goodly chunk of those bonds is for the new refinery expansion (puerto la cruz) coming online next year that can process Orinoco Heavy. This will deny business to US Gulf Coast refineries that presently do that work. More reason for they (and their banks) to be unhappy.

Oh, one last item of complexity. JP Morgan has an index product of emerging market debt. Venezuela bonds are IN THE INDEX. Investors parking money in that EM Debt index are lending money to Venezuela, propping up the regime, angering the US gubmint.

I posted this at the end of the last oil post, but I will repost it here. Seems relevant.

“Yet markets’ dependence on central-bank largesse appears largely unabated. The decline of volatility readings and the rise of valuations in all asset classes seem to presume any market shock or economic downturn can be handily contained. Perhaps some lessons are easier learned than others.”

https://www.wsj.com/articles/aug-9-2007-the-day-the-mortgage-crisis-went-global-1502271004?=e2fb&mod=e2fb

Anyone trying to assess what is happening in Venezuela with MSM news from the US or the UK is just being throughly brain washed.

It is a race against time, with China and GS betting that things will work out.

Don’t know if iI would bet against them.

Senators urge Trump to avoid blockade of Venezuela oil shipments

“We believe it is critical to consider the role the U.S. energy industry and refining sector play in our economic and national security interest,” the senators wrote. “Blockading imports could inflict great harm on this industry and burden U.S. taxpayers with the cost.”

https://www.reuters.com/article/us-venezuela-politics-usa-idUSKBN1AR00Z

If you want to understand Venezuela’s current situation, read this:

https://www.ricknevin.com/

The childhood lead poisoning – violence link PREDICTED the current violence in Venezuela. It was predicted years in advance and the timing was predicted.

Venezuela had exceptionally large amounts of leaded gasoline burning until a very late date.

“. Useful to understand that Forbes and others call these loans . . . “money for Venezuela”, but they are actually money for the state owned oil company, and a goodly chunk of those bonds is for the new refinery expansion (puerto la cruz) coming online next year that can process Orinoco Heavy. ”

Wow. More banks setting fire to money for, I don’t know, personal entertainment? We’re going into a world oil glut, and they’re borrowing money building a refinery expansion to process oil which is relatively expensive to extract. Probably to produce worthless gasoline or diesel; I doubt they’re smart enough to build a petrochem-only refinery.

The banks seem about as sane as the KLF…

https://www.google.com/search?q=burn+a+million+quid&ie=utf-8&oe=utf-8

Here is perhaps the most important bit of information contained in the entire OPEC report.

Oh, heavens no. The most important information in the OPEC report is Libya output spiking. They’ve added 800K bpd in less than a year. The US will take years and years and years, if ever, to add another 800K bpd, given Alaskan declines.

That Libyan flow is high diesel liquid going right to Europe.

Also, that suggests that if shale declines in the US, we better make plans for a future with less oil. If geology doesn’t cooperate, or funding is cut off, things start to fall apart.

I suspect the companies cutting back on projects already see that. Get the money out of the company while you still can.

If OPEC had won its price war against US shale, the United States would be in a world of hurt, as would all oil consumers of the world.

At some point they likely will unless you think the US will out produce OPEC and continue to do so.

Boomer II: I’d be particularly interested to see an analysis of which companies are cutting back on or halting expansion (I believe Suncor, right?) vs. which ones are continuing to throw their money down holes in the ground. Might give us a better sense of who will survive the shakeout.

“Get the money out of the company while you still can.”

Rex Tillerson seems to be the true master of this, having engineered an excuse to sell out his entire holdings in oil companies, including huge amounts of restricted stock which he wasn’t really supposed to be allowed to sell for 10 years. Incredibly slick move.

Libya has had zero oil rigs since the end of July 2015. Production has been on an increase over the last 10 months or so. I calculate they produced about 208 Million barrels of crude in the last 10 months. I wonder how long Libya can maintain 1 MM BBLS day assuming there are no more war related disruptions let alone reach 1.4 MM BBLS day with zero rigs running.

What are the decline rates in Libya like? Is there any water or gas injection necessary to maintain pressure and production. Does starting and stopping production damage the reservoirs? Are they producing oil to maintain EUR’s or are they producing flat out? What about repairs and maintenance? What else?

Any insight would be appreciated.

Good questions all.

This is not shale oil. Libyan oil is like Ghawar. A well can flow big numbers for decades and decades.

Arguments in shale unfold about 400K or 700K total ultimate recovery for a well over what, 7 yrs?

Libyan wells will be talking about 73 MILLION barrels total ultimate recovery over maybe 20 years.

The point being that decline rates can be pretty damn small. 10,000 bpd day 1 and declines 100 bpd per year or something absurd like that. That’s what proper oil wells do.

Libya reserves 50-70 billion barrels, some of it shale. Most of it right and proper oil.

Libya has some of the best oil on the planet.

I think they are mostly water flood. I remember something suggesting that a prolonged shut down for them wouldn’t be good. Before the war there were (maybe still are) a few western countries there: Eni, Wintershall, Marathon, maybe Shell(?). There were reports of high depletion rates, shortages of injection water and looking at EOR, water-alternating-gas (WAG) injection and ESPs. They are the sort of things that go with extra mature fields. I doubt if anyone can tell you if they have maintained voidage replacement in some of the fields that have been on and off a lot, it might take a long time and a lot of seismic and flow tests to find out what things are going on.

Oddly enough, Suncor owned some Libyan wells. Maybe have sold them.

Libya’s largest oil field is El Sharara.

Mind boggling middle distillate yield.

Product %wt

C1 to C4 2.65

Naphtha 25.42

Kerosene 18.87

Gas Oil 28.33

Atmospheric Residue 24.73

Hmm needs revisiting. Thats by weight.

Revisited. Mind boggling is real. That stuff is LOADED with Kerosene and Diesel.

Looks like about twice what shale oil has.

Wow. My long-term projections say that gasoline demand will decline sharply, diesel demand will decline sharply, and kerosene demand (for aircraft) won’t. This puts Libya in the catbird’s seat, doesn’t it? They’re set up to have one of the highest kerosene contents per barrel (with very little refinery tweaking). The napthas will have to be cracked to NG, but there’s a huge demand for NG in Europe too, particularly with the desire to stop depending Russian supply.

EIA twip shows crude stock declines still continuing at the quite high rate seen over the last couple of months – down 6.4 mmbbls (about 1.4%) – but gasoline was up 3.4 and distillate down 1.7

Trump just said, on national TV, that the US is now an exporter of oil and gas. Sure we export some oil products but we are a net importer of oil and gas. We import approximately twice as much oil as we export. Our net petroleum imports average just under five million barrels per day. That does not make us an oil exporter. Trump and every one that supports him are goddamn idiots.

Also, politically if prices rise locally, voters could come back and ask why we are exporting it.

Ron Trump has lots of alternative facts that he hasn’t used yet. Its really all pretty laughable until you consider the consequences of having new alternative facts 24/7.

count me as a god damn idiot and freaking proud of it??

Already done, most here aren’t idiots

I would agree Huntington most here are not idiots… time/life wasting ignorant socialists yes…idiots no. I am glad to be the latter as productive member of our society who contributes in many ways to the quality of life my fellow country men enjoy. ON the other hand, just like roaches and rats we need to keep the time/life wasting ignorant socialist scope and influence to a minimum, as they will surely destroy the quality of life the productive “god dam idiots” produce in pursuit of their imaginary utopia.

I am glad to be the latter as productive member of our society who contributes in many ways to the quality of life my fellow country men enjoy.

You Sound a lot like Col. Jessep…

You Can’t Handle the Truth! – A Few Good Men

https://www.youtube.com/watch?v=9FnO3igOkOk

What a self-righteous prick … that Colonel Jessep was.

If HuntingtonBeach were running POB and not Ron and Dennis. I would ban “god dam idiots” until they paid an annual fee of $100. Because “god dam idiots” can’t appreciate something unless they pay for it in a capitalist system. Plus Ron and Dennis deserve compensation for running this “social utopia” site. Which also makes texas tea is a hypocrite cashing in on free social media (food stamps) “just like roaches and rats”.

Now man up to your words and send Dennis a check freeloader. And by the way, clean air isn’t free either. So if your business is polluting the lungs of others and your not paying them for it. Your a freeloader and not counting the social costs of doing business. So starting tomorrow lets make the oil industry pay for all asthma inhalers and related doctor visits needed.

A Day in the Life of a True Conservative[edit]

Joe Conservative wakes up in the morning and goes to the bathroom. He flushes his toilet and brushes his teeth, mindful that each flush & brush costs him about 43 cents to his privatized water provider. His wacky, liberal neighbor keeps badgering the company to disclose how clean and safe their water is, but no one ever finds out. Just to be safe, Joe Conservative boils his drinking water.

Joe steps outside and coughs–the pollution is especially bad today, but the smokiest cars are the cheapest ones, so everyone buys ‘em. Joe Conservative checks to make sure he has enough toll money for the 3 different private roads he must drive to work. There is no public transportation, so traffic is backed up and his 10 mile commute takes an hour.

On the way, he drops his 12 year old daughter off at the clothing factory she works at. Paying for kids to go to private school until they’re 18 is a luxury, and Joe needs the extra income coming in. Times are hard and there’re no social safety nets.

He gets to work 5 minutes late and misses the call for Christian prayer, and is immediately docked by his employer. He is not feeling well today, but has no health insurance, since neither his employer nor his government provide it, and paying for it himself is really expensive, since he has a precondition. He just hopes for the best.

Joe’s workday is 12 hours long, because there is no regulation over working hours, and Joe will lose his job if he complains or unionizes. Today is an especially bad day. Joe’s manager demands that he work until midnight, a 16 hour day. Joe does, knowing that he’ll lose his job if he does not.

Finally, after midnight, Joe gets to pick up his daughter and go home. His daughter shows him the deep cut she got on the industrial sewing machine today. Joe is outraged and asks why she doesn’t have metal mesh gloves or other protection. She says the company will not provide it and she’ll have to pay for it out of her own pocket. Joe looks at the wound and decides they’ll use an over the counter disinfectant and bandages until it heals. She’ll have a scar, but getting stitches at the emergency room is expensive.

His daughter also complains that the manager made suggestive overtures towards her. Joe counsels her to be a “good girl” and not rock the boat, or she’ll get fired and they’ll be out the income.

His daughter says she can’t wait until she’s 18 so she can vote for change or go to the Iraq War.

They get home and there’s a message from his elderly father who can’t afford to pay his medical or heating bills. Joe can hear him coughing and shivering.

Joe turns on the radio and the top story is a proposal in Congress to raise the voting age to 25. A rare liberal opinionator states that it’s an attempt to keep power out of the hands of working class Americans. The conservative host immediately quashes him, calling him “a utopian idealist,” and agreeing that people aren’t mature enough to make good choices until they’re at least 25.

Joe chuckles at the wine-swilling, cheese eating liberal egghead and thinks, “Thank God I live in America where I have freedom!”

Answer me this ?

“WHAT THE FUCK ARE THESE WHITE PEOPLE FIGHTING FOR?”

https://twitter.com/JuliusGoat/status/896326301832925184

This Is What ‘Oppressed’ White Men Look Like:

http://www.huffingtonpost.com/entry/what-oppressed-white-men-look-like-charlottesville_us_598f2ff4e4b09071f699f123?ncid=inblnkushpmg00000009

They all look like they are doing Alec Baldwin doing Trump.

6.5% of global GDP still subsidizing fossil fuels, study finds

The report’s authors work at the International Monetary Fund (IMF) and specialize in quantifying accuracy when it comes to subsidy payments that are often hidden from plain view.

The cost analysis looked beyond typical payments normally considered a direct subsidy, and examined also the other social and environmental costs that the world must bear in order to keep fossil fuels viable.

The authors stated that they looked at “not only supply costs but also (most importantly) environmental costs like global warming trends and deaths from air pollution and taxes applied to consumer goods in general”. According to the authors of the report, such a broader view is justified and accurate because it “reflects the gap between consumer prices and economically efficient prices”.

Direct, measurable subsidies for fossil fuels – grouped in the report as ‘pre-tax’ – amounted to 0.7% of global GDP in 2013, but when the wider view is taken – ie, applying the authors’ broader understanding of what constitutes a subsidy – then that figure rose to 6.5% global GDP in 2013 and has remained there until 2015 (latest data available).

By fuel type, petroleum and coal were the largest recipients of subsidies, the report found, with the China ($1.8 trillion in subsidies), the U.S. ($0.6 trillion) and Russia ($0.3 trillion) the three top subsidizers by nation. According to the authors’ reading of the data, the European Union (EU) collectively subsidizes less than half the amount that the U.S. does.

I guess the tentacles of the deep state how now captured the IMF too!

texas tea,

Just like Richard Rainwater, I used to be quite the fan of peak oil theorizing. But then the facts changed, so I changed my mind.

The most hardcore peak oil enthusiasts, and that’s just about all that’s left on the peak oil sites these days, don’t have much use for Trump’s pragmatism, as described here by Newt Gingrich:

If you don’t believe that crude oil is a finite and a non-renewable resource, you’re opinion doesn’t count. That includes Glenne.

The math that we do here to describe oil depletion is appreciated by many of the commenters on this board. That does not include Glenn.

What do we conclude by this? (1) Glenne believes in infinite oil and (2) is a neo-Luddite when it comes to technical modeling analysis. Like Trump, he is set in his ways and won’t learn anything new. Instead, he will find whatever marketing data supports his views and grinds on that … over and over.

Hi Texas Tea,

So you believe that the US is a net exporter of oil and natural gas in barrels of oil equivalent?

Aren’t you embarrassed to have a president that does not get his facts straight?

The rest of the World and the majority of US citizens just roll their eyes or shake their heads when they hear the crap that Trump spews.

Dennis,

If Trump said that “the US is now an exporter of oil and gas,” that is a empirical claim that is true.

And while the importance of this factually true statement (that the US is now an exporter of oil) may be lost on you, it is certainly not lost on those with skin in the game, like Harold Hamm, texas tea and myself.

US refineries are not set up to refine a great deal of LTO, which is a light, sweet crude that is similar in quality to WTI. That’s why exporting LTO/WTI to countries whose refineries are set up to refine light sweet crude is important. Exporting sufficient LTO/WTI to eliminate the current domestic glut of light sweet crude will eliminate the current discount that WTI trades at in comparison to Brent ($3.31 per barrel at yesterday’s closing).

Hamm spoke briefly about this on Wednesday:

Here’s the transcript of Hamm’s conference call:

.

Hi Glenn,

Yes it is true the US exports oil products and some crude.

It is also a fact that the US imports more crude plus products than it exports.

Now if one is then going to claim the US is “oil independent”, the claim would be false.

You are correct that moving light oil to where it can be refined more efficiently makes sense.

Trump was implying that the US was a net exporter of oil and natural gas.

Most US citizens are unaware of the distinction between net exports and exports.

Bottom line, the US produces far less oil than it uses and is highly dependent on oil imports. That is a fact.

Hi Glenn,

And here are crude imports for the US. The net crude imports (my chart below minus your chart above for the most recent month is about 7 million barrels per day. Also a fact.

Hi Glenn,

Net imports of crude oil from the EIA.

I wonder what that spike was in 1958? (US exports graph)

Suez Crisis, I think.

You must be right, thanks for the reply.

By support, do you mean those people who prefer him over the leader of North Korea, or terrorists? Isn’t idiots and politics the same thing?

Everyone who supports him is supposed to be anyone who is patriotic. Although, if the shoe fits, call a cow paddie a cow paddie.

You actually think that our only choice is between being a Trump supporter or supporting the leader of North Korea? Good gravy! Like I said earlier:

“Trump and every one that supports him are goddamn idiots.”

No. I don’t care if he is a Democrat, Republican, Independent, or whatever; he is President of the US. No matter how stupid. I didn’t bother to become a veteran, to ignore our system. If you don’t like it, you are entitled to complain. Got pelted by complainers when I got back from duty. I had to finally realize I did it for them, too. I may be an idiot, but I am proud to be a US citizen, and proud to have served.

The most profound election data item I watched election night was the inability of polling experts to grasp the key fact.

Populations of Michigan, Wisconsin and Pennsylvania are falling. They spent the whole night comparing Trump performance to Romney and Hillary to Obama in various counties of those states, and the population is less than it was. The comparison could not make sense, but they percolated along talking about it.

BTW, that key fact has a corollary. The people leaving aren’t leaving multi-generation family farms. They are leaving ghetto cities. That ain’t gonna reverse by 2020 and reapportionment of electoral college votes from the 2020 census won’t be in place by November because the census won’t be done.

Watcher, you simply haven’t checked the demographics. The cities themselves are still actually growing, in Pennsylvania and Wisconsin. (Michigan is a special case.) The people leaving ARE, in actual fact, leaving the farms.

Sorry to spoil your theory, but you have to adapt it to the evidence. The rural-to-urban population move continues unabated.

A Nazi tolerating asshole will never be my President, never be my Commander in Chief, and will never be welcome in my community.

https://www.scientificamerican.com/article/richard-dawkins-offers-advice-for-donald-trump-and-other-wisdom/

BEHAVIOR & SOCIETY

Richard Dawkins Offers Advice for Donald Trump, and Other Wisdom

The biologist and atheist, whose latest book was released this week, talks about the reliability of science, artificial intelligence, religion and the president

A question posed to Richard Dawkins By John Horgan on August 10, 2017

…In your new book’s introduction you allude to Donald Trump’s election, and say that now “more than ever, reason needs to take center stage.” What would you say to Trump if you had his ear? Do you think you could reason with him?

Mr. Trump, you appear to be laboring under the delusion that you have the necessary qualifications to be president. The manifest failure of almost everything you have attempted during your first six months, coupled with the anarchic chaos that pervades your White House, should give you pause—or would give pause to any person of normal sensitivity.

What advice would I give? Get your news, not from FOX but from all the sources available to a president, many of them not available to the rest of us. Announce your decisions after due consideration and consultation, not impulsively on Twitter. Cultivate common good manners when dealing with people. Do not be misled by the crowds that cheer your boorish rudeness: they are a minority of the American people.

Listen to experts better qualified than you are. Especially scientists. Be guided by evidence and reason, not gut feeling. By far the best way to assess evidence is the scientific method. Indeed, it is the only way if we interpret “scientific” broadly. In particular—since the matter is so urgent and it may already be too late—listen to scientists when they tell you about the looming catastrophe of climate change.

No I don’t think I could reason with Trump. Why would I succeed where so many have failed?

But he is so angry!

When it becomes obvious that there is not a rational response to Dawkins.

Liberals are especially good at the “angry” meme.

Dawkins has the equanimity of “a saint”.

Sorry Cabbages For Christ.

Ron Patterson

Oil for sure. But when it comes to natural gas, not any more.

Hi Glenn,

It was pretty clear that Ron was talking about the sum of oil and natural gas net exports in barrels of oil equivalent.

If we look at total petroleum (oil and natural gas) net exports for the US in barrels of oil equivalent, the number is negative, well over 10 million barrels per day.

Hi Glenn,

The “well over 10 million barrels per day” statement is wrong. I did not double check the data and remembered incorrectly. Net exports of crude oil is about 7.5 Mb/d for the US for the most recent monthly data reported by the EIA.

“Net exports of crude oil is about 7.5 Mb/d for the US for the most recent monthly data reported by the EIA.”

BIG typo I’m thinking.

Could someone in the know comment on the most recent shale profile.com update for the Permian? It shows a considerable decline. Just wondering thoughts. Will this be revised? Are some companies not reporting? Active areas not covered? Etc

Thanks much appreciated

What in the Permian is in decline? The old vertical wells are declining? Or as some wags suggest, are they drilling too many wells and demolishing the Permian? Probably, six months ago, I suggested it may happen to the conventional. EIA seems to forget there is a conventional Permian, and a horizontal Permian. Treats them both the same. Pretty stupid huh?

Then again, reality is not what the press or EIA is really concerned with.

http://www.rrc.state.tx.us/all-news/081017a/

Many people criticize the EIA for their accuracy [or lack there of]. So, why would you want them to report more?

???I would not want that. Merely pointing out that completions in Texas are 60% of what they were last year, and by this point last year, overall production started to decline. So, if some point, we see declines in Texas, it’s not a complete surprise.

The previous hype about the Permian increasing Texas production by the EIA and the press is pure BS. There may be a lot of extra DUCs, but they do not PRODUCE! They are also limited to future increases by the dearth of frac crews. In addition, Permian conventional continues to decline. The EIA projection of US production reaching 9.9 million barrels a day by the end of 2018 makes “Jack and the Beanstalk” look highly rrealistic. The oil companies started this with their profitable $40 oil junk.

EOG has managed to show a very slight profit by drilling 90% in their sweet spots. They have the biggest portion of sweet spots. $40 to 55 oil price will never get us to 9.9 million barrels. As gun shy as the upstream companies are about oil prices, a quick upshot in oil price, won’t make much of a difference.

“EIA seems to forget there is a conventional Permian, and a horizontal Permian. Treats them both the same. Pretty stupid huh?”

Excuse me! I thought that you were wanting the EIA to separate their projections of future oil production from the Permian into a conventional projection and a horizontal projection. Unless they do, it is impossible to determine that they are overstating/understating one or the other.

Hi Evolve,

The “decline” is due to incomplete production data from the Texas RRC. It takes about 6 to 12 months for all the production data to get reported.

The EIA’s LTO estimate for the Permian Basin is in the chart below. This estimate is different from Enno Peter’s estimate because it includes LTO output from both vertical and horizontal LTO oil wells.

Enno’s estimates include horizontal wells only and leaves out about 7% of wells where estimates are difficult due to multi-well leases with horizontal and vertical wells. Texas reports at the lease level so estimating well profiles is a challenge on leases with multiple wells that start production on many different dates.

Dennis: where do you think US production will end up this year and next year. You had a post earlier where you showed Permian will grow by 154000 barrels/day/year. What is your new estimate?

Hi Krisvis,

There are a lot of moving parts to such an estimate.

There is the Gulf of Mexico, Alaska, all US LTO plays and onshore conventional.

Let’s say GOM output remains flat at May 2017 levels (EIA expects a 300 kb/d increase by Dec 2018). We could also assume LTO besides the Permian will remain flat (slight increase in Bakken and slight decrease in Eagle Ford balance out). Assume onshore conventional and Alaska output decline at about 5% per year. That is about 3200 kb/d of onshore conventional plus Alaska with about 160 kb/d of decline each year.

Based on the 12 month trend of Permian output I expect about a 360 kb/d annual increase in output (difference in yearly average for 2016 and 2017).

So subtracting the conventional decline from Permian increase I expect about a 200 kb/d increase each year for the next two years.

A critical assumption is that oil prices remain $60/b or less over this period.

A spike in oil prices might lead to higher output than this very rough guess.

So 2016 output was 8850 kb/d and I expect 2017 output to be 9050 kb/d and 2018 output to be 9250 kb/d, if oil prices remain under $60/b (2017$) until Dec 2018.

Higher oil prices ($100/b) might result in the US surpassing the previous peak in annual output (9637 kb/d in 1970), perhaps by 2020. If this occurs it will be short lived and US output is likely to decline fairly sharply (4%/year or more) by 2025 even if oil prices are high (over $120/b in 2017$).

This is mostly because the sharp rise in LTO output is likely to be followed by a sharp fall in output between 2025 and 2030.

This is clearly speculation on my part. Future changes in technology, wars, economic crises and so forth will make these guesses incorrect no doubt.

A Saudi singer was arrested after dabbing during a concert

http://stepfeed.com/a-saudi-singer-was-jailed-after-dabbing-during-a-concert-3732

Wrong thread!

No, wrong site altogether…

IEA OMR Aug: https://www.iea.org/oilmarketreport/omrpublic/

Historic demand has been overstated, demand this year looks strong, global stocks are down (US is falling of a cliff).

Assuming demand remains healthy, all eyes are now on Libya and Venezuela.

“New data for non-OECD countries for 2015 reduces global oil demand by an average 330 kb/d in 2015-2018. For 2017, growth has been revised up to 1.5 mb/d, with demand reaching 97.6 mb/d.”

“OECD industry stocks fell in June by 19.3 mb to 3 021 mb on strong refinery runs and oil product exports, but are still 219 mb above the five-year average. In 2Q17, global oil stocks drew by 0.5 mb/d, including 0.2 mb/d in the OECD. Provisional data shows further falls in July, including the largest monthly US crude stock draw for more than three years.”

“Producers should find encouragement from demand, which is growing year-on-year more strongly than first thought. Our growth estimate for 2017 has been increased to 1.5 mb/d, including very strong data for 2Q17 when demand increased by 1.8 mb/d.”

I’ve stopped paying attention to small fluctuations in the demand numbers since I figured out that China’s strategic reserve increases show up as “demand” and their strategic reserve releases show up as “reduced demand”. They don’t disclose their stocks.

Makes a mess of the global numbers.

total world oil/liquids consumption for 2018 forecasted to be 100 million bd… 1.6 million bd higher than 2017.

https://www.eia.gov/outlooks/steo/marketreview/crude.cfm

sure glad some of us goddamn idiots are out there trying to find the stuff instead of spending their life on earth telling others what idiots we are for doing so?

Suppose someone found some oil and decided to keep it in the ground for their grandchildren as a mechanism towards achieving global domination in the future.

We humans discount the future, among other traits that at one time brought genetic fitness, but are now liabilities.

Got a problem with that in an Orwellian sense. The page is called “crude.cfm”, yet the numbers are in “all liquids”.

Crude is not the same as “all liquids”.

“goddamn idiots are out there trying to find the stuff “

So, you are finding the stuff in corn rows?

http://peakoilbarrel.com/wp-content/uploads/2014/01/C+C_detail_jul131.png

Some service companies maybe running out of room to keep cutting prices to try and stay in business, I think anything heavily into deepwater is especially getting clobbered).

OIL SERVICE FIRMS SEE FEWER, BUT BIGGER, BANKRUPTCY FILINGS IN 2017:

http://uk.reuters.com/article/us-oil-bankruptcy-idUKKBN1AQ2IC

http://www.haynesboone.com/~/media/files/energy_bankruptcy_reports/2017/2017_ofs_bankruptcy_tracker_20170731.ashx

This is terribly interesting. I would not have guessed that the first move in the collapse of the industry would be for the oilfield services companies to get sequeezed on price and declare bankruptcy, but I guess it makes sense.

It makes me wonder what the next domino to fall will be. Standalone refinery companies? Gas stations? Gasoline distributors? Perhaps someone with a better sense of the internal details of the oil supply chain can help me out here.

We know that the profits on oil are shrinking, because demand for the major products is flat-to-shrinking (over the several year horizon) while the cost of extraction from the ground and the cost of refining is increasing. The question is, *which segment* of the industry gets its profit margin squeezed to zero next? Eventually it’ll be nearly every segment, but they’re going to go down one at a time.

Kemp: Oil Market Marches On Towards Backwardation

http://www.rigzone.com/news/oil_gas/a/151360/Kemp_Oil_Market_Marches_On_Towards_Backwardation

Harold Hamm is also bullish about the long-term prospects for the price of oil:

Continental Resources CEO: Absolutely No New Debt

http://www.rigzone.com/news/article.asp?a_id=151354

Yes, and the longer it stays at this level, the harder it will spike.

You can’t even crank up fracking oil fast when most service teams are fired, no piplines are build to transport the stuff away.

No deepwater projects financed, old fields running dry and no enhanced recovery installations planned. When the decline starts kicking in, it will take years before the new production can kick in in acceptable numbers. These deep sea platforms, CO2 injection installations and pipeline networks for increased fracking don’t build themselves overnight.

High oil price over several months (investors are burned enough) first -> investing plans -> getting financing -> project planning, political troubles -> build the things while all service companies have shut down their services to minimum -> testing -> more oil.

At the moment we are still in the pipeline of projects financed in the “good years” with 90$ oil and buffered by fracking the middle of the sweetspots and the unlikely recovery of both Lybia and Nigera (together more than the LTO recovery 2016/17).

If there is a price spike, it should be good fun. It will simply cause increased substitition.

High oil price over several months (investors are burned enough) first -> investing plans -> getting financing -> project planning, political troubles -> build the things while all service companies have shut down their services to minimum -> testing -> more oil.

Now, consider the other sort of investing plans which happens in response to a high oil price. Investing in electric car and truck factories.

This is historically a slow process, but once a first factory for a given model is up and running, I’d daresay it’ll take about a year to clone it. It’ll be pumping out cars before the oil company’s hole in the ground is actually producing any oil.

Glenn, sometimes you post about how low oil prices are great for Americans and how we’re screwing OPEC in the process. Now you are posting about how oil prices will rise.

Your positions are all over the place. The only consistency is that you like oil and the Permian.

Hi Boomer II,

Glenn’s position is that we don’t know what the future oil price will be. There are those that argue that it will climb higher and others who argue that oil prices will remain low.

If that is his position, I agree that nobody knows for sure. My guess is that between now and 2020 oil prices will rise, but cannot predict the path that oil prices will follow from now until then.

My position is that from now to 2025, oil prices will definitely fall (in inflation-adjusted terms). However, I have two working scenarios: one involves a steady decline with plateaus, while the other involves a gigantic price spike followed by a monumental crash.

I honestly can’t say which is more likely. It’s an unstable system and it depends on the exact timing of a number of things relative to each other.

Reminder to the gentle decline people.

You don’t have to have a production peak to get global nuclear war derived from inadequate supply. You just have to have, precisely that, inadequate supply. That comes from demand that exceeds consumption.

If you want more than you can have, if you need more than you can have, you will take it from someone else by force.

Another thought: developing India / Africa / Middle/South America to a higher level would take more oil than even the most optimistic experts expect to produce. We would speek about more than 200 million barrels + / day.

So worldwide poverty is given with clinging to fossil fuel age – we have to break out here.

I think poverty is a given if driven by fossil fuels because I don’t see there will be a sufficient market for what those countries have to sell to get the money to buy the fossil fuels. If global trade slows down, developing countries don’t have a source of income.

I am more optimistic with clean energy technology because fuel supplies won’t be an on-going expense, which will give countries more economic autonomy. Plus, for countries like China and India, becoming a supplier of energy technology gives them something to sell which might be purchased by more affluent countries.

I’m looking at economic strategies and what might provide a better chance for economic survival in the future.

Hi Watcher,

The gentle decline assumes no nuclear war and no severe recession. Either assumption and perhaps both assumptions may prove incorrect. Hopefully nuclear war will be averted, I doubt that a severe recession will be averted between 2030 and 2040 so gentle decline (2%/year or less) might only occur until the severe recession begins. A Great depression would lead to sharp decline in global oil demand, low oil prices and falling suppy (probably at least 4%/year).

We’re not going to have a recession until the renewable energy boom starts hitting saturation point. That’s the lesson I take from previous technological transitions: they prevent recession until the majority of people have converted.

At that point the market can’t support continued expansion at the same rate, so a bunch of people get laid off, boom, recession.

This won’t be news to most here.

This is what the end of shale will look like

https://www.forbes.com/sites/ellenrwald/2017/08/11/this-is-what-the-end-of-shale-will-look-like/#51e9e6915a05

I stopped reading right there.

You are as dumb as they come. Don’t you get tired of being the pob useful idiot?

Interesting theory. With some underpinning.

Her position is lower costs are coming from cutting payroll expense, which is somehow aligned with oil price. The higher the price, the higher the wages. Somehow.

Then there is her graph:

https://blogs-images.forbes.com/ellenrwald/files/2017/08/Shale-breakeven-e1502399519233.jpg?width=960

I remember discussion here at $105/b in 2013 challenged whether or not shale was making money. A lot of analysis said no. Shale fracking was well underway by 2011, but stock prices for, say, WLL didn’t explode from 2011 to 2014. At all.

Even CLR only doubled. One would think a profitable activity that was drilling hundreds of new holes AND FRACKING THEM (no DUCs then) in NoDak each month should have translated into explosive profit for CLR if each well were profitable, but nope. The S&P rose something like 50% 2011 to 2014 and CLR only added another 50% to that.

This is not the stuff of big profits at higher oil prices. So she may be right. Price won’t save shale.

In the context of shale drillers getting their service providers to take less money so that “lower costs” were reported — a post or two ago I found Halliburton quarterly report text announcing increases in US shale revenue from their fracking services.

And so, now . . . Schlumberger: They lost money 2017Q2. From the CEO:

“North America revenue increased 18% following our rapid deployment of idle hydraulic fracturing capacity as land activity further accelerated during the second quarter, partially offset by further weakness offshore in the US Gulf of Mexico. In US land, revenue grew 42% sequentially, a rate almost double that of the 23% increase in land rig count, driven primarily by hydraulic fracturing revenue that grew 68% as completions activity intensified and pricing continued to improve. Directional drilling revenue in US land was also higher as longer laterals requiring rotary steerable systems and advanced drillbit technologies continued to drive drilling intensity. Despite the significant costs associated with reactivating equipment, all of our US land product lines were profitable in the second quarter, driven by higher pricing, market share gains, improved operational efficiency, timely resource additions, and proactive supply chain management.”

So . . . SLB and HAL aren’t taking those hits. Who is?

Baker Hughes (NYSE:BHGE): Q2 EPS of -$0.11

Calfrac Well Services (OTCPK:CFWFF): Q2 EPS of -C$0.15

Dril-Quip (NYSE:DRQ): Q2 EPS of $0.09

Halliburton (NYSE:HAL): Q2 EPS of $0.23

Weatherford (NYSE:WFT): Q2 EPS of -$0.28 in-line.

U.S. Silica (NYSE:SLCA): Q2 EPS of $0.38 in-line.

No, you have to get revenue. Not EPS. Did they get more money from their fracking services or not. Not earn more. Get more.

Don’t matter if they did so profitably. The question is were they the source of lower costs for their customers.

2017-08-11 North Dakota June production down -9 kb/day at 1.032 million b/day vs 1.041 million b/day in May. Producing wells rose to record 13,915 in June – NDIC.

North Dakota Directors Cut

The number of well completions decreased slightly from 66(final) in May to 63 (preliminary) in June.

Estimated wells waiting on completion is 865, up 35 from the end of May to the end of June.

Estimated inactive well count is 1,458, down 53 from the end of May to the end of June.

POST PEAK MEDICINE:

Dr Peter Gray: “Once collapse is in full swing health care will disappear almost overnight. Of all the industries in our complex world medicine has become one of the most energy-intensive, technology-dependent, and thus fragile endeavors that exists…”

http://www.postpeakmedicine.com/PostPeakMedicineBook.pdf

Conventional Oil Peaked in 2006 –IEA

http://imgur.com/a/hccu9

New Oil discoveries by scientists have been declining since 1965 and last year was the lowest in history -IEA

http://imgur.com/a/W60yn

International Energy Agency Chief warns of world oil shortages by 2020 as discoveries fall to record lows

https://www.wsj.com/articles/iea-says-global-oil-discoveries-at-record-low-in-2016-1493244000

Saudi Aramco CEO believes world oil shortage coming despite U.S. shale boom

http://www.foxbusiness.com/markets/2017/07/10/saudi-aramco-ceo-believes-oil-shortage-coming-despite-u-s-shale-boom.html

UAE warns of world oil shortages ahead by 2020 due to industry spending cuts

http://www.arabianindustry.com/oil-gas/news/2016/nov/6/more-spending-cuts-as-uae-predicts-oil-shortages-5531344/

HSBC Global Bank warns 80% of the worlds conventional fields are declining and world oil shortages by 2020

https://www.research.hsbc.com/R/24/vzchQwb

UBS Global Bank warns of industry slowdown and world Oil Shortages by 2020

http://www.telegraph.co.uk/finance/newsbysector/energy/oilandgas/12136886/Oil-slowdown-to-trigger-supply-crisis-by-2020-warns-bank.html

German Army (leaked) Peak Oil study concludes world oil shortages would collapse the world economy and world governments/democracies

http://www.spiegel.de/international/germany/peak-oil-and-the-german-government-military-study-warns-of-a-potentially-drastic-oil-crisis-a-715138.html

Perfect Storm: Energy, Finance and the End of Growth; Dr Tim Morgan Global Head of Research

https://www.tullettprebon.com/Documents/strategyinsights/TPSI_009_Perfect_Storm_009.pdf

For every one percent of conventional oil production that declines. Shale oil would have to increase by twenty percent to cover the difference.

-Douglas B Reynolds Professor “Oil and Energy Economics”

Special Report: Vladimir’s Venezuela – Leveraging loans to Caracas, Moscow snaps up oil assets

http://mobile.reuters.com/article/amp/idUSKBN1AR14U

texas tea,

Talking about being a “productive member of our society who contributes in many ways to the quality of life my fellow country men enjoy,” it looks like you guys up there in Oklahoma are doing all the good.

I saw this about the STACK and the SCOOP from Continental’s conference call:

“TRES C FIU 1-35-2XH float at the remarkable rate of 1,021 barrels of oil and 29.6 million cubic feet of gas per day or 5,953 Boe per day. This was a 9,750 foot lateral and it produced this rate at an impressive 6,500 PSI full income casing pressure. Adding in the additional 1,978 barrels of anticipated natural gas liquids post-processing, we estimate 24 hour rate for the TRES C would be 7,442 Boe per day with 40% of the production being liquids on [indiscernible] basis. Now I have to say, this is the strongest flowing well I’ve ever been associated with in my career.”

What? Strongest in his career?

But that is just pathetic.

The KSA Original Magnificent Five dwarf that pitiful thing. They are magnificent not in being the best, just being old. There are far better wells there than this one below. But this one is one of the originals.

‘Ain Dar well has flowed 66 yrs. Average flow (not initial flow, average flow) for 66 friggin years — 7180 barrels/day. These shale wells debate over whether they can ultimately recover what, 400-700K barrels? That Ain Dar guy has recovered 152 MILLION barrels to date, and is still flowing at 2100 bpd when it is 66 years old.

What bizarre hype from those CLR people.

CLR is a good company to review with regard to US onshore unconventional profitability. They sold just about all of their conventional wells, have not diluted shares and have not engaged in many joint ventures or other complicated transactions

CLR is out of the ordinary in that it is controlled by one investor, Harold Hamm. As I stated in the last thread, he started the company 50 years ago with one water truck.

I encourage readers to look at CLR financials from 2012 to present. Despite gains in greatly reduced service costs and increased IP’s, CLR hasn’t overcome the drop in oil prices from WTI 90+ and Henry Hub 4+.

Although I have also discussed that SEC PV10 is not particularly a good metric, I do think it is worth some noting of CLR PV10 in 2014, 2015 and 2016.

I agree with Mr Hamm, sub $50 WTI and sub $3 Henry Hub doesn’t work for most US onshore E & P. However, it could take US onshore E & P drilling through most of its reserves before prices rise, which would take more than 5 years.

Great for consumers, not so good for those investing in US onshore focused E & P’s. As consumers greatly outweigh the investors, overall a net positive for US economy.

Continental’s Achille’s heel is that most of its oil production comes from the Bakken, and Bakken crude sells at a substantial discount to WTI because of high transportation costs.

Traditionally this has amounted to about $8.50/barrel. However, as Continental reported,

The biggest reason the differentials are coming down is undoubtedly because the Dakota Access Pipeline became operational on June 1, 2017.

The large crude differentials also explain why North Dakota rig counts haven’t recovered the way those in Texas and Oklahoma have. It certainly isn’t because of poor well productivy. Well productivity of Continental’s new wells in the Bakken is almost double what it was before the new wave of completion techniques began being rolled out (starting in the second half of 2015).

CLR’s problem, as is the problem with most of lower 48 onshore, is the price of oil and gas is not high enough, even with lower costs for services and more productive wells.

I suspect we will see several years of low prices, similar to the 1990s. US shale will drill through the bulk of its reserves, and break even, with small profits and losses on either side.

Once the majority of locations have been drilled, maybe the price will rise assuming demand is still increasing. Then, a company like CLR will make money as a stripper well operator, operating 10,000 wells making 200K net BOEPD.

That is the goal of the private equity firms buying in the Bakken, I presume. I have seen some of the PE firms’ joint interest billings to non-operated owners in the Bakken. 15-75 gross BOPD wells with LOE & overhead of $8-15K per month. Routine work overs are lower, it seems, $25-50K. The PE firms have no production growth pressure, so they will maybe keep one rig active till it makes sense price wise to do more.

Hi Shallow Sand,

I think before long the OPEC cuts and the lack of investment in new large projects since 2016 (besides LTO plays) will start to reduce supply, demand will continue to grow, stocks will decrease and prices will rise.

I expect by late 2018 we may reach your preferred oil price level (55-65/b as I recall) and by the end of 2019 we might see oil prices reach $80/b (these are monthly average prices for WTI).

It might take oil prices at $120/b to cause another oversupply of oil (relative to demand at that price). Or we might never reach an oversupply situation for oil unless EV sales expand at 20% per year or more for a decade or two or there is a depression.

Dennis, you’re going to be wrong about demand. I run a lot of peak demand models. The older ones were pointing at 2030. The more recent ones were pointing at 2025. But the new models are pointing at 2023, because displacement of heavy trucks displaces an unusually high amount of oil demand, and I’d left those out of the previous models.

“Or we might never reach an oversupply situation for oil unless EV sales expand at 20% per year or more for a decade or two or there is a depression.”

I have no idea why the rate of growth of EV sales would DROP to 20% per year. This is not an evidence-based number.

The growth rate of EV sales, worldwide, has been *averaging* roughly 50% per year for the last 5 years. There is now evidence that it’s going to *accelerate*, particularly due to Chinese policy and expansion there. It’ll probably hit a battery raw material supply bottleneck at some point, since mines don’t seem to be opening fast enough, but that’s best described as a speed bump.

So you you think it’ll take a decade of EV sales expanding at 20% per year… it’ll only take 5 years of EV sales expanding at 50% per year.

My projections are based on the point when the rate of displacement of oil demand by EV purchases exceeds the *natural* decline rate of the fields. Basically every oil exploration & development project brings my date for the permanent oil glut closer to the present. Fields with accelerated depletion such as US shale push the date out further into the future, however.

But as one person commented, looking for the *permanent* oil glut is a bit pessimistic. We could see permanent low oil prices before the permanent glut hits: investors are forward-looking, sources of temporary glut could be ongoing shortly before the permanent glut hits, there could be half-finished oil wells still in the pipeline.

Hi Glenn Stehle,

It is the number of wells completed that matters, rig count is a very rough indicator of this as availability of fracking crews becomes an issue as output ramps up.

texas tea,

Don’t know if you saw it, but Michel de Rougemont wrote a rebuttal to the paper that alleges that fossil fuels are subsidized to the tune of 6.5% of GDP.

Here’s a link to the paper he is criticizing:

http://www.sciencedirect.com/science/article/pii/S0305750X16304867

And here’s Rougemont’s rebuttal:

http://blog.mr-int.ch/?p=4217

I thought this passage from de Rougemont was most germane to the discussion regarding a “productive member of our society who contributes in many ways to the quality of life my fellow country men enjoy”.

Also, as a higher carbon dioxide concentration in the atmosphere clearly favours stronger plant growth, huge agronomic benefits must be subtracted from damages allegedly due to climate change.

You’re both an imbecil and a demagogue! Guess you slept through Plant Physiology 101! And probably most other science classes as well…

https://www.khanacademy.org/science/biology/photosynthesis-in-plants/photorespiration–c3-c4-cam-plants/a/c3-c4-and-cam-plants-agriculture

Introduction

High crop yields are pretty important—for keeping people fed, and also for keeping economies running. If you heard there was a single factor that reduced the yield of wheat by 20% percent and the yield of soybeans by 36%, percent in the United States, for instance, you might be curious to know what it was.

As it turns out, the factor behind those (real-life) numbers is photorespiration. This wasteful metabolic pathway begins when rubisco, the carbon-fixing enzyme of the Calvin cycle, grabs O2

rather than CO2. It uses up fixed carbon, wastes energy, and tends to happens when plants close their stomata (leaf pores) to reduce water loss. High temperatures make it even worse.

Some plants, unlike wheat and soybean, can escape the worst effects of photorespiration.

C4 and CAM pathways are two adaptations—beneficial features arising by natural selection—that allow certain species to minimize photorespiration. These pathways work by ensuring that Rubisco always encounters high concentrations of CO2, making it unlikely to bind to O2

In the rest of this article, we’ll take a closer look at the C4 and CAM pathways and see how they reduce photorespiration.

Glenn,

You should be more critical of information that seems to support your ideas. For example, this guy doesn’t understand the concept of externalities.

with just muscle power we would still be at medieval levels

That’s not an externality, it’s a direct benefit enjoyed by the direct purchaser/consumer of energy products. And, as it happens, it’s a benefit available from a wide variety of energy products, not just fossil fuels.

Hi,

Here are my Bakken updates. A big drop in production for the 2010 wells. Production is now about the same as the 2007 wells when they were at the same age even though the initial production for the 2010 wells were more than 50% higher. Big drops also for the 2014 and 2015 wells. 2014 thereby continue to follow 2013 which follow 2012 which was a bad year. 2015 has dropped to the 2011 curve but is still above 2014 and 2013.

2007 to 2009 has seen increases in production lately.

GOR continue to increase for wells later than 2009, but the increase is maybe slowing down again. GOR increases for 2007 to 2009 seems to have leveled off.

For water cut 2007 to 2009 are again different from the other curves. Notice how water cut has increased significantly lately at the same time as oil production has increased.

Wouldn’t it be easier to compare wells by showing the GOR and water cut the same as production against months from start-up rather than against actual date?

Yes I see you point. When I first started sharing those graphs I wanted to show that the increase in GOR started around the same date. I have only been interested in seeing if GOR increases and how much it increases and not so interested in comparing that with other years. So I have not seen any need to change it. But I could provide that sort of graphs too if that is of interest.

Hi FreddyW,

It would be of interest to me. If it’s not too much work to produce.

Thanks.

Ok here it is.

Note that using this way of presenting the data, the first 12 months should be ignored as new wells are added every month and confidential wells are added until month 17 (also true for above graphs).

Measurement artifact? Gas takeaway capability is increasing.

Possibly – Freddy can you confirm that the GOR is based on wellhead numbers rather than sales?

Hi George,

I asked this question in the past, my recollection is that it is production not sales. Freddy W please correct me if I am wrong.

Yes it is production as I have said before.

Also if it was takeaway capacity, then I would have expected more sudden jumps and not a steady continues increase over many years as it is in the graphs.

And here.

Thanks – I don’t know what it all means exactly but the trends are really consistent, and much more evident than I expected, and you would think they can’t go on like that for many more years. It’s either completions method or geology or both, and you’d think the opposite would be happening if it was geology, given that the last couple of years the wells have all been in core locations. It seems to all fit with higher initial flow – i.e. higher flow, will decline faster so more gas, and also can carry more water overall, but I find it difficult to image that won’t mean a much faster decline at some point.

I can also mention that 95 wells were put on production in June which is the highest number since September 2015.

Hi Freddy,

How many of those 95 wells were confidential wells and were the remainder Bakken/Three Forks wells?

Thanks for the info.

I created two scenarios for future Bakken output based on the assumption that the current new well EUR remains constant until December 2019 and then decreases after that based on the number of completed wells (a higher completion rate causes new well EUR to decrease at a faster rate).

The lower scenario has 95 wells per month completed until the end of 2030 and then fewer wells are completed (one less each month) until no further wells are completed in December 2038. Total wells completed is 31,840 wells from 2005 to 2040. URR is 9.1 Gb for this scenario through December 2040.

The higher scenario reaches a maximum of 160 new wells completed per month with an increase of 5 new wells per month until 160 new wells per month is reached. The number of new wells completed decreases by 1 each month starting in Jan 2026 until reaching zero. Total wells completed is 40,000 and the URR is 10.9 Gb though 2040.

The peak of the low scenario is about 1100 kb/d and the peak of the high scenario is about 1550 kb/d in 2021. Lower or higher scenarios could be created, but my expectation is that there is about a 90% probability that the actual output will fall between these two scenarios, with the most likely scenario near the average of these two scenarios as far as peak output (1325 kb/d) and the timing of the peak (2020 to 2023). I also expect URR from 2005 to 2040 to be about 10 Gb (about 2.2 Gb has been produced through June 2017).

The precise path of future North Dakota Bakken/Three Forks output is impossible to predict.

24 wells are non-confindential. I don´t know how many are Bakken/Three forks wells, so there could be conventional ones among those 95 wells.

Or actually 49 are non-confidential. But only 24 of those have been added to this page:

https://www.dmr.nd.gov/oilgas/bakkenwells.asp

The rest could be conventional wells or will be added to that page later.

Hi Freddy,

Is there any evidence that many of the 2008 wells were refracked after about 75 months online? This would have been in 2014 to 2015, I am not sure if there is anything in the NDIC data that confirms this, as it is speculation on my part.

I suppose it could be due to closely spaced wells near these 2008 wells that were completed around this period (2014-2015) that might have affected the 2008 wells.

It seems strange that mostly 2008 wells were affected, perhaps there are more 2008 wells in the “sweet spots”.

Hi Dennis,

I don´t know which wells are have been refracked. But, if you remember, I did a deeper investigation of the data at the time and found out that most of the wells (but not all) which hade significant increases in production were in Parshal and close to newly completed wells. EOG drilled a lot of new wells in that area at the time. So my theory has always been that it was because of the “halo effect”. Also, I think someone here on the forum said that refracking is not very common. But maybe that has changed now?

Freddy, if we’re talking about the red line’s uptick before resuming decline, useful to note the axis. The uptick is only what, 20 bpd? Not very big numbers in the overall scheme of things.

No not if it quickly goes back to previous levels. But if it stays higher than it should have been if it did not happen, then it will add up to a large amount in the end. Hard to say though what production should have been and what it will look like in the future.

Thanks for reminding me, I had forgotten that you had confirmed that the “halo effect” was the likely cause of that increase.

“2015 has dropped to the 2011 curve.”

As has been mentioned before, this bespeaks faster decline for longer laterals and newer technology. 2015 wells were longer than 2011 with different choke management. Stage count increased in those 4 yrs, but those longer wells are now flowing what 2011 wells flow, despite their longer length? Do I have that right?

If so, this is grim.

It could be that because of close well spacing, many of the new wells are completed in partly depleted areas which more frack stages and more proppants cannot fully make up for. Pumping up the oil faster, as faster increasing GOR suggests, can temporarily increase production but it will deplete the reservoir faster and cause higher decline rates later as we now see.

Hi Watcher,

My understanding is that the lateral length has remained relatively constant in the Bakken/Three Forks from 2008 to 2017 (and possibly since 2005).

In the Permian basin there has been an increase in lateral length based on Enno Peter’s work at shale profile.

You are definitely correct that there has been an increase in frack stages and proppant per well in the North Dakota Bakken/Three forks.

The ‘shale revolution’ ends with a bang

http://consciousnessofsheep.co.uk/2017/08/12/the-shale-revolution-ends-with-a-bang/

[…] above graph, taken from the ‘OPEC July Production Data” post at the Peak Oil Barrel blog, shows total oil production, in thousands of barrels per day, for the 13 members of OPEC, for the […]

China production had a good month in June, but gave it back in July. They have held a plateau for about a year though after big drops earlier (numbers based on 7.5 bbls per tonne). I think they have one platform shut in because of a leak, but I don’t know it’s production.

This seems to be making the news today: Chinese crude oil refinery input in July at 10.7 million b/day, which is down 0.5 from June. But its still up year over year…

Reuters

Chinese refineries processed 0.4 percent more crude oil in July than a year earlier at 45.5 million tonnes, or about 10.71 million barrels per day (bpd), data from the National Bureau of Statistics showed on Monday.

“Runs were slightly below our expectations, as fuel demand growth remained tepid and stocks were brimming,” said Harry Liu, a downstream consultant with IHS Markit.

https://www.reuters.com/article/us-global-oil-idUSKCN1AU03C

Chinese crude oil imports, seasonal, chart on Twitter

https://pbs.twimg.com/media/DHLfjiuXYAENSXj.jpg

Chart of Chinese inventory from the OPEC MOMR to June

Typo, missed the units, “down 0.5 million b/day from June”

Regarding refinery runs, I don’t know if the drop is seasonal or not. In 2016 China’s statistics bureau shows a dip at this time of year whereas JODI Data only has an activity dip in October.

“stocks were brimming”

They are not “brimming” in the graph. And why did the Chinese build up crude stocks when the price was high and then has been selling off the crude stocks after the price dropped (or at least not imported enough oil)? This makes no sence at all.

Yes, not much sense looking at the official data. I’m guessing that those official figures don’t include independents inventories. The independents have been building their own tank farms.

There must be something going on as there is said to be a “retail petrol price war”…

BEIJING (Reuters) – Chinese oil refineries operated in July at their lowest daily rates since September 2016, official data showed on Monday, to ease brimming inventories as state-owned oil giants faced off independents in a retail petrol price war.

Amid the glut of refined fuel products, Sinopec and state-owned rival PetroChina have been waging a retail price war against the independents known as “teapots” at the nation’s petrol stations. The competition for sales started in late March and by June had spread beyond the most heavily oversupplied provinces in the north.

https://www.reuters.com/article/us-china-economy-crude-output-idUSKCN1AU18K

And there is this too…

2017-08-08 Saudi Aramco to cut crude oil supplies to Chinese customers by 5% – 10% in September

It would have been interesting to know where the persons who say the inventories are brimming get their data from. It´s clearly not from the official data.

Hi FreddyW,

Maybe Fox news 🙂

Yes maybe :).

Platts – OPEC cuts and the light/heavy oil imbalance – August 14, 2017

Now seven months into the OPEC/non-OPEC deal, and the agreement has not yielded the desired affects, particularly because the cuts have proved toothless in tackling the imbalance of light and heavy crudes.

The cuts have largely come from oil producers that produce heavy and sour oil, and the glut of light sweet oil remains.

Libya and Nigeria, the two countries exempt from the deal, produce mainly light sweet crude, and with production in both recovering, this imbalance has been further skewed.

Libyan output is now at four-year highs and Nigerian production is close to 18-month highs.

To make matters worse, 2017 has also seen the resurgence of shale oil, resulting in yet more light more sweet oil, in a market awash with oil of this quality.

Platts: http://blogs.platts.com/2017/08/14/light-sweet-crude-barrel-glut/

I suppose this should go in the non petroleum thread, but it’s old and about dead, and besides, what happens in Venezuela is very important in terms of world oil markets.

I copied this directly from Fernado’s blog, which hit my inbox a few minutes ago.

“Beatriz, a Venezuelan lawyer, and her son reached Chile yesterday at 4:30 am, made it through Chilean immigration ok. She was robbed by Venezuelan border guards on her way out, but she managed to get away with $1000 she had put in a very secret place (I had told her she was likely to be robbed, to keep a believable amount of money in her purse, and hide everything else).

She says the border guards were very happy to see she had USA dollars they could steal, and since she kept quiet they didn’t search her bag thoroughly, so she managed to arrive in Chile with her diplomas, birth certificates, reference letters, and other documents which will help her get a visa. Chile is being very kind with Venezuelan refugees, so there’s a huge flow by road and air.

Beatriz says it’s very cold in Santiago, so she was going to buy two air mattresses and two blankets. She has friends who took her in, but they don’t have the furniture or beds for her to use. I suggested she also buy warm clothing, and go to the market, buy vegetables and chicken to make soup, because she has to keep herself and her son warm. Getting sick at this point in time would be a serious blow because she’s there on a tourist visa, and has no right to public health care services.

Based on the number of Venezuelans who went to the opposition sponsored consultation on July 16th, there are 2 million Venezuelans abroad, and roughly 50 thousand per week are leaving. This exodus doesn’t seem to get much coverage. ”

It surely does seem to me that what’s going on in our own backyard in Venezuela ought to be making headlines day after day, at least here in the USA.My personal opinion is that Venezuela gets twenty percent, or maybe a little more, of the coverage that would be easily justified, in our Yankee msm.

Maybe the mainstream media are embarrassed to cover Venezuela NOW because they ignored the situation there for so long, possibly because of political biases on the part of managing editors. This last remark is MOSTLY sarcastic in nature.

It’s hard to predict how much longer the Maduro regime will be able to keep oil flowing …

How much would it affect the oil markets if production there crashes to pretty close to zero?

Hi Old Farmer Mac,

Please do not post instructions on how to sabotage an oil field on this blog, some of the other stuff is interesting.

Also not that non-Petroleum comments can be posted in the Electric Power Monthly post.

In general there will be occasions where there are two posts and the second post may be on a non petroleum topic (such as electric power or renewable energy), any non-petroleum topic can be discussed in that second thread.

Wait, sabotaging oil fields is CRITICALLY important information. I don’t see it in his text.

Sabotage from the perspective of bombing pipelines or blowing up some pumps . . . no one cares about that. Too obvious.

But if someone has a way to inject something into the ground, or execute some water drive procedure that PERMANENTLY destroys oil in a field, that is something that should be discussed.

We had a conversation some years ago about bioengineering the oil spill cleanup bacteria to function at the temperatures and pressures of oil underground. Doug had excellent info on that and how difficult that environment is. If there’s a different technique known, that needs to be talked about.

Hi Watcher,

Then find some other blog to discuss it on.

Dood, we already did. Extensively. You are changing censorship policies?

Hi Dennis,

I get it, and will not post any comments in the future that can be construed as directions or suggestions for saboteurs. Sorry about that, I failed to think about implications for the blog.

But the question is still a valid one. Considering the situation in Venezuela, it’s entirely reasonable to speculate that oil industry there will collapse for lack of spare parts and other necessary inputs that must be imported.

Most of the key skilled workers from other countries are apparently already gone.

So- Does anybody have an opinion as to how much the price of oil might go up if the Venezuelan oil industry goes belly up?

I don’t have a clue, because I’m guessing that maybe a couple of countries such as Russia and Saudia Arabia might have enough spare capacity to take advantage of the opportunity to sell enough more to offset the loss of Venezuelan production.

Consider this: Angola kept producing oil for decades despite a really nasty and long-running civil war. Nigeria keeps producing oil even though rebels keep attacking and seizing the oil fields (the *rebels* sell the oil).

The problem with oil is that, once you’ve got the well and the pump, it just comes out of the ground. It can, therefore, be *stolen*. Like gold. Or jewels.

It’s not like… say… expertise. You can’t “steal* scientists because they will just refuse to work for you, or sabotage your work. One reason the Nazis had a disadvantage was that scientists were frequently volunteering to work for the US and Russia, while many were half-heartedly trying not to finish their assignments for the Nazis, or were defecting if they could.

There is a theory that war is decreasing throughout the world because it’s impossible to take home booty. The US is known for its great universities… attempt to conquer them by force, and you get nothing.

But oil can just be taken. Venezuela’s fields are not super complicated. I see no reason why it would be disrupted more than *Angola*.

Looks like the “bubble point death” theory is stiking out one more time.

Hi Glenn,

Permian output has risen by about 200 kb/d in the first 6 months of 2017 based on EIA tight oil estimates. Perhaps the second half will be better (300 kb/d), but according to several companies there were plans to cut back on capital spending in the second half of the year.

If there is more natural gas produced this will increase the barrels of oil equivalent produced, but the aim for Permian producers is oil not natural gas. Texas and New Mexico have pretty strict regulations on the amount of natural gas that can be flared and I wonder if pipeline capacity and flaring regulations might limit output in the second half of 2017.

Also for the past 4 months (February through June) Permian output has only increased by 60 kb/d, if that rate continues through December 2017, then Permian output would only increase by 90 kb/d in the second half of 2017. Time will tell, my guess is 150 kb/d for the second half of 2017 with a low to high range of 100 kb/d to 200 kb/d.

Oh and this “bubble point of death” is not a widely held theory as far as I can tell and it’s not Art Berman’s theory.

Link to post on the theory below by Scott Lapierre: