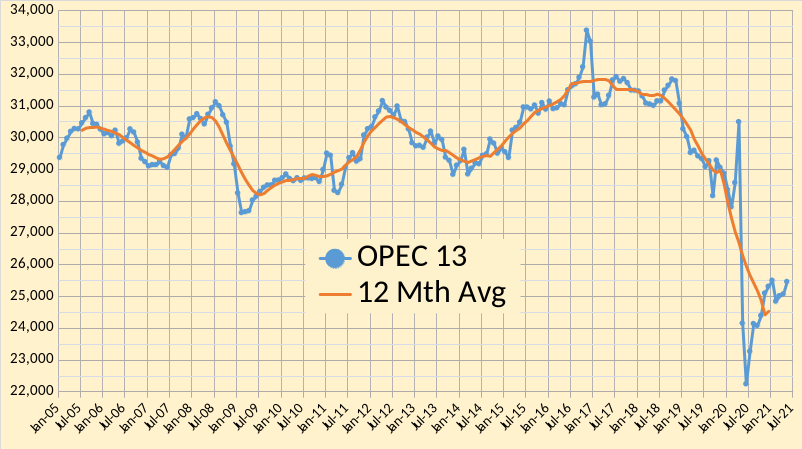

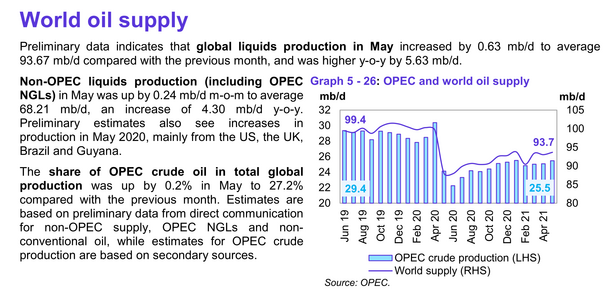

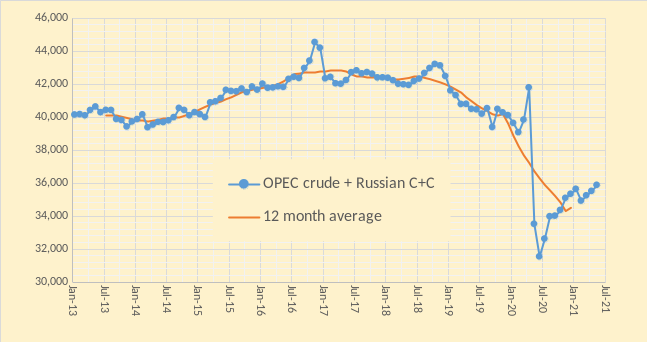

The OPEC Monthly Oil Market Report for June 2021 was published this past week. The last month reported in each of the charts that follow is May 2021 and output reported for OPEC nations is crude oil output in thousands of barrels per day (kb/d). In the charts that follow the blue line with markers is monthly average output and the red line without markers is the centered twelve month average (CTMA) output.

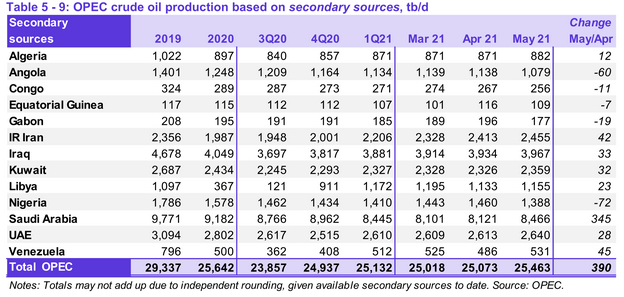

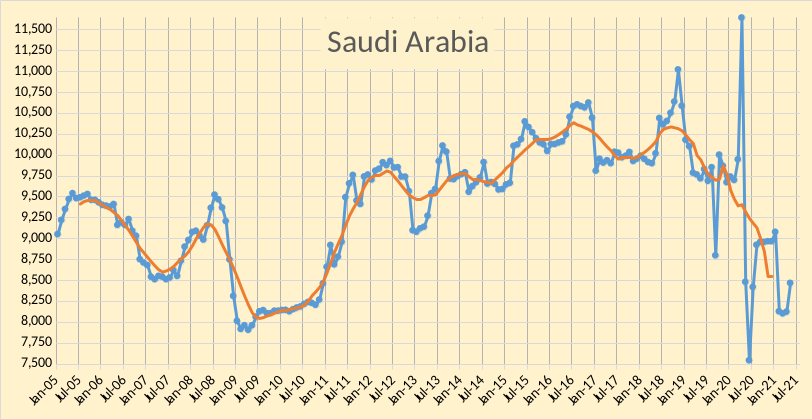

Only a small revision in OPEC output from last month’s April estimate (-10 kb/d), and a slightly bigger revision for March (-39 kb/d). OPEC output was up by 390 kb/d in April with most of the increase coming from Saudi Arabia (345 kb/d).

The OPEC world oil supply estimate of 93.67 Mb/d for May 2021 is about 6.4% higher than the World oil supply estimate for May 2020. Output remains about 6% below the level in April 2020 (99.5 Mb/d).

The chart above uses data from the Russian Energy Ministry and converts from metric tonnes to barrels at 7.3 barrels per tonne, the combination is OPEC crude plus Russian C+C output. Russian output decreased by 23 kb/d in May 2021 to 10410 kb/d, April output was revised up by 16 kb/d. OPEC13 crude + Russian C+C output increased by 367 kb/d in May 2021 to 35873 kb/d. The centered 12 month average OPEC crude plus Russian C+C output in Dec 2020 (most recent data point) was 34504 kb/d an increase of 197 kb/d from the Nov 2020 level.

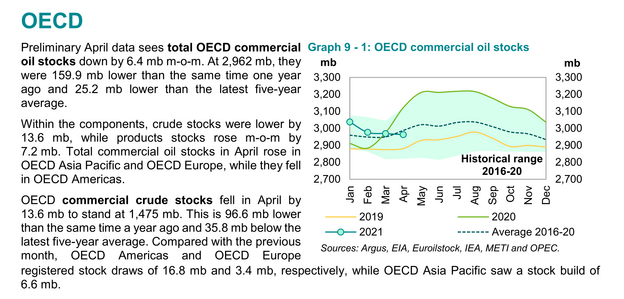

April OECD commercial oil stocks were 25,200 kbo below the 5 year average (see figure 18 above). OPEC crude output for the March to May period was was about 25,200 kb/d. OPEC estimates demand for OPEC crude in the second quarter of 2021 will average about 27,090 kb/d. If the OPEC demand estimate for OPEC crude is correct and OECD oil stocks roughly reflect the level of World oil stocks, then for the remaining months of the second quarter of 2021 (May and June) we would expect OECD oil stocks to continue to decrease. For OPEC to balance the World oil market at their expected levels for non-OPEC output and world Demand for the third quarter of 2021 would require an increase in OPEC output of about 3.4 Mb/d to and fourth quarter output would need to rise by another 600 to 700 kb/d to meet world demand for oil.

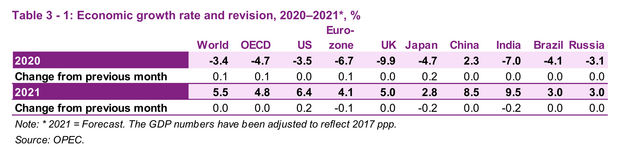

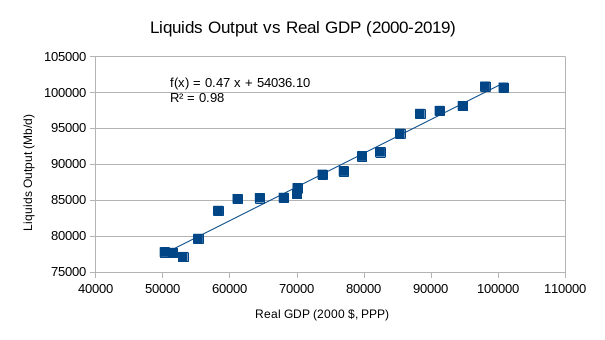

Consider figure 21 above which estimates World real GDP growth (using PPP) in 2021 at 5.5% (IMF estimates about 6% growth in 2021). Also consider figure 22 above which considers World liquid fuel output from 2000-2019 (EIA data) on y axis versus World real GDP (in 1982 international dollars based on PPP) on x axis. If real GDP grows at the rate estimated by OPEC in 2021 and oil demand follows the 2000-2019 trend, then a demand for oil of 102.4 Mb/d would be expected in 2021. For comparison the OPEC estimate for World oil demand in 2021 is 96.6 Mb/d. It is doubtful that the 102 Mb/d estimate is correct, but it is possible that OPEC may be underestimating demand in 2021. If so, we may see $90/bo for Brent (in 2021 US$) by the end of 2021.

183 responses to “OPEC Update, June 2021”

Dennis, you wrote: Russian output increased by 23 kb/d in May 2021 to 10410 kb/d,..

No, Russian output decreased by 23 kb/d in May.

43403 42877.1 44207.6

…….31 ………. 30 ………31 (days in the month)

Mar-21 Apr-21 May-21

10,263 10,476 10,453 (barrels x 7.33)

I use 7.33 barrels per ton while you use 7.3. And you forgot the “Read More” link.

Otherwise great post, Thanks

Thanks Ron. Corrected.

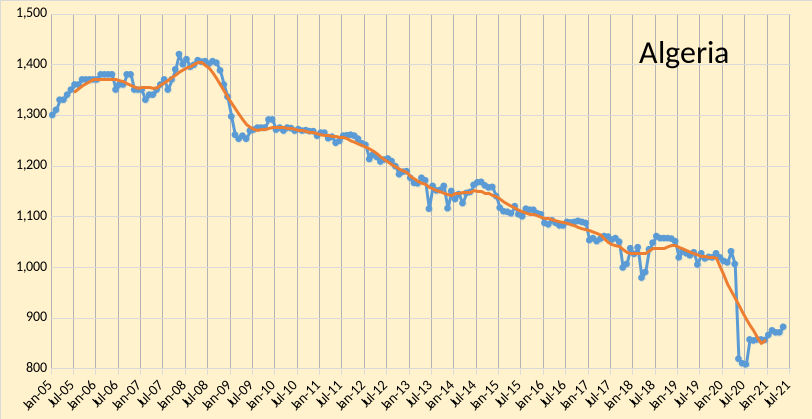

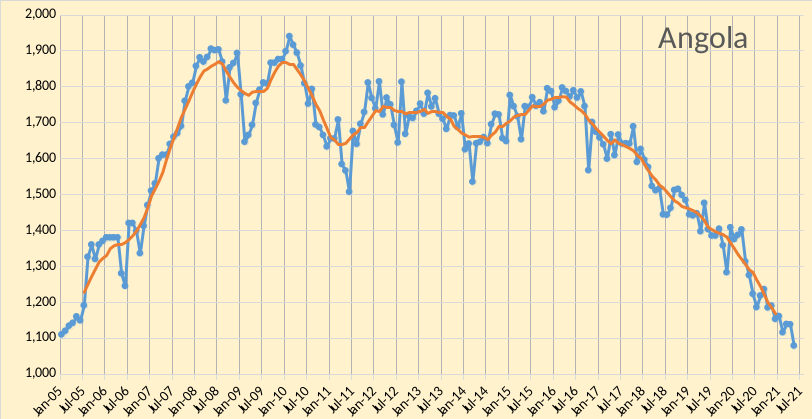

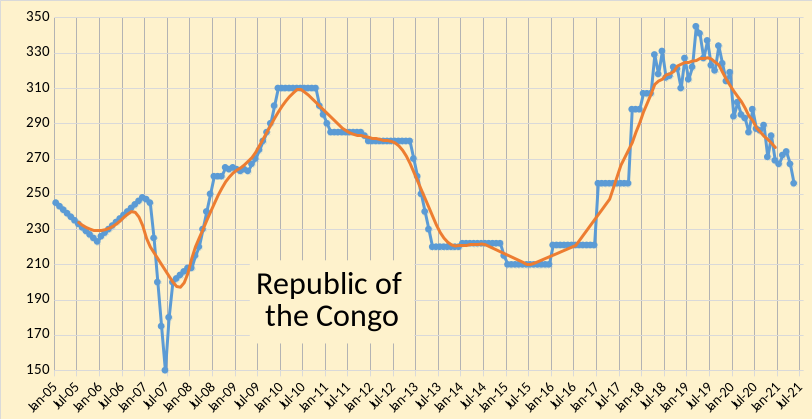

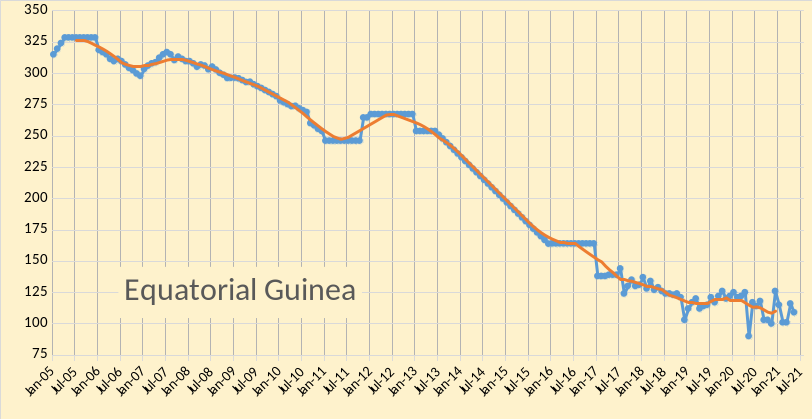

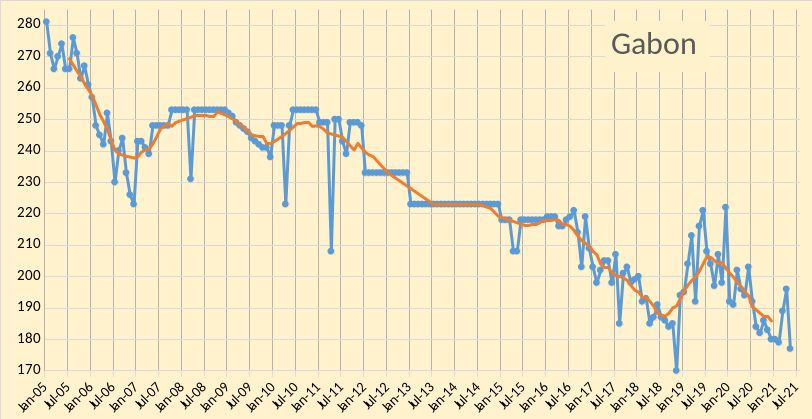

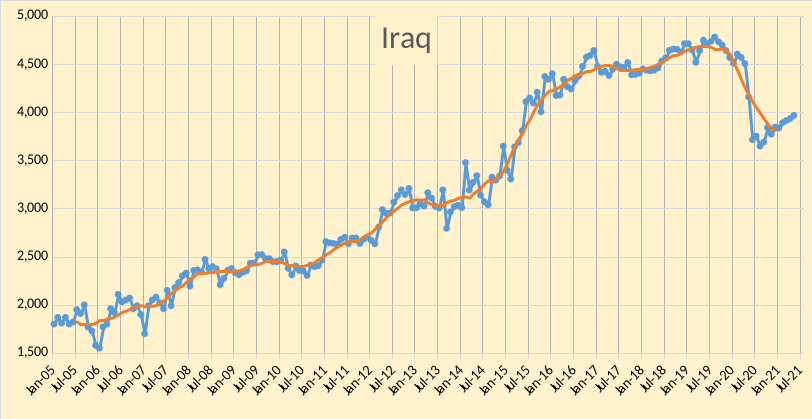

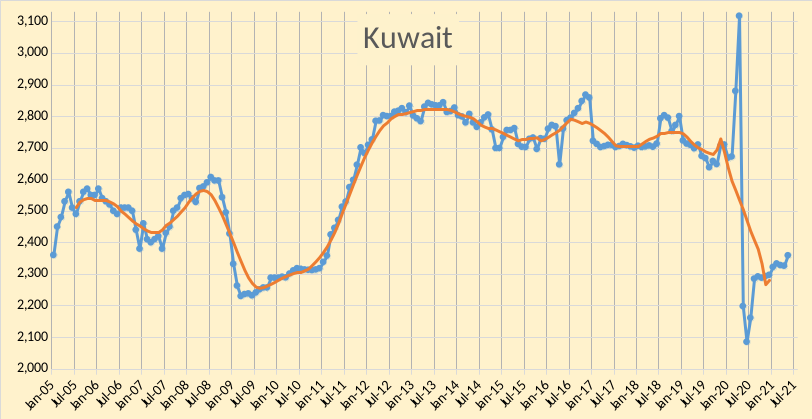

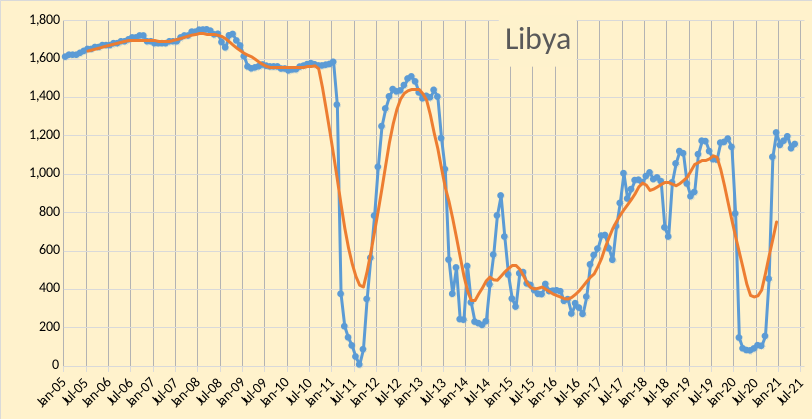

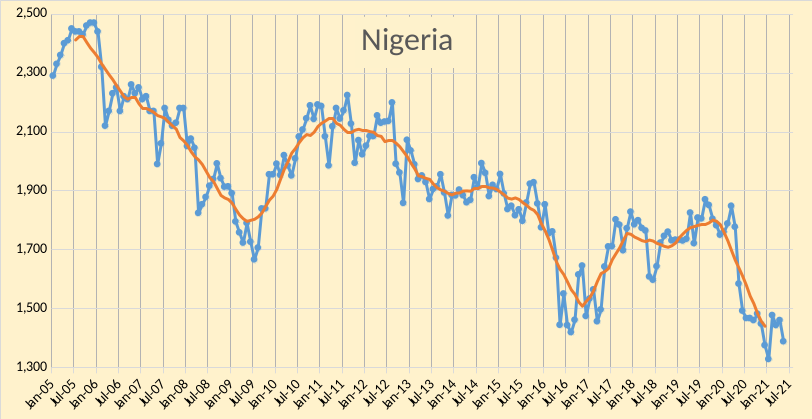

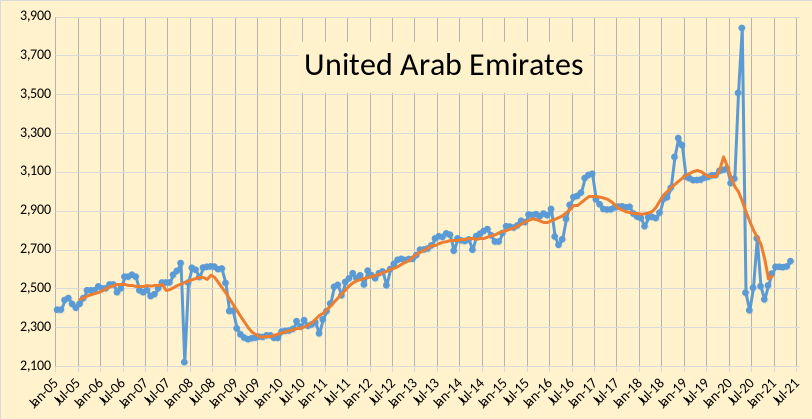

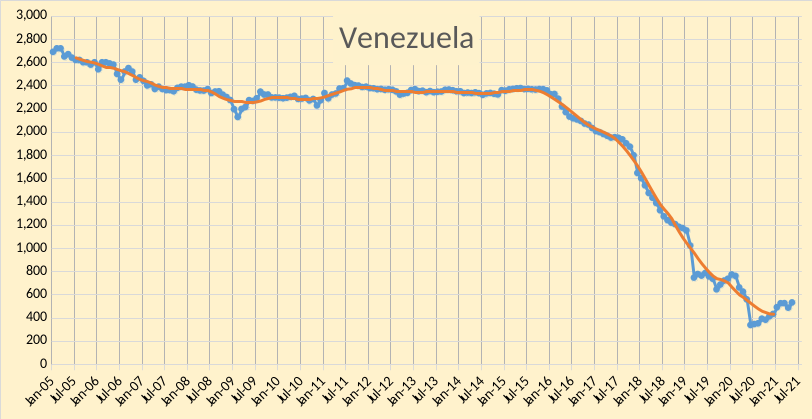

OPEC is basically 5 oil-producing nations, Iran, Iraq, Kuwait, Saudi Arabia, and the UAE. The “Other Eight” Algeria, Angola, Congo, Equatorial Guinea, Gabon, Libya, Nigeria, and Venezuela are all in decline. And that decline will continue.

I know, Venezuela’s decline is all political but that will likely last for another decade at least.

Below is a production chart of the Other Eight.

The “other 8” OPEC members in Ron’s chart above had average output fall by about 300 kbo/d each year on average from 2005 to 2020.

We can also consider the top 15 producers for World C+C from 2010 to 2019 (based on average output over those 10 years and choosing the top 15 producers from that sorted list. The 15 nations are:

Russia, Saudi Arabia, United States, China, Iran, Iraq, Canada, United Arab Emirates, Kuwait, Brazil, Mexico, Nigeria, Venezuela, Angola, and Kazakhstan.

As a group these nations produced 78% of total World output from 2010 to 2019 and 80% of World C plus C output in 2018.

When we consider a longer term from 2000 to 2019 and look at trends for the top 15 producers and the rest of the World (based on 2010-2019 average output ranking). For the top 15 output increased at 1059 kb/d on average each year over the 2000 to 2019 period or about 4.9% per year. Over the same period, rest of world (ROW) C plus C output decreased at 275 kb/d on average each year (1.6% per year). Chart below gives visual, click on chart to make it bigger.

For the chart above it appears that growth slowed in recent years (2014 to 2019)for the top 15 C plus C producers, but the decrease in the rest of the world’s(ROW) C plus C output has also slowed.

For top15 the 2014-2019 rate of increase slowed to 864 kb/d each year on average (1.3% rate of increase) and the ROW decrease was 71 kb/d annually on average over the 2014-2019 period (about 0.4%).

Chart below shows this, click on chart for larger view.

Notice that the top 15 peaked in 2018. That is even apparent in your charts Denis. OPEC peaked in 2016. Russia, which now admits they have peaked, peaked in 2018. The USA peaked in 2019, though you dispute this. But the point is, all this happened before covid started to slam production in May 2020.

Of course, most of the world was increasing production before the peak in 2018. If not then the peak would have been prior to 2018.

Ron,

Yes the peak at present is 2018. There is a good explanation for a decrease in output in 2019, there was an oil glut, OPEC cut output (as did Russia) and output decreased.

I agree that US output is unlikely to surpass the 2019 peak, but think US output can return to the 2018 average level and perhaps higher, it will depend in part on the price of oil. When it gets to $80/bo for Brent in 2021 $ or higher, we might see tight oil output take off especially in the Permian basin, other basins such as Bakken and Niobrara where the oil is expensive to transport to refineries may need $90/bo to see much increase in output, not sure about Eagle Ford, I think they will be lucky to maintain a plateau as the sweet spots may be fully drilled there and the field may continue to decline even with higher oil prices.

I doubt we will see a big increase in World output beyond the 2018 level, just a couple of million barrels per day to 85 Mb/d or so, supply is likely to be tight and prices will be high. In the past I have tended to underestimate future output, and this time is likely no different.

There have been lots of oil peaks in the past, prior to the 2018 peak, you were convinced in 2015 that we were at the peak. My guess is the final peak will be 2027/2028 with a 60% chance that the 2018 annual C plus C peak will be surpassed by the end of 2023 (we will have the data in April of 2024 to confirm).

Currently the highest centered 12 month average output is 83157 kb/d in November 2018, this number is likely to be surpassed by the end of 2023.

Dennis, you wrote: There is a good explanation for a decrease in output in 2019, there was an oil glut, OPEC cut output …

True, but OPEC produced flat out in the months of October and November of 2018, positioning themselves for 2019 quotas. And even these two months were 1.5 million barrels per day below their 2016 peak.

(as did Russia)

Nope. You better check that data again. Russia produced flat out the entire year of 2019 and did not cut output until May of 2020.

Okay, I got 2015 wrong. But that was just a wild-ass guess. It is different this time. I have analyzed things more carefully. You know Russia peaked in 2019, or you should if you believe what they said. They hope to keep production at around 11.2 million barrels per day thru 2024, but all the analysts are laughing that off. They say no way that can happen. And you seem to be coming around to the opinion that the US has peaked also. Well, congratulations. 😉 That’s two of the world’s three largest producers. That leaves Saudi Arabia, the third. Saudi is part of OPEC. OPEC obviously peaked in 2016.

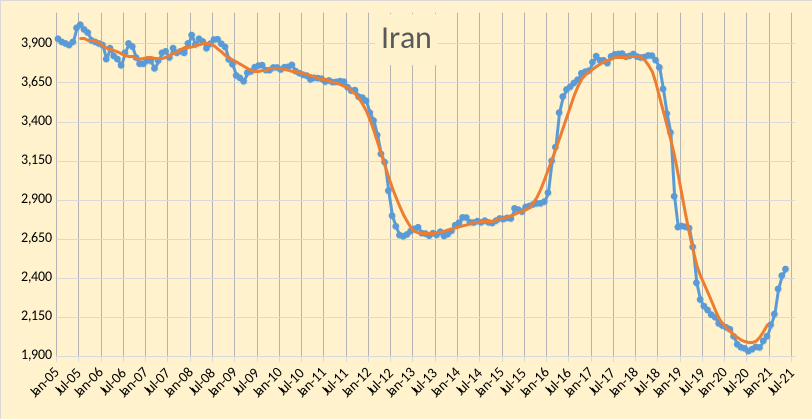

Iran says they can produce 4 million bpd if sanctions are lifted. They just may be able to do that or at least come close. However, that is only 1.5 million barrels per day above what they are producing right now. That will not be nearly enough to make up for the decline in the rest of OPEC since 2016.

But I wonder where you think all this oil will come from that will push us past the 2018 peak.

Ron,

I have answered that before. Iran, Iraq, UAE, Kuwait, Brazil, Canada, and Norway will as a group produce more than in 2018 at the previous peak, Saudi Arabia, Russia, and US only need to match their combined output in 2018, though I believe they will be able to surpass that level. It is not a lot of extra output I am proposing, only 2000 kb/d by 2028, over a 5 year period from 2023, that is 400 kb/d each year.

Also note that the top 10 producers peaked in 2019 rather than 2018 and further that US output was under 11 Mb/d in 2018, the US surpassed that even in 2020 and output will increase further in the US after 2020, though I do not think the peak of 2019 will be surpassed, I do think output will remain above the 2018 level in the US until at least 2027. Chart below shows top 10 producers from 2010 to 2019 vs rest of world. The annual increase for World C plus C output over that period was about 997 kb/d, World output will quickly bounce back to 2018 output level over the 2021 to 2023 period if oil prices continue to rise (Brent at $73/b and WTI at $71/b as I write this).

Dennis,

What if you take out US shale from your chart and plot it separately? How does the top10, shale and the rest look in that case?

I believe that your top 10 production output chart looks good because of US shale. Once you remove that, it won’t look so good. And the US shale phenomenon is in the past. They have ‘drilled the heart out of the watermelon’ at least in all other basins apart from Permian. And Permian will struggle to make up the deficit of the other shale basins. In the Permian, average productivity has been declining for a couple of years now. Tier 1 is nearly all drilled out. Productivity will decline even more going forward. So, growth is shot in US shale.

So, where is the growth coming from?

Ancientarcher,

Yes much of the growth has been from tight oil, tight oil output will continue to grow, especially in Permian basin.

Also note that average output from tight oil in 2018 (year of peak) was about 6500 kb/d. For US tight oil even a very conservative scenario (which assumes oil prices at $65/bo in 2020$ or lower for the future) has tight oil output above 6500 kb/d. See chart below with a low price, high price and “average tight oil scenario.

Of the OPEC 5 , Iraq and Iran are highly vulnerable . In Iraq the problem is electricity generation . Come summer and rioting is an yearly event as electricity is routed to the oil industry from households . Second the oil in Kirkuk is controlled by the Kurds . They do not accede to control from Baghdad . Most of this oil is smuggled and sold “off books ” to Turkey . Baghdad controls the oil from Basra and other small fields . Iranian regime survives thanks to US sanctions . Sanctions are the glue that hold the people together otherwise the current regime would have been long uprooted . Electricity shortages here are also an issue . Needless to comment that WATER is a consistent problem for not only the OPEC 5 but the whole MENA region .

I am seeking an explanation for the idea that peak oil has been/will be/could be a low price event.

Under current conditions I don’t get how this is applicable.

I understand some theoretical reasons how this scenario could be real, including

1-prolonged global economic downtown, such as we have seen recently with the pandemic or could see if global population was in decline

2-economic activity continued at a slowly growing pace, but GDP suddenly became/becomes unhinged from oil consumption despite the historic relationship

2a- replacement transport mechanism available at lower cost, such as widely deployed electrical transportation

2b- conscious effort was made globally to suddenly live life without frivolous or wasteful consumption despite ability to afford liquid fuels.

My sense is that none of these possibilities are at play in a significant way currently (unless the pandemic economic damage/demand decline persists for another 5 years).

Note that the 2a and 2b scenarios are just theoretical examples of how gdp could be decoupled from liquids (I don’t think these are currently in play, and are just served up as examples).

If you are aware of other relevant possibilities that I have failed to see, I would appreciate any help with my understanding on it..

And secondly, if you see ‘peak oil with low price’ as true and/or likely- which of the factors I listed is the predominant reason? Thanks with help on understanding this.

Pardon if I missed some previous statements on this.

Hickory, it is just not that complicated. None of the reasons you listed seem very likely to me. But there is one thing you completely overlooked. When we hit or will hit, peak oil, no one will realize that we have hit peak oil. In fact years after we hit peak oil, there will be deniers that peak oil is in the past. The obvious example of that is right here on this blog.

But, quite obviously peak oil will be a time when everyone is producing flat out. When everyone is producing flat out, it is far more likely that there will be a glut, with low prices, than a shortage with high prices. Just think about it, that is obvious.

OPEC peaked in 2016 with a secondary peak in 2017. Every OPEC nation, including Iran, was producing flat out at the time. Non-OPEC peaked in 2019 and every Non-OPEC nation, including the USA and Russia, was producing flat out at the time. The monthly peak was November 2018. All those times were a period of low prices. No one had the slightest idea that this was the peak. Well, except a few of the smarter ones of course. 🙂

Only when production is falling, years after peak oil, will it be realized that the peak has passed. And prices will then increase. Because only then will supply fail to meet demand.

Hickory and Ron. Good observations.

Predictions of the future are impossible, but these observations make sense.

I will add that since 2008 GFC, a real wildcard is governmental monetary policy. It is clear to me governments will try about anything to keep the growth ship afloat.

This will have a huge impact on oil prices going forward. Volatility will increase IMO.

But, I could be wrong, lol. The mere fact that I am still allowing my financial health to be even partially dependent on the price of crude oil should cause anyone to question my views. Lol!!

I agree, monetary policy is playing a huge role since 2008, which will impact oil from the supply and demand side.

The amount of debt in the system will have a huge impact once interest rates need to be increased due to inflation which seems like it’s already here, but the fed is claiming its transitory. Volatility will increase.

I understand your point Ron, and am in agreement.

I should have been more clear in my question-

I was not referring to the moment (or year) of peak oil in my query.

What I am wondering is if anyone sees a reason why the time after peak, (when production is starting to fall enough to be commonly realized), could or will it be a low price time for oil? I am talking about this very decade.

Regarding monetary policy, the global central bank strategy to have increasing debt and money printing sustain short term economic growth , rather than sitting back and allowing contraction, certainly has its downsides and the central bankers are more aware of this than anyone. The downsides include the penalty of slower potential future growth, the inherent instability of going faster than your vehicle is optimized for, and the need to gradually devalue/debase the currency. The upside is that the economy doesn’t contract and then contract more. The choices may be tragic either way, and they have no right answer to what ails us (growing beyond our means). But in real dollar terms the mismanagement or lack of management of money supply could affect oil price primarily on the demand side. A broken financial system could cut demand extremely hard and fast. They will keep kicking the can down the road as long as possible. And if/when they fail to kick effectively, no one will want to be a witness, since all witnesses will be victims of the situation.

As I see it.

Hickory,

Much depends on the timing of the peak and decisions by OPEC as the peak approaches. There is a possibility that OPEC might carefully adjust output to keep prices just high enough to limit demand to balance supply and in an attempt to keep oil prices in check (under $85/bo for Brent in 2021 $) so that the transition to non-oil transport does not accelerate.

Should such a scenario occur (which I think unlikely), then we might arrive at a peak/plateau at 85 Mb/d with relatively stable or slowly rising oil prices. By 2030 we might see demand start to fall at a rate that is greater than the fall in crude oil output at $80 to $90/b and oil prices might start to fall, by 2035 demand may be dropping by a much faster rate than the fall in oil supply and prices would start to fall more rapidly. This last part of the scenario seems more likely but in the interrim oil price volatility seems much more likely. Many other possible scenarios exist, but if OPEC does not make the bonehead move they made in 2015 to defend market share, I think the idea that low oil prices at the peak are more likely than low prices at the peak simply is a matter of demand relative to suppy at the time peak oil is reached. As we come closer to a geological peak in supply as is likely in the next 5 to 8 years the more likely it is that demand will be outrunning supply and oil prices would be relatively high (likely $110/bo or more in 2027 in 2021 $ for Brent crude.)

Much depends on the timing of the peak and decisions by OPEC as the peak approaches.

Surely you jest. Right now OPEC is 75% Saudi Arabia and 25% Iran, Iraq, Kuwait, and the UAE. All these countries are in denial of any approaching decline. But they all probably realize their peak was in 2016. When prices start to spike they will all produce every possible barrel.

Ron,

Up until now they have been fairly disciplined, they may indeed produce every possible barrel to keep prices in check and may also develop resources more aggressively in an attempt to keep prices at reasonable levels. By 2027 or 2028 it will be obvious that World C plus C output can no longer increase and prices may need to spike to over $120/bo to match demand with supply. This is likely to accelerate the transition to electric transport for light vehicle land transport and possibly for short haul heavy transport as well, at some point long haul transport might move to rail and rail might be electrified if oil prices remain high (Brent of $120/bo or more in 2021$).

I believe I said the scenario was not likely (which for me means less than a 25% chance). The future is difficult to predict.

What I am wondering is if anyone sees a reason why the time after peak, (when production is starting to fall enough to be commonly realized), could or will it be a low price time for oil?

A low price time for oil? Not bloody likely. No, when the world realizes that the world is running out of oil, just as the economy is booming and oil likely to be in high demand, prices will spike.

Yes. I thought some had been suggesting the opposite

Are we currently in such a situation?

No, but we are pretty close. I expect to see far more “oil scarcity” articles appearing on the mainstream news very soon. They will creep in, one by one, and by late 2022 there will be an avalanche of such articles and news reports.

It takes a while for the world to wake up from it dream state and realize just what is happening. And everyone will be saying something to the effect of: “What, what the hell is happening?”

It will be the shock heard around the world. (Notice the play on words, shock not shot. 😉 )

In fact, the first obvious excuse will be: it takes time to (re)-develop production after COVID19. Then as in 2008, production will not follow the growth of demand while at the same time production countries will continue to push for production increase. Oil price will sky rocket and economy will drop,… while oil production is still increasing from new developments. Oil price will then drop … so low price at (local) peak.

Then, the question will be: what is the wild card after? More and more production countries are already past peak. Will there be another “Shale oil” somewhere?

My gut feeling is this time is different with big/giant oil fields at their very end years of production.

Curious to know whether we are past peak or close to it. Acceleration of efforts by so many countries to organize and speed up the energy transition (including SA) should not be only for the beauty and the sustainability of our planet.

Well, the logic goes like this – the peak is caused by affordability dynamics. At high prices, demand is destroyed by economic contraction. Growth is constrained by expensive energy, and is so inelastic that meaningful reductions in consumption will collapse economies.

Chris , some answers . There are no wild cards . Even shale was not a wild card . Fracking was a tech known before the shale ballgame started . Experts like Art Berman called it a Ponzi from day one . He called it a ” retirement party ” . Peak was (is ) 2018 . There will be no more peaks . Sorry to say but energy transition is too little to late . The wolf stands outside the door or even better the title of Dimitry Orlov’s latest book ” The Arctic Fox cometh ” . Be well .

Venezuela currently has fuel shortages and the lowest gas prices in the world. My guess is that this is due to government policy. Actually there are many scenarios that would result in low oil prices post peak. One possibility is wealth inequality. Suppose the median wage falls and only the super rich can afford fuel. Well suddenly demand falls because oil is too expensive for the median salary but cheap for top wage earners. Another scenario might be a world war which kills 80% of humanity. There will be less oil but more than enough for the survivors. Another scenario is that people realize that there will be less and less oil and organize their lives to consume less. Our family has been doing this for years. I own 4 bicycles in addition to a tandem and an electric bicycle for the family. We heat with our own wood (the ashes are used to make cleaning fluid for clothes and dishes). In another two years, we hope to be self sufficient with respect to water and a significant amount of food. I see a tremendous amount of fuel waste in the economy that will soon stop.

Another scenario is that some exporting nations realize they will need this oil as the world stares into a scarcity of oil. They might say: “Shit, why are we selling this stuff when we will desperately need it for ourselves in a few years?” And as they cut back, or stop exporting altogether, the problem gets a lot worse, and prices spike even higher.

L.O.L. The decision concerning the proportion of a domestic resource that should be preserved for domestic needs, and how much to export, is interesting. China’s REE deposits come to mind. Also, the impact of the immediate use of a resource versus a lower level of exploitation over time might come into play in some (perhaps unrealistic) scenarios as well. Not many examples of countries that have exhaustible natural resources saving some for future generations I’m aware of; probably would result in an unwelcome war or another ugly result!

BBC had lately two articles about electric cars (IIRC they will take over in less than a decade) and about the future of gasoline stations (they should transfer to car charging and to whatever the e-car owners need during the wait…) so in a way something is filtering to news already although it isn’t directly about peak oil…

There was a headline this morning about GM investing $35 billion in electric cars in the next two years. Ford is also investing big, consider their decision to sell an electric F-150 their cash cow. If anyone is studying the future of petroleum products it has to be those two.

Speaking with some local contractors there seems to be quite a bit of demand for electric pickup trucks. They think that the fact that they tend to drive not very much, and always end up back at the shop and the end of the day, combined with low fuel efficiency (high cost per mile) leading to quite a bit of savings.

Because electric trucks are significantly more expensive than ICE trucks and you save money for each mile driven, it makes sense for high use cases, not low use cases. If you don’t use it much, it will just sit there and depreciate at a much higher rate. Plus you will have to change the battery after 6-7 years. The deterioration of EV batteries has a time element to it that will add to the depreciation.

Ancientarcher, the price will not be very different between EV trucks and ICE trucks.

the price will not be very different between EV trucks and ICE trucks.

Dennis, what data are you basing the above statement on? I am speaking of 18 wheelers. I don’t think any of them are around yet.

I understand they will then be called 26 wheelers. You will need an extra 8 wheels to carry the battery. 😉

Ron,

Weekendpeak spoke of electric pickup trucks used by many local contractors, ancient archer was answering that. There are no electric pickup trucks being produced yet, but the projected price will be similar to ICE pickup trucks well equipped which usually are around 45 to 50k. Heavy duty trucks will be futher into the future maybe another 3 to 3 years, electric pickup trucks are expected to roll off assembly lines by late this year (Tesla) maybe early 2022. Ford is advertising F150 EV for Spring 2022.

Frito Lays in Modesto, CA expects delivery of 15 Tesla Semis by the end of 2021.

https://insideevs.com/news/496788/FritoLay-Expects-15-Tesla-Semi-This-Year/

Frito Lays in Modesto, CA expects delivery of 15 Tesla Semis by the end of 2021.

Great, potato chips! Yeah, we should be able to make a battery with enough power to haul potato chips. The next big test, bread trucks. Bread is heavier than potato chips but, with a lot of effort, we should be able to make that hurdle in a few years. 😉

Hi Ron,

Some of the other companies that have reserved the Tesla Semi are Pepsi, Walmart, Anheuser-Busch, UPS, FEDex, DHL, there are others in the article linked below

https://www.businessinsider.com/companies-that-ordered-tesla-semi-2017-12?op=1

It is a simple answer- lack of capital investment. With the Majors having an identity crisis and the shale industry consolidating rapidly. We have already seen the best of the shale in the rear view mirror and now less productive zones and child wells will not ever bring the production to levels seen in 2018,2019 and the Permian is a pin cushion with dwindling inventory. Growth will come through horizontal combination and not through the drill bit. Internationally I also believe the lack of investment in 2020 has set the industry back 7 years at least. You can look to Iran and Iraq but the Saudis just floated a 6 billion dollar bond to finance part of their dividend payment. They are on their last leg and fading. Charts are meaningless if investment doesn’t come back and fast.

LTO survivor,

As oil prices increase so will investment, what is your expectation for peak output in the Permian basin for tight oil? My best guess is below (ERR=58 Gb).

LTO Survivor,

Do you mean lack of capex in 2020 has set the whole oil industry back by 7 years or just US shale?

I believe 2020 capex was half of 2019 capex, so there is damage for sure, but that big? Why do you think it is that big of a damage?

Thanks

Hickory, “prolonged global economic downtown” (1) seems most likely to me, i.e. more countries going the same way Lebanon is currently going:

Lebanon: Mass queues and growing frustration over fuel shortages

“Lebanon has been afflicted with a crippling fuel shortage amidst ongoing economic turmoil in the country.

According to the report, Lebanon’s GDP fell from close to $55bn in 2018 to around $33bn in 2020, causing a surge in inflation which is expected to worsen this year.”

If there was plenty of cheap oil to produce available (no peak oil in 2018), Lebanon would probably be in a much better position right now. However, I don’t think anyone is talking about peak oil in Lebanon right now. The same thing could happen globally.

Kuwait rig count continues to fall despite higher oil prices. Rig count was 14 in May, down from 19 in April.

Last year, Kuwait scrapped an awarded oil project and intended to freeze more projects.

Moreover, Kuwait will probably burn record amount of crude oil this summer:

Kuwait faces crude-for-power demand as heat rises (June 7)

“Kuwait could be set for another summer of surging crude burn in its power plants, with electricity demand already hitting a record high as temperatures soar.

Peak power demand passed 15.07GW, a new record high, yesterday when the temperature rose above 50°C, according to the ministry of electricity and water (MEW).

Its peak load reached a then-record 14.96GW in July 2020, pushing it to burn around 184,000 b/d or nearly 10 times the amount used for power in 2019.”

The economy is also in big trouble:

Kuwait facing ‘immediate crisis’ as it seeks cash to plug deficit (3 Feb)

““It’s a very immediate crisis now, not a long-term one like it was before,” said Nawaf Alabduljader, a business management professor at Kuwait University.”

Dennis,

Kuwait, SA, and UAE datasets. What is going on between jan20-Apr20, that massive spike in production? Seems to be a glitch in the data.

Iron Mike

That is when SA asked OPEC to go to maximum production in response to Russia not agreeing to help OPEC reduce production at the beginning of the CV epidemic. The question is: Was that real production or some extra crude coming out of inventory?

Thanks Ovi, was that the only OPEC countries that “maximized production” after that event?

I remember now yes. That is when prices started to collapse.

Frequently S.A. and Kuwait increase production before an OPEC meeting so that they can “decrease” to previous production levels. In 2020 this was amplified because they were playing chicken with US LTO and Russia. This was a case in which, as Ron says, they were all producing flat out into a pandemic that destroyed demand. All the players took a big financial hit and we are watching the fallout with great interest.

Libya’s Oil Production Drops By 200,000 Bpd (Jun 09)

“Libya’s crude oil production has declined by more than 200,000 barrels per day (bpd) in recent days, or by almost 20 percent, on the back of pipeline leaks and maintenance at the biggest oilfield, Bloomberg reported on Wednesday, quoting sources familiar with the situation.”

The shale exit continues.

https://mobile.reuters.com/article/amp/idUSKCN2DP0K5?__twitter_impression=true

Exxon (XOM) Sees US Shale Oil Production Decline Per Well Bold mine.

Exxon Mobil Corporation XOM has been generating fewer barrels of oil from the prolific shale fields of the United States since 2019, per Reuters.

According to a latest report, the company’s oil wells, which are involved in some of the most promising shale fields, produced fewer barrels of oil per well despite an increase in overall expenditure and production.

In 2017, Exxon, which is one of the largest shale oil producers, acquired $6.6 billion of net acres in New Mexico, which doubled the company’s assets in the Permian basin that spans west Texas and New Mexico. Notably, the company intends to boost shale output in the New Mexico portion of the Permian basin to 700,000 barrels per day (bpd) by 2025.

Per data released by the Institute for Energy Economics and Financial Analysis (“IEEFA”), Exxon’s average liquid output for the first 12 months of a well dropped to 521 bpd in 2019 from an average of 635 bpd in 2018 in its Delaware basin assets of New Mexico.

That’s an 18% drop in production per well. And this was before the pandemic

Looks like they bought trash in Delaware then. Like a rigged gold mine in the 19th century, with nuggets inserted with a shotgun to fool investors.

At shaleprofile most basins are still at peak productivity – not getting better anymore, but not declining, too. At least not by much – 18% is huge. With this decline they can write off these acres soon.

Great work and good timing as seen by the comments so far . Hope the world starts to smell the coffee .Tks Dennis .

The IEA called for OPEC+ to stop investing in oil and gas and now tells OPEC+ to produce more oil and gas????

Oil Markets Baffled As The IEA Calls For More Production

In its latest Monthly Oil Report, the IEA called on OPEC+ to increase production in order to counter higher demand in 2022.

The agency claimed that, based on current global economic growth expectations, demand for crude oil and petroleum products will be reaching pre-COVID levels by 2022. The Paris-based energy watchdog, which has come under fire after its shocking Net-Zero by 2050 report called for no more investments in oil and gas, stated that “OPEC+ needs to open the taps to keep the world oil markets adequately supplied”. At the same time, the IEA has also reiterated that market realities are at odds with its proposed strategies to reach net zero-emission levels by 2050. Criticism will likely be harsh for the “former” leading oil and gas agency, as the agency has called upon the world to double down on renewables and commit to the Paris Agreement while admitting that the global economy continues to demand vast amounts of hydrocarbons.

The relevance of some of these reports will have to be reassessed, especially when looking at the high-profile “Golden Age of Gas” report and the “Net Zero by 2050” roadmap. When asked what needs to be done, the IEA indicated that the call on OPEC+ will be very strong, as the international oil and gas producers group will need to increase crude oil supply to the market by 1.4 million bpd in 2022. Which would mean a significant increase over its current July 2021-March 2022 targets.

They are clearly playing both sides of the fence since they probably receive funding from oil and gas as well as governments and “green” industries who have “committed” to net zero emissions.

IEA is the epitome of a confused mouthpiece.

The IEA has recently stated two positions, and contrary to many headline soundbites the statements are not in conflict with each other.

The first was the report on 2050 net carbon zero pathway that said if the global goal is net carbon zero then the major producing companies/countries must stop exploring and producing in new basins [if net carbon zero by 2050 is the goal]. That will be decided by others. Or should I say that decision will be largely avoided by others.

The second statement was relating to short term oil supply demand balance as Ron referenced.

Surely we are able to make the simple distinction.

Here is the net carbon zero report press release- https://www.iea.org/news/pathway-to-critical-and-formidable-goal-of-net-zero-emissions-by-2050-is-narrow-but-brings-huge-benefits

IEA going to one extreme to another is the headline news, yes. Too small investments (2017), demand falling of a cliff or too little oil again. The spin goes in all directions.

I think it is not very easy to keep oil prices low (from 2015 to now there have been several downside “chocks”). The middle east reduced drilling as soon as the democrats in US won the election. Major oil producers are ok with reducing production if prices are going higher. I do think it is very difficult to pursue a policy where reduced energy per capita is offered. So the way I see it, is that electric energy based on wind and solar has to balance reduced fossil energy. Electric transportation and heat pumps being the low hanging fruit. It can prolong energy scarcity problems in developed nations for many years, and therefore I think that is likely. The easy going higher energy/capita era, will be replaced with a more complacent energy stagnation/capita era for a while. And not without conflicts, since there are going to be winners and losers. Not just winners (broadly speaking) like the last 40-50 year period.

Could shallow sand or possibly Mike comment on this?

https://twitter.com/sand_frac/status/1404476730266447872?s=19

The EIA’s Drilling Productivity Report came out today. Everything looks pretty flat in the shale patch. Below is the total of all seven basins. The last three months of this chart, May, June, and July are just estimates. But they are likely pretty close, especially for May. And I think this is total production from these basins as it is slightly higher than the Light Tight Oil report that comes out later.

Except for the bad weather month of February, production has been virtually flat for a year now.

Total DUCs in shale basins are falling at the rate of about 250 per month. I don’t know how long this can continue. I have been told by some experts in the field that there are some DUCs that will never be completed because they would not produce enough oil to pay the completion cost. So we just cannot count the DUCs and divide by 250. The decline in DUCs will have to stop sooner or later.

What I don’t understand is why wells are drilled but not completed right away?

Frugal, I am not an oilman, and an oilman could obviously give a better answer than I. But I will give it a shot, and hopefully, I will be corrected for any mistakes I make.

Drillers are not frackers and frackers are not drillers. That is an entirely different operation requiring different crews, different equipment, and different CAPEX. But the driller leaves behind samples from the well, indicating just how productive the well should be. The best wells will obviously be fracked first. The less promising wells will be left for times when the price is high enough to justify the fracking cost.

But…. the total cost of the well is the drilling cost plus the fracking cost. And in a DUC, the drilling cost has already been spent. So when times get hard, and you can get a well, though it might not be the best well, you have already paid the drilling cost, so you can get it for only the fracking cost now. So you pay the fracking cost and recover what you can. And this would be the case especially if the new wells that are coming in are less promising than the poor wells already drilled.

But then, that’s just my opinion, for what it’s worth.

Yes this makes seance — the productivity of a well being somewhat unknown until you get your hands on the core samples. You have to drill to know what’s down there.

There has to be a certain delay just from a logistcs perspective, I think from some reports this is around three to six months but do not have first hand knowledge. This allows the drilling program and the completion program to be planned separately so that the do not interfere with each other. With most of the wells being drilled from pads around 8 to 10 would be drilled before the rig moves off and the completion crews move in. In that period things may change. On the commercial side prices may fall, companies go bust, liquidity dry up, transport or marketing deals change (e.g. so that gas capacity becomes limited), cracking crews become unavailable because of problems with the service company etc. The drill cores from pad may show some wells to be marginal or less attractive than originally expected or while the pad is being completed the rilling results on the next pad show it to be much more commercially beneficial to be completed immediately or a well may be found to be problematic and need special completion methods. Weather or unplanned maintenance delays may also play a part.

If one or more well is left incomplete on a pad, for any reason, it would become difficult and more costly to schedule the completion crews to return later (which may interrupt their planned programs and require loss of production from some of the other operating wells on the pad) and a decision to do so requires a new economic assessment, with the original return on investment expectations and sunk cost for the previous drilling now irrelevant. Once this new assessment is made there may be newer data available for expected recvory or initial flow etc. as well as a new price scenario to be factored in and a different appetite for risk in the E&P (none of the calculations are exact they are all based on on assessment of prababilities for best, median, worst scenarios)..

Ron, thanks for this.

Few are aware that the decline in the US LTO extraction in recent months has been slowed by

1) Drawdown of the DUC inventories (less CAPEX to bring in new wells).

2) Reducing the number of wells classified as inactive (does not take much $$$.)

All it takes is a look at the hard data, narratives, and wishful thinking never beats hard data:

Anyone doubting should look at the relationship between the number of fracking spreads and drilling rigs. For some time, the capacity from the fracking spreads has been running ahead of the requirements dictated by the number of (active) drilling rigs.

There will always be some cushion in the DUC numbers due to logistical reasons. We know little about the quality of the DUCs and how many of these are “dead “DUkCs.”

The above factors make it challenging to make reasonable forecasts on the future developments (like the next 9 – 12 months) in total US LTO extraction.

I know because I have been there for years, looking both at the Bakken and the Permian [tons of this information has not been made available in the public domain, but shared, discussed with insiders willing and able to pay] and all of this has been juxtaposed versus data from SEC filings for public companies.

Anyone who wants to know who “LTO Survivor” is, I could narrow it down to 3 names!

The near-term [6 – 9 months] trend in US LTO extraction will be downward as most companies now are CAPEX constrained (they recognize this.)

IMO, the best indicator for US LTO extractions’ future direction comes from studying the CAPEX budgets for public companies from their most recent SEC filings.

Looking at the trends, the first 12 months cumulative for younger LTO wells (Bakken may have “peaked” in 2018, referring to productivity or EUR) has been on an upward trajectory, but looking at the relative decline rates [from actual data] for these now supports the impression that longer laterals, more proppants loadings, and more fracking stages has helped pull extraction forward in time [which is good from a Net Present Value Perspective, NPV] and how this affects the EUR remains to be seen.

I am in the process of completing what in my world is referred to as a “post-project audit” for the Permian, which follows the template as my most recent post for the Bakken [looking at the Permian as one big project, and if anyone thought Bakken was bad…], but with data for the Permian.)

Initially, my Permian post was scheduled for publishing in late 2019, but I have been bogged down by many other commitments like the chairman of some boards.

I recently [as in for some years] have focused on oil price developments by looking at things like the credit impulse, the exchange rate of the USD [versus other currencies, and the most recent data {May-21} would surprise or shock most people], movements in the US 10 YT rates, fiscal and monetary policies, consumers affordability and many other parameters/metrics. This will give some clues about the oil companies’ willingness to invest in future oil capacities (NOTE I did not say growth in oil extraction!)

Much of this work has happened under the radar screens and little of it has been published.

All of these say now there will come a decline in the oil price [in USD] (it is easy to understand the reasons for the direction [of the oil price] but very hard to predict the timing.

I now expect the [present] oil price to come down later this year (2021). It is oversold!

As many more brilliant people than me put it, “if you get the USD right, you get a lot of other things right,” like the oil price as the oil is still [this could change!] priced in USD.”

Just my 2 cents in a hurry, and again Ron, thanks, and my money is on you [wrt timing the global peak, some of your opponents have not studied the hard data, and hard data still trumps everything else!]

Thanks Rune . Enlightening post . Await your research on the various subjects you are working on . Rgds .

I echo H in H

Rune

I have been tracking Frac spread crews with oil rigs and since September there have been 0.7 frac spreads added for each oil drill rig. This may not be a fair comparison because the Frac spreads may also contain NG wells. Regardless it seems that the addition of Frac spreads is lagging rigs. What is even more puzzling is that frac crews are fracking DUCs which I thought would have resulted in a higher ratio.

Ovi, the amount of time it takes to drill a well is not necessarily the same amount of time it takes to frack a well. I don’t know what the average time for each is, an oilman will have to tell you that, but there would likely never be a one-to-one ratio. So there would be no need for the number of crews to match.

Second point. You said: What is even more puzzling is that frac crews are fracking DUCs which I thought would have resulted in a higher ratio.

Ovi, a DUC is the only thing a fracking crew can frac.

Ron

Agreed. My point was fracking DUCs adds fracas and no rigs so that would make the ratio higher.

Ovi, see my post below. I put it down there to get more width for the chart. It’s all about capex.

Ovi,

Look at the other section of your chart where at 225 frac spreads there were almost 600 rigs, compared to about 360 rigs currently. The fact that there are nearly half as many rigs running for the same number of frac spreads suggests more DUCs are being completed. Basically we expect the ratio of frack spreads to rigs to decrease when a higher proportion of DUCs are being completed.

It will be interesting to see if rig and frack counts accelerate with higher oil prices.

Dennis

“Basically we expect the ratio of frack spreads to rigs to decrease when a higher proportion of DUCs are being completed.”

I see it the other way. If frac new crews need to be assembled to frac DUCS and no rigs are being added, the frac spread to rig ratio would be increasing..

Ovi,

Let’s take a couple of data points from

https://www.aogr.com/web-exclusives/us-rig-count/2020

and

https://www.aogr.com/web-exclusives/us-frac-spread-count/2021

March 13, 2020 frac spreads=298, oil drilling rigs=683, frac spread to oil rigs ratio=0.44

June 11, 2021 frac spreads=230, oil drilling rigs=365, frac spread to oil rig ratio=0.63.

Since the middle of 2020 DUC count has been decreasing. Basically fewer drilling rigs are needed when frac spreads are busy bringing the DUC inventory to a lower level.

Dennis,

Why is this happening now? Why did it not happen three years ago? I know, we had a pandemic, but why did this make companies to suddenly decrease their DUC inventory? That is, why are they drilling so many fewer wells than they are completing?

Ron,

Prices during 2020 (April to December) were very low, much lower than in 2018, that is a part of the explanation, also investor sentiment has changed and they are demanding a return on investment.

Ron,

In addition we had a very big drop in demand for oil that was very sudden, this left a lot of DUC inventory ready for fracking so drilling slowed down while DUCs were completed to bring down excess DUC inventory, at some point drilling levels will increase as DUC levels fall to levels companies are more comfortable with, we may be close to that level soon (within 3 to 6 months is my guess).

Ovi,

Yes you are correct, as a higher proportion of DUCS are completed (so that DUC inventory is decreasing) the ratio of frac spreads to oil rigs will increase as it has from March 2020 when the ratio was about 0.4 to June 2021 when the ratio has increased to 0.7 or so.

Ovi,

Let me share some numbers based on data from Shaleprofile (numbers could be subject to future revisions) that covers the big 4: Bakken, Eagle Ford, Niobrara, and Permian.

Until Apr-20, there was a general build of DUCs in these 4.

As from May-20, a significant drawdown in DUCs started (this as the oil price collapsed and completing DUCs would allow more wells to be brought to flow as the lower oil price constrained access to CAPEX.) For the Bakken and the Permian, cash flow from operations (CFO) was still negative. These operations (drawing down DUC inventory [each DUC is about $3-4M yielding nothing]) allowed to slow down the decline in LTO extraction.

For the period May-20 – Jan-21, 3 100 additional wells were brought to flow for the big 4.

About 47% of these came from the drawdown of the DUC inventory.

ON DEVELOPMENTS IN THE FINANCIAL WORLD

I do not think I have publicly used the term “financial crisis,” though I expect developments in the financial world to affect the oil market and the oil price. Not using the word “financial crisis” does not mean that there is no tail risk (low probability) of this happening.

Then again, what is the definition of a “financial crisis”?

The financial world is opaque, ref the Eurodollar system, which is out of the jurisdiction of the Federal Reserve.

Apart from that, some crucial indicators may give away trend directions 6 – 9 months into the future. One example is the credit impulse for China which recently turned negative, signaling an economic slowdown, and as China slows, many more follows.

The yield on the US 10 YT, which recently has come down. In other words, the bond market does not foresee much economic growth and the current US inflation (about 5% YoY) to last.

Mar-20 – Jun (4th)-21, the correlation between the US 10 YT and the oil price (Brent spot) was 0,84, which is substantial.

Jan-21 (1st)- Jun (4th)-21, the correlation between the US 10 YT and the oil price (Brent spot) was 0,86, which is substantial.

A rising US 10 YT signal more robust growth and higher inflation and vice versa, spilling into the oil market.

Relations change over time, but a test going back to 2017 found a strong correlation of 0,79 between the US 10 YT and the oil price from then to now.

It now appears the Fed policies are aimed at deleveraging US public debt by accepting higher inflation.

A negative real interest rate is one way to get there, and the more negative, the better,

which is a subtle form of default like negative bond yields

THE OIL PRICE

A lasting structural imbalance where demand runs ahead of supplies gives support for growth in the oil price.

The market now expects economic activity to pick up from the easing of Covid restrictions.

Now and from my perspectives, there are/will soon be several headwinds for continued growth in the oil price;

– Cutbacks in the US stimulus packages

– Likely an end to the mortgage forbearance

– Likely an end of the rent moratorium

– Slow/no real wage growth for employees

– Slow credit growth

– Consumer spending sentiment souring

– Lower yields

– The global credit impulse (ref China above)

– OPEC in the process of adding some 2 Mbo/d to supplies

– and many, many more

Recently I have not dived into the data to look at speculative momentums for oil.

Technical Analysis using tradingview or similar has some merit, reflecting some collective expectations or behavioral economics.

I still expect to see “poor” consumers start to reject a sustained higher oil price (around $70/Bo) by reducing demand.

Since 2019 about $70/Bo (Brent spot and nominal) appears to be a threshold where consumers with the least affordability start making cuts in their demand.

Could the oil price go above $100/Bo (in nominal terms)?

IMO yes, and that is related to developments in the exchange rate of the USD. Which again becomes derived from US fiscal and monetary policies.

Some analysts expect the USD to lose 30 – 40% of its purchasing power 2 to 5 years from now.

Anyone who understands the implications of such a “devaluation” to the USD would not like to go there, especially those living on a fixed income.

Lower US treasury yields equal tight monetary conditions. Interest rates aren’t low enough to pull economy forward anymore. Credit is where you need to look at to determine which way dollar is going and ultimately the direction of everything else. Corporate USA has 11.5 trillion dollar of credit extended to them. In order for this credit not to contract there has to be ever increasing loans and ever decreasing interest rates. The likely hood of a major dollar spike is greater than a collapse in value of the dollar IMO. It is just a matter of timing it.

Credit contracts when loans are paid off btw. Not just when loans are defaulted on.

Eurodollar market is likely twice as big as onshore dollar market and FED has zero control over it. Dollar shortage can show up outside USA in a hurry and totally screw up any theory on why oil prices or the price of anything else should go higher. And remember while banks outside USA can loan US dollars. They can’t print them to make people whole when a dollar shortage shows up.

The spike in usage of reverse REPO at the FED should be very alarming to everyone. Banks have plenty of bank reserves but not enough collateral. Collateral is pretty important when you have to borrow on a daily basis as banks do. Without enough collateral Eurodollar market doesn’t get enough dollars to function properly. You get a dollar shortage cause by FED’s QE taking too much collateral out of market.

The FED is between a rock and a hard place.

They have to control the yield curve, as you stated – companies can’t pay hight interrest rate anymore. In the current enviroment with starting inflation higher than 5% and increase in minimal wage on the table, nobody would lend money to a company under 7% for a few years -15-20% for junk ratings. At least in normal times.

And this would cause a bloodbath in the economy, and states, too. That’s why the collateral problem and the reverse repo problem is the smaller evil at the moment.

A comment posted on ” The Automatic Earth ” . Self explanatory .

“Dr D: ““Stocks fall on Powell threat to (maybe) raise rates a tiny bit TWO YEARS from now …”

I saw that yesterday and had to read the sentence a few times, think about what year we are currently in (2021), convince myself the year 2023 wasn’t a typo, then reread how little the rate would be raised … ??

Alice, my dear, we ain’t in wonderland anymore.

The stock market moves when Powell passes gas, doesn’t really mean much. 🙂

The real question is just how steep is Seneca’s cliff. Drilling these past 2 years have been way down everywhere.

That includes SA, Kuwait, and the rest of OPEC. Output in places like Angola, Algeria and Nigeria is not coming

back without a lot of investment. By who? Not the majors. Shell will not drill in Texas, much less Nigeria.

US tight oil appears flat for now, but the last few months have been estimates by the EIA. So far drilling has

been slow to recover even with substantially higher prices. Canada can grow some, but not a lot until there

are more pipes or prices high enough to pay for rail. Russia? The North Sea? Alaska? Kazakstan? None

of it looks to even get back to 2019, much less grow. Ron is right, 2018 was it. But how steep the

slide is now the question. Do we see $100 next year? $150?? Even so, and if drilling picks up, you can’t get a child

in less than 9 months even if you get a dozen girls pregnant. Except for shale, that 9 months is more like 5 years. look

at Guyana. Just an opinion.

Pilot,

Consider Rune’s post above where he expects oil prices will fall in the near future and your opinion that we will see a Seneca cliff in oil output.

The only way that both of these scenarios could be appropriate for World output is a severe Worldwide economic depression.

Is that your expectation? My guess is the odds are less than 1 in 25 that expectation would be correct over the next 10 years.

Perhaps when peak oil actually arrives and we see World output falling by 2% per year or more with high oil prices (over $100/bo in 2020$) due to lack of oil supply (circa 2030-2031) we might see a severe World Depression (Great Depression 2). Much depends on the speed of the transition to alternatives to liquid fossil fuel for transport, a slower transition makes the prospect of an economic depression far more likely.

Dennis- “and we see World output falling by 2% per year or more with high oil prices (over $100/bo in 2020$) due to lack of oil supply (circa 2030-2031)”

I put more chips on the high price scenario where that time frame (2030) is moved forward about 5 years due to sub-optimal human management of economy and politics (rather than geologic/technical constraints). Take your pick- resurgent nationalism in places like USA, war in the middle east, china asserting its muscle in its front yard (south china sea), Russia moving to assert re-control over its neighborhood, breakdown of civil society due to rising food prices or military coups, for example.

Of course, these kind of factors have huge uncertainty and don’t mix well with models.

When it comes to oil, some countries are much more vulnerable to price rise/supply disruption than others. For example, in this decade Russia, Canada and the USA are in a far different category than China, India, Japan, Korea, and most countries in Europe. The second group are examples where the pain could come fast and hard. It won’t be a quiet world if affordability or supply shifts unfavorably.

Hickory,

It is possible it will be 2035 or so, but my guess is that the transition to electric transport will be far enough along in 2035 that demand will fall below supply and we will see falling oil prices by that point in time. A slow transition to EVs due to supply contraints on batteries or other material shortages leading to high prices for EVs would be consistent with your scenario, 15 years is a long time so predicting that far forward is likely to lead to poor predictions (same can be said for 5 or 10 years, but bigger time spans will lead to much poorer accuracy).

In the past I have tended to underestimate the growth of oil output, projections have tended to be on the conservative side.

See

https://peakoilbarrel.com/2017/03/

for my expectation for tight oil in 2017 and note that most did not predict the pandemic of 2019-2021 in 2017, chart below is from that old post.

Pilot,

Fair point!

The big problem that I see is the lack of capex. There has been a lack of discoveries since 2005 and that will add on to it, but the big problem now is the inability/unwillingness of companies to spend capex on oil developments. This is partly because of the ECG and climate change narrative and partly because of weak balance sheets of o&g companies.

2020 O&G capex was a sharp drop over 2019 and 2021 is not much better, in fact it’s looking worse than last year. This will all come back to bite us all and not just the virtue signalling idiots pushing the climate change narrative.

I don’t agree with Rune that oil prices are going to decline. I don’t see demand declining for the next 5-7 years at the least and I don’t see supply keeping up. How can we have a low oil price in that scenario??

“The big problem that I see is the lack of capex. ”

With the prices levels for oil of the past 5 years (mostly between $45-75/barrel) , just what projects or type of projects are starved of capex currently?

Apparently most of the eager money has gone to LTO production, yet

“Despite rising production over the past decade, free cash flow per barrel of oil equivalent produced has been negative. Exhibit 1 plots production alongside free cash flow for a sample of 36 leading independents that we studied across unconventional basins.”, according to analysis by Mckinsey as of 2019.

https://www.mckinsey.com/industries/oil-and-gas/our-insights/paths-to-profitability-in-us-unconventionals

And if the LTO industry has not been rewarding capex, then what are the other projects that would?

It looks to me that prices will have to get higher and be sustained for quite a while to really get capex flowing strongly.

Ancient Archer,

I agree oil prices are likely to rise. If that is correct we are likely to see increased CAPEX in the oil industry which will tend to boost supply relative to a lower level of CAPEX. My expectation is that prices will rise to a level where supply increases and demand decreases to the point of market balance. The oil price where this occurs is anyone’s guess, my guess for 2023 is $90 to $100/bo for Brent in 2021 US$ in order to balance the market, but it might be anywhere from $80 to $120, very difficult to predict ad there are many potential wildcards.

Dennis,

The only issue here is lead time.

As Pilot said above, it takes 9 months to get a child. You can’t process this thing in parallel. Getting 9 women pregnant won’t get you a child in 1 month.

Same goes for capex. There is a lag of around 4-5 years (I think) before higher capex has an effect on oil production. If oil goes to $120 tomorrow and everyone and their aunts wants to invests in capex, it will still take a long time for the high capex level to make an impact. Higher production won’t tomorrow just because you invested an insanely amount of capex now. You have to wait. And in the meantime, depletion won’t be sleeping.

Then we come to the 2nd point – about the lack of discoveries in the last 15 years. So, it’s not that if you want to invest capex, you will be able to. There are very few new conventional discoveries in which to put the money to use.

And lastly, all this has come to pass because of a lack of capex since 2015. Most of the capex in O&G after 2014/15 has been in shale and has been pissed away. US shale production from wells drilled prior to 2020, declined by 2mmbpd in 2020. The capex that was invested in shale is not equal to the capex invested in deep water when looking at long term production.

So, you have a situation where the industry has been starved of capex for the last 7 years and they are still cutting capex. The oil price has been low for the last 7 years primarily due to (a) the long lead time nature of capex – capex cuts also took 5-6 years to affect production, and (b) fast flowing shale – but that growth is now history.

Your idea of high oil prices immediately impacting supply is bonkers. If you incorporate a 4yr wait from capex to production, how does it impact the demand and supply situation?

Ancient archer,

Not all capex takes 4 years to impact output, in some cases it is as little as 6 to 9 months, it depends on the project. Onshore infill drilling will have a pretty quick impact, also expansion of already developed oil sands projects might impact output pretty quickly once FID is made.

Arctic and deepwater offshore clearly take longer especially for a new project, but even in those places expansion of existing facilities will have shorter lead times than a new field development.

Can someone explain to me how oil prices will decline when supply will not keep up with demand in the future?

Johnny,

Rune may foresee a financial crisis in the near future, I don’t see it, but I have missed these in the past and future crises I am unlikely to predict, Rune studies financial markets more closely than me and probably knows more.

I don’t think it is possible to predict the timing of financial crises, if I could I might be a very wealthy man, alas I am not.

If the forecasts of major agencies (OPEC, IMF, World Bank, etc) are close to being correct, I expect real oil prices (in constant dollars at market exchange rates) will rise over the next 2 years, likely reaching $90/bo for Brent in 2021 US$ by the end of 2022 for economic growth rates forecast by the IMF in April 2021.

We are in for an uncomfortable number of years. Here I am in Texas and being told by ERCOT that we have to raise our thermostats, not wash clothes, power down electronics because (now at the beginning of summer) we can expect rolling blackouts. How can that be? It is always hot in Texas in the summer. The electric grid which requires a certain amount of green energy cannot handle the load. Now imagine about 5 million new EVs in Texas. This country is so woefully inadequate and unprepared for to the infrastructure needed to supply electricity needed in coming years and it will take a long time.

As I read this blog and I see the discussions, all I can share is what I have experienced. When we started drilling in 2014 we had over 1200 locations in the Permian Basin . Today in 2021 we have drilled over 130 wells and we have approximately 300 safe drilling locations remaining. In other words we have roughly 1/4 of the locations we had originally expected. So when I see the lack of CAPEX, the rate of consolidation, and the fewer number of quality drilling locations remaining, I look at the charts that predict significant production increases in the Permian through 2030 and I say no way! We will be lucky to be where we are today production wise in 2030 even if the the price was $500 per barrel. Locations are not infinite for $9 million dollar wells. With. $100 oil, I could expect spacing could narrow and we could add another 20% to the drilling inventory (max). Again it is simple. Follow the money. Companies are not putting out more drilling rigs and instead they are buying other companies because the producers know that inventory is dwindling and the best way to outsmart the neophyte analysts on Wall Street is to divert their attention to a new activity which is M & A. However if you look closely at all of the small public’s PUDs and Possible you would realize that we are closer to the end than the beginning.

The world has enjoyed cheap energy and this era is over until we discover new forms of cheap and abundant energy with or without a climate change concern.

Its Texas——

Good luck!

In the half century I’ve been an oil and gas operator, with a check book, I’ve learned two things I could always hang my hard hat on. One, never try and predict the price of oil, make financial decisions on reality, not hope, and…Two, never bother trying to explain well economics, or how the the oil and gas business works in reality, with people that have never owned working interest. It can’t be done. Most of the charts and wild ass predictions being made here are being done by people who have never seen a drilling rig.

The ultimate proof in your beliefs, your opinions, your analyses, is to put your money where your mouth is, then reap the rewards or suffer the consequences. Not many google minded analysts have the cajones to do that.

$70 WTI will not help the US shale oil space, nor will $80, even $90. You’ll get that soon enough, even those of you who don’t care whether the public or private shale oil industry pays back the nearly $300B of long term debt it has…that is still growing, by the way. The idea that the Permian is going to be able to pay back over $100B of debt between now and 2025, and still grow production levels, is ludicrous. YOY base decline rates in the Permian alone are 2 MM BOPD.

The rest of oil producing world has been set back on its heels the past decade. Low, volatile oil prices have disrupted the entire world oil order; capital to replace falling PDP reserves has been wacked and no noteworthy discoveries have been made worldwide other than Eastern South America. $70 oil will help the rest of the world much faster than US shale oil, but even that is going to take years.

So, hold on to your knickers, the price of oil is, near long term, going thru the roof. As the world suffers thru the economic ramifications of higher oil prices remember who the culprit is behind all this shit. Its US shale oil. US shale oil put 4.8MM BOPD of leveraged LTO on a balanced world oil market and in 2015 the price collapsed accordingly. Since then US shale oil has KEPT prices low and volatile, in spite of OPEC’s best efforts, and sucked capital necessary to arrest decline and replace PDP… from the entire rest of the world.

I said six years ago the US shale oil phenomena was going to prove harmful to the world’s oil future and here we go.

https://www.oilystuffblog.com/forum/forum-stuff/snakey

Mike, from your link:

I mean, think about it…why on earth would we want to be using cheap OPEC and Russian oil when the good ‘ol US of A can borrow money to drill unprofitable shale oil, flare its gas, deplete groundwater resources to frac it with…all so we can export the last of our natural resources to other countries, now?

Damn good question. Anyone got an answer?

Capital that needs a home, combined with good PR.

We built a water recycling facility. I truly can’t understand why the states don’t mandate a certain percentage of frac water be from a recycling source. It is a travesty and wasteful. Of course it raises the cost of Drilling amd Completions but not that much and should be required by all LTO E&P companies.

Good post Mike.

Thank you, LTO. Everything you say about the HZ tight oil space in the Permian, its declining well productivity, pressure depletion, remaining “drillable” locations, etc. is very much worth paying attention to and learning from, not arguing about.

Hi Mike,

I have run the numbers for the Permian basin based on shaleprofile output data for oil and natural gas for average 2019 wells, I assume productivity declines going forward and use the medium TRR estimate from USGS as a baseline, a wellhead price of $70/b and NG prices at $1.75/MCF at wellhead and NGL sold at 25% of wellhead crude price, well cost assumed to be $10 million, royalty and taxes at 28.5%, operating costs about $13/bo. Well payout is at about 30 months and the net present value of future net revenue over the life of a new well using a nominal annual discount rate of 30% is about $10 million. The Permian tight oil debt is paid back under most reasonable scenarios by 2025 or so.

Johnny —

In a free market economy, prices are set by marginal costs. That is the theory anyway. The idea is that competition drives prices towards marginal costs, and damn the torpedoes. If I can sell cheaper than the competition and still make a buck, who is there to care about tomorrow?

Oil prices tend to be driven by the futures market, which is based on changes in stored quantities, horoscopes, herd instincts and whatever scare story happens to be in the papers today. This is probably only possible because oil is very cheap in practical terms. By that I mean oil is too cheap to encourage conservation. So the price wanders around in the wide margin suppliers really need and consumers can really afford. The fact that there isn’t any handy replacement for storing energy in a moving vehicle helps.

But futures markets are basically a casino. There is no realistic, generally accepted take on future supply, as the whole bruhaha around Peak Oil shows.

So, as Ron points out, the mostly likely result is that oil will be sold cheap until it suddenly runs out. That has happened to fish stocks many times in the past. The only realistic ways out are governments slamming on the brakes before the economy hits the wall, or a better alternative appearing, which some are betting is batteries.

“probably only possible because oil is very cheap in practical terms. By that I mean oil is too cheap to encourage conservation”

That’s a very interesting way to look at it. Not many people do.

Indeed $3 is really really cheap for the amount of energy you get. Just try pushing a wheel barrel full of gravel up a hill for mile, or plow a rocky field behind a horse, to get a real good sense for how cheap gasoline or diesel is.

Very few things in the world give you such a big bang for the buck.

You can purchase roughly 4 gallons of gas for one hour work at minimum wage here in the states!

Never in history has such an incredible energy deal been available, and to so many people.

The success of the industry at bringing huge supply to the global market has the enabled incredible growth of humanity..overgrowth many would say.

And the billions of us all have gotten used to the idea of inexpensive fuel, and have learned that it is normal state of affairs to use the energy on a whim, for fun or entertainment, or with no regard to efficiency of use or the precious nature of the energy. As if it will always be cheap and there will always be enough.

This not the normal state of affairs in the history of humanity. We are in pretend mode with our way current way of life. We even consider flying in a plane as routine, rather than as an extraordinary (in the extreme) use of energy.

Unless you have unlimited budget for fuel in your personal and business life (and this applies to everyone and the country as a whole), better get used to living with a lot less fuel in the post-peak era.

I suppose this is all obvious, but it seems that the prevailing view of the culture is to somehow consider gasoline to be expensive. People are in for an education on that.

Hickory —

Oil is expensive compared to coal, which is why it plays a marginal role in electricity generation. But $3 a gallon is too cheap to conserve. In Europe it costs twice that, and consumption still isn’t close to optimal.

In America the rich buy new gas guzzlers and the poor buy used gas guzzlers, which skews the market towards waste. In Europe the poor have other options, like public transportation and mixed use zoning, which reduces consumption somewhat, especially in cities.

But if push come to shove I bet economies could cut fuel consumption by half without creating any real economic problems.

“But if push come to shove I bet economies could cut fuel consumption by half without creating any real economic problems.”

The USA could, but it would be extremely painful for the sectors that rely on discretionary/optional use of fuel. If the loss of oil happened quick it will be depression level economics, for a very long time/indefinitely. If it happens slowly the economy could adapt to a large degree.

Over the past few years, we have seen prices drop because of oversupply: it is difficult to increase usage quickly to take advantage of low prices, hence the price drop. My guess is that this inelasticity will not work in the other direction. There is so much wastage (perhaps overuse is a better term?) because of low prices that there will be little problem with cutting back: the pandemic proved it. I see the chance of a slow clawback of usage: maybe a foregone flight here, an electric bicycle purchased there. Essentially, a lack of clear market signals: the same process that convinced people that investing in LTO was a profitable idea. Over the past 10 years, there has been a $100 a barrel price fluctuation in WTI, masking useful price signals because of the multi-year time frame between finding oil and bringing it to market (I am in accord with Ancientarcher on this point).

I expect to see the same thing on the way down. For a period of time, LTO investors in the process of losing their money will continue to depress the market. An ongoing low-price market depends on geological, political and financial factors: a bobble in any of these leads to fluctuations in price (like we have seen in the past ten years). I expect this to continue. Something momentous (a war, a Seneca cliff in Saudi, a depression, an ecological tipping point) could lead to an ongoing higher price market.

So there you have it: a) current conditions favour low prices because of opaque market signals, and will probably continue for some time, and b) Something bad could happen, leading to higher prices.

Lloyd,

Short supply relative to demand will likely lead to rising oil prices. If OPEC plays it smart, oil prices could remain at $80 to 90 per barrel for many years (until 2030 or so). By that time we will have reached the ultimate peak in oil output as determined by the combination of demand and supply (which will be in part determined by a combination of geological and technological factors). After that it will depend on whether we have planned for the peak and have started to transition away from fossil fuel. Poor planning and a failure to see the coming peak will lead to a spike in oil prices followed by a potential economic depression. Better planning might lead to more balanced demand and supply of oil with moderate or even falling oil prices under the most optimistic scenario (low odds of this in my view before 2035, less than 1 in 10).

My guess for the final decline in oil market is a very bumpy price curve.

Nobody wants to do giant investing into a declining market – so big project will be rare. Squeezing out existing fields will be the way to go.

And when the demand decline is slower than the decline in the fields, prices will shoot up. Especially deep sea fields can decline very fast, or creamed giant fields.