Guest Post by

Dr. Minqi Li, Professor

Department of Economics, University of Utah

E-mail: [email protected]

June 2018

This is Part 1 of the World Energy Annual Report in 2018. This author has developed world energy annual reports that have been posted at Peak Oil Barrel since 2014. The purpose of this Annual Report is to provide updated analysis of the current development of world energy production and consumption, consider possible scenarios of world energy supply over the 21st century, and evaluate their implications for global economic growth and climate change. This year’s Annual Report includes multiple parts:

Part 1 World Energy 2018-2050

Part 2 World Oil 2018-2050

Part 3 World Natural Gas 2018-2050

Part 4 World Coal 2018-2050

Part 5 Global Carbon Dioxide Emissions and Climate Change 2018-2100

Part 1 summarizes the general findings of this year’s World Energy Annual Report. Given the currently available information, world oil production is projected to peak in the early 2020s, world natural gas production is projected to peak in the 2030s, and world coal production is projected to peak in the late 2020s. Wind and solar power is projected to grow rapidly and account for about one-third of the world energy supply by the mid-21st century. Despite the rapid expansion of renewable energies, global energy supply and economic growth are expected to decelerate over the coming decades. By the mid-21st century, the energy-constrained global economic growth rates may not be sufficient to ensure economic and political stability for the existing world system. Although world carbon dioxide emissions are projected to peak before 2030, cumulative carbon dioxide emissions over the 21st century will be sufficient to result in global warming by more than two degrees Celsius relative to the pre-industrial time (assuming there will be no large-scale carbon sequestration programs).

Part 2 through Part 5 of this year’s World Energy Annual Report will be posted at Peak Oil Barrel in the coming months. Figures and tables are placed at the end of each section.

World Energy 2017

According to BP’s Statistical Review of World Energy, world primary energy consumption reached 13,511 million tons of oil equivalent in 2017 (BP 2018). Between 2007 and 2017, world primary energy consumption grew at an average annual rate of 1.5 percent.

World oil consumption (including biofuels) was 4,622 million tons of oil equivalent in 2017, accounting for 34 percent of the world primary energy consumption (BP revised the measurement of oil consumption in 2018).

World natural gas consumption was 3,156 million tons of oil equivalent in 2017, accounting for 23 percent of the world primary energy consumption (BP revised the measurement of natural gas consumption in 2018).

World coal consumption was 3,731 million tons of oil equivalent in 2017, accounting for 28 percent of the world primary energy consumption.

World consumption of nuclear electricity was 596 million tons of oil equivalent in 2017, accounting for 4.4 percent of the world primary energy consumption.

World consumption of hydro electricity was 919 million tons of oil equivalent in 2017, accounting for 6.8 percent of the world primary energy consumption.

World consumption of wind and solar electricity was 354 million tons of oil equivalent in 2017, accounting for 2.6 percent of the world primary energy consumption.

World consumption of geothermal, biomass and other renewable electricity was 133 million tons of oil equivalent in 2017, accounting for 1.0 percent of the world primary energy consumption.

According to the World Bank and IMF data, gross world product (global economic output) was 116 trillion dollars (in constant 2011 international dollars) in 2017. Between 2007 and 2017, global economic output grew at an average annual rate of 3.2 percent (World Bank 2018; IMF 2018).

World average energy efficiency was 8,617 dollars per ton of oil equivalent in 2017. Between 2007 and 2017, world average energy efficiency grew at an average annual rate of 1.7 percent.

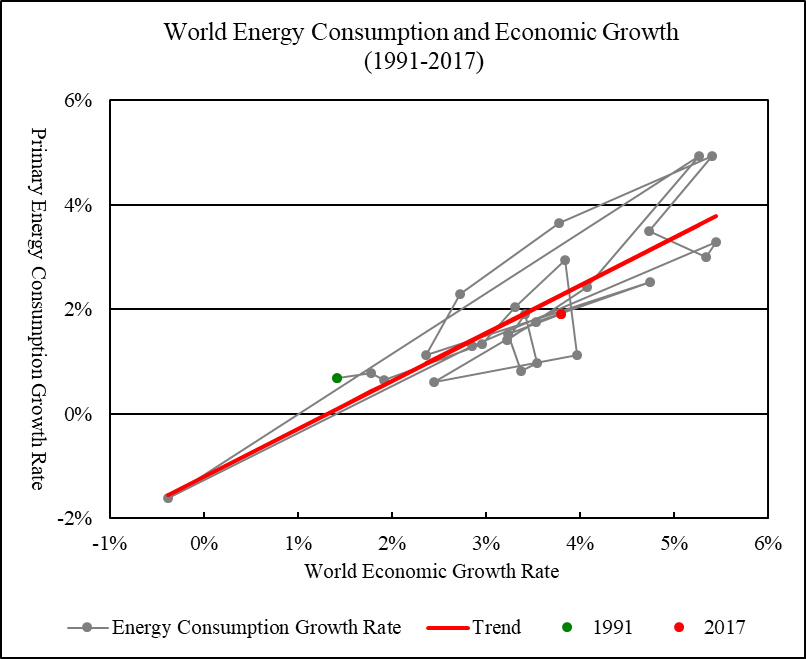

Figure 1 compares the historical world economic growth rates and the primary energy consumption growth rates from 1991 to 2017. The primary energy consumption growth rate has an intercept of -0.012 at zero economic growth rate and a slope of 0.914. That is, primary energy consumption has an “autonomous” tendency to fall by about 1.2 percent a year when economic growth rate is zero. When economic growth rate rises above zero, an increase in economic growth rate by one percentage point is associated with an increase in primary energy consumption by 0.91 percent. R-square for the linear trend is 0.75.

In 2017, world primary energy consumption grew by 1.9 percent, a rate that is 0.4 percentage points below what is implied by the historical trend.

Figure 1 World Energy Consumption and Economic Growth, 1991-2017

Linear Trend: Primary Energy Consumption Growth Rate = -0.012 + 0.914 * Economic Growth Rate (R-square = 0.751)

Sources: World primary energy consumption from 1990 to 2017 is from BP (2018). Gross world product in constant 2011 international dollars from 1990 to 2016 is from World Bank (2018), extended to 2017 using growth rate reported by IMF (2018, Statistical Appendix, Table A1).

Energy Consumption by Major Economies, 1990-2017

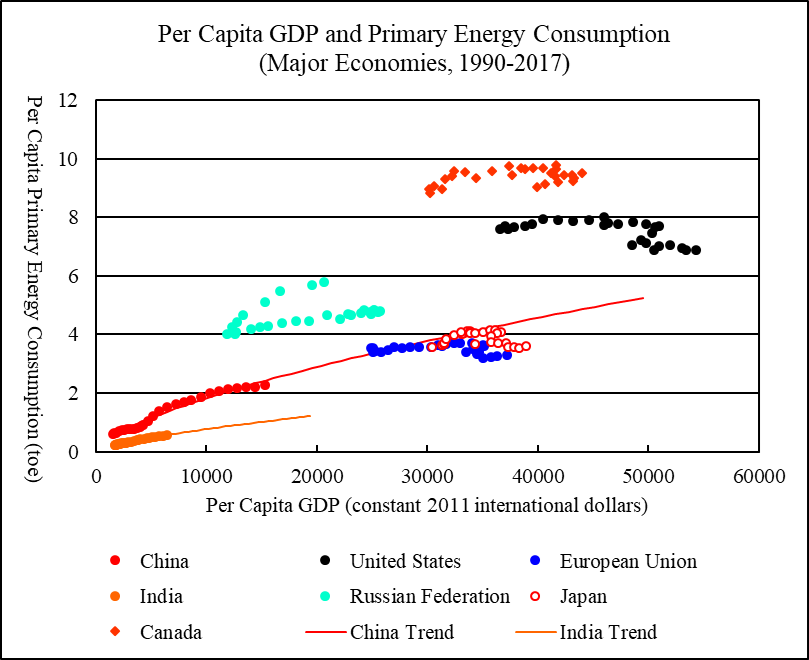

Figure 2 compares the per capita primary energy consumption in relation to per capita GDP for the world’s six largest national energy consumers and the European Union.

China is the world’s largest energy consumer. In 2017, China’s primary energy consumption reached 3,132 million tons of oil equivalent, accounting for 23 percent of the world primary energy consumption. From 1990 to 2013, China’s per capita energy consumption surged from 602 kilograms of oil equivalent to 2.14 tons of oil equivalent. Since then, China’s energy consumption growth has slowed. By 2017, China’s per capita energy consumption rose to 2.26 tons of oil equivalent, which is still substantially below the per capita energy consumption levels of advanced capitalist economies.

If China’s per capita energy consumption were to follow its historical trend in relation to per capita GDP, China’s per capita energy consumption would rise to 5.26 tons of oil equivalent by 2050 (when China’s per capita GDP is projected to rise to about 50,000 dollars). China’s population is expected to peak before 2030 and decline to 1.36 billion by 2050. Given these projections, China’s energy demand will exceed 7 billion tons of oil equivalent by 2050.

The US is the world’s second largest energy consumer. In 2017, the US primary energy consumption was 2,235 million tons of oil equivalent, accounting for 17 percent of the world primary energy consumption. The US per capita energy consumption peaked at 8.01 tons of oil equivalent in 2000. From 2007 to 2009, the US per capita energy consumption fell sharply from 7.7 tons of oil equivalent to 7.04 tons of oil equivalent, reflecting the economic damages caused by the “Great Recession”. Since then, the US per capita energy consumption has trended down, falling to 6.87 tons of oil equivalent by 2017.

European Union is the world’s third largest energy consumer. In 2017, the European Union’s primary energy consumption was 1,689 million tons of oil equivalent, accounting for 13 percent of the world primary energy consumption. The EU per capita energy consumption peaked at 3.71 tons of oil equivalent in 2006. As the European Union struggled with both the global economic crisis of 2008-2009 and the Southern European financial crisis, the EU per capita energy consumption fell to 3.2 tons of oil equivalent by 2014. By 2017, the EU per capita energy consumption recovered to 3.29 tons of oil equivalent.

India is the world’s fourth largest energy consumer. In 2017, India’s primary energy consumption rose to 754 million tons of oil equivalent, accounting for 5.6 percent of the world primary energy consumption. As India’s economy grew rapidly, India’s per capita energy consumption grew from 225 kilograms of oil equivalent in 1990 to 562 kilograms of oil equivalent in 2017. If India’s per capita energy consumption continues to follow its historical trend in relation to per capita GDP, India’s per capita energy consumption will rise to 1.21 tons of oil equivalent by 2050 (when India’s per capita GDP is projected to rise to about 19,000 dollars). India’s population is expected to grow to 1.72 billion by 2050. Given these projections, India’s energy demand will exceed 2 billion tons of oil equivalent by 2050.

The Russian Federation is the world’s fifth largest energy consumer. In 2017, Russia’s primary energy consumption was 698 million tons of oil equivalent, accounting for 5.2 percent of the world primary energy consumption. In 1990, when Russia was a part of the Soviet Union, Russia’s per capita energy consumption was 5.8 tons of oil equivalent. As the Russian economy was torn apart by the disintegration of the Soviet Union and the neoliberal “shock therapy” (free market economic policies of privatization and liberalization), Russia’s per capita energy consumption collapsed to 4.03 tons of oil equivalent by 1998. Since then, Russia’s energy consumption has grown steadily. In 2017, Russia’s per capita energy consumption reached 4.83 tons of oil equivalent.

Japan is the world’s sixth largest energy consumer. In 2017, Japan’s primary energy consumption was 456 million tons of oil equivalent, accounting for 3.4 percent of the world primary energy consumption. Japan’s per capita energy consumption peaked at 4.15 tons of oil equivalent in 2005. Since then, Japan’s energy consumption has tended to fall as the economy struggled between recession and stagnation. By 2016, Japan’s per capita energy consumption fell to 3.55 tons of oil equivalent, lower than Japans’ per capita consumption level in 1990. In 2017, Japan’s per capita energy consumption recovered to 3.6 tons of oil equivalent.

Canada is the world’s seventh largest energy consumer and has the highest per capita energy consumption among the world’s major economies. In 2017, Canada’s primary energy consumption was 349 million tons of oil equivalent, accounting for 2.6 percent of the world primary energy consumption. Canada’s per capita energy consumption peaked at 9.77 tons of oil equivalent in 2007 and fell to 9.03 tons of oil equivalent in 2009. Since then, Canada’s energy consumption has slowly but steadily increased. By 2017, Canada’s per capita energy consumption recovered to 9.5 tons of oil equivalent.

Figure 2 Per Capita GDP and Primary Energy Consumption, Major Economies, 1990-2017

Sources: Per capita primary energy consumption and per capita GDP are calculated using data for primary energy consumption, GDP, and population. National and regional primary energy consumption from 1990 to 2017 is from BP (2018). National and regional GDP from 1990 to 2016 is from World Bank (2018), extended to 2017 using growth rates reported by IMF (2018, Statistical Appendix, Table A1, A2, and A4). National and regional population from 1990 to 2016 is from World Bank (2018), extended to 2017 by assuming that the 2017 population growth rates are the same as the 2016 growth rates. To project China’s and India’s per capita primary energy consumption, a log-linear relationship is estimated between the per capita primary energy consumption and per capita GDP for the period 1990-2017. China’s and India’s GDP and population projections from 2018 to 2050 are from EIA (2017, Reference Case, Table A3 and Table J4), adjusted to make the projected GDP and population levels in 2017 matching the levels reported by World Bank (2018).

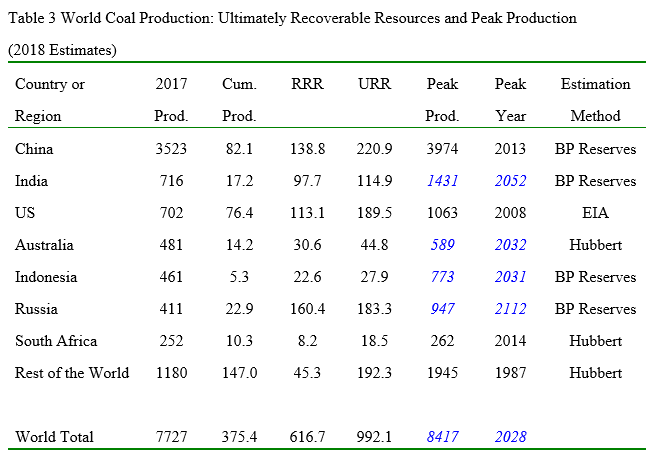

Oil: Ultimately Recoverable Resources and Peak Production

World oil production (including crude oil and natural gas liquids) was 4,387 million metric tons (92.6 million barrels per day) in 2017. Between 2007 and 2017, world oil production grew at an average annual rate of 1 percent.

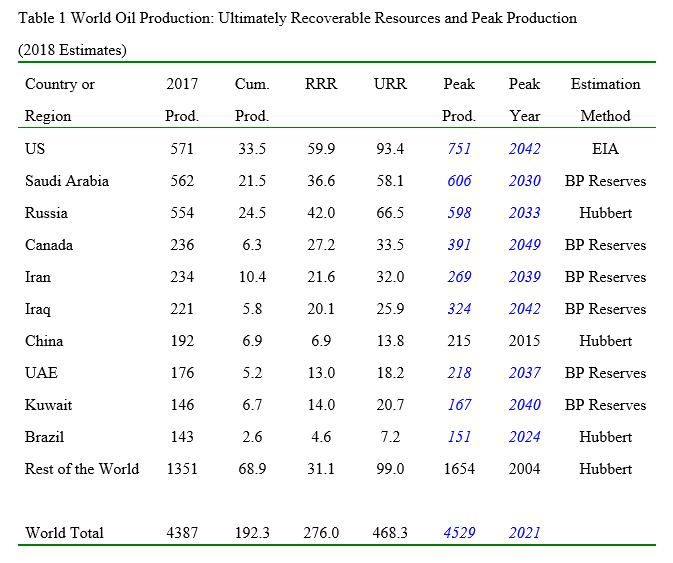

Table 1 summarizes the estimated ultimately recoverable oil resources as well as the projected peak production level and year for the world’s ten largest oil producers, the rest of the world, and the world as a whole. Part 2 of this year’s World Energy Annual Report will discuss the details of oil production projections and show figures of historical and projected oil production for individual regions.

Where available data on historical production allows for the establishment of a Hubbert linearization trend with reasonably high confidence (that is, a clear downward linear trend of the annual production to cumulative production ratio can be identified), Hubbert linearization is used to estimate the region’s ultimately recoverable resources as well as the peak production level and year. This is applied to the Russian Federation, China, Brazil, and the Rest of the World.

For the other large oil producers, it is premature to apply Hubbert linearization. For Saudi Arabia, Canada, Iran, Iraq, United Arab Emirates, and Kuwait, the ultimately recoverable resources are assumed to be the sum of cumulative production and official reserves reported by BP. For the US, the Energy Information Administration’s official projection is used to project the future oil production from 2018 to 2050, extended to 2100 using Hubbert linearization (EIA 2018, Reference Case, Table A1).

World cumulative oil production up to 2017 was 192 billion metric tons. The world’s remaining recoverable oil resources are estimated to be 276 billion metric tons and ultimately recoverable oil resources are estimated to be 468 billion metric tons. By comparison, the BP Statistical Review of World Energy reports that the world oil reserves at the end of 2017 were 239 billion metric tons.

World oil production is projected to peak at 4,529 million metric tons in 2021.

2017 Production and Peak Production are in million metric tons; Cumulative Production, RRR (remaining recoverable resources or reserves), and URR (ultimately recoverable resources) are in billion metric tons. For Peak Production and Peak Year, regular characters indicate historical peak production and year and italicized blue characters indicate theoretical peak production and year projected by statistical models. Cumulative production up to 2007 is from BGR (2009, Table A 3-2), extended to 2017 using annual production data from BP (2018).

Natural Gas: Ultimately Recoverable Resources and Peak Production

World natural gas production was 3,165 million tons of oil equivalent (3,680 billion cubic meters) in 2017. Between 2007 and 2017, world natural gas production grew at an average annual rate of 2.3 percent.

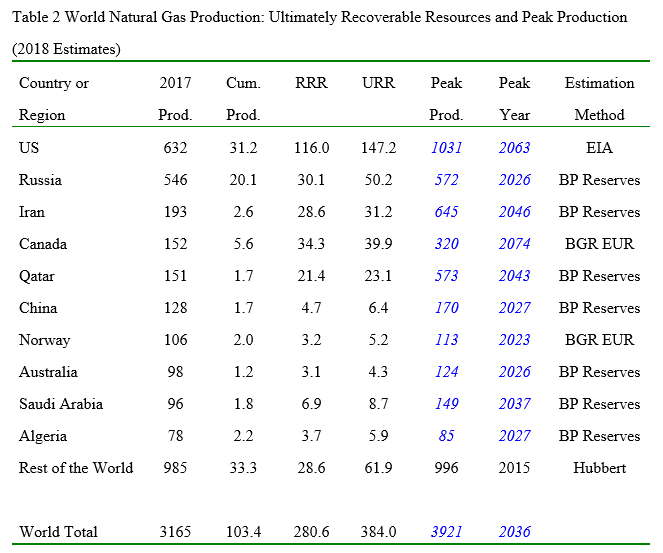

Table 2 summarizes the estimated ultimately recoverable natural gas resources as well as the projected peak production level and year for the world’s ten largest natural gas producers, the rest of the world, and the world as a whole. Part 3 of this year’s World Energy Annual Report will discuss the details of natural gas production projections and show figures of historical and projected natural gas production for individual regions.

For the “Rest of the World” (world excluding the ten largest natural gas producers), a clear downward linear trend of the annual production to cumulative production ratio can be identified for the past several years. Hubbert linearization is used to estimate the region’s ultimately recoverable natural gas resources as well as the peak production level and year.

Meaningful Hubbert linearization trends cannot yet be established for the ten largest natural gas producers. For the Russian Federation, Iran, Qatar, China, Australia, Saudi Arabia, and Algeria, the ultimately recoverable resources are assumed to be the sum of cumulative production and official reserves reported by BP. For Canada and Norway, the official reserves reported by BP appear to be too conservative. The ultimately recoverable natural gas resources estimated by the German Federal Institute for Geosciences and Natural Resources are used for the two countries (BGR 2017, Table A-15). For the US, the Energy Information Administration’s official projection is used to project the future natural gas production from 2018 to 2050, extended to 2100 using Hubbert linearization (EIA 2018, Reference Case, Table A1).

World cumulative natural gas production up to 2017 was 103 billion tons of oil equivalent. The world’s remaining recoverable natural gas resources are estimated to be 281 billion tons of oil equivalent and ultimately recoverable natural gas resources are estimated to be 384 billion tons of oil equivalent. By comparison, the BP Statistical Review of World Energy reports that the world natural gas reserves at the end of 2017 were 194 trillion cubic meters (166 billion tons of oil equivalent).

World natural gas production is projected to peak at 3,921 million tons of oil equivalent in 2036.

2017 Production and Peak Production are in million tons of oil equivalent; Cumulative Production, RRR (remaining recoverable resources or reserves), and URR (ultimately recoverable resources) are in billion tons of oil equivalent. For Peak Production and Peak Year, regular characters indicate historical peak production and year and italicized blue characters indicate theoretical peak production and year projected by statistical models. BGR EUR refers to the ultimately recoverable resources estimated by the German Federal Institute for Geosciences and Natural Resources. Cumulative production up to 2007 is from BGR (2009, Table A 4-2), extended to 2017 using annual production data from BP (2018).

Coal: Ultimately Recoverable Resources and Peak Production

World coal production was 7,727 million metric tons (3,769 million tons of oil equivalent) in 2017. Between 2007 and 2017, world coal production grew at an average annual rate of 1.5 percent.

Table 3 summarizes the estimated ultimately recoverable coal resources as well as the projected peak production level and year for the world’s seven largest coal producers, the rest of the world, and the world as a whole. Part 4 of this year’s World Energy Annual Report will discuss the details of coal production projections and show figures of historical and projected coal production for individual regions.

Where available data on historical production allows for the establishment of a Hubbert linearization trend with reasonably high confidence, Hubbert linearization is used to estimate the region’s ultimately recoverable resources as well as the peak production level and year. This is applied to Australia, South Africa, and the Rest of the World.

For the other large coal producers, it is premature to apply Hubbert linearization. For China, India, Indonesia, and the Russian Federation, the ultimately recoverable resources are assumed to be the sum of cumulative production and official reserves reported by BP. For the US, the Energy Information Administration’s official projection is used to project the future coal production from 2018 to 2050, extended to 2100 using Hubbert linearization (EIA 2018, Reference Case, Table A1).

World cumulative coal production up to 2017 was 192 billion metric tons. The world’s remaining recoverable coal resources are estimated to be 617 billion metric tons and ultimately recoverable coal resources are estimated to be 992 billion metric tons. By comparison, the BP Statistical Review of World Energy reports that the world coal reserves at the end of 2017 were 1,035 billion metric tons.

World coal production is projected to peak at 8,417 million metric tons in 2028.

2017 Production and Peak Production are in million metric tons; Cumulative Production, RRR (remaining recoverable resources or reserves), and URR (ultimately recoverable resources) are in billion metric tons. For Peak Production and Peak Year, regular characters indicate historical peak production and year and italicized blue characters indicate theoretical peak production and year projected by statistical models. Cumulative production up to 1980 is from Rutledge (2011), extended to 2017 using annual production data from BP (2018).

World Electricity 2017

According to BP’s Statistical Review of World Energy, world electricity generation reached 25,511 terawatt-hours in 2017 (BP 2018). Between 2007 and 2017, world electricity generation grew at an average annual rate of 2.5 percent.

Electricity generation from oil was 883 terawatt-hours, accounting for 3.5 percent of the world electricity generation in 2017. Electricity generation from natural gas was 5,915 terawatt-hours, accounting for 23 percent of the world electricity generation in 2017. Electricity generation from coal was 9,723 terawatt-hours, accounting for 38 percent of the world electricity generation in 2017. Nuclear electricity generation was 2,636 terawatt-hours, accounting for 10 percent of the world electricity generation in 2017. Hydro electricity generation was 4,060 terawatt-hours, accounting for 16 percent of the world electricity generation in 2017. Non-hydro renewable electricity generation was 2,152 terawatt hours, accounting for 8.4 percent of the world electricity generation in 2017.

Renewable energies are mainly used to generate electricity. The degree of electrification will set the limit to the penetration of renewable energies from the demand side. The energy electrification index is defined as the thermal equivalent of electricity generation as a share of the world primary energy consumption. The thermal equivalent of 4.4194 terawatt-hours of electricity is one million tons of oil equivalent. This is based on the assumption of 38 percent efficiency in conventional thermal electricity generation and is the formula used by BP’s Statistical Review of World Energy to convert nuclear and renewable electricity into primary energy consumption.

Measured by the energy electrification index defined above, world energy electrification was 31 percent in 1985, 33 percent in 1990, 35 percent in 1995, 38 percent in 2000, 38 percent in 2005, 40 percent in 2010, 42 percent in 2015, and 43 percent in 2017. In average, the world energy electrification index has increased at a pace of about 2 percentage points in every five years. At this rate, the thermal equivalent of world electricity generation should account for about 55 percent of the world primary energy consumption by 2050.

The electricity de-carbonization index is defined as the electricity generation from de-carbonized sources (nuclear and renewable energies) as a share of the total electricity generation. Measured by this index, the world average degree of electricity de-carbonization was 36 percent in 1985, 36 percent in 1990, 38 percent in 1995, 36 percent in 2000, 33 percent in 2005, 33 percent in 2010, 34 percent in 2015, and 35 percent in 2017. Despite rapid growth of renewable energies in recent years, there has been virtually no progress in world-wide electricity de-carbonization since 1985. However, as wind and solar electric power continues to grow rapidly, the pace of electricity de-carbonization should accelerate in the coming years.

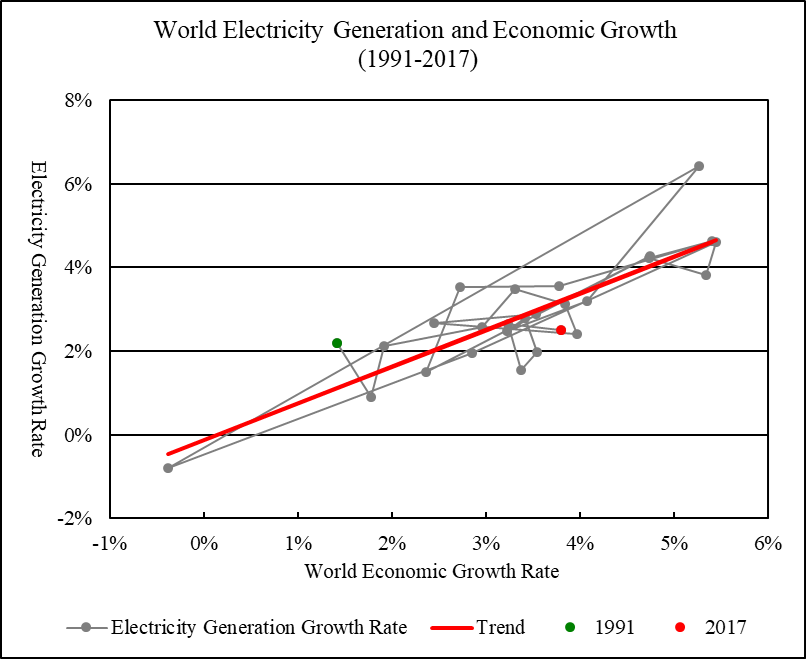

Figure 3 compares the historical world economic growth rates and the electricity generation growth rates from 1991 to 2017. An increase in economic growth rate by one percentage point is associated with an increase in electricity generation by 0.88 percent. R-square for the linear trend is 0.73. In 2017, world electricity generation grew by 2.5 percent, a rate that is 0.7 percentage points below what is implied by the historical trend.

Figure 3 World Electricity Generation and Economic Growth, 1991-2017

Linear Trend: Electricity Generation Growth Rate = -0.001 + 0.878 * Economic Growth Rate (R-square = 0.725)

Sources: World electricity generation from 1990 to 2017 is from BP (2018). Gross world product in constant 2011 international dollars from 1990 to 2016 is from World Bank (2018), extended to 2017 using growth rate reported by IMF (2018, Statistical Appendix, Table A1).

Electricity Generation by Major Economies, 1990-2017

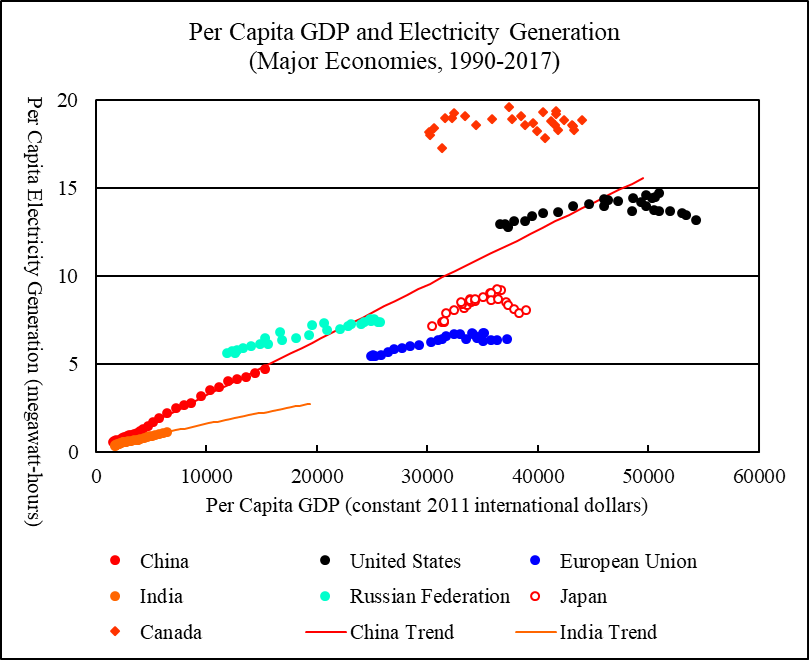

Figure 4 compares the per capita electricity generation in relation to per capita GDP for the world’s six largest national electricity generators and the European Union.

China is the world’s largest electricity generator. In 2017, China’s electricity generation reached 6,495 terawatt-hours, accounting for 25 percent of the world electricity generation. From 1990 to 2017, China’s per capita electricity generation surged from 547 kilowatt-hours to 4,686 kilowatt-hours. If China’s per capita electricity generation were to follow its historical trend in relation to per capita GDP, China’s per capita electricity generation would rise to 15,573 kilowatt-hours by 2050. As China’s population is projected to be 1.36 billion by 2050, China’s total electricity demand will be about 21,000 terawatt-hours by 2050. In term of generation capacity, this is equivalent to the electricity generation by 4,800 gigawatts of coal-fired power plants with 50 percent capacity utilization or by 16,000 gigawatts of solar electric power plants with 15 percent capacity utilization.

The US is the world’s second largest electricity generator. In 2017, the US electricity generation was 4,282 terawatt-hours, accounting for 17 percent of the world electricity generation. The US per capita electricity generation peaked at 14,712 kilowatt-hours in 2007. Since then, the US per capita electricity generation has trended down, falling to 13,160 kilowatt-hours by 2017.

European Union is the world’s third largest electricity generator. In 2017, the European Union’s electricity generation was 3,287 terawatt-hours, accounting for 13 percent of the world electricity generation. The EU per capita electricity generation peaked at 6,770 kilowatt-hours in 2006. The EU per capita electricity generation fell to 6,272 kilowatt-hours in 2014 and recovered to 6,406 kilowatt-hours in 2017.

India is the world’s fourth largest electricity generator. In 2017, India’s electricity generation rose to 1,497 terawatt-hours, accounting for 5.9 percent of the world electricity generation. As India’s economy grew rapidly, India’s per capita electricity generation grew from 331 kilowatt-hours in 1990 to 1,118 kilowatt-hours in 2017. If India’s per capita electricity generation continues to follow its historical trend in relation to per capita GDP, India’s per capita electricity generation will rise to 2,731 kilowatt-hours by 2050. As India’s population is projected to grow to 1.72 billion by 2050, India’s total electricity demand will be about 4,700 terawatt-hours by 2050. In term of generation capacity, this is equivalent to the electricity generation by 1,070 gigawatts of coal-fired power plants with 50 percent capacity utilization or by about 3,600 gigawatts of solar electric power plants with 15 percent capacity utilization.

The Russian Federation is the world’s fifth largest electricity generator. In 2017, Russia’s electricity generation was 1,091 terawatt-hours, accounting for 4.3 percent of the world electricity generation. From 1990 to 1998, Russia’s per capita electricity generation fell from 7,298 kilowatt-hours to 5,601 kilowatt-hours. Since then, Russia’s electricity generation has grown steadily. In 2017, Russia’s per capita electricity generation reached 7,547 kilowatt-hours.

Japan is the world’s sixth largest electricity generator. In 2017, Japan’s electricity generation was 1,020 terawatt-hours, accounting for 4 percent of the world electricity generation. Japan’s per capita electricity generation peaked at 9,243 kilowatt-hours in 2008. By 2016, Japan’s per capita electricity generation fell to 7,893 kilowatt-hours. In 2017, Japan’s per capita electricity generation recovered to 8,041 kilowatt-hours.

Canada is the world’s seventh largest electricity generator and has the highest per capita electricity generation among the world’s major economies. In 2017, Canada’s electricity generation was 693 terawatt-hours, accounting for 2.7 percent of the world electricity generation. Canada’s per capita electricity generation peaked at 19,624 kilowatt-hours in 2000. In recent years, Canada’s per capita electricity generation has stayed above 18,000 kilowatt-hours. In 2017, Canada’s per capita electricity generation was 18,893 kilowatt-hours.

Figure 4 Per Capita GDP and Electricity Generation, Major Economies, 1990-2017

Sources: Per capita electricity generation and per capita GDP are calculated using data for electricity generation, GDP, and population. National and regional electricity generation from 1990 to 2017 is from BP (2018). National and regional GDP from 1990 to 2016 is from World Bank (2018), extended to 2017 using growth rates reported by IMF (2018, Statistical Appendix, Table A1, A2, and A4). National and regional population from 1990 to 2016 is from World Bank (2018), extended to 2017 by assuming that the 2017 population growth rates are the same as the 2016 growth rates. To project China’s and India’s per capita electricity generation, a log-linear relationship is estimated between the per capita electricity generation and per capita GDP for the period 1990-2017. China’s and India’s GDP and population projections from 2018 to 2050 are from EIA (2017, Reference Case, Table A3 and Table J4), adjusted to make the projected GDP and population levels in 2017 matching the levels reported by World Bank (2018).

Wind and Solar Electricity

In 2017, world consumption of wind electricity was 1,123 terawatt-hours, accounting for 4.4 percent of the world electricity generation; world consumption of solar electricity was 443 terawatt-hours, accounting for 1.7 percent of the world electricity generation.

Wind and solar are renewable energy resources. However, wind and solar electricity is intermittent. Integration of wind and solar electricity into electric grids requires maintaining a large backup generating capacity or large-scale storage technologies that are yet to be developed. In the long run, wind and solar electricity will also be limited by the availability of land and mineral resources.

Despite these limitations, it is not unreasonable to assume that wind and solar electricity is likely to keep growing through the 21st century. I assume that the total or cumulative installation of wind and solar electric power will keep growing in the future. However, I assume that the annual installation of wind and solar electric power (that is, the annual addition to cumulative installation) will rise to a plateau and then stabilize.

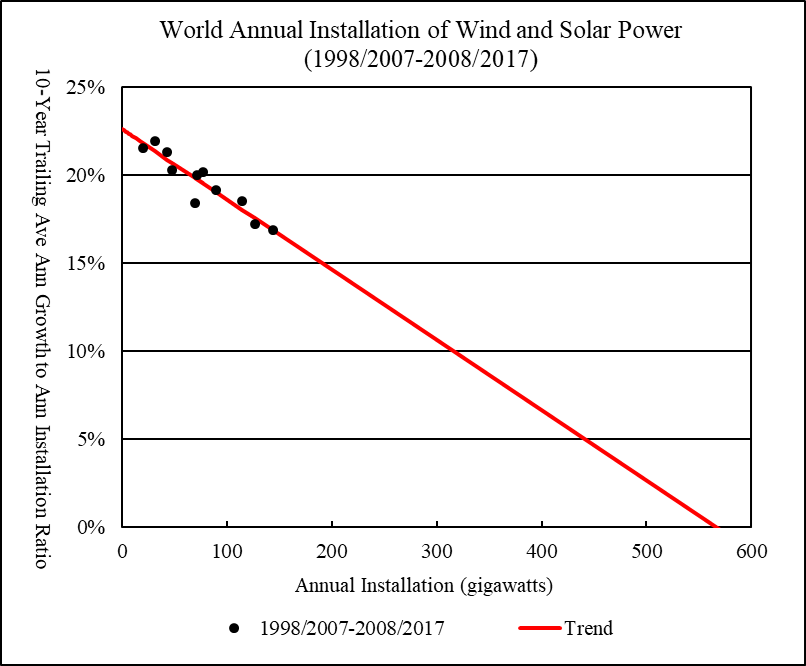

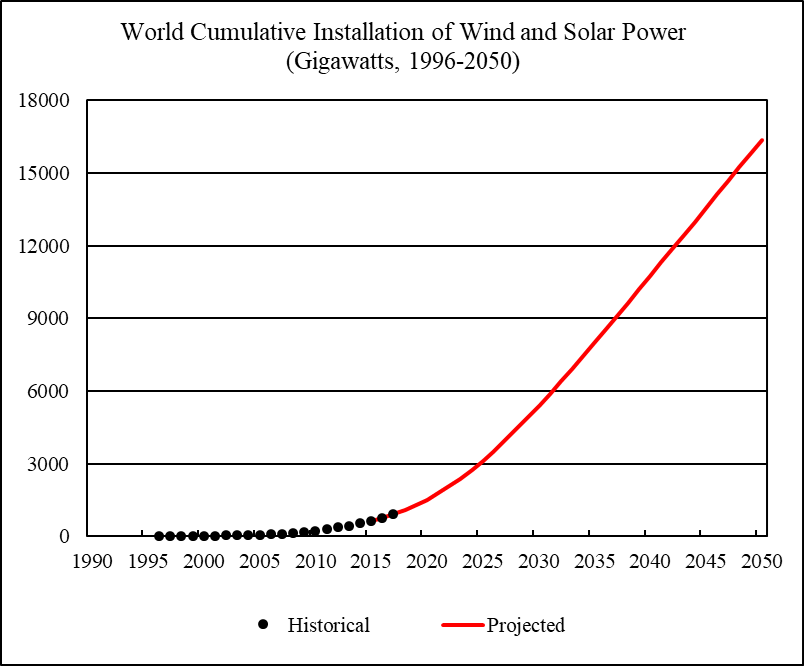

In 2017, the world installed 47 gigawatts of wind generating capacity and 97 gigawatts of solar generating capacity. Figure 5 compares the historical relationship between the annual installation of wind and solar generating capacity and the annual growth to the annual installation ratio from 2007 to 2017. The annual growth to annual installation ratios fluctuate wildly between individual years. To smooth out the fluctuations and establish a more reliable linear trend, I use ten-year trailing averages of the annual ratios. The downward linear trend indicates that the annual installation of wind and solar generating capacity should eventually approach the maximum of 566 gigawatts (where the linear trend meets the zero horizontal line). The regression R-square is very high (0.87).

The parameters of the linear trend shown in Figure 5 can be used to project the future installation of wind and solar generating capacity. The world’s cumulative installation of wind and solar generating capacity is projected to rise to about 16,400 gigawatts by 2050 (Figure 6). By comparison, the US Energy Information Administration projects that the world’s total installed generation capacity of all types of electric power will be about 9,800 gigawatts by 2050 (EIA 2017, Reference Case, Table H-1).

The future wind and solar electricity generation can be estimated using the following formula:

Electricity Generation (current year)

= (Beginning-of-year Generating Capacity + End-of-year Generating Capacity) / 2 * 8760 Hours * Capacity Utilization Rate

In 2017, the observed world average wind electric power capacity utilization rate was 26.1 percent; the observed world average solar electric power capacity utilization rate was 14.4 percent; the observed world average wind and solar electric power capacity utilization rate was 21.2 percent. From 1997 to 2017, the world average wind and solar electric power capacity utilization rate averaged 21.6 percent. These capacity utilization rates are calculated using wind and solar electricity consumption and generating capacity data provided by BP (2018).

I assume that from 2018 to 2050, the world average wind and solar electric power capacity utilization rate will be 21.6 percent.

Figure 5 World Annual Installation of Wind and Solar Power, 1998/2007-2008/2017

Sources: Annual installation of wind and solar generating capacity from 1997 to 2017 is calculated using cumulative installation data from BP (2018).

Figure 6 World Cumulative Installation of Wind and Solar Power, 1996-2050

Sources: Cumulative installation of wind and solar generating capacity from 1996 to 2017 is from BP (2018).

World Energy 2018-2050

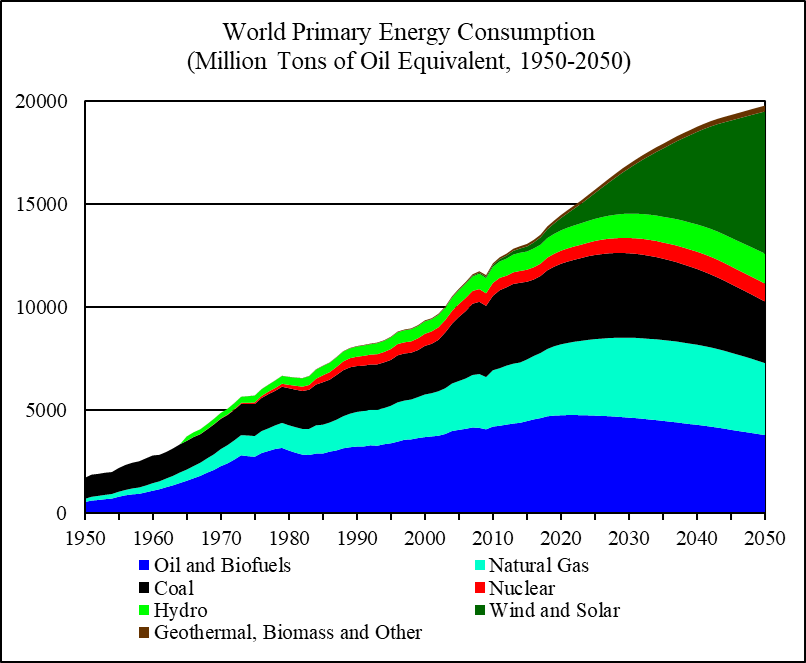

Figure 7 shows the historical and projected world primary energy consumption from 1950 to 2050.

World historical consumption of oil, natural gas, and coal from 1950 to 1964 is estimated using carbon dioxide emissions from fossil fuels burning (Boden, Marland, and Andres 2017).

World primary energy consumption and its composition from 1965 to 2017 is from BP (2018).

World oil consumption from 2018 to 2050 is assumed to be the same as the sum of the world oil production and world biofuels production. Future world oil production is based the projections reported by Table 1. Oil in metric tons is converted to oil equivalent using the formula: 1 metric ton of oil production = 1.034 tons of oil equivalent (using the observed world average ratio in 2017). Future world biofuels production is based on the US Energy Information Administration’s projection (EIA 2017, Reference Case, Table G3), adjusted to make the projected biofuels production level in 2017 matching the level reported by BP.

World consumption of natural gas and coal from 2018 to 2050 is assumed to be the same as production. Future natural and coal production is based the projections reported by Table 2 and 3. Coal in metric tons is converted to oil equivalent using the formula: 1 metric ton of coal = 0.488 tons of oil equivalent (using the observed world average ratio in 2017).

World consumption of wind and solar electricity from 2018 to 2050 is based on the projections shown in Figure 5 and Figure 6.

To project the future nuclear electricity consumption, I use the US Energy Information Administration’s projection of net nuclear electricity generation (EIA 2017, Reference Case, Table H16), adjusted to make the projected nuclear electricity generation in 2017 matching the level reported by BP (2018).

To project the future hydro electricity consumption, I use the US Energy Information Administration’s projection of net hydro electricity generation (EIA 2017, Reference Case, Table H18), adjusted to make the projected hydro electricity generation in 2017 matching the level reported by BP (2018).

To project the future consumption of geothermal, biomass and other renewable electricity, I use the US Energy Information Administration’s projection of net geothermal electricity generation and net other renewable electricity generation (EIA 2017, Reference Case, Table H20 and H22), adjusted to make the projected sum of net geothermal and other renewable electricity generation in 2017 matching the level reported by BP (2018).

World consumption of nuclear, hydro, wind, solar, geothermal, biomass, and other renewable electricity from 2018 to 2050 is converted to their thermal equivalent using the formula: 4.4194 terawatt-hours = 1 million tons of oil equivalent.

World primary energy consumption is projected to rise to near 20,000 million tons of oil equivalent by 2050. Oil is projected to account for 19 percent of the world primary energy consumption in 2050, natural gas will account for 18 percent, coal will account for 15 percent, nuclear electricity will account for 4.4 percent, hydro electricity will account for 7.4 percent, wind and solar electricity will account for 35 percent, other renewable electricity will account for 1.4 percent.

World carbon dioxide emissions from fossil fuels burning are projected to peak at 36.5 billion metric tons in 2028. Part 5 of this year’s World Energy Annual Report will discuss the details of carbon dioxide emissions projections and the implications for climate change.

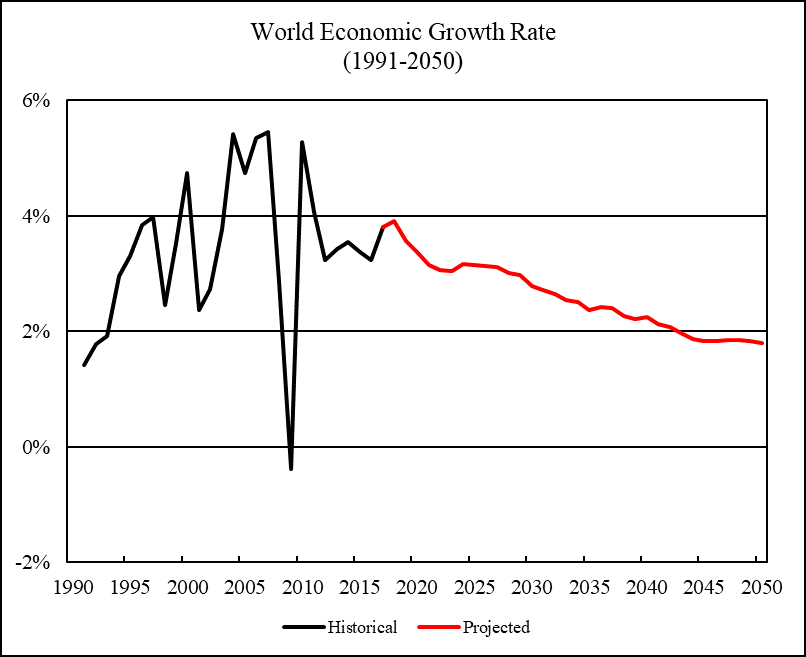

The International Monetary Fund predicts that the world economic growth rate in 2018 will be 3.9 percent (IMF 2018, Statistical Appendix, Table A1). For 2019-2050, global economic growth rate is estimated by using the linear relationship between the primary energy consumption growth rate and the economic growth rate observed for the period 1991-2017:

Economic Growth Rate = (Primary Energy Consumption Growth Rate + 0.012) / 0.914

Figure 8 shows the historical and projected world economic growth rates from 1991 to 2050. World average economic growth rate is projected to fall from 3.7 percent in 2001-2010 and 3.6 percent in 2011-2020, to 3.1 percent in 2021-2030, 2.4 percent in 2031-2040, and 1.9 percent in 2041-2050.

Since the end of the Second World War, global economic growth rate has fallen below 2 percent only in several occasions. During 1913-1950, when the global capitalist system suffered from major wars, revolutions, and the Great Depression, world economy actually grew at an average annual rate of 1.8 percent (Maddison 2010). Thus, by the mid-21st century, although the global economy will continue to grow, world economic growth rate may become too low for the global capitalist system to maintain economic and social stability.

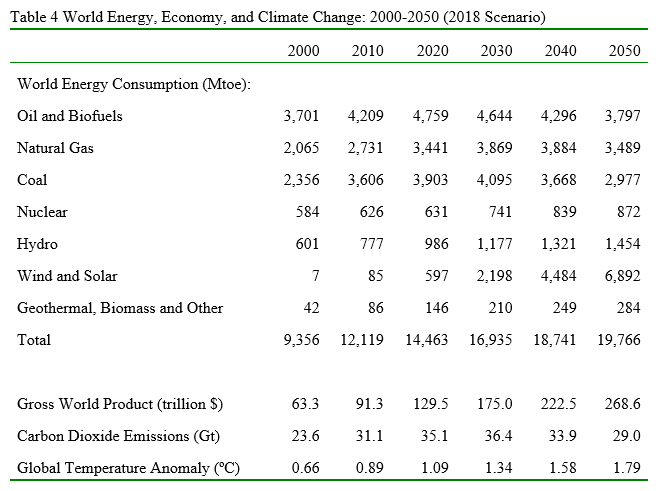

Table 4 summarizes the main findings of this year’s World Energy Annual Report.

Figure 7 World Primary Energy Consumption, 1950-2050

Sources: World historical oil, natural gas, and coal consumption from 1950 to 1964 is estimated from carbon dioxide emissions (Boden, Marland, and Andres 2017); world primary energy consumption and its composition from 1965 to 2017 is from BP (2018); world primary energy consumption and its composition from 2018 to 2050 is based on this report’s projections.

Figure 8 World Economic Growth Rate, 1991-2050

Sources: World economic growth rates from 1991 to 2016 are from World Bank (2018); world economic growth rates in 2017 and 2018 are from IMF (2018, Statistical Appendix, Table A1); world economic growth rates from 2019 to 2050 are based on this report’s projections.

Mtoe: million tons of oil equivalent.

$: constant 2011 international dollars.

Gt: giga-tons or billion metric tons.

Global Temperature Anomaly: ten-year trailing average of the difference between the global average surface temperature and the 1880-1920 global average surface temperature.

334 responses to “World Energy 2018-2050: World Energy Annual Report (Part 1)”

I know very little about the other energy sources, except oil. That it would peak within 2021 give or take a couple of years is a good probability. Using EIA as the source and 2042 as the year for the US, should keep the thought police away, but not very original. After it peaks, it declines. The decline rates do not look as high as I would think they should look. Then again, we have never been here before, and I have nothing to measure against. Or, I guess we have been, in centuries passed, before oil, electricity, and some of the new producers of electricity. We maxed out whale oil.

CO2 and climate change continue their upward trajectory after peak oil, gas and coal peaks? What will they have to bang on after they are gone? However, if Energy production does not meet energy needs, the CO2 could come from burnt trees.

Or, India can accomplish their objective of obtaining helium-3 from the moon, and provide a source of fusion energy for centuries. Though, no doubt, that would provide its own unique dangers to the ecological systems. Nothing will stop the fact, that our continued existence and expansion on this world is an extinction process.

India is a Thorium centric country.

Another one of those– well, never mind.

Poll ranks India the world’s most dangerous country for women

https://www.theguardian.com/global-development/2018/jun/28/poll-ranks-india-most-dangerous-country-for-women

Or, India can accomplish their objective of obtaining helium-3 from the moon, and provide a source of fusion energy for centuries.

Guym, you should put a smiley face after such comments. Otherwise, some goddamn fool out there may think you are serious.

Sorry, of course there should have been a smiley face. Doing anything on the moon, other than scientific studies should be prohibited by international law. Moon mining does not fit into that, nor does colonization. They recently recovered some old data from the first moonwalk. It showed temperatures were far above normal in that area for a long time, just because we were there. We created Moonal warming?

https://amp.livescience.com/62805-moon-surface-warming-apollo-astronauts.html

Which raises the question to me, is our mere existence the major contributor to global warming?

Hi Guym, please note in Table 4 the emissions decline after 2030 (the cumulative emissions of course will continue to rise)

The actual peak emissions year is 2028 under the current projection

Details of emissions will be explained in part 5 of this report

Thank you, Professor.

Hi

How are you?

What do professor Coyne, Kaplan and Patternson think about peak years?

Oil 2021, Gas 2036 and coal 2028?

What are yours peak years?

Sorry by my language im from uruguay

Thank you

Cecilia, I will have a post coming out on July 4th on US and World production. I will give my opinion on the predictions, of oil production, then. So you will just have to wait.

However gas and coal are out of my range of expertise so I will have no opinions or predictions on the peak of these two energy sources. Actually, oil is also out of my range of expertise but I sometimes fake it. But I do have definite opinions on oil which I will give in that post.

But I am with you, I would like to hear other opinions on these peak dates. I think Dennis has already predicted 2021 as the year of peak oil. And I would agree with that. Well, somewhere between 2018 and 2021, but no later than 2021.

But what I find very interesting is the prediction that the USA will peak in 2042. I think that is about as likely as a snowstorm in hell. But you will just have to wait for my post on July 4th to give a more detailed explanation of my prediction.

Well, that will be interesting to read. I look forward to it. I’m sure it will just confuse the hell out of me.

This current article: would this be “cornucopian”?

After over a decade of reading and thinking about this (and fancying myself informed because I studied geology in college), I don’t know what the fuck to believe anymore. US peaked in 1971–no, wait: “shale” topped that–but a peak in 2042?

Poor Deffeyes in dead. I miss 2005, when it seemed the experts had a handle on this.

This one may be “cornucopian” in the sense that it makes major upward revision of projected wind and solar growth in comparison with previous reports

I myself still think this is likely to be revised down in the future. Nevertheless, the report itself is intended to show what the currently available data indicate

As is explained in the first few paragraphs, the basic theme of the report is that exponential economic growth cannot be compatible with climate stabilization

My detailed oil projection will probably be posted after Ron’s

It will be very interesting to compare these. But it is important to note that all projections are based on currently available information and certain assumptions

If you want to dance with the stars, get a good partner. EIA can’t keep a beat. The guy running it, was going to eliminate it in one of his Presidential debates, but he couldn’t remember its name. Still forgetting stuff. He thinks that SA and Russia oil additions are going to take care of Iran additions. He forgets that they are only trying to make up for existing OPEC losses. He forgets that the Permian has logistical constraints, and they are still projecting oil additions to it for 2018 and 2019, of which, more than one million barrels a day will not make it out of the ground in time for 2019. The world believes that organization, and they will get an unjust penalty for doing so. Peak in 2042 is really, really dumb. The Permian peak has a two year hiatus, but US will peak by 2024 to 2025, maybe sooner.

Every time I try to convert your tons to barrels for the US, I get too many. 59.9 billion times 7 is about 419 billion barrels of commercially recoverable in the US? Rystad recently had a dream we had 310 billion barrels. 79 years of it. I really don’t think so. If I tried to imagine hard with some good smoke, I could go 100. But, what’s the difference? It’s only numbers.

“Dumb” or not, peak in 2042 is what EIA is currently projecting

It does no harm to know what the “mainstream” institutions are thinking

It’s obvious that you put a lot of thought into this paper. I am only trying to offer constructive comments, though “dumb” should never have been used. The EIA has some good points, and some bad points. Accumulation of monthly production reports are good. They rely upon a large source of external information to get there. Projections are their weak points. Very weak. Drilling productivity reports belong in the garbage. Dennis has posted a projection on US shale which was good. I would not, personally use EIA as a projection source on which I based my conclusions on. Reference for mainstream, OK.

It would be useful if you split crude oil and NGL when you estimate emissions. I use refinery runs to calibrate the NGL out of the total figures, then account for plastics and asphalt, which leads to lower emission totals. Don’t forget the BP oil figures do include NGL (to an unknown extent).

As people who work with this kind of data know BP always report “oil production” as crude oil and NGL. There is no separate data for crude oil or NGL

EIA does report crude oil plus condensate and NGL separately, but in barrels only, not comparable to BP’s data, and (I think) for period only after 1980

One universal truth for empirical study is that you have to live with the less than perfect world (and data)

Maybe you should footnote your answer. I notice that NGL production is growing at a faster rate than crude and condensate. This is reasonable when we consider that LTO is overloaded with NGL, and that many regions are now processing gas in cryogenic plants.

Fernando,

Yes NGL is growing faster than crude, but eventually Natural gas and NGL will also peak and decline. My medium natural gas scenario results in a URR for NGL of about 300 Gboe. So my “medium” scenario has about 3700 Gboe (505 Gtoe) for C+C+NGL.

Scenario below has World C+C+NGL scenario in Mtoe/year), peak is 2027 at 4682 Mtoe/year (or 94 Mboe/d).

I don’t think the peak or peaks matter so much as when we cease to have enough cheap energy to support the global system we currently have created over the past 200 or so years, which is a result of growing fossil fuel supplies more than anything. It’s possible we are already past that point or, if not, soon will be.

I recently read a book called ‘Scarcity’, quite short though, ironically or not given it’s subject matter, could have been shorter. It presents many examples showing that as we experience shortages of resources – money, time, health etc. – we make increasingly bad, usually meaning more short term focussed, decisions. I don’t remember them going into the reasons so much but I think one explanation is that those bad decisions made now were actually the best choice in our environment of evolutionary adaption as small nomadic tribes in the African Savannah (and that would mean the only chance not to make bad decisions is not to have scarcity, and we’ve got as close to that as we are now likely to get).

Despite our overall wealth there is plenty of scarcity in OECD countries with families holding three or more jobs and still living pay cheque to pay cheque. Real shortages have been growing or covered over by increasing debt, but virtual or perceived shortages engendered by SmartPhones, social media and the advertising industries have been going exponential. Perception of conditions relative to current surroundings or history is what mostly influences behaviour, not absolutes. Therefore, I think as things continue to decline personal, local and global decision-making will deteriorate and considerably exacerbate the problems, and we won’t be getting nice exponential decay curves but extreme volatility and variation both over time and location, with little chance of recovery from each successive dip.

The other reason fossil fuel peaks might not matter is that it looks increasingly like we are past the threshold where tipping points kick in and climate change enters runaway, or at least past the point where the human race is going to choose to do anything meaningful that might prevent passing there eventually. Carbon sinks are turning to sources, ancient carbon in permafrost is starting to be released, the melting of the Arctic ice, currently only about half way complete, is already causing weather disruptions that are becoming increasingly chaotic. The collapse that will come with a 3 or 4°C warming (or more) is going to make an oil peak look like a stroll in the park on a balmy spring day. It might not happen this century but history doesn’t stop at 2100, although if Trump or somebody worse gets elected next time, which is not unlikely given scarcity based decision making, maybe it will.

ps – your English is better than my Spanish, the best I manage is just go backwards and forwards on google translate and then give up. Good luck in the World Cup – I think Uruguay is the country that has consistently punched highest above it’s weight in international competitions given it’s population.

George K said “I recently read a book called ‘Scarcity’, quite short though, ironically or not given it’s subject matter, could have been shorter. It presents many examples showing that as we experience shortages of resources – money, time, health etc. – we make increasingly bad, usually meaning more short term focused, decisions. ”

I would like to add that due to the extreme polarity of the two party system in the US the decisions on the national and sometimes state level are similar to the decision making of of a person with bi-polar disorder. Sometimes the decisions are OK (remission), sometimes they put off or ignore making decisions (depressive state) and then the manic state where they run rampant making numerous harmful decisions.

Here in the US we seem to be in the manic state after having a remission/depressed state for 8 years, after a previous 8 years in the manic/depressed state.

Recovering from the manic state harm and ignoring state is touch and go and usually is a descending downward spiral.

So how is Britain doing?

Lengthy and detailed.

2021 if the EIA “estimate” is correct about how much the US can expand production (Permian overcoming all peak/declines and to that degree???) and the various NOCs aren’t lying seems about right. Evidence has been good everyone else is tapped out and China’s declines will be large in % and large in aggregate.

The unanswerable question is what the real reserve numbers at the Gulf NOCs and Rosneft are.

Yes, even assuming EIA is “correct”, it turns out world oil production might still peak in 2021

I will show these next month

“Yes, even assuming EIA is “correct”, it turns out world oil production might still peak in 2021”

Interesting, since 2021 or 2022 is when every US Federal tax dollar will be need just to service the debt & entitlements. If I recall correctly 2021 is the year when the most (peak) Shale debt comes due. If 2021 does become as Peak Oil production, than the world is going to be filled with a lot of unhappy campers around 2022-2024.

Of course a global recession could mask peak Oil production, or postpone it a bit if the recession is deep enough to impact global consumption.

Dennis Coyne Wrote:

“My guess for Oil peak is 2023 to 2027, though possibly a plateau might be maintained from 2024 to 2030. We don’t have as good info on coal or natural gas”

Coal & NatGas don’t have the same impact as Oil, since Oil is the primary transport fuel source. It is not as if 1.2 Billion vehicles on roads today can be converted to burn coal, natgas or electricity, or converted\replaced fast enough to avoid declining production. All that infill drilling is likely going result in significant production declines in the future. Perhaps it would have been better if infill drilling was never used, global Oil Production would have probably peaked in 2005-2008, but the decline would have been considerably less, and it may have the kick in the pants for the world to get serious about migation.

Techguy,

Oil prices will rise and consumption of oil will adjust to available supply, the 1.2 billion personal vehicles turn over at about 75 million per year as old cars get scrapped, so about 16 years to zero ice vehicles if 100% of new cars were plugins, probably a realistic estimate might be 25 to 30 years to reduce fuel for personal transport to zero.

If there are 1.2 billion personal vehicles in the World and the average fuel economy is 20 MPG and average miles driven per year is 12,000, then those cars use 17 Gb of gasoline and diesel per year. In 2017 the World production of C+C was about 30 Gb and roughly half (57%) this volume was consumed by personal vehicles under these assumptions.

I agree coal and natural gas won’t impact transport very much, but they are used to produce a lot of electricity and that is important as well. That issue can be solved as wind and solar output increase.

The cost of materials to make batteries will go through the roof. I’d better work on a project to make biodegradable batteries from sugar cane bagasse or something similar.

Fernando,

As costs rise, more supply may become available as more mines may be opened and more technology applied, also more material will be recycled and in some cases substitutes may be found.

Dennis Coyne Wrote:

“As costs rise, more supply may become available as more mines may be opened and more technology applied”

Doubtful since the Debt Tsunami is going to hit. We are already seeing cracks in the debt market start to emerge. The Debt issue is going to become much more of a problem by the 2020s as boomers retire and start drawing down on entitlements, pensions, and Healthcare services.

All that extra mining & refining will need more energy inputs. Energy inputs is probably about 1/3 the costs of a battery, since it takes a lot of energy to mine, refine, assemble Lithium batteries.

If I was a betting man, I would place my bet on a long term recession\depression. People will simply to reduce consumption & living standards once energy costs rise.

Of course usually declining living standards leads to riots, revolutions, totalitarian gov’ts and more wars. Pretty much the what happen between 2008 & 2012 when oil prices were above $100/bbl.

Techguy,

A recession is certainly possible and I think likely by 2030-2035 if my peak oil scenario proves correct.

I don’t see the debt problem that others imagine at this point. There will be enough energy, prices will adjust to allocate scarce resources efficiently.

In addition, there will be a lot of opportunity for innovators in the EV, battery, solar, wind, and net zero energy home businesses. Also rail, light rail, building walkable neighborhoods, HVDC transmission are other opportunities.

How it all plays out is difficult to foresee.

Haha, battery prices have crashed with no bottom in sight and you are predicting they will “go through the roof” based on zero evidence.

The beauty of the circular economy is that you never run out of resources because you reuse them.

Hi Minqi,

The EIA’s tight oil projections are likely to be too high by about a factor of 2. if we assume a linear decline from their projection in 2050 for US tight oil over 10 years, the URR for US tight oil is about 100 Gb for the EIA’s AEO 2018 reference case (using EIA’s tight oil estimates for Jan 2000 to Dec 2017 and the projection from 2018 to 2050.) A more reasonable estimate is about 50 Gb for US tight oil URR. Remember that economists t the EIA often assume technology will allow more to be produced whereas the geophysicists at the USGS realize there are physical limitations on how much oil is likely to be produced. I go with the physicists’ estimates at the USGS over the economists’ estimates at the EIA, every time.

The technically recoverable resource(TRR) estimates for US tight oil from the USGS are about 38 Gb for Wolfcamp and Spraberry in the Permian basin and North Dakota Bakken/Three Forks, David Hughes (in Drilling Deeper) has estimated about 8 Gb for the Eagle Ford for a total of 46 Gb, other US LTO plays might have another 10 Gb of TRR. When realistic economic variables are applied (well cost, oil prices, taxes, and operating costs) the economically recoverable resources are reduced to about 90% of the TRR even under a high oil price case where oil prices reach $150/b by 2025 and remain at that level until 2045 before declining gradually to $60/b over the 2045 to 2060 period (assuming substitution of other means of transport for ICE vehicles).

The recovery limits are set by petroleum engineers and geoscientists (also known as humanity’s best friends), not physicists. I’ve never allowed one of those guys to enter the secret rooms where we do that kind of work.

Mostly they are set by politicans, banks and investors (+ silly money) how much they want to invest / throw out of the window.

There must be oil – but the decision if we drill this tier 3 tight oil field or the remote deap sea oil patch depends on money and politics.

Venezuela could produce more than 5 mb/d – with money and other politics. The stuff in the ground is there, and the engineers could be paid to get it.

Fernando,

The technical knowledge to recover the oil is in the hands of engineers, geophysics is the basis of geoscience, and my guess is that petroleum engineers know a fair amount of both physics and geophysics.

The point was mainly that physical scientists (which would include engineers and geoscientists) probably have a better handle on how much oil will be recovered than social scientists (such as economists at the EIA), or in my opinion that is the case.

Dennis, thanks for the comments on EIA

I think I tend to agree with you and I also trust David Hughes’ analysis

But as we know very well, in past Hubbert linearization tends to underestimate the URR and make premature peak oil predictions. So I think it does no harm to err on the conservative side.

Again, if EIA does substantially overestimate the shale/tight oil, that would reinforce the case that world oil production is likely to peak in 2021 (or earlier)

Minqi,

I agree Hubbert linearization tends to underestimate, that’s why my Low case for oil is based on Hubbert linearization, my high case is based on USGS estimates (which may be high for the World due to optimistic reserve growth estimates) and my medium case is in between.

My best guess remains about 2025+/-2 years for peak C+C output, if NGL is added (consistent with your analysis), it would probably be 2026+/-2 as rising Natural Gas output will increase NGL output.

Chart below has an oil shock model scenario based on 2800 Gb of conventional C+C, 500 Gb of extra heavy C+C (Canadian oil sands and Orinico belt), and 100 Gb of C+C from tight oil.

Interesting how a number of car manufacturers are planning on having a large number of EV models available around 2023, similar timing for peak oil. Coincidence or planning?

Gonefishing,

They must be reading POB. 🙂

Could be. Otherwise why the rush?

Toyota has been taking it’s time developing full EV’s even after it’s Prius success. However, even they announce at the end of last year they will have 10 full EV models available in the early 2020’s.

Could be smarts, could be just staying with the competition. Either way, it works out to have models and production ramped up during a high oil price period.

Hi Dennis,

A rough calculation suggest that your model of 3400 Gb of crude corresponds to URR of 466 billion tons, which is similar to my URR of 468 billion tons (though mine is for crude plus NGL)

I was actually looking for your post including that graph above but cannot locate it. Can you share the link here?

Minqi,

It was just a comment not a post.

It follows the reasoning of the post below

http://peakoilbarrel.com/oil-shock-models-with-different-ultimately-recoverable-resources-of-crude-plus-condensate-3100-gb-to-3700-gb/

The difference is that I have separated out both tight oil(LTO) and extra heavy oil(XH) from conventional oil.

Also it uses a separate fallow, build and mature stage with each set with an average time of 13 years (using a maximum entropy probability distribution) applied to conventional C+C (or C+C-XH-LTO).

When C+C+NGL is considered, my scenario has 508 Gboe of C+C+NGL.

Hi Dennis, you meant “5080” Gboe?

Sorry, no I meant 507 Gtoe for C+C+NGL URR for the World. 508*7.3 b/tonne=3700 Gboe. So it should have been tonnes not barrels. I have NGL URR at 300 Gboe or 41 Gtoe.

Professor.Well, it would (2021) except we have an extended hiatus on Permian production. I’d give it 2023, at least.

That’s possible.

Again, my purpose is not to show that I have any particular insight regarding the future (which I don’t)

All I want to do is to demonstrate that given a particular set of data and given a set of clearly laid out assumptions, we can say some thing like, if these happen and if these trends continue, the following will happen.

Another purpose of this study is to illustrate clearly the dilemma/incompatibility between economic growth and climate stabilization. Any delay in peak oil may be marginally better for economic growth, but it is always worse for the climate.

But I will argue that even with an “early” peak oil in 2021, it is virtually impossible to limit global warming to no more than two degrees.

Another purpose of this study is to illustrate clearly the dilemma/incompatibility between economic growth and climate stabilization.

That’s an assumption: it rests on the assumption that wind and solar power cannot replace fossil fuels.

Yes, I personally do not think wind and solar will ever 100% replace fossil fuels

But the current study has already projected a level of renewable energy consumption that is much larger than all the mainstream energy projections.

The projected sum of wind/solar, hydro, other renewables, and nuclear is about 47 percent of the world primary energy consumption by 2050.

The current world electrification index (see text) is about 43 percent. Even if we assume the electrification index continues to grow according to the trend (which may not, electrification seems to have stalled in advanced capitalist economies; and world average electrification has been driven by China and India), world electrification index by 2050 may be about 55 percent. So renewable/nuclear penetration will also be close to their limit from the demand perspective, even if we assume the electricity sector can be 85% decarbonized and the massive installation of gigawatts can be realized (without China’s building boom, given the kind of building pace you observe in the US, the projected 600 GW of wind/solar annual installation can never be realized)

Will have to encourage more nuclear power. I think building costs will cone down as the industry goes through a learning curve and we see smaller modular reactors evolve.

Minqi,

Never is a long time, but if we say “before 2100”, I would agree we probably won’t reach 100% replacement of fossil fuels (for energy use) by 2100, we may be at 95 to 99% replacement and might never reach 100%, but 99.99% will be close enough. 🙂

Often technology accomplishes some amazing things, so it’s difficult to predict what might occur.

Actually it seems the most important factor for future world oil decline is “the rest of the world”

Rest of the world, about one-third of the world oil production, peaked in 2005

Minqi Li Wrote:

“Rest of the world, about one-third of the world oil production, peaked in 2005”

Realistically Global Oil production probably would have peaked in 2005, perhaps late as 2008, without infill drilling and Shale. Post 2008, we were trying to maintain business as usual, by forcing fields output to remain steady even though they were past half-way depleted.

well-

It is unlikely that OPEC reserves are as high as given in BP Statistical Review. Jean Laherrere estimates that conventional OPEC 2P reserves are about 300 Gb less than the 1P reserves given in BP Stats, I think he is correct.

My guess for Oil peak is 2023 to 2027, though possibly a plateau might be maintained from 2024 to 2030. We don’t have as good info on coal or natural gas, but I think Minqi’s dates for those peaks are probably close. It is difficult to predict the exact shape of the output curve accurately, but if we put a 2 year window around Minqi’s estimate for coal, it may be about right.

The estimate for natural gas is similar to my medium estimate from 2015 (a peak in 2040) see

http://peakoilbarrel.com/world-natural-gas-shock-model/

I like Minqi’s estimate better than mine for peak year, say 2035+/-5 as my guess today.

See also

http://peakoilbarrel.com/coal-shock-model/

where I have a coal peak ranging from 2015 to 2045, with the medium scenario peaking in 2025, today I would guess 2030+/-5 for peak coal.

If we have a hot summer and a cold winter will we have a natural gas shortage next year?

Nah. You’ll just have to pay a little bit more for natural gas.

Flirting with low storage. http://americanoilman.homestead.com/GasStorageGraph.html

Hi Dennis,

As about peak coal, by the way, USA peaked in 2008 and China peaked in 2013. These are 2 countries with most abundant reserves in the world. Why this happened, is there any logical explanation? USA production went down a third from its peak.

The price of coal has gone up last 2 years. See:

https://www.indexmundi.com/commodities/?commodity=coal-australian&months=120

and

US coal share in electric energy production is still going down to 28%, as compared to about 40% ten years ago. Can you imagine US coal production rebounding for exports and americans making a fortune as coal exporters?

With respect to the Chinese coal, there is still a large degree of uncertainty. The remaining recoverable resources are still large. BP currently reports China’s coal reserves to be 138 billion tons. But if environment is not the constraint, the remaining recoverable could be well over 200 billion tons.

In Table 3, I did indicate China’s coal production peaked in 2013. But China’s coal production growth resumed last year and the grow seems to have accelerated over the first half of 2018. So I would not completely rule out the possibility that China’s coal production might again overtake the 2013 peak some time in the future

China is investing heavily in production of very large coal reserves in Pakistan.

For global export and Pakistani domestic use in industry, one assumes.

Eurasian belt and road expansion may bring new capital, new transport infrastructure, new coal resource exploitation.

China curtailed their coal consumption growth somewhat because they began to choke to death.

USA coal consumption peaked because of cheaper alternatives- esp fracked Nat Gas, and now wind/solar.

Thank you for the excellent presentation Prof Li.

Although Aleklett (those Swedish Uppsala people) does think the Saudi oil reserves are reasonable

Hey, if you can’t beat them, join them! 😉

https://www.theguardian.com/business/2018/jun/28/bp-buys-uks-biggest-electric-car-charger-network-for-130m

BP buys UK’s biggest electric car charger network for £130m

Erginbilgic said BP was doing more on electric car infrastructure in the UK than any other market, although the firm is also piloting chargers in Germany later this year.

The company said the rebadged BP Chargemaster would prioritise ultra-fast 150KW charging, which can add around 450-600 miles of range per hour of charging. That would mean a car such as Jaguar’s new I-Pace could add about 100 miles in 10 minutes

“I won’t slave for beggars pay.

Likewise, gold & jewels.

But I would slave to learn the way

To sink your ship of fools.”

— The Grateful Dead, Ship of Fools

The BP business model involves providing charges at cost to have customers stick around for 10 minutes to one hour, keep them consuming at the restaurant and convenience store, which will be expanded with more tables and other means to get fat profits.

Peak mining & implications for natural resource management

(embedded video, length 49:30)

Trends like this might hasten a push for driverless trucks.

https://www.washingtonpost.com/business/economy/americas-severe-trucker-shortage-could-undermine-the-prosperous-economy/2018/06/28/61c19e12-7595-11e8-b4b7-308400242c2e_story.html

Just give lots of these mexican migrants a driver education.

We have lots of truck drivers here in Europe, mostly from east europe. No natvie people do this anymore, since the wages are deeper down than for serving burgers or cleaning restrooms.

I think driverless is a bad, bad idea. But, only enough deaths will change the supposition that is wave of the future.

I agree Guym. I maintain that driverless should first be fully tested on closed, or semi-closed, rule based systems, such as railroads and commercial airways.

Level 5, fully autonomous, for trains should be simpler than the ‘wild west’ of the open road. And yet it remains relatively uncommon and tends to be used only on small rail networks that are isolated from the main network. Often cited is the argument that signalling is too expensive if ‘SPADs’ (signal passed at danger) are avoided by full automation. Well that’s good to know.

If the software and hardware needed to run an autonomous railway, where you know the position and speed of every train, and the state of every switch, is not today a comparatively straightforward exercise in logic, then I remain wholly unconvinced that it is sensible or safe to intend deployment of ‘intelligent’ vehicles onto road networks where almost anything goes. Roadworks, floods, ice, no road markings, potholes, poor signage, something falls out of the van in front – the list goes on and on. Ok, people make mistakes, but AI makes mistakes and no one can work out what went wrong or why.

And btw: they are a terrorists charter. A driverless delivery van turning up at a sensitive building or office – I think not.

Doubling or tripling Rail is the best option. Realistically just about all long haul transport should be handled by train, and reduce trucks to local delivery. The US had the best (or near best) rail system prior to 1960s when rail beds were replaced with freeways. You can beat rail for efficiency and speed. Even if trains are manned. one or two train operators can transport the same amount of goods as hundreds of trucks.

I would say prior to 1945.

They were taken down– LA had one of the best rapid transit systems around.

My father used to go from San Gabriel to the beach on the trolly in LA in the 1930’s.

We need to upgrade to a third world status in the US.

There is all this talk about electric cars and lithium batteries, and still some are able to overlook that electrifying and upgrading the rail network to haul more sets up for very efficient use of electricity. And indirectly will reduce oil consumption as well. When lack of transportation fuel starts to hurt then big changes will most likely start to occur; the low cost per kg of rail transportation and shipping will make key harbours and locations connected by railway more attractive. To secure access to relatively cheap power and transportation will be even more important for the industry than today; some will be forced to shut down or relocate because of a bad location.

We kill around 40K persons per year in the US using non-driver less technology. That should be enough deaths to think that maybe they might be a better way.

You can prevent deaths if you want to.

https://eu.freep.com/story/money/cars/2018/06/28/suvs-killing-americas-pedestrians/646139002/

The reason there is so much mayhem on America’s streets is that nobody cares.

People don’t want to be haul truckers anymore because the compensation has been driven so low it in no way justified the lifestyle costs. Those who do already have CDL are getting jobs with local construction (this is advertised nonstop in growing metro areas) or fracking trucks (which DO pay well). OTR trucking pay may sound decent at first but there are huge out-of-pocket costs from traveling all the time, physical costs (sitting all day in a cab isn’t good for you) and family stress. OTR should pay more like what offshore oil or other encampment work does.

It’s another thing to file under “I don’t pay my workers why do I have a labor shortage.”

So, we should have fleets of driverless tank trucks hauling hundreds of thousands of barrels of oil up and down the highways? Steven King would be given more to work with. Terrorists would love it.

“People don’t want to be haul truckers anymore because the compensation has been driven so low it in no way justified the lifestyle costs. Those who do already have CDL are getting jobs with local construction (this is advertised nonstop in growing metro areas) ”

Oil Patch truck drivers earn between $80K & $100K per year. Fleet truck drivers average around $70K/year. Median for all US truck drivers is about $40K/year & the Median salary for Construction Workers is about $33K/year.

I think the issue with the Truck driver shortage, is finding drivers that can pass a drug test, as most companies face drug use problems hiring workers. Some companies have abandon drug testing to fill jobs, but I believe the DOT requires drug testing.

The issue is that Boomers are retiring and Millienials don’t do blue collar jobs. To be honest, I rarely see an employed millennial outside of a retail job. This is going to continue to be growing problem as more boomers retire. Either the US is going to have to import blue collar workers or face permanent workers shortages for jobs that cannot be automated. The issue is that importing skilled\semi-skilled blue collar workers is going to also be a challenge since the rest of the industrial world has the same demographic problem as the US (or worse – Europe & Japan)

“The issue is that importing skilled\semi-skilled blue collar workers is going to also be a challenge”-

People would come here to work, if they were treated with respect and paid decently. Two big if’s. Especially the respect part.

I wonder when a combination of higher fuel prices and higher labor costs combine to raise trucking costs enough to negatively impact the entire economy.

Aerial ropeways: automatic cargo transport for a bargain

Cable Cars Are Changing the World

Image attached of various cargo/material aerial cableways in illustrative support of my preceding comment.

The data above largely comes from BP and BP just a few weeks ago said global consumption was up 1.8% and global production up much less.

Oh and heads up to the OP, BPs data for oil is all liquids. This matters. It’s not all transportation relevant, which is really all that matters (if you want to eat food that moves). So BP is presenting feedstock for plastics and fuel for cigarette lighters. They are consistent, but keep it in mind.

Projections are largely silly, of course. Consumption was larger than production last year. Drained storage? That’s a lot of storage. The 2017 difference in consumption vs production was 6 million bpd. Think about that, sports fans.

I do applaud the OP for using “consumption” and not “demand”.

The best projection is to ask yourself what happens when a country can’t consume the oil it needs to produce and move food because the oil is not available. But their neighbor did get enough to move food to the cities. What happens then? What’s that projection?

Hi, professor Minqi Li,

I noticed 2 errors in Table 1. It’s understandable that URR = Cum.Prod + RRR, as it is for all countries, except China and Brazil, where RRR and URR were swapped. With these corrections, the world RRR should be 277GT and world URR should be 468.3GT.

Thanks a lot. I will ask Dennis to correct them.

Thanks Alex.

Should be corrected now.

The EIA estimations for USA oil and natgas reserves are simply astonishing. It would imply that in USA there are oil reserves (RRR) for 105 years of 2017 oil production and natgas reserves would suffice for more than 180 years of last year’s production. Not only this, the estimations are made with less than 1% error ( 3 decimal digits ). What are they smoking?

Actually, the US “official” reserves are extremely conservative (only worth a few years of current production).

But that will not prevent EIA from “projecting” sustained growth of oil and gas in the future. The RRR listed in Table 1 and 2 are remaining recoverable resources implied by EIA projections (in the Estimation method, I wrote “EIA” not “EIA reserves”)

I guess about renewable energy that wind and solar energy should not be grouped together. Solar energy only is growing 40%/year for more than 10 years. As PV costs are going down, the trend is expected to continue.