All data below is from various sources. All US data is from the EIA. Unless otherwise noted is in thousand barrels per day.

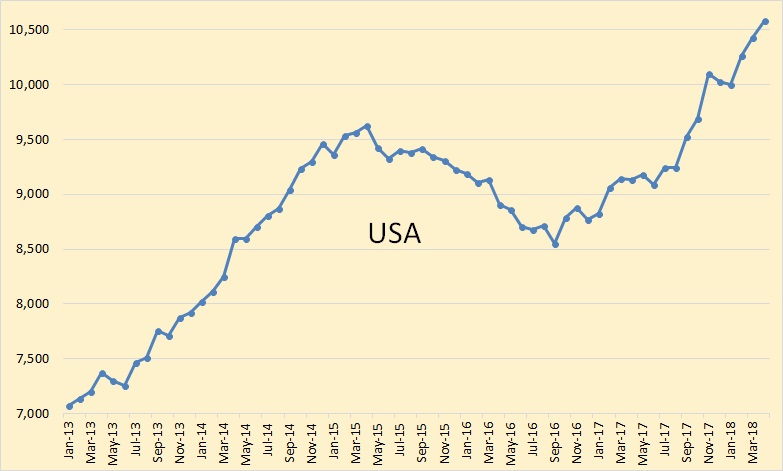

US C+C production through April, 2018. For the last 8 months, the average increase in US production has been 168,000 bpd. Most of this has come from the Permian.

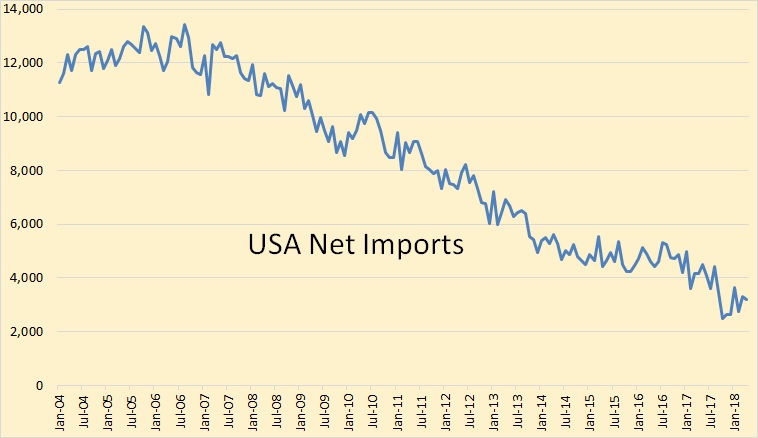

This chart is through February, 2018. US net imports peaked in 2006 and have dropped about 9.5 million barrels per day since then.

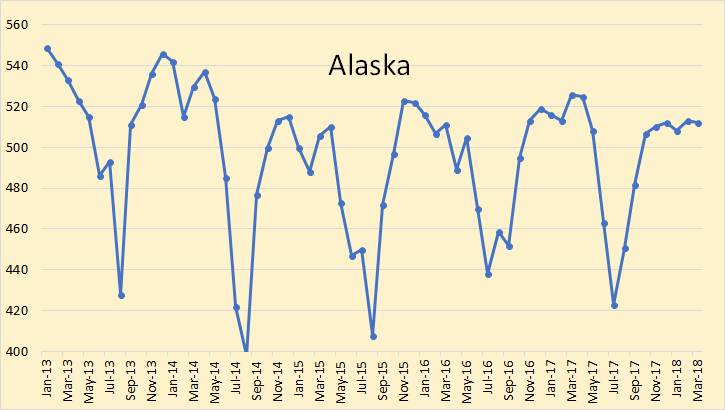

Alaska through March, 2018. Alaska’s decline has definitely slowed.

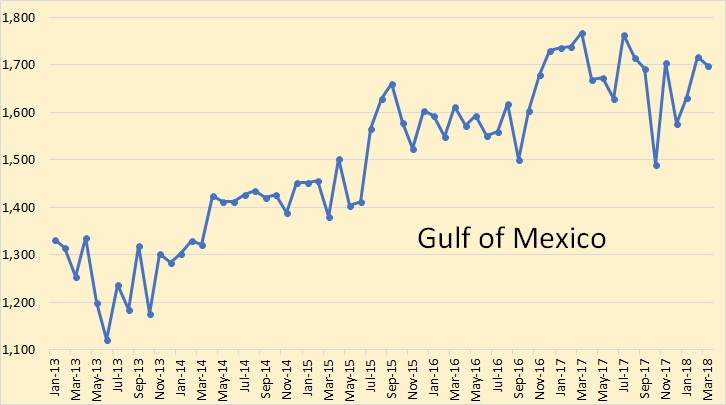

GOM through March. The resurgence in GOM production seems to have petered out about a year and a half ago and is now holding at about 1.7 million barrels per day.

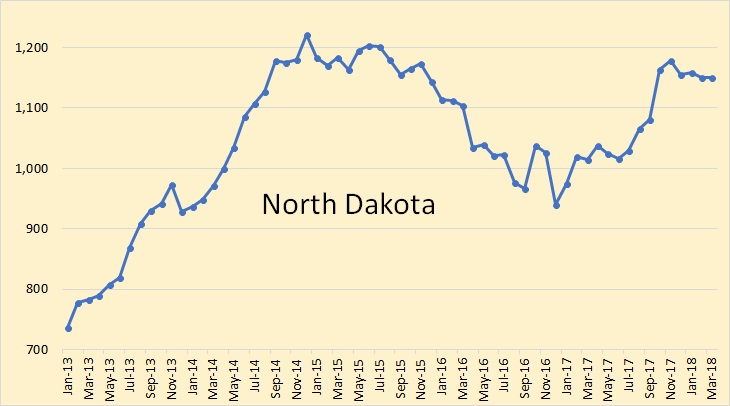

North Dakota through March. Has shale production peaked in North Dakota? It does appear that they are having trouble increasing production in the last six months.

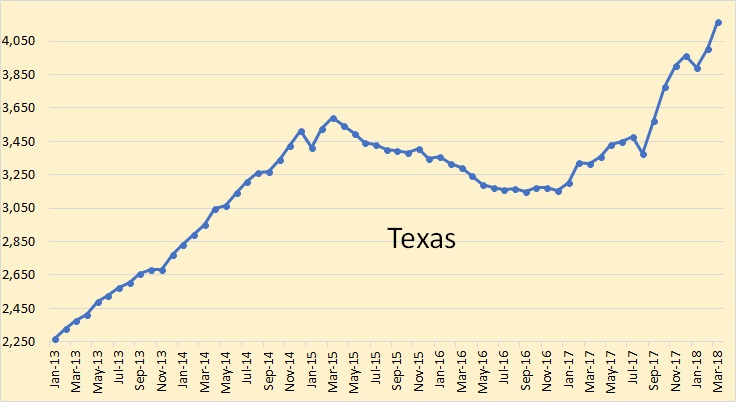

Texas through March, All that increase in US production has come from Texas, primarily from the Permian. For how long and for how much will this increase continue? I have no idea but guesses will be welcome in the comments below.

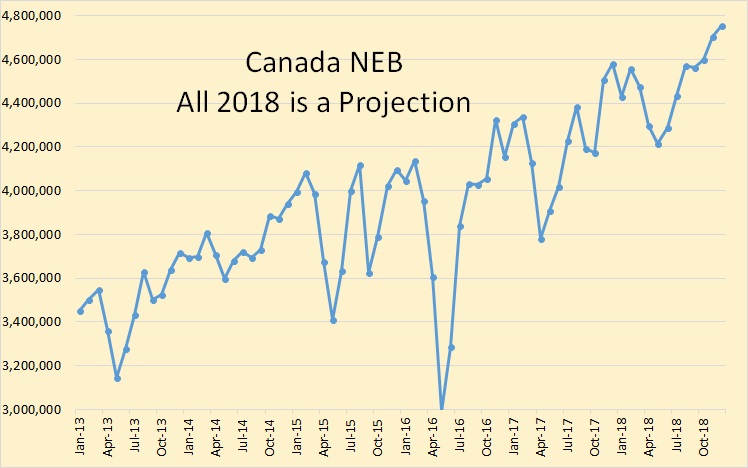

This data is from the Canadian National Energy Board and is through December, 2018. They say all data from September 2017 through December 2018 is an estimate. They are expecting production to bottom out in May 2018 and then increase for the remainder of the year.

This data is from the Russian Minister of Energy and is through May, 2018. Russian production has been almost flat for the last three months. Data from the Russian Minister of Energy averages about 400,000 barrels per day higher than the EIA’s estimate.

China through February, 2018. China is clearly in decline though the decline seems to have slowed.

Mexico through February, 2018. Mexico is in a slow decline though the decline has slowed in the last few months.

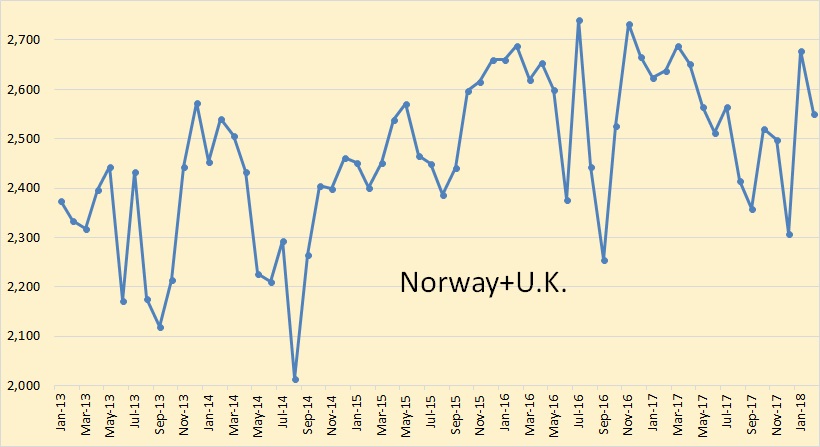

Norway + U.K. through February, 2018. I have combined the two to show what is happening in the North Sea, with the exception of Denmark of course. But I find this a little shocking. The decline in North Sea production seems to have completely halted with even a slight increase.

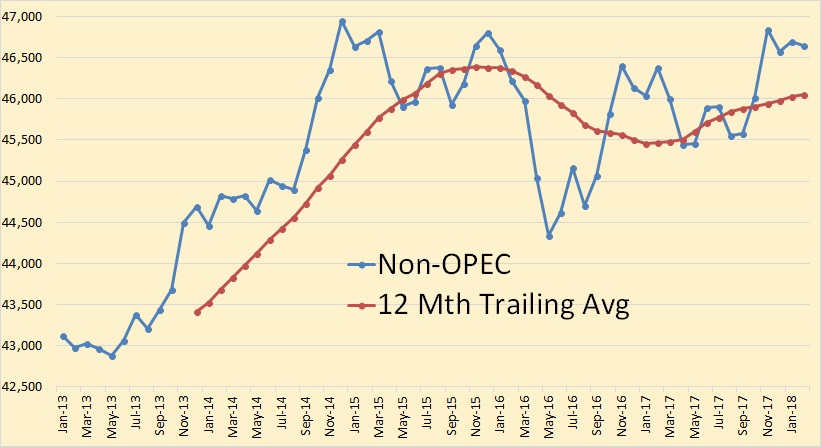

Non-OPEC C+C through February, 2018. Non-OPEC production, even with the increase in US production peaked, so far, in December of 2014. The 12 month average peaked, again, so far, in 2015. But there is no denying that Non-OPEC production is on that preverbal bumpy plateau.

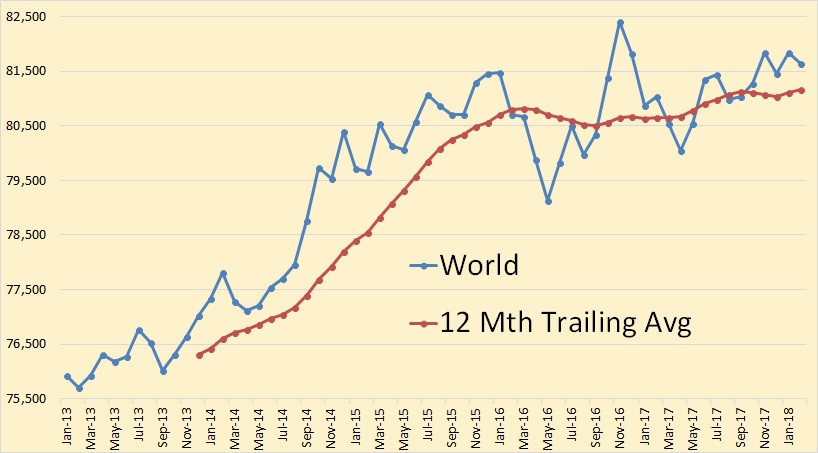

World C+C production through February, 2018. World production seems to have been on a slow steady three year increase in production after making a huge jump in 2013 and 2014.

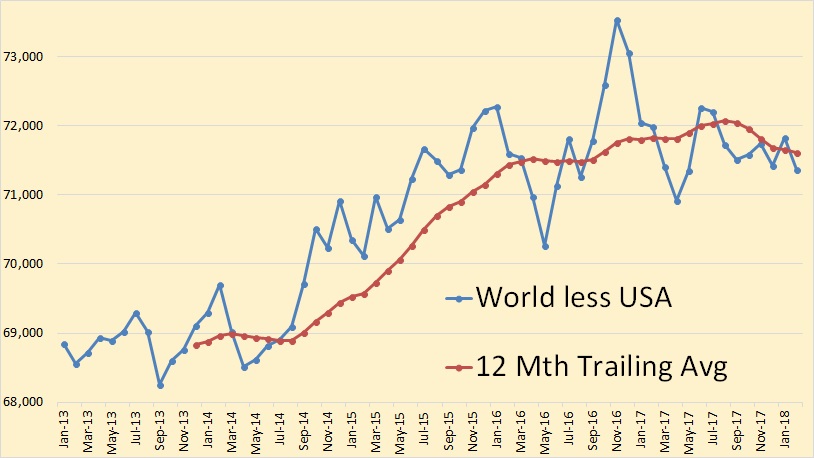

This data is through February, 2018. Just out of curiosity I thought I would show the US’s part in keeping peak oil at bay. Significant I would say.

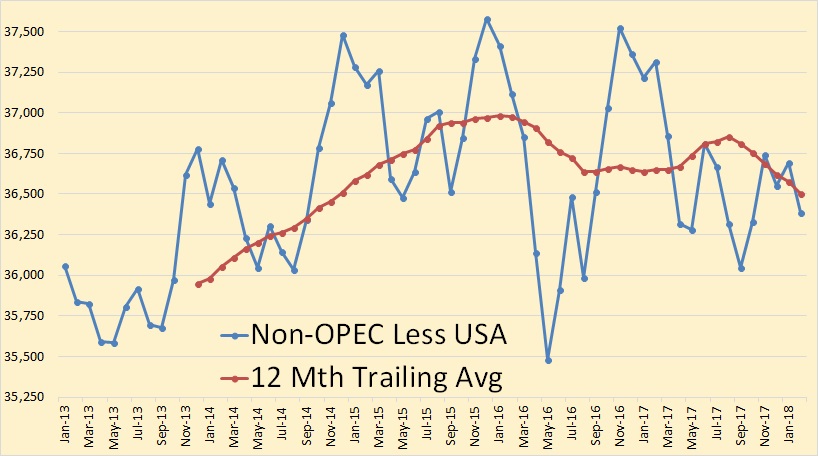

And the US contribution to Non-OPEC production is even more significant. Again, the data is through February, 2018.

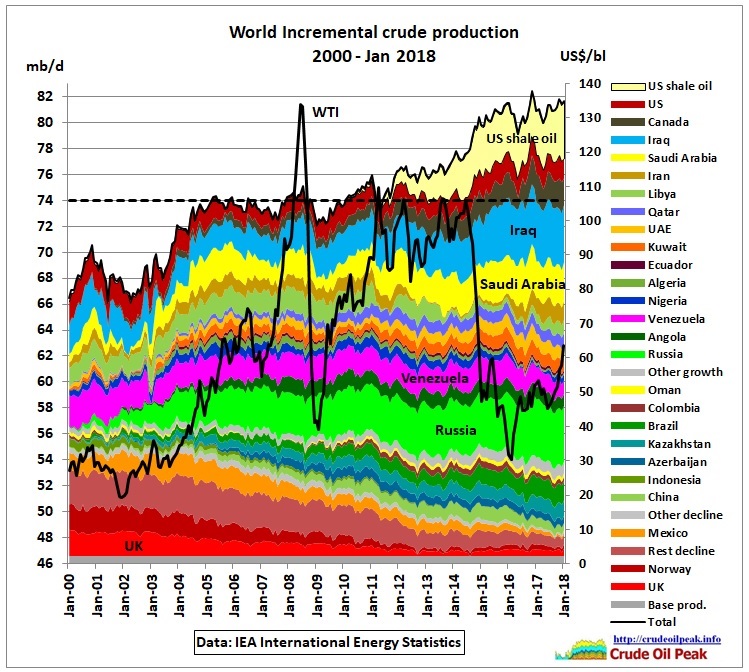

Thanks to Mushalik for the above graph.

218 responses to “USA and World Oil Production”

Why do you think Alaska’s decline has slowed? Thank you.

Because….

Natures way of telling you—-

Because there is a minimum of about 500K BPD the pipeline needs to flow in the winter and production has to meet that need

Incremental graph with all data from EIA until January 2018

http://crudeoilpeak.info/latest-graphs

Thanks, Mushlik, I have inserted your graph into the post.

Are the Saudi and Iraq output reversed on that graph?

Convoluted depiction, as it’s incremental. Starts off with a “base” production of a little over 46 million. How much of each country is “base”? To me “base” would imply something that won’t change, although there is no such animal. All production has decline.

Re: UK & Norway production so I’m guessing that the slight increase is all Norway?

Nope, slightly more from the U.K. than Norway.

That really puzzles me

How much oil comes from fracking the World total at this point, is it correct to assume UK was one of the early adopters of fracking along with US?

Nope, I don’t think that is the case. Fracking, as it is done in shale oil basins in the USA is only done in “tight oil” cases. That is where the source rock is so tight that the oil never left to enter the “reservoir rock” stage.

US EIA estimated technically recoverable tight oil in shale:

Russia: 75 billion barrels

United States: 78.2 billion barrels

China: 32 billion barrels

Argentina: 27 billion barrels

Libya: 26 billion barrels

Venezuela: 13 billion barrels

Mexico: 13 billion barrels

Pakistan: 9 billion barrels

Canada: 9 billion barrels

Indonesia: 8 billion barrels

World Total 335 to 345 billion barrels

Those are EIA estimates and may be taken with a grain of salt. Also “technically recoverable” does not mean “economically recoverable”.

But notice the UK has no shale oil so no fracking there.

Right now I don’t know of any fracking done outside the USA though there may be some done in Canada. But someone else could answer that question better than I.

https://www.spe.org/en/jpt/jpt-article-detail/?art=4223

Argentina, but it appears to be mostly gas.

There seems to be a lot of shale gas in the UK at least:

https://www.scribd.com/document/168260016/BGS-DECC-Bowland-shale-gas-report-Main-Report

37 billion cubic meters.

Don’t expect a lot of it to be recovered since the UK has the population density of Connecticut.

Hi Ron,

There is some LTO being produced in both Argentina (Vaca Muerta) and Canada, I believe it’s probably less than 450 kb/d combined.

Canada 350 kb/d at the end of 2017 (link below)

https://www.neb-one.gc.ca/nrg/ntgrtd/mrkt/snpsht/2017/06-03cndntghtlprdctn-eng.html

In Argentina the data I have found is in barrels of oil equivalent and much of this is shale gas. The numbers are around 90 kboe/d, I have no idea what percentage is C+C.

https://www.epmag.com/producers-set-sights-vaca-muerta-1690866#p=full

Supposedly the Vaca Muerta in Argentina may reach 700 to 1200 kboe/d in 2030, again I don’t know what the split between oil and gas is, but the play is often compared to the Eagle Ford in Texas, which peaked at 1600 kboe/d of C+C and will probably have a URR of about 6 to 8 Gb.

Rosneft is trying in the Bazhenov shale and Argentina is trying the Vaca Muerta.

I hear through industry that the Middle East producers are starting to look at their source rocks.

China’s appear to be garbage.

The Bakken and Three Forks run into Canada and produce over 100 kbd from wells that are Fraced (no k).

Since the Bakken is not as deep there, an extensive water flood is in operation and an estimated 30% to 40% of the 5 Billion barrels of OOIP is expected to be recovered.

I assume they are flooding a sand member. Water flooding shales to recover 30 to 40 % would seem to be very difficult to accomplish.

George has a lot of info on the North sea but basically the UK is bringing online the last of the big projects right now.

Econ GAS warfare and 4D Chess: NordStream Saga. After wrecking a pillar of the US Economy with mandated Health Care via Restraint-of-FreeTrade-Price Fixing-Racketeering, The DC Mob attempts to stomp free trade in Euro Zone via sanctions. The almost 20% US Nuclear electrons require imported processed reactor grade Uranium fuel processed from Russia’s sphere of influence. CHECKMATE. Overheard something like six months worth of US reactor grade inventory on hand? Much of North American uneconomical processing facilities are too contaminated to restart. Saving while destroying the remaining life left in Commercial Nuclear Generation facilities? Could always just wait 25,000 years and re-burn the “spent” rods without processing. Does the Council of Foreign Relations really believe the US IS a NET exporter of Energy? Boston did import Russian LNG this Spring.

https://www.zerohedge.com/news/2018-06-04/nordstream-2-reveals-extent-us-weakness

https://www.zerohedge.com/news/2018-06-02/american-empire-its-media

Could always just wait 25,000 years

I thought it was 24,000?

Pu-239 half life 24,110 yrs. But that still leaves 1/2. Just as bad for you as the first 1/2.

No the second half will decay with a half life of 24,110 yrs so after 24,110 yrs 1/4 will be left. So the second half is only half as bad as the first half.

After the second 24,110 yrs I should have said.

After 3 half-lives (72,330 yrs) you will still die with your whole life.

Of course that was a half life——

But it seems to be the marker of choice.

“Much of North American uneconomical processing facilities are too contaminated to restart”

Well that’s double bad since the damned things aren’t economical now with cheap commie Uranium.

Graph for non-OPEC less US. Does that include Russia and the other non-OPEC signed on with the “cut”?

Yes, that is all Non-OPEC nations. And that includes Russia.

U.S. to ask OPEC for 1 million barrel a day output hike

The U.S. government has quietly asked Saudi Arabia and some other OPEC producers to increase oil production by about 1 million barrels a day, according to people familiar with the matter.

The rare request came after U.S. retail gasoline prices surged to their highest in more than three years and President Donald Trump publicly complained about OPEC policy and rising oil prices on Twitter. It also follows Washington’s decision to reimpose sanctions on Iran’s crude exports that had previously displaced about 1 million barrels a day, or just over 1 percent of global production.

While U.S. lawmakers have habitually criticized the Organization of Petroleum Exporting Countries at times of high oil prices, and the government has on occasion encouraged the cartel to pump more, it’s unusual for Washington to ask for a specific output hike, the same people said, asking not to be named discussing private conversations. It’s not clear precisely how the request was communicated.

The American request was debated at a meeting of some Arab oil ministers over the weekend in Kuwait City, the people said. A statement published after the talks pledged to “ensure stable oil supplies are made available in a timely manner to meet growing demand and offset declines in some parts of the world.” Saudi Arabia and Russia last month proposed a gradual production increase, although other members of the group have yet to agree.

Wonder what they can come up with? Russia and Sauds are the big wildcard. The original cap was about 32.73 as I remember. Now at 32 with Sauds pumping more for internal use. Obviously, .73 is gone from Venezuela and Angola. The ones that were exempted have recovered and are reflected in the 32. That would leave about one million if they could get that high again. With unknowns, what is a way of guessing? I read that Russia (Rofsnet) capped old production so it could be brought back online quickly. Maybe 300k from Russia short term, but Sauds? As the price is dropping now, what real impetus would they have to run up production by a million? Doesn’t make sense. Plow capex into a dropping price? Surely, they have more sense than the Permian idiots.

I wonder if Trump knew, or even knows now, that Iran is an oil exporter and member of OPEC.

I forgot to tell Bolton that following Netanyahu’s orders and sanctioning Iran would reduce supply, increase prices, and create more employment in Texas. Meanwhile I’m advocating strict flaring controls by the Texas Railroad Commission to make sure prices stay high and Texas benefits from it.

When you start with “I wonder if Trump knew…” I think I already know the answer.

Ron,

Could you show Texas and GOM going back to the 70’s?

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFPTX2&f=M

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFP3FM2&f=M

From EIA going back to 1981.

Texas back to 1935.

http://www.rrc.state.tx.us/oil-gas/research-and-statistics/production-data/historical-production-data/crude-oil-production-and-well-counts-since-1935/

gulf back to the 50’s

https://www.data.bsee.gov/Main/HtmlPage.aspx?page=annualRegion

The EIA data only goes back to January 1981.

And here is Texas.

Thanks. The Texas chart is very dramatic since shale started.

https://oilprice.com/Energy/Crude-Oil/Venezuelas-PDVSA-Fails-To-Meet-Oil-Supply-Obligations.html

Guess we dropped about 700k a day at least for a month. If that will continue, the whatever the Permian does will not make a difference in 2018-19. And any OPEC increase would be offset by what was lost previously. Or, a big black swan. Traders have a hard time seeing the forest with all those damn trees in the way. The ones hurt most are China and Russia as most of the oil goes free to pay off past debts.

Am I wrong to feel humiliated by these developments, given how convinced I was by Deffeyes, Campbell, et al. back in 2005 that we were on the verge of the Great Decline? These charts show scenarios that would have been deemed absolutely impossible back then. What say you to this?

Micheal B. You can feel humiliated, sure.

On the other hand, I feel lucky. Lucky that gas is still affordable (and thus food and heat).

Without the innovation of hydraulic fracturing, oil/gas would be very very expensive- I would be very interested to hear some educated guesses on that.

This innovation was not predicted. Perhaps there will be more to come. Perhaps not.

It has bought us time to adapt. Insulate and electrify. Deploy renewables. Learn to live with less.

Time generally wasted it looks like to me.

I’m leery of trusting any forecasts now.

About this comment,

It has bought us time to adapt.

I say, “Ha!” We’ve pissed away all that light, tight oil (and oil sands) on bigger, louder trucks; Sunday driving; stupid toys; “wasted time,” as you say.

I don’t feel lucky at all, because if the Hubbertian view has any credence, the sequel could be worse–much worse–than anyone could have anticipated, on the back side of the curve. Who the fuck knows when it will happen, though.

Right now, it just seems that all the know-nothing idiots were right, and those of us who studied the issue hard were wrong.

It has bought us time to adapt.

Yes, we did have time to adapt. But we didn’t. We just wasted all that time. And when the crunch comes, it will still be just as bad as it would have been if it happened 15 years ago.

No it won’t be just as bad if peak oil had happened in 2007. We had no PHEVs and EVs back then. Now we do. By 2020 you will be able to buy a 200 mile EV for $20,000. Current cost of producing and storing renewable energy is also very low compared to what it was in 2007.

EV’s are pointless, since 75% of electricity comes from fossil fuels. Renewables (excluding Nuclear) only. All your doing is pushing transportation from Oil to Coal & NatGas. EV’s solve nothing.

Low hanging fruit to help with the pending energy crunch:

1. Add more rail to handle more passengers & freight. High speed rail could subsititual a lot of air travel (ie regional air travel) and more rail freight would reduce long haul trucking.

2. Making homes & business more energy efficient (ie better insulation, higher efficienct HVAC systems). reduce/eliminate the daily commute for office workers, should be able work from home or set up local community office spaces for workers. The internet makes most commercial office buidings obsolete. Why Heat/Cool/Power an office building, when all your workers can work remotely from home (remote access, WebEx, Teleconferencing etc). How much Billions of BTUs wasted in commercial office buildings for office space?

3. Build more pumped hydrostorage systems to aid intermittent power sources (wind & solar) and make base load plants more efficient (running a constant load 24/7/365) – thus reducing the need to spool up peak demand natgas plants, or fire up old coal plants.

4. Stop spending Trillions on Military defense & starting more politicially\idealogy wars (USA).

5. Fix\replace aging critical infrastructure (ie water & sewage systems, Bridges, long distance power distribution system,

6. Build new aqueducts to bring in ample fresh water for farm land irrigation. Stopping building bigger cities in regions that need high HVAC inputs & also don’t have any water (ie Southwestern USA for example).

Tech guy- “EV’s are pointless, since 75% of electricity comes from fossil fuels”

Well, not quite. I know individuals who drive entirely on photovoltaic power, and many who drive primarily on it. Things change. Slowly.

I went to the grocery store and the hardware store today, purely on PV power. It was real. Torque right back back up 600ft to my house on the ridge. Fast.

I have a Chevy Volt. I’ve only put 12 gallons in it in 15,000 miles. We have a 75% renewable utility so I’m pretty much driving EV on renewables. If I was more careful I could have gotten by with 1/2 as much gas.

I agree with your list but disagree that EVs solve nothing. Renewable energy is growing very rapidly and the cost of storing it is also falling rapidly. If you put 3.3 kW solar panels on your roof you will produce enough electricity to drive for 12000 miles per year. EVs have enormous and obvious advantages over ICE cars. They do solve the problem of making personal transportation a lot less dependent on oil.

Hi Suyog,

That statistic of 3.3kW solar panel will give you 12,000 miles/year.

Wouldn’t that depend on where on the earth you reside?

Certainly Iron Mike. Where I live (38 degree N), and with an ‘average’ EV, I would get closer to 15,000 miles. In Fairbanks, you would probably get well less than 5,000 (guess), mostly for 3 or 4 summer months.

That statistic is applicable in a place like Chicago which is not exactly known for sunshine. As the cost and efficiency of solar panels improves it will get better.

Solar panel prices will drop over 30% this year due to huge oversupply caused by Chinese dumping. This in turn is caused by the Chinese government, which has reduced the solar power subsidies. It seems they have installed too much solar and it doesn’t contribute as much energy as they expected.

‘It seems they have installed too much solar and it doesn’t contribute as much energy as they expected.’

How do you reach this conclusion??? Perhaps it is the opposite- their grid can’t absorb as much solar production as they installed, so they will try to sell the inventory of uninstalled panels until they get more grid capacity built out.

btw- PV energy is fairly predictable- this isn’t the first rodeo for the Chinese.

Hickory, if their grid can’t absorb the solar power peaks then I have to conclude they have installed too much solar power capacity. It could be a combination of lack of sufficient transmission as well as other factors such as inability to avoid grid instabilities. In any case they decided to cut subsidies and the installation pace has collapsed, leaving manufacturers with stock they’ll have to dump.

As far as I am concerned this is good for my son who is in the solar power racket in the USA.

You seem to have a strong propensity to disparage your son, or the Chinese, or is it solar, or the commies, or…

Racket- A racket is a planned or organized criminal act, usually in which the criminal act is a form of business or a way to earn illegal or extorted money regularly or briefly but repeatedly. A racket is often a repeated or continuous criminal operation.

The real reason solar panels are falling in price so fast is that costs cutting measures being adopted by manufacturers have the side effect of increasing production capacity.

For example, new cutting machinery reduces the amount of silicon needed to make a wafer out of a chunk of silicon, but it also cuts faster. So the same machines can crank out more.

In addition, most of the cost of making a panel is in the factory, so producers are fighting for market share to pay off their investments.

Did you factor in Trump’s new tariffs?

Also, keep in mind with EVs that even in cases where the power comes from fossil fuels the electric motor is so much more efficient that much less CO2 is emitted vs an ice.

Sorry you don’t understand:

Everyday, your food travels an avg of 1200 miles by truck and they consume a lot more energy than your EV. A EV is essentially a personal transportation vehicle. It does not not transport the food from farms to your grocer. It does not transport the clothes you wear or any thing you depend on.

EVs sales are practially microscopic to the number of new trucks and ICE power vehicles. In the US for 2017, only 200K EV’s were purchased, compared to 17M cars & light trucks.

Renewable energy grow is dismal compared to New NatGas turbines being added. FWIW: using a name plate power output figure for Solar or Wind is useless, because both sources are very intermittment. a 3.3.KW solar array will only generate about 14Kwh per day (avg in CONUS in adjusted for population in regions). In comparison, the average american household uses around 35Kwh per day (electricity, HVAC, DHW, Cooking, etc). Another issue with Solar is that there will be periods when there isn’t enough solar to run the car: for instance during overcast days, or during winter (snow, ice reducing output). People that need to commute daily are not going to wait a couple of days for their EV batteries to recharge.

I also presume your not factoring in heating and AC use in vehicles. Also a 3.3Kw panel will not produce 14Kwh of power for a vehicle, since there are conversion losses: Voltage step up/down, Wire losses, charging losses, Battery balancing losses. etc. No energy system any where close to 100% efficient. Also your estimate does not include terrain (ie hilly or mountainous regions), Stop and Go traffic (but with the AC or heater operating near continuously). There are so many factors you are excluding to make your estimate way off what is possible. You must also consider that many people live in apartments or locations where they cannot install solar panels (due to folage, other nearby buildings, or terrain. Also consider that an average household has more than one vehicle. Most married couples have 2 vehicles and both commute to seperate jobs. Then consider they may have kids (adult or of driving age) or parents living with them. Thus a household mak need 10KW to 20KW in panels just for household vehicles.

You are cherry picking the best possible situation instead of apply realistic & critical thinking.

There is no significant advantage of EVs. They will remain as novelty among the greater public.

Consider that even ICE cars are become unaffordable for the major that are deep in debt. Car loans are now beginning to outlast the life of vehicles. The duration of the average car loan is now about 6 years, but a significance number of loans are now around 10 years. Ford is exiting the consumer retail car market, realizing that cars are become unaffordable for the masses. Another financial crisis could wipe them out when large numbers of these drivers default. As did GM & Chrysler in 2008/2009. GM and Fiat\Chrysler will go bankrupt again during the next recession due excessive loan defaults. Subprime Auto loan delinquencies is now at a 22 year high. If the public cannot afford Cheap ICE cars, they aren’t going to afford more expensive EVs. I believe the real cost of an EV, Excluding gov’t subsidies and tax breaks is around $45K. If EVs were produced in the millions there is no way he gov’t could afford to continue the subsidies offered. Thus the consumer would be force to bear to full cost of EV’s.

Nearly the entire industrial world is depend on Debt for BAU. US Consumers, Corporations, and gov’t borrow around $1.3T per year which is unsustainable. My guess 2018 will be a blow out year, and total new debt in the US will exceed $1.6T (guess).

FWIW: We are heading into a three headed storm: Debt, Demographics, and resource depletion. When all three meet together it will result in a long term global economic depression, that will almost certainly cause another global war.

I don’t think the next crisis is far off. Probably sometime between 2019 and 2023. Certainly no way will EVs be produced in the 10’s of millions by then.

Tech

I don’t really disagree with your summary, you’ve hit the notes and painted a very depressing potential future.

So do you have any idea what you can do about it.

I’ll keep it short TechGuy- I generally agree with your gist. EV’s are sure better than nothing (no attempt at adaptation), however. And you may be surprised how the implementation dynamics of EV’s improve (especially compared to ICE) over the next decade.

And I certainly agree with- “FWIW: We are heading into a three headed storm: Debt, Demographics, and resource depletion.”

dclonghorn asked:

“So do you have any idea what you can do about it.”

No. All I can tell you is that I relocated to a rural region and I am building a homestead. Currently working on building an energy efficient home. I guess its my way to separate myself from the insanity of the world. At least I can grow a lot of food that its GMO/Herbicide/Pesticide contaminated.

If I am right about a nuclear war, I doubt I will be able to survive long term. All those Nuclear power plants will meltdown resulting in the doomsday device from Dr Stranglelove.

In the last 15 years world population increased about 1.2 billion people. So audience participation will be uplifting!

This might interest you.

http://www.diva-portal.org/smash/get/diva2:1206408/FULLTEXT02.pdf

Michael B,

The amount of resource that can be extracted profitably is difficult to predict.

Post below (from 2015) has predictions based on assumptions about extraction rates made at that time.

http://peakoilbarrel.com/oil-shock-models-with-different-ultimately-recoverable-resources-of-crude-plus-condensate-3100-gb-to-3700-gb/

An update to this simplified model (using a “full” shock model with separate fallow, build, and maturation stages) from this year is below, this is similar to the medium scenario in the post linked above (similar URR). This newer model uses a separate model for World LTO output and for World Extra Heavy Oil output. Note that the extraction rate for the more recent model is for C+C minus extra heavy oil and LTO, the 2015 model has the extraction rate for C+C minus extra heavy oil, LTO was not modelled separately in the earlier model.

The shock model above assumes a fairly low extraction rate for conventional C+C (C+C that is not extra heavy oil (oil sands) or LTO), in 1973 the extraction rate (production divided by producing reserves) was about 12%. Clearly we can only guess about what future extraction rates might be, from 2000 to 2017 the range was about 5.5% to 6.2%, but oil output was relatively abundant. Peak output of C+C is likely to occur between 2023 and 2032, an alternative model is presented with higher conventional oil extraction rates which peaks in 2032 at 88 Mb/d. An undulating plateau is maintained until about 2037 (output only falls at an annual rate of 100 kb/d from 2033 to 2037).

The cumulative C+C output through 2100 is 3050 Gb for this scenario, with 2700 Gb of conventional, 100 Gb LTO and 250 Gb of extra heavy oil. The higher level of output in this alternative scenario through 2040 (compared to the previous scenario) leads to higher annual decline rates. For the previous scenario the annual decline rate remained below 2.5% until 2067 vs reaching 3.5% in 2067 for the scenario with higher extraction rates. Bottom line is that higher output in the near term leads to faster decline rates in C+C output after the peak.

If my guess for URR is correct (Jean Laherrere believes 3000 Gb is a more reasonable estimate and the USGS thinks conventional and non-conventional C+C resources are roughly 4000 Gb), my estimate is between these at 3400 Gb with roughly 3000 Gb produced between 1850 and 2100), reality may fall between these two scenarios.

I guess I would say, that if it happens this year or next and you knew it was coming for fifteen years, and did nothing personally to prepare for it (house, lifestyle, transportation, etc), then you deserve what you get. Unfortunately most folks won’t give a rat’s ass until it punches them squarely on the jaw. We are discussing an unprecedented moment in geological and biological history, the consequences and exact timing of it cannot be known. But we all know it will be a very big deal, likely the biggest deal ever. Don’t kick yourself too much for not being able to figure out when and/or how it will play out. Just do what you can to prepare and then, when it does happen, hold on for dear fucking life.

Yes, this is what I suspect, but I no longer have much “faith” in my own abilities to assess the situation.

Our “preparations” have included learning not to go much of anywhere, growing and making much of our own sustenance, and living in comfortable, intentional poverty. Will it matter? Who knows!

Michael B,

I’m on the same boat.

I 1st became aware of peak oil in 2006 as an explanation for rising gas prices and what turned out to be a multi-year stagnation in global supply.

From 2006-2009 everything that was predicted by Chris Martenson, Colin Campbell, Matt Savinar, Richard Heinberg, Matthew Simmons, Stephen Leeb, Robert Hirsch, and others unfolded precisely and as horrifically as predicted.

It is undeniable that the global economic collapse, and near failure of our global financial system was the result of a system that requires infinite growth meeting the reality of a finite supply of energy.

Malthus was right; the Club of Rome was right; the 2nd Law of Thermodynamics drove our civilization.

Yet here we are 10 years later.

Innovation has rendered decades of the Hubbert curve, the relationship between discovery and production, the bell curve, Matthew Simmons predictions on Saudi production, all invalid (or meaningfully delayed).

I cannot describe the internal emotional vacillation I consistently experience. I am jubilant that my worst fears, which after 2008 I felt were 100% going to unfold, were completely misplaced and wrong in their timeline.

I am also constantly weary that we may be in the 2003 of the next cycle and that we got lucky in 2008 to have the political and economic establishment save the financial system from complete collapse. For many reasons I feel as though the necessary political/economic response to 2008 would be impossible to repeat in today’s environment.

Were it not for the passage of TARP… the entire global economic system was literal hours away from completely freezing and collapsing. If global production plateaus for 3 years again, much less permanently declining, we are in for a world we scarcely recognize.

That being said, that doesn’t appear to be unfolding anytime soon, and in the meantime the world is significantly more prepared to transition from oil than it was 10 years ago. The best selling midsize sedan in the U.S. is the Model 3, an electric vehicle. The best selling luxury sedan is the Model S, an electric vehicle.

I’m still extremely skeptical of our ability to transition in time to avoid an economic catastrophe, but I also recognize that we are better off and better prepared today than we were in 2008. Every year we can delay a plateau/peak feels like a blessing that makes us slightly more prepared to weather the decline.

The best selling midsize sedan in the U.S. is the Model 3, an electric vehicle. The best selling luxury sedan is the Model S, an electric vehicle.

Huh? Tesla is only claiming that the Model 3 will soon be the best selling midsize “premium” sedan, in the same class with BMW, Audi, Mercedes and Lexus.

Conventional gasoline cars like the Honda Accord and Toyota Camry each sell far more cars than Tesla Model 3.

Besides, mid-size sedans are being shunned in favor of pickups and SUVs. Ford will likely sell a million F-series pickups this year alone, more than three times as many vehicles as Tesla has ever sold.

Brian

If you went through every oil producing country, you would realise that global peak oil is between 5 and 8 years away.

When Colin Campbell et al made their predictions they based them on quite low URR figures. However even optimistic URR numbers does not delay peak oil for long. It simply allows consumption to grow far more, resulting in higher depletion rates.

Back in 2005 there were too many countries like Columbia whose contribution pushed global peak oil further out.

https://tradingeconomics.com/colombia/crude-oil-production

China kept on increasing oil production far longer than they expected.

https://tradingeconomics.com/china/crude-oil-production

However now, out of the major 50 oil producing countries 40 are past their peak!

US shale oil has simply masked the global reality, US shale will peak between 2022 and 2025. Since shale wells decline by 80-90% in the first 3 years, it will require an inordinate amount of drilling to maintain 9/10 million barrels per day. If it gets that high.

If you write a list of countries past peak, you will see that most of them peaked in the last 20 years. So modern technology did not save them.

Also consider all of the horizontal drilling that permitted large fields to continue to steadily produce oil, even though those fields are well over half depleted. Its likely that once horizontal drilling has run its course production will drop very rapidly, instead of a modest production decline rate.

There is a good chance that the next global recession will be start of peak production: A global recession will cause demand destruction & a decline in prices resulting is less CapEx. A lot of Shale driller debt comes due between 2019 & 2023, and its likely that there will be bankruptcy and consolidation.

Its likely the next recession will also trigger a demographic crisis as aging populations and lack of jobs result in much higher retirement rates. Since 2008 Boomers have opted to remain employeed in order to sustain their living standards or increase retirement savings. Since no industrialize nation has saved for promised entitlements, taxes will increase & benefits will be slashed likely causing a long term recession or depression, as well as currency deprecation as gov’ts monetize debt.

Tech Guy, et al. above:

If what you say is true (big “if”, as I’ve learned to qualify), then that means not heeding the warnings of near-term peak, circa 2005 (in spite of their turning out to be incorrect) has made the problem worse, orders of magnitude worse. We’ve “extended and pretended”; and when our illusions are upended, it will be–catastrophic.

I keep hearing the words of Colin Campbell, who always insisted that the exact date of the peak is not relevant; what’s relevant is “the vision of the long decline” after peak.

Hi Michael,

You shouldn’t feel bad. In my worthless opinion, complexity and the gene deep human desire for more, which is often underestimated makes the analysis of the situation very hard to grasp.

The issue of peak oil is as complex and arguably even more complex than climate change. It just has so many variable factors, and no matter how powerful your supercomputers and simulation software, you just don’t know for certain what will happen in the real world. You might get an idea of this or that might occur, but to get a timing on the events to pass is i dare say, impossible.

All living systems are at war with entropy. But any logical person would know, that entropy will eventually win, because it never stops working.

My worthless guess is, climate change, peak oil or peak energy, and overpopulation and environmental destruction will bite from different angles all at once, and i think humans will most definitely be extinct. When will it start?

I think after there is a PHYSICAL LIMIT in supply. Like Ron said before, as long as there is money flowing in, for e.g. in shale plays etc there will be oil pumping even at a loss.

When we see Ghawar struggling (which will be hard because of all the secrecy in Aramco) and the shale and tar sands struggling. Then you’ll know you are close to a supply constraint. But until then, there will be recessions and financial crisis’s that the world will recover from, same old cyclic shit. Until economics meets that physical limit (where EROI << 1), the game will continue ad nauseam. That's my worthless 2 cents.

We are constantly told that shale (tight) oil is being produced at a loss. If that is the case, how come production keeps increasing? Who keeps investing more and more money in a losing business?

Also, several years ago we were told that shale oil wells have a short lifespan and they decline rapidly and by now the production should be collapsing. Yet production keeps increasing.

It looks like no one – least of all the experts – know how to predict future oil production. They were all wrong. I will be extremely wary of trusting any future production forecasts.

Two things. Oil can be produced at a loss as long as there are investors who are willing, or unknowingly, accept that loss. Sooner or later, however, the chickens must come home to roost. When the investors lose all their money then the shale oil producers must find some other source to fund their fracking operations. And if they cannot?

Second, yes, shale oil wells have an extremely high decline rate. They decline in one month what conventional wells decline in one year, or somewhere close to that figure. The EIA confirms this in their “Drilling Productivity Report”. Google it if you doubt what I am saying. But the investor’s money just keeps pouring in and new wells keep getting drilled and fracked.

As to future oil production forecast. Hell, it all depends on the price of oil. I will not try to predict that.

“They were all wrong.” Yes, that will probably continue to be true. Finding a bunch of big new conventional onshore wells is probably a peak that is over. New production is now being driven by technology. It could possibly change. Any prediction now can change because of economic, political, or technology reasons. But, oil is finite. At some cost, alternative energy will take over.

Non predictable systems are chaotic systems. Not a good base for stable development. Even if the ride goes on and on and on …

New production is mostly driven by higher oil prices. Most of the “new technologies” are refinements and improved versions of 30 year old knowledge, made feasible by higher oil prices. Why don’t you try to see how much drilling would be done at $30 per barrel?

Suyog- the LTO wells do have a very rapid decline rate. Production is maintained, or increased, by drilling a huge amount of wells- pincushion.

We do have to remember that LTO wells would make excellent 10 BOPD strippers if price goes over $100. They’ll decline at a very low rate once they are barely breathing.

Even if they reach a low decline rate, won’t their extreme length and curve may them expensive to operate and therefore unprofitable at low volume.

I think Shallow Sand wondered about the costs of these strippers;

What if you get a coffee can sized plug of sediment blocking the well half way down a lateral,

How much to fix scale or waxing up,

What will the talcum sized component of propant do to your lifting pumps if it flows back?.

If the wells were drilled in a hurry, will they be sufficiently true vertical to avoid tubing holes/ broken rods used with a Lufkin?.

Even if ZIRP continues there will still be bondholders to pay. And the principle to pay back.

Shale wasnt profitable when the wells were mostly young last time oil was 100USD. A minority of wells should pay their way, but will the average/below average be going concerns as strippers?.

I don’t have an answer because I don’t have the well design, such as the directional plan, casing sizes, etc. Lets say oil price is $150 per barrel and we put a horizontal well on clock to make 300 BO, 300 BW, and 600 MCF per month. The oil fetches $120 after royalty, gas $2 after royalty. So the well makes about $33000 a month. The question is what can be done to lift that well cheaply while avoiding treatments and workovers. That’s where I get lost because I don’t have the chemical analysis to see if it’ll scale, whether there will be a need to corrosion treat, and what will be used to lift it. I think I could play around with say 100 wells and eventually figure out how to squeeze profits. But the price will have to be really high.

Fernando, I suppose it always depends on the unique characteristics of a given well. However, i had been led to believe that generally these LTO wells would not make good strippers, because basically they had more potential problems than the typical conventional well. So, once they get down to a low production level and need a new pump, or something else happens down hole will they be worth reworking. Or will we see a lot of these wells abandoned beginning around 10 years.

Many of the big shale operators have based their presentations on projections of these wells being economic for 30 years, with a large part of the total EUR coming from that long tail.

I’m thinking that 2010 and 2011 Bakken wells are the best group to watch to see indications of how these LTO wells will age.

Dclonghorn, I assume (but im not sure) a depleted LTO well producing from a very low permeability rock will have a very low productivity index. Such wells can be lifted inefficiently because dropping bottom hole pressure to the max doesn’t increase rate much and causes gas lock and scaling.

I’m thinking of getting the well lifted with a jet pump, and powering it with cool de-gassed produced fluid, without working too hard to get water cut way down. The pump itself can be replaced with wireline, so the pump seat ought to be placed where the hole is fairly straight, near the kick off point. I think it’s better to keep it simple and use triplex pumps set at the well site to get pressure up to at most 4000 psi if the casing and wellhead can stand such a pressure. Otherwise will have to power to say 2500 psi.

Anyhow, there are quite a few options but I think at very high prices we can work out something. But this will require at least several dozen wells to play around with for a couple of years.

After studying lease operating statements in 2015 and 2016, it appears to me shale stripper wells will be more risky than conventional stripper wells.

Downhole failures are much more costly. The pay being located in the lateral part of the well is an issue. Plugging and abandonment costs are much higher.

I’d take 100 1,000’ wells producing 100 BOPD over 10 15-20,000’ hz wells producing 100 BOPD, generally speaking.

I would negotiate to have the seller of marginal wells keep the P&A and surface cleanup responsibility and post a bond to make sure it will do it. We do those kind of deals with offshore property sales, so I think it’s doable if you buy say 200 horizontal wells located on pads close to each other.

Russian crude oil exports in May 2018 at 5.08 million b/day (7.33 barrels/ton)

Down -0.39 from May 2017 5.47 million b/day

Russian refinery runs increased by +0.42 million b/day in May from May last year

https://pbs.twimg.com/media/De9WKlsX4AELGQg.jpg

? ? ? ?

2018-06-05 (Argus Media) Venezuela’s state-owned PdV is considering a declaration of force majeure on some of its oil supply contracts in June unless its clients agree to accept volume reductions of up to 50pc, PdV officials tell Argus.

Would you consider this a “black swan” potential? A sudden 700k bpd drop? Recovering from that is going to take some serious money, I would guess. Money that they do not have.

At what world market price Venezuela will be able to produce bitumen oil with a profit? Until then, they are certainly doomed …

Yeah, they were eventually doomed, anyway. What I am saying is that the drop is so big it may constitute a black swan event. If it continues. In my estimate the 700k drop would offset production in the Permian this year with all the constraints. If OPEC and Russia ramp up a million, it will only compensate and add maybe 200k a day for what Venezuela and Angola lost before this month. Or production only several thousand barrels a day compared to last year with over one million barrel a day increase in demand. Plus, excess capacity gone.

They are just cutting back on what they committed to deliver, but some oil will still be coming out. Production is a bit over 1.4 mmbopd. They have to satisfy the internal market, which is very depressed as the economy is barely functioning and the number of vehicles on the road is about half of what it used to be. They also prioritize sending oil to their Cuban masters, but even that has been cut back. And they are struggling to pay the Chinese loans. But there’s a bit leftover.

I follow Pdvsa president’s Twitter, lately he’s into blaming corrupt mafias for breaking pdvsa. What he doesn’t say is that those managers were designated by Chavez and Maduro. But wait, it could get worse. We are now working to take away the regime control over Citgo and use the cash flow to help over a million refugees scattered all over the Americas. Stay tuned.

Fernando,

Could you give us your optimistic (Maduro is removed from power and a freely elected democratic government, free from Castro influence is installed) or pessimistic, output predictions for Venezuela in Dec 2020?

Dennis,

if Maduro stays and oil prices remain below $100 per barrel:

P90: 0.5 million BOPD

P50: 1.2 million BOPD

P10: 1.8 million BOPD

If Maduro falls in early 2019 after a violent conflict

P90: 0.5 million BOPD

P50: 1.4 million BOPD

P10: 1.8 million BOPD

In a case where Maduro falls there’s not enough time to swap management and make plans to really have much impact. The longer Maduro stays in power the more people flee and will be reluctant to return.

Yesterday they reported polio cases for the first time in over three decades, there’s all sorts of epidemics being covered up, AIDS patients are denied medicine and are allowed to become infection hot spots, so the problem will be refusal by qualified personnel to move into that mess. I keep reading pleas for medicine on Twitter for the simplest medicines, such as the ones for diabetics and people with high blood pressure. So the country is going on what appears a full meltdown. And the communists will never give up. They have to be forced out and that’s not going to be pretty.

Thanks Fernando,

Taking P50 we have 1.2 to 1.4 Mb/d in Dec 2020.

For the optimistic case, do you believe output might get back to 2016 levels (2 Mb/d) or possibly even higher (3 Mb/d) by Dec 2025, assuming a US or European style democracy were firmly established by Dec 2020?

There won’t be an European style democracy. Venezuela has a republic style of government with president and congress, and I suspect a new constitution would continue that tradition.

I cannot see Venezuela exceeding 2.5 mmbopd by dec 2025. And I don’t think it can reach 3 mmbopd until 2030.

By the way, I hear two upgraders are shutting down and the remaining two are expected to shut down by early July. I think we may get to see Maduro hanging from a highway overpass if things keep going this way.

How could they lose 700K bpd in one month? That’s like Iraq invasion type of numbers. I’m having a hard time understanding how that kind of production collapse could happen so quickly, and I feel like I’ve been pretty good at keeping up with the Venezuela thing.

https://www.platts.com/latest-news/oil/singapore/china-independents-look-for-other-crude-oil-grades-26969014

It’s a reality. Stephen. I am not sure. I can find no news, other than the Conoco stranglehold in the Caribbean, and that’s over. Another pure guess was that the refineries temporarily taken over by Conoco could have provided dilutants for Orinoco???? Or, have their partners finally gotten fed up with them?

https://www.platts.com/latest-news/oil/caracas-venezuela/feature-venezuela-girds-for-further-deterioration-10400558

Then the agreement may only apply to the refinery. It is not clear. Exxon/mobile is right behind Conoco, so even if it is temporary in nature, there may be more coming.

Maybe Fernando can shed some light?

Ok, found more. It is a not so temporary problem as a result of Conoco. Looks like the refinery was settled, but not everything.

https://www.reuters.com/article/us-venezuela-pdvsa-contract/venezuelas-pdvsa-mulling-force-majeure-on-oil-exports-sources-idUSKCN1J132Q

http://www.businessinsider.com/conocophillips-could-bring-deeper-trouble-to-venezuela-2018-5

My guess all this will take awhile, and they will come nowhere close to recovering to near where they left off. The ports have to be completely in shambles. And if they are not moving it, did they have to shut some in?

And Maduro had the nerve to laugh at Conoco, because they only had a 2.2 billion award. If you lose a billion a month in exports, why not just pay up? It looks like a swan, it flaps like a swan, but it is probably not a swan as it is black. Ok, maybe not normally big enough to be a full grown swan, but Permian takeaways (500k below expectations?), and Venezuela 900kbpd (adding 200 since December) production drop, at least get to qualify as swanletts, or whatever you call baby swans. Another swanlette, er think Iran, and the swanlettes qualify as a big damn black swan. I think OPEC has to take some kind of action to make it look like production increases now, though it is doubtful that they come anywhere near that. This is bound to draw attention sometime soon.

Energy news had this posted towards the end of the last post. This is taking a lot of time for people to take notice.

There seems to be too much faith in general that there are ways to quickly fix the supply problem. As we are witnessing with shale oil, the infrastructure requirements of many sorts are still there if production needs to be ramped up. When the oil industry is starved for 3+ years, there is just potential for so many surprises to the downside.

There seems to be too much faith in general that there are ways to quickly fix the supply problem.

Agreed, or maybe people know they don’t have any answers so aren’t looking too closely. Not the least problem with fixing any coming supply gap is the dramatic drop in discoveries, both oil and gas, which is certainly not just due to a lack of investment because the decline started in 2010 and has followed a pretty good exponential decay since then, even through the high price years.

…production drop, at least get to qualify as swanletts, or whatever you call baby swans.

What? You never read Hans Christian Andersen?! They’re called, ‘Ugly Ducklings’! 😉

The communist dictatorship won’t pay because there are hundreds of companies trying to recover more than $20 billion in lost properties, unpaid product deliveries, foreign exchange allocations, and others who have been ripped off by the regime.

They have 600 kbpd upgrader capacity with four flexicokers, I can’t imagine these are in great shape and without them they can’t refine the XH crude. There was a report of maintenance on one being delayed to July, but maybe it didn’t make it that far. They could all go off line eventually. Even without that problem add in shipping issues, pipeline issues, not enough new wells, workers leaving because it cost’s them more to get to work than they get paid, foreign companies not approving expenditure as they can’t be sure of payment and the whole thing could easily collapse at once.

Thanks for all this, very insightful. It’s like you wake up in the morning, have an old jalopy that’s barely getting you to work, and the battery goes out, you get fired for being late again, the landlord kicks you out because he heard you got fired and you haven’t paid rent in two months, and your wife leaves with the kids because you have nowhere to live, the cell phone company turns off your phone for nonpayment, and by the end of the day you’re living under a bridge without a dollar in your pocket.

Sounds like a pretty good country and western song, except there probably needs to be a faithful old dog in it somewhere.

Dog died.

It always does in the best songs, maybe by your own pick-up during your get away.

Or run over by a reindeer.

The upgraders are limping along, but the issue isn’t the upgraders. Their problem is more a lack of diluent, and the overall collapse of production as qualified personnel flees the country. These guys are applying communism to the max, following Cuban advice they are using high levels of repression and torture, have arrested people for refusing to break the law, and this has created a panic. Right now I’m hearing they have arrested engineers trying to leave on zero charges. So it’s getting like Cuba. A real tragedy.

I correct myself. I just heard two upgraders are in shutdown schedule, and the remaining two will shut down by early July. That takes out about 600,000 BOPD of processing capacity, which they need to offset importing light crude to make dilbit.

The Wall Street Journal has a new article about increasing oil stockpiles in China.

“China’s stores are only growing, according to the International Energy Agency, which estimates Chinese inventories by comparing the amount of crude processed in refineries and imports. In its latest monthly report, the Paris-based energy watchdog estimates Chinese crude oil stocks rose by 13.7 million barrels in March from the previous month and continued growing in April.”

People keep citing increased global demand for oil. But buying oil to save it is different than buying oil to use it. If you don’t use it, you have it to either release on the market as you choose or you have it as shortages hit elsewhere.

Chinese demand is growing strong. And with higer demand, increasing reserves is a logical step.

Additional, higher demands means more pipelines, more raffineries, more everything oil infrastructure. And this needs to be filled to some degree for working smoothly.

On the other hand the communists in China are somewhat realistic. They see all the possible supply problems very clear – and a filled storage is the best to have when some chaos happens. Best to be independend for a few months, until the shooting up prices kill enough demand to be able to start buying again.

Also…don’t think that a Strategic Petroleum Reserve (SPR) in China won’t continue to be developed. As a percentage of the population China’s SPR is still much smaller than U.S. India is just starting to develop their won SPR. Development for SPR’s will continue for many years.

Not sure if this has been posted:

http://m.miningweekly.com/article/bhp-is-said-to-get-shale-bids-valuing-unit-up-to-9bn-2018-06-06/rep_id:3861

Longer term move – Focus now on the exploding future demand for Electrical Grade Copper and the strategic metals that comes with copper mining. We may be surprised at how quickly the shale sweet spots will be fracked up.

Have a history of being unable to use the search tool on this site. Searched for Puerto just now, to find the status of the new Rosneft/China upgrade funded heavy oil refinery in Venezuela. It’s been discussed here before.

Search finds no Puerto.

Puerto means port. As far as I know there’s no new Rosneft/China funded refinery. There’s a project at the Puerto La Cruz refinery with some funding by ENI. The proyect involves construction of a unit which uses PDVSA technology to upgrade asphalt to refinable oil. The PDVSA technology was a modification of expired Veba technology with expired patents. What both ENI, PDVSA, Rosneft and the Chinese have been missing is the operational pilot documents for the unit built in Germany about 25 years ago. And even if they had, the PDVSA process involves a slight variation, therefore this Puerto La Cruz unit should be considered a pilot.

I knew the ENI Venezuela president many years ago (his daughter was an engineer I advised because she was being directed towards a shitty career outcome by one of her father’s hoitty toitty female friends who didn’t know anything about engineering but presumed to know how a young woman should develop her career). Anyway, I remember having a brief conversation with the guy and I warned him ENI was getting in serious trouble trying to help PDVSA with exotic technology piloting when PDVSA was technically incompetent, corrupt, and had its low quality management distracted trying to please Chávez with all sorts of political acts and parties.

It’s possible that ENI gave up on the project, sees that PDVSA is building a unit that’s probably going to explode within days of start up, and wants nothing to do with it. Which means PDVSA (which is losing personnel in large numbers) invited their old standbys to see if they can take over as project advisors. Whether those two decide to do it is doubtful. But if they do I anticipate the unit will probably have growing pains and will not work half the time. If it does it’ll process resid into lighter hydrogenated streams, but the volume won’t make a difference in the great scheme of things. PDVSA loses more production each month than that unit would crank out at 100% efficiency.

Look up “Puerto La Cruz Proyecto de Conversion Profunda” if you read Spanish.

Try putting this in google:

site:http://peakoilbarrel.com puerto rico

US ending stocks June 1st

Crude oil up approx +2.1 million barrels

Oil products up +6.6

Overall total, up +8.7 (shown on chart)

Natural Gas: Propane & NGPLs up +6.5 (not included in chart)

(Memorial Day in both 2017 & 2018) https://pbs.twimg.com/media/DfBt3v1WkAYBKX9.jpg

https://pbs.twimg.com/media/DfBu-UDW0AAFJk1.jpg

U.S. Petroleum Balance Sheet, Week Ending 6/1/2018

The weekly production number is now rounded to the nearest 100 kb/day

http://ir.eia.gov/wpsr/overview.pdf

Saxo Bank charts

https://pbs.twimg.com/media/DfA-g91X0AADRJK.jpg

https://pbs.twimg.com/media/DfBDwT6XkAAz3qe.jpg

We are up two million barrels a day in production from this time last year. This time last year we were up 3 million barrels total stock. 8 million is no big deal.

https://oilprice.com/Energy/Crude-Oil/Venezuelas-Oil-Meltdown-Defies-Belief.html

Most recent. Conoco definitely made an impact.

Great article find. Guym – between you and Energy News – you are crushing it with the updates and honest non-partisan analysis. Thanks from the pleb gallery.

https://www.hellenicshippingnews.com/china-end-april-fuel-stockpiles-drop-led-by-diesel-decline/

China’s demand sounds pretty healthy.

The US has not prevented the world going into decline, in fact I would say it has increased the risk of that decline happening even sooner.

US shale production has increased by an amazing over 4 million barrels a day in the last 8 years or so.

This started to impact oil prices and OPEC had the choice of reducing production to make way for increased US output. OPEC decided to do the opposite and tried to put expensive shale out of business.

What the Saudi did not bargain for is how much debt the shale companies could raise to keep on going.

https://www.rystadenergy.com/newsevents/news/newsletters/UsArchive/shale-newsletter-january-2018/

After several years of low oil prices, indebted OPEC countries realised they had to cut production or go into further debt, this they did in 2016 along with Russia.

https://www.economist.com/finance-and-economics/2016/12/03/opec-reaches-a-deal-to-cut-production

So the graph showing production decline, simply shows when the production cut agreements took effect.

The effect of the low oil prices has caused the major oil companies to make deep cuts to exploration budgets

https://www.ft.com/content/ccad0710-32b8-11e6-ad39-3fee5ffe5b5b

https://www.statista.com/statistics/654847/global-upstream-oil-industry-capex/

Shale oil companies crashed the oil price and only continued to exist by persuading investors to pile in more and more debt.

Oil companies that actually have to provide a return on investment had to cut global exploration which caused the lowest discoveries ever and will bring forward peak oil.

In a sane world, shale oil production would have grown far more slowly, meeting annual demand increases and shale oil companies would not be allowed to get into debt as they have done. Oil prices would have stayed over $100 and global exploration would have continued as it should have done.

“Oil companies that actually have to provide a return on investment had to cut global exploration which caused the lowest discoveries ever and will bring forward peak oil.

In a sane world, shale oil production would have grown far more slowly, meeting annual demand increases and shale oil companies would not be allowed to get into debt as they have done. Oil prices would have stayed over $100 and global exploration would have continued as it should have done.”

So how do you explain why discoveries took a nose dive several years before the price crash?

It’s not enough to invest in exploration. There must be oil in the ground too.

Jeff

Which year did it nose dive?

https://www.ft.com/content/441d0184-f13f-11e6-8758-6876151821a6

I don’t have a FT subscription.

https://www.iea.org/newsroom/news/2017/april/global-oil-discoveries-and-new-projects-fell-to-historic-lows-in-2016.html

Oil discoveries peaked in the 60’, annual discoveries have been less than consumption from mid-80’s onward (with one or two years exception), there was a discovery peak in 2009-2010 (offshore hurray) then it went down. Yes, 2015-> has been a disaster but you would have to go back a lot longer to find the good years.

It cost a lot more these days to find oil, we don’t find that many brl anymore and when we do the findings are smaller than they used to be. In fact, we found more oil in the 1920 than 00’ yet technology has improved quite a lot (understatement of the year). The world is finite. period.

From the article showing frontier wildcat wells: cliff – 2009, bit steeper cliff – 2015, recovery in high price years – none. It would be nice to get some kind of quantitative summary over the years for world lease sales, but I haven’t found one, but from the ones I’ve followed – UK, GoM, Brazil, Mexico, Norway, offshore Africa, Oman – there seems to have been a general tailing off which doesn’t seem to be correlated with prices at all.

There’s another chart of discoveries which is a pretty steep exponential decline fro 2010, that could be called a cliff or not depending on your view point, but discoveries are heavily stochastic while frontier exploration is budgets are wholly deterministic.

This is from IEA using, I think, Rystad numbers. The drop in discoveries is clear but so is the nutjob boom in FIDs (a result of exactly the same attitude seen in shale companies) which hoovered up many of the available projects back to discoveries in the 70s, including heavy offshore oil, high sulphur oil, ultra deep highly compartmenatilised fields, almost all simple tie-backs etc. What’s left is the real dregs or the shrinking pool of new discoveries. Even the switch to gas doesn’t look that easy as those discoveries are also drying up, though there might be more currently stranded assets to develop (but dependent on high gas prices that are not indexed to oil so much these days) – and gas can, and likely will if the price is right, be replaced by coal.

Oil discoveries have been dropping for years, during high prices and low prices. They have been dropping because there is less oil to find.

Yes oil discoveries have been falling for many years but the crash in oil prices made 2015, 2016 2017 and probably 2018 exceptionally bad.

This will have an impact in decline rates in a few years time just when shale oil is showing it’s limitations.

There is one thing the shale bangers keep overlooking as a benefit that will last for much longer than oil. Hopefully, it will help the US eventually transform into renewables without extreme pain. That is that nasty byproduct they flare now. Natural gas. It has enabled our economy to do much better as a result of lower electrical cost. It used to sell for four times the price as it is now. There is a bunch more down there.

I hope it will be used for transformation – otherwise it won’t hold for long, too.

If you substitute all coal and all oil simply with gas without thinking, a comfortable 100 years supply can shrink to a mere 30 years, too.

A nat gas- plugin hybrid vehicle would be nice one to have.

Guym

In the UK petrol prices are $6.84 a gallon and that is not enough to transition people into electric cars.

There are lots of Volkswagen cars but I have never seen a VW egolf, simply because it costs £12,000 more than a petrol one.

Also the depreciation of many electric models is horrendous.

http://www.autoexpress.co.uk/best-cars/94305/fastest-depreciating-cars-top-10-worst-motoring-money-pits

People who buy electric cars like this have simply not researched the costs.

Ok! Then why do you suppose they did this?

https://electrek.co/2018/05/04/vw-doubles-electric-vehicle-battery-contracts-billion/

VW doubles its electric vehicle battery contracts to $48 billion

https://www.youtube.com/watch?time_continue=7&v=CkdepmXzbKc

Volkswagen I.D. R Pikes Peak – Test USA

This is a quote from the first link:

“The supply of automotive grade batteries is currently extremely limited and it can be difficult for automakers, especially startups, to secure supply with manufacturers.

It’s why many are considering building their own batteries.

Volkswagen considered it too, but the company finally decided against it. Instead, they are signing those long-term contracts with manufacturers to encourage them to invest in their own production capacity in order to grow with Volkswagen electric vehicle production capacity.

While those contracts are binding at some levels, they likely include clauses based on the progression of battery technologies and cost over the next decade – something that is expected to improve dramatically.”

The European Union has a somewhat irrational set of economic and immigration policies which are slowly tearing it apart. VW is simply trying to hedge to be able to function in this irrational environment, which is likely to destroy the eu within a decade if it’s not changed.

Fred

I did not say some mugs are not buying these cars. What I said is the ones that have bought them, are shocked when they come to sell the electric car and find it is worth so little. This on top of the fact that an electric car costs about £10,000 more than the equivalent petrol model.

After 5 years and only 40,000 miles a Nissan leaf which cost £30,000 new is worth only £7,000, a loss of £4,500 per year, you got to be rich or stupid to buy one.

Probably be a lot smarter to buy a used one.

YouTube is full of videos on cheap battery rebuilds and EV car repair, so being afraid of a used BEV or PHEV/HEV is not very reasonable.

Rebuilding a Prius battery.

https://www.youtube.com/watch?v=lSwUEVx5G3U

Getting around the high cost of fixing a Tesla.

https://www.youtube.com/watch?

v=ZptvOUXBkdY&t=49s

Did you see the video of the Tesla on autopilot that killed the driver after accelerating to 71 mph as it approached a cement barrier? Looks like driver error, he allowed the autopilot to control the vehicle at high speed.

Peter- “In a sane world”

Agreed. But I’ve given up on expecting a sane world.

First time I learned it was when intruders came into our village and killed all who did not escape into the woods (this was many, many thousand years ago).

I have been reminded of it every day since.

Most tribes don’t find it hard too remind themselves, tribes like the Pomo, the Hebrews, the Inca, etc, etc.

Just more Permian frency:

With oil price round about at 45$ when you don’t have a waterproof pipeline contract, well cost gets cheaper and cheaper when we believe the papers of the companies.

https://oilprice.com/Energy/Energy-General/Hiring-Frenzy-Spurs-Wage-War-In-The-Permian.html

Paying double wages to snipe off the workers from your neighbor in spe oil baron won’t rise completion cost by anything…

There has been some discussion in our field of single workers leaving here for the Permian.

Married ones with families do not seem as keen on it, once they look into cost of housing and other factors.

US – update through February 2018 – Enno Peters

https://shaleprofile.com/index.php/2018/06/07/us-update-through-february-2018/

Do I see shale peaking in that graph similar to 2015??!!

No. US tight oil not peaking yet. Enno uses RRC data for Texas, which is incomplete for about 6 to 12 months.

EIA estimate for US tight oil through April 2018 in kb/d below.

… still a very similar pattern as in late 2014, early 2015 though. But you are certainly right that that “peak” is caused by incomplete data. Too early for drama.

Westtexasfanclub,

If we see prices cut in half like in 2014/2015, ($110/b to $55/b), for example we see Brent go from $80/b (near term peak) to $40/b, then we will probably see a near term peak in US tight oil output.

I think without a major Global recession (similar to 2008/2009 or worse), an oil price crash to $40/b in the near term is highly unlikely.

If I am correct we are likely to see a rise in US LTO output to 6.4(low oil prices under $75/b) to 8 Mb/d (higher oil prices up to $95/b by 2023) by 2023 (from 5.3 Mb/d in Dec 2017), Brent oil prices in 2017 US$.

2018 EIA Energy Conference Presentations

https://www.eia.gov/conference/2018/?src=home-f2

2018-06-04 (Trafigura) US Crude & Products Exports

Trafigura pdf on the EIA website: https://www.eia.gov/conference/2018/pdf/presentations/saad_rahim.pdf

Fuel hubs, total product stocks, monthly but with the latest weekly number shown for June

Chart on Twitter https://pbs.twimg.com/media/DfHKxWHX4AM8_EL.jpg

A question for the oil field guys. I read something about sugar being used in well cement to act as a retarder. Is this so? Is there a simple reference I can use that shows ratios, retarding times, final strengths etc? The local builders just tend to add more water if their cement starts to harden before they have used it all so I am interested in retarding the set.

NAOM

suger is kept on surface to prevent cement from setting in case you get it back. i never heard of it being added as a planned component.

Make a quart of cement and add a spoonful of corn syrup, let me know what happens. It’s cheaper than sugar.

Sugar will retard cement but there are other types of more sophistcated retarders, both organic and syntethic used at high temperature and longer wells. Suger is as mentioned most used for retarding return cement, often in together with citric acid.

if you used it in an actual structure you’d be risking a pocket of uncured concrete. Like the others have said – unless you’re about to lose your mixer, concrete pump, or hose, there’s never a really good time to use sugar. Even a smudge of sugar in a project (caught by an inspector, in a midsize and up city) would mean all the connected concrete would have to be jack-hammered out.

Unless… they don’t have enough fresh water or the temps are too hot. seems like an awful risky way to save a few bucks.

If a single horizontal well collapsed though, how big of a deal would that be? It seems like there’s a lot of branches and fairly tight spacing. Maybe the risk / reward is worth using cheap retardants.

I’ve seen a couple of things about an attempted assassination of the Saudi prince MBS on April 21, 2018. Does anyone have any idea whether this is real or bull. Link to an oilprice article follows.

https://oilprice.com/Geopolitics/Middle-East/Oil-Kingdom-In-Crisis-Saudi-Royal-Family-Rift-Turns-Violent.html

Using fingers and toes.

Do traders and analysts have a reality disconnect, or are they mathematically challenged? Before everything started to implode recently, The EIA had a slight oversupply into 2019, and the IEA had a slight undersupply heading into 2019. That was based on the US producing 1.2 to 1.3 million, and another half a million from Canada and Brazil. Common sense should tell these people that with the constraints, that expectation is far fetched. Best case scenario, I see the shortage in the US figure somewhere between 400k to 500K. Next, we have Venezuela imploding, where their expectation for June shipments will be about 700k short, and that is on top of a 200k drop they have had since the first of the year. Some of this may come back later, but it does not appear to have a solution, yet. Now, with the Iran sanctions, Europe is fighting it, but insurers and shippers are not cooperating, and most of the refineries in Europe have already cut Iran oil to zero. The largest refinery in India is also no longer purchasing Iran oil. If the US, Venezuela, and Iran can’t ship the oil, do they keep producing??? So, if OPEC ups shipments by one million, we may be still almost short that much, in my loose calculations.

Or, will they keep continuing to look at EIA weeklies to determine the status of world oil supply?

2018-06-08 Platts Oil OPEC Survey has OPEC crude output at 31.90 mbpd in May, a 13-month low, down -0.1 mbpd m/m

Table https://pbs.twimg.com/media/DfKlpwEW4AAYHSQ.jpg

Angola chart https://pbs.twimg.com/media/DfKpIwdW0AAlhgG.jpg

Venezuela chart https://pbs.twimg.com/media/DfKp62bWAAAoolt.jpg

Baker Hughes (GE) International Rig Counts for May 2018

Oil 743 down -13 month/month

Natural Gas 192 up +2 month/month

Venezuela 28 down -7 month/month

http://phx.corporate-ir.net/phoenix.zhtml?c=79687&p=irol-rigcountsintl

Baker Hughes weekly U.S. rig count, oil: +1 to 862 rigs.

Natural gas: +1 to 198

Permian: +3 to 480

Cana Woodford -3 to 73

Rising demand for middles distillates – Saudi Arabia exported a record volume in May

2018-06-08 (ClipperData) This week’s global middle distillates report examines record middle distillate exports tracked from the Kingdom over May, feeding northwest Europe’s summer demand for jet fuel, gasoil and diesel

Export chart: https://pbs.twimg.com/media/DfJbB1FW0Ac43Mw.jpg

https://twitter.com/ClipperData

Rising oil demand in Asia

The increase in imports into Asia is up nearly +5 million bpd last month versus the 2016 average

http://blog.clipperdata.com/sneak-peak-at-clipperview

Saudi Arabia – Crude Oil Exports – Seasonal – JODI

Chart https://pbs.twimg.com/media/DfM6dx0WsAET4lS.jpg

Saudi Arabia – Crude Oil Production – Seasonal – OPEC MOMR secondary sources (kb/day)

Chart https://pbs.twimg.com/media/DfM3Bq4WkAApmgB.jpg

Saudi Arabia’s production statistics – For anyone who hasn’t had time to look at the statistics for themselves. The Direct Communication number for Saudi Arabia is worth looking at because the Secondary Sources data is often revised towards it.

Chart on Twitter: https://pbs.twimg.com/media/DfPVShbW0AEJ7cr.jpg

That’s a great observation, wonder if it’s been spotted before. That means production is declining when it should be going up for local A/C power; couple that with continued stock draws, declining exports and still no news on Khurais expansion start-up – what does it all mean?

I was only looking at Saudi production because the WSJ is saying that production is rising. I guess it’s due to seasonal power demand as you said above. But I don’t know what it all means. Watching the Direct Comms numbers has been mentioned before.

2018-06-08 (WSJ) Saudis Start to Ramp Up Oil Output, Ahead of OPEC Meeting

Kingdom began producing 100,000 barrels a day more last month and plans to raise output again by at least that much, in shift from earlier plan

Oil data consultancy Kpler, meanwhile, said it was seeing an uptick in crude oil exports from the kingdom. The firm, which tracks vessels leaving Saudi ports, said it estimates Saudi boosted exports by an extra 300,000 barrels day in May.

https://www.wsj.com/articles/saudis-start-to-ramp-up-oil-output-ahead-of-opec-meeting-1528490019

I just have zero belief that Saudi Arabia has no problems with declining mature fields by now. To fully exploit Manifa was the last big positive influx for production. The most optimistic scenarios by critics a decade ago were that peak would be about now. It is not difficult to see why the more pessimistic scenarios did not occur (better mapping of reservoirs, targeting oil left behind, better recovery factor for some fields; Haradh in South Ghawar was a success for example, more oil fields found than initially mapped, successful secondary and tertiary recovery methods and not at least very efficient horizontal wells etc.) To keep a lid on detailed information can not hide what is going on for long. I suspect Saudi Aramco IPO could fail because investors are not totally morons looking into these things. Drawing from storage (150 kbpd pace according to JODI) and in addition ramping up for summer A/C requirements internally. At least 400 kbpd is needed for this according to some sources, remember some higher numbers being stated in prior years close to 1 mill b/d but there has been a lot of noice about natural gas and solar power lately; don’t know just how much A/C requirements are right now. Anyway, KSA still are supposed to have close to 1 mbpd of reserve capacity to throw into the market. They don’t have me onboard on this, but 90%+ of the market participants believe it, it seems. For now.