A post by Ovi at peakoilbarrel.

All of the oil (C + C) production data for the US state charts comes from the EIAʼs Petroleum Supply monthly PSM. After the production charts, an analysis of three EIA monthly reports that project future US production is provided. The charts below are updated to January 2020 for the 10 largest US oil producing states.

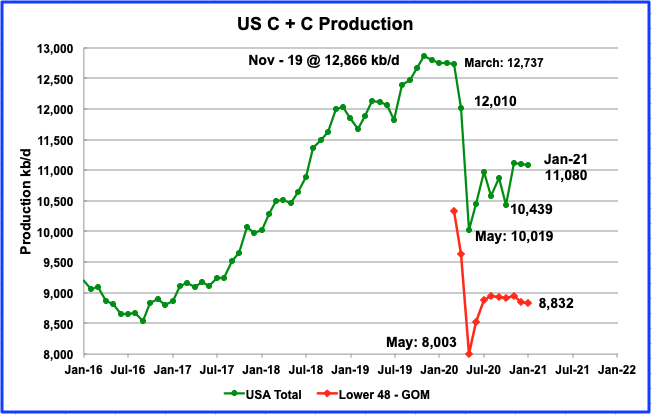

Note: This post is not an April Fool’s joke. I really am publishing the latest official EIA information available, January production in April.

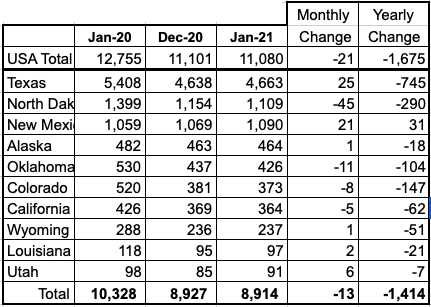

Januaryʼs U.S. production decreased by 21 kb/d to 11,080 kb/d from Decemberʼs output of 11,101 kb/d. The decrease was largely due to North Dakota’s decline while being offset partially by Texas’ and New Mexico’s increase. Note that December’s output of 11,063 kb/d in the February report was revised up by 38 kb/d to 11,101 kb/d in the current report.

Production decreased by 11 kb/d in the onshore L48, red graph.

Listed above are the 10 states with the largest US production. These 10 accounted for (80.5%) of US production out of a total production of 11,080 kb/d in January 2021.

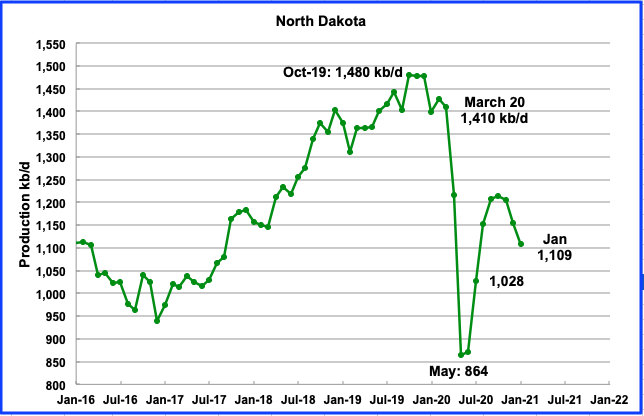

Of all these 10 states, North Dakota had the biggest percentage drop, close to 4%, relative to December and could fall behind New Mexico in production ranking next month. On a YoY basis, New Mexico was the only state that recorded an increase in January.

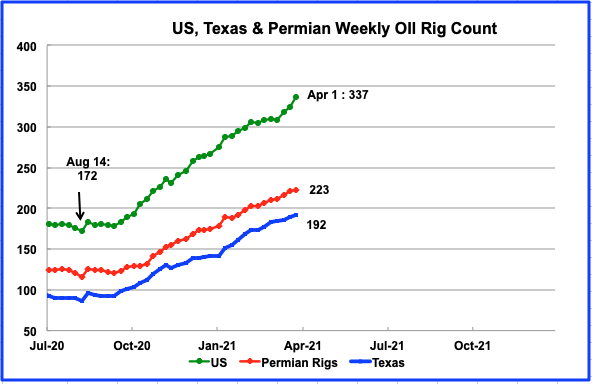

While significant rig additions continued in the US from the July and August lows of 172 to the beginning of April, there is no comparable increase in US oil output. During the week ending April 1, 13 oil rigs were added bringing the total 337.

The rate of adding rigs appears to have changed in the week of Mar 19. During February, approximately 1 rig per week was being added. On March 19, the rate increased to 9 per week. This was probably associated with the price of WTI moving above $60 in February,

Production by State

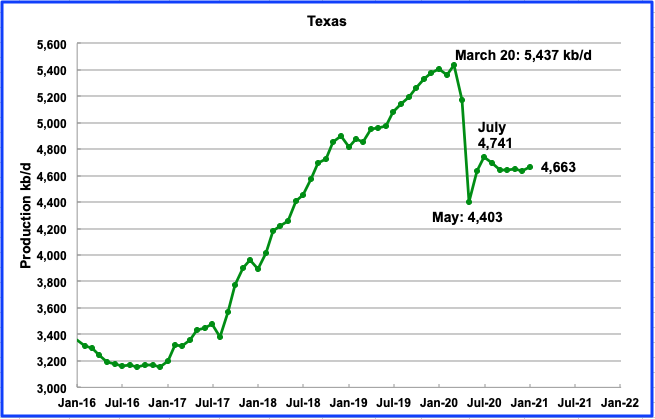

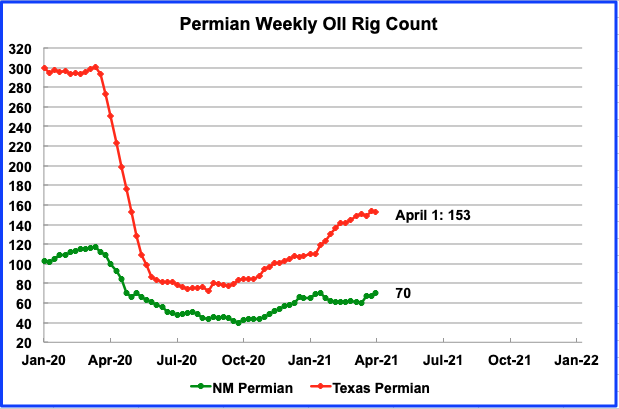

Texas production increased by 25 kb/d in January to 4,663 kb/d and still remains 78 kb/d lower than July 2020. In the meantime the number of oil rigs operating in Texas in January has gone from a low of 90 in July and August to 155 in January. There are currently 192 rigs operating in Texas in the week of April 1.

Will the increasing number of rigs in Texas be sufficient to increase production or just hold it at a steady level?

January’s output was 1,109 kb/d day, a decrease of 45 kb/d from December. North Dakota’s rig count was flat at 11 rigs in mid January. It then started to increase through February to 14 by the beginning of April.

In a recent statement, Helms noted North Dakota needs 60-70 completed new wells coming on each month to maintain production of 1.2 million b/d.” The number of wells operating in the Bakken from December to January increased by 88 from 13,579 to 13,337, respectively, according to this source and production still dropped.

New Mexico’s production increased every month from March to January except for December. Januaryʼs New Mexico production increased by 27 kb/d to 1,090 kb/d. Can New Mexico’s output increase be attributed to an increase in drilling in their part of the Permian? See next chart.

From March to September, the number of rigs operating in the NM Permian dropped from over 100 to a low of 42 in September. In the meantime oil output increased. Does this imply that DUCs were being completed during this time? After September, the oil rig count began to increase.

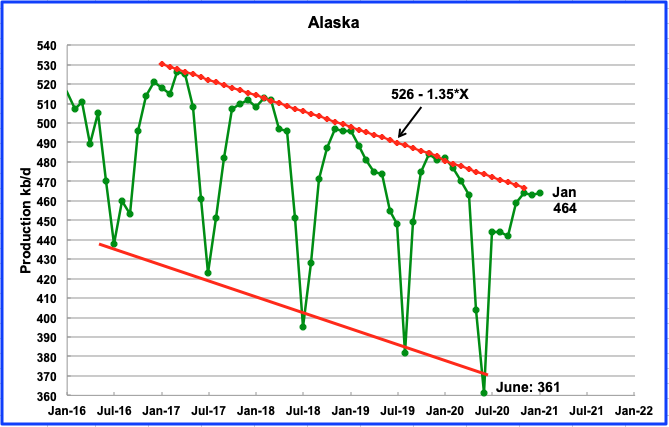

Alaskaʼs January output increased by 1 kb/d to 464 kb/d. The EIA’s weekly production report shows that output in March was closer to 450 kb/d.

According to this source, one new project, the ConocoPhillips’ GMT-2, in the National Petroleum Reserve-Alaska is on track to be completed and in production in late 2021 with a peak rate of 35,000 b/d to 40,000 b/d.

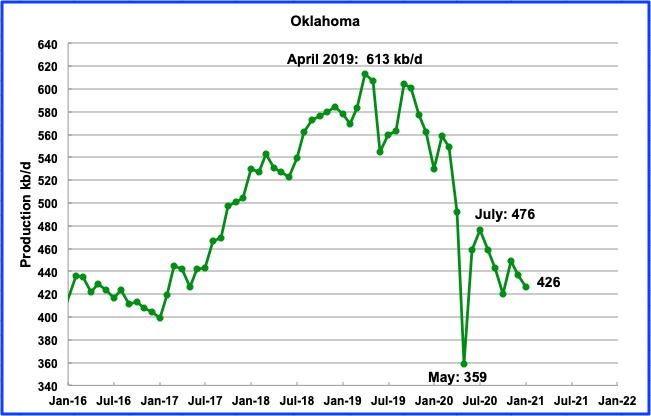

January’s output decreased by 11 kb/d to 426 kb/d. During January, 17 rigs were operating. The number fluctuated around 17, +/- 1 up to late March but in early April, 2 more were added for total of 19.

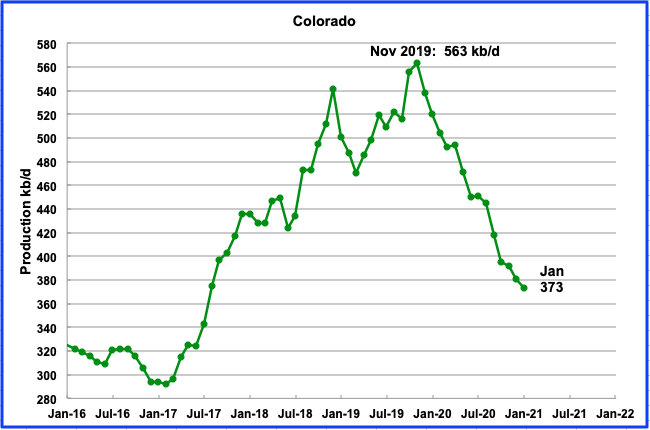

Coloradoʼs January output decreased by 11 kb/d to 373 kb/d. Colorado had 7 rigs operating from mid-January to mid-March but increased to 9 in the first week of April. Declining production continues to be associated with the pandemic and new environmental regulations, according to this source. However one company , PDC Energy, plans to submit a 500 well program for the Denver-Julesburg basin.

“PDC also does not need to rush to get new drilling permits approved as it holds an inventory of 200 drilled-but-uncompleted wells and 300 drilling permits for new wells in Weld County, the core of the DJ Basin.”

“Internal rates of returns in US shale basins, both crude and gas focused, look much more appealing in recent weeks with around $60/b oil at WTI and nearly $3/MMBtu at the Henry Hub. The DJ has jumped to 22% IRRs in the current pricing environment, according to S&P Global Platts Analytics.”

“IRRs of at least 10% is the threshold typically needed to encourage operators to bring new wells online. Platts Analytics IRRs are based on a half-cycle, after federal corporate tax analysis, which excludes sunk costs such as acreage acquisition, seismic and appraisal drilling.”

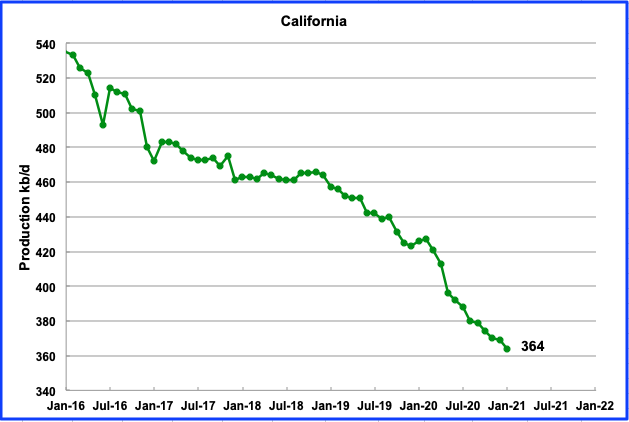

Californiaʼs slow output decline continued in January. Its production dropped by 5 kb/d to 364 kb/d. From May 2020, output has dropped by 32 kb/d for an average of 4 kb/d/mth.

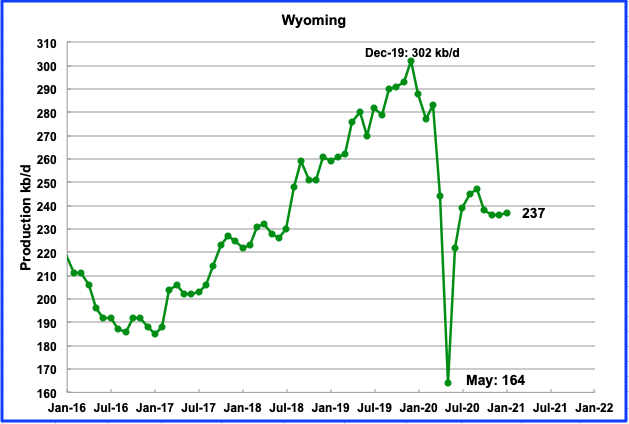

Wyomingʼs production in January increased by 1 kb/d to 237 kb/d. Wyoming had 3 oil rigs operating in January and they were increased to 4 in February through to the beginning of April. Wyoming’s oil production appears to be stabilizing around 240 kb/d.

“Wyoming is one of thirteen states suing the Biden administration Wednesday (March 31) to end a suspension of new oil and gas leases on federal land and water and to reschedule canceled sales of leases in the Gulf of Mexico, Alaska waters and western states.“

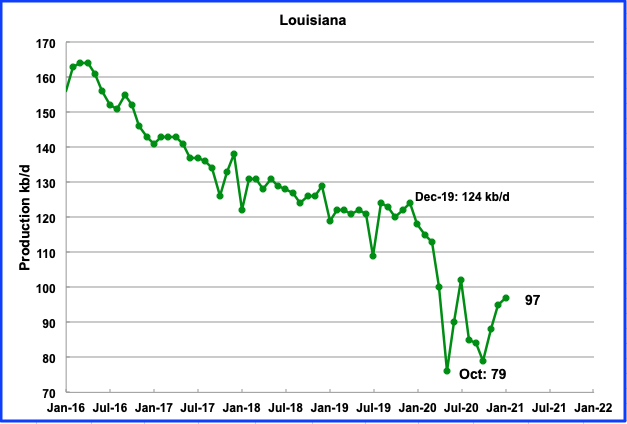

Louisianaʼs output increased by 2 kb/d in January to 97 kb/d. In January, Louisiana had on average 17 rigs operating. However more recently the number declined to 14 in early April.

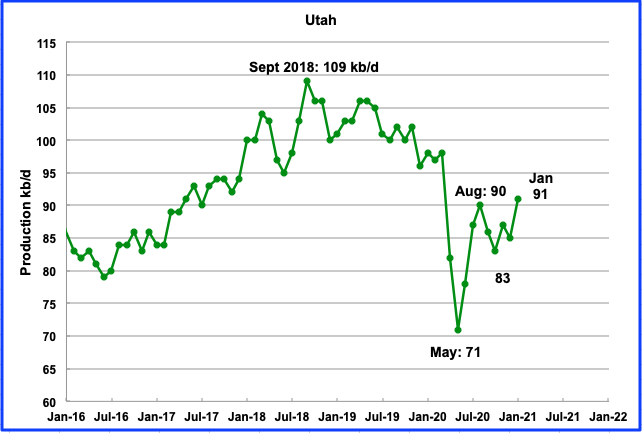

January production increased by 6 kb/d to 91 kb/d. Three oil rigs were operational from January to mid-March. However by the first week of April, they had doubled to 6.

Utah joined 12 other states Wednesday (March 31) in a lawsuit against the federal government challenging the Jan. 27 executive order issued by President Joe Biden to ban any new oil and gas leasing on federal land and offshore waters.

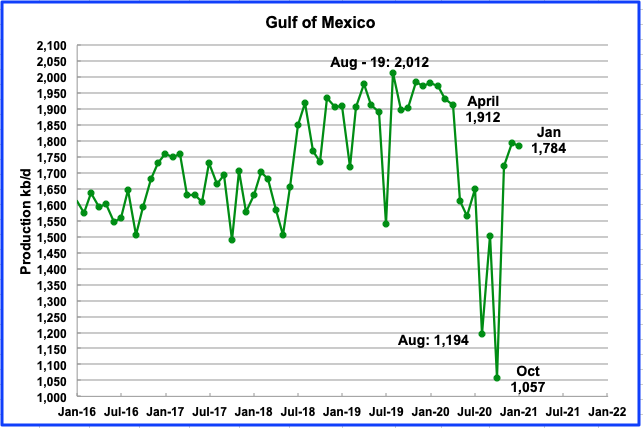

Production from the GOM dropped in January to 1,784 kb/d, a decrease of 11 kb/d. If the GOM were a state, its production would rank second behind Texas.

UPDATING EIA’S THREE OIL GROWTH PROJECTIONS

1) SHORT TERM ENERGY OUTLOOK (STEO)

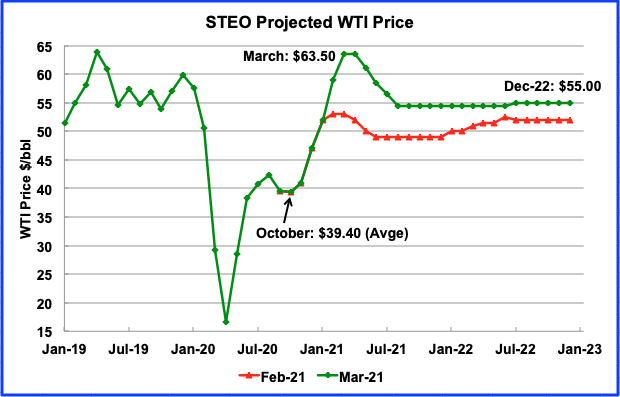

The STEO provides projections for the next 13 – 24 months for US C + C and NGPLs production. The March 2021 report presents EIAʼs updated oil output and price projections to December 2022.

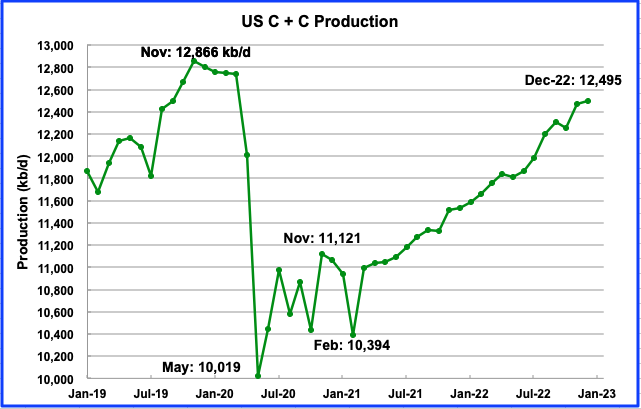

According to the STEO, US output is projected to increase in March 2021 after recovering from the February low of 10,394 kb/d. Starting in June 2021, the average projected rate of increase is expected to be close to 70 kb/d/mth. This larger rate increase was not projected in the February report and can be attributed to the projected price increase for WTI.

The STEO’s January oil output projection of 10,942 kb/d does not compare well with the actual production which was reported as 11,080 kb/d in the first chart above. In general, the EIA appears to under estimate forward production since most production revisions are increases.

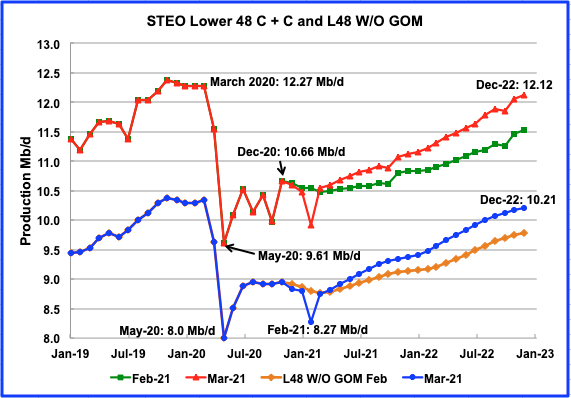

The March STEO output projection for the L48 states is dramatically higher from the one provided in the February. The projection reflects the current new higher WTI price environment. The EIA is now projecting a significant increase in production in the L48 starting in March 2021. From March 2021 to December 2022, the US will add 1.57 Mb/d, going from a daily production rate of 10.55 Mb/d to 12.12 Mb/d.

In the onshore L48, L48 W/O GOM, production starts to increase in March 2021 from 8.75 Mb/d to 10.21 Mb/d in December 2022, an increase of 1.46 Mb/d. The average monthly increase in production rate is 76.8 kb/d/mth.

How much will the drillers/companies have to ramp up their drilling activity to achieve this production rate. Maybe the EIA’s model, based on pricing, indicates a significant increase in drilling activity and output. However, the issue that remains is “Will the company management allow increased production or will they just hold back to let oil prices strengthen.

It should be noted that the rate at which rigs have been added since March 18, has increased to 9 rigs per week. Throughout February, roughly 1 rig per week was being added. This could be related to the price of WTI moving above $60/b in February.

The 2021 STEO is projecting a WTI price of $63.50/bbl through March/April 2021 before beginning to decline back to $55/b in August, a $5.50 increase over the previous February report.

The May WTI contract settled at $61.45/bbl on April 1, $2 lower than the EIA projection.

To support oil prices close to $60/b, OPEC + on April 1 announced it would cautiously increase production quotas.

“The 23-nation coalition will boost output by 350,000 barrels a day in May, add the same volume again in June and increase by 450,000 barrels a day in July, Prince Abdulaziz told reporters after the meeting. On top of that, Saudi Arabia will roll back its voluntary extra 1 million barrel-a day cut, adding 250,000 barrels a day in May, 350,000 in June and 400,000 in July, he said.”

2) DRILLING PRODUCTIVITY REPORT

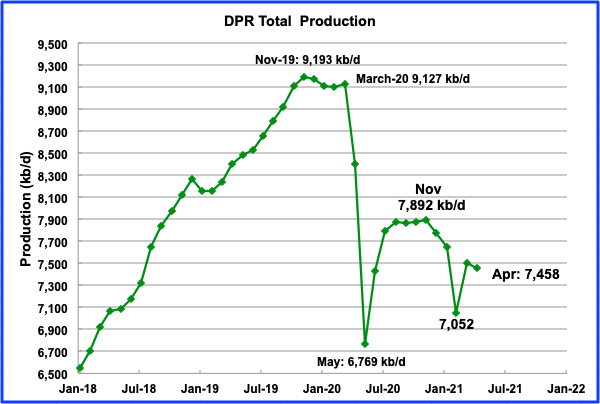

The Drilling Productivity Report (DPR) uses recent data on the total number of drilling rigs in operation along with estimates of drilling productivity and estimated changes in production from existing oil wells to provide estimated changes in oil production for the principal tight oil regions. The following charts are updated to April 2021.

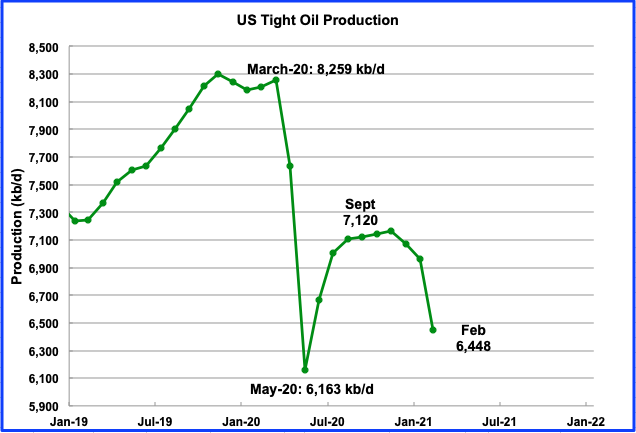

Above is the total oil production from the 7 basins that the DPR tracks. Note that the DPR production includes both LTO oil and oil from conventional fields.

After bottoming in May at 6,769 kb/d, production rose rapidly to November to 7,892 kb/d primarily by reopening shut in wells. However after November, drilling levels have not been sufficient to offset decline. The DPR is projecting output for April 2021 to be 7,458 kb/d, up 406 kb/d from February’s snow storm induced drop.

Ignoring the February drop, the average decline rate since November has been close to 86.8 kb/d/mth. In the L48, close to 337 oil rigs are operating in the first week of April and these are projected to not be sufficient to increase LTO and conventional production in the seven DPR basins.

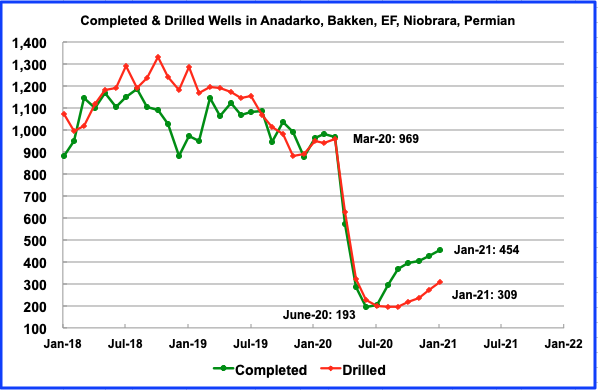

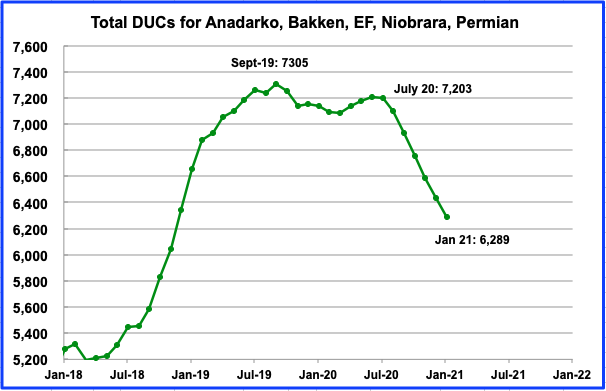

This chart shows that more wells have been completed than drilled in the DPR basins since July. It also indicates that the number of DUCs is falling and drillers are trying to reduce their costs.

The total number of DUCs began to decline in August 2020. Since then, 914 DUCs have been completed. On average 152 DUCs have been completed every month since July. It is not clear from the DPR data whether the completions include both oil and gas wells.

The oil contribution from three of the DPR/LTO basins is shown in the charts below.

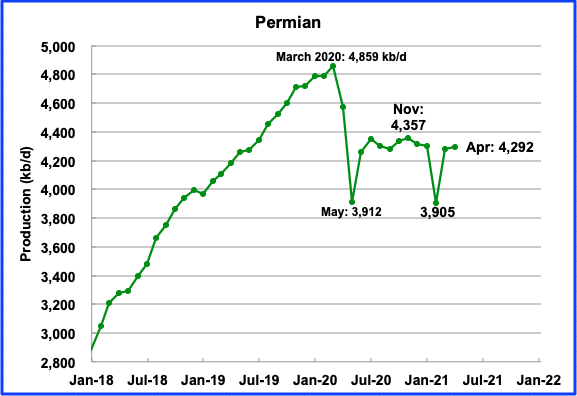

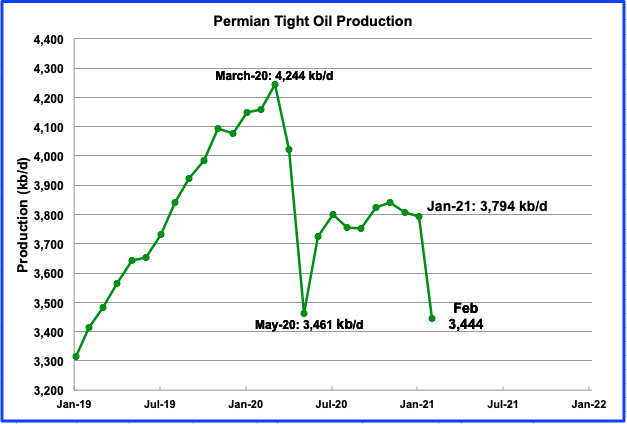

Permian output in April 2021 is projected to be 4,292 kb/d, up by 11 kb/d from March. The affects of the February winter snow storm show up in the the February drop of 396 kb/d from January to 3,905 kb/d.

In the week of March 12, 211 rigs were operating in the Permian, up from 100 in November. These 211 rigs appear to be sufficient to offset the decline from older wells since production is essentially showing no growth or decline. In the first week of April, the number of operating oil rigs had increased to 223.

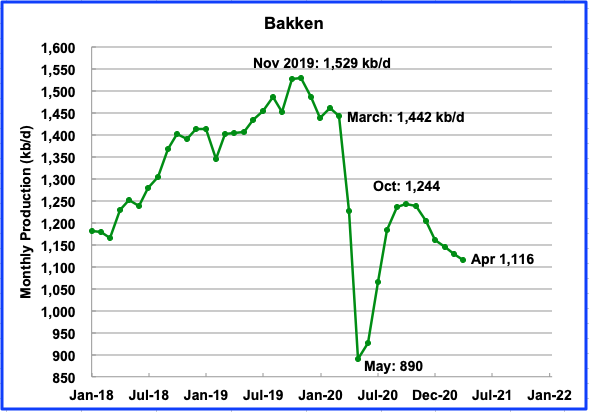

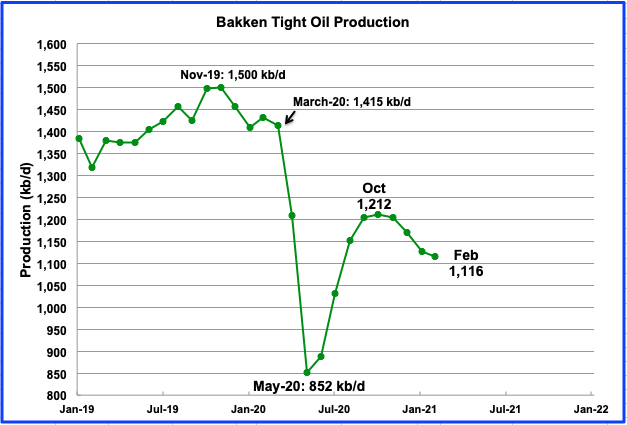

Bakken output in April is projected to be 1,116 kb/d a decrease of 12 kb/d from March.

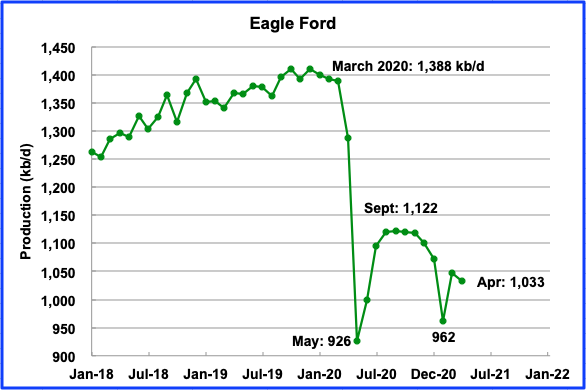

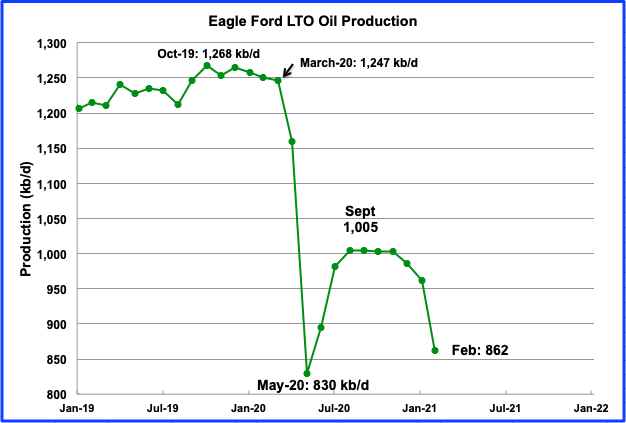

After bottoming in May, Eagle Fordʼs output reached a recent peak in September and then began to roll over. In April, Eagle Ford’s output is projected to drop by 15 kb/d to 1,033 kb/d. Note that March’s output in the February DPR was revised up by 39 kb/d to 1,048 kb/d in the current report.

3) LIGHT TIGHT OIL (LTO) REPORT

The LTO database provides information on LTO production from seven tight oil basins and a few smaller ones. The March report projects the tight oil production to February 2021.

Februaryʼs LTO output is expected to decrease by 512 kb/d to 6,448 kb/d due to the severe winter snow storm that hit Texas and New Mexico in February.

Permian LTO output in February is projected to be 3,444 kb/d, a decrease of 350 kb/d from January due to the severe winter snow storm that hit Texas. There were 187 oil rigs operating in the Permian in January. By comparing December and January production, it appears that 187 rigs are not sufficient to keep up with the decline.

The Bakkenʼs February output is projected to continue to decline after the recent peak was reached in October. February production dropped by 12 kb/d to 1,116 kb/d. In December and January, close to 11 rigs were operational and they increased to 14 in February.

The Eagle Ford basin is expected to produce 862 kb/d in February a decrease of 99 kb/d from January. EF output was also impacted by the severe winter snow storm that hit Texas.

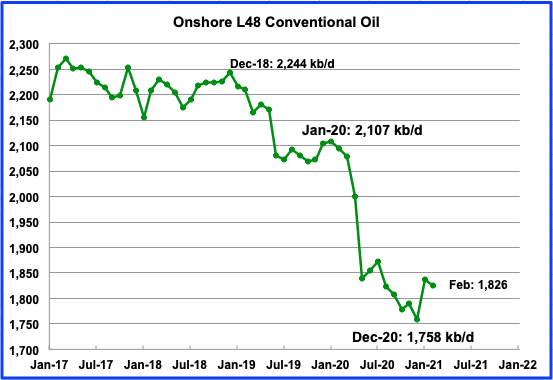

Conventional oil output in the On-shore L-48 is expected to drop by 11 kb/d to 1,826 kb/d in February 2021. This estimate is based on a combination of the March LTO report and the STEO March report that projects US on shore L48 to February.

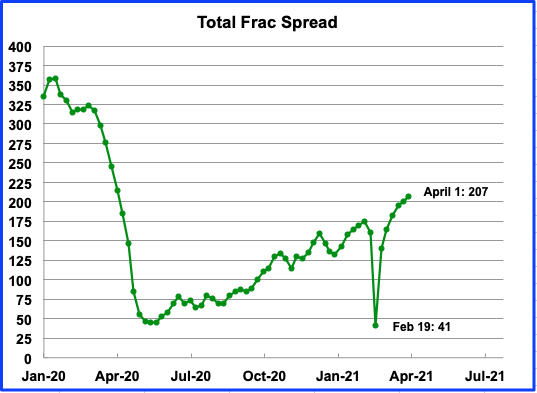

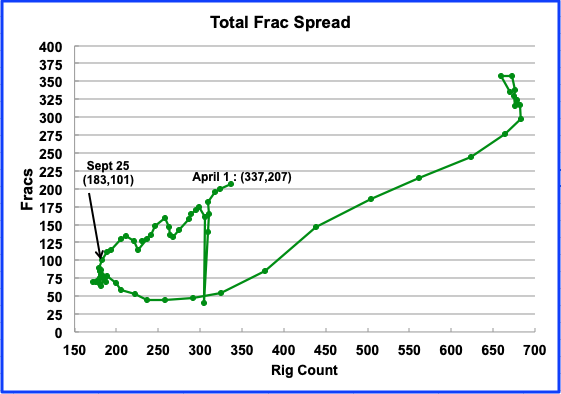

Fracs and Rigs

At the end of May 2020, 45 frac crews were active. In March 2021, 195 were active. Over the 10 months, 150 frac crews were added or 10 per month.

This chart relates the weekly oil rig count with frac spreads. Currently the relationship between frac spreads and rigs is on a different trajectory than earlier last year. From Sept 25 to April 1, roughly two frac spreads were added for every three rigs.

118 responses to “US January Oil Production Continues Slow Slide”

Thanks Ovi,

You’re work is much appreciated.

Schinzy

Thanks. Much appreciated.

Pretty dry stuff.

Ovi , ” Pretty dry stuff ” . Please don’t be apologetic . You are doing terrific . Kudos and keep guiding us . Appreciated .

Ovi,

For the first time ever, I agree 100% with hole in head. 🙂

Great job, thank you.

Comment on last chart of post.

The upper right part of the chart has “normal” rig to frac spread ratio of about 2 rigs per frac spread, pre- pandemic. Most of the data on the down slope to the minimum was during the worst parts of the pandemic and may not be representative of “normal” rig to frac spread ratios.

As excess DUC inventory gets completed we will may see a return to normal levels of rigs to frac spreads, though “normal” can change as the efficiency of drilling rigs and frac spreads might change at different rates. If service companies start to replace older diesel powered frac spreads with e-frac fleets, we might see a rise in the rate of frac fleet efficiency improvement relative to drilling rigs (this would be measured in feet drilled per week for rigs and in wells completed per week for frac spreads.

In short, “normal” will always be a moving target.

Venezuela and Russia Ramp up Economic Ties with 10-Year Plan

https://venezuelanalysis.com/news/15163

The current government is not going away.

We shall see what emerges with production.

So here we are. Maduro remains in power. If we had believed American Media 2 years ago the entire population would have starved by now. Doesn’t seem to have happened.

As money loses its meaning, so will sanctions.

Ah yes, the awesome power of sanctions: North Korea is estimated to have enough fissile material for about 90 nuclear bombs (and counting).

NORTH KOREA’S TACTICAL NUCLEAR WEAPONS EXPAND

“North Korea appears to be well on its way to becoming a mature nuclear state despite longstanding United Nations sanctions, after Pyongyang’s tests in late March of cruise and ballistic missiles capable of carrying tactical nuclear warheads.”

https://www.aljazeera.com/news/2021/4/3/north-korea-expanding-and-enhancing-its-weaponry

What is the link with oil production?

JFF

In the second line of the post click on PSM. It is the link to the source. In the upper left click on the menu to get monthly- thousand barrels per day. The default is “Monthly -Thousands barrels

Oh, thank you. But I wasn’t thinking to this. Actually, I didn’t understand the link between the fact that NK has enough fissile materials to make 90 atomic bombs and the production of oil in USA.

HT , Venezuela is so far down the tube as far as oil production is concerned that any return is a ” pie in the sky ” . Russians + Chinese + Tom ,Dick and Harry can’t put Humpty Dumpty back again .

Agree—

With the attempted coup of Chavez, they are very cautious of turning over anything again to foreign powers.

I’ve never been– but was in Colombia for quite a while.

Many comrades have spent time there.

Many here are much more knowledgeable of the situation than I am.

Consolidation continues in the Permian. Pioneer CEO Sheffield has stated repeatedly recently that the goal is free cash flow now and not growth at all costs. As smaller producers continue to get marginalized, rapid production increases in tight oil are likely a thing of the past. Most likely a good thing for everyone.

https://www.msn.com/en-us/money/news/fracking-titan-is-bulking-up-with-dollar64-billion-acquisition-as-oil-prices-recover/ar-BB1ffqwP

Stephen,

I would say bigger fish swallowing smaller fish with rising prices is a recipe for higher output.

In other words I interpret that article in exactly the opposite way that you interpret it.

Dennis.

Why do you think that?

Shallow sand,

Following quote from article suggests higher output to me.

“DoublePoint has amassed an impressive, high quality footprint in the Midland Basin,” the eastern part of the Permian Basin, Pioneer CEO Scott Sheffield said in a statement, adding that the deal “will complement our unmatched position in the core of the Permian Basin.”

The deal will give Pioneer access to about 97,000 contiguous net acres of mostly undrilled land, bringing Pioneer’s total position to more than 1 million net acres, the company said.

It expects the new acreage to be producing around 100,000 barrels of oil daily by late in the second quarter.

In general if poorly run oil companies are acquired by well run oil companies, the resources are likely to be produced at lower cost and higher profit.

The key is higher oil prices, if they remain low, less oil will be produced profitably and if oil prices rise more oil may be produced profitably.

I expect WTI may be at $70/bo by October 2021. As you know I am wrong on oil prices about 100% of the time. 🙂

SS, $ 6.4 billion is no small change . How did they finance this ? Junk bonds at 6-7 % ? There is a line at the end of the article but that is above my pay scale .

Dennis , not all buyouts and mergers are successful . Often then not they are flops . Example Times Warner ,AOL, CNN . I can prepare a list of failed buyouts and mergers to confirm my statement .

So they only needed $1B in cash to complete the deal apparently. The bulk will financed through share dilution.

And no junk bonds required. They issued notes in January for the Parsley deal at rates from .75% to 2.15%. They appear to agree with many others: if you can borrow money for a percent or two, why not buy some stuff?

Shallow,

Pioneer first acquired Parsley and now Double Point (Double Eagle) for one thing… and one thing only… UNDEVELOPED NET ACRES.

Pioneer has BLOWN through 91% of their Net Acreage with only 65,000 net undeveloped acres remaining, they were forced to acquire companies with UNDEVELOPED acres or DIE. How do you continue growing production with only 9% of your net undeveloped acreage remaining??

Pioneer bought some time with more debt. Thus, the Shale Ponzi continues.

Steve

Duanex and Steve , thanks for shedding light on the buyout .

Dennis

This is what intrigued me.

“It expects the new acreage to be producing around 100,000 barrels of oil daily by late in the second quarter.”

The IP of 2020 Permian wells are coming in close to 800 b/d. That means they have to bring on at least 125 wells, probably closer to 150 to get to 100 k/d by end June.

Any idea on what it will take to do this in terms of rigs and wells. If their second qtr ends on June 30, they need to bring on line an average of 1 1/2 wells each day. Sounds challenging.

Scott Sheffield’s words are the speech of a street entertainer of fair.

Ovi,

The average for all new Permian wells is about 800 bo/d, EOG average Permian wells come in at 1436 bo/d, Pioneer around 960 bo/d (average wells for these companies), Devon around 990 bo/d. There is a lot of variation so if Pioneer meets its average it would need about 100 wells, I don’t know how many rigs and completion crews it has and often CEOs overstate things. Most months in 2020 Pioneer completed 20 to 30 wells in the Permian basin, so if they complete 30 wells each month of the second quarter that would be 90 wells times 960 barrels per day per well for about 86 kb/d.

On re-reading Stephen Hren’s comment, I think I understand.

If we focus on rapid increase in production, I would agree, larger companies may ramp up output in a more gradual manner than smaller companies. My focus was on companies having financial resources and potential access to capital, some smaller companies that have become overextended will stop producing all together as they become bankrupt.

My thinking was that larger, stronger well run oil companies might buy up resources and eventually develop those resources which would lead to higher output than resources that remain undeveloped.

I agree that the rate of increase in output in percentage terms is likely to decrease in the future relative to 2018 when annual tight oil output in the Permian basin increased by 54% above the 2017 level, by 2019 this had fallen to 31% and in 2020 to 4%. My Permian model (recent version) has Permian output increasing at a maximum future annual rate of 11% in 2023 with a gradual decline to a 2% annual rate of increase in 2027 and falling to zero in 2033 followed by declining output.

Mike S has the future of the Permian with a different angle and some humor also .

https://www.oilystuffblog.com/single-post/back-to-the-future?postId=606861b3ae30670015999919

hole in head,

Obviously Mike’s post is a spoof and I agree funny.

My scenario is intended to be serious, all debt paid back by the end of 2023 and wells financed from cash flow after that. Peak output is 5700 kb/d in 2032, total horizontal wells completed 180,000 with the last well completed in 2050, total tight oil produced from Jan 2010 to December 2079 is 63 Gb (mean USGS TRR is 75 Gb).

Dennis , Mike’s post is reality laced with sarcastic humor . However it is good to learn that he has a ” not always serious” side to his personality . Regarding your scenario , all I can say (as you do) we will see . 😉

hole in head,

For a low price scenario (maximum Brent oil price of $56/bo after 2019 in 2019 US$) with an assumed maximum completion rate in Permian basin of 400 new wells per month (2024 to 2032) with a gradual ramp from 350 wells per month in March 2023 to 400 completions per month in Dec 2023 and with completions decreasing to zero in June 2039, we get chart below.

Doubt it would be lower than this.

For all US tight oil using the low price Permian scenario above and a low price scenario for the rest of US tight oil we do not return to previous peak, the secondary tight oil peak is in early 2027 at about 7220 kbo/d. URR for this low price US tight oil scenario is 66 Gb.

Click on chart for larger view,

This chart, and comment, however, is MUCH funnier than my spoof. In my shop we think an RRR of 90% or so (production to stay flat in 2021) will require the Permian be cash flow neutral for the entire year. That leaves just two years, in this, this, scenario, above, to pay down $120B of deployed capital, expenditures over cash flow, the Permian has made in the past six years, or drug with it to the Permian from other failures in other basins. That’s public debt, data we can see…private debt we believe is way more.

These sort of generalizations are meaningless and do NOT serve the people of America well. People deserve to know the truth about their hydrocarbon future and THIS is not it. The truth is better left to people IN the oil business, that understand the ramifications of declining PDP and where the money has to come from in the future for oil production in America not to drop like a ship anchor dropped in the open ocean.

The last consolidation has no relevance in the big picture whatsoever, that is two sisters in law swapping spit. It means nothing. DE was stressed; they went as far as they could on borrowed money and that was all she wrote. Lawn balling is more productive than analyzing anything that happens in the Permian right now.

Mike,

Glad to make you laugh. Hope the higher oil prices of late are good for you and shallow sand.

For the “low tight oil scenario above”, the oil price scenario used is below. WTI would be about $5/bo lower.

The model focuses on Permian basin as far as debt etc, and assumes no debt in Jan 2010 (start of model). Well cost in 2019 $ is assumed to be 10 million (full cycle) for the average well throughout the model (2010 to 2033 while new tight oil wells are drilled and completed). I use the estimates you have given in the past for OPEX, royalties, taxes, etc, assume annual interest rates on debt of 7.5% and assume an annual discount rate of 10%. A discounted cash flow model is used where it is assumed that the discounted net revenue over the life of the well (for the oil price scenario assumed below) must be positive for a new well to be completed after Jan 2020 (previous completions are based on historical output data and average well data from shaleprofile.com. The average well for December 2019 is assumed to have an EUR of 420 kbo and this decreases over time based on number of wells completed. For the low price model the EUR of final wells completed in May 2039 is 353 kbo, with a gradual reduction over time (right axis chart below). Maximum monthly completion rate is 400 new wells per month after Jan 2021 starting in Dec 2023 and ending Jan 2033. Total wells completed from Jan 2010 to May 2033 for scenario is 105,700.

What is your expectation for future US tight oil output (or just Texas tight oil output)?

Chart is small, click on it for bigger chart.

Dennis.

It might help if all here do some more reading about the Double Point deal.

What I have read is that the assets already are producing 100,000. I note the articles say barrels, I suspect BOEPD.

Double Point is owned partly by Double Eagle, which is owned by two younger guys (39) who were teammates on the Texas Tech football team. They have made a fortune leasing acreage and then selling it. They started doing that in 2009.

There are also quotes from the Double Eagle owners indicating they intend on keeping their PXD stock because they will be working with PXD to further develop the acreage, and also because they like PXD’s announced “variable dividend” policy. There is also discussion from them about a disciplined strategy to develop the acreage.

Double Eagle is backed by more than one large private equity firm.

The deal values the flowing production at about $30K per BOEPD (again I am assuming BOEPD, articles say barrels) and the undrilled acreage at about $40K per acre. Per the reports, both of these numbers are on the high end. I suspect the 100K BOEPD is mostly of the high decline variety.

I looked at shaleprofile and found Double Eagle is an operator of 167 wells in the Permian as of December, 2020 with gross production of 52K BOPD. 88 of the wells were completed in 2020, and the remainder were almost all completed in 2019. Production from pre-2019 wells was negligible.

I doubt that PXD completes wells any more aggressively on this acreage than Double Eagle did in 2019 and 2020.

To add:

I assume the ultimate goal of PXD is to sell to CVX or XOM. I suspect CVX is the preferred company, but hard to say. Seems CVX has most of its shale assets on the TX side of the Permian, as does PXD.

Likely much of the motivation for this deal, IMO.

Shallow sand,

As usual, you know much more than me. Perhaps this will lead to a slower ramp in Permian output.

My model has Permian output increasing by about 200 kbo/d in 2021 and by about 400 kbo/d in 2022. Completions rise from 350 per month in early 2021 to 460 per month by the end of 2022 (this is close to the level in March 2020).

Dennis, in your answer to Mike there are too many assumptions and in my opinion all of them have very weak or no legs to stand on . If the basic hypothesis is incorrect then the final answer will also be incorrect . I stand by my assessment that USA will never touch 13 mbpd again . This year maximum will be 11 mbpd +/- 10 % . In 2022 will be much lower ,WAG is between 9.5-10 mbpd . This is total US production ,most of the decline will come from shale plays .

hole in head,

Frac spread count continues to increase so the increase in Permian completion rate is likely if oil prices hold.

Note that my model has US output lower in 2022 than in 2021 as well.

As far as accurate assumptions about the future, none exist. Possible futures are infinite, chances of choosing the correct one are exactly zero. This is basic statistics.

My tight oil model below, over the short term.

Another article on Pioneer/Doublepoint merger.

https://www.naturalgasintel.com/pioneer-natural-building-permian-midland-stronghold-with-6-4b-doublepoint-deal/

Dennis. This is an informative article and does state the 100K production is BOE.

Also, note PXD will drop rigs on the acreage from 7 to 5 and reduce activity by 30%.

My reading indicates much of the increased activity in the Permian Basin is by private companies like Double Point.

It would seem to me consolidation would result in less or flat activity, not more, based upon the stated narratives of the large public companies, being lower CAPEX and return of cash to shareholders.

It would be interesting to see the current rig counts and frac spread counts of each company in the Permian, as well as which have added since the “COVID crash.”

I continue to think PXD is for sale. Just not sure if it can get one of the majors to pay a premium.

shallow sand,

Yes you may well be correct. I was thinking Pioneer was buying a distressed company on my initial assessment, clearly that is not the case.

Output from Double eagle and Pioneer in Permian in chart below from

https://shaleprofile.com/blog/permian/permian-update-through-december-2020/

shallow sand,

My Permian scenario is fairly conservative over the 2021 to 2022 period. In chart below note the small rate of increase in Permian output from Jan 2021 to Dec 2022 (610 kbo/d increase) and compare with Jan 2018 to December 2019 (output increase of 1662 kbo/d). In other words, the projected 2021-2022 increase is about 37% of the increase in 2018-2019.

top 10 operators in Permian (in terms of oil output), chart from shaleprofile.com.

Note that Permian output as reported by shale profile was 4252 kbo/d in March 2020 and was 3653 kbo/d in December 2020.

It seems the large producers aren’t doing (as a group) what they claim in terms of limiting output, based on chart below.

Hi Dennis,

note that COP production includes Concho since the merger.

To anyone who can answer . Which of these 10 companies make profit out of ” pure ” shale operations ? Any idea ?

Hole in head,

EOG

See

https://finance.yahoo.com/quote/EOG/financials?p=EOG

2020 was a bad year, but net income from 2017 to 2020 (4 years) was 8.1 billion.

Dennis.

I think you need to adjust not only for the COP Concho merger, but also PXD Parsely?

Can you post a chart including those two both pre and post merger?

Or is that accounted for. For example, seems COP had a huge boost, which I assume is adding in Concho.

For that matter, since the graphic goes back many years, would need to adjust for many acquisitions and mergers.

Shallow sand,

I will try to get to it at some point, the steep increases reflect the mergers, so including Parsley and Concho would correct the top operator chart.

chart with parsley and concho included with 10 top operators.

This recasting of the graph is MUCH more meaningful for me.

Jay Woods,

I agree, the earlier chart was missing the Parsley and Concho mergers with larger companies, including them gives a more accurate picture. Thanks for the suggestion shallow sand and Toby.

Is anyone else watching the Ukraine situation.

https://www.voanews.com/europe/ukraine-russia-massing-troops-border-us-warns-moscow

Lightsout , yes I am being in Europe . Here the public is unaware as the media is silent . Have not seen any coverage on TV or newspapers . 99.9% of the population here in the Benelux is blank . Maybe the Baltics, Poland etc are worried . All is about Covid wave and lockdowns for the moment . I suggest you visit Gail’s blog and you will find very interesting comments on this topic .

They appear to be moving an awful lot of military hardware around on trains. Could be testing the political response but not sure Ukraine is a strategic prize. It could be Putin’s last throw of the dice, if their production is on the verge of collapse it will be hard for his methods of persuasion to continue.

You are wrong, because the Western press is not a free, independent media, but a biased system reflecting government policy, a brainwashing machine.

Specifically, according to the situation: Russia is demonstratively increasing its military grouping on the border with Ukraine in order to avoid the Ukrainian military operation, before that long ago Ukraine had increased its grouping in the east by 3 times, bought a lot of ammunition and military equipment, Turkish drones are arriving in large quantities. I think they are preparing the Karabakh option The government of the Russian Federation is deliberately warning against this.

Western media – give false information – do not notice the facts of compromising Ukrainian fascists. For example, they rarely write about civilian and military losses in the eastern republics of Ukraine. And always about losses in the Armed Forces of Ukraine.

You are wrong, because the Western press is not a free, independent media, but a biased system reflecting government policy, a brainwashing machine.

Bullshit! Only Fox news ever reflected government policy. But their fascist ideologue is now gone. Now there is no one to cheer on Putin and his corrupt government.

Why do some people feel free to blame the press for everything. The press is just a bunch of people, all with different ideas. They attack each other with a vengeance. To say that they are all following orders from the government is just stupid. Sounds like something Qnon would spout.

Not this way.

“The press is just a bunch of people, all with different ideas.”

—-

No. The owner of the press gives direction to the management what policy should be pursued. The management leads the selection and has authors whose political views they like. This is self-censorship. Nothing needs to be ordered. The correspondents know what is required of them.

Example: The armed forces of the Georgian Republic on 08.08.2008 suddenly attacked their autonomous region-South Ossetia with Rocket Artillery on the city blocks.

There were also peacekeeping forces: a battalion of Russian peacekeepers (without heavy weapons) and a battalion of Georgian peacekeepers. The Georgian battalion secretly left.

Rossiyskiy was fired upon by artillery. It would take a long time to describe the events in detail. Therefore, I will write that the media only voiced the Georgian version. And this is always the case.

I agree that the government of the Russian Federation is corrupt, but while the government of the alcoholic Yeltsin was even more corrupt, they did not notice this and treated him better.

—

“Why do some people feel free to blame the press for everything. The press is just a bunch of people, all with different ideas. They attack each other with a vengeance. To say that they are all following orders from the government is just stupid . Sounds like something Qnon would spout. ”

____

Of course so. But this is a specially selected group, selected by the leadership. They know what the leadership wants from them. They know the mood in society. On some issues they can say whatever they want, on others they understand that it is punishable …

No. The owner of the press gives direction to the management what policy should be pursued. The management leads the selection and has authors whose political views they like. This is self-censorship. Nothing needs to be ordered.

No, no, no, you seem to think that the entire media world works just like Rupert Murdoch runs his organization. Not even close. All the other networks are owned by corporations. Corporations have a CEO and a board of governors. They give their media outlets great leeway as to what they can air.

Newspapers are a little different. Most of them have either a liberal or conservative viewpoint. But they fight like cats and dogs. The New York Times and the New York Post have diametrically opposite points of view. Ditto for the Washington Post and the Washington Times.

Bottom line, the government of the USA does not control the media. You are still hung up on the Trump era where Fox News was the official mouthpiece of the Trump White House. But they were not the mouthpiece for Congress. No one was.

Stop trying to use the press for your devil. It gets old after awhile.

Glen Greenwald’s new book:

https://bookshop.org/books/securing-democracy-my-fight-for-press-freedom-and-justice-in-bolsonaro-s-brazil/9781642594508

Greenwald resigned from The Intercept (https://theintercept.com/) which he co-founded in 2016 because he felt editorial pressure to conform and went to https://substack.com/. He has been writing about how Mainstream Media (MM) is attacking independent journalists for encroaching on their hegemony of influence. Everyone is for freedom of the press when it applies to their own freedom. Many outlets are against the freedom of others when they find themselves criticized. Journalists working for MM have been advocating shutting down substack.

That’s all well and good Schinzy. The media are all fighting amongst themselves. So the big guys in the media are trying to tell the little shits to shut up. I think that has always been the case. No? And, in general, they have not had a lot of success.

But that is not what Opritov Alexander’s post was all about. He was bitching about the government controlling the media. He says, in effect, that they, under the governments’ direction, are picking on poor innocent Russia and taking sides with that devil Ukraine. A totally different argument altogether.

Oh, rumor has it that since the departure of the previous POTUS from the WH, Qnon is no more spouting anything. Highly coincidental, of course.

In the early 2000s, Mikhail Leontyev was a Russian journalist, and today the press secretary of Rosneft tells that he met with a media tycoon in London.

Who in a private conversation talked about the censorship system in his empire. So a new employee, a correspondent, an analyst is given a job. After a while they watch how he sees the situation, how he places accents if they do not coincide on critical parameters, he is transferred to another job Gradually, there is a consensus in the team on certain issues. Of course, there will always be a range of opinions. I have no doubt that there is freedom of action. But no one will oppose the most important established stereotypes.

True, concepts, stereotypes are always changing. For example: 70 years ago there was racial segregation, homosexualists were persecuted by law, most of society considered it right. Now this is not so. Who knows what will happen in 50 years?

On the basis of false anti-Soviet, mainly fiction, stereotypes of Russians in the form of slaves, fanatical communists, and now corrupt criminals have been created. This is not true. Everything is very difficult and impossible to briefly describe the situation. Moreover, it is not interesting to anyone. Only short conclusions are interesting, unfortunately. they do not correspond to the truth. Without knowing the situation, you will act incorrectly.

Alexander, yes I am sure Russia is really a free country and all this shit about Putin trying to become the new Czar of Russia is bullshit. Well, not really Czar, just “President for life”. Nonsense, pure nonsense, something the government ordered the press to print.

Putin signs law allowing him to remain Russia’s president until 2036

Moscow — Russian President Vladimir Putin signed into law on Monday a change to the country’s constitution that will allow him to run for two more six-year terms, granting himself the chance to remain in power until 2036. The Russian leader, 68, has already run the country for more than two decades, and with his recent crackdown on political opponents and civil society, he has made it clear that there’s little room for dissent.

A copy of the new law was posted on the government’s legal information website on Monday, confirming that the legislation — the success of which was really never in doubt — had been finalized. Prior to the new law, Putin would have been required to step down after his fourth and current term in 2024.

Meanwhile his political opponent, whom he tried to poison, is in jail and near death.

According to the situation briefly. Yes, the revolution in Ukraine was supported by the US government politically and money (apparently Ukrainian oligarchs). Otherwise, you cannot explain the content in the center of Kiev. Salary, food, accommodation, toilets for thousands of hired fascists from western Ukraine.

The East and Crimea of Ukraine is inhabited by Russians, the language is Russian. Very few people understand Ukrainian. Yes, of course, there was an operation in Crimea under the leadership of the Russian government. But there was a referendum. Before that, there was a precedent in Kosovo.

In Donbass, Lugansk and Kharkov there were uprisings against Ukraine, they were not supported by the government of the Russian Federation.

A retired FSB colonel Strelkov with a group of initiative citizens arrived in Donbas without the knowledge of the government and special services. Surprisingly, supported by local residents and the oligarch Malofeev’s money, he managed to create a combat-ready defense, seize weapons depots, maintain discipline. It was unacceptable for Putin and the government of the Russian Federation. But not to support These separatists meant to lose the support of voters. Almost all of Strelkov’s assistants were killed by the FSB of the Russian Federation. He, on pain of death, had to leave the Donbas in the fall of 2014.

There are fascists in Kiev. The murders of political opponents are not being investigated. Hundreds of people of certain views disappear without a trace.

YouTube channel of retired FSB colonel Igor Strelkov: https: //www.youtube.com/watch? V = UBB5izbc3c0

Ron, you wrote part of the truth. I am not trying to justify Putin. Moreover, I do not like him and his government. But there is no other. He is better than Yeltsin. Here is what I think is not true:

and with his recent crackdown on political opponents and civil society, he has made it clear that there’s little room for dissent.

There is no repression, he is constantly scolded and condemned in the media, YouTube, there are millions of views. But they hate the “opponents” more, it’s dangerous to say – ordinary people can knock on the head. Yes, the Russian Federation is a very conservative country, but homosexuals and the opposition are not persecuted.

Putin is not a stupid person, I doubt very much that he will stay until 2036. Power in the Russian Federation is not consolidated in the hands of Putin alone, there are many groups. Yes, it is based on corruption. All 100% of the oligarchs (Khodorkovsky is one of the big killers) made money by cooperating with the government. They are responsible for thousands of murders.

—-

“Meanwhile his political opponent, whom he tried to poison, is in jail and near death.”

This is an obvious example of the lies of the Western media. Nobody tried to kill him. This is a funny tale. They tried to kill him for 4 years. If they wanted to kill him, they would kill. There is a video of him being in prison, he walks with coffee. He is breaking the regime. The guards are afraid of him. He provokes. Soon he will start beating the guards, because the provocations fail.

Because of the lies of the media, you will not be able to see the truth, and therefore do the right thing …

And yes “Meanwhile his political opponent, whom he tried to poison, is in jail and near death.”

This opponent is a puppet of one group within the government of the Russian Federation. Although it sounds strange. Within the government, there are groups, each with its own oligarchs. They see different ways of development. (there are no communists) And it looks like a bulldog fight under the carpet.

I wrote: “Meanwhile his political opponent, whom he tried to poison, is in jail and near death.”

You replied: This is an obvious example of the lies of the Western media. Nobody tried to kill him.

Bullshit! This was not the first time Putin had someone poisoned. That is his M.O. It is obvious that you are totally fucking brainwashed.

I will not reply to any more of your posts. Have a nice evening.

Lightsout

Now that Putin’s friend has left the WH, he can now restart to play chess on the world scene. Has this something to do with that pipeline going to Germany which the US is trying to stop.

The worst part is what can the World/Nato do about it. Nothing happened after he moved into the Crimea. If Nato just put in some troops it would be escalation. The only thing that might help are well equipped mercenaries with face masks. Just like those loyal Russians who felt they needed to come to the aid of the Russian Ukranians.

Putin was doing things even with his supposed “friend” in the WH. Didn’t stop anything in the way of Active Measures from going on, or did we all forget Salisbury?

There is nothing in Ukraine to get het up about and start WWIII, and if the Ukrainians think the Russians genuinely wanted in, they’d have done it when they annexed Crimea. It wouldn’t take seven years, it’d be done in seven hours. And nothing would have happened as consequence.

Remember Georgia? Yeah. No one cares, and it’s irrelevant unless it involves pipelines directly breaking geopolitical plans (the Syria conflict springs to mind).

If anything was going to trigger WWIII, it’d probably be China taking Taiwan and the 7th Fleet getting involved in a shooting war. Russia isn’t going to invade Ukraine, much as their leaders and press seem to lose sleep endlessly over it.

Kleiber , the folks at CIA, Pentagon and MI 6 were wearing half pants when Putin was already the boss at KGB (FSB) . They are no match for ” The Old Fox ” . You are correct for the rest of your post . Putin has repeatedly said he has no desire to invade Ukraine , Baltics or Poland the biggest crybabies . His reasoning is very simple . Why should Russia take on the pension liabilities and pay for healthcare of these states full of old people and few resources?. However the West ” the deep state ” can make an ” error of judgement ” which might force him to take his glove off and crack the iron fist . He has had more than enough time to prepare for the stupidity of the West . Germany is the key . The German public wants no war with Russia ,but the politicians are a different story . Did GW II listen to the public in the case of Iraq ? If war was to breakout the result would be of course Ukraine would get smashed in 24 hrs like Georgia . What VDP would do is pullback, incorporate Donbass , Lushank and other Russian speaking areas into Russia . The rump Ukraine would be for the EU ( Germany ) to handle . The USA will just drop it like a hot potato .

P.S : ” The Old Fox ” was a popular TV series in Germany in 80’s about a police detective who in his last years before retirement always stumped the newcomers in the force . One of my favorits .

> Russia isn’t going to invade Ukraine, much as their leaders and press seem to lose sleep endlessly over it.

This is about blocking North Stream 2. Ukrainian government is a puppet in a bigger geopolitical game and will do what they are told to do.

If they were ordered to invade Donbass Russia might intervene. I think Russia movement of troupes was a pre-preemptive move to block a joint plan of the USA and some Eastern(Poland) and Western European states to create a crisis and bury North Stream 2 by the attempt to retake the territory by force (Georgian scenario).

While writing resolutions in which they essentially declare war on Russia (retaking Crimea by force as a new Ukrainian government policy) Ukrainian government clearly understands that any significant military move in Donbass might be the end of Ukraine as we know it. So they are afraid to do anything without strong Western support, including military. That’s why Biden administration made a statement about the support of Ukrainian sovereignty and, at the same time, probably pushing Ukrainians to make a move in Donbass.

There are two parts of Ukraine with different history and affiliations: Eastern Ukraine and Western Ukraine.

The regime in Kiev represents Western Ukrainian nationalism and it is/was to a certain degree resented in Eastern Ukraine (where manufacturing is concentrated) as provincial, incompetent and corrupt. It is controlled by a handful of oligarchs — a classic neoliberal oligarchic republic so to speak.

That does not mean that Eastern Ukraine would welcome Russians now (after seven years of anti-Russian propaganda by the government), but please do not write about things you have no clue: in 2014 the situation was different with several uprisings against Provisional government in Eastern Ukraine.

IMHO it was Putin’s decision to limit Russia role that led to the current situation. As far as I know the only large city which supported Provisional government in the East in 2014 was Dnepropetrovsk ( the home town of oligarch Kolomoyskyi, and nationalistic politicians Kuchma and Tymoshenko.)

IMHO Putin has the ability to occupy all Eastern Ukraine without a single shot and establish separate “Eastern Ukrainian republic” government. But he decided not to do as the it would result in crushing Western sanctions (which was Washington’s policy from the very beginning (google Nulangate); and that’s why 2014 EuroMaidan putsch was organized and financed by the USA with Poland, Germany and Sweden in supporting roles).

Add to this the necessary to feed pensioners (mentioned above) and the amount of money necessary to resurrect the manufacturing which would compete with Russian’s own. Which Russia probably could not afford at the time.

Putin just went shit scared into his basement with a bottle of vodka on seeing this photo of defense ministers of some NATO members . 🙂

https://media.gab.com/system/media_attachments/files/070/421/209/original/be1c4bc547657d60.jpeg

I would run scared too ;-). They probably have a deep sense of inferiority and as such are extremely dangerous.

Commander in Chief of NATO . Putin just dirtied his pants . 🙂

https://apnews.com/article/rachel-levine-health-secretary-4eee53439e9c2b4c27fcf4e7f572cb0e/gallery/eb139aeb303941a4bfd18d263407c323

Checkmate .

https://www.themoscowtimes.com/2021/04/05/putin-signs-law-paving-way-to-rule-until-2036-a73430

” The Old Fox” outsmarts the hounds once again . Don’t mess with Mr Putin .

Hope the current cold spell in Europe will enlighten Mvr Merkel on which side the bread is buttered .

” ” The Old Fox” outsmarts the hounds once again .” I don’t see the point to call Putin an Old Fox. It’s a brutal autocrat who is knowing only power struggle and is seeing negociation and compromise as a weakness. I know him also as to be a murderer of his own compatriots (destruction of civilian buildings in 1999, political assassinations…) and a slaughterer of civilians, for example, in Syria, as Russians did participate to the bombing campaign of Syrian civilians. And, internally, Russia is a dying country : alcoolism and tuberculosis are ravaging the society, the Russian state did become a kleptocracy with the alliance of Justice, secrets services and criminality to despoil local and foreign investors, corruption is generalized, the population is decreasing (who would want to have children in such country?) and the young and educated people are emigrating from Russia because they know that there is no future in this country. The only thing that prevents Russia to be forgotten is the hydrocarbons exports and the possession of nuclear weapons. I can’t imagine what will become of Russia when Putin will be stricken by oldness and senility. And what will happen the day he will dye : that’s not going to be glorious.

JFF , first I am no fan of VPP as a matter of fact I detest all politicians . The great Machiavelli says ” It is better to be feared than loved ,if you cannot be both ” . Putin chooses fear ,what is wrong with that ? He inherited a mess and he has taken hard decisions to straighten things out . He is running a country and is not auditioning for American Idol or XXX got talent contest or in race for the most popular leader on the planet . As to Syria let us not go there because then I can add Iraq ,Afghanistan etc to the list where some countries have tried to implement ( or impose) democracy against the people’s will with a lot of bloodshed . As to Russians emigrating I can tell you from my personal experience in Benelux I have never met a Russian youngster in the last 10 years . I work with students at Ghent University that come under the exchange programs from all over Europe . At the food stores I see cars with PL , RO,BG ,LT, LV, E , P, number plates never with a RU number plate . Yes , the population is decreasing but that is because the death rate is high and not because of a negative birth rate . Just for your info Russia is the only country in Europe where the birth rate has been reversed and increasing . This indicates that the young see a better future . As to the rest of your post that applies to politics and politicians from Japan across the oceans to Eurasia and USA . Show me an honest politician and I will show you a virgin prostitute .:-) . I am yet to meet a politician with hands in his own pockets — Howard Hughes .

Hydrocarbons and Nuclear = Russia . Nuclear and Reserve currency = USA . Not a lot of difference . What will happen when Putin dies ? Answer I don’t know . We can say the same for many nations ? In India we had the same questions for Gandhi and Nehru . In Egypt was same for Nasser in Indonesia for Sukarno , Malaysia Tunku Abdel Rehman , Singapore ‘s Lee Kuan Yew , Taiwan’s Chiang Kai Shek or is as Gaddafi said ” After me the deluge ” . Somebody will come , nature and politics abhor a vacuum , time and circumstances will decide the individual . Will he be bad ,good or good ,bad is an area of speculation .

P.S ; It is well said ” Politics is the last refuge for a scoundrel “

In your post, you have collected all the lies about the Russian Federation that have been pouring into your ears for 74 years now.

Tuberculosis and alcoholism are especially encouraging. These are all lies. Where is your proof? It is a matter of fiction of dedicated reporters, funded by fifth column grants.

Actually, you are right about one thing: the country is dying from the destruction of industry, factories and the desolation of fields. Capitalism and the ability of corrupt officials, courts, law enforcement agencies to take property and industry. A person needs not only food, but also Demand, work, employment. Without this, it degrades. As in the United States, the level of consumption of the parasite does not correspond to the level of industrial development and is associated with the extraction of hydrocarbons. The same is true within the States, but this includes printing $, issuing loans, and owning profitable businesses around the world.

In healthcare at the level of the best countries in the world, everything is practically free and you can always make an appointment with specialists. Tuberculosis and alcoholism are not for us. I have not heard or seen about the open sale of drugs. I can travel at night to any place in cities and villages without crime. There are no weapons at hand either.

https://www.youtube.com/watch?v=486yZ9e96aI&t=27s

https://www.youtube.com/watch?v=OADV_F4etW4

https://www.youtube.com/watch?v=c_1tzrwVWOI&t=298s

https://www.youtube.com/watch?v=WCOtDhgwN30

Ovi,

I am fairly certain that the DPR DUC data is for both oil and gas wells. For the basins that you chose, most of the DUCs are likely oil rather than gas.

World outside US has a shortage of US dollars. Not enough to go around. We flipflop between global reflation and global deflation. Dollar becomes a wrecking ball. As dollar strengthens it does cause inflation in currencies outside US but it makes it much harder to repaid borrowed US dollars outside US. It’s the global Eurodollar system that is everybody’s problem.

2008 was a collateral shortage. There wasn’t enough collateral in the system to keep loan generation going. With ungodly amounts of QE being done there is an acute shortage of collateral right now. A smaller amount of collateral is being used to make loans. Before the same collateral might have been used for 10 loans. Now it is double that or more. What I am saying is we are primed for a much larger 2008.

Watch price of oil. watch US treasuries on the long end 10’s and 30’s and watch the dollar. The reflation is turning into deflation will equal oil down, yields on treasuries down and dollar up. Treasuries yields are currently higher but will be rejected as loans for housing are tied to them.

Oil supply may continue to contract. But if what I am seeing is correct it won’t matter to price. Price will go down. OPEC cuts maybe become permanent.

Great chart on well productivity for Permian from Enno Peters(original at link below)

https://shaleprofile.com/wp-content/uploads/2021/03/Well-productivity.png

Chart resolution is not great here, but link above has better resolution.

When we adjust for lateral length. Average well productivity per lateral foot has been decreasing slightly since 2016. My models assume Permian average well productivity starts to decline in Jan 2020. Productivity was relatively stable from 2016 to 2018 with perhaps a 3% decrease in productivity from 2016 to 2017, little change from 2017 to 2018 and then further decrease in 2019 and 2020.

frac spreads

WTI down over 5% today.

What am I missing?

HT , what are you missing ? I have been lamenting that there is never going to be a pre covid normal , the world does not have a liquidity crisis ,it is a solvency crisis . The demand/ supply equation is broken , the “affordability ” factor has taken over . 2008 crisis saw 100 year old companies go belly up , when this crisis unfolds we will see sovereign countries go belly up . The train has left the station . Buckle up and enjoy it while it lasts . Be well .

The demand/ supply equation is broken

Thanks

Oil Drops With Virus Risks in Europe Dimming the Demand Outlook

(Bloomberg) — Oil plunged the most in nearly two weeks as growing delays in Europe’s reopening and looming Iranian supply dampened hopes for a swift decline in global inventories.

Futures in New York slumped 4.6% on Monday, sending prices to the lowest in more than a week and markedly below U.S. crude’s 50-day moving average. The U.K. may delay global travel beyond May 17 if Covid-19 infections continue to surge around the world, while Italy also extended some restrictions for travelers, adding further pressure to a recovery in oil consumption.

Meanwhile, Iran, the U.S. and the remaining members in the 2015 nuclear deal are set to gather in Vienna on Tuesday to discuss potentially resurrecting the agreement, presenting a possible path toward removing sanctions on the Middle Eastern country’s oil exports. Yet, Iran indicated talks won’t succeed without the U.S. fully removing sanctions.

“OPEC+ deciding to phase in production increases over time, when combined with news that potentially there could be more Iranian output, could very well mean that the market perceives there will be an imbalance more than previously,” said Bart Melek, head of commodity strategy at TD Securities. “Demand from Europe being significantly slower may derail” the near-term outlook for consumption.

More Iranian supply coming back to the market and renewed lockdowns complicate the picture for OPEC and its allies, which agreed last week to raise production by more than 2 million barrels a day over the next several months. Iran’s exports of crude, condensate and oil products could easily reach as much as 2 million barrels a day in the coming months amid a relatively muted U.S. response to higher shipments, according to consultant FGE.

Still, Goldman Sachs Group Inc. sees “a lot more” output being needed over the northern hemisphere’s summer to meet rising demand, and OPEC+ can adjust their decision as needed when it meets next at the end of April.

Saudi Arabia on Sunday raised prices for May oil shipments to Asia. Aramco, the state energy firm, will increase its grades to the region by 20 to 50 cents a barrel from April. Most prices for northwest European customers won’t be changed, while most grades to the U.S. will be cut by 10 cents. The move hinted at Saudi Arabia’s confidence in Asian demand recovering further.

From Art Berman

http://www.artberman.com/2021/04/01/super-cycle-silliness-why-oil-prices-will-not-increase-much-further/

I have discussed that hedging WTI crude oil via floors (also known as puts) has become expensive due to price volatility.

Got a quote this morning for a calendar 2022 $52 WTI floor. $6.09 per barrel.

So, for a little more than $2.2 million payment today, one could buy 1,000 BOPD floor insurance for calendar 2022.

There will be more Iranian oil coming to market over the next couple years.

The Trump admn policy of withdrawing from the International nuclear limitation deal failed, and Iran has begun to ramp up nuclear development despite sanctions during the last 3 years.

Most countries in the world want to get a nuclear limitation agreement back in force.

In return Iran will demand the re-opening of the oil business door.

They could produce an additional 2 Mbpd, or thereabouts.

And then they will use the money to beef up their regional campaign to extend a Shiite Military Theocracy to the greater middle east.

Not pretty.

Theocracy is never pretty.

Separation of Church and State was a guiding principle of the founders of this countries constitution.

Most of the money that will purchase the Iranian oil will come from China.

They also will provide the industrial muscle and engineering to ramp up the production, if needed.

China does not concern itself with the geopolitics of the middle east too much (so far), as long as the oil export machine functions.

The new global currency is getting closer to the point where international transactions, such as Chinese purchase of Oil, will be conducted in the Digital Yuan

https://www.thestreet.com/mishtalk/economics/anxiety-in-the-us-as-china-creates-the-first-major-digital-currency

I think a combination of China’s lack of credit impulse due to Beijing telling banks to cut credit through rest of 2021 and Biden’s infrastructure plan not being able to get passed will weigh on markets and prices over rest of the year. 10 and 30 year US Treasury bonds are starting to price this in.

As yields sink back towards zero. It’s not dollar positive at first. But as everything tied to growth and reflation starts to realize what they thought was coming actually isn’t coming things start to unwind.

I expect oil price to follow treasury yields lower then dollar strength later on. Equity markets might like lower yields at first but later realize growth and reflation isn’t coming. That is when dollar really starts to strengthen.

Central Banks are out of tools. Not that the tools they have been using actually ever worked.

HHH, I agree . The reflation trade and the second infra plan is dead in the water . How will China react to a strong dollar ? Cannot increase interest rates so it will be QE infinity .

HiH,

I think China wants a stronger dollar and weaker Yuan. Which will relate to more GDP for them.

The EIA’s Short-Term Energy Outlook came out two days ago. WorldOil has picked up their prediction and commented on it…below.

While OPEC ramps up production, U.S. oil output is projected to fall

U.S. oil output is set to reach 11.04 million barrels day this year, down from last month’s forecast at 11.15 million after a deep freeze in February that shutdown the oil industry in Texas, according to U.S. government data. The Energy Information Administration also lowered its output forecast for 2022 by 100,000 barrels a day.

STEO World liquids output

STEO US L48 excluding Gulf of Mexico

There is much discussion about the end of oil and gas “income tax preferences” in the United States.

So far, the Biden Administration has been vague. I suspect there will need to be horse trading with Senator Manchin to get rid of these. It is easy to forget that West Virginia is a “shale state.”

Dennis, if the expensing of intangible drilling costs for independent producers (which is everyone but Chevron, ExxonMobil, Royal Dutch Shell, BP, Total and Eni) is eliminated, you will need to rework your shale predictions.

The shale companies do not pay much, if any, Federal income tax because of IDC expensing. I have posted ad naseum of Pioneer Natural Resources having a $5 billion Net Operating Loss for Federal income tax purposes.

If IDC expensing goes away, intangible drilling costs will be required to be deducted over the life of the well for income tax purposes, and I predict activity will drop significantly, at least until oil prices rise significantly.

Of course, the stripper well preference, percentage depletion, is likely on the chopping block as well. As I have also posted, ad nauseum, percentage depletion is a deduction limited to the first 1,000 per BOEPD per taxpayer. It is a deduction taken by the over one Million royalty owners across the USA, in addition to the stripper well operators. It is also a deduction that is afforded to all mining, not just oil and gas, and not just fossil fuel mining. I presume lithium and other US based rare earth miners deduct the greater of cost or percentage depletion.

I would also note that oil and gas seem to be the only mining wherein percentage depletion is limited by volume.

I give the Biden Administration credit. Unlike the Obama Administration, they are not using the phrase “ending Big Oil tax breaks.”

Big Oil is defined as the integrateds, which I do not believe benefit from IDC expensing and also just get to deduct percentage depletion on the first 1,000 BOEPD like any other tax payer.

John Tester of Montana might be another that will require some horse trading.

Shallow sand,

I will redo the model when a law is passed. Right now there is a proposal, which will change quite a bit before it becomes law (and it might never be passed.)

True. I did qualify my original post in that way.

Peak oil production in Russia is expected in the period 2027-2029

April 09 / 06:40

Moscow. Peak oil production in Russia, excluding gas condensate, is expected in the period 2027-2029. This is stated in the draft general scheme for the development of the oil industry until 2035.

“In all these scenarios, based on the PDD (design and technical documentation – ed.), A declining nature of oil production (without gas condensate) is predicted after passing its peak in 2027-2029,” – stated in the document, which is at the disposal of RIA Novosti …

It is noted that this forecast does not take into account possible artificial restrictions on oil production in the period after April 2022 within the framework of OPEC + or other international agreements.

“If artificial restrictions on oil production persist after April 2022, the achievement of the peak oil production in Russia in all scenarios may be shifted forward in time compared to the forecast level, while production during the period of these restrictions will be lower than the indicators of the scenarios under consideration”, – added in the document.

According to the Ministry of Energy of the Russian Federation, in order to maintain a stable level of production in Russia in the future until 2035, it is required to increase oil reserves in the period from 2021 to 2035 in the amount of at least 10.4 billion tons. The average annual increase in reserves during this period should exceed the annual level of oil production by an average of 1.2 times.

The department believes that until 2035 the West Siberian, Leno-Tunguska, Caspian, Timan-Pechora and Volga-Ural oil and gas provinces on land will remain the main areas of growth in oil reserves. At the same time, an increasing share of the increase in reserves will be associated with the development of deposits on the continental shelf, in particular in the Caspian, Barents, Kara and Okhotsk seas.

Views 68

Is this the new official (government) timeframe? What did the old outlook look like? It thought it was plateau:ish starting in about 2020- if so, is there any new fields that explain where all the new supply will come from in the next 5 years or so?

Yes, this is the official assessment of the Ministry of Energy of the Russian Federation today. In my opinion, it is too optimistic. Intensive drilling continues in West Siberia, which has slowed down the decline.

Previously, it was assessed there:

The peak of oil production in Russia will be in 2028-2029. and will be from 504 million to 590 million tons / year with a subsequent decrease in the period until 2035 to 414-494 million tons / year.

This is stated in the draft general scheme for the development of the Russian oil industry for the period up to 2035, prepared by the Ministry of Energy of the Russian Federation, which is reported by TASS and RIA Novosti.

In 2020, production without gas condensate in Russia amounted to 476.4 million tons.

Taking into account the existing restrictions under the OPEC + agreement on production cuts, oil production in 2021 in Russia will grow to 478 million tons

Without taking into account the OPEC + agreement, in 2021 Russia would have produced from 494 million to 520 million tons, and in 2022 – from 490 million to 522 million tons.

The peak of oil production in Russia will be in 2028-2029. and will be from 504 million to 590 million tons / year, after which it will fall to 414-494 million tons / year by 2035.

At the same time, in the event of an extension of the OPEC + agreement, the achievement of the peak of production may be shifted forward in time.

The document clarifies that all scenarios under consideration are based on the potential production capacity of the Russian oil industry, and not on expected demand.

Capital investments for oil production will increase until 2027 inclusive, after which they will begin to decline slowly.

For 5 years from 2021 to 2025, the total capex should be from 6.31 trillion to 8.23 trillion rubles.

For 10 years from 2026 to 2035, investments are estimated at between 14.61 trillion to 19.02 trillion rubles.

Oil reserves in Russia in the period from 2021 to 2035 will grow by 10.4 billion tons.

The average annual increase in reserves will outpace the level of oil production by 1.2 times.

The main areas of growth in oil reserves will remain the West Siberian, Leno-Tunguska, Caspian, Timan-Pechora and Volga-Ural oil and gas provinces (OGP).

At the same time, an increasing share of the increase in reserves will be associated with the development of deposits on the continental shelf.

It is on the Arctic shelf, due to its low level of knowledge, that there is the greatest likelihood of discovering large and unique oil fields.

Inventory of oil fields, during which 60% of the current technologically recoverable reserves were studied, showed that from 36% to 64% of oil reserves remain profitable, depending on the macroeconomic scenario used.

The inventory also showed the need for additional incentives to enter unprofitable reserves to maintain current production levels.

The study of the oil fields was supposed to be completed in 2020, but its dates were postponed to 2021 due to changes in macro parameters as a result of the COVID-19 pandemic.

A number of fields with special tax regimes were excluded from the inventory perimeter: PSA, NDD, Samotlorskoye field, Priobskoye field, as well as small fields.

As a result, the number of fields included in the inventory perimeter decreased to 352 with total technologically recoverable oil reserves of 17.2 billion tons, or 60% of the current technologically recoverable reserves of the Russian Federation.

O+A quoted the Russian Oil Minister:

The peak of oil production in Russia will be in 2028-2029. and will be from 504 million to 590 million tons / year with a subsequent decrease in the period until 2035 to 414-494 million tons / year.

Doing the math, multiplying those figures by 7.33 barrels per day, then dividing by 365.25 days per year, we get: 10,114,497 to 11,840,383 Barrels per day. The average of those two numbers is 10,977,440 barrels per day. That is less than their 2019 average of 11,252,000 barrels per day.

Note: Sorry, I have had to keep deleting this post then reposting to correct mistakes.

O+A , Igor Sechin had said some time ago maybe an year or two, but not later that ” Please do not expect anything extra from Russia from 2022” . They are at a peak or maybe past peak but 2027 is way out . No I am not saying that you are incorrect just that no government will admit to reaching peak . It would roil the economy .

My takeaway from what the Russian Oil Minister is saying is: “We hope to hold Russian oil production at close to 11 million barrels per day for several years.” That is longer than his previous estimate of four years. At any rate, they do not expect any great increase in production.

They are hoping, desperately hoping, that new production in Eastern Siberia will replace the dramatic decline in Western Siberia. About 60% of Russian oil is now produced in Western Siberia.

Oil reserves in Russia in the period from 2021 to 2035 will grow by 10.4 billion tons.

That’s 76.2 billion barrels. WOW! They are really hoping for a miracle.

Basically, oil reserves are growing due to revaluation of existing fields or exploration of small ones with reserves of up to 5-10 million barrels, in this case, the profitability of development depends on the availability of infrastructure. There were precedents for changing existing estimates downward.

And yes, probably in the Russian Federation, the peak of production really was in 2019

Ron these estimates exclude condensate, I do not know how much of 2019 Russian output was condensate rather than crude. The peak 12 month output so far (2013 to 2021) has been about 562.7 million tonnes per year in 2018/2019 (12 months ending August 2019). This figure includes gas condensate and does not give any crude only figure. Russia produces a lot of natural gas so gas condensate output may be significant.

Does anyone have a link to the Russian forecast?

I found paper at link below published in September 2019, but it is not from the Russian Energy Ministry.

https://www.oxfordenergy.org/wpcms/wp-content/uploads/2019/09/The-Future-of-Russian-Oil-Production-in-the-Short-Medium-and-Long-Term-Insight-57.pdf

Ron these estimates exclude condensate,

I am not doubting your word Dennis, but I think you may be mistaken. I have never seen any quote out of Russia that did not include condensate.

At any rate figure 17 from your link says it all. Please check it out and reply.

Notice that the Minister of Energy’s target, in the above chart, does include condensate. Notice the dramatic decline in Russia’s brownfields. This is all of Western Siberia plus one more of Russia’s five largest fields in the Urals.

Dennis, it is not possible that “approved greenfields” can make up for this dramatic decline.

Bottom line, the Russian Oil Minister is living in fantasyland if he really believes his target will be reached. And notice that even this fantasy only hopes to keep production on a plateau.

Ron,

There are lots of potential areas in Russia that could be developed, whether oil prices are high enough to support this and the investment will be made to accomplish it is unknown. Note also this forecast was made prior to the pandemic, the oil production in 2020 and 2021 was lower than this forecast and that oil remains in the ground to be produced later, essentially the plateau would be moved out to 2025 or 2026. I do not expect Russian output will exceed its previous peak, but I think it will return to around 11 Mbo/d and remain at that level from 2024 to 2026 and then begin to decline. The rate of decline will depend in part on the price of oil.

https://minenergo.gov.ru/node/1209