I am starting this post off with a news article because it explains why JODI has U.S. production numbers wrong for July.

No, U.S. Oil Production Probably Didn’t Rise in July

The Joint Organizations Data Initiative (JODI) releases monthly oil supply-and-demand data for about 80 countries, which it gathers by directly surveying the countries. It is widely cited by analysts, especially for its figures on demand, imports and exports.

The latest JODI data released Sunday showed that U.S. crude-oil production rose from 9.3 million barrels a day in June to 9.5 million barrels in July.

But the EIA’s latest forecast called for July production to fall to 9.2 million barrels a day in July, continuing the trend of declining U.S. production as companies cut spending in the face of low prices.

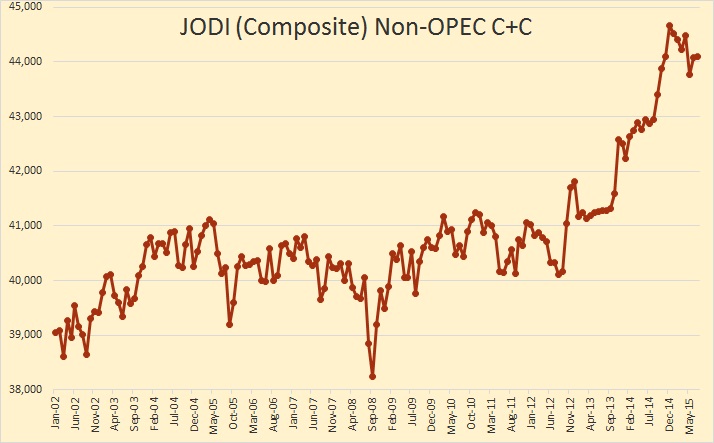

For the charts below I have used JODI data for all Non-OPEC nations except those that do not report to JODI. For them I use the EIA data and carry forward the same data that the EIA reported, (April). For the USA, since the JODI data is obviously wrong for July, I simply carried forward the June data which also came directly from the EIA. And for OPEC I use the OPEC MOMR’s “secondary sources”. JODI also uses the MOMR for their data but uses the “direct communication” data instead of the secondary sources data.

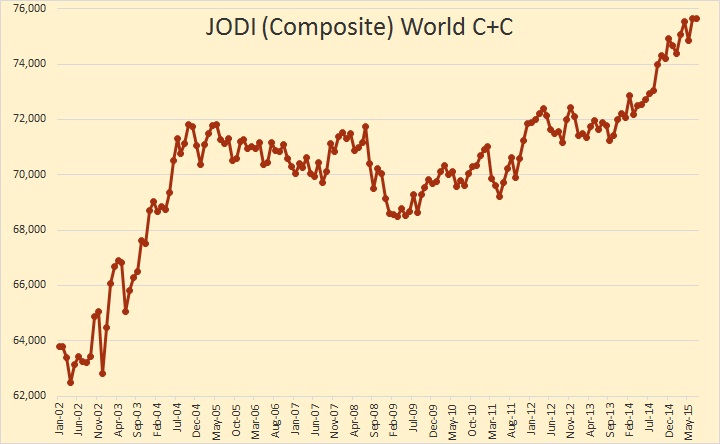

The data below is through July 2015 and is in thousand barrels per day.

In July we remained at or near the world’s all time peak at 75,631,000 barrels per day, down just 15,000 bpd from June.

JODI Non-OPEC stood at 44,100,000 bpd in July, down 567,000 bpd from the peak in December.

JODI Non-OPEC less USA stood at 34,804,000 bpd in July, down 900,000 bpd from the most recent high in December 2010.

The below table, Giant Oil Fields of the World Data as of 2013 is from Art Berman. It was complied by Mike Horn and Associates and is on the AAPG records. The Excel file that I received was far more extensive than the below. It contained the 738 largest oil fields and 1048 total oil and gas fields. I have shortened it to only fields above 5 billion barrels of oil, ultimate recovery estimate.

Five fields above 5 billion barrels ultimate recovery are not included. Three, Vostochno-Prinovozemelsky, Kaigan-Vasyugan and Kurmangazy (Russia and Caspian) because there was no data and Manifa and Khurais (Saudi Arabia) because due to decades mothballed off line, I found their data to be inaccurate. Mike Horn and Associates apparently calculated production from the date they first came on line and made no allowance for their decades off line. They had Manifa and Khurais far more depleted than I thought to be the case. But that still left 56 giant fields above 5 billion barrels ultimate recovery.

Horn and Associates calculated the decline, from first production, using three decline rates, 6.7 percent per year, 3.4 percent per year and 1.4 percent per year. Then they calculated the decline rate using an average of those three decline rates. The average of the three is the one used here when I calculated the remaining reserves from the original ultimate recovery estimate. The average of those three works out to be 3.83% decline per year. I think that number is very conservative.

{kind=link}

Unfortunately Horn and Associates did not calculate remaining MMBO, only MMBOE. For the 733 total oil fields with ultimate recoverable one billion barrels or more, the total ultimate recoverable oil came to 1,435,993 MMBO. That is 1.436 trillion barrels of oil in giant fields only. But the MMBOE in those 733 fields came to 4,674,021 MMBOE. That’s 4.674 trillion barrels of oil equivalent.

Of that original 4,674,021 MMBOE 1,479,623 MMBOE or 31.66% of the original ultimate recoverable oil, gas and condensate remain.

There were 310 other fields in this study but they were gas only fields and none of those were included in any of the calculations above.

__________________________________________________________

I send out an email notice whenever I have a new post. If you would like to be included in that notice then please post me at DarwinianOne at Gmail.com.

211 responses to “JODI Data and Giant Field Depletion”

A similar study from 1978 http://www.rand.org/content/dam/rand/pubs/reports/2006/R2284.pdf

Three decades ago ~50% of expected recoverable crude source was supergiants.

And now? MMBOE trickery only to rope investors?

More from Richard Nehring – 2007. http://www.resilience.org/stories/2007-10-08/interview-richard-nehring

Over the past fifteen years I have read over twenty books on peak oil (Campbell, Deffeyes, Simmons, Heinberg, Kunstler, Greer, etc) and read at least one peak oil site every day (oil drum, resilience, this one, etc). The consensus seems to have been that depletion would run at least 2% a year, and this report suggests more. Well, it has now been ten years since the plateau around 2005, implying that the world should have been down by 15-20 million barrels a day by now. My question is this, even allowing for the additional 6 million added by the US, Canada, and Iraq in the last few years, why is the world not down 10-14 million barrels a day by now?

Take away the hype and fanfare, and the simplest explanation is what is most likely to be true – there is no oil shortage. Why is the consensus so often wrong? The consensus, but its nature, is not likely to challenge the established thought patterns. Moreover, are books more likely to be sold based on a shortage or a surplus? Does good news sell better or bad news?

Let me see if I follow your reasoning:

1. The simplest explanation is likely true.

2. Consensus is often wrong.

3. Book sales are inversely correlated with reality.

And this is how you’ve evaluated the validity of peak oil?

Robert, I do not challenge the validity of peak oil at all (and by peak oil, I am assuming you mean peak oil production). Debating when peak oil will occur interests me less than the reason peak oil occurred – was it (or will it) be because the finite supply of remaining oil could not be extracted fast enough or efficiently enough to satisfy growing demand – or that demand for oil simply declined to the extent that there was no more need for expensive oil – there were other energy sources that were more abundant. I should say that I am not a peak oil expert like the others on this site, so my opinions should be taken with a grain of salt.

… or that demand for oil simply declined to the extent that there was no more need for expensive oil – there were other energy sources that were more abundant.

That is a possibility, provided peak oil does not happen for another half a century or more. Because that is about the rate other energy sources are replacing oil.

Peak oil will happen when rising prices can no longer bring enough new oil on line to replace declining production. It is that simple. Nothing complicated about it.

Also, prices will rise only after oil peaks, not before or even during the peak.

Peak oil will happen when rising prices can no longer bring enough new oil on line to replace declining production. It is that simple.

That’s actually very helpful, and having followed this conversation for more than a decade, I never really thought about it that way.

Thanks.

Hi Ron,

If there is a plateau in output, where would the peak be? It seems to me it would be called the middle of the plateau. If such a plateau occurs prices will rise unless there is a decrease in demand for some other reason (a recession perhaps), also the peak will not really be apparent for a few years, there have been many false peaks in the past, we will need to see a 2% decline before the peak might be called (though this would not have worked for the 1980 peak where output declined by 12% from 1980 to 1983.) Oil prices are unpredictable, the could rise before peak, during peak or after peak, it will depend on both supply and demand.

If there is a plateau in output, where would the peak be?

That would require a perfectly flat plateau. Not a chance of that happening. Therefore the peak would be the highest point in the plateau.

There is a possibility that the peak will not be known for years afterward. On the other hand if there is a sharp peak and a swift decline then we can know only a year or so afterward. It all depends on circumstances and the state of the economy.

we will need to see a 2% decline before the peak might be called…

Really Dennis, neither you nor I have any idea what the decline might be after the peak. I am obviously expecting a much steeper decline than you are. Only time will tell us which one of us is closer to the truth.

The decline in the early 80s, of which you speak, was caused by the Iran-Iraqi war and the resulting “Tanker Wars” in the Persian Gulf. Only a damn fool would have thought the decline was because of peak oil. So please don’t bring that old saw up as an example of a decline that could have fooled anyone. I lived through that decline and very well remember the cause. We all knew what the cause was. In fact I was in Saudi at the time. It is very clear to me. I was in Ras Tanura at the time and very well remember Saudi making deliberate deep cuts. And I also remember the massive oil pollution of the Persian Gulf.

Hi Ron,

I am not talking about 2% per year,just that output falls 2% from the peak. It can be 1 month or 10 years, you are correct that we do not know what it will be. I did not claim that we were not aware why output fell in 1980-82. There may have been those that thought output would never recover to 1979 levels, in fact it took until 1996 before the annual C+C output was higher than 1979 annual output (that is 17 years). Were you sure over that period that output would surpass the previous peak? If there is a steep decline as you foresee, that would be best as there will be a crisis that will precipitate the changes necessary for transition, hopefully you will be correct. I think my scenarios are far more likely and although an undulating plateau may occur (as has happened several times in the past) many will think that is a pause before the next increase in output. If C+C output falls by 2 or 4% from the peak with high oil prices, reality may finally sink in for the average person.

I didn’t start to follow this closely until Matt Simmon’s published Twilight in the Desert in 2005, so I did not really think about peak oil very much before that.

There may have been those that thought output would never recover to 1979 levels, in fact it took until 1996 before the annual C+C output was higher than 1979 annual output (that is 17 years). Were you sure over that period that output would surpass the previous peak?

No Dennis, it was not all that dramatic. Production started to rise in 1984, leveled out in 1985 then took off again, leveled out for two years in 91 then continued upward from that point. We all knew during that time that peak oil was not in sight. It was not a subject at all in those days. That is late 80s and early 90s.

Dennis, for god’s sake, we knew what caused the crash in the early 80s. I remember it very well because I was right in the middle of it. Peak oil was not even on the horizon then. We all knew what caused the oil crises of the 70s and early 80s. It was OPEC! There was never any doubt about that and there was never any doubt that we would recover from that.

Hi Ron,

Here is the World C+C chart from 1965 to 2014 (EIA annual C+C data).

”Also, prices will rise only after oil peaks, not before or even during the peak.”

”Peak oil will happen when rising prices can no longer bring enough new oil on line to replace declining production. It is that simple. Nothing complicated about it.”

I am strongly inclined to agree with you.

But as far as the RATE at which other sources of energy replace oil is concerned- just about all the ones that MIGHT serve can at least potentially grow at exponential rates.

If lithium does indeed turn out to be too expensive to be used by the hundred pound in car batteries on the grand scale, there is still the possibility that fuel cells will scale up and there is little question that hydrogen will be affordable – at least for truly ESSENTIAL transportation.

I am hoping some chemical engineer who might be knowledgeable about the electrolysis of water, or any other industrial process that yields purified hydrogen will chime in and tell us if hydrogen production can be efficiently tailored to the use of intermittent energy.

If the infrastructure for producing it from water is not outrageously expensive, then we can get plenty of hydrogen from wind and solar power. A hydrogen pipeline from the deserts of New Mexico and Arizona to the Northeast would cost an arm and a leg- but the sun shines very dependably in the southwest and solar farms there could be built to the extent that hardly any natural gas at all would be needed during daylight hours to fire power plants. Any excess at off peak hours could be fed to the hydrogen plants.

Ditto wind in other parts of the country.

Sometimes things get built without much if any immediate consideration being given to making a profit by anybody except the contractor doing the actual building.

Armies, navies, air forces and interstate highway systems come to mind.

I have not found any recent figures put out by an apparently reputable researcher, but I suppose it is reasonable to expect that the cost of building HVDC power lines- very high capacity long distance transmission lines- will fall by five percent or more per year, at the end points, which is where the super expensive equipment is needed – one installation at each end.

The actual construction of power lines is a mature industry and the cost per mile of such lines will probably just go up with the cost of materials , men and machinery.

In the event of an emergency being declared, there will be PLENTY of machinery and men.The machinery can be diverted from building new highways and shopping malls. Aluminum might be in short supply. Steel will not be- not if an oil shortage has forced the scrapping of tens of millions of older gas hog cars and trucks.

In the event of the prez declaring a national emergency, which could easily come to pass, environmental reviews and right of way issues could be dispensed with very quickly indeed, thus expediting the construction of renewable infrastructure wherever it can be built to best advantage.

I can easily envision the production of pure electric and plug in hybrid cars increasing by a hundred percent a year for four or five years – assuming the battery manufacturers can keep up.

After that the rate of growth would probably slow substantially but plug in hybrid production could probably be increased by ten to twenty percent a year for a long time- as long as the supply of lithium holds out.

Driving a plug in hybrid with two seats fore and aft and a ten kWh battery and a muscular lawn mower engine would be infinitely preferable to giving up the mcmansion for a non existent decent apartment downtown.

There is no real reason such a car couldn’t be built out of well painted high strength steel, ( which is already in common use in cheap cars), fiberglass , aluminum’ and maybe a little carbon fiber etc. A car built along these lines could easily be made to last a lifetime with a few repairs..

Tradesmen and engineers know that most machinery including heavy trucks is built to be very easily repaired – with all the major components having standardized dimensions and fasteners etc. You don’t buy a new electric motor or chain or bearing or hydraulic pump or cylinder from the OEM- unless you want to. You just give your jobber the description and he can provide you will a functionally identical part for a quarter of the money – or twice the money- depending on the brand name on the part.Sometimes I have found it worth paying twice the price myself , for example for tires, shock absorbers, mufflers, and other parts -because twice the price can buy you five times the warranty as well as greater safety reliability fuel economy etc.

I once had a friend who could RandR an old VW beetle engine without any help and very few tools between breakfast and lunch and smoke cigarettes and drink cokes and bullshit right along and finish up with time to spare. Cars CAN be built to last- and they CAN be built to be easily repairable.

As the Snap On guy sez, the sweetness of quality is remembered long after the sting of high initial price has been forgotten.

A MAN SIZED fuel cell could easily be fitted into the space occupied by big diesel engine radiator transmission and diesel fuel tanks on a heavy duty truck.

Hydrogen is very light and it might actually be practical to swap out hydrogen tanks on cars and trucks after the fashion that some people thought batteries could be swapped out in cars.

I have swapped out propane tanks on forklifts by hand, and the process takes hardly any longer than filling up with gasoline, maybe five minutes or so.

You would not have to worry about getting a worn out tank because you would only be keeping it until you swap out again for another full one.

With current technology, either you’re converting to electricity with a catalyst which is very expensive and low power/weight, or the energy efficiency of the process is awful.

Interestingly, this method is close to the cheapest there is for low duty cycle peaking power, i.e. the power plant that you run only during the record or near record cold snaps and heat waves. If you have natural gas available at a reasonable price it loses to that, but not by all that much.

The reason it does so well is that for a low duty cycle, only the fixed cost/kilowatt matters, and the variable cost/kilowatt hour is close to irrelevant.

You really, really don’t want to mess around with swapping out hydrogen tanks. 10,000 psi rating, exotic carbon fiber construction. Ding it in a swap, oh, boy. Boom.

Here’s a Youtube link to the Toyota Mirai fuel tanks and drive system being assembled.

https://www.youtube.com/watch?v=bge5K4lt-ow

And the fuel cells have their own exotic materials requirements – platinum, etc. operate at 700 degrees F.

Makes an EV look like a simple toy by comparison.

But it isn’t the hardware that is the death-knell for renewable hydrogen. It’s the thermodynamics. Only about 35% of the electrical energy generated at the power source (power plant, wind turbine, etc.) can be delivered to the vehicle motor. There isn’t a lot of thermodynamic room for efficiency improvements at the fuel cell or electrolyzer level. The well-to-motor efficiency for EV’s using lithium batteries is about 80-85%. In an energy-constrained world, the huge efficiency difference between fuel cell-hydrogen and EV-battery technologies is just too high a price to pay for the luxury of improved energy density or fast fueling.

We could use a tritium fusion process to generate heat, melt salt, use the salt to make steam, use the steam to generate electricity and use the electricity to drive electric motors. The tritium container for a four passenger vehicle will be the size of a hand grenade.

I am ready bet against fuel cells becoming a practical option in cars myself, anytime SOON, but what do the people at Toyota know that I don’t?

I can answer THAT question easily enough- PLENTY.

Most people get old and get firmly set in their opinions , but I continue to change my own as evidence to the contrary comes in.

The company I worked for had a hydrogen fuel cell vehicle running around, it was 100 % bullshit.

If transport by others. Choices choices – Bags of NPK or used Li Car traction Batteries in the barn? Li Batteries can be stored for long periods at 50% charge which would kill other chemistries. but must be protected against self discharge at all costs. – 20 watt PV panel can do this. Perhaps Indestructible Nickel Iron Edison cells better choice for stationary apps.

“Peak oil will happen when rising prices can no longer bring enough new oil on line to replace declining production. It is that simple. Nothing complicated about it.”

WTF is rising prices? From current 48 usd/b to 50 usd/b? Or from current 48 to 300 usd/b? Do you think that there will be peak oil at 300 usd/b? If oil goes to 300 usd/b there won’t be peak oil for couple of decades. I’m amazed how some people still talk about “rising prices” when it’s obvious that it will be the opposite.

Mistruz, if you don’t know what rising prices are then any dialogue with you would be useless. But I will assume the question was rhetorical.

No, small fluctuations in the price are not rising prices. And no, prices will not reach $300 a barrel. Rising prices was what happened in 2009 after they reached a low of $37 a barrel. Rising prices would be if they did that again. But if they did that would very likely bring more oil back on line. But if those rising prices fail to bring production back to the previous peak then we will have very likely reached peak oil.

I’m amazed how some people still talk about “rising prices” when it’s obvious that it will be the opposite.

It is obvious that prices will continue to fall? Thank goodness that we have such wisdom reading this list when most of us mere mortals are not so sure about it. But you can continue to be amazed because I think prices will rise again in a few months…. give or take.

Hi Mistrzu,

So how low do you think prices will go?

You think it is unlikely that prices will rise above $50/b, long term? You are sadly mistaken. Oil will be above $75/b within 12 months, when the peak arrives in 2020 (or perhaps by 2017) then oil prices will continue to rise, probably to $120/b, at that point we might see an economic crash, it depends how steeply oil output declines, I think we might muddle through until 2030 to 2035 (unless a major war breaks out), then we will see Great Depression 2.

I don’t see why it’s obvious to you that prices should fall. Oil people don’t work for food, dude.

The depletion rate is the rate that we consume remaining recoverable reserves, and remaining recoverable reserves are always depleting, i.e., it’s a one way street. But production can increase, stay flat or decline, and an increase in production correlates to an increase in the depletion rate.

The most compelling example I can cite of the enormous difference between rates of change in production, versus depletion, is the Six Country Case History*. From 1995 to 1999, their combined production increased by 2%, but over the same four year period they had already shipped 54% of their total cumulative volume of post-1995 net exports (CNE).

In regard to rates of change in production, IMO actual global crude oil production probably peaked in 2005, while global natural gas production and associated liquids, condensate and natural gas liquids, have (so far) continued to increase:

http://peakoilbarrel.com/jean-laherreres-bakken-update/comment-page-1/#comment-534101

And a link to a related comment:

http://peakoilbarrel.com/texas-rrc-oil-gas-production-2/comment-page-1/#comment-539428

*Major net exporters that hit or approached zero net exports from 1980 to 2010, excluding China:

http://i1095.photobucket.com/albums/i475/westexas/Slide2_zps55d9efa7.jpg

John, depletion and decline are two entirely different things. Every oil field in the world that is producing oil is also being depleted, every year, by the amount of oil that the field produced that year. That does not mean that oil field is declining by that same amount. Production in any field may be increasing while the field is being depleted by from 2, 3 or more percent per year.

Depletion rate is what happens below ground. It is how fast the oil in a reservoir is being depleted, or pumped out. Decline rate is what happens above ground. It is how fast a field’s production is declining. And that number could be zero or even a positive number. But the depletion rate is always a negative number. Unless oil is being created faster than it is being pumped out, the number cannot possibly be positive.

Back in the early part of this century Saudi Arabia found most of its fields declining by an average of 8 percent per year. But they found a fix, massive infill drilling. The below was written in 2006.

Saudi Arabia’s Strategic Energy Initiative

Scroll down to “Saudi Oil Field Depletion Rates”. That should read “Saudi Oil Field Decline Rates”. Some folks are continually confusing decline rates with depletion rates.

Without “maintain potential” drilling to make up for production, Saudi oil fields would have a natural decline rate of a hypothetical 8%. As Saudi Aramco has an extensive drilling program with a budget running in the billions of dollars, this decline is mitigated to a number close to 2%.

So Saudi Arabia managed to get its decline rate down to almost 2% by massively increasing its depletion rate. And by bringing new fields on line they managed to more than replace the 2% decline they were suffering in their older fields. They brought on Shaybah, Khurais, and Manifa.

So Saudi Arabia has managed to actually increase production while their older fields were declining by greater than 2% per year while their depletion rate is likely upwards of 8% per year or possibly greater. Similar things have also been happening in many other oil producing nations.

Hi Ron,

In Twilight in the Desert on page 378, Matthew Simmons says the Saudi 2P Reserves in early 1979 were 178 Gb and on p 379 that an estimated 33 Gb of undiscovered reserves (in 1979) had been discovered by 2005. So total 2P reserves including reserves eventually discovered were 211 Gb in 1979. Using BP data to subtract oil produced from 1979 to 2014, the depletion rate would be 4.4% in 2014 if there had been no reserve growth.

Using BP data to subtract oil produced from 1979 to 2014, the depletion rate would be 4.4% in 2014 if there had been no reserve growth.

I think you mean the depletion rate would be 4.4% per year from 1979 to 2014. There is just no way you could know exactly what it was in 2014… or in 1979, only that the average depletion rate was 4.4% for those 35 years.

It stands to reason that if you produce the same amount every year, or nearly so, then your depletion rate must increase each year. That is you are producing the same amount of oil every year from an ever depleting resource.

Therefore I would submit that in 1979 the depletion rate was well below 4.4% and in 2014 it was well above 4.4%. Because if the average was 4.4% over the 35 year period then it could not possibly be otherwise.

Hi Ron,

I have assumed there were 211 Gb of reserves in 1979 and no reserve growth. Each year production is subtracted from reserves (note by using BP data I overestimated the reduction because NGL is included in the production numbers. Using BP’s Stats in 2014 Saudi output was 4.2 Gb and 2P reserves (subtracting 1970 to 2013 cumulative output of 111.5 Gb) of 95 Gb. The depletion rate in 2014 is 4.2/95=4.4%. The average depletion rate from 1979 to 2014 was about 2.2%.

Well hell, I would say that a 4.4% depletion rate is really pretty alarming. That takes you down over 50% in just 16 years.

Goddamn, that is absolutely scary! That ain’t nearly enough time to get those so-called “renewables” up to spped.

Hi Ron,

As you said decline rate and depletion rate are not the same thing. Saudi Arabia is only one country and the reserves I used ignore reserve growth. Note that Saudi Arabia claims to have 267 Gb of reserves, this might be 3P reserves and 2P reserves would be about 190 Gb. That would mean depletion in 2014 was about 1.9% (using EIA C+C output data for 2014).

My main point was that your 8% depletion rate estimate was not correct, it is 4.4% at most, and more likely to be about 1.9%.

Edit:

I just re-did the calculation using EIA C+C output data for KSA and the depletion rate in 2014 with no reserve growth would be 3.3%. If we assume output remains at 2014 levels until 2030 (not very likely, it will fall) depletion would be 7% in 2030 and reserves would fall from 107 Gb to 51 Gb, assuming no discoveries or reserve growth.

The “no reserve growth” assumption does not match what has happened in the US or the UK.

Well perhaps. But Saudi Arabia themselves were the ones who said their decline rate was 8 percent. And they were the ones who said that infill drilling had gotten that decline rate down to just over 2%.

Soooo…. what can we infer from that?

I think you should forget about reserve growth. Reserves don’t grow. Previous reserve estimates that may or may not have been too low may be updated. But you should call it “more accurate reserve estimates”, not reserve growth. Again, reserves don’t grow. And I do hope, I mean I really do hope, that you know that.

Hi Ron,

Yes I do. Most people know that “reserve growth” is a revision of reserve estimates, and I certainly would not insult your intelligence by assuming you did not know that. Some people are more polite than others.

You had said earlier that the depletion rate was 8%. Perhaps you misstyped.

You said (bold added by me):

So Saudi Arabia has managed to actually increase production while their older fields were declining by greater than 2% per year while their depletion rate is likely upwards of 8% per year or possibly greater. Similar things have also been happening in many other oil producing nations.

I meant depletion rate. If their decline rate was 8% and they started pumping much faster to get their decline rate down to 2% then they had to dramatically increase their depletion rate. Perhaps it was not that high but 4.4% is still an alarming rate.

My point about “reserve growth” is that is a very erroneous term. There is no such thing as reserve growth and people should just stop using the term because it gives the impression that they really believe it. I would never use a term that I knew was an impossibility. Of course I was being sarcastic when I suggested that I hope you knew better. Of course I know you know that reserves do not grow.

But then that begs a very serious question… why do you still use the term?

Hi Ron,

Every term that refers to a physical measurement is always an estimate so when someone says “reserve” it is always an estimate, nobody has ever or will ever know exactly what the level of reserves are.

As to “growth”, this is commonly understood as something getting bigger.

That is exactly what has happened to reserve estimates.

For example, in the US from the end of 1979 until the end of 2009 there was an increase in the estimates of US reserves (aka “reserve growth.)

Proved plus probable (2P)reserves were about 51 Gb at the end of 1979 (proved reserves times 1.7). From 1980 to 2009 there were 18 Gb of cumulative discoveries and 70 Gb of cumulative output.

So reserves in 2009 should be 51+18-70=-1 Gb if there was no increase in reserve estimates over the 1980 to 2009 period (no reserve growth). The proved plus probable reserves at the end of 2009 (assuming 2P reserves=1.7 times 1P reserves) were 35 Gb, an increase of 36 Gb. Reserves may not “grow”, but there was an increase in the estimate over the 1980 to 2009 period. Most people use the shorthand “reserve growth” to refer to these increases in reserve estimates.

Note that the “reserve growth” could be eliminated if we assume 2P reserves are 3.45 times 1P reserves.

Oh! Reserve estimate growth. Well why don’t they call it that instead of reserve growth? It is the estimate that grows, not the reserves.

Oh well, the misuse of the English language is rampant.

Hi Ron,

Just as you do not refer to C+C output estimates, I leave the word estimate off as many people know that every measurement is an estimate with some degree of uncertainty.

My “misuse” of the language is no different from yours.

JohnH Wrote:

“The consensus seems to have been that depletion would run at least 2% a year, and this report suggests more. Well, it has now been ten years since the plateau around 2005, implying that the world should have been down by 15-20 million barrels a day by now. My question is this, even allowing for the additional 6 million added by the US, Canada, and Iraq in the last few years, why is the world not down 10-14 million barrels a day by now?”

Simple: Horizontal drilling and other advanced recovery has delayed production declines. Fields are depleting faster then 2% per year, but the newer tech has permitted extraction to remain stable or increase. Although they did it with a heck of lot of drilling and infrastructure investment. Big Oil spent more $4T since 2005 to keep conventional oil production flat. Another words, depletion and extraction are running at two different rates, for now. At some point, the curves will cross.

When horizontal drilling runs to a conclusion, and we will see much, much higher depletion rates. Instead of a natural bell curve decline, will might just see something like a cliff (Depends on how far they can press it). It probably would have been better if newer tech was not not used to artificiality prop up extraction rates since the shallower long term decline curve would have bought more time. Since total production increased, it permitting BAU to continue rather then permitting the global economy to adjust over a longer period. In my opinion, the world set it’s house on fire to stay comfortable for a wee bit longer.

Of course, its economic growth that keeps the debt bubble at bay. Perhaps if oil production followed depletion rates, the debt bubble may have popped earlier and created a global depression instead of deferring it.

1. The biggest issue with peak oil predictions is the lack of clear data as to the remaining reserves.

2. The shale oil desperation and hype was not taken into account by peak oil predictions. The fact that we are even going there is proof in itself that we are moving into last ditch territory.

3. Enhanced recovery methods have enabled for example Saudi Arabia to continue pumping. However when the peak finally happens there, the decline will be sharp.

In the big scheme of things it is not that important to predict the date by the day. We know peak oil will happen. We know we have created a civilization that is utterly dependent on oil. We therefore know that fundamental changes will come our way when oil production finally does decline.

We have Jeffs ELM. Rocksmans POD. LTO .. Now SOD… Shale Oil Desperados

Depletion rate is MANAGED, it doesn’t just happen. In many cases it’s managed to allow production to decline. The USA has been somewhat of an exception, because prior to the 1970’s the field rates were restricted using allowables. Most USA states also imposed well spacing rules. These weren’t fully optimized, which led to infill drilling (mostly to optimize water flood performance).

OPEC nations also manage production. This was quite evident in field performance, but today they seem to be straining to sustain production and the cash flow they require.

In other cases we see production impacted by facilities limits, for example North Sea fields are usually designed to plateau for a few years. This causes an odd looking “decline curve”.

But if you study the subject in detail you will see that oil fields do decline. So how gave we been able to sustain and increase production? We simply slowed down activity, which allowed prices to increase, and the higher prices allowed development of previously non commercial fields. If you look at the production curves for Norway, United Kingdom, Indonesia, etc, you will see that in spite of higher prices, they could not keep up.

So the question really should be: what’s left out there we can tap to produce enough to offset the production decline we KNOW is taking place? Not that much. I happen to have been in the oil business for 40 years, but I can’t disclose details. What I can do is point out that Shell has spent billions of $ to set up and drill the Burger prospect in the Chukchi Sea offshore Alaska. This sends a clear signal that very intelligent and well trained managers and technical professionals feel the prospect is worth the risk, even though it will require $80 plus per barrel prices to be commercial (and $100 plus per barrel to have justified the exploration expense). Thus one of the few remaining giant fields we visualize requires very high prices to fly.

So what else is out there? Heavy oil? Most of it requires $100 per barrel. Deep water? Deep water won’t increase beyond this year’s rate unless oil prices increase beyond $100. Shales? Most of them require $80 per dollar or more.

And what happens after we get the better shales, the better heavy oil, and the little bit of deep water oil that’s out there? We will need higher prices.

But higher prices imply more inputs. More steel, more cement, more chemicals, and more people. And as the amount of stuff we demand increases we see our prices go up. Which gets us on a spiral. To make matters more complicated we have to account for response time. Let’s say Shell gets through the regulatory hurdles….getting to first oil will probably take 7 to 10 years after they delineate the field. A large heavy oil field will take 7 years if it requires an upgrader. The only “quick response” we have is the USA light tight oils, with a much smaller potential available in Argentina’s Vaca Muerta, and possibly in Western Siberia.

Those who think we can keep this endlessly and brag about technology or getting smarter are peddling. The truth is all that fancy technology and smarts costs a lot of money. Simple physical properties of rocks full of tiny holes located thousands of feet below the surface, and fluid properties limit what we can do.

good post, thank you.

I am well aware of the major additions to all liquids production since 2005. Some sources even quote numbers in the 95 million barrels per day range. Most reports of conventional production, however, only show the US, Canada, and Iraq, plus a little bump by Saudi Arabia and Russia, as increasing over that period. For the conventional total to go from 72 to 76 million barrels per day implies virtually no decline in 10 years for the rest of the world. This is not what most authors were expecting, and I have seen little in the way of explanation as to who or how this was accomplished.

I’m not differentiating conventional versus non-conventional.

I’m attempting to differentiate actual crude oil production (generally defined as 45 API gravity and lower crude oil, from all sources), versus liquids associated with natural gas production–condensate and NGL.

As noted above, in my opinion despite trillions of dollars in upstream capex, it’s very likely that actual global crude oil production has been approximately flat to down since 2005, while global gas production and associated liquids have so far continued to increase. To answer your question directly, actual crude oil production probably peaked, while global gas production has clearly not peaked.

Hi JohnH,

One area of difficulty is that there are different definitions of “conventional oil”. For some authors the division is based simply on API gravity. For example Jean Laherrere divides crude plus condensate (C+C) production into two parts C+C less extra heavy oil (XH) and XH where XH has an API gravity of 10 degrees or less. Colin Campbell has a much more restrictive definition of “conventional” oil.

Jeffrey Brown would like to exclude condensate and consider crude only, but we don’t have very good data for that except for OPEC and Texas.

High oil prices have resulted in investment in enhanced oil recovery and new onshore and offshore developments which have added to output. The oil industry has been more resilient than many peak oilers thought possible in 2005 or 2008. Also high oil prices were tolerated better by the World economy than many expected, but demand did grow more slowly due to high oil prices. The peak in oil output(C+C) will arrive, but maybe not until 2018 to 2020, if NGL is included, the peak in C+C+NGL may be in 2024.

For what it’s worth, we also have the EIA’s estimates of US C+C by gravity, from 2011 to 2014:

Hi Jeff,

Yes but we do not have a good estimate for the World. Better to focus on C+C because we have fairly good data.

I’m reminded of the old joke about the drunk looking for his keys late at night under a streetlight. He lost his keys down the street, but the light was better under the streetlight.

Hi Jeffrey,

Well you can make your estimate of crude oil output for the World, and some may believe it. Ron’s focus on C+C makes more sense to me, much easier to get people to take it seriously when there is relatively good data to back up what you are saying.

So, if a patient is critically ill, should the doctor focus on what can be easily measured, or should the doctor focus on what is actually wrong with the patient, even if the diagnostic data are less than ideal?

In any case, I think that we can all agree that a probable “Undulating plateau” in actual crude oil production, despite trillions of dollars in upstream capex since 2005, does not fit your worldview.

The available data:

Following are links to charts showing normalized production values for OPEC 12 countries and global data. The gas, natural gas liquids (NGL) and crude + condensate (C+C) values are for 2002 to 2014 (except for gas, which is through 2013, EIA data in all cases). Both data charts show similar increases for gas, NGL and C+C from 2002 to 2005, with inflection points in both cases for C+C in 2005. My premise is that condensate production, in both cases, accounts for virtually all of the post-2005 increase in C+C production.

Global Gas, NGL and C+C:

http://i1095.photobucket.com/albums/i475/westexas/Global%20Gas%20NGL%20C%20amp%20C_zpskb5bxu6d.jpg

OPEC 12 Gas, NGL and C+C:

http://i1095.photobucket.com/albums/i475/westexas/OPEC%20Gas%20NGL%20C%20amp%20C_zpsox3lqdkj.jpg

Currently, we only have crude oil only data for the OPEC 12 countries and for Texas, although the EIA has some 2011 to 2014 estimates for actual US crude production (note that what the EIA calls “Crude oil” is actually C+C).

Also following is a link to OPEC 12 implied condensate (EIA C+C less OPEC crude) and OPEC crude only from 2005 to 2014 (OPEC data prior to 2005 was for a different set of exporters than post-2005). Obviously, data quality is an issue, and the boundary between actual crude and condensate is sometimes fuzzy. In any case, we have to deal with the data that we have.

OPEC 12 Crude and Implied Condensate:

http://i1095.photobucket.com/albums/i475/westexas/OPEC%20Crude%20and%20Condensate_zps12rfrqos.jpg

As of 2014, OPEC and the US accounted for 53% of global C+C production (41 MMBPD out of 78 MMBPD). Implied OPEC condensate production increased by 1.2 MMBPD from 2005 to 2014 (1.2 to 2.4). The EIA estimates that US condensate production increased by about 1.0 MMBPD from 2011 to 2014. I’m estimating that US condensate production may have increased by around 1.2 MMBPD or so from 2005 to 2014. Based on the foregoing, increased condensate production by OPEC and the US may have accounted for about 60% (about 2.4 MMBPD) of the 4 MMBPD increase in global C+C production from 2005 to 2014.

Combining the US and OPEC estimates, the US + OPEC ratio of condensate to C+C production may have increased from about 4.6% in 2005 to about 10% in 2014. If this rate of increase in the global condensate to C+C ratio is indicative of total global data, it implies that actual global crude oil production (45 and lower API gravity) was approximately flat from 2005 to 2014, at about 70 MMBPD.

In other words, the available data seem quite supportive of my premise that actual global crude oil production (45 API and lower gravity crude oil) effectively peaked in 2005, while global natural gas production and associated liquids, condensate and NGL, have (so far) continued to increase.

If it took trillions of dollars of upstream capex to keep us on an “Undulating Plateau” in actual global crude oil production, what happens to crude production given the large and ongoing cutbacks in global upstream capex?

Dennis, I don’t focus on C+C because I think it makes sense. I focus on C+C because no one tracks Crude only except OPEC, Mexico and Norway. I would use crude only if it were available for every nation.

Hi Ron,

It makes sense because that is the data we have.

Hi Jeff,

Doctors act on those factors which they have good data on. They try not to guess except in emergencies.

Thanks for both of your replies, and for your invaluable contributions to the peak oil community over the years. While Saudi Arabia has had the money and expertise to maintain its production, it seems remarkable that the rest of the world has done as well as it has. It will be interesting to see how well they can keep it up as the world economy rolls into recession.

… it seems remarkable that the rest of the world has done as well as it has.

I don’t find it remarkable at all. Old oil fields have very low lifting costs. Every major oil country in the world can afford massive infill drilling and they have taken full advantage of the process.

Of course the USA exhausted their old fields many years ago. We were the original “infill drillers” and started the process years before we peaked in 1970. In California I have seen pump jacks only a few feet apart. But they were idle, the oil below them pumped out many years ago. And that was in 1959.

But then came the shale revolution and all that it wrought…

I remember one of the EIA forecasts for US production from 2006 or thereabouts, it showed growth in tight oil as this teeny tiny sliver that would maybe amount to 750 kb/d in 2030 or something pitiful. According to this graph our production would grow, of course – mostly courtesy UDW. No one foresaw tight production as much of anything to write home about.

Without the tightoil input I’d warrant we’d have seen bona fide shortages by now; or sustained super high prices impacting demand/economic growth. As it happens we had merely high prices and sluggish overall growth in production.

Hi KLR,

Very true that nobody saw LTO coming in 2009 or so. Without LTO oil prices would definitely be much higher, but we also might have seen more oil sands development and deep water drilling if oil prices had been very high (say $125/b or more from 2011 to 2015.) The high oil prices would also have reduced oil demand growth. Impossible to determine how it would have played out, but the LTO boom may be over soon (2018) and it will be difficult to replace that oil as it declines. The peak will be evident by 2020 to 2025. Oil prices will be well over $100/b by then.

The peak will be evident by 2020 to 2025. Oil prices will be well over $100/b by then.

hahaha

Hi Ron,

You may not be surprised, but the general consensus at the oil drum in 2008 or so was that it would be impossible to stem the decline. I was in agreement with that assessment at the time and I don’t remember you dissenting from the consensus view at the oil drum.

Hindsight is 20-20.

I haven’t a fucking clue as to what the hell you are talking about. I remember a lot about folks thinking the peak was in 2005 but I don’t remember anyone saying that 2008 was the peak.

Hi Ron,

I guess you weren’t paying attention.

http://www.theoildrum.com/node/5177

Obviously I was not paying attention to that particular post. You will notice I had no comments on that post.

Please keep in mind that I called peak in 2015 back in the summer of 2014, well before the price collapse or any decline in production. In fact production was still rising fast at the time.

Of course I could be wrong. I don’t see why you get so paranoid about calling peak. People make predictions all the time that are wrong. So what? I say 2015 will be the peak because I have been following every oil producing nation for years and I believe that there will be more oil in decline, post 2015, than oil increasing. It is that simple. I am 95% confident that I am right. But there is still a chance that I am wrong. So what?

Personally I’m not concerned with the precision of the peak oil date. To me peak oil is important only to the extent that it changes economic and lifestyle behavior. Until people, companies, and nations acknowledge that from some point on there will be less oil becoming available each year and we must plan accordingly, the peak oil concept doesn’t mean much in the greater scheme of things.

And as people have pointed out here, we likely won’t know we’ve hit peak oil until some point after it happens and it becomes obvious.

HI Ron,

I think it is rather likely you will be right about this year being the peak.

Are you willing to share your opinion as to how long it will take the MSM to acknowledge the peak?

Of course I will share my opinion on that because I really don’t have an opinion on that. But now that you mention it, I will give it some thought.

Thought……

About a decade or so I suppose.

Hi Ron,

If wrong, it will be only one among many incorrect predictions(not by you, but by many peak oil predictions by others). It won’t really matter, I think there might be a near term peak, but it will be surpassed as oil prices rise. My prediction is 2018 to 2020.

I thought Art Berman’s report, posted near the end of Ron’s last post, is a very good one, worth reading.

A lot of it touched on the shale mal investment, and how it continues due to ZIRP and hype.

That leads me to a specific question, which I think Enno, Freddy or others can answer.

I read some Seeking Alpha articles on shale now and then. It never ceases to amaze me, the hype spinners of shale on that site. In particular, those touting the likes of SD, HK, Magnum Hunter, Linn Energy, and many others that are trading at penny stock levels.

In particular, there is a nice guy over there named Michael Filloon who has a big following. He writes articles that tout increased production rates in the Bakken, and now seems to have also moved to the Permian Basin.

Every once in a while over there in the comments, I do one of my simple calcuations of a Bakken well assuming a certain production rate and certain (low) oil and natural gas price, which always shows the well big time underwater after 60 months, and even worse if interest expense is added.

I try to shoot for what I think is a decent Bakken well, 220K to 250K BO in 60 months, 220K-250K mcf gas in the same time frame, 100% gross working interest, 80% net revenue interest (20% royalty) 10% severance tax, $14K per month non down hole repair OPEX, $100K annual down hole repair OPEX, $2 per BOE g & a.

No one ever questions any of my expense assumptions, even though from looking at Bakken well lease operating statements, those can vary quite a bit depending in particular on amounts of produced water, how it is handled, and down hole failure rates.

However, I am always criticized as to the 60 month production estimates, and usually someone refers me to Mr. Filloon’s articles, which from my experience never go past 6-12 months, other than to mention the dreaded 1 million plus BOE EUR’s that apparently almost every LTO well will achieve after most of us are dead and gone.

Have new wells really gotten much better in the Bakken? Seems like from what I read here, the answer is not much. There is suspicion that new wells are not being properly choked, in order to achieve high IP/early months production, which will likely hurt in the long run.

I guess, for the future, when I get ticked off by yet another Bakken, “Look how Shale R Us is kicking it in the Bakken at $30 oil” article on Seeking Alpha, I would like to be able to use what the people here think would be the best 60 month oil and gas cumulative production amounts.

Also, if anyone has any better suggestions on OPEX, G & A, or net revenue interest (i.e. royalty burden percentages) please advise as well.

I probably just need to quit reading the hype, but it is interesting that Mr. Berman seems to think it is still alive and well and is still, even at sub $40 oil and sub $2 gas in the field, leading to mal investment in the LTO patch. Given that there are articles daily about companies that have .30 stock prices and billions of debt, with recommendations to buy such companies’ equity, Mr. Berman may well be right.

I suppose if we have to live with low oil prices until all the shale locations have been drilled up, that will take many years. It will really be interesting to see the endgame.

I did read an article over lunch about O & G financing in the Oil & Gas Reporter. It looks like, yet again, banks may let a lot of loan covenants slide this fall.

Why do shale companies insist in digging the hole even deeper? It is ridiculous IMO.

I continue to be a proponent of OPEC and Russia targeting $75 Brent, setting that price and adjusting every month, with the threat of abandonment of the target if North American production beings to grow.

I think LTO is such an investment hoax, it will continue to draw money in at $35 or $70. At least at $70, the rest of us who are just trying to mind our own business do not need to worry about the shale hoax.

Michael Filloon is a nice guy, but he has his analyses backwards. From a few nice wells, and company presentations, he draws his conclusions about a whole play or even US shale production. I have never seen him looking at all the available data for a certain play. Only if you look at all the wells in an area in a certain time frame, can you see what is really happening. On average (over all well locations in the play), an operator can only expect an average well. This point seems to be lost on him.

In the following 2 charts I show what is happening in the Bakken (July 2015 data). I show both the average Middle Bakken (MB) well, and the average Three Forks (TF) well, per year in which it got flowing. I chipped off a few data points at the end to include more data (except for 2015), but anyway there are no major differences between years. The point is: these charts include all MB & TF wells (that are currently not confidential), so there is no selection bias. I only include oil, as nobody drills for gas in ND.

In 2015, from what I can see so far (as for confidential wells this is not provided), the split between MB and TF wells is 56 %vs 44%, which was close to 80%/20% in 2008 to 2011. As TF wells are clearly worse, it appears that operators are forced to go for TF wells as well, as MB starts to slowly run out.

Despite improvements in both MB wells, and TF wells, as the focus is slowly shifting to TF, the average Bakken well is not getting much better. Fracs are larger, and also more costly (Continental mentioned a significant increase in completion cost for 2015). Do you see any proof that this makes a big difference in the long term?

On the longer term, there is no proof what these wells can do, and you understand the economics way better than most, incl definitely Michael. From a NPV point of view, it also doesn’t really matter probably what these wells do after year 8 or so. This is because by far the most profit comes from the early rapid flow, when OPEX/BOE is still low, and the time value of money still high. I see clear discrepancies between actual well results, and the results provided in investor presentations by the same companies. Caveat emptor!

Very nice stuff, Enno. Very interesting that 2013 is converging to 2010 after a better start. It chimes with some of our statistical research suggests that IP gaming increased after January 2013 – early month production increases but at the expense of later production.

Having trouble posting the graph, but just did some work to show the percentage difference from the 2010 benchmark of later years. The trends are clear – they are all regressing towards 2010’s cumulative figure, despite beating it early on.

gwalke,

Thanks for your comments, and I fully agree with you. It is a pity that there seems to be such a promotion culture among the public shale companies, but I guess that is what you get with the incentives involved.

If you want to post a picture, I recommend the png format, and make sure the size of the picture is below 50kb. Then there should be no issue.

If you want to post a picture, I recommend the png format, and make sure the size of the picture is below 50kb. Then there should be no issue.

Enno, you have it exactly backwards. The graph below is 43K in Gif, 56K in Jpg and 77K in Png. Png takes more space than any of them, almost twice as much as Gif. That’s why Gif pictures suffer some color distortion. The graph below was posted as a Gif.

What exactly do I have backwards??

I didn’t say png is the smallest format, but it’s still very efficient. But almost all of the graphs I post are png, which means no loss in quality (which jpg will cause), and support of more than 256 colors (which gif can’t).

Well excussssse me. I thought you were explaining the best way to make sure your graph gets posted. If bluehost is limiting the size of graphs it is allowing then the best way to get a graph posted is to make it use as little memory as possible. Png graphs use far more memory space than the others so they are more likely to get rejected.

OK let’s see if this worked. This is the percentage difference in cumulative production for average wells by year, with 2010 as a benchmark. As we can see, the most recent years look swell in that initial stage, but are all trending back towards 2010 levels as time moves on.

and the average for TF wells.

The above applies even more here, as high front month production ends up producing converging or lower cumulative production. As an industry, they are frontloading production and claiming that the gains will be felt across the decline curve – and they are lying.

So, based on these graphs, can someone answer the following questions:

Since 2008, what has been the average annual increase in well performance for MB wells?

Since 2011, what has been the average annual increase in well performance for TF wells?

Hi Enno,

Nice charts, thanks.

Can you remind us what it looks like for all MB and TF wells taken together? For the MB at 12 months it looks like 2014 is about 10% better than 2012, for the TF its about the same, the split is roughly 50/50 so I would think the combined MB/TF average well was about 5% better in 2014 vs 2012 (and 2015 looks similar to 2014 so far). Is that approximately correct?

Hi Dennis,

At the moment, that would not be a trivial exercise, as I had the above graphs ready. But it is indeed just a weighted mix of the above 2 charts.

The wells represented in these 2 charts, constitute about 85% of the overall ND oil production.

Thanks Enno.

shallow sand said:

Well it’s not like we haven’t seen this movie before:

shallow sand,

I fail to understand what all the wailing and gnashing of teeth is about. It’s clarion what’s going on here. What more is necessary for you to see what is happening before your very eyes?

The emotional distress you exhibit very much reminds me of something Reinhold Niebuhr observed:

From the same program linked above, here’s another telling segment:

Glenn: I hope that SS reads your comment. In essence, it is my philosophy. You can only make a lot of money when every one else is wrong. But, you have to be right when that happens – which is not all that unusual for smart people.

Sir John Templeton: You can’t earn above average returns doing what everyone else is doing.

But if there are 1000 things people are not doing, and only 1 will get you an above average return, and it’s totally random . . . . . . .

Everyone learns to manage from the same cookbook. Pretty much everyone who rises high at a company isn’t stupid. But companies still failed pre bailout. Results being dependent on smart decisions vs random decisions . . . not a lot of evidence of it. The list of CEOs hired from a previous spectacular success to then fail miserably is long.

Gets longer in a recession.

Well, at least the Clown Bus is getting smaller:

Glenn. Slept on your words. I’m going to try to take a break from this. I’m really very lucky in total. As I said before, 2003-2014 was a very good run, more than we deserved. Also, very lucky to quit buying while we were ahead. I am aware of many sales 2012-2014 that were financed almost 100% with the assumption of at least $80 oil for thru 2018. We are talking $100K+ per barrel.

I guess the hope on the oil is to live for another day. People that hung on through 1986-1999 were rewarded 1999-2014 and many sold out and retired. If this is a ten or so year down, ok.

I’m not so sure what is clarion. There is a lot of gloom and doom here, so maybe end of the world as we know it is what you mean?

Hi shallow sand,

Clarion it is that bankers are in the business of creating debt, and sometimes that can become very pernicious.

Debt is their product, just like yours is oil. If they don’t create new debt, then there is no way to grow and expand their business.

The rub is that debt, for the aggregate economy, is a double-edged sword. It can be thought of like white blood cells. A little debt, under the right circumstances, is good, even necessary to spur on growth in the real economy. Too much debt, however, is deadly.

The finance sector, needless to say, is loathe to admit this. To do so would dampen its growth prospects. One always has to keep in mind a key fact: the finance sector’s product is debt, and for it to grow it must produce more debt.

The onslaught of producing grotesque amounts of debt began in earnest in the U.S. in the 1980s. From the graph I have attached below, one can see that in 1985 the finance sector garnered only 10% of the nation’s corporate profits. By 2003 it’s share had grown to more than 30%, and has since fallen back to about 20%.

But the finance sector, needless to say, is not happy with the loss of this part of the nation’s profit pie. It would like to garner a much larger share of the profit pie. Blowing debt bubbles in the oil and gas sector, in the EMs, and in other sectors which produce primary materials is its way of maintaining and attempting to grow debt, and thus its profits.

Keep in mind that these inordinate profits of the finance sector are profits that other sectors — manufacturing, mining, retail, IT, transportation, etc. — are deprived of.

But depriving productive sectors of the economy profits is only part of the harm that a bloated finance sector causes. For as it grows and consumes an ever-increasing share of the nation’s profits, it also begins to capture and exert growing influence in other areas of the society and culture which lie outside the economic realm: in the intellectual, religious, social, political and military realms. Thus an overgrown finance sector has a corrosive effect on the very knowledge, values, morals, and ethics that underpin the society.

For instance, we know that maximizing aggregagte utlity is the holy grail of classical economics, of capitalism. But it is quite clear that an overly-indebted economy is an impediment to achieving this goal. It thus becomes incumbent upon “the lords of capital and their hired liars and bumsuckers,” as Orwell called the assortment of economists, evolutionary scientists, preachers, etc. which financiers gather around them, to create “facts” which are, in reality, defactualized.

As Neibuhr noted:

[T]he intelligence of privileged groups is usually applied to the task of inventing specious proofs for the theory that universal values spring from, and that general interests are served by, the special privileges which they hold.

This is what is clarion to me, but maybe not so much to others.

http://www.yardeni.com/pub/ppphb.pdf

Here’s a graph from Kevin Phillips’ Bad Money which shows the grotesque amount of debt the U.S. has built up since the 1980s.

As Phillips notes, when he uses the phrase “bad money,”

Money is “bad,” in the historical sense, when a leading world economic power passing its zenith — before the United States, think Hapsburg Spain, the maritime Dutch Republic, and imperial Britain just before World War I — lets itself luxuriate in finance at the expense of harvesting, manufacturing, or transporting things. Doing so has marked each nation’s global decline….

“Bad” in the sytemic sense further applies to letting a financial elite elevate, expand, and entrench itself as a country’s GNP- and profits-dominating sector. Doing this so hurridely has wound up institutionalizing runaway public debt and private debt, gross speculative biases, tenfold and twentfold leveraged gambling, unchecked and barely regulated “product” innovation, and a tendency toward periodic panics and instability…. As for the financial sector’s behavior in such circumstances, surely there must be some applicable variation of Lord Acton’s famous thesis about the greater the power, the greater the abuse and corruption.

The growth of the financial industry has been a boon for its highly-paid managers.

According to New York University economist Thomas Philippon, “total compensation of financial intermediaries (profits, wages, salary and bonuses) as a fraction of GDP is at an all-time high, around 9% of GDP.”

http://www.tcf.org/blog/detail/graph-how-the-financial-sector-consumed-americas-economic-growth

Great post.

I said great post, but didn’t indicate which post I was referring to and it got buried down the thread.

It was this post.

Debt is their product, just like yours is oil. If they don’t create new debt, then there is no way to grow and expand their business.

shallow sand,

In my view it is important to understand what kind of game is currently going on. It is clear that many shale companies are not sustainable when oil prices are below 50 USD/barrel. So, the strategy of many companies is to woo as many private investors as possible with stories about flooding the market with cheap – but economical – oil and gas through high efficiency. At some point many companies will go bankrupt and the small investors will be holding the bag. Yet, the companies will still produce and the smart money can come in buying debt free companies, which are much more competitive. This has happened already with Samson, where 10000 small investors have lost 7,2 bn. Yet the company is still producing under new owners, who own now are much better company. So, it is very important to be out of the sector and wait until the storm is over.

Is it only me who were surprised by the EIA today? Lower 48 flat and Alaska +19.000/day

the weekly numbers have a very high error margin (as the EIA explains), so I would not read too much in them.

Unfortunately the market does, but it does some crazy things so. Can someone answer what differs in the data collection/projections/calculations between the API numbers and the EIA? Thanks

Agreed. I’ll take a figurative chill pill.

This post was a reply to Glenn and clueless. Somehow it ended up here.

I would not be TOO surprised if the spot price of oil falls down to the twenty dollar range – for a VERY short period of time, maybe a few weeks. There could be bad economic news and people who are stuck with big inventories and incoming deliveries might have to have a fire sale – but fire sales by their very nature are short lived affairs.

Now let us suppose we are the ministers running a nationalize oil company, and our direct day to day expenses are forty dollars a barrel, and we are getting thirty five. We might want to keep producing and selling in order to prevent civil disruptions in our country, to avoid laying off men, mothballing equipment, maybe damaging some wells permanently. I am not too sure about that last but the hands on guys indicate it does happen.

It is perhaps possible to make up that five bucks by deferring maintenance, raiding certain accounts such as ones holding retirement funds, or by selling some assets such as a water treatment plant or something.

Immediate panic could be avoided, and there would be a strong hope that prices would soon go back above day to day break-even .Relationships with buyers and shippers would be maintained.

BUT- suppose the price DOES drop to twenty bucks- the loss would be so great that we as ministers or managers would be COMPELLED to just shut in our oil, excepting maybe a little for domestic consumption or some delivered to close allies and friends for reasons having to do more with the alliance than the money. We might swap some for grain or meat if we are food importers.

But in the main we would HAVE to shut down, pretty soon, because we would be losing our pants as well as our shirts by continuing to produce. Losing the shirt is one thing, the shirt PLUS the pants is another altogether.

I am guessing but my guess is that a very significant portion of the oil produced on a day to day basis is produced on an ongoing cash expense basis that exceeds thirty to forty dollars. This portion is something I can only guess at -twenty percent? thirty percent? Maybe ever forty percent ?

It seems extremely unlikely that ANYBODY or any combination of anybody’s has the ability to increase production enough to make up for the loss of five or ten million barrels per day.

Doesn’t it seem reasonable to predict that a price below thirty bucks would result in millions of barrels a day being shut in on fairly short notice?

So I believe there is basically a near zero chance that oil will go below thirty five or forty bucks for any significant period of time. Hundred car and five hundred car freeway crashes do happen of course- and something similar by analogy could happen in world oil markets forcing prices WAY down for a LITTLE while.

http://www.nytimes.com/2015/09/24/sports/baseball/yogi-berra-dies-at-90-yankees-baseball-catcher.html?_r=0

I would never have predicted that.

From Bloomberg:

Oil Drillers’ Credit Lines to Shrink as Banks Revalue Assets

http://www.bloomberg.com/news/articles/2015-09-23/oil-producers-credit-lines-to-shrink-as-banks-revalue-reserves

Oil producers in the U.S. are about to see their credit lines shrink, just when they need the money most.

The latest round of twice-yearly reevaluations is under way, and almost 80 percent of oil and natural gas producers will see a reduction in the maximum amount they can borrow, according to a survey by Haynes and Boone LLP, a law firm with offices in Houston, New York and other cities. Companies’ credit lines will be cut by an average of 39 percent, the survey showed.

Lenders are using $48 a barrel to value assets in the third quarter, down from $77 at the end of last year, according to a quarterly bank survey from Macquarie Group Ltd. And reserve growth has slowed because companies are spending less on drilling. The redetermination, which takes place around April and October, comes as investor appetite for energy company debt is fading.

Whiting Petroleum Corp. may see the maximum amount it can charge on its credit line lowered to $3.75 billion from $4.5 billion, James Volker, the Denver-based company’s president and chief executive officer, said in a Sept. 9 presentation.

The biggest risk is to borrowers that have already tapped their credit lines. If the borrowing base is cut to less than it already owes, the company will find itself abruptly facing a large repayment.

The biggest risk is to borrowers that have already tapped their credit lines. If the borrowing base is cut to less than it already owes, the company will find itself abruptly facing a large repayment.

That’s default territory.

wait there’s only 1.4 TB oil but 3.2 TBOE of gas/condensate in the 733 largest oil fields? really? i thought there was more oil than gas in the ground…

There is. I don’t bother with BOE, it’s a bullshit number. Look at the molecules and their mass. There’s more mass in oil. This gets complicated, gas recovery factor is a lot higher, it moves better from source to trap, and it also escapes the trap a lot easier. But if more means mass, there’s more oil mass.

i am talking about BOE in the ground, a unit of energy, and the most relevant metric. the numbers given here are obviously wrong. the 56 giant fields have 786 GB oil and 917 GBOE, but the 738 large fields have 1.4 TB oil and 4.7 TBOE, not even counting the gas only fields? i think they accidentally multiplied gas/condensate by a factor of 10.

So you are talking about the BOE in place? Not recoverable?

yes. keep in mind these are the giant OIL fields, not gas fields. i believe it is thought that there is more original extractable oil in place than gas, especially because we’ve extracted so much more oil. less is known about gas, and reasonable people don’t assume massive quantities of gas if we don’t actually know what’s available. what is absolutely certain though is that we have used up a lot more oil than gas, and the numbers quoted in the article are not consistent with this fact.

My comment up the thread on actual crude oil versus liquids associated with gas production, condensate & NGL:

http://peakoilbarrel.com/jodi-data-and-giant-field-depletion/comment-page-1/#comment-539573

RBN has a new current production chart by natural gas region. This would be a lot more useful if they defined the regions. The difference between Utica region and NE PA production is rather striking, especially as there are currently around 9 rigs working NE PA, depending on where you draw the boundary, and around 19 currently working OH according to Baker-Hughes, who say their data is from RigData. Their location data shows all of them in the EIA Utica region.

The current EIA “Drilling Productivity Report”, on the other hand, for some reason reports the current number of Utica rigs as 5.5. I believe that I have figured out how to calculate the number of rigs drilling in the Utica area, as reported in the EIA report.

Using the spreadsheet data, take the change in output over the previous month, add the monthly decline for that month, and divide by the reported rig productivity. This will give the number of rigs for 2 months prior. For example, for the August 2015 rig count, B106=(H108-H107-G108)/F108. This works back to Jan 2015, but not before then. I assume prior reported rig counts are actually measured and not calculated values.

In other words, the EIA rig counts reported for the Utica region for 2015 are exactly the rig counts necessary to match their smoothed production and rig efficiency model, with a 2 month delay. The connection to the actual number of rigs remains mysterious.

Month Baker-Huges Ohio EIA Utica Rig Count Calculated EIA Rig Count

Jan 45 25.6 25.5990949835

Feb 37 21.25 21.2509381696

Mar 31 18.0 18.0001687556

Apr 26 13.75 13.7497686263

May 24 12.6 12.6007535201

Jun 20 10.5 10.500347427

Jul 19 7.2 7.199513278

Aug 19 5.5 5.4998439337

Blaine

There may come a time, hopefully sooner rather than later, that the distinction between the Marcellus, the Utica and the Upper Devonian formations are more clearly identified.

Some analysts are projecting that Utica output will soon surpass the Haynesville to become the second largest in the country after the Marcellus.

Interestingly, there is a deeper formation, the Trenton Limestone (sometimes referred to as Trenton Black River) that has a very long and productive history. Several of Shell’s wells in Tioga county target both the Utica and the Trenton on their permits.

In 2006, a well, the Stoscheck 1, targeted the Trenton and produced 8 Bcf its first 18 months.

This well still puts out 600,000 cfd and is located across the border in NYS.

Thank you, Blaine. I have been disturbed by this weirdness for some time.

From the footnotes at the footnotes at the end of the September 2015 EIA Drilling Productivity Report:

3. The monthly average rig count used in this report is calculated from weekly data on total oil and gas rigs reported by Baker Hughes.

Obviously this is a lie. There are 14 gas directed rigs in the Utica according to the last Baker Hughes report. EIA says that one rig will add 7,484 per month. Those units are Kcf/d. That should add 104,776,000 cf/d. Legacy decline for October is projected by EIA to be 44,715 Kcf/d and total production is expected to be roughly 3.5 Mcf/d lower, an extremely modest decline. However, 104.8 Mcf/d of new production is a lot higher than the 44.7 Mcf/d decline and would actually project a total Utica production of 60.1 Mcf/d higher.

So either the EIA does not have a clue about how productive the rigs are or they don’t have a clue about how much gas will be produced. They obviously don’t care that their published rig counts radically mismatch Baker Hughes. What should we do to figure out what is really happening?

EIA uses only the total, and ignores the gas/oil label, so their rig number should be 19.

Mostly the EIA is just rehashing the state data. You can go download the OH numbers directly. It’s only available quarterly, so most recent are Q1 and Q2 2015, and I had a look at these.

The rig count is just wrong. The other numbers don’t look off by that much. Obviously the rig count being off will throw the rig productivity high and the production projections low. I’m only seeing around 5% monthly decline in the larger wells which are off plateau, which is relatively low.

The rig count was up really high for a long time without much production to show for it, which seems hard to square with the claimed high productivity. On the other hand CHK had 490 flowing wells in OH in 2Q 2015, more than half of the wells in the state, and mostly in Harrison, Jefferson and Columbiana counties. The average flow was 1866 mcf and 49 barrels “oil” per day. None of these are that old, and the decline rate isn’t that high either. The same stat for the non-CHK wells gives 3287 and 65. I think I can figure out where the wasted drilling effort went.