Many different oil shock model scenarios have been presented over time at Peak Oil Barrel. Information on the Oil Shock Model, originally developed by Paul Pukite can be found in Mathematical Geoenergy. The future is unknown, so future extraction rates from conventional (excludes tight oil and extra heavy oil) oil producing reserves are unknown. Also not known are future oil prices which will affect the amount of tight oil and extra heavy oil that is ultimately produced.

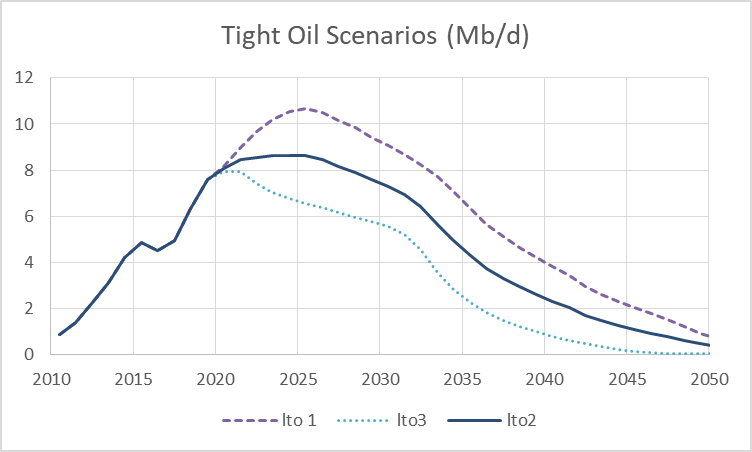

For tight oil I have created three scenarios corresponding to a low, medium and high oil price scenario. Likewise I have created three scenarios for extra heavy oil which correspond to the same low to high price scenarios used for the tight oil scenarios.

The mean estimates by the United States Geological Survey (USGS) for technically recoverable resources in tight oil plays combined with reasonable economic assumptions and data gathered from www.shaleprofile.com are used to model tight oil output. The EIA’s AEO 2018 reference oil price scenario is used for the high oil price case and the low scenario uses the AEO reference price case up to the date when it reaches $70/b in 2017$ and assumes oil prices remain at $70/b for all future dates. The medium oil price scenario is the average of the low and high price cases.

The high tight oil scenario is lto1 and corresponds to the high oil price scenario, likewise lto2 and lto3 are the medium and low tight oil scenarios respectively and correspond to the medium and low oil price scenarios.

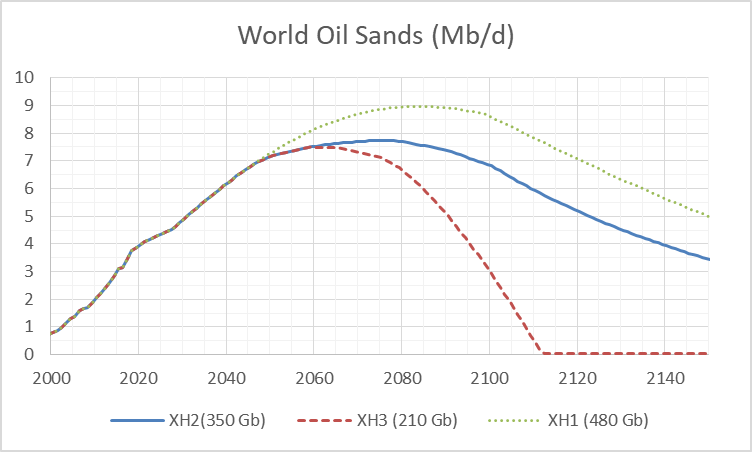

For oil sands I use an oil shock model with 500 Gb of resources discovered initially and it is assumed that development of the resource is very slow with an average time from discovery to a barrel becoming part of producing reserves set at 100 years with a maximum entropy probability distribution used for the statistical spread in the years from discovery to mature producing reserve. The year for the start of the producing reserves being developed is set to 1960 with output starting in 1967, extra heavy oil production data was gathered from papers published by Jean Laherrere for Venezuela and from the Canadian Association of Oil Producers (CAPP) for Canada.

Jean Laherrere for many years used a 500 Gb estimate for extra heavy oil URR, this was recently revised to 215 Gb. I have used 200 Gb for the low estimate, 500 Gb for the high estimate, and 350 Gb for the medium tight oil estimate. Forecasts by CAPP were used as the basis for future Canadian oil sands output through 2035, Venezuelan output is assumed to grow very slowly until 2030 and then roughly follow the path of Canadian oil sands output from about 1000 kb/d to 4000 kb/d over 30 years. It is assumed that Canadian Oil sands output flattens after 2040 and declines after 2050, Venezuela’s output mimics the Canadian output path with a delay of 25 years (peak in 2065 and decline in 2075). The low , medium and high scenarios are created by using low, medium and high extraction rate scenarios where it is assumed that low oil prices result in lower extraction rates and high oil prices result in higher extraction rates due to increased profits.

XH1 is the high oil sands scenario, XH2 is the medium scenario, and XH3 is the low scenario. The scenarios have URRs of 210 Gb, 350 Gb, and 480 Gb for the low, medium and high scenarios respectively.

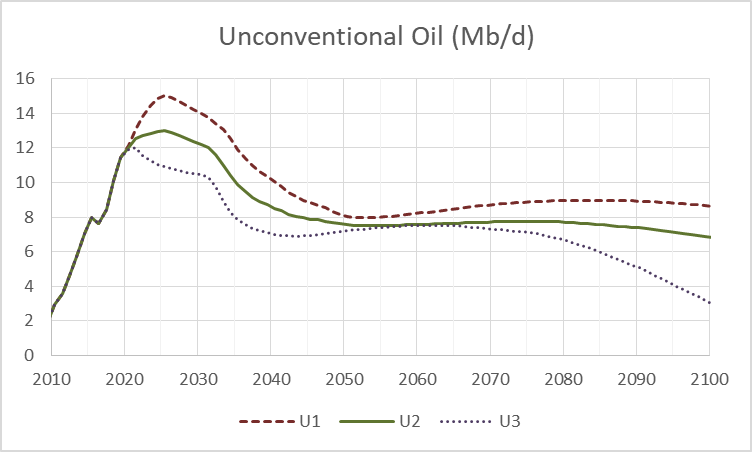

The tight oil and oil sands scenarios are combined into 3 unconventional oil scenarios where

U1=lto1+XH1 = high unconventional oil scenario

U2=lto2+XH2 = medium unconventional oil scenario

U3=lto3+XH3 = low unconventional oil scenario

I define conventional oil as all crude plus condensate (C+C) that is not tight oil or extra heavy oil (API gravity of 10 degrees or less). For my low estimate of conventional resources I use a Hubbert Linearization which results in about 2500 Gb for conventional URR. The USGS estimated about 3000 Gb of conventional oil resources in 2000, I add 100 Gb to this estimate for 3100 Gb for my high conventional oil resource estimate and my medium estimate is 2800 Gb for conventional oil resources.

Using these resource estimates and backdated oil discovery data, a dispersive discovery model can be fit to discovery data, with cumulative discovery modelled to match the low, medium, and high oil resource estimate. An oil shock model can be applied to the discovery model and production data to estimate past extraction rates that correspond with discovery and output data. Future output will depend on future extraction rates from proved producing reserves which are generated by the model assuming stochastic behavior following a maximum entropy probability distribution for the development rate of oil resources. Future extraction rates might increase, decrease, or remain constant. Past behavior shows an increase in extraction rates from 1960 to 1973, a sharp drop from 1979 to 1984 and then a gradual drop from 1985 to 2007, extraction rates have been flat to slowly rising from about 2013 to 2018, but we can only guess at future extraction rates. A conservative guess would assume the extraction rates will remain at 2018 average rates going forward.

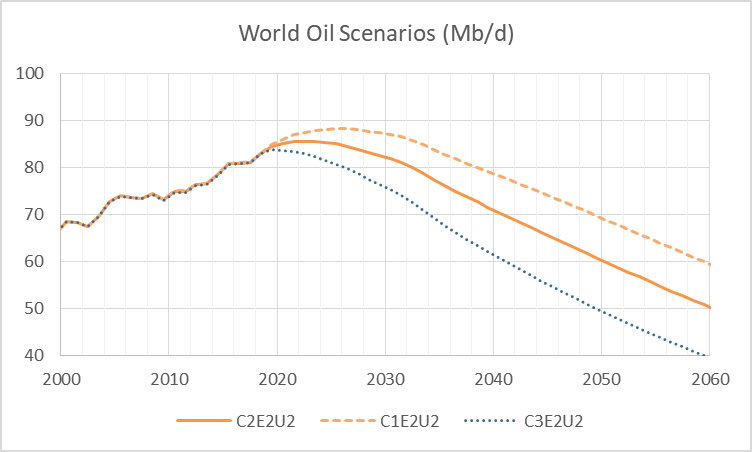

The models presented below will use the following convention for labels C1, C2, and C3 denote the high, medium, and low Conventional (C) oil scenarios respectively. Likewise E1, E2, and E3 will denote a high, medium, and low extraction rate scenario respectively, where E1 has extraction rates increasing until a peak in output is reached and then remaining flat after the peak, E2 has constant extraction rates, and E3 has extraction rates decreasing to nearly zero over time. The rate of increase or decrease is matched with the model’s rate of decrease in extraction rate over the 1985 to 2007 period with the extraction rate being gradually increased (or decreased) to this rate (the absolute value of that rate) and then gradually flattened towards a zero rate of change over time.

A model denoted C2E2U2 would suggest URR for conventional resources is 2800 Gb (medium scenario), constant rate of extraction from producing reserves (E2) and a medium URR for unconventional resources (U2) of about 450 Gb from 1967 to 2300.

Below I present 3 models, C1E2U2, C2E2U2, and C3E2U2, the only change being the conventional URR in each of the models with URRs (for C+C) of 3500 Gb, 3200 Gb and 2900 Gb respectively. The high model peaks is 2025 at 88.2 Mb/d, the medium model peaks in 2022 at 85.4 Mb/d, and the low model peaks in 2019 at 83.7 Mb/d with the constant extraction rate assumption.

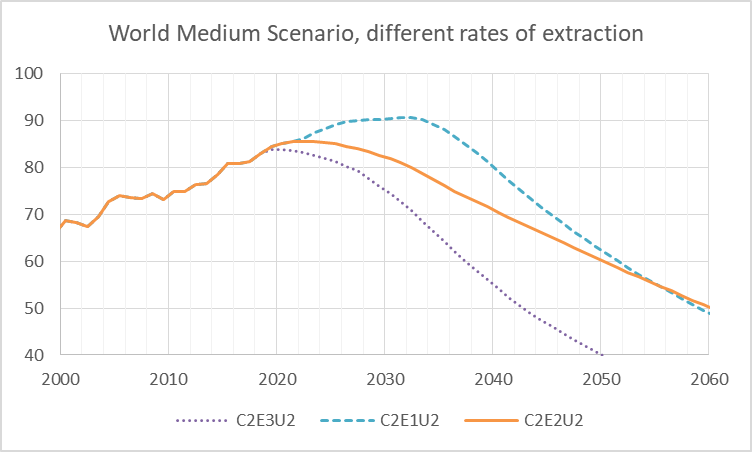

As an example of how changes in extraction rate can change the output path we will focus on the medium (C2) model with medium unconventional resources (U2) with all three extraction rate scenarios (E1, E2, and E3).

The low extraction scenario (C2E3U2) has lower a lower URR of 2600 Gb than the medium and high extraction rate scenarios (URR=3200 Gb). The medium scenario is unchanged from the previous chart, the peak of the low scenario is in 2019 at 83.1 Mb/d and the high extraction rate scenario peaks in 2032 at 90.6 Mb/d.

High extraction rate scenario with extraction rate on right axis, the low extraction rate scenario is below.

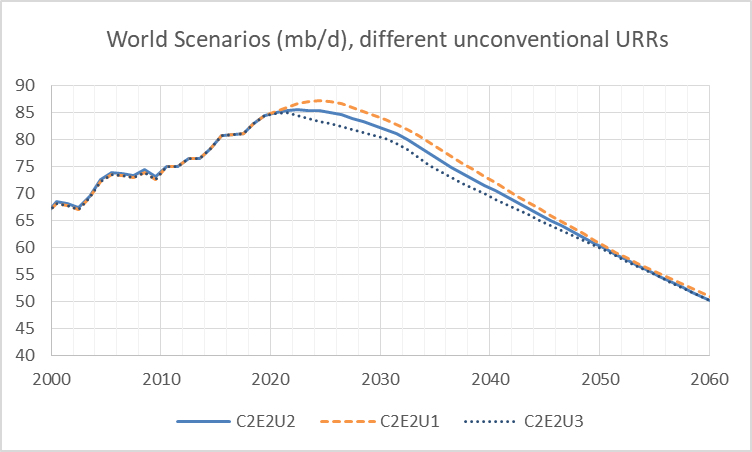

We often make much of tight oil and oil sands output, but as we show below, they have only a small effect on the peak. We choose the C2E2 model and vary the unconventional scenario from U1 to U3, so we have C2E2U1, C2E2U2 (presented in several charts already), and C2E2U3 in the chart that follows.

The C2E2U2 Scenario peaks in 2022 at 85.4 Mb/d, the C2E2U3 scenario peaks in 2021 at 84.9 Mb/d and the C2E2U1 scenario peaks in 2024 at 87.1 Mb/d, the URRs vary from 3060 Gb to 3600 Gb, but the output from 2019 to 2060 is affected very little from this difference.

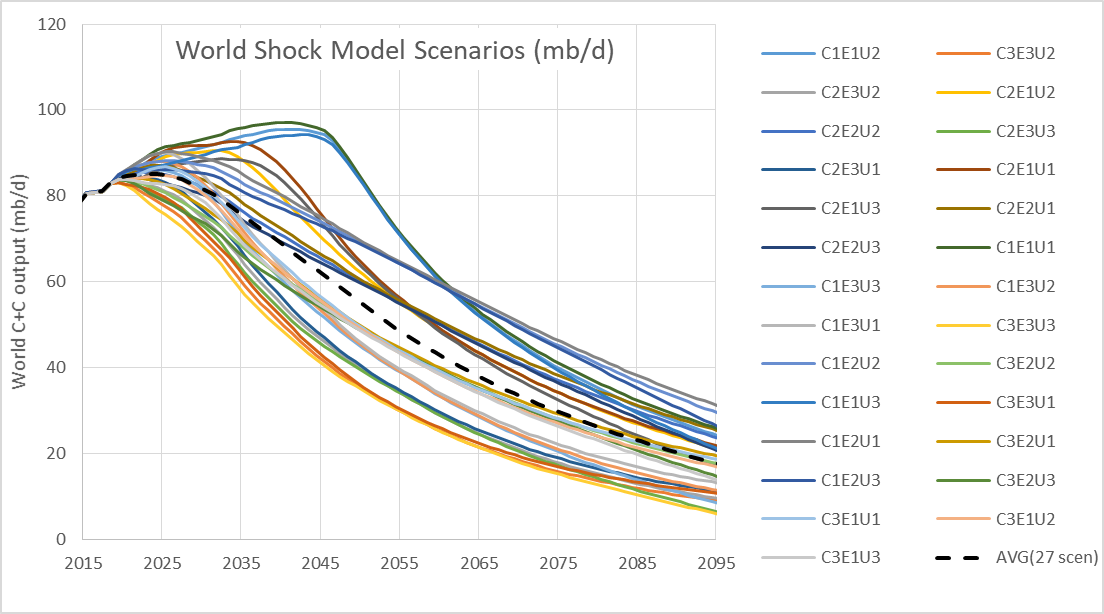

The combination of C1, C2, and C3, with E1, E2, and E3, and with U1, U2, and U3 allows 27 different scenarios to be created.

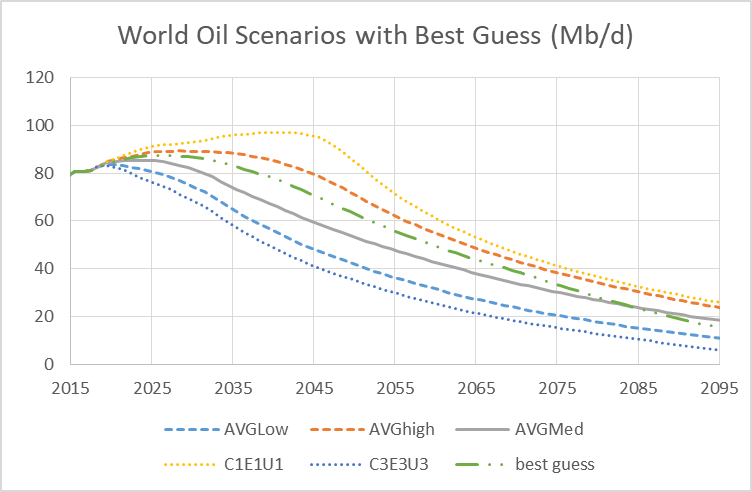

I realize this chart is not very readable, the point is to show the spread of the various possible models, there is fairly dense coverage of the envelope from 2019 to 2040. Note the dashed black line which is the average of all 27 scenarios. The ensemble average has a URR of 3000 Gb and peaks in 2023 at 85 Mb/d, the average scenario has a plateau between 84 and 85 Mb/d from 2019 to 2026.

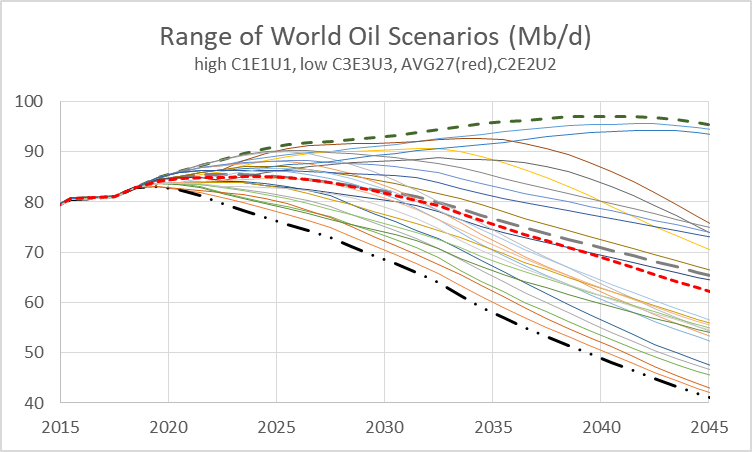

Chart above shows the range of the scenarios with the dashed lines called out in the title. The high black dashed line is scenario C1E1U1 and the low dash and two dot line is C3E3U3, the middle dashed gray line is the C2E2U2 medium scenario and the red dashed line is the 27 scenario average.

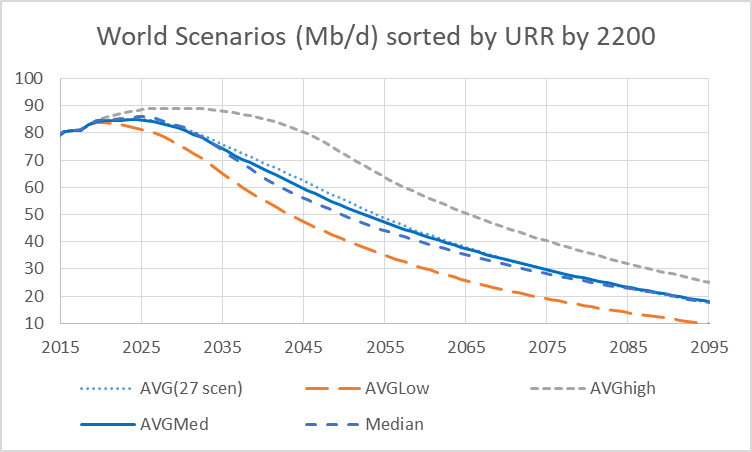

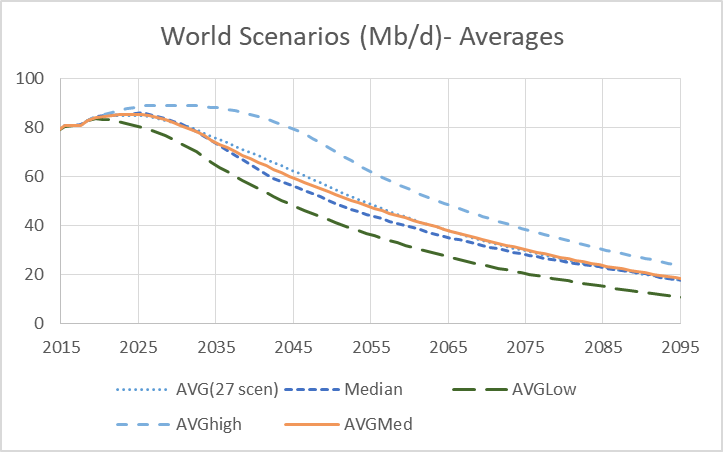

The chart below takes the scenarios sorted from high URR to low URR (through 2200) and then finds the average of the highest 9 scenarios (AVG high), the average of the middle 9 scenarios (AVG med), and the average of the lowest URR scenarios (AVG low).

The median scenario takes the median of all 27 scenarios at each individual year, it has a URR through 2200 of 2900 Gb, peak output of 86 Mb/d and peaks in 2025, the 27 scenario average has a URR of 3000 Gb, peak output of 85 Mb/d in 2023. For the AVG Med 9 scenarios URR is 3000 Gb, with peak output of 85 Mb/d in 2024. The AVG High 9 scenarios URR is 3400 Gb with peak output of 89 Mb/d in 2028. The AVG Low 9 scenarios URR is 2600 Gb with peak output of 84 Mb/d in 2019.

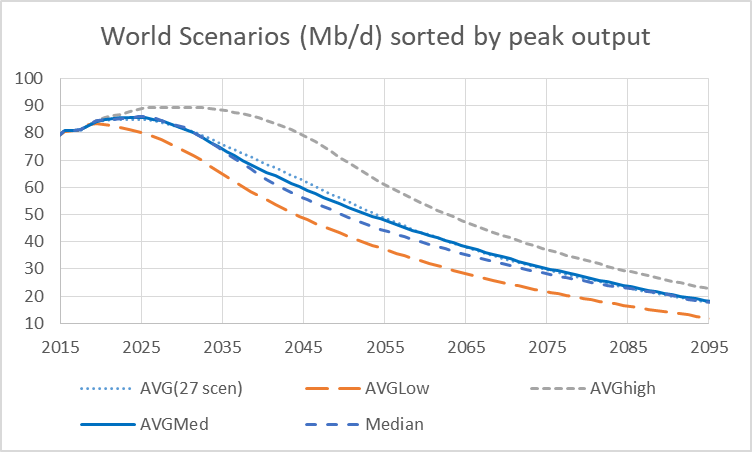

The next chart sorts scenarios by peak output and then groups by top, middle and low 9 scenarios based on peak output.

For AVG Med URR is 3000 Gb with peak output of 86 Mb/d in 2024, AVG High URR is 3300 Gb with peak output of 89.5 Mb/d in 2028, and AVG Low URR is 2700 Gb with peak output of 83.5 Mb/d in 2019.

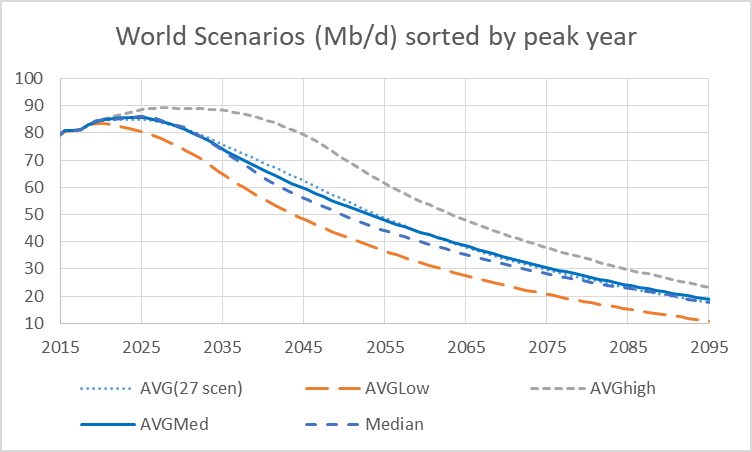

Chart below sorts scenarios by peak year and splits scenarios in 3 groups of 9 from latest to earliest peak year.

For AVG Med URR is 3000 Gb with peak output of 86 Mb/d in 2023, AVG High URR is 3300 Gb with peak output of 89 Mb/d in 2028, and AVG Low URR is 2700 Gb with peak output of 84 Mb/d in 2019.

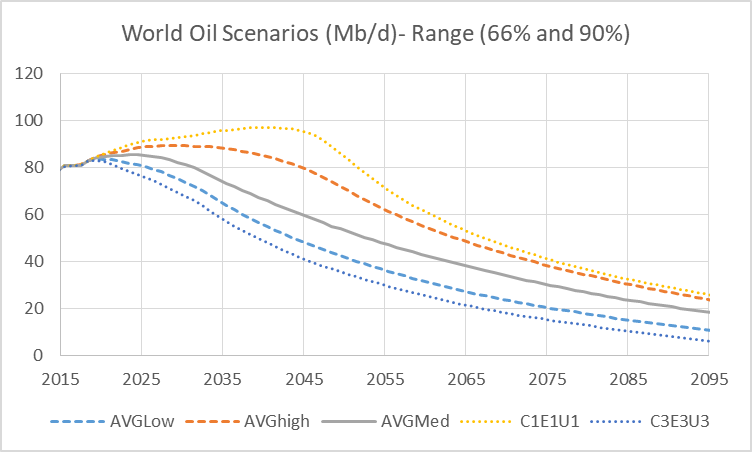

As it is not clear which sorting method gives the greatest insight, the chart below takes the average of the 3 methods where AVG Low takes the average of the 3 AVG Low scenarios in the 3 previous charts, the same is done to find an AVG Med and AVG High scenario. The envelope between the AVG low and AVG High scenarios might represent about a 66% probability that World output will fall within that envelope, with perhaps a 17% probability that output might be either above or below the envelope.

The AVGMed scenario URR is 3000 Gb with peak output of 85.4 Mb/d in 2023, AVGHigh URR is 3400 Gb with peak output of 89.2 Mb/d in 2028, and AVGLow URR is 2600 Gb with peak output of 83.6 Mb/d in 2019.

The dotted lines are the highest and lowest of the 27 scenarios presented and might represent a 90% confidence interval, so perhaps a 5% probability that output might be higher than the yellow dotted line and about a 5% probability it might be lower than the blue dotted line. The dashed lines may represent a 66% confidence interval with the gray solid line roughly representing the 50/50 line where there is an equal probability output might be above or below that line.

Note that these are subjective probabilities as we have no statistical data on future output. I have simply assumed in the absence of any knowledge of the future that each of the 27 scenarios presented is equally likely. In reality the lowest and highest scenarios are probably less likely than the medium scenarios so this is a conservative assumption.

My best guess for future World oil output in the absence of a major economic crisis in response to peak oil has extraction rates gradually rising from 2025 to 2045, remaining flat until 2050 and then decreasing at a gradually increasing rate. The extra heavy oil scenario that I believe is most likely is 210 Gb with a tight oil scenario of about 85 Gb (these correspond with the XH3 and lto1 scenarios presented earlier.) Conventional oil with the extraction rate scenario I believe most likely has a URR of 2700 Gb, with the World C+C scenario having a URR of 2985 Gb through 2200. Scenario presented in chart below.

Chart below shows where this “best guess scenario” falls relative to the 27 scenarios presented earlier.

The best guess scenario peaks in 2026 at 87.3 Mb/d. Output remains on a plateau between 86.5 Mb/d and 87.3 Mb/d from 2022 to 2030 in the “best guess” scenario. A safer guess for the peak in World C+C output would be 2024 to 2028, if this guess is close to being correct. A severe recession between starting any year after 2023 would probably mark the peak in World oil output.

391 responses to “Oil Shock Model Scenarios”

excellent!

Thanks Fernando.

https://www.woodmac.com/news/feature/non-opec-decline-rates-remain-stable-until-2020/

What we have seen is low oilprice also increase decline rates as maintenance work are skipped to save money. As I see todays oil production is about 80.6 mbpd and your best suggestion is peak at 87.3. According to EIA oil demand grows with aproximately 1.5 Mbpd. It should than remain 4.3 year or 2023.

Freddy,

From 1983 to 2018 the average rate of increase in World c+c output was 800 kb/d each year.

So that would be about 5 years if the rate continues to increase linearly. It is likely to gradually slow over time as the peak approaches. Perhaps 800, 700, 600, …, 200,100, 0.

Freddy,

In 2018 World C+C average output was about 82.84 Mb/d, so my “best guess” (which could indeed be incorrect) scenario sees an increase of 4.46 Mb/d from 2018 to 2026. An average annual rate of increase of 637 kb/d. Over the past 10 years the average annual rate of increase in World C+C output (2009 to 2018) has been 854 kb/d. Over the past 36 years the average annual rate of increase has been about 816 kb/d. As oil supply becomes short and oil prices increase we may see a gradual decrease in the rate of increase in oil consumed. We cannot consume more oil than is produced except by drawing on oil stocks and those are limited.

From 2019 to 2030 the output in Mb/d is as follows for my best guess scenario:

84.29

84.98

85.82

86.47

86.89

87.18

87.32

87.34

87.25

87.11

86.81

86.48

I have two other models which are pointing to 2023 as peak oil demand.

Dennis’s analysis in this post…isn’t really any good. It’s making the same mistake the oil companies are making: it’s not taking peak demand seriously enough. You can’t just Wild-Ass-Guess three supply-based scenarios based on the assumption that lower demand means lower drilling: we know from the frackers that sometimes they’ll drill more even as profits disappear. If you seriously assume that the market will balance after filling storage, then you have to run a pure demand-based model; after storage fills, supply will have to be shut down to match demand, period. (Rational companies would have been doing this already, but there are a lot of irrational companies.)

Nathaneal,

I have also analyzed peak demand, a realistic model does not arrive at peak demand until 2035 under very optimistic assumptions. If you are correct about peak demand and it occurs before 2026, then output will simply follow one of the lower scenarios which peak as early as 2018 for the lowest cases. Perhaps 2023 might be correct, it is possible that neither of our best guesses will be correct, the possible future scenarios are literally infinite so the odds of being correct are approximately zero.

Thanks for sharing your models!

I think you are right when you predict peak demand at earliest 2035.

Not many, if any, do stochastic models, which takes into account uncertainty.

World oil reserves could be unlimited, but if the cost of obtaining the oil grows faster than the economic benefit that can be obtained from it, Peak Oil will still take place regardless of reserves. That’s why I think oil reserves are irrelevant for Peak Oil and plenty of oil is going to stay in place. It will not be extracted because the economy will not bid its cost of extraction.

Javier

Correct reserves are the oil that can be extracted profitably. Technically recoverable resources are not the same as economically recoverable resources. URR=ERR.

When the cost of substitution drops low enough, there are no economically recoverable reserves.

Nathanael,

There are a number of uses that are difficult to substitute such as air travel, farm equipment and so forth. There is some oil which is quite in expensive to extract in the middle east and in Russia and even some US onshore resources. Those resources will still be economically recoverable even at $20/b in 2017 $.

above I said “in expensive” and meant to say “inexpensive” ie there are cheap oil resources in the Middle East and Russia, probably profitable at $20/b in 2017$, not enough for 80 Mb/d, but probably adequate to provide 20 Mb/d for 30 years or more.

Nice try, Dennis! Great effort. Thanks for putting all the labour in this post.

Future will tell if you’re right or wrong, that’s the way it works 🙂

You know my point of view: oil production is not price related. Nevertheless I like people publishing their ‘best guess’ about the global predicament of peak oil, based on whatever reasonable idea they may have.

Verwimp,

Interesting.

I am pretty sure oil prices change the amount of oil produced.

Maybe producers could chime in.

Perhaps I am wrong.

There is some connection between production and price, but there is an awful lot of play in the market. The cost of oil is much lower than the price consumers are willing to pay in a pinch.

This explains why the oil industry is so profitable. It allows “rent taking”. It also explains why sudden lurches in the price are possible. They are based on trader psychology not supply and demand.

The huge gap between cost and value to the consumer is visible in Europe, where very high taxes on fuel at the pump fail to dissuade consumers from wasting the stuff. The gap results in much of the resource being squandered on oversized vehicles designed to be ego boosters or status symbols.

I am thinking more about oil supply. I assume demand will continue to grow at an annual rate of 800 kb/d each year until high oil prices destroy enough demand to balance with available supply. This is likely to be the case until peak oil is reached between 2024 and 2028. I do not expect substitution will lead to prices falling before 2045. It will take time to replace 1 to 2 billion ICEVs.

Right, I don’t comment on oil supply directly, since I don’t know much about it. As mentioned elsewhere there is some connection between price and supply.

I expect substitution to start having a big effect by the late 2020s. I expect the number of ICE vehicles on the road to stop growing before that — maybe even as early as 2023, depending on battery production, and also on the autonomy wildcard. This sounds a little like science fiction, but just look how the car industry is panicking right now.

Alimbiquated,

I agree. For all road transport oil use, I have the peak in my model in 2026, but demand and supply fall at the same rate until about 2032, after that demand falls faster than oil supply leaving a demand gap and excess oil supply, then oil prices start to fall, potentially this could limit the adoption of BEVs, though it depends upon how fast the prices of EVs fall, it may be that by 2033 EVs are considerably cheaper than ICEVs and the price of oil may not longer have any effect on their adoption as the capital cost of the vehicle may be considerably lower and EV charging infrastructure may have been built out making adoption easier.

It will be interesting to watch.

Substitution is not about EV alone.At least in developing countries like India where I stay it is about public transport,ride share, railway electrification etc .In densely packed cities and towns of India public transport provides the desired frequency to act as an alternative.

I, too, think there is too much focus on substitution linked to EVs. People don’t have buy EVs. They just have to drive ICE vehicles less or at least switch to far more efficient ICE.

Much driving could be eliminated altogether. We will be okay if all recreational driving ends, if necessary trips are consolidated into fewer of them, etc.

Life would be different with less driving, but certainly survivable. And if people did more human powered transportation, they would be healthier.

Boomer,

I agree it will be a combination of substitution (in all forms, public transport, walking, biking, ride share, car pool, and EVs) as well as using transportation less and choosing more efficient means of transport.

It is difficult to model all of these factors, a choice of focusing on EVs alone would tend to give a high end estimate of demand for oil because many other means of transport and increased efficiency are ignored. Note that the effects from all the other factors you mention have been in place over high oil price periods so we can see how they have affected things in the past. From 1980 to 1985 we saw a dramatic reduction in the proportion of primary energy supplied by oil use, in later periods such as 2007-2008 and 2011-2014 the effect was less dramatic. It is unclear if we will see oil prices that are high enough for the non-EV type substitution you envision to have substantial effects.

The focus on EVs is due to it being a recent development which may potentially change things, much like cell phones and the internet have caused changes in society which were difficult to predict in advance.

Yeah, well. that will be rational, but ppl are irational…plus diminishing returns don’t seem to work to change the human lifestyle until SHTF doomsday really becomes a posibility. I find this equivalent to those ppl trapped in a burning airplane which, instead of f…king jump out, try to rescue their luggage

The new Volkswagen and Jaguar I-Pace commercials make me think that these vehicles are going to sale very well. Did Tesla even run car commercials? I am changing my mind on how fast the switch away from ICE vehicles will happen.

Above I say 2045 for falling oil prices, on further analysis my guess would be 2035 to 2040 when EVs and other types of substitution such as public transport, biking, walking, moving closer to work and in a walkable neighborhood, and car pooling, ride sharing, combining trips and buying more efficient icevs lead to demand falling below supply. The focus is on EVs alone, but high oil prices might lead to other effects becoming significant. Autonomous vehicles and increased ride sharing have not been considered. All these other effects would tend to push peak demand to an earlier date, but the scenario is optimistic so any earlier than 2035 is low probability and 2040 is probably the best guess in my view.

As has been pointed out here before, even if people want oil, demand can only go as high as supply.

If the economics of oil supply makes production less attractive, we will hit peak demand no matter how long it takes to convert the world to EVs.

Will demand drop before supply does? I don’t know. But if oil execs and investors and lenders want to get out sooner than later, supply drops. I see signs now and think it may pick up speed within the next few years.

Boomer,

By peak demand I mean a situation where we have falling oil prices, peak supply would be a situation where oil prices are rising because at prevailing prices people would want to consume more oil than is available. If oil producers cut back on investment for whatever reason (low oil prices might be one reason of many possibilities). My thinking is that low oil prices are leading to less investment at present. If supply is short prices may rise and investment may increase.

Demand and supply are always matched by the price of oil, the difference between peak supply and peak demand is the direction of oil prices after the peak. Peak supply will see rising oil prices and for peak demand oil prices will be falling.

I am much less confident than you that rising prices will increase supply.

1. The oil may not be easily accessible no matter the money.

2. There may be industry people who want out no matter the price.

With enough people projecting the end of the oil age, why stay tied to it if you can put your money, time, and skills elsewhere?

These days the very wealthy are less likely to be involved with commodities than other opportunities.

Note that I said investment will increase, rather than supply. If prices are higher then investment is likely to be higher than an equivalent situation where oil prices are low, that is all I am saying.

In general if there is money to be made by producing oil, then it will be produced, if not then it won’t. Pretty simple 🙂

Europe, where very high taxes on fuel at the pump fail to dissuade consumers from wasting the stuff.

Prices matter. Europeans use about 20% as much fuel for passenger transportation as Americans, per capita. 40% fewer cars, 40% less fuel per kilometer, 40% fewer kilometers per vehicle.

European industry, on the other hand, wastes fuel because they don’t pay the same taxes.

Verwimp,

I thought about your comment a bit more. Perhaps you believe demand for oil is relatively insensitive to the price of oil. I agree with that especially in the short run. Longer term consumers will adjust their behavior based on prices, consider 1979 to 1983 as an example of this behavior. In 1984 I bough my first Toyota a 1980 Tercel that got about 35 MPG highway and about 30 MPG in the city, my previous car was a 1968 Pontiac Catalina which got perhaps 16 MPG highway and 12 MPG in the city, so for an equivalent amount of travel I used half the fuel. Demand for oil correlates best with real GDP rather than the price of oil. Supply will track demand, however if the price of oil is so low that oil production is not profitable for the marginal producer, then supply will not be sufficient to meet demand and oil prices will be bid higher.

My discussion of oil price in the post was to do with this effect. Consider tight oil output for example in the US. Output was increasing strongly from 2011 to 2015, but the large change in prices from $110/b to $40/b lead to a drop in tight oil output.

There were those who believed that this was because tight oil production had peaked, but time proved this thesis to be incorrect and tight oil continued to increase as oil prices increased making tight oil production marginally profitable. Likewise Canadian oil sands output has decreased due to falling prices for Western Canadian Select.

So the story in the post is that lower oil prices will have an affect in tight oil and extra heavy oil output and may also reduce extraction rates for conventional oil (especially expensive resources like ultra deep water and Arctic oil) as the World reaches peak demand in 2035 or so due to the adoption of BEVs for road transport.

I was not very clear about this in the post, though we have discussed this before and you have not found this argument convincing.

It seems Shallow sand has often commented that when oil prices get below $45/b he lets low producing wells become idle if they need maintenance and does the minimum capital spending necessary because oil production is barely profitable in his field at that price. No doubt there are many other producers in the same boat who reduce output or expand output more slowly in response to lower prices. This is introductory microeconomics, pretty sure most people have a handle on this.

Dennis, what I have seen working for unconventional small to mid sized oil companies through the ups and downs is oil price can impact supply, but not usually the way we would expect. A significant amount of unprofitable wells were drilled in the post recession years driven by low interest loans to oil companies, and a significant access to capital due a lack of other profitable investment opportunities to hedge funds and retirement funds. In those days growth was the mantra, everyone needed to grow reserves and additional locations to drill, and production, never mind each quarter the company’s dug themselves further in to debt. Even in the oil crash of 2014, not enough companies took advantage of the decline in prices to go through bankruptcy and reduce debt loads. Most just kept piling on debt to drill wells that were not economic, but needed to grow reserves, and production, and to hold the acreage they spent so much money on.

Rig count tended to loosely follow oil price, but it was mostly dictated by if companies could get loans to fund their drilling. We have reached new heights of production mostly because we have also reached a point where most of the acreage in these plays is held by production, or a unit, or a continuous drilling provision. This allows companies to drill their most profitable locations during a lowish oil price and try to get into the black for once. The problem is in a lower longer price scenario, we bleed through all of the best locations trying to stay afloat, leaving increasingly worse oil production on all future wells.

Currently rig count is dropping, far faster than it should be with the oil price, but that is due to capital markets drying up to oil companies. Without access to new debt, they have to try and live within cash flow, which means cutting rigs, and cutting staff. Most of these small and mid sized companies also have a huge debt burden that comes due in a couple years, that they are incapable of paying off.

This is a long way of saying that right now it doesn’t matter in the US unconventional world if oil price climbs to $80, without access to new debt, or debt refinancing, companies will have to focus on paying down debt first, and adding rigs later. Production in the US has essentially peaked already, and I am not sure who else can fill in the gap.

Thanks JG Tulsa,

Let’s take a hypothetical case where an oil company is well run and either has low or no debt and mainly operates by plowing cash flow back into capital investment when it is profitable to do so based on the current oil price level. In that situation, where it exists, would you expect with all else being equal, that an increase in well head prices would tend to increase or decrease output for such an oil company?

I agree the tight oil companies have not operated their businesses very wisely and in many cases have seem relatively unaffected by the price of oil. I doubt that way of running an oil company will continue for much longer, many of these companies will go bankrupt or may be bought up by stronger companies.

Hi Dennis,

It is absolutely reasonable to scale down production when prices are low and vice versa. Those who are able to do so, will do so most probably. Nevertheless we saw production in Bakken and Eagle Ford go down in 2015 and 2016, while Permian was going up during these same years. Same price, other change in production. Also we see, for example during 2017-2018: Mexico and Norway down, China and UK steady, USA and KSA up. Same price, other change in production.

It would make things less complicated if production numbers were closely related to oil price. But I do not see this connection.

I am willing to see it, but I don’t. It is not that your argument are not convincing to me. It’s just the data telling me another story. A more complicated story.

Best regards,

Bruno

Verwimp.

Yes the relationship is not straightforward. Consider tight oil production as a whole and the effect is pretty clear. The capital can move from the more expensive plays to those that are less expensive and the Permian was less developed in terms of horizontal tight oil production in 2015 relative to the Bakken and Eagle Ford so costs were going down there as the recipe for the most efficient way to produce the tight oil using modern methods was being worked out in the 2014 to 2016 time frame in the Permian basin. A look at average well profiles makes this pretty clear (see chart below). wellpro1 is the 2010-2012 average and each well profile from wellpro2 to wellpro6 corresponds to 2013-2014.5, 2014.5-2015, 2015, 2016, and 2017.

For tight oil as a whole we see output decrease from March 2015 to September 2016 from 4892 kb/d to 4307 kb/d where in the 21 months previous to March 2015 output had increased from 3012 kb/d to 4892 kb/d, the net change in the rate of increase in tight oil output went from an 1880 kb/d increase to a 585 kb/d decrease which adds to 2465 kb/d, a pretty significant change in my view.

Likewise for Canadian oil sands we saw an average annual rate of increase for the 21 months before March 2015 of 252 kb/d and for the March 2015 to Sept 2016 period output increased at an average annual rate of 9 kb/d. A less dramatic change, but this would be expected for oil sands where capital investments are longer cycle and larger.

I focus on the forest rather than the trees 🙂

“Nice try, Dennis! Great effort. Thanks for putting all the labour in this post.”

Thanks, lots of upfront work went into the post. Dennis has some cool computational features built into his spreadsheet.

Thank you Paul for creating the original model circa 2005.

https://mobjectivist.blogspot.com/2005/09/oil-shock-model.html

Quien sabe? But, each is based on some reality, each of which could happen.

Nadie sabe.

Hi Dennis, and anybody else who crunches numbers,

What is your opinion as to the price necessary for oil companies to make money in Texas these days , and over the next couple of decades, in constant money?

A high and low estimate or range would suit my purposes just fine. Thanks anybody and everybody!

All that, depends on the cost. The cost can run anywhere from about 800k for shallower sands to over 10 million plus plus for a Permian shale oil well. Each will produce different amounts per month. There is no “Texas” figures. Texas has a HUGE amount of different formations.

But a rough estimate to make numbers is about 60 to 70 dollar WTI price. Some can make it for less, but most are sucking wind at 55, unless you are in shallow sands, which is not so available anymore.

OFM

I assume you are asking about tight oil. About 70 to 80 per barrel in 2018 $ will be needed for Brent oil price for oil companies to make money. WTI about 61 to 71.

Yeah, I’ll agree with that. And we ain’t there yet. With the stipulation that some oil companies could not make a profit at $90 a barrel. And Bubba flat don’t need them.

The decision parameters are extremely simple. It is history, whether on RRC, or wherever. Location makes X amount of oil in Y amount of time. No brainer.

Oh my.

Well, we’re never going to see WTI over $60 again. It’s capped by substitution around $50.

I managed to do a more detailed version of my substitution price model — not just including the difference between gasoline and electric costs, but also including the current upfront price difference between an average gas car and a Tesla Model 3 with a reasonable options mix as a “cost per mile”. And surprise surprise, it produces something close to the current WTI price. That’s a nice result.

As electric cars get cheaper, the substitution effect should bring the cap down from $50 to $20 pretty quickly. It’s going to be a *bloodbath* financially for the oil companies.

My question is: how much financial bleeding before they actually stop drilling? Frackers have been drilling for a decade while burning billions in other people’s money.

We drive a 9 year old Prius and a 4 year old Honda Accord. The Accord is ranked tops for dependability. I see no need to pay anywhere near $30,000 for a new car

Robert,

A 4 year old Model 3 will save you money. Currently a new Accord will have higher 5 year ownership cost than a Model 3.

I don’t understand. I could probably get a new Accord in this area for under $22,000. If less affluent would settle for a Civic. We have no available garage and would not be fond of electrical wiring in the driveway. At least we don’t burn the coal directly in California. I have not encountered a Tesla in Leisure Village this year. Did see one last year

robert

the accord with similar features to the standard plus model 3 would be 30k there are considerable fuel savings with tesla not for everyone charger can be an outside outlet on the side of house condos can be a problem

Robert

Accord Hybrid Touring which has somewhat similar features to model 3 is about 32.5 k according to true car, thats about 4k under msrp.

When extra cost of fuel for Accord is considered over 100k miles the cost of Accord goes up by 4500 to 37k. The Model 3 is about 39k, it is a far nicer car than the Accord. Not everyone wants to spend that much. I used 3 dollars per gallon and 12 cents per kwh I assumed 40 mpg for Accord Hybrid. It is likely that gasline will increase in price.

Hi Dennis,

I remember that calculation was very dependent on estimation of resale value. Also estimated resale value was used in financing capital cost so basically result comes out as autor wants it or as he estimates resale value on the model 3 as there is yet only estimations and no history available.

I dropped the discussion as i realised your financing of cars are very different how financing is done in my country so i would say that “cheaper than accord” applies to US with that resale value estimation of the model 3. Perhaps it applies in other countries also but for sure not in mine.

So the truth is probably not so black and white but more of situation dependent.

I still think comparing lease costs between whatever models you are interested in would tell alot, since leasing companies for sure have taken in consideration all costs over the period of the lease and added a profit margin. Then it just becomes the question do they apply same margins on all brands and cars, probably not but i think this would better indicate actual cost of a car model over time

What is leasing cost for an accord and a model 3 in the us? About same?

Ok i checked leasing costs in my country, model 3 standard edition about 550 dollar/month

Accord was apparently not available in my country so i instead selected a honda SUV Honda CR-V

It was about 450 dollar / month to lease

So about same price then for those two since you get about one full tank a month for the difference to put in that SUV.

Personally im leasing a ford focus combi atm with a decent amount of extra stuff in, i pay 230 dollars / month for that one. If i can find a hybrid that match my cost i will switch next time but so far i haven found one that is similar in size and price (in my country)

Baggen,

At some point cheaper EVs will be built.

I imagine it is cheaper to buy a used car than to lease. In a few years used Tesla Model 3 can be purchased more cheaply.

Baggen,

The author used research by Kelly Blue Book to estimate resale value.

https://mediaroom.kbb.com/2019-01-23-Kelley-Blue-Book-Names-2019-Best-Resale-Value-Award-Winners

Part of the savings would come from fuel savings. This varies by nation as taxes on fuel varies.

Hi Dennis,

I realize the author used an estimation by someone else, but its still just a guess and that guess more or less makes up the entire calculation so it comes down to if you believe the estimation/guess the author referring to and are going to get a new car in the US then calculation is correct and you put down your own money.

If you have doubts about that estimation panning out to be true and you live in the US perhaps you hold of putting down own money.

Or if you as i live in another country where financing looks very different you dont come close in a cost calculation with the tesla/hybrid vs options. Not yet anyway hopefully in a couple of years.

And i promise you i live in a nation with much higher fuel taxation and price compared to the US but it wont come close to even it out anyway.

Compare my current leasing cost vs the cheapest model 3, more than double. Sure you can argue its a much nicer car than my current one. But is it that much nicer so i should basically pay another 2-300 dollars / month to watch it next to my garage? It wont happen in my case.

But probably this is something we all do to an extent using our own reality and applying it on the world when the truth is probably more of a shade than black and white.

As i said i do want to have a hybrid as that would be a perfect fit for my driving patterns, but it needs to come down about 10000 dollars in purchase price for one in similar size as my ford focus combi. Then i will save money on the switch. My lease will be up in 15 months or so hopefully that has happen by then.

Baggen,

Wouldn’t buying a used car save you quite a bit?

I never lease, makes more sense to buy and drive for 10 years or even cheaper to buy used and drive for 7 years. Especially if you buy Japanese.

Hi Dennis,

“Wouldn’t buying a used car save you quite a bit?

I never lease, makes more sense to buy and drive for 10 years or even cheaper to buy used and drive for 7 years. Especially if you buy Japanese.”

Of course a used car would be cheapest, but the article we are both referring to was not about used cars it was about total cost of owning a car over a period of time if you had decided to get a new one. Specifically comparing purchasing a new Model 3 against other new cars.

Personally I dont want an old used car i prefer a new and i actually own two one that i bought cash (2016) and one that im leasing (2018).

Leasing is actually very close in cost compared to buying it cash up front it was a difference of 1500 dollars for 3 years when i estimated/guessed value loss on the purchase option and then i dont own it so i wont have to deal with selling it down the road i will just switch to a new. If i also include capital cost witch i should in the lease vs buy the lease is by far a superior option to me financially.

“At some point cheaper EVs will be built.

I imagine it is cheaper to buy a used car than to lease. In a few years used Tesla Model 3 can be purchased more cheaply.”

I agree used model 3 will be cheaper in a couple of years, especially if tesla manages to get price down on new production. But that doesent go together especially well with that calculation we are referring to witch is heavily dependent on the high estimated resale value of the model 3.

We cant both have high resale value in a couple of years at the same time as we have cheap used model 3. At least i find that outcome unlikely.

Baggen,

Well yes if resale value is high, then buying new may make more sense. You are skeptical of high resale value, if you are correct then used might make more sense.

For me saving money was not really the aim, for the US if the Kelley Blue book estimate is correct for resale value then the Tesla is competitive. Again for me the lease is not the better deal and in many cases lately I was able to get zero percent financing, just paid cash for the Tesla. It’s been a great car so far, big step up from my Camry Hybrid and Prius.

It is not going to be as cheap as a subcompact car.

Dennis,

“Baggen,

Well yes if resale value is high, then buying new may make more sense. You are skeptical of high resale value, if you are correct then used might make more sense.

For me saving money was not really the aim, for the US if the Kelley Blue book estimate is correct for resale value then the Tesla is competitive. Again for me the lease is not the better deal and in many cases lately I was able to get zero percent financing, just paid cash for the Tesla. It’s been a great car so far, big step up from my Camry Hybrid and Prius.

It is not going to be as cheap as a subcompact car.”

I am skeptical of the high resale value yes but that is not my main point. The original question was if buying a new model 3 vs a bunch of other new cars were cheaper to own and operate for a period of 5 years according to that article.

Im simply pointing out that the calculation is heavily tilted towards an estimation of a resale value, and the calculation is also US localized. If you live in the US and agree with that resale estimation then its a go.

As i said personally im not in the market for a used car, but of course that will always be cheapest option if that is your only preference of consideration.

“Again for me the lease is not the better deal and in many cases lately I was able to get zero percent financing, just paid cash for the Tesla. It’s been a great car so far, big step up from my Camry Hybrid and Prius.”

Yeah as i said we live in different worlds come to car financing and that was also my point that the calculation we are both referring to is US localized.

0% financing what do you mean by that, you borrowed money from the bank at 0% interest? Or your using your own money and calculate the cost of that to 0%?

“It is not going to be as cheap as a subcompact car.”

What is a “subcompact car”? like a really small car?

I know you own a model 3, if you could provide me with the average distance you get per kWh i could do a quick example of my reality with numbers, if we select the pay with own cash for entire car option. So i can include the Model 3s lower operating costs.

Baggen,

My 2013 Camry Hybrid and 2015 Prius Plugin have a zero % interest rate. Financing through Toyota, so agreed on purchase price first then arranged financing, though it is likely the agreed price was based on the assumption that I would get the loan at 0%, so possibly the price was higher to account for that. I used a Web service that gave me the “fair price” for the specific model I wanted and got that price in each case. I usually keep my cars for 10 years or more, (2004 Prius traded sold in 2015, 1997 Camry gave to my Dad in 2009, 1994 Accord replaced with 2004 Prius and 2009 Prius replaced with Model 3 in 2018 (sold that one early at 9 years) Some cars in between went to kids 2009 Prius went to daughter and she got the 2015 Prius when we got the Tesla.

So I buy rather than lease because I keep the car for 9 to 10 years, works best financially for me.

Dennis,

“My 2013 Camry Hybrid and 2015 Prius Plugin have a zero % interest rate. Financing through Toyota, so agreed on purchase price first then arranged financing, though it is likely the agreed price was based on the assumption that I would get the loan at 0%, so possibly the price was higher to account for that.”

Ok now you have to explain how this works to me 😀

So the car dealer gives you a 0% loan on the full amount of the agreed value on the car? Am i getting that correct?

where is the rub? I doubt they give you a car for free, so where do they get their money if they finance it for 0% for you for full amount?

When you trade it in for your next car do you get a new 0% loan on the new car then – value left on your old?

You never ever hand the dealer any money at all?

For me the cheapest way to finance a car would be using bottom loan on my house at about 2%, if i exclude the alternative cost on that borrowed money from the bank. If i include it then leasing will be my superior option.

Baggen,

I think it was something like $1000 down, so if the car was 26k, then 25k is “financed” and payments cover principle only over 5 years so to keep math simple if it was 31k including sales tax and we put 1k down, we pay 500 per month for 60 months. Then I own it, next time I buy a car the interest rate is probably higher, these days around 1.99% is common in US for those with good credit scores. Tesla did not offer financing or I didn’t like their rate so I just paid cash.

Dennis,

“I think it was something like $1000 down, so if the car was 26k, then 25k is “financed” and payments cover principle only over 5 years so to keep math simple if it was 31k including sales tax and we put 1k down, we pay 500 per month for 60 months. Then I own it, next time I buy a car the interest rate is probably higher, these days around 1.99% is common in US for those with good credit scores. Tesla did not offer financing or I didn’t like their rate so I just paid cash.”

Ok then i understand, so you basically payed cash but payments are stretched over a 60 month period to reach the agreed upon price. That total price is probably a little bit higher compared to if you would have payed full amount cash upfront, sort of a hidden interest for the dealer for offer this financing.

I use 7% capital cost/alternative cost for spending my own money and i would apply it in both cases above 60 months payment plan or cash up front. This is why a more expensive car like a hybrid or EV will never catch up to the cheaper purchase option even if their operation cost is significantly lower. What i miss out on alternative income eats up any savings i do in operational costs.

This is also why the lease option is the most profitable one for me.

So it comes down to how much more do i want to spend per month to have a car that is a bit or a lot nicer. Changing my Ford focus to a model 3 for instance would cost me about 2-300 dollar per months in difference and im not willing to spend that to mostly look at it parked. I rather have the difference of the capital employed, have a higher income and look at my somewhat less nicer car.

Baggen,

I guess even with the opportunity cost of the capital one needs to consider that at the end of 5 years in one case you own the car and in the other case you do not. If one is willing to keep the car for the following 5 years (for a Toyota this is usually the case) the cheaper option is to buy rather than lease. There is a differential between trade in value and purchase cost that is significant after 5 years, I also typically drive my new cars more than the typical lease mileage.

The main thing is that there is more to the decision than the money from my perspective. Also my wife didn’t like the Prius, she wanted something nicer, she likes her new Model 3 so it works for me.

Dennis,

“I guess even with the opportunity cost of the capital one needs to consider that at the end of 5 years in one case you own the car and in the other case you do not.

if one is willing to keep the car for the following 5 years (for a Toyota this is usually the case) the cheaper option is to buy rather than lease. There is a differential between trade in value and purchase cost that is significant after 5 years, I also typically drive my new cars more than the typical lease mileage.”

No, not for me i will miss out on that extra income every year that i own the more expensive car if i select to purchase with own money, not counting value increase in investment either just cash flow. As i said i did the calculation value loss vs lease cost and came up very even 1500 dollar difference in 3 year. Of course then i have estimated value loss but at least i have history of same model to use for estimation. And i dont want to own a car that starts to get old, just a personal preference of mine so that weighs into my decision process that is not pure economical if it were i would only buy old used cars. Yes as you say it also depends on your driving habits i dont drive much so leasing is a valid option for me, but if you exceed those 15000 km/year in distance the lease option gets uneconomical quite fast. Probably you have similar ranges in your lease options and penalties for exceeding them.

“The main thing is that there is more to the decision than the money from my perspective. Also my wife didn’t like the Prius, she wanted something nicer, she likes her new Model 3 so it works for me.”

Totally agree, same in my case not only based on money/profit as i do have some other variables that are “musts”.

But hopefully we can agree that the reality is not as black and white as that referred calculation in the article made it out to be, but how that affects EV adoption if it goes faster or slower i would not dare to guess but i dont think economy is the main driver for switching for alot of people rather other values.

Im hoping for a hybrid similar size to my current car that comes down about 10.000 dollar in price in 1.5 years, then its a deal in my case when i make next switch 😛

Baggen,

An alternative is to buy a nicer car than a Ford, maybe a Toyota or Honda and run the numbers for using the car longer than just 3 years. If you are in a nation with high fuel prices, the economics might work out if you keep the car for 10 years, and Toyotas and Hondas are quite reliable over 10 years/150,000 miles.

I may be a little more frugal as far as spending on cars.

The Wall Street Journal today has an article about how sources of funding have dried up for frackers.

I’m not sure substitution will kill oil prices. And while I know peak oil will happen, putting a date on it doesn’t much matter to me.

What most interests me is when investors, lenders, and execs at oil companies decide having their money tied up in petroleum just doesn’t make financial sense and it is time to bail.

LTO is going to have to slow down with low prices and less access to capital. North Dakota drilling in at least the past 8 months is going to lose money. Getting mid-$40s at best and in December much worse in the initial flow burst is no bueno. Even if hedged, it’s still an overall economic loser with operators having no positive free cash flow. Cash for additional drilling *has* to come from investors or lenders. That gets choked off, theres no money to pay the up front capital and labor costs of new wells.

Boomer the exact date does not matter, but higher oil prices that are likely from 2022 to 2035 will affect the economy. Higher oil prices will also make unconventional oil resources more likely to be recovered.

My expectation is that high oil prices will eventually lead to substitution of EVs and AVs to the point where oil prices fall in the 2035 to 2050 time frame. This causes much of the extra heavy oil to be left in the ground, about 300 Gb that might have been recovered at a price of $100/b or more in 2017$. A lot of tight oil may also remain in the ground along with deepwater resources.

“Well, we’re never going to see WTI over $60 again”

I think that one is going to bite your ass.

Nathaneal,

I approach it differently and look at realistic rates of sales growth in EVs.

Replacing 1 billion cars takes time, until that is done there will still be demand for oil. one cannot simply assume the sales growth rate of plugin vehicles (about 30% growth for the past few years) will continue indefinitely, the rate of growth will gradually slow over time until the sales rate reaches 70 to 90 million vehicles per year, then it will still take a few years to replace the fleet, a similar model can be created for commercial vehicles. In my model demand falls below supply in 2033, at that point oil prices start to fall, though the rate of decrease is unknown. Oil prices might reach $20/b by 2050 when demand reaches about the current level of OPEC output, difficult to predict what happens to oil prices, but they will go down as the transition occurs. We agree on that point, just not the timing.

According to Mark Papa in Q4 2018 presemtation EOG did not see any possibility to increase oil production as they need 75 usd / bbl WTI. They priority to pay depth , interest and dividend to their investors. If the vreak even price WTI average shale oil is 65 usd today , I doubt this will be reduced the next 3-5 years as the rock formation will have reduced production Quality, the max. latitude lenght and number each drill pad might be reach, now I read gaz is injected to stimulat production the impact of this remain to see. Higher labour cost , increase cost of funding as oil & Gaz is already less popular because of environmental issues. Than there is some increase offshore activity, and onshore drilling in Europe. But even the oil majours want cheeper wells and service work it will not be any cheaper because all need profit to grow a healthy Buisiness. In the mean time about 15% of the oil produced are replaced adding 6-7% decline rate to that and at least 1% growth in demand even with trade war it seems clear the world need significant more oil that is profittable to develop to a cost consumers around the globe , mostely poor in development Country can afford to buy and during time there need to be less energy made from fosil fuel.

I saved the Rystad article that has US at 12.5 now, and 13.4 by the end of the year. I will revisit it from time to time. It’s classic BS to the point of being really funny. Like “Little shop of Horrors” (the original, not the 1986 remake) the really bad SF movie.

I mean, really. We were at 11.9 the end of March per EIA monthlies. With no substantial increase in completions and drops in active rigs, we have increased 600k in two months??? Then in the last half of 2019, we are going to increase another 900k per day, when prices are less than $55 now? Well, if your going to lie, tell a big one. My Venus flytrap ate my homework?

GuyM,

I think we might get to 12.4 Mb/d by Dec 2019, I agree the Rystad estimates are likely too optimistic.

A month ago, I would have agreed that 12.4 was pretty reasonable. Not so sure, now.

No, too optimistic would apply if they were making this Wag at the beginning of the year. By mid year, it can only be defined as intentional BS.

GuyM,

I took a look at the drilling productivity report(DPR) to see if it was wildly optimistic and that was the source of the very bad Rystad estimate. It turns out that the DPR is not terrible, the trend for their estimate from Sept 2018 to June 2019 has a slope of about 666 kb/d each year. If we use the equation of that trend line (based on the 10 months from Sept 2018 to June 2019) to find December 2019 output we get output that is 574 kb/d higher than Dec 2018 output. If we assume Alaska, GOM and L48 onshore conventional are flat from Dec 2018 to Dec 2019, and also assume the trendline based on Sept 2018 to June 2019 data continues to track tight oil output through Dec 2019, then output in Dec 2019 would be 12,537 kb/d.

This is probably a high side estimate in my view probably 12,250+/-250 kb/d would be my guess for US C+C output in Dec 2019 (low end for lower prices and high end for higher prices).

For average annual output, 2019 would be about 1080 kb/d higher in 2019 than in 2018 with average output at 12,040 kb/d in 2019, it was 10,960 kb/d in 2018.

Related: https://oilprice.com/Energy/Crude-Oil/How-Oil-Defeated-The-Nazis.html

Worth A Repost: Mike’s take on this foolishness: – many Texans are in Left Feild.

https://community.oilprice.com/topic/6209-why-is-america-texas-burning-millions-of-dollars-per-day-of-natural-gas/

Damn thats great work Dennis.

I see a few take home messages-

Assuming the world economy continues on without huge disruptions for the next three decades-

there is a huge amount of oil still to be delivered,

we are very close to peak [+/- 5%],

there is still a massive slug of CO2 to be ‘delivered’, and

there is still some time for the world economy to make the technological and policy adaptations to get by as oil depletes.

What could severely disrupt the smooth path ( or result in big under-performance of the potential) displayed in the charting?

To me the big ones seem to be-

warfare and failed states in the mideast,

economic depression severe and long long lasting, and

rapid replacement/substitution by electrification around early 2030.

I assume that Nat Gas will remain in highest level demand in the scenario where electrification of transport becomes pervasive. I also assume that national policy initiatives to rain in crude oil consumption due to climate change, such as carbon taxes, will do little to affect consumption. Countries will focus much of the climate change angst on coal for the next 20-30 yrs, and climate change effects will be felt primarily after oil is on the steep decline part of the curves anyway (2040’s and beyond).

Regarding Nathaniels severe criticisms- you can’t quantify these variables and factors accurately, such as failed states, substitution rates, and national economic policies. That is not what Dennis is presenting.

Hickory,

Thanks. Criticisms are fine there are many points of view. Nathaneal is just more optimistic than I am about how fast BEVs can ramp up. Chart below shows model from 2025 to 2070, and note that it is assumed oil used for things other than road transport is assumed fixed at 2025 levels, a more realistic model would have these uses increasing through 2070 when World population might peak and then potentially decreasing thereafter, the focus was on EVs replacing ICEVs both personal and commercial vehicles. Higher oil prices might also lead to more electrified rail, light rail, buses on overhead wires, etc.

My revised EV transition model has demand falling below supply in 2033 for my best guess models of supply and demand. From 2022 to 2033 oil prices are likely to be high while the transition proceeds. I expect oil prices to rise by $8/b each year until reaching $100/b in 2022 and then the rate will slow to about $2/b per year (constant 2018$) from 2023 to 2033, with oil prices reaching $120/b, then oil prices will start to decline as demand falls below supply after 2033.

Scenario below matches supply with the demand scenario from my EV transition scenario. In this case extraction rates fall and decline rates rise due to a lack of demand for oil (demand below supply) after 2032. We would expect oil prices to fall from about $120/b in 2032 in 2018$, the rate of decrease in oil prices will be whatever is needed to stop the more expensive oil from being produced. It is not clear what the cost curve will look like in 2032 so prices would be impossible to predict (not surprising as we cannot predict oil prices tomorrow with any accuracy). It seems likely that by 2050 or so that oil prices may have fallen to $30/bo or less, if the transition to EVs and other non-oil transport happens fairly rapidly from 2030 to 2050. Note that some commercial vehicles may move to compressed natural gas along with the BEV transition, there may also be a move to rail for long haul shipping.

Thanks for the efforts Dennis, much appreciated.

As you already know these models assume stable conditions. In my opinion this doesn’t seem to be the case at the moment. I am specifically talking from an economic standpoint and obviously there is a myriad of different factors as you already know which i will not go into here.

It seems to me the world economy is heading into uncharted territory, all the major economic powers (I will hesitantly include China too) are going through a period of low interest rates and low growth. There is talk that the Federal reserve will most likely cut interest rates this month I believe in the 18-19 June meeting.

Obviously trumps trade war is a factor in this and it will continue to be so, a drop in copper prices are also reflective of a drop in world trade.

All of this and more that i haven’t mentioned just from an economic standpoint will affect oil prices. If global growth is diminishing, which seems to be the case. This will have negative pressure on oil prices and therefore output, especially from the unconventional side.

It seems to me, central banks around the world are doing everything in their power to keep asset prices that banks hold up. What will be the outcome? I believe no one knows. For me this current situation is a notch beyond Keynesian economics.

Iron Mike,

The economy is difficult to predict. There have been many times in history where there has been political turmoil, perhaps today is worse than other times, this is by no means a given, different historians and economic historians would have widely different perspectives on this question.

For any 3 economists you would likely get at least 9 different predictions for future economic growth with very little overlap in their respective scenarios.

My standard guess includes a recession in 2030. So in the scenario below I have added a GFC2 type recession from 2030 to 2031 where extraction rates decrease over those 2 years, then extraction rates resume their increase from 2032 up to 2039 and then gradually flatten to 2044 and remain flat to 2050 and then decrease. URR for this scenario is 2970 Gb, with peak of 86.2 Mb/d in 2026. Obviously this is one of an infinite number of possible guesses.

I think twentieth and twenty-first century economic trends may not be enough to predict the future. I believe what we are seeing unfold is more comparable to the Industrial Revolution. Massive realignments.

While we haven’t seen the end of oil, I believe we are currently living through the end of the oil age. What the world will look like in the future will greatly depend on available resources, new technologies, and political alliances. While it is possible that the world might come out of this transition a better place, most of us here assume it will not.

The main problem with any transition is the sheer number of people.

Boomer II,

The only thing that is constant is that things never remain constant.

Somebody above talked about Europe and big cars. Europe has a problem. OPEC’s recent world statistical report (BP’s due this week upcoming) quotes global oil consumption growth at 1.5% for 2018.

The growth concentrated in Asia and North America. I believe Europe was quoted as a tiny decline. It didn’t happen from substitution, of course. They have a weakening economy.

This is a double whammy. This will hit EU tax revenue, from lower fuel tax revs. Latest estimate I’ve seen says the EU member states get about 7% of their total taxes from fuel. Pretty much all of them are running a deficit, some have negative interest rates, and this isn’t going to help.

Even with a weak (aging) Europe, and growth disruptions like trade wars,

we will be at 8 billion people in a few years, marching on to 9 Billion.

That is lot more consumers, and many will be able to afford some oil consumption.

There is a lot of wind in the sails of demand.

EU has big current account surplus.

Dennis, from your reply to Freddy:

In 2018 World C+C average output was about 82.84 Mb/d, so my “best guess” (which could indeed be incorrect) scenario sees an increase of 4.46 Mb/d from 2018 to 2026.

Okay, that ain’t all that unreasonable except… except… you have C+C production in 2019 increasing by 1,449 over the average of 2018. February 2019 World C+C production was 82,389,000 barrels per day. Your 2019 average is 1,901,000 barrels per day above that figure. Dennis, that just ain’t gonna happen.

The below chart is through April 2019.

OPEC + Russia + Canada accounts for 55% of the World’s oil production. These 14 OPEC nations plus Canada plus Russia averaged 47,849,000 barrels per day in 2018. Their average for the first four months of 2019 was exactly 46,000,000 barrels per day or 1,848,000 barrels per day below their 2018 average. Their April output was 2,352,000 barrels per day below their 2019 average.

If World C+C is higher in 2019 than in 2018, who will make up this huge difference. US Shale?

Scary Chart!

Canada still has lots of potential, their tars sands are just declining because of low oil prices.

I believe that the Aberta Tar Sands are pretty much “guaranteed” (much less risk compared to drilling for nothing) as long as the price is right. They are definitely there.

I am sure that statement will be destroyed by oil professionals (which I am not). But RockMtnGuy from Oil Drum who used to work on them I think, said pretty much the same thing.

thanks for your work Ron.

Hi Ron,

The model assumes extraction rates in 2019 for conventional oil producing reserves are the same in 2019 as in 2018. If they decrease, output could be lower than my best guess scenario. Output can increase in the final 8 months of 2019 and output data is often revised. I primarily use the EIA C+C data, the average World output for the first 2 months of 2019 was 411 kb/d below the average 2018 World C+C output. In 2018 average output was 1750 kb/d higher than the 2017 average.

My best guess may indeed be too optimistic for 2019, it was a simple constant extraction rate model through 2023 with increasing extraction rates through 2040 then constant then declining.

A modified model below has extraction rate decrease in 2019 so output is slightly less in 2019 than 2018. After that a similar scenario is followed as my previous best guess. For those who complain that the World economy will experience a recession, I agree but I cannot predict those.

Isn’t the answer the difference will be made up by drawing from storage until the price gets high enough to bring more production on? $120 barrel is going to get offshore fired back up and maybe even Venezuela.

No, there is just not that much storage. A nation can draw from storage for only a couple of months until they run out of storage. That is unless they have a tremendous amount of storage. Not many nations have that much storage. 120$ a barrel? You’re dreaming. Perhaps in a decade or so.

The problem is that now even 80 usd/barrel hurts world economic growth.

name,

Any evidence for that assertion?

So I found the downloadable data from OPEC’s Annual Statistical Bulletin noted above. I spent some time comparing their 2017 consumption numbers to BP’s.

They aren’t the same. They are quite a lot different in certain countries.

ASB says world consumption 2017 was 97.32 mbpd. BP says 98.2 mbpd. Not huge diff.

But KSA’s consumption is ASB 3.272 mbpd and in decline since 2015. BP says 3.92 mbpd steady increase since 2015 with a tiny downtick 2016-2017.

Someone has agenda on that.

BP shows KSA having almost overtaken Japan as #4 consumer in the world. ASB shows KSA far under Japan.

BP’s footnotes are far superior for explaining definitions, etc.

I seldom take BP’s word for anything. But in this case, I think they are a lot closer than OPEC’s Annual Statistical Bulletin. I am sure they get their numbers directly from Saudi Arabia. And Saudi will just make the numbers whatever they want them to be.

The ASB KSA consumption numbers are pretty glaring in how they diverge from BP.

Sometimes these numbers reflect domestic refining and the products get shipped off, but in this case KSA’s domestic refining capacity is almost exactly equal to their ASB consumption numbers. With BP saying that’s nearly 700K bpd low, there would have to be some petroleum product importing going on.

A search for Saudi gasoline import does find some hits, the most significant one from 2012 from an Arab newsletter.

What role do the giant oil fields play? As I write in my book “When trucks stop running:

the average size of new oil fields has declined, leaving us heavily dependent on the original giant oil fields discovered many decades ago.

Of the roughly 47,500 oil fields in the world, 507 of them, about one percent, are giant oil fields holding nearly two-thirds of all the oil that has ever been, or ever will be produced, with the largest 100 giants, the “elephants,” providing nearly half of all oil today

Since giant oil fields dominate oil production, the rate they decline at is a good predictor of future world oil production. In 2005, they provided 60 % of world oil. Giant fields only begin to decline after a long plateau phase where production fluctuates within a 4 % range. In 2007, the 261 giants past their plateau phase were declining at an average rate of 6 % a year. Their decline rate will continue to increase by 0.15 % a year, to 6.15, 6.3, 6.45 % and so on. By 2030 these giants, and the other giants joining them as time goes on, will be declining at an average rate of over 9 % a year

Since nongiant oil fields decline at much higher rates, especially offshore and tight oil, by 2030, the average decline rate of all oil fields past their peak production will be higher than 9 percent.

by 2030, from half to two-thirds of global crude oil production will need to be replaced—40 to 50 Mb/d of today’s 77.8 Mb/d

Making up this shortfall will be difficult, since four out of five barrels now come from fields found before 1973 and the majority of them are declining.

So far, Enhanced oil recovery in giant fields has increased the decline rate after peak production, because oil extracted now is unavailable after the peak, making the decline rate steeper. For example, Cantarell in Mexico, the second largest oil field ever found, declined at 20 % rates due to the EOR used to increase the maximum rate of production

Aleklett, K., et al. 2012. Peeking at peak oil. Berlin: Springer.

Hook, M., et al. 2009. Giant oil field decline rates and their influence on world oil production. Energy Policy 37(6):2262–2272.

Murphy, D.J., et al. 2011. Energy return on investment, peak oil, and the end of economic growth. Annals of the New York Academy of Sciences 1219: 52–72.

Thanks Alice, that was very informative. That is why I believe the decline curve will be much steeper than the ascension curve. Individual fields, of course, reach their peak production in only a few years and their decline could take many years. But I am speaking of all the world’s production combined. I think the decline curve will shock most people.

I once made a large poster about this 1978 Rand study. Had become interested in resource studies years earlier and occasionally lectured at ZPG and elsewhere. https://www.rand.org/pubs/reports/R2284.html

Thanks Robert.

I have read that report in the past, it is excellent. A snippet from page xi

That’s very informative, Alice. Very rough estimation from that, is that if shale were able to eke out another 600k increase a year, for a year or two, it could not possibly keep up with current decline rates in the bigger fields. Especially, when that shale increase is not going to start in 2019. World will be down, and add on another year of decline. 2018 will be looking more like peak year.

This poster has been considering post peak for, obviously, years. Kudos, this stuff is good!

http://energyskeptic.com/

Hi Alice,

There is no reason the decline rate will accelerate, especially for onshore fields. The UK declined at about 8.5% per Year after peak. That might be typical for offshore production which is a small proportion of World output. Cantarell is not likely to be typical for Giant oil field decline rates. US decline rate for C+C output from 1985 to 2010 was about 3.5% per year for lower48 excluding Gulf of Mexico and tight oil output.

A simple model can be created with 20 giant oil fields each that produces 4 Mb/d. Each field is assumed to decline at 5% per year and each year from 2019 to 2039 1 field goes from plateau to decline.

From 2019 to 2024 the World decline rate is less than 1% per year, from 2025 to 2031 decline rate is 2.4%, from 2031 to 2040 decline rate is 4.4% per year and from 2040 to 2050 decline rate is 5.1%.

Note that such a model does not account for the development of new producing reserves each year.

The oil shock model takes account of all oil discovered to date and assumes there will be some new discovery and reserve growth.

The oil shock model accounts for this fact. At the end of 2018 of 2800 Gb of World cumulative plus future discoveries and reserve growth about 1810 Gb of cumulative oil discovery had been developed into producing reserves leaving another 1000 Gb of resources to be developed in the future (this is conventional oil only and excludes extra heavy and tight oil resources). At the end of 2018 World producing conventional reserves were about 476 Gb for the medium oil shock model. The blue curve in the chart below shows the new producing reserves that are added each year to the pool of producing reserves. The red curve is oil produced (extracted) each year and the green curve is the modelled dispersive discovery curve (based on backdated oil discovery).

One way to think of producing reserves is a big pool filled with 477 billion barrels of oil.

There is a big pipe flowing into the pool which is a flow supplied by new producing reserves each year as new wells are brought online and adds to the pool of producing reserves. A second pipe flows out of the pool which consists of the oil produced each year. The extraction rate % is the oil produced divided by the producing reserves at the end of the previous year. Chart below shows each of these quantities for my recession model (recession in 2030 and 2031). This is for conventional resources only, tight oil and extra heavy oil are modelled separately.

Note the legend has an error, the extraction rate is on the left axis. Sorry.

Alice,

I was wrong about offshore being a small part of world output in 2015 it was 31% of World C+C+NGL. I still believe the undeveloped resources will offset decline in existing fields and thereby reduce decline rates.

First of all, oil field geography (not geology) can be changed. So that can be one source of corruption in whatever number you want to quote for field production.

Second of all, choke management can also corrupt whatever number you want to quote for field production.

And how about third of all you can change the definition of oil and call all sorts of liquids coming up the well bore “oil” regardless of API density and corrupt whatever number you want to quote for field production. Executives are paid for production, agencies collect taxes for production, royalty recipients are paid regardless of profit, so who is it that would oppose manufacturing any number for production you want to quote? Lenders? The Fed is providing nearly 0% interest rates. Why would lenders care? Maybe refineries would care, but you can probably cut them in.

So you can pretty much put numbers and conclusions about flow to bed.

Watcher,