By Ovi

The focus of this post is an overview of World oil production along with a more detailed review of the top 11 Non-OPEC oil producing countries. OPEC production is covered in a separate post.

Below are a number of Crude plus Condensate (C + C) production charts, usually shortened to “oil”, for the oil producing countries. The charts are created from data provided by the EIA’s International Energy Statistics and are updated to December 2025. This is the latest and most detailed/complete World oil production information available. Information from other sources such as OPEC, IEA, STEO and country specific sites such as Brazil, Norway, Mexico, Argentina and China is reported to provide an extra one or two month production preview beyond the EIA.

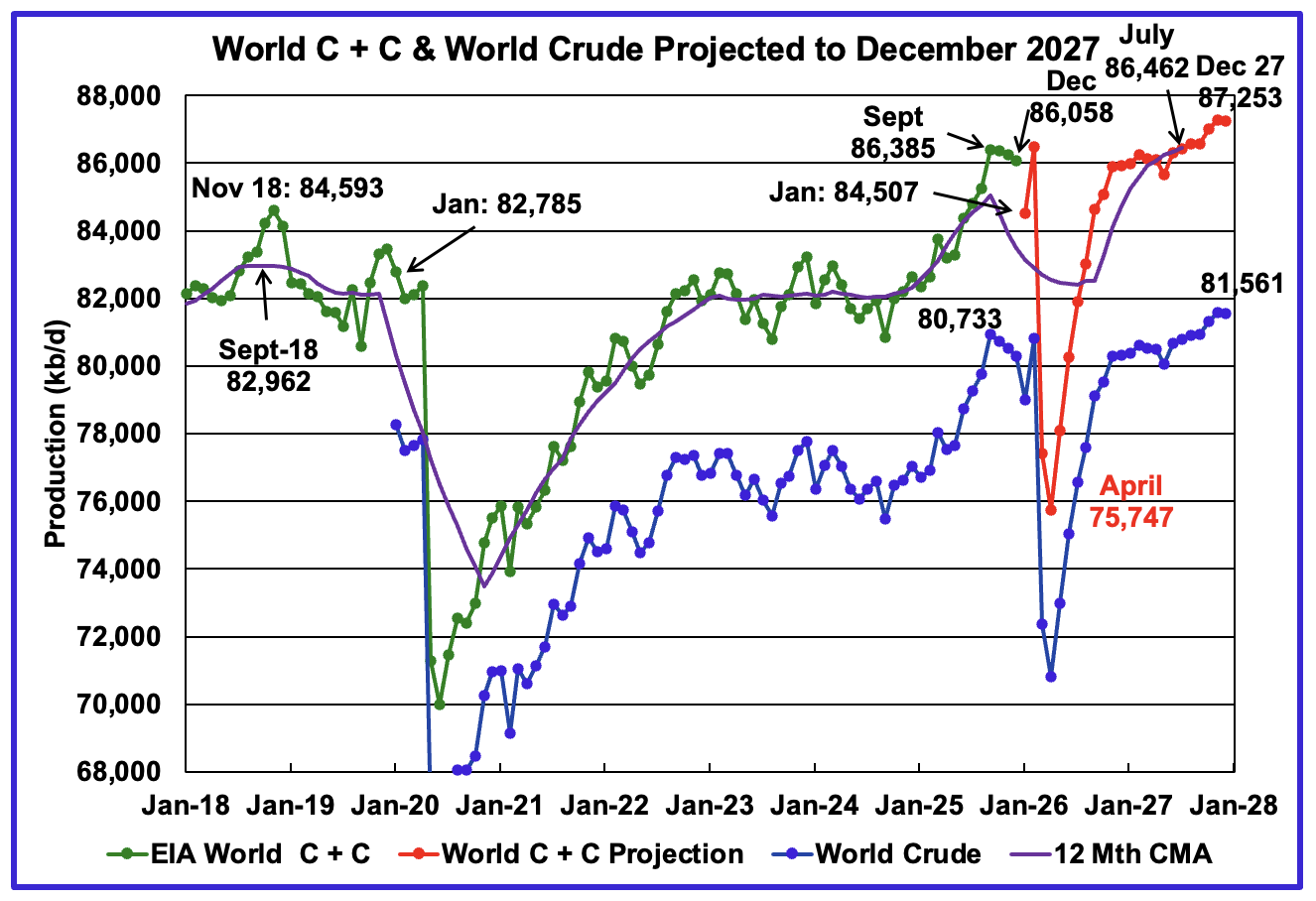

The EIA’s April STEO report has made significant and major revisions to the projected World oil production due to the US/Iranian war. Also US projected production has been significantly revised upward. See US chart at the end.

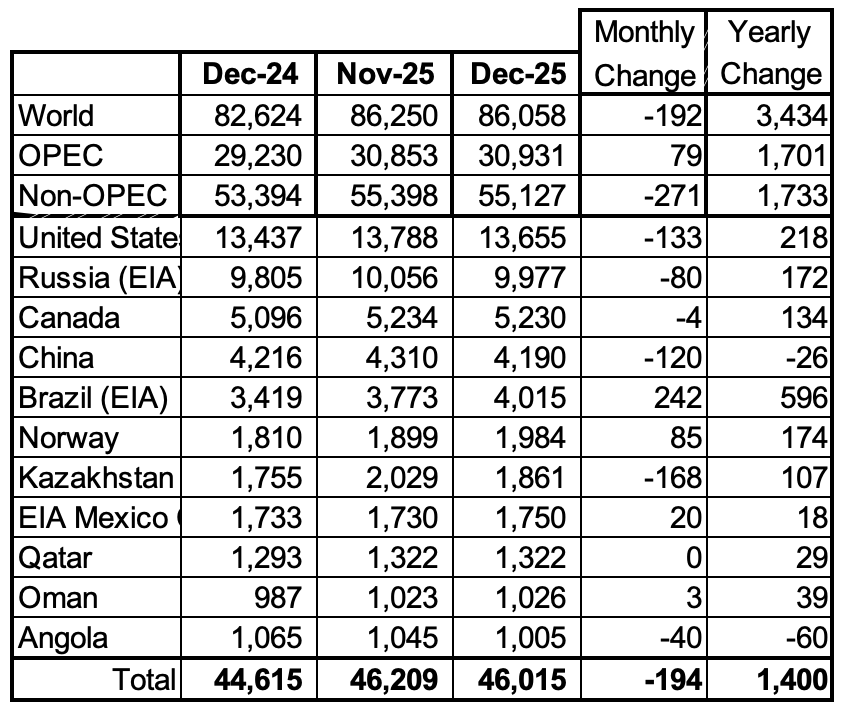

The World’s December oil production decreased by 192 kb/d to 86,058 kb/d.

September 2025 is the new current World Peak Oil at 86,428 kb/d for the next year and a half when more oil production is brought online in late 2027. Note that after the March 2026 output crash, oil production only gets back to the November 2025 production level in February 2027.

This chart has been updated using the April 2026 STEO to project World C + C production out to December 2027. It uses the STEO report along with the International Energy Statistics to make the projection. Production in January 2026 is projected to decrease by 1,551 kb/d to 84,507 kb/d. March/April production drops by more than 10,000 kb/d due to the Iran/US war. April production at 75,747 is 10,722 lb/d lower than March 2026.

The 12 month Centred Moving Average shown at July 2027 is 86,462 kb/d vs the September 2018 12 month CMA of 82,962 kb/d.

For December 2027, production is projected to be 87,253 kb/d, a new projected high and an upward revision of 219 kb/d from the previous report. Most of that increase is from the US. See US chart below.

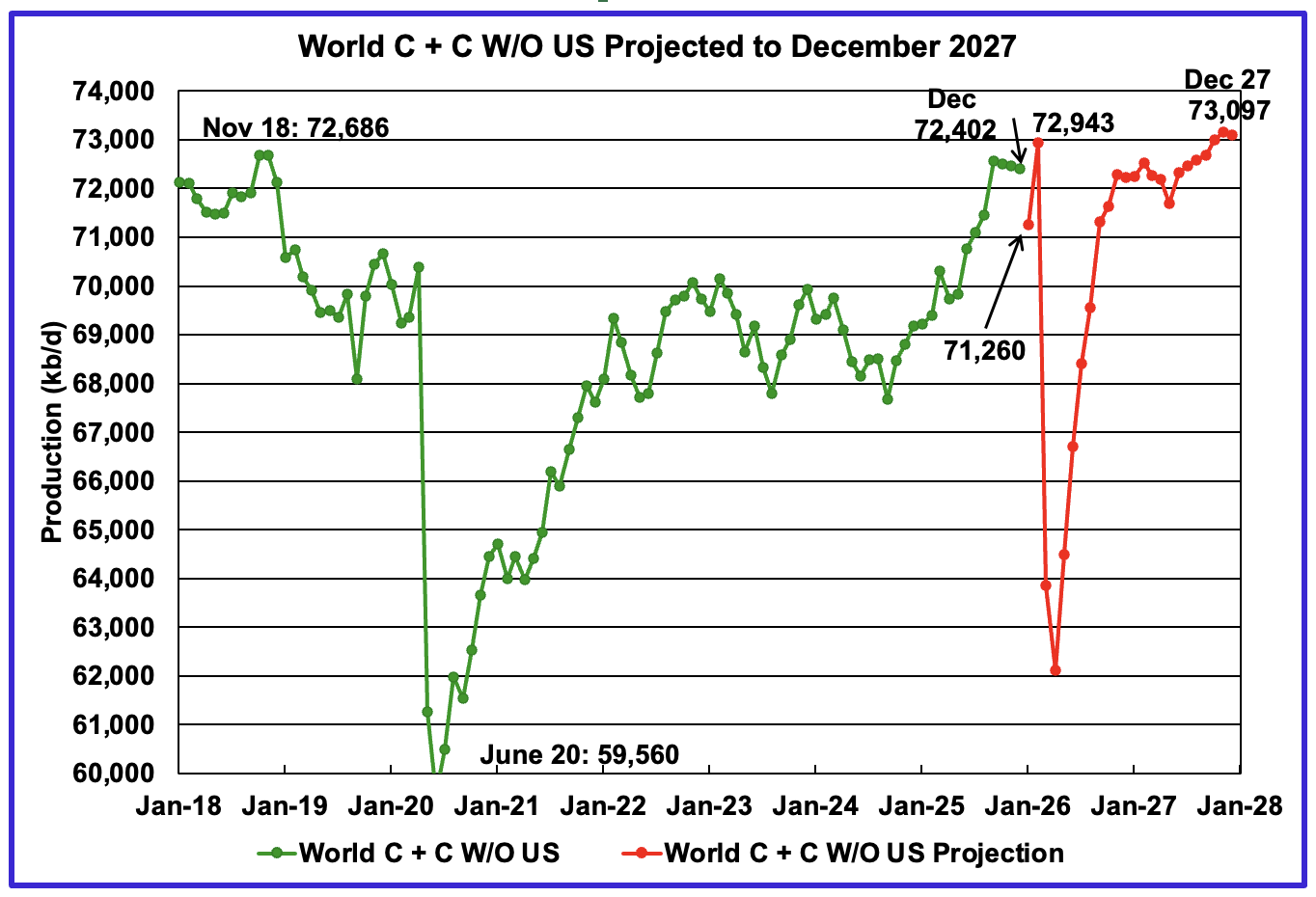

December’s World oil output W/O the US decreased by 59 kb/d to 72,402 kb/d. January’s production is expected to decrease by 1,142 kb/d to 71,260 kb/d.

The projection is forecasting that December 2027 World W/O US oil production will be 73,097 kb/d. This is only 154 kb/d higher than the expected February production of 72,943 kb/d. Very little growth expected from the Non-US World oil producing countries.

A Different Perspective on World Oil Production

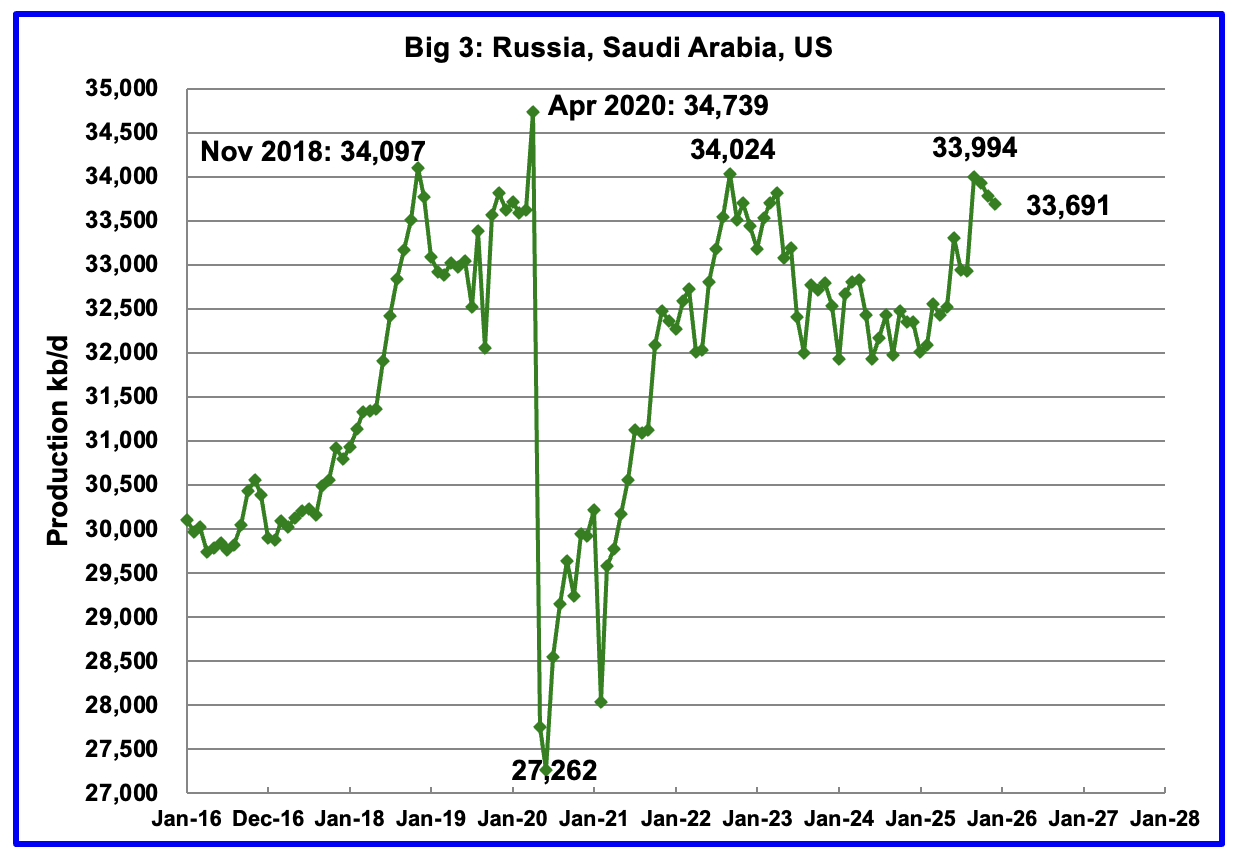

December’s Big 3 oil production decreased by 93 kb/d to 33,691 kb/d. The US December drop was offset by the Saudi Arabia increase.

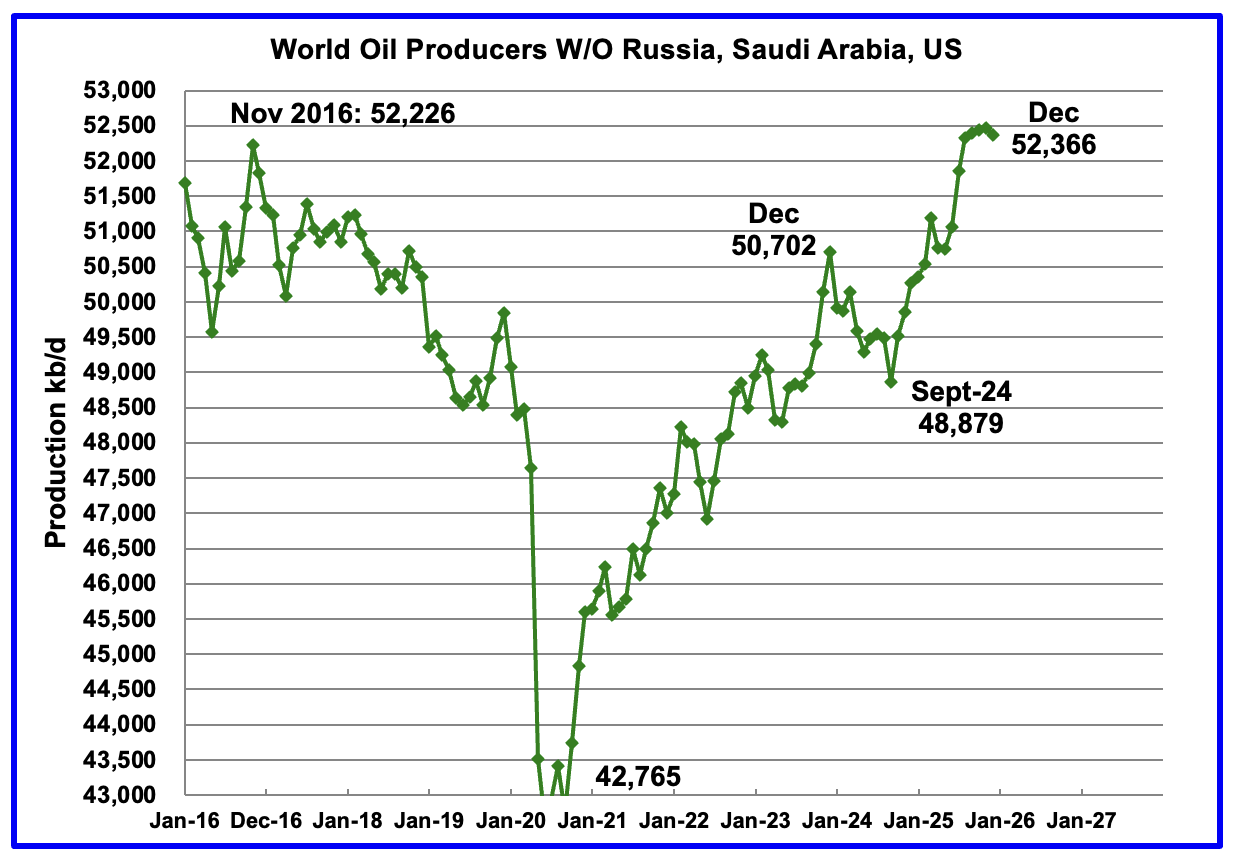

Production in the remaining countries has been slowly increasing since the September 2020 low of 42,765 kb/d but dropped in December. December 2025 production dropped by 100 kb/d to 52,366 kb/d. Gains in Brazil were offset by losses in Kazakhstan, China and Iraq,

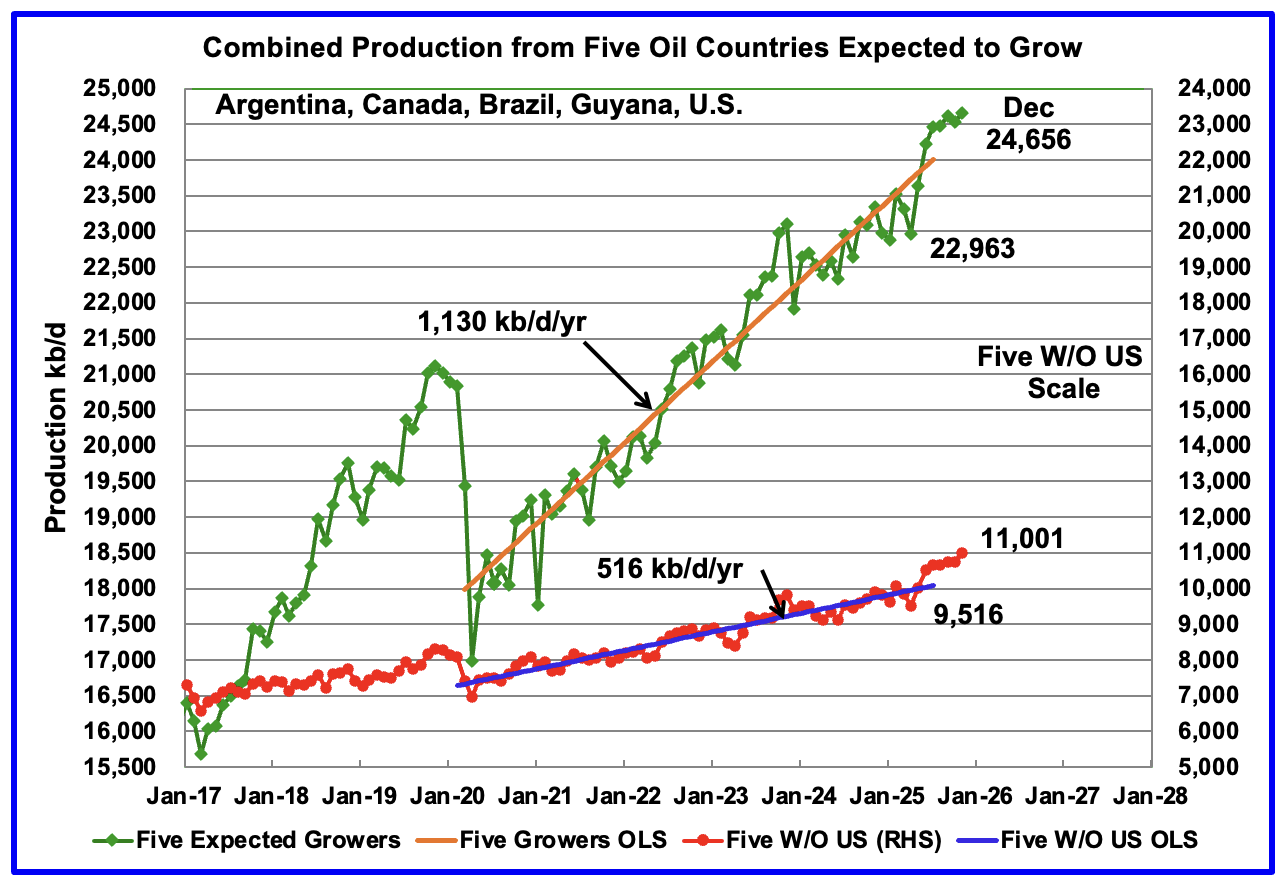

Countries Expected to Grow Oil Production

This chart shows the combined oil production from five Non-OPEC countries, Argentina, Brazil, Canada, Guyana and the U.S., whose oil production is expected to grow. These five countries are often cited by OPEC and the IEA for being capable of meeting the increasing World oil demand for next few years. For these five countries, production from April 2020 to July 2025 rose at an average rate of 1,130 kb/d/year as shown by the orange OLS line.

To show the impact of US growth over the past 5 years, U.S. production was removed from the five countries and that graph is shown in red. The production growth slope for the remaining four countries has been reduced by 614 kb/d/yr to 516 kb/d/yr.

December production has been added to the five growers chart and it rose by 118 kb/d to 24,656 kb/d. December’s production increase was primarily due to the large Brazilian increase offset by the US drop. For the Five growers W/O U.S., December production rose by 251 kb/d to 11,001 kb/d, with Brazil contributing 242 kb/d.

January’s production for the five countries is expected to drop due to drops in Brazil and the US.

Note: The OLS lines are updated to July 2025.

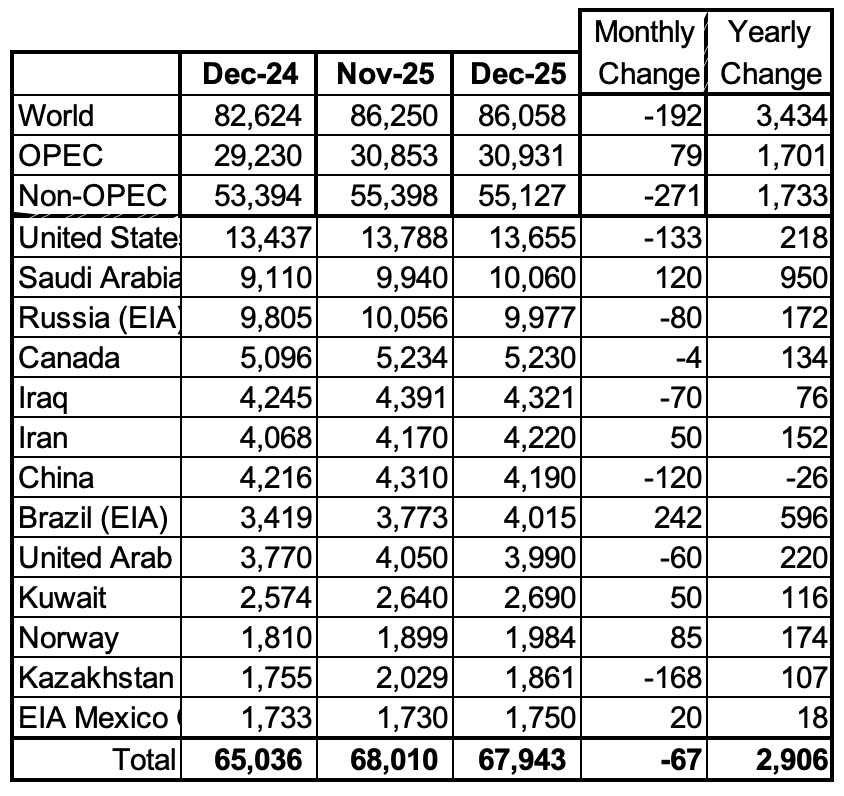

World Oil Countries Ranked by Production

Above are listed the World’s 13th largest oil producing countries. In December 2025 these 13 countries produced 78.9% of the World’s oil. On a MoM basis, production decreased by 67 kb/d in these 13 countries while on a YOY basis production rose by 2,906 kb/d. Note the large YoY increases from Saudi Arabia and Brazil.

December Non-OPEC Oil Production Charts

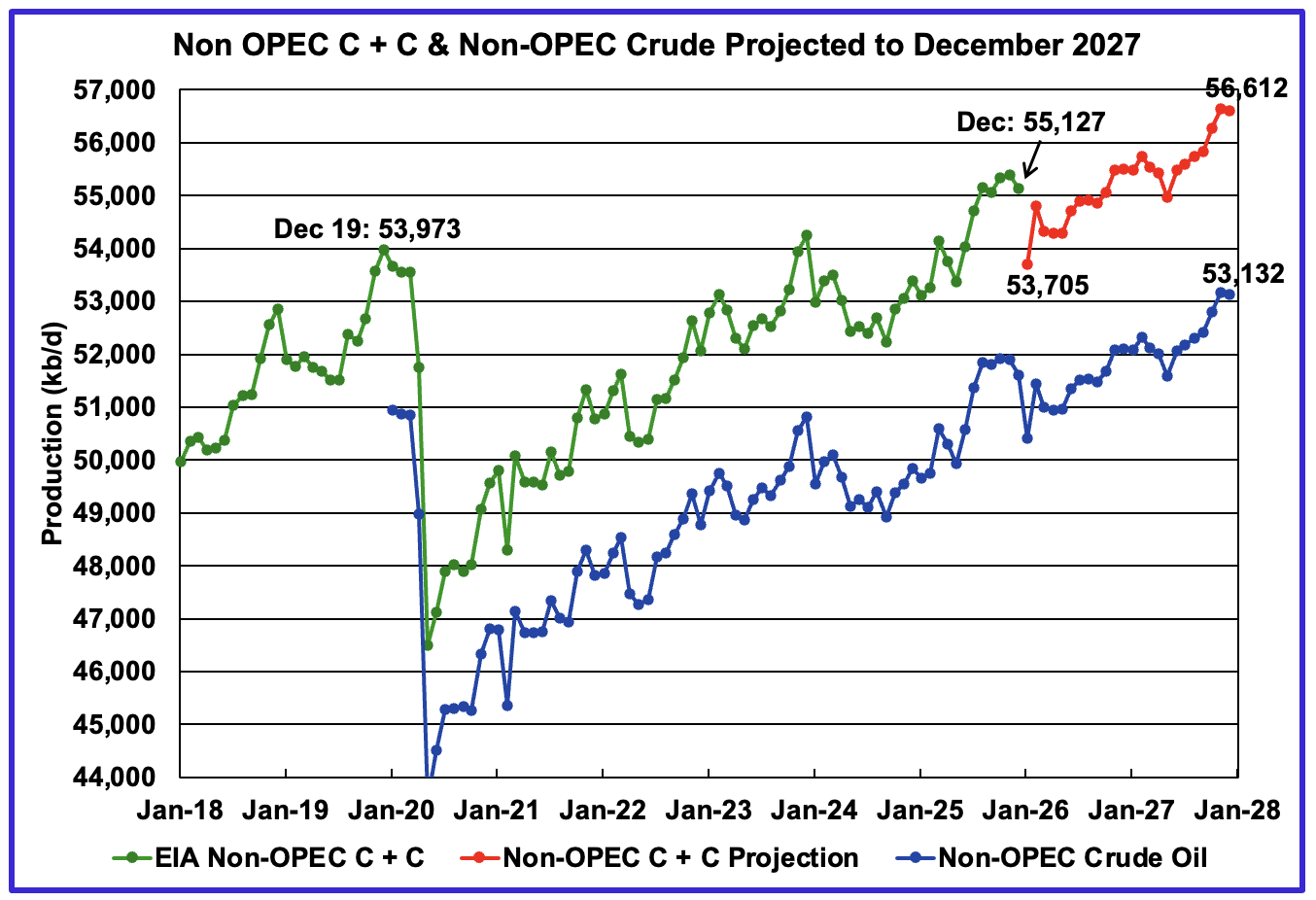

December’s Non-OPEC oil production decreased by 271 kb/d to 55,127 kb/d. January is expected to drop by 1,422 kb/d to 53,705 kb/d. This large production drop is due to large drops in Brazil, China, Kazakhstan and the US.

Using data from the April 2026 STEO, a projection for Non-OPEC oil output was made for the period January 2025 to December 2027. (Red graph). Output is expected to grow by 1,489 kb/d from December 2025 to reach 56,612 kb/d in December 2027.

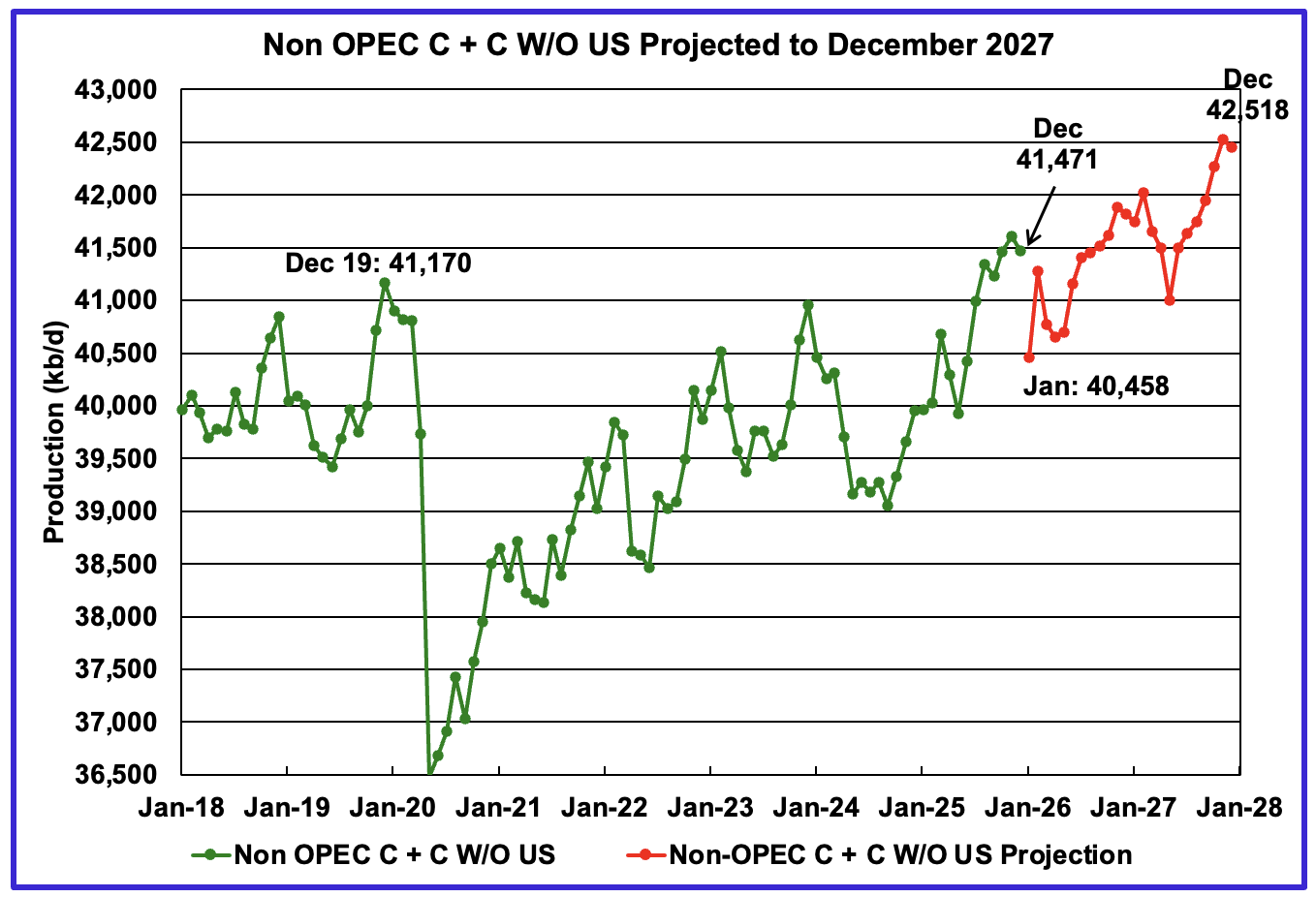

December’s Non-OPEC W/O US oil production decreased by 137 kb/d to 41,471 kb/d. January’s production is projected to drop by 1,013 kb/d to 40,458 kb/d.

From December 2025 to December 2027, production in Non-OPEC countries W/O the U.S. is expected to increase by 1,047 kb/d to 42,518 kb/d.

Non-OPEC Oil Countries Ranked by Production

Listed above are the World’s 11 largest Non-OPEC producers. The original criteria for inclusion in the table was that all of the countries produced more than 1,000 kb/d.

December’s MoM production decreased by 194 kb/d to 46,015 kb/d for these eleven Non-OPEC countries while as a whole the Non-OPEC countries saw a yearly production increase of 1,733 kb/d to 55,127 kb/d. Major yearly gains came from Brazil and the U.S.

In December 2025, these 11 countries produced 83.5% of all Non-OPEC oil.

Non-OPEC Country’s Oil Production Charts

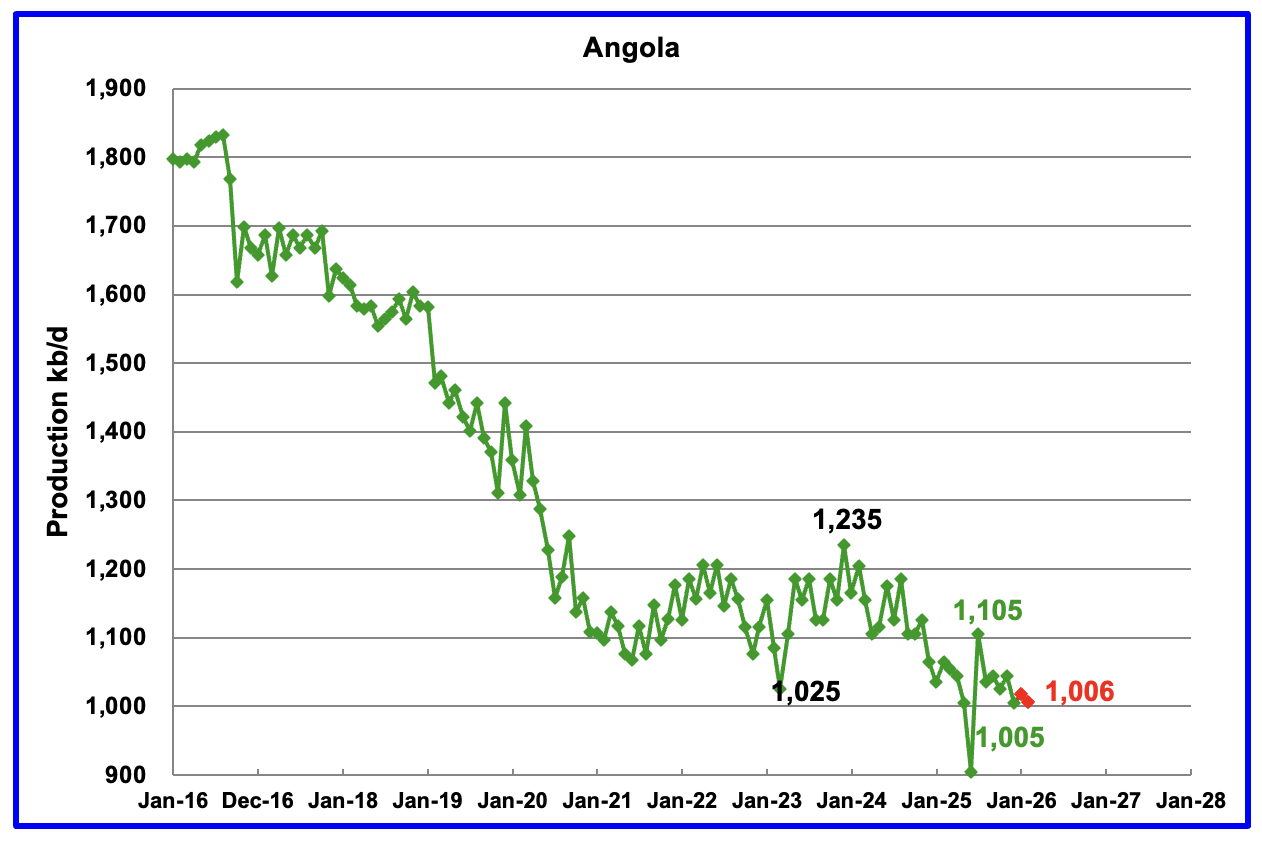

The EIA reported Angola’s December oil production dropped by 40 kb/d to 1,005 kb/d.

According to Angola’s National Agency for Petroleum, December’s production was 1,028 kb/d. Production in February was reported to be 1,006 kb/d, red markers.

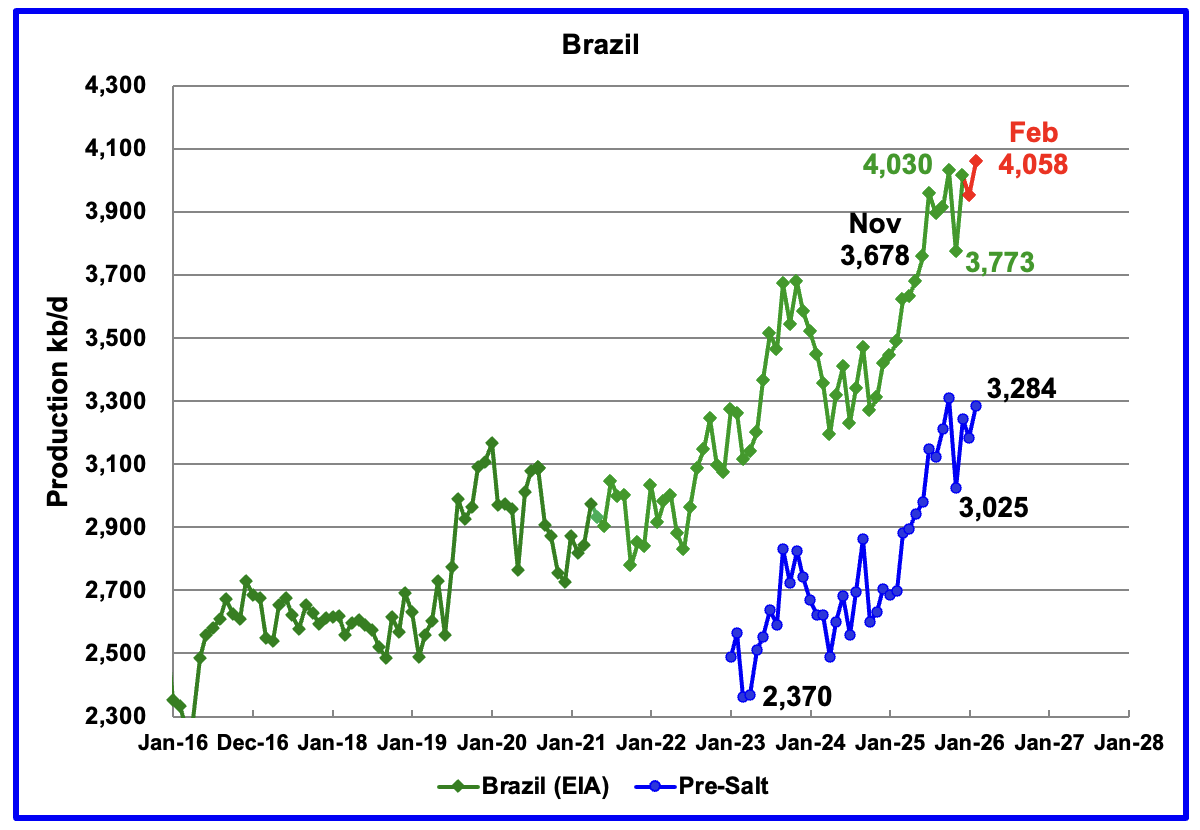

The EIA reported that Brazil’s December production rose by 242 kb/d to 4,015 kb/d. According to this Article, the pre-salt reservoirs remained the backbone of national production, accounting for nearly 80 per cent of total oil and gas output.

Brazil’s National Petroleum Association (BNPA) reported that production dropped in January and rose to a new high in February to 4,058 kb/d.

Pre-Salt production was a major contributor to December’s rebound.

According to the March OPEC MOMR: “Oil project start-ups are expected at the Buzios and Wahoo fields, as well as from the Albacora Leste Cluster. However, operational challenges and unexpected disruptions on certain platforms may still affect the anticipated production timelines.

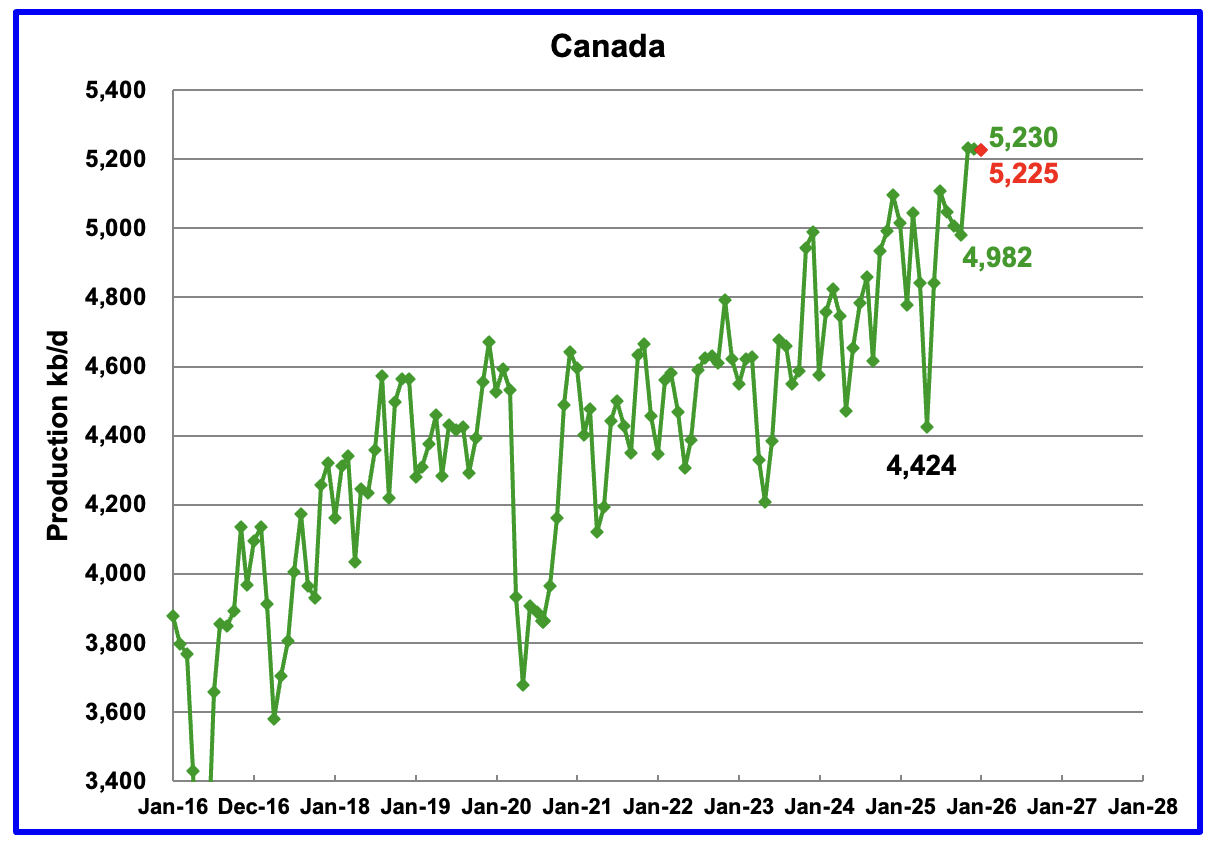

Canada’s oil production decreased by 4 kb/d in December to 5,230 kb/d.

A projection has been made for January production based on preliminary production provided by the Canada Energy Regulator (CER). January’s projected production is expected to drop to 5,225 kb/d, red marker. The CER estimate contains some NGLs which have been removed from the projection. On average the EIA reduces the CER’s monthly production by 375 kb/d which was also done for the December estimate.

According to this Article, Canada is in talks with US officials regarding a proposed revival of part of the canceled Keystone XL oil pipeline.

“The project proposed by Calgary-based pipeline company South Bow and its U.S. partner Bridger Pipeline – which could increase Canada’s crude exports to the U.S. by more than 12 per cent if it goes ahead – was one of the topics Hodgson said he and Canada’s Ambassador to the U.S., Mark Wiseman, discussed with U.S. Energy Secretary Chris Wright and U.S. Secretary of the Interior Doug Burgum.

Canada is framing the prospect of a new cross-border oil pipeline as a way it can help the U.S. achieve energy security even as the war in Iran disrupts supplies and raises prices for consumers, Hodgson said in an interview at the CERAWeek by S&P Global conference.”

The EIA reported China’s December oil output dropped by 120 kb/d to 4,190 kb/d. On a YoY basis, China’s December production decreased by 26 kb/d. For January and February, China reported average production of 4,423 kb/d.

Note the large drop of 310 kb/d from March 2025 to December 2025. That appears to be a record drop over those nine months.

For the last two years, March has proven to be a record production month. Will this March become another new record?

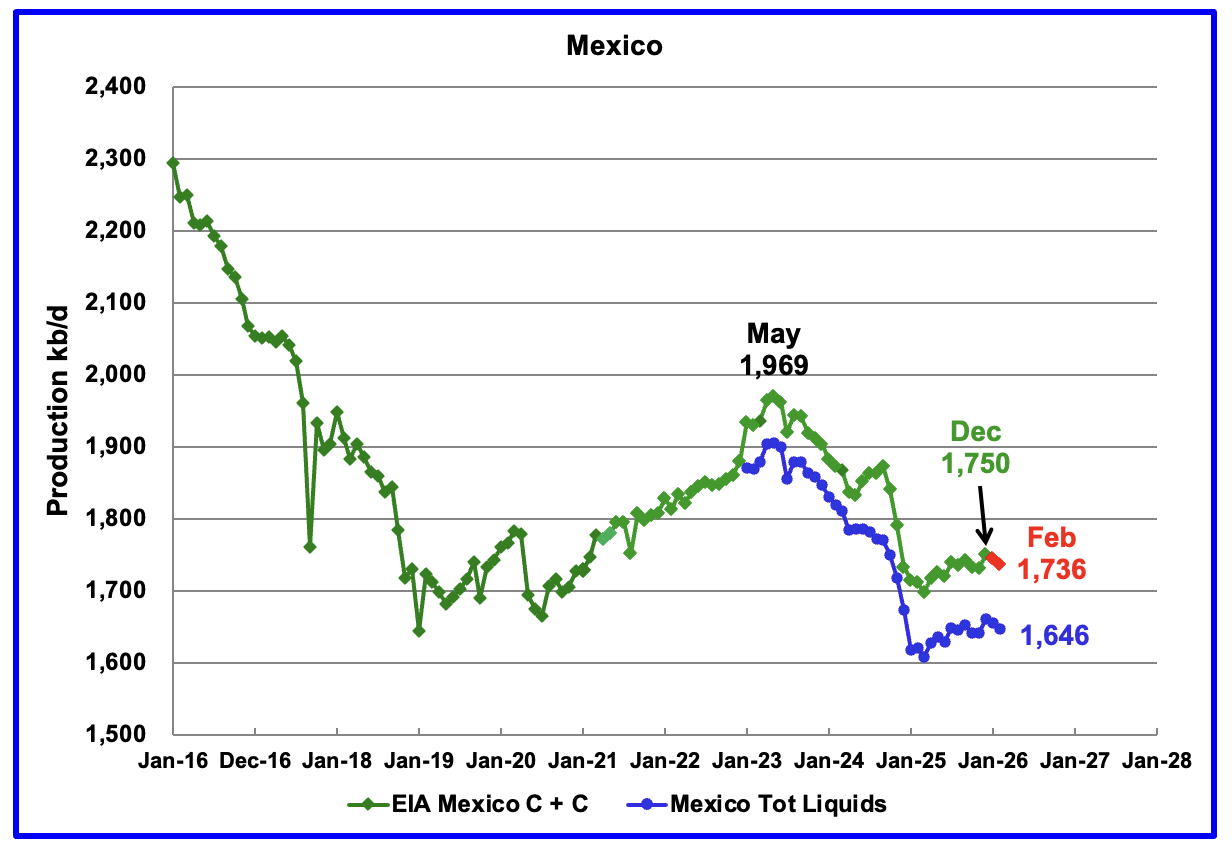

According to the EIA, Mexico’s December output rose by 20 kb/d to 1,750 kb/d.

In June 2024, Pemex issued a new and modified oil production report for Heavy, Light and Extra Light oil. It is shown in blue in the chart and it appears that Mexico is not reporting condensate production when compared to the EIA report.

In earlier EIA reports, they would add close to 55 kb/d of condensate to the Pemex’s “Total Liquids” report. More recently the EIA has been adding 90 kb/d of condensate to Mexican production. For January and February production, 90 kb/d have been added to the Pemex report. February’s production is estimated to be close to 1,736 kb/d. Note that Mexico’s production, as reported by Pemex for the last eight months has stabilized around 1,650 kb/d.

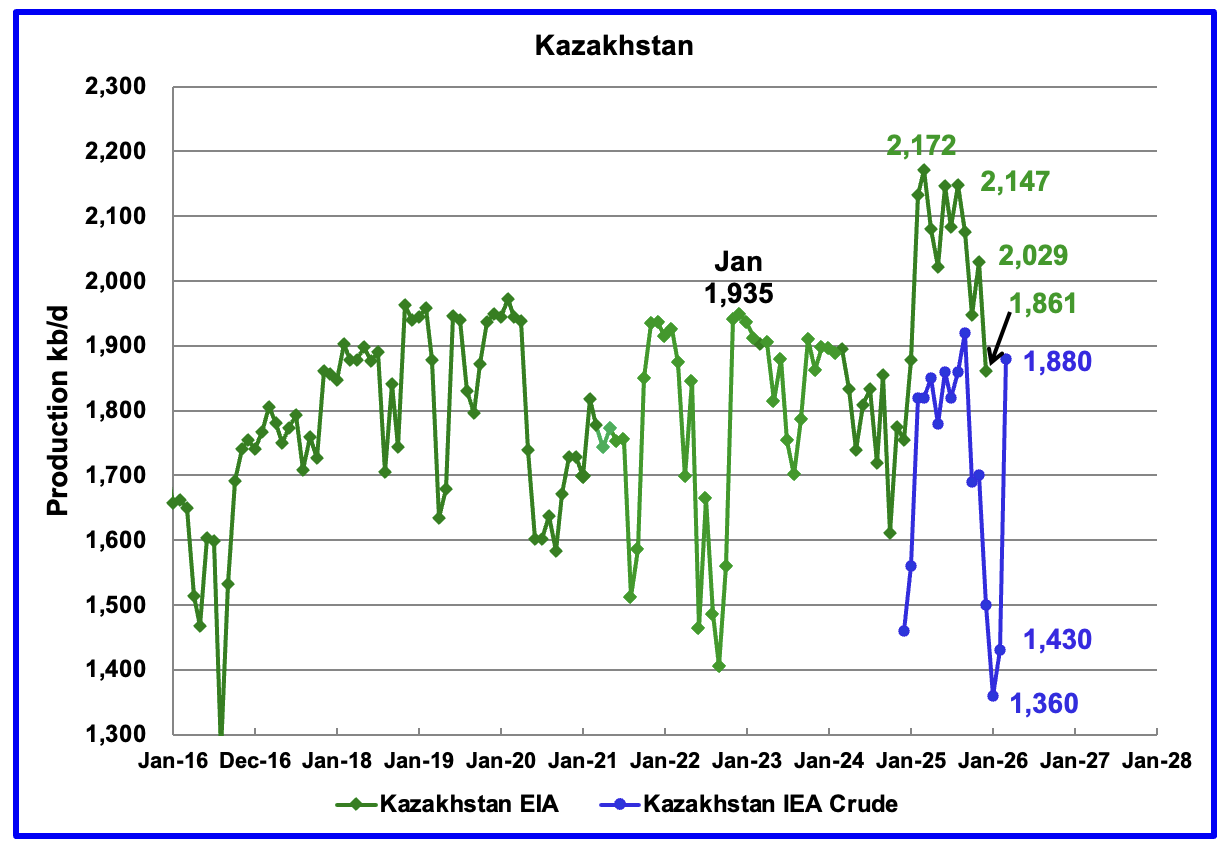

According to the EIA, Kazakhstan’s December oil output decreased by 168 kb/d to 1,861 kb/d.

Since Argus no longer reports OPEC + crude production, production data for Kazakhstan will now be taken from the monthly IEA reports. The IEA’s March OMR reported January 2026 production was 1,360 kb/d. The April OMR reported that production rebounded in February and March. March production rebounded by 450 kb/d to 1,880 kb/d even though this Report stated that Kazakhstan was supposed to reduce production in March.

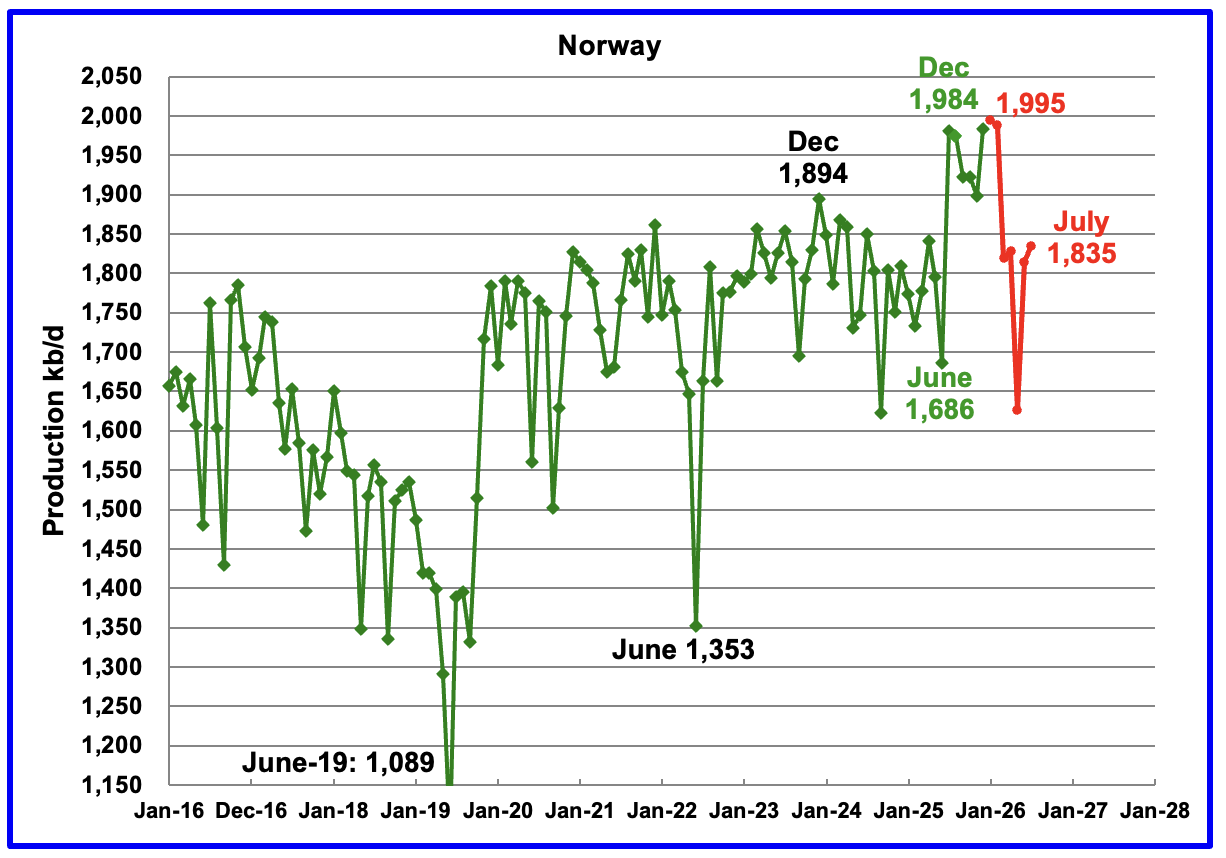

The EIA reported Norway’s December production rose by 85 kb/d 1,984 kb/d.

Separately, the Norway Petroleum Directorate (NPD) reported that January’s oil production rose to 1,995 kb/d, a new high, red markers.

The Norway Petroleum Directorship also reported that February’s oil production dropped to 1,988 kb/d and was 5.7 % above forecast. The red markers are the NPD’s production forecast.

According to OPEC’s March MOMR: “Norwegian liquids production is forecast to drop by about 40 tb/d to average 2.0 mb/d in 2026. Several projects are scheduled to ramp up through the year, including Balder/Ringhorne, Heidrun, Gina Krog, Maria, and Snohvit.

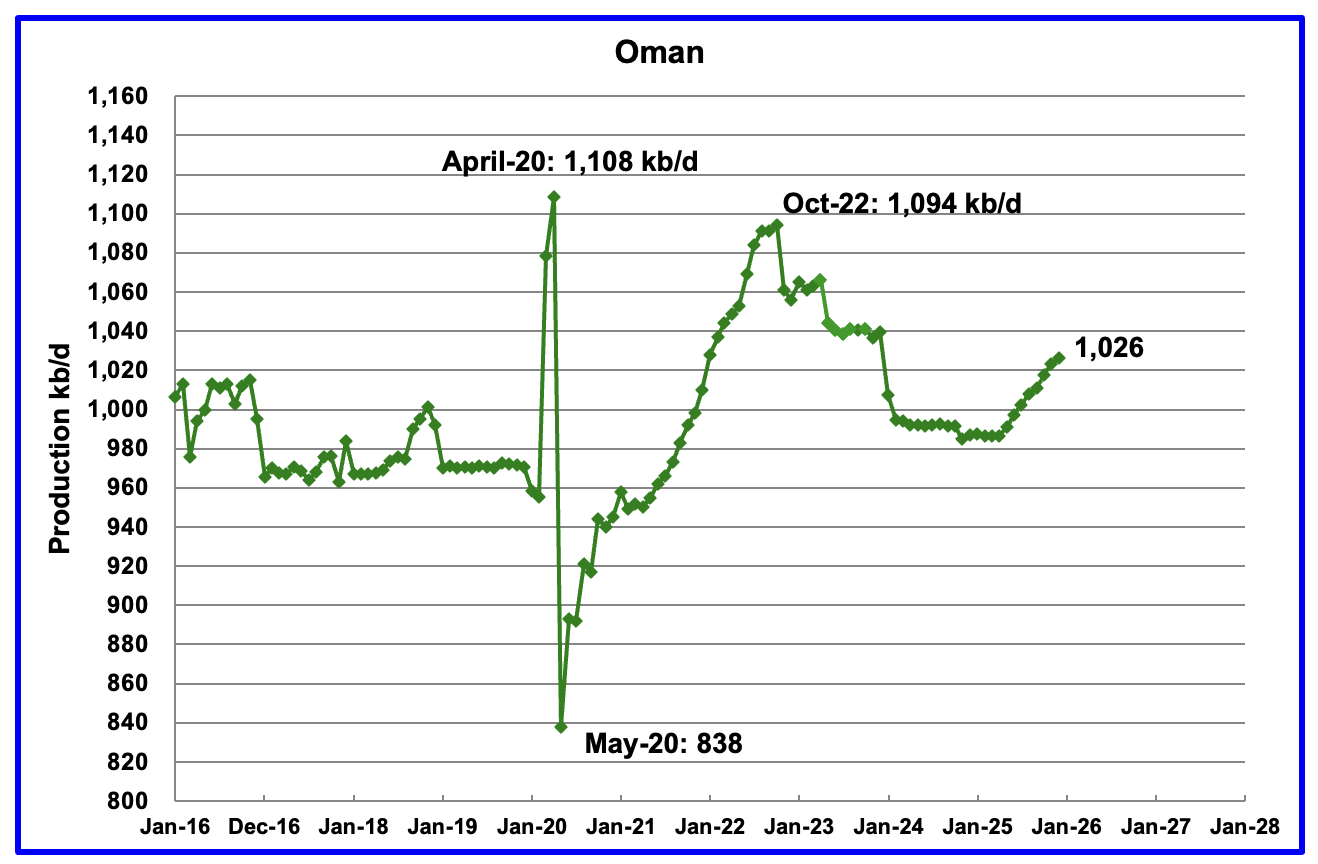

According to the EIA, December’s output rose by 3 kb/d to 1,026 kb/d. Oman’s production appears to have started a budding growth phase. Previous production peaked in October 2022.

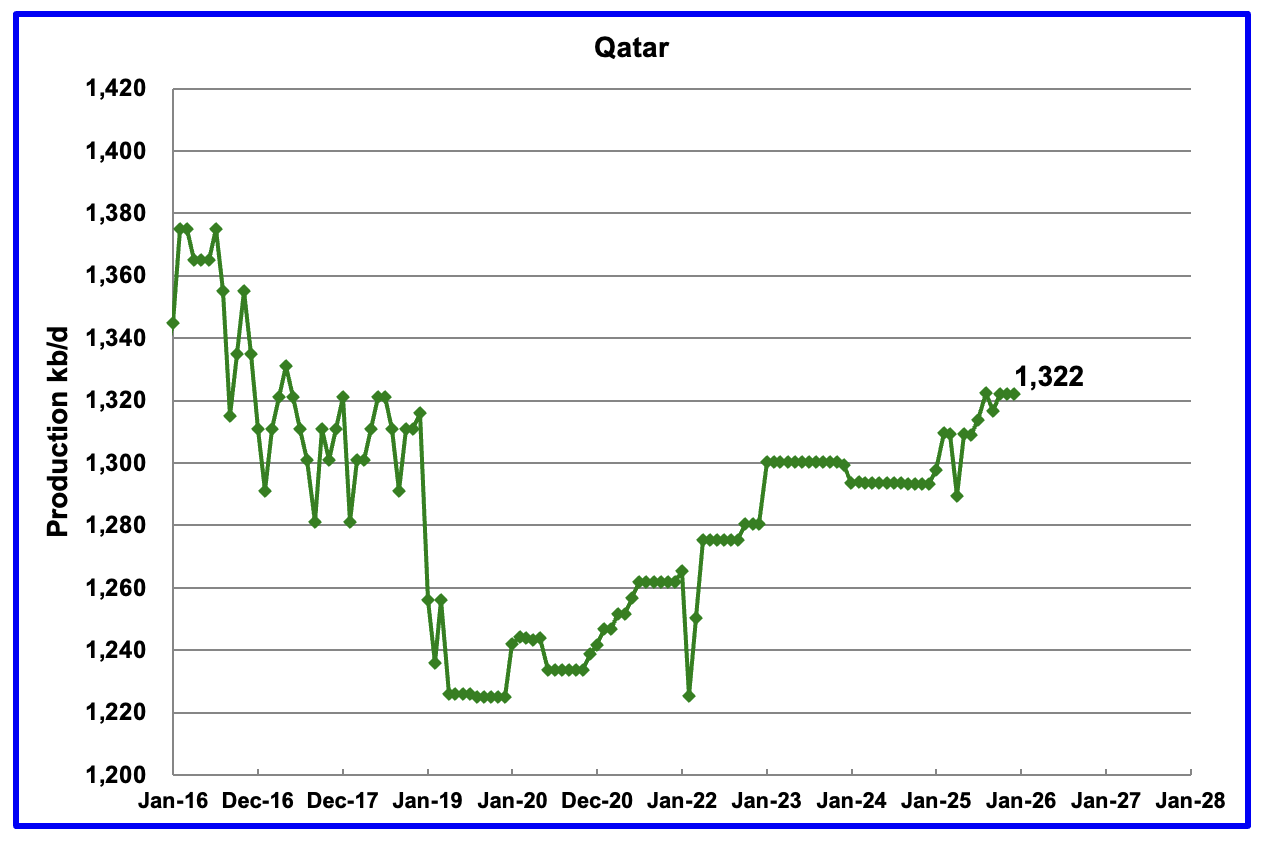

Qatar provided the EIA with monthly updated oil production back to January 2025 but seems to have stopped again in August. Qatar’s December output was reported to be 1,322 kb/d, unchanged from November.

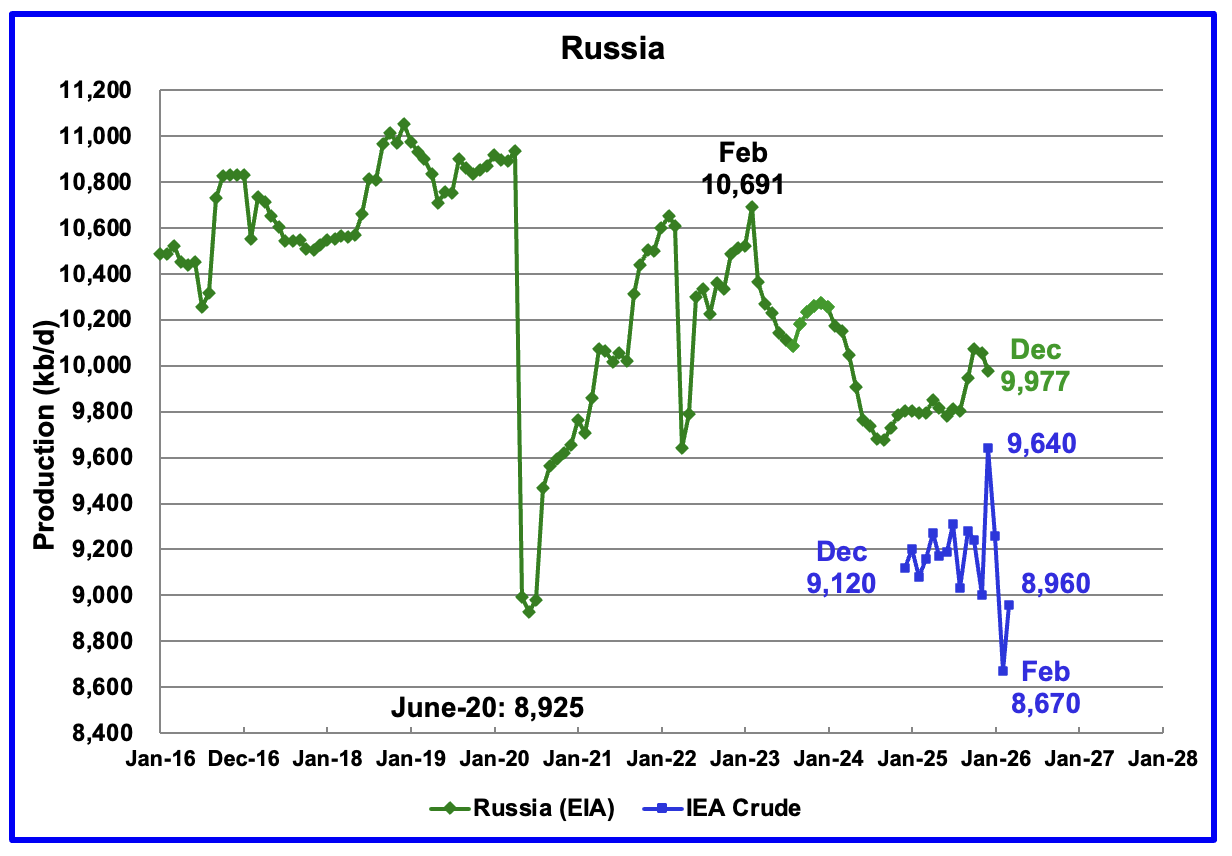

The EIA reported Russia’s December C + C production decreased by 80 kb/d to 9,977 kb/d and was up by 172 kb/d from December 2024.

Up to August 2025 Argus Media used to report OPEC + crude production which included Russian production. That monthly report has now been discontinued. The above chart now shows Russian production as reported by the IEA. It is difficult to assess the accuracy of the IEA report but over the last few months before publication stopped the IEA’s Russian production had been around 100 kb/d to 150 kb/d higher than Argus’ Media. The best that can be done at this time will be to compare the production trends between the EIA and the IEA. I think that Russian oil production continues to be a major state secret at this time because of the damage being caused by the heavy bombing to its related crude oil processing facilities.

According to the IEA’s February report, December’s crude production rose by 640 kb/d to 9,640 kb/d. The April IEA OMR is reporting that Russian crude production hit a new February low of 8,670 kb/d and rebounded to 8,960 kb/d in March. This is the first clear indication that Russian production is being affected by the Russia/Ukraine war.

The OPEC April MOMR is reporting Russian Crude production in February and March was 9,164 kb/d and 9,167 kb/d, respectively. February does not compare well with the IEA’s 8,670 kb/d but March is a bit better with OPEC’s estimate being 207 kb/d higher than the IEA’s 8,960 kb/d.

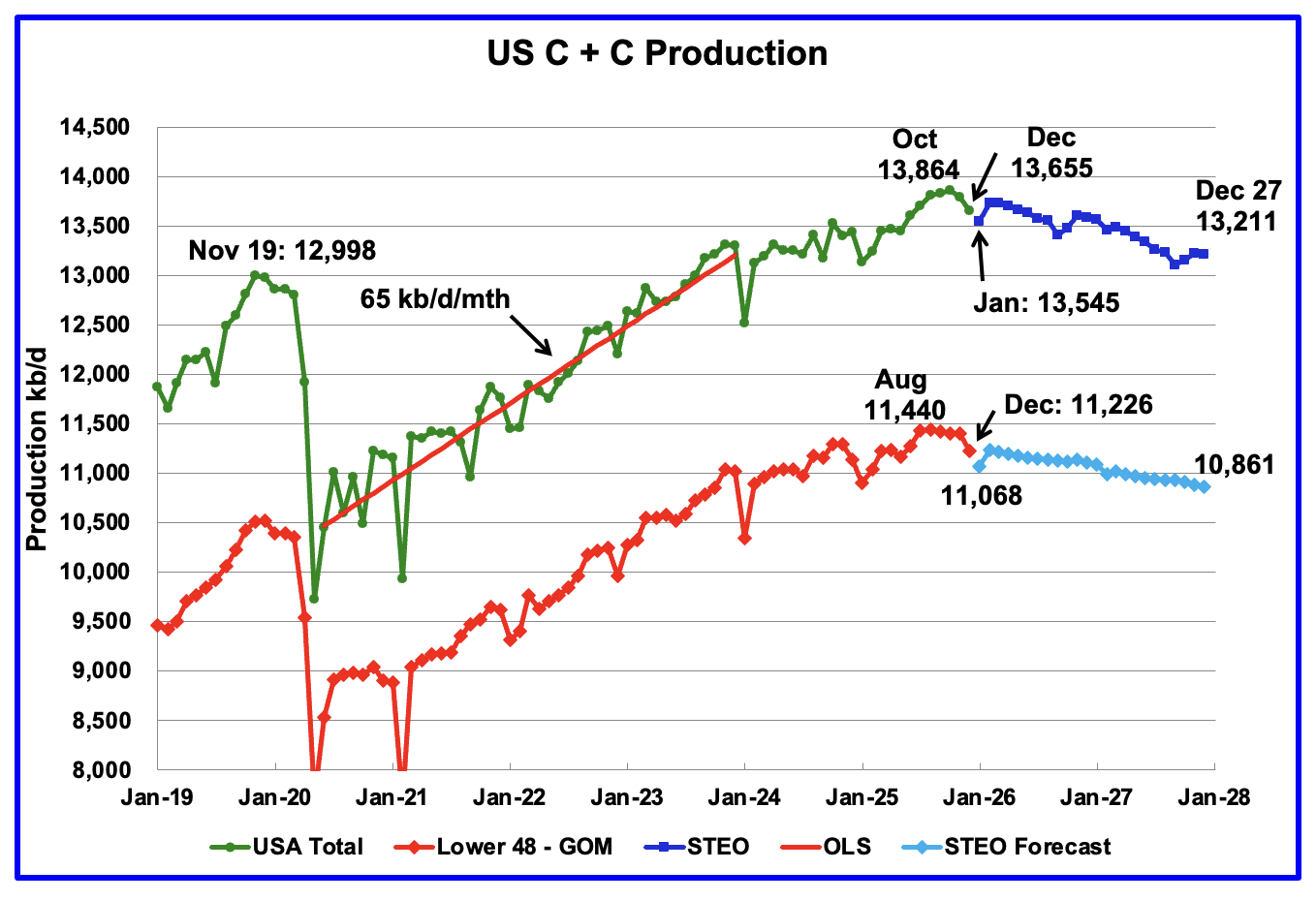

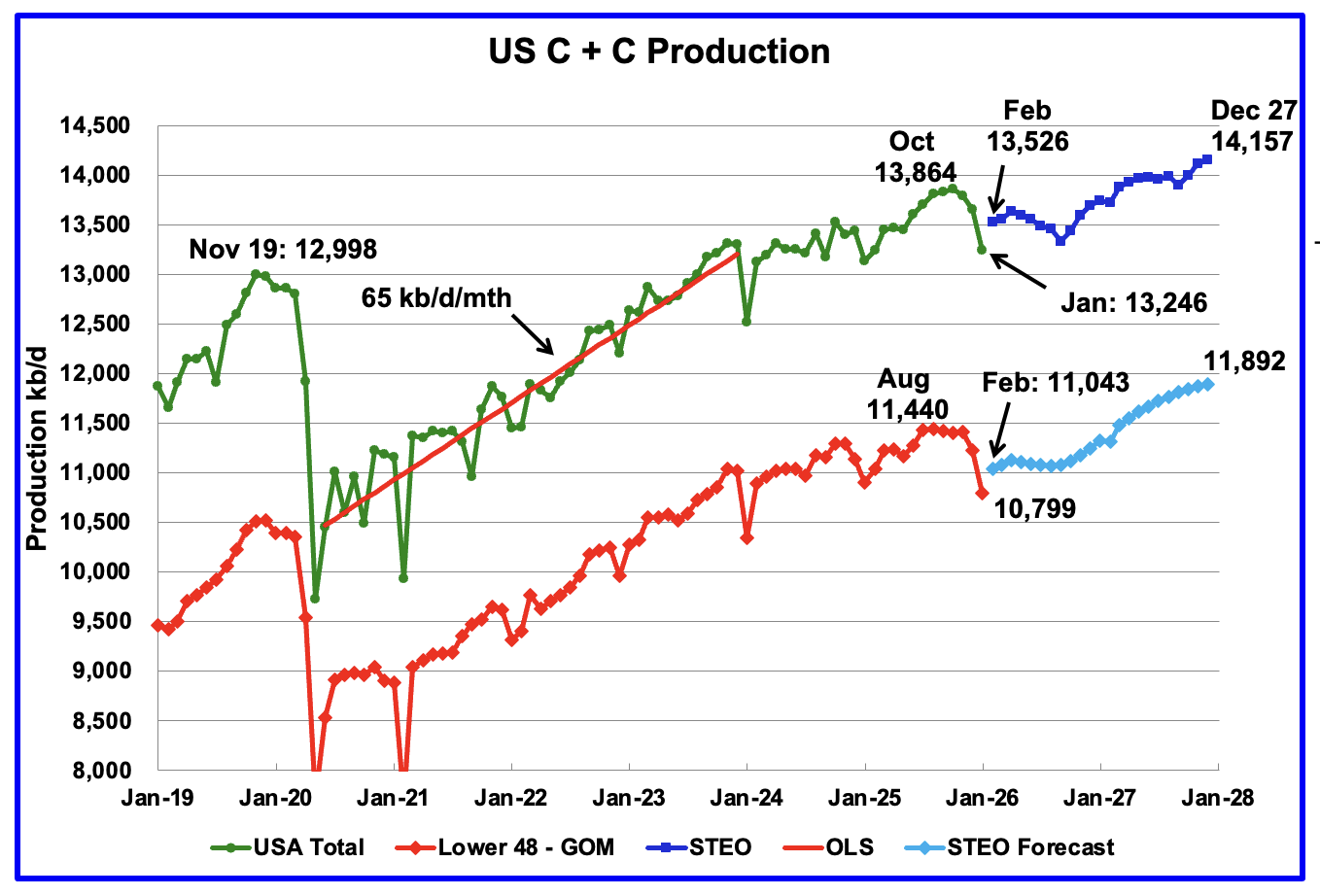

February STEO Projection

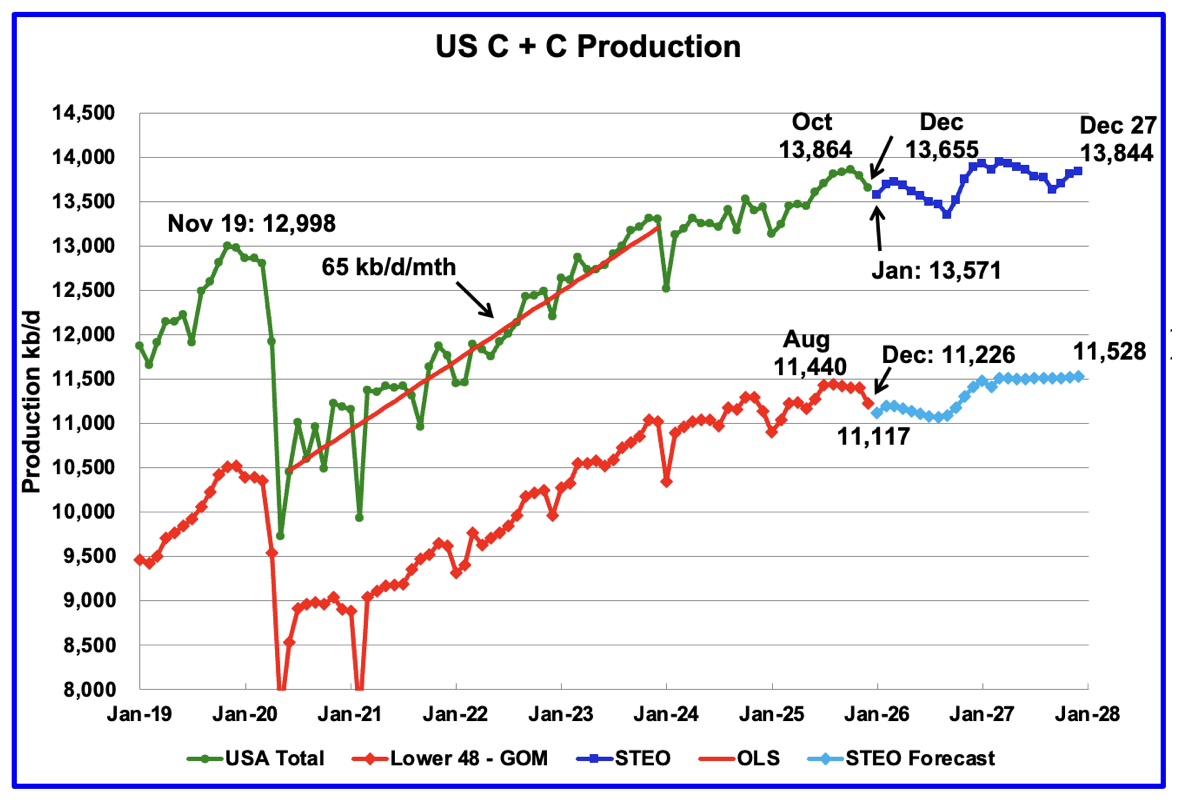

March STEO Projection

April STEO Projection

This last US production chart showing output up to January 2026 is the same as the one published last week in the US update. However the projected portion of the two production graphs, light and dark blue, have been updated according to the April 2026 STEO.

This is a case where a few pictures are worth a 1,000 words. To show how significantly the STEO projections have changed over the last three months, the STEO projections for February, March and April are posted above for comparison.

For US production, December 2027 production has gone from 13,211 kb/d in the February STEO to 14,157 kb/d in the April STEO, an increase of 946 kb/d. For Onshore L48 production, December 2027 production has gone from 10,861 kb/d in the February STEO to 11,892 kb/d in the April STEO, an increase of 1,031 kb/d. The rising production comes from increases in the Permian, Bakken and Eagle Ford basins.

Clearly the STEO’s price projection to $109/b for WTI in April and then slowly dropping back to $64/b should induce more drilling. However there is no indication of the quality of the wells the new drilling will be bringing on.

We need to track the upcoming weekly rig counts and keep a close eye on them. The weekly oil rig count has been essentially flat at close to 367 operational rigs since August 2025.

Argentina’s production has grown by 115 kb/d since May. Red markers are production as reported by the Argentina Ministry of Energy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply to DC Cancel reply