By Ovi

The focus of this post is an overview of World oil production along with a more detailed review of the top 11 Non-OPEC oil producing countries. OPEC production is covered in a separate post.

Below are a number of Crude plus Condensate (C + C) production charts, usually shortened to “oil”, for the oil producing countries. The charts are created from data provided by the EIA’s International Energy Statistics and are updated to November 2025. This is the latest and most detailed/complete World oil production information available. Information from other sources such as OPEC, IEA, STEO and country specific sites such as Brazil, Norway, Mexico, Argentina and China is reported to provide an extra one or two month outlook.

The EIA March STEO report has made significant and major revisions to the projected World oil production due to the US/Iranian war. Also US projected production has been significantly revised upward. See US chart at the end.

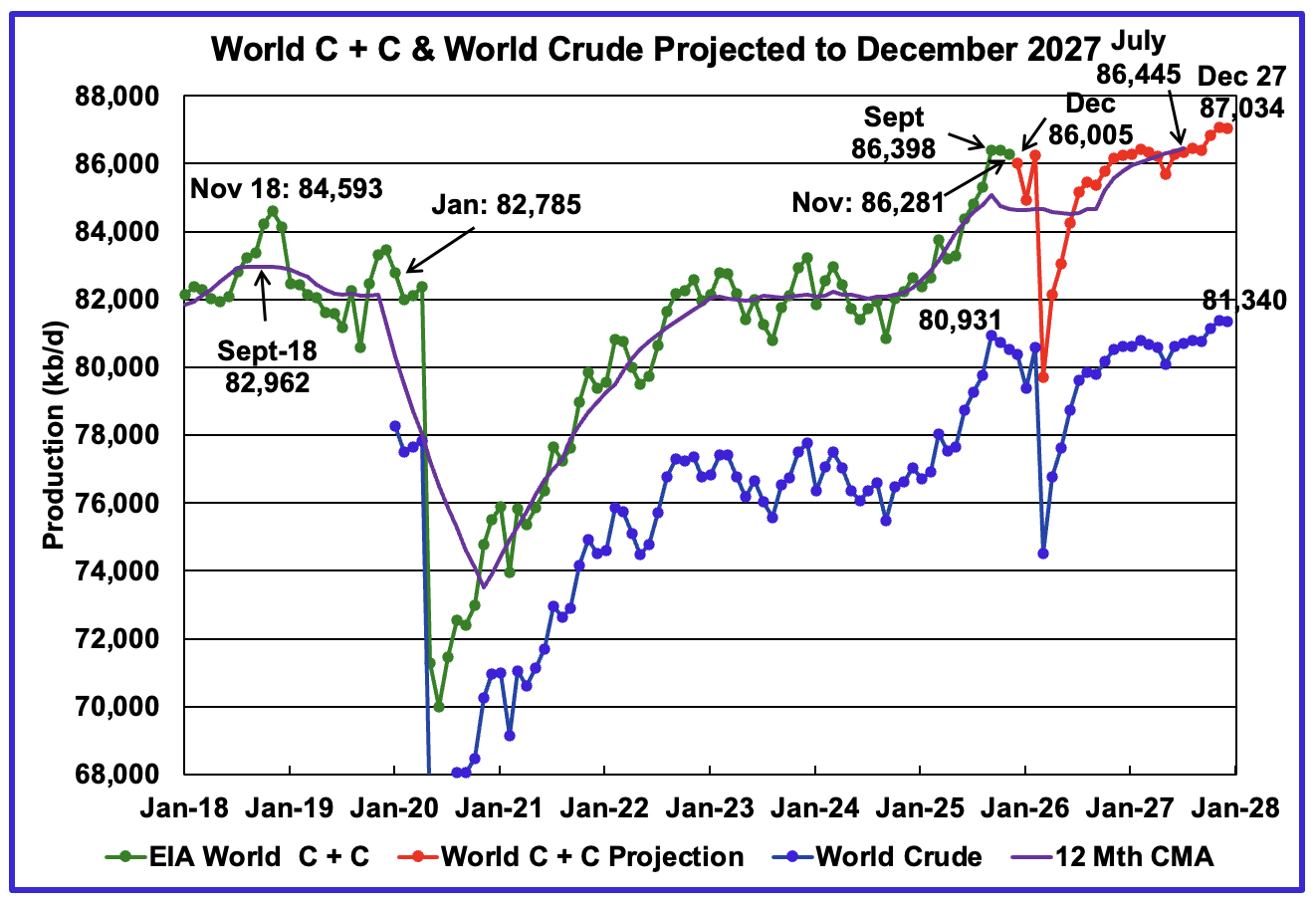

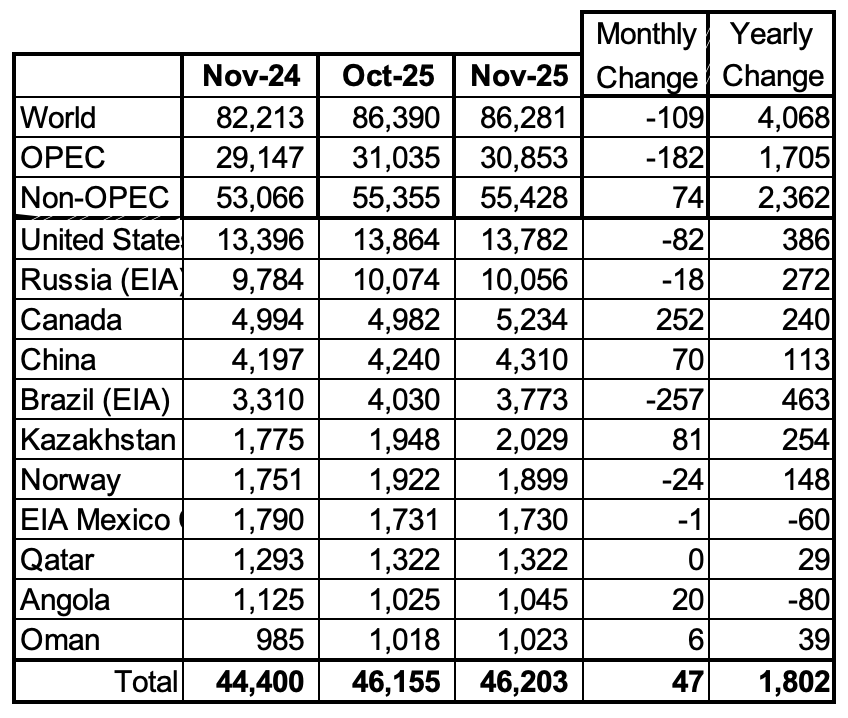

The World’s November oil production decreased by 109 kb/d to 86,281 kb/d.

September 2025 is the new World Peak Oil at 86,428 kb/d for the next year and a half when in late 2027 more oil production is brought online. Note that after the March output crash, oil production only gets back to the November 2025 production level in November 2026.

This chart has been updated using the March 2026 STEO to project World C + C production out to December 2027. It uses the STEO report along with the International Energy Statistics to make the projection. Production in December 2025 is projected to decrease by 276 kb/d to 86,005 kb/d. March production drops by more than 6,000 kb/d due to the Iran/US war.

The 12 month Centred Moving Average shown at July 2027 is 86,445 kb/d vs the September 2018 12 month CMA of 82,962 kb/d.

For December 2027, production is projected to be 87,034 b/d, a new projected high and an upward revision of 674 kb/d from the previous report. Most of that increase is from the US. See US chart below.

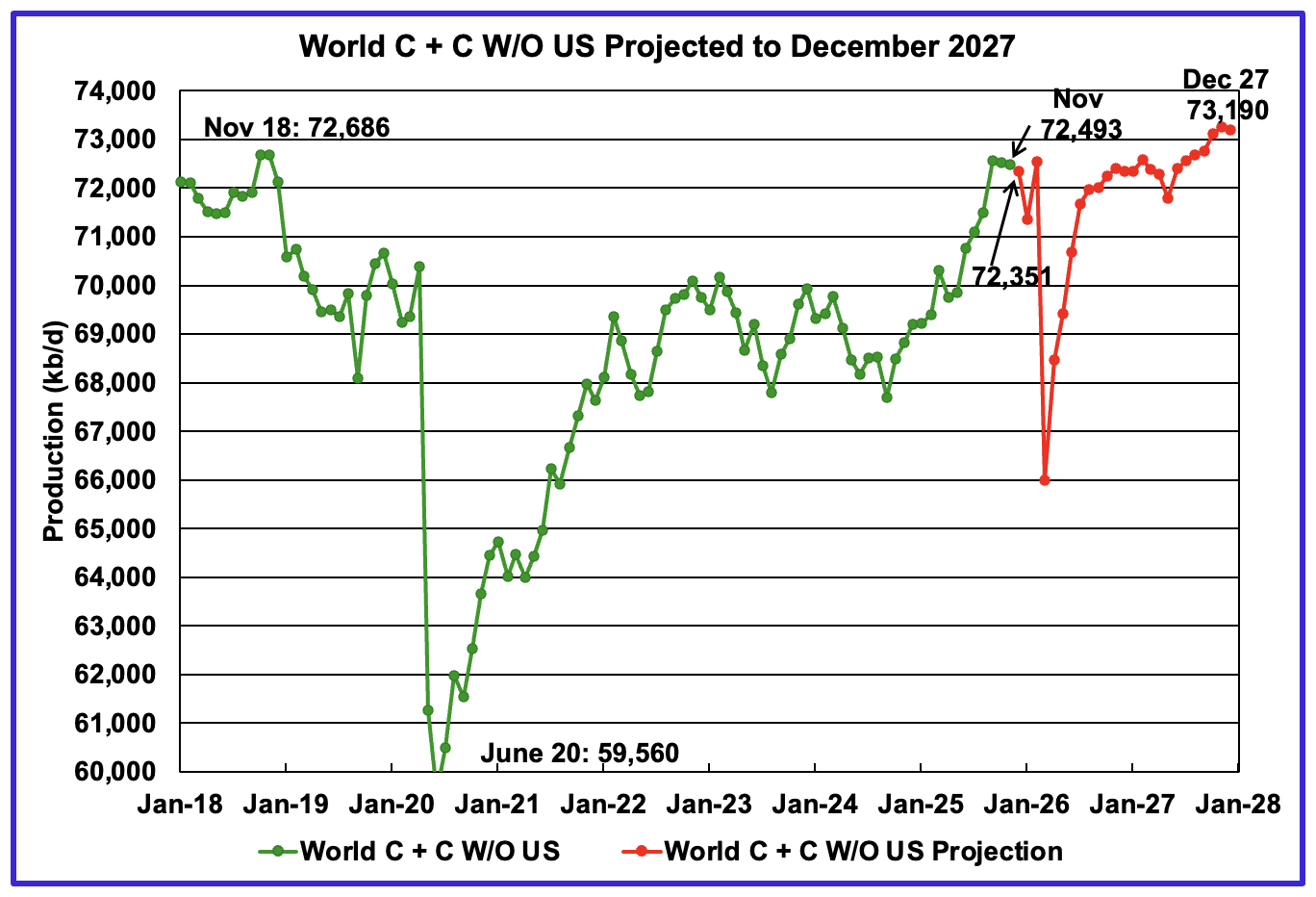

November’s World oil output W/O the US decreased by 33 kb/d to 72,493 kb/d. December’s production is expected to decrease by 142 kb/d to 72,351 kb/d.

The projection is forecasting that December 2027 World W/O US oil production will be 73,190 kb/d, an increase of 697 kb/d from November 2025.

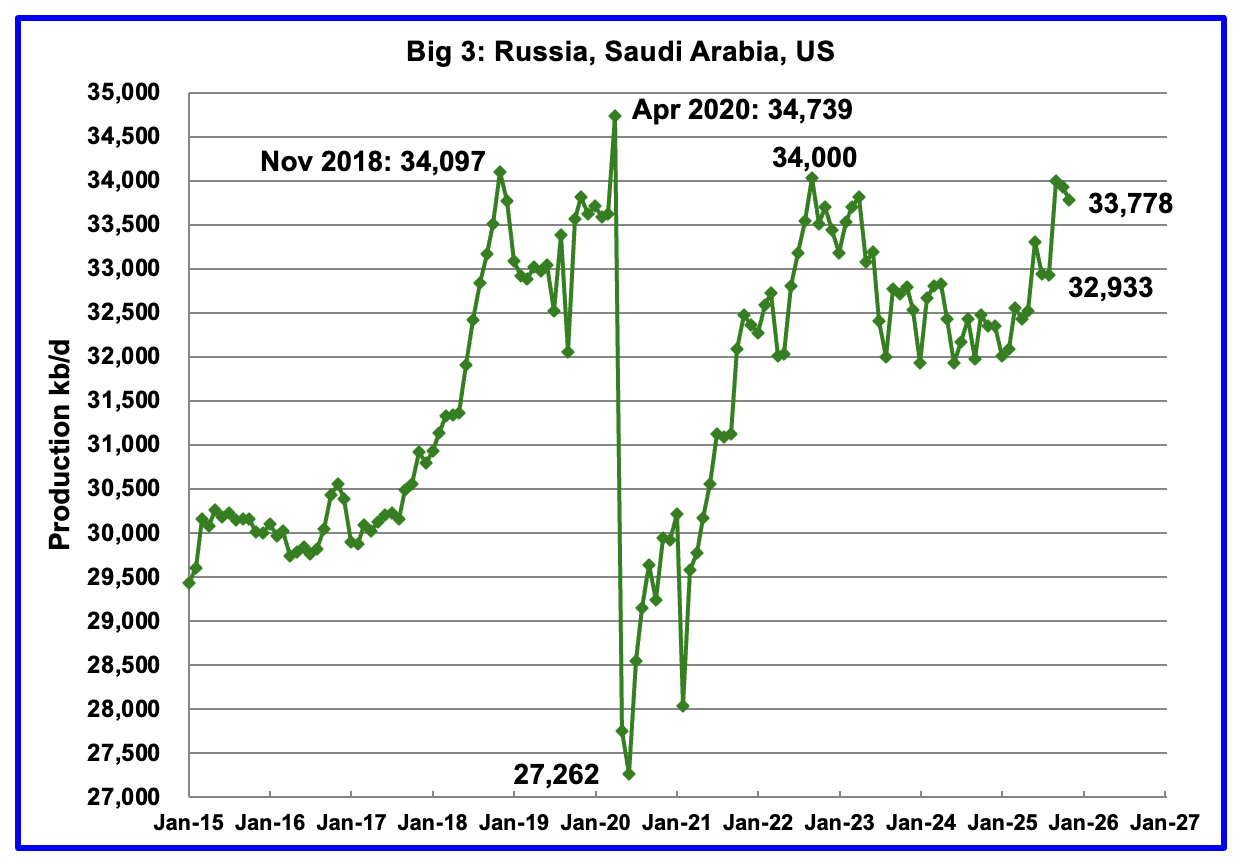

A Different Perspective on World Oil Production

November’s Big 3 oil production decreased by 150 kb/d to 33,778 kb/d.

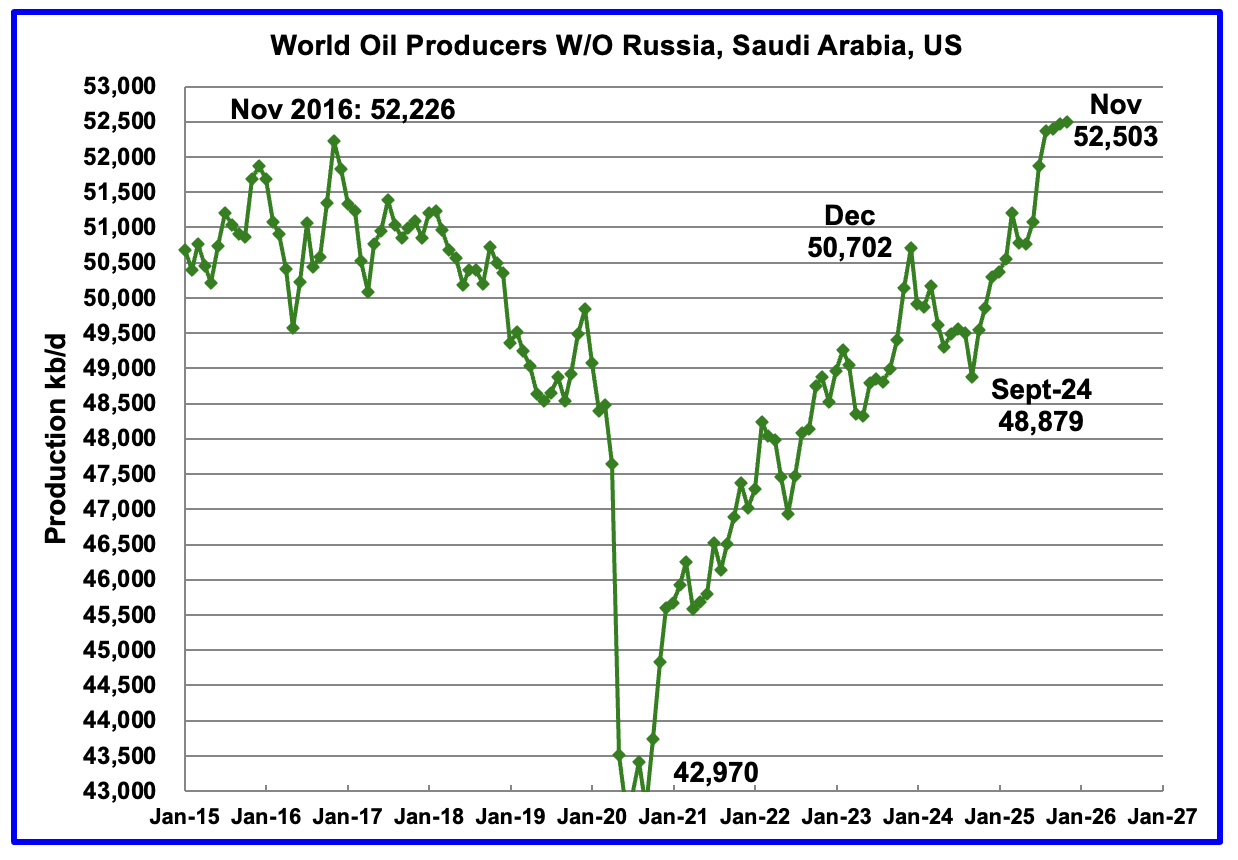

Production in the remaining countries has been slowly increasing since the September 2020 low of 42,970 kb/d. Production rose in November 2025 by 41 kb/d to 52,503 kb/d.

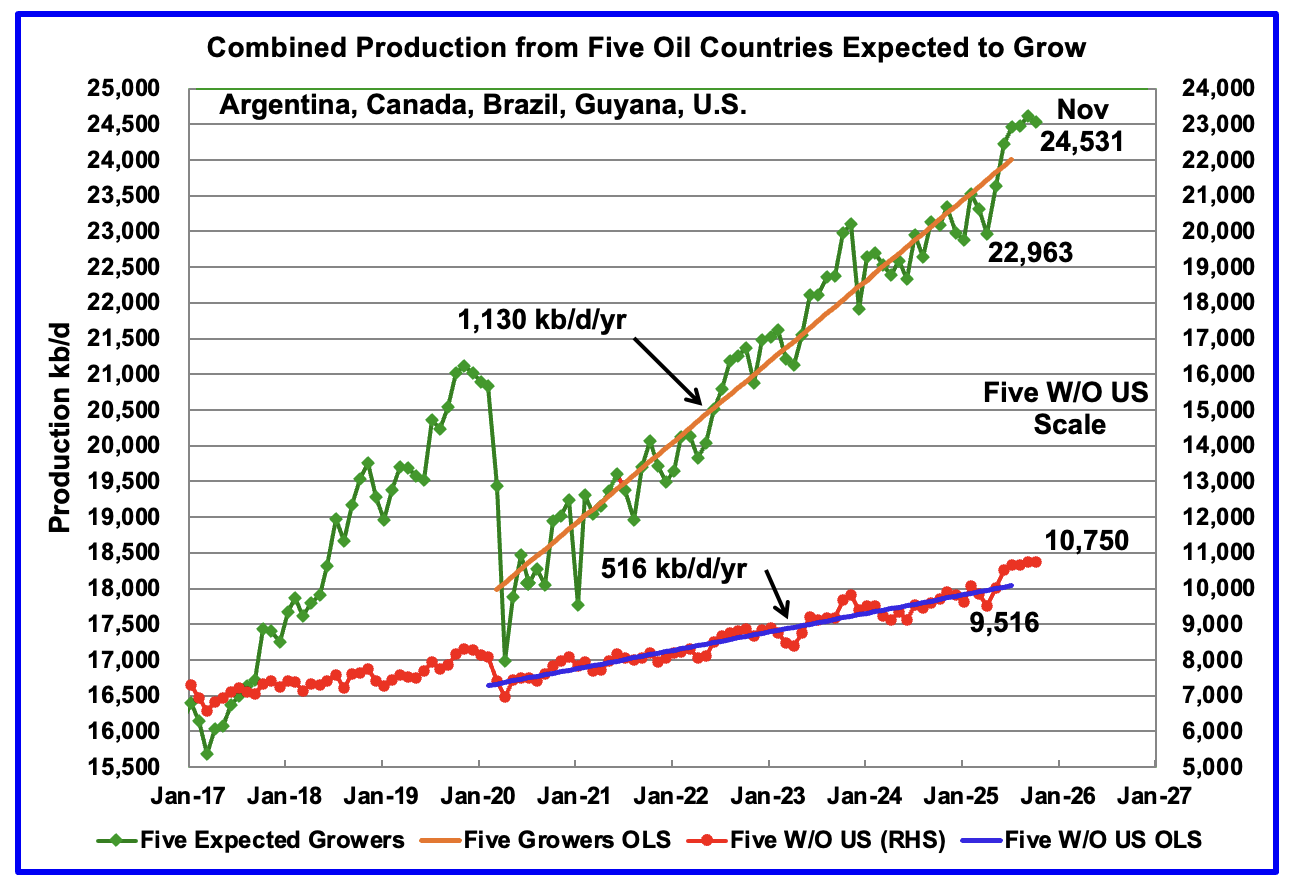

Countries Expected to Grow Oil Production

This chart shows the combined oil production from five Non-OPEC countries, Argentina, Brazil, Canada, Guyana and the U.S., whose oil production is expected to grow. These five countries are often cited by OPEC and the IEA for being capable of meeting the increasing World oil demand for next few years. For these five countries, production from April 2020 to July 2025 rose at an average rate of 1,130 kb/d/year as shown by the orange OLS line.

To show the impact of US growth over the past 5 years, U.S. production was removed from the five countries and that graph is shown in red. The production growth slope for the remaining four countries has been reduced by 614 kb/d/yr to 516 kb/d/yr.

November production has been added to the five growers chart and it dropped by 90 kb/d to 24,531 kb/d. November’s production drop was a mix of small gains and declines. For the Five growers W/O U.S., November production dropped by 7 kb/d to 10,750 kb/d.

December production for the five countries is expected to be up a bit and then drop in January,

Note: The OLS lines are updated to July 2025.

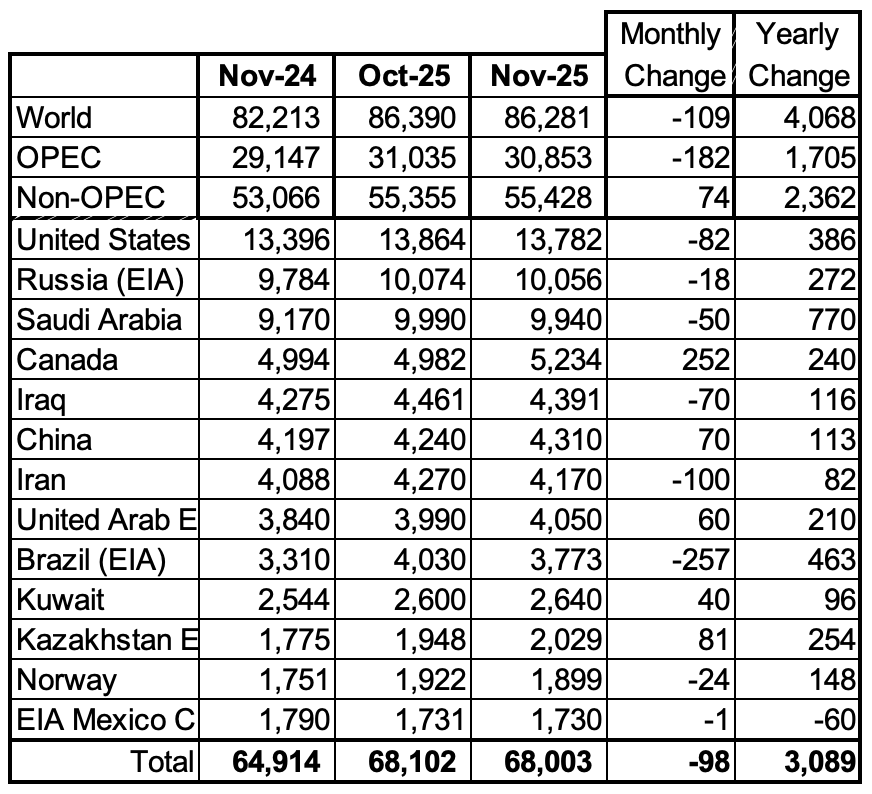

World Oil Countries Ranked by Production

Above are listed the World’s 13th largest oil producing countries. In November 2025 these 13 countries produced 78.8% of the World’s oil. On a MoM basis, production decreased by 98 kb/d in these 13 countries while on a YOY basis production rose by 3,089 kb/d. Note the large YoY increases from Saudi Arabia, Brazil and the US..

November Non-OPEC Oil Production Charts

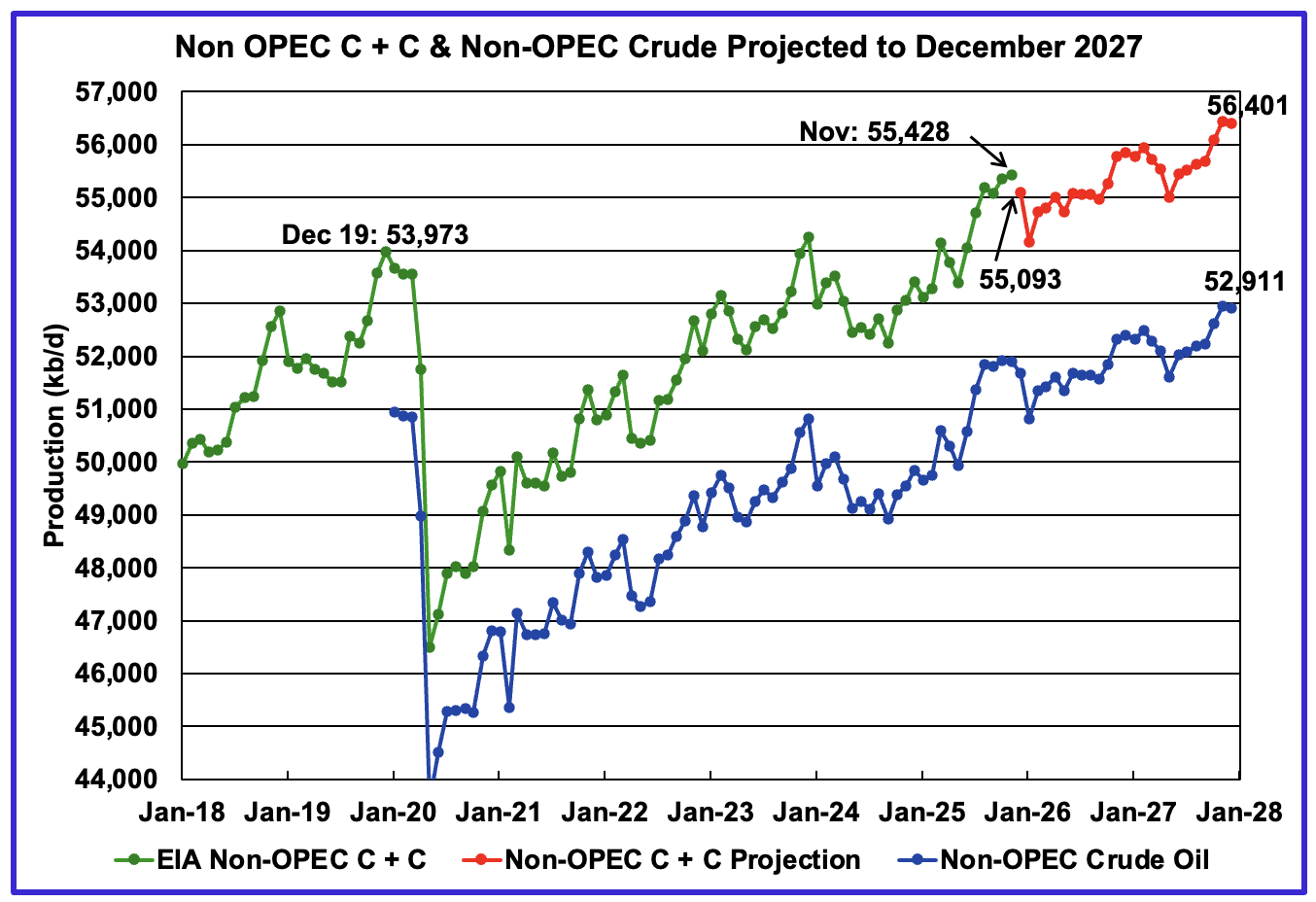

November’s Non-OPEC oil production increased by 74 kb/d to 55,428 kb/d. December is expected to drop by 335 kb/d to 55,093 kb/d. A much lager drop of 935 kb/d to 54.157 kb/d in expected in January.

Using data from the March 2026 STEO, a projection for Non-OPEC oil output was made for the period December 2025 to December 2027. (Red graph). Output is expected to grow by 973 kb/d from November 2025 to reach 56,401 kb/d in December 2027.

December 2027 production was revised up by 681 kb/d from 55,720 kb/d. The increase came mostly from the US.

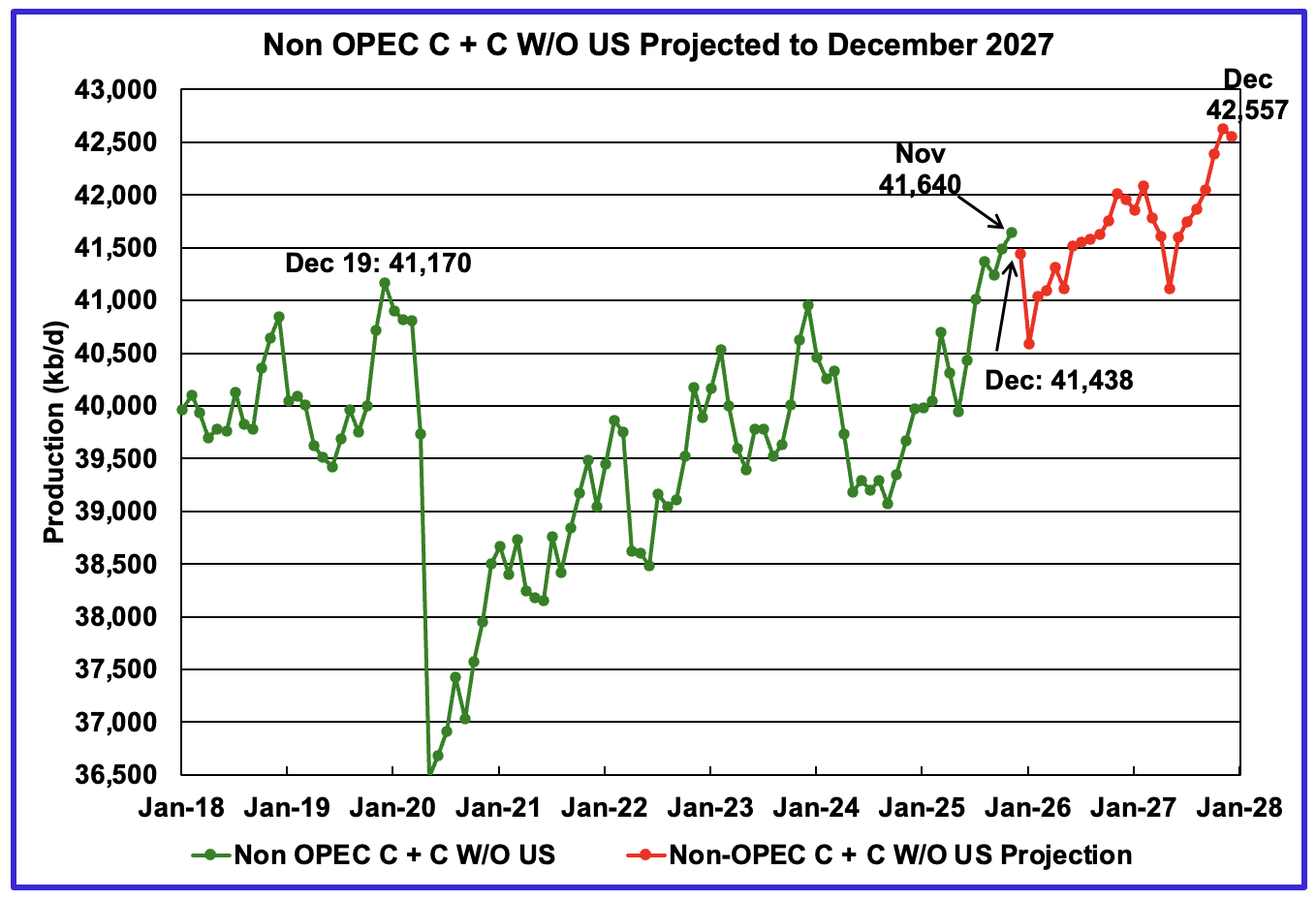

November’s Non-OPEC W/O US oil production increased by 149 kb/d to 41,640 kb/d. December’s production is projected to drop by 202 kb/d to 41,438 kb/d.

From November 2025 to December 2027, production in Non-OPEC countries W/O the U.S. is expected to increase by 917 kb/d to 42,557 kb/d.

Non-OPEC Oil Countries Ranked by Production

Listed above are the World’s 11 largest Non-OPEC producers. The original criteria for inclusion in the table was that all of the countries produced more than 1,000 kb/d.

November’s MoM production increased by 47 kb/d to 46,219 kb/d for these eleven Non-OPEC countries while as a whole the Non-OPEC countries saw a yearly production increase of 2,362 kb/d to 55,428 kb/d. Major yearly gains came from Brazil and the U.S.

In November 2025, these 11 countries produced 83.4% of all Non-OPEC oil.

Non-OPEC Country’s Oil Production Charts

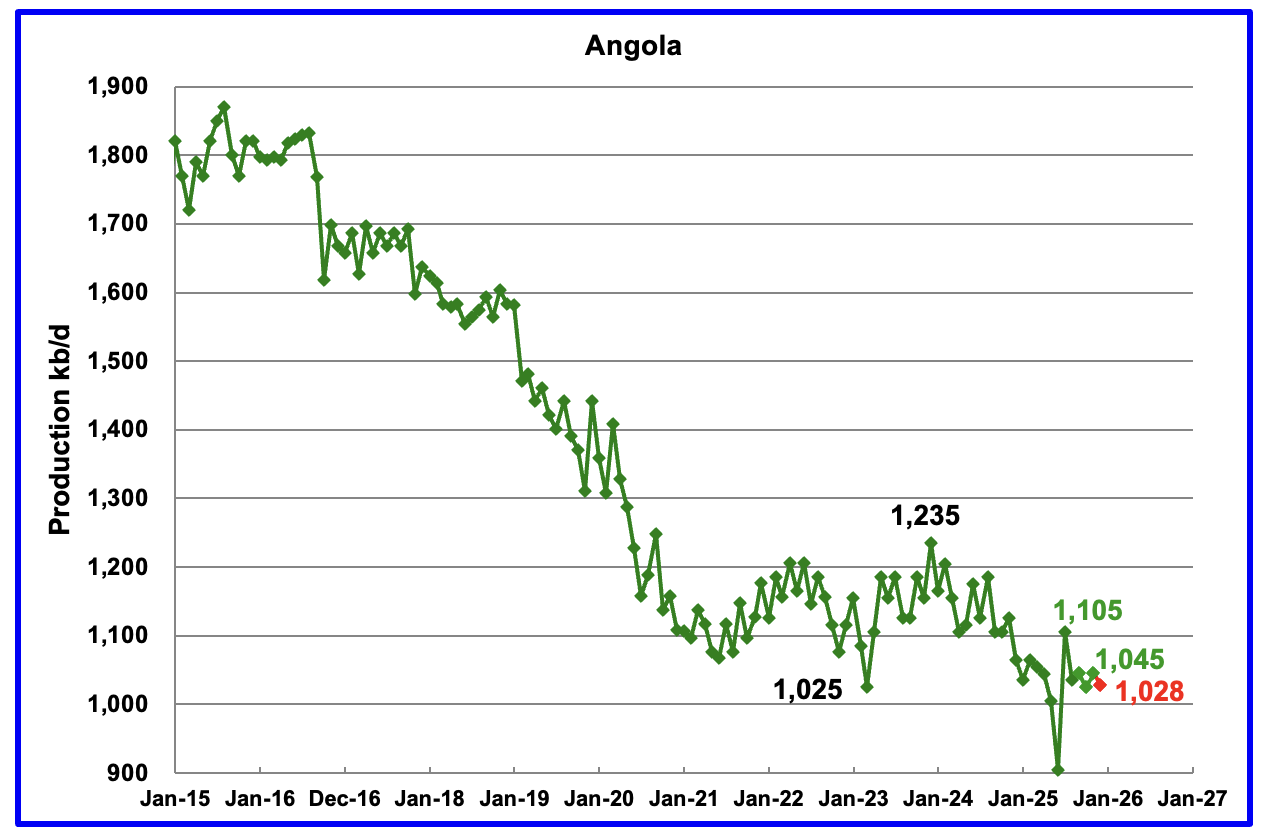

The EIA reported Angola’s November oil production rose by 20 kb/d to 1,045 kb/d.

According to Angola’s National Agency for Petroleum, December’s production was 1,028 kb/d, red marker.

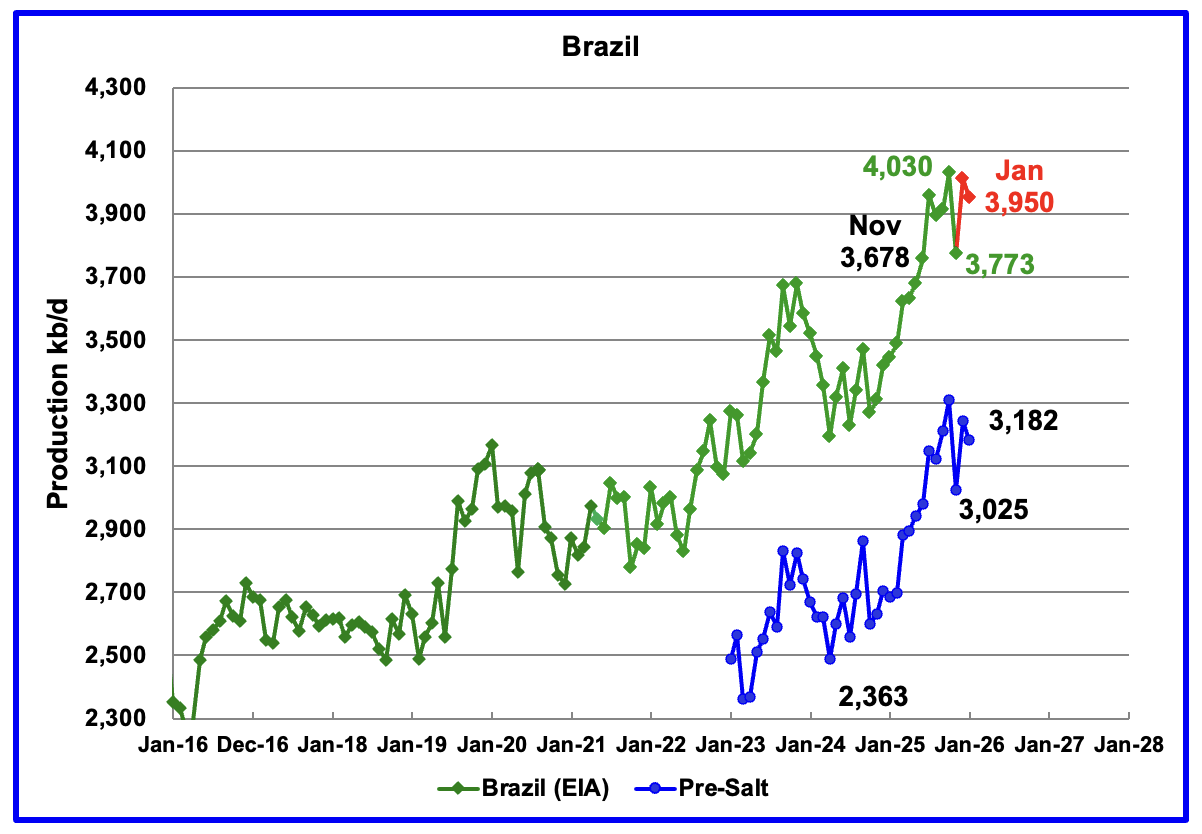

The EIA reported that Brazil’s November production dropped by 257 kb/d to 3,773 kb/d. According to this article, the November Production drop was due to platform outages at offshore fields.

Brazil’s National Petroleum Association (BNPA) reported that production rose in December and dropped to 3,950 kb/d in January. December production rebounded to 4,012 kb/d. Pre-Salt production was a major contributor to December’s rebound. Pre-salt production decreased by 61 kb/d in January to 3,182 kb/d.

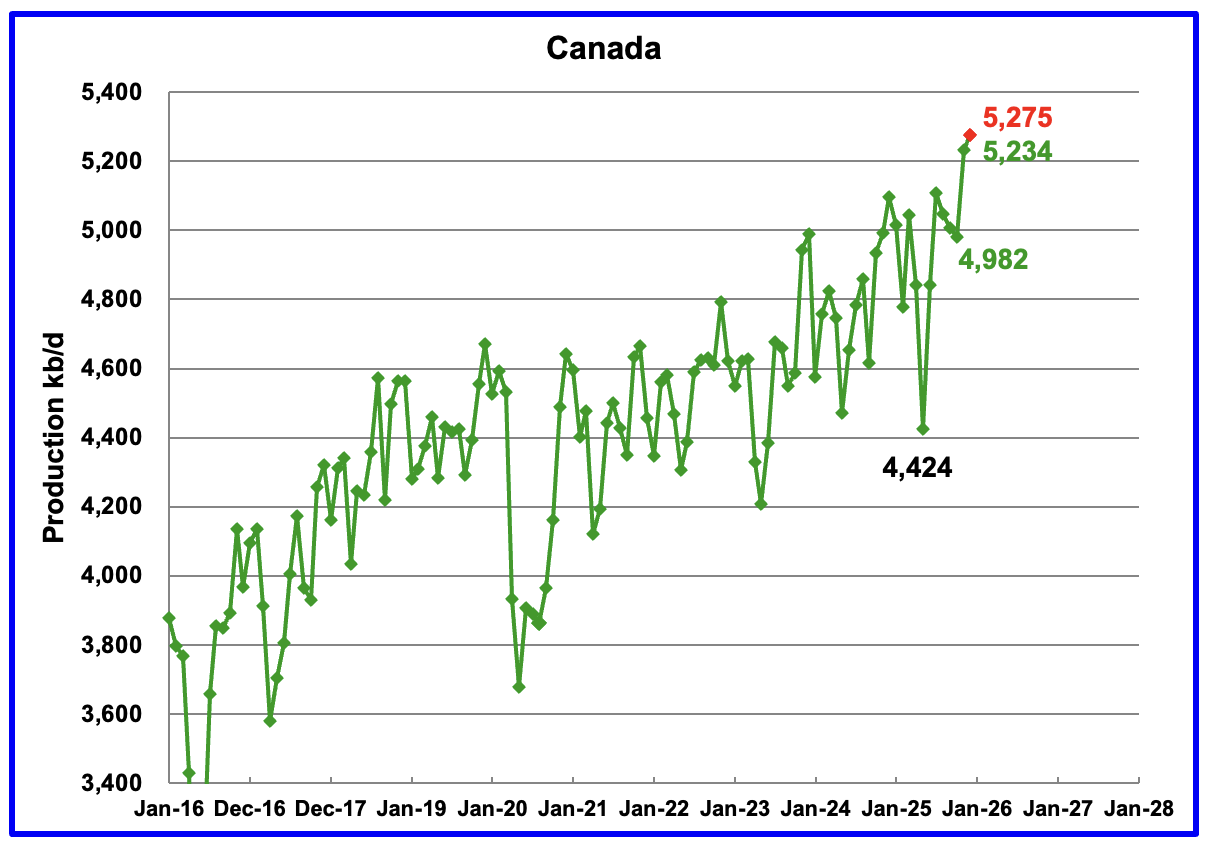

Canada’s oil production increased by 252 kb/d in November to 5,234 kb/d.

A projection has been made for December production based on preliminary production provided by the Canada Energy Regulator (CER). December’s projected production rose to 5,275 kb/d, a new record high, red marker. The CER estimate contains some NGLs which have been removed from the projection. On average the EIA reduces the CER’s monthly production by 375 kb/d which was also done for the December estimate.

According to this Article Canada has agreed to “do its part” to help the IEA release of oil reserves.

“Hodgson said Wednesday Canada will support those efforts but didn’t say what form that would take.” In a later release he said he would ask oil companies to release oil from their reserves.

The EIA reported China’s November oil output rose by 70 kb/d to 4,310 kb/d.

The China National Bureau of Statistics reported December production dropped by 120kb/d to 4,190 kb/d. No report is available for January due to Chinese New Year.

On a YoY basis, China’s November production increased by 113 kb/d to 4,310 kb/d.

Note the large drop of 310 kb/d from March 2025 to December 2025. That appears to be a record drop over those nine months.

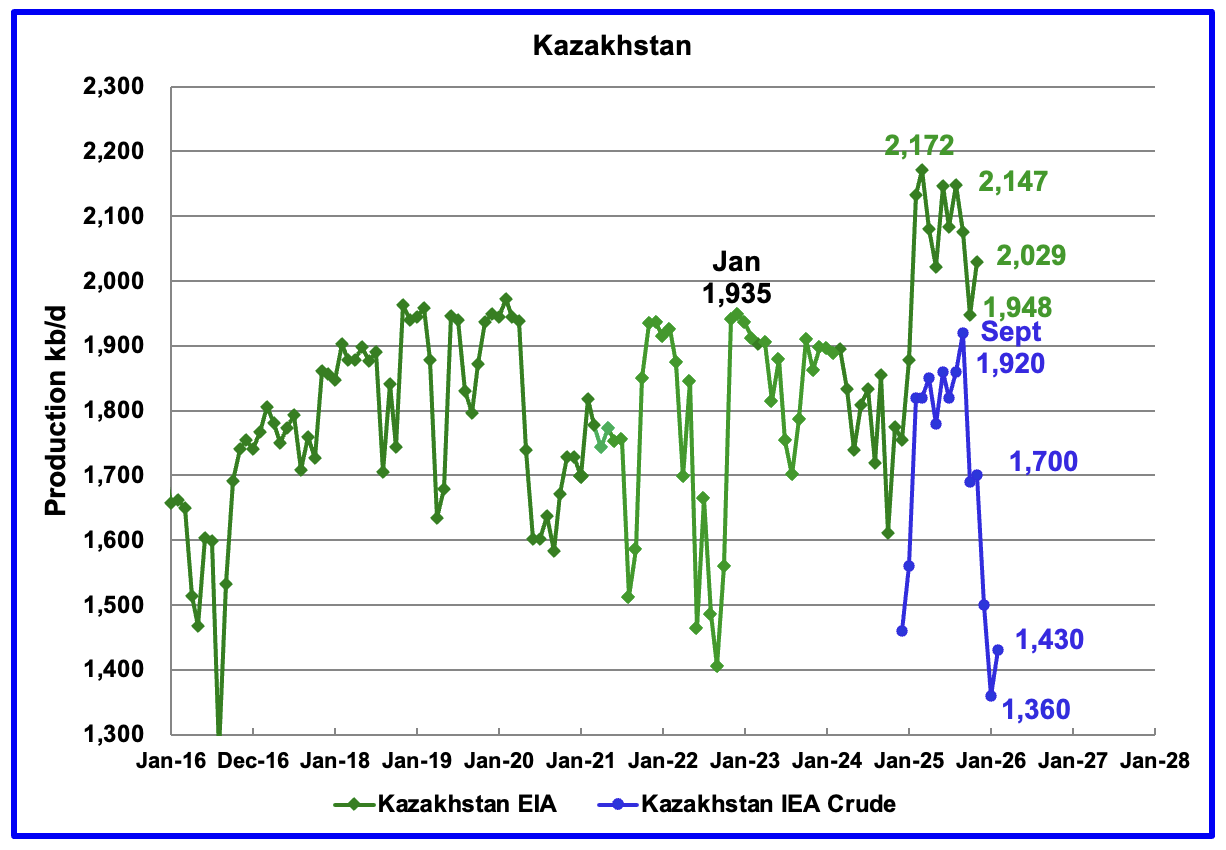

According to the EIA, Kazakhstan’s November oil output increased by 81 kb/d to 2,029 kb/d.

Since Argus no longer reports OPEC + crude production, production data for Kazakhstan will now be taken from the monthly IEA reports. In December 2025 pre-salt crude production was 1,500 kb/d. The March IEA OMR reported January 2026 production was 1,360 kb/d and February rose to 1,430 kb/d.

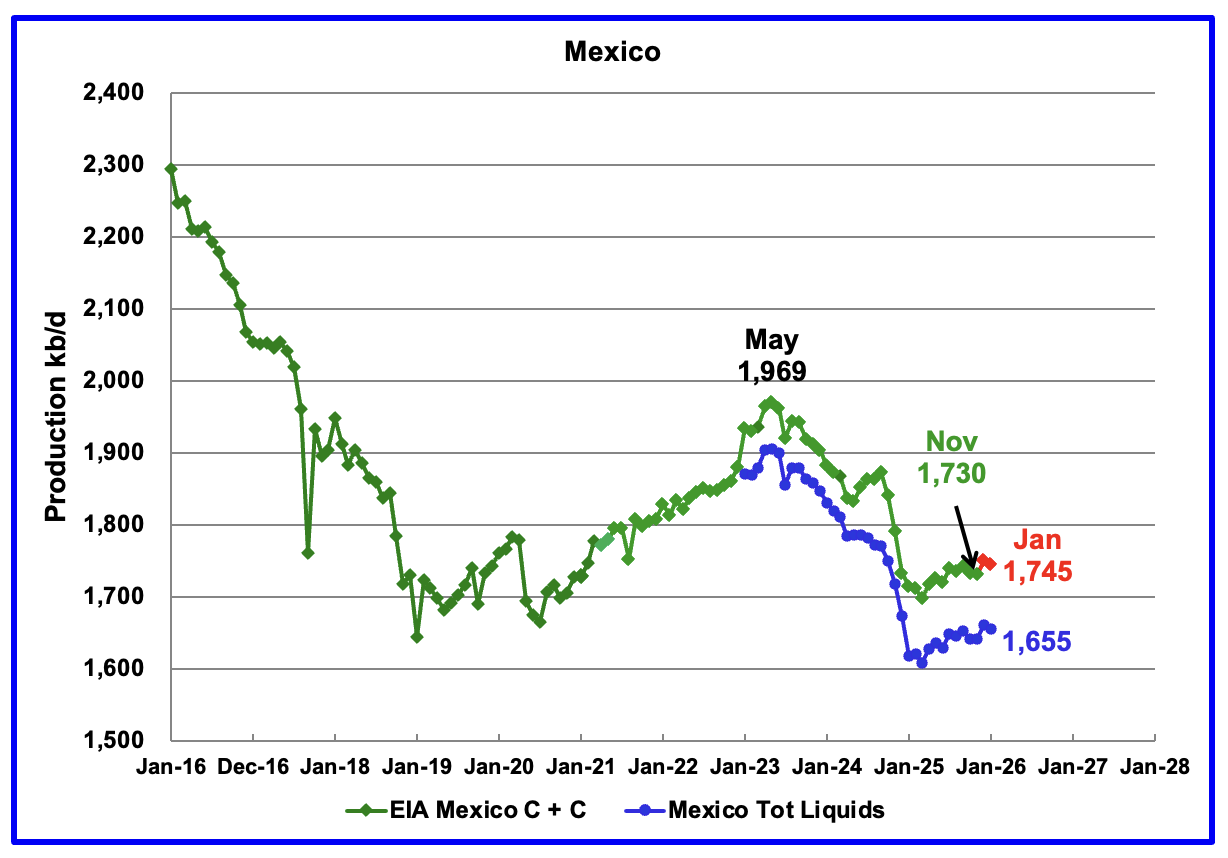

According to the EIA, Mexico’s November output dropped by 1 kb/d to 1,730 kb/d.

In June 2024, Pemex issued a new and modified oil production report for Heavy, Light and Extra Light oil. It is shown in blue in the chart and it appears that Mexico is not reporting condensate production when compared to the EIA report.

In earlier EIA reports, they would add close to 55 kb/d of condensate to the Pemex’s “Total Liquids” report. More recently the EIA has been adding 90 kb/d of condensate to Mexican production. For December and January production, 90 kb/d have been added to the Pemex report. January’s production is estimated to be close to 1,745 kb/d. Note that Mexico’s production, as reported by Pemex for the last seven months has stabilized around 1,650 kb/d.

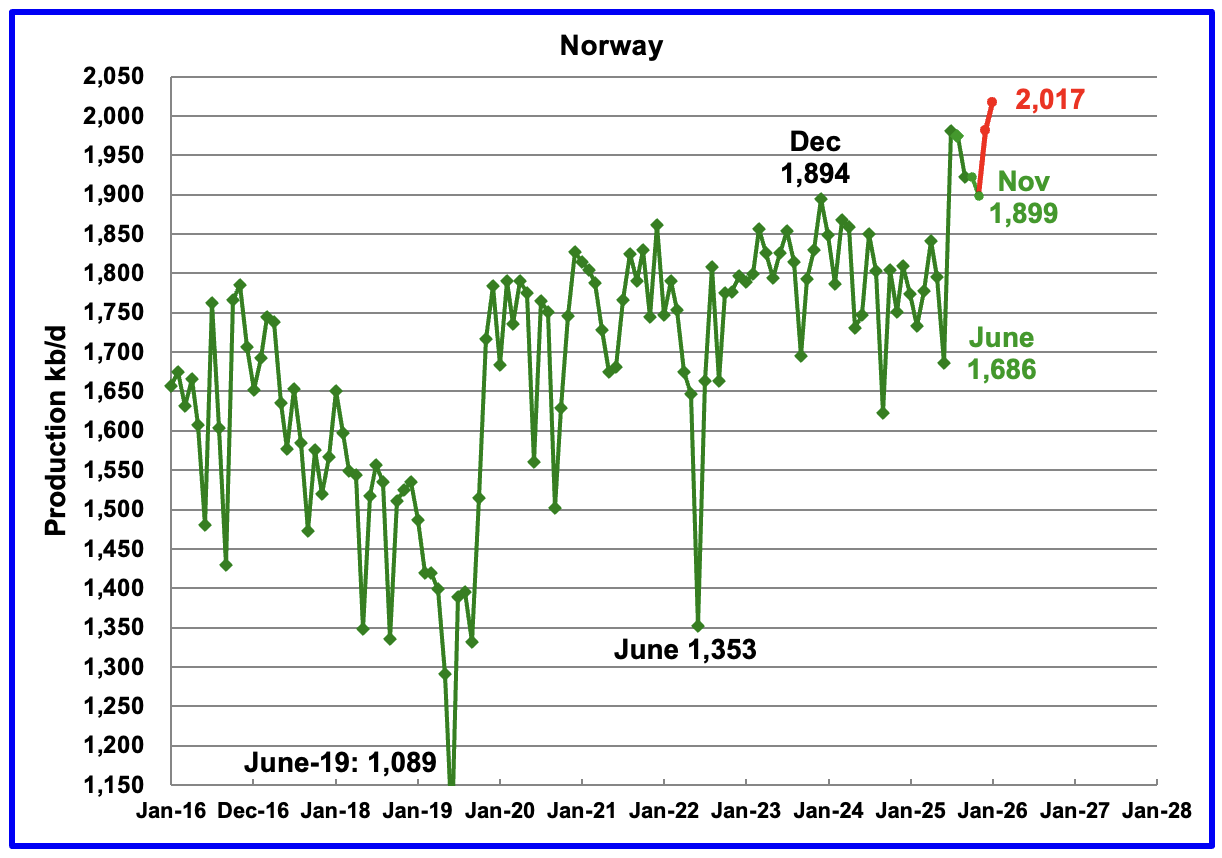

The EIA reported Norway’s November production dropped by 24 kb/d 1,899 kb/d.

Separately, the Norway Petroleum Directorate (NPD) reported that January’s oil production rose to 2,017 kb/d, a new high, red markers.

The Norway Petroleum Directorship also reported that January’s oil production was 6.3 % above forecast.

According to OPEC’s March MOMR: “Norwegian liquids production is forecast to drop by about 40 tb/d to average 2.0 mb/d in 2026. Several projects are scheduled to ramp up through the year, including Balder/Ringhorne, Heidrun, Gina Krog, Maria, and Snohvit.

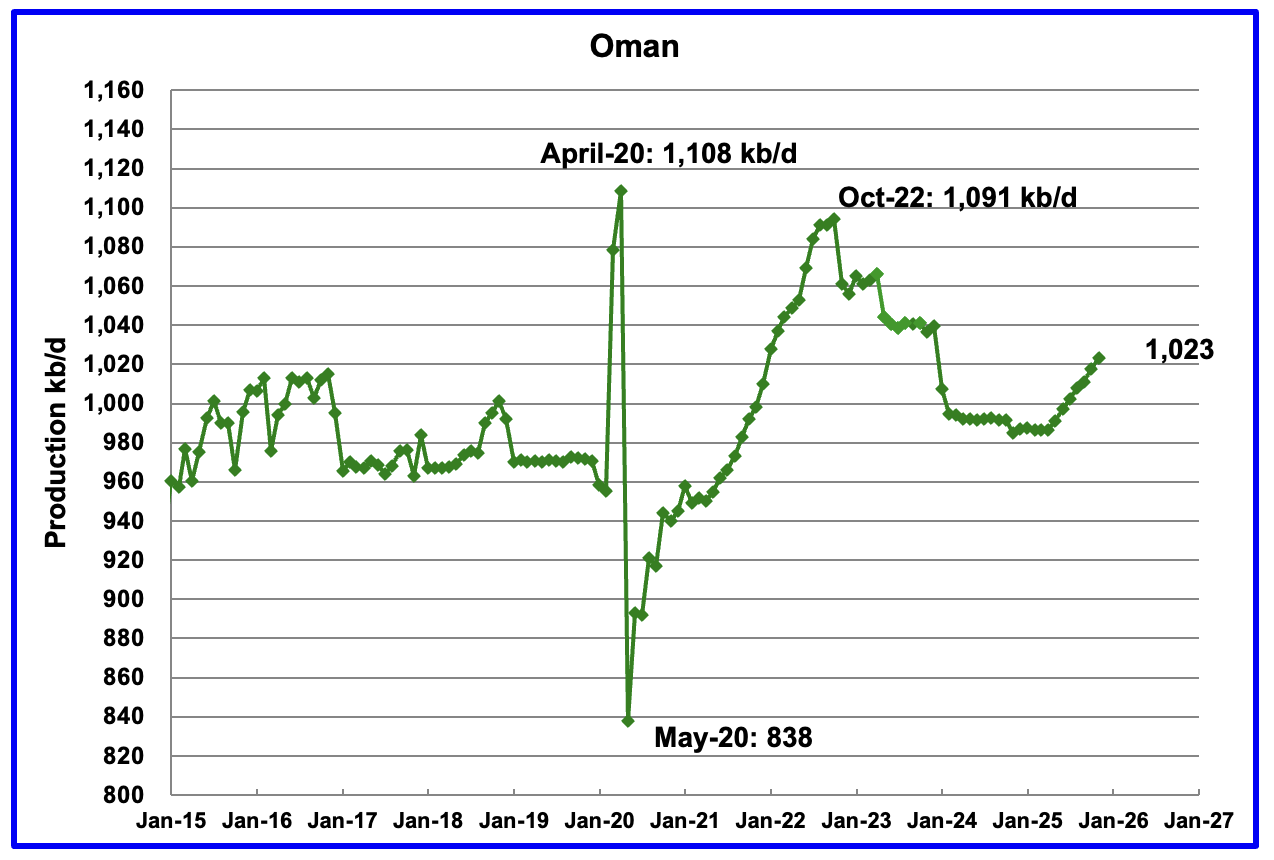

According to the EIA, November’s output rose by 6 kb/d to 1,023 kb/d and appears to have started a budding growth phase. Previous production peaked in October 2022.

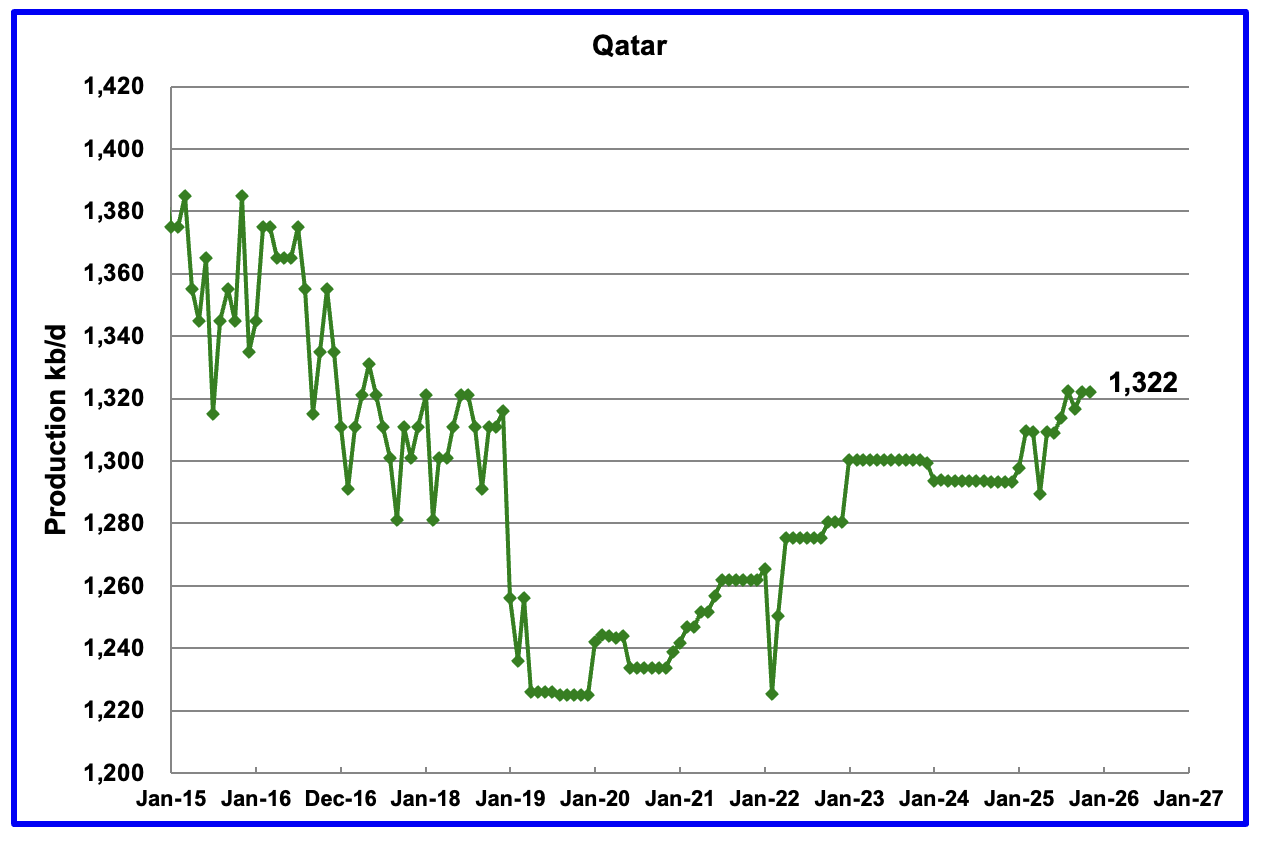

Qatar is now providing the EIA with monthly updated oil production back to January 2025. Qatar’s November output was reported to be 1,322 kb/d, unchanged from October.

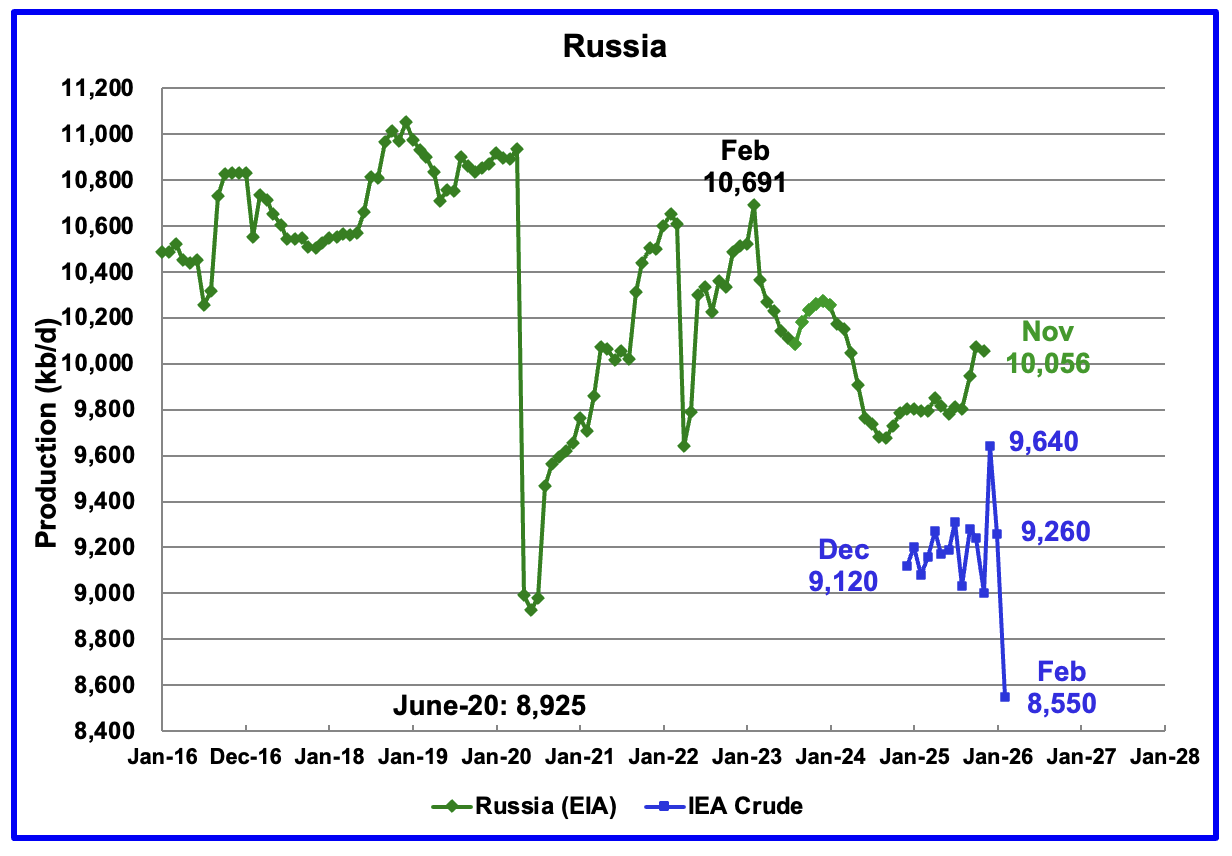

The EIA reported Russia’s November C + C production decreased by 18 kb/d to 10,056 kb/d and was up by 253 kb/d from August 2025.

Up to August 2025 Argus Media used to report OPEC + crude production. That monthly report has now been discontinued. The above chart now also shows Russian production as reported by the IEA. It is difficult to assess the accuracy of the IEA report but over the last few months before publication stopped the IEA’s Russian production had been around 100 kb/d to 150 kb/d higher than Argus’ Media. The best that can be done at this time will be to compare the production trends between the EIA and the IEA. I think that Russian oil production continues to be a major state secret at this time because of the damage being caused by the heavy bombing to its related crude oil processing facilities.

According to the IEA’s February report, December production rose by 640 kb/d to 9,640 kb/d. The March IEA OMR is reporting that Russian crude production dropped to 9,260 kb/d in January and then hit a new February low of 8,550 kb/d. This is the first clear indication that Russian production is being affected by the Russia/Ukraine war. The March OPEC MOMR is reporting Russian February crude production was 9,184 kb/d, a new recent low.

According to this Article, Russia’s ability to store oil is nearing its limit since the majority is on ships and very little is stored on land.

Russian seaborne crude exports fell to 3.4 million barrels per day (bpd) in January from 3.8 million bpd in December, and are currently tracking around 2.8 million bpd in February, according to analytics firm Kpler.

At the same time, the volume of Russian oil held on ships has climbed to a record high above 150 million barrels in recent months, while many tankers have also slowed their speeds – both signs of weaker buying.

The size of Russia’s onshore storage capacity is unclear, as the government does not publish data, but the amount remaining appears limited. Onshore oil inventories stand around 16 million barrels, or about 51% of capacity, based on satellite monitoring of tanks, according to Kpler senior crude analyst Naveen Das.

For Comparison: US production in last post.

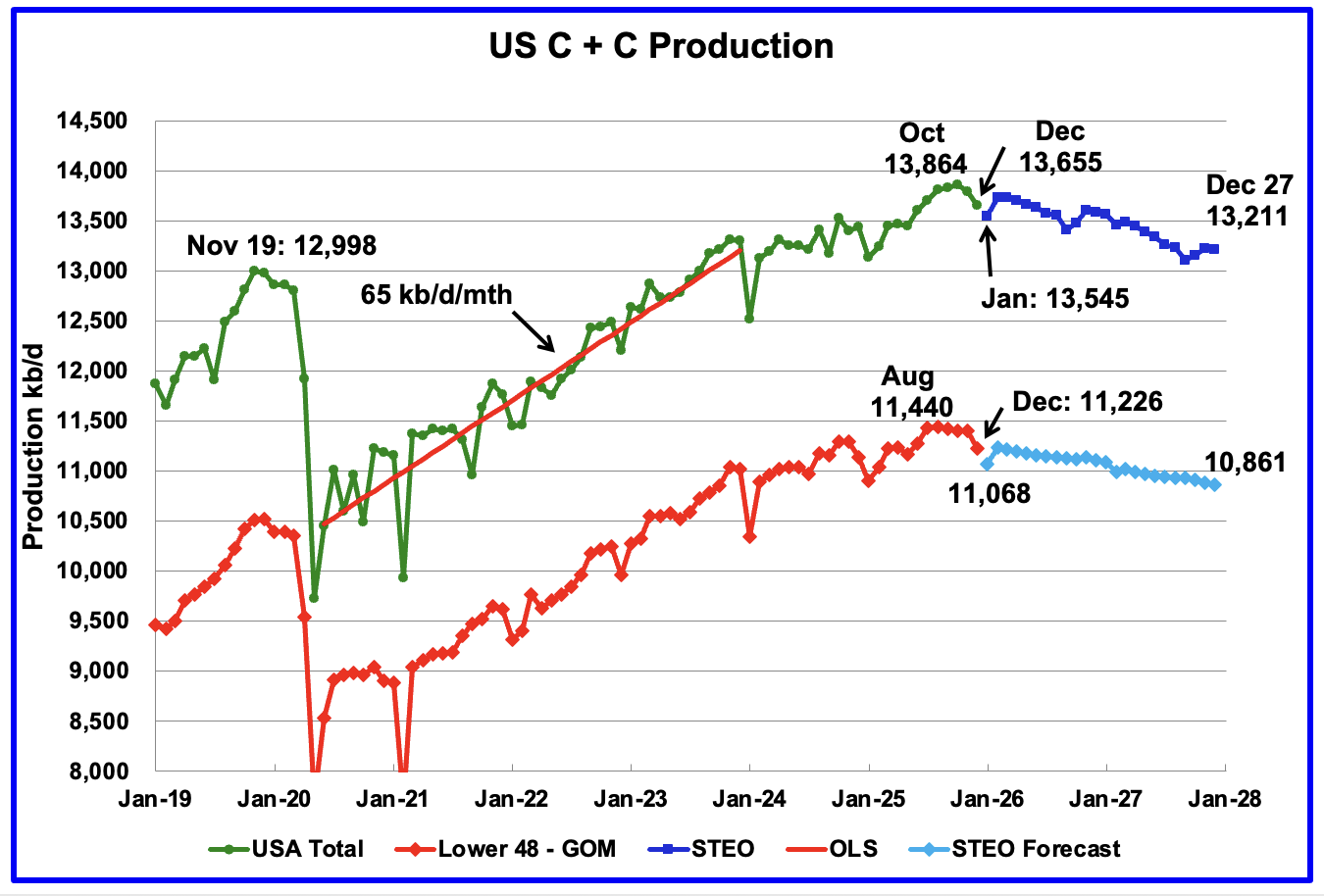

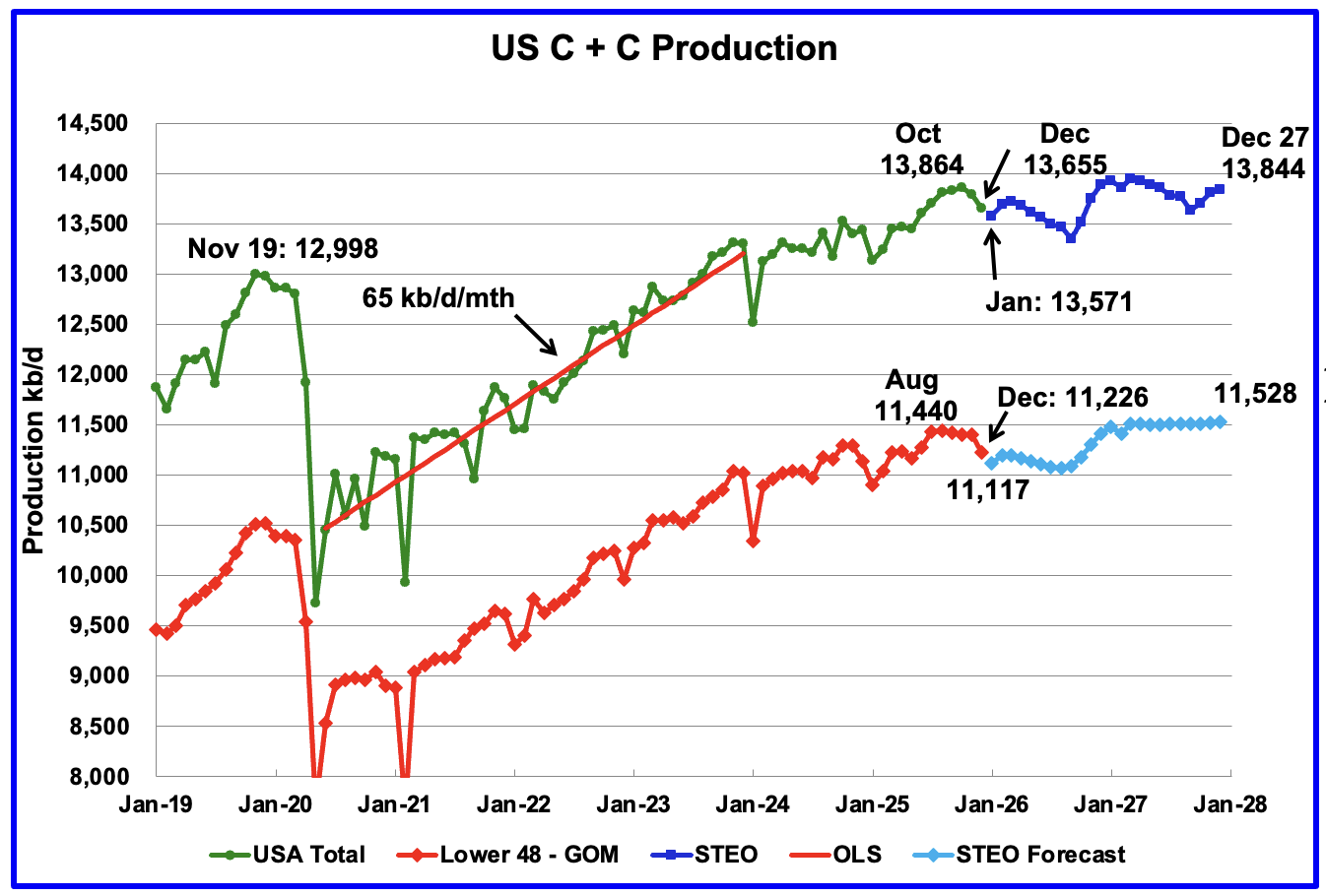

This US production chart up to December 2025 is the same as the one published last week in the US update. However the projected portions of the two production graphs have been updated according to the March 2026 STEO.

This is a case where a picture is worth a 1,000 words. Last week’s chart is posted above for comparison. US total production for December 2027 is expected to be 13,844 kb/d which is an upward revision of 633 kb/d from least week’s US report.

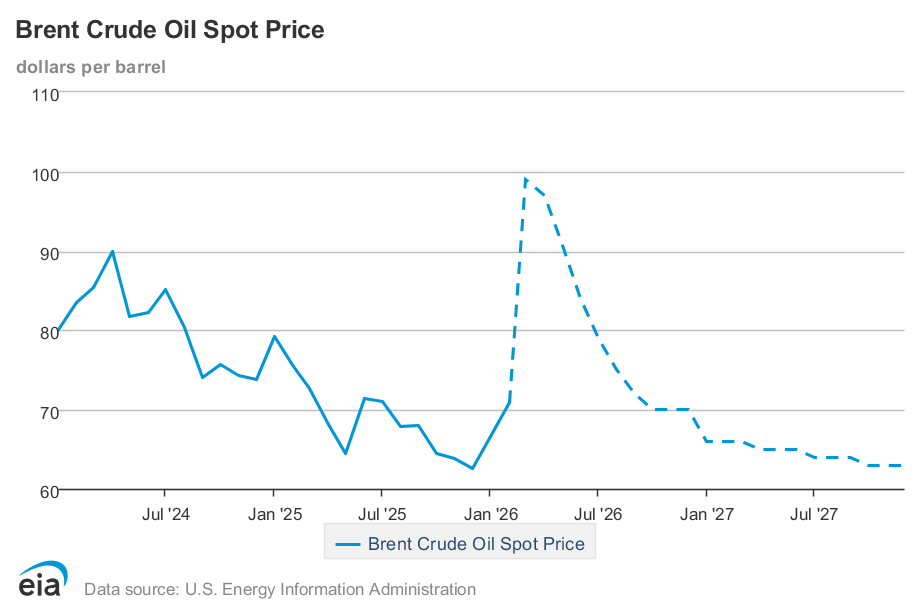

What happened/changed between the February and March STEO’s? Was a new field discovered? Were more oil rigs activated in the STEO model in late 2026? Were five mile wells developed and made operational in late 2026. Was there a significant price increase in WTI. See Brent price chart below which was posted by Dennis in the comments in the previous post. After the March 2026 price spike, the price returned to $62/b in December 2027, same as December 2025.

We will need to track the upcoming weekly rig counts and we will keep a close eye on them. The oil rig count started to increase two weeks ago.

U.S. January projected production is expected to drop to 13,571 kb/d. January’s drop to 13,545 kb/d reflects the severe storms that hit the mid US and the Permian basin.

216 responses to “November World Oil Production Slides”

Here is my lay person’s retrospective on “peak oil.” It was finished before the current war, so I’m sure it seems a little quaint already. I’ve tried simply to be even-handed and detached in my approach to the failed predictions of PO. Thank you for the permission for charts, POB and Mr. Mushalik.

https://3quarksdaily.com/3quarksdaily/2026/03/world-oil-production-has-surpassed-another-peak-alls-good-no.html

Thanks Mike, very nice work.

Here is a shock model I did for World C+C in November 2025, my best guess at that point in time. Future extraction rates and discoveries are not known, so this is likely (or certain) to be incorrect. The scenario has a plateau in World C+C output between 85.1 and 85.8 Mb/d from 2026 to 2032.

See chart linked below.

shock2511c

Ovi, I take it that the huge dip in oil production prediction is March 2026. And it shows oil production rebounded in April. That means the war will be over later this month.

I really don’t think so. Perhaps the EIA felt that if they did not predict that oil production would increase, Trump would fire them.

Also, the decline they show for March is approximately 9%, then declining in percent each month after that. That seems overly optimistic. Is the EIA getting political with their predictions?

Ron

Yes that big dip is March. I don’t think the rise in April, May or June says anything about the war. I think it is related to Saudi Arabia’s ability to shift its oil exports to their Red Sea port, which as best I recall can export around 5,000 kb/d. Not sure how much is used now and how long it will take to redirect the flows.

I would agree that the production estimates after July are questionable.

Hi there Ovi, thank you for the thorough work as usual. There isn’t a more useful source on petroleum production.

Regarding the war on Iran, you project a decline of 4 Mb/d this month, and an immediate rebound. Apparently you are only counting with Iran’s production being affected, and for a short time. We know now Saudi, Iraq, Kuwait and the UAE are also shutting in production. And after such destruction, Iran is unlikely to return to 4 Mb/d any time soon. In contrast, sanctions on Russia have been lifted, it will be able to move all that floating petroleum.

Not criticising, just would like to understand the rationale behind the projection. Best.

Luis, these are not Ovi’s predictions. That crime belongs to the EIA. Ovi just posts what the EIA predicts. And your guess is probably as good as his as to the EIA’s rationale in making these predictions.

Luis

Thanks, much appreciated.

Ron is partially correct in saying that these are not my predictions. The EIA predictions are for World Crude, the Blue graph. Dennis and I have developed a methodology to convert those crude numbers into C + C.

This is just wishcasting by people who are about to understand that material reality still exists.

Possible Answer to rising US oil Production in 2027

In the comments under the US Chart, I raise the question of what causes US production to begin to rise in late 2026 into 2027.

The headline in the attached article gives a possible answer. More gas pipelines out of the Permian.

US natgas prices at Waha Hub in Texas remain negative for record 25th day

“Longer-term, energy firms will likely boost Permian output when more gas pipes enter service as soaring oil prices from the Iran war encourage oil and associated gas production, and as gas demand rises to feed fast-growing U.S. liquefied natural gas (LNG) exports and to produce electricity for power-hungry data centers running artificial intelligence (AI) technologies.

Analysts have long said negative prices, which force some energy firms to pay others to take gas associated with their oil production, were a sure sign that the Permian region, which spans West Texas and eastern New Mexico, needs more gas pipes.

More pipes are on the way this year, but not soon enough to handle all the gas currently coming out of the ground.”

https://boereport.com/2026/03/12/us-natgas-prices-at-waha-hub-in-texas-remain-negative-for-record-25th-day/

Ovi.

In the STEO report they say:

“U.S. crude oil production

Higher crude oil prices lead to more U.S. crude oil production in our forecast. We expect crude oil production in the United States will average 13.6 million barrels per day (b/d) in 2026 and 13.8 million b/d in 2027. Our 2027 forecast is an upward revision of about 0.5 million b/d (4%) from last month’s Short-Term Energy Outlook (STEO). The West Texas Intermediate (WTI) crude oil price in our forecast is substantially higher than last month, averaging $74/b in 2026 and $61/b in 2027, compared with $53/b and $49/b, respectively, in the February STEO. ”

So basically their higher price forecast results in higher production for this month’s report compared to last month.

See page linked below

https://www.eia.gov/outlooks/steo/report/petro_prod.php

Dennis

I saw that comment but I could not square it with the price of WTI that they reported in the STEO tab 2. December 2025 $57.97/b. December 2027 $59.00/b. Negligible change. Seems like they are banking on the average price.

I recognized your quote from the STEO document. The link you attached did not get me the quote I was looking for but it did provide this gem that corresponds to the article I attached.

From your link:

“The higher prices support increased drilling activity across most basins, and expanded pipeline capacity in the Permian region allows more associated natural gas to be brought to market, further supporting oil-directed operations. We increased our forecast for crude oil production in the Permian region by 6% in 2027 as new pipeline capacity and price incentives support growth.”

Maybe the increase in gas pipeline exits may be the more critical factor.

I also asked Mike for his thoughts on the article and the STEO forecast.

He said: “For the Permian Basin to grow 633K BOPD by 2027, that is to say that the Permian Basin will actually have to increase tight oil production by 3.1 MM BOPD by 2027. That includes the annualized decline rate of existing Permian production that must be replaced, before growth of 633K BOPD can occur. ”

https://www.oilystuff.com/groups

Ovi,

I doubt the EIA STEO forecast is correct and agree with Mike that it is doubtful that the Permian will see a 600 kb/d increase, certainly not with the oil prices that have been forecast in the most recent STEO.

I agree more gas pipelines and higher gas prices at WAHA will help a bit, along with higher oil prices to increase profits in the Permian. The big question is whether producers believe the higher prices will be sustained. If we see a significant increase in horizontal oil rig counts in the Permian basin, then perhaps output increases a bit (maybe 100 kbo/d for Permian tight oil output by Dec 2026.) We will see. No increase in Permian horizontal rig count this week, producers may be taking a wait and see approach.

Thanks Ovi. I googled Saudi exports via the Red Sea and this is what I found:

Saudi Red Sea oil exports to hit record high in March, shipping data shows

Yanbu loadings rise to 2.2 million bpd, could reach 4 million bpd

Saudi used to export 6 million bpd via Hormuz

Production cuts spread across Middle East

LONDON/OSLO, March 10 (Reuters) – Saudi Arabia’s oil shipments via the Red Sea are on course to hit record highs in March although they are still far below the levels needed to compensate for the drop in flows from the Strait of Hormuz, shipping data showed on Tuesday.

The kingdom relies on the Red Sea port of Yanbu to help it boost exports to avert steep production cuts as its neighbours Iraq, Kuwait and the United Arab Emirates have already reduced output amid the U.S.-Israeli war with Iran.

Ron

Thanks.

So they are exporting 2.2 million barrels per day today and it sounds like exports will be rising.

The first chart above shows a production rise of 4 Mb/d by June.

Another Pipeline that Avoids the Strait

Wondering whether Iran might attack a Saudi pumping station.

https://www.youtube.com/watch?v=AjRdQ9Hudt8

Given the biggest oil shock of our lifetimes, do you think you could do a post that focuses on that? If not maybe just shut down the website at this point. Thanks!

A common argument against renewables is what is referred to by the German word Dunkelflaute — a prolonged period when the sun doesn’t shine and the wind doesn’t blow. Something similar happens to oil from time to time. The causes tend to be political instead of meteorlogical.

Maybe you can do the work got2surf.

Dennis, Ovi and Ron do this for free.

Not pushing a biased solar panel agenda because got2surf gets paid for that.

got2surf,

Feel free to write the post, send it to [email protected] and if it is worth publishing, it will be published. If you don’t like the site, don’t visit.

Here you go got2surf :

https://geoenergymath.com/2026/03/15/claude-code-oil-shock-model/

This took me a minute to create a Claude Code prompt, and then it brewed on a solution for 2 minutes.

I ran the resultant Python program from a terminal console and it created 3 nice plots that look reasonable (should check tho).

Give it a try.

Here’s a repo for the simulation software:

https://github.com/pukpr/OilShockModel

Two versions: One created by Copilot and one by Claude

https://makisw.substack.com/p/breaking-news-grok-admits-it-had?utm_source=post-email-title&publication_id=1385328&post_id=190801490&utm_campaign=email-post-title&isFreemail=true&r=1igaa&triedRedirect=true&utm_medium=email

AI “Hallicinates” and damages thousands of Cancer patients

FYI As of oil price today.

As of today, the price of Brent crude oil is $99.19 per barrel and the price of WTI crude oil is $95.49 per barrel.

As of 6 PM Eastern US time Brent futures at $104/b and WTI futures at $99/b.

Futures curve falls to less than $70/b by March 2031 and falls to less than $80/b by Feb 2027 (as of 6 PM eastern time US on March 13, 2026.)

“Iran is considering allowing a limited number of oil tankers to pass through the Strait of Hormuz, provided that the oil cargo is traded in Chinese yuan”

Trading in a currency doesn’t mean much. The oil importer uses dollars (or whatever) to buy yuan, uses it to buy oil, and the oil exporter sells the yuan for dollars (or whatever they want). The seller ends up with the currency they normally want, held in whatever bank they want. A little more bother and cost for the currency conversion. Not a big deal.

@Nick G

Many countries have swap agreements with China. So, allowing only tankers traded in Chinese Yuan is a direct thread to the petrodollar. Actually, a large number of decisions/actions taken/started by the current POTUS are leading to a decrease of the dollar as worldwide exchange currency. We see this accelerating quickly.

Meanwhile China is preparing the future with some sort of gold backed currency or similar. Remember which one it was until the early 1970s…

At 7 PM Eastern time, Trump announced a massive bombing of Kharg Island, although the oil infrastructure was not hit.

He declared that if Hormuz was not promptly ‘opened’, the next step would be complete destruction of the facilities.

I suppose we ‘all’ have been following recent events closely and may have varying perspectives on what is unfolding.

I strongly feel that we are on the cusp of the unfathomable as …

1. Iran will absolutely NOT acquiesce to Trump’s demands (even though selective passages will continue)

2. Should Iran’s oil infrastructure be damaged, I GUARANTEE that a large percentage – as in approaching 100% – of the region’s hydrocarbon producing/refining/transporting capabilities will come to an abrupt halt.

For a long, long time.

keerist

Coffee. Surely USA will not bomb the oil and gas infrastructure on Kharg Island. Huge economic AND environmental issues.

Yes.

This president is very well known to bluff, exaggerate and not follow through – it would be foolish of the Iranians to believe him. Even if they did, it’s very hard to imagine that Iran would acquiesce. And, very large damage to Iranian oil infrastructure will almost certainly cause the Iranians to do as much damage to their neighbors.

This president is astonishingly incompetent. Every time we think we’ve seen the worst of his incompetence, he tops himself.

The world is full of economists and military strategists who know that the Strait of Hormuz is important. I was discussing it 2-3 weeks ago on POB, just before this war started. And yet, somehow this president, his sycophant loyalist staff and the military that he and his secdef have molded didn’t know it.

Wow.

The US has confirmed that 2500 marines are in transit (by sea) from the far east to the middle east. The clear threat is that if Iran does not capitulate, the US will perform a sea born invasion of Tharg Island, and hold 90% of Iran’s oil exports to ransom, Venezuela style, presumably until the Iranian regime agrees to Trump’s commands, which I fully expect will involve very large oil redevelopment and repair contracts for US corporations at very favourable rates.

It seems clear to me that economic control of, and profit from the Iranian oil reserves was and is from day one the only US war aim of this special military operation.

With my political /theocratic hat on, I predict that any attempt to seize control of the island will

1. Cost a lot of US military lives

2. Face continuous drone and missile attacks from Iran

3. trigger Iran to attack ALL oil production/refinery or transport infrastructure within the range of their remaining missiles and drones

4. trigger global depression within weeks

and potentially

5. trigger collapse of the global financial system.

From this point on we are past economic peak oil as I see no way of re-instating the lost transit of oil out of the gulf region without major conflict and damage to the infrastructure. We are at risk of a major step down towards the post oil age of the human species.

Ralph,

Re ‘storming’ Kharg …

Military analysts would ask on what transports would the 2,500 jarheads embark/invade?

How fast do said transports travel?

Waterborne distance to be traversed?

As China/Russian/possibly Iranian satellites would be tracking every movement by this proposed expedition, how is the element of surprise to be effectuated?

Supplies of water/food/ammo to be delivered how to any surviving, landed Marines?

No, Ralph, your conclusions are, tragically, spot on in regards to likely directions in which this tragedy may continue to devolve.

A step-downwards of the escalation ladder goes nukes<desalination plants<power-electric plants<hydrocarbon infrastructure.

We are demonstrably on the verge of widespread destruction of oil/gas facilities which – as horrific as these ripple effects will be – are only a prelude to further degradation of the human condition … globally.

And yet, here we are.

Since the attack was completely unprovoked and Trump’s behavior is getting more and more erratic as he panics about the midterms and Epstein, “capitulating” would do Iran no good whatsoever.

You can’t rely on any promise he makes. Remember he ran on publishing the Epstein files, reducing fuel prices and no new wars. Recall how quickly he reneged on the trade deal with the EU.

There’s no point in giving in to Trump at all, because it just encourages him to demand more. He even humiliated the sycophants in his cabinet by making them wear clown shoes. Laughing at all his “jokes” and defending his lies in public just encourages him.

Defy him and he loses interest, as in Greenland and Canada.

Iran’s only sensible choice is to create as much pain for Trump as possible and wait till he decides on another hobby, maybe invading Cuba or something. It’s not a great strategy, but they don’t really have any other choice.

It seems to be working.. Trump is now claiming Iran wants to negotiate, but he doesn’t want to. This is an old trick of his. He once called the Washington Post calling himself “John Miller” and told them Madonna was “rabidly” chasing him, but that he had “zero interest”. He’s feeling the pain.

So I think the blockage of the Strait will last a month or two.

Alim, Iran basically said normality as it was pre-28 February for the strait is not coming back, so here we are. They’re going to be forced to relinquish it, or it stays in this state.

And there’s nothing stopping a few ballistics and drones hitting those fields outright if they have got go mediaeval.

Rig Report for the Week Ending March 13

The rig count drop that started in early April 2025 when 450 rigs were operating dropped this week. Drilling continues at a steady rate of 365 ± 5 rigs per week since August 2025 while WTI settled at $98.71/b today

– US Hz oil rigs dropped by 2 to 369, down 81 since April 2025 when it was 450. It was also up 7 rig from the low of 362 first reached in the week ending August 1. The rig count is down 18% since April 2025.

– New Mexico Permian was rose by 1 to 92. Eddy added 1 rig to 34 while Lea held steady 58.

– Texas dropped 1 to 169. Midland dropped 1 to 20 while Martin was unchanged at 23. There were minor changes in a few of the smaller oil producing counties

– Eagle Ford added 1 to 32.

– NG Hz rigs added 2 to 114.

A Rig

Thanks Ovi,

The key number for me is Permian Basin Horizontal rig count, no change. Brent (which is a better proxy for World oil prices than WTI) closed at about $104/b on Friday March 13.

Dennis

I also find it so amazing that NM has been very close to 92 rigs since October 2025.

Frac Spread Report for the Week Ending March 13

The frac spread count rose by 2 to 172. From one year ago, it is down by 40 spreads and is down by 43 since March 28.

A frac

World Oil Specialist on Supply Cut due to Strait Blockage

World supply cut by 11 Mb/d even after allowing for Saudi re-direct to Red Sea.

https://www.cnbc.com/video/2026/03/10/high-oil-prices-could-force-a-u-s-pivot-in-the-iran-war-says-energy-aspectsa-amrita-sen.html

Ovi,

Saudi can redirect about 5 Mb/d around Hormuz with the east west pipeline to the red sea. UAE can use its pipeline to redirect about 1.5 Mb/d around Hormuz. Combined this is 6.5 Mb/d of C+C, in 2025 the average level of OPEC C+C exports through Hormuz (excluding Iran) was about 13.3 Mb/d, so subtracting the 6.5 Mb/d of pipeline work arounds we have roughly 6.8 Mb/d of reduced exports through Hormuz. The IEA SPR release is about 3.3 Mb/d over 120 days, so the World remains short by 3.5 Mb/d (about 4% less than 2025 average output of 84 Mb/d for World C+C).

Dennis

Not quite sure why the average flow through the Strait in 2025 was so low compared to previous years. According to this chart the average passing through the straight has been closer to 14.2 Mb/d.

So using your figures and Q1-25, the world remains short by 4.4 Mb/d. That extra 0.9 Mb/d is significant increase when supplies are tight.

Trump is certainly changing his tune from “We won in the first Hour” to demanding help from Nato and China to open the strait. It’s becoming clearer every day T did not anticipate what would happen. His top General did.

https://finance.yahoo.com/news/trump-demands-help-other-countries-001639208.html

A Str

Hi Ovi,

See link below from IEA on C+C through Hormuz

https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

All C+C is 15 Mb/d with 1.7 Mb/d from Iran, net of 13 .3 from nations that are not Iran. IEA says 3.5 to 5.5 Mb/d can avoid Hormuz using pipelines, so less than my 6.5 Mb/d estimate, if we assume 5.5 Mb/d we would have 7.8 Mb/d of oil taken off market, then subtract 3.3 Mb/d from SPR release (400 Mb over 120 days) and the World would be short by 4.4 Mb/d. Note also that output in 2025 may have been 2 Mb/d above demand fro crude, which would suggest only a 2.4 Mb/d deficit. Higher oil prices may hasten the transition to electric transport which may reduce demand in 2026 compared to 2025.

Dennis

Sounds like we agree. “The World would be short by 4.4 Mb/d”

“

Ovi,

I have read that Saudis can transport 5 Mb/d to Red Sea and UAE can move 1.5 Mb/d by pipeline to the sea south of Hormuz, if that is correct, the shortage is reduced to 3.4 Mb/d. If there was a surplus of output of 2 Mb/d in 2025 above demand for C+C the shortage is reduced to 1.4 Mb/d (if demand remains at 2025 level). There might also be increased output from Canada, Guyana, Brazil, and Argentina in response to higher crude oil prices and perhaps lower demand than 2025 also due to higher oil prices.

We will see, but the predictions of $150 to $200/b may not be accurate. Futures market expects $75/b for Brent by July 2027 (and under $80/b by Jan 2027). See link below and click on futures next to live price.

https://oilprice.com/futures/brent/

https://oilprice.com/Energy/Crude-Oil/Futures-Market-Misreads-the-Hormuz-Oil-Shock.html

Physical crude prices are much higher than futures market. Many analysts see crude oil reaching $150 to $200/bo.

See

https://oilprice.com/Latest-Energy-News/World-News/Banks-Hike-Oil-Price-Forecasts-and-Some-See-150-Crude.html

To keep this in perspective, nobody is going to bomb Kharg Island. It would create the mother of all environmental messes, bring about the wrath of the world, and serve no pragmatic purpose. That said, I do believe that the U.S. has to abide by the Pottery Barn rule. That means occupying Kharg Island, and, alas, probably also occupying Iran. I’m talking about a full-scale invasion.

We were assured by Israel and our U.S. experts that Iran was insistent upon producing a nuclear bomb, and also the ICBM’s to send nuclear devices to both Israel and the U.S. They kept chanting Death to Israel and Death to America. Well, somebody had to stop that. For decades, U.S. presidents have been saying, We can’t allow Iran to develop nuclear. No one did a thing. Until now. Stopping these tyrannical idiots is a massive service to all humanity.

The Iranian shoreline with the Persian Gulf is 600 miles. The Strait of Hormuz is a hundred miles long. There is another 500 miles of shoreline with the Gulf of Oman. That’s 1,100 miles of Iranian shoreline along the world’s most important waterway. If left to its own devices, lashing out, Iran could cause this to be a killing zone for years, and upset the world economy. So whether we like it or not, the U.S. is going to have to occupy and police Kharg Island and displace the Islamic Revolutionary Guard. Knowing how Mr. Trump operates, I imagine we’ll charge a toll for keeping the place operational.

Until the above is implemented, oil could very easily reach $200/barrel. Not because it’s that scarce but because it trades on a goofy inelastic commodities scale, and even a five-million bopd supply shortage would create chaos. If this happens, a global recession will follow.

Even hiding behind your cute little aliases, some of you lefty guys are showing your ass. I don’t have the faintest idea where some of you guys are from but you obviously hate America, and it has messed up your moral code. It’s up to Mr. Coyne whether or not you get to spew your hatred, but you’re going to have to live with the knowledge that you’re not worth much as a man.

Gerry, the US doesn’t have sufficient forces or popular support to occupy a nation of 90 million people.

Cheney and the neocons had 9/11 to build on. Donald doesn’t have a similar real life event to work from. His gas lighting doesn’t work against real adversaries.

Gerry,

It was this kind of behavior that created a nuclear threat in Iran: the US invaded Iran in 1953, destroyed a new, promising democracy and installed a dictator (the title was Shah). That bloody dictatorship lasted until 1979 when a newly radicalized country rejected that dictator and turned, as newly radicalized people often do, to a new bloody dictatorship.

Now we’ve probably lost Iran for another long period, probably at least 50 years, and if this president were to follow the insane advice that we find in your comment, we would probably have another Vietnam, Iraq and Afghanistan all rolled into one.

There is one rule for how to unite a country under its leadership, no matter how bad the leadership is: have an external enemy. Bush had an apparent external enemy after 911, and it allowed him to invade Afghanistan and Iraq. This president doesn’t have that.

On the other hand, the Iranian leadership has, in its lexicon, the mother of all external enemies, the Great Satan itself, making itself as evil as possible. What will happen? It will unite Iranians against the US.

And, what’s the lesson in this war? We’re not attacking countries that have nuclear weapons, like N. Korea. We’re not attacking Pakistan or India. We got LIbya to agree not to pursue nuclear weapons, and then…we attacked it. The US and Russia got Ukraine to give up nuclear weapons, and Russia promptly attacked it (and the US under this president hasn’t been helping Ukraine lately and even worse we just released Russia from oil sanctions). We’ve attacked Iran twice, and both of its next door neighbors Iraq and Afgahanistan. We negotiated an agreement with Iran to limit nuclear development, and then this president killed the treaty in his first term. Obviously, the lesson that this teaches is that the US is dangerous and can’t be trusted, and the solution for self-defense is to obtain nuclear weapons quickly and secretly.

Invading was a bad idea. It happened, in part, because process matters. This president doesn’t believe that – he thinks he can improvise his way through – but democratic process matters because it produces better decisions.

Ask yourself – if agreeing with your president means that you love America, and disagreeing means that you don’t, then…did you agree with everything Biden did, because he was your president?? When you disagreed, were you spewing hatred? Were you less of a man?

It’s not about being left or right, it’s about being in touch with reality.

Nick,

Agree it’s not left or right, but thinking differently, which may in fact be more realistically. Who else does this kind of math? The state of geology, geophysics, Earth sciences, even climate science is stuck in the stone age and the media doesn’t realize this.

Gerry,

We have bombed Kharg Island already.

See link below (hopefully not too left wing for you)

https://www.foxnews.com/politics/trump-says-u-s-obliterated-targets-strike-key-iranian-oil-hub

Old men shouldn’t decide what causes young men should die for.

We can let the Israeli’s invade Iran.

The people claiming that Iran was intent on pursuing a nuclear weapon are Trump’s real estate cronies, they are far from experts.

The Israeli’s should not be deciding US foreign policy in my view.

Just read through all comments. Seems you think any criticism of Trump should be considered hatred of America.

Trump makes very bad decisions and he should be called on it. Most Americans do not support this war, it was a dumb move in my view and is likely to make matters worse rather than better.

We have a son who still has over one year IRR left as an Army Reservist. A lot of IRR’s were called back into duty during The Global War on Terror.

So we are nervously watching this. He already served a 10 month deployment and his 6 years, just has the clock running on the 2 year IRR. He married and then left 3 months later on that deployment. He’s a police officer and a volunteer firefighter, living a life of service.

Please keep all of our military in your prayers during this difficult time of war.

Shallow sand,

I hope no US service members are killed or injured. Not getting involved in a war of choice would be a way to reduce this risk.

I hope Trump is smart enough not to choose a ground assault, but his choice of advisors has not been good in his second term, Hegseth in particular seems moronic.

Shallow Sand,

Your situation is exactly why everyone should have a vote, regardless of their age, education, etc.,: anyone who can be called to war, or who has loved ones who could be called, should have a voice in whether we go to war.

The US is not invading Iran. It would literally be the world’s biggest suicide pact if the Pentagon even tries.

Kleiber,

You’re assuming a rational commander in chief, advised by experienced and rational military advisers.

If that existed, this war wouldn’t have happened.

Let’s not forget another one of Andre’s brilliant predictions,

General Mad Dog Mattis ( Trump loved the name ) was Trump’s first Secretary of Defense.

Led a team, that predicted Peak Oil in 2015 and likely by 2018.

That predictiion was wrong, but appears sensible.

How did Trump interpret that information? Are we finding out now?

Venezuela and Khang Island?

What about child slave labor in the Congo for cobalt? No oil there!

Trump may be distracting from Epstein and Israel.

But he got his oil ideas from Mad Dog Mattis.

Mad Dog resigned. Said it was because of how Trump was managing long term Middle Eastern relationships.

Trump f****s everything up!!!

Given the British report today that confirms the Omani negotiations report, it is very likely that Witkoff and Kushner are in league with Israel and forced Trump to go down this route. Treasonous behaviour given it’s leading to the US getting kicked out of the ME and the petrodollar being at risk.

Let’s not forget that from 1992 conventional oil growth over a 16 year period was more than 2% each year (1.1 mbpd annually).

Something peculiar happened for the next decade. Growth was much less, only around 1/3 of the previous rate.

2015 thru 2018 marked the conventional crude peak, since then we have steadily lost 0.5 mbpd of conventional crude oil production each year.

We can expect the decline rate to accelerate, one might argue that it already has…

Dennis: “We have bombed Kharg Island already.”

Not the oil facility, which was the subject of the hysteria.

We merely took out the Kharg Island military implants, presumably so we can occupy the place.

Non-oil comment.

Gerry, Occupying the island doesn’t do anything without securing facilities on shore and a free flow of traffic through the straits.

Donald has said that Kharg was demolished. Now that might mean anything from a guy known to misrepresent the truth 24/7 but what it doesn’t do is bring stability to an already unstable situation.

. https://www.theguardian.com/world/2026/mar/16/oil-prices-rise-after-trump-claims-us-totally-demolished-irans-vital-kharg-island-export-hub

The US president claimed on Saturday that US strikes had “totally demolished” most of Kharg Island, telling NBC News that its military may hit site “a few more times just for fun”.

It’s time for the tired old folks carrying the last generation’s tired old dogma and thinking to fade away, and let the new people take over.

The idea that Israel is an ally, that Israel needs protection, or that Israel is anything but a vicious and lawless state that deserves what it gets is old thinking.

For people who know that war crimes are bad and perp’s need punishing, just where to set up the gallows to start hanging the Israeli leaders is the primary question.

We do all agree that war crimes are bad – right Gerry?

And before you blow a gasket talking about Iran’s ‘war crimes’, you should start closer to home, and with what everyone else is looking at, not some old 20th century crap you’re fixated on that the rest of the world has rightly moved on from.

If you think the USA can get a ship within a hundred miles of the gulf, you’re on drugs.

Gerry,

I was responding to what you wrote, that is “nobody is going to bomb Kharg Island”.

You are correct that the oil facilities were not bombed, though Trump has threatened to do so if his demands are not met. Hopefully he is bluffing, though Iran may call his bluff.

Does this military action help to extinguish the Iranian theocracy, and its ultimate goal of creating the United Islamic Republic across the Muslim world?

Doubtful- they have a firmly entrenched authoritarian power structure within Iran and will do anything it takes to hold its grasp over the country.

As I said before, it would take a massive ground invasion or a civil war to displace the regime of the Islamic republic of Iran. Neither scenario is likely, and neither would be guaranteed success. Both would likely degrade the capacity to export oil, nat gas, fertilizer, aluminum from all the Gulf countries for a very long time.

“Approximately one-third (roughly 30-33%) of the world’s seaborne fertilizer trade passes through the Strait of Hormuz”

Ironic that Trump has kicked mud in the face of a dozen countries that had long been reliable US military allies, acted as an arrogant bully on the world stage and imposed harsh tariffs on our ‘partners’,

and yet now pleads for their help to rectify a problem he created (warships to capture the Gulf waterway).

This irony is not lost on the citizens of world. Is it lost on the Americans who voted for Trump?

.

Yes. See Gerry, above.

Follwup comment- I think Trump is seriously considering sending in the Marines to take Kharg Island, as the only way to avoid being seen as a loser (his worst fear).

If he can’t force the IRI to comply, he can shut off their revenue source.

No doubt his circle is being tasked with coming up with the pros and cons.

“POLITICO poll taken last month found that 57 percent of Canadians would prefer their country depend on China instead of Trump’s America, [up from 19% prior to Trump presidency]”

God help the fools and children!

For the record, Iran is currently exporting as much or more oil than before any of this began. Iraq isn’t, nor is the UAE, Bahrain, Oman or Kuwait. The Saudis have diverted close to 5mbopd through their east-west pipeline to the Red Sea and Iraq is sending what they can through a pipe to Turkey. The UAE has a pipe to take their much-desired Murban crude to a loading port on the shore of Oman, well below Hormuz, but they’re afraid to use it right now. So while nobody else in the Gulf is exporting oil, Iranian exports have gone untouched. That speaks volumes for Mr. Trump’s intentions.

A massive array of pipes bring over two million barrels of oil from the (untouched) Iranian oil fields each day. These pipes dive into the Strait of Hormuz, travel on the floor of the Strait for about 15 miles, then emerge to fill a battery of storage tanks on Kharg Island. From there they supply several loading docks from an unusual jetty, which is both unique and fragile in the extreme. When built, it was also a brilliant piece of work, because the main channel of the Strait of Hormuz is 200-300 feet deep and needs no maintenance dredging. The jetty at Kharg Island in no way interferes with normal traffic in the Strait.

Also for the record, I use my true name, am a registered Republican, but am not a huge fan of Mr. Trump. I do not, for example, endorse his every move. But from what I understand, the mullahs that took charge of Iran some 47 years ago have created an incessant mantra: “Death to America.” Couple that with a dogged determination to create a nuclear weapon in facilities 60 feet in the ground and superlative ability at making missiles that travel further and further each year, and I can see where it might be best to destroy their evil endeavor before they succeed in their mission.

To wit, however, it would be sheer unadulterated craziness to destroy the Iranian oil facilities. The Iranian people, in general (at least the ones I’ve worked with), are good people who deserve prosperity. They are smart and make good partners. It’s the damn mullahs that destroyed the country of Iran. The young people have no jobs, no hope, no income. They are oppressed. I am almost never in favor of one country deciding another country’s leadership. However, we can’t have them trying to build a bomb to destroy America.

When this is all over, the 70-million Iranian people will need the income from this oil; it’s almost 60% of their GDP. The world will need their oil. Right now, a few radicals are throwing a temper tantrum. They will, by hook or by crook, be put out of commission. And the Strait of Hormuz will be reopened. And tankers will be able to load at the dock of their choosing. I strongly suspect an invasion will be necessary to ensure this. I sell oil and gas but I don’t want excessive prices. The world needs $80-$90 oil and $4-$5 NG. The inelastic trading platform for oil and gas is a joke, and manufactures these extreme prices by sheer algorithm action.

Gerry,

The idea that Iran wants to destroy the US with nuclear weapons is highly unrealistic. Here is a pretty good AI summary:

Iran’s “Death to America” (Marg bar Amrika) chant is a 1979 Islamic Revolution slogan, often understood as “Down with the USA,” aimed at ending U.S. hegemony rather than wishing death on individuals. It reflects deep resentment over the 1953 U.S.-backed coup, support for the Shah, decades of economic sanctions, and perceived interference in the region.

Key reasons for the rhetoric include:

Historical Grievances: The 1953 CIA-backed coup that overthrew Iran’s democratic leader to restore the Shah, followed by decades of support for his authoritarian regime.

The 1979 Revolution & Hostage Crisis: The revolution fundamentally defined itself as anti-imperialist, viewing the U.S. as the “Great Satan” interfering in Iran’s sovereignty.

Hostile Policies: Iran cites U.S. support for Iraq during the 1980s Iran-Iraq war, the 1988 shooting down of an Iranian passenger plane, and ongoing economic sanctions [12].

Regional Conflicts: The stance is reinforced by U.S. military presence in the Middle East and support for Israel, which Iran deems an existential threat [13, 16].

Political Identity: The ruling elite uses this rhetoric to maintain ideological unity and support its network of regional allies, although many citizens consider the chant outdated [15].

The chant is not directed at the American people but rather at American foreign policy and government leadership.

————————————-

The importance of the bullet point called Political Identity can’t be overstated: both the US and Israel are essential bogeymen/external enemies, which provide a reason for the current regimes existence. The problem here is that both the US and Israel have provided plenty of ammunition for this role. Sadly, this amunition was beginning to fade with time, and now this war provides infinitely larger support for it.

Like many of the projects of the current president, this war is deeply counterproductive.

Kharg Island and the Strait are 300 miles apart.

Gerry,

You are right, around 70% of Irans population weren’t even born when the 1979 revolution happened. They find it extremely hard to relate to a 7th Century ideological death cult. They have no future under this barbaric regime. They are cheering on the bombings which are weakening the regime piece by piece.

Irans regime is an oligarchy. A handful of families control most of the wealth and apart from lining their own pockets with luxurious assets worldwide, they fund terrorist organisations domestically and abroad, while the Iranian people struggle to make ends meet.

Trump did not want to go to war with Iran. He tried to avoid it as much as possible, but when the Iranian foreign minister Aragchi allegedly told Witkoff that Iran has 440kg of 60% enriched uranium, enough for 11 nuclear weapons, he realised there is no dealing with these spastics. Aragchi of course denied this, but anyone familiar with the regime knows this is something they would do, boasting and taunting.

Israel attacked shortly thereafter which got the U.S directly involved too.

Meanwhile what some of the “experts” here fail to mention is the Obama administration which gave Iran $1.7 billion, ( $400 million regimes money + $1.3 billion accrued interest ). Granted it was Iran’s money, but what do you think they used the money for ? Surely not for humanitarian purposes….

Granted regime change will be complicated, but i remain hopeful. Iran has a lot of potential for a bright future given the countries resources and young workforce given the demographics.

One thing that scares me is relationship between al-qaeda and IRGC. There seems to be evidence of cooperation throughout the years, and in Iranian channels there have been suggestions that the uranium has been smuggled out of the country through al-qaeda. I hope it is just rumours. I believe U.S will send commandos into Iran looking for this uranium at some point.

Finally, Russia is benefiting the most from this war at the moment. They would love this to drag out as long as possible.

“ Never,” Robert Pape, a political scientist at the University of Chicago who studies air power and regime change, replied when I asked whether what Washington was doing in Iran had succeeded elsewhere. “Bombings have never led people to take to the streets and topple their leader.”

There are two main reasons why air power has such a terrible record. The first, Pape said, is because bombings often prompt citizens to turn against the domestic opposition — no matter how much they hate the leader. “Even the hint that you are siding with the attacking state is used by rivals to stab you in the back,” he told me. To understand why, he asked liberals to consider how Americans might respond if Iran killed Trump and then encouraged the Democratic Party’s supporters to seize power; conservatives might imagine what would have happened if Iran did the same to Barack Obama. Just because you don’t like your country’s leaders, it doesn’t mean that you want to side with an external enemy who deposes them. The second reason is that bombings by themselves rarely fully decimate a government’s repressive capacity. “In order to save the pro-democracy protesters, you’ve got to be right there,” Pape told me. “You have to have troops on the ground.”

https://www.politico.com/news/magazine/2026/03/01/iran-uprising-trump-khamenei-regime-change-00806179

Gerry,

You said this, “And the Strait of Hormuz will be reopened. And tankers will be able to load at the dock of their choosing. I strongly suspect an invasion will be necessary to ensure this.”

The opening of the Straits of Hormuz would indeed be a good thing for the Global Economy.

However, it seems that the Iranian Ruling Party & the IRGC have implemented what is a Four-Tier Level of Ship flow through the Straits.

In a nutshell, there are those countries that they label as ALLIES of IRAN can have passage through the Straits, while those countries that are not their enemies and ask permission to cross are allowed to cross.

Those who cross without permission have been attacked with Drones, etc.

This is why we are seeing some traffic currently moving through the Straits of Hormuz. Thus, some believe Iran is losing control as ships are making it through the Straits.

Those Iran and IRGC see as enemies will not be allowed to cross the Straits.

So, it will be interesting to see how the U.S. Military is able to use its force to open the Straits, which would be a good thing for the USA and the global economy.

steve

Oil flow from straight of Hormuz

Hormuz

Interesting perspective on Oil prices

https://oilprice.com/Energy/Energy-General/The-Global-Campaign-to-Control-Oil-Prices.html

@ Hickory & DC

FYI

This is an excellent piece on cascading global risks from closure of the strait with a focus on economics and industry.

https://open.substack.com/pub/ctindale/p/systemic-risk-a-12-order-cascading?utm_campaign=post&utm_medium=web

Thank you. Its a good write-up.

The Gulf nations import roughly 70% of the their food through the Gulf maritime route too.

One interesting aspect of this war is that Iran seems to have damaged or destroyed five TPY-2 radar components of American THAAD missile defense systems.

It’s not clear (to me anyway) how many exist worldwide, but maybe 10-15. There were 13 in May 2025.

The manufacturer, Raytheon, can’t import anything from China, as it is is classified as “unreliable” by the Chinese government. This is part of Trump’s trade deal with China, which allows some, but not all, rare earth imports. The devices use gallium nitride chips, and China has a near monopoly on gallium.

It’s also worth mentioning that the radar system alone is said to cost $300,000,000 , and they were knocked out by drones that costs maybe $30,000.

The US and China squabbled about the installation of a THAAD system in South Korea a few years ago, but that system is being partially dismantled and shipped to the Middle East now.

All this is just stuff I read on the internet, I’m not an expert, so feel free to fact check me. But it does suggest that asymmetric warfare based on cheap smart(ish) drones may disrupt modern warfare assumptions outside of Ukraine.

I’ve read an analysis that suggested that the Iranian drones cost only about $4,000 to build.

The AN/FPS-132 costs over a billion, and as there were fewer than a dozen THAAD batteries, it’s kinda academic anyway. They can’t get the rare earths from China for rebuilding, and they’re not rebuilding them in an active warzone and the missile defence dream since Star Wars under Reagan has been, once again, shown to be smoke and mirrors for MIC grift.

This played out in Ukraine, and it was ignored. It is now playing out with Iran, and we are seeing that cheap, mass produced and reliable weapons from a country with industrial capacity will outcompete whatever wunderwaffen the other side has.

If anyone in the West in power still has a functioning brain cell, they will be cutting the private sector capitalists out and renationalising defence and focusing on things that aren’t artisanal superweapons that mean you lose one unit and your forces are combat ineffective or they only have so many munitions or maintenance time for a week of operations tops.

This shit was evident in 2002 with the Millennium Challenge. Col. Van Riper was 100% vindicated.

BLOOMBERG: The Biggest Oil Risk Is at the Bottom of the Barrel

March 15, 2026 at 12:00 AM PDT

Updated on March 16, 2026 at 12:32 AM PDT

By Javier Blas

Fuel oil is now an ultra-expensive commodity due to the Iran war, which is bad news for the global economy.

The shipping industry is sounding the alarm as some key ports may run dry, forcing ships to halt, with fuel-oil supply very low in locations such as Singapore and Fujairah.

The traditional relationship between crude and fuel oil is broken, with fuel oil prices much higher than expected, trading at $140 a barrel in Singapore and nearly $160 in Fujairah.

https://www.bloomberg.com/opinion/articles/2026-03-15/iran-war-the-biggest-oil-risk-is-at-the-bottom-of-the-barrel

————————–

With Singapore, the world’s largest bunker fuel port, handling 55 million tons per year, and Rotterdam, a distant second at 10 million tons per year, the situation for tankers and container ships will become more problematic as the Middle East War continues.

steve

Oil is cheap and flagrantly wasted. Wild swings in the price have cause severe economic pain four times in my life time that I can remember. This is the fifth.

The real problem is short sighted investment that ignores the inevitability of the next crisis. Europe and Japan have done a little better than most. High fuel taxes discourage waste, so price swings are proportionally less significant.

The world is facing a similar crisis to the one the Germans faced in 1916, when the British torched the Romanian oil fields. how long will it take for people to figure this out?

Alimbiquated,

Such a good question. I’ve been reading a pretty good book on that: The Collective Edge, by Colin Fisher. He argues that people generally follow their group’s ideas, and some people are unlucky about what group they’re born into, and they’re in a group with ideas that are…unrealistic, counterproductive.

Currently we have groups that are tied to old religions, to old industries, to obsolete ideas and practices. They’re being manipulated by powerful interest groups – oil, etc., and corporate media. They believe what they’re told.

How do we break the spell of group identification? I don’t know – I’ve had family members killed by their beliefs. They knew it too, but they thought their beliefs were more important than the obvious and and looming risk of dying.

How do you break through beliefs that strong??

And while I’m on a rant, note that Chinese battery makers are betting big on sodium based batteries, because they might not be able to get there hands on lithium.

https://www.reuters.com/sustainability/climate-energy/china-battery-makers-bet-big-sodium-move-away-critical-minerals–ecmii-2026-03-16/

Thinking ahead.

If you buy a gas guzzler on the assumption that fuel will always be dirt cheap, you’re up a creek without a canoe when the price spikes.

Interesting opinion on Iran war

https://www.middleeasteye.net/news/us-israeli-war-iran-founded-two-huge-miscalculations

As of this posting (9:40 AM EDT), the IRGC just announced an evacuation warning for oil/gas production facilities in KSA, Qatar, and the UAE.

This in response to the attack a few hours ago on their South Pars facilities.

While Hormuz blockage is – theoretically – reversible in hours, infrastructure destruction will cause years’ long diminishment of hydrocarbon availability.

The escalation ladder is being implemented this very moment.

Coffee. Any thoughts on why USA/Israel would strike South Pars infrastructure?

Shallow,

I strive to avoid speculation in general and purposefully/strenuously steer clear of online politically tinged discourse.

That said, in respect to all the years of our interacting on this site …

It should be clear that Israel and Iran (the current regime) are locked in an existential struggle. (Reports are that it was the Israelis that attacked both the Tehran oil facilities and now South Pars. Verification in these matters is always tenuous, at best.)

As a life long, serious student of military conflicts throughout history, my ‘take’ is that – absent some near-divine intervention – both of these entities (Israel/Iran) will plunge onwards towards ever expanding kinetic action until it becomes physically impossible to continue.

Use your imagination as to the scenarios implicated by that statement.

My sincere best wishes to you, Shallow, your family and especially your son.

Goes for all of us, actually.

In addition to the South Pars infrastructure being attacked, the nearby Asaluyeh processing plant was also targeted.

Depending upon the extent of the damage, ~75% of Iran’s natgas supply could be offline.

As ~80% of Iran’s electricity generation is from natgas, regional blackouts seem imminent.

Since the IRGC has declared on an ongoing basis that they will respond to attacks in a reciprocal fashion, we could see the ‘unfathomable’ consequences that I highlighted earlier manifest shortly.

Coffee. Thanks. Praying a lot.

I won’t attempt to rationalize any particular action of the war participants, or to justify the existence of any country in the world.

But I will point out a few critical differences in motivations, as an outside observer. Keep in mind that participation in conflict (kinetic or otherwise) is always an existential threat for any particular regime, as are its policies in regard to domestic economic performance. That applies to all governments, even the most authoritarian ones to some degree.

-For Iran, the 47 year Israel destruction project is entirely an optional fundamentalist project, a keystone of the larger plan. This long war is not an existential threat to the integrity of Iran, rather just its government as it now exists. The exception to this is the slight chance of country fragmentation in a severe civil war scenario. Very slight…probably less than most countries considering the geography and very very long history.

-For Israel this long conflict is an existential threat to the current government, but also to the existence of the actual country and population. If one doesn’t understand this, and the very long specific cultural history of living under severe duress, then it will be hard to understand the deep seated sense of desperation that underlies the behavior of that nation and all of its people.

With those motivations/distinctions in mind, don’t be surprised by any act by of the actions of both Israel and Iran. The Iranian regime won’t rest/relent until their project of Israel erasure from the maps is complete. This is intense fundamentalist religious fervor in action, with a huge collective ego stake in the project. And for Israel, the whole of Israel society will struggle to the end to survive. To the very end if that’s what it takes. They will return the favor of attempting to destabilize the Iranian regime, just as the regime has been working to destabilize the nation of Israel for the past 47 years.

The motivations of the rest of the world in this are a very mixed bag. Most simply want stability, and an economic sense of fair play.

Hickory,

I think you might be underestimating the importance of Israel as a convenient external propaganda enemy, used to prop up the legitimacy of the unelected regimes in the ME, including Iran.

I think it’s also possible to forget just how much Netanyahu has been fighting for his political life, and how convenient foreign wars are to someone in that position..

And, of course, the same logic applies to the US president.

Dennis – Please let me know where your models are pointing…mine suggest near-term delcline rates of 7% for around 5 years, then tappering to ~4-5% annually…This would put world production at half of current level in 2040…steep decline will be from the unconventional resources…

Kengeo,

See chart at comment linked below

https://peakoilbarrel.com/november-world-oil-production-slides/#comment-795505

or direct link to chart below

https://peakoilbarrel.com/wp-content/uploads/2026/03/shock2511c.gif

Note that this model is from November 2025, before Feb 2026 US/Israeli attack on Iran.

That will be another oil shock which will reduce World output of C+C for some unknown period of time. Perhaps it will be similar to the 1980s shock due to the last major war in Iran.

Brent futures contract for May 2026 at about $110/bo as of 6 PM US eastern time on March 18.

It occurs to me that the earth is a little overpopulated with fire-apes.

In fact, I think the whole ape thing was/is a wrong wrong wrong turn.

+1

Human civilization has just tipped over the Seneca Cliff.

We will be fighting over the scraps all the way down from here

https://www.youtube.com/watch?v=X_gI1zTYGp8

Gentlemen it is upon us.

My god, I don’t know how this can continue:

https://rayonegro.substack.com/p/la-mayor-crisis-de-la-historia

https://market-ticker.org/akcs-www?post=255104

Another perspective.

Trump must ban all exports now.

For what it’s worth, bold mine:

Peak Gas

Peak gas is the point in time when the maximum global natural gas (fossil gas) production rate will be reached, after which the rate of production will enter its terminal decline.[1] Although demand is peaking in the United States[2] and Europe,[3] it continues to rise globally due to consumers in Asia,[4] especially China.[5][6] Natural gas derived from fossil fuels is a non-renewable energy source that produces significant greenhouse gas emissions.

Natural gas is expected to peak after other fossil fuels.[7] One forecast is for natural gas demand to peak in 2035.

The concept of peak gas follows from Hubbert peak theory, which is most commonly associated with peak oil. Hubbert saw gas, coal and oil as natural resources, each of which would peak in production and eventually run out for a region, a country, or the world.

And Hubbert thought we should pursue solar as a replacement.

Nick —

Solar is now the largest supplier of electricity in Texas, so that is happening.

https://www.reuters.com/sustainability/climate-energy/texas-makes-clean-power-breakthrough-solar-output-overtakes-coal-2025-12-09/

Calm. The Strait of Hormuz will be open soon. It is telling that Iran is the only Gulf country that has been exporting oil right through the conflict. We could hit Kharg Island at any time, and yet it hasn’t been done—due to the explicit orders of President Trump. Warthogs are taking out the remaining Iranian mining vessels. Bank accounts have been frozen. The regime is in tatters, and the smart survivors will be defecting soon. This has come nowhere close to pushing us over the Seneca Cliff. Hell, the price of WTI has fallen like a stone today—does that look like the end of the world? So far this has taken less than three weeks and an awful nuclear threat has been eliminated. We should see WTI of $75 by this time next week (which is too low for long term viability, but ho-hum). LNG prices may remain high because the Iranians did some serious damage to their Arab neighbor, Qatar. I would imagine that, once they’ve had time to think it through, many countries will come forward to see to a welcoming, wide-open Strait of Hormuz. All in all, this has been a very well executed military operation. I continue to be dismayed to read the posts of so many lefties on this site. That economist/activist who singlehandedly kept Austin weird has no sense and no purpose. What do you lefties find so attractive about a peak oil blog? Writing enthusiastically about hunger for all? Going helplessly over some imaginary Seneca Cliff? Holy smokes, boys, enjoy the day, and then tomorrow, and the next day. This has become a blog of nervous nellies and soothsayers, lifting their skirts and twisting their prayer beads. Have a bit of optimism! The U.S. and Israel are leaving the Iranians a way to make a good living once the fighting is over, and once again, they can prosper and move about the world in freedom. What we are witnessing here, in real time, is a rearranging of the Middle East geopolitics for a better future. Rejoice.

Gerry wrote: We should see WTI of $75 by this time next week (which is too low for long term viability, but ho-hum).

Nope, it ain’t gonna happen. This war is a horrible mistake and will cause many thousands of innocent lives before it is over. Over one hundred elementary school girls were killed by one bomb.

The ONLY people who will benefit from this war are oil producers. They are all now happier than a pig in a mud wallower. But we, not just Americans, but everyone on earth will now have to pay higher prices for everything.

Don’t be happy because of Trump’s huge mistake. It will cost you dearly. Well, that is unless you are an oil producer.

Dr. Maddox; from your social media experiences in the past I know you are a doctor of internal medicine; from my personal communications with you in the past I know you to be a sophisticated mineral owner AND, most importantly, a working interest owner in countless oil and gas wells throughout the country, from the Bakken down to Texas. In other words, you place your money where your mouth is. and understand well economics very well. In further words, you know more about oil and gas than any internet expert on this forum. Everybody. Pretty much combined.

But you are making the same mistake hundreds of others before you have made and that is to buck the liberal politics this forum is all about, that Ron Patterson created years ago and passed down to hand picked others.

This is a place of incognito, angry, bitter people who hate America, want desperately for it to fail….so they can tell future people that have entered the country illegally, that are sucking it dry of money, and morality, they told you so.

I have not looked in on this shit hole for two months, I just did, whoa Nellie.

Liberals here are not interested in your oil and natural gas experience, the title of the forum is misleading; they dislike what you have to say, they are trying to control the content of blog, to make it only about their sick way of thinking… they would like you gone.

My father use to say about dog turds; the more you kick them, the more they stink.

You are a brave man, sir, and I appreciate you.

Dr. Maddoux, I sure hope you are correct in your views.

I honestly don’t know how this is going to turn out.

What things make you think this won’t be another long-term occupation in the Middle East?

If it isn’t, and we leave fairly quickly without killing all of the Iranian regime (reportedly over 1 million people) why won’t they just come back out of the woodwork and go after Israel and their Gulf neighbors? Seems like they have been doing that since 1979. They have long freaking memories. Heck, they still hate the Brits as much as us because of the 1953 coup, even though none of the fighters were alive then.

I do agree the WTI market thinks this thing will be over soon. Middle Eastern grades are trading as high as $170. I don’t pretend to understand oil trading. But it seems to me maybe the people trading those Middle Eastern grades might be a little closer to the situation on the ground than the WTI traders? I could be dead wrong on that?

In any event, I’m praying for no boots on the ground and that you are right, that this will be over soon with no US military return (because of things going to hell when we leave.)

As for the right and left stuff, I think we make a huge mistake when we let ourselves get sucked into that. I have to deal with people from all walks of life in my job, and I don’t give a crap about that. I’m going to engage with them regardless.

Personnally I don’t see any contradiction in realizing that this war on the IRGC is, -once it is over-, on the middle/long term :

– good for the Iranian people

– good the overall world C+C production

– good for Israel security

– good for the middle east security

– good for the US and Western oil majors in general

– good for the Iranian economy

– good for western (Israel included) economies

– good for the overall strategic advantage of the US towards China (Carter doctrine 2.0)

But at the same time, the overall “peak oil background” remains what it is (a kind of atrocious banality), and on this subject, having an honest look at the associated oil history, would perhaps rings some bells. Typically realizing that the first oil shock structural cause was first and foremost the US 1970 conventional peak, and the “arab embargo” narrative a great opportunity to “put the blame on the Arabs” (but also for the GCC countries a great opportunity to say “we have done something for the “palestinians””

Overall a major wake up call almost totally missed.

Reminder :

US production and imports around 1970 :

https://iiscn.wordpress.com/wp-content/uploads/2026/03/us_oil_production_and_imports_1920_to_2005-1.jpeg

US production up to now :

https://iiscn.wordpress.com/wp-content/uploads/2026/03/us-oil.jpg

I read somewhere the eia is targeting US tight oil “peaking” or “plateau-ing” in 2027 or 2028, is that correct ? (have to re check)

Note : trying to put two pictures, not sure how to do it, replaced by links

us oil

Some years ago, I was walking with my dog through a wood, and there we met a neighbour armed with a shotgun, a very fine expensive shotgun. He was a wealthy executive and entirely a man of the town, not a countryman, and no understanding of nature, country life, farming, or hunting. But we greeted each other civilly and then he annonced that there was a hornets’ nest further along the path and that he intended to destroy it by blast iting with the shotgun. I looked down at my dog who looked back up at me, and both of us recognising a madman when we saw one. Quickly, I bade goodbye to the lunatic and wI and the dog got out of the vicinity double quick. A couple of seconds later there was a loud BLAMM BLAMM sound as the shotgun was fired, and then a prolonged AAARRRGHGHGH yell/scream whatever. It’s not hard to imagine the effect of discharging a shotgun into a hornets’ nest. And it’s not hard to imagine the effect of the stings of a hundred or more surviving hornets on a crazy fool’s face. Doubtless the queen hornet died, but what of so many of the other sting equipped terrors ……..? I hadn’t thought of this incident for many years until President Trump decided to unleash thye most powerful best equipped formidable fleet of the USN on Iran.