North Dakota published their monthly report on Bakken Production and All North Dakota Prouction. Nothing to get excited about. Bakken production was up 28,285 barrels per day while all north Dakota was up 27,864 barrels per day. This means that North Dakota production outside the Bakken was down 421 bp/d.

The Director’s Cut comments on the price they are getting for Bakken Oil:

Oct Sweet Crude Price = $85.16/barrel

Nov Sweet Crude Price = $71.42/barrel

Dec Sweet Crude Price = $73.47/barrel

Today Sweet Crude Price = $71.25/barrel (all-time high was $136.29 7/3/2008)

Interesting that they are selling their oil at about a $21 discount to WTI about a $35 discount to Brent. More of the Director’s comments:

The drilling rig count was unchanged from Oct to Nov, but the number of well

completions dropped from 166 to 138. Days from spud to initial production remained

steady at 114. Investors remain concerned about the uncertainty surrounding federal

policies on taxation and hydraulic fracturing regulation.

We estimate that at the end of Nov there were about 510 wells waiting on completion

services, an increase of 50.

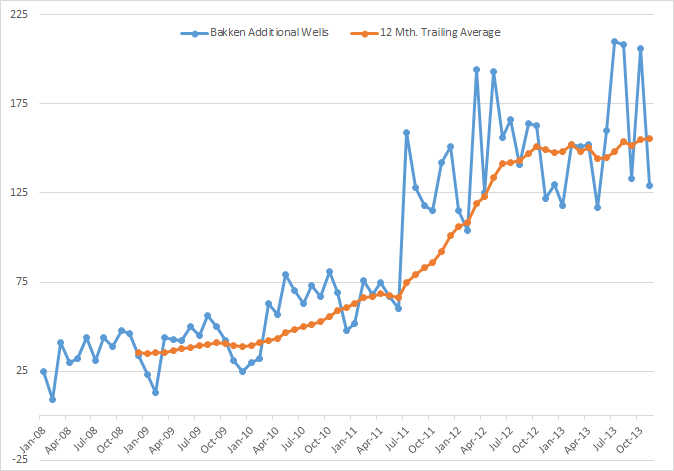

This plot is “Bakken Additional Wells” and the 12 month trailing average. As you can see the average for the last 15 months or so has been pretty flat, around 150 additional wells per month.

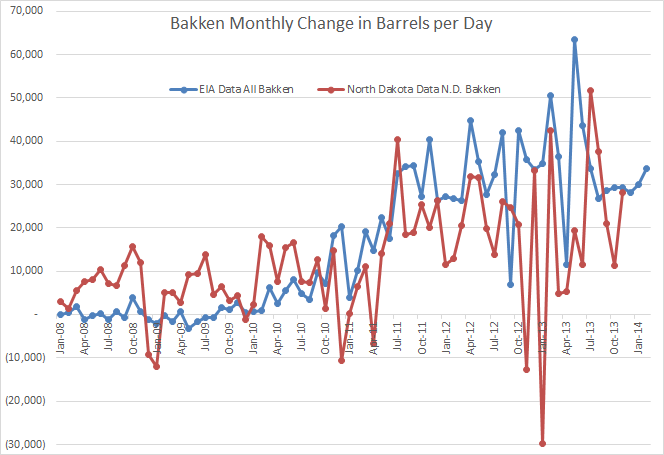

I find the following two charts very interesting. I am comparing the EIA data, that came out Monday with the North Daakota data that came out Tuesday. Keep in mind that the EIA data includes the Montana part of the Bakken and the North Dakota data does not. Montana Oil Production was 77,000 bp/d in October down from 82,000 bp/d in April of last year. They reached a high of 102,000 barrels per day back in September 2006 so they are in general decline. Also, the Montana data is for all Montana, not just their share of the Bakken

The EIA data is through February 2014 and the North Dakota data is through November 2013. The data is actually additional barrels added to production. The Bakken was up 28,285 bp/d in November.

Notice that, on average, the EIA monthly additional barrels is a lot more than the North Dakota additional barrels. This cannot be accounted for by Montana production because it is down the last few months and it has very little change from month to month.

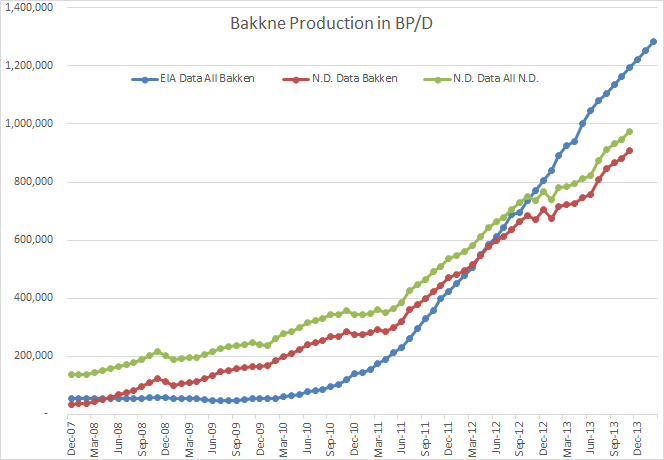

But this chart is the one that blows me away:

In November North Dakota had their share of the Bakken at 908,304 bp/d and all North Dakota at 973,280 bp/d. For the same month, November, the EIA had the Bakken at 1,193,496 bp/d. So even if you add Montana’s 77,000 barrels to the N.D. Bakken you only come up with 985 kb/d or so.

And how could they have the total Bakken lower than just the North Dakota part of the Bakken from June 2008 through January 2012?

The following comments and charts are provided by Wes538. Thanks Wes.

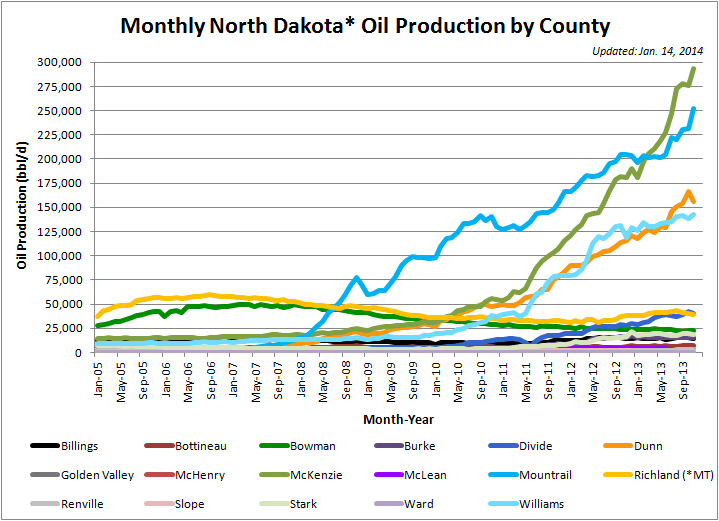

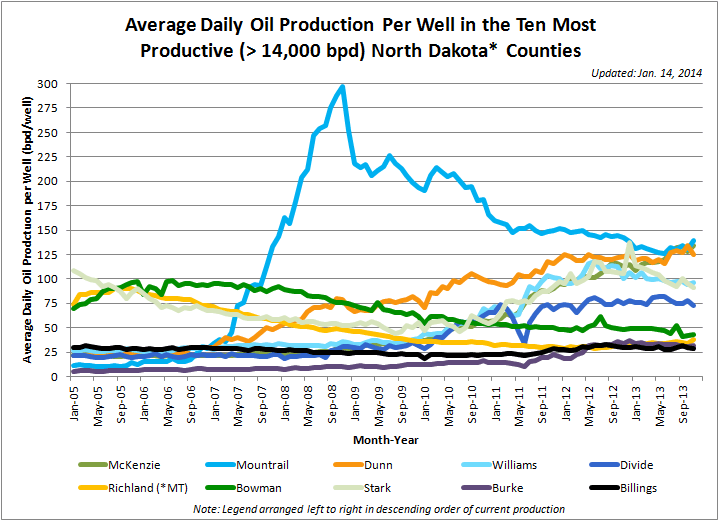

Following the release of production data from last November today by the North Dakota Oil & Gas Division, I have updated county-by-county production charts. Hopefully I have used the image upload feature correctly and they display.

Although I still have them labeled as North Dakota production, that is no longer strictly the case, as I have begun to include production data from Richland County, Montana. More than any other county, I thought Richland ought to be included due to being the most noteworthy county within the Bakken in Montana as well as the historical significance of the county being home to the Elm Coulee oil field, where about a decade ago early indications as to the potential of the Bakken formation were obtained.

Going back to North Dakota, McKenzie and Mountrail Counties had an especially good month in November. Oil production in Mountrail County increased by a little over 20,000 bbl/d, the biggest one-month increase in the history of the county and one of the largest monthly increases of an individual county in North Dakota history. For Mountrail, this comes on the heals of a 17,480 bbl/d monthly increase in July 2013 that was the largest monthly production increase in county history at the time. Evidently writing off production Mountrail County may be a bit premature.

Here is an up-to-date chart of daily oil production per well in the ten most productive “North Dakota” counties (Richland County, Montana is included, too; it would be the sixth most productive North Dakota county).

To see all comments, or to leave a comment, click on the COMMENTS link below this line.

RON,

Great Post. That chart showing the difference between the EIA and ND of the Bakken is quite interesting. As you stated, even adding the 77,000 bd from Montana, the EIA is still more than 200 kb a day more than what ND is showing.

The EIA data of the Bakken & Eagle Ford always seemed a bit unrealistic.

steve

Hi Steve,

I noticed pretty early (along with Ron and others) that the DPR data did not look very realistic. Keep in mind that if one aspect of the report is bogus, the report should probably be ignored altogether. So the legacy decline estimates are also likely to be bogus. I used to trust the EIA data to some degree, but reports that are as bad as the EIA’s DPR are an embarrassment.

I used to attempt an estimate of Eagle Ford output by using EIA data to adjust the data from the Texas RRC (which is also pretty bad for the most recent 12 months, but gets more accurate further back in time), but the EIA has just been adding a 50 kb/d increase to Texas C+C output since March 2013 which is not credible. Budget cuts in DC are affecting the EIA’s ability to do its job.

Texas C+C (kb/d) starting in March 2013: 2402, 2452, 2502, 2552, 2602, 2652, 2702, 2752 (Oct 2013 is last data point). See

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFPTX2&f=M

See chart below for my estimate of Texas C+C and for more info see

http://oilpeakclimate.blogspot.com/2013/08/eagle-ford-shale-may-soon-reach-1.html

A new chart has been added to the bottom of the post showing the change in RRC estimates from Jan 2013 to August 2013.

DC

Dennis,

Thanks for the reply and the graphs. Yes, I now agree 100% with your assessment on the EIA… total rubbish. You’re exactly right. If I look at your chart with the EIA’s production figures for Texas from Jan 2013… it’s a damn straight line. There is no bumps or valleys.

Here is a question. If you believe both the EIA and Texas RRC data is both lousy, which is the least lousy? I would imagine it would be the Texas RRC.

So, if we consider that the EIA has overstated the Bakken by 200 kb and Texas by 500-600 kb, is overall production in the U.S. much less than what the EIA is stating on its website?

Dennis, if you had to guess what the Bakken and Eagle Ford are currently producing together, what would you believe that figure would be?

By the way, is there any way I could get your graphs above?

Thanks,

steve

Hi Steve,

It is only the DPR which should be ignored. The EIA data for C+C, though not perfect is still much better than RRC data for the most recent 12 months. The estimate line in my previous chart is my best guess for the “true” TX C+C amounts. It is the average of the EIA and C+C data up to Sept 2012 and 98.2 % of the EIA data from Oct 2012 to Oct 2013.

So a rough rule of thumb would be the EIA-RRC avg up to 12 months ago and then 98 % of the EIA estimate for the most recent 12 months will be pretty close.

Below I show a chart with RRC and EIA Texas C+C data downloaded in March 2013 and November 2013. Notice that the March EIA data is much closer to the Nov RRC data than the March RRC data. If one had chosen to believe the EIA estimate, they would have been much closer to the truth. Also notice that the EIA data changes very little from March to November (because the estimates are much better.)

The short answer to your question about data for Texas is that the EIA data is much better especially for recent months. For Bakken data go with the NDIC data and ignore the DPR altogether, the model is flawed. Eagle Ford data is hard to come by, but my estimate for July was nearly 1000 kb/d, I will update that soon.

Edit(1/17/2014 8:15 AM) You can right click on the chart and choose save as in MS Windows (I am unfamiliar with other types of OS).

Dennis

Chart on Eagle Ford and Bakken below, data through Oct 2013 (last data for Eagle Ford).

Note that I have adjusted the Eagle Ford data upwards for the last 12 months due to the poor data from the RRC, Oct 2013 C+C is about 1070 kb/d for the Eagle Ford, if we use the 17 % adjustment factor suggested by the RRC the EF is 930 kb/d for Oct 2013, but I believe this adjustment factor should be about double that (34 %). The raw data for Oct 2013 for the Eagle Ford is 793 kb/d for Oct and it was at 892 kb/d in June, both of these numbers will increase in future revisions to RRC data, my guess is one year from now the RRC will report 1000 kb/d for June and 1070 kb/d +/- 1% for Oct 2013.

One more chart for Eagle Ford C+C (kb/d), EIA and RRC data compared.

In the last chart, what is going on in Williams? What caused per well productivity to take off? Did they drill into a “conventional” pool?

I think you’re thinking of Mountrail County, where production shot up to almost 300 bpd/well in November 2008 (I’ll make a note to modify the Mountrail/Williams colors for future charts).

Mountrail is largely where the first “modern” Bakken wells in North Dakota were drilled in the mid-t0-late 2000s. Presumably this county led the way because many of the sweetest of the “sweet spots” are there, as detailed by Rune Likvern in his January 4th post on this blog.

My best explanation for what happened with the per well productivity takes mainly a mathematical approach. Prior to 2007 Mountrail County had been a relatively insignificant oil-producing county, with a relatively low active well count and production. Under 2% of all the wells capable of producing in North Dakota at the end of 2005 were located in Mountrail County, while today over 17% are. Increasing the active well count by a factor of 3.5 from May 2007 to November 2008 by bringing 186 very good wells online led to an incredible 14-fold increase in overall county production during the same period and caused the per well productivity to make an incredible surge. Mathematically speaking, in terms of bpd/well, the numerator had a much larger proportional increase than the denominator.

But then, something obviously happened in December of 2008 to cause the per well productivity in the county to crash. Drilling slowed down around that time, likely due to winter weather and the recession, but more importantly daily production declined that month and once more a month later in January 2009. By the summer of 2009, drilling in the county had picked back up, with more than double the number of wells brought online between May and September 2009 as had been brought online between May and September 2008. However, the increase in production from these new wells was not as great, on a strictly percentage basis, compared to the previous wells. Both the numerator and denominator of bpd/well continued to increase, but the numerator began to increase at an increasingly lower rate. Mathematically, the production per well had to decrease.

Drilling in Mountrail County has not really significantly slowed since 2009 (though has not necessarily increased in intensity, either), but obviously per well production is nowhere near the high reached in 2008 as the rate of production has tended not to increase as much as the rate of wells being brought online. Put another way, this can be used as another illustration of how an increasing number of wells are required to maintain or increase production.

Below is a potentially useful chart that shows the monthly percentage change in oil production and active wells in Mountrail County. Note how completely out of sync the two were prior to the second half of 2008.

Wes, thanks for the explanation. So basically from a standing start in 2007 they drilled a few good wells.

Elsewhere in the world, troubles continue….. Data are to Sep 2013, Libya, Sudan and Syria are all pretty well off line…

The Arab Spring – Impact on Oil Production

“Oil production has fallen by over 2 million barrels per day in five MENA countries (Libya, Syria, Yemen, Tunisia and Sudan) affected by violence stemming from the Arab Spring that began with riots in Tunisia in December 2010.”

http://rbnenergy.com/could-new-tank-car-rules-derail-the-bakken-crude-boom

“The recent tragic spate of four rail accidents involving crude-by-rail, three of them carrying crude from North Dakota, have increased pressure for regulation of rail tank car standards. The railroad industry- through the American Railroad Association (ARA) – proposed improved safety standards in 2011 for tank cars carrying hazardous materials including crude oil. These standards have been adopted by US tank car builders and were mandated this week by the Canadian Government for new tank car construction. If the new standards applied to all existing tank cars then at least 75,000 cars manufactured before 2011 would require retrofitting. Today we examine the impact hastily implemented new regulatory requirements might have on Bakken crude oil takeaway.”

The article goes onto show industry concerns that regulations may come into mandate all the old tank cars need to ungraded, and provide numbers to show the dislocation it would involve. There must be some worried people in North Dakota.

This ironic thing to me is by making the tanks stronger, means WHENthey BLEVE the explosion will be bigger. Being stronger, may help some of the oil from being spillt in the first place, but if one car is spilling its 600 bbls of oil and it catches on fire, light oil then very easy, then any full intact tanks will merely heat up, boil off, build pressure, and BOOM. But a bigger BOOM as the new stronger tanks will require a higher pressure to rupture the skin of the tank.

So if they continue railing these extreme light oils, I feel the 4th of July will continue to be more than a once in a year event. The strange thing is the heavy oils from Alberta will probably be tarred with the same brush, no pun intended.

Terrific video from New York Times about the life of a young woman working in the oil fields of North Dakota. Puts a a human face on the “fracking miracle.”

http://www.nytimes.com/video/opinion/100000002648361/running-on-fumes-in-north-dakota.html?playlistId=1194811622182

Maybe I missed it, but why is the price per barrel dropping so fast?

Pssst, maybe because kerosene and diesel are in demand and there isn’t much of those fractions in LTO.

https://rbnenergy.com/i-m-waiting-for-the-crude-gulf-coast-pricing-scenarios-after-the-flood

“If the flood of new crude arriving at the Gulf Coast during the first six months of 2014 overwhelms refiners in the region, then the pricing consequences may very well be quite radical. Could prices at the Gulf Coast flip to trade at a discount to West Texas Intermediate (WTI) crude delivered at the Cushing hub that is home to the CME NYMEX contract? Even if Gulf Coast crude retains its premium over WTI, deep discounts may be required to encourage refiners to process increasing quantities of light sweet crude. A downward spiral of crude prices could ensue. Today we lay out possible price scenarios.”

This link is currently available, but at some time it revert registration be required.

The Keystone pipeline from Cushing to the Gulf coast opens very shortly, plus the 2nd Seaway pipeline starts in a few months. There is concern there will be too much oil in the Houston area for the refineries to handle. The link explains what some people in the industry predict may happen.

The glut of oil has moved from Cushing to Houston and now needs to move to Mississippi and La, or find a ship and head to the east coast or Canada, unless they lift the export ban.

Now I say glut, that is a glut in very light oilsm as the Gulf coast refineries can handle the Canadian crude, it just needs to push out the imports from Mexico, SA and Vz. We do live in teresting times.

If you want diesel . . . if you are a refinery and you have a customer demanding diesel, then you don’t refine Eagleford oil. There’s no diesel in it. If you have a different oil, from Nigeria that has diesel in it as well as gasoline and other fractions, then you refine it to satisfy all of your customers. Why buy the Eagleford product?

perhaps declining gasoline sales

http://www.zerohedge.com/sites/default/files/images/user5/imageroot/2013/03/Weekly%20Total%20Gasoline%20Retail%20sales%20By%20Refiners.jpg

But those are retail sales by refineries. Eric Pfeiffer says:

This data shows sales that are direct from refiner to US retail outlet. Most refiners have largely ended that process as the retail sales margins are too small. Refiners instead sell to third parties who sell to retail. There is another EIA data piece displaying that.

Refiner sales of gasoline to the US market continue at a pace last seen in about 1997. US refiner sales of gasoline to markets outside of the US have increased allowing increased output.

The days of people buying gasoline at “66” stations or “Valero” stations or ” Standard/American” stations has become a memory we recall as we watch older movies,as those refiners now sell to Super America chains, “Holiday” chains and such which are third party vendors.

It is however boom times for refiners as exports of gasoline grow due to cheap US shale oil allowing refiners to underprice countries relying on conventional oil production like Brazil, Mexico, and Canada

The EIA says USA 2012 gasoline consumption was six percent less than 2007 which was our USA peak year for gasoline .

I expect the 2007 record to stand, given the less than robust economy, more efficient cars and light trucks, and highly probable increases in the price of oil.

I suppose most people will think I’m slipping pretty bad when I say that there is also a significant possibility we will be paying higher taxes on gasoline in the not too distant future.

But we’re headed for a time when if the people in for instance Northern Virginia want more freeways and less potholes , the only way to get what they want might be a new gasoline tax.

We’re also going to see a smaller portion of the people in the country driving a car as time goes by, and non drivers will be glad to see drivers pay more taxes in hopes of paying less themselves.

A dime added to every gallon sold in and around a big city would go a long way towards paying for a new street car line or a fleet of buses .

Hi Mac,

You state: “I expect the 2007 record to stand, given the less than robust economy, more efficient cars and light trucks, and highly probable increases in the price of oil.”

Let’s not forget what may be the biggest driver of reduced gasoline consumption over the next two decades–the retirement of the baby-boomers.

Best,

Tom

“Most refiners have largely ended that process as the retail sales margins are too small. Refiners instead sell to third parties who sell to retail. ”

How does adding another layer of middleman improve margins?

Because the refineries, or oil companies, actually owned and operated the retail outlets. They were in the “gas station” business. They are getting out of the retail business because the overhead is just too high.

They find it more profitable to sell wholesale at just a few cents under the retail price and forego those few cents instead of owning and operating the service stations themselves.

Hmm. The big refiners are Valero, Marathon and Tesoro. I do see the occasional Chevron retail outlet, but not refiners, though I’m sure there probably are some.

The chart is 131K bpd. Not big numbers, but regardless of all of this, the avalanche clearly correlated to Lehman.

Hi Ron,

If demand for gasoline was high, then why is the price of LTO very low? Why pay a premium purchasing conventional oil when LTO sells at such a steep discount? Either there are problems with refining LTO that refineries are discouraged to use it, transportation bottlenecks, or demand for gasoline isn’t high enough to drive up prices for LTO. The prices dip started back in October, which is usually the end of high demand for gasoline in the US (seasonal demand). It seems too close of a coincidence not to consider gasoline demand declines as a possible cause. If I understand it correctly usually during the fall refineries produce more diesel/home heating fuel to meet season demand for these products.

Is there a chart or data that shows the amount of gasoline being produced at refineries? FWIW: I think the economy (globally) is slipping back into another recession. I’ve seen articles about a significant slowdown in developing countries and I think the US is about to double-dip into a deeper recession. If this turns out to be correct, then we might see a decline in conventional oil prices globally.

The other question I’ve been thinking about is how low can LTO go before drillers shutdown production. They may already be in negative profit territory, and I suspect they are riding this through, hoping that prices swing up again in the spring with increases from seasonable demand for gasoline to make up for any losses.

LTO, or Light Tight Oil, sells at a discount because it is so light it is mostly condensate. It makes pretty good gasoline but you get no diesel, kerosene of jet fuel from it. Gasoline sells at a pretty good discount to diesel these days. And as you probably know condensate, or very light liquids, have a much lower BTU rating than does the heavier stuff.

Yes there is an EIA site that gives us: Net Production of Finished Motor Gasoline. I can spot no downward trend in the data. It looks pretty flat to me.

The last I heard it was costing drillers about $60 a barrel to produce LTO and deliver it to the refineries.

“FWIW: I think the economy (globally) is slipping back into another recession.”

The Baltic Dry Index used to get discussed from time to time back on TOD as an indicator of recession. It’s definitely taken a sharp turn down since Dec: http://www.bloomberg.com/quote/BDIY:IND

I have updated my model with the latest ND Bakken data from the NDIC. The average well in this model uses a hyperbolic decline model with qi=13.1 kb per month, b=1.0 and di=0.142. First month production is 400 b/d, 30 year EUR=365kb, 10 year EUR is 267 kb. It is assumed that new well productivity starts to decrease in June 2015 (average EUR starts to drop) and this productivity decrease accelerates over time reaching its maximum rate of decrease by 2018. By that time profitability starts to decrease and wells are added more slowly. Peak in 2017 and total ERR (economically recoverable resources) are 8.4 Gb from 1953 to 2073.

DC

THis is week old news now but I just ran across it myself and h don’t remember seeing it posted here.

http://www.vancouversun.com/business/National+Energy+Board+decision+among+pipeline+milestones/9369456/story.html

A major expansion of pipeline capacity to the western Canadian coast is now officially rubber-stamped and there is no doubt whatsoever in my mind that the oil will go west in pipes unless the Keystone gets quick enough approval to satisfy the Canadians – meaning before they are deep enough into the process to just go ahead and follow thru and quit monkeying around with the Obama administration.

Some people think the “real Canadians” meaning I suppose an alliance of the First Nations and Canadian environmentalists can stop the the building and or expansion of the proposed new pipelines.

I would happily bet my last can of beans that the opposition will be bought off when it can be bought in the form of nice little hospitals, schools, cell towers , four wheel drive pickups , internet access, and tons of other temptations all easily provided with a minor g fraction of one percent of the money at stake.

Those who can’t be bought will be bulldozed out of the way.

This sort of thing is a federal question in Canada, and the opposition hasn’t a snowball’s chance on a hot stove over the long term. The votes ares in the cities rather than the thinly settled wilderness.

OFM,

Don’t underestimate the strength in the courts First Nations have stemming from their treaty rights. Some communities can be offered enough incentives to, as you say, be “bought off”, but for others their just won’t be enough in it to replace all that will or could be lost.

This’ll be in the courts for a good while.

I agree it will take a while- but people are pretty much alike all over the world, and when the have nots- in terms of having not the modern conveniences and luxuries- are offered an opportunity to become haves, the end result is a foregone conclusion.

The old people who value their way of life are never the less quite often in real need as as they grow even older, and allowing the pipelines to cross their land is their only real hope of getting the things they need.

Out of a hundred young people there might be a dozen or two dozen at most who will choose to pass up the goodies the oil companies , the provincial governments, and the Canadian federal government will offer in exchange for a right of way for an oil pipeline.

After a while , a large enough percentage of of the First Nations people will want the goodies bad enough to force the holdouts to go along.

A showdown in the court system probably won’t be necessary but if it comes to that, the rest of the Canadian people will find a way to force the pipelines thru anyway.

I know it sounds very cynical of me, but laws and treaties were made to be broken when enough people want them broken.

Here’s something that just hit my news feed from

faux news :

http://www.foxbusiness.com/industries/2014/01/16/canada-loses-patience-on-keystone-xl-tells-us-to-decide/

The only surprise is that Public support in Canada for the Keystone seems r to be slipping but no reasons were given for the slippage. Maybe the People there ares content to see the oil shipped by train , which is working for now at least, so as to avoid a fight with the First Nations over the right of ways for new lines inside Canada.

OR maybe they’re just running short of patience and ready to say to hxxl with Obama and build pipelines themselves.

But there’s one thing I’m convinced of until I see some very hard proof otherwise; they’re not going to walk away from all the goodies that the oil will buy for them. It will get to market one way or another.

F-150 Sheds 700 Pounds as Ford Plans to Show, Not Tell

By Craig Trudell, Bloomberg, Jan 13, 2014 3:19 PM ET

Ford says more cars are not the answer to cities’ problems

By Robert Wright in Detroit, FT.com, January 14, 2014 6:20 pm

Ford is a big enough and capable enough company to build almost anything conceivably related to transportation except maybe stuff such as large aircraft or ships and AN y really good top level manager should be looking twenty thirty or forty years ahead.

It would be foolish for motor vehicle company management to actually say “peak oil” out loud in a public place, but the action of all the larger manufacturers speak a lot louder than their lack of worlds in this respect.

It’s not just fear of environmental legislation that’s driving them to electrification , extra light designs, fuel cells and downsizing!

There’s no reason Ford shouldn’t build street cars or passenger rail cars if the market for them expands to the point the company sees an opportunity to build them in quantity; most of the assets material and human are already in place.

It does s seem obvious to me that barring collapse the cities of the world are going to grow larger and larger and traffic congestion has already gotten so bad a car is almost worthless already in many cities, never mind the possibility that affordable fuel for it might be scarcer than the proverbial chicken teeth.

But I do often really wonder why people actually need to move around so much within cities.

Maybe in the future we will have cities where it’s easy for people to live and work and shop and play within a very limited area and solve most of there transportation issues by eliminating the need for most transportation.

There’s really no need for a doctor who wants the city life style to live ten miles from the hospital where he works if he’s a renter; the hospital amps of the future may very well include professional housing in a way reminiscent of the way coal companies used to provide company housing for miners- within walking distance.

Covered car free bike and pedestrians paths may be the future , alongside the more obvious subways and streetcars of course. The doctors housing on such a campus so provided with covered car free paths or lanes would need be only close enough t for a Segway or a bicycle- probably an electrified bicycle at 5that , meaning as much as a five mile bike ride could be as fast or faster than using a subway or street car door to door and much faster than a car in heavy traffic.

Minisplit Heat Pumps and Zero-Net-Energy Homes

What we know, what we wish we knew, and an invitation to readers to ask more questions

Posted on Jan 9 2014 by Marc Rosenbaum , greenbuildingadvisor.com

Robert Dumont’s Superinsulated House in Saskatoon

One of the superinsulation pioneers behind the Saskatchewan Conservation House built a house for his family in 1992

Posted on Dec 24 2013 by Michael Henry, greenbuildingadvisor.com

So much wealth wasted burning NG and heating oil for heat, just to have it radiate or escape from the building envelope. When it comes time to point fingers look to the builders/developers who built our dismally inefficient housing stock.

Australian Heat Wave

Heatwave Strains Australia Power Supply With Mercury Set for 115

By Jason Scott and Ben Sharples, Bloomberg, Jan 15, 2014 8:37 PM ET

Have to laugh, to keep from crying, at the perverse anthropogenic positive feedback that arises from global warming. As it gets hotter we’ll burn more fossil fuels, for example coal in Australia and oil in Saudi Arabia, to keep cool.

There is a certain rich irony that so soon after having elected Tony Abott (Australia’s climate change denier Prime Minister) the Australian electorate are being subject to these record breaking heat waves. Having recently spent a few weeks in Australia I have come to the conclusion that the only way the public there is going to learn the harsh truths about AGW is to be blasted by its effects, year after year. When cities such as Adelaide regularly start getting subjected to 50C temperatures (and are thus rendered effectively uninhabitable in summer) then they might learn that voting for politicians who are in the pockets of the mining mafia is perhaps not in their best interests. By then it will probably be too late.