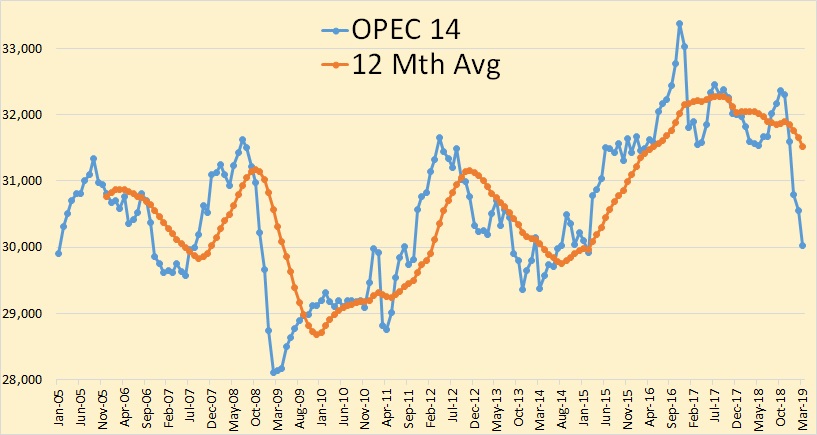

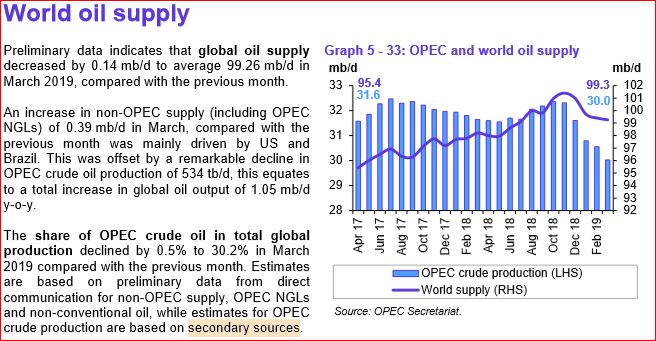

The below OPEC charts were taken from data in the OPEC Monthly Oil Market Report. All data is through March 2019 and is in thousand barrels per day.

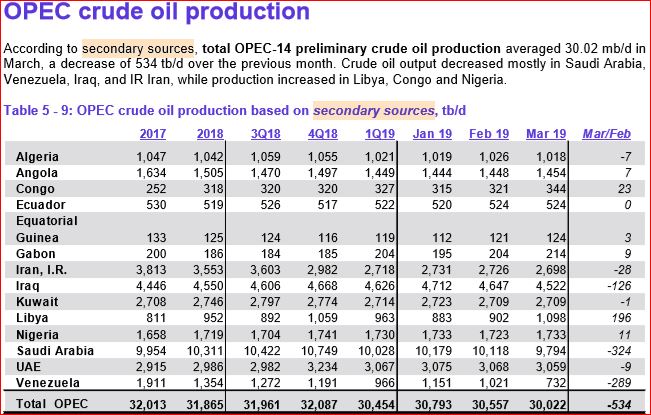

There was another big decline in OPEC production in March, down 534,000 barrels per day.

The decline was mostly Saudi Arabia, Venezuela, and Iraq.

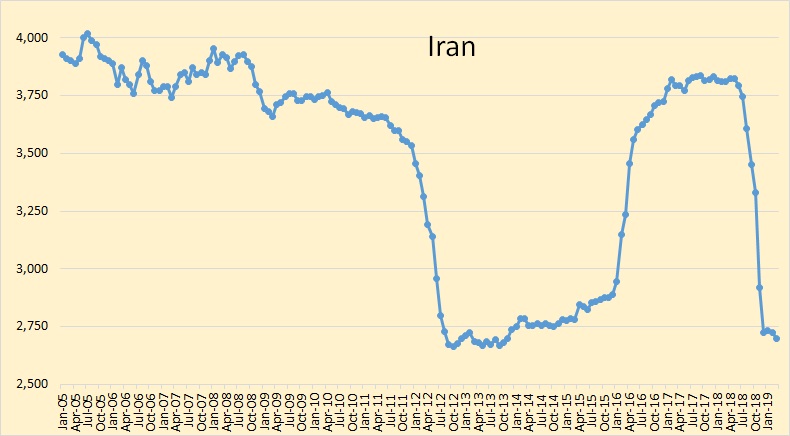

Iran, Libya and Venezuela are exempt from quotas. Everyone except Saudi Arabia are near their quota. Saudi is over half a million barrels per day below their quota.

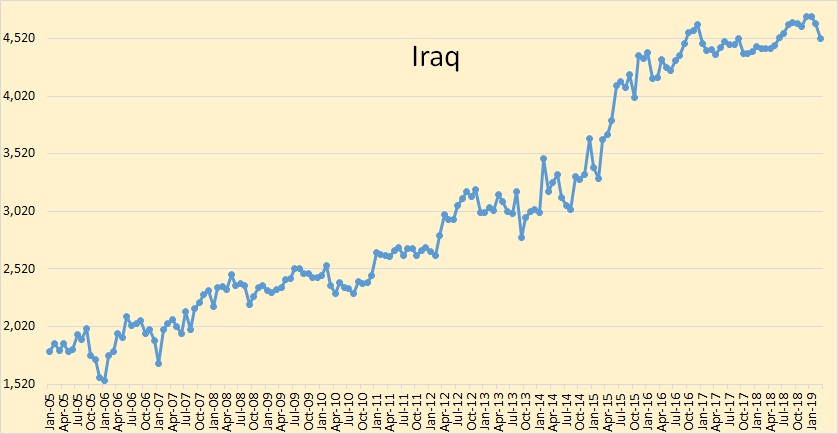

Although Iraq was down 126,000 bpd in March they are still at their average for the last two and one-half years.

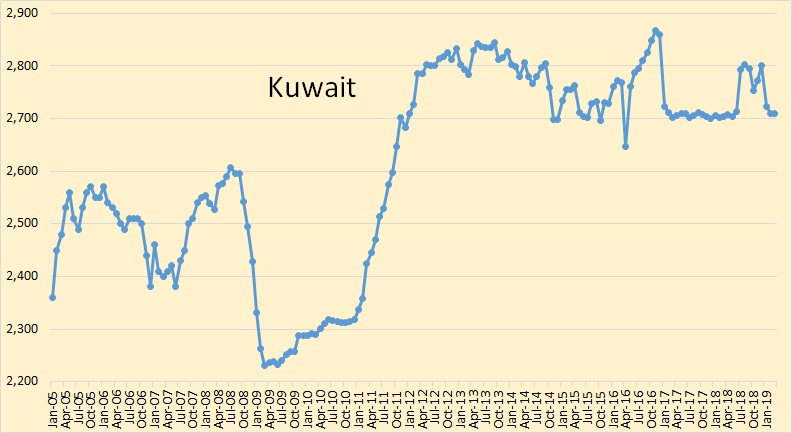

I think Kuwait is at, or very near, peak production except for their share of the neutral zone. That is shared 50/50 with Saudi Arabia. Their share would be about half a million barrels per day. It is shut down because of a political disagreement between the two countries.

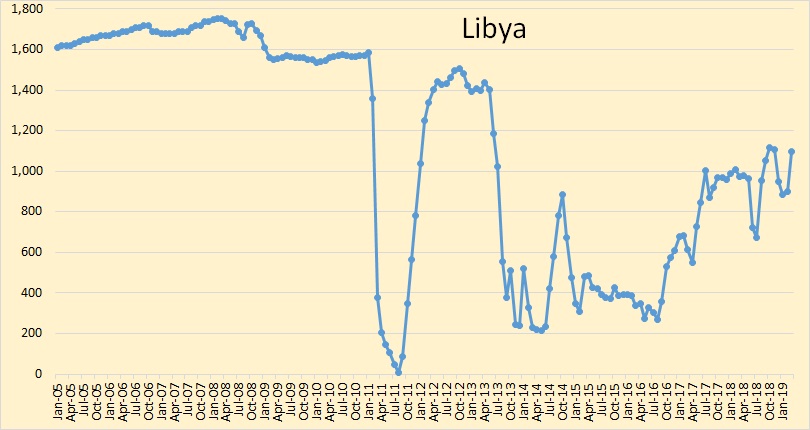

Lybian production was up 196,000 in March. They will likely be down again in April as fighting there has escalated.

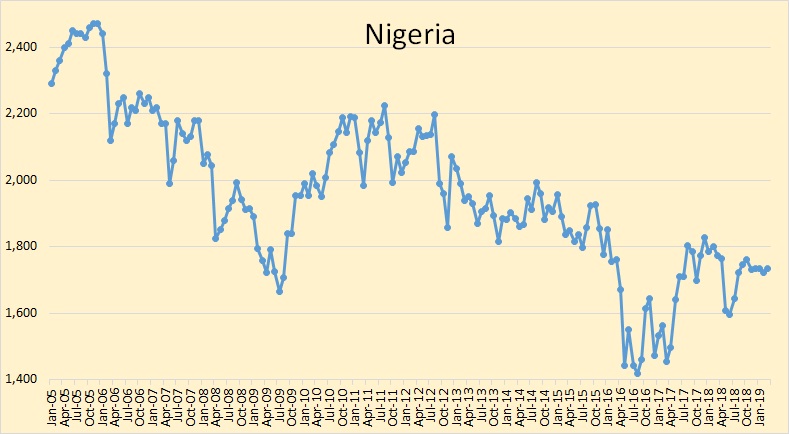

Nigeria appears to be in slow decline. They are still producing well above their quota.

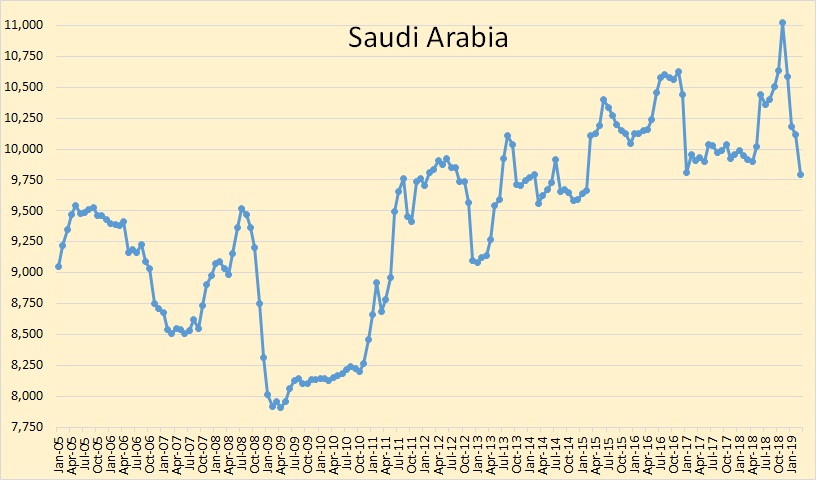

Saudi Arabia is another story altogether. They are over half a million barrels per day below their quota.

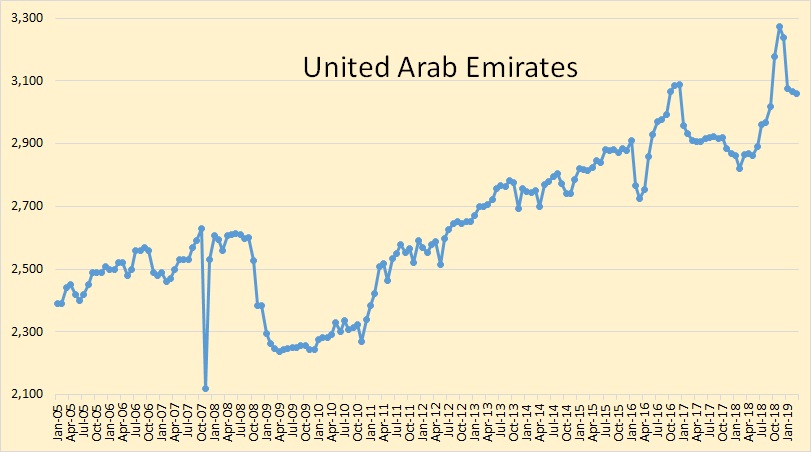

The UAE is producing slightly below their quota. The October, November, December spike in production was obviously a heroic attempt to increase their quota as they are still producing well above their average before that three month period.

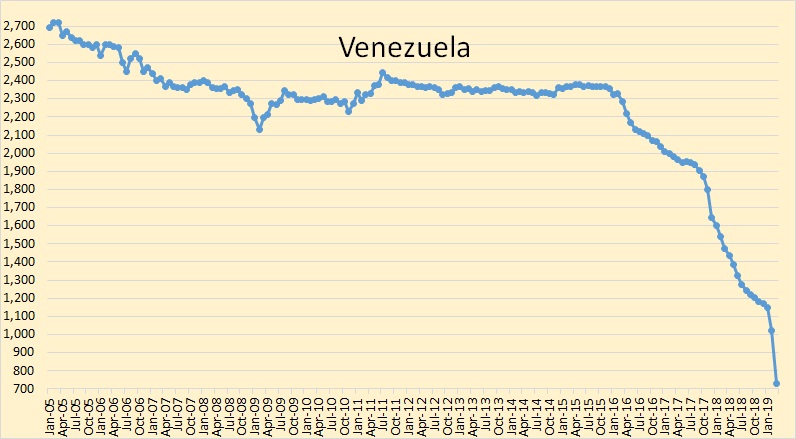

Venezuelan production was down 289,000 bpd in March. The blackouts there hit them hard. I would be afraid to even guess where they are going from here.

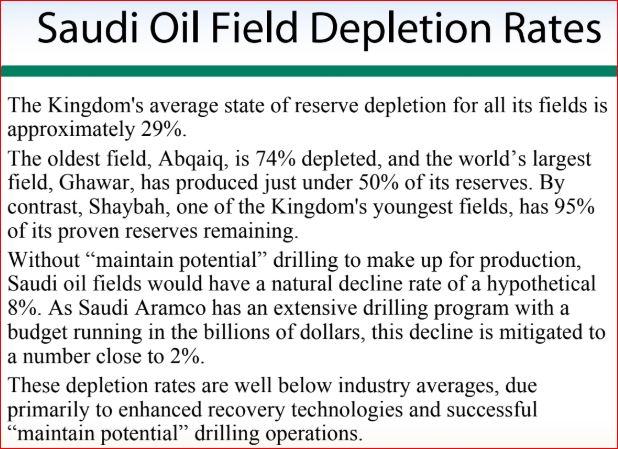

Concern Saudi Arabia’s Oil Reserves

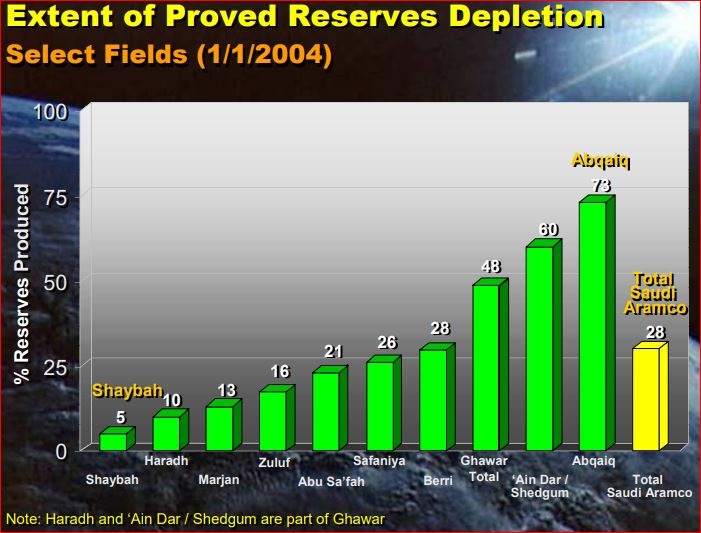

In February 2004 Saudi Arabia published a slide PDF stating, among other things, their current depletion status. But first, I want to post a bit of their history.

Crude Oil Supply Scenarios: Saudi Aramco’s Perspective

Saudi stated, fifteen years ago, that Ghawar was 48% depleted and the Ain Dar/Shedgum section of Ghawar was 60% depleted.

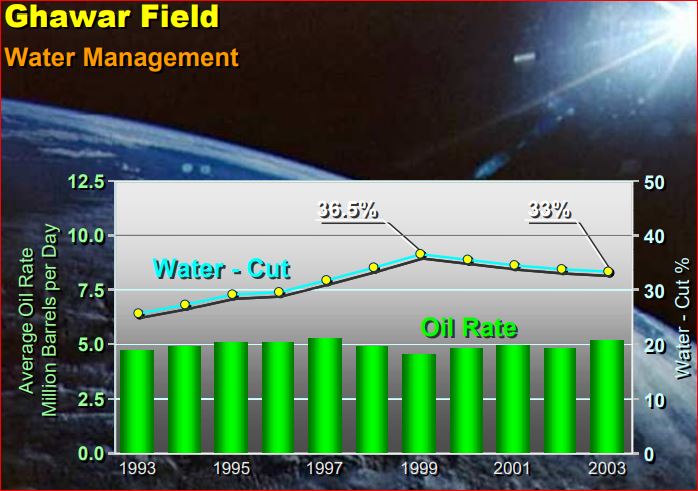

They stated, in the same PDF, that they had gotten their water cut under control. But what happened, around the year 2000, that resulted in this improvement?

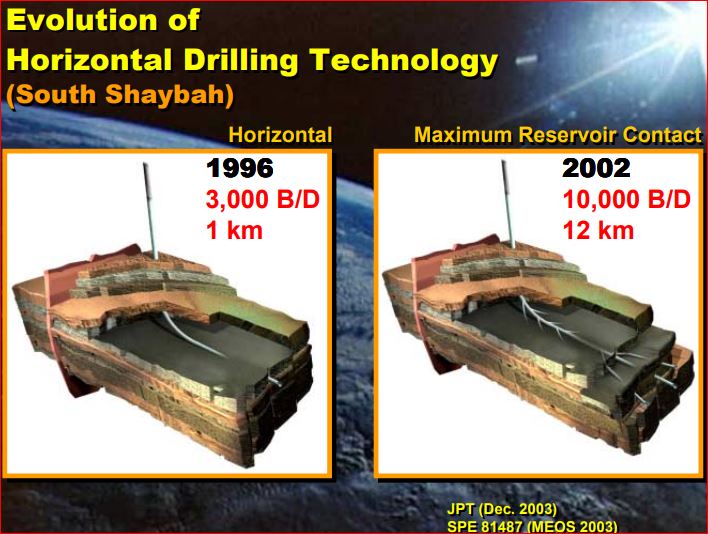

Injected water was rising fast in their reservoirs. They began to plug vertical wells just below the oil line. And they began an infill drilling program with new horizontal wells, then horizontal MRC wells, that pulled the oil from the very top of the reservoir.

It was not until 2005 when the infill drilling program began in earnest. It slowed down in 2008/2009 when prices collapsed. But it picked up again as prices recovered and they needed more infill wells to keep production up.

Saudi stated such in this remarkable PDF they posted in November 2006:

Saudi Arabia’s Strategic Energy Initiative: Safeguarding Against Supply Disruptions

The above statement is really astounding. One needs to read it carefully to fully understand the claims made here. They are saying that their fields have a natural decline rate of 8%. But with their massive infill drilling program, they have gotten the decline rate down to almost 2%. Their new horizontal wells are pulling the oil right off the top of the reservoir so they get less water. They are pulling the oil up a lot faster so their decline rate drops to almost 2%.

But the most astounding thing here is that last sentence: These depletion rates are well below industry averages… Now just a cotton picking minute here. We are talking decline here, not depletion. They are entirely two different things. If you suck the oil out faster, causing the decline rate to decrease, you have to be increasing the depletion rate.

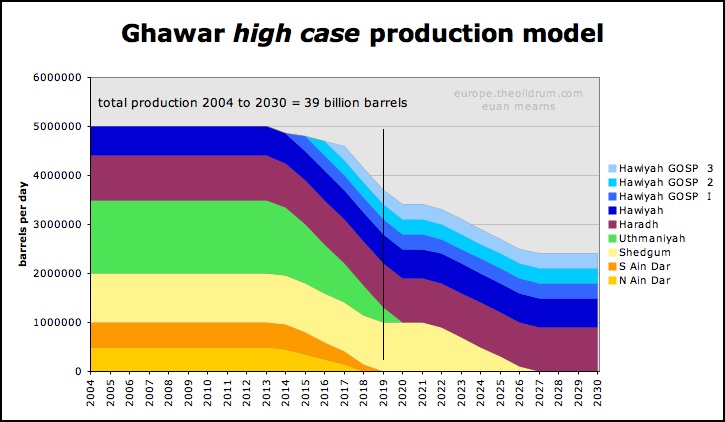

Euan Mearns posted in April 2007, using 2004 data:

GHAWAR: an estimate of remaining oil reserves and production decline

Euan posted two scenarios, base case and high case. The high case hit the nail on the head, 3.8 million barrels per day in 2019.

It is important to note that Ghawar’s older northern fields have a much higher decline rate. Also Ghawar showed no decline until around 2013. This is because they were not producing the field at full capacity. Then around 2013, the depletion caught up with them and, as they admitted, they began producing at full capacity.

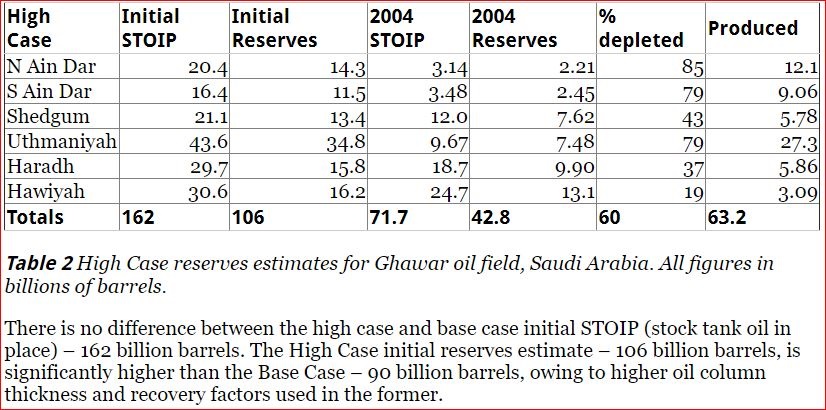

Here is the data Euan used to make his assessment. He had Ghawar at 42.8 billion barrels of recoverable reserves in 2004. If Euan was correct then Ghawar likely has about 18 billion barrels of recoverable reserves left.

Ghawar’s top three fields have been producing for 70 years. Why is anyone surprised that they are now in serious decline?

A few days ago Saudi Aramco has published a bond prospectus, the first ever since the total Saudi takeover of ARAMCO in 1980. There have been several reviews of this prospectus on line:

From Bloomberg

The biggest Saudi oil field is fading faster than anyone guessed

And from OilPrice.com

Aramco’s Mythical Ghawar Field Could Be Its Weak Spot

The online version of the prospectus is quite long, 235 pages plus a 10-page introduction. But it is extremely revealing. It has generated a lot of controversies. For instance, on page 21 we find this, bold mine:

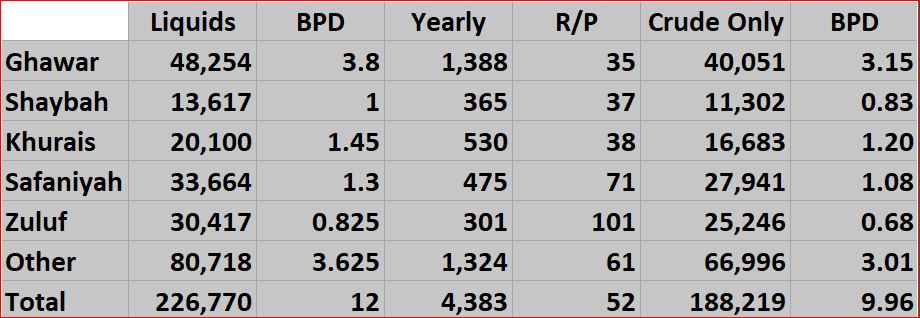

Based on the initial 40 year period and 20 year extension of the Concession, as at 31 December 2018 the Company’s reserves were 256.9 billion barrels of oil equivalent (sufficient for proved reserves life of 52 years), consisting of 201.4 billion barrels of crude oil and condensate 25.4 billion barrels of NGLs and 185.7 trillion standard cubic feet of natural gas.

Their claimed proven reserves have been downgraded by 10 billion barrels but that is not all. Those reserves are BOE. That is crude oil, plus condensate, plus other liquids, plus natural gas. Crude + Condensate is only 201.4 billion barrels. Assuming their percentage condensate is 5.5%, a very conservative estimate, that would mean, that they are claiming, their “crude only” reserves are around 191 billion barrels. So the below reserves what Saudi Arabia claims they have, in billion barrels.

BOE ———————– 256.9

Total Liquids ———– 226.8

Crude + Condensate – 201.4

Crude Only ————- 191

On page 88 we find this:

Notice the last line, MSC or maximum sustainable capacity.

MSC refers to the average maximum number of barrels per day of crude oil that can be produced for one year during any future planning period, after taking into account all planned capital expenditures and maintenance, repair and operating costs, and after being given three months to make operational adjustments….

Based on the initial 40 year period and 20-year extension of the Concession, as at 31 December 2018 the Company’s reserves were 256.9 billion barrels of oil equivalent (sufficient for proved reserves life of 52 years).

In their definition of MSC they say crude oil but in their 52-year projection they use their “combined reserves” figure, (BOE), so which are they talking about. If we multiply 12,000,000, (their MSC), times the number of days in 52 years, we get a number close to 227 billion, their “combined reserves” figure. So their MSC of 12 million barrels per day is, very likely, total liquids. However, they mix their data so often it is hard to tell.

On the same page they say:

The Company generated revenues by utilizing the spare capacity provided by MSC of SAR 133.0 billion ($35.5 billion) from 2013 to 2018.

In their own words, they have been producing at maximum sustainable capacity since 2013. Let’s see what the numbers say. According to their data above, LNG is 11.72% of their reserves, and we assume, of their production. So if we assume condensate is at least 5.3% of production, (in the US it’s between 8% and 16%), then we add 17% to get Saudi total liquids production.

So yes, Saudi has been producing at maximum sustainable production, at least for the last four years. That is not to say that they are currently producing at MSC levels.

I have created the below table using 17% for Condensate + NGLs. All data except the R/P ratio is in million barrels. Understand these liquids reserve numbers are Saudi’s own figures, not my estimate. The “crude only” numbers are assuming condensate plus NGLs are approximately 17% total liquids.

Dr. Mamdouh Salameh has commented on this prospectus. I thought his comment worthy reposting here. And I might add I agree completely with his conclusions. Bold mine.

Dr Mamdouh G. Salameh is an international oil economist. He is also a visiting professor of energy economics at the ESCP Europe Business School in London. Dr. Salameh holds a PhD in Economics specializing in the economics and geopolitics of oil and energy.

There was a lot of fanfare about Saudi Arabia created by investment banks which are destined to benefit hugely from Saudi Arabia seeking to launch a major bond issuance to help finance its acquisition of 70% stake in Saudi petrochemical giant Basic Industries Corporation (SABIC).

With supposedly 266 billion barrels (bb) of proven reserves, exports of some 7 million barrels a day (mbd) providing an annualized revenue of $171.19 bn at current oil prices and production costs of $7.5 per barrel before tax, Saudi Aramco could to all appearances be confirmed as the world’s most profitable company. However, appearances could be deceptive.

To help a successful bond issuance, Saudi Aramco has for the first time since it has become a fully-owned Saudi company issued a prospectus in which it shed some light on its finances on what is being touted by investment banks like the discovery of the secret of long life.

However, the prospectus left many crucial questions unanswered. Prominent among them is the real size of Saudi proven reserves and the production levels of its very aging oilfields which underpin its current production.

Four giant oilfields Ghawar, Safaniya, Hanifa and Khafji (shared with Kuwait) all of which are more than 70 years old and which are being kept producing by a huge injection of water, have over the years accounted for more than 90% of Saudi oil production with Ghawar accounting for 50% of the total.

Now the Saudis are saying that Ghawar which is the core of Aramco’s oil production and which has been for years contributing 5 mbd to Saudi total production, can only produce 3.8 mbd. If this is the case, then the persistent reports about depletion of reserves which have been circulating for years about Ghawar must be true. It is fair to suggest that the same depletion would have also affected the other aging oilfields. This is supported by the fact that Saudi oil production peaked in 2005 at 9.6 mbd and has been declining since. In a nutshell, Ghawar could be the Achilles heel of Saudi oil production.

This also gives the lie to Saudi claims that they have a production capacity of 12 mbd meaning a spare capacity of 2 mbd.

Meanwhile, the persistent question marks about the actual size of Saudi proven reserves will continue unabated until a truly independent audit is undertaken.. Far from having proven reserves of 266 bb, I estimated the remaining Saudi proven reserves at no more than 70-74 bb. By adding Saudi production since the discovery of oil in 1938 till now (for which we have figures) and then deducting them from Saudi claimed proven reserves along with an annual depletion rate of Saudi aging fields averaging 5%-7% for the same period, my calculations came to around 70-74 bb of remaining reserves.

The fact that Saudi Arabia’s proven reserves remained virtually constant year after year despite sizeable annual production and a lack of major new discoveries since 1965 is due to the Saudis increasing the oil recovery factor (R/F) and the oil initially in place (OIIP) to offset annual production. The Saudis have been declaring an R/F of 52% or even higher when the global average is 34%-35%. They have also increased the OIIP from 700 bb to 900 bb on the basis of Saudi Aramco projecting new discoveries which are yet to be discovered.

And for a different opinion from Michael Lynch:

Declining Production At Saudi Arabia’s Largest Oil Field Is Not Cause For Concern

Why did Ghawar’s production decline? Since the field still has 48 billion barrels of proved reserves (according to Aramco’s numbers), maintaining 5 mb/d should be technically easy. However, the field is not a stand-alone operation; Aramco has a choice of investments among numerous fields, and explicitly chose to add capacity elsewhere, as proven by the fact that the national capacity is 12 mb/d, showing no signs of decline.

Got that? Ghawar is declining simply because ARAMCO chose to move production elsewhere. Lynch is right if Ghawar still has 48 billion barrels of oil. Euan Mearns estimated that Ghawar had 43 billion barrels of recoverable reserves in 2004. If that is close then Ghawar should have about 18 billion barrels of recoverable reserves left.

Michael Lynch and Robert Rapier are among a dwindling few oil people who still believe Saudi Arabia’s absurd reserve numbers. After this Saudi prospectus, it is likely that the vast majority now agree with Dr. Salameh. However, it is possible that Robert could have revised his opinion after reading the Saudi prospectus.

And another contrary opinion from climate change denier site WUWT

No… “The biggest Saudi oil field is [NOT] fading faster than anyone guessed”…

The author of this article, David Middleton, makes the absurd claim, “The MSC rate is more of a minimum rather than a maximum. That sentence just shows the absurd levels of twisted logic deniers will go to in order to deny the obvious.

There are many replies to this WUWT post, pro, and con. Many of the replies are from people who actually worked, or talked to people who worked on Ghawar. I will quote one of them, Mr. Glen Morton.

Conclusion:

In 2004 and again in 2006, we had hints, from Saudi officials themselves, that Saudi oil fields were beginning to have serious water cut and depletion problems. Now with this bond prospectus, we have the coup de gras. Ghawar and the majority of Saudi’s other super-giant oil fields are in serious decline.

The idea that Saudi still has 266 billion barrels of proven reserves must now be regarded as pure fiction. The Saudis themselves are no longer supporting that figure. They are now saying 256.9 billion barrels of oil equivalent. That included condensate, NGLs, and natural gas. Their oil reserves, they say, are 201.4 billion barrels of C+C. But even those numbers are absolute fiction. They have been lying for years so why should we start believing them now. Then they say they got their decline rate down to almost 2%. But then they confuse things by claiming this is also their depletion rate.

My estimate of Saudi reserves. I agree with Dr. Mamdouh Salameh, Saudi likely has between 70 and 74 billion barrels of recoverable reserves.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

I am a geophysicist and former exploration director for a large independent oil company. At one time I had the top web page on Ghawar on the internet and have studied this field extensively. At one time, I was in charge of reservoir simulation for my company. Every seminar and meeting I went to I talked to people who had worked Ghawar doing reservoir simulations. Absolutely everyone of them said the field didn’t have the reserves people thought it did in the West. In 1996 at the SEG convention, a Saudi Aramco employee gave a paper showing the water level for northern Ghawar and it was nearly at the crest of the field. Yes, the southern part of Ghawar had less permeable and porous rocks than the north and that was developed in a drilling mania in the first decade of this century. I for one do not think you are correct about Ghawar not declining fast. One guy told me that they had drilled a well for a core below the water level to see how much residual oil was left in northern Ghawar. Because of the vugular nature of the rock, there was only about 10% residual oil saturation. I for one find the Bloomberg article consistent with everything I know about Ghawar. I think Ghawar’s problem is why the Saudi’s were unable to ramp up production fast enough to kill off shale in 2014–go look at their production and it gradually rises from something like 9.5 million a day to 10.5 a day over a period of a year or so. That is my recollection of that curve. There was no step function in Saudi production.