Guest Post by George Kaplan

Brazil is a major oil producing country, but in 2016 was still a net importer, though imports dropped significantly and they have been a slight exporter overall so far this year. It is one of the few countries that have consistently grown production over recent years, and possibly the only non-OPEC country that will show overall growth of conventional crude in the ten years to (say) 2022.

Production

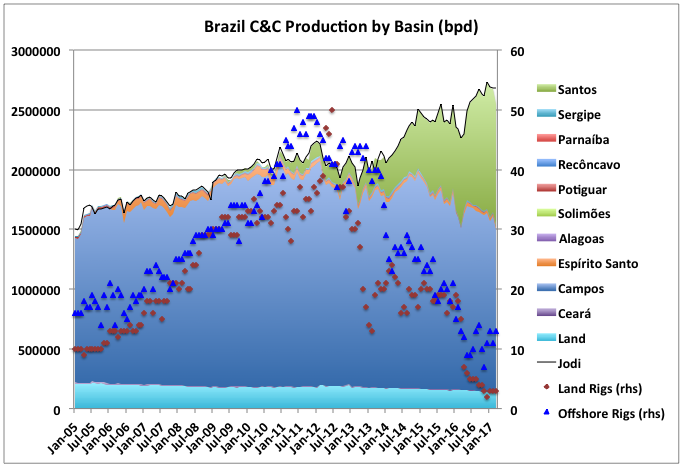

Brazil ANP or anp (Agência Nacional do Petróleo, Gás Natural e Biocombustíveis) publishes Excel files for monthly production on all wells. In theory it should be easy to extract field data from these, in practice not so much. The files are downloaded from a database but not always consistently, sometimes in field units sometimes SI, sometimes one month per file sometimes more, around 2010 onshore and offshore was split but naming conventions weren’t always followed, handling of wildcat wells seems a bit arbitrary, and spelling conventions can change. However after more effort than I expected I did download the data and split it by basin and field.

The total production fits Jodi data well except for three periods: 2005 when the reports stated, and doesn’t make much difference; 2010 when ANP split offshore and onshore reporting and the well files are a complete mess; and 2017, which may indicate that some of the data is revised (this should become evident as more releases are made over the next months).

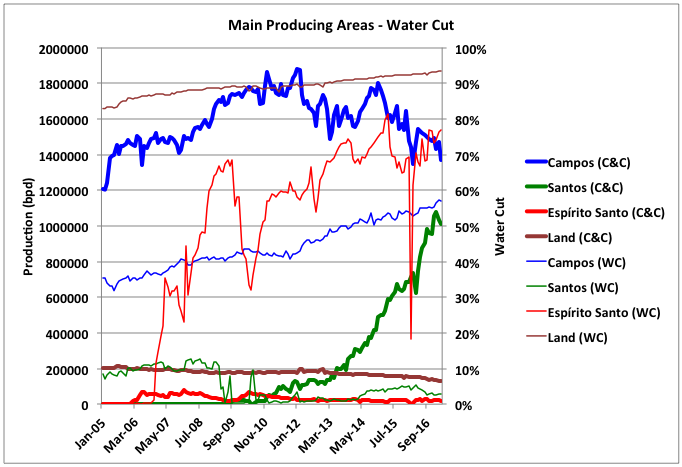

Land based production is a small component at about 130 kbpd. It averages over 90% water cut (and increasing) and is in long-term decline at over 9% per year (which also appears to be increasing recently). Petrobras is trying to sell off some of their holdings.

The gas and oil rigs combined for onshore and offshore are also shown. The majority is oil rigs for both off and onshore. It is interesting that their numbers started to decline in mid-2012 when oil prices were high and rising. I don’t know the reason – could be to do with the financial and political problems in Petrobras, or associated with geology (i.e. a lack of exploration targets and development projects, which is probably the case for onshore drilling), or a move from many smaller shallow fields to fewer deep and ultra -deep rigs offshore.

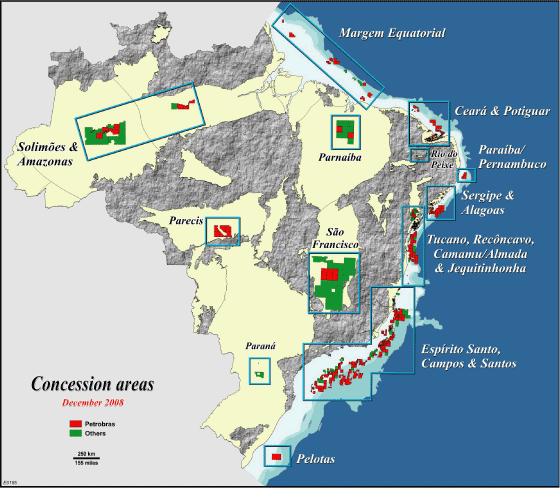

The locations of the basins are shown here:

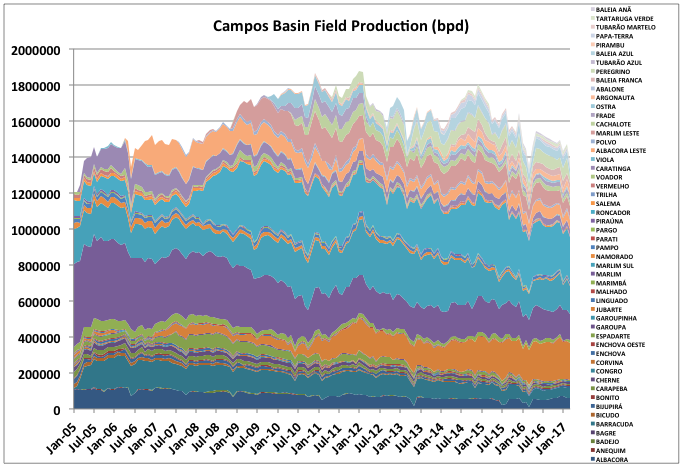

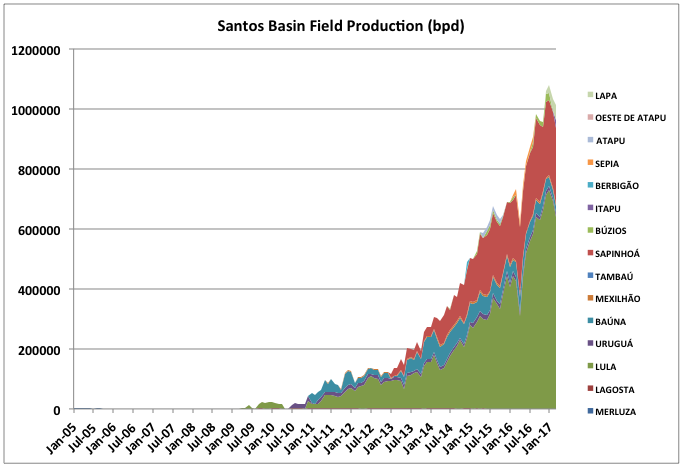

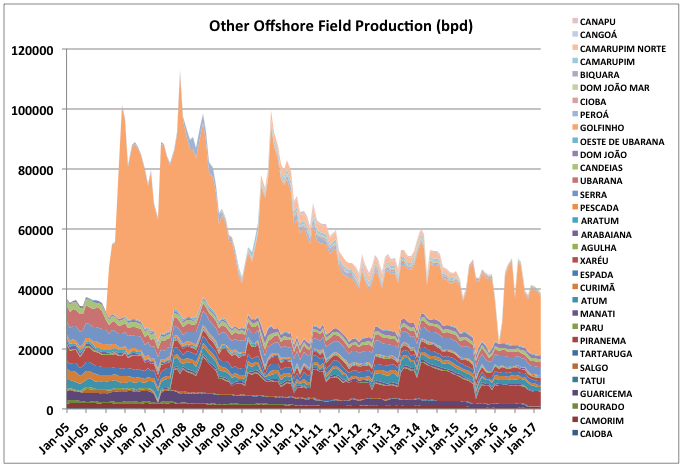

Most of the production to date has come from the Campos basin (Campos actually just means fields in Portuguese). It and Espirito Santo are older basins now in decline at about 9% per year, combined. The big recent additions have been in the Santos basin, particularly Lula (which was Tupi at one time) and Sapinhoá. Note that gas production is not considered here though there are significant gas or gas/condensate fields in these basins, such as the Jupiter field. The charts below show C&C production from individual fields within Campos, Santos and others offshore. There isn’t enough detail to show much of interest, but they are quite colourful.

Most of the offshore production comes from large FPSOs, but there are shallow water platforms in smaller fields. Each of the larger fields in the charts above would have one to three FPSOs. Historically the FPSOs seem to start declining after about a six to twelve-month ramp up period. There are few showing any long plateau periods, though this may be different for Santos. Decline rates can vary from 5% up to 20% per year – i.e. to maintain production in a basin new FPSOs need to be continually bought on line.

Water cut seems to be the biggest impact on decline rates. Campos and Espirito Santo started to decline once water cut hit 50%, and it is still rising in both. Santos fields seem to be low in water at the moment.

Reserves

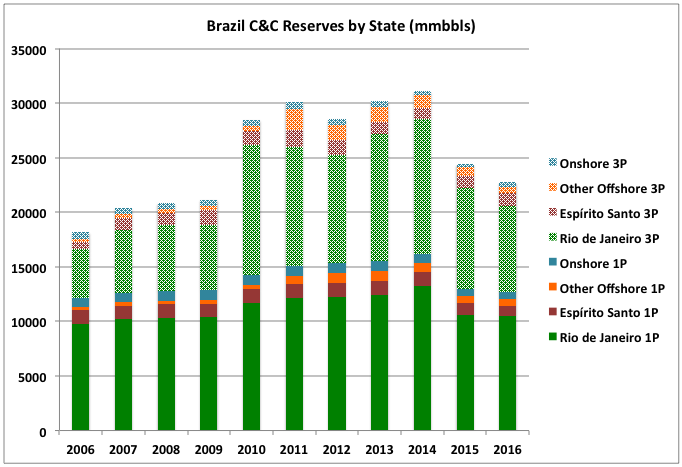

ANP provide reserve data following SPE guidelines, however they seem to give only 1P, 3P and 1C numbers in their bulletins – i.e. providing upper and lower limits but not an expected 2P number. They give all numbers to six significant figures, so I guess they must be right. The stacked chart below shows the history for 1P and 3P crude and condensate reserves by state. Almost all the reserves are offshore in Rio de Janeiro and Espirito Santo States – i.e. the Campos and Santos basins. Note I could only find 2016 data by basin, some basins (e.g. Campos) split across two states so I pro-rated numbers bases on 2015 figures – the totals remain as given by ANP.

There was a big hit to reserves in 2015. This may have been partly price related but Forbes reported Petrobras as saying “…decline in reserves was due to other factors, primarily revisions of well estimates at its pre-salt sites offshore.” In the context of the article the word “other” used there makes no sense, so there’s still some ambiguity.

Future Projections

From the 2016 reserves bulletin I estimated remaining recoverable reserves assuming 97% of 1P (which equals P1) and 50% of P2 plus P3 (which equals 3P minus 1P), as below. I didn’t use 1C numbers but include them to show there isn’t a huge upside there (these should be less than 10% probability of production). Numbers shown are mmbbls, converted from Mm³ used in the ANP report.

| 1P | 3P | 1C | 2P (Calculated) | |

|---|---|---|---|---|

| Santos | 6,116 | 12,621 | 1,945 | 9,185 |

| Campos | 5,741 | 8,733 | 2,479 | 7,065 |

| Total | 12,666 | 22,742 | 4,579 | 17,324 |

| Others | 809 | 1,388 | 155 | 1,074 |

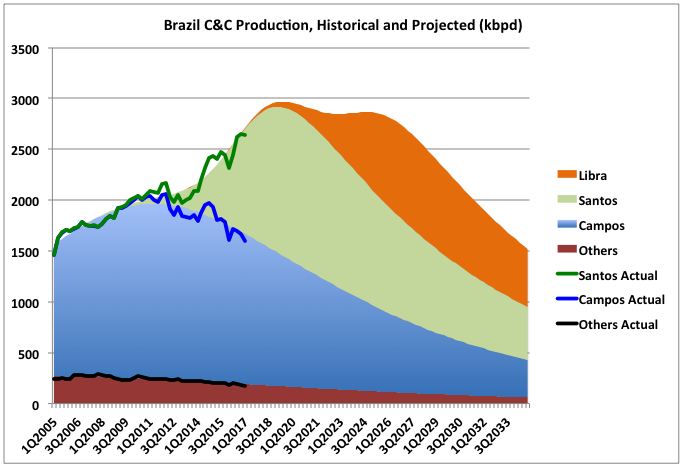

I fitted Verhulst equations for each of the three categories (Campos, Santos and others) based on the production data from 2005 till now, and ensuring the remaining production (out to infinity) equaled the numbers calculated above. I also added a guess at Libra production assuming 6,000 mmbbls (a bit less than the 8,000 sometimes reported, but then there hasn’t been any production yet and it looks like their other pre-salt fields might not be as good as originally thought, and some of the reserves are already included in the ANP Santos numbers). To match the profile shown they would need to be approving major FPSO and drilling budgets next year, so the profile shown may be unrealistically aggressive as the Libra extended well test project hasn’t even started yet.

(Sorry about the random changes in units.)

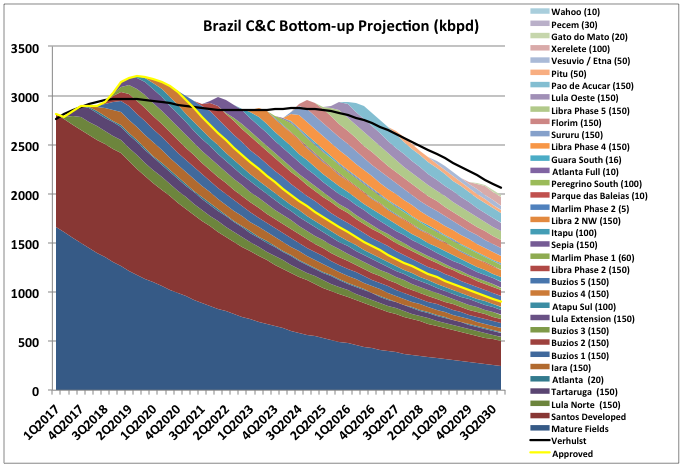

An alternative view of the future is to look at bottom up projection based on the projects identified by the E&P companies. Below shows such a scenario. Only the projects up to Bezios 4 have been approved and are under construction (plus possibly Peregrino, although I don’t think there has been a formal FID). After that the capacities (shown as kbpd nameplate after the project name) and start up date are guesses. Most of the projects are in Santos but some (e.g. the Marlim revamp) are in Campos. Some have been cancelled, so I’m assuming these would be revived given high enough prices.

Meeting this schedule for new projects in 2020 to 2023 is now unlikely. For Campos Petrobras use cloned FPSO designs that can be built in around three years, but these may not be suitable for the need for gas reinjection and ultra deep wells in Libra. They currently have higher priorities than development, in particular reducing debt (their interest is $6 billion per year), so other E&Ps would need to get involved. The developments also need latest generation drilling rigs and for Libra would be waiting for initial extended test results from the pilot projects. Petrobras vessels also have a history of major lost time incidents; only one or two such would knock production down considerably. While cloned designs reduce costs they can incur common mode failures; for example as all the gas injection risers on recent FPSOs seem to be seeing (pretty much the highest risk component on any offshore development) and such failures may also produce large downtime across several facilities.

Near term these projections are in-line with IEA (from OMR, June 2017): “In all, Brazilian production is forecast to increase by 190 kb/d in 2017, with gains ramping up to 260 kb/d in 2018.” The EIA STEO also has projections for Brail, but includes ethanol, which is highly seasonal and makes the numbers difficult to follow.

For longer term the new Santos pre-salt fields are the big hope. Lula is in production and Libra is being developed. Libra was discovered in in 2010 and may have up to 8 to 12 Gb recoverable, but it is expensive oil: ultra-deep, difficult wells, 40% carbon dioxide content in sour gas. The high CO2 means the gas has to be reinjected and provides pressure support, but even with this, extensive gas treatment facilities are required on board the production facilities. A consortium of companies won the rights to development, comprising Petrobras (the operator), Shell, Total, CNPC and CNOOC, They are starting with smaller developments to find the problems. To save money, I’ve seen that they are looking at combined water and gas injection, which may not be ideal for the reservoir and introduces hydrate risk.

There have been reports that there may be over 100 Gb other oil in the pre-salt play (unrisked), but there is little current exploration – in addition to the price collapse, possibly because of Petrobras finance and corruption issues, or waiting for results from the initial Libra production tests or for help from outside interests (e.g. Statoil, ExxonMobil, Shell, Total, CNOOC, Repsol etc. are invested or looking to invest there). There have been other fields discovered in Santos, e.g. Iara and Iracema in 2008/2009, but there were also a number of high profile dry wells (i.e. expensive and operated by IOCs) in the basin in the years between the Tupi and Libra discoveries, and not much positive news since Libra, with some leases being given up even in the high price years. In addition the Santos basin geology is somewhat mirrored offshore Angola in the Kwanza province, which has proved pretty barren (and expensive) for the E&Ps. BP recently took a $750 million write-off against dry wells and lease costs there and have given up all leases. Other majors, including Statoil and Total, haven’t done much better. Cobalt (Cameia) and Maersk (Azul) seem to have the only announced discoveries there, but there’s been little news on developing them; Cobalt is in litigation and Maersk has gone very quiet on Angola in general. There are differences with Brazil though, e.g. Santos is deeper and would have a better chance to seals the oil traps.

So overall does this indicate a coming Brazil peak? Probably yes near term, say around 2019/2020, but only more exploration and development will tell whether that could be exceeded again longer term. Statoil plan to be drilling wildcats later this year, the 14th bidding round has four significant offshore blocks up for lease starting in late July, but such things seem to go very slowly in Brazil: another Libra or another Kwanza – who knows, until they drill?

421 responses to “Brazil: Reserves and Production”

I wonder what happened to that dood who posted here some detail on the software for seismic imaging past salt domes, which in the past had prevented such things. The focus was Brazil in what he was talking about.

Brazil’s oil consumption was down last year amid their political disaster and an ongoing GDP recession dating to 2014 (appears derived from a Volker-like 10+% interest rate CB-imposed to crush inflation, now down to 4%). That is pent-up demand coming. GDP growth was 1% Q12017, with the CB cutting rates, most recently May 2017 (albeit “down” to 10.25%).

Oil is 8% of GDP. GDP dominated by their powerhouse agro industry in the Matto Grasso. When oil scarcity starts generating wars and starvation, Brazil is where people should go.

It was not long ago that the Matto Grosso was one of the last truly wild places on earth. Explorers often did not come back out of there.

http://www.pbs.org/wnet/secrets/lost-in-the-amazon-about-this-episode/808/

Oil is 8% of GDP. GDP dominated by their powerhouse agro industry in the Matto Grasso. When oil scarcity starts generating wars and starvation, Brazil is where people should go.

It’s Mato Grosso… and what makes you think Brazil will welcome all those starving refugees with open arms? Especially refugees of the ‘Gringo’ variety. Hey maybe they will limit immigration from certain countries and impose a travel ban! MBGA!

On the other hand Brazil has recently impeached one corrupt president, tried and convicted a previous one, is in the process of trying a third and has been vigorously pursuing corrupt businessmen and politicians and putting them in jail.

However they do consider Health Care a universal right and it is written into the Brazilian constitution. Maybe the US could learn a thing or two from the Brazilians!

Hi Fred,

If I were a Brazilian, I would advocate sharply limiting immigration into my country, so as to better preserve it from the ravages of ill considered development.

I would also prefer to see the economy developed in such a way that the country is as REASONABLY self sufficient as possible in terms of manufactured goods, investment money, etc, so as to better preserve the environment.

There’s WAY MORE to be considered than just simple minded arguments about greater prosperity being associated with greater trade.

If Brazil winds up gut hooked on exporting agricultural goods, like a fish that has swallowed a baited hook, the result will be the destruction of what’s left of the Amazon rain forest, etc.

Forgoing so much international trade in agricultural products means less overall prosperity NOW of course but it can also mean a FAR HEALTHIER and FAR MORE PROSPEROUS Brazil a few years down the road.

How about translating MGBA into gringoese for those of us who don’t know the prevailing lingo ?

I am impressed with just about every thing I hear about Brazil, with a couple of exceptions. One is public corruption, but progress is being made in that respect.

The other is that a lot of people appear to be getting treated VERY poorly indeed, especially the original peoples who live in the wilder areas, and laborers on giant farms, but I am not very well informed about these issues.

Any reply placed over in the not petroleum thread will be appreciated.

Brazil is accepting the refugee flow from Venezuela, many of them native indians fleeing Amazonas state. They have 7000 at a camp near the border. I don’t have a head count for flows heading south, but two days ago Colombia reported 26 thousand Venezuelans crossed into Cucuta, the Maduro dictatorship lets them go bacause they are mostly poor people from Tachira, who have been fighting regime forces with a bit more muscle than Venezuelans elsewhere.

The Campos Basin was named after the town officially named São Salvador de Campos de Goytacazes about 350 years ago, these Indians are better known as the Goitacá nowadays. So the origin of the basin’s name comes from a town named “Sainted Saviour of the Fields of the Goitacá”.

Hi Fernando,

Can you point me to a source for data on Venezuelan output (annual data is all I need) for the Orinoco Belt?

At PDVSA they claim 1442 kb/d output in 2015 from Orinoco.

The strategic plan calls for 4000 kb/d by 2019 from Orinoco, this seems highly unlikely.

Do you know if they have been able to maintain Orinoco output at 2015 levels in 2016? Do you think the PVDSA estimate of 1400 kb/d in 2015 is overstated? And finally does 2000 kb/d from Orinoco by 2020 under an assumption that the political crisis resolved by 2018, seem reasonable.

I realize that the assumption that the political crisis is resolved by 2018 is not likely to be reasonable.

Thanks.

Dennis, there is no reliable data. A couple of years ago I saw two PowerPoint presentations by high level faja managers, and they didn’t show the same production curves. In other words, things are so shoddy even PDVSA managers can’t get their lies straight.

PDVSA “strategic plans” are never met. As regards conditions on the ground, a few hours ago the boys were laying out how to blockade PDVSA support bases, including those operated by foreign companies.

By the time this is over it’s possible Venezuela may look a bit more burnt down, because eventually the emerging resistance will start burning the wells.

Ok,

Do you have any guesses for Faja output 1000 to 1200 kb/d maybe in 2016?

No doubt your guess would be better than mine.

Would a rough guess maybe be OPEC reported output from secondary sources subtracted from the output reported by Venezuela and then multiply by 0.8?

There is an article speculating oil prices could go up $7 if US sanctions Venezuela.

http://oilprice.com/Energy/Crude-Oil/Barclays-Oil-Could-Rise-By-7-If-US-Sanctions-Venezuela.html

The situation there seems to be coming to a head, and Trump could use a diversion. Trump also likes to project strength.

I don’t know what will happen there, and it may be good or bad for the people of Venezuela, but I expect something big.

Brazil is accepting the refugee flow from Venezuela, many of them native indians fleeing Amazonas state. They have 7000 at a camp near the border.

True, the Average Brazilian is a lot more compassionate than most politicians and they do have a lot of empathy for the plight of the Venezuelan people. But for ‘Gringos’ not so much…

I worked in the Campos Basin and know the history quite well.

I fully approve of Brazil accepting such refugees, and of the USA, my own country, accepting REAL refugees.

What I don’t approve of is accepting enough to significantly accept population now, and in the future.

We are just about there, in terms of birth rates being low enough in the USA to allow our population to peak, except we take in so many people.

Make Brazil Great Again!

I could give a very long response to all your points. The short answer is Brazilians are not stupid and they have some pretty good scientists and engineers and also some of the most corrupt politicians on the planet… but I’m sure you already knew that 😉

Current President Temer has an approval rating of 5% right now.

Thank you for another informative post!

Thanks for another great post, George.

This puts the Brazil pre-salt in better perspective for me. So do you think Shell’s acquisition of BG was a good deal? The Brazil pre-salt was supposed to be one the big prizes.

Interesting how the Santos basin production has been increasing over the last few years (perhaps peaking in late 2016?) in spite of low oil prices – similar to the deepwater GOM – Petrobras and other companies made FID commitments in times of high oil prices, and when prices crash, come hell or high water, the projects get executed.

SLG – thanks. I think there was more to Shell buying BG than just the Brazil assets, in particular further diversification from oil to natural gas. I don’t know if they have sold off enough assets fast enough to please the shareholders and they’ve also had some terrible exploration results so it’s difficult to exactly see cause and effect, but I think the BG part in Brazil will work out OK for them.

Santos growth was really fast, they took on huge debt and are paying for it now, it’s also difficult to know how much corruption influenced the decisions – it looks like a considerable amount (you can’t get kick backs if there are no contracts). The development momentum is a big factor. PetroBras seemed to place rolling contracts for cloned FPSOs and rigs, and maybe it was more difficult and expensive to stop these than on one off projects, though they did cancel a lot of the rigs. Of course the other side of that is what happens when the project pipeline dries up and it takes five years to bring new production on, which I think we will start to see late next year. In the mid eighties crash I seem to remember there were a lot of cancellations of well advanced projects, not so much in the late nineties. Maybe interest rates play a part, or the higher sunk cost for the deep water mega projects.

I don’t think Santos basin peaked in 2016 – more likely 2018 or 2019, but it depends also on how the extended well tests and pilot plant goes on the Libra field. There are some more data from anp for April and May which show more increase from the dip, though I’ll probably wait to update with June numbers when available.

George Kaplan said:

Brazil pre-salt includes many projects that Goldman Sachs says are “so uneconomic, so stranded, that we almost don’t see any scenario under which they would be developed….”

“Not all projects that are currently in the pipeline will be needed. Shale has substituted the need for a lot of the more complex deep water, heavy oil projects and so we estimate that between $700 billion and $1.3 trillion of projects will not be needed any longer.”

Lower for Longer? The Impact of the New Oil Order: Goldman Sachs

https://www.youtube.com/watch?v=Zilqznc5LCc

Goldman Sachs isn’t known for their industry expertise. They and Morgan Stanley seem to believe shale oil will last forever. Or maybe they are trying to profit from bonds issued by OPEC nations and oil companies. They have a missing ethics department.

Brazil has shale potential, but not a great deal according to a study conducted for the EIA:

Technically Recoverable Shale Oil and Shale Gas Resources: Brazil

lhttps://www.eia.gov/analysis/studies/worldshalegas/pdf/Brazil_2013.pdf

South American shale is Vaca Muerto in Argentina.

Vaca Muerta. The a ending in Vaca makes it female, therefore it has to have an A in the adjective (there are few exceptions to this rule).

When will you guys learn that only thing that matters is price per barrel? If you’re interested in Peak Oil, then every article on this site should be about what is the current maximum price of barrel of oil, that won’t trigger demand destruction.

Please understand that reserves, and resources estimates are laughable, and the only thing that matters is what the economy can pay.

People just don’t seem to enjoy numbers. Maths was never a popular subject.

Thanks for the update doc. You just blew my mind.

dood, you do realize where dollars come from? and why price therefore has no physical relevance?

If you quantitative ease dollars into existence in an entirely whimsical way, why would you think they matter to something measured in joules?

Good points ‘name’less, but the information that you reference [the current maximum price of barrel of oil, that won’t trigger demand destruction] is something no one produce any good data for.

So we are left with wondering and speculating about it.

“When will you guys learn that only thing that matters is price per barrel.” – maybe when there’s some evidence to support it. If you have some I’m sure Dennis would welcome a post. I’d try to make some constructive comment for you rather than some trite, fact free grandstanding.

Demand is highly inelastic, supply has a 3 to 5 year delay between project start and delivery, price responds immediately to stock level changes not the other way round: all those say today’s price doesn’t really matter that much.

Exploration is continuous and continuously more expensive, public companies share price is highly influenced by their reserves, debate about OPEC reserves never stops, France has never produced more than a trickle of oil whatever the oil price (it doesn’t have any): all those say reserves and resources are quite important and far from laughable (whatever you may mean by that, assuming you know).

Hi George,

I believe that he means the estimates of reserves and resources are not very precise.

Certainly for OPEC resources I would agree, and for much of the World we don’t have a good handle on either conventional or unconventional resource estimates for crude plus condensate, in my opinion.

Though research that you have done sure helps make things clearer in the Gulf of Mexico and Brazil. We also have good data for the US, UK, and Norway, and perhaps Canada and Mexico. OPEC is a huge problem as far as transparency, a black box really.

But by his assertion reserves and resources don’t matter, only the price, so why should it matter whether they are known accurately, or even whether they exist at all?

Price does not appear to have much of an effect on demand, see my comment below.

Price never has much effect on demand when demand is HIGHLY INELASTIC, by definition of the term.

Apparently this is a term that is not well understood by the vast majority of people, excepting the handful that have taken a basic economics course.

The consumer will buy almost the same quantity of a good that displays high price inelasticity, no matter how high the price goes, because he MUST HAVE that good. Milk for the little kids is such a good, and parents will pay any amount for it, up to the limits of their ability to pay.

But it doesn’t matter if the price goes down to a fifty cents a gallon retail, they won’t buy more milk for their kids, beyond the amount the kids will drink, because it will be tossed out with the trash.

The demand for my apples is not highly inelastic, because there are many suitable and affordable and readily available substitutes for apples.

For now, and for some time to come, probably at least a few more decades, NO affordable, suitable and readily available substitute exists for oil in terms of the big picture. Yes, you can buy an electric car, but you can’t buy an electric over the road truck, or bulldozer, or farm tractor.

Hence the demand for oil is highly inelastic in the short to medium term. The customer has GREAT NEED of his usual amount, but hardly any need at all for MORE, and beyond the amount he NEEDS, he WILL NOT buy MORE , short term.

What would the average driver do with an extra couple of gallons of gasoline THIS WEEK? Take a forty mile pleasure drive? A few might, but only a VERY few.

Now if gasoline stays cheap three or four years, the customer may be tempted to buy a BELCH FIRE V8, rather than a more sensible car…….. TIME matters.

The demand for oil is nearly fixed short term, but it obviously varies over the long term.

In general terms, the price of oil, short to medium term, is basically determined by the quantity that is coming to market. When producers bring MORE THAN USUAL to market, the price crashes, it’s as simple as that. When they bring LESS, the price spikes.

When producers over produce, the price will go low enough that enough that some producers EVENTUALLY drop out thereby lowering production, and THEN the price will go up again.

This statement is entirely justified by what lawyers and judges refer to as the “preponderance of the evidence”, lol.

Given that most of the oil in the world is controlled by GOVERNMENTS rather than ordinary for profit oil companies, and that governments have other priorities than profit and loss, and that governments are notoriously slow to react to changing circumstances, it can and does take years for them to get around to curtailing money losing production.

Then there’s the higher priority of WAGING ECONOMIC WARFARE………..

Hi OFM,

In the short term oil demand is inelastic, over the longer term people buy more efficient vehicles and demand becomes more elastic, so over the short term (1 to two years) oil demand is relatively inelastic (though people may vacation closer to home so there is still a small effect), over the longer term (5 to 10 years) demand will respond to higher prices as it did during the 80s in the US.

Another way to look at price, demand and elasticity with oil is as a two-tiered system.

There is a highly inelastic demand for essential uses such as basic industry, food production, commuting to work, delivery of basic goods.

On the other hand there is a type of demand which is very flexible, such as vacation and entertainment travel, production and transport of discretionary (luxury) products, and even commuting in single occupancy vehicles., for example.

Hi hickory

I agree with your analysis in the short term of 2 years or less, longer term even the first tier of demand will be reduced as oil is used more efficiently by changing equipment, smaller cars more efficient trucks and tractors a d substitution of alternative fuels such as natural gas and renewable power.

Some industrial/commercial demand is relatively elastic: both container ships and long distance trucking can slow down and dramatically reduce fuel consumption; trucks can add aerodynamic modifications; petrochemicals can switch to different feeds (ethane vs natural gas); plastics users can modify containers, switch to other materials; electrical generation can switch between coal and nat gas; etc.

I’d say that an important thing here is that demand elasticity is somewhat non-linear: if fuel prices rise by 10% that doesn’t really get anybody’s attention. If fuel prices double, that will get some users serious attention. For instance, trucking fleets might launch a wholesale aerodynamics modification program.

Another important concept is “hysteresis”: efficiency modifications and substitution will stick around even if prices go back down.

Which is why the US should institute a tax at the pump that increases by two cents a month for a few years and then levels off.

Yes, that has the beauty of getting people plan for the day when taxes are very high, without actually shocking them right now.

Of course, everyone has to believe that it will really happen – that’s a tough order.

I’d say 5 cents per month for 5 years…

Hi George,

Yes on re-reading the comment you are correct, I initially interpreted the comment as saying that the oil price is important, which I agree with.

What he seems to miss is that the price is determined by supply and demand, not demand alone. So resources will matter because it will determine supply when costs of production and oil prices affect the economic decisions of oil companies in determining proved and probable reserves.

Mr Name seems not to understand that production cost and oil price is implicit in the estimates of reserves.

Hi name,

We can only speculate what the demand response will be to higher oil prices, at present there is an excess supply at current prices (high inventories). The data on oil stocks is not very good at the World level so the changes in stock levels are largely unknown (except perhaps in the OECD).

Can you tell us what the maximum oil price is that will result in demand falling below supply? My guess it is around $90/b, but there are at least as many guesses as there are observers.

Please enlighten us. 🙂

According to data from the EIA, even with the low prices the last few years, we have finally reached the peak usage of gasoline we saw back in 2007. The high prices and recession caused less than a 10 percent drop in gasoline use. So doubling the price has a small effect and halving the price has a small effect on consumption. Not much linkage there, more likely the steady increase in use over the years had more to do with more population, business activity and more cars than price had to do with it.

So to stifle demand of gasoline would probably take a large increase in price. maybe up to the $6 to $8 a gallon range. I would say we have no data here. Since it is a necessary commodity, people and business will give up other things and delay other purchases before really reducing their consumption of fuel.

No one really knows the breakpoint for the price of oil. If they do, they are keeping quiet. All we think we know is that oil production will eventually fall at these prices and maybe even at higher prices. We also do not have a case to examine where oil production was not subsidized.

Agreed. the system in most cities doesn’t really encourage reducing fuel consumption with even significant fuel price rises. If you have a car you are already paying insurance (and possibly car payment) whether you use the car or not. If you want to take public transportation the most affordable option is typically the monthly pass, and even then it is usually a significant cost ($90+). So you are committing to not commuting by car for the entire month. You are probably saving money (if fuel costs are high and assuming some wear and tear) but if the time difference to commute is significant its not a high savings per hour.

Long term demand elasticity is higher than short term. And…substitutes are improving…

What counts is return on capital employed. That in turn is influenced by costs, taxes, production profile, financing costs, and risk. Focusing on price only can bankrupt you in a hurry.

Yep. I can sell nice red oak logs for five hundred dollars EACH- except I don’t have any big ones, lol.

The red oaks will grow back , EVENTUALLY. I didn’t harvest the ones on my property, but my grand parents did. I won’t live to see the ones I have reach maturity, that will be another fifty years plus.

Oil is a depleting one time gift of nature, and it will never sell , over the medium to long term, for less than it costs to get it out of the ground and get it to the nearest refinery. Oil does sort of “grow back” but it takes millions of years, lol.

And on average, the cost of every new barrel coming to market is going up, rather than down.

Oil won’t stay cheap unless the electric vehicle market goes NUTS, and sooner than most people think it can.

The name Elon Musk has been well chosen; it defies categorization as to race, class, religion, etc.Ever met or even heard or read of an Elon, or a Musk? So rare a combination as to have no established profile.

People of a certain kind, created in large numbers by our education system, can project themselves onto the Elon image, and feel very pleased with themselves:‘He’s young, cool, hopeful, clever and rich, cosmopolitan just like me,and will take us to another world now this sad old mud ball is nearly finished!’

We are witnessing one of the most brilliant propaganda creations, appropriate for late-stage industrial, mass, civilization!

It’s really quite staggering that the propaganda and mind-conditioning system is projecting Elon Musk as the man to solve ALL our problems, and that this is being pushed energetically on children in school

The Soviet Union could not have done better: it’s Uncle Joe Stalin – he’d even pop up and fix your car if it broke down, with a cheery smile and a ‘No problem, Comrade!’ as he lit his pipe and waved you on your way.

The majority of people are so historically ignorant -and have been kept so – that they can’t see this for what it is.

Oh come on, that is a bit over the top. Everyone knows that the inventor of the laser bar code reader produced our modern civilization. Next RFID and just walk your shopping cart right on out the door, you will be charged on the fly, just like at toll booths. No more waiting in line. Now that is modern civilization.

Elon is just improving cars, improving rockets, and trying to improve on an old idea of underground mass transit. So far success at improving on what is already there. Not so sure about that Mars thing though. But as we all know failure is the best teacher. Still, everybody likes flames, explosion and glitz.

He is South African born Canadian-American. A man of the world with out of this world ideas. Remember much of the actual work and invention goes on in the background.

Elon R. Brown (1857–1922), American politician

Elon Howard Eaton (1866–1934), American ornithologist

Elon J. Farnsworth (1837–1863), American general

Elon Galusha (1790–1856), American preacher

Elon Ganor (born 1950), Israeli businessman

Elon Gasper (born 1951), American computer scientist

Elon Gold (born 1970), American comedian and actor

Elon Huntington Hooker (1869–1938), American businessman

Elon Lages Lima (born 1929), Brazilian mathematician

Elon Lindenstrauss (born 1970), Israeli mathematician

Elon James White (born 1978), American journalist

NEW DELHI: About $23 billion is planned to be invested in the oil and gas fields of the KG Basin, Oil Minister Dharmendra Pradhan told Parliament on Monday.

“The operators of blocks /fields in KG basin under Production Sharing Contract (PSC) regime and nomination fields have submitted DoC (Declaration of Commerciality)/FDP (Field Development Plans) for the commercial oil and gas discoveries along with projected investment estimates,” Pradhan said, adding that the estimated investment from these plans were $22.9 billion.

The new oil and gas production from these fields in the KG Basin is expected to reach up to 22.27 billion cubic meters of gas and 4.68 million metric tonnes of oil by 2021-22, Pradhan said.

http://economictimes.indiatimes.com/industry/energy/oil-gas/23-billion-to-be-invested-in-kg-basins-oil-gas-fields-dharmendra-pradhan/articleshow/59740589.cms

LONDON (Reuters) – Britain will ban the sale of new petrol and diesel-powered cars from 2040 as part of a plan to get them off the roads altogether 10 years later, environment minister Michael Gove said on Wednesday.

It follows a similar announcement earlier this month by the French government, while German cities including Stuttgart and Munich have also said they are considering banning some diesel vehicles.

Ahead of a June election, the governing Conservatives pledged to make “almost every car and van” zero-emission by 2050.

http://uk.reuters.com/article/us-britain-autos-idUKKBN1AB0U5

By estimates based on low global resources and rising internal producers use there won’t be much export crude around by 2040, maybe just enough for some heavy transport, the military and the emergency services, so going petrol free on personal transport by then probably isn’t much of a stretch. How much power is available and where it ultimately comes from is another matter. The biggest potential energy source by far in the UK is subsea coal (stand by for lots of replies about wind and tides), whether it is technically or commercially recoverable is another matter, but a lot of people think it is, including the government which has already issued development licences in some areas.

Our government has a split personality in many areas when it comes to climate and energy – e.g. we have a law that states we must meet certain emission targets, but another (I think the same law actually) saying we must use as much of the North Sea resource as possible and a department with a part mandate to help export our North Sea expertise and equipment supply

“Our government has a split personality in many areas when it comes to climate and energy”

I think this pretty much mirrors Norway as well who have infuriated environmental groups by opening up a record number of blocks in the Arctic for oil exploration. The oil ministry is offering 93 blocks in the Barents Sea, entirely in the Arctic Circle, with applications by companies expected by the end of November. FWIW my Norwegian niece (and keen environmentalist), who is an EV driving Petroleum Engineer, insists every last barrel of oil in Norway will be pumped and exported as quickly as humanly possible; so much for “stranded oil”.

I’m still holding on the hope that someone finally makes a breakthrough with thorium fission or fusion. Or more efficient solar, maybe this: https://en.wikipedia.org/wiki/Optical_rectenna

The Chinese have totally overinvested in solar PV production, pretty much killing the hope of innovation for a few years. They have about 75 GW of annual solar panel production, which they will max out for cash flow reasons, even though the investments will never pay themselves off.

They are at 50 cents a watt, and may fall even farther. At that price there isn’t much incentive to build new PV production capacity or develop new technology — you’d have to target 10 cents a watt or something.

There is about 350 GW of solar PV installed now. So in five years there will probably be 75*5+350= 725 GW installed. If it runs at a quarter capacity, then average output will be about 160 GW.

There is about 400 GW of nuclear running at 80% so it is about 320 GW on average. So in 5 years solar output should be about half the size of nuclear. Feel free to challenge my numbers, they are very rough.

What is more interesting is the 725 GW max, which will wreak havoc on existing electricity grids unless storage ramps enormously. Not surprisingly, hundreds of gigawatt hours of annual battery production capacity is in planning for the next few years.

The great thing about oil is not that it is a good source of energy. Coal, for example, is much cheaper. The great thing is that oil is a good store of energy. So solar’s real contribution in the short term will be to force the pace of battery production, and that will spill over from the electricity market into the oil market via electric vehicles. And the oilmen will find that their product is too expensive.

Absolutely, EVs are the best way to smooth out renewable power.

EVs with 200-300 mile range have a lot of flexibility for when they charge. Even short range EVs can charge pretty much when they want to during the night.

If these guys are right and we are close to peak oil, the stuff may be selling for $300 per barrel in 2040 and the U.K. would suffer from extreme energy insecurity depending on the Kalifah of the United Arab Islamic Federation for its oil supply.

Oil prices will never stay above $200 for long: it’s not worth it. There are very good substitutes for most of it’s use above $100, and at $300 even the things that really require liquid hydrocarbons would be replaced by synthetics.

As usual , Nick

You are overselling your case.

When the opposition quotes remarks like yours, and Joe Sixpack reads your quoted words, it’s FINE grist for the Koch brothers propaganda mill.

There AREN’T any good substitutes for oil at a hundred dollars a barrel, or even two hundred dollars a barrel, that are READILY AVAILABLE and that can be quickly scaled up to the volumes needed to replace oil, and there WON’T be any such substitutes for quite some time to come, most likely ten to twenty years at an absolute minimum.

The best we can realistically hope for, being believers in GEOLOGY, is that renewable energy and electrified cars, etc, will displace oil fast enough that the price of it DOESN’T go two hundred bucks a barrel, bringing on GREAT DEPRESSION II, which would of course drive the price down again.

I have high hopes that we will indeed eventually manage a successful transition to renewable energy, but it’s going to be a GODDAMNED long time before any substitute is available for oil in the quantities needed, excepting one possibility- synthetic oil made from coal.

And even additional quantities of coal based synthetic oil can’t be brought to market in less than maybe five years or so , even on an emergency basis, because it would take that long to design and build a coal to liquids plant.

Maybe in the event of a national security emergency, we could build a coal to liquids plant here in the USA in less time, but still not less than a couple of years bare minimum, and that would only be possible in the event of a lasting national emergency with EVERY usual environmental and permitting regulation out the window.

It bothers me that people so well informed as the regular members of this forum seldom seem to realize what is actually written, or broadcast , and BELIEVED, for good reasons ( from the point of view of readers, watchers, and listeners ) in the anti environmental and anti renewable energy press.

Hi OFM,

Any reasoned argument can be quoted out of context and be made to look foolish.

Nick’s point is that oil at 200 or 300 per barrel will make EVs and other substitutes more attractive so that over time demand for EVs will increase and demand for ICEV will gradually decrease.

He is not speaking to the right wing who for the most part will only be convinced that this will happen after it has occurred and then will wish for the good old days. Like we all wish for points and carburetors because they worked so well 🙂

Thanks, Dennis. That’s exactly right – I wasn’t talking about liquid substitutes, I was talking about a wide range of things that people will choose instead of very expensive oil. Synthetic liquid fuel is still expensive – it’s far from the first thing that we’ll use to replace oil.

It’s worth mentioning that $200 oil would bring forth a very wide range of responses, some of which are very short term: three obvious ones are aerodynamic retrofit modifications for trucks, slower speeds for trucks and container ships, and expanded carpooling (which is already larger than mass transit for commuting).

A much more meaningful policy/headline would have been a ban by year 2030.

Good chance that by 2040 the process of a switch away from ICE will largely complete anyway.

Meanwhile cities in Germany are getting ready to ban diesel

https://global.handelsblatt.com/companies-markets/diesel-ban-hits-home-804779

Well, Stuttgart anyway, which has air quality problems because of its geography.

a view of the real world

https://wattsupwiththat.com/2017/07/25/u-s-becomes-global-fossil-energy-giant-feeding-hungry-world-energy-markets/

Hi Texas Tea,

The US produces a lot of coal and natural gas. We have gone from being a natural gas importer (mostly from Canada) to self sufficiency in natural gas, and that is good, I agree. At some point natural gas in the US will peak(but probably after 2035). Coal has not been imported to the US (on a net basis) for over 100 years, so not really a big deal for US “independence”.

Do you expect that US oil output will increase to 16 or 17 Mb/d? Unless US demand for crude oil decreases, that is what is needed for US oil independence. I am highly skeptical that US C+C output will ever break 12 Mb/d. Note that NGL helps very little in producing gasoline, diesel, or jet fuel, the major products needed from US oil refineries which currently have inputs of about 16.5 Mb/d of crude oil.

The discussion here is mostly about liquid fuel rather than coal or natural gas.

The fact is that the US is very far from oil independence at present.

I doubt this will change very much unless demand for crude falls in the US.

That is a possibility by 2030 when oil prices may be much higher than today, probably over $100/b in 2017 $.

Dennis,

The title of the post that texas tea linked reads “U.S. becomes global fossil energy giant feeding hungry world energy markets,” not “U.S. becomes global oil giant feeding hungry world oil markets.”

another glimpse into the real world

http://www.worldoil.com/news/2017/7/26/wood-mac-shale-sector-to-be-cash-flow-positive-by-2020

Andy McConn, principal analyst at Wood Mackenzie,said: “We are confident in tight-oil producers’ ability to grow and generate free cash flow in a $50/bbl oil-price environment.”

He added: “We’re only in the early stages of tight-oil development. Like any high-growth, capital-intensive investment, the first years are a poor indicator of future profitability. To date, high early-life costs have weighed on cash-flow metrics, but tight-oil producers have made great strides in honing technology and reducing costs. Collectively, that progress – as measured by well productivity and companies’ cost structures – have improved immensely during the downturn, providing the necessary structural stability for sustained profitability.”

I guess that service companies like Halliburton will have to provide their services at a loss forever.

Actually Halliburton posted positive earnings of 3 cents per share and Schlumberger posted a loss of 5 cents per share.

Both pretty darn close to break even, which is the definition of success in the commodity bear market.

Hi shallow sand,

Would you agree that a large portion of the cost savings in the LTO focused companies has been due to lower prices from service companies?

At some point these companies will no longer be viable if they continue to work at a large discount.

I also question whether these LTO companies will remain cash flow positive at oil prices under $50/b.

Have we seen many 2Q earnings? Are these companies now showing positive earnings? 2016 was a disaster, it is not clear that 2017 will be much better.

Dennis. I agree, but I base that on the Haynes and Boone bankruptcy monitor for service companies, along with service company earnings. Finally, our costs are down significantly in almost all areas.

Of course, many would argue that by reducing our workforce, we have achieved efficiency gains. Labor is a very large expense in the industry, so reduced headcounts, wages and benefits could be where much of the efficiency gains are occurring?

If the men on the frack crew were earning $50 an hour in 2014 and are now earning $25 I assume that would be deemed an efficiency gain?

Hi Shallow sand,

It is not clear that there will be much of a ramp up in output if they don’t find some people to frack those drilled wells, no doubt there will be shortage of workers before long and wages and service costs will increase.

Have you looked at any 2Q reports for large LTO players, you follow the financial stuff closer than I do?

Maybe a post on this would be good, just shoot me an email if you have the time or interest. Just a summary of top 10 US LTO focused companies (leave out majors) is one suggestion, but it is entirely up to you of course.

Dennis.

I think a post comparing earnings in the US E & P space to other major US industries would be noteworthy.

Just today, COP reported adjusted EPS of 14 cents, which was a beat. However, actual was a quarterly loss of $1.1 billion, due to recognition of losses from sales in the Barnett Shale and San Juan Basin, both of which are in the lower 48. Further, COP is guiding year end 2017 production of under 1.2 million BOEPD. That is down almost 400K BOEPD from 2014.

So, while 14 cents is a beat, they are shrinking the company and still borrowing to pay the dividend. Plus, the stock price is half of three years ago, with a lower dividend. Compare that with other major US industries, such as banks, industrials, technology, consumer staples, etc.

I assume investors have been bottom fishing since the crash, hoping to cash in when oil and gas rises. But, as traders are pricing oil and gas prices primarily off US production and inventories, prices cannot recover as long as US E & P’s keep growing production. Catch 22 deal. Further, many of the companies are very overvalued if prices stay where they have been the last three years. Break even, whatever that means, doesn’t sound like a good goal.

I still think $55-65 WTI and $4 gas would be good, but whenever I mention that, my comments get smacked by some here and elsewhere.

I posted this before. It compares net margins across many industries.

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/margin.html

Hi shallow sand,

I used to think $55-65 would not be high enough to increase LTO output, but clearly I was wrong. Whether World output will continue to meet demand at $55-65 per barrel remains the question. Currently stocks are falling and if OPEC continues its cuts along with the 10 non-OPEC countries, eventually the lack of new projects in the pipeline will begin to hit World output, probably by 2019 or 2020.

At that point even if OPEC and LTO producers produce as much as possible profitably, output is unlikely to satisfy demand.

It is for this reason that I expect by 2020, $65/b will be too low an oil price to keep the oil market in balance.

I never get these price predictions right, so maybe oil prices will remain less than $65/b until 2030. 🙂

Note that I don’t think shallow sand has ever suggested this, I think he might mean $55-$65/b for 2018 to 2019.

Dennis,

When it comes to predicting future oil prices, there are as many different predictions as there are different people making them.

Yesterday Shell CEO Ben van Beurden said the company has adopted a “lower-forever mindset,” as peak demand should hit within a decade.

Shell braces for ‘lower forever’ oil amid electric vehicle boom

http://www.telegraph.co.uk/business/2017/07/27/profits-surge-van-beurden-puts-focus-discipline/

Hi Glenn,

I agree future oil prices are not known.

If prices are low, supply is more likely to grow more slowly. In the short term (3 to 5 years) demand is likely to outstrip supply which implies oil prices will rise.

How much they will rise and the precise demand and supply response are unknown.

So as you have said, a precise prediction of future oil output given these uncertainties is “a fool’s errand” (I believe that is the term you used).

XOM US upstream reported a loss of $183 million for Q2, 2017.

CVX lost $102 million on US upstream in Q2 2017.

Bloomberg just released a report by Denning on Hess, specifically its Bakken-centric operations.

Sheds some light on sub $50 WTI effects on shale E&PS.

Here’s the article link. Sounds like Hess isn’t a rousing success, but doing as badly as it could be. The title is more favorable than the article.

https://www.bloomberg.com/gadfly/articles/2017-07-26/hess-earnings-holding-on-and-making-opec-nervous

I meant to say it isn’t doing as badly as it could be. The tone of the article seemed to be cautiously optimistic.

From the article, it looks like shale is the only place where Hess and Anadarko are making money.

The importance of that, then, is how long the LTO lasts. That’s why I am so interested in decline rates. If there isn’t global potential, the the future of oil is up to LTO. So goes LTO, so goes the oil industry.

Haven’t we gone over this before? You can’t believe a word the shalie huxters say about costs or economic returns. Just look at their financial statements. None of them make money. The numbers don’t lie.

Boomer

Although I’m far more positive regarding the longer term production capacity of LTO than you might be, the natgas supply will tend to overwhelm its liquid cousin in future decades.

One aspect of LTO beyond its individual decline profiles (still leaving about 90% hydrocarbon unrecovered), is the expanding areas that are becoming more economically feasible as the industry matures.

Known formations such as the Powder River Basin, Uinta, Rogersville, Tuscaloosa Marine and several others might attract increased development if the economics warrant.

However, on another site, an interesting update on the Utica was presented by the “Father of the Marcellus”, William Zagorski.

28 page graphic rich pdf is titled “Discovery of the Utica Shale: Update on an Evolving Giant”.

Although it is a bit wonky and not inclusive of the most recent data, the sheer size of this resource should indicate what is possible to produce in decades to come.

John, we must also factor in where investors and lenders put their money. Why be satisfied with an industry barely hanging on when they can finance industries with more potential?

Hess lost $340 million in US upstream in Q2, 2017 and lost $14 million in International upstream in Q2, 2017.

I didn’t see that Anadarko broke out US v International in Q2, 2017, but I just scanned the press release and didn’t look at the 10Q.

As I recall, in Q1, 2017 and in past quarters as well, companies that broke out US or North American operations v International all showed much heavier losses in US/North American. Examples would be XON, CVX, OXY and COP.

My previous paragraph is from memory, so if anyone wants to actually look at the numbers instead, please correct me if I am wrong.

Really interesting how long these companies have went with substantial negative EPS.

Hi Coffeguyzz,

I agree the natural gas shale resource is large, the LTO resource not so much especially at current oil prices. When oil prices increase to $100/b or more, then more of the LTO resource will be economically recoverable.

It will be interesting to see what happens to the well profiles of the more productive Bakken wells that have started producing in 2017.

Most petroleum engineers believe the overall EUR will be no different, production is simply pulled forward to earlier months, this helps the finances as long as the increased cost of more proppant and a higher number of frack stages does not offset the increased net present value of the output (due to faster recovery in the early months).

The above comment refers to the Bakken where lateral length has remained at about 10,000 feet for many years. In the Permian basin much of the apparent increase in new well productivity is due to increased lateral length, if we double the lateral length from 5000 feet to 10,000 feet then the well produces 2 times the oil per well, but unless the prospective are also increases by a factor of two, the number of prospective wells decreases by a factor of 2 ceteris paribus.

Hi shallow sand

Thanks.

Many of the LTO players are also cutting back on capex so we may see flatter LTO growth in Q3 and Q4.

Hi Glenn,

I suppose the US could export some coal, not really very interesting for a peak oil discussion in my opinion.

Not to mention that coal is pretty cheap per BTU/joule. Even if the US were to export enough coal to balance it’s crude imports, the US would still have a large dollar deficit.

OTOH, crude oil is cheaper than refined products. I’d be curious to see an analysis of dollar-weighted energy imports/exports.

Hi Nick G,

Then do it and I will post it.

Dennis says upthread” Most petroleum engineers believe the overall EUR will be no different, production is simply pulled forward to earlier months, this helps the finances as long as the increased cost of more proppant and a higher number of frack stages does not offset the increased net present value of the output (due to faster recovery in the early months).”

please provide where you got that bit of information. I do not think you truly understand what is happing in the real world where frac technology is advancing and will advance too. I am not saying you are wrong, i am saying you do not know yet what will be the impact on EUR. By the way neither do I, but i can say what I am seeing is VERY encouraging, I will more than surprised if EUR is not increased (significantly) by these new technologies based on watching production on my wells for over 30 years.

texas tea,

The peakists, whose beliefs are about as doctrinaire and dogmatic as they come, operate in what Nassim Nicholas Taleb calls the “platonic fold”:

That sounds a little like epistemological nihilism.

I share your frustration with many Peak Oil analyses. I have often argued that PO enthusiasts should acknowledge the large uncertainties involved. They should think in terms of risks, not certainties.

But, I think Dennis is sincerely trying to get it right, and I think his projections are pretty good. I would do them a little differently if it were up to me, and I sometimes give him somewhat unsolicited advice. But….Dennis is willing to do pretty complex and very time consuming analyses for free and that’s astonishing! I think he deserves enormous credit.

Forecasting and scenario analysis is often very hard to do, but it’s still necessary. Every large organization does it (including oil companies!) – they know that they are very, very imprecise, but you have to make your best guesstimate of what’s coming in order to plan.

Forecasts are a necessary evil. Don’t complain – make substantive and constructive suggestions, or, even better, do your own.

.

And what evidence does Pascal provide for this idea?

It seems to be simple, old fashioned religion – the assumption that reason cannot fully understand our world, or find meaning in it.

Reason includes biology and psychology, and it is completely arbitrary to assume that these things cannot help us understand why we do what we do, and what can make us happy and give our lives meaning.

Pascal died at the age of 39, after a life of illness. “Pascal’s ascetic lifestyle derived from a belief that it was natural and necessary for a person to suffer. In 1659, Pascal fell seriously ill. During his last years, he frequently tried to reject the ministrations of his doctors, saying, “Sickness is the natural state of Christians.”[31]”. Wikipedia.

Medicine, biology, psychology – these disciplines didn’t really exist during Pascal’s life – he was just born too early.

Nick G,

Five hundred years after the rebirth of the Platonic doctrine “that reason can fully understand our world, or find meaning in it,” can you marshall empirical evidence demonstrating the truthfullness of that claim?

Of course – there has been enormous progress in understanding the world in the last 500 years. There’s really no sign of that progress stopping (please don’t respond with statistics about patents – I think any reasonable person can see that progress still continues – just look at energy engineering and medicine.

Two hundred and fifty years ago Franklin invented the lightning rod. Churches were the last to accept them, arguing that lightning strikes were the wrath of god, and it was defying gods will to stop them. They only accepted lightning rods after churches kept burning down. Theologians are not a reliable source about the limits of science.

I don’t know whether Plato really applies here – I don’t think he was really thinking of the Scientific Method. When I refer to reason, I’m referring to the idea that we think for ourselves, rather than going by ideas laid down by prophets, preachers, and other authorities who ask that we take their ideas on faith. That made sense in a world where change was very, very slow and we knew little about how the world works – accumulated human wisdom could be fossilized into rigid doctrines, which then fought each other in clashes of empires and civilizations. It doesn’t really make sense now. There are better ways to develop and continually improve our “map” of how the world (including humans) works.

Does human understanding have limits? Who knows? Who cares? Why try to prove a negative? In the end, pretty close to 100% is almost certainly good enough.

But certainly theologians are not a reliable source on the subject.

Pascal did a lot of groundbreaking work on statistics. His work was based on gambling games like cards, dice and roulette wheels. All games with well defined rules.

As Pascal’s Wager shows, he really didn’t understand statistics in a situation with incomplete information.

Bayes figured it out the statistics of uncertainty in his abortive attempt to prove the existence of his god.

Hi Nick,

I always clearly state my assumptions and present various scenarios because I recognize the future is not known, we can only make reasonable guesses as to how it might look by using several different assumptions. For conventional oil my URR estimate is between 2400 and 3600 Gb of conventional C+C. For unconventional (mostly extra heavy oil sands and LTO) my estimate is 300 to 1000 Gb (250-600 Gb for extra heavy oil and 50 to 400 Gb for LTO). So for all C+C the range is 2700 Gb to 4600 Gb.

The best way to approach a high uncertainty analysis is to use the maximum entropy probability distribution, I would set 2700 Gb to zero and use a mean and standard deviation of 1000 Gb for such an analysis. This results in a mean of 3700 Gb and a median (50% probability of URR being higher or lower) of 3400 Gb. There is about a 66% probability that the URR would be less than the mean (3700 Gb).

hmmm. So what would the 95% confidence interval limits (IOW, a double tailed distribution with 90% of the curve between the two limits) be for the date of Peak Oil?

Hi Nick,

The analysis points to URR and the 90% interval is 2750 Gb to 5700 Gb with a median (50% probability) of 3400 Gb.

The date of the peak depends on demand, this has further uncertainties which are more difficult to model (how fast do substitutes develop, how fast do technology improvements in oil extraction occur?).

It is possible that lack of demand and low oil prices are more responsible for the peak than lack of oil in the ground and the ability to extract it.

Extraction at a profit over the long term is a key point. When the maximum output point will occur is a very difficult problem, which I have always acknowledged.

Hi Glenn,

The beliefs of the cornucopians are equally dogmatic in my opinion.

Of course name calling by you or I proves very little.

Dennis,

Ah, but my name calling is backed up by hard evidence.

See, for instance, this thread below:

http://peakoilbarrel.com/brazil-reserves-and-production/#comment-609888

You cherry pick the evidence that conforms to your peak oil dogma, and ignore any evidence that contradicts it. The bottom line is that what you end up with are distortions and partial truths, and of course a failure to accurately predict.

Hi Glenn,

I use empirical evidence to model the past, then assume the future will be similar,

you assume that it will not be similar.

We have no empirical evidence of the future, we can only speculate based on past experience.

The arrow of time goes from past to future in my experience, I believe this will continue to be the case.

I am not the one who initially claimed those who disagree with my view are “dogmatic”, that was you, backed by nothing but opinion.

Oh and your accurate predictions can be found where?

That’s right they cannot be found.

I have never claimed to make accurate predictions, it cannot be done.

I can usually create low and high scenarios which bound reality fairly well and I adjust my thinking based on evidence. For example the scenarios I created in 2012 are more consistent with conventional oil output which will probably be in the range of 2400 Gb to 3200 for URR, where I picked a single case of about 2800 Gb. Later I used (in 2015) 2500 Gb to 3100 Gb (where LTO was included in this estimate) since that time there have been new estimates by the USGS on LTO resources and I also have more information on LTO output from the EIA and Shaleprofile.

I use all the evidence I have, but an assumption that new well EUR will continue to increase is unproven and might lead to inaccurate estimates of future output, if one were to make such an estimate using that assumption.

We are in agreement that the future is not known, I have never claimed otherwise.

For an example of a past scenario which has done pretty well so far bounding World C+C output between a low and high scenario see the following from July 2012:

http://oilpeakclimate.blogspot.com/2012/07/an-early-scenario-for-world-crude-oil.html

Dennis Coyne said:

“I use empirical evidence to model the past, then assume the future will be similar, you assume that it will not be similar.”

Right.

You assumed those pre-2015 type curves and resultant EURs were engraved in stone.

Fast-forwarding to 2017, that doesn’t look like a very sure bet any more.

Your only hope now is for the newer completion techniques to prove to be a failure.

Hi Glenn,

You are incorrect, I did not assume the 2015 type curves were engraved in stone, I simply don’t know how they will change in the future, productivity may increase or decrease, I cannot predict the future so I assume it will be similar to the past, I also cannot accurately predict the number of new wells completed, so I guess what the future number might be based on completion rates in the past.

When I have enough information to estimate a new type curve, I do so, but this requires about 11 months of data minimum.

In the Bakken the EUR was stable from 2008 to 2013 and has increased since then, the higher EUR well profiles are included in my models, as I said before, future improvements in the well profile cannot be anticipated in advance, at least by me.

We don’t really know what a well will produce with any certainty until it has been produced.

The model makes the simplifying assumption that the well profile will not change because of my lack of clairvoyance.

No doubt you could do much better. 🙂

Dennis Coyne said:

“I did not assume the 2015 type curves were engraved in stone, I simply don’t know how they will change in the future, productivity may increase or decrease….”

You can say that with a straight face, after having just claimed that “the overall EUR will be no different, production is simply pulled forward to earlier months”?

Hi Glenn,

The shape of the type curve can change so that more of the oil is produced in early months and less in later months, potentially this can lead to a higher EUR depending upon the economics at the tail. It may be the case that EUR increases or decreases depending upon where the economic cutoff is. In almost every case faster extraction in the early months will lead to a higher overall EUR even if the tail of the high output wells (in the first 24 months) falls below the lower output wells after 24 months, it is unlikely the difference in the tails would offset the higher early output unless the wells were produced to very low output levels (say to 2 b/d).

My models adjust the well profiles as I have enough data to estimate them.

In the simplified LTO model I linked to, the well profile was held fixed for simplicity of presentation.

No glenne, the premise is that fossil fuels are a finite and non-renewable resource. This is not really a belief but empirically true based on all known evidence.

The ones with the strange dogmatic beliefs are those that believe that fossil fuels are infinite or regenerate in some fantastical fashion, perhaps abiotically.

@whut said:

“….the premise is that fossil fuels are a finite and non-renewable resource. This is not really a belief but empirically true based on all known evidence.”

No, the “premise that fossil fuels are a finite and non-renewable resource” is not an empirical truth. It is an analytic truth.

We’ve already been through this once before, but you don’t seem to be able to move beyond your same old hackneyed talking points and strawman arguments.

http://peakoilbarrel.com/opec-june-production-data/#comment-609029

Hi Glenn,

Interesting that you would claim it is not an empirical truth.

You made fun of me in a previous comment for my claim that all oil fields peak and decline (almost every field that has started producing oil has exhibited this behavior), suggesting that this was self evident.

Are you now questioning this “self evident” assertion?

Perhaps not. Maybe you believe the rate of abiotic oil production is greater than the rate that oil is used worldwide or that the number of oil fields that are yet to be found are unlimited?

How exactly would you prove that oil is not a finite resource? I have a hard time understanding your position.

I think most in the oil industry would not agree with the proposition that the oil resource is infinite.

If that is correct, then it is finite.

Whether that is empirical or analytical (in fact it is a combination of reason and observation which is true of all scientific understanding) is really beside the point.

It is a widely accepted truth.

Dennis,

Is it possible for you and @whut to make an argument without alleging an absurd absolute or standing up some strawman?

Can you show me exactly where I “made fun of you in a previous comment for your claim that all oil fields peak and decline.”

Sure, go ahead and show me where I did that.

Of course all oilfields will eventually “peak and decline,” but they may not do so on your schedule.

The debate is not over if peak oil will happen, but when it will happen.

Peak oil may have already happened, or it may not happen for another 100 years or more. There’s a big difference between those two, believe it or not.

Notice that every time this guy glenne ends up talking circularly? See :

I think this is the reason for having this blog in the first place! All the charts that are posted here and all the interactive apps that are created are for the benefit of people that are interested in following the trajectory of the oil depletion timeline.

The term “peak oil” is to oil depletion as “global warming” is to climate change. It’s but one property of the overall process.

Hi Glenn,

You don’t remember what you post?

You seemed to question the fact that oil is a finite resource.

Are you walking back from that stance?

This absurd absolute was suggested by your argument and I agree that indeed it is absurd.

Yes peak oil is a question of when, experts put the conventional resource at about 2000 Gb to 4000 Gb and unconventional oil resources at 250 Gb to 1000 Gb.

Even the very optimistic estimates of 5000 Gb for C+C would peak before 2050, most experts expect a peak between 2020 and 2030 (the most likely scenario), those with a more pessimistic view believe it will be before 2020, only those with an extremely optimistic outlook believe oil will peak after 2050.

I agree with the expert consensus of 2020 to 2030, the higher end of the range of URR estimates might result in a later peak than 2030, but the probability is less than 10%, about 2.5% for 2040 and maybe 1% for 2050 or later.

Hi Texas tea,

Fernando has suggested this and another engineer named Frank Liu who comments at shaleprofile.com. For the Bakken so far the well profile falls to the level of earlier wells after 12 to 18 months.

I mention as a possibility that the increased technology might increase the speed with which the oil is extracted but might not increase the total oil recovered.

At this point the wells are mostly less than 10 years old so we can only speculate.

Hi Texas Tea,

The relevant comment thread is at link below:

https://shaleprofile.com/index.php/2017/06/08/permian-update-through-february-2017/#comment-1158

An excerpt:

As a reservoir engineer, I think the some presentations mislead investors for using such a big EUR to get a very small break even oil price. They may find an excuse since no one knows the exact EUR until the well was abandoned. The type curve analysis they used to get such a high EUR is mainly based on the high initial rate and apply the same decline rate as they used before for lower completion efficiency wells. The decline will not follow the type curve that they used, and the EUR will not reach more than 1 million BOE on an average basis that Pioneer Natural Resources used for Wolfcamp B completion 3. Increasing stage and cluster density only increases well completion efficiency, it can’t increase EUR if the well spacing is the same and also assume there is no economic production rate cut off.

…

To make a summary for high completion efficiency resulted by high stage and cluster density, it makes early time rate high that otherwise should be low. The EUR can’s be significantly boosted by increasing completion efficiency. Without increasing the distance between two wells, I would expect the oil rate of late drilled wells will all cross over with that of early drilled wells for similar reservoir. The higher the density of stage and cluster, the quicker the rate cross over. The reservoir is a close certain amount for both. If more is recovered earlier, less will be recovered later. The expected more than one million BOE EUR will not be reached due to use the same decline curve analysis. The late fast decline is the wrath of science. The low breakeven price based on such a high EUR is not true. Investors should be alerted.

Follow the entire thread looking for Frank Liu’s comments (mine can be ignored), the man really knows his stuff.

Maybe Fernando could comment as well as he is well versed in this area (reservoir engineering).

And if many LTO companies are operating as Ponzi schemes, it is in the management’s best interest to get the oil out fast, collect as much money from willing lenders and investors as they can, transfer it to their personal accounts, then walk away when it all collapses.

thanks Dennis to be accurate perhaps you overstated your case, where “some” engineers or perhaps a “few” or maybe to be most accurate you should of said “a couple of engineers” instead of MOST?

Hi Texas Tea,

I only have a sample of two, perhaps they are not representative, but their views also confirm what Mike Shellman and Shallow Sands have been saying. In addition the data Enno Peters provides at shaleprofile.com also confirms this.

I tend to go with the empirical evidence.

Dennis Coyne said:

“I tend to go with the empirical evidence.”

Oh really?

Can you show me where the empirical evidence exists on this graph from shaleprofile.com that leads you to “believe the overall EUR will be no different, production is simply pulled forward to earlier months”?

Hi Glenn

For the Bakken where lateral length has been consistent the barrels per month falls to the level of older after 12 to 18 months. The cumulative well profile does not show this as clearly.

Also you need to give us more information.

Where are those wells?

In some LTO plays the length of the laterals has increased, this increases the area accessed by the well and increases output per well but decreases the number of wells that can be drilled per unit area. The net increase in URR would be zero.

Hi Glenn,

Using data from the following Bakken post at shaleprofile.com

https://shaleprofile.com/index.php/2017/07/17/north-dakota-update-through-may-2017/

The chart below is from the Well Quality tab using years from 2008 to 2017 for all North Dakota Bakken/Three Forks wells which started producing between Jan 2008 and March 2017.

By 25 months the higher productivity wells have fallen to the same or less output than the earlier less productive wells. This is despite a higher number of frack stages and more proppant being used in the newer wells.

Any increase in cumulative output is during the first 24 months, after that output is the same or less.