By Ovi

The focus of this post is an overview of World oil production along with a more detailed review of the top 11 Non-OPEC oil producing countries. OPEC production is covered in a separate post.

Below are a number of Crude plus Condensate (C + C) production charts, usually shortened to “oil”, for the oil producing countries. The charts are created from data provided by the EIA’s International Energy Statistics and are updated to February 2025. This is the latest and most detailed/complete World oil production information available. Information from other sources such as OPEC, the STEO and country specific sites such as Brazil, Norway, Mexico, Argentina and China is used to provide a short term outlook.

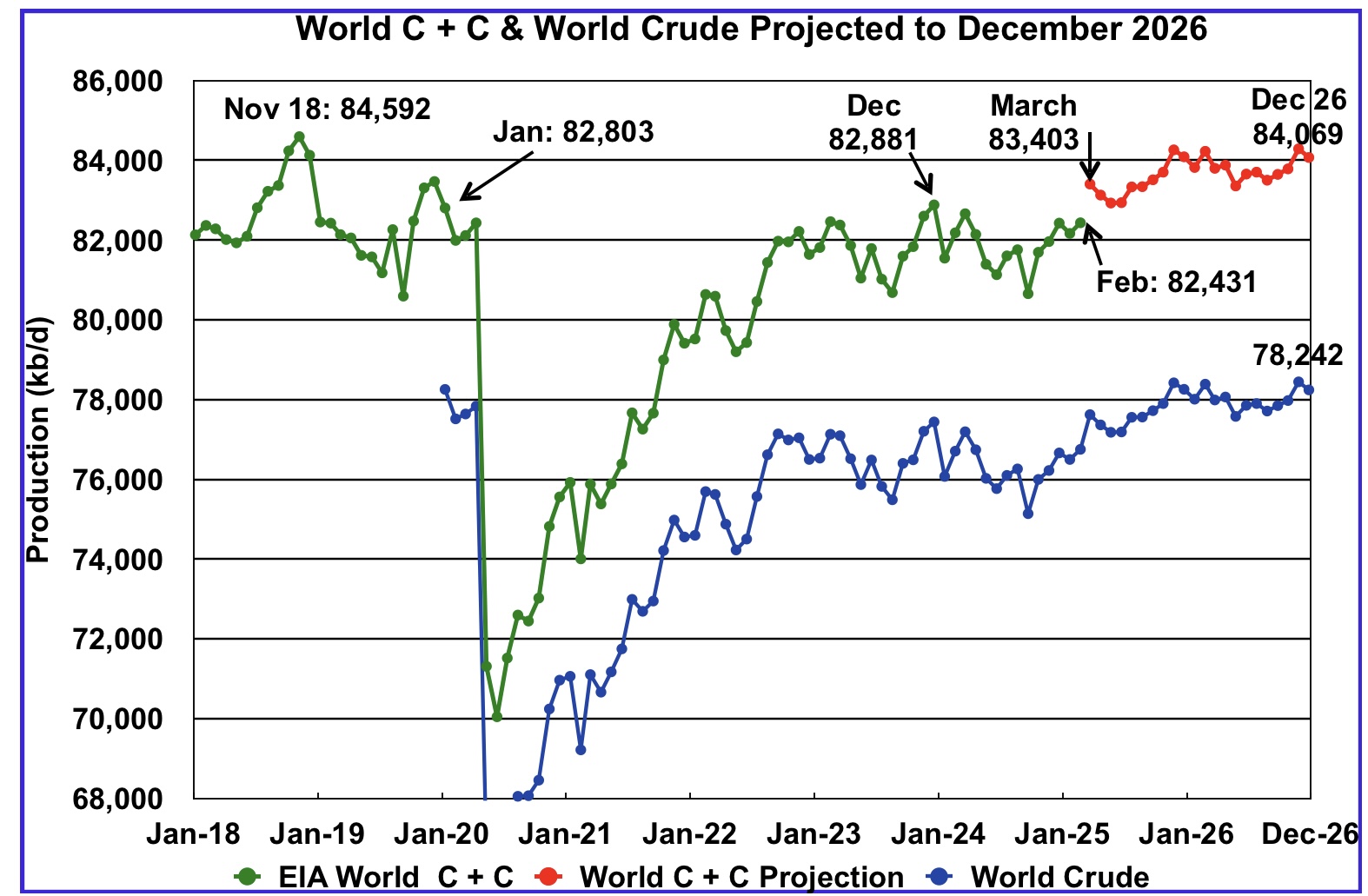

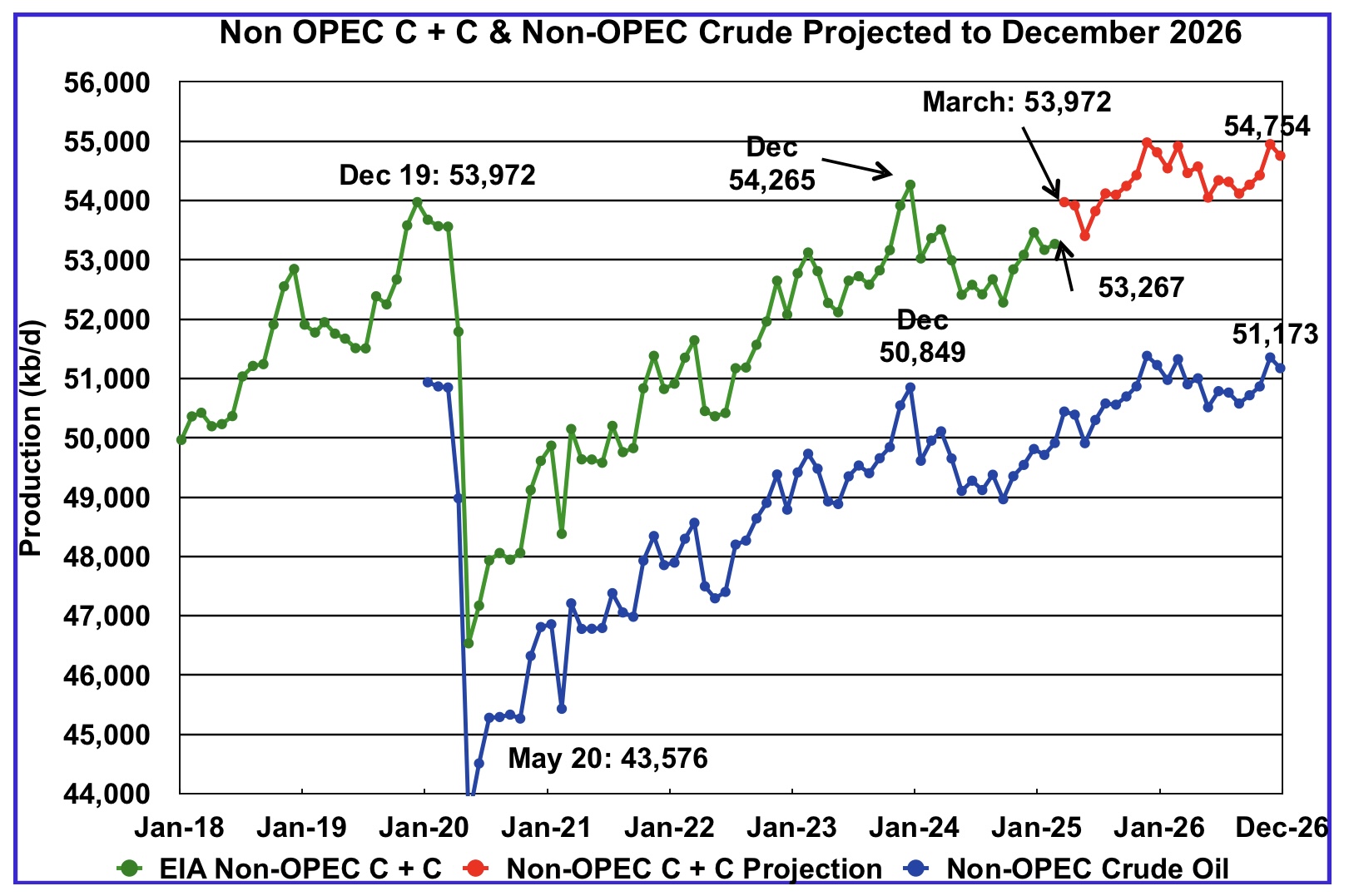

World oil production increased by 267 kb/d in February to 82,431 kb/d, green graph. The largest increase came from the Kazakhstan, 254 kb/d largely ‘offset by Canada’s drop nof 232 kb/d. March World oil production is projected to increase by 972 kb/d to 83,403kb/d.

This chart also projects World C + C production out to December 2026. It uses the June 2025 STEO report along with the International Energy Statistics to make the projection.

For December 2026, production is projected to be 84,069kb/d. The December 2026 oil production is lower than the November 2018 peak by 523 kb/d. December 2026 production has been revised up by 249 kb/d from the previous report.

From December 2023 to December 2026, World oil production is estimated to increase by 1,188 kb/d.

February’s World oil output without the US increased by 168 kb/d to 69,191kb/d. March production is expected to increase by 724 kb/d to 69,915 kb/d.

The STEO is forecasting that December 2026 crude output will be 70,716kb/d. Note that the December 2026 output is 1,969 kb/d lower than the November 2018 peak of 72,685 kb/d.

World oil production W/O the U.S. from March 2025 to December 2026 is forecast to increase by a total of 801 kb/d.

A Different Perspective on World Oil Production

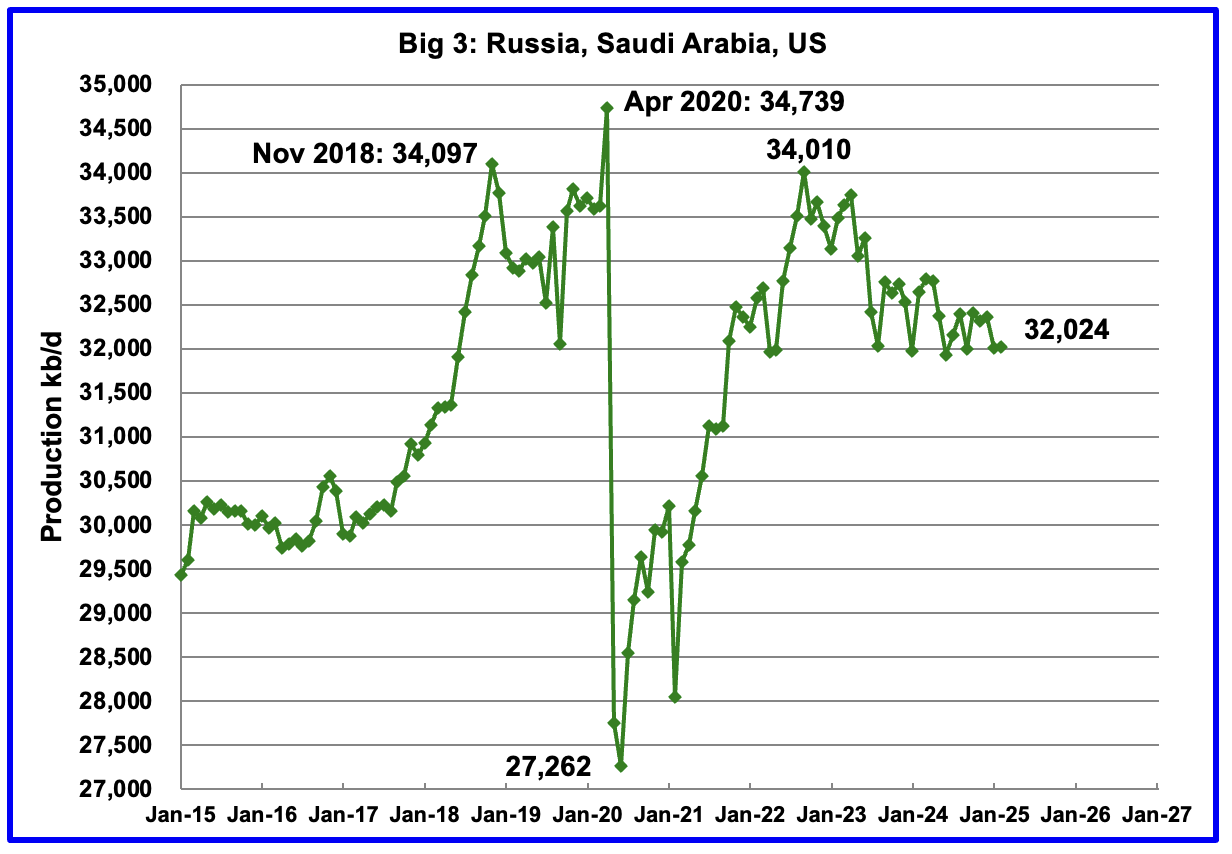

February’s Big 3 oil production increased by 19 kb/d to 32,024 kb/d. Production in February was 1,986 kb/d lower than the September 2022 post pandemic high of 34,010 kb/d. OPEC has announced it will start increasing production in May so the 1,986 kb/d drop should start to get smaller.

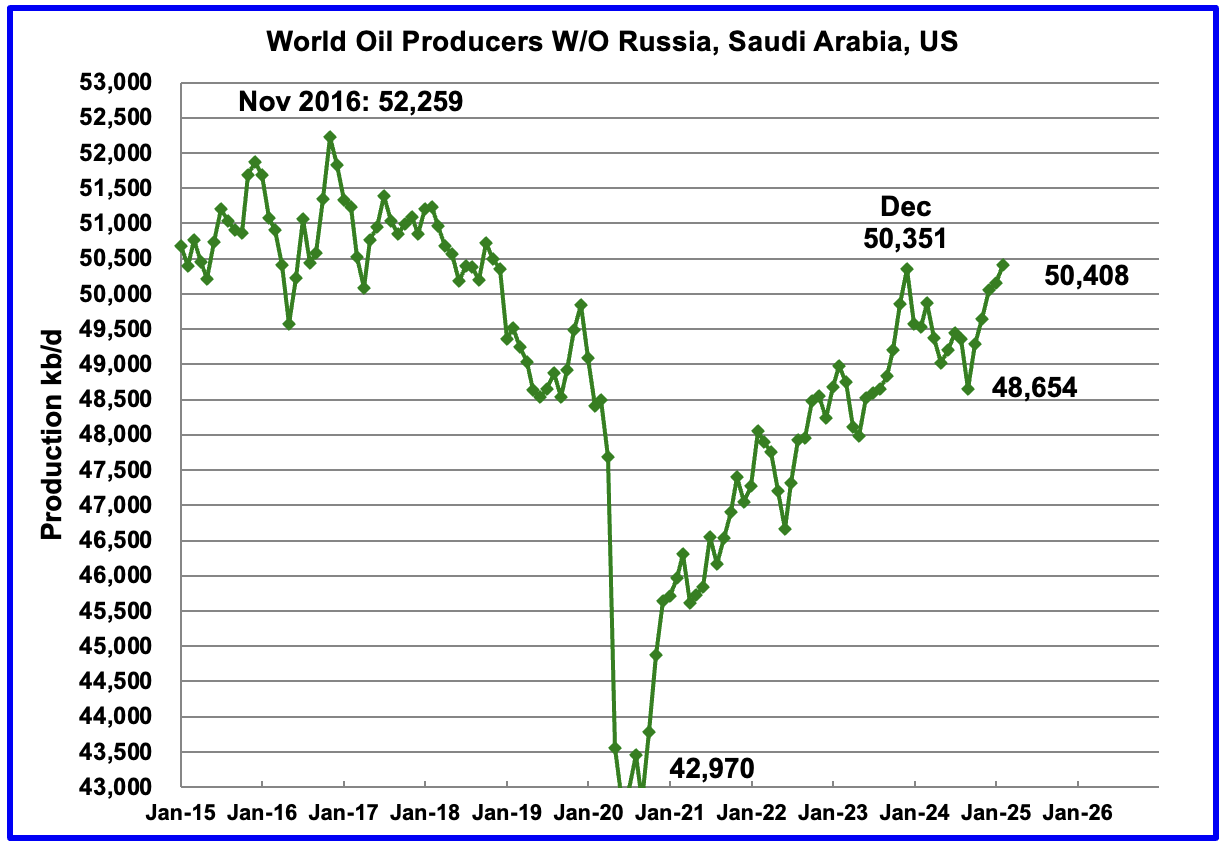

Production in the Remaining countries had been slowly increasing since the September 2020 low of 42,970 kb/d to December 2023. Production has risen for the last five months and output in February increased by 248 kb/d to 50,408 kb/d and is now 57 kb/d higher than December 2023.

Countries Expected to Grow Oil Production

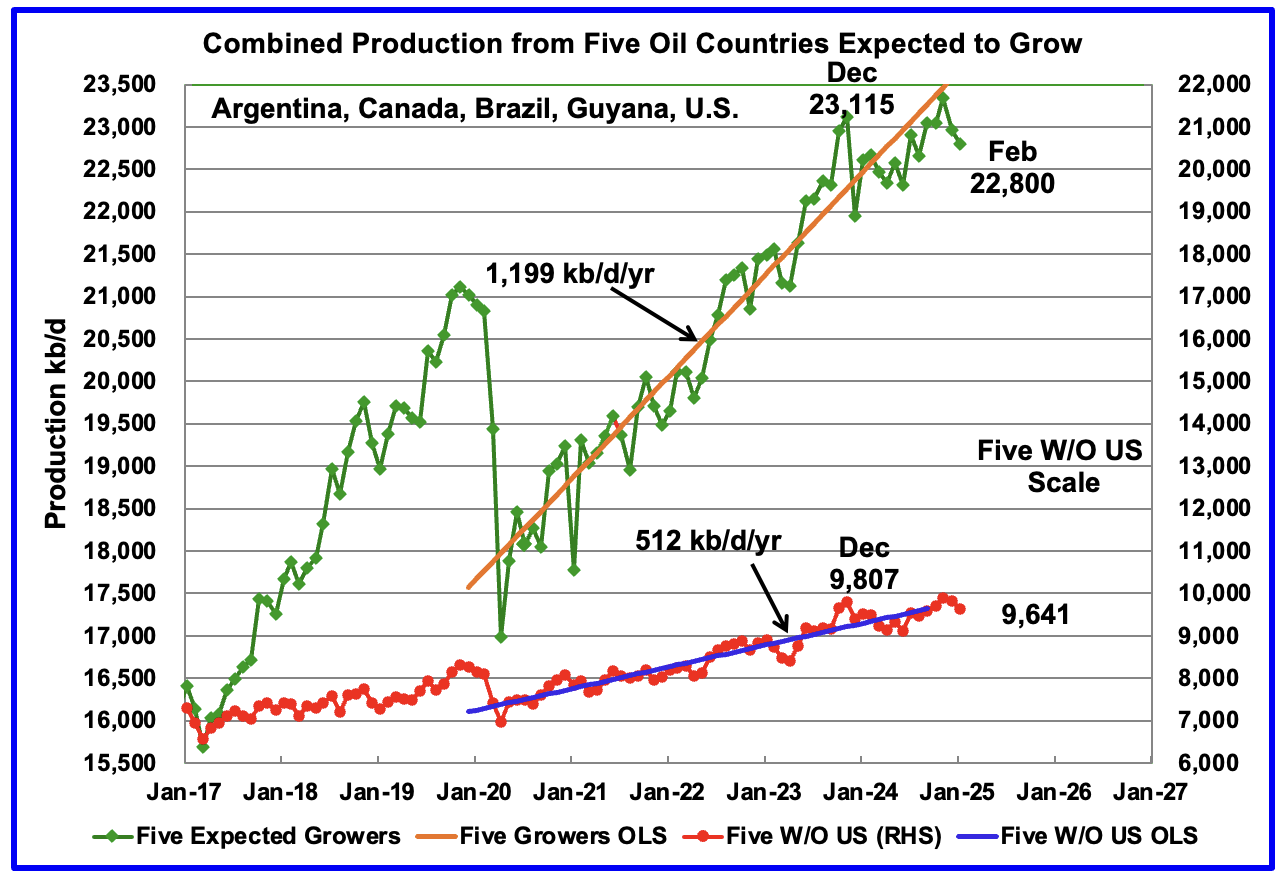

This chart was first posted a few of months back and shows the combined oil production from five Non-OPEC countries, Argentina, Brazil, Canada, Guyana and the U.S., whose oil production is expected to grow. These five countries are often cited by OPEC and the IEA for being capable of meeting the increasing World oil demand for next year. For these five countries, production from April 2020 to August 2024 rose at an average rate of 1,199 kb/d/year as shown by the orange OLS line.

To show the impact of US growth over the past 5 years, U.S. production was removed from the five countries and that graph is shown in red. The production growth slope for the remaining four countries has been reduced by 687 kb/d/yr to 512 kb/d/yr.

February production has been added to the five growers chart, down 163 kb/d kb/d to 22,800 kb/d. For the Five growers W/O U.S. January production dropped to 9,641 kb/d, down 192 kb/d from January 2025 and is 166 kb/d lower than December 2023.

The OLS lines have not been updated and will not be updated going forward unless additional production data provides a strong indication that production is rising/changing.

Production up to December 2023 may be a situation where the past is not a good indicator of the future. In this case it may be more important to focus on what has happened to production after December 2023 rather than before.

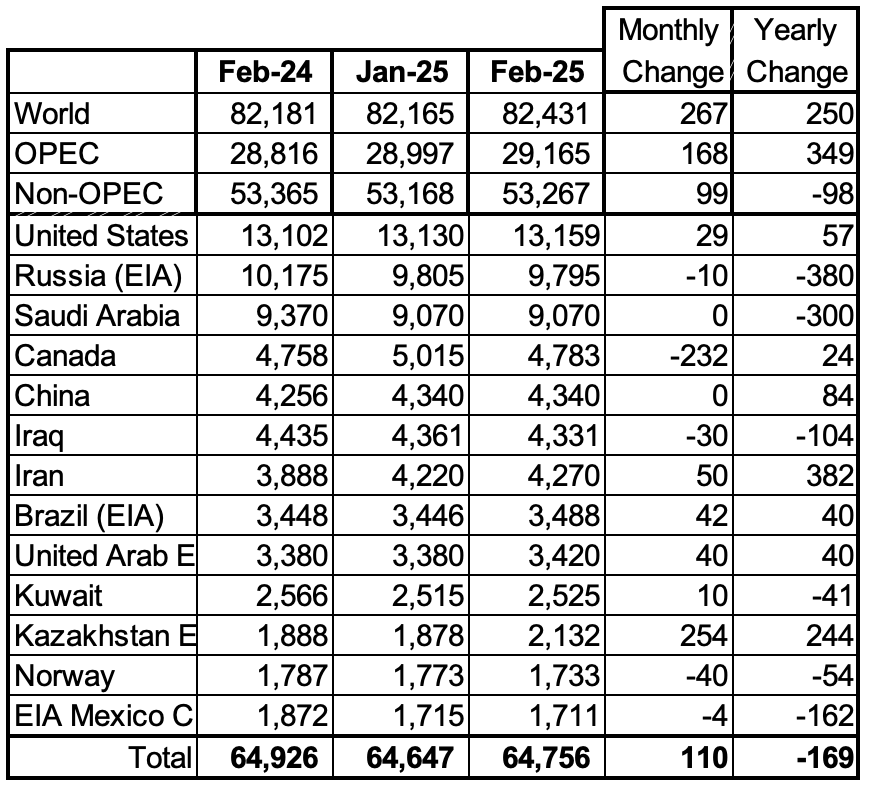

Countries Ranked by Oil Production

Above are listed the World’s 13th largest oil producing countries. In February 2024, these 13 countries produced 78.6% of the World’s oil. On a MoM basis, production increased by 110 kb/d in these 13 countries while on a YOY basis, production dropped by 169 kb/d.

February Non-OPEC Oil Production Charts

February’s Non-OPEC oil production increased by 99 kb/d to 53,267 kb/d. March is expected to add 705 kb/d to 53,972 kb/d.

Using data from the June 2025 STEO, a projection for Non-OPEC oil output was made for the period February 2025 to December 2026. (Red graph). Output is expected to reach 54,754 kb/d in December 2026.

From March 2025 to December 2026, oil production in Non-OPEC countries is expected to increase by 782 kb/d.

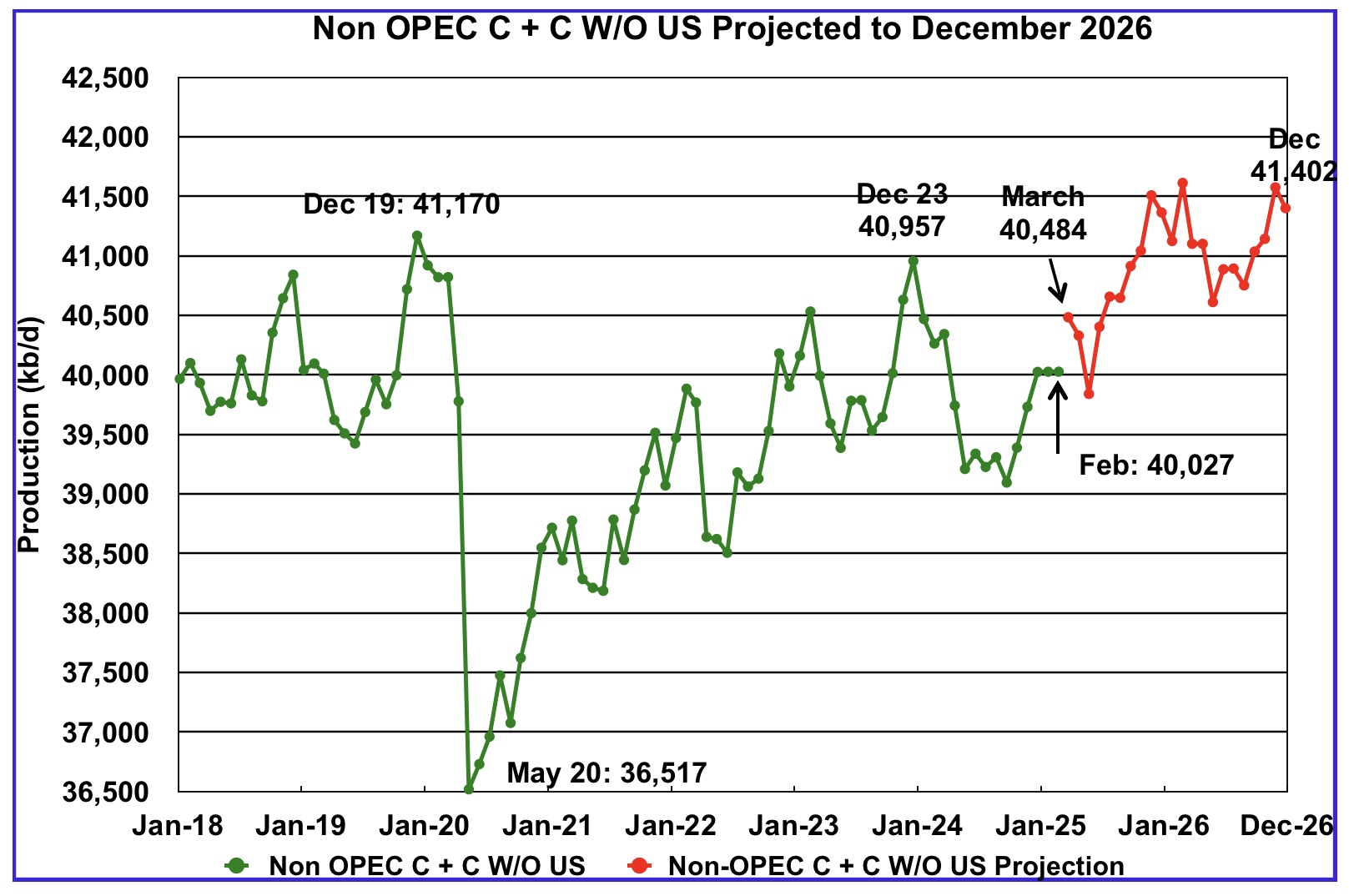

February’s Non-OPEC W/O US oil production was unchanged at 40,027 kb/d. March’s production is projected to rise by 457 kb/d to 40,484 kb/d.

From March 2025 to December 2026, production in Non-OPEC countries W/O the U.S. is expected to increase by 918 kb/d. December 2026 production is projected to be 230 kb/d higher than December 2019, essentially no growth over seven years.

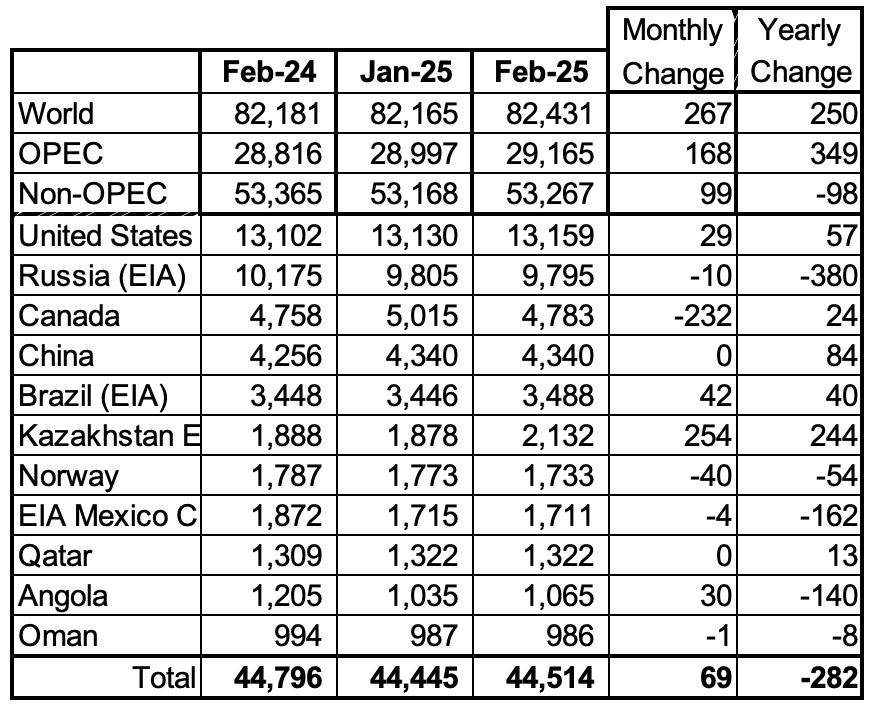

Non-OPEC Oil Countries Ranked by Production

Listed above are the World’s 11 largest Non-OPEC producers. The original criteria for inclusion in the table was that all of the countries produced more than 1,000 kb/d. Oman has recently fallen below 1,000 kb/d.

February’s production increased by 69 kb/d to 44,514kb/d for these eleven Non-OPEC countries while as a whole the Non-OPEC countries saw a yearly production decrease of 98 kb/d to 53,267 kb/d.

In February 2024, these 11 countries produced 83.6% of all Non-OPEC oil.

Non-OPEC Country’s Oil Production Charts

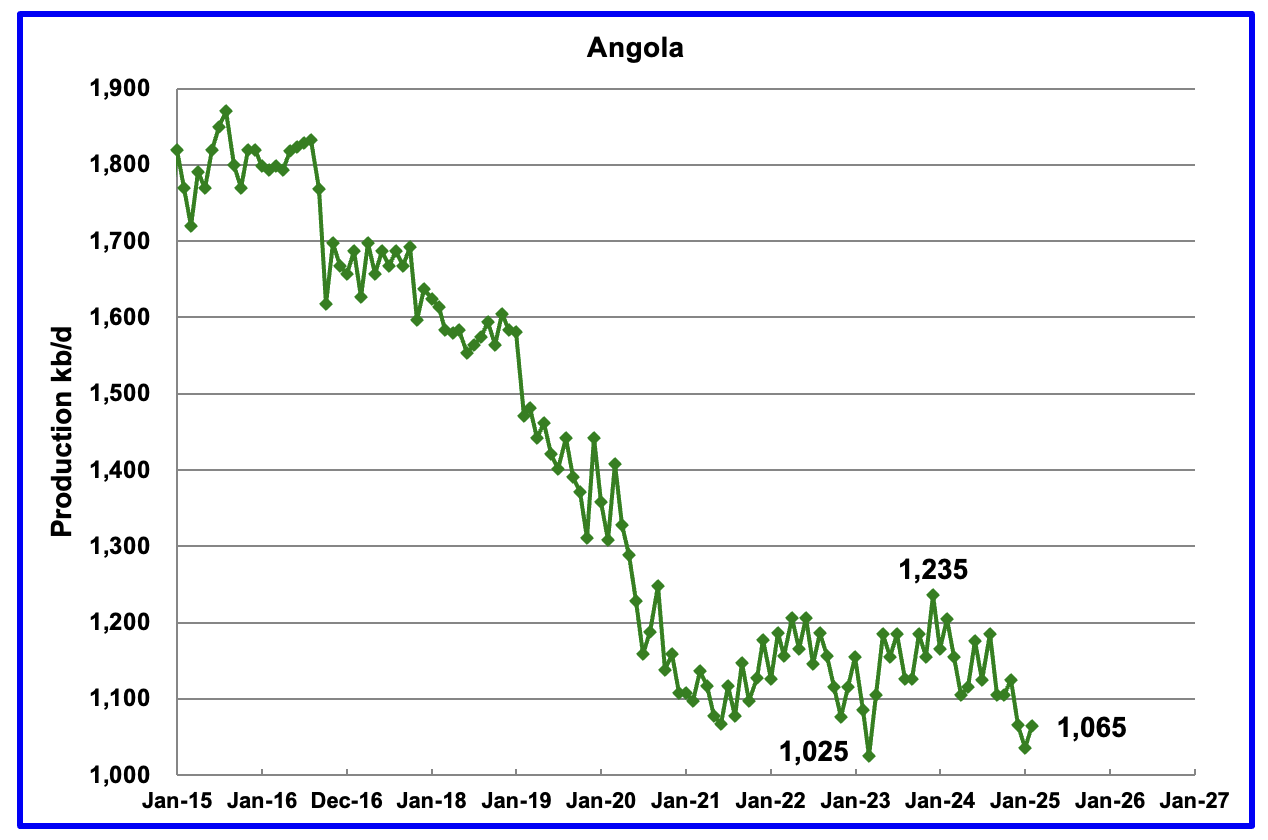

Angola’s February production added 30 kb/d to 1,065 kb/d. Since early 2022 Angola’s production settled into a plateau phase between 1,100 kb/d and 1,200 kb/d. However December to February brought a drop below the lower plateau.

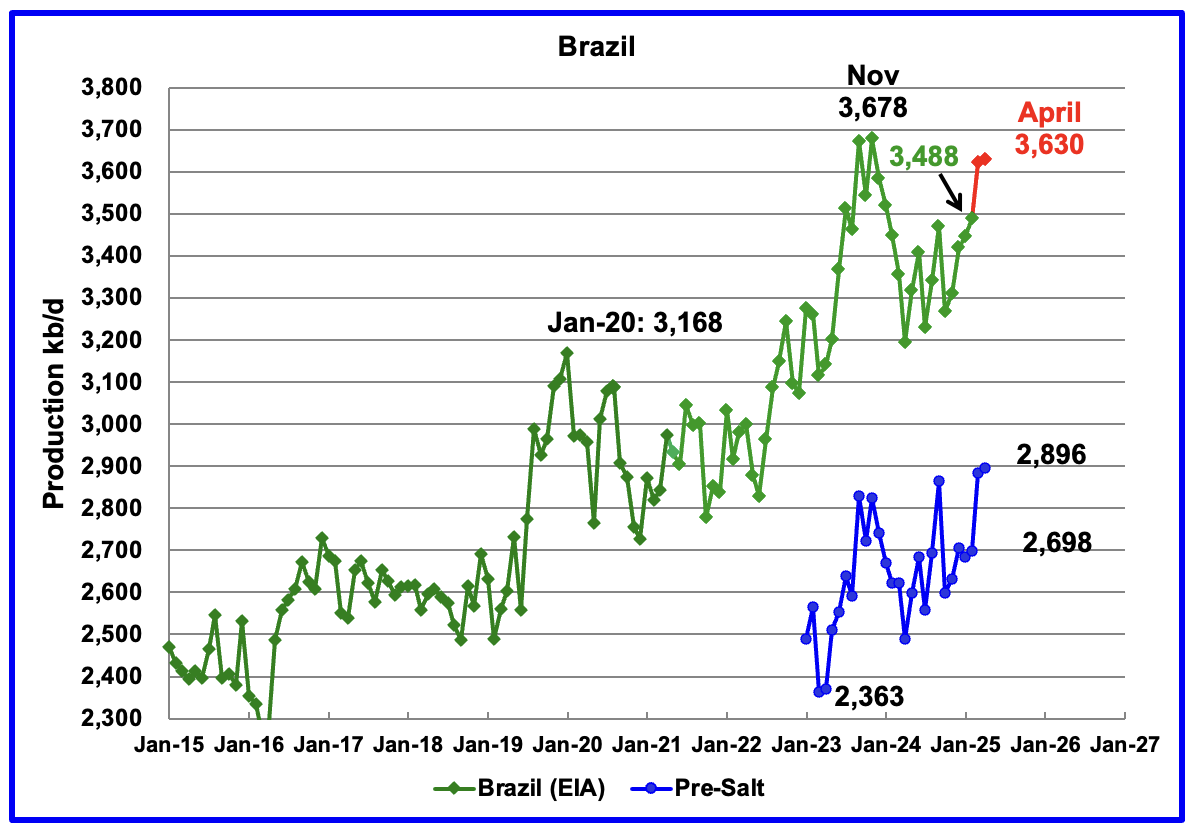

The EIA reported that Brazil’s February production increased by 42 kb/d to 3,488 kb/d.

Brazil’s National Petroleum Association (BNPA) reported that production increased in March and April to 3,630 kb/d. The pre-salt graph tracks Brazil’s trend in the oil graph. For April, pre-salt production increased by 13 kb/d to 2,896 kb/d, a new high.

The February to March increase could be related to the addition of the two new floating platforms. The December OPEC report states that two new floating production storage and offloading (FPSO) platforms came online in November. It also mentions operational issues and slow ramp-ups in several offshore platforms continue to be an issue. Perhaps this explains the delayed March production ramp up.

The April OPEC report states that the March crude increase was “supported by production ramp-ups from recently operated FPSOs.

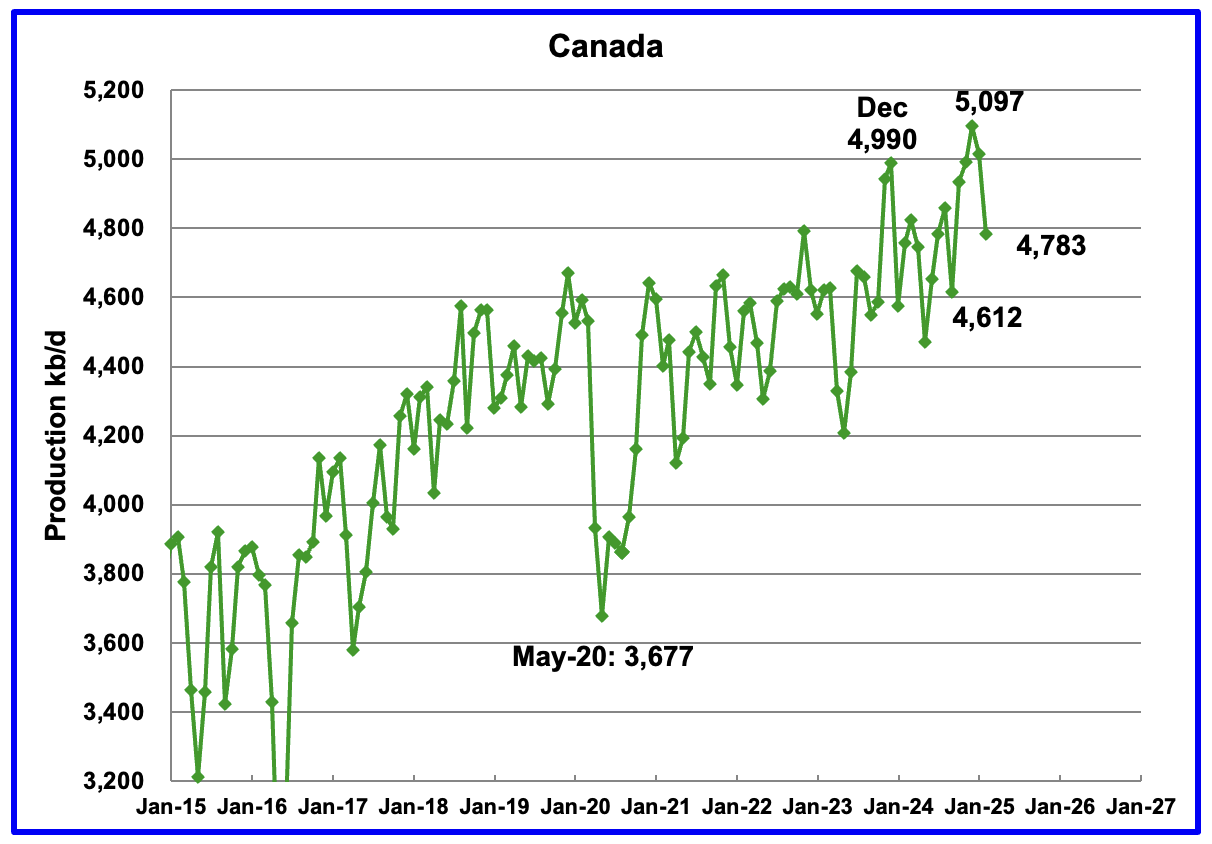

Canada’s production decreased by 232 kb/d in February to 4,783 kb/d after hitting a new high of 5,097 kb/d in January. Oil sands operations in February in the very cold Fort McMurray region are very difficult.

The Alberta premier is asking that the new Prime Minister Carney ease the anti oil sands policies of the previous government. The Alberta premier is asking for another pipeline to the west coast. However according to this Article the BC premier is not supportive of the plan.

The EIA reported China’s February oil output was unchanged 4,340 kb/d.

The China National Bureau of Statistics reported production for March and April. The Bureau reported that March oil production surged to a new high of 4,480 kb/d before falling in April back to 4,313 kb/d. Previous highs have not seen such a huge drop the following month.

On a YoY basis, China’s February production increased by 84 kb/d from 4,256 kb/d.

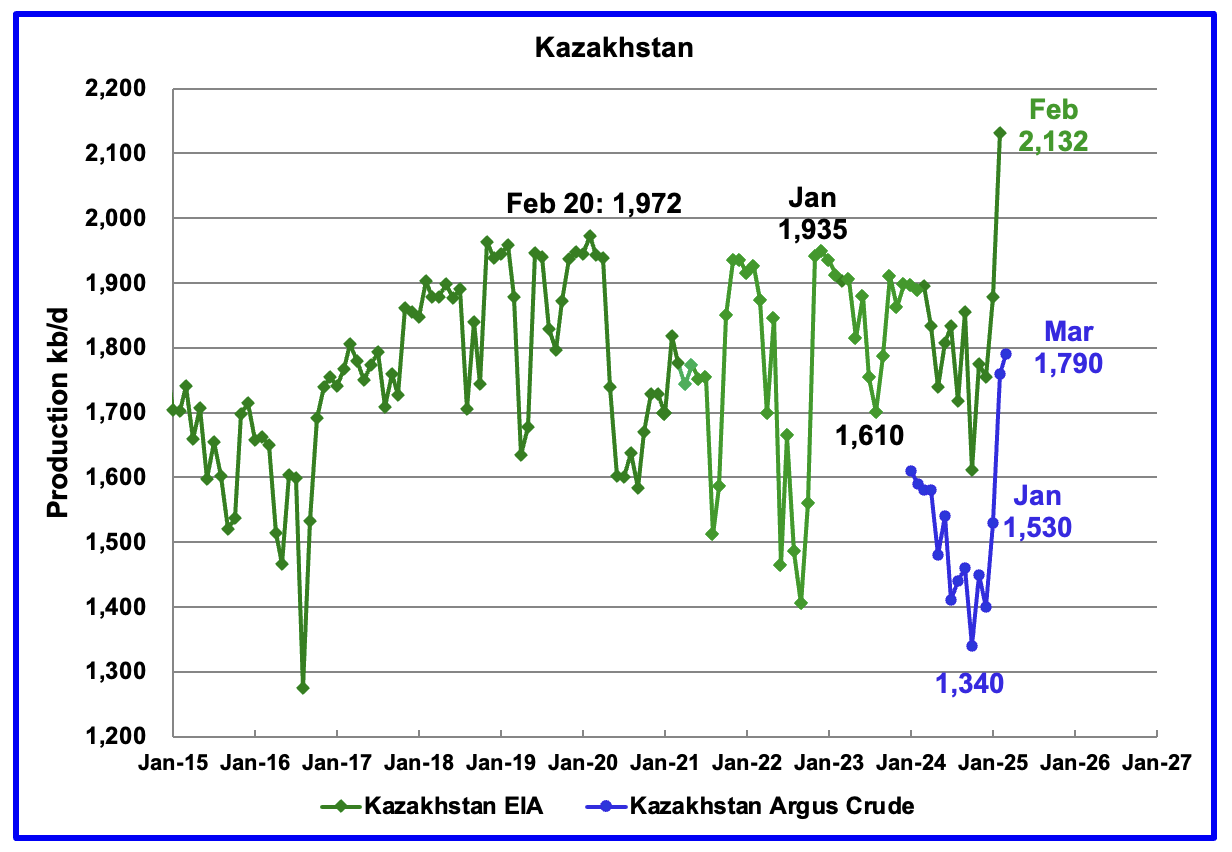

According to the EIA, Kazakhstan’s oil output increased by 254 kb/d in February to 2,132 kb/d, a new record high.

Kazakhstan’s recent pre-salt crude oil production, as reported by Argus, has been added to the chart. In October pre-salt crude production dropped by 120 kb/d to a low 1,340 kb/d. Since then production has risen by 450 kb/d. February/March production came in at 1,790 kb/d due to a New Field coming online. Note this is crude whereas the EIA’s numbers are C + C.

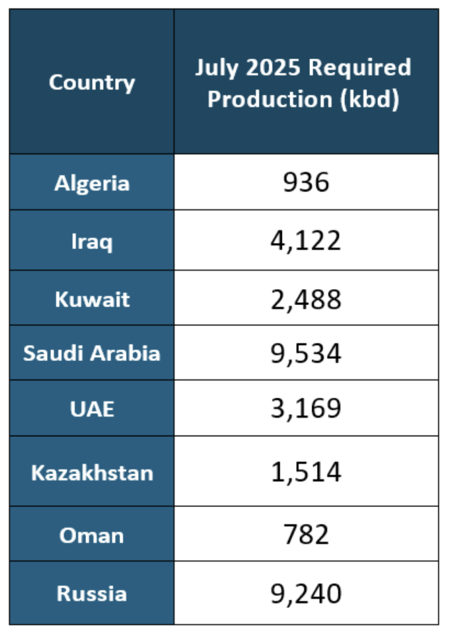

Kazakhstan’s July OPEC crude production target is 1,514 kb/d. At 1,790 kb/d, Kazakhstan is 276 kb/d over their target. According to this Article, Kazakhstan says it has no plans to cut oil production this month (May) after massively exceeding its Opec+ target in March.

Since Kazakhstan’s reduction promises have not materialized, OPEC announced it would “accelerate plans to revive halted supplies in May/June/July, with an increase triple the size originally scheduled of 411 kb/d in each of May/June/July”.

OPEC is trying to send a message to Kazakhstan to comply with its production target, but they are not listening.

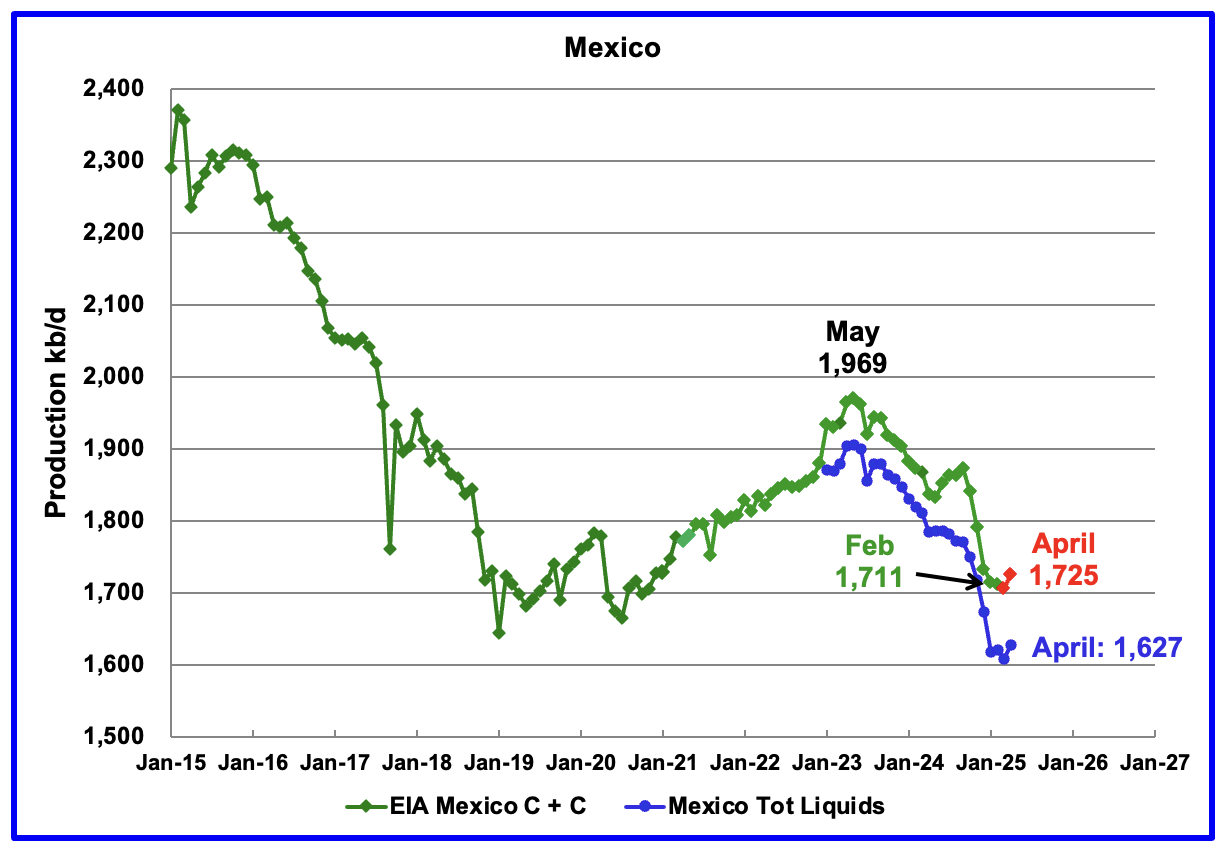

According to the EIA, Mexico’s February output dropped by 4 kb/d to 1,711 kb/d.

In June 2024, Pemex issued a new and modified oil production report for Heavy, Light and Extra Light oil. It is shown in blue in the chart and it appears that Mexico is not reporting condensate production when compared to the EIA report.

In earlier reports, the EIA would add close to 55 kb/d of condensate to the Pemex report. However for October and November it was increased to 122 kb/d and 117 kb/d respectively. For December, the condensate addition returned close to its original increase of 55 kb/d. The February addition was 98 kb/d.

For March and April production, 98 kb/d have been added to Pemex’s production to estimate Mexico’s March and April C + C production, red markers. Note that Mexico’s production for the last four months has stabilized at slightly more than 1,600 kb/d according to Pemex.

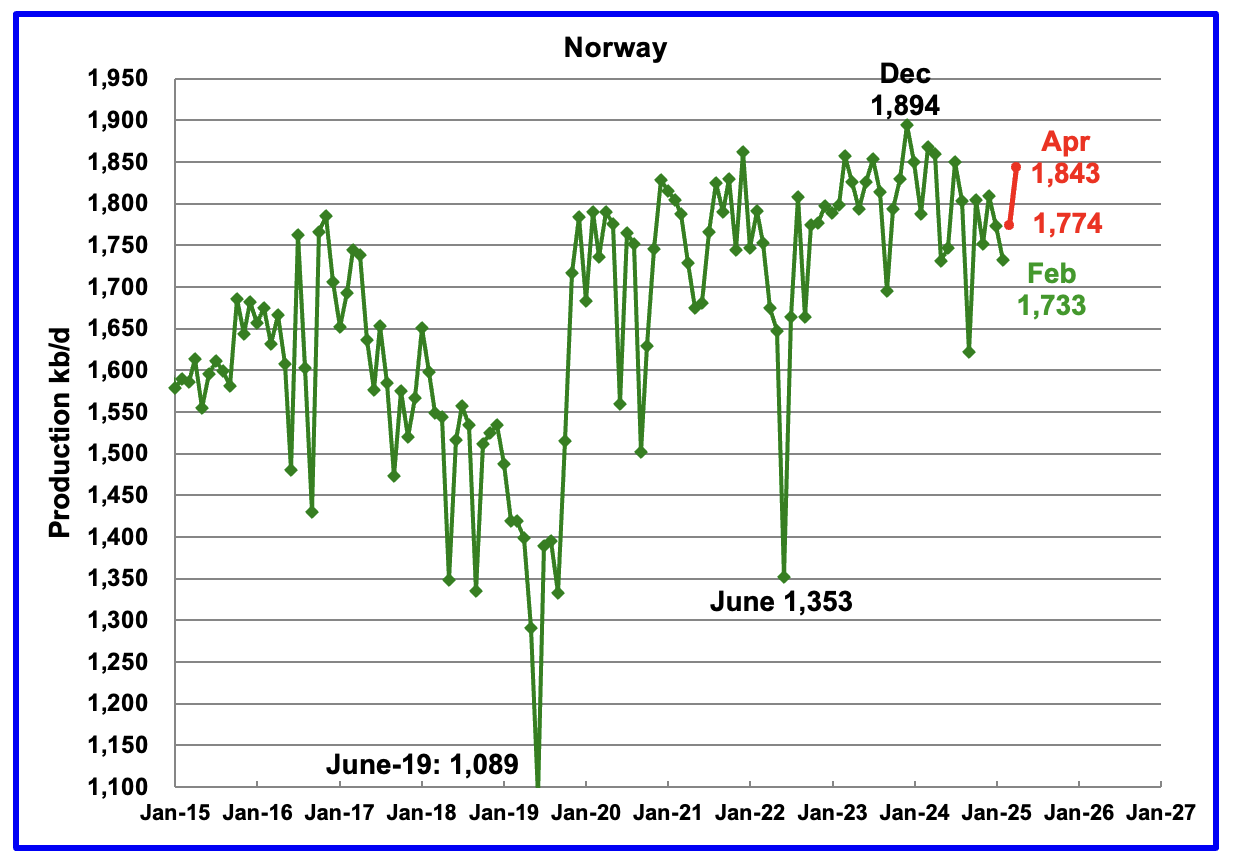

The EIA reported Norway’s February production declined by 40 kb/d to 1,733 kb/d.

Separately, the Norway Petroleum Directorate (NPD) reported that March production rose by 41 kb/d to 1,774 kb/d and April added another 69 kb/d to 1,843 kb/d, red markers.

The Norway Petroleum Directorship reported that April’s oil production was 3.5% above forecast.

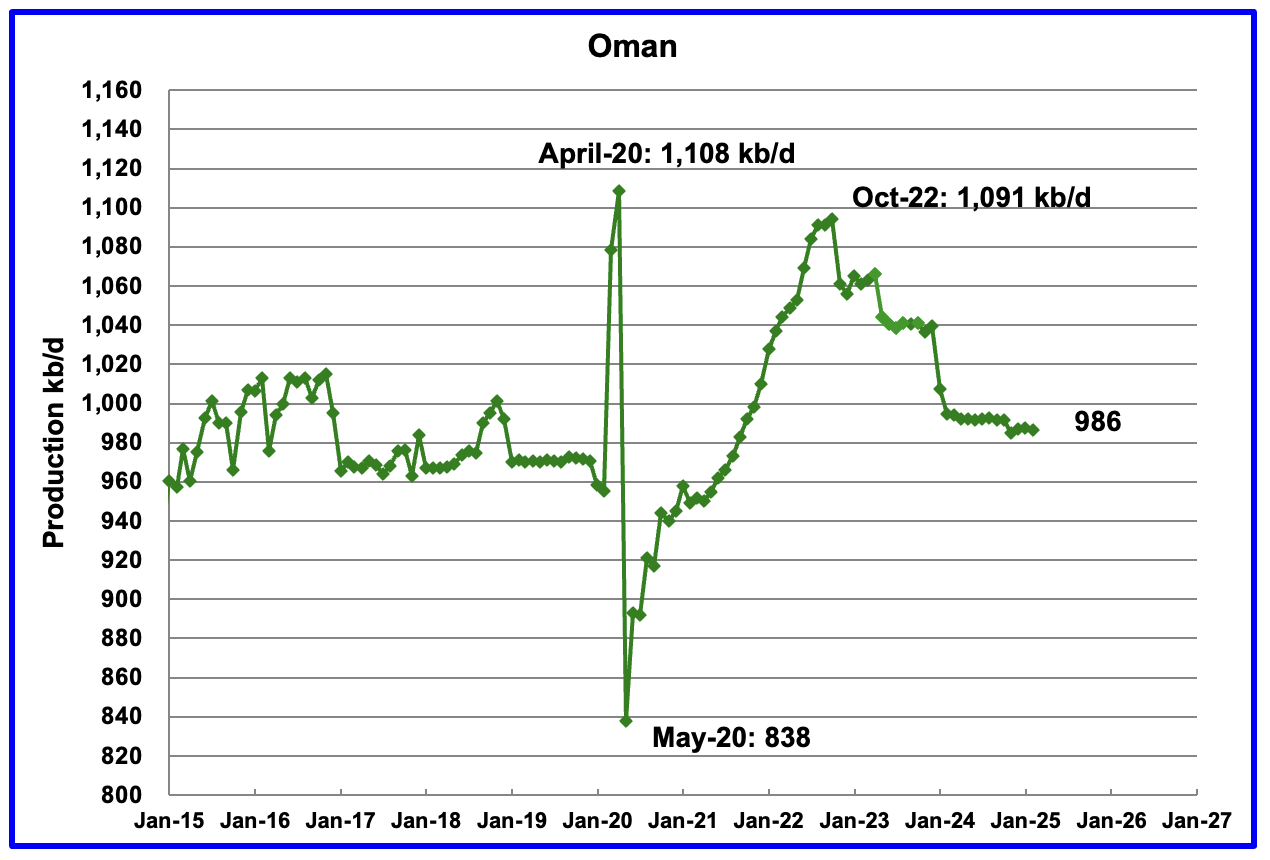

Oman’s production had risen very consistently since the low of May 2020. However production began to drop in November 2022. According to the EIA, February’s output dropped by 1 kb/d to 986 kb/d.

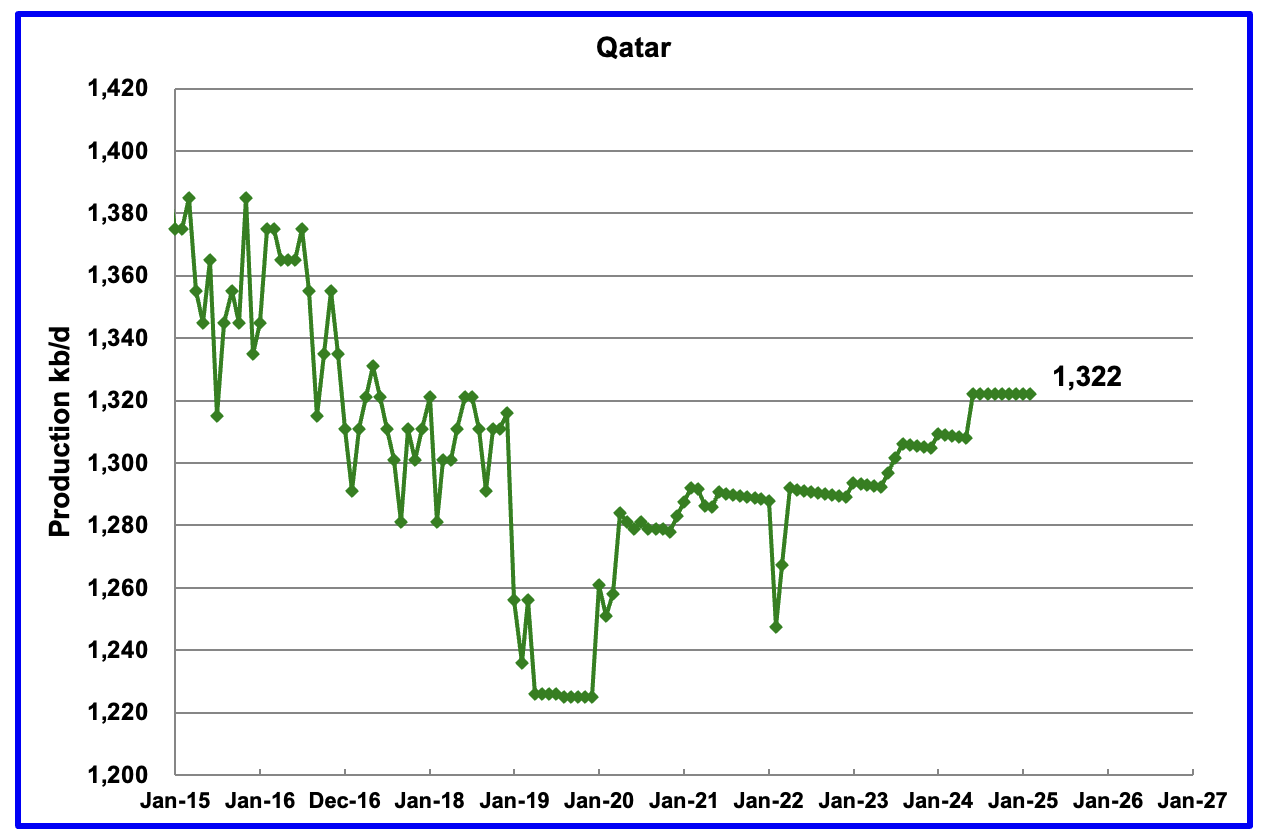

The EIA had been reporting flat output of 1,322 kb/d for Qatar since early 2022. However the EIA revised down all of the previous production data up to April 2024. May 2024 production reverted to 1,322 kb/d. Qatar’s February output was reported again to be 1,322 kb/d.

The EIA reported Russia’s February C + C production dropped by 10 kb/d 9,795 kb/d and was down 465 kb/d from March 2024.

Using data from Argus Media reports, Russian crude production is shown in the blue graph. For March 2025, Argus reported Russian crude production was 8,970 kb/d. Adding 8% to Argus’ March crude production provides a C + C production estimate of 9,688 kb/d for Russia, which is a proxy for the Pre-War Russian Ministry estimate, red markers.

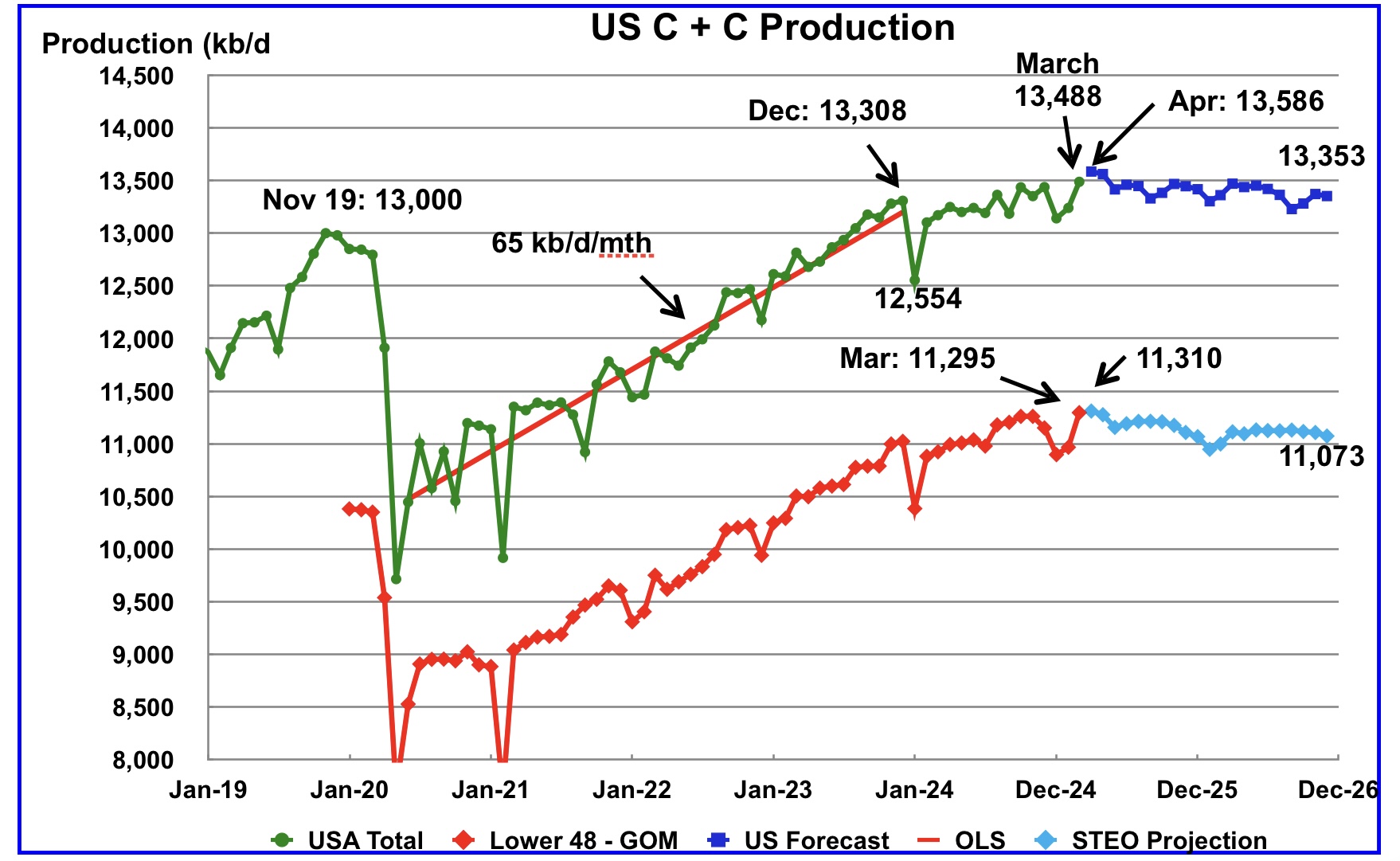

This US production chart is very similar to the one published last week in the US update post. However the STEO portions of the two graphs have been updated using the June 2025 STEO.

Production in December 2026 is expected to 13,353 kb/d. Production starts dropping in May.

Normally, Argentina’s oil production is not reported because its production is lower than 1,000 kb/d. However production has been steadily rising over the last five years due to the startup of shale oil and gas production in the Vaca Muerta basin.

For February, the EIA reported Argentina’s production dropped by 3 kb/d to 745 kb/d.

The Argentinian Energy Secretariat reported oil production in March rose by 2 kb/d to 747 kb/d and dropped by 29 kb/d to 718 kb/d.

Is Argentina’s production growth about to slow on its way to an expected 1,000 kb/d a few years down the road?

57 responses to “February World and Non-OPEC Oil Production”

Great job Ovi. Thank you.

The new STEO looks more reasonable, but I think flat output in April and May at roughly the March 2024 level is a bit more likely with the June 2025 to Dec 2026 part of the forecast looking fairly realistic for the oil prices forecast in the STEO.

On Kazakhstan, they could remain a member of OPEC plus like Mexico that does not have an output quota or could choose to leave OPEC plus if they decide being a member has no benefit.

Dennis

Thanks.

Not sure if you are referring to the US or the whole STEO. I agree the US part of the STEO looks more reasonable.

Looking at the World production jump for March, there are sizeable jumps for Kazakhstan, China and Brazil. Canada could rebound in March from its weather related February drop. It could be a one month wonder. The large jump also shows up in thec rude chart.

As for Kazakhstan, one has to wonder why they joined OPEC . What benefits do they get by joining.

Ovi,

I was only referring to the projection fro US C plus C, for the World things are less clear.

Israel Attacks Iran… Oil Goes BOOM!

It looks like things are about to get a lot more interesting, above and beyond the Orange Clown Show taking place in DC.

Also… I forgot to mention… Gold also Goes BOOM!

steve

Steve, you have been spot on regarding Gold.

SHALLOW,

I actually thought we would see a bit of a correction in the gold price back in Q3-Q4 2024, but then Trump got elected, and dangled the Tariff issue.

This caused serious havoc in the Gold Futures Market, as Banks that tend to be short due to hedging could suffer 25% losses if Tariffs impacted gold. So, massive Gold Flows from the LBMA and elsewhere into the New York COMEX occurred, driving up the EFP—Exchange For Premium and thus much higher prices.

This Imbalance continues, and now, adding more juicy “War” Geopolitics, we could see much higher Gold prices, and maybe Silver. But at some point, I do think we will see U.S. and global economic weakness Q3-Q4 2025, that could negatively impact the Broader Markets, Energy, and the metals.

But, before then… who the hell knows what is going to happen when we add more WAR fireworks to the Orange Clownshow Uncertainty.

steve

Did Andre The Giant predict an attack on Iran for them trying to assassinate Donald Trump?

Yes, Yes, he did….he did

OVI break out the predictions!

Why would Israel attack Iran due to an assassination attempt on Trump?

They have been wanting to do it. Got the nod from USA.

USA 7th fleet controls that area.

Amazing coincidence!

https://www.usatoday.com/story/news/world/2025/06/14/iran-reuters-trump-israel/84200412007/

“We knew everything” – Trump

https://oilprice.com/Energy/Energy-General/Oil-Prices-Soar-After-Israel-Targets-Irans-Nuclear-Program.html

Above is a nice summary of recent Oil and gas news

Also

https://oilprice.com/Latest-Energy-News/World-News/Oil-Prices-Surge-Over-8-as-Iran-Retaliates-With-Major-Missile-Strike-on-Israel.html

Excerpt:

Oil market watchers are also bracing for further escalation. Analyst Daan Struyven at Goldman Sachs raised his short-term price target, warning that the conflict could briefly cut 1.75 million bpd of Iranian oil, pushing Brent above $90, but expects prices to fall back to the $60s by 2026 as supply recovers.

…

Still, some are skeptical the rally can last. Spare capacity from OPEC+ members like Saudi Arabia and the UAE, along with potential increases in U.S. shale output, could ease the impact of any short-term supply shock.

My guess is that if this stays under control with just some back and forth from Israel and Iran without hitting major oil and gas facilities that in two weeks WTI oil prices will fall back to under $65/bo as OPEC plus increases output.

Chris Wright probably was pre- informed of the war now.

As supply recovers? Where did his crystal ball that expands on the reasons for that come from? His arse?

“Oh, there’ll be short term pain, but once the nukes fly we think things will begin to settle again as volatility along with all complex life ceases to be an issue.”

Why do we listen to these guys, exactly?

The oil price increase seems like pure panic to me. Iran produces less than 5% of world output and OPEC is struggling with excess supply anyway, or claims to be.

It’s not up that much IMO. Back to where it was before Trump started his tariff stuff. That’s it.

Shallow Sand,

I agree not that big an increase in oil prices, but if this price should stick, it might be enough to bring some rigs back to tight oil plays. I think oil prices may drop if OPEC increases output as much as they claim in the next few months.

Any uptick in oil prices will have a deflationary effect on global economy. Bond yields in China, the entire yield curve under 2% is screaming loud and clear. No growth and no inflation are expected in China.

Currently the $12 or so uptick in oil prices might just be enough to send the global economy into an official recession. If oil gets back to $80-$90 or higher. The greater the cooling effect on the economy will be.

The global economy is neither strong or resilient.

Total lack of inflation due to tariffs.

People are worried about price increases in a low to zero growth environment makes no sense.

The Big beautiful bill will likely not be inflationary. It’s likely not big enough to offset the contraction in global dollar funding that is in the works.

$72 is not a high oil price. It didn’t cause a global recession in 2023-24, and it wont now either.

I guess maybe I need to know your definition of global recession. There have been four since WW2 according to the IMF. 1975, 1982, 1991 and 2009.

The desire for extremely low oil prices is so strong. Trump wants $50 or below, for example.

Well gee, I wish my McDonald’s breakfast wasn’t over $10, but it is. It was $5 in 2012 when oil was $90-$100.

Now tariffs might do a lot of damage, but don’t blame $72 oil on an economic slowdown.

China is the new Japan. They will never have growth over 1-2% ever again. Regardless of what they publicly say they have.

I’ll put some numbers to it. Over the last 40 years the Chinese banking sector has loaned out in dollar terms $60 trillion. These aren’t dollar denominated loans. These are yuan denominated loans. Most of these loans have a 4-5% interest rate attached to them.

The Chinese economy is 3 times as leveraged as the US economy.

Got growth? The reason the Chinese are buy gold isn’t about the dollar I can assure you.

Deflationary tsunami brewing over in China. Looking over in Europe. Inflation is back below

2%.

We had a supply side shock due to Covid and government lockdowns.

We greatly increased debt across the board. The growth required to repay the debt will be missing.

We will keep adding debt but the growth will never come.

The war. Best to not do black and white hats.

Before Israel tightened down media there was rather a lot of footage of explosions and fires around Tel Aviv and elsewhere.

This, frankly, is the only thing that matters. We are witnessing the destruction of the narrative of Iron Dome and Patriot systems. They don’t stop enough, and if you have nukes just one getting through is the end.

So Iran and Hormuz? If your goal is to destroy US shale, you don’t want higher oil prices. Russia’s exports remain 6 mbpd (until about 2 weeks when the new Bible releases) and a few dollars more per barrel is rather less important than crushing US shale output. One suspects this will be discussed with Iran.

Also btw, there were rumors of Israeli plane / pilot capture. Instantly denied, of course. But if even one F-35 goes down, that wreckage will be in Moscow within hours.

Iran’s nuclear facilities were just the first target. The oil and gas infrastructure is next. The fact that the Iron Dome is getting overwhelmed by sheer volume. Pretty much insures that more has to be done inside of Iran. Not less.

I’d expect the goal will have to be changed to make the light go out in Iran. 14 days of strikes won’t be enough.

Oil gave back a bunch of the gains by closing on Friday. Closed about $5 lower than the highs. But when it becomes clear that all the oil infrastructure is being targeted too. That is oil and gas that won’t be coming back online anytime soon.

We will have much higher oil prices on an economy that’s already struggling.

The Hormuz might come into play as an act of desperation. At that point it isn’t just the Iranian oil coming offline.

If Moscow really wanted to inflict damage on the rest of the world they don’t have to use nuclear weapons. All they have to do is stop exporting oil and gas. The global economy would absolutely fucking implode. If done abruptly.

Why export oil and gas to China so China can send cheap solar panels to Europe? If Russia really wanted to hurt the West all they have to do is close up shop.

HHH & et al,

The next several days and week, will undoubtedly be quite interesting. Iran has been claiming it has thousands of missiles hidden underground and will, QUOTE, “Rain Down Hard on Israel & the United States, if attacked.”

Furthermore, Iran claims it also has hypersonic missiles, called the Fattah, which several could take out any Large U.S. Aircraft Carrier… as defense against hypersonic missiles is quite challenging at best.

Thus, if Israel, with the assistance of the United States decide to “Escalate” the attacks on Iran to destroy Iran’s Oil & Gas Infrastructure & Attempt to take down the National Grid… Then, we would find out once and for all if the Iranian Regime was just BRAGGING about their Attack Capabilities or not.

If Iran was mostly bragging, then this won’t be much of a challenge… we will see.

GRAB YOUR POPCORN.

steve

BBC News just had a banner with the IDF saying no rockets hit Haifa.

This was ten minutes after I watched a half dozen videos of a dozen plus ballistic missiles rain down on the place with very obvious impacts. The censoring is gonna run into some major problems when reality is hitting the people you’re trying to fool.

And this is before Iran uses any of the masses of drones and modern hypersonics they’ve got to go with the tens of thousands of MRBM and IRBMs.

Israel has massively fucking miscalculated here. I think they, and the US, expected a decapitation strike and internal regime change deal, like Putin did with Ukraine by a simple show of force. Iran has managed to get its shit together faster than I expected after being caught totally flat footed before. They won’t be making that mistake a second time.

They’ve also got oil and gas fields alight right now. So the gloves are off for critical infrastructure.

Straight of Hormuz?

Any thoughts on this from those with a strong chemical engineering background?

“MIT adapts desalination tech to filter crude oil, offering a greener, scalable alternative to energy-intensive refining”

https://interestingengineering.com/energy/crude-oil-energy-reduction-membrane

This is nothing new and not likely to make any impact at all. Oil co’s are conservative and any new technology takes decades to be accepted. What we are being told is BS and all that is required is yet another grant for research. Also known as grifting.

The cited example is hardly groudbreaking. Separating C7 toluene from C15 tri-isoproylbenzene . Big deal. Membranes have been used for years- ultrafiltration -but their application in a refinery where the carbon numbers range from C1 all the way to C50 means that there will be mutliple types of membranes all requiring pumping and in some cases heating to reduce viscosity. Then there are to different species- paraffins, iso paraffins, naphthenes and aromatics, many of which will have side chains and some being multi ring structures.

Separating iso paraffins from normal paraffins is a possibility and likewise paraaffins from aromatics will also work in some cases. But separating crude oil into LPG, naphtha, jet and diesel is wishful thinking. Zeolite mocecular sieves can do some separation but the applications are limited. Membranes are and will remain a niche.

Thank you Carnot. Appreciated.

Rig counts from Friday, June 13, 2025. US Horizontal Oil Rigs (HOR) excluding Ohio down 3 WOW and down 3 and Permian down 2 WOW. Other major tight oil basins unchanged WOW (week over week) including Bakken, Eagle Ford and Niobrara (these three basins have 66 rigs turning on June 13), other non-Permian basins (excluding Ohio) have 78 rigs running as of June 13.

Year over year (YOY) US HOR excluding Ohio are down 32 rigs, Permian is down 34 rigs, Eagle Ford down 15, Bakken down 4, and Niobrara down 5, this implies other basins besides big 4 (Permian, Bakken, Eagle Ford, Niobrara) are up 26 YOY.

US Horizontal Gas Rig (HGR) count. Count unchanged Week over week, up 10 YOY and up 16 since March 16, 2025.

Dennis

Thanks.

For our readers, I am on holidays for two weeks in Germany and Dennis has kindly agreed to fill in for me regarding the weekly rig report.

I have just checked the Frac report for June 13 and they are down 4 to 182, a new recent low.

The latest OPPEC MOMR is out with data for May. OPEC 12 was up 183,000 bpd and the other 10 of OPEC+ was down 3,000 bpd, fir a total change of up 180,000 barrels per day.

That big increase just did not happen.

Only Saudi Arabia had any significant increase. They were up 177,000 bpd. I think it highly likely that everyone else is producing near their peak and Saudi is not far from it.

Oil has already slipped this morning to $69 WTI.

To MAGA, that is still about $20 too high.

Shallow Sand,

The inflation or price increase have already happened. Average rent in the US is over $1600 a month. $70 oil is too high for the consumer.

I get that oil producers need higher prices. No arguing there. Oil is becoming uneconomical. Consumers can’t really pay more unless they cut spending elsewhere.

I read a startling report that something like 25% of everyone making $100,000 a year in the US are living paycheck to paycheck. And of course it’s because they are up to their eyeballs in debt.

Student loan debts have also kicked back in for 45 million Americans. Average payment $460 a month.

We are getting back to the conundrum of oil prices increasingly getting too low for producers and too high for consumers. Short term I am sure there are options to keep it all in some sort of balance. But longer term there is no option at all when it comes to keeping oil prices too low for too long. It would not work. The steel and aluminium prices keep going up along with wages. The falling demand due to various reasons make the math as to which people can afford higher oil prices in the industrial world very interesting – and also what can be afforded in developing world. That is not to be overlooked going forward. The availability of transportable gas and to a much lesser degree transportable coal comes into the picture too. That is why I am of the opinion that the overall energy market have the potential to move slowly over time – even given sudden shocks (it is just too big). And possibly metrics like joules of energy expenditure or joules per capita could become ever more useful.

Talking about oil specifically: there is also the possibilty that we are beginning to draw down storage capacity around the world not easily measured – then it is an open question at what rate and how long it can go on.

Took a quick look at recent USGS assessments of Uinta Basin from 2015 and 2016 see link below

https://www.usgs.gov/centers/central-energy-resources-science-center/science/uinta-piceance-basin-oil-and-gas

The Niobrara formation has a mean TRR of 74 million barrels (or 0.074 Gb) of oil (this primarily in Colorado) this study was published in 2015. The Uteland Butte member of the green River Formation is in Utah only and has 177 MMb in the continuous part of the formation and 37 MMb in the conventional part of the formation for a total of 214 MMbo. The total for both studies is 288 MMbo or 0.288 Gb. Utah has produced about 740 MMbo from 2000 to 2024, and about 340 MMbo since 2017, if we assume about 75% of this is from Uinta that would be close to the USGS mean TRR estimate, so that estimate might be on the low side.

See also

https://www.oilystuff.com/forumstuff/forum-stuff/the-next-great-shale-basin

that’s quite similar to what happened in Vaca Muerta,

the initial EIA estimate has gas to oil in VM TRR as 3:1, but in fact, it is 1:1 or even 1:2.

that’s the magic of Low-GOR-Black-Tight/Shale-Oil, where the EUR is much higher than high-GOR-Light-Tight/Shale-Oil. Similar thing might be happening for conventional oil in Gulf of America Deep water, where the Low-GOR-Black-Oil has obviously higher EUR and recovery and productivity than high-GOR-light-oil. The Uinta also started in the high GOR part and only changed to low GOR part 5 years ago and outperform Permian. see,

https://www.linkedin.com/pulse/uinta-rise-us-lacustrine-shale-oil-lowering-gor-sheng-wu-dajoc

Initially, VM was focusing on the higher GOR part, and oil was just as good as Permian at the best, with GOR over 3MCF/bbl. Oil EUR per well only started fly to 2X Permian best when they drilling in the low GOR (IP GOR<350scf/bbl) part where the blocks were actually considered before as close to zero BO TRR. See,

https://www.linkedin.com/pulse/low-gor-black-shale-oil-news-from-vaca-muerta-rio-negro-sheng-wu-5fhpc

I was told a story from a senior field geologist in China, where he observed the hypersaline lacustrin conventional oil in China are obviously denser, thicker and lower gas than US or Arabic oil. His conclusion is that the source rocks are different, but the maturities are close. one could see that isotope-maturity reads are indeed close, VM-Permian (VM and China's Jungeer)-Bohai.

Similar for Uinta, the maturity probably is higher than the Permian/EF/Bakken, but the GOR is lower, the oil is thicker, especially on the surface, where the high wax content make one believe they just can not even move. But down in the reservoir, the oil flows just fine, and the bottleneck is the PVT phase separation. In the US, most production petro-engineers know PVT and practice almost daily because for light oil with high gas, PVT-bubble point is a serious issue; while in China, most petro-engineers learnt in the school but soon forgot it for good — there is little need to worry about it in the real world. In Shengli or Bohai to Jungeer in Xinjiang, the gas to oil ratio in conventional field is usually 10:1 to 20:1, and API<27~8deg, high wax content, some field could outproduce Saudi wells, but limited size limit peak years to 1-2 only.

In context, the PVT-bubble point is easy to understand and conventionally intuitive; but to truly appreciate its implication, i.e. lower GOR black oil, aka "low shrinkage oil" in professional engineering means higher productivity is quite unconventional, and not to mention the high wax content that make them so poor in production or deal with on surface.

Thanks Sheng Wu,

I no longer have data to use for this so no way to check what is going on. Looking a bit more closely at the Novi Chart at Oilystuff, it looks like average new well EUR increased by about a factor of 3 after 2015, perhaps as they realized what you are referring to.

The USGS estimate was using the older well data so maybe their estimate is about one third of what it should be. Hopefully the USGS will revisit with updated well data. It is possible this sweet spot is small, or it may be large, impossible to guess with the very limited information at hand.

Since April 2021 horizontal oil rig count has averaged close to 8 rigs per week in Utah due to logistical constraints on local refinery capacity and transport infrastructure constraints. The waxy nature of the oil makes transport and processing more challenging.

Investigating further using Chat GPT, I found average EUR for Uinta Basin tight oil wells at about 450 MMbo with about 2000 to 3000 potential locations, this gives a low side estimate of maybe 2000 times 0.4=0.8 Gb and a high side estimate of 3000 times 0.5=1.5 Gb, with a mean of 1.125 Gb for economically recoverable tight oil resources from this play, this is almost 4 times larger than the USGS TRR mean estimate from 2015.

D C,

I read about Uinta progress from TGS (https://www.tgs.com/weekly-spotlight/06-16-2023) only in middle of 2024, after VM production news from Rystad (I believe it was in middle of 2023).

The waxy nature makes transport actually easier than volatile oil, as it only requires some heating, whereas safty is relaxed with lower GOR and much lower volatility.

Sheng Wu,

Much of the information in Chat GPT was sourced from TDS. It is not clear that the railway investment will be worth the money spent as the resource may not be very large. If the oil companies want a railway, they should pay for it. It is not cheap to heat the rail cars, especially in winter.

I have long explored the Roan Plateau, which is on the Colorado side of the Douglas Arch. For those of you interested in the Uinta basin, there is a massive jump in magnetic amplitude that runs almost parallel with the Utah-Colorado border, resulting from a deep fault down into the magnetic rock of the basement. This arch–mostly subterranean but with some structural relief–separates the Uinta from the Piceance basins, which are adjacent but entirely different in the composition of hydrocarbons. Incidentally, the railway would run alongside the Book Cliffs, thrown up from the Laramide orogeny on the Colorado side, and these are unusual enough in their own right (looks like a shelf of library books). But the real gem is the interior of the Roan Plateau, which looks ordinary from a distance but is verdant with clear high mountain streams like the Trapper and Parachute Creek, home to an almost Darwinian isolation that has preserved a species of cutthroat trout in their genetically pure status, and also a three-toed hummingbird that is found nowhere else in the world. This area (on both sides of the Douglas Arch) is unlike any other in the world. I haven’t fished up there for five decades (to get to Trapper Creek is a Herculean task) but the trout are protected by Trout Unlimited, and the biodiversity on the Roan Plateau is unequaled in the United States. Lots of anticlines were thrown up when the big fault tore into Precambrian rock. Like many places where magnetic amplitudes change abruptly, there’s waxy oil on one side, and not on the other. Sheng Wu will know about this: likely lacustrine from a billion years ago with a very long maturation.

only need to heat up the oil tank loading and unloading, and then it is safe if oil solidify during transportation.

There are some magic numbers in the hypersaline lacustrine shale oil. The latest results from a small fragmented block in CHina, Subei, has very good low GOR shale oil output. Yet, the TOC is so low ~<1%, it is considered as no good as source rock. My model for this type of source rock is that they could generation just oil and with large carbon numbers, i.e. heavy oil (CnH2n, C:H~1:2) and so little gas (CH4, C:H~1:4), and therefore the process of oil generation only depletes the C at twice the rate of regular marine source rocks, and also maturity is so high, that they already reached the end of oil and gas generation, and yet still not much gas. The deposition environment might also suppress oil cracking into gas, and therefore so little gas generated. So, in VM, the gas TRR is probably overestimated by EIA, and it might be only 60~80% of original EIA estimate.

Gerry,

I am not familiar with the area, hopefully I will have a chance to visit before it is destroyed by this proposed railway. It sounds spectacular.

Mr. Wu, you are clearly very critical of the current political situation here in the United States; are you an American citizen? Were you educated here in the U.S.; what exactly is the basis of your criticism of my country? For you to have credibility, its a fair question. Do you have a right to vote, sir?

I am sensitive to this issue because today I have discovered that China owns over 250,000 acres of farmland in Texas, along with hundreds to thousands of acres in other states. Texas, not the U.S., is still exporting shale oil to China, as well as refined products, and today China openly condemns U.S. involvement in the Israel/Iran conflict. That can be interpreted any number of ways, Mr. Wu. None of them good, IMO. There was an article today, somewhere, about more intellectual theft of valuable American data…I wish I could find it. Google today that China is stockpiling a great deal of US imports and well, you can see its sort of concerning to me. The open communication with colleagues in China that you have, about American oil, deeply concerns me. China is not a drinking buddy with the U.S., mate; I assume you get that. If you don’t, you should.

Look, man…I don’t mind you criticizing everything I write, on my personal blog, I simply wish to say, whatever your education is, whatever your motives are, you know NOTHING about operational issues in the U.S., nor well economics and corporate finances here in the U.S. People here are desperate for information about oil and gas, but not bad information.

The VM in Argentina is interesting, and clearly a primary source for your analytical income, but of little relevance to the U.S. None of that oil will ever remotely reach U.S. shores.

I am getting a little pissed at foreigners, like pompous D. Heads from Great Britain and Europe, both entirely economic shit holes-waiting on the U.S to bail them out, criticizing my country, constantly. Anonymously, naturally. Nobody likes EVERYBODY in their family but we tend to be protective of family, and country, anyway.

Some of us, anyway.

Mike,

‘China is not a drinking buddy with the US’. Indeed. Nations have strategic interests that are often in conflict. Much as we might wish it otherwise, history is clear that the world is not a friendly place. Increasing constraints on energy and other resources aren’t likely to change that in a good way. I take many of your comments about exports and optimized production as driven by very pragmatic, ‘realpolitik’ assessments of what is in the best interests of the US. Agreed.

Who among us is not an immigrant, or from immigrants…living on this land and on this earth as short timers?

“Someone must have slandered Josef K., for one morning, without having done anything truly wrong, he was arrested.”

Mike has made revisions to the Uinta post, so go back for a re-read as there have been a few corrections/improvements to the original post.

https://www.oilystuff.com/forumstuff/forum-stuff/the-next-great-shale-basin

Sheng Wu has a PhD in Chemistry

https://peeri.org/

“Who among us is not an immigrant, or from immigrants…living on this land and on this earth as short timers?”

The Shellman family name has a documented presence in Westphalia region of Germany since at least the 13th century. Families with this surname also migrated to the United States, with a notable concentration in New York in the 19th and early 20th centuries. The name likely originated from a descriptive nickname for someone who was considered “noisy” or “loud,” as the German word “schel” means “noisy” or “loud”.

The US trade deficit with China has grown considerably since the 1980s, reaching a peak of $382 billion in 2022. In 2024, the US goods trade deficit with China was $295.4 billion. This represents a 5.8% increase compared to 2023. In 2024, US goods exports to China were $143.5 billion, while imports from China totaled $438.9 billion.

The United States imports a wide range of goods from China, with the top categories being electronics, machinery, toys, and furniture. Specifically, the US imports significant amounts of electrical machinery, nuclear reactors, boilers, and mechanical appliances, along with toys, games, and sports equipment, plastics, and furniture from China.

While Chinese entities have acquired land in Texas, it’s a small fraction of total foreign land ownership and primarily concentrated in a few large transactions. Concerns about national security and food security have led to legislative efforts in Texas to restrict foreign land purchases, particularly from countries like China. Chinese investors own less than 1% of all foreign-held acreage in the United States, according to the United States Department of Agriculture’s 2021 land report.

Meaning of trade: buy and sell goods and services, exchange (something) for something else, typically as a commercial transaction.

Asian Americans have a high rate of educational attainment in the United States, with over half holding a college degree, significantly higher than the national average.

The US education system, while striving to provide opportunities, also presents challenges that can contribute to insecurity. Basic needs insecurity among students is a serious issue that needs addressing. Additionally, a culture of comparison and emphasis on external achievements can negatively impact self-esteem, even for those with high levels of education. However, factors like supportive environments and personal traits like optimism can help mitigate these negative effects. This lack of basic needs can significantly impact the ability to succeed academically and potentially lead to emotional stress and mental health concerns.

,

Mike Mr. Shellman,

The politics in US is well-known to be extremely polarized, unlike a one-party political system in China. No surprise that my opinion about energy and industrial policy surely will clash with others, e.g. the “left-extremists” that I used in my posts.

However extremely polarized, the freedom of speech is still much withheld till now, demonstrating its resilience. This forum is also open to all users in the world, and I could access while I was traveling in China, and there is no requirement of US citizen to post here?

To summarize the agreements and disagreements between you and me in energy policy,

1. shale oil — you and I both agree the drilling has been overdone and should be regularted, resulting in fast pressure dropoff, early arrival of bubble point and fast deterioration of EUR. You also strongly oppose shale oil export and want a ban or limit from Federal/State, while I am neutral on this because it is a free market to start with. These regulation actually is against the free market in US, and only could be expected in a monopoly market like in China’s oil and gas market.

On the other hand, China’s renewable energy market is like US shale oil and gas industry, they probably lose 100s of billion dollars investments, while exporting at a loss like there is no tomorrow. I expressed my strong opinion that the “left-extremists” in the west used stupid government policies to promote the “green energy” while destablize domestic industry and energy; and in this sense, the Chinese government had a much better well-planned energy policy, even though all inevitably create more fossil fuel consumption.

2. shale gas — you and D C seem to propose the limit or regulation in drilling and export of shale gas as well, while I think there are plenty of gas in US and worldwide, and US better export more LNG for now to boost wellhead prices and US presence/influence in global energy market.

H. Beach, that is the third time that you have insulted my family, directly, and/or my family’s name, I think for no reason other than you are miserable son of a bitch and don’t like my political beliefs.

I am at a distinct disadvantage in this regard because I do not even know your name. You insult people, anonymously, because you are a coward. I know you are an ultra left-wing wacko that lives in Huntington Beach, California, an otherwise conservative stronghold in a state that is dying a slow, ugly death from liberal policies. You sold insurance for a living, I recall, and though you despise everything about America, including the American hydrocarbon industry, you appear to be hypocritical enough to be very defensive of your dividend income from Exxon and Chevron. You own a little boat, I think you have bragged.

I have a Citation standing by and can be at John Wayne in 4 hours…let me know. I would relish in actually meeting you whereby you could insult me to my face.

None of my comments to Mr. Wu have anything to do with immigration issues. They have to do with the hate, and anger, and unwillingness to accept the current reality of who is in charge of running the country. This too will pass, like all other piss poor presidents in the U.S. pass, including Democratic presidents.

So don’t lecture me about immigration, Hickory. I know who you are; you went ape shit on my blog about men participating in women’s sports, over a photograph I posted of an executive order signing by Trump. I have daughters who were world class athletes. You want to deal with immigration, come to South Texas.

The name calling, the disrespect for my country, the fear mongering has to stop. We are on the prepuces of a world war. If you allow this hateful rhetoric you are part of the problem. Does nobody have pride in country anymore? Or is it directly tied to a stupid president in office for 4 years?

Dennis, sorry, mate. We have seldom agreed but might have learned a lot more from each other had you not allowed politics to eat your blog from the inside out. You should decide which it is, a respected forum for the discussion of affordable peak oil matters, or just another toilet for political hate.

Mr. Wu, you have a PhD in Chemistry? Wow, I thought you were an oily engineer, or geologist. I have a PhD too, man. In post hole digging. People like you will ultimately lead to the U.S. someday not having enough natural gas to transition to reasonable, affordable renewables. Will you happily accept the responsibility of that?

Señor Shellman for the record, California has the largest economy in the United States and if it were a country. It would be the 4th largest economy in the world and is lot larger than Texas. Here is the real kicker about the California economy. We are practicing the policy of drain Texas first by restricting oil production here in the Golden state. Because here in California, we understand oil is a finite resource and respect that fact. Also, California is the leading state in EV sales and Californians don’t fly half way across the country because of blogger issues. I think you’re just looking for an excuse to visit HB for a vacation and boredom relief.

Have a great day in Fredonia

BTW, Valero is my largest holding and it paid it’s dividend yesterday. What you dont seem to not understand, it’s the capital gains that are the real winner buddy, got them in back in 09 at $15. Click, click beats the hell out of dig, dig. And you will love this, all with zero debt. Let me know when you check in to the Paséa Hotel & Spa. I’ll show you where you can eat the best Mexican food in America.

Sheng Wu,

There is no requirement that someone is a US citizen to comment here, and in general I believe anyone can criticize any government regardless of citizenship.

I appreciate you sharing your knowledge here.

Note that my expectation is that US natural gas is more limited than many believe. I do not support a ban on natural gas exports, but would caution those investing in LNG exports that there is likely to be excess capacity once LNG projects that have started construction are completed and natural gas output starts to decline around 2028-2032 due to falling associated gas from tight oil plays. Those LNG export facilities are likely to become stranded assets. My most recent shale gas scenario below, conventional gas is likely to decline at an annual rate of 5% per year.

It is possible that the US will transition to non-fossil fuel and reduce its need for natural gas domestically, but the time to export natural gas is after that occurs rather than before in my view. To me it is just bad policy to deplete our energy resources rather than conserve them for future generations, it is also a national security risk.

Shock Model for World Natural Gas (Gross minus reinjected), best guess scenario.

Mike Shellman. I don’t think I’ve ever been to your blog. I have a pretty good memory still.

“The International Energy Agency forecasts global oil demand to peak and plateau by the end of this decade, with China’s demand peaking earlier than previously anticipated.”

Thats nice, for demand to peak roughly when supply does.

The next challenge will be to reduce demand roughly in step with declining supplies.

Not as if there will be a choice.

Although there will be choices about how, when, where to fight for the residual supplies.

New posts are up

https://peakoilbarrel.com/opec-update-june-2025/

and

https://peakoilbarrel.com/opec-thread-non-petroleum-june-18-2025/