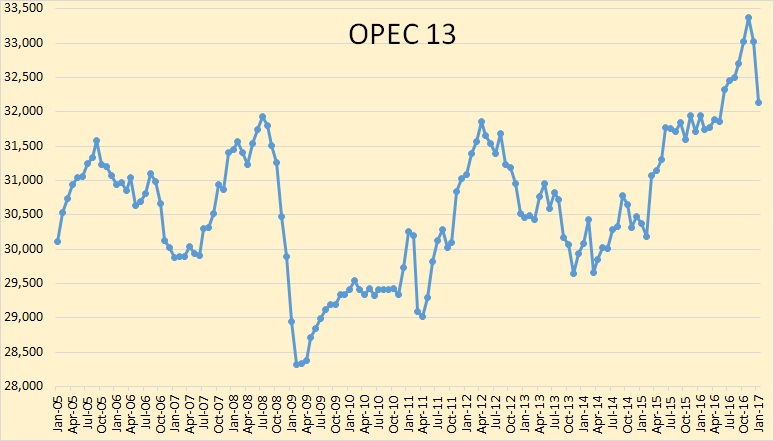

The new January OPEC Monthly Oil Market Report is out with crude only production numbers for January 2017. All charts are in thousand barrels per day.

OPEC crude oil production dropped to 32,139,000 bpd in January. November production was revised upward by 68,000 bpd while December production was revised downward by 56,000 bpd. So Peak OPEC production was in November 2016 instead of December as they had it last month.

Officially OPEC agreed to cut production by 1.2 million barrels per day beginning in January. So OPEC missed their mark by 310,000 barrels per day.

OPEC’s December production represents an all time high for the cartel.

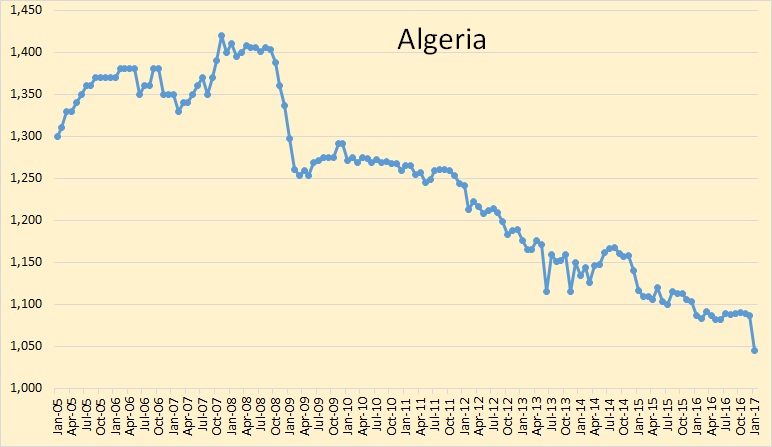

Algerian production was down by 41,700 bpd. This was a lot more than was expected.

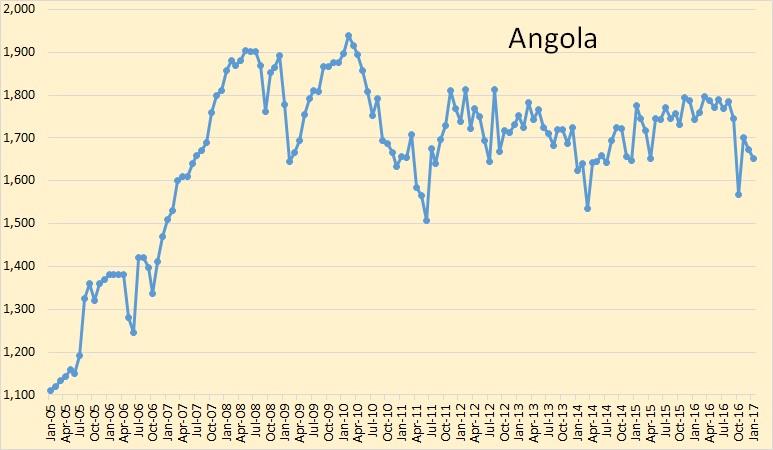

Angola’s production was down 23,200 bpd in January.

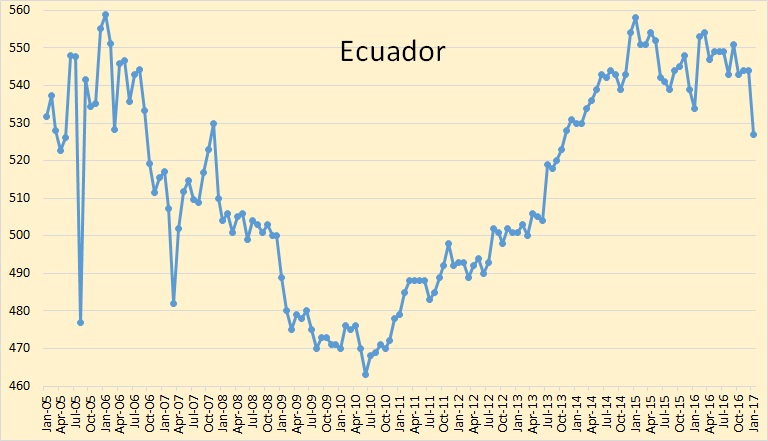

Ecuador’s production dropped 16,700 bpd in January.

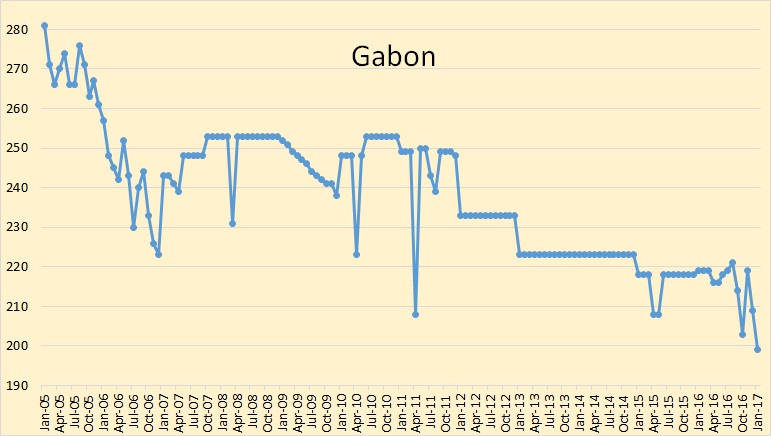

Gabon dropped 10,000 bpd in January and reached a new low at just below 200,000 bpd.

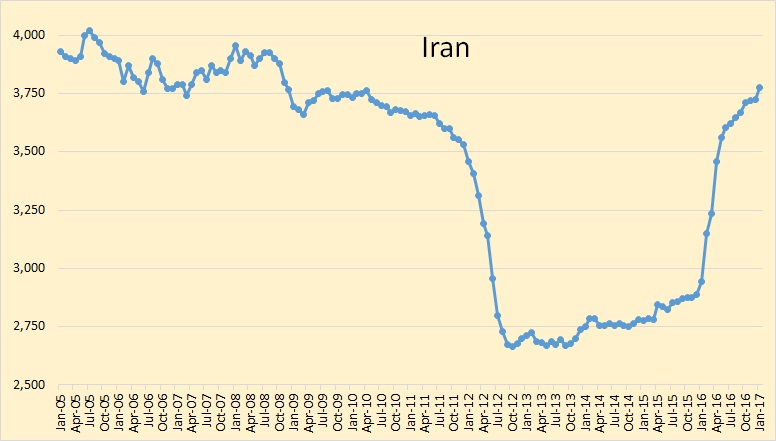

Iran’s production actually increased 50,200 bpd in January. I guess they are thumbing their nose at the rest of OPEC. In January their crude oil production was 3,775,000 bpd, their highest point since November 2008, well before sanctions.

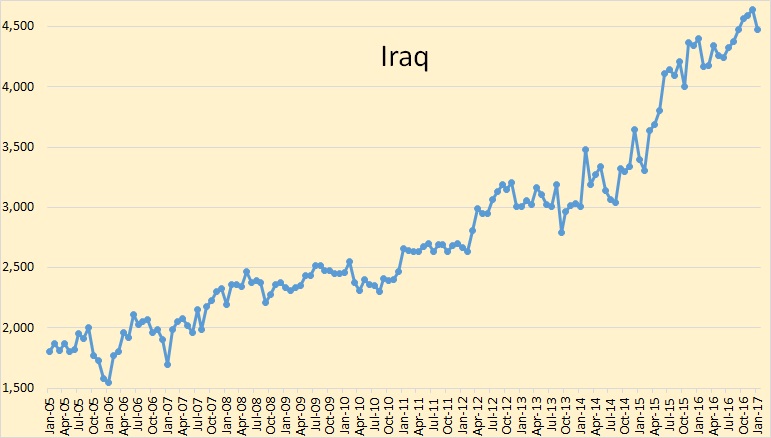

Iraqi production was down 165,700 bpd in January. This was a shock. Few expected them to cut this much. Of course much of this decline could be just that, natural decline.

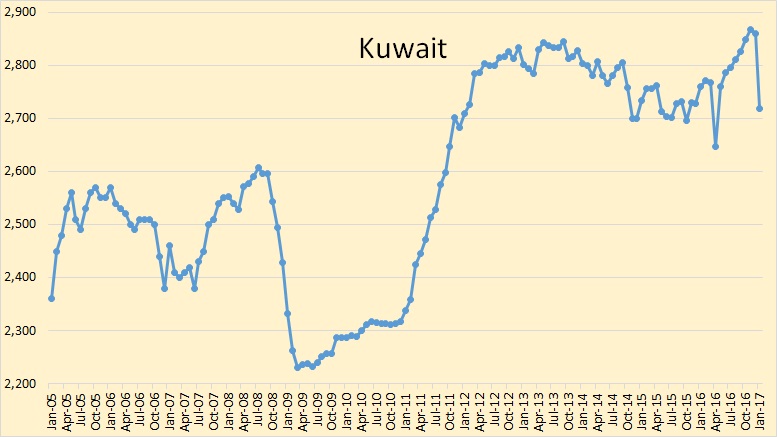

Kuwaiti crude production declined by 141,200 bpd in January. Quite a drop for them.

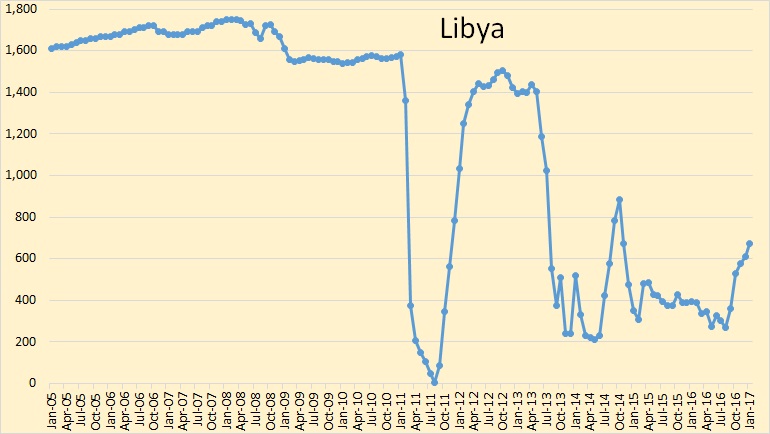

Libya’s production continues to increase. They were up 64,700 bpd in January. Libya, because of their political problems, is exempt from those OPEC cuts.

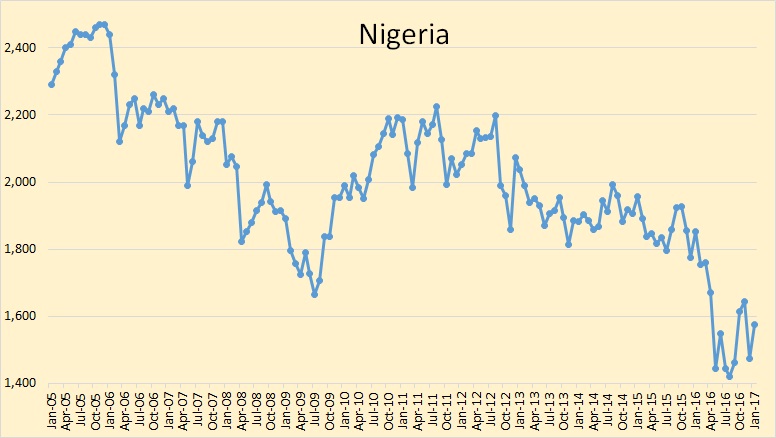

Nigerian production was up 101,800 bpd in January. Nigeria, because of their problems with the rebels, are also exempt from OPEC cuts.

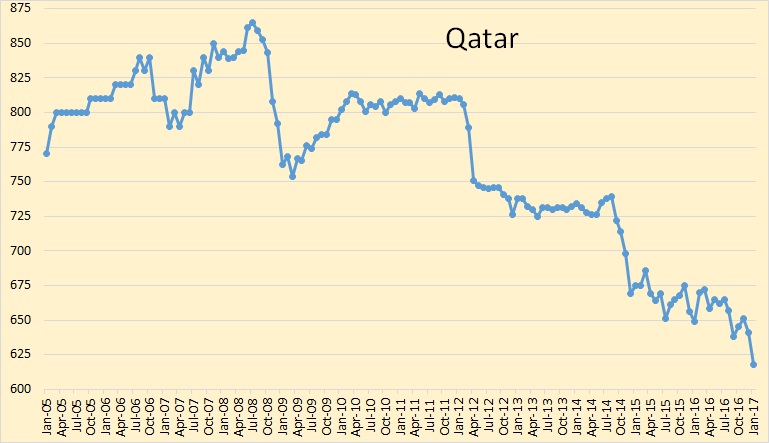

Qatar’s crude oil production declined 22,500 bpd in January. Qatar has been in an almost steady decline since 2008.

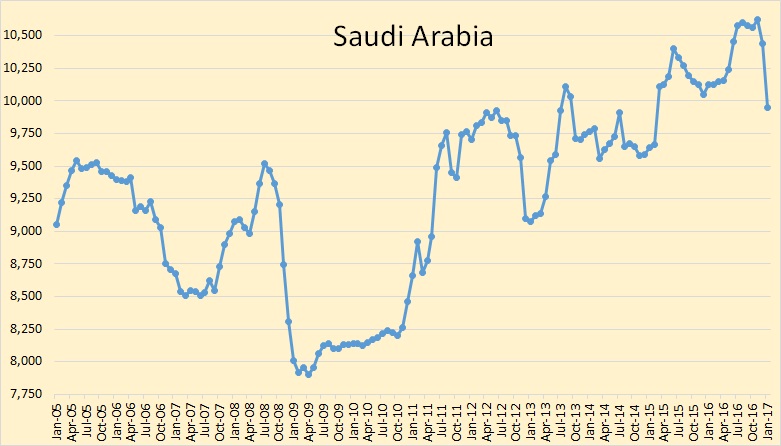

Saudi crude oil production declined by 496,200 bpd in January to 9,946,000 bod. This is their lowest point since February, 2015.

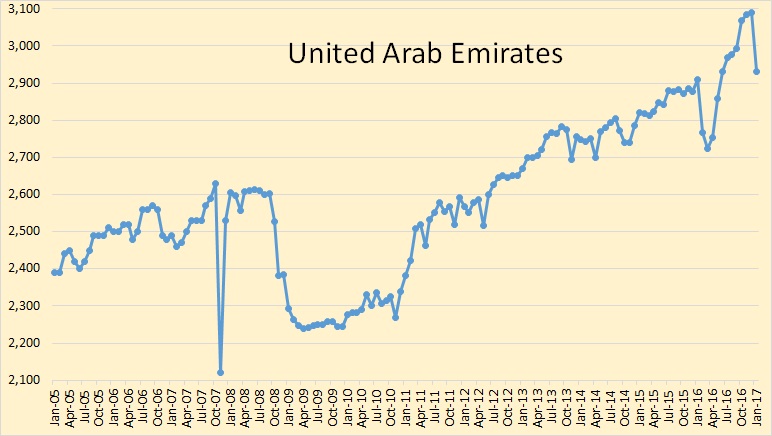

UAE production was down by 159,300 bpd in January. The UAE had been making heroic attempts to increase production in the last 6 month in preparation for the expected cuts.

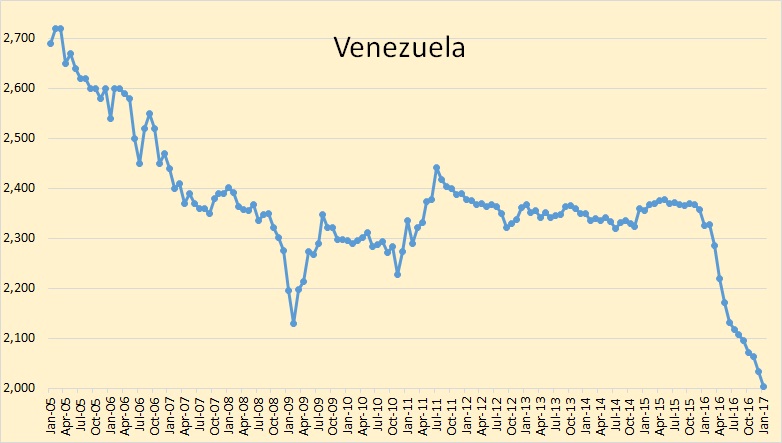

Venezuelan production dropped by 30,500 bpd in January. They are now barley above two million bpd now. I doubt that any of this decline was intentional. Look for their decline to continue.

OPEC says world oil supply was down by 1,290,000 bpd in January.

Here is what OPEC expects Non-OPEC production to be in 2017.

150 responses to “OPEC January Production Data”

Second half of 2016 looks like a last hurrah for OPEC, that is back to the 32 mbpd production that has visited multiple times since 2008. Almost 10 years ago.

Peak Oil by any other name is still Peak Oil.

Interesting link to a piece on the Bakken i found. http://en.angi.ru/news/553-Contemplations%20over%20the%20sinking%20Bakken/

I have mentioned before that I am using the Bakken as an indicator of what might happen if oil production is expanded in the populated areas of Colorado.

This article mentions two things which might present problems in Colorado. The amount of water involved in the production and the amount of gas produced.

Good article but it gets downright silly at the end. Concerning the Bakken, nobody is blaming anything on the Russians.

I think he is being sarcastic. He could have also said “Obama did it” and we’d get his point. There are people in the US who don’t accept that oil fields can decline, and decline quickly, and look to place blame elsewhere.

Yes, I realized it was sarcasm, but silly misplaced sarcasm. Russia actually did the things the CIA and other intelligence agencies said they did, like meddling in the US elections. So he is, I think, trying to say that we try to blame the Russians for a lot of things they did not do, That is bullshit.

I agree that from our perspective, Russia is not a victim.

Maybe Russians feel otherwise.

More important is how the administration reacts. I think we have more self-interest in continuing to work with China than with Russia. Many businesses depend on China both as a producer and a buyer.

From what I have read, trying to cut deals with Putin hasn’t worked out so well for Americans trying to do so.

Sorry, Ron, it was joke, of course. Look for the last sentence:

Then all joking aside, there is a lot of work ahead.

The editor said me, that Americans don’t like such joking. But I wrote this article for Russians, they enjoy it.

“Concerning the Bakken, nobody is blaming anything on the Russians.”

Yes, Bakken is not mentioned, but Russia is blamed for anti-fracking propaganda.

https://www.bloomberg.com/news/articles/2017-01-10/putin-s-other-american-propaganda-effort-anti-fracking-news

http://europe.newsweek.com/intelligence-putin-funding-anti-fracking-campaign-547873?rm=eu

Hi Alex,

Let’s put aside a political jabs from media because it is just the smoke screen for the masses and let’s look just some of the conclusions from the Russian author of the text:

” The proved reserves of shale oil in the four largest fields in the US are recovered by 59%.The increase of prices that happened, facilitated drilling in Permian Basin by 1.5 times, but it only slightly affected the other fields. Nevertheless, some increase in the shale oil production is possible this year due to drilling the remaining highly productive areas. Then the production in the USA will start declining slowly irrespective of increase in the prices.”

This is pretty much what few of us suspected that will happen. Also there is Bruno’s model that is pretty much still relevant. So I really don’t see any huge increase in shale oil production in near future even if today’s oil price holds or go little bit up. I believe you don’t feel the same. Are you willing to modify your opinion if the price remains between $50 and $60 WTI in 2017 and good part of 2018 that any total shale output (4 largest fields in US) has already passed their peak?

Thanks

Given that the fracking “miracle” is likely to be short-lived, Russia is probably better to focus on that, as the Bakken article does.

Yes, Bakken is not mentioned, but Russia is blamed for anti-fracking propaganda.

And I take it Alex, that you don’t believe a damn word of it. 😉

Ron:

Could you comment on the discussion in the article about water cut? I think he was saying that most, or much, of the water cut was due to damaged cement seals. In the “Peak Oil News” forum (comments of which have become almost unbearable) “Rockman” has been asserting for years that the cement seals are never, or almost never, a problem.

JJHMAN, I think you are laboring under a false assumption. You think I am an oil field expert. I am not. I spent my entire career as a computer hardware engineer. Rockman, or almost anyone else on this blog, knows far more about the subject than I.

So I will leave it to them to reply to your request.

JJHMAN,

If what you’re referring to is Rockman’s constant references to cement seals during drilling, he’s emphasizing that a seal rupture is not a big thing because they’re ready for it. They’re common. He usually says that they even keep the equipment for dealing with these failures either on the rig or at the site (I’m not sure which.)

Is that what you’re referring to?

I have not seen rockmans comment, but cement bond failures are a huge issue. There are mitigating measures in the short-run (most of them with fairly poor records), but in the long run they cause big issues with underground cross-flow of hydrocarbons into shallower zones.

prove it Daniel, show this board and the entire world your facts….bet you can’t.

Allow me to say about my impression.

Usually it is not annular channeling along the cement seal. Such issue should be indicated during a few months of well operating.

But often the water flow appeers later, after formation pressure decreasing up to very low level, 600-800 psi. In this case, I think, water is draining through the new fractures in tight shale, mudstone or siltstone.

Ron,

1) Anti-fracking propaganda was certainly not born in Russia. There is a lot of antifracking, anti-oil and anti-fossil fuels propaganda in the West.

2) Sometimes it is difficult to see the difference between propaganda and expression of someone’s opinion. For example, you liked Alexander Khurshudov’s article on the Bakken (except his sarcastic sentences), but some people could view this article written in English by a Russian expert as Kremlin’s anti-fracking propaganda. Furthermore, some very conservative people could view POB and other peakoil websites as anti-fracking and anti-oil propaganda outlets.

3) Do you think that Russia’s, China’s or someone else propaganda could affect public opinion in such a great super power like U.S.?

but some people could view this article written in English by a Russian expert as Kremlin’s anti-fracking propaganda.

Yeah, and some people are stupid conspiracy theorist. While others are just paranoid.

Furthermore, some very conservative people could view POB and other peakoil websites as anti-fracking and anti-oil propaganda outlets.

Yeah, I agree. Most conservatives are just fucking stupid.

Look, some people on this blog are always accusing others are being a paid shill for this industry or some other. No, they are just people expressing their opinion, however naive they may be. I do not believe anyone who ever posted here was a paid shill for any group or industry.

Some people are just too conspiracy minded. No, people are just people with opinions, although usually really stupid opinions. And they want to spout them somewhere and some find their way on this blog. I usually shoot them down if I happen to be monitoring posts that day. But if not, what the hell?

As to the article, I thought it very interesting. Too bad he had to really fuck it up with those stupid sarcastic comments at the end.

3) Do you think that Russia’s, China’s or someone else propaganda could affect public opinion in such a great super power like U.S.?

Really now? That question is… is… really incomplete and silly. How strong would be the propaganda and how would it be delivered? Public opinion and the fact that the US is a super power are two different things that are totally unrelated. The public is not the power and the power is not the public.

Really Alex, I think you need to rephrase that question. But shit posted on blogs on the internet has little, if any effect, on public opinion.

Neither that article, nor anything posted on this blog, will have any effect on public opinion. Okay, perhaps one in a few million or so. Not enough to make any difference in the grand scheme of things. Not even close.

“Yeah, I agree. Most conservatives are just fucking stupid.”

and/or just flat out lie

it’s conservatives that are stupid…really?

https://twitter.com/NDAA2012/status/831327072400318464/photo/1

Yes. Really. Lower cognative ability is predictive of right wing ideology.

http://journals.sagepub.com/doi/pdf/10.1177/0956797611421206

“I did not mean that Conservatives are generally stupid; I meant, that stupid persons are generally Conservative. I believe that to be so obvious and undeniable a fact that I hardly think any honourable Gentleman will question it.” ~ John Stuart Mill, in a Parliamentary debate with the Conservative MP, John Pakington, May 31, 1866.

TeaBag, your connection between the failure of the concrete spillway and Liberals. May I say it. Is just fucking stupid.

Thank you for an excellent example

http://www.latimes.com/local/lanow/la-me-ln-oroville-dam-release-20170214-story.html

Ron says – “Neither that article, nor anything posted on this blog, will have any effect on public opinion. Okay, perhaps one in a few million or so. Not enough to make any difference in the grand scheme of things. Not even close.”

That may be the wisest comment ever posted on this blog.

This blog does get read by oil people, and not just retirees. The comments probably as much as the posts.

The more precise perspective would be “nothing said here is going to influence oil scarcity in any way.”

Now that’s accurate.

AlexS, I agree. But be sure none of RT staff has the slightest idea of fracking. RT is seeking the opposit opinions and try to show it. If your authorities abuse fracking, RT will find and show the persons to compliment it.

On the other hand where is fracking prohibited? In France, Germany, New York State. Not in Russia. I’d managed my first frac job 40 years ago and now more than 3,000 frac jobs a year are accomplished here.

It is foolish to abuse the thing which you use with pleasure.

Nigeria production must be getting close to their maximum capacity now. They only had about 100 to 120 kbpd additions in 2015 and 2016. There is nothing due this year I know of, but Egina at 200 kbpd in 2018. Their own oil company admits that onshore production is in decline and there isn’t much left to develop – they are promoting gas, like a lot of other mature producers. Their deep offshore has 10 to 15% decline rates so extending the decline curve from 2015 gives a production about what they have know, and likely to continue down for at least the next two years.

OPEC give average production for 2017 for GoM at 1.673 mmbpd, that is slightly lower than December EIA numbers, (i.e. suggesting there will be overall decline through this year) and a lot lower than EIA predictions for the second half of the year, but in line with IEA numbers, and I think much more realistic than EIA. Exit rate for 2017 might be below 1.6 and declining.

George,

Nigeria could significantly increase output just by reducing supply outages, which are a result of internal political instability.

Unplanned Crude Oil Production Outages in Nigeria (kb/d)

source: EIA STEO February 2017

Maybe – but I doubt that EIA have allowed for any natural capacity decline through 2015 and 2016 when things have been offline. I think that would take out 150 kbpd or so, which means they might have another 150 from somewhere, but that would easily go from natural decline this year.

Hi Alex S

Do you think it likely that political problems in Nigeria will be resolved in the near term? That seems to be a wishful thinking scenario.

Dennis,

I don’t know in details what’s going on in Nigeria.

But there are several cases when oil production shut down by political instability was restored relatively quickly.

For example, Libya has recently increased output by 400 kb/d (from 275 to 675 kb/d) and is planning to increase it further to 900 kb/d this year.

Of course, Libyan output may drop again, but who knows.

In Russia, oil production declined from 11.4 mb/d in 1987 to slightly above 6 mb/d in 1996, and nobody (including the Russian government) did expect it to recover to previous highs.

There are also recent examples of Iraq and Iran.

My point is that we should distinguish between natural declines, lack of new discoveries, on the one hand, and various issues (political instability, accidents, cyclical downturns, etc.), that may lead to temporary declines in production.

Hi Alex

I agree.

I am just trying to avoid optimistic scenarios that assume all political problems disappear overnight.

I also do not know the details of Nigerian conflicts.

At some point both Nigeria and Libya might reach their previous peaks or maybe not because they are battling depletion as well.

Even very optimistic resource scenarios such as USGS would require unreasonable extraction rates from producing reserves to reach the EIA AEO 2017 reference scenario in 2030.

Dennis,

Unplanned supply outages have significantly increased in volume in early 2011 (with the “Arab Spring”) and since then have remained a serious factor for the global oil market.

According to the EIA, such outages in OPEC and non-OPEC countries were at 2.3 mb/d in January 2017; and in 2014 they had exceeded 3 mb/d.

I agree that all political problems cannot disappear overnight.

On the other hand, we cannot assume that oil production negatively impacted by political problems will never recover.

If I were an oil price forecaster, I would elaborate several possible scenarios, with future supply outages being one of the key uncertainties.

Hi AlexS,

My point is simple, the odds are relatively low that the problems since 2011 will go away in all places at around the same time. Different areas are more likely to recover politically at different times and all the while there is very little oil being discovered. On can assume that estimates of recoverable resources will increase over time as they have in the US, but OPEC reserve estimates are already very aggressive (likely to be overestimated), but for the most part these are state secrets.

You are very familiar with the Russian oil industry, do you expect that oil output will continue to increase through 2040? Eventually a peak in World C+C will be reached, probably some time between 2020 and 2030 and probably about 82 to 85 Mb/d at most.

I followed the Nigerian conflicts for a while. There is no chance of them being resolved sufficiently to stop the constant oil supply disruption. None.

If oil stops being valuable and the oil industry disappears, on the other hand, the conflicts might actually die down. The oil is a source of wealth which the people on the various sides of the conflicts are fighting over.

If the oil wealth is gone, they will still fight over ethnic “right to have our own country” separatism, probably, but the money fuelling the fight will go away, and the result will either be that the locals will not care so much about secession, or that the national government will not care so much about secession, or that the outside agitators will find some other region to raid, so you’ll probably see a resolution fairly quickly.

Yes, apparently the EIA has assumed relatively flat production capacity for Nigeria.

But there are other estimates that their unitilized capacity is around 500 kb/d instead of EIA’s 600 kb/d estimate.

From Bloomberg:

“Nigeria has roughly 500,000 bpd offline because of security issues, Manji Cheto, senior vice president for West Africa at Teneo Intelligence, told Bloomberg.”

https://www.bloomberg.com/news/articles/2017-02-08/nigeria-struggles-to-boost-oil-output-that-s-good-news-for-opec

Nigeria crude oil production and unplanned supply outages (kb/d)

Source: EIA STEO February 2017

The baseline should, at best, be what they were able to achieve in 2012 to 2013, not an assumed 100%. They have very old and poorly maintain infrastructure. I know from (not quite) first hand experience that they have to run some of the pipelines at reduced flow to keep the pressure down and prevent leaks. It’s not just security issues they have problems with. And I think the curve shown through 2016 is wrong, it doesn’t include for decline in deep water production, which in past years has needed at least one large FPSO per year (plus some minor tiebacks) to maintain production – which they didn’t get, and won’t again this year. Plus planned maintenance has almost certainly been cut back further than usual, even in the IOC operated fields, as oil prices have kept low and interest in new develops has been falling.

Financial Times have an article:

“Oil and gas discoveries dry up to lowest total for 60 years”.

Behind a paywall, but if you go through google I think you get one free view.

They quote IHS with 2017 discoveries at 8.2 Gboe. but I think that includes the Smith Bay find at 1.8 Gb (maybe even 4 Gb). Even if there are 6 to 10 Gb OOIP, I really doubt they are going to get 30 to 40% recovery – maybe more like 0 to 15%.

There were 174 discoveries (less than half the number in 2013), which would give 45 mmboe average, but there were two or three big plays (the Alaska one and two gas fields) and I think a lot of very small on shore discoveries (e.g. in Pakistan and Australia). They quote $40 billion budget last year, by Rystad that is supposed to decline slightly this year but the number of wells will increase as drilling costs have declined. They have success rates for wildcats at 1 in 5, which is much higher than the 1 in 20 the recent HSBC report had (more like a decade average than last year’s number maybe).

They kind of hint at problems with supply 5 or 7 years down the road, and there is even a bit of acknowledgement that geology plays a role and the larger discoveries are drying up, but still you get the feeling that they think with enough money spent we’ll just keep on finding stuff for ever.

“They kind of hint at problems with supply 5 or 7 years down the road, and there is even a bit of acknowledgement that geology plays a role and the larger discoveries are drying up, but still you get the feeling that they think with enough money spent we’ll just keep on finding stuff for ever.”

To acknowledge that sources of oil are becoming less likely would require them to confront the realities of that. They probably aren’t ready to do that. It’s less scary to say we’ll find more oil with more technology and more money. Of course, even with that, they will have to deal with the fact that the money needs to come from somewhere.

Boomer says “they will have to deal with the fact that the money needs to come from somewhere.”

yes and it will. The value of keeping the system up and running will guarantee it. I don’t have the time or inclination to explain why again, but will ask rhetorically, what is the value of water when you are dying of thirst. Absence of the political will to begin to build out nuclear capacity here and in the industrial world we are going to burn fossils fuels until the relative scarcity that “peak oil” implies kicks in and prices rise accordingly. The money will come because without it everything thing else grinds to a halt. I have ask before why do you think companies like exxon continue to BUY oil and gas assets here in the US when they have the scope and resources to play anywhere in the world. If you say to con investors it will only prove just what little understanding you have about the subject and your time would be better spent feeding ducks down at the park.

I’ve been citing analysts who are also doubting that Exxon has much of a plan other than to borrow money and sell assets to give stockholders dividends.

There are enough articles by analysts questioning the viability of the major oil companies that I think attitudes are shifting.

Sounds like you think society will keep paying money to oil companies to keep them afloat even if no one has the money to pay for high oil prices.

If the world economy slows down enough, people don’t need most of what oil gives them. They can stop flying for vacations. They can stop commuting to work if they have no jobs.

When it comes to essentials, oil can be substantially cut back.

You can keep believing what you believe, but that doesn’t mean there isn’t evidence to support what others of us believe. You’re not here among a group of true oil believers. Most of us see a near or immediate term slow down for oil, no matter what the price. Too low and companies go out of business. Too high and demand goes down. And when it starts to run out, there isn’t much to do to get more of it no matter what the price.

You do realize NOCs are scooping up resource?

Exxon buys assets in the US because PetroChina, Statoil, Pemex et al have bought it all up elsewhere.

You are way off base if you think it’s some US geology superiority. What it is — is global scarcity.

The value of keeping the oil supply system up and running is zero in the long run.

That’s what oilmen like Texas Tea have not figured out. Their minds are too narrowly focused on oil; they think it’s all-important or essential, and it simply isn’t. We don’t need it.

It’s already been driven out of every significant market except transportation fuel (it’s simply too expensive to compete with the alternatives — even at current prices), and it’s being driven out of the transportation fuel market as we speak, by the same dynamic. I haven’t bought gasoline in four years.

Oil would have to go to a price below $20/bbl to be competitively priced as transportation fuel. Think about what that means for the future flow of money.

There are opportunities for sharp investors to make huge fortunes right now in renewable energy and electric cars. Several very big investors have already done so.

Other, stupider investors are losing huge fortunes in oil and gas. And they will continue throwing their money down ratholes, never to see it again, because there are lots of stupid people who are very slow on the uptake. But eventually the stupid guys will have no money left. Not quite sure when that happens.

I’m still inclined to believe that people who come to this forum to post about great oil investments are looking to sell.

As some of the articles I have posted point out, to have prices go up, you need people willing to sell. (That’s common sense, but still worth saying.) It’s not always clear who the buyers and sellers are.

This forum, by focusing on production numbers, eliminates some of the opportunity for hype. So when one is trying to predict the future of the oil industry, it is helpful to have some data that isn’t being used to promote investing and political agendas.

” but will ask rhetorically, what is the value of water when you are dying of thirst.”

but if you are burn more oil looking for oil than you find in discoveries, one might need to ask another rhetorical question, one you may have heard at some point – ‘what’s worth more, a bird in the hand or two in the bush’

I’d add that so far things are significantly worse than last year. I think there has been only one oil discovery announced, which was yesterday at about 30 mmbbl (oil) recoverable for Lundin. CoP announced a find in Alaska and Anadarko in GoM in January but they are included in 2016 (definitely for CoP anyway). I can remember one gas find for Statoil, and maybe one other somewhere. Things are normally slower in the first half so may pick up, but even successful appraisal well results have been rare so far.

And one of last years touted “new” discoveries (Apache, Alpine High) looks like it might be coming in on the lower side for reserve estimates:

http://seekingalpha.com/news/3243230-apache-minus-3-percent-alpine-high-results-seen-disappointing

(That is shale and was already known as a discovery, so wouldn’t appear in IHS estimates for 2017 on both counts.)

From Lundin: “The gross resource estimate for the Filicudi discovery is between 35 and 100 million barrels of oil equivalents (MMboe). Well results indicate significant upside potential that require further appraisal drilling.” https://www.lundin-petroleum.com/Press/pr_norway_13-02-17d_e.pdf

The EIA’s Drilling Productivity Report is out with their shale outlook through March. Looks like they do not have much faith in the Bakken either.

And here’s their take on Eagle Ford:

That is pretty much the opposite of what I thought would happen – I figured the smaller producing wells in EFS would make it difficult to recover. Bakken may still be able to get a plateau later this year, if it doesn’t then it definitely means that they’ve run out of core sites to drill. I think net permits this month might be low again based on daily reports so far. Both DUC numbers and open permits are declining – slowly but steadily.

A feature or a bug?

Transparency repealed: On February 3, the Republican-led Senate used an obscure procedural tool to end a bipartisan provision meant to fight corruption and overseas oil bribery, a rule opposed by Rex Tillerson as head of ExxonMobil. The Securities and Exchange Commission’s transparency rule, part of the 2010 Dodd-Frank financial reform bill, was created to reduce corruption by requiring drilling and mining companies to disclose royalties and other payments made to governments in exchange for oil, gas, and mining extractions

Well, it’s obviously extremely corrupt, but I can’t honestly say that it’ll have much effect. When Exxon is losing money, does anyone really care whether they’re losing money while mailing checks to Russia or losing money without mailing checks to Russia?

I suppose it is relevant if you want to monitor what deals with foreign governments your politicians (or their donors) are cutting.

But if you assume that your government (and their political donors) are corrupt and the voters either don’t care or don’t notice, it won’t make much difference.

I was doing some speculating about the fact that if Exxon hadn’t played up its deal with Russia, and then blamed sanctions for losing money, then the company and his CEO wouldn’t be so linked to Russia and political intrigue.

Exxon’s mistake may have been to try to use its Russian connections for PR purposes. Maybe it should have used bribes, and then kept all that from the public.

Rex Tillerson may have left Exxon at right time – Feb. 14, 2017: “Exxon’s stock is now lower than where it was the day before Trump was elected. And it has lagged the broader rally despite an uptick in oil prices. Crude prices have surged nearly 20% since Election Day and are now hovering around $53 a barrel.”

I’ve been mentioning this since Tillerson’s first announcement of his plans to “eliminate conflict of interest”. I have said on several websites that the guy was a genius who just figured out how to cash out of Exxon, *even selling out of restricted stock*, which is quite a trick. It’s nice to see the news propagate to CNN.

I suspect he has zero loyalty to the industry. He figured out how to cash out.

“I suspect he has zero loyalty to the industry. He figured out how to cash out.”

That’s what I am hoping and why having him as Secretary of State is less troubling to me than some of the other people in the administration.

If Tillerson knows the future of gas and oil (as an insider likely does), he may see more clearly than a politician who sees only what he wants to see.

I assume Tillerson is smart, so he could probably be a good Secretary of State if he learns what he needs to know and hows how to deal with situations diplomatically.

From today.

COT: Money Managers Were Selling Oil And Actively Buying Corn And Wheat | Seeking Alpha: “The money managers’ net position is approaching the plateau phase, during which, judging from the previous three years, the money managers are not predisposed to actively buy oil.”

An article from yesterday.

Oil Majors' Plans – No Relief For Offshore Drillers | Seeking Alpha: “Management surely understands the key driver behind the stock price. Not surprisingly, they want the upside to continue, which is favorable both for them and their shareholders. Thus, they prefer short-cycle projects over long-term projects because longer-term projects are an immediate hit on the bottom line, while the results will be seen later.

During the earnings call, Chevron said the following: ‘We’re further reducing capital spending in 2017 and investing a larger percentage of capital in short-cycle high-return opportunities presented by our advantaged portfolio.’ The company added: ‘Our actions support our number one financial priority which is maintaining growing the dividend as the pattern of earnings and cash flow permit.’”

“If you believe that OPEC/non-OPEC deal is a game changer, you’d expect that oil majors will be more focused on their growth plans. However, they appear to be more focused on their EPS or debt management, as highlighted by Exxon Mobil’s intention to use excess cash balances to pay down debt or buyback shares.”

This is from an hour ago. This is the dilemma that the pro-oil folks face: increase production and see lower prices. People can talk about the industry being cyclical or how it is always investing in long-term projects, but it appears the major oil companies aren’t doing that right now, either (see my previous posts).

And investors and commodities traders who might boost oil prices and stocks have lots of other places to put their money, so they aren’t currently being persuaded.

Oil pares gains as U.S. supply concerns overshadow OPEC cuts | Reuters

Two hours ago.

U.S. Shales' Resurgence, and Not OPEC Cuts, is the Oil Story To Watch – Pg.2 – TheStreet: “But with oil markets still finely balanced the U.S. rig resurgence could be enough to put a cap on oil prices and disappoint anyone hoping that OPEC can drive prices higher.”

From BP’s Assay page I looked at some fields labeled “condensate”.

First, Brent

API 37.5

Kerosene 14.37%

Gasoil 25.46%

NorthWest Shelf Condensate (offshore Australia)

API 63

Kerosene 18%

Gasoil 7%

Bontang Return Condensate (Indonesia)

API 77

Kerosene 0%

GasOil 0%

Tangguh Condensate (Indonesia)

API 45.6

Kerosene 17.1%

Gasoil 20.75%

Sharjah Condensate (UAE)

API 64.8

Kerosene 13.47%

Gasoil 1.41%

Algerian Condensate

API 68.6

Kerosene 18.25%

Gasoil 2.3%

The last two are interesting. Diesel and jetfuel content is very regional and NOT entirely correlated to API. More middle distillates in the higher API Algerian stuff than the UAE stuff. Counter intuitive.

If I were making an oil investment (which I’m not going to), I would dig down through refinery data to figure out which refineries and which sources of crude were the best for making jet fuel. Jet fuel seems likely to have strong demand much longer than anything else.

Can’t be bothered to do it, though. Someone else might find it entertaining to do so.

This is the Permian according to the Drilling Productivity Report. They have the Permian up by 70,250 barrels per day in March and up by about 180,000 bpd from the last RRC report in November.

Is this realistic?

Sure. The Permian’s the only oil boom area right now (except maybe that field in Kazakhstan). The modern fracking etc. techniques mean that the results from drilling are pretty quick, though they run out faster. The Permian had more conventional oil than the other fracked areas as well, which makes it more cost-effecrtive.

Given the “gold rush” in the Permian right now it probably won’t peak for a year or two; it’s behind the other fracked areas on timeline. The interesting thing is the degree to which it is the last. Everyone and his brother is rushing to this fairly small field *because they can’t find anything profitable anywhere else*.

I’ve raised this question here before. People who are touting the great future for oil might be the ones who are actually selling right now. This article goes into the idea in depth. This author suggests that the sellers will be in better shape than the buyers.

Why a NYMEX Veteran is Getting Nervous about Oil | Wolf Street: “In other words, US producers are hedging their production by selling futures. So Dicker asks, ‘Are they necessarily more right than the speculators?

‘History – or at least my long history in futures – says that they almost always are. In a battle between pure money on one side and commercial physical assets that are the underlying “currency” of the bet, the commercials almost always come out on top.’”

Dood, what does great future mean?

Does it mean oil is civilization’s lifeblood and will continue to be that in 2017? Then yes. 2018? Yes.

Does it mean tractors can’t plant enough food within a growing season to feed 7 billion people unless they have oil in 2017? Then yes, a great future. 2018? Yes. 2019? Yes. 2020? Yes. 2021? Yes.

Does it mean oil is getting more and more scarce and the price will rise? Well, that’s half true. So half great.

Does it mean consumption will continue to rise, as all statistics show it is doing? No. You can’t consume what doesn’t get produced. Demand — in the context of an urgent desire for it — will rise. Consumption will not.

So that would say oil’s future is less great if it can’t be produced to meet demand. Does this mean the price will rise? No. (Gasp) Does it mean the price will rise to induce more production and end scarcity? No. Scarcity will defy price because geology overwhelms economics.

So oil’s future stops being great. As does yours.

I assume your comments are directed to those here who think oil production will continue to rise, but at the same time prices will also rise, making it a great investment.

I’m a peak oil believer and think we should prepare for that future. I cite a lot of sources because sometimes folks here try to tell me I don’t know what I am writing about. So if they don’t want to believe me, look at what business writers and analysts are saying.

We’re dealing with both facts and perceptions. The facts are what amounts of oil and gas are currently being produced. The perceptions are political and investment sentiment. People are trying to manipulate those two all of the time. That’s why I appreciate this forum because it mostly focuses on facts.

I’ve been particularly interested in what the Trump administration plans to do with the gas and oil industry. Seems like most of his talk has been to open the floodgates for more development. Geology aside, more product is likely to mean lower prices, which discourages production.

We have talked about sanctions. Some people have said that sanctions against Russia haven’t hurt its production, and yet talk of sanctions against Iran seems to boost market sentiment concerning oil prices. So are sanctions an effective way to pull oil off the market and therefore raise prices, or not?

So while it is all politics, politics does seem to influence oil prices, oil production, and oil trade. Of course, as oil runs out, politics will change. Will there be wars to conquer supplies? Or will countries have switched over to renewables so peak oil won’t affect them so much?

So p9litical statements and political actions do either directly or indirectly affect the economics of oil.

Optimal war is not likely to be conquering supplies. That’s just foolish. They are vulnerable to the next guy. And while the conquering is going on, supply doesn’t flow.

The Watcher Spectrum of Oil Conflict is this:

Phase 1. Use force to secure supply flow. Pretty much flowing to anyone. This is why varied military presence in the Middle East has been a reality for what, 40 yrs?

Phase 2. Use force to deny flow to a consumption competitor. And probably revector the flow to oneself. This would be China interdicting flow to Japan.

Phase 3. Use force to reduce the competitor’s consumption via population reduction. This will occur in a two step process. First, you embargo oil from the competitor and do NOT reduce their population. You wait for that full population to consume their on site storage. Then Step 2 is you wait for surrender and then manufacture a violation of the surrender to justify forced population reduction so they don’t consume as much in the ensuing peace.

From yesterday.

How to Raise Oil Prices Without Really Cutting – Bloomberg View: “The developed world’s commercial oil stocks dropped in January, but they still stand at around 299 million barrels above the five-year average. If the stocks fell by the entire amount of the January production cut, it would take them 200 days or more, depending on whether the IEA or OPEC got the size of the cut right, to get them to that average level. Of course, the stocks won’t fall this quickly because the market is not balanced yet.”

Gobbledygook. What good is a 5 yr average with relentlessly increasing consumption, similarly relentlessly shortening the period of time represented by a given (alleged) storage amount.

Art Berman posted a new one

http://www.artberman.com/oil-prices-are-at-least-7-per-barrel-too-high/

The article by Aude Illig and Ian Schindler is now published in its final version “Oil Extraction, Economic Growth, and Oil Price Dynamics” in Charles A.S. Hall et al. journal Biophys Econ Resour Qual. It can be downloaded from http://link.springer.com/article/10.1007/s41247-016-0016-6

The study has been discussed here before.

It’s a good article and gives a perfectly reasonable hysteresis-based model for oil market price cycles, both in the increasing-volume period and in the declining-volume period.

Unfortunately it only spends one sentence on the substitution effect. Demand for oil can drop without reducing standard of living if there is a cheaper substitute. And, of course, there now is.

“Demand for oil can drop without reducing standard of living if there is a cheaper substitute.”

I guess you mean: “Demand for oil can drop without reducing standard of living if there is a cheaper substitute that can be scaled up faster than oil declines.”?

Net energy supplied to society and energy carriers than can be used in available technology is the key. I think there will be a new oil price rally/boom cycle sometime between 2020-2023. EVs will still have an insignificant market share, depletion never sleeps and there aren’t much new supplies coming onstream. The alternative is economic meltdown to kill demand.

A map of every active oil and gas well in the United States

The Washington Post (Feb. 14, 2017)

There are more than 900,000 active oil and gas wells in the United States, and more than 130,000 have been drilled since 2010, according to Drillinginfo, a company that provides data and analysis to the drilling industry.

https://www.washingtonpost.com/graphics/national/united-states-of-oil/?tid=ss_tw

Genscape – Keystone XL, Dakota Access Could Cause Bottlenecks at U.S. Mid-Continent Storage Hubs, Shift Crude Prices

At the beginning of February, there were 18 pipelines carrying crude into Cushing, totaling 3.6 million bpd of capacity, compared to 15 pipelines with nearly 2.7 million bpd of capacity carrying crude out of the hub. Inflow capacity is currently outpacing outflow capacity, with a net capacity of 841,000 bpd. The imbalance is actually 221,000 bpd greater than in 2012 when Cushing bottlenecked. However, no bottleneck has occurred in the past year because of a difference in capacity utilization for pipes moving in and out of Cushing.

http://www.genscape.com/blog/keystone-xl-dakota-access-could-cause-bottlenecks-us-mid-continent-storage-hubs-shift-crude

Do these pipelines make economic sense right now?

Pipelines are the cheapest way of transporting oil and gas. So of course existing pipelines make economic sense. The only question is “does building new pipelines make economic sense”? That would depend on whether or not the oil they will deliver will keep coming out of the ground.

That’s what I meant. Does it make economic sense to add the two pipelines that Trump has approved?

Oil prices wobble after EIA reports large rise in US crude stockpiles: “U.S. inventories rose by a larger-than-expected 9.5 million barrels last week to a total of 518.1 million barrels in the week through Feb. 10, the Energy Information Administration (EIA) reported. Analysts expected U.S. crude inventories to rise by 3.5 million barrels.”

I ran the estimates for those two pipelines; the tar sands one can probably recover its upfront costs within two years, so it’s mildly profitable. The one to the Bakken is probably not profitable. Neither of them is what I’d call a *good* investment (poor rates of return).

I assume Trump and the GOP won’t actually be able to slap a tax on all imports, but that possibility has been given as another reason why Canadian oil producers may be looking for somewhere else to send their oil than to the US.

The Bakken data is out with the December production numbers.

Director’s Cut

Bakken production down 86,150 barrels per day 895,330 bpd.

North Dakota production down 92,029 bpd to 942,455 bpd.

That’s an 8.9% drop in one month. However that was partly due to the shutting down of a lot of wells. The number of producing wells dropped by 183, from 13,520 to 13,337. 81 new wells were brought on line so that means 264 wells had to be shut down.

The above well count numbers are from the Director’s Cut. The numbers from the North Dakota official data has the well count going from 13,201 to 13,013, a decline of 188.

I will have a Bakken post out Friday.

You gonna do a full Ronpost?

Re pipelines and the Prez.

1) They are about jobs. There are worse things they could be about.

2) No spike in US consumption. BP says 20 mbpd. Only a slight rise for 2015 and no evidence of any big 2016 delta. Probably up a smidgeon. Hard to make a case for new impacts on Cushing if outflow is what it has been. Operative word “new”.

I’m not talking about why Trump okayed the pipelines. I’m talking about whether they will be built.

I mean, if the government wants to pay out its own money for jobs, then we could be paying for road and bridge repair.

If it falls to private companies to foot the bill for the pipelines, then will they do so right now?

Don’t think there has ever been a presumption the gubmint would pay for the pipeline. Privately owned.

Lotsa handwaving and talk of consumers paying for it in amortized pricetag, but there’s no gubmint fiscal line item.

I realize there hasn’t been talk of the government paying for it. But it’s not going to be as big a job creator as other projects. So the jobs issue is kind of a wash at best.

Trump was always going to support the pipeline because it makes him look like the “anti-Obama” and a friend to the oil industry.

He has nothing to lose by supporting those projects.

It has already been suggested that the pipelines may no longer be economically viable. And the Cushing article just seems to add another reason to potentially delay or shelve the projects.

You gonna do a full Ronpost?

I have changed my mind.

Okay, Bruno just posted me a couple of charts so I will have enough for a Bakken post. It will be out Friday.

The directors cut also has natural gas declining 221, 464 mcf/d. About a 12.5% month/month decline.

I’m trying to think what happens to the excess pipeline capacity.

I guess maybe Dakota Prairie Refinery gets shut down first; it’s already economicallly unsound.

Hi. In my data, were confidential wells are not included, production dropped by around 10%, which is a huge drop MoM. Total number of producing days dropped around 3,5 %. So it can only explain some of it. Looking at the graph bellow we can see that production dropped quite a lot for all years. It doesn´t look natural. So I believe the companies are doing something.

In this graph we can see that GOR also dropped for all years. Maybe they have started to choke the wells and perhaps it could have something to do with the new flared gas regulations that came in 2016? But I thought they came in November and not December.

” production dropped quite a lot for all years. It doesn´t look natural. So I believe the companies are doing something.”

This was the biggest monthly decline in Bakken’s history. I agree that it doesn´t look natural.

How about the recent odd rise was bogus and they are fixing it?

One explanation is that the odd rise immediately followed by the odd fall was just bad data. Or “noise” as the math guys like to say.

Could drop have something to do with weather?

“There were three significant precipitation events, fifteen days with wind speeds in excess of 35 mph (too high for completion work), and nine days with temperatures below -10F. January 2017 will be more of the same.”

15 days without completions but they managed 81 versus 84 previous month, and DUCs dropped 32, so it was mainly spuds that were down, so maybe not. The cold weather might disrupt things though, possible frozen pipelines or water storage, but then only 54 additional wells were taken offline. If it is weather the production will likely not recover until February numbers.

They state: “The percentage of gas flared increased to 14% due to winter weather related freezing problems.” So there obviously have been some problems. The rate increased by 3%, but at the same time they have been bringing on line other gas handling facilities so the weather impact may have been greater. If they are coping with the issue by flaring then there would not have been such a big impact on oil production, but I think it the most likely explanation – maybe they flare until they rich their limit and then have to shut in.

Yes that sounds plausible. But on the other hand, it is winter every year and the problems have not been this big before.

Maybe they had more leeway with flare allocation before so could keep producing the oil, or maybe they were growing so aggressively that the issue didn’t show up, or maybe it’s been a really bad winter – which it has over the holidays: the hot air in the Atlantic pushed cold air south, I think there has been about 5 foot of snow on the ground and near blizzards.

In the AEO 2017, the EIA projects Bakken output to peak at around 2 mb/d by 2030.

Looks quite optimistic given the current production trends

http://www.eia.gov/todayinenergy/detail.php?id=29932

Assuming the rate declines at 10% per year after their 2050 number (which they give in the data table) that graph means they are assuming over 100 Gb of recoverable oil in the tight plays, on top of what has been produced. Looks to be split about 30 / 15 / 40 /15 – i.e. 30 Gb in the Bakken, about 40% up on even their ‘optimistic’ 18 Gb from last month and five times the estimate from the Carbon Institute analysis. And given that kind of reserve there is no possible way the E&Ps would keep production flat for 25 years, they would go for full boom and bust like they always do.

In AEO-2016, LTO production projections were even higher, with the Bakken peaking at around 2.5 mb/d

In oil mystery, traders resort to ‘buy the builds’ mantra: “Doug King, co-founder of the $229m Merchant Commodity Fund, said he saw ‘a lot of agendas’ behind the buying, from big macro hedge funds defending bullish positions to Opec countries trying to ensure the market rides out excess stocks before the group’s cuts are felt.”

“It is difficult to identify buyers given the anonymous nature of futures markets. A trader at a big US energy merchant said the surge of post-report volume was unmistakable, even as he had ‘no clue’ who it was. ‘Everybody sees it,’ he said.”

“Olivier Jakob of Petromatrix, a Swiss-based energy consultancy, said strong buying volumes generally came about 10 minutes after the reports.

‘It seems clear that someone there is implementing a defined strategy, but we are still in a price range because the strong buying that systematically comes after the release of the weekly report is not followed by continued strong buying on the Thursday and Friday,’ he wrote in a note last week.”

The pattern happened again today.

Oil reverses course and pulls back after brief rally | Reuters

I put this in the wrong location, so I am reposting it here.

Oil prices wobble after EIA reports large rise in US crude stockpiles: “U.S. inventories rose by a larger-than-expected 9.5 million barrels last week to a total of 518.1 million barrels in the week through Feb. 10, the Energy Information Administration (EIA) reported. Analysts expected U.S. crude inventories to rise by 3.5 million barrels.”

Ron, if you do a full Bakken Ronpost, I’ll repaste this.

Went thru Director’s Cut and the notices of proposed rulemaking and new rules in general.

Two are eye catching.

1) There’s a blurb about change of measurement methodology. Doing more reading because it seems to be about redefining what API number is quoted for Bakken flow, but that is not the thrust of the measurement focus. Rather, they want to avoid getting a “variance” from BLM for reporting flow/day for royalty purposes.

2) This one is eyebrow raising. 1/10/2017 a notice of proposed rulemaking is quoted that would require new Reid Vapor Pressure number limits on railcar transport. NoDak takes issue with the number because it would significantly reduce how many railcars qualify. Political suspicions would frown at the date and sabotage, but probably of more significance is the whole exploding railcar thing has been off the radar screen for what, years? So why now?

If I’m not mistaken, this means that the North Dakota production (BPD) is now only slightly more than than the existing pipeline capacity leading out of North Dakota (BPD), which is 851,000 at the end of 2016. Production will probably be down to the existing pipeline capacity by March.

https://ndpipelines.files.wordpress.com/2012/04/williston-basin-transportation-table-nov-2016.jpg

Now this isn’t quite comparable because part of the Williston isn’t in North Dakota, so I’d have to look at the Montana numbers. But still, it looks likely that the moment Dakota Access is built, there will be a pipeline capacity glut.

So is the Dakota Access Pipeline going to be half-empty, or will some of the other pipelines be empty and go bankrupt? They’re fighting over market share in a surplus-capacity environment.

Nah. The pipeline will collect its own $$/flow number. You don’t go bankrupt when revenue is coming in for not much labor costs. At most it just extends the payback period.

You still build it. No rule of the universe says you have to have pipeline capacity equal to flow. Better more capacity than less.

Construction costs can be covered even if oil prices are low and there isn’t much oil flowing through the pipeline?

If it extends the payback period far enough, is the pipeline company going to go forward?

Are the numbers going to look good enough to investors and lenders?

Didn’t the producers have to agree to pay a certain amount to the Keystone XL pipeline? I thought that’s why it’s now iffy. They don’t necessarily want to do that anymore.

US bankruptcy judge lets oil company shed pipeline contracts: “A judge has allowed a US oil and gas company to abandon pipeline contracts while in bankruptcy in a decision that could rattle investors in energy infrastructure.”

This is a PDF document, so I am linking to the cached version.

The High-Risk Financing Behind the Dakota Access Pipeline – Ieefa: The rush to build the controversial Dakota Access Pipeline stems largely from the financial motivations of Energy Transfer Partners, motivations that do not necessarily coincide with the interests of Bakken oil drillers or with any economic rationale for increased regional pipeline capacity. The contracts for DAPL were signed in a radically different economic environment in which Bakken oil production was growing and drilling companies were doing well financially. The DAPL is a superfluous project being built to preserve the favorable contract terms that its developers negotiated in 2014.”

The problem is that the pipeline had to be completed by January 1, 2017 for those contracts to hold. Now that it is past the date, the producers can get out of the contracts they signed.

You guys are going wacko.

Reduced flow isn’t going to stop the build. It hasn’t stopped drilling so why would it stop the build.

It’s about jobs. Whenever you feel your arms start to flail above your head repeat that to yourself. The Prez wants jobs, and before you think short term jobs don’t mean anything, remember that short term jobs don’t get automated.

Who is going to pay for the build? More clueless investors and greedy lenders?

Why would that be any different from the oil fields themselves? And the Prez wants it. They’ll ingratiate.

True, we have investors and lenders throwing money at unprofitable oil companies. Those same people may throw money away at unprofitable pipelines.

Now, if they are doing it because Trump wants it, then they are even more deluded. Investing in companies because “the president wants you to” is not a sound investment principle.

Oh well, fleece those Trump investors so they have less money. Will they get mad, or just disappear into a lower net worth category?

I’ve published my take on the new Bakken numbers here.

Enno,

Thanks for the update.

You numbers for ND oil production are slightly lower than NDIC numbers, but slightly higher than NDIC numbers for ND Bakken.

Are you including confidential wells?

Some calculations for N.Dakota based on your numbers:

In December 2014, there were 2277 wells that started production in 2014, with combined output of 595 kb/d and average output per well of 261 b/d.

In December 2015, there were 1535 wells that started production in 2015, with combined output of 404 kb/d and average output per well of 262 b/d.

In December 2016, there were 736 wells that started production in 2016, with combined output of 245 kb/d and average output per well of 333 b/d.

In December 2016, news wells (that started production in 2016) were producing 158 kb/d less than new wells in December 2015, and 350 kb/d less than new wells in December 2014, despite much higher average output per new well.

The number of wells that started production in 2016 was more than 2 times less than in 2015, and about 3 times less than in 2014.

Even more striking declines in drilling/completion activity for individual operators.

In December 2016, Continental had only 21 producing wells that started production in 2016, with combined output of 8.6 kb/d

In December 2015, it had 152 producing wells that were started in 2015,

with combined output of 45.1 kb/d.

In December 2014, it had 253 producing wells that were started in 2014,

with combined output of 58.9 kb/d.

So, the number of new producing wells for CLR in 2016 was 12 times less than in 2014.

CLR guidance for 2017:

“The Company plans to complete 131 gross (100 net) operated wells out of its Bakken uncompleted well inventory with first production commencing by year end. In addition, Continental plans to complete with first production approximately 17 gross (8 net) newly drilled Bakken wells in 2017. At year-end 2017, the Company expects to have 140 Bakken wells in inventory, of which 72 gross (40 net) wells will have been completed but waiting on first sales and 68 gross (47 net) operated wells will be waiting on completion.

The Company also plans to participate in completing 40 net non-operated wells in 2017, 35 of which will be in the Bakken.

Continental expects to grow Bakken production by approximately 26% in 2017, when comparing the 2017 exit rate to the fourth quarter 2016.

Approximately $550 million, or 70%, of the operated Bakken capital investment in 2017 will be focused on completing wells from the Company’s uncompleted well inventory. The Company has five stimulation crews working currently and plans to average seven crews for 2017 as a whole.

Continental plans to apply various enhanced stimulation techniques on all Bakken completions in 2017 to define the optimum designs for future completions. This includes larger proppant loads, diverter technology, shorter stage lengths and shorter cluster spacing. The Company is also applying high-rate production lift technology to accelerate fluid recovery and early production rates. Combined, these techniques add an average of approximately $1.4 million to the previous standard enhanced completion cost of $3.5 million.

For the uncompleted well inventory, the average budgeted completion cost for the larger enhanced completion is approximately $4.9 million per well. The incremental investment is budgeted to deliver an average estimated ultimate recovery (EUR) of 980,000 Boe per well, or approximately 15% over the previous average EUR of 850,000 Boe per well. At $55 per barrel WTI, these completions should generate a cost forward average rate of return in excess of 100%.

The Company also plans to maintain four operated drilling rigs in the Bakken throughout 2017 and drill 101 gross (57 net) operated wells, with 17 gross (8 net) of these wells completed in 2017 with first production. The 17 gross wells will have an average budgeted well cost of approximately $7.0 million. The average EUR for wells drilled in 2017 is expected to be 920,000 Boe per well. At a WTI price of $55 per barrel, these wells should generate over a 40% rate of return.”

http://nocache-phx.corporate-ir.net/phoenix.zhtml?c=197380&p=irol-newsArticle&ID=2239817

Are they producing mainly gas?

According to Enno, an average Bakken well gives about 200k+ of oil, not 900k. It looks like it’s much more gas than oil, or the numbers are completely bogus. Or they have bought the sweetest center of all sweet spots in Bakken?

Questions over questions…

As of 3Q16, oil accounted for 61% of total CLR output.

Apparently, oil’s share in CLR production in the Bakken is higher.

According to Enno, CLR Bakken wells with the first flow in 2014 have on average already produced > 200kb of oil. Their average EUR may exceed 400 kb and probably reach 500 kb.

Wells with first flow in 2015 and 2016 perform better.

That said, even including gas, EURs of 900 kboe look unrealistic

AlexS.

I have mentioned company proved reserves and PV10 quite a bit here in the past two years.

I am coming to the opinion that these numbers, required by the SEC, have too many uncertainties to make them worthwhile, at least as to PUD. PDP may be useful.

shallow sand,

I agree. I think PUD estimates for tight oil formations are much more uncertain compared with conventional fields.

They appear to have been increasing well performance since 2014, maybe getting above 400k for oil if the curves continue (as below). It looks like they recomplete after some time. It will be interesting to see how the two 2016 curves go – started high and then the first took a dive. The late 2015 wells did the same and then jumped up, which looks like a re-completion. How much area does one of their new wells drain? Presumably the savings must mostly be on reduced drilling and completions cost, and maybe front loading the returns with higher initial production, not overall additional recovery.

Marathon announced today they’d have six rigs average this year – up one – not sure if that is enough to hold the decline near present levels, mostly that depends on completions rather than rigs though, but they are going for “multiple enhanced completion trials” and expect to increase overall USA production by up to 20% (also six rigs in Eagle Ford).

http://www.marathonoil.com/News/Press_Releases/Press_Release/?id=1012103

“The incremental investment is budgeted to deliver an average estimated ultimate recovery (EUR) of 980,000 Boe per well, or approximately 15% over the previous average EUR of 850,000 Boe per well. At $55 per barrel WTI, these completions should generate a cost forward average rate of return in excess of 100%”

The estimated EUR’s appear VERY high for Bakken wells by my untrained eye. Any thoughts from the resident experts?

I am certainly not an expert on tight oil but see above. If they get 30 to 40% extra from gas I think they might make it (GOR of 1500 adds 25% I think, and it looks like it will be more than that for most wells). What I don’t get is a ‘previous average’ of 850,000. There’s not even one well that looks like that at the moment, based on Enno Peters’ charts.

Ya know what catches my eye on the supercool graphs?

Look at the decline slopes just past the peak for 2010, 2011, even 2012.

Compare to the damn near vertical 2014 decline curve, which would be the last year before price smash changed behavior. That looks a LOT like geology is speaking. Those earlier years were MUCH more shallow a slope.

Yes, the graphs’ parameters are fun.

old – but useful to discussion:

http://www.hawthornoiltransportation.com/tariffs/ND_RatesRegs_070112.pdf

FYI BP posted an earnings miss today. 4% stock drop. Dividend yield now 7.1%.

No more profits to be capitalized, time to socialize the costs.

Alberta orphan oil well tally jumps as Lexin licenses suspended

By Nia Williams | Reuters | CALGARY, Alberta Wed Feb 15, 2017 | 2:41pm EST

Alberta’s Growing $30-Billion Liability: Inactive Wells

Compared to other jurisdictions, province lets oil firms off the hook when it comes to cleaning up.

By Andrew Nikiforuk 13 Feb 2017 | TheTyee.ca

Mexico’s Gulf of Mexico: Round 2 – shallow water licensing

map https://pbs.twimg.com/media/C4u4mhiUYAAmLBJ.jpg

Delayed by three months as they didn’t get enough interest with the first try in December. I don’t know if they’ve changed anything in the leases to make them more attractive or are just relying on more optimism and available money in the E&Ps.

Rystad Energy have a new article…

2017 offshore activity shows remarkable competitiveness against shale

One of the key reasons for offshore projects starting to becoming competitive again, is the strong deflation of unit prices which is actually higher for offshore than onshore. In 2016, unit prices for offshore developments have been reduced 27% from the peak in 2014 for awarded contracts. One of the key segments, which have helped the offshore cost to come down, is related to the immense pressure on dayrates for drilling rigs. Here, prices have come down more than 50%.

https://www.rystadenergy.com/NewsEvents/Newsletters/OfsArchive/ofs-february-2017

How U.S. crude-oil inventories rose to their highest level ever – MarketWatch: “Demand slowdown: S&P Global Platts estimated Chinese oil demand growth of 1.3% in 2016 to 11.35 million barrels a day, but that was down from 6.6% growth in 2015, when price declines boosted demand.

Reuters calculated Chinese oil demand growth of 2.5% in 2016, based on official data—a three-year low—down from 3.1% in 2015.”

These numbers are not consistent with the BP bible, which can be downloaded as a vast, detailed spreadsheet free from their site.

There can be some mild variation oil vs all liquids, but 2015’s Chinese consumption growth was 5% to just about 12 mbpd. Seems unlikely all liquids added 2 full % to Chinese consumption growth over oil.

One would expect variance in estimates, but that’s a lot.

2% of 12 mbd is 0.24 mbd. Some of that may be explained from different assumptions on how much that goes into strategic stockpiles. I think that BP only include commercial inventory – not sure tough.

I recently emailed BP about a question that arose here about a cosumption variance from JODI or IEA data. To my surprise a reply arrived in which they noted that essentially they are more comprehensive in capturing consumption than they (BP, they carefully did not comment on the other org’s methods) had been previously and laid out details.

Those folks know their stuff. China’s consumption growth in 2015 was 5%. (India’s was 7%)

Btw, a purchase for storage is demand, not consumption, trala trala.

Bakken data were out yesterday and we have seen a steep drop below 900 000 bbl/d nearly 300 000 bbl/d below its peak of 1.164 mill bbl/d in December (see below chart). Well performance (new and existing wells) is down to a five year low of 83 bbl per well and falling -20% year over year. This means a cost increase per produced barrel of 20%, even if new wells are performing better and costs per rig are down.

Since the well production declines by -20% over two years now, costs per produced barrel are up 40% and rising fast. No wonder companies seem to abandon Bakken for less mature fields such as the Permian. New permits are at five year low and rig count is also grinding down slowly. Inerestingly, number of wells are also falling – down 100 wells in December – which has been deemed as impossible in some forecasting models.

Perhaps the Dakota access pipeline can be extended to Canada and used instead of Keystone XL?

North Dakota completions for Jan & Feb in both 2014 & 2015 looks like they took a big dip probably due to the weather, not sure about December production…

In their 11th annual review of oil sands supply costs, the Canadian Energy Research Institute (CERI) concludes all new oil sands projects unprofitable (at current oil prices) . . .

The plant gate supply costs, which exclude transportation and blending costs, are C$43.31/bbl for a SAGD project and C$70.08/bbl for a stand-alone mine.

After adjusting for blending and transportation, the WTI equivalent supply costs at Cushing for SAGD projects is US$60.52/bbl, and US$75.73/bbl for a stand-alone mine. In comparison to last year’s update, the WTI equivalent costs for a greenfield SAGD project are 25 percent lower and 16 percent lower for a stand-alone mine based on lower operating costs, changes in US/CDN exchange rate assumption and a lack of premium on diluent costs. At current WTI prices of just above US$50/bbl, one can assume that these greenfield projects are not economic or have to accept a lower rate of return.

http://resources.ceri.ca/PDF/Pubs/Studies/Study_163_Executive_Summary.pdf

Suncor Energy announced a scope change, construction delay and capital cost increase for its upcoming Fort Hills Oil Sands Mine. The revisions were blamed on the Alberta wildfires and design changes made to the plant’s Froth Treatment facility. Despite the cost increase, Suncor says the project’s capital intensity remains in-line with its sanction guidance of CAD$80,000 to $83,000 per flowing barrel, excluding foreign exchange impacts.

Partner Teck Resources put out a more cautious forecast and estimates the plant will produce 186,000 bbl/day over the life of the project. Factoring in a lower Canadian dollar (which has declined over 20% since the project was sanctioned in 2013), capital intensity could be as high as C$91,000/bbl.

As a point of comparison, capital costs for Imperial Oil’s Kearl Oil Sands project (which has a comparable process and product), were estimated at $22 billion for 220,000 bbl/day of bitumen production, or C$100,000 per flowing barrel.

http://www.oilsandsmagazine.com/oilsands-weekly/2017/2/10

Western Canadian Select (WCS), Jan 2017: CAD$52.3 and USD$39.6

Dennis Coyne

If you can provide me with your email privately I will forward the data bases for the reserves for Saudi Arabia, Iran, Iraq, Kuwait and UAE which I know George Kaplan and other might be interested in.

Hi RK,

I can be reached at peakoilbarrel at gee male dot com