A guest post by George Kaplan

Norwegian oil production peaked in 2000 to 2001; gas production may be peaking about now. Oil hit a low in 2013 and then recovered towards a new local peak, probably concurrent with the gas.

Drilling and Development

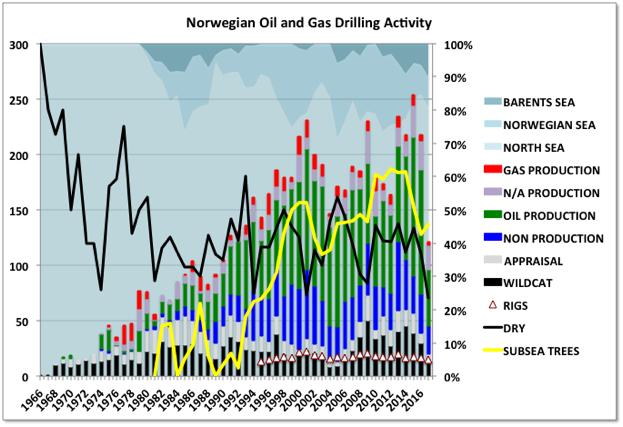

The most surprising thing I find with their industry is that the drop in oil price made almost no difference the drilling activity shown here (all data here and below taken from the NPD – Norwegian Petroleum Directorate – which provides more data than just about any other such organisation).

The chart shows numbers of wells drilled, as stacked bars, and number of operating rigs (unstacked) against the left hand axis, other curves are ratios of total against the right axis. There was a high level of drilling activity in 2013 and 2014 which then actually increased in 2015 and was still high in 2016, although exploration well numbers look to be decreasing now. This may be just a consequence of the momentum built up in the high price years, or because of the influence of Norwegian regulatory regime (which has always sought to smooth out development activity, though less so recently with new Conservative governments), or a move to new frontiers in the Norwegian and Barents Seas (the background area chart shows proportion of wells in each sea). The development wells marked N/A (information not available) are probably mostly oil judging by the fields being drilled, the non-production wells are mostly injection with a few for observation and disposal. The number of rigs and proportion of dry wells have remained pretty steady, as has the proportion of subsea wells. A few of their platforms have dedicated drilling rigs, which means it’s fairly cheap to drill new wells and allows even small, near field deposits to be developed – for example Troll Brent B is a new field in production this year with only 24 mmbbls OOIP (and likely relatively low recovery), and Sindre another which is so small there are no estimates yet. They also use wellhead platforms with jack-ups, which allow lower cost wells than a full subsea development.

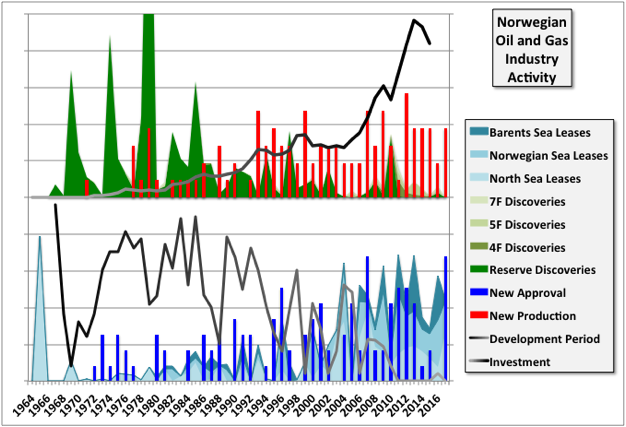

The drilling has not resulted in many discoveries, only the two small fields mentioned above are true ‘reserves’ added in the last five years, although there are a few potential ‘resource’ finds (for description of the meaning of the resource categories 4F etc. see below). Overall, though, there has been a decline in industry activity. Approvals for development fell a lot in 2015 and 2016, but there has been a recovery this year – mostly for small near field tie backs or outreach wells I think – and in particular overall investment fell markedly for the first time in 2014, and then moreso through 2015, after almost continued exponential growth; and will likely be down again in 2016. The number of new fields coming on stream has been steady – a result of past decisions, and lease activity has actually increased, with the Norwegian and Barents Seas attracting more interest (though the North Sea looks close to the end now). The time to develop fields from discovery has reduced as the basin matures, this closely matches the UK and probably most other areas: currently, for fields in development, it is averaging around four years, which means most of the developments are small and require relatively little appraisal, design and construction effort (the chart only shows fields in production and the recent development time is near zero refelecting the two small fields that were immediately tied-in after discovery). In the chart below all the values have been normalised against cumulative totals and adjusted to fit on a common axis with a maximum scale of 10% (leases by acreage, discoveries by recoverable oil equivalents, approvals and new production by number of fields).

Production

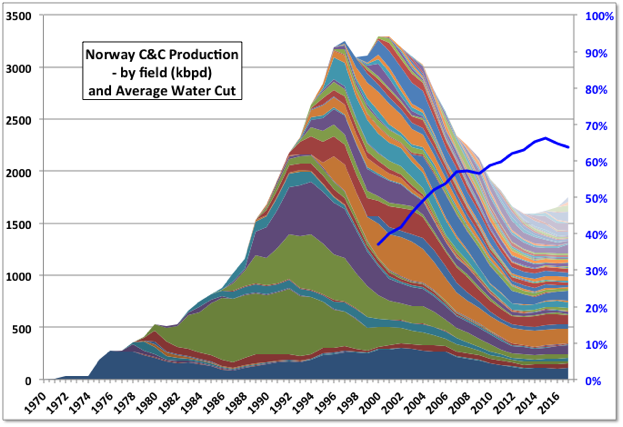

Despite the maintained drilling activity oil production is likely to start falling again in the next couple of years.

The big fields, Ekofisk, Statfjord, Gullfaks and Oseberg, are now close to exhaustion and some are in gas blowdown phase; recent growth has been from many small fields, often subsea tie-backs. The drilling activity from 2010 seems to have arrested a lot of the decline in the older fields and produced a plateau, with newer fields providing a slight increase.

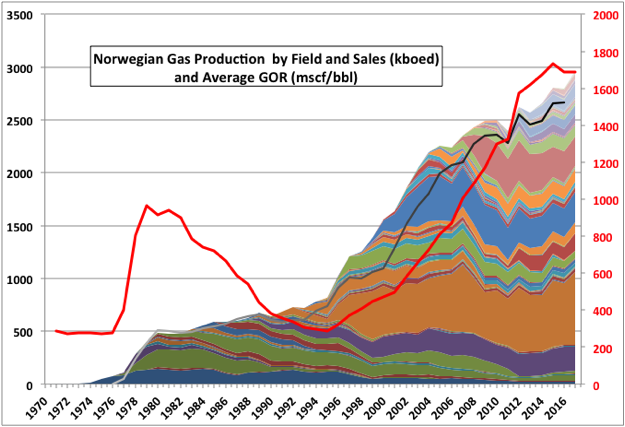

Their more recent successes have been from gas production growth, with Troll the biggest producer by far, but also from Snohvit (producing LNG in the far north) and Aasgard, Sleipner and Ormen Lange. However they are producing these fields hard (possibly to meet sales agreements) and production may be peaking now: and recent additions have been from increasingly smaller fields. Ormen Lange is definitely in decline and Troll production allowance was recently increased by the government, possibly to fill the gap. LNG fields often have long delivery agreements, twenty or more years, and fixed production over that period, but I don’t know if that is the case for Snohvit (they could have come up with a better name as well, if you ask me – I actually did some work on it a very long time ago when they were looking at a floating option, and did bits and pieces on a lot of the other fields too).

Note that the chart shows actual field wellhead production, however a lot of the gas has been re-injected for pressure support on some of the bigger fields, and is (or will be) only produced for sale later in the field life.

Reserves

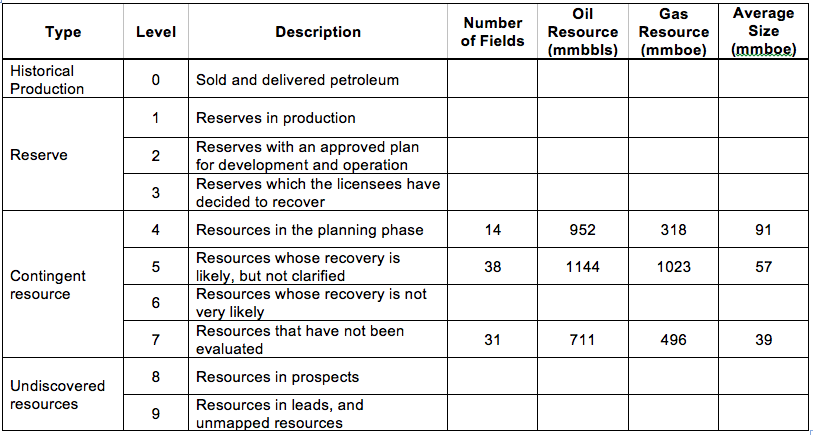

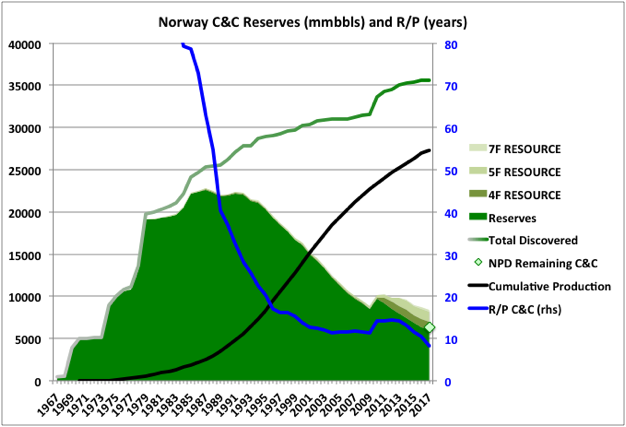

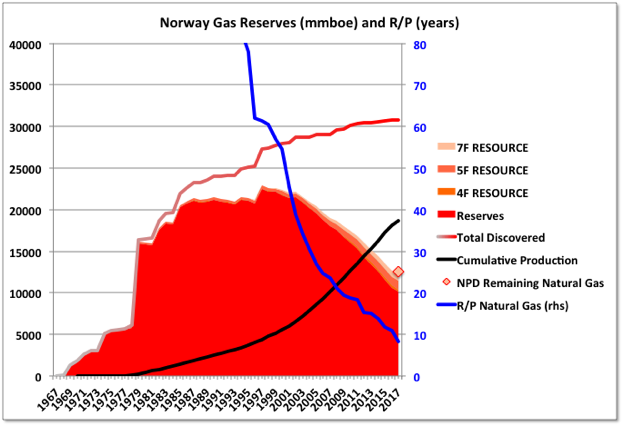

The evolution of reserves for oil and gas is shown below. NPD provides initial discovery and current reserves. I couldn’t quite match these up with production numbers. It’s pretty close for oil but not for gas. I used sales figures for gas (to allow for reinjection) but even so there was about 25% more gas than the reduction in reserves (compared with only 1% for oil). This may be partly to do with measurement issues or with conversion between gas volumes and equivalent barrels (or partly my misunderstanding – if anyone knows more please elaborate). I’ve shown the NPD remaining reserve number against 2017 in the charts.

NPD do not follow the proven-probable-possible-contingent categories used most other places but have reserves and resources at various levels depending on their stage of development. They also split things as ‘F’ for first, and ‘A’ for additional (which I think covers things like EOR if it is being considered). The numbers given below are all for ‘F’ resources only (it might be there are no ‘A’ allowances in any of the fields currently). I’ve only included details for the resource values that might be developed, that doesn’t mean the empty entries are zero.

The big uptick in 2010 is from the Johan Sverdrup discovery, which was almost 2 Gb, found in an area which had been thought to be fairly well explored already. The largest field in the resource categories is Johan Castberg, which is in the Barents Sea. It is a marginal development at current prices, as it needs an FPSO, presumably with some kind of ice resistant hull, and extensive subsea infrastructure. Most of the other resource-only fields are pretty small.

It’s also fair to say that the progress for exploration and development in the northern seas has not been particularly positive. The Snohvit LNG plant and Goliat oil platform each had significant start-up issues. There were high hopes for (expensive) oil exploration wells that have come in dry or with small gas finds (e.g. Korpfjell and Gemini Nord for Statoil this year). Smaller oil discoveries, like the Kayak well at 20 to 50 Gboe and near the expected Johan Carlsbad development, cannot be developed as easily as in the North Sea as there is far less infrastructure (e.g. making gas monetization very difficult so it has to be reinjected) and fewer anchor facilities (i.e. only one at the moment) that can support tie-backs.

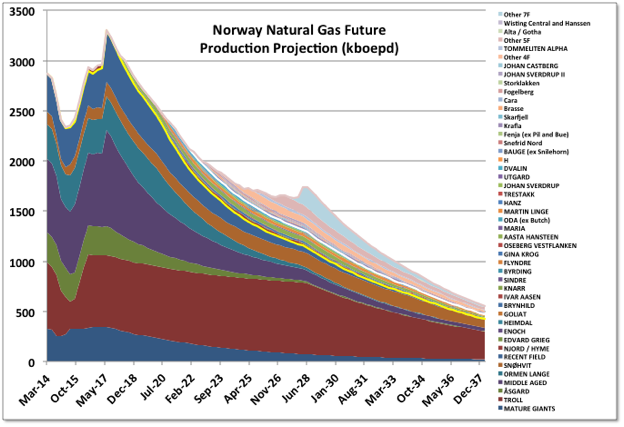

Future Projection

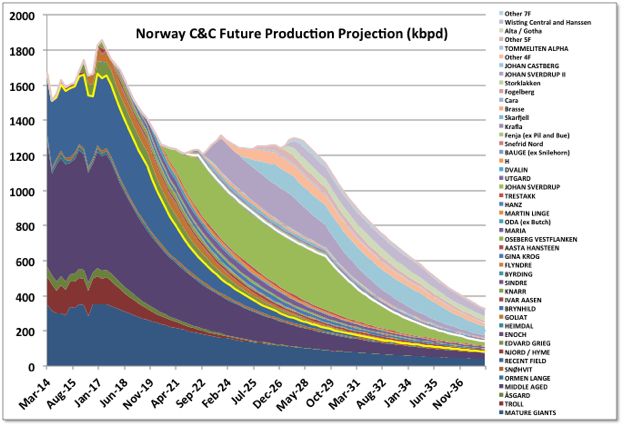

I had a go at projecting oil and gas production based on stated reserves and resources, projects in production and development, and known discoveries. The dominance of gas production makes some of this quite difficult – small gas fields might be produced for only a few years, whereas large ones have long, steady plateaus (maintained by adding compression and new wells) and then can die suddenly.

I’ve included all 4F resources, most 5F and about half 7F (such fields are in lower case). The yellow line shows the limit for fields in production, the white one shows fields in development and those above are in appraisal. The new oil production is dominated by the Johan Sverdrup field, its phase II development is not yet approved but will almost certainly go ahead. Johan Castberg is the second largest, and also pretty likely to proceed (eventually). The total developed liquids, assuming the curves run out forever is 15% above the NPD remaining reserve and resource number (thus allowing for some earlier end-of-life shutdown and a bit of reserve growth). I’m not sure if the decline around 2019 will actually be seen – it’s similar to numbers seen before 2010, but much steeped than has been maintained since. However if the decline rate is reduced near term then it will have to get steeper some time as depletion always wins in the end. To some extent they look to be in a red queen race – trying to maintain a short term plateau to 2030, even the Johan Sverdrup development has much higher production rates than would have been used in the past for such a fields size.

There are some other probable projects that might add more oil. These are redevelopments of existing mature fields. I have included some, e.g. Njord-Hyme, Snorre IOR and Frigg, but there are other possibilities. One of the biggest is Yme, which is an old field abandoned as uneconomic in 2001. NPD do not list any reserve for it, but only about 15% of the OOIP has been recovered. Repsol installed a jack-up to start redeveloping the field, but it was declared structurally unsound and was removed without ever operating in 2013. They are likely to have another try soon.

For gas things are dominated by the long plateau on Troll. There are far fewer undeveloped resources and reserves than for oil and it looks to me that production is peaking about now and decline will soon be obvious. The yellow and white lines show producing, in development and appraisal fields and, as for oil, the total developed natural gas (and NGL), assuming the decline curves run out for ever, is a bit above the NPD stated remaining combined reserves and resources for the fields included.

Off Topic Finish

And to finish here is “Artistin-Marcella” by Ernst Kirchner – nothing to do with Norway that I could find but maybe with a relevant story given some current political trends, and also the flip side of the Renoir in the post about UK production. There is nothing much innocent here. The model was only fifteen but there are suggestions of various kinds of debauchery around. The girl and the cat both look a bit pissed off. All his early paintings make me think it’s raining, or has been raining, or is about to rain. He used various shades of green for almost anything including faces, and they always look great. A painting that somehow makes you want to keep looking and wondering, I think, which I guess is a lot of what Expressionism was all about: it is supposed to be an example of ideal composition with the important elements lined up on the diagonal.

Before WWI Kirchner lived a pretty louche lifestyle: basically a hippy. He volunteered for the army in the war and had a nervous breakdown, followed by alcohol and morphine addiction. A lot of what he painted was probably designed to shock and question, especially the early stuff like this (painted in 1910). His work was declared degenerate by the Nazis and much of it confiscated and/or destroyed. He lived in exile and was very anti Nazi in the inter war years, and he killed himself in 1938, partly over worry of a Nazi invasion of Switzerland to where he had moved. He’s pretty popular now, considered the “German Picasso”; the last major work of his sold was a picture that the Nazi’s had confiscated and had been eventually returned to the original owner’s heir, and it went for $38 million.

Great analysis, again. Thanks very much.

Off topic is the situation in Texas that is likely to confuse until Houston refineries are up again. Most of you have kept up with the fact that most Houston refineries have ceased production, and some damaged. Corpus only received some wind damage, and are expected to be up and running, along with the port by Sept 4. Houston, I expect will take much longer. What has been missed by most of the press and experts, is the amount of production that has been shut in. Some reports are that about 500k a day or more has been shut in for the Eagle Ford. Two major pipelines that run from the Permian to Houston have been shut down. That transports about 625k barrels a day. I don’t think there is any option that they have to shutting down production for that. That’s only what I have heard, so far, sure it is worse than that.

As a consequence of having to shut down all this, I would guess that analysts projections of huge inventory builds are not too well thought out. In total, it would support world inventory decreases, without a doubt.

My guess is that it will wind up decreasing refined products inventory, a lot more than it will increase US inventory builds for crude.

Even when they bring these wells back online, we are likely t continue to see a decline in Texas production for awhile. The shut in wells may not be as good, and what moron is going to complete a well if the piggy can’t go to market?

Hi all,

I got in touch with Mike from Texas and he is doing ok, but said it has been a tough week. He has evacuated a few friends from the coast and delivered supplies to a shelter in Houston. He said things are much worse than most people imagine and that 4 feet of rain in a week is an amazing thing to witness. He expects the 500 kb/d of Eagle Ford output that has been shut in may not come back and wonders if pipeline shutdowns may start affecting the Permian LTO output as well. He expects to get his wells ramped back up starting today.

My best wishes to him and all Texans.

Thanks Dennis.

Good to hear Mike is OK.

Thanks Dennis. Happy to hear he is ok.

Best, Dean

Thanks for that, Dennis.

Days passed before we knew Katrina’s full impact. Likely a wait before the situation here is clear.

Agree. Oil news pales in comparison to the other damage.

Platts does a free daily update & Valero are posting their own updates…

Platts: While some Texas refiners were beginning to restart operations Wednesday as Tropical Storm Harvey moved into Louisiana, others were bringing plants down, causing a further reduction in available refining capacity.

https://www.platts.com/latest-news/oil/newyork/oil-factbox-usgc-refinery-outages-port-closures-26796285

Valero Hurricane Harvey Updates – Update #8 – August 30, 2017 – Released at Noon CST

Refinery startup is underway at Valero’s Three Rivers facility. While we continue the startup process at Corpus Christi, we are closely working with our business partners and port operations to ensure the availability of critical transportation and logistics infrastructure needed to resume all operations.

Houston and Texas City continue to operate. Due to flooding and potential power supply interruption, Valero’s Port Arthur refinery has shut down in a safe, controlled manner. We continue to closely monitor the storm and any impact it may have on our other Gulf Coast operations.

https://www.valero.com/en-us/Pages/HurricaneHarveyUpdates.aspx

EIA refinery map: https://pbs.twimg.com/media/DIVGfrsWsAASFiZ.jpg

About 250,000 cars were destroyed when Sandy hit the East Coast, Smoke said. Car ownership is higher in Houston than New York, which could help explain why the number of cars destroyed by Harvey may be so much higher.

Smoke said it would be “sobering” if Houston lost more than 300,000 cars given that the Houston area has seen 325,000 new vehicle sales in the last 12 months

http://money.cnn.com/2017/08/29/news/harvey-half-a-million-cars/index.html

Could be more, Harris County population is over 4 million and 30% flooded. Most cars are parked on the street. These days the water only has to reach the electronics under the front seat and the car will be a write-off.

According to this video: Motiva and XOM Baytown shutting down CONFIRMED. GS says 23% of US Refining capacity now off-line. Big Q – for how long?

https://www.cnbc.com/2017/08/30/arkema-ceo-no-way-to-potentially-stop-an-explosion.html

Reuters has some good illustrations of how much capacity that has been affected by Harvey and when (http://fingfx.thomsonreuters.com/gfx/rngs/STORM-HARVEY-ENERGY-INFRASTRUCTURE/010050M21F9/index.html). On average it seems to be about 2 mbd of refining capacity that is shut in (less so the first days and now 4+). Refineries that are not affected will compensate some of this (e.g. there is overcapacity in China) but how much remains to be seen and will be affected by the spread as well as available tankers that can ship products.

Considering production, about 20% of GoM is shut down (0.35mbd). Onshore, Eagle ford is also affected because of pipeline and well issues. A figure of 0.5mbd keeps popping up but I can’t find a reliable source. Does anyone know? I haven’t found anything on Permian take away capacity. There is also a disruption in Libya, approx. 0.35mbd.

To sum up, it seems that slightly more than 1mbd of production is currently unavailable and perhaps 2-3 mbd of refining capacity. The temporary supply disruptions add to the current deficit of 1mbd, i.e. making it 2mbd in total which is in the same ballpark as the refinery outages.

Refinery runs are typically lower during the autumn so there should be sufficient refinery capacity available in the coming months even if the damage would take some time to repair. The net effect in a few months’ time should be lower oil stocks but I don’t see product stocks dropping that far. Therefore, I don’t see the oil price fall and gas price rise as sustainable.

The Longhorn and BridgeTex pipelines, that transport crude from Permian to Huston, have been suspended but there is storage capacity in Permian so production is probabaly not affected much.

“Operations on our other crude oil pipeline systems in the Houston area including Longhorn and BridgeTex remain suspended although we are continuing to receive west Texas crude oil into our storage facility at the origin of the Longhorn Pipeline system in Crane Texas.” (https://www.magellanlp.com/Safety/MediaAdvisory.aspx).

What are the decommission costs waiting for Norway?

This is NPD report from 2010:

http://www.npd.no/Global/Engelsk/3-Publications/Reports/endelig-avvikling-rapport-engelsk.pdf

They have fewer installations than UK but more larger ones, and they will be slightly behind the UK in decommissioning effort so they’ll get better estimates based on that previous work. I think you can probably at least double the figure above before adding on the costs from removing the concrete structures (which are 70% of total weight so a pretty big omission) and well P&A (I’m not sure whether pipelines are included in the above numbers or not, but I guess some of those would be abandoned in place). Has a concrete structure offshore ever been removed? At one time there was a plan to turn Statfjord into a hotel / casino and leave it in place.

http://oilprice.com/Latest-Energy-News/World-News/Democratic-Senator-Urges-Trump-To-Sell-Oil-In-Strategic-Reserves.html

“An immediate release of gasoline or crude oil, if also warranted, from the SPR would help protect consumers from price spikes at the pump and tame any market speculation that could be unduly affecting markets and harming consumers,” Markey wrote, according to The Hill. ** An immediate release of gas-o-line from where again? ** What is this Senator’s vocation again? Rehab?

Great display of Markey’s acumen in the hydrocarbon world.

He played a prominent role in blocking gas pipelines into New England while staunchly advocating offshore wind farms.

Hi Coffeeguyz,

Is he on the Supreme Court in Massachusetts?

No.

http://www.pressherald.com/2016/08/17/mass-decision-throws-fate-of-n-e-pipeline-project-into-question/

The Massachusetts Supreme Judicial Court ruled against the state’s Department of Public Utilities’ requirement that electricity customers help subsidize construction of private gas pipelines. The court said private companies should bear all the financial risks.

I am not suggesting that Markey did not applaud this court decision, simply that Massachusetts Law forbids the requirement that electricity users subsidize these pipelines. It is up to the Massachusetts legislature to change those laws if they believe that is best for the people of Massachusetts.

Last time I checked, Markey was not a member of the Massachusetts legislature. This matter is up to the states unless the US Supreme Court decided the Commerce clause overrides (I am not a lawyer and have no clue whether the commerce clause would apply in this case).

In Maine we heat with wood 🙂

Random Assay info of Norway fields:

Ekofisk really proper oil at API 39.9 and 39% middle distillates.

Aasgard pretty light API 53.7 (condensate) only about 11% middle distillates

Troll Blend proper oil API 35.9 30+% middle distillates

Statoil has an assay subpage

The newer fields for Norway and UK are tending to be heavier, some more than others (e.g. Kraken where API 13.7 oil has been partly blamed for start-up delays – that doesn’t separate from water very easily, so there probably more problems to come). Most of the new oil in Norway will be from Johan Sverdrup which is API 28. Asgard is a mixed oil and gas/condensate development, so no surprise that it’s blend is light, I think the oil has declined faster than the gas so I don’t know if they have to blend other oil in to meet the sales assay.

Their page has a lot of Norway listings. No surprise.

No listing for Sverdrup or Kraken. 13.7 would be lower than anything they have listed.

https://www.statoil.com/en/what-we-do/crude-oil-and-condensate-assays.html (scroll)

The spreadsheet they offer for each oil source is excellent for getting jet fuel and diesel.

That Bakken number is just so glaring after years and years of 39 claim. Pre Permian, those Eagle Ford numbers might have gotten them sued.

Many of the other Norway listings I don’t think you mentioned in the article. Are they subsets, or synonyms for fields?

Those assays are really for sales – i.e. to allow bidders (really the refineries) to set a price, JS isn’t producing yet and Kraken is UK and nothing to do with Statoil. The assays are based on the originating field but I don’t know that the oil would necessarily solely come from that one field in all cases.

That reads as if you mean that the oil is tailored and presented to a refinery or refineries. The details on the spreadsheet look an awful lot like they are describing the constituent parts of the oil from that source. The %yield of each level of temperature is laid out.

The tailoring concept is pretty cool and that is certainly done with Suncor output in Canada. The .xls doesn’t look like that, but if that’s what it is, definitely pretty cool.

FYI BP’s site also has an assay sub page.

The blend would need to be something close to what the buyer is expecting, but I don’t know what ranges they have or if they have the ability to change the blend. Output from a facility doesn’t generally change composition very quickly unless a new, and different, field is tied in. A lot of the Norwegian facilities facilities are offloaded by shuttle tanker, so the composition is known well ahead of time. If I had to guess I’d say those assays are from a typical early analysis, and are not continually updated with each new cargo, but wouldn’t be surprised to be wrong.

nod

The assays are dated. Skarv (not Norway) and Stratfjord (on the Norway UK border) are 2017. Troll Blend all the way back to 2011.

Bakken and Eagle Ford 2017.

Bakken liquid has either changed its nature or they were lying 5 yrs ago.

Hi Watcher,

I believe in the Bakken GOR has increased, this usually indicates there would be more condensate as the condensate is part of the gas stream.

You have seen Freddy W’s posts on this, I think.

This is the explanation that requires no accusations of lying.

That is an explanation that doesn’t address where the samples were taken in each year.

That’s how you lie, btw. Be specific what samples you allow.

Skarv is Norway (operated by BP), it’s another oil and gas/condensate mixed development; Statfjord, I think, is in gas cap blowdown. It’s possible they have to update the assay more often for such products because it changes as the ratio of different fields in the mix changes, and/or as the pressure in the gas cap drops the condensate composition changes (probably gets a bit heavier but not necessarily). Troll is a really big field and probably stays pretty constant – though it too has an oil rim and a gas development.

Things are restarting, but the Exxon Baytown refinery and the Port Arthur refineries are likely to take a while as they were flooded. And not seen any news on Exxon Beaumont?

As of 2 p.m. Wednesday, ports of Houston, Texas City, Galveston, Freeport opened with restrictions, Houston ship channel partially re-opened: u.s. coast guard.

Marathon Petroleum reportedly is restarting its 459K bbl/day Galveston Bay refinery after it was shut by Tropical Storm Harvey.

Buckeye Partners is said to have re-started its Corpus Christi terminal after shutting down due to Harvey.

EIA twip: crude dropped 5.4 mmbbls (1.2% and about inline with average trend since April), gasoline no change, diesel up 0.7 mmbbls. I guess Harvey will change things around quite a bit, so trend info will be lost.

https://www.eia.gov/petroleum/weekly/

Hi George,

Below is a chart of US crude stocks (including SPR) from Jan 2016 to Aug 2017 and the average Jan 2014 to Dec 2015 (weekly data) is shown for comparison. Stocks have been falling at about 18 Mb per month since March 31, 2017 and the 2014-2015 average stock level was 1079 Mb and the 5 year average stock level was 1105 Mb. An alternative way to consider stock levels is to look at crude inputs to refineries compared with crude stock levels. From Jan 2012 to Dec 2014 there was an average ratio of crude stocks(including SPR) to crude inputs of 2.21 and by May 2017 the ratio was 2.25 and by the week ending Aug 25 it had fallen to 2.11.

Part of this change is seasonal, so for comparison in 2016 for the week ending August 26 the ratio was 2.35 relative to the 2017 ratio of 2.11, so progress in stock levels has been made since 2016 and the US may be getting close to the “normal” level relative to the past 5 years. At some point we may see crude prices start to move after the dust settles from the recent disaster in Texas.

EIA released updated World C+C estimates on Aug 28. Click on International Petroleum at link below

https://www.eia.gov/totalenergy/data/monthly/index.php

Chart below has monthly data in kb/d and 12 month centered averages.

For 12 month centered average the peak was Sept/Oct 2015 (as predicted by Ron Patterson) at 80,684 kb/d.

The monthly C+C output peak it was 82,991 kb/d in Nov 2016. May 2017 monthly output was 80,364 kb/d and the most recent 12 month centered average was 80,616 kb/d in Nov/Dec 2016. 12 month centered C+C World output has been between 80 and 81 Mb/d from Mar/April 2015 to Nov/Dec 2016.

EIA U.S. June crude oil production 9,097 kb/day, down -73 kb/day m/m. May revised up +1k/day to 9,170 kb/day. The gap between weekly and monthly has grown to 220 kb/day

EIA 914 link: https://www.eia.gov/petroleum/production/#oil-tab

GoM down 23 kbpd m-o-m to 1636, Alaska down 45 kbpd (I guess for maintenance, but also down 7 kbpd y-o-y), North Dakota down 8 kbpd and 4 on the year. GoM might recover a bit in July but with Harvey hitting August and September numbers and maybe Irma to contend with too for September, and now nothing much new due, it looks like decline will dominate, with only a small blip early next year for Stampede.

A long term chart on twitter (from Jan 2010)

https://pbs.twimg.com/media/DIlNsKdXcAAQoCL.jpg

BOEM numbers for GoM have a 43 kbpd drop from 1673 in May to 1631. There are quite a lot of leases not reporting for May or June so there will be some adjustment for both EIA and BOEM numbers, but the higher fall seems more in line with some facilities off line for Hurricane Cindy as well some turn around actiivity (.g I think Thunder Horse was off line for some of the time).

It’s still a long way out but the most likely path for Irma looks set to go straight through the central and east GoM production areas and hit the Tx/La border. I think the GoM waters are still pretty warm so it could pick up a lot of energy especially if it misses any land in the Caribbean.

Irma is a real beast.

This is going to get real interesting.

Perhaps the $.25/gal increase in today’s NYMEX gasoline is an indication of how interesting it is already getting.

If NYMEX traders make things uncomfortable, no reason the government could not intervene and declare the price of gasoline to be whatever they wish, and hide behind the claimed temporary nature of what they do to conceal the reality that price can be decreed.

Pretty easy. Suspend some or all of the tax, but that takes revenue from the government rather than inflict punishment on the traders. Probably more palatable to just declare the price.

Hi Watcher,

That worked so well in the 70s, why not try it again. 🙂

Irrelevant.

If you like long lines control prices. Works every time.

In regards to horizontal drilling with long laterals, I have not read about this, but, rather heard this verbally from friends in the industry. I was wondering if anyone here can confirm:

I have been told that now it is routine to mix 150,000 – 180,000 gallons of diesel fuel into the drilling mud. [Note: nothing to do with the fracking. In the very early 1990’s we used to sell, e.g., 60,000 gallons of diesel fuel to frack a well (pre- sand and water)] The story is that is a key reason for the reduction in time to drill the laterals. The diesel fuel aids in making the bore hole slippery for the drill bit.

They do have a problem of disposing of the drilling mud that is saturated with diesel fuel. But, some counties will allow them to use it on rural road beds and some companies are trying to come up with a recovery method.

I would note that, if true, that created a new market for a lot of diesel fuel that is now harder to get.

To change the subject, there was an article in the Daily Oklahoman a couple of days ago about frac sand. They are opening up sand pits in Texas now. The sand is not the favorite, but they do not need trains to get it to the Permian. So they were touting the huge savings since it is 40% cheaper without the rail cost. However, they also mentioned that in some cases they are using 4 times as much sand per well as a couple of years ago: no mention of the increase in cost that entails.

Clueless

The Bakken offers many leads into how this shale stuff has been evolving – its ‘early in the game’ status along with the relative transparency of operations being prime factors.

Many of the Bakken operators used water based mud as a rule, due to cost and handling issues, while others opted for oil based mud, at !east for the laterals, to reduce friction throughout the 2 mile long laterals.

As time went on, it seems the standard has become more OBM up there.

Other shale areas still have 5 to 7 thousand foot long laterals – along with 6 to 8 thousand foot vertical depth (Bakken is 10/11k) – and as such less of a need for the more expensive OBM. As the laterals continue to lengthen (15,000 to 20,000 foot is the goal for many in the AB), oil based mud will probably become more widely used.

WPX just announced an 8,370′ long lateral drilled in 24 hours in the San Juan basin … 350’/hour.

That is probably the most anywhere in that time frame, although several Appalachian Basin operators regularly drill a mile a day now.

More significantly than the speed, perhaps, is the precision in targeting.

Normal to be within a 5 foot vertical target zone 90/100% of the time now with the hardware and software available.

The huge amounts of sand, especially the tiny 100 mesh, is needed due to the far more extensive fracturing currently being done versus 24 months back.

Alberta’s June total production of 2,996 kb/day which is down from the February high of 3,323 kb/day. Some of Syncrude’s Mildred Lake plant was still offline in June. Not sure if there was anything else?

Hi George

Do you intend to do a post on Dutch production to complete the set. I know it’s predominantly gas but is significant to the European energy mix. I do know extraction from Groningen is under constant review due to all the damage from earthquakes.

Could do I suppose – depends on if the data is available. Denmark also, which is in the end stages. Groningen and some of their other gas fields come from gasified coal rather than kerogen if I remember correctly and they don’t produce much oil or condensate so it would be mostly about gas. I didn’t cover gas much for the UK, more so for Norway though.

Thanks for your good analysis George.

For all the folks interested in renewable power generation, and this whole fossil fuel/alternative situation in general, today’s heat wave in California can offer some good info.

At this posting, 3:30 PM/1530 local time, the caiso.com site shows what’s going on. Specifically, clicking on the “show more’ beneath the current usage (52,000 Mwh … big state, California), the solar input is about 9,400 Mwh. Huge.

If it follows yesterday’s trajectory, it will start to plummet to nothing shortly, just as the 5 to 8 PM surge kicks in.

This is the crux of this whole ‘dispatchability’ situation.

Cali’s solar is producing half of all New England’s current demand, yet in a few moments it will be going bye bye for the night when people still need moar.

Today is both a vivid example of what is possible as well as the vulnerabilities involved.

Yes, solar’s variable production is well known. But note:

It’s not random: we know exactly when and how quickly it will decline; and, solar is just as dispatchable as nuclear – the French make nuclear dispatchable by building it up to handle peak demand, then turning it down when less is needed.

Now, that doesn’t work at night, but don’t forget wind power, which is on average slightly stronger at night. Wind can be made pretty manageable with geographic dispersion, forecasting, etc. And, again, wind can be made dispatchable with overbuilding.

And, don’t forget Demand Side Management; lots of things can be scheduled during the day, especially charging EVs.

Eventually we’ll probably need batteries to get through the night. That’s not a big deal – it’s no more expensive than natural gas peaker plants.

” …need batteries to get through the night”.

Catchy slogan there, Nick.

A lament often put forth by women in this modern age.

But solar does not need to be the only power source. The more solar you use, the less fossil fuel you need. It doesn’t have to be all solar or all gas/coal.

Boomer

That is partially the issue, as Gail Tverberg pointed out in her piece the other day.

Amongst other issues (intermittency being the biggie), when solar is cranking during the day, thermal (gas/coal/nuclear) is not needed as much.

So, these privately owned companies stand around making no moola until sundown, or cloudy days.

This is one reason these guys – especially the nukes – are going bust.

Then, you can throw in a bunch of other stuff like the solar guys getting put first inline to sell their juice.

I think this trickles down to the rooftop guys in some areas where they sell to the utilities.

It’s kind of a hodgepodge of factors that differ somewhat around the globe.

Geography, politics, alternative fuels, economics are all gonna play a big role in how this ultimately shakes out.

Coffeeguyz- I think its a misconception that solar and wind generation “gets put first in line to sell their juice”

It is a generally a difficult process to get a grid interconnection permit for small to medium operators, onerous in fact. Baseload generators such as coal have priority generally. I am not criticizing this policy.

Secondly, the grid operators have a formal curtailment program where they in effect shut off electricity from solar or wind when they have too much.

http://publications.caiso.com/StateOfTheGrid2014/RenewablesIntegration.htm

Hickory

I know very little about the California market specifically, and not a whole lot more about the renewable impact on the global power market in general, but what I am finding out is there exists widely variable policies, resources, incentives and results.

If you check out the feed in tariffs in South Australia’s solar market, those homeowners both get priority and hefty compensation for rooftop juice.

The Scot wind producers are cranking out more electricity than the grid needs, but seem to be compensated by amount of power produced, whether it’s needed or not.

Major disruptions can arise when incorporating these various sources and the distortions, as Tverberg pointed out, can become greatly magnified the more uncertainty/intermittency become part of the system.

It was a very hot one here in Calif today. For example, San Fran (usually cooled by proximity to 57 degree ocean) reached its all-time ever high recorded temp at 106 F.

But the grid kept up with no big outages.

And thanks to first inning solar deployment, the state required much less fossil energy than would have been otherwise needed.

note- it is also very smokey in much of Oregon and N. Calif due to widespread fires.

Well, almost no one here in S.F. has an air conditioner. Not much extra demand. Today I discovered that my imac has an internal fan. I had never heard it turn on in the ten years I’ve lived here. Inside of my house is 104f.

Hi Coffeguyzz,

Comments on renewable energy should be on the other thread which deals with that subject specifically.

I have composed a response to this in the non petroleum thread. Being able to take advantage of solar power to provide cooling after dark is of intense personal interest to me and I have come to the conclusion that this is a huge challenge anywhere air conditioning is regularly used worldwide. It must be a huge opportunity for any smart appliance manufacturers that can bring a effective elegant solution to market. This should be a very big deal.

https://www.energyvoice.com/oilandgas/149338/iraq-fallen-agreed-oil-production-cuts/

(Might be a paywall with limited free articles)

IRAQ HAS FALLEN BELOW AGREED OIL PRODUCTION CUTS

Both the Iraq minister and the article make it sound like there’s day-to-day control of the production, which there isn’t – natural decline would look no different to what has been happening.

Just been having a look at Norway’s forecasts. They give a new forecast every December.

Looks like Irma is going to miss the GoM and Texas, so no oil supply disruption, but might be heading towards Washington DC or New York.

East Coast impact is getting more likely.

Small chance of GOM, as it has been going further west than expected.

Hard to imagine a trajectory with potential to cause more damage than the present one – Washington, Philadelphia, New Jersey Suburbs, NYC, maybe Boston, East Coast Canada – all in it’s sights – and could be them all not just one. Hopefully it will swing out to sea, I think they often do. The East Coast is due gas shortages next week as Harvey impact is seen, I wonder what that will do to any evacuation orders? This should probably be on the other post but you have to reckon with the Jarsier over there.

This is the weatherunderground track ensemble.

EURO just came in with things a bit more east.

Could even be a fish storm.

Will know a lot more by Tuesday.

Yeah – I wouldn’t want to be on one of the oil facilities offshore Newfoundland if the current route holds. Hibernia might be OK but there are two moored FPSOs (might be a drilling rig as well). The FPSOs can be disconnected for ice bergs, but I wonder if they would also for a hurricane.

I should of said the lower 48—

Canada is still in play with that run.

But that is a long way off.

Lorenz helped develop chaos theory with weather models.

Climate Reanalyser has it as a direct hit on North Carolina, I think as a high end category 5, and then probably moving up the coast. Though I think their forecasts aren’t very good more than 3 or 4 days out.

Looking like a SE hit now.

Has drifted much further west.

But still a long way off.

135 kt winds heading for Miami now. It’s moving pretty fast too so the north side is really going to get hit. All the ensemble models seem to be converging now.

Current Landing prediction:

https://uploads.disquscdn.com/images/e5e78708ea8732e302a9ca5d6cfd4b3b7e1bd823b75d488d72b1f98df24eaf91.png?w=800&h=458

Latest tracks are catastrophic for Florida.

Really scary–

We shall see

A couple of models have it hitting central Cuba now – presumably it would then go into the GoM, and probably strengthen again like Harvey as the waters in the east have about 2K anomaly. The main ones (GFS and ECMWF) and all the ensembles have a direct hit on Miami and then moving north almost directly over the shore and eventually into North Carolina. The one good thing looks like the predicted strength (wind speed and minimum pressure) is gradually easing off with each new prediction.

ps Jose looks certain to form as a hurricane just a bit south of where Irma formed. Unless all the troughs and ridges have changed significantly it’s likely to follow Irma west rather than the usual hook into the Atlantic.

Scott just declared a state of emergency in Florida.

All the talk is of running out of water – do people not think just to fill up a container from the tap. When I lived in Houston we had a couple of big collapsible plastic containers that you could fill, I think they were 5 gallons each, and the bath tub would hold as much again.

Argus Media has free updates for oil and gas, Harvey news.

http://www.argusmedia.com/pages/NewsAll.aspx

Saturday, BSEEgov data: 106,813 b/day of Gulf of Mexico oil production (6.1%) is still offline from Harvey, down from the peak last Saturday of 428,500 b/day.

Wonder what the figures are for the Eagleford?

As far as I know the Eagle Ford producers that have stopped are waiting for mid & downstream to restart? In the news…

Baytex – There is currently a limited ability to produce as downstream markets are closed or significantly curtailed.

Statoil ramping up Eagle Ford crude, gas output After Harvey, Rate of resumption limited by bottlenecks in infrastructure. BBG

ConocoPhilips said its Eagle Ford offices had reopened, but it had limited ability to move its oil to market. “Due to limited off take capability, our production in the Eagle Ford has resumed on a limited basis in some areas,” the company said.

Marathon Oil Corp.’s field offices had opened too, and it was assessing its locations and restarting production as “market access allows” Marathon expected to start drilling and completions again this week, too.

Platts (2 Sep 2017) US Gulf Coast refineries, pipelines and ports were in the process of returning to service Saturday as the industry continued its recovery efforts following Hurricane Harvey.

https://www.platts.com/latest-news/oil/newyork/oil-factbox-texas-refineries-pipelines-ports-21824122

Phillips 66 Operations Information Center – Updated Sept. 2

http://www.phillips66.com/EN/newsroom/stormcenter/Pages/index.aspx.

I wonder how many pipe/tubular suppliers, maintenance shops, fabrication yards, engineering offices are out either because of direct impact or as their staff have nowhere to live or nothing to travel by.

It will be interesting to see what impact Harvey had on crude production, both in the EFS and GOM, as well as gasoline supply and demand. Finally, I assume Harvey affected crude imports as well as crude and gasoline exports in a big way.

As we know, EIA weekly tends to be inaccurate and TX data is slow to be complete. We might have a clear picture by November/December.

Read that Denbury Resources shut in about 16,000 BOPD of production in areas impacted by Harvey. I think they are secondary/tertiary recovery barrels.

Apache shut in 30,000 bbls in the Permian last Friday according to An Apache field superintendent I know.

Norway consumption 242K bpd. Production about 2 mbpd. Looked it up to see if they would need import tanker terminals soon. Nope.

They don’t give separate numbers for oil and natural gas, only boe numbers…

Bloomberg with data from consultant Wood Mackenzie Ltd. – 4 September 2017

The U.K. North Sea is on track for the biggest year of oil and gas field startups in a decade, continuing the aging province’s surprising resilience to the crude-market slump.

Fourteen projects with combined peak production of 230,000 barrels of oil equivalent a day will start in the region this year, according to data from consultant Wood Mackenzie Ltd. That’s the most since 2007, reflecting the payoff from multiyear investments begun when oil prices were still over $100 a barrel.

“It’s really the fruits of a very high level of investment in the 2010 to 2014 period,” Mhairidh Evans, senior research analyst for North Sea upstream at Edinburgh-based Wood Mackenzie, said by phone.

Eight fields have already started up this year with an estimated peak production of 140,000 barrels of oil equivalent per day, Wood Mackenzie data show.

https://www.bloomberg.com/news/articles/2017-09-04/u-k-north-sea-oil-field-startups-surge-to-highest-in-10-years-j75n10pi

Very few of the UK fields have recorded numbers for May, when they were due this month, must be vacations, but the spring/summer turnarounds should be knocking down production temporarily. The chart below shows how bonkers the industry went when oil went above $100 and are now paying for it. Basically any discoveries that were half way attractive got developed and are now coming on stream; and there are therefore none left now. Decommissioning costs are going to be 50 billion GBP – maybe more, but I don’t know if that would all show up on this chart – a lot is tax recovery. E&A (exploration and appraisal) numbers are trending towards zero. I think operating costs increased mainly because of inflation created by the development boom. Note the expenditure numbers are stacked.

The North Sea is said to be expensive, the most taxed production in the world. And there must be lots oil companies around the world that are trying to earn some of their capex back rather than making a profit at the moment. Such as Canada…

OilPrice.com – Insolvencies Jump In Canada’s Oil Country – By Irina Slav – Sep 04

Canada’s oil-producing regions saw the highest increase in insolvencies over the 12 months to June 2017, according to the latest insolvency report by the federal government. Total insolvencies in Alberta were up 11.6 percent over the 12-month period to June, with actual bankruptcies up by 4.5 percent to 5,346, and bankruptcy proposals up by 16.9 percent to 8,015.

In Saskatchewan, actual bankruptcies were up 5.5 percent to 1,504, and proposals were up 29.7 percent to 1,682. Total bankruptcies increased 17 percent, making the province the one with the highest increase in total insolvencies.

http://oilprice.com/Latest-Energy-News/World-News/Insolvencies-Jump-In-Canadas-Oil-Country.html

The Russian Federation collects production data very quickly, August numbers released today…

According to BofA Merrill Lynch, Russia still has some projects to complete (chart from January)

If they have 7% natural decline on mature fields and add 400 kbpd per year new production you’d get pretty much the 300 kbpd decline they show since last September.

Yes I was wondering if natural decline could account for it

Hi George

Saw this today.

http://www.bbc.com/news/uk-scotland-41122892

Not much of a surprise. The industry is winding down. There have been 10 to 15 major projects coming to completion so all the design teams (including purchasing, project controls etc.), then construction, then completions and installation, and then commissioning and start-up are finishing and have nothing else to go to. At the same time operations and logistics are declining as platforms are shutdown and decommissioned. Exploration drilling has almost completely stopped. None of that is going to reverse without major discoveries (in number and/or size). The next thing to go is likely the service and equipment supplier companies, which at the moment still have some overseas market.

Just a heads up that 7.xx ton to barrel conversion is one of those age old standards that need re-examination if the C&C ratio edges towards condensate. Hmm, I think it would understate the barrel count.

Yes that’s a good point. I only use the 7.33 barrels per ton conversion because its the one that the news agencies and others use.

According to JODI Data the conversion factor for the Russian Federation is 7.356 b/ton. And I guess JODI must know?

According to BPs Statistical Review the 7.33 conversion is based on worldwide average gravity. And so I guess thats why the press use it.

The last time that I saw the EIA post a list of conversion factors, back in 2008, they listed Russia as 7.27 b/ton.

The home of STACK and SCOOP, June figures and July rig count…

OKI GOR study – both April and May natural gas production revised up by over 100 MMcf/day. June numbers…

Mike

I know you got much greater concerns at the moment. However this is the latest update for the HRZ shale well Alaska.

The Icewine#2 well was shut-in on 10th July to allow for imbibition and pressure build up to occur within the HRZ shale. Flow testing re-commenced on 31st August at 10:26 (AK time), and is ongoing. Results since flow testing recommenced are summarised below.

The Icewine#2 well is located on the North Slope of Alaska (ADL 392301). 88 Energy Ltd (via its wholly owned subsidiary, Accumulate Energy Alaska, Inc) has a 77.55% working interest in the well. The well was stimulated in two stages over a gross 128 foot vertical interval in the HRZ shale formation, from 10,957-11,085ft TVD, using a slickwater treatment comprising 27,837 barrels of fluid and 1,034,838 pounds of proppant.

The well was initially flowed back on a 6/64 inch choke and was reduced to a 4/64 inch choke after 26 hours to maintain pressure. Approximately 370 barrels of frac fluid had been recovered as at 1730 on 3rd September (AK time) at an average rate of 100 barrels per day. Hydrocarbon indications have been minor and are associated only with the formation of gas hydrates in the choke manifold. Methanol injection has been initiated to prevent the surface manifold equipment from freezing thereby ensuring free flow of produced fluids through the choke.

Wellhead pressure built to ~3,500psi during shut-in and has dropped to 1,130psi since flowback commenced. Initial analysis of the pressure data from both the build-up and flowback indicates limited connection to the reservoir prior to the last 24 hours. At 0550 on the 2nd September (AK time) a small pressure build-up was observed, potentially indicating the first contribution to pressure from the reservoir itself. This is the first time that this has occurred since flow testing was initiated, including the previous testing period prior to shut-in. To date the cumulative amount of stimulation fluid produced from both testing periods is 4,802 barrels, 17.25% of fluids injected.

The current flowback procedure is early stage and the significance of an implied pressure contribution from the reservoir and formation of gas hydrates cannot yet be determined.

Petrobras says that their m/m decrease is due mainly to the scheduled stoppage of platform P-58, which operates in the Campos Basin

ANP – Natural gas production in Brazil hits record

(There is a typo on this page, it gives oil production as 2,263 kb/day a 13% decrease) http://www.anp.gov.br/wwwanp/noticias/anp-e-p/3995-producao-de-gas-natural-no-brasil-bate-novo-recorde

The typo only appears when you use Translate…

Já a produção de petróleo totalizou 2,623 milhões de barris por dia (bbl/d)

Oil production totaled 2.263 million barrels per day (bbl / d)

http://www.telegraph.co.uk/business/2017/09/04/big-oil-usurped-gas-little-decade-experts-warn/

BIG OIL TO BE USURPED BY GAS IN LITTLE MORE THAN A DECADE, EXPERTS WARN

I guess it’s not much use to anyone. Just some updated natural gas production figures, I had to divide US production by 4 to make it fit on the chart with the others.

Another view, Brazil is obviously not connected by pipeline to Henry Hub prices, but left it in anyway 🙂

Wood Mackenzie Upstream Russia

Russian oil production fell to 10.92 Mb/d in August due to regular maintenance.

https://twitter.com/WM_Russia

Brazil is managing to increase its net exports. Due both to an increase in production and a decrease in domestic demand caused by the recession. The increase in production and decrease in demand both started in 2014.

Brazilian Demand

HOUSTON, Sept 5 (Reuters) – ConocoPhillips said on Tuesday that oil output from the Eagle Ford shale region of Texas is near 80 percent of levels from before Tropical Storm Harvey.

The company pumped 130,000 barrels per day from the Eagle Ford before the storm. It said in a statement it expects to resume that production level within the next week or two.

https://www.reuters.com/article/us-storm-harvey-conocophillips/conocophillips-says-eagle-ford-shale-output-nears-pre-harvey-levels-idUSKCN1BG2TF

Coast Guard limits vessel traffic for Puerto Rico ahead of Irma

NuStar Energy L.P. has shut down operations at St. Eustatius oil terminal in Caribbean ahead of Hurricane Irma.

Tolls on Florida roadways will be suspended at 5 p.m. Tuesday because of Hurricane Irma @MiamiHerald

Irma cone: http://www.nhc.noaa.gov/refresh/graphics_at1+shtml/205803.shtml?cone#contents

“Significant improvements in the last six years

Overall, improvements over time are obvious, with current wells far surpassing those of only a few years ago. Continued improvements in completions techniques have allowed companies to drill increasingly effective wells, which has helped companies better endure the current price downturn.”

“2017 wells set new EUR records

Wells in 2017 have continued the trend of improving results, with this year’s wells already exceeding those of 2016. The best well drilled so far in 2017 is predicted to produce over 4.5 MMBOE, the best of any unconventional well in the Bakken so far. For reference, this is nearly three times the production of the best unconventional well in 2012, when 1.68 MMBOE was a record-setting result. ”

https://www.oilandgas360.com/meet-best-best-bakken/

same thing happening in Scoop and Stack… what the article fails to mention, while production numbers are as stated, drilling and completion cost are down by ~30%-50%. Hmmm what does one get when production goes up, drilling & completion cost go down and oil prices get back above $55…..profits coming to a oil company near you?

What is the worst well predicted to produce?

Mexico imports a lot of energy from USA: petroleum products, probably mostly from Houston area refineries, which have been falling; and natural gas, all from Texas, which has been rising. They’ve been a slightly net importer by value for just over two years, but were just about neutral in July. August and September numbers might be significantly different with Harvey impacts included. In the chart exports are positive.

Hi all,

A new post by Mr. Kaplan on the Gulf of Mexico is up at link below

http://peakoilbarrel.com/gom-june-production-update/

and also a new Open Thread Non- Petroleum at link below

http://peakoilbarrel.com/open-thread-non-petroleum-september-6-2017/