A Guest Post by George Kaplan

Short-term trends for UK oil and gas production and, to a lesser extent, Norway can be rendered a bit meaningless by seasonal impacts from summer maintenance turn-arounds and cyclic gas demand. Overall, though, both are at or approaching the tail end of the production curve, but with slight upticks in the nearer term. Barring several large and unlikely new discoveries over the coming years the industry will continue winding down in both countries, with the UK ahead of Norway, and exploration and development leading operations and finally decommissioning. However some Norwegian gas production still has a multi-decade plateau to come and there are a couple of large oil projects due on-line in each country which will run for twenty to thirty years.

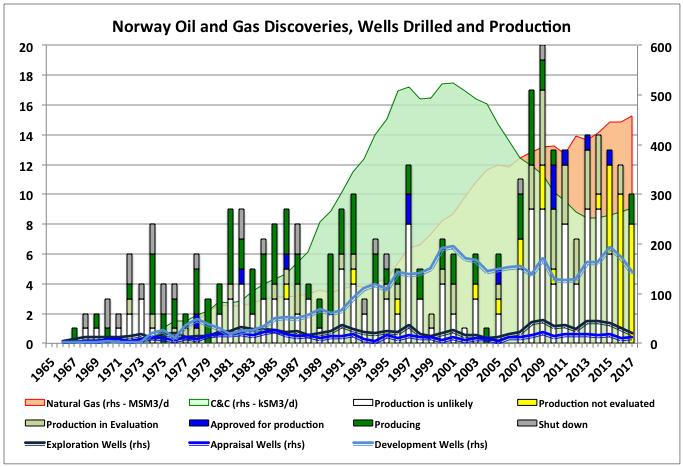

Norway Drilling and Discoveries

The usual patterns of exploration wells and discoveries following a bell curve that is matched by a later development curve (see below for the UK example and note that production is in cubic meters as it fits on a common axis better that way) is not seen so much in the Norwegian numbers. There are a number of reasons for this: 1) the wells and discoveries shown are for oil and gas and Norwegian gas development has been several years behind oil; 2) Norway really has three basins which have been explored somewhat sequentially – the North Sea, then the Norwegian Sea and then the Barents Sea; 3) the NPD includes as discoveries ‘hydrocarbon shows’ which will never be developed and skew the numbers, additionally in the chart the large number of ‘not evaluated’ finds in recent years will mostly become ‘unlikely to be developed’; 5) in the past Norwegian governments has made efforts to spread development of the resources through approval and leasing timing; 6) I think there are tax breaks in Norway that encourage exploration drilling even at low oil prices and low discovery rates; and 7) the chart shows numbers of discoveries rather than size, which would show a much clearer bell curve.

The success rate including the ‘hydrocarbon show’ discoveries has been around one in two to one in three, but for commercial discoveries it is more like one in ten to one in twelve (and likely to be lower in recent years once all discoveries have been evaluated). For 2017 there have been two small oil discoveries, drilled as outreach wells from platform drilling rigs, , there was one small gas discovery in the Barents Sea and the others are likely to be found non-commercial (including a couple of high profile wells in the Barents Sea).

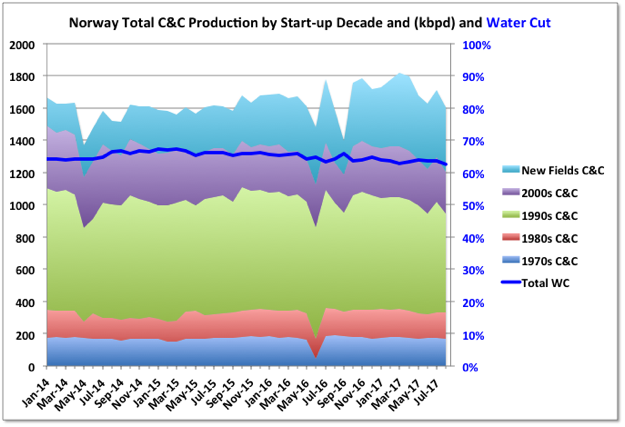

Norway Oil Production

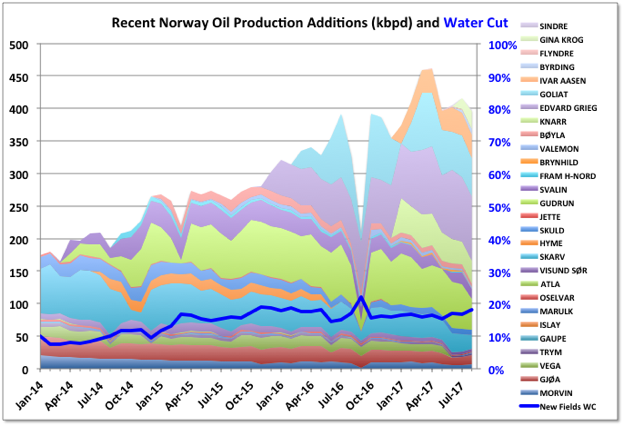

Norway NPD reports monthly production after about seven weeks, and I don’t think it gets revised, or very rarely. Norway oil production is on a short plateau with a secondary peak (after the main one in 2001) but likely to start a slight decline now. The old giant fields from the 70s and 80s are holding pretty steady, but surprisingly the biggest decline is coming from the newest fields, most of which are small. A lot of those fields were brought on line with fairly short development times from the high price years in 2011 to 2014. One of the new platforms, Goliat with 100 kbpd nameplate, is shut down at the time of writing because of safety concerns around its electrical system, but its numbers show in the August figures reported here. It is unknown when it will restart. It has also been discussed as something of a white elephant in the Norwegian parliament, because of its low reliability since start-up.

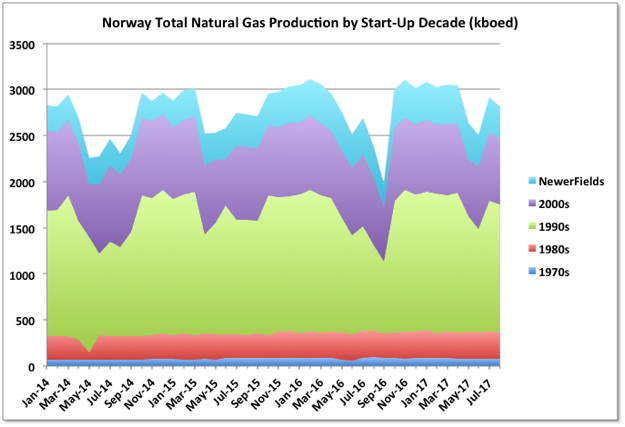

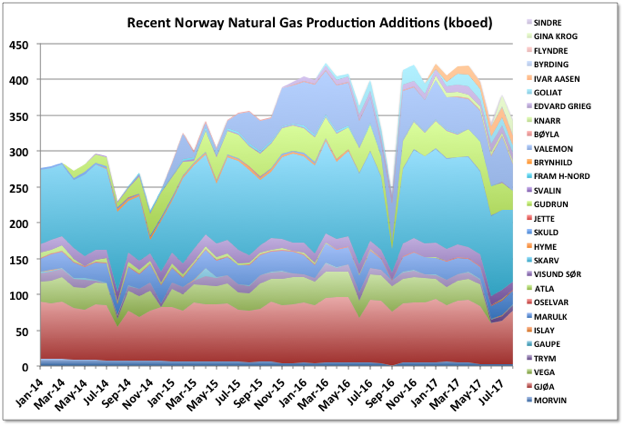

Norway Natural Gas Production

Gas in Norway has been developed about ten years behind the oil. It is currently around its peak level and likely to decline now, year-on-year – January 2016 might have been the peak month, but production is highly seasonal so that doesn’t mean much. As for oil there have been a few fields added over recent years and they look to be declining fairly quickly. The big producer is Troll which is on a multiyear plateau, though I think the Norwegian government has recently agreed to increase its production level, probably to compensate for other declines. Snøhvit is another big gas producer and is an LNG plant, which would have been designed for a long, steady plateau.

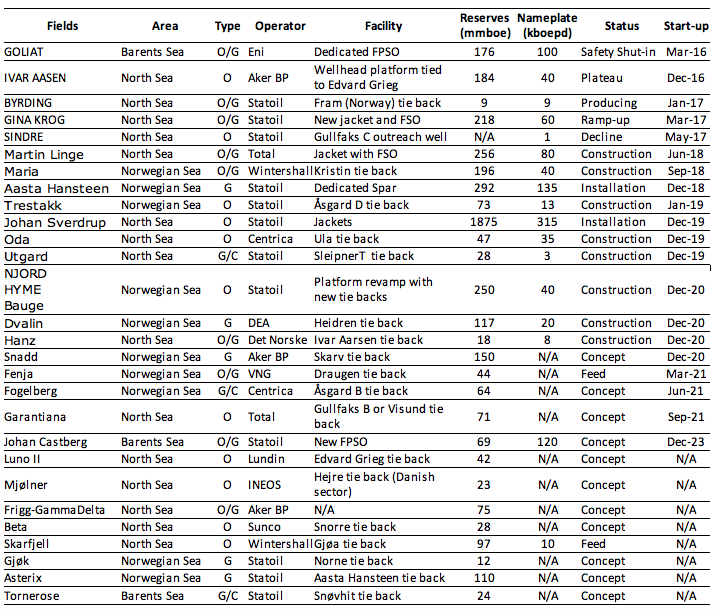

Norway Current Activity Summary

The table below shows recent start-ups and fields under active development or close to FID (termed “in clarification” by NPD). Fields that are, or have been, produced are shown in uppercase. Norwegian NPD tends to include smaller discoveries in with their main development field so there are actually more individual fields than it appears (compare with the UK, below, which keeps all the field names individually). There are other discoveries: 35 classified as “production likely but unclarified”; and 36 “production not evaluated”, most of which are likely to end up as “production unlikely” based on recent history (e.g. all the dry wells drilled in the Barents Sea this year, such as Korpfjell which Statoil declared as an uncommercial gas show, are included in this category). This year’s starts-ups have been Sindre, a small field produced immediately after discovery through an extended reach well from Gullfaks C, and Gine Krog, which is a fairly large ($3.7 billion investment), stand alone oil development.

The reserves data in the table below are taken from NPD and some of it wouldn’t count as a strict P50 number by SPE rules; the nameplate capacity is a bit more approximate, not least because it’s not always stated whether oil alone or total equivalent fluids is being considered; it has been taken from NPD or trade media descriptions (sorry for the bastardised units throughout this post).

There are a few larger developments due through 2020, but it is likely oil production will decline until the Johan Sverdrup start-up gets into swing. Gas production may peak this year, it’s a bit difficult to tell month-to-month because of the seasonality of the demand. Note that there is a second phase development for Johan Sverdrup, which is likely to go ahead soon and would markedly increase the nameplate capacity (maybe to 500 kbpd), but would not be on-line until around 2022 or so. At the moment the final big development will be Johan Castberg in the Barents Sea, which is likely to come on line in 2022 also, but by then overall decline is likely to have taken over again from the Johan Sverdrup bump.

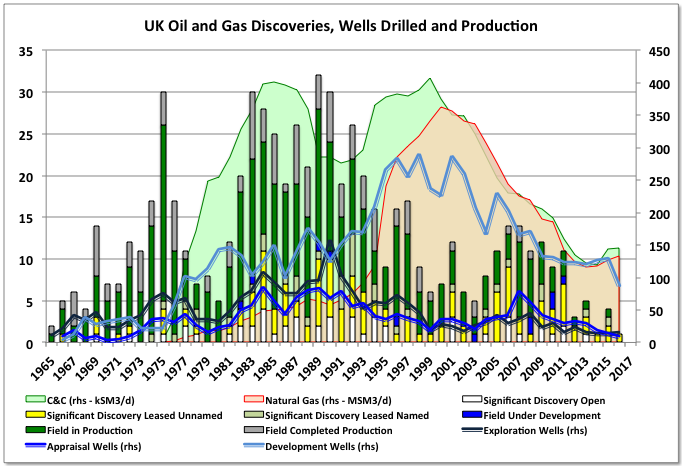

UK Drilling and Discoveries

The UK production for both oil and gas follow fairly good bell curves about ten years behind the equivalent exploration drilling and discovery curves. There’s been a small uptick recently which is likely to continue rising into 2018. The new production is mostly coming from older discoveries that were approved for development in the high price years, rather than an opening of a new exploration frontier. There’s a rising proportion of heavy oil in the new production (and the outstanding discoveries not yet being developed). Note that I think gas production before 1995 isn’t fully reported as there is no available data for dry gas before then.

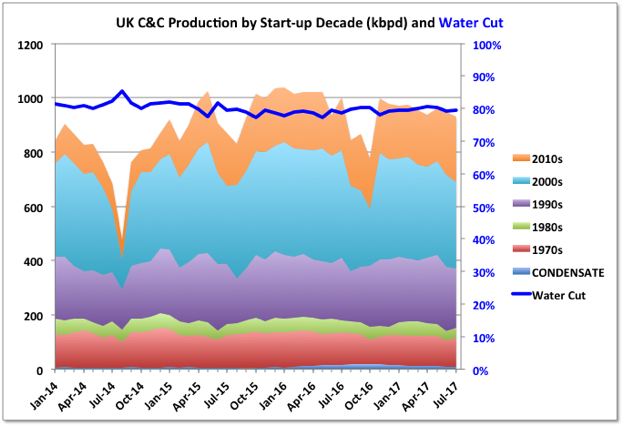

UK Oil Production

Month-to-month UK oil production has been gently falling recently after a local peak last year, but after this year’s maintenance period it’s likely to start increasing through 2018 as new developments are brought on line and ramped up.

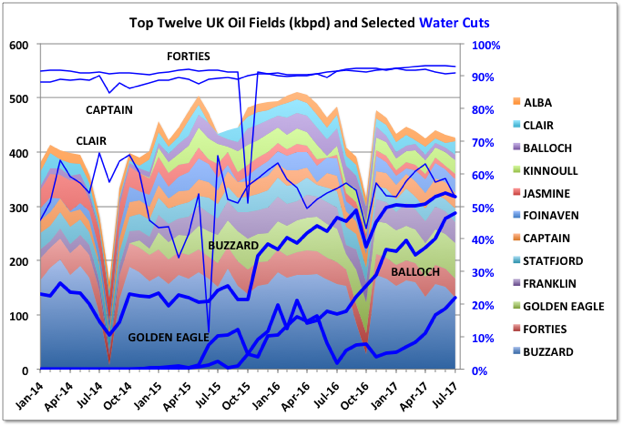

The overall rate of increase and final peak (a local peak, still well below the 1999 maximum) depend on how fast the decline in some of the existing, larger producers, especially Buzzard and Golden Eagle, sets in. That in turn depends a lot on water break through. Buzzard is showing clear signs of decline as the water cut increases above 50%. Nexen, the operators of Buzzard, have announced an FID for a phase II of Buzzard development, a four well tie back, is likely next year with first production in late 2020. That could indicate they expect rapid decline to set in now, but also that there is still some reasonable oil reserves left (Buzzard has so far done much better than originally expected).

Golden Eagle and Balloch also have rapid water breakthrough this year. I haven’t shown all the other fields. The older water flood fields, Alba, Forties, Captain and Statfjord, have water cuts above 90% and it’s just a question of when they become uneconomic and get shut down, though Captain has some EOR planned to extend it’s life (I think polymer flood). Statfjord field straddles the UK/Norway border so some production is booked to the UK (Flyndre and Utgard, two recent developments, are similar). Clair field production will increase significantly when the Clair Ridge project ramps up next year. Jasmine and Franklin are really gas-condensate fields, although their production is reported as oil and associated gas, and have sustainably low water cuts.

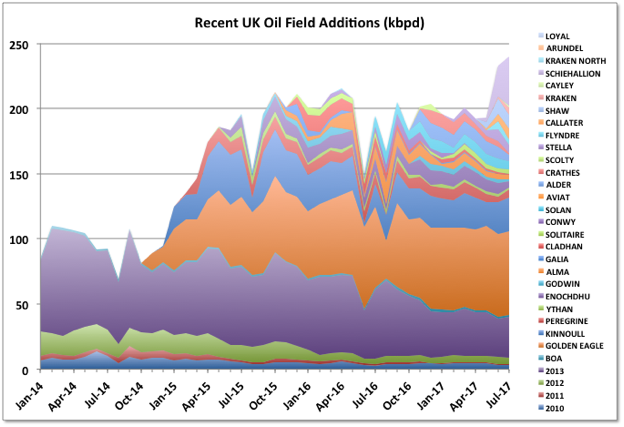

2010 to 2013 was a fairly slow period for new oil before Golden Eagle and Kinnoull. The projects that were brought on are fairly short-lived (overall they show about 26% decline rate since 2014, with no sign of amelioration). There were a series of small projects in 2014 and 2015, and some of the more recent additions have proved really short lived and have died after less than two years, I don’t know it f there are plans in place to get them going again, but now the larger projects approved in the high price years are coming on line. Cayley and Shaw are part of the Montrose Area redevelopment and started up in May. They are currently at about 12 kbpd combined, but the project has nameplate of 40 kbpd so should see ramp up over the next year. Kraken is heavy oil and having a difficult start-up. The big jump, which will continue, is from the Glen Lyon FPSO, which is a redevelopment of the Schiehallion area and includes the Loyal field. See below for more details on these fields and ones due shortly.

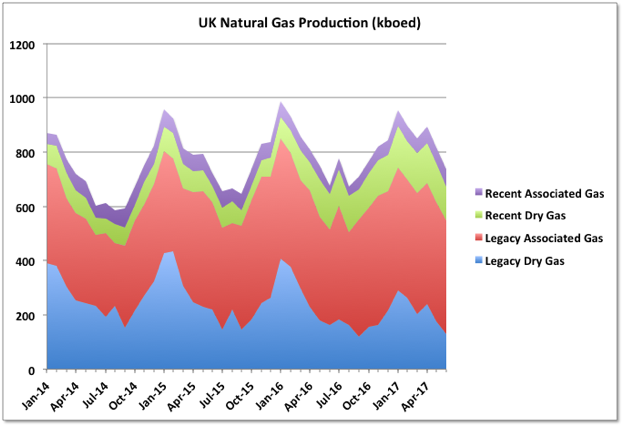

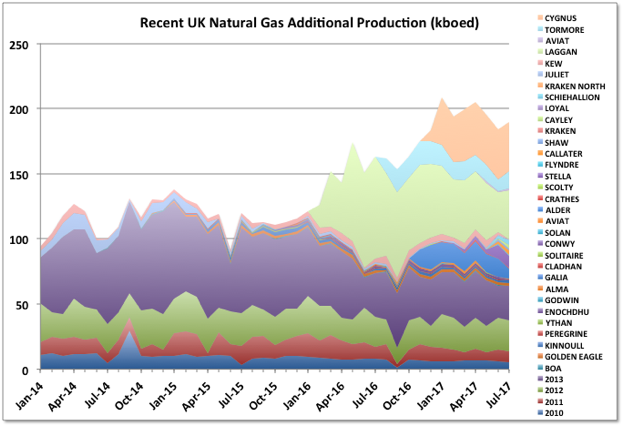

UK Natural Gas Production

For the UK the North Sea has produced more equivalent barrels of gas and condensate than oil, and still does. Gas production is highly seasonal but generally now showing a decline, in particular from the older dry gas fields. This is probably going to accelerate now, but may be ameliorated for a couple of years by the associated gas from the new oil fields and the Culzean project currently in development.

The Laggan-Tormore Project is the largest recent addition for local gas supplies. It was advertised as supplying 5% of the UK needs, which it did – for nine months and is now in decline. I’m not sure if there are other wells due there that will boost supply again, if not it looks like the reserves might be less than expected (the development was well over budget, so they would have been hoping for something better). Cygnus, discovered in 1988, is another relatively large field. It too was advertised as supplying 5% of UK gas needs, but it is being developed in phases and has not hit that mark yet. The only major gas development in the works is for Culzean, due in 2019. There is likely to be continued decline in the medium to longer term. With Ormen Lange, which exclusively supplies the UK from Norway, also in decline let’s hope there’s enough LNG for sale, otherwise the UK is going to be looking for any fuel it can find and never mind the consequences. In July the big seasonal storage field at Rough was closed, so LNG will also become more important as a long term emergency back-up fuel in the future.

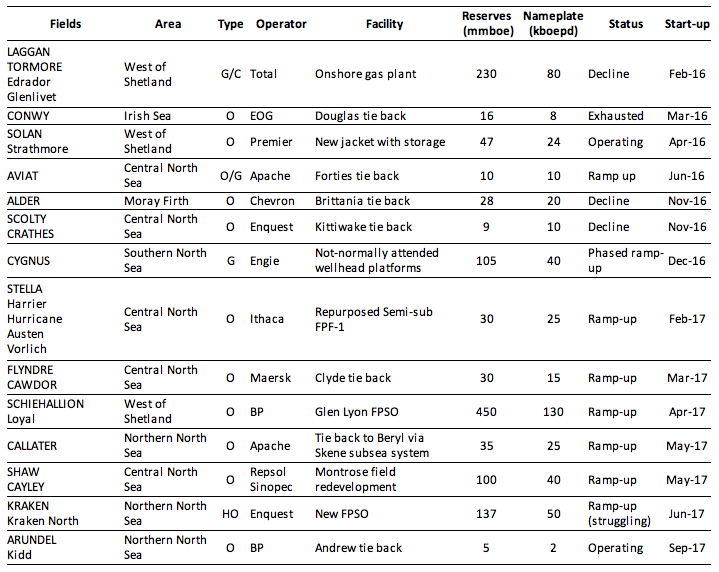

UK Current Activity Summary

The table below shows recent and approaching start-ups. The troubled WIDP development was installed and is now being hooked up to the Harris and Barra field subsea wells. It is three years late (assuming it does get started soon) and might actually lose money without a big bump in oil prices and/or some successful near field discoveries. The Greater Catcher development should start up in December. The FPSO is now on station. It will eventually service three fields: Catcher, Burgman and Varadero. Arundel is a small tie back to Andrew for BP, which started in September, and the Cawdor field, a small tie-back as part of the Flyndre development, also started up recently.

Other projects in development are Clair Ridge, to be installed this year and likely to be a big producer but on a part of an already producing reservoir (hence not in the table); Mariner, which is a heavy oil project for Statoil; and Culzean.

Culzean was initiated by Maersk but presumably will now be taken over by Total. After 2019 new oil coming on line will be very sparse and rapid decline is likely to take over. Note that the caveats for nameplate and reserve capacity given above for the Norway fields also apply here – more so for the reserves as the UK Oil and Gas Authority doesn’t supply their own estimates so the numbers are taken from trade media reports and company investor presentations.

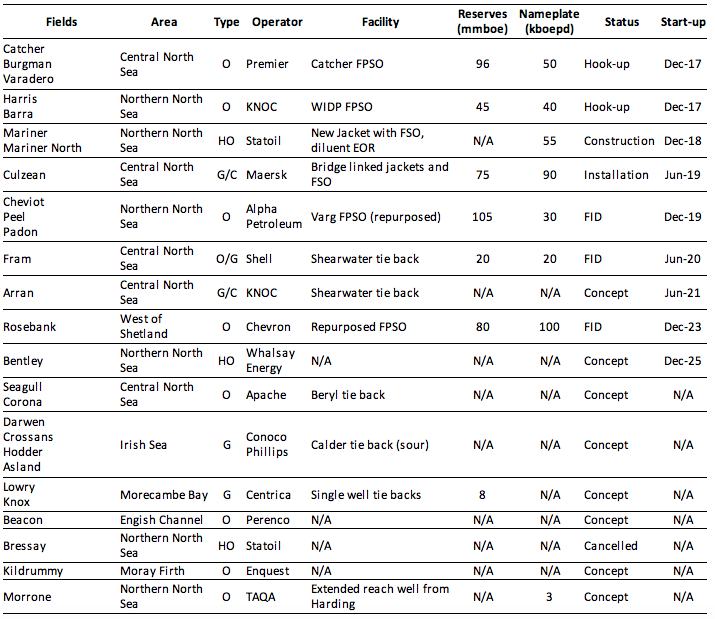

The second table shows significant discoveries that are likely to be developed. Fram is a gas field with a thin oil or condensate rim, which has been around a long time. At one time it was planned as a stand-alone FPSO development, but now, following some poor results from reservoir analyses, Shell are planning on a twenty mile tie back to Shearwater. The production rate and eventual recovery will be lower than the original proposition. After Fram Chevron’s Rosebank might be the only largish stand-alone project left to be developed. It too has been around for a number of years without yet finding a commercial development option, although I think they are trying again at the moment, possibly with a leased, refurbished FPSO. There are some smaller undeveloped fields, often for heavy oil, that could see platforms rather than tiebacks and the result of the pilot project for the Hurricane basement rock reservoirs may lead to bigger things as well. There are a couple of fields that might be redeveloped but most undeveloped SDs (significant discoveries) will be small tiebacks and a lot might end up stranded and non-commercial. There are few to none other discoveries that might be developed other than those above. There is still some exploration drilling but it has been fairly disappointing so far (only one significant discovery, by Statoil, and that not necessarily big enough to be commercial unless there is an available tie back opportunity). There are still a couple of high impact wells to be drilled in the West of Shetland area this year. In October there were six operating offshore rigs for the UK, the lowest in Baker-Hughes records.

Off Topic Finish

The Spanish Civil War is still redolent, partly because of the romance of artists going off to fight fascism (and often not coming back), plus local deaths like Lorca’s and the literature that these influenced (even The Prime of Miss Jean Brodie). It was also a war of posters, which were highly artistic (they had a few movements to draw on: Cubism, Suprematism, Art Deco, Surrealism, Futurism) as well as politically direct, and produced by both sides, though mostly the Republicans. With current events in Catalan these may still be relevant. I guess Instagram and Twitter would replace the posters, though they seem to me to be facile and “meta” and probably full of fake news, but then so were the posters, but done in a way that is somehow more acceptable (but maybe just because of the passage of time).

The posters came in various languages: Spanish, Catalan, Esperanto and the one below, showing a child killed in fighting in Madrid, is in English. It’s been used a few times since, with appropriate modifications, in stories covering different wars, e.g. for mocked up newspaper front pages, also the inspiration for a clever, and these days highly apposite, song by the Manic Street Preachers, though I’ve been told I’m too old to be allowed to appreciate them.

130 responses to “Norway and UK Production Update”

Seasonal drop in Chinese crude oil imports and a big increase in import quotas for 2018

Reuters 2017-11-08 China’s October oil imports fell sharply from a near record-high of about 9 million barrels per day (bpd) in September to just 7.3 million bpd

“Lower imports reflected less purchases from independent refineries as many of them are running out of crude quotas for this year,” said Li Yan, oil analyst with Zibo Longzhong Information Group.

For next year, however, independent refiners are likely to boost their imports again as authorities on Wednesday raised the 2018 crude oil import quota by 55 percent over 2017 to 2.85 million bpd.

https://www.reuters.com/article/us-global-oil/oil-dips-on-lower-china-crude-imports-but-market-well-supported-overall-idUSKBN1D805

Crude imports, seasonal chart: https://pbs.twimg.com/media/DOGwA0aX0AIoVfN.jpg

China imports, Saxo Bank: https://pbs.twimg.com/media/DOF2iacW4AAAw-4.jpg

BEIJING, Nov 8 (Reuters) – China has raised its 2018 crude oil import quota for “non-state trade,” generally meaning independent refiners, by 55 percent over 2017, raising the clout of the independents in the global market after a setback this year.

https://uk.reuters.com/article/china-oil-imports/update-2-china-sets-2018-non-state-crude-oil-import-quota-55-pct-higher-than-2017-idUKL3N1NE1IG

OPEC World Oil Outlook 2017 (just released):

https://woo.opec.org

Thank you George. IEA will release their WEO next week (14th).

From the OPEC-report:

“Total non-OPEC liquids supply is now forecast to grow from 57 mb/d in 2016 to 62 mb/d in 2022, with the US alone making up 75% of that increase.”

The section on decline rates was interesting too (p.184):

“the WOO analysis suggests an average implied decline rate of around

4.4 mb/d in the 2018–2028 period, or 7%, of underlying non-OPEC supply. Note that this

compares with previous, more in-depth, work done by the Secretariat, which indicated

that underlying observed decline rates in non-OPEC were lower – on average around

5.4% – though with significant regional variations.

On the one hand, this analysis shows the challenge facing the upstream sector, with

a requirement for more than 5 mb/d p.a. of new supply, if annual average demand growth

of 0.9 mb/d in the Reference Case is added to the implied 4.4 mb/d ‘lost’ due to natural

decline. On the other hand, the calculated implied decline rates and substantial new

upstream volumes coming online suggest that overall upstream investment activity is

perhaps higher than a quick glance at headline capex numbers would suggest…”

“with tight oil making up a substantial and growing share of total non-OPEC

supply (around 12% in 2016), and given its innate rapid decline rates after initial production,

this may in a sense have accelerated the underlying decline. In other words, the system

can said to be coping, with supply growth meeting demand needs at the moment”

“that overall upstream investment activity is perhaps higher than a quick glance at headline capex numbers would suggest …” Nope it would suggest that the developments coming on line now follow a normal project S-curve with the big investment costs in the middle then slowing down during installation and commissioning. There aren’t many projects in the middle of the development so costs are down but the new production coming on line is still fairly high (until the second half of next year). The investment problem isn’t going to show up really until a couple of years out, but it can’t be halted by anything that’s done now, just like the over-investment impact kept running even as oil prices crashed.

With all the kerfuffle in Saudi whatever happened to the independent assessments of their reserves? There was a leaked report that said everything was exactly as the Saudi had ben reporting, which couldn’t possibly have credibility as it came out about a week after the consultants had started work so they wouldn’t even have got their computers working properly yet, and then something about the reports being released early next year – and since then nothing.

Deleted

Hi George,

Nice post.

On the oil and gas discoveries charts, what are the units for the left hand vertical axis, is it number of discoveries? Is it possible to show this as barrels (or Mb where M is mega or million) rather than number of discoveries (assuming my assumption that this is not the case is correct). It may be that the oil and gas is thrown together as boe so this may not be possible.

It’s just a number of discoveries. Norway has reserve data by field, which I’ve posted in a previous thread I think (if not I’ll show for next update), UK doesn’t. They both have totals of remaining oil and gas reserve by year and I’ve posted those before.

Here: http://peakoilbarrel.com/norway-oil-and-gas-reserves-production-and-future-projection/

But I guess I could split reserves into the same categories as above and show by year rather than cumulative.

I think Dennis may be interested in oil in place volumes for the “Production is unlikely” fields. At least I am. There are quite a lot of them. I had a quick look in the npd page and could not find that information though.

Oil and gas are separated for each year, but the categories are stacked for each type. There are no numbers for the “production is unlikely” fields, from the few I’ve looked at they are usually categorized as “hydrocarbon show” and non-commercial by the E&Ps – i.e. they have no resources by most criteria.

Ok thanks. Technically recoverable resources are probably very low for those fields then.

Hi George,

How many oil reserves have been discovered by Norway (included in NPD numbers) since 1993. It looks like cumulative reserves plus cumulative production has increased by approximately 5 Gb from 1993 to 2017 (based on chart below from your earlier post).

If we had cumulative discoveries over that period we could estimate reserve growth to see if it is zero. We may not expect this to be the case as Norway does not use SPE guidelines for reserves (I think that is what you said.)

All reserve changes are backdated against the discovery date so I don’t think you can do that unless you have the history of reserve estimates, and I don’t think you get that from NPD (only BOEM that I have found, unless you save the data yourself each year). For example in theory last year every field could have been considered exhausted, and then suddenly a load of growth applied to them all – and the curve would look exactly like the one above (where that definitely didn’t happen).

There certainly was growth in the old giant fields like Statfjord and Gullfaks through the 80s and 90s because the recovery ratio was improved markedly, I think a lot of the technical improvements that allowed that, like improved reservoir modelling, precise horizontal drilling, partly came out of Norway.

Try this for more recent growth:

http://www.npd.no/en/Publications/Reports/Evaluation-of-reserve-growth-for-oil-/

Looks like about 2.5Gb (be about 7%) growth recently on older fields, but going flat at the end, so maybe not much more to come.

I should caution that the results for Norway won’t be applicable to deep water, or necessarily anywhere else – the old fields there all have their own drilling rigs and can keep drilling wells at relatively low cost by reusing well slots or working over existing ones. Deep sea tend to be wet trees in subsea completions which are more limited, and need to contract (still) expensive DP rigs for new drilling.

By the way since it’s revamp BOEM is now the best site ahead of NPD; the UKOGA has also relaunched and it’s pretty good, I think especially if you are a prospective lease operator.

Also looking through that report, much of the gain was from Troll which is fairly unique with a large but thin oil rim, only a few meters thick, that was drilled with precise long reach horizontal wells, that I’m guessing was the bigger unknown in the original reserve estimates.

Also I don’t know how the NPD reserve estimates compare with a typical proven or proven-plus-probable estimate in other authorities, they may be more conservative and therefore have more upside potential, or they may not.

Thanks for the info.

I am a little confused by how the NPD defines “reserve growth”, especially “total reserve growth” in figure 10 of the report you linked (last chart in the report).

Does it seem that they are including “new discoveries” as a part of “total reserve growth”?

Yes – I’d say that includes any additions, so new or existing discoveries that are approved for production plus any brownfield work that increases reserves on producing fields.

Looks a bit optimistic to me, I think about 50% to 75% of their projected “reserve growth” looks more reasonable.

No doubt your estimate would be lower maybe 25% to 50% of the NPD projection for 2014-2023 ?

A lot of that growth would have been Barents Sea, which looks like it might be a complete dud – maybe two more wells to find out for sure.

Hi George,

Thanks. Maybe 0 to 25% of the NPD projection of 6 Gb cumulative discovery (new discovery plus reserve growth) from 2013 to 2023 would be your guess?

That is 0 Gb to 1.5 Gb over the 2013 to 2023 period.

More than that I think, but I’ll wait for the next couple of exploration wells. So far since 2013 there have been 200 mmbbls C&C discoveries (less gas) but only a small part of that has been approved for production. There has been some older discoveries approved – I think Johan Sverdrup approval might be in that window, so that would exceed 1.5mmbbls already and with Johan Castberg to come.

Dennis – these are what have been approved 2013 to 2017: quite a few, but Johan Sverdrop dominates with about 75% of the total reserves, which are 2.35 Gb C&C, and 720 Gboe gas and NGL, and noticeably tailing off in size since the price collapse.

BYRDING

DVALIN

FLYNDRE

FRAM H-NORD

GINA KROG

HANZ

IVAR AASEN

JOHAN SVERDRUP

MARIA

ODA

TRESTAKK

TROLL BRENT B

UTGARD

AASTA HANSTEEN

Hi George,

Thanks.

So 39% of the 2013 projected “reserve growth” has occurred through 2017 (2.35 of 6 Gb), so my initial guess that maybe 50% to 75% of the 2013 projection might be achieved (3 to 4.5 GB) by 2023 may be pretty good. Though I admit this was just a lucky guess on my part as I did not realize approvals from 2013-2017 were so large.

I realize now that when you said “we will see” earlier that perhaps you thought 25% to 50% was too low. I mistakenly assumed you thought that estimate was too high.

If oil prices rise to $70/b or higher perhaps they will hit the target of 6 Gb as contingent resources may become viable.

I don’t know enough about the details to make a good judgement.

I suppose 2.5 to 6 Gb is one potential WAG.

Many years ago, my mother showed me an old black and white photograph of her first cousin, a 19 year old who had been raped and murdered by communist forces associated with “La Pasionaria”, a communist who showed up in several towns in Cataluña during the Spanish Civil war. La Pasionaria used to go around with a coupled of Soviet commissars, and has been identified as person who gave orders to murder hundreds of persons in Barcelona. Many years later she was acclaimed by the socialists and cheered as she entered parliament after Franco’s death. That cheering drove my mother nuts, she thought it was a gross injustice that such a murderess would be cheered by anybody in public. I noticed quite a bit of misinformation going on in the English language media, especially the left leaning types who are tied to ERC, CUP, and other red separatist parties. As they like to say in the USA, today we see a lot of fake news, disinformation, and so on. I’m going to be out of touch for a while, so I’m not going to be able to comment more on this matter. I did put a single post in my blog about what’s going on.

Catalonians got screwed by both the Soviets, and of course, Franco the Butcher.

Read Orwell’s Homage To Catalonia for a primary perspective from someone there at the time.

(Orwell’s most repressed book)

https://www.youtube.com/watch?v=VWXYsi3zoCQ

Guernica is probably the best, and most influential painting of the 20th Century, showing the atrocities of the

Fascists.

(The painting was created in response to the bombing of Guernica, a Basque Country village in northern Spain, by Nazi Germany and Fascist Italian warplanes at the request of the Spanish Nationalists.)

Franco used mainly North African Mercenaries for his bloody assault on the Republic.

I live in Spain. My great grandparents were from La Rioja, Cataluña, and Galicia. But one ancestor part Dutch part Chinese, born in Indonesia. In general my family is hard core capitalist, although one granduncle was a senior communist party member. The international left is focused on undermining the European Union, in this they are aligned with the ultra nationalist right. There’s also reports in the media that Russian cyberwarriors have increased their pro separatist propaganda on the Internet. So it seems separatism is a hybrid, pushed by discrete groups from the hard right, to corrupt politicians who want to avoid being prosecuted, to leftists, including hard core communists, all of this aided by the Russians.

From someone who left Cuba, after a Right Wing Dictator was overthrown, and chose Fascist Spain, under Franco, as his country of choice.

I value your insight into oil , but your politics are quite questionable.

Your Russian stories need a bit more complexity.

(I have a degree in Russian History)

Most of my comrades joined the Vermos to help with the sugar cane harvest in the 1960’s.

Fernando

I have read many of your comments on various sites over the years and always benefited from your insights.

Reading of the Red Terror by the Bolsheviks, the Spanish Red Terror, alongside recounting of Chiang’s takeover of Taiwan, the aftermath of Sukarno’s overthrow, might all offer a horrific – yet seemingly common – view of both human nature and repetitive cycles in history.

Best wishes to you on your hiatus.

Yeah, Spain is one country I would love to visit. With my limited Spanish, I could, at least, get them to laugh at me. My wife is from Belarus, so we have visited a few Russian speaking countries, and the people have always been friendly, and I would love to go again. But, Damn, we both love Texas.

U.S. Petroleum Balance Sheet, Week Ending 11/3/2017

Saxo Banks chart summary: https://pbs.twimg.com/media/DOHugA7X0AE-kzV.jpg

EIA pdf: http://ir.eia.gov/wpsr/overview.pdf

EIA weekly change in ending stocks (crude+products).

Overall stocks down 0.56%, pretty much inline with recent trends, crude up 2.2 mmbbls, gasoline down 3.3 and distillate down 3.4. But the only number that matters to the traders is the crude and because it is up price falls and it’s reported we must be back in a glut. Bonkers.

I think we are in refinery maintenance season now, so crude stocks should increase normally. Interesting to note is that gasoline and distillate stocks are back to normal levels. So they will have to draw a lot more from crude stocks going forward.

Same principle drives lemmings, I think. They have to be over the cliff, before they will recognize it is there.

An insult to lemmings:

“The misconception of lemming “mass suicide” is long-standing and has been popularized by a number of factors”

https://en.wikipedia.org/wiki/Lemming

It probably is a gross insult to lemmings. However, the article referenced does not deny they jump off cliffs and drown, it just says they do not “commit suicide”. They are trying to migrate. Migrate in an insane manner, but they are dying while migrating. They are not committing suicide. Probably smarter than the authors of the article referenced, so I apologize to the lemmings.

Dept of unnecessary trivia: it appears movie makers faked the cliff scene. There appears to be no evidence that lemmings ever jump off cliffs, or in fact do stuff that one might consider unnecessarily risky. Apparently they do swim rivers as part of their migration, and a few of their group drown on the way, but…no cliffs.

“ A Canadian Broadcasting Corporation documentary, Cruel Camera, found the lemmings used for the 1958 Disney film White Wilderness were flown from Hudson Bay to Calgary, Alberta, Canada, where they did not jump off the cliff, but were in fact forced off the cliff by the camera crew”

That’s enough to make Micky kneel when Disney plays their music preceeding their films. Fellow rodent.

https://oilprice.com/Energy/Energy-General/The-US-Export-Boom-Goes-Beyond-Crude.html

Yeah, George, this is what the were missing in the huge oil inventory increase they were crying about.

However, the more I think about it, it looks like US finished supplies may run short , long before they balance crude supplies. They ran at 89% last week, and it still dropped like a rock. What’s gonna be the story in June 2018?

That article pegs ethane export out of Marcus Hook at 35,000bpd, which I believe is incorrect (the EIA is the source, so I’ll do some deeper checking).

The smallest liquid ethane carriers – so called Dragon ships – hold about 175,000 barrels.

Newer, bigger ones are above 500,000 barrels.

Mariner East ships 70,000 bbld to Marcus Hook – propane and ethane in batches.

My understanding is that MH has 4 berths, but I do not know how the piping is set up.

When the much delayed Mariner East 2 and 2X are operational, shipments could exceed 6/7 hundred thousand barrels per day.

For context, Antero is now US’ biggest NGL producer at over 100,000 bbld. Yet it STILL rejects 125,000 barrels per day ethane into the pipelines.

CNBC is claiming the US set a “record” with regard to oil production last week.

Hi Shallow sand,

As I am sure you know the record was Nov 1970 at 10,044 kb/d for the monthly average US C+C output.

This past week was 9620 kb/d, over 400 kb/d below the record. (This weekly data is probably too high by at least 300 kb/d and perhaps as much as 600 kb/d.)

If they are talking about C+C+NGL, we don’t have data going back to 1970, but maybe they are talking about C+C+NGL which might be higher than Nov 1970, no NGL data so it would be a claim that is hard to refute with data.

Not a record for crude plus condensate. Also not a record for products supplied that was 21,666 kb/d in August 2005, last week was 21,301 kb/d.

Dennis. Yes. Just pointing out another dubious MSM story.

Hey shallow sand,

WTI is looking pretty good, here’s to $65/b soon!

Despite impressions to the contrary, I do hope all you oil guys do well.

I expect prices will tend to be high from now until 2030 so it will be good for the nest egg, or for selling your property at retirement time.

I likewise wish all the regulars here, and all the hands on people in the oild industry, well. And there’s every reason in my own personal opinion to believe that times will be good for them for another ten or twenty years at least.

But I wouldn’t advise a child of my own to make a career out of oil. There’s no stopping depletion. It can’t even be fought to a draw like the sea, one voyage at a time.

Somebody somewhere must have compiled a list of oil towns and communities in the USA that went broke when the oil ran out, locally. I’m hoping to discover it someday and put it in my book. It’s probably a pretty long list.

A lot of people think otherwise, but I’m dead sure there will be a market for oil even at two hundred dollars a barrel, in present day money, for at least another twenty or thirty years. It would be much smaller market, but it would still be there, because it’s not likely imo that we can electrify all the industries that depend on oil any quicker……… if we can do it at all in some industries.

After a century plus of constant improvement, we don’t have internal combustion engines five times as good as we did a century ago. There’s no guarantee we will ever have batteries five or more times as good as the ones we have now.

OFM. When our field came in during the first decade of the 1900s, a stop on the railroad grew to over 10,000 people, many living in tents. A post office, bank, hotel and 13 saloons were built.

Current poplulation is 100. Just houses, no businesses. But hundreds of oil wells still pumping in all directions, to this day.

Is this stripper business, or still active development?

I can’t imagine hundreds of wells in maintainance without a local support industry: repairing shops, truck yards for all the special vehicles, a burger shop for the wait times and so on – business around oil. Mainly maintaince, but you can’t order always a worker from hundred miles away to fix broken pumps, electric, mechanics, pipes, valves, have transport trucks (or is it all pipelined?).

Oil business is not my speciality, but when I was in the USA in the oil provinces there was lots of business around oil. Lots of installations means lots of people having to do with them normally.

I was just referring to a boom town in the middle of the field.

There are roughly 25,000 people that live within a half hour of the field. Two supply stores. Lots of service companies. Proabably 100 or so directly employed. Most are not employed directly re upstream, but many others who have jobs related to ff.

we don’t have internal combustion engines five times as good as we did a century ago.

I’d bet that automotive ICE’s last 10x as long now as they did a century ago. I’d bet that they cost 10% as much per horsepower.

Ford Model T used about 11-18 (13–21 mpg) liters to creep 100 km. Maximum speed 60 km/h – realistic it will have been 30-40.

With a weight of 540 KG, you could build a thing like this going on less than 2 liters with no problems, when this little maximum speed is necessary.

The next battery generation is at the doors – Toyota and Dyson are touting about it. It won’t be the last generation.

Dennis. Thanks.

We don’t know what the future will bring, but I’m just hoping for $55-65 WTI for awhile. Gasoline here is $2.51 per gallon, which I don’t think is hurting consumers all that much.

I don’t think you are wishing anyone ill. Actually, I think most would not think poorly of operations like ours or Mike’s.

There is no debate that some petroleum will need to be produced in the future, even by the most ardent of those anti oil.

Operations like ours are producing high quality crude from mostly pre-existing wells, with new ones added in small quantities only when economics merit. The typical land taken up by a well we operate is about 12’ x 20’. A typical tank battery takes up 30’ x 25’ x 3.5’ high.

A high percentage of royalty owners in our field are retired. For example, one lease we operate is located on 40 acres. It is owned by a widow who lives on it. The lease produces right around 1,000 BO per year. The cumulative production is over 50,000 BO since the early 1980s.

The landowner receives 1/8 of the oil sold, free of all expemses except taxes. Even at $40 oil, $5,000 per year gross.

I am sure there are many examples like mine.

I would go with your “perhaps as much as 600 kbd” amount. Probably more now, as completions are dropping, Within 200k barrels is an acceptable “who knows”.

I think the August monthly estimate is about 200 kb/d too high and the most recent weekly estimate is between 400 and 600 kb/d too high.

Generally the weekly estimates are very inaccurate, smart people ignore them except maybe to take advantage of the ignorant.

I think the spread may now be over 600 too high, since I am pretty sure Texas has been declining even more since August. But that guess will not be able to have real substantiation until Oct numbers are posted on the RRC site sometime next month after the 17th. September won’t tell us squat because of Harvey. August completions were low, at about 401. September was lower at 318, and October hit a new low at 257. Unless, it is much higher, in that case miracles are happening, and I need to keep out of projections on trends, as God has truly taken over.

These decreases in well completion numbers are easily predictable, and as such do not constitute new information which should alter production forecasts.

Over the past two years, lateral lengths have have seen a dramatic increase, particularly in the Permian Basin, where they had for a long time lagged increases nationally. Nowadays, everyone seems to be targeting a lateral length of 2 miles minus setback requirements. Sand utilization seems to be stabilizing at around 1800#-2000#/linear foot, after a decade of rapid increase.

Common sense tells us that, barring a dramatic increase in completion employment relative to historic trends, which we haven’t seen, or a dramatic in the labor efficiency of, say, truck driving, which we also haven’t seen, the number of wells completed will vary inversely with the effort expended on each individual well. And we’ve seen a massive increase in the completion efforts directed at each individual well, so of course the number of wells completed has dropped dramatically as well.

Well completion numbers have dropped dramatically, and

production per well has dramatically risen, but overall production hasn’t been much affected.

So long as we stay in approximately the $50-$80/barrel range, and barring significant resource exhaustion which seems unlikely in the near future, we’re still on track for around 10%/year unconventional production increases which closely track reasonable fracking activity indices and in general poorly track the 2-month lagged rig count which so far as I can see the EIA seems to use as the basis for all their black-box forecasts of undisclosed methodology.

They’ve been the same length for a while, and I’m the past few months the numbers have dropped by half. Logic would tell you production will drop. You only have to peruse the numbers for last year to see how quickly it can drop.

If you take the number of rigs (wells) and wait two or four months to multiply estimated production per well, you still are not going to come any where close to what production is. It’s a dumb way of doing it, at this time. EIA could revise their reporting to include completions, and come up with a much more reasonable estimation using completions instead of rig counts. When the Eagle Ford was first gearing up in 2013, there was a nine month lag for completions. That’s when they had unlimited funds to gear up to get to a higher level. Now, we are back in the same situation which has additional factors, like bantering over price, and decisions to hold off on completion. EIA does not factor in reality, at times.

Hi Guym,

Often the output numbers don’t sync with the completion numbers, not sure why, maybe late reporting, who knows, also it will depend where the completions were and the output of those completed wells.

I agree it will be the output numbers that tell the story, and those don’t tell us a lot because we have to guess at how “complete” the data is.

The truth is we won’t know what Texas output for Oct 2017 truly is until June 2019 when the RRC data becomes relatively complete. It is pretty frustrating because in North Dakota we will know the output level about 18 months sooner.

The fact that Texas has the most wells and has been doing this longer than anyone (except perhaps Pennsylvania) should be a reason that they are the best at getting accurate data out.

If I were a Texan, I would be embarrassed at how poor a job the RRC does.

I’m not embarrassed. You have a corn up your rear about RRC, I have one for EIA. There are 316k active producing oil and gas wells. There are 60k operators registered in Texas, which is a bigger problem than the number of wells. Problems are bigger in Texas.

And countless times I have agreed with the same thing. Actual is not going to be recorded for months. So what.

By comparison North Dakota has under 14k producing wells with 125 active operators. Just trying to keep it in perspective. Plus there is only a small variation after 6 months, now.

Hi Guym,

It is what it is, the EIA monthly data is much closer to final output than RRC estimates for the most recent 6 months.

The drilling productivity report and weekly estimates should be ignored, as should uncorrected RRC output data for the most recent 6 to 9 months reported.

Dean Fantazzini’s estimates are pretty good, but for the most recent 2 months possibly an average of Dean’s estimate and the EIA monthly estimate is roughly correct.

Hi Guym,

Probably 99% of the output comes from the top 250 producers. You think Texas cannot do it, but I think you sell your fellow Texans short.

We agree that we don’t know what Texas output is, if Texas doesn’t care, that is fine with me.

I imagine there are solutions to this problem, but again if nobody cares, it is all good.

CNBC is just another lemming, being led by the lead lemming, EIA.

U.S. Coast Guard & BSEE responding to fire on Shell Enchilada oil platform in GOM, oil production shut, sheen spotted: Coast Guard statement.

Hess Shuts 2 Gulf Fields on Shell Enchilada-Salsa Site Outage

ConocoPhillips Magnolia Field Shut on Shell Enchilada Outage

I assume they mean this high volume hub???

Oil & Gas Journal

The Enchilada pipeline hub provides oil producers with a wide range of options utilizing two sales oil export pipelines. (subscription but one free view) https://goo.gl/xiFNz5

Bloomberg – BSEE: about 81 kb/day oil, 167 MMcf/d gas shut in due to Enchilada outage

SeekingAlpha: Shell says production at the Auger, Enchilada and Salsa platforms in the Gulf and nearby fields has been shut in, as well as a 30-inch gas pipeline.

https://seekingalpha.com/news/3309926-shell-shuts-gulf-mexico-platforms-fire

Magnolia is pretty small but I think production from Baldpate/Salsa, which is quite a big gas/condensate field, and Cardamom, reasonably big oil field that goes to the Augur platform, might go through there to get to the pipelines.

It sounds like one of the main pipelines may have leaked (could be corrosion or mechanical failure). If it’s outboard the main isolation valves that will be a very long shut-in (and possibly bigger issues if there is unnoticed corrosion along the pipe which will have to be replaced. If it’s inboard, – easier, but still a long job I’d guess. A lot of aging facilities out there, and corrosion can get worse when production is down as things cool down faster so water condenses and then pools as it doesn’t get pushed along properly.

I was looking for that sort of information, seems hard to find without subscriptions. The fire is said to have been on the platform and so I guess the leak is inboard.

SHELL HAS NO TIMELINE FOR RESTARTING NORMAL OPERATIONS ON A PLATFORM WHICH WAS SHUT DOWN IN THE US GULF OF MEXICO DUE TO A FIRE, A NEWS REPORT SAID.

“Though the structure is visibly sound, crews will continue to determine the integrity of the platform and formulate a plan for damage repair,” the oil major told Reuters.

Shell added there was no oil in the water as a result of the incident.

The fire on the Enchilada facility involved a 30-inch gas export pipeline.

All 46 personnel working at the Enchilada facility were safely evacuated. Two Shell employees were injured. Both have been treated and released from the hospital.

https://www.energyvoice.com/oilandgas/americas/155833/no-timeline-resuming-operations-shells-stricken-enchilada-rig/

Fixing 30″ pipelines, especially when there might be common cause failure in other places, isn’t going to be quick – could be offline well into 2018. The fire kept on burning for some time, which implies there was a big inventory of gas to be released, which in turn implies it might be outboard the isolation valves, or at least outboard the platform valves, there may be a subsea valve on the sea bed.

http://www.worldoil.com/news/2017/11/13/hess-corp-issues-statement-on-impact-from-incident-at-shell-enchilada-platform

HESS CORP. ISSUES STATEMENT ON IMPACT FROM INCIDENT AT SHELL ENCHILADA PLATFORM

NEW YORK — Hess Corporation has released a statement about the impact on its operations resulting from a fire at the Shell Enchilada platform in the Gulf of Mexico. Shell advised in a statement on Nov. 12 that a plan for repairing the damaged portions of the asset is being developed. All production coming into the Garden Banks Gas Pipeline system also remains shut in until further notice.

Hess production is shut in at its Baldpate, Conger and Penn State fields. Production is also shut in at the Shell-operated Llano Field (Hess 50% interest). Hess production at these fields is approximately 30,000 boed.

Hess continues to work closely with the operator to understand the timing for a restart.

They might have to purge the pipeline -that will be a huge job.

George, at what point do offshore wells become uneconomical with the water cut? An old article I read suggested around 80%, but UK Forties and Captain are running over 90% per your chart. Seems like it’s mainly recycling water.

Each field is different but they usually run well into the 90s for water cut before they give up – it depends on how much the operators are having to pay in maintenance on the aging facilities and maybe for treatment chemicals. I don’t think much of the North Sea water is recycled – i.e. sea water is injected and the produced water is treated and sent overboard (in Norway, in my time anyway, at lot was injected into an aquifer). Re-injecting produced water can be a problem – e.g. scaling if different types of water are mixed, corrosion, souring because the produced water can contain a lot of absorbed long chain acid molecules (from the oil) which the sulphur reducing bacteria use as food.

So, that’s mainly water drift into the formation that is driving the oil for North Sea? Or, like you said, injecting seawater into an aquifer? The more I read, the less I always realize I know.

It’s almost all water injection, I don’t know of any aquifer flood in the UK North Sea, there may have been some gas flood, but can’t remember exactly, if so it’s probably in blow down now. On the Norway side the aquifer (is it called Utsira, my memory is not good for that sort of thing anymore) is just for disposal (rather than going overboard) where it is available – i.e. can be drilled into from the field location. Where there is injection it’s put under the producer wells so it moves up slowly and evenly and sweeps as much of the oil as possible from the rock pores. With natural aquifer flood (i.e. water just flows in from underneath and the sides as the oil is removed) there is less control, and the reservoir pressure has to be reduced to allow the water to flow, which isn’t always good, and sometimes the water is quite nasty stuff (e.g. in Kuwait).

Thank you! Excellent post!

Guess you all are hearing of reports of KSA having a new king within next few days.

Buckle up.

Googled, did not find anything to that effect. Still, makes sense to consolidate power, if the old King is abdicating.

On sputnik so … ? But he was reported to have bad dementia about a year ago and I’d guess anything with his name on recently is just coming from MbS, and he just signs where he’s told to. The army doesn’t like MbS so it could be them vs the National Guard in the worst case.

Zero Hedge 11:00 AM posting – referenced Brit Express and Iranian Press TV as sources.

So, once again, what is true and what is not?

Info/propaganda has become so effectively ‘weaponized’ in this era of global, instantaneous dissemination.

I believe there is some truth to that, except the abdication to MBS was supposed to happen within a year, as was previously planned, as I remember reading. I know there were stories of his dementia, before he even took over. When he was in the spotlight, everyone said he appeared fine, and free of any mental impairment.

Ongoing drumbeat to declare Venezuela’s oil bonds in default.

Amused by the phrasing “as Venezuela struggles to make payment”. The only struggle is getting banks to process the transaction amid sanctions. The phrasing suggests they don’t have money to pay, but they do.

Good old ISDA has been asked to declare default, but the asker is not at risk. This looks like a swamp dweller maneuver. Recall ISDA was the agency that managed to declare that Greece was not in default when bond maturities were moved out 30 years and bond holders were threatened by the EU with insolvency if they didn’t agree, thereby making it “voluntary”.

I see above in the article talk of Norwegian plateau. Yo, Douglas, you know anything about what the Norway Sovereign Wealth Fund projects for their revenue influx?

Hi Watcher,

What leads you to think Maduro still has money enough to pay off debts?

Rolling them over might still be within the realm of the possible, if his Chinese buddies are willing to buy them up and pretend he’s going to pay up, in exchange for becoming the de facto mother country, and Venezuela the de facto colony.

Personally I find it very hard to understand why the country hasn’t erupted into outright civil war already, considering everything. But I suppose he still has supporters enough dependent on whatever his welfare state can provide to them, while starving the opposition, to hold on a little longer.

Does anybody know anything about what’s going on inside the country in terms of the Venezuelan oil industry?

What little I read indicates that production will continue to fall rather sharply at least until the price of oil goes up quite a bit, and even then probably for another year or two while getting the industry back into some sort of proper working order.

Ven does not have much debt, by international standards.

And while no Chavez, he has support— Ven is not going back to being a US Client State.

The US has about 10 months to torpedo Ven (GS, China, andRussia are betting it can’t).

The Chinese Heavy Oil Refinery goes online in 2018, which will be game over for US control of refinery production.

We shall see——-

Mostly that.

Banks do not like people who do not borrow money. Ven debt is just tiny in comparison to assets underground.

Sep 2015 total was $110 Billion. Down from $130 Billion in 2013. Banks do NOT like seeing country debt decreasing, and you can guess for yourself what % of that 110 is owed to Russia and China and entities who have nothing to do with the US or US banks.

The latest story not clearly one of propaganda was that Russia was trying to divest itself of CITGO (CITGO is a big Ven owned refinery inside the US, 49% Russia owned) and trade their position for a share of Ven oil fields.

In terms of these debt payments, the amounts are single digit billions. They have oil. They have benefactors. What they do not have is a mechanism for payment that is not obstructed by sanctions.

To some extent, the banks may be doing some self harm. They are asking for more than interest payments. This, in effect, reduces Ven debt even further.

Final item, Ven GDP has been falling. Debt/GDP is 28% and ALSO falling. Even with the denominator falling, the ratio is too.

The new refinery will enable shipments of food and goods much more cheaply inside the country. Largely, things can indeed turn around from it, if they even need to. External propaganda is rampant. Population of Ven growing at about 1%. Repeat. Population is growing in this allegedly starvation smashed country. Life expectancy 75 for both males and females averaged.

The propaganda is truly amazing!

It would be making Goebbels blush.

Bidness is bidness. Unless, it’s not bidness.

The latest story not clearly one of propaganda was that Russia was trying to divest itself of CITGO (CITGO is a big Ven owned refinery inside the US, 49% Russia owned) and trade their position for a share of Ven oil fields.

Probably to reduce exposure to sanctions or seizure of assets.

But that would be pretty bold, even by HRC as Secretary of State standards.

Something I would like to know more about is the storage portion of the oil and gas industry.

Is there any body here who can write about it or comment on it extensively?

Most of the regulars would probably be quite interested in learning more about storage, such as who owns it, where it’s located, how much spare capacity is available, how much is being built or planned, and so forth.

Mac

Kinda timely question regarding storage, particularly in light of what is heading your way in the coming 2 decades.

I am completely unfamiliar with oil storage, but natgas storage info can be had on the EIA site. It is both impressive and crucial as reliance upon natgas continues to increase.

As far as NGL storage, however, just today an announcement was made regarding Chinese investment in, and collaboration with, West Virginia authorities to facilitate over $83 BILLION in plants, infrastructure, downstream components – including storage – within the state over the next 20 years.

Appalachia Rising!

Thanks CoffeeGuy,

The data at EIA is great, and all you need I guess, to figure out the gas market based on seasonal gluts and shortages and so forth.

But it doesn’t say much if anything at all about HOW the gas is stored, or where, other than maybe by country, who owns the storage facilities, how they are operated, and so forth.

I’ve learned a hell of a lot about the hands on side of the oil industry by following this site, enough it would be safe to chain me to a post with a short enough chain I couldn’t touch anything important, so I could watch a drilling crew set up or tear down, lol.

But there’s no place I know of that discusses storage in any detail, except for the volumes of oil involved.

At the end of the American Revolutionary War, the British band played a tune called The World Turned Upside Down, or something close to that.

Stupidity on our part, and long range planning on their part, may well result in the Chinese turning our Yankee world upside down.

We’re now the colony, rather than the center of the empire, in some respects, and perhaps more respects from year to year from here on out.

The fine hardwood logs harvested here go overseas.We don’t have anybody left to use them, locally. We brag about exporting grain and meat, not realizing the implications. Farming is high tech, but nothing like as high tech as the industries that send stuff back here, in payment.

Colonies have historically supplied natural resources such as oil and raw or partially finished materials to the mother country in exchange for manufactured goods.

If the Chinese wind up owning enough of their state, West Virginia hillbillies may “nationalize” foreign investments at the state level.

They’re practical enough to understand that they can tax the hell out of anything in the state, if they choose to do so.

You can’t move a pipeline the way you can move a factory full of looms and sewing machines or furniture machinery.

What the rest of the country may do is indicated by the fact that we elected Trump prez. When enough people get scared for their economic welfare…….. there will be a political backlash of such magnitude that it’s hard to guess what sort of laws and policies will be adopted.

Helium storage is also interesting. https://en.wikipedia.org/wiki/Helium_storage_and_conservation

https://pubs.usgs.gov/of/2017/1111/ofr20171111.pdf

I haven’t seen this posted before, so may be of interest: it’s a USGS assessment of undiscovered conventional resources in the Wilcox play onshore on the north coast of GoM (Texas and Louisiana mostly), issued in September. Not much oil but a P50 of 78 tif of gas. The fields are pretty deep so maybe a bit hot for current technology?

Baker Hughes U.S.A oil rig count up +9 to 738…. natural gas unchanged at 169…. Permian +6

Canada oil rig count: up +8 to 108…. natural gas up +4 to 95

SINGAPORE (Reuters) – The amount of oil stored on tankers around Singapore has dropped sharply in the last few months. Shipping data in Thomson Reuters Eikon shows around 15 super-tankers are currently filled with oil in waters off Singapore and western Malaysia, storing around 30 million barrels of crude. That is half the number of ships in June and down from 40 tankers holding surplus fuel in mid-2017.

http://www.reuters.com/article/us-asia-oil-storage/sinking-feeling-asian-floating-oil-storage-declines-as-crude-market-tightens-idUSKBN1DA0D7?il=0

GRAPHIC: Volume of oil stored on tankers in Singapore, Malaysia drops: http://reut.rs/2zqNvXZ

The free tanker tracking service only covers Malaysia Sungai Linggi.

http://tankertrackers.com

All My Frac Sand Comes From Texas – Major Changes Afoot In Sand Use, Supply And Prices

RBN Energy – Thursday, 11/09/2017 – Published by: Taylor Robinson

In the past year, there have been major changes in the frac sand sector. Exploration and production companies in the Permian and other growing areas have significantly ramped up the volume of sand they use in well completions, catching high-quality sand suppliers in the Upper Midwest off-guard and spurring sharply higher frac sand prices due to the tight supply. At the same time, development of regional sand resources has taken off in the Permian — with close to 20 mines announced with upwards of 60 million tons/year of nameplate capacity possible — and, to a lesser extent, in the SCOOP/STACK, Haynesville and the Eagle Ford.

https://rbnenergy.com/all-my-frac-sand-comes-from-texas-major-changes-afoot-in-sand-use-supply-and-prices

Yeah, every mining operation upsets some sort of an ecological balance. In Texas, it’s lizards. Sand mining would have started quicker, and bigger, if they didn’t have to try to count lizards.

Bahrain calls pipeline blast ‘terrorism’ linked to Iran

( I have a feeling things are going to get even more interesting)

https://www.reuters.com/article/us-bahrain-pipeline/bahrain-calls-pipeline-blast-terrorism-linked-to-iran-idUSKBN1DB0NW?feedType=RSS&feedName=topNews&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+reuters%2FtopNews+%28News+%2F+US+%2F+Top+News%29

https://www.epmag.com/oil-service-managers-deliberate-direction-2018-1656506

Stimulation costs per stage went from a little over 33k in 2016 to 75k per stage mid 2017. That would have to affect budgets of how many to complete, especially when budgets are contracting during the year.

I would love it if I am proven wrong. That is, oil prices go up, and massive production will be happening by the end of 2018, proving EIA correct. Why? Because some of that money could be mine. But, it’s not going to happen, because of equipment, manpower, and budget constraints. Probably will by the end of 2019, I hope, but not 2018.

US – update through July 2017

https://shaleprofile.com

OPEC, citing secondary sources, says its October oil output decreased about -150,000 bpd m/m to 32.59 million b/day (It’s actually -160 kb/day as September has been revised slightly lower)

OPEC MOMR table on twitter https://pbs.twimg.com/media/DOgroDXV4AA9o0a.jpg

OPEC says OECD commercial oil stocks fell 23.6 mil bbls in Sept to 2.985 bil bbls, still 154 mil barrels above 5-yr avg https://pbs.twimg.com/media/DOg6S7iX0AAQexL.jpg

OPEC significantly revises up its forecast of 2018 demand for OPEC crude: 33.42 mil b/d, up 340,000 b/d from last month’s

I guess due to economic growth, chart of global PMIs: https://pbs.twimg.com/media/DOf_Qn5WAAA8aEM.jpg

World supply/demand, 1st 3x Qs of 2017 compared to 1st 3x Qs of 2016, chart on twitter https://pbs.twimg.com/media/DOgzcn2V4AAedqm.jpg

I think Ron will post an update on Wednesday, mostly Iraq though.

Anyone know how much the Bahrain pipeline exposition might take out – it has 230,000 bpd capacity, but might not run full and/or there might be alternative export routes.

2017-11-11 Saudi crude oil flows to Bahrain have now resumed – Bahrain News Agency.

http://www.bna.bh/portal/en/news/810695

Chinese inventories – these figures are available earlier from the Xinhua news agency but it’s subscription.

As of this posting, spot wholesale price of electricity in New England is $133/Mwh – more than four times the price in the nearby PJM region.

Oil and coal providing 7% of the juice.

To be burning oil (6%) in the year 2017 to provide electricity when the largest natgas sources on the planet are a short car ride away is stunning in its scope of irrationality.

Looking to be a long, cold, expensive winter up there.

I will keep reading this blog, because there are valuable contributors. Posting? Nah!

GUYM says: “Posting? Nah!”

In rememberance, a few highlights from this thread only. Gone (?), but not forgotten.

“Same principle drives lemmings, I think. They have to be over the cliff, before they will recognize it is there.”

“That’s enough to make Micky kneel when Disney plays their music preceeding their films. Fellow rodent.”

“Yeah, Spain is one country I would love to visit. With my limited Spanish, I could, at least, get them to laugh at me. ”

“Bidness is bidness. Unless, it’s not bidness.”

“CNBC is just another lemming, being led by the lead lemming, EIA.”

http://www.zerohedge.com/news/2017-11-13/peak-permian-only-3-years-away

I think I can see why so many people have such uncertainty about this shale stuff … the article from ZH being a case in point.

That author, along with at least two other writers from oil price.com (the original source of the article), consistently writes highly dubious pieces that invariably minimizes future unconventional output.

From a purely financial perspective, perceived scarcity is a boon for producers.

But, even a minimal understanding of what is going on in West Texas AND New Mexico, should enable one to recognize that there are decades of highly productive output ahead.

Three years … gimme a break.

That’s like the Post Carbon Institute claiming the Marcellus would peak in 2016.

Hi Coffeguyzz,

If the median USGS estimates are correct, then I expect the peak output for US tight oil to be around 2026 at about 7.2 Mb/d, though it will depend on completion rates, this is a high scenario which will see fairly rapid decline post peak. A slower ramp up would mean lower output (maybe 6 Mb/d) but more of a plateau that might extend to 2030.

Much will depend on oil prices, higher prices are likely to lead to a faster ramp and a higher peak. Oil prices are difficult to predict.

Dennis

An observation from me regarding your ongoing analysis of all these hydrocarbon matters …

The awareness of the dynamically evolving nature of this stuff must not be underrated.

Specifically, your use of USGS data is both rational and justifiable as, being an impartial, highly regarded source, the USGS cannot be beat.

Top notch outfit through and through.

But …

As the USGS folks themselves continuously point out, their evaluations are based primarily on historical production records, stratographic info collected over eons of time, AND projecting – to the best of their abilities – future applications of existing technology.

That “existing” phrase is where so much confusion, mis predictions, even contemporary evaluations can go awry.

2015 article (Myths of the Bakken) by Bakken legend/geologist Kathy Neset succinctly describes the brief evolution of Bakken development regarding unit drainage, well placement, etc.

The 7% recovery – presently – that she mentions will most assuredly NOT remain that low.

Advances in increasing lateral lengths by pioneers like Eclipse Resources (just did a 20,800 footer – Mercury well), mass simultaneous production from multiple pads like Rice and Encana are doing, incredible completion techniques from EOG are ALL – sooner or later – adopted by the bulk of remaining operators.

Mr. E., down below, questions the size of the Permian.

When the remaining USGS numbers are published, wouldn’t surprise me a bit to see a Ghawar size resource claimed to be in the ground.

Dennis, these guys are now going spud to TD in 5 to 14 days everywhere.

They are fracturing 50 to 120 stages all over.

They are monitoring and controlling frac propagation with real time seismic and diversion processes.

They are increasing the size of the Stimulated Reservoiur Volume dramatically with the recent introduction of Microproppants.

Most recently, the highly restricted choke management is producing very high early month production.

If you want a glimpse at the future, keep an eye on the outliers, the Powder River Basin, the Unita, the Rogersville.

These nascent areas are increasingly viable as the cost to D&C, the speed and precision of drilling, the recovery rate all enhance the fringier areas ‘doability’. This applies to non core areas in current plays.

And there are MANY more, (just east of Montreal, Questerre is set to drill a bunch of Utica wells next two years. Yes, east of Montreal, the Utica has a production history that might surprise you).

Lottsa moving parts, Dennis.

Hi Coffeeguyzz,

Just projecting based on the data I see plus USGS estimates.

Most of the technology advances allow faster extraction, but it is not clear that EUR per lateral foot drilled has increased by very much, take the most mature areas such as the Bakken or Eagle Ford and look at the average well output at shale profile, the changes over the past 3 years have been very small, despite all the amazing technology applied. Perhaps tight oil URR will be a little bigger than I have estimated, time will tell.

With the information I have I think a 50% probability that US tight oil URR will be between 40 and 60 Gb is correct. This also implies there is a 25% chance it will be less than 40 Gb and a 25% chance it will be more than 60 Gb.

IEA World energy outlook (WEO) 2017 released:

http://www.iea.org/weo2017/

http://www.iea.org/publications/freepublications/publication/WEO_2017_Executive_Summary_English_version.pdf

I haven´t read the report, just the publicly available summary. They now think, or say, that US will become a net oil exporter in the late 2020s and fill the gap from decline elsewhere.

“With the United States accounting for 80% of the increase in global oil supply to 2025 and maintaining near-term downward pressure on prices, the world’s consumers are not yet ready to say goodbye to the era of oil.”

“A remarkable ability to unlock new resources cost-effectively pushes combined United States oil and gas output to a level 50% higher than any other country has ever managed; already a net exporter of gas, the US becomes a net exporter of oil in the late 2020s. In our projections, the 8 mb/d rise in US tight oil output from 2010 to 2025 would match the highest sustained period of oil output growth by a single country in the history of oil markets.”

Cost-effectly? Why do these companies earn so little money, every other business that produces for 30 and sells for 50 swims in lakes of money. And now the utility companies wants a healthy increase in payment – they have to invest heavy in new equip when output growth is needed. Pulling the equip from 2014 out of the barn and working for a flat 0 is one thing, doubling capacity is another.

And, thats my question, how big are these shale ressources? More oil than Saudi Arabia? The gas ressources seem to be huge. But gas is better for fracking, much less possiblily to block the fracked fissures with gas than with liquids.

Indeed.

The Shale Gas undiscovered resource estimate (F50) by the USGS is about 960 TCF (166 Gboe), where the undiscovered tight oil is about 36 Gb (about 4.6 times smaller in energy terms).

Even with this very large natural gas resource, US natural gas is likely to peak by 2035 and perhaps sooner (it will depend how quickly conventional natural gas declines as shale gas ramps up). The growth in US Shale gas from 2011 to 2015 was about 15% per year, if growth continues at this rate soon all US natural gas output will be from shale gas. If the URR of shale gas is about 1300 TCF and peak is at about 650 TCF cumulative production, a 10% annual shale gas growth rate until 2024 followed by a 2%/year growth rate until 2035 will lead to cumulative shale gas output of 650 TCF by 2035. From 2007 to 2015 cumulative shale gas output was 70 TCF with 15 TCF produced in 2015, Total US natural gas output was 33 TCF in 2015.

And with this tiny 36 Gb resource they are tooting around of producing 12 mb/day or more from shale oil? Do they have discovered another 100 or 200 Gb to support this?

https://oilprice.com/Energy/Crude-Oil/US-Shale-To-Beat-Saudi-Production-Growth.html

Hi Eulenspiegel,

The 36 Gb is undiscovered oil, there is probably another 14 Gb of 2P reserves (discovered resource) for a total of about 50 Gb (note that I include any reserve growth as an undiscovered resource).

The IEA is including both NGL from shale gas and tight oil in their 12 Mb/d estimate, I doubt their estimate is correct, but my modelling based on production data through June 2017 and USGS estimates suggests a peak as high as 6.9 Mb/d in 2024 is a possibility with rapid decline by 2034 (16%/year or more). In 2016 about 3.5 Mb/d of NGL was produced in the US, if we assume the barrels of NGL per cubic foot of natural gas produced remains unchanged we would need to see shale gas output triple from 15 TCF in 2015 to 45 TCF in 2024 to reach 12 Mb/d of C+C+NGL output. I doubt this will happen, but shale gas output may increase to 33 TCF by 2024 so the C+C+NGL from shale gas and tight oil might reach 10.4 Mb/d (6.9 tight+3.5 shale gas NGL).

Thank you.

Even at 6.9 Mb/d it is usage of 2.5 Gb / year of a roundabout 50 Gb ressource – a really fast production speed.

All this investing in service technology, pipelines, even steelmills, trucks, hightech, seismic equip … has to pay out in only a few years of boom – half of the production will be in a long tail from squeezing out old holes and fracking the borders of the ressources.

I think with this crazy production speed much of the investment won’t pay out – for example if you have a peak of only a few years all these extra pipelines you can close after a few years have to be paid down.

A production over 30-40 years of this ressource at constant output would be much more cost effective, everyone would earn more money.

Hi Eulenspiegel,

Much of the infrastructure is in place already, quite a bit of this is from the Permian basin which has been producing oil for a long time, perhaps this level of output will be too much for current pipeline infrastructure, in which case rail or trucks could be used.

Much will depend on prices which for these scenarios I have assumed reaches about $120/b by 2025, lower prices may mean lower output. Clearly I am unable to accurately predict future oil prices.

Chinese crude oil refinery runs holding up at record highs…

2017-11-14 Reuters – October domestic crude oil production inched down 0.4 percent on year to 16.01 million tonnes, or 3.77 million bpd, hovering close to August’ s record monthly low of 3.75 million bpd.

Meanwhile natural gas output rose 15 percent in October from the same month a year ago to 12.4 billion cubic meters, the highest since March. Demand for the cleaner fuel is set to grow at the fastest pace sine 2011, spurred by Beijing’s gasification drive.

https://www.reuters.com/article/us-global-oil/oil-steady-tempered-by-caution-over-rising-u-s-output-idUSKBN1DE04H

https://www.ft.com/content/88bc3246-c8f4-11e7-ab18-7a9fb7d6163e

“Standard & Poor’s has declared that Venezuela is in default after it missed two interest payments and following a meeting in Caracas that left investors with little notion of how a default on its $60bn debt pile can be avoided.

S&P, which is the first rating agency to say the country is in default, said on Tuesday that Caracas had failed to make $200m in coupon payments for global bonds due in 2019 and 2024 within the 30-calendar-day grace period.

The agency said it had downgraded the issue ratings on those bonds to D from CC and cut the country’s long-term foreign currency sovereign credit rating to selective default, or SD, from CC.”

Whether a person or a country can pay a debt has as much to do with the ability to earn money or draw down savings as it does with the size of the debt.

Venezuela’s debts may not be very large, as national debts go, but the country is apparently busted, financially.

I’ll leave it to somebody else to explain the implications for the oil market.

Does that mean they have to stop exporting oil – otherwise it could be seized as an asset by creditors? Either way they seem to have no way of getting any income now, unless they can come to some deal, probably involving giving ownership of the oil facilities to someone else.

George. I believe creditors could try to seize oil shipments.

I wonder, however, how they will keep producing oil without outside help. I think I have read where Schlumberger and Halliburton are owed large sums. I assume foreign firms will not provide any more services on credit.

I know very little about operations, but I suspect everything is in disrepair?

They are not permitted to pay, and what wasn’t paid was insignificant. They paid $2B over the past 2 weeks.

Creditors seizing assets may not be in the cards. The bondholders of significant size said recently they know payments were late and why they were late, but they were made and they are happy. They don’t really want to alienate an entity with that much collateral.

This is all about ISDA and NY banks who have their own agenda.

There are supposed to be talks today on restructuring some loans with Russia, though Rosneft has said it won’t loan anymore. International bonds total $60 bn and including bilateral and other loans it’s $150 bn, which overall would be second in size only to Greece if it is restructured. The meeting on Monday was reported as “crazy stuff” by the creditors. FT is reporting an expected “cascade of defaults” now, with a bail out by Russia as Maduro’s only hope. Lowest bonds are worth 25c on the dollar at the moment, and falling.