A Guest Post by George Kaplan

This briefly covers the production side as the hurricane outages are dominating the trends at the moment, but there’s a section at the end on discoveries and reserves that may give some pointers to future expectations.

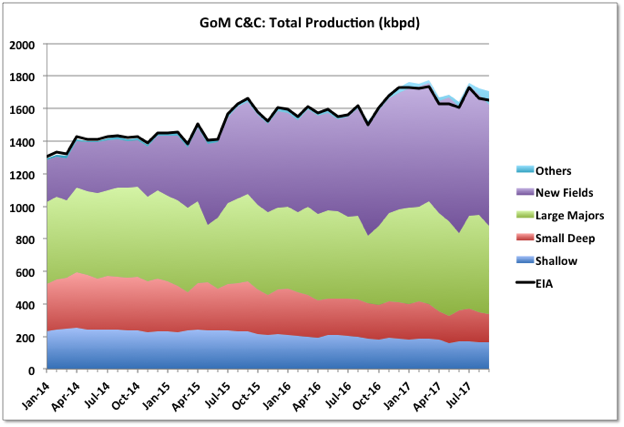

The tables below show the production numbers for September, and their relation with previous months from BOEM and EIA, which are pretty close, but for some reason never the same and have actually diverged quite significantly at the moment. Both sets of data get revised, possibly up to a year later, usually those from EIA more than those from BOEM, and they end up with much closer, with EIA usually slightly lower

| BOEM | C&C Production (kbpd) | m-o-m (%) | y-o-y (%) | Average Annual (kbpd) |

|---|---|---|---|---|

| July | 1756 | |||

| August | 1722 | -2.0% | ||

| September | 1706 | -1.0% | 12.2% | 1707 |

| EIA | C&C Production (kbpd) | m-o-m (%) | y-o-y (%) | Average Annual (kbpd) |

|---|---|---|---|---|

| July | 1732 | |||

| August | 1665 | -3.9% | ||

| September | 1650 | -0.9% | 9.9% | 1677 |

For August Hurricane Harvey knocked out about 80 kbpd, Irma in September had a similar impact, but some of the increased drop might be natural decline. Nate in October took out about 250 to 300 averaged over the month. In addition there have been some other unplanned shut downs: Thunder Horse for a few days from an electrical failure following restart after Irma, Delta House following a subsea failure, and a pipeline rupture on Enchilada which took out about 75 kbpd in early November (and is still offline). The Delta House outage has not been reported very extensively but the Rigel field may still be offline, losing 25 kbpd. There is also continued decline in mature fields at about 12 kbpd, which may be accelerating as some of the newer fields are now in decline, and there are no new greenfield developments due until Stampede in first quarter of 2018 – though there may be some in-fill drilling still on some of the larger fields (e.g. Mars, Thunder Horse) and a couple of wells for Phoenix and Holstein (see below).

It remains to be seen but with these outages it looks like this year will not exceed 1700 kbpd on average; it will however still be a record a year, although well down on most predictions from last year, and the exit rate will be below last year’s. Recent adjustments to the EIA numbers now mean that September 2009 remains their peak month, with March this year the secondary peak. Without the outages August might just have edged a new overall peak.

C&C Production

BOEM issue three sets of data that can be used to give total production per month: by well, by lease and their own estimated total. Over time the total by well and their estimate tend to converge (there is usually some missing date in the wells data for as long as twelve months), though for some reason they are never exactly equal – the monthly estimate seems to be about 2,000 bpd higher for most months once all data has been collected. The total lease estimate is always about 10 to 20,000 bpd lower, mostly because of production from test wells and wells with “NO LEASE”, which it doesn’t include. It appears EIA use this lease data with some adjustment for missing numbers in their estimates, though there’s a difference between their STEO and the GoM pages. I use the well data as it’s easy to download and update to the charts in one go. The trouble with that method is that data might be missing for recent months and it’s not easy (i.e. requires more work than is worthwhile) to spot missing data versus data showing no production. If I notice something missing I assume constant production from the last known data point, but might miss some, especially for shallow water leases. However for this month almost all the shallow leases have missing data so I’ve kept them all constant. I’ve extended the data back to 2013 as this shows plateaus versus peaks a bit better, and simplified a couple of the charts.

The new fields look like they are plateauing and maybe starting to decline. The Mars-Ursa fields have been increasing production through 2016 and 2017, mainly from ramp-up of new fields at West Boreas and South Deimos, but also it looks like additional development wells on older fields (without which the total new production only would almost certainly be showing clear decline). I haven’t seen any announcements but it seems unlikely there will be much more net increase for these fields (see below for a bit more discussion on reserve growth here). Lucius, Cardamom and Great White are three medium sized fields that look to falling fairly quickly at the moment, but there is ongoing or soon to be drilling at them all.

Cardamom is a recent start-up and is one of the deep pre-salt fields in the GoM. It is produced to an old Shell platform, Augur, and has shown quite rapid decline. Augur is one of the platforms currently shut down because of the Enchilada pipeline failure, together with Magnolia and Baldpate/Salsa.

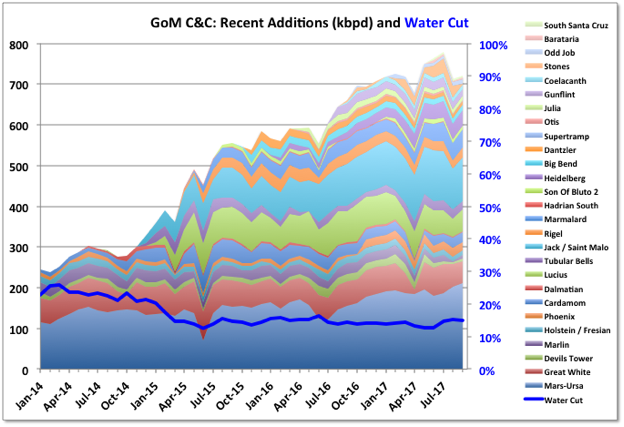

The Delta House fields are Rigel, which was where the recent subsea connector failure occurred, Marmalard, Odd Job, Otis (mostly a gas field) and Son of Bluto 2. They got to 92 kbpd in September, which is probably about as good as they can do on average without exceeding nameplate. There hasn’t been much information on the extent of lost production there, from either LLOG or BSEE, and it might not become apparent until the November field production figures are released. Also notable is that Stones was offline for most of the September after just about reaching nameplate.

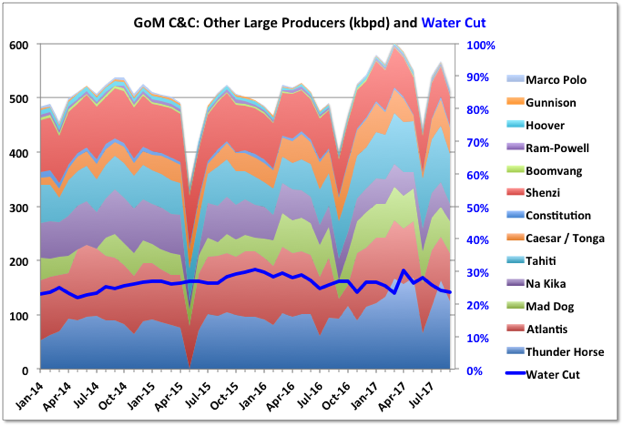

I’ve lumped all the fields operated by the larger producers that are not shown in the new fields chart here. This is the group that was most affected by the forced outages in August and September. They are holding a plateau, with a slight increase recently because of Thunder Horse South, but it takes continuous drilling to keep them there and that may start to become less effective as most of the platforms are getting past 10 years, which is usually the limit for plateau design.

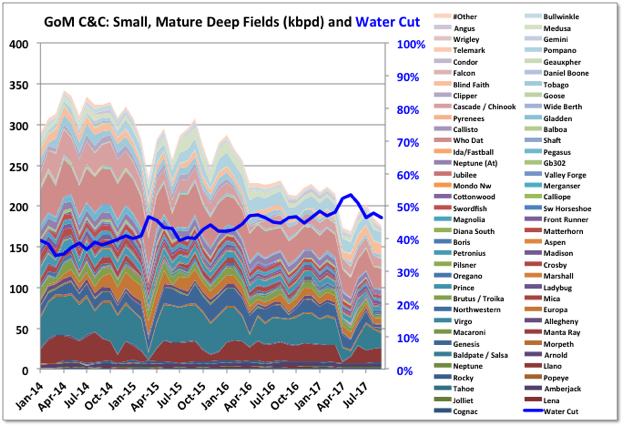

The mature deep-water fields continue to decline; possibly slightly accelerating. The two largest producers, Llano and Baldpate/Salsa (brown and cadet blue near the bottom) will both be shown offline from November because of the Enchilada issue, but even before that they were in fairly rapid decline).

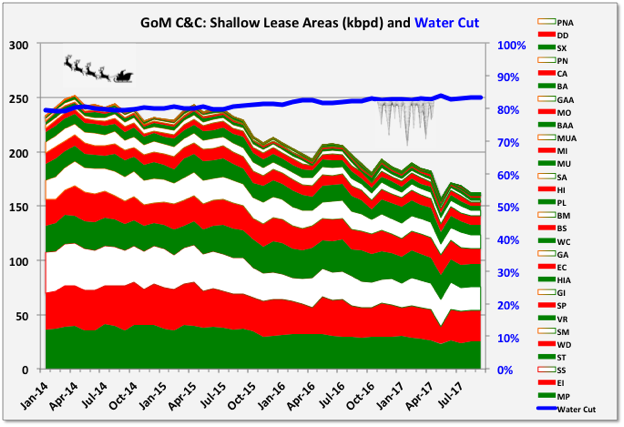

There wasn’t much new data for the shallow fields in September, possibly because of hurricanes, but there’s no reason to think the general decline won’t continue (see below).

Deep Water Drilling, Discoveries and Production

The chart below shows details for deep-water leases only (including production, and also note the units which allow things to fit better on the right hand access). Gas is a pretty reasonable bell curve, but influenced a lot by increasing associated gas, which changes in line with the oil. The C&C might have been closer to a bell curve except for big bites taken out by the 2008 financial crisis and the drilling hiatus following Deep Horizon. It’s difficult to pick out a pattern that would indicate what the exact delay between wells/discoveries and production but it looks to be around fifteen years.

New wells and discoveries are tailing off. I think this year will be in line with the declining trends. What this chart doesn’t show, but see below, is the discovered reserve size, and this is tending to decline faster than the actual number of discoveries. There aren’t many undeveloped leases remaining (shown as qualified – mostly newer and likely to be produced, or open – older and maybe waiting for much higher oil prices). There may be new fields in operating leases, which wouldn’t be apparent (one of the difficulties of the way BOEM reports against lease numbers) but I don’t think there are many.

GoM drilling over the past six months is at all time lows for the period since Baker-Hughes data has been available, but a lot in the past were for gas and oil rig numbers are still fairly robust. The E&Ps definitely went full on boom cycle in the GoM during the high price years from 2012 to 2015, possibly partly catching up from the hiatus after Deep Horizon.

Future Production and Developments

Anadarko are cutting overall investments in 2018 compared to this year and are starting share buy backs; they have stated that they will drill a maximum of five GoM development wells on a budget of $1.1 billion. I’d estimate that would give 20 to 30 kbpd new production. There was no mention of new tie-backs so they seem likely to be wells into existing fields using existing subsea infrastructure (e.g. for Marlin/King/Horn Mountain, where they have had successful new wells this year, Lucius/Hadrian North or Holstein/Fresian). They and BP are also developing the Constellation tie-back to Constitution, expected for mid year at about 12 kbpd average oil. The Phobos appraisal well was not encouraging and they have shelved that tie-back, which would have gone to Lucius, at least for now. They also have options with the Shenandoah complex, which has been downgraded from a stand-alone project but may be amenable to tie-backs, and also have the Warrior discovery under appraisal, which would go to Marco Polo (but one section of that area has been investigated and found to be unattractive so reducing the resource base).

LLOG have given details of a number of developments for Crown and Anchor, Claiborne, Blue Wing Olive and Red Zinger. Unlike Anadarko these wells exist, drilled for exploration or appraisal, but require new flowlines and umbilicals for production. Tie-back wells typically flow 3 to 10 kbpd, though some can get to 20 kbpd initially, but usually immediately start to decline at about 20% per year, sometimes higher.

Stampede will start up early in the year and has pre-drilled wells so should ramp-up quickly, but I think they only have nameplate well capacity for about 40 kbpd oil (average production will be less, especially in the first year). Big Foot is not due until the fourth quarter, has only two fully pre-drilled wells and likely won’t contribute much in 2018. The other thirteen wells have the top two conductor sections drilled but will be completed by the platforms rig; it is fairly heavy oil so will likely need all available wells, which will use ESPs, to achieve full capacity at 75 kbpd.

The Atlantis North development should continue through the year, but for all the publicity about new seismic technology uncovering new oil this year, it seems they are only just about able to maintain a plateau there as the wells decline very quickly.

Talos made a discovery at Tornado II in October, which will be tied in with the Helix Producer in December. It flowed at 16.8 kboed on test, but that will be lower (say by 20%) for oil only and less overall against the backpressure of a flowline; and may also back out other online production if it raises overall backpressures on producing wells, so probably less than 10 kbpd of oil net average increase. The switch to lower risk, near field exploration is allowing some companies to reduce overall decline rates on existing facilities, but it is a bit of a Red Queen treadmill, and eventually the prospects are going to dwindle.

BHP, which operate Shenzi and have other holdings in GoM where most of their conventional oil and gas is produced including a 44% stake in Atlantis, are expecting a 9% decline next year, despite some planned in-fill drilling.

ExxonMobil aren’t a big player in the Gulf but have spudded a wildcat, Antrim, in the Green Canyon area. I haven’t seen data but get the impression they are having a higher exploration success rate than most, maybe because they are ultra conservative or maybe they have better technology – they’ve certainly invested a lot into modelling an visualisation.

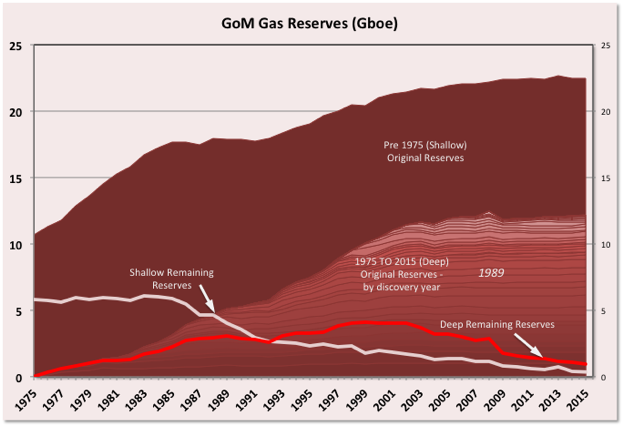

Reserve Evolution

BOEM issue a yearly update on reserves that includes the estimate for current numbers and revisions to the original estimates for each field. It is part of BOEM’s remit that they develop these estimates independently, but they use the same SEC/SPE methods as the E&Ps. The data comes out in December for the previous year, so 2015 data is the latest available. The way that BOEM hold everything based on leases, and each lease is associated with a single field, makes some of the adjustments a bit ambiguous – e.g. a new field found in a lease will go against the main field name and would look like growth (and presumably the opposite is possible though less likely: a small field that was thought to be commercial is written off and looks like negative growth on the main field).

The charts for oil and gas below are turned on their side compared to normal reserve curves. Usually the curves show original reserves against their year of discovery and any changes in the understanding of what was actually discovered, or in expected recovery (i.e. ‘growth’) is backdated, so all the points on the curves can move up and down each year as they are updated, but they always increase from one year to the next along the x-axis. The curves below show how the estimates of original reserves have evolved, they don’t change (only get added to for each new year), and they can decline from year to year. The more common sort of curve would be a taken from the right hand axis, with the backdated reserve numbers being where each year’s reserve wedge intersects the axis. I’ve split them as pre-1975, which is all in shallow water (the first deep discovery, Cognac, was in 1975) and lumped together; and post-1975, which are mostly deep water, and are split up by discovery year. There have been about 1.1 Gb C&C and 4.5 Gboe of gas added from shallow fields since 1975, though 85% of this was before 1985.

Despite the lease issue I think the growth trends come out as reasonably indicative of what’s going on. For C&C there was growth in reserves up to about 2002 from discoveries, but also from a big reserve growth in old, operating shallow fields. Shallow fields were discovered as far back as the 40s to 60s, and developed with fairly ad hoc methods. Therefore the growth in the shallow reserves comes from three main sources, all of which are probably related to availability of better technology (seismic, drilling, fluid analysis, reservoir modeling): 1) better understanding of the oil in place meaning accurate, rather than conservative, estimates can be made); 2) higher recovery rates on what is there; and 3) some new shallow field discoveries or new development of technically difficult old discoveries.

Similar growth has been seen on the old US and Middle Eastern conventional fields, although there isn’t really a way to predict how much growth can be expected from each field.

Since 2002 there hasn’t been much overall growth with one particularly notable exception. In fact some of the deep water fields discovered up to then have shown some significant negative growth. There have been some, generally small, discoveries, but for those found before 2008 the reserves mostly had to be taken off the books following the rule changes requiring that reserves only apply on operating fields or those with definite development plans. These are now gradually being added again as projects reach FID and now make up the bulk of recent growth, exceeding additions form newer discoveries.

The largest field is Mars-Ursa, and this has shown significant growth, though much is really new discoveries rather than moving “possible” to “probable and proven” categories from the original discovery estimates. The original field, Mars, was discovered in 1989 with Ursa and Princess in 1991, and Deimos discovered in 2002 (all at different depths, and processed through two platforms: Mars and Ursa). More recently two smaller fields – West Boreas and South Deimos, discovered in 2009 and 2010 respectively, were started up via a new platform, Olympus TLP, which was added to develop these and other parts of the leases. All these fields’ reserves go against the 1989 discovery. Notwithstanding that, however, I also think there has been some significant increase in recovery rate through improved water injection strategy and well design, which would be genuine “reserve growth”. Note that two other fields, Crosby and Europa are developed through the Mars platforms but are reported as separate leases with their own reserve numbers.

Against this some of the other large, deep fields have had significant write downs of their initial reserve estimates, notably the BP fields of Thunder Horse, Mad Dog and Atlantis, but also the BHP operated Shenzi field which lost over 70% of it’s original reserve estimate. Thunder Horse, Atlantis and Mad Dog all have extensive brownfield work just completed or in development so some of these reserve downgrades may reappear, though it’s not clear if they should count as growth or new discoveries.

I’ve shown some other fields as more representative of how the deep fields have behaved: Tahiti/Caesar/Tonga is a field split between two operators and has been up and down but overall has grown, and might again when the 2016 and 2017 figures come out as there has been a lot of brownfield work there; Great White has declined slightly overall (especially in 2015 which might be price related); Cascade is a small field that has been pretty disappointing and dropped almost 60% from it’s original estimate; and Devil’s Tower looks like it has grown significantly for oil, but initially it was producing from three gas fields and subsequently Kodiak, an oil field discovered in 2008, has been added (from what I can see Kodiak production looks pretty disappointing and it is currently cycled, so a reserve downgrade might be on the cards).

Natural gas is similar to C&C in that there was large growth in the operating shallow fields as new technology become available in the 80s; deep water field discoveries added notable reserves were until about 2002 but then petered out (most of the gas is associated so no surprise there) and no discernable growth in the original estimates on any years except maybe for Maars-Ursa from 1989.

Off Topic Finish

Last month an ultra modern designed library opened in Tianjin, China. I find these futuristic designs look great in isolation or amongst similar buildings on a mocked up sci-fi green screen, but not so good when surrounded by more traditional designs. In contrast to that below is one of the oldest libraries, this one for wooden printing blocks, at The Tripitaka Koreana, Haeinsa Temple, South Korea, founded in 1231 (well before Gutenberg). It is managed by monks and has limited access. The blocks are perfectly preserved because of the natural ventilation and shelter allowed by the building’s design and year round cool air, as it is half way up a mountain.

(p.s. This is my last post for the year so Merry Xmas, Happy Holidays etc. to you all, whichever of the various entities supposedly born or created on the 25th December you may or may not celebrate.)

164 responses to “GoM Production: August and September Update”

Concerning the comment about loss of reserves due to either an SEC rule change, or the removal of a project due to, perhaps, a change to budget — in what category of the 1P 2P or whatever sequence would one find a declaration by the company that there is simply less oil there than expected?

We have often discussed the usually failed attempt to delineate economics vs geology in defining how much oil is in a field. But this first derivative event of a change in declared reserves might not suffer from the same lack of delineation. Perhaps it’s much easier to identify a change in reserves due to economics vs. a declaration that the geology wasn’t as expected.

Once projects are at FID and on the books it’s difficult to see individual field changes as company reserves are reported at best only per region or country (maybe one reason for the rule change was to stop sudden drops). Before FID there can be some big changes e.g. Kaskida for BP in GoM was going to be huge after discovery, then not so good after a couple of appraisals and then the lease was given up. Phobos mentioned above looked good initially but not after the recent appraisal well. Thunder Horse was built with a much bigger nameplate throughput than it would have been if the shrinkage to reserves had been foreseen (i.e. they might have been advised to do an extended well test or a couple of more appraisal wells).

Hmmm.

So final decision is made to invest to produce from a field. It starts flowing. Then it stops. Early.

Surely this has happened. Does not the reserves estimate get cut? Sure will make the executive decision look bad, so maybe not, and that’s pretty scary. There could be much less out there than expected.

OTOH Ghawar has pumped longer than expected, so maybe it works in the other direction, too.

The reserves would get cut – but they’d know about it long before it went offline – but company reserves don’t get reported by field, generally only as a totle or by region 9e.g. USA, rest of world), so it wouldn’t necessarily be obvious what has happened amongst other growth, depletion, discoveries or revisions.

This is said to be from an RBN Energy article but I couldn’t find it on their website

Permian Production

Increasing looks like associated gas takeaway and ability (inability) to flare excess gas will be most critical factor for aggressive production growth in the Permian in years to come

Chart: https://pbs.twimg.com/media/DQUPWzaV4AANeKj.jpg

RBN Energy Blog https://rbnenergy.com/daily-energy-post

I guess that these new gas pipelines could keep natural gas prices steady this winter?

Nov 8th – Marcellus/Utica natural gas production volumes this past Saturday (November 4) set a record high of more than 23 Bcf/d, according to pipeline flow data. As a result, overall Northeast production flows on the same day also posted a milestone, with volumes approaching a record 25.3 Bcf/d. This is up ~2.7 Bcf/d from where they started the year. These gains have been made possible because of the numerous pipeline projects that have added takeaway capacity from the region, about 2.4 Bcf/d since last winter alone. Moreover, another ~4.3 Bcf/d in new takeaway capacity either was approved for in-service last week or is expected online before March 2018.

https://rbnenergy.com/fill-me-up-buttercup-northeast-gas-pipeline-takeaway-capacity-set-to-balloon-this-winter

The 3 big feeder laterals into the Rover pipeline – Seneca, Berne, and Clarington – are complete and are awaiting FERC approval to add almost 2 Bcfd more into the mainline.

Approval is expected any day.

Several of the other pipelines and expansions are not particularly long.

If not by winter’s end, then by mid to the end of 2018, there should be significant increase in capacity.

Cove Point’s LNG plant is liquifying gas this week.

According to your data there is only 6 years of production left in the GOM at the current production rate – not much. They need a lot of discoveries, or at least making lots of the “propable” reserves real.

There’s about one to two billion discovered but not yet at FID in December 2015, which will extend things a bit longer (e.g.Vito, Appomattox, Anchor).

George,

Regarding your graph titled “Selected Fields Original Field C&C Reserve Evolution” – this represents, I believe, BOEM’s evolution of their best estimate of the “most likely” ultimate recovery from the selected fields as of 1/1/16.

There are quite a few fields on that graph where I believe BOEM is underestimating the most likely recovery.

Atlantis has already produced over 300 mmbo. According to the chart, it should only produce any 30-40 mmbo, which I find hard to believe, especially since they have recently sanctioned another project based on the “200 mmbo of resources” recently uncovered by Full Waveform Inversion, and is still producing 80-90 mbopd.

The Mad Dog 2 project was recently sanctioned, which, if project scope means anything, should be a 500 mmbo or larger project – in addition to the existing production. (Mad Dog total production is already at the total shown on the chart).

Shenzi, Great White, and both Thunderhorse and THN will ultimately, I believe, exceed BOEM’s 1/1/16 estimates as well.

While I know BOEM’s data is thought to be the best data to make projections about future deepwater GOM production and ultimate recovery, I would use it with caution.

Hi SoLaGeo and George Kaplan,

What do you guys think bout the EIA’s STEO for the GOM? Is their projection reasonable? If not, how much too low or too high is it, 5%, 10%?

I can never seem to find the offshore GOM STEO on the EIA website, but in the past they have always been too high. I have one old projection (maybe from late last year or so) where they project GOM production at the end of 2017 to be around 1.9 mmbo. October will be down because of Hurr. Nate, but I think November and December will be 1.65-1.75 – so that would suggest EIA is about 10% too high, but, again, I’m sure they have more recent STEOs than what I’m referencing.

Hi SouthLaGeo,

Thanks.

I use https://www.eia.gov/outlooks/steo/query/

Chart below has STEO forecast from Oct 2017 to Dec 2018.

The Dec 2017 estimate is 1.73 Mb/d, the average output in 2018 is 1.76 Mb/d.

Thanks Dennis,

I was almost there in my search, just didn’t dig down deeply enough.

I think the issue a number of us have had with EIA GOM STEO is seeing enough near-term projects to not only offset decline but increase total production. My estimate is that 2017 production will average about 1.68 mmbo or so. I can’t see 2018 production getting to much over that – I would probably say between 1.65 and 1.70.

I think I’d go a bit lower than SLG. From last year I estimated a minimum around 1450 on known fields and plans. I think there are about 80 to 120 kbpd additions from new discoveries or accelerated development compared to my guess, plus maybe another 20 to 50 immediate discovery to production if this year is repeated. But a bigger unknown might be whether Shell can keep Mars on plateau or even still increasing. I expected it to decline slightly last year but it had a fairly big rise, trouble is there’s no real information to base a guess on until the BOEM reserves come out (and then still a year behind). On the other hand Hopkins and Stampede are smaller than I had estimated and some of the newer fields look like they are ready to start accelerated decline. The time to get Enchilada fully back on line will factor into the average annual as well.

Thanks SLG and GK.

For the 1.67 Mb/d estimate, the STEO is about 5% higher and perhaps GK would guess about 10% lower (a guess on GK’s guess as I don’t know how much a “bit” is) 🙂

I have no clue as I follow GOM output much less closely than either of you.

The data is for December 2015, there should be more for 2016 in January. They publish reserves and production to date and, and none I saw left a negative. The numbers do not include fields with known reseorces but no FID for their development. I think Mad Dog was down as the extra couldn’t be produced through the existing structure and the FID for Mad Dog II hadn’t been approved in 2015. Similarly the new Atalntis find wasn’t known. Shenzi has had a couple of additional near field discoveries or growth, but BHP are expecting significant decline next year. I kind of hinted at that above: “Thunder Horse, Atlantis and Mad Dog all have extensive brownfield work just completed or in development so some of these reserve downgrades may reappear”.

ps have you heard anything on expected schedule for repairs to Enchilada and current status for issue on the Delta House subsea failure?

Sorry, I missed your “extensive brownfield work “comments – typical of my “ready – fire – aim” mentality.

Don’t have any insights yet into the Enchilada or Delta House issues either.

2017-12-06 Venezuela is planning to load 1.34 million barrels a day of crude this month (December), according to a preliminary loading program obtained by Bloomberg.

2017-12-02 Venezuela loaded 1.25 million b/d crude oil in November (-12% m/m), the lowest this year – Bloomberg

I doubt the Senate version of tax reform will survive the House, but if it does, will these same issues affect gas and oil producers, too?

“For coal companies, it could be a double-whammy. It would preserve the Alternative Minimum Tax (AMT) and impose new limits on the interest payments that businesses can write off. Murray Energy estimates that these changes would raise its tax bill by $60 million per year.”

https://www.msn.com/en-us/money/companies/coal-ceo-senate-tax-plan-wipes-us-out/ar-BBGifbl?li=BBnb7Kz

I thought the draw this week was tremendous, the market didn’t like a gasoline build. Including SPR total crude was down by 8.1. Total crude (including SPR) plus all stocks were down by 5 million barrels. Exports about the same as last week at close to 1.4 million a day.

I don’t understand all this fuss about US storage build influencing the global oil price that much.

It’s only one market, it is not accurate – but it’s a simple number. It’s a bit like of trying to get the BIP of the USA by watching one walmart center very closely, and getting in panic when toilet paper doesn’t sell good this week.

Gasoline build? Compare it with the sale on 1000 widely clustered gas stations in the USA to give this number any credibility. Stock build? There are so much giant tankers underway, paperwork doesn’t get finished at Friday and will continue Monday.. weekly data is just white noise, only if you step 3 meters back and see only months, and worldwide storages you’ll get a picture.

But this data isn’t easy available.

Yeah, I think Perry had it right the first time, even if he couldn’t remember the name. Even non-paid members of this board get it closer than they do. It basically shouldn’t exist, except for nuclear purposes. With their track record with tracking oil, then the nuclear part really worries me.

https://oilprice.com/Energy/Crude-Oil/The-GOP-Tax-Bill-Is-A-Big-Win-For-US-Oil-And-Gas.html

?

Ok, Dennis, I got the file. Major pain the first time, but probably much easier in the future. Has all the way back to 2005. Massive file. Once I was able to input the right delimiter, it converted fine into excel, and sorting by year and month was easy. I still think we are missing one element, and that is the unposted condensate, plus there is still an amount of unreported, obviously, from looking at it. Just not as much unreported as first thought.

Just to check it out, I took the initial production from January (oil and condensate) which was 83,276,123 and added the total of pending leases from January of 6,967,538, getting 90,243,661. RRC total now is 96,970,419. EIA has 99,262,000.

September initial production was 76,578,264, and the pending lease total was 13,485,897, giving 90,064,161 total initial. Pretty comparable to January production. So, it’s not up or down much, it’s flat from January. My guess is EIA is about 350k a day overstated for Sept. monthly, and over 650k a day on their weekly. If you will give me your email, I can send the file.

Thanks Guym.

I would expect for January the RRC plus pending lease data should match with the drilling info data.

Maybe it’s the missing condensate data?

For Jan 2017 drilling info has 3196 kb/d, EIA has 3202 kb/d, your estimate is 3128 kb/d, is there a pending lease file for gas wells? This might give you the missing condensate.

If my email to you does not get through I can be contacted at [email protected]

I tried to contact you, but the email listed didn’t work.

It has the gas info, too. I’d say the pending data file does not include condensate, it only lists liquids. In the production queries, you can get oil and gas info, but condensate data is not available. My guess is the pending info is comparable to the queries. However, there is only a one million barrel a month difference between the original reporting of condensate to what is now reported, so late reporting had to amount to about 5 million. There are two files, one is the name of the lease and other info, the other is production. I am sure you only need the production file, but if you want the other I will send it. I haven’t done any work on it yet, so it looks pretty messy.

Send both if you don’t mind, I am trying to reconcile the difference between your January estimate and the drilling info data. My understanding was that drilling info gets there data from a combination of RRC online query and pending lease data, but maybe I am missing something.

Got your email sorted I think. Not sure if it’s the one you use though.

It may be true that it is a combination of online queries and pending data. But the issue may be in the timing of the queries. Maybe, a month or so after the RRC issues initial data, most of the late reporting has happened. I have noticed an unusual spike before, when RRC was late over a week in releasing data?

I will go back and look at 2017, of which I have kept both the initial oil and condensates for to see if there are any trends. I can get initial oil for 2016, but have few numbers of condensate that I have kept for initial production for 2016.

To me, what I received was not useless for $10 and a little time. It confirms that production was not dropping as severe as first glance at initial production figures. So, I was wrong, there. It just has not confirmed your expectation of an increase, yet.

There is one more possibility with it, as a comparison to when October’s numbers are out, and a new Sept total is posted, I just don’t know if my excel programming skills are up to it.

Unless, you are cleared with the RRC to do so, robotic online queries are not supposed to be possible. There is a limit, also, of how much data you can pull up manually.

Hi Guym,

I ignore weekly data. I still think EIA estimate for Sept is about 75 kb/d too high, in the past the 914 survey has been about 340 kb/d below drilling info estimate (for most months from July 2016 to June 2017). Possible it was different in Sept, time will tell. Looks like for the current month about 500 kb/d is missing from RRC data (including pending lease data), if my guess for Sept of 3500 kb/d is correct.

Your belief is in EIA data being consistent, but I think this one of the months they will need to adjust later. There is something missing for January, and it may be late reporting. My first guess is that there is some operator/owners who may late report as there are no royalties to pay, hence no liability. Probably, there is some delay on brand new wells (month and a half, or so), as first royalties have almost a three month lag. But, we are down to a lower amount to scratch our heads over.

I sent a file, let me know if you don’t get it.

i estimated the difference would be about the same as January, which was about 6 million barrels a month. To get to your figure, you would have to estimate another 9 million barrels a month were missing, yet.

I thought I might show you guys where all the stupid (according to ron) live;

https://www.citylab.com/equity/2017/04/is-this-the-ultimate-2016-presidential-election-map/521622/

please forgive me if I posted in the wrong area, after all I am stupid and I am sure Ron and all his “gentlemen” friends would agree and forgive me?. Ohh and to cover my bases: oil and gas are good, the more the better

According to this article, any company wanting to sell cars in China must be focused on EVs.

https://www.nytimes.com/2017/12/05/business/ford-china-electric-cars.html

If you can’t read the article, here is a summary.

http://www.carscoops.com/2017/12/ford-confident-china-will-lead-ev.html

And this.

https://www.ft.com/content/3fe38e12-d9c9-11e7-a039-c64b1c09b482

Grid charged EVs in China will be using power generated mainly from FF burning.

2016 statistics, from:

https://blog.energybrainpool.com/en/power-statistics-china-2016-huge-growth-of-renewables-amidst-thermal-based-generation/

Coal 64%

Gas and other thermal 8%

Nuclear 3.5%

Hydro 19%

Wind 4%

Solar 1%

Not especially ‘green’, but reducing emissions in towns and cities.

Lots of announced plans for EVs.

I have a plan to buy bitcoin two years ago.

EV engines are four times as efficient as ICEs on average. So yes fossil fuels but a quarter the amount.

It’s true that electric motors are mostly in the ninety percent range in efficiency, but this is a misleading fact. A coal plant, even a new one, is less fifty percent efficient, so that effectively more than halves the true overall energy efficiency of electric cars, in terms of emitted air pollution, if the juice is coal sourced.

There are lots of other factors to be considered as well, such as transmission losses, and emissions produced in the process of manufacturing an electric car, etc, but painting fast with a broad brush, electric cars have the potential to halve air pollution per car even if the juice is sourced from a new coal plant.

The thing to remember is that China is run by people who take the long view. The long view is embedded in the culture, and has survived right thru history, including the pure commie era, and is alive and well.

The Chinese leadership doesn’t want to spend good hard cash on imported coal, or anything else, unnecessarily, and it does want to export out the ying yang, and it understands depletion. Exports include wind and solar infrastructure and expertise and services.

So they’re pedal to the metal on wind power, and putting in solar too.

Later on that one percent solar figure going into charging electric cars, if it’s accurate , will be four or five percent, and wind will be thirty or forty percent, and some time after that…… If the new paradigm of mostly or all renewable energy economy survives and thrives, the Chinese will be getting eighty maybe even ninety percent of the juice they need to run cars and light trucks, and trains as well , from the world’s largest by a country mile installed capacity wind and solar capacity.

I haven’t heard much about their capacity to build pumped storage facilities, but considering that they are willing to sacrifice men, money, and environment to whip poverty and morph into a fully modern country, I expect they will be building pumped storage out the ying yang, even if it costs an arm and a leg, in Western terms.

Once that pumped storage is in place, and a few tens of millions of electric cars and trucks are hooked into a Chinese smart grid, they can go whole hog on even MORE wind and solarpower.

We Yankees, other than scientists and a few people such as hang out in forums such as this one, don’t understand the long term. We’re little kids by comparison.

Most Europeans have the necessary cultural heritage, but a hell of a lot of them have forgotten it, if they ever bothered to learn about it.

Think of the Chinese allowing all the pollution, the unsafe working conditions, etc, they allow now, and then consider their REAL SITUATION.

Think of the leadership as generals in the field, fighting a war, knowing that if they don’t WIN it within a given period of time, they WILL LOSE IT.

The smarter members of this forum understand depletion, they understand overshoot, they understand the consequences of overshoot.

If they stop to think about it, I believe they will agree that the Chinese leadership understands these things too, and is fighting like hell, like generals in the field, to modernize their country while IT’S STILL POSSIBLE to do so, and that they are sacrificing some people and some portions of their environment in the process just like generals necessarily sacrifice some of their men and equipment in battles.

When coal and oil and gas get to be so scarce as to become prohibitively expensive, the Chinese will be as far along in the transition to renewable energy as any other country in the world, barring a few postage stamp sized countries lucky enough to have almost unlimited hydro potential or geothermal potential, etc.

Now I realize this comment sounds like a choir boy praising his preacher, in a sense, and that the people running China are hard nosed sob’s out as much or more for themselves, personally than they are for their country. But then so’s HRC for instance. This doesn’t mean that she wouldn’t have done a lot of things good for the USA if she had been smart enough to beat Trump. Trumps’s out for himself and his buddies too, but even so, he is doing some things, or tryin to, that HE THINKS are good for the USA….. the fact that he’s generally wrong about what’s good for the USA doesn’t invalidate my argument.

The reduction in emissions will show up more and more as China builds out the nation’s domestic wind and solar power industries.

There’s no better way to cut back on both emissions and the purchase of imported oil than the combo of renewable electricity and electric cars. The Chinese government has made it clear it will do whatever it can to reduce the expense of importing oil, and there’s no better way to make good use of the fluctuating production of wind and solar electricity than to use it to charge up batteries, if enough batteries are available to be charged. When electric cars start selling by the millions per year……….. China is going to be saving a hell of a lot of money on imported oil.

It’s a classic two for one, too good to turn it down deal. Renewable electricity and electric cars ( and light trucks, city buses, etc, as well )

Mr. Kaplan

Thank you for your interesting article. Roger Blanchard published an article in January 7, 2013 http://www.resilience.org/stories/2013-01-17/aspo-commentary-us-doe-eia-forecast-estimates-face-reality/ as during 2012 the EIA claimed that GOM production will be 1.93 mill bbl/d in Dec 2017 (amongst the claim that US production will be higher than Saudi production in 2017). Furthermore the AEO 2010 estimated that GOM production will go over 2 mill bbl/d beyond 2020 and reach 2,35 mill bbl/d in 2035, which is according to your article unrealistic. The low drilling activity alone suggests that such an outburst of production is not possible.

Blanchard challenged this forecast and predicted basically exactly what you have presented in your publication. He also predicted that Eagle Ford and Bakken will peak in 2014 +/- 1 year, which so far is also correct. This is just an example how irresponsibly EIA and IEA play with public opinion as many investors believed these organisations.

This is a very long and a very good article but it is behind a Wall Street Journal paywall.

Wall Street Tells Frackers to Stop Counting Barrels, Start Making Profits

The shale-oil revolution produces lots of oil but not enough upside for investors.

Twelve major shareholders in U.S. shale-oil-and-gas producers met this September in a Midtown Manhattan high-rise with a view of Times Square to discuss a common goal, getting those frackers to make money for a change. In the months since, shareholders have put the screws to shale executives in ways that are changing the financial calculus of hydraulic fracturing and could ripple through the global oil market. In the past decade, the shale-fracking revolution has made the U.S. the world’s largest oil-and-gas producer and reshaped markets. Yet shale has been a lousy bet for most investors. Since 2007, shares in an index of U.S. producers have fallen 31%, according to data provider FactSet, while the S&P 500 rose 80%. Energy companies in that time have spent $280 billion more than they generated from operations on shale investments, according to advisory firm Evercore ISI.

SNIP

Thirty companies produce about 70% of U.S. shale oil, according to energy consulting firm Wood Mackenzie. If shareholders could prod most into focusing on profitable drilling, it might also have the side benefit of achieving what the Organization of the Petroleum Exporting Countries, the global oil cartel, couldn’t accomplish—getting shale companies to help shrink oil supplies and boost prices.

An appropriate sentiment for the shareholders’ benefit. As for decreasing shale production, it has the same benefit of closing the barn doors after all the animals have run out of the building.

Ron,

However, I have the impression that this article has been just published for soothing the nerves of investors. In reality just yesterday, the shares of many once proud and strong companies (RRC, CHK, WLL….) fell closely to their all time lows. Having sacrified themselves and their shareholders, they are nearly empty shells with depleted assets and high debt and little value.

Many investors just realized that now as the oil price is actually reasonably high and many shareholders thought their shares will soar as well. In fact, the ratio of stock price and underlying oil priced slumped to all time lows for many companies leaving many shareholders realizing they are holding the bag for the shale miracle and they will never see their money again. Of course, Wall Street has to pretend that they will do something. However, they are very likely to keep on going to keep oil and gas cheap and well supplied – at the expense of investors.

And isn’t it a great time to expand Alaska drilling. Companies can’t make money now, so they are expected to bid up leases there.

Baker Hughes international rig count for November: http://phx.corporate-ir.net/phoenix.zhtml?c=79687&p=irol-rigcountsintl

Total rigs down 9, offshore down 21 to 183 (lowest since 2000), land up 12. Oil up 7, gas down 11, misc down 5. Norway dropped 3 – I think maybe as Barents Sea drilling stops for Summer. China and Saudi also down. Indonesia added 5 onshore. Mexico dropped two offshore one land and are at all time low (as recent as 2010 they had 100 land and 25 offshore now 1 and 8).

It would be interesting to know how many of the offshore rigs are MODUs (i.e. to some extent discretionary) and how many on production platforms (fairly cheap tp run on an opportunity basis or committed to drilling on recent start-ups) but that costs money I think (e.g. from Wood Mac).

https://www.chevron.com/stories/chevron-announces-18-3-billion-capital-and-exploratory-budget-for-2018

“Our 2018 budget is down for the fourth consecutive year, reflecting project completions, improved efficiencies, and investment high-grading,” said Chairman and CEO John Watson. “We’re fully funding our advantaged Permian Basin position and dedicating approximately three-quarters of our spend to projects that are expected to realize cash flow within two years.”

Few to no long term developments even as the oil price steadily rises.

Yeah, but when it gets past $90, we will soon be reminded that tigers do not change their stripes. It’s still the oil bidness.

ALASKAN OIL LEASE SALE BRINGS FEW BIDS DESPITE VAST TERRITORY OFFERED

https://www.reuters.com/article/us-usa-alaska-oil/alaskan-oil-lease-sale-brings-few-bids-despite-vast-territory-offered-idUSKBN1E109Q

An oil-and-gas lease sale that raised concerns with environmentalists due to the vast amount of acres offered in Arctic Alaska drew few bids on Wednesday, government officials said.

Seven bids were received, covering about 80,000 acres – or less than 1 percent of the 10.3 million acres offered in the National Petroleum Reserve in Alaska by the Trump administration.

…

ConocoPhillips Alaska Inc, in partnership with Anadarko Petroleum Corp, submitted the seven bids, totaling $1.16 million.

I’d say that counts as an abject failure.

$14.50 an acre. Big spenders.

Yeah. As if there is going to be huge demand for ANWR. This administration appears not to have much of a coherent energy policy.

Unlike a ANWR, NPRA had some exploratory drilling just a few years ago. I think somewhere in the archives of this blog the matter was discussed.

It was reasonably big news the reserves estimate crashed something like 95% or more as a result of the exploratory drilling showing nothing.

That should sort of render this a non-event

US – update through August 2017 – Enno Peters

https://shaleprofile.com

well look…another super major adding to US LTO budget. I suppose they can’t do math or engineering either just like the rest of us, right mike? Steve do you have some expert commentary about ponzi schemes or super secret, only you know information, maybe you should send to them and try save their foolish shareholders.

https://oilprice.com/Latest-Energy-News/World-News/Chevron-Cuts-Total-2018-Capex-Boosts-US-Shale-Investment.html

TT.

Chevron has been losing money on US upstream during the entire bust.

Chevron cut upstream CAPEX overall, I would note.

I suspect the idea is that, despite little to no profit margin, Shale is much less risky than other world wide upstream investments, given great price and political risk.

I have read some recent articles about shale needing discipline, panic in the Permian, etc.

I am holding to my prediction, shale and the inability to reign it in will keep prices low till it is mostly drilled through. I am just hoping “low” is $55-65 WTI and not sub $50 WTI.

I see CLR is offering 4 3/8% notes due 2028. $1 cool billion worth.

Ss i know you know this but it should be said… just about everybody in the oil business gets hurt with sub $70 oil, even you guys with wells paid for and no drilling budget barely make it at $60.

Now, apparently folks like me, who have been in the business for 35 years, who have drilled 100’s of wells in several states and who has the capacity and foresight to not only understand the direction the industry will go but why, is mocked, which is fine, I am laughing all the way to the bank rather then complaining…just saying

I am a bit more optimistic than you with regard to prices but I was surprised at the recent collapse of nat gas, hell it’s snowing down here in texas where i live, that is about a 1 in 10 year event

Tee tee, Chevron is losing money hand over fist; almost everyone is these days that is actually IN the oil business and not a royalty owner getting money free and clear of all costs. These big integrated majors are flocking to shale plays because, drum roll please…there is not very much else left for them to do. And they don’t have to look for anything, thankfully, because they can’t find anything anyway; they can just go out almost anywhere, slam holes in the ground and start cramming sand into them. Pretty much anybody can do that. Chevron, by the way, has the leg up on a lot of PB operators because they actually own a lot of the minerals under their enormous acreage blocks. Get somebody to explain to you how much 25% royalty burdens diminish the economics of a well.

And as to shareholders, get somebody to read you this. Ask them to read very slowly and be prepared to repeat often: https://www.wsj.com/article_email/wall-streets-fracking-frenzy-runs-dry-as-profits-fail-to-materialize-1512577420-lMyQjAxMTA3OTAzNzQwNDcyWj/

there is being wrong and then there is Mike who takes being wrong to an olympic level not saying gold medal but he will damn sure place?

https://oilprice.com/Energy/Crude-Oil/US-Shale-Cautious-As-Oil-Majors-Invade-Texas.html

https://oilprice.com/Energy/Energy-General/Why-Isnt-Wall-St-Backing-The-Next-Shale-Boom.html

put me down with this guy

I hope that guy is correct. Seems like everyone assumes the shale companies can grow production big time, and really they have since the 2016 monthly lows, so not so sure this guy is correct.

If demand hits 100 million BOPD worldwide by Q4 2018, and then grows another 1.5 million for a few more years thereafter, I’d say there could be a supply crunch.

I am still waiting to see Tesla number two in my county of 20K people. I suspect I will keep waiting. My friend who owns the only one I am aware of still owns three gasoline powered vehicles as well.

4,000 single family residences’ electric demand = what it takes to fully charge one Tesla semi (that won’t be built for years) and 3.3 acres of solar panels in Phoenix, AZ to provide the electricity to daily charge that one Tesla semi.

Have to be an eternal optimist if you own oil wells and grow grain.

An ordinary Semi would suck a stripper well dry alone – feeding these big trucks costs a lot of energy, they need about 0.2 to 0.3 barrels / hour.

I didn’t look at this charging thing, but everything that counts is the total energy consumption. A big charging station at the interstate will charge one after the other, they’ll just need a middle sized connection to the grid in future, so as today they receive several arrivals of gas trucks they suck dry.

Tesla has stated that they want to buffer the spike demand of that charging to the grid with stationary batteries at the gas station.

Nothing is for free.

100? Beyond even India’s consumption growth rate.

The guy that wrote this dumb article is a former Hess employee, also on the ropes, who connects Wall Street money to the shale oil industry. “It only takes a few Wall Street firms recommending rotation into the energy sector and “The Herd” will follow.” He is part of the herd. He wrote this article to counter the Wall Street article suggesting that shareholders, that actually own the company, have had enough of fiscal irresponsibility and are starting to say, loudly…sho’ me the money !!

Wall Street is “backing off” the shale oil industry because it is over $200,000,000,000 in debt and can’t make enough profit, even at $50 oil, and vastly improved productivity, to pay back its indebtedness. Continental Resources is a perfect example of that; its long term debt increased YOY. It is a train wreck.

I am astounded at how few people understand the “business” of oil extraction, that focus only on data and a handful of “super hog” wells but have never even bothered to look at a Q, or a K, that do not seem to understand that money coming in must exceed money going out for the “business” to be sustainable. One CANNOT ignore well economics and the financial condition of individual corporations, therefore the shale industry as a whole, and believe the shale oil industry is going to grow and take us to the hydrocarbon promised land. The US shale oil industry MUST start making profit, for the first time ever, or, short of direct government intervention and financial help, more subsidies, growing the national debt, it is in big trouble.

What’s the big deal about that? That’s the oil business; ideas come and go, “plays” come and go, companies come and go. Fields and wells come on line in a roar, then they deplete in a whimper. Its been that way for over a 125 years. There is nothing “special” about using old technology to squeeze oil out of a tight, shalely resource rock and time is proving, will ultimately prove, that it could not be done economically. Its not big deal. Good grief; that’s the way it works.

Lying about it all, on the other hand, for personal reasons, to make personal money, to promote a personal agenda IS a big deal. Its deceiving the American public about its energy future.

There is a difference between shale oil and the 125 years of oil business: In most times, companies made tons of money when an oil boom started somewhere.

Standard oil wasn’t without reason the most valuable companie of it’s time – not because of windy wallstreet constructs, but through making big profits.

And gulf oil is about making money, too, not burning money.

Only in shale oil they never got the trick of making money after the first investments.

Big oil is in big trouble, too – most good fields are in state owned company hand, the free leases and fields are scare now.

Wonder why it took so long for Wall Street to catch on to shale lack of profit, without very high oil prices? Of course, I am posting this jest.

Was looking at OXY Statistics. Trailing P/E of 100. Borrowing to pay dividends still.

I feel pretty good right now, at $57 WTI. Doesn’t look like OXY does so good at $57 WTI, small profits, much worse than 15 years ago at $25 WTI.

It is getting really expensive to get this oily stuff out of the ground. 30% increases in service costs year over year in the shale fields, and the service companies are still not making money.

Wouldn’t it be something if some of these guys start losing $$ on EPS at $57 WTI? Or some, like Hess and Whiting, can’t get over the hump at $57 WTI?

what you call a lie, most reasonable people would call a difference of opinion. Now when those opinions come from people properly educated in their field, with decades of actual experience they are anyting but lies and would be better characterized as informed opinions, not lies. I will also note that upon the release of the CLR earnings, the details of which were discuss above, the stock went UP. So who is lying, the market or you, relating to the interpretation of those facts.

The facts are the world will not invest in new production at a level required to supply future needs because the “world in general” can not compete with US shale. The US Shale will be developed, the cost will come down as all land, acquisition, seismic and infrastructure have been expensed and only the development well cost are left. If you can’t compete with that, or find some way to be involved in that, you will be left behind, that is no lie and you can take that to the bank.

https://oilprice.com/Energy/Energy-General/Are-US-Shale-Stocks-Finally-Set-For-A-Rebound.html

love it when a plan comes together

Nobody is lying here. I am pulling information right off of the 10Q for CLR.

It can be difficult to wrap your head around valuations when the numbers are in the billions, so maybe we should divide by 1,000 to discuss CLR.

The market is telling us that a company which has $10,000 cash in the bank, earned $10,000 in the most recent three months, lost $53,000 in the most recent nine months, owes $6,600,000, and has $660,000 in accounts payable has assets that have a fair market value of $24,600,000.

Yes, $660,000 in accounts payable with just $10,000 cash in the bank. And, to keep production flat needs to invest north of $2,000,000 in CAPEX annually.

Hey, one Bitcoin is valued at $15,629 and Tesla has a market capitalization of $53 billion, with over $20 billion of debt and 14 years of consistent losses.

But, crypto currency, electric cars and shale are all valued on the potential to take over the world, not today’s performance. Been told that repeatedly.

The lecture about the difference in opinions and lies was directed at me, Shallow.

I think that if one looks at factual financial data filed by corporations to the SEC, or looks objectively at realized production data and how that data compares to fictitious, exaggerated EUR’s created by the LTO industry, and can STILL say the US shale oil industry is a success and America is on the path to hydrocarbon independence… one is either dumb, or a liar. My industry has a fiduciary responsibility to tell the truth about the oil and natural gas we have been charged to extract; how much oil is left in America and what its going to cost to get it out of the ground…without increasing the national debt. Clearly, however, that is not a “reasonable” belief.

As to investing in CLR, I’ll stay in the truck on that one:

https://www.macroaxis.com/invest/ratio/CLR–Probability-Of-Bankruptcy

Bubbles. Houses, cars, oil, can be bubbles. Overinflated price. Crypto currency is not even a bubble, it’s more like gas. Smells like it, too.

I agree totally with your statement “no one is lying here”. for the record my only association with CLR is they operate some well for us (yes working interest) but I do following them. I have some issue with CLR mainly with regard to management, so they do not get my investment $$$ but I am heavily invested in the space, as over the last 2.5 years we have not have enough drilling opportunities.

There are some real opportunities out there however for those with even the slightest amount understanding of the transition “my” industry is involving into.

With regard to debt…I made the point years back, debt is everything and debt is nothing at the same time. The amount of wealth tied up in the shale resource plays is enormous, the ripple effect to individual mineral owners, tax agencies at all levels, retail sales in all jurisdictions demands that the resources be development. To not appreciate this and its implications both within our boarders as well as foreign policy advantages , indicates 1st graders understanding our how our economy works and the world in general. If we create some debt to develop these resources we will, take that to the bank.

Bitcoin is a great example of speculative mania. And how money shifts from one bubble to another. Shale is no longer of interest and probably never will be again.

That’s the challenge for LTO companies. There are other places for investors/speculators to put their money and they have realized it and moved on.

“If we create some debt to develop these resources we will, take that to the bank.”

Yeoww ! Now we’re getting somewhere, tee tee, thanks. What I construe that to mean is if folks like you, the direct beneficiaries of the shale phenomena, the free loaders with royalty, free and clear of all costs, the CEO’s*, the Central Banks on down to the private equity providers that borrow from the Central Banks (the America taxpayer) and loan to shale companies and make tens of billions of dollars per year on interest income…if that provides cheap gasoline to the American consumer, by God…your are entitled to that debt. Whether you can pay it back or not. Is that right? That is what you just said. Wow.

What did the WSJ just print, that a handful of shale oil CEO’s* the past 8 years have earned over $2.5B of compensation even though they could not provide a dime of positive free cash flow for their stockholders? They created debt for their own personal benefit, and by golly took that to the bank, didn’t they?

You are an embarrassment to my industry, tee tee. I operate (oil and gas wells) in an environment where borrowing money I cannot pay back is shameful, where not paying my vendors for 120 days at a time is disgusting and a threat to jobs and the people that I need to stay in business. Where letting people go because of my own stupid mistakes is cause to crawl under a rock. You don’t seem to think anything of that. Its nothing to you, as long as you benefit personally.

If “your” new oil industry is good with craping out of $80B of debt, and counting, of hiring people two years on and three years off towers because of fiscal irresponsibility, of owing as much as the entire country of Venezuela owes, and can’t pay back either, of lying to the American public about its hydrocarbon future, you can take “your” industry and shove it up your ass.

Its not my industry.

Texas tea,

One way to look at the performance of any commodity company is the ratio of stock price versus the underlying commodity as the stock price includes all costs and also the judgement about future developments. This shows if a company can create value at any given commodity price. The shape of this curve can give also a glimpse on future development.

Given this ratio, most Shale companies and even the majors see a dramatic fall in this ratio, – despite the recent rise in oil price. There maybe many reasons for this trend, depletion, hedging at too low prices, yet in my view the main reason is that Shale needs now many more wells to achieve the same production as a few years ago. This increases costs per produced barrel, even if the cost per rig is the same. As this trend accelerates exponentially this could be a severe drag on companies ability to generate cash from oil production. Accordingly this will affect financial performance.

Hi SS,

I can remember talking to my maternal grandfather about the first car, and first airplane, and first train he ever laid eyes on, when he was just a kid. None of these things were to be seen in the back of the backwoods around here prior to 1910 or 1915 or so. There were cars in town nearby, but he didn’t see one himself until he was old enough to clearly remember the occasion. Ditto a train. He saw an airplane about the same time or maybe a little later, around 1915 or so , when a barnstormer came thru putting on an airshow or something along that line. Airshows were popular back then, and people would pay a hard earned dime to get a good close look at an airplane.

He owned a car prior to 1930, and a tractor pretty soon after that.

Every body he knew back in his youth was sure the automobile wouldn’t ever amount to anything other than a rich man’s toy.

And being vertically integrated, as economists put it, he was able to “manufacture” his own horses and mules, lol. Tractors required hard cash.

Once upon a time I found a list of the names of oil towns where the oil ran out. It was a very long list. I wish I could find it again.

Looking at CLR 10Q.

Cash of$10,765,000. Was $16,643,000 12/31/2016.

Long term debt of $6,612,281,000. Was $6,577,697,000 12/31/2016.

I believe the little long term debt that has been paid down has been via asset sales.

Q3 earned $10,621,000 or 3 cents per share. First 9 months of 2017 lost $52,467,000 or 14 cents per share.

(So, CLR has 3 cents per share of cash on hand).

They are just refinancing $1 billion of long term debt, it appears.

I would also note accounts payable are up almost $200 million from 9 months earlier.

Have to question if the Bakken and Oklahoma resource plays are a good investment at 2017 commodity price levels. If we were looking at any other business besides US shale (or electric cars) I question whether these numbers would be considered a success.

Wait; mighty Continental Resources, the tower of power, the big cheese, the LTO Kahuna, the Bakken Ayatollah of Rock ‘n Rolla has just enough cash on hand to drill one lousy shale oil well… did I read that correctly? It has over $6.6B of long term debt, $671,000,000 of accounts payable, and only $10M in the bank, waiting on this months checks to come in, living hand to mouth??!! Wow! Now THATS embarrassing. Discount its over exaggerated reserves by 50% and this company meets every definition of the word, insolvent.

Some interesting information on shaleprofile.com regarding CLR Bakken wells. (Unfortunately Enno Peters does not access to OK data).

May, 2015 CLR produced 156,825 BOPD from 1,590 wells.

August, 2016, CLR produced 99,483 BOPD from 1,651 wells.

August 2017, CLR produced 140,174 BOPD from 1,692 wells.

It appears CLR sold some wells between August, 2016 and August, 2017, because of that 140,174 BOPD, 51,532 BOPD or 37% is coming from 105 wells with first production in 2017.

It appears, however, that after the first four years on production, the wells settle out in the 30-40 BOPD range, which does not sound bad. I wonder how many have been re-completed? If none, looks good, if several re-completions, not as good, given the additional CAPEX required.

Want to make clear, I meant to say Enno Peters does not have access to OK production data, at least last I knew.

Hopefully he will at some point. One heck of a website he has built.

Where is Diesel feed source to drill, truck sand, pump. frack, etc?

http://www.zerohedge.com/news/2017-12-07/irresponsible-unwarranted-saudis-condemn-trumps-jerusalem-recognition-warn-serious-c

https://oilprice.com/Latest-Energy-News/World-News/Mexico-Cancels-Deepwater-JV-Tender-Due-To-Lack-Of-Interest.html

Well, George, here’s another one you won’t have to track.

The article identifies the project as Maximino-Nobilis, with project costs of over US $10 billion, reserves/resources in the 500-700 mmboe range, and development costs of $27/barrel. If those numbers are correct, I can see why there was no interest. US deepwater projects are FIDed at development costs maybe in the ~$16-$23/barrel range. (I realize the cost/tax structure is different in Mexico. That probably ends up making the $27/barrel even less economic, though I don’t know for sure. Also, the terms of the farmout that Pemex is offering are not stated, but that, in itself, can only add costs to the potential farmee)

This is one of a number of Perdido fold belt discoveries Pemex has made. BHP is going to jointly develop another one of the discoveries, the Trion project, with Pemex. I’ve never seen a per barrel development cost estimate for Trion.

Maybe shale is too big to fail. What happens then?

Shale is big enough and critical enough to get bailed out, on the taxpayer’s dime, with the bankers getting rich ,personally, and the banks coming out whole.

I don’t often agree with Watcher, but he does makes some very solid points once in a while. He’s right this time , implying that the shale industry will get a bailout if it comes down to that.

Sometimes it takes a person hated on both sides of the politicial aisle to point out the truth. George Wallace, a famous ( infamous I should say I guess ) racist is well known for saying something along the line, paraphrased, as ” there ain’t a dimes worth of difference between them”, referring to the Democrats and Republicans. He was dead wrong and lying about that in respect to civil rights at the time, but he was right on the money in some other respects, such as both parties being controlled by various special interests by way of providing money, air time, newspaper coverage, the various high ranking members of both parties mostly being lawyers and mostly all being very well to do, and having invested money, and money to invest, etc, so all of them were ( and still are, in the main) looking out for themselves as much, and mostly MORE SO, than they are for the country.

So……. neither the D’s nor the R’s have any real interest in straightening out the mess financial mess which to me looks like a black hole that is the shale industry financial appears to be.

Cheap gasoline is good for incumbent politicians, and the thing that scares them most, is that the economy turn sour on them, because that’s the biggest threat to their reelection, whether they’re D or R, either side, it doesn’t matter at all to an incumbent, as a general rule. He wants the economy to hum.

(This of course does not mean the “out’ politicians aren’t happy sometimes when the economy is sour, because that ups the odds in their favor of winning.

There is such a thing as deliberate neglect, and it is often demonstrated by cops and politicians. I’m thinking this concept throws quite a bit of light on the reasons why the shale industry has been able to borrow so much money on such shaky security.

A wink is as good as a nod and a nod is as good as a direct order, if underlings are looking for guidance but the boss doesn’t want to issue explicit orders. Loan officers work according to guidelines approved by higher management, and if higher management has been satisfied with the way money is lent to shale operators, well, individual loan officers are not be held responsible, they document their work and send it upstairs for approval.

Politicians of both parties fully understand that by the time the problems they create are obvious to the voting public, they are more than likely to be dead, or at least safely retired.

I’m not as radical as a couple of other people in this forum, but I have no love for either party. Ya gotta hold them to account. The problem with doing it is that most of us are too apathetic, too ignorant, or just plain too busy to the doing of it.

Baker Hughes US oil rigs +2 week/week to 751, Permian +3, Eagle Ford +3 , Williston -1, Niobrara -2

Natural gas rigs unchanged at 180

The potential for a 1970s type embargo revisited:

https://oilprice.com/Latest-Energy-News/World-News/Malaysia-Suggests-Muslin-Countries-Stop-Trading-Oil-In-US-Dollars.html

Texas Tea.

I put this down here because it got too narrow on me up hole.

Do you borrow money to pay the AFE’s on the shale working interests you own, or do you have a ton of cash?

The reason I ask, is I just think it would be difficult, especially since the 2014 collapse, for a private, non-operated working interest owner to borrow much money from a bank to pay shale PUD AFE’s.

I would be really interested to know how you do this. Are you able to access operator data, such as seismic and engineering?

Also, do you hedge? I would think hedging high decline new wells would be difficult. I would think hedging a non-operated WI in a high density drilling unit would be a real challenge.

I am envisioning a scenario where the price runs up $10 and your high density unit is shut in for three months so some nearby wells can be completed. How do you pay the counterparty on that project hedge when you have no barrels to sell while shut in?

Shale just doesn’t seem to be set up for a smaller non-operated WI owner. Too much money upfront, too little control, and too hard to hedge.

But maybe you have a ton of cash. That’s the only way I can see how you are investing in non-operated shale PUD.

Items

India consumption growth advance look

Passenger vehicle sales April-Aug 2017 up 8.67% over same period 2016.

Two wheel vehicle sales April August 2017 up 10.41% over 2016 same months.

They ain’t slowing down.

Question about Russian Oil

If I calculate Russian oil production from the Russian Oil Minister, using 7.3 barrels per ton and compare that with what the EIA says Russia produces, the Russian Oil Minister data averages about 400 barrels per day above what the EIA says Russia is producing. If I use 7.03 barrels per ton then the numbers match. (Average for the last 5 years.)

How heavy is Russian oil? Does anyone have a number?

Russian Oil Minister data: http://minenergo.gov.ru/en/activity/statistic

EIA Russian Oil data: http://www.eia.gov/beta/MER/index.cfm?tbl=T11.01B#/?f=M (Tabel 11.1b)

I don’t know either, everyone gives a different number.

JODI Data has the Russian Federation crude oil production, conversion factor: barrels/ktons at 7,357

The EIA said back in 2008 that Russia was 7.27 (I’ve not seen a recent number from them).

The news agencies all use 7.33 (The last time that I compared)

Russian crude grades are 30 to 38 which is bbls per tonne of 7.2 to 7.5. 7 bbls/te is API 26 which is pretty heavy, especially if they have a lot of condensate.

https://en.wikipedia.org/wiki/List_of_crude_oil_products.

URAL NWE assay is API 31.78 (Primary export)

34% Kerosene and Diesel , light stuff is only 13%

barrels of oil per tonne –> (API Grav + 131.5) / 22.49) (31.78 + 131.5) / 22.49 = 7.26

Russian refineries capacity 4+ million bpd. Present consumption is less than 4.

Hi Ron,

Using BP data for 2016 (which is C+C+NGL) it was 7.41 barrels per tonne in 2016.

Okay, but we are not talking about NGLs here, we are talking C+C only. That is what OPEC reports, that is what the EIA reports and that is what the Russia Oil Ministry reports. There is no need to muddy the waters even more with “other liquids”, that is “bottled gas”. There is no definite answer here so I am going with 7.3 barrels per ton. Or, if you prefer, metric tonnes.

EDIT: Well no, OPEC uses crude only, no condensate. Sooo…

Hi Ron,

The BP data is all I have for density of Russian oil output. Your estimate of 7.3 b/t is probably close enough.

Baker Hughes International Oil Rig Count (Land + Offshore). This is without the USA or Canada.

An article on ‘well bashing’ – the downside of closely spaced fracs of different ages . Essentially the new fracs tend to frac into the depressurised depleted halo of the old bore’s region of influence, bypassing fresh rock.

http://www.upstreampumping.com/article/well-completion-stimulation/2016/well-bashing-due-asymmetric-fracturing-mitigation

Apologies if its been posted before.

Ian

Just wrote a lengthy response and lost it.

In a nutshell, the protective refracturing seems to be what is going on in the Bakken.

Parent wells are offline 3 to 5 months when 2 to 3 offsets are completed.

When parent well is turned back online, results are regularly astonishingly high, often exceeding original IP.

Info is very scarce on what precisely is going on, but this downspacing issue may be in the process of being successfully addressed.

Ian, if I may; well bashing is not the same as frac communication with wells that have been drilled on too close of spacing and that interfere with each other. Frac bashing is this: https://www.oilystuffblog.com/single-post/2017/09/21/Another-Big-Ol-Frac-Boo-Boo. It is a situation where frac’s travel up, out of zone and harm shallower wells nearby and the correlative rights of the operators that operate them, and the royalty owners that have interest in them. Please ready my comments about frac bashing and decide for yourself if this phenomena is good for the American oil industry and good for America’s oil future. You decide for yourself if this sort of thing is a threat to groundwater.