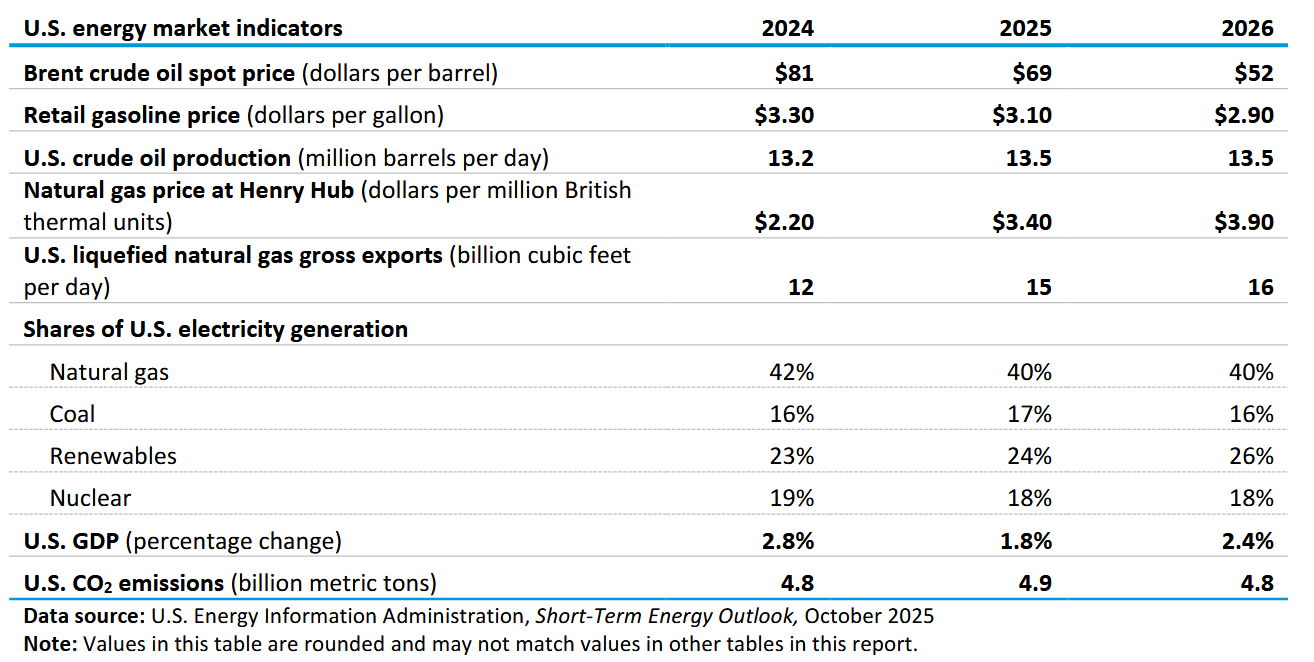

The EIA Short Term Energy Outlook (STEO) was published recently. A summary in chart form.

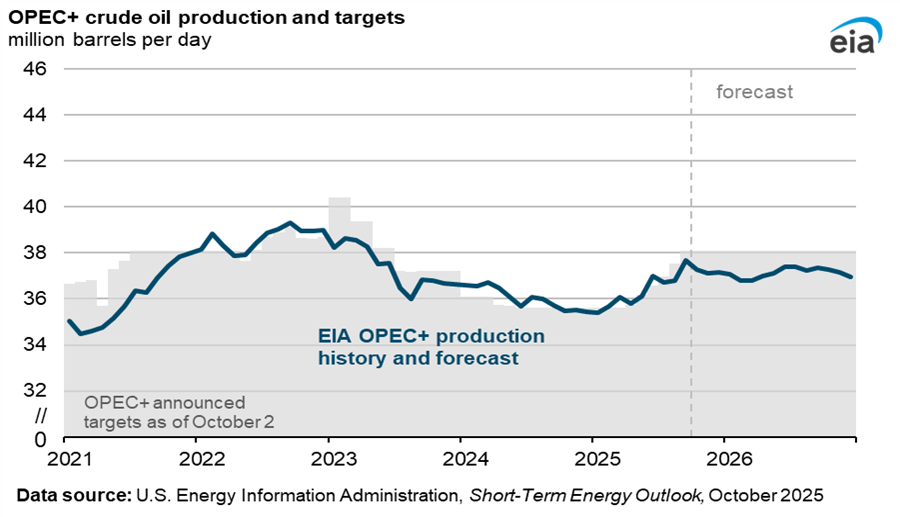

The EIA expects that OPEC+ will fall short of its targets after September 2025.

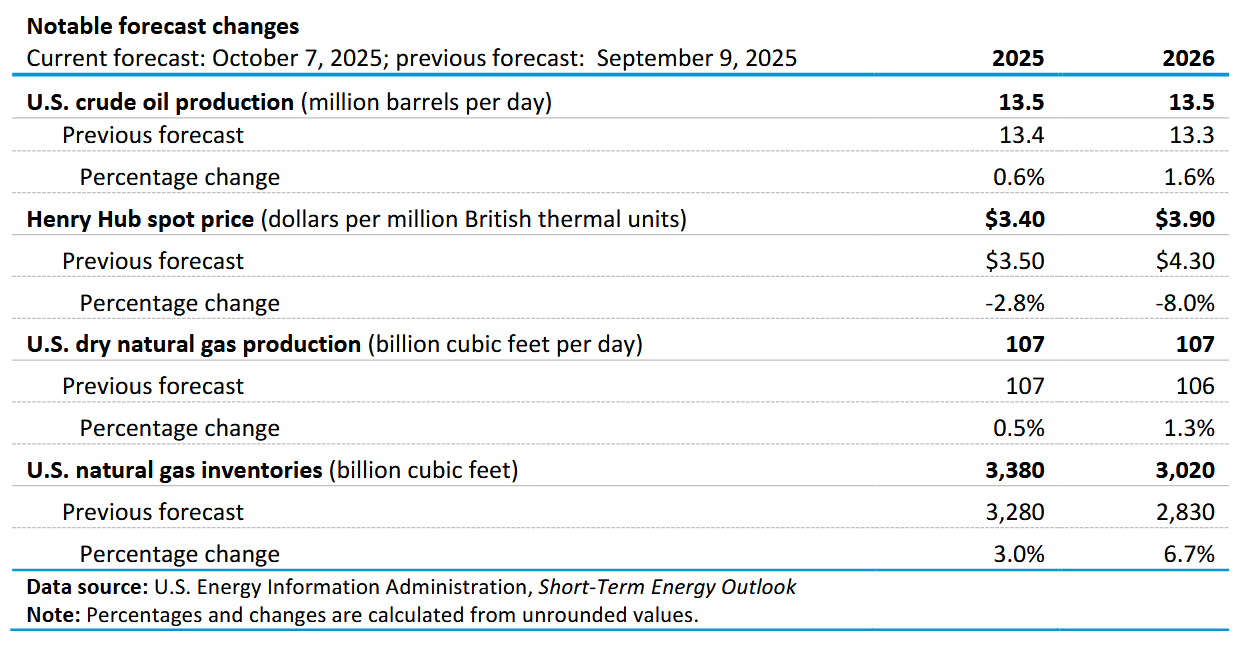

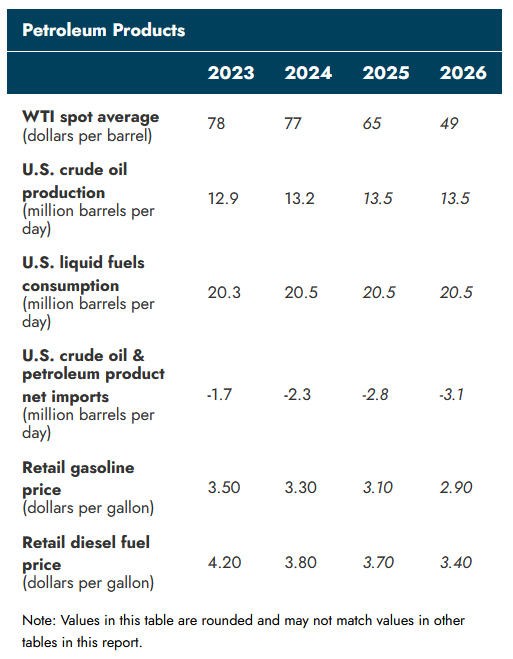

WTI has been revised higher compared to last month’s STEO due to higher expected demand.

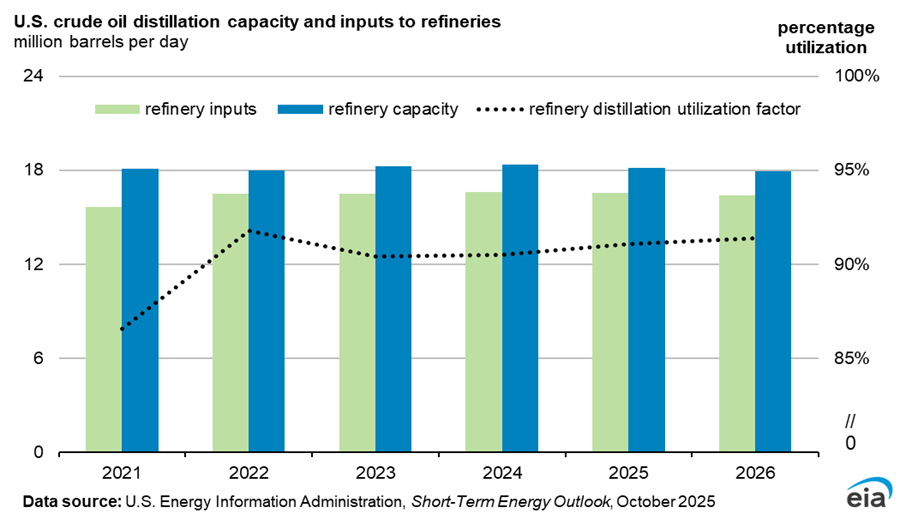

Refinery utilization is expected to increase as west coast refineries are closed.

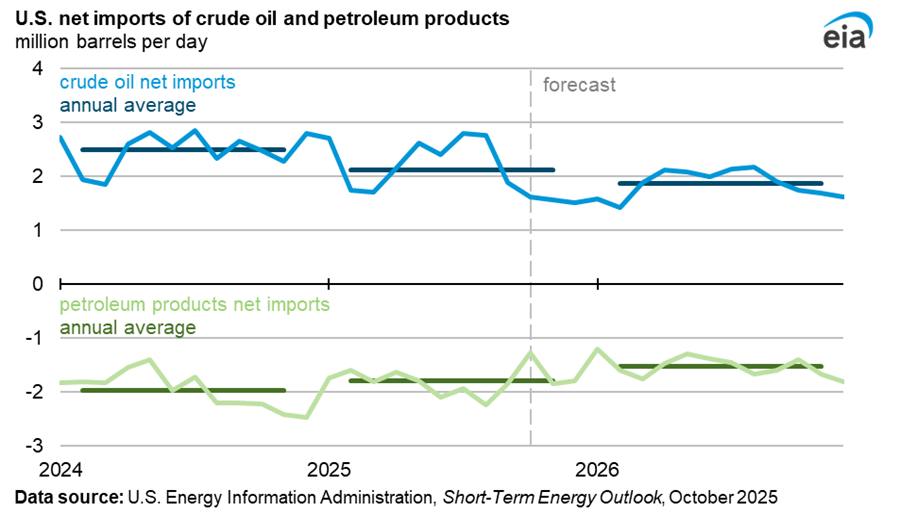

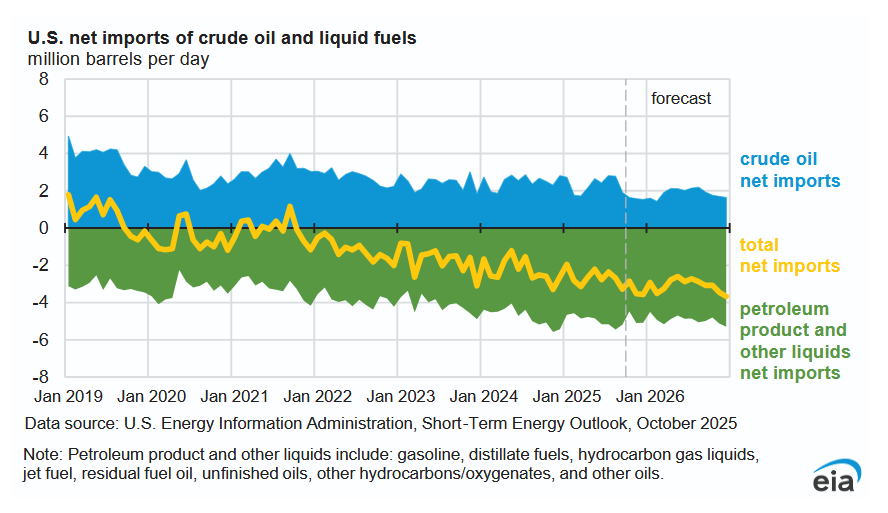

The EIA expects crude builds in the US as refinery inputs fall due to lower refinery capacity, higher net imports of petroleum products are also expected.

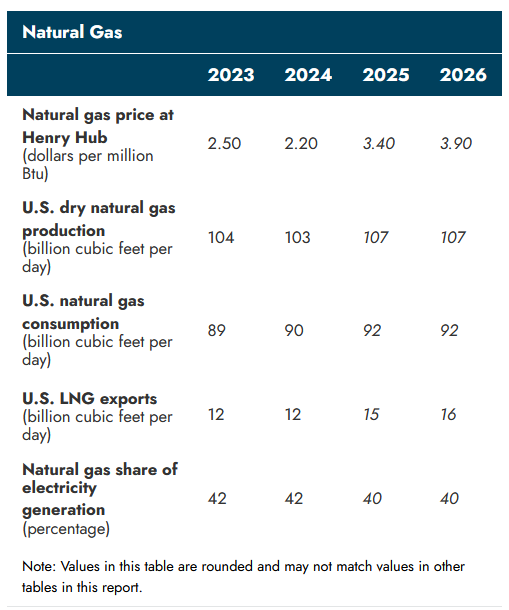

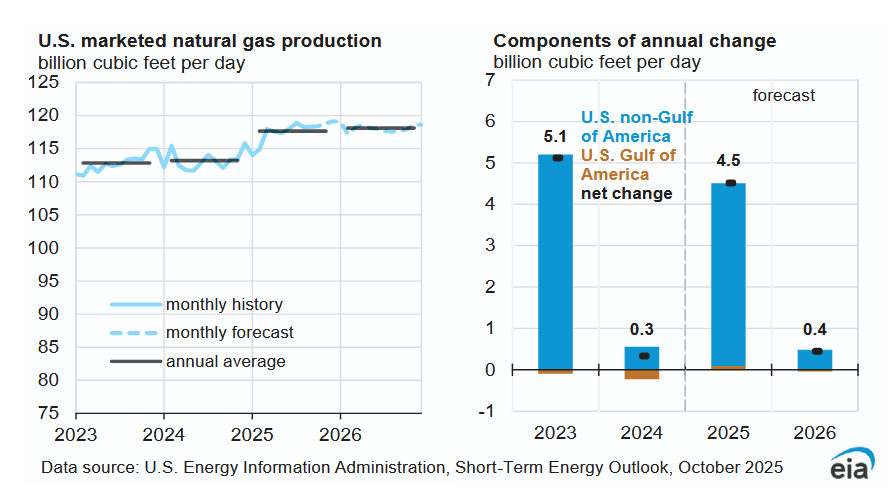

Higher production of natural gas in 2026 than forecast last month leads to a lower natural gas price forecast in 2026.

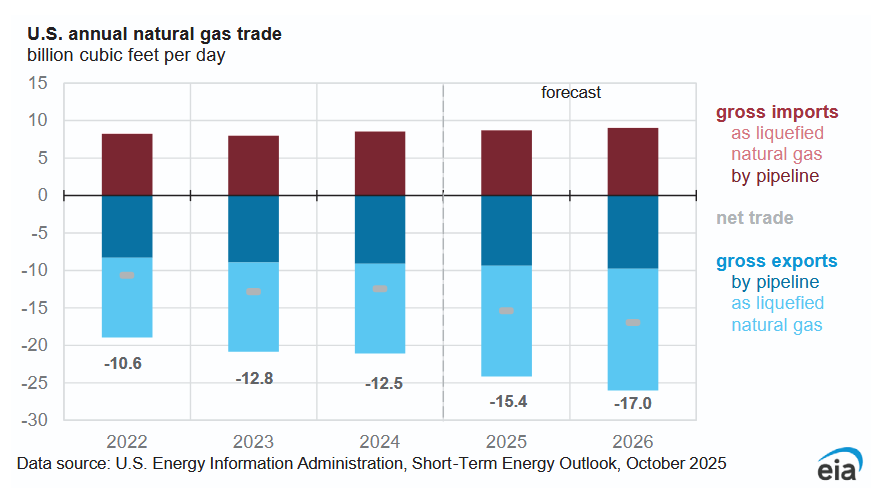

Exports of natural gas are expected to increase by about 4 BCF/d from 2024 to 2026.

From the STEO:

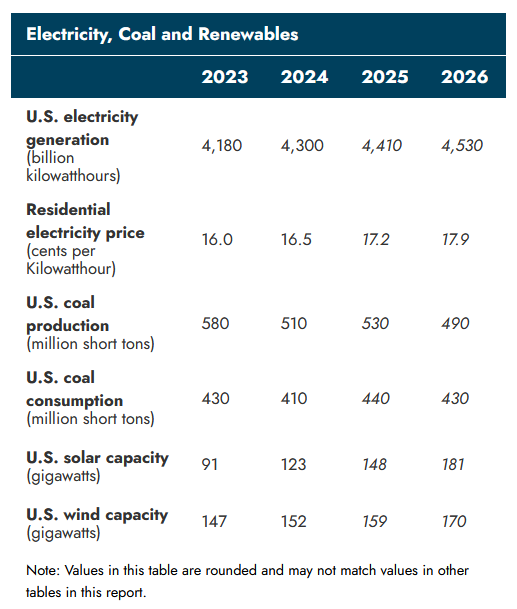

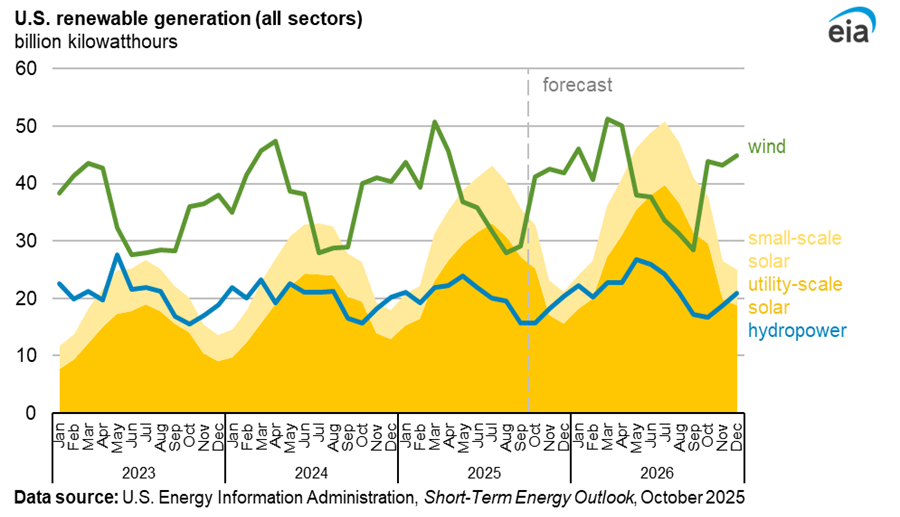

Total solar electricity supply in our forecast is 380 BkWh in 2025, including small-scale solar, while wind generates 470 BkWh. In 2026, we expect solar will generate 17% more electricity than it has this year, approaching 450 BkWh. Wind generates 490 BkWh in our forecast for 2026, 5% more than this year.

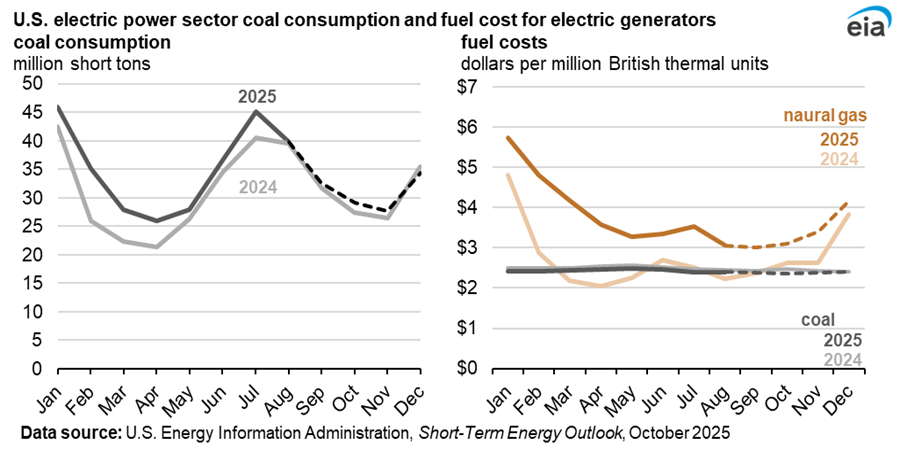

Higher natural gas prices and a cold winter in the Southeast where more electric heat is used resulted in higher coal consumption for electric power in 2025 compared to 2024.

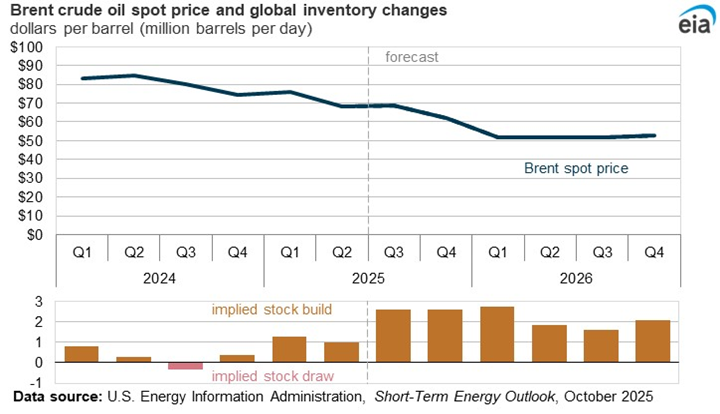

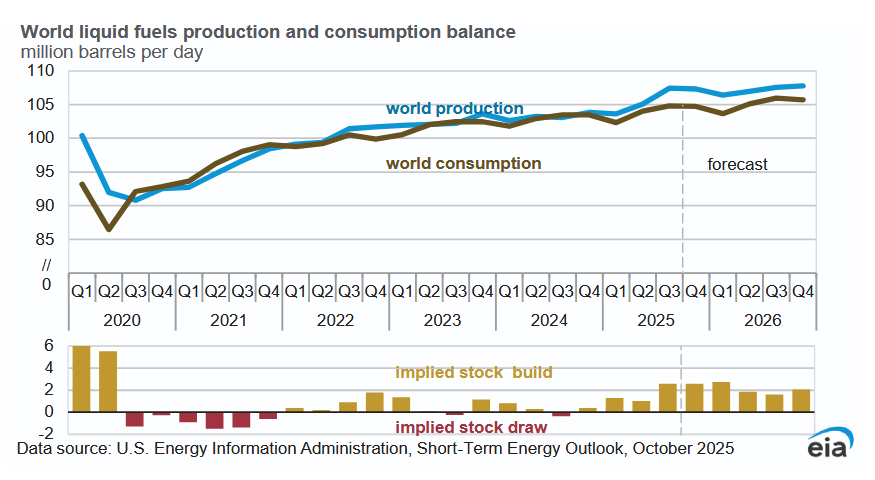

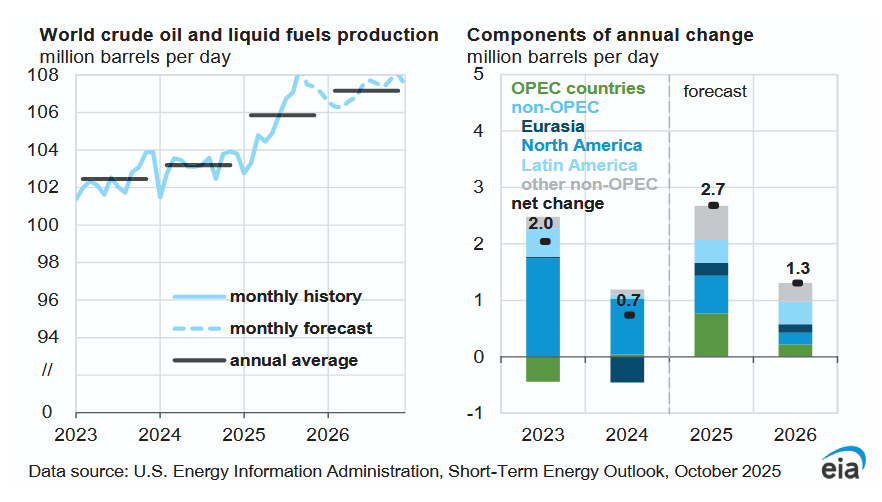

Note the stock build in 2025 and 2026 which leads to lower oil prices in 2025H2 and 2026.

A much larger increase in Petroleum output is expected in 2025 compared to 2024, 50% smaller increase is expected in 2026 due to higher stock levels and lower oil prices.

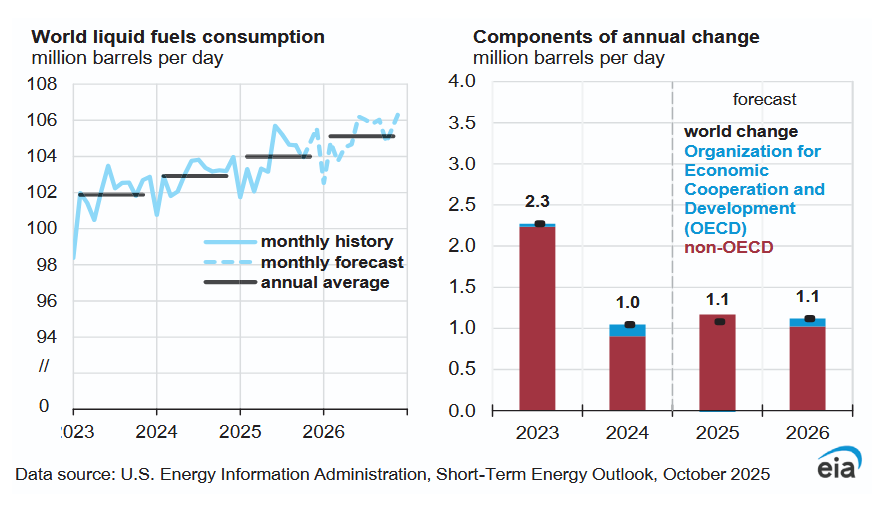

The lower consumption expected in 2025 (1.6 Mb/d less than output) leads to a corresponding build in petroleum stocks in 2025.

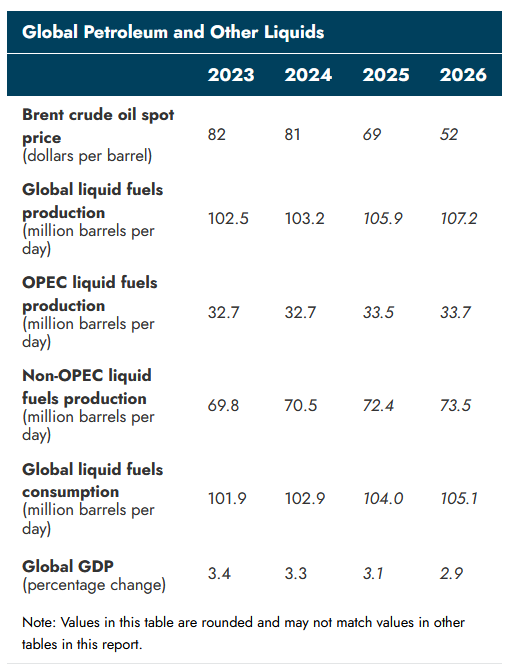

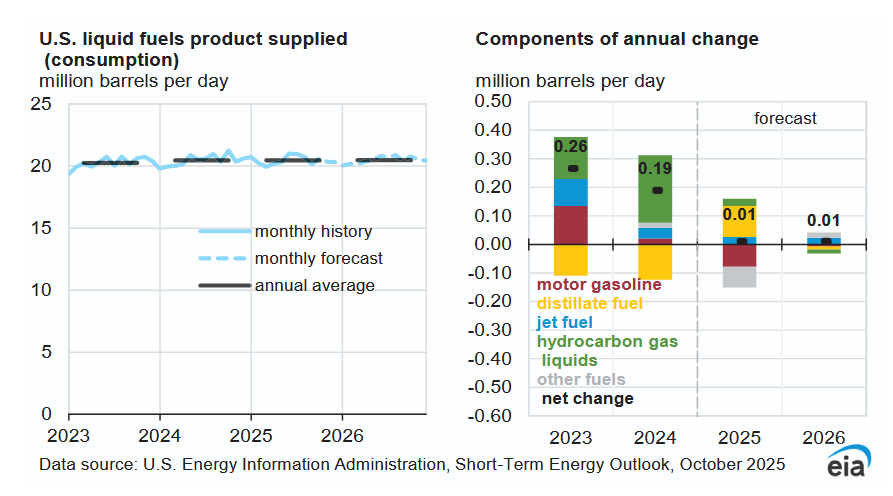

The chart above includes NGL and biofuels along with C+C.

The difference between production and consumption is net exports of liquids (including Hydrocarbon Gas Liquids or HGL).

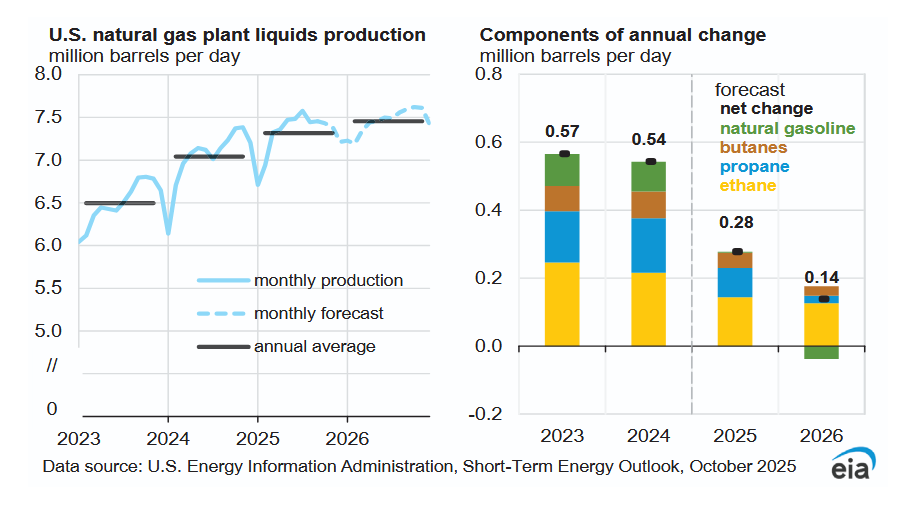

NGL output increases by about 0.5 Mb/d from 2024 to 2026.

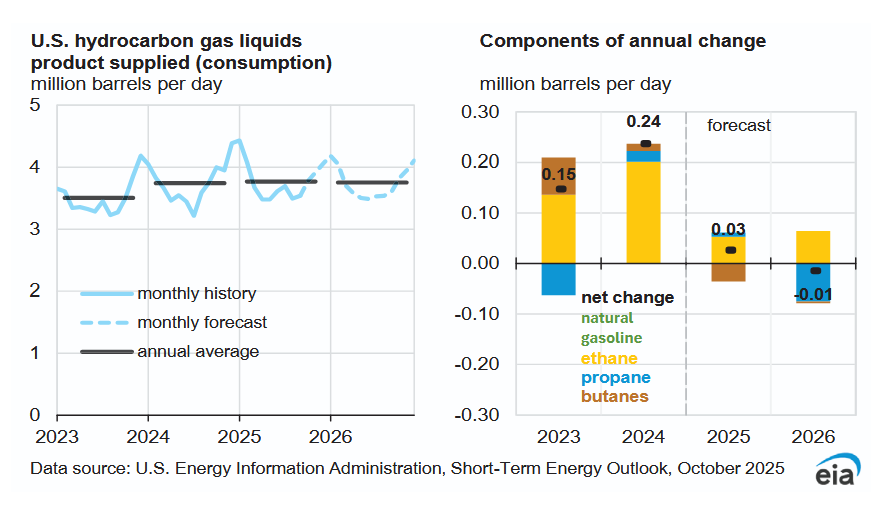

HGL is the product name for NGL, the difference between NGL production and HGL consumption is the net export of HGL.

About 3 Mb/d of HGL net exports are expected in 2025.

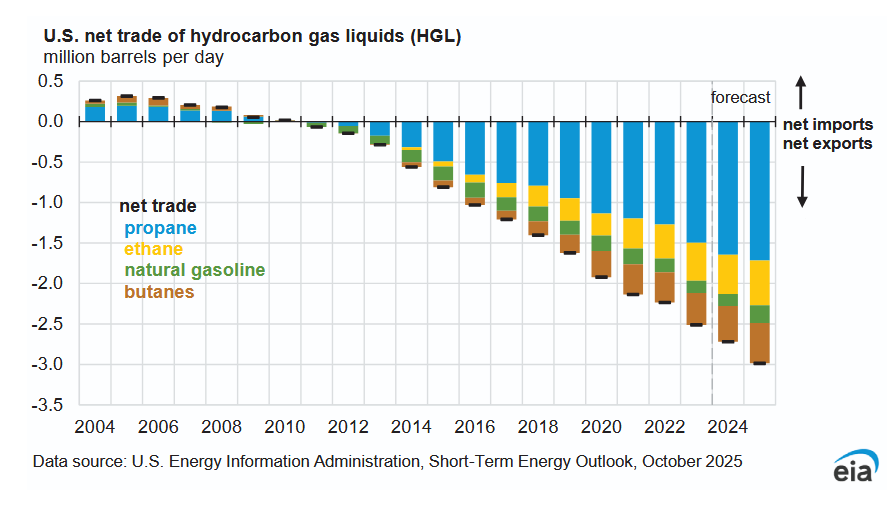

Almost all net exports of petroleum liquids from the US are HGLs. Note that in the previous chart HGL exports for 2026 are not shown, 2025 is the final year in that chart whereas the chart above ends in 2026.

Large increases in 2023 and 2025, probably due to large LNG export capacity increases in those years compared to 2024 and 2026.

The difference between production increases in 2025 and 2026 compared to consumption increases of natural gas allow increased net exports of natural gas over the 2025 and 2026 period.

Net exports of natural gas increase by 4.5 BCF/d in the 2025-2026 period.

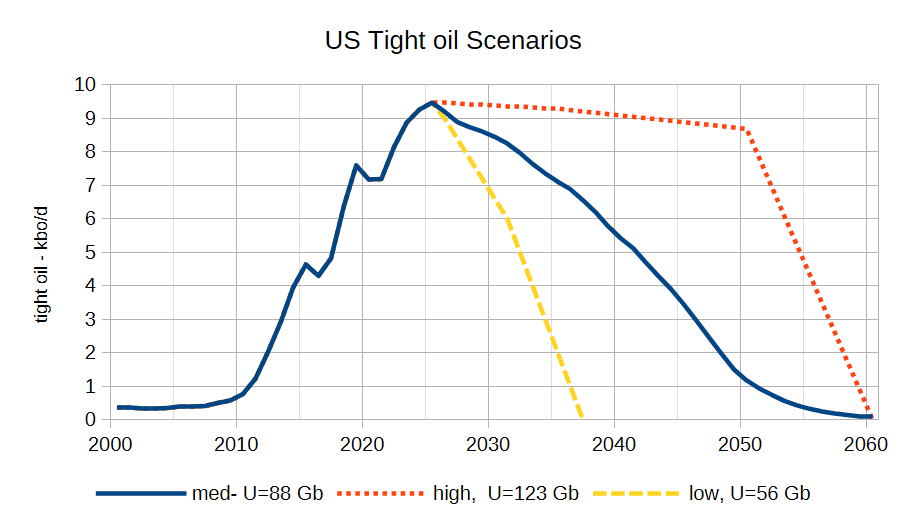

The tight oil scenarios above use a negative exponential probability distribution where remaining resource mean is equal to standard deviation at 31 Gb, which at the low scenario of 56 Gb has about a 90% probability of actual URR being higher than this level which corresponds to proved reserves plus cumulative production, the medium scenario is the mean URR with a 37% probability that URR will be higher than this scenario and the high scenario corresponds to a 10% probability that URR might be higher than this level. The median URR with a 50% probability that the URR might be higher or lower is 70 Gb.

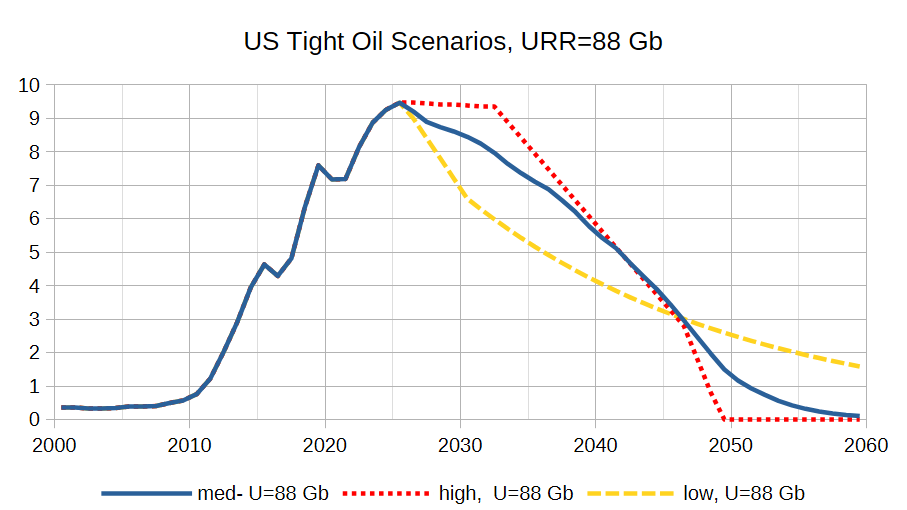

The scenarios above are intended to illustrate that there are an infinite number of different scenarios that can be created with a URR of 88 Gb (the medium scenario in the previous chart), the chart above selects three scenarios from this infinite set. It is certain that none of these 3 scenarios would be correct as there are many complexities both known and unknown that will affect future oil output making it virtually impossible to predict.

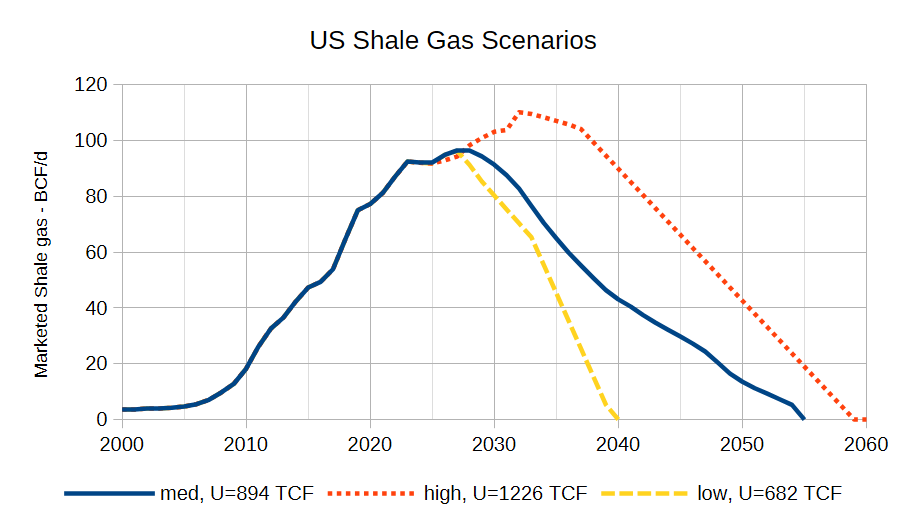

The shale gas scenarios in the chart above also use a negative exponential probability distribution where the low scenario corresponds to cumulative production plus proved reserves and has a 90% probability that the URR will be higher than 682 TCF for marketed US shale gas. The medium scenario is my best guess for the scenario with a mean URR of 894 TCF which has a 37% probability that the URR will be higher than this level. The high scenario for marketed US shale gas has a 10% probability that the URR will be higher than this level. As in the tight oil case the scenarios that could be created for any URR are infinite, so for each of the three URRs presented, the path of future output is unknown, and of course the future URR is also unknown, All that is known is output from 2000 to 2024, beyond that it is guesses which are certain to be incorrect.

104 responses to “Short Term Energy Outlook, October 2025”

https://abcnews.go.com/Politics/trump-confirms-authorized-cia-operations-venezuela-land-strikes/story?id=126563281

Trump says he has authorised CIA and Special Ops operations in Venezuela (the worlds largest oil reserves).

I am not sure that announcing that to the world, is the best way to keep those missions secret???

Remember General Jim Mattis was Trumps first Secretary of Defense.

General Jim Mattis organised the infamous “Peak Oil 2015” paper.

https://peakoil.com/production/us-military-warns-oil-output-may-dip-causing-massive-shortages-by-2015-2

“By 2012, surplus oil production capacity could entirely disappear, and as early as 2015, the shortfall in output could reach nearly 10 million barrels per day,” says the report, which has a foreword by a senior commander, General James N Mattis.

“By 2012, surplus oil production capacity could entirely disappear, and as early as 2015, the shortfall in output could reach nearly 10 million barrels per day”

Interesting–that article was posted in 2010, when many of us were convinced of an imminent peak in oil production. I know I was. A professor of mine even published an article in Nature magazine about it in 1998.

We should all stand in awe of the ignorance of those who led us to that conclusion. This is not meant to dis them, either, as these were not rubes and dopes: Deffeyes, Campbell, Laherierre, as well as Hubbert, all power houses, all capable, experienced, academic geologists. But, oh, how woefully inadequate the data they relied upon!

Peak extraction rate is unknowable and will probably remain unknown until long after it happens — whenever that is — because there will always be a chance that ten-fifteen post “peak” a recovery will happen, because look at history? So far, history is a story of recovery. History is a story of things that were not counted as “oil” suddenly taking on huge significance. After years of paying attention to this, I’m not even sure I know what “oil” is anymore.

In the meantime, things are as Monbiot said a long time ago: “There is enough oil to fry us!” (or something to that effect). I continue to watch that frying happening, even as I lose interest in watching the rate of oil production increasing.

Mike B,

“… how woefully inadequate the data they relied upon!”

I hesitate to challenge that statement – nor, certainly, the rest of your excellent comment – but I feel describing the data/info as ‘inadequate’ crucially minimizes the wildly divergent current reality with the projections of so many knowledgeable experts from a decade back.

Mike, there were ENORMOUS amounts of rapidly evolving data back then that showed huge amounts of recoverable hydrocarbons were soon-to-be-accessible via the directional drilling/frac’ing method.

For whatever reasons, those experts CHOSE to disbelieve/disregard this data and rely upon – as you have noted – ‘inadequate data’.

This is NOT a nit picking distinction as it may be highly relevant this very moment to so many of you all who still maintain a looming hydrocarbon scarcity will arise in the near future.

While Nony has been repeatedly trashed for his brash style, and Texas Tea, likewise, for his direct, not-so-gentle comments, these 2 commentators (and very few others over the years) have attempted to point out info/realities that have conflicted with the seemingly pre-adopted mindset of imminent oil/gas scarcity that permeates so many readers of POB.

This mindset has inhibited an open minded, expansive evaluation of info from a wider realm of ongoing events.

While strictly confining this comment to the hydrocarbon world, it is my firm conviction that a great deal of today’s broader socio/political contentiousness arises from this (largely unrecognized) biased/prejudiced mindset that colors so many of our responses to significant events of the day.

Bottom line … not so much the inadequate data was a root cause of gross error as the collective, willful choice of choosing and relying upon said data.

This protocol exists even today.

Jes’ my 2 cents.

Coffeeguyzz,

Seems this simply shows that the future is difficult to predict. The paper was published in 2010 by the US Military, probably based on data through the end of 2009.

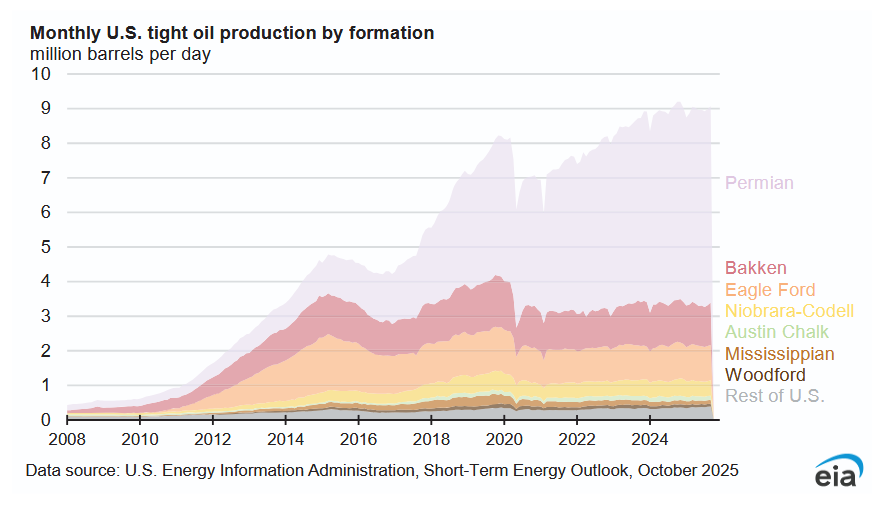

The increase in oil output since 2009 has primarily come from tight oil.

Here is the EIA’s AEO reference case from 2011, it was wrong, but this was what the bast Energy Analysts in the US Government expected in 2011, in 2024 US C plus C was projected at about 6 Mbpd. This was not just peak oil predictions, it was the main stream expected.

chart(111)

My point was to simply say that this guy had Trump’s ear in his first term.

As we all know, humans don’t like to admit when they were wrong and will usually double down on the ideas they have invested in.

What do you think they discussed in their meetings?

Trump is aware of Peak Oil would be my bet.

And he would see it as a way to profit.

https://www.foxnews.com/politics/trump-says-venezuelas-maduro-doesnt-want-f-around-us

Trump confirms Maduro offered him access to nations resources not to attack him (huge peak oil implicatins here IMO)

Trump declined putting 50 million dollar (USD) bounty on Maduro. (That’s ALOT of Venezuelan Bolivars!!!)

This aint about “narco-terrorism” (many USA citizens want drugs)

This kind of argument I saw in the conspiracy talk. “Peak oil is a myth because look we exceeded records.”

Everyone knows that Tight oil saved the day. Peak conventional is still behind us in 2005 and it wasn’t surpassed until now.

And look at Tight oil, it peaked at the beginning of 2024 at least with the October EIA data:

I remember in autumn of 2023 Mike Shellman predicted this.

Even if that peak is surpassed once more down the road it still looks like an undulating plateau.

https://peakoilbarrel.com/wp-content/uploads/2025/10/blog251018dd.png

blog251018dd (1)

Rig Report for the Week Ending October 17

The rig count drop that started in early April when 450 rigs were operating and rebounded over the past few weeks added 4 this week.

– US Hz oil rigs rose by 4 to 377, down 73 since April 2025 when it was 450. The rig count is down 16% since April.

– New Mexico Permian rigs rose by 1 to 92 while Texas added 2 rigs to 182.

– Texas Permian added 2 to 142. Midland rose by 2 to 22 while Martin added 3 to 20. Upton was down 2 to 13. Reeves was down 1 to 18. Glasscock was down by 1 to 4.

– In New Mexico Eddy dropped by 5 to 36 while Lea added 6 to 56. Lea County rigs have risen by 10 rigs over the last 2 weeks, i.e. from 46 to 56. Clearly something new/big is happening in Lea county.

– Permian rigs were up 3 to 234.

– Eagle Ford dropped 1 to 32.

– NG Hz rigs rose by 2 to 109.

A Rig

Frac Spread Report for the Week Ending October 17

The frac spread count was unchanged at 175. From one year ago, it is down 63 and down by 40 spreads since March 28.

A Frac

Hi Ovi,

As of the end of 2023, the county with the highest average EUR in the Permian was Lea county.

This may still be the case and current low oil prices may lead to high grading.

Data from Novi from Jan 2024, 2020-2023 wells in selected Permian Counties,

At 24 month cumulative output is

301 kbo for Lea

272 kbo for Eddy

274 kbo for Loving

235 kbo for Ward

230 kbo for Martin

226 kbo for Midland

226 kbo for Reeves

https://public.tableau.com/shared/QDXQ8K3FP?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Lower resolution at link below

permian counties

Hi Dennis

That is as good an explanation as ever. I also wonder if the drillers have found a new layer in their county or as you suggest they explored that layer in the past and put it on hold.

Lea county appears to have the best rock in the Delaware basin.

Ovi,

I doubt it is anything new, the layers have been well explored, the best formations in Lea County as of Dec 2023 are the Wolfcamp A, Second Bonespring, Third Bonespring and Wolfcamp B. I doubt this has changed since 2023. Chart at link below has the Lea County formations with the most wells completed from 2019 to 2023, all other formations have lower EUR than these.

https://public.tableau.com/shared/BZGQDC6MC?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

This is just a matter of economics and the need to make money from the best wells, though it would be smarter to just wait for the glut to subside imho and stop drilling new wells for now.

Chart at link below is from the chart linked above, showing only cumulative output for these Lea County Formations.

Cumulative output at 24 months for 2020-2023 wells (to compare with Lea county average of 301 kbo from earlier comment)

Wolfcamp A – 334 kbo

Wolfcamp A(xy)-330 kbo

3rd Bonespring-307 kbo

2nd Bonespring-305 kbo

Wolfcamp B-254 kbo

See

https://public.tableau.com/shared/CHGGSXRQK?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

About 80% of all horizontal wells completed in Lea County from 2020 to 2023 were in the 5 formations shown above (1078 of 1350 wells). The average cumulative output at 24 months for just these 5 formations in Lea County for 2020-2023 wells was 314 kbo.

lea formations

Hi Dennis

Maybe it’s a layer they discovered earlier and put it on hold for a time like now. Also any chance they could be child wells. As I understand it, child wells are not as good as the parent wells.

These drillers seem to find new tricks and there is no way we can keep up.

Hi Ovi,

Most wells in core areas completed in the past few years will be child wells. Some formations will be better than others and the best formations are drilled first. So speculation that some new formation is attracting more rigs seems unlikely from my perspective. The rigs are likely moving to Lea County simply because that’s where the profits are likely to be found.

Also very likely that I am wrong because you are correct that I do not know much. Just repeating what I have learned by looking at the available data (see link below.)

https://novilabs.com/blog/permian-update-through-jan-2024-2/

One can easily look at all the formations for Lea county, see link below which covers all years from 2020 to 2023

https://public.tableau.com/shared/GRDKZ5JXN?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Dennis

I Hope that is a typo in your response. I did not say or imply that you don’t know much. I appreciate your knowledge and your willingness to put up models.

Ovi,

I was alluding to your comment that there is no way we can keep up. I agree with that. I simply am stating that there is much that I do not know, my models may be of some interest, but they are no doubt flawed by my limited knowledge.

My speculation on NM versus TX:

In general, NM had less initial development than TX did.

And it is very nice rock.

Add onto that, that there’s a lot of drilling on Federal land in NM (but not in TX). And it takes time to get permits, leases, roads, gas gathering and water gathering pipes, etc. It’s nothing the industry can’t handle. But it does slow the development even when they know this is the best rock (NM Delaware sweet spot).

Standing ovation for such a detailed report of wide scope, once again.

Still trying to adjust to idea that there is oil in $50’s without global decline in GDP, population or industrial output- which is up about 10% in the past 5 years (after the covid drop).

world instrial

Thanks Hickory,

Demand for oil has not been increasing as fast as in the past. I am also surprised by the low oil prices, at some point prices may rise as resources deplete, though it depends on future rates of decline of supply relative to demand. This is impossible to predict.

Dennis

Thanks for another very detailed STEO report.

Attached is a chart which shows the difference between your World’s Liquid Production and Consumption chart to give a clearer picture of the massive monthly over production that began in August and will peak in January 2026. In January 2026 production will exceed demand by 4 Mb/d. The average monthly over production for 2026 will 2.05 Mb/d.

Not sure how the 2.05 Mb/d translates into over production for C + C but it could be close to 1.6 Mb/d using an approximate 0.8 for (C + C)/All Liquids ratio.

A oil

Here’s a relevant chart from the August STEO. We see that renewables are providing almost all of growth in electrical generation, with coal and gas stagnating and nuclear growing slightly – the current STEO is similar, with gas declining a tiny bit, coal and nuclear growing slightly and renewables providing 78% of overall growth. In the rest of the world (per Ember) the picture is even more dramatic, with renewable generation growing faster than overall electricity consumption (in MWh terms) in the first half of 2025, displacing some FF generation.

This is the inevitable result of renewable generation growing at a much higher percentable growth rate than overall consumption.

250800 STEO

Nick

It really does not matter one jot how much solar and wind power there is. What matters is how much coal, oil and gas are burnt.

https://ourworldindata.org/emissions-by-fuel

All that matters is how many millions of acres of forests are smashed down and how many more burn in fires.

https://www.globalforestwatch.org/dashboards/global/

The water cycle is governed by trees, they capture vast amounts of water releasing it slowly, providing rain to distant places. billions of tree lost in Africa is causing drought in The Middle East.

In 40 years of looking at data, we are always told oil burning will dramatically reduce as will coal and we will stop tearing down trees and polluting the rivers with toxic chemicals and plastics.

Too much money to be made destroying the world

“Too much money to be made destroying the world”

Too true. There is enormous resistance to a transition to net-zero from those who are protecting their FF-related incomes and assets. We see that especially in the US.

On the other hand, the cost of alternatives (solar, batteries and electric vehicles) is still plummeting. It has fallen well below the TCO of FF and is still falling fast. This is forcing a transition – we’re seeing it around the world. Not as quickly as would be desirable, but it is happening.

IVER

Too much money to be made destroying the world

That’s why I think the fact that solar has zero cost at the margin is so interesting. All the investment is up front. The marginal cost of producing an additional KWh is zero. That makes selling solar electricity a cutthroat price war to win market share.

Back in the 90s Bill Gates said about the internet, “I don’t know what it’s good for, but it’s going to be a lot harder to make money selling software with that thing out there”. He was worried about uncontrolled distribution of free (at the margin) software.

For all its weaknesses, solar is already making it harder to earn money by setting stuff on fire. And it is spreading rapidly.

Alim

Obviously if a government puts massive carbon taxes on coal and gas and forces energy to buy solar and wind first or they get massive fines. Sure they make money and coal will struggle.

However in countries that do not tax coal such as India and China then coal does very well.

Global temperatures already hitting +2c above pre industrial times.

The permafrost is now melting and scientists say nothing will stop it now.

Nick G

There are hundreds of trillions worth of oil, gas and coal assets.

No country in the world which has invested heavily in oil, gas and coal could simply shut down these assets until they have made a good profit. Remember profits are jobs, repayment of loans so banks do not go bust. Profits pay for pensions and taxes.

People who years ago and even now talk about stranded assets really don’t know how the world works. As long as there is oil and gas drilling rings will work. As long as there’s coal miners will dig it out and it will be burnt in power stations and steel works.

The U.K being run by financially illiterate grand standers is paying the highest electricity prices in the world.

So your claim that wind is cheap does not gel with reality. The networks are costing billions to upgrade and billions is spent on half employed backup. Billions more on storage.

Do you know where is the cheapest electricity in the world?

Alim,

“solar has zero cost at the margin”

Yes, and that means that it should be (and typically is) always dispatched first. There’s no need for government to “force” this, as Iver suggested.

OTOH, it’s still possible for FF to make money. Utilities can and do pay “capacity” fees to keep generation available regardless of utilization. This is an expensive option: solar+batteries are increasingly making this uncompetitive. Nevertheless it is an option.

Iver,

“No country in the world which has invested heavily in oil, gas and coal could simply shut down these assets until they have made a good profit.”

So, you’re arguing that we should stick with FF power even if it is more expensive than renewables, because that would be good for the economy?

Iver,

If the electricity produced with coal and natural gas is more expensive than electricity produced with wind, solar, hydro, and or nuclear power, it will need to reduce its price to be competitive, at some point when enough wind, solar, batteries, hydro, and nuclear power electricity is available to meet demand, the fossil fuel power plants will be shut down because they no longer are profitable.

Do you remember film cameras? Around 1995 they were the only game in town, now they are a specialty item used mostly by hobbyists. Lots of stranded assets in that industry as film cameras were replaced with digital cameras. This is currently occurring in land transportation as EVs continue to fall in cost, eventually oil will no longer be used for land transport as nobody will be willing to pay a higher price to drive a fossil fuel powered vehicle. As demand for oil falls, oil prices will fall to a level that it is no longer profitable to produce.

There are lots of examples in history of products becoming obsolete and the assets used to produce those obsolete products becoming stranded assets.

Dennis is right. It’s the nature of things that industries become obsolete and are replaced. There will always be stranded assets, investors will have losses, but the overall economy will be fine.

The FF industry simply doesn’t have complete control over what happens. Consumer/importers like China are aggressively pursuing renewables, batteries, electric vehicles, etc. Producer/exporters will simply lose customers, and as the alternatives continue to multiply and become even cheaper the industry will decline sharply and irreversibly. The industry will attempt to fight a rear-guard action but this will become politically infeasible when the cost difference becomes dramatically clear to the public.

The Republican Party can attempt to protect the American FF industry, but the longterm effect will be to make the US poorer and less competitive with the rest of the world: this effect is most striking for the US car industry, which is quickly losing the race with Chinese car makers. If this continues eventually they will be crushed by the Chinese car industry the way they were the 1980’s by Japanese small car producers. It will be sad to see GM go bankrupt again…

Dennis:

My advice would be to do a separate article, where you break from the EIA and start showing your scenarios. You have a view that is (a) more pessimistic and (b) long term, versus the EIA STEO. It’s not even apples versus oranges, but apples versus fish (since you are looking at the long term).

If you did the STEO, it could just be on it’s own. Apples on their own. If you have a competing short term forecast, fine. But I actually think it’s not even that controversial what happens in the next year or two–it will be similar to now! Maybe a little up, little down. But close to now.

The long term article could consist of the your scenarios juxtaposed with the AEO. That would be fish versus meat. Capisce?

Note that the AEO reference case is sort of similar to your “high case”. They have high and low, but bracketing your median case.

I think it’s pretty unlikely we have anything as conservative, over next 10 years, as what you are showing for your median case. All the industry analysts (by which I mean people being paid to do this stuff like Woodmac, EIA, Novi, Rystad…not peak oil bloggers) expect a sort of near flat production for 2025-2027, with a very slow/slight decline down to 11.25 (see the EIA reference case) by 2035.

Who knows what we have after 10 years. But…I think your median case is too conservative for next 10 years. Or even next 5 years.

I don’t see this purely as an issue of X amount of barrels and how you exhaust them. This has been a very long peak oil crutch to want to think of draining a tank. But in actuality, it’s a resource pyramid, with different production at different cost curves (and as technology improves, even just incrementally, we can access more of the pyramid even at a given cost). And the sunk costs (roads, pipelines, tank batteries, seismic shoots, etc.) tend to give a “tail” of production, versus an Ace mountain decline or a Seneca shark fin curve. Rockman discussed this well.

Nony,

See G & R, who are not peak oil bloggers.

https://www.gorozen.com/

specifically

https://www.gorozen.com/commentaries/2025-q2

See also post below from Novilabs

https://www.linkedin.com/posts/jorge-garzon-ph-d-00633672_in-the-midland-basin-rules-of-thumb-might-activity-7383871228975112192-CKB6/

Here is the Permian scenario used for my US tight oil medium case (which is the mean rather than the median estimate, the median estimate would be about 10 Gb less). Many future output paths are possible(an infinite number) for a 55 Gb URR for the Permian Basin. So this scenario is certain to be incorrect, true of all projections.

Note there is a strong tail in my projections, just not the plateau envisioned by the EIA in the AEO 2025 reference case. Resources deplete just a fact.

permian scen2510

The Gorozen Permian future scenario at link below for comparison. About 3.5 Mb/d in 2038 vs 4.6 Mb/d for my medium Permian scenario CTMA in 2038.

gorozen permian

Regarding the STEO, as I said last month, I think the EIA is too negative on price. Who knows, they might end up being right. But the “table odds” are strip that is being traded. And it sure doesn’t have $49 WTI. Now, we have moved down several dollars since last month, so they look a little bit less off than last month…but they are still way more negative than the betting odds.

And in any case if we DO have $49 WTI, I doubt we ALSO have 13.6 MM bopd. I am actually sounding the non-cornucopian word of caution here. One or the other. At most! But not both. I just don’t think the industry can pump that much at that price!

Nony,

I agree that if the price forecast by the EIA is correct, that US output is likely to be lower than the STEO forecast.

Currently the June 2026 futures price for WTI is $57.41/b and the Jan 2026 futures price is $56.59 with the low for the day at $55.99.

I’m going to have to change my screen name as I’m slowly divesting my consulting portfolio out of LNG and into just power generation jobs. The writing is on the wall for me regarding new LNG facilities getting permitted.

I’m now working three powergen jobs, huge ones, all solely for data centers. I primarily work in the PJM realm and there’s a lot of trouble getting grid-connected generation for data centers so they’re mostly going islanded. Frame-7 combined cycle units by the truckload seems to be the favored solution.

The power profile for these data centers is absolutely insane. I’m working on job with 7 combined cycle units in islanded grid fashion and the power swings from the data centers are so extreme that they’re having to add multi-hundred MWh battery systems to handle the load swings. One customer we have has indicated that when their AI chips go into learning configuration that they sync up and drop 200MW and jump of 600MW every 250ms. That’s four 900MW swings per second.

This sort of thing is so dumbfoundingly insane it’s hard to imagine. One data centers I’m dealing with will consume the equivalent power usage as all the homes in the entire state of Massachusetts. I have no idea how this is all going to end but there are going to be a lot of tears she’s by somebody. In the meantime it’s making me all sorts of money so I’m going to ride the ship til it sinks.

“The writing is on the wall for me regarding new LNG facilities getting permitted….in the PJM realm…there’s a lot of trouble getting grid-connected generation”

PJM seems to be having a lot of trouble connecting new generation in general. They have an insane backlog of interconnection requests, and they’re spending way too much money on capacity fees keeping old non-competitive generation online.

LNG Guy,

Fascinating stuff.

What you described re islanding and truckloads of Frame-7s dovetails with my recent venture of granularly looking into the production histories of the fringiest of Marcellus/Utica wells in northwest Pennsylvania.

Absolutely eye opening stuff.

Both Range and Coterra have just taken over several ~15 year old wells in McKean county and have tripled/quadrupled output virtually overnight.

More to this ‘story’, I am sure, but – suffice to say – my bullish stance on future Appalachian Basin output may prove to be vastly understated.

Thanks for posting.

Coffeeguyzz,

See recent Gorozen newsletter where they say:

“Unlike oil, shale gas is still climbing. After what looked like a sequential peak in December 2024, the latest data show production recovering, up by 2 billion cubic feet a day. But the pace is not what it was. From 2019 through 2023, dry gas output surged by 16 bcf a day—3.2 each year. Since then, the rate has slowed by nearly ninety percent, to barely 1.8 bcf a day in total, or 0.4 annually. And the gains that remain come almost entirely from two sources:

Appalachia—the Marcellus and Utica—and the associated gas flowing out of oil wells in the Permian.

Through 2019, the Marcellus was a marvel—growing by 3.5 billion cubic feet a day, every year, as if on autopilot. Then, as if a switch had been thrown, the growth stopped. Since late 2023, production has been flat. The standard explanation is familiar enough: takeaway constraints. Prices in the Northeast sag against Henry Hub, and critics argue the bottlenecks alone explain the stall. Perhaps they do, in part. But the evidence is harder to square. The Mountain Valley Pipeline came online recently, and with it 2.8 bcf a day of fresh capacity. Yet production barely budged. Contrast that with the years between 2015 and 2021, when nearly 15 bcf of capacity was added and production leapt almost in lockstep. In those days, new pipe was met almost instantly with new gas.

The other, less comfortable truth is that productivity per lateral foot in the Marcellus has begun to fade. Since 2023, new output per foot has fallen nearly six percent from the peak years of 2016 to 2020. If takeaway were the only choke point, companies would still be drilling their best wells and productivity would hold steady. Instead, it is slipping—just as it did in the Permian before that basin rolled over. We see little reason to believe Appalachia will prove the exception.”

LNGGuy aka Electroman,

From what you are seeing/hearing what are the electricity generating mechanisms that you think will have the greatest deployment value and prospects over the next ten years?

A few factors that have been acknowledged by many include a considerable shortage of and long lead time for gas turbines, and the long ramp time of the nuclear industry. On that latter point, it is unlikely that nuclear generation will gain even 1% of national generation share by 2035, despite the enthusiasm being directed at new projects. In fact, it may have trouble even holding steady given the old age of the current fleet.

btw- the Global Nuclear Report 2025 came out last month. I have not yet looked it over. https://www.worldnuclearreport.org/IMG/pdf/wnisr2025-v1.pdf

Dennis,

I rarely follow G&R’s work as they have – in my view – routinely presented ‘Berman/Hughes’ level of analysis regarding the App Basin … that is to say consistently wrong to the downside.

One example – if there has been no typo in your comment – is the claimed 2.8 Bcfd capacity of the MVP.

It is 2.0 Bcfd and has frequently been underutilized due to both lack of downstream demand and bottlenecks at the Transco 5 interconnect.

Of course the EUR in the AB may have ‘peaked’. But before the hydrocarbon haters break out the kazoos and party hats, know well just what 3 and 4 Bcf per thousand feet lateral – as Susquehannah and Bradford have produced – truly means.

As ‘lower quality’ wells of ‘only’ 2 to 3 Bcf/1,000 are routinely 15,000 footers, one is still looking at 30 to 40 Bcf cums.

3 bucks per 1,000 cubic foot STILL throws off 100 million dollah gross.

Which brings me to my above stated efforts of discerning just what the heck Tier 2/3 rock may offer up in the coming decades. (My poring through the several hundred well records in the 9 county northwestern corner of Pennsylvania leads to a very preliminary view that there is a LOT more acreage that will be developed profitably.

Apparently the big boys have been well aware of this as CNX and Expand have joined Range and Coterra (likely EQT, as well) in regaining operational control of several wells just this past – August – reporting period.

Natgas output will continue to rise, plausibly jumping from the current ~35 Bcfd in the AB to over 50 Bcfd in the Appalachian Basin in little over a decade’s time, as the EIA predicts.

Hickory,

What I see is data centers driving all the grid expansion right now, at least at the large scale. And they (almost) all want gas fired combined cycle units because they are known, respond to load changes quickly, built in the US (at least GE) and are the most available. I hold judgement on the battery grid stabilizing part until I see the first units go into service.

I liken the whole setup to what my car does – it’s a hybrid supercar. The ICE provides the bulk of the base load power but the electric motors fill in the gaps for instant torque response. These islanded grids work the same way with the CTGs/STGs providing the base load and the batteries fill in the electromagnetic torque (frequency) support during the load swings.

We’re starting to see SMRs proposed to some jobs but given the mad dash to get these AI centers up and running, everybody is trying to get cheaper proven tech (CC units) as quick as possible.

I am old enough to remember pets.com and I’m getting very similar feelings this go around as well. But as I said earlier, there’s money to be made now so you just have to ride the wave til it breaks.

Need any overpaid, underqualified help. Asking for “a friend”. 😉

Thanks LNGGuy.

“GE Vernova (GEV), formerly General Electric’s power business, has a multi-year backlog for gas turbines that extends until at least 2028, with delivery queues potentially stretching into 2031.

The backlog is driven by soaring global electricity demand from data centers, electrification, and grid expansion.”

There are 3 dominant electric generation turbine manufacturers outside China- GE Power, Siemens Energy Inc, Mitsubishi Heavy Industries Ltd.

Higher electricity prices are in the cards for the nation.

Hickory –

Yes there are long backlogs at this point. But depending on how many you are ordering and your purchase history you can pay to get slotted in earlier with GE. But it’s getting late in the game to do that.

Electric prices have already skyrocketed. I’m on PJM at my primary residence and our rates have gone from 9c/kwh to 19c/kwh in just the past several years. A clean doubling and our electric co-op has warned that prices are going up further at their last shareholder meeting. A lot of people on heat pumps (myself included) are going to get a rude awakening if we get major cold this winter.

Dennis

As I said the best who used to post here no longer bother because you are utterly incapable of learning anything from anyone.

You totally dismissed my factual statements and can’t even be bothered to answer the question I raised.

This is not respectful interesting exploration of the issues facing us. You repeat a brain washed mantra of a simplistic economic view.

For those who are willing to fit the truth into their belief system.

China and India have the cheapest electricity other than a few long ago built hydropower.

They both generate the vast majority of their electricity from coal.

https://www.researchgate.net/figure/Electricity-generation-from-various-sources-in-India-2017_fig1_325911049

Countries with the most wind and solar have the highest electricity costs. Mor ons who keeps saying solar is cheap simply are too lazy and self delusional to understand how a stable grid works.

An engineer who works on grid stability has posted of the vast problems and costs of wind and solar but after several replies from Dennis. Has given up.

Dennis:

G&R are not just bloggers, granted. But they are pretty fringe-y and pretty small. Looks like the G guy has “emeritus disease” even if he did have a Wall Street career at one time. I don’t know anyone doing deals through them.

Or…really even what services they offer. I guess they have a mutual fund…just looked:

https://www.gr-funds.com/

So, so performance, pretty GDPish. I bet a lot of their gains are from gold. See the weighting. I have no clue what the load/expense percentage on this little thing is. About the last thing in the world I would do is give them some cash though!

And they are hard core peak oilers for a long time. Sort of price bulls forever. HFIRish. Shale doomcasters from c. 2015.

They do have that ‘proprietary neural network’ model, though! 😉 Even some of the people on their side (price bulls and peak oilers…two highly overlapping circles on the Venn diagram) roll their eyes at the sooper seekrit neural network!

Dennis:

I’m well aware of the Novi posting on how depletion affects Tier 1/2. They said from the begining that they were looking at geology first, then at pressure depletion next (parent child). So, I completely expected this followup. No “aha” for me.

It’s sort of a stray insight, not directly relating to the issue of long term expectations. I.e. EIA reference case from the AEO versus Dennis Coyne median scenario.

What Novi has said on podcasts is that they expect a plateau in the Permian for about ten years, given current price outlook (a few bucks higher, low 60s when they said it). They would definitely pump the brakes on anyone thinking oil will explode given Biden is gone. But then they also are far from peak oiler catastrophists, even lite ones like yourself. I see them as in sort of the boring EIA camp.

Rystad is similar in public discussions. Team plateau. Super slow decline. EIAish. Not DCish.

Much depends on future prices, the AEO 2025 reference case has US tight oil output falling by 1.6 Mbpd from 2027 to 2038, while real oil prices rise from 79.50 to 83/b in 2024$. My medium tight oil scenario has tight oil output falling by 2.4 Mb/d over the same period. Note that my expectation is that oil prices will be in the $70-$80/b range in 2024 $ over this period (Brent Prices).

Higher prices might allow higher output, future prices are unknown. Even if the EIA’s reference oil price scenario is correct, it is unlikely in my opinion that their reference scenario for tight oil output will be correct, far higher oil prices would be needed in order to turn a profit as new well EUR per foot of lateral continues to fall as resources deplete.

To me, it is interesting to look at the CPI calculator, when discussing energy prices.

https://www.bls.gov/data/inflation_calculator.htm

Prices are actually lower than most people (myself included) intuitively think about them. I mean, there was a time when a six figure salary was a big deal. But you almost need to double it (1.87 times it) to make a 2025 salary that is equivalent to one in 2000. Or in other words, 100,000 now is like $54,000 back in 2020!

We had a period of medium-highesh (for post Volker world) inflation from 2020-2025. And then even the generally low inflation from 1990-2020 kind of adds up over time.

So…connecting it back to energy:

The current $57 WTI (world benchmark, really…as the diff from Brent is small and relatively constant and WTI actually trades more even on the world stage) equates to $42.11 ten years ago. Yes…we are currently living with “low 40s” in “real 2015 dollars”. Like…basically the same as the “crash” from 100s, that we had in late 2014. And here we are ten years later!

The current (US, HH) $3 natty price equates to $2.22 in 2015 dollars. I.e. even AFTER a bunch of LNG exports coming on line (enough to make the US the number one LNG exporter), prices are still sub 2.50 in 2015 real dollars. And just imagine how bad they would be if that LNG offtake wasn’t there. 2ish?

I’m just having a hard time squaring all the scarcity worries of the peak oilers, given how low world prices for oil are. (And NAM prices for natural gas.)

Of course, TOD and ASPO had already shut down from shame a couple years prior to 2015. But if I benchmark to 2012 or 2010, the “real” (time then, carried forward) prices look even lower. And I don’t need to salt the dig. Even just adjusting back to 2015, these price are LOW.

It is good to be a consumer! Gas is cheap: natty, and what I put into the stick shift two-seater. They are both just below $3!

But…damn, prices look high in restaurants. I mean I can afford it…and rationally I know that there has been inflation. But it still feels strange.

Nony,

Yes prices are cheap, and if they remain so there will be less investment in oil and gas making it more likely that supply will decrease. Some argue that the demand numbers from the IEA and EIA are wrong (they are much different from OPEC’s estimates for example) and that the “glut” in oil supply is a mirage. These analysts argue that oil and gas are a good investment opportunity as prices are likely to increase as the World comes to realize that demand is higher than is being reported. The yard stick doesn’t really matter, it is how prices in X dollars have changed over time that matters (where X is some year in time whether 1973, 1982, 2005, or 2024 is not important, it is like changing from meters to feet). Yes inflation is real, that’s why a popsicle cost a nickel when I was 5.

Garzon at Novi seems to be pretty pessimistic, at current prices only tier 1 and tier 2 economics work and not a lot of Midland Permian locations left with tier one and tier 2 economics.

So far Garzon has not discussed the Delaware Sub-basin. Though a webinar indicated less of a hit by parent/child well interactions in Delaware Basin.

The cure for low prices is low prices. And US onshore is probably the most responsive area. OPEC is quota driven (cash costs per bbl are $10ish). Other areas like offshore and tar sands and Caspian Sea and the like tend to be megaproject driven. Not fast on/off.

Of course US shales is not AS fast to respond to low prices as OPEC and peak oilers think. But it WILL respond.

—

But on the supply side, the bigger issue is really OPEC. If they want to continue to unwind, we will be in the 40s and the EIA price forecast will be on target (even high). I suspect they chicken out though. And at least pause the unwinding.

—-

I’m actually more in the near term low demand belief than OPEC (I think this puts me on the peaker, or at least anti-corny side…at least this issue). I just feel like there is something weighing on the economy. And Trump keeps screwing with tarrifs and tweets and the like. It’s not a great situation. Not end of the world. But not great. Oh…and data centers and AI and the like are ready for a correction. Dotcom 3.0.

“Some argue that the demand numbers from the IEA and EIA are wrong (they are much different from OPEC’s estimates for example) and that the “glut” in oil supply is a mirage. These analysts argue that oil and gas are a good investment opportunity as prices are likely to increase as the World comes to realize that demand is higher than is being reported.”

Where can we read about this Dennis?

Skeeboo,

See https://www.gorozen.com/commentaries/2025-q2

If you put in your name and email you get access to a link which they ask that you not distribute, but this link is ok with them. Also there is https://blog.gorozen.com/blog/natural-resource-market-commentary where in the oil section they discuss this, but the commentary in the first link is a fuller discussion in my view.

Coffee:

Marcellus is definitely being held back by a lack of demand, not a lack of supply. You can see this with prices, being half a dollar to a dollar less than HH, in general, for last few years.

How can you expect Marcellus to grow, or make a big peak oiler hubub about it “plateauing”, when the demand is being constricted, because of a lack of basin egress? And then look at businesses setting up in basin, just to use that trapped gas!

FWIW: here is the spot pricing per EIA (not strip, spot):

https://www.eia.gov/todayinenergy/prices.php

You can see NY and Mid Atlantic three quarters of a buck less then Gulf Coast. That’s a transport problem. That’s a demand problem. That sure as heck ain’t a “don’t have enough supply” problem with Marcellus gas at less than $2!

Nony,

Yeah, I’ve been aware for some time that the AB is kind of like Secretariat being hobbled by infrastructure constrictions, but it is only recently that I started looking at the real ‘dog’ wells up in the northwest of PA.

Real interestin’ how wells have stayed on Active status for over a decade with daily production measured at 10 to 80 Mcf.

That is – quite literally – a thousand fold less than the big ‘uns throwing off 20 to 30 MMcfd for many, many months running.

One old well is producing – like a Swiss watch – between 1 and 4 Mcfd every month for over a decade.

While these wells are clearly money losers, there must be some good reason to keep them online. Maintaining the acreage leases would be my guess.

But the sheer areal expanse of the producing wells is what surprised me most. There are modestly effective wells within 5 miles of the NYS line in Warren and McKean counties.

Except for Seneca targeting some Utica hotspots in Elk county, there has been zero new work here for over a decade.

Dunno what that Patzek guy was smoking when he claimed ~14 year well life for the Marcellus, but if these long running low producers are any indication, 30+ years might be a more accurate (probably underestimated) guess.

Lottsa gas in the AB.

Yeah…the short well life stuff is and has been one of the goofier items of copium/hopium from the peak oilers, for years. It’s pretty effing trivial to find MT hz tight oil wells or Barnett gas wells that are 20 years old now. And almost nothing plugged and abandoned.

Maybe they cycle them. But big deal…that’s still production. Who cares if the well is only online half the year. It’s still producing. It did “X” for the year, regardless of if that was 6 months of X/6 or 12 months of X/12. I just look at the annual result. Can see it clear as day in the Novi data (which includes idle and plugged wells within generational averages)…and sure as heck doesn’t show the 15 (or even 10!) year lifetimes that the peakers were talking about.

Coffeeguyzz and Nony,

None of us know what the operational details are for oil and gas wells. In many cases those wells will have downhole failures after 15 or 20 years where a low output well will be shut in because the repair does not pencil out (unless the well has very low or no liquids production). If the well has low liquids output then it is possible that no downhole repairs would be necessary as the artificial lift might be at the surface.

The question becomes if it is worth drilling these low output dry gas wells in McKean County. The 4 wells completed in 2010 had average cumulative output of 1.6 BCF at 144 months, if we assume 80% of revenue goes to the working interest (it is likely lower than this) and zero operational cost (it is likely higher than this) and $2/MCF and no NGL (or negligible) we would have about 2.5 million in revenue for the average 2010 well over 144 months. This may explain why so few horizontal gas wells were drilled in McKean County from 2010 to 2022 (only 134 wells total), seems these would not be very profitable ventures. Link below to novi data for Wells in McKean County.

https://public.tableau.com/shared/96ZMTHTYM?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Dennis,

The status/history of McKean county wells may provide an excellent ‘window’ into what to expect in the AB in the coming decades.

That Marcellusgas.org site was glitching on me just now so I was unable to gather more detailed info.

That said, using your own parameters – when applied to Real World snapshot scenarios in Anno Domini 2025 – ought to give you pause …

In 2010, virtually all laterals were 5,000.

Today? While 15,000 footer laterals should be the norm targeting 5,000’/6,000′ deep Marcellus McKean county wells, one could use just a 10,000 lateral length for an illustrative example to double your 1.6 Bcf right off the bat.

Now, gotta AT LEAST double the estimated output due to familiarity, tech advances, etc. over the years (these guys were frantically wildcatting/land grabbing back in 2010).

So … we’re talking a 6 Bcf cum estimate modern Marcellus well for starters.

In fact, Seneca has a 19 well pad in McKean (58 Bcf cum, so far) with almost a dozen Marcellus wells near or above 4 Bcf at 45 months online.

One 8 year old Marcellus well has passed the 5 Bcf mark.

While the half dozen Utica wells on this pad are fairly strong, the Marcellus wells have a VERY low decline rate.

Total pad August daily flow rate (for 17 wells) at over 8 MMcfd throwing off about $750,000 for the month.

(Another reason why only 37 rigs are drilling the AB while output remains a staggering 35 Bcfd).

Why no recent development in this region?

Well …

Over in Tioga county, Seneca has a 5 well pad that is averaging almost 7 Bcf each in less than 9 months … on restricted choke, no less.

My goat pasture research is far from done, but the productive footprint has already increased dramatically in my opinion.

Best is yet to come.

Coffee:

This is a very non-researched guy-on-the-Internet impression, but I sort of see the Utica (especially in PA) as more uniform than the Marcellus. We sort of saw that when exploring the Deep Utica was all the rage a few years ago. Closer to a continuous fairway from SW to NE than the Marcells, which has super hot spots in the SW and NE.

Not some crazy insight. Obviously all shale plays have sweet and less sweet areas. But the amount of differentiation will vary from stratum to stratum. So one of them has to be more uniform than the other.

My intuition is that when they eventually get back to the DU (not for a while at these prices), they get more than the peakers expect, because of Utica being more uniform. (NOT completely uniform, just more uniform, or if you prefer, less differentiated.) I.e. I think we see more development in central PA, which basically doesn’t happen now at all, for the Marcellus. Of course then the sunk costs of gathering pipes and roads and pads from the DU drilling may make some Marcellus wells drillable, even if not that sweet. Since the pad is sunk. Just a thought….and not something to worry about until 2040.

Nony,

Here is Utica/Point Pleasant wells from Novi by county

https://public.tableau.com/shared/T6YGCPZX9?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Not so uniform, there are definite sweet spots.

Here is Marcellus for comparison, by county

https://public.tableau.com/shared/8X2M97N6T?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Nony/Dennis,

Yeah, I think there is little doubt that the Utica is far larger than the Mighty Marcellus in areal extent.

Heck, Questerre drilled a productive Utica well just south of Montreal, O Canada back around 2008.

It is also discontinuous with minimal hydrocarbon presence throughout much of its footprint.

However, the much-prized overpressurized spots also exist and this is where some (much?) uncertainty lies … at least to the general public.

Here’s a weird, over the top story …

About 12 years ago, on a website dedicated to local AB land/mineral rights owners, there was a Rockman-type poster who actually worked in the industry locally.

One time, he said that he was on a rig drilling in Susquehannah county and the Company (name unmentioned) drilled much deeper than the Marcellus formation for prospecting purposes. He said that they encountered such a high pocket of pressure that there were fears of loss of well control. (Sounds like the 10,000 psi encountered when the Scott’s Run was first drilled.)

Anyway, as far as I know, all info gleaned from prospecting – as long as no production takes place – is considered proprietary and legally shielded from disclosure.

It was 2014 when Shell rocked the ‘gas world’ with the Tioga county Utica discovery well – the Neal. This was ~200 miles northeast of the recognized Deep Uticas in SWPA and virtually no one thought it likely to be productive that far east.

Well … 6 months back, Expand just took out a Utica permit right on the New York State border in Susquehannah county.

Mebbee this time next year we might find out just a wee bit more about the Big Brother in the basement.

Nony,

I use 20 year well life as an approximation for tight oil wells based on advice from an oil company CEO with 50 years of experience. My Marcellus model uses a 30 year EUR, when I adjust my Utica model from a 25 year to a 30 year type curve, the URR for Utica increases from 94 to 96 TCF (about a 2% increase).

Coffeeguyzz,

The average horizontal gas well in PA completed in 2020 had cumulative output at month 28 of 6.813 BCF, for McKean County at 28 months the average 2020 well had cumulative output of 2.43 BCF or about 36% of average PA horizontal gas well output. Note also that through 2022 the 2020 wells were the highest output wells in McKean County. See link below for McKean

https://public.tableau.com/shared/226HH8J8N?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

link below has all PA horizontal wells

https://public.tableau.com/shared/3D58CHM6R?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

Not much money is being made on these low output McKean county wells which is probably why only 8 wells were completed in 2020 in McKean County out of 565 horizontal gas wells completed statewide in 2020.

EIA Today in Energy article on the LNG expansion:

https://www.eia.gov/todayinenergy/detail.php?id=66384

NAM is going to more than double its production from 2024 to 2029. This is all under construction projects. Something might get delayed…but it is incredibly rare for a cancellation to happen after FID (because of sunk costs for long lead time equipment). So, this is just a train coming down the track, effectively. No stopping it.

Most of the advances are coming from USA, but Canada is starting to grow and even Mexico, a little.

Note that USA does approximately a quarter of total global LNG. So doubling it is like adding 25% to the world. And we are only doing about half of global growth (Qatar, et al have firm projects also). So…we are looking at about 50% extra getting dumped on the market in the next 5 years.

Even if demand growth is healthy at 5% per year, that implies a 25% oversupply. Can you say…low spot prices! 😉

I don’t know what the 2029-2035 outlook looks like. I would think that the industry takes a pause though and lets some of the overcapacity get worked off. Like a 5 year pause or so. (This isn’t uncommon. We have had these sort of 5 year cyclical over/under builds before.)

Here is a good link for the global build: https://www.iea.org/data-and-statistics/charts/cumulative-lng-liquefaction-capacity-additions-from-post-fid-projects As you can see, USA is number one adder (F. Fesharaki calls the USA the suicide bombers of LNG). But Qatar is number two. And Canada is actually number three (in additions).

Good graphic for showing the current supply leaders (not the additions, but current and history):

https://www.eia.gov/todayinenergy/detail.php?id=64844

USA, Qatar, and Australia are the traditional top three. But USA has been pulling away recently. And will do so more in next four years. Qatar is adding some, but not as much as USA, but more than Australia. So we should expect a more clear one, two, three picture in 2029 with USA on top, then the Qataris, then the Ozzies. What can I say…it’s like Lake Placid in 1980 hockey!

I think this may lead to higher natural gas prices in the US as supply may have difficulty meeting the demand for natural gas used to feed these exports, note that there is also gas demand to fulfill the energy needs of the LNG export facilities (about 15% over and above LNG output for cooling and transport.) So if LNG capacity increases by 12 BCF/d, demand for natural gas increases by 12*1.15=13.8 BCF/d if all of the LNG capacity is utilized.) These LNG assets, if built, are likely to be money losing ventures. Can US shale gas output increase from 86 BCF/d to 100 BCF/d (this does not take account of falling conventional gas output)? Over the next 4 years. In the past 12 months average 12 month shale gas output has increased by about 2 BCF/d, if that continues we would be short by 6 BCF/d, maybe prices increase and demand for natural gas decreases, but data center demand seems to be booming so natural gas prices may increase if shale gas cannot deliver.

The trend from Oct 2021 to Sept 2025 (48 month trend) has been an annual increase in shale gas output of 2.4 BCF/d so for 4 years this would be about a 10 BCF/d increase to 96 BCF/d, so a slightly higher rate of growth would be needed, about 3.5 BCF/d annual increases to fill the LNG demand if other US demand for natural gas remains unchanged.

So effing what!This is classic supply and demand, Dennis. Of course natty prices would be cheaper if exports were restricted. We saw this with crude oil prior to the lifting of the export ban. I briefly worked at a refinery that was getting export controlled oil and making massive bank, because of the diff between domestic and international oil prices.

However, consider:

1. Any export that is restricted will lead to cheaper prices internally. This is the same for grain, for instance. Should we prevent ALL exports from the USA?

2. Restriction of trade (in either direction, tarrifs OR export controls) are a bad idea and protectionist. The market functions better when we sell what we have more of and buy what we have less of. Instead of trying to do everything ourselves (tarrifs) or keep everything internal (export controls), we sell what we can produce cheaper and buy what others can produce cheaper. This is free markets 101. Read Free to Choose or watch the PBS series.

3. Natty prices will be lower THAN THEY WOULD HAVE BEEN if you constrain exports. For example, if you look at real natural gas prices over the last 20 years, the trend has been down. EVEN WITH LNG added! This happened despite the pushing out of imports (by competition) and the growth of exports. The shale gale was just that strong. But yes…prices would be EVEN LOWER if we didn’t have that LNG that got put in. [I went through the trend in real gas prices with you before, and the volume increase.]

4. Natural gas and oil doesn’t belong to you. It doesn’t belong to the nation. It belongs to the mineral owners. The USA is the one country like that. In every other country oil and gas and minerals are considered like deer in Nottingham Forest, the property of the king, not the landowner. But not in this great country built by ballsy pioneers. Those MAGA farmers own that oil and gas. It doesn’t belong to you. It doesn’t belong to the country. It belongs to the individuals.

Nony,

Should everything be exported? Military hardware for example. When there is a national security concern exports get restricted as crude was from 1975 to 2015.

As to higher prices, the point that you seemed to miss is that US LNG will not be able to compete on World Markets if US natural gas prices rise. You say so what, not my problem.

It is a problem for those investing in LNG export capacity, they are likely to lose big.

For a different perspective on Friedman see

https://www.nytimes.com/2020/09/11/business/dealbook/milton-friedman-doctrine-social-responsibility-of-business.html

Natural gas prices are low due to the shale revolution, if output continues to grow as fast as LNG export capacity and data server demand grows, prices will remain low.

I am highly skeptical of that outcome, the low cost resources will deplete and higher cost resources will require higher prices or they won’t be produced.

Also tight oil output is likely to decline and with it the associated gas from tight oil plays, this will put further pressure on natural gas prices.

I am all for higher natural gas prices as it may lead to less use of natural gas and more buildout of solar, wind, batteries, and perhaps small nuclear power plants, and some pumped hydro, as well as demand response solutions and perhaps some vehicle to grid solutions.

All of these, along with heat pumps may lead to natural gas being relegated to a backup role as an electric power source. In that case prices fall due to lack of demand for natural gas and a lot of the expensive tier 3 and higher shale resource remains in the ground.

Also note that I did not say exports should be restricted, I was pointing out that prices would rise and thought it would be obvious that this affects LNG exports and how profitable they will be with a higher input cost.

So obvious, I did not believe it needed to be stated.

DC –

A lot of LNG contracts are “take or pay”. These are long term contracts where the buyer is basically just paying for the service from the liquefaction operator, they have to source their own gas and the plant just liquefies it for the buyer. For these contracts the buyer has to pay the LNG facility whether they bring ships or not, they’re paying for the capacity. So the export terminal might not load any ships at all for a year but they’re still getting paid by the customer.

Not all contracts are that way, of course, and those that operate off the spot market are at higher risk as you point out.

Also, we usually use 9% as the overhead for fuel gas and pretreatment scrubbing. It depends on how wet the incoming gas is and exactly how they’re making their power, of course.

LNGGuy,

I am including the gas used transporting the LNG as well, though probably that should not be included, as if there is 1 BCF/d of LNG produced, some of it will be used in transport (varies by length of trip). Thanks for the info, so 9% added to demand to account for natural gas used to condense the gas to liquid (and other stuff I am unaware of). Finding the gas input may be difficult as associated gas from tight oil plays decreases over time and Haynesville and Appalachia may not be able to fill the gap. Contracts can be broken and companies can go bankrupt, without enough natural gas this may become a problem, we will see.

Interesting discussion of US imports to Mexico:

https://www.eia.gov/todayinenergy/detail.php?id=66404

The first graphic is not that dramatic. Going from about 5 to 7 BCF/d (i.e. adding 2) over last 6 years.

The reason (as it has been for last 10 years) for the slow growth is more on internal piping within Mexico, not the intrinsic industry and population demand. They just don’t have a great internal gas pipeline setup. And they take forever to do anything. See second graphic for a map of the pipes, including new internal Mexico pipes.

One interesting aspect is the LNG plants being done in Mexico. They are small (not sure what is behind the size decision). And I sort of wonder why they have the Atlantic coast ones (versus just doing projects in the USA). But the Pacific coast one is quite interesting as it will have way better transit to Asia. And there is a fascinating (internal to Mexico) pipe going in just south of the US border to supply that plant!

That Baja plant is north of Ensenada. You could go by it if you were doing the Rosarita to Ensenada 50 mile bike ride. (Great time, did it twice, lots of girls from LA coming down. First time I did it, I was strong and young and fast…actually opened up the dance floor at Papas y Beer, with a Hollywood camerawoman. Second time, I was fat and slow and…well…older.)

https://www.youtube.com/watch?v=0hkHcYVhZGY

There is a killer hill in that ride…about 0:17 in the video. You end up being on the “free highway” (older one) for most of the ride. It goes inland away from the ocean, so you are separated by a pretty decent ridge. Hot as hell…not the typical beach weather. More like desert, not like San Diego. And then you have to get up that couple-mile long hill. I saw a lot of people have to stop and walk the bike. Or husband/wife teams on tandems having arguments: “honey are you pedaling back there!?”

Re’ NG supply and demand:

Coffeeguyzz is right: there is a lot of NG in the USA. The question is how much, really, and will it be enough to supply the homeland, esp in light of the planned LNG exportation?

Prices have been distorted by glut and clean energy subsidies for so long it’s almost impossible to evaluate where this is going—on either the supply or demand side. Not only have domestic prices been subdued but there has developed an impossible dichotomy between NG hubs. At a time when the WaHa was minus $8/tcf and the Columbia (AB) was $1/tcf, the Henry was a fairly solid $2.50-$3/tcf. On top of that, the LNG prices charged to European countries were atrocious.

It’s going to take a lot of demand to outstrip the current glut in the heart of Permian production selling into the WaHa. The Desert Southwest pipeline is underway to take large volumes (from WaHa) to the burgeoning data center/AI/chip industry that is developing in the Phoenix area. The Taiwan Semiconductor Manufacturing Co plants there are $180 billion-dollar investments and the nearby data centers are energy hogs. The richest of the rich are building beside old nuclear plants (MS, Google, Amazon) but the bulk of bridge fuel to manufacture electricity for most data centers is going to come from NG. Theoretically, if the world (including the USA) were serious about reducing the carbon footprint and also the spew of carcinogenic compounds into the air, all this NG would be treated to the clean-up of LNG trains, for the comparison between global use of pipeline NG versus LNG is simply astounding. SMR’s are on their way, but it’s going to take a couple of years, maybe more. The EU and the UK are losing ground very rapidly in the world of competitive finance and manufacturing. To prevent a disastrous European free fall they’re going to have to compete in AI and thus use LNG. Either that or continue the use of Putin’s dirty NG (the stuff that he pipes to them is so dirty that burning it has probably negated the clean air measures they’ve put in place regarding wind and solar and electric vehicles; it is foul stuff and Angela Merkel knew full well it was).

Conventional NG was mentioned. There are still a few places where economical vertical wells high in gas can be drilled, but they’re getting few and far between. I have part interest in one that has been producing about 50 bopd and 5MM cfpd. During this price massacre, the NG has carried the well, because it sells into the Henry Hub. Had that same well been in the catchment of the WaHa, it would have been a disaster. During the last several years and even now, comparing NG production in one area with that in another is an exercise in futility. Trying to estimate how long the bridge fuel of NG will last as a generator of much-needed ramping-up of electricity is in the same category. Because of all the above, the data centers that build next door to an electricity-generating power plant amply supplied by NG, wind and solar, and also nuclear will carry the day. That’s a hard set of circumstances to come by. Fermi America in the outskirts of Amarillo is actually the only one that I know of. As such it’s likely to become an international showcase.

Gerry,

“continue the use of Putin’s dirty NG”. Could you elaborate on your comment of dirty Russian NG. I cannot find any source that suggests that the Russian NG is significantly worse than any other. The pipeline spec is about 95% methane and others (nitrogen, E,P,B). Acid gases would have been removed at the gas treating plants. I cannot see the EU allowing dirty NG imports, but I am open to persuasion.

Good RBN post on latest FID(s) for LNG plants. Couple more trains.

https://rbnenergy.com/daily-posts/analyst-insight/rio-grande-train-5-adds-2025s-record-fid-haul

So…that’s actually more than the EIA chart I linked earlier.

Note also that the RBN chart goes out into the 2030s. By 2032, capacity will be 33 BCF/d.

Good thing we have all that shale gas. And to think…you can still find videos from David Hughes about Peak Gas and how we can’t build import fast enough. Or from Berman on how the Marcellus will disappoint.

Make sure to read the link soon. The RBN blog posts go behind the paywall after a few days online.

Nony,

About 29 BCF/d of capacity up to 2029, with 12.2 BCF/d already in commercial operation and another 3.5 BCF/d in commissioning phase (ramping up to full capacity) and 13.1 BCF/d under construction scheduled to be complete by 2029. So the RBN piece has other projects reaching FID, adding another 4 BCF/d by 2032 out of a bucket of 14 BCF/d of approved projects on the books. So it looks like another 10 BCF/d of potential LNG facilities which could bring the total to about 43 BCF/d, about 29 BCF/d more than today. Add in the energy for cooling to condense and for transport about 15% and the 43 BCF/d becomes about 49 BCF/d of dry gas demand, assuming this all comes from shale gas and demand for other uses does not fall then about 125 BCF/d of shale gas would be needed or about 46 TCF per year. Below we have a “high2 scenario” as well as the AEO 2025 reference case, with the high2 case assuming all approved LNG projects reach FID and are built by 2035. My estimate is that there is about a 10% probability that shale gas URR will be 1228 TCF or higher. The AEO 2025 reference case has a URR of 1413 TCF at minimum, my estimate suggests there is about a 5% probability that the US shale gas URR will be 1413 TCF or higher.

shale gas scenarios2510

America, like many countries, has produced an energy crisis for itself. Mostly having to do with the tremendous dichotomy in NG prices, lack of sufficient pipelines, and local geopolitics.

I pointed out in my earlier post that of the three “hubs,” it is possible on the same day to find NG at minus $8/tcf at the WaHa, $1/tcf at Columbia, and $3.50 at the Henry. This while many of our NG riches are being squandered in exports and others aren’t used at all. The North Slope of Alaska (like Russia in this regard) contains vast quantities of NG. The state doesn’t allow flaring so they inject the associated gas that drives oil into the wellbore as a miscible agent to enhance oil recovery. One of life’s great inequities is that the bulk of Alaska’s population (~70%) pays upwards of $12/tcf for gas that the state’s North Slope has in abundance.

NG should be more evenly distributed in the United States of America instead of cooled down and put on LNG carriers to be sold internationally–even if the tankers are powered by boil-off gas. I’m all for commerce, but we really should be taking care of our own people first, especially the “First People.” I hadn’t mentioned Alaska in my pricing dichotomy because the state doesn’t produce much commercial NG. But if they don’t do something soon, they are estimated to run short in a couple of years–even as the price spirals even worse. The northern Athabaskans will freeze.

Mankind procreated in the caves, then spread over the globe in a giant diaspora. As conditions improved, so did health and longevity. We are now almost 9 billion, all with electronic devices. I’m pretty sure that if all 9 million deleted their photographs, texts, articles and other electronic debris, it would lessen the load on data centers that make up the ephemeral “cloud.” And if we said, no friggin’ robots or artificial intelligence, there would be no need for more data centers.

However, ever since the concept of Shrodenger’s Cat, people have tried to determine if that damn cat was alive or dead–or both. Using qubits in quantum computing as a notion of superposition, a form of humanlike thinking has derived. It can learn on the go (machine learning) and it has a gazillion thoughts at one time (deep neural circuits). Now, despite the fact that it’s totally possible some Americans could primitively freeze from the cold, we are trying to let Shrodenger’s cat out of the box using quantum computers, eating up more and more and more electricity for the chips and to store the logarithmically greater “reams” of electronic data that comes from humanlike thought. This has evolved to an existential problem, and whoever achieves singularity (the point where humanlike thoughts and plots exceed those of the smartest humans) could easily control the universe. At this point there’s no way to let up. It’s full-throttle or take a language course.

So anyone who thinks that we’re not going to require truly vast amounts of electricity to drive this revolution in quantum computing and super-human artificial intelligence has not studied the mechanics of how qubits grind out information using super-positioning and tunneling, and so forth. These quantum computers, coupled with the electricity needed to store the usual electronic junk “in the cloud” threaten not only to outstrip our most aggressive efforts to generate electricity but to undermine our entire electrical infrastructure, which is mostly electricity – carrying conduits that are between fifty and a hundred years old, covered by easily-frayed rubberized insulation, the cause of the bulk of our forest fires and outages.

We need our domestic NG for our own people. And if we’re to produce enough super-human superiority that no one messes with us, we’re going to have to wake up to the need for NG pipelines to power utility plants to produce prodigious amounts of electricity the likes of which nobody has ever seen. I’ve come full circle. At the most primal level of humanity, there are people in the USA who are using food money for their basic electricity needs, while at the most sophisticated level of humanity very rich men are gobbling up cheap electricity by building data centers in the NG fields or at the end of a giant NG pipeline. Across America, NG goes all the way from the idiocy of flaring it into the atmosphere or paying $8/tcf to have it piped away, to $1 at Columbia pipe, $3 at the Henry Hub, or, my gosh can you believe this, $12 in the natural gas rich state of Alaska. What a mess!

To Carnot re’ dirty NG:

I am eighty and opinionated, and I may have let my fingers get ahead of my brain. You’re probably right, the NG the Europeans imported from Russia likely wasn’t that much different than NG from anywhere. Actually, it was likely that I extrapolated when I shouldn’t have. In the Druzhba pipeline a few years back they had high levels of organic chlorides. But I think that was oil only. Then when the Nord Stream pipeline was sabotaged there were found large levels of lead and some chemical that affected the endocrine system. I am not sure but I think they finally decided those had been stirred up from old seabed contamination.

All that aside, the Russian oilfield is a nasty thing. Methane gas leakage is almost legendary. To be fair, I think they have so many methane gas caves from underground propulsion, especially in the region below the Siberian Traps (burned-out volcanic mountains overlooking methane coal beds) that they just naturally assume a little methane leakage here and there won’t harm anyone. It always amazed me that the meticulous Germans would buy gas from the methane-leaking Russians.

Anyway, I think your comment was valid. The Germans doubtless tested every day for impurities.

https://www.oilystuff.com/single-post/the-end-of-the-world

I admire your enthusiasm for oily/gassy things, Dr. Gerry. Had you spent a lifetime in it, with tens of millions of dollars spent out of our own check book, you might be a little less enthusiastic. Its a common and unpreventable faux pax. I try hard to understand that.