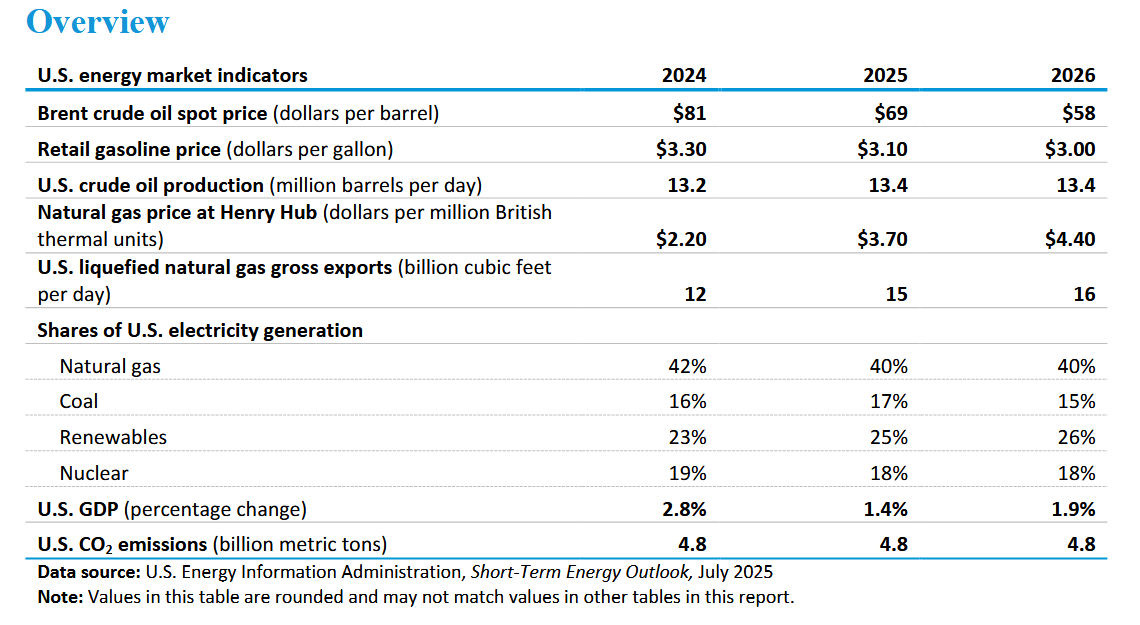

The EIA Short Term Energy Outlook (STEO) was published recently. A summary in chart form.

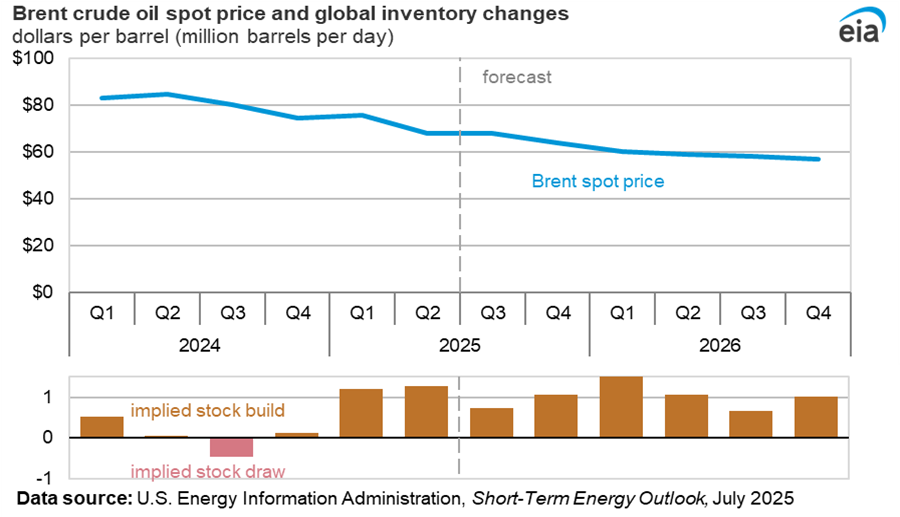

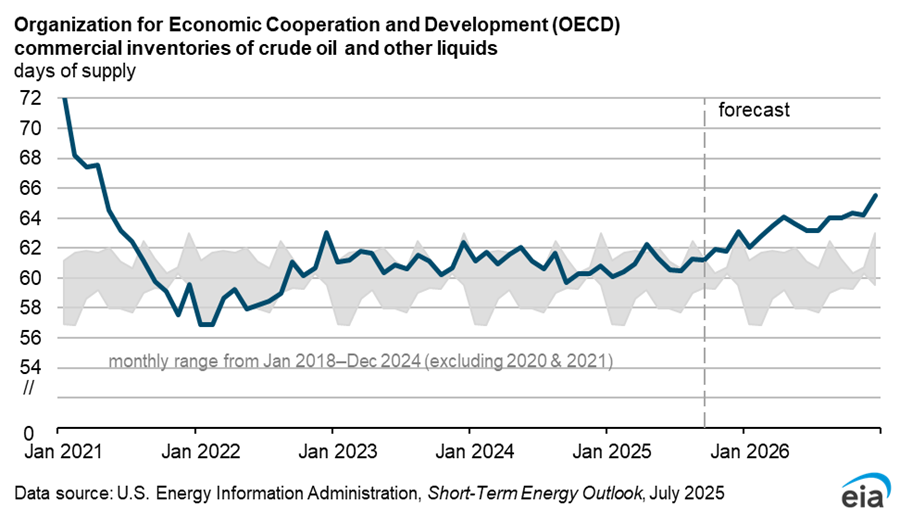

Commercial OECD inventory is expected to rise to 66 days of supply by 2026Q4, since the pandemic stocks have been in the 57-62 day range. High stock levels lead to the low oil prices in the previous charts.

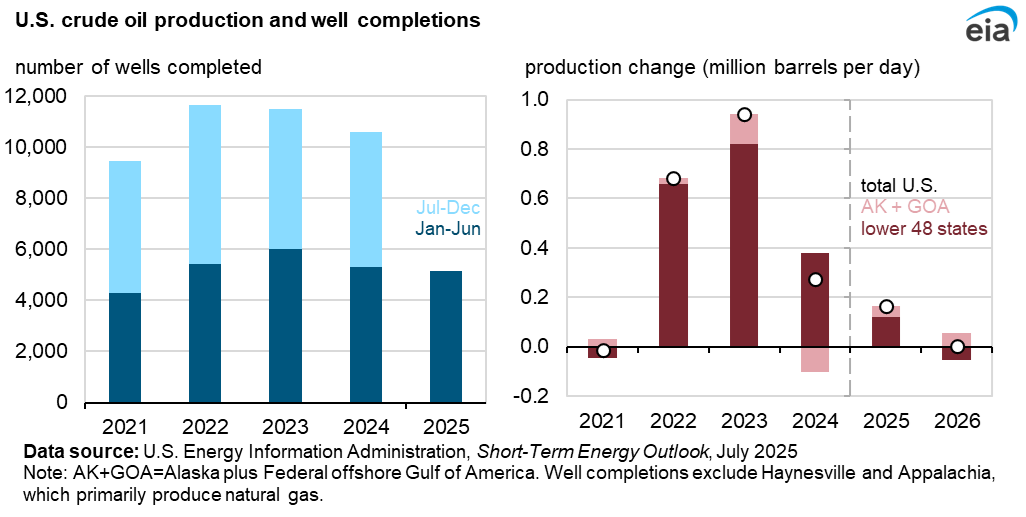

Lower completion rates and lower new well productivity lead to slower growth in US output in 2025 and 2026, Completion rates are expected to be even lower in 2026 due to very low oil prices (WTI=$55/b) leading to no increase in US average output in 2026 compared to 2025.

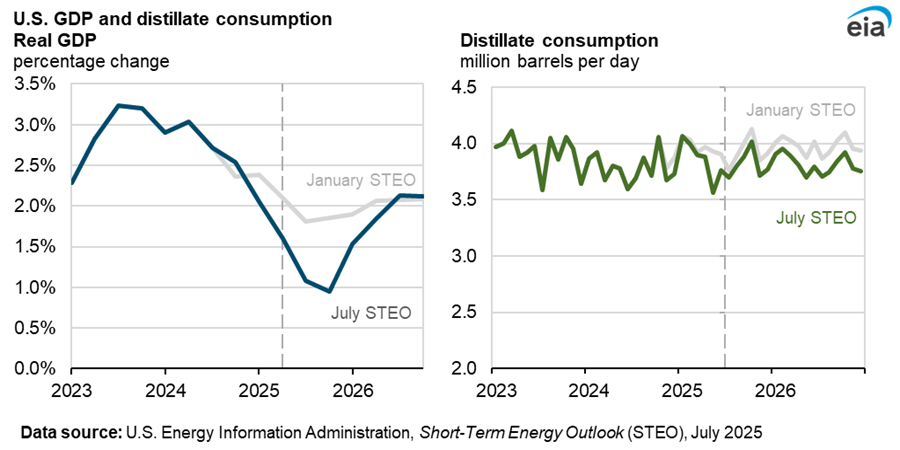

US GDP and distillate consumption are closely correlated and the outlook is less optimistic now than in January 2025. The rebound at the end of 2026 for US GDP looks like wishful thinking to me.

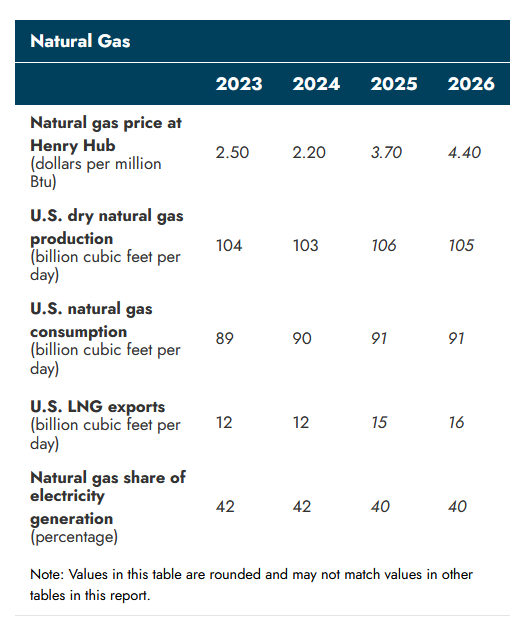

Higher natural gas storage levels in October 2025 lead to lower natural gas prices than in last month’s STEO. This is due to higher output than expected and lower demand for natural gas from power plants due higher natural gas prices.

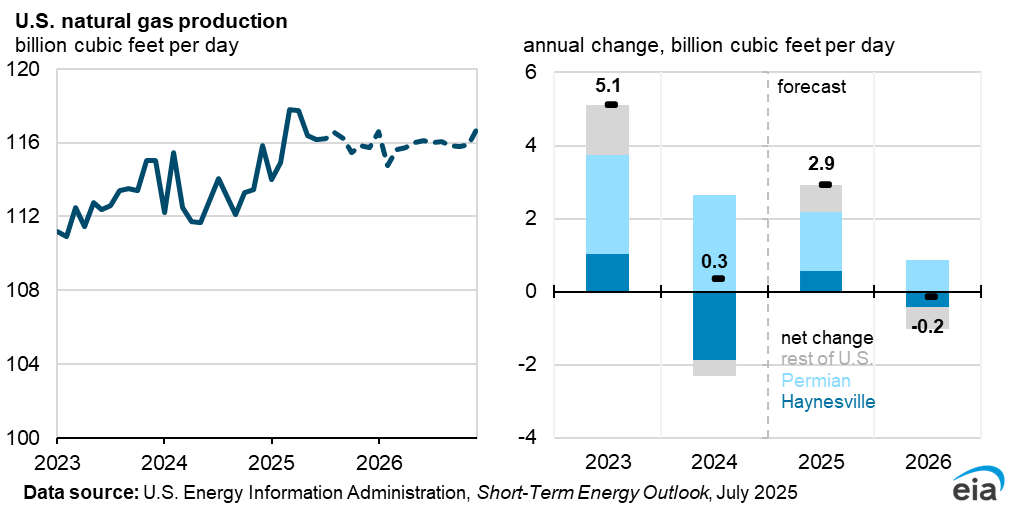

Marketed natural gas output is 2.9 BCF/d higher in 2025 than in 2024, but in 2026 output decreases slightly by 0.2 BCF/d due to low natural gas prices.

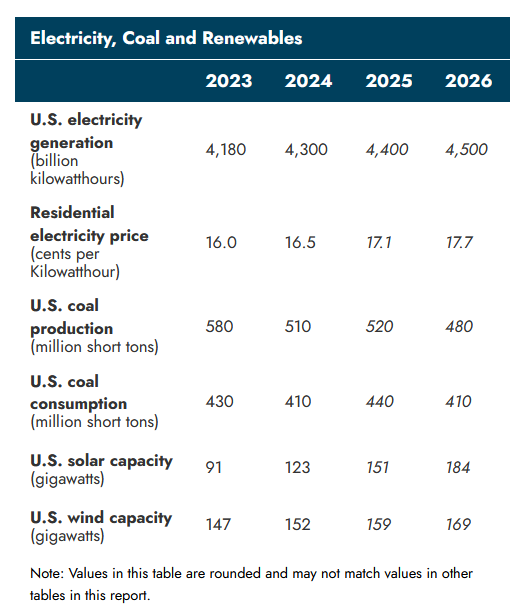

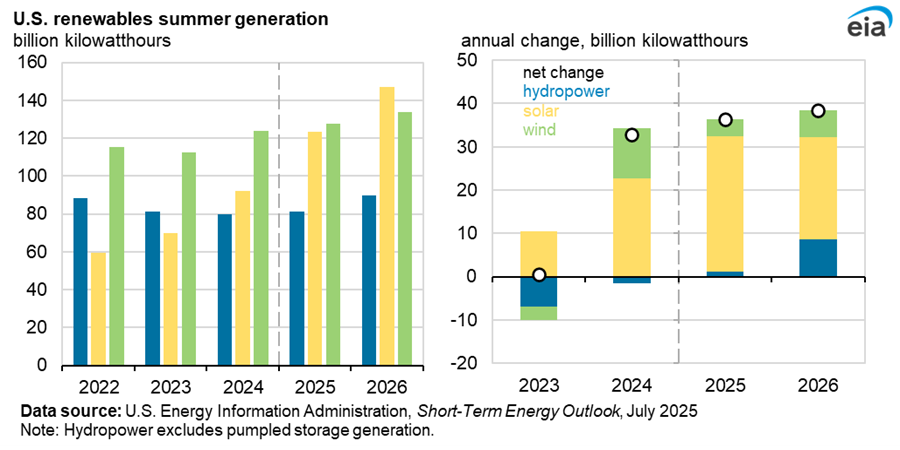

Solar is expected to surpass wind in 2026 to become the largest source of renewable power in the US.

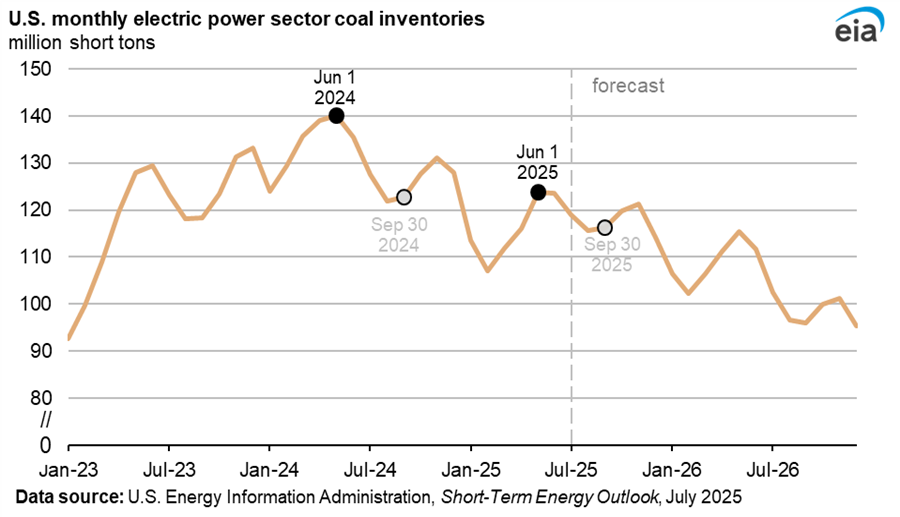

Inventories of coal at US power plants are expected to continue the decline that started in 2024 through 2026.

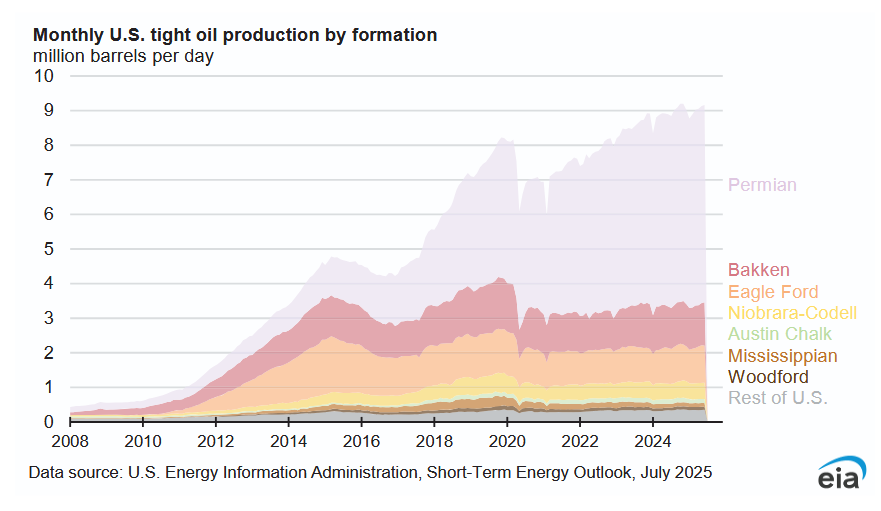

US tight oil output has not increased much since early 2024.

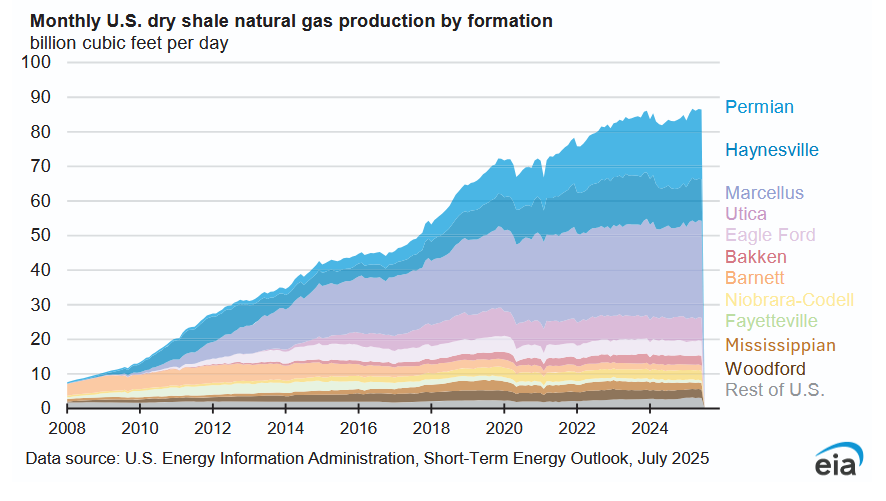

US Shale gas output has been relatively flat since 2023.

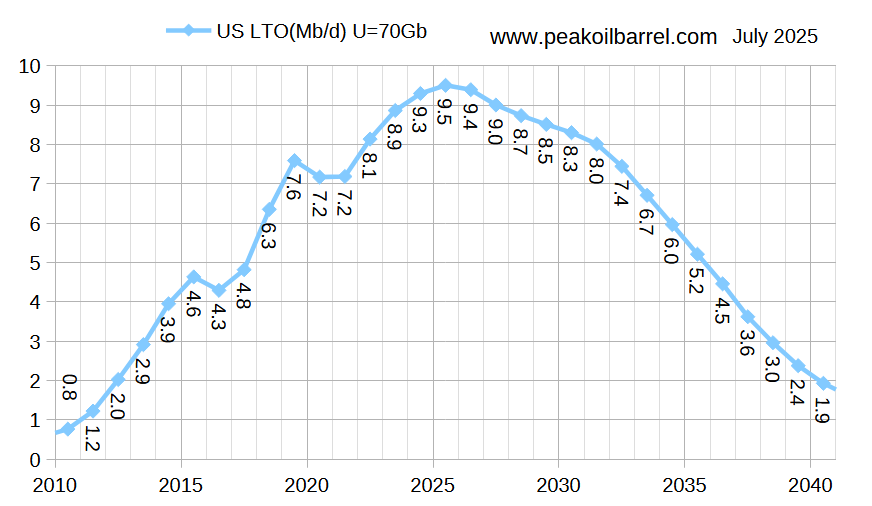

This updated tight oil scenario expects the peak to be in 2025 for US tight oil, a year earlier than last month’s scenario.

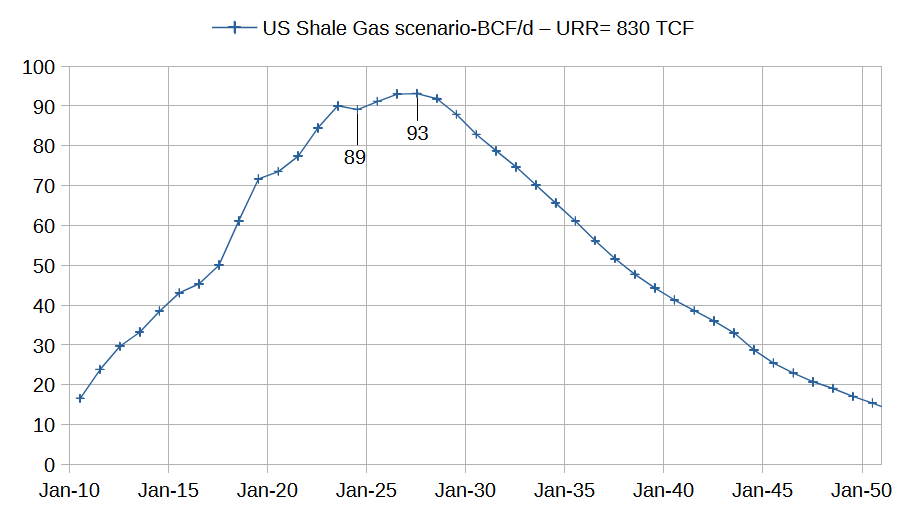

The scenario above attempts to model marketed shale gas production where it is assumed that dry shale gas is about 92% of marketed shale gas production.

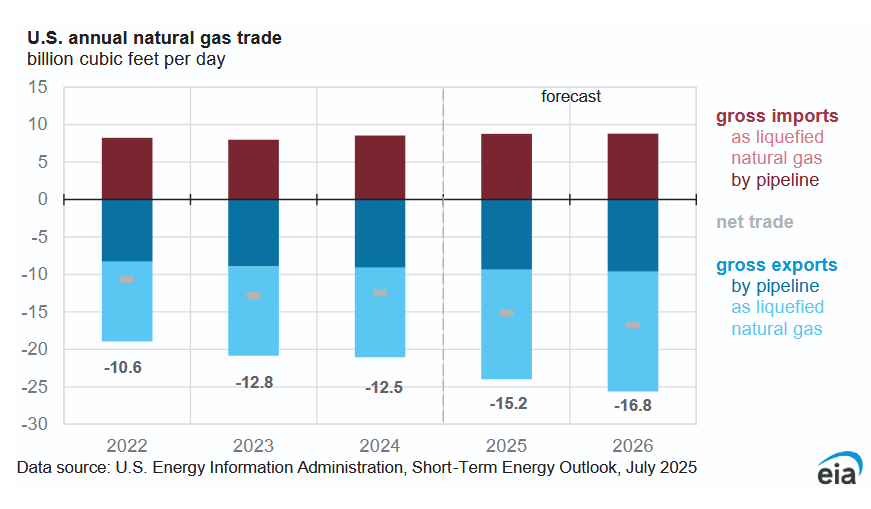

Net exports of natural gas are expected to increase by 4.3 BCF/d from 2024 to 2026 and there are 24 BCF/d of LNG capacity under construction or approved which are expected to begin exports between 2024 and 2030. Assuming all of this is developed and net pipeline exports are unchanged the net exports would increase by 24 BCF/d from 2024 to 2030. It looks to me that unless natural gas consumption in the US drops by 20 BCF/d, there will not be enough natural gas produced in the US to meet the demand from LNG exporters. In the next few years we will see just how much natural gas can be produced in the US, it may be much less than many believe.

185 responses to “Short Term Energy Outlook, July 2025”

Thank you, DC. Looking at your outlook on shale oil and shale gas production, I believe that investments should be made to determine the feasibility of large-scale methane production through methanization of microalgae biomass, another kind of renewable energy. Indeed, it remains only 25 years before 2050.

Thanks for all that information Dennis.

At some point there looks to be a lot of US LNG export capacity that will end up short of product. The populous and industry will eventually demand that domestic consumption be prioritized.

Its a lot of capital at risk-

“Mar 6, 2025 — On its current trajectory, the US LNG Export industry will experience cumulative capital and operating expenditures exceeding $938 billion”

https://www.spglobal.com/en/research-insights/special-reports/major-new-us-industry-at-a-crossroads-us-lng-impact-study-phase-2

Who knows?, but I believe it would be unwise to underestimate demand for Nat Gas, and that increased offtake (pipeline) capacity will enable higher production than you project in the 2030’s.

Hungry data centers are a big ingredient to consider. That industry pays more for electricity, enabling higher production attempts from all sources. Same goes for the electric transport industry demand- will pay more for electricity from any source in the 2030’s as petrol production declines.

Hi Hickory,

My shale gas scenario does not assume there is a lack of demand, but that the resource that is profitable to produce is limited. I agree US consumers may demand that fewer new LNG facilities are built in order to reduce demand for natural gas and keep prices low in the US. The EIA’s most recent AEO has natural gas prices rising to $4.70/MCF by 2047 in 2024$, natural gas exports rise to 32 BCF/d in 2047 from 13 BCF/d in 2024. They also assume that US consumption starts to decrease after 2032 and that US production of dry natural gas peaks in 2032 at 118 BCF/d, but the EIA assumes much more available natural gas than is likely, they expect roughly 1557 TCF of dry shale gas output from 2008 to 2070 (if we assume a linear decrease to zero output from 2050 to 2070.) This is more than 2 times what I expect. Note that the AEO estimate for tight oil using similar methodology from 2008 to 2070 is about 140 Gb, also about 2 times my tight oil estimate.

Perhaps my estimates will be too low. They are certain to be wrong, whether too low or too high is unknown.

Bottom line, both my tight oil and shale gas scenarios are supply curves that are independent of demand for oil or natural gas, I assume oil prices of $75/b or less in 2024$ and natural gas prices of $4/MCF or less. It is possible that ver high oil or natural gas prices might increase the URR somewhat, but I doubt this will be more than 20%, so for tight oil maybe a URR of 84 Gb and for marketed shale gas perhaps a URR of as much as 996 TCF in a high oil and natural gas price scenario. My best guess for URR remains what is shown in the charts in the post with a margin of error of plus or minus 20% for the 95% confidence interval for tight oil and shale gas URR.

On the data centers, they are businesses and will buy the cheapest electricity they can find. If supply of natural gas is short which may lead to high natural gas prices, there will be alternative forms of electric power that are cheaper whether nuclear, solar, wind, hydro, or coal.

I share the view that there may be US gas shortage by the end of the decade. The original plans were based on the assumption that solar and wind would displace some NG generation and the gas would be freed for export. I am not sure about that.

In Canada, however, there’s a gas glut. The way things shake out may be that US imports more from up north…

Kdimitrov,

I guess the US could import natural gas from Canada so they can export as LNG, or Canada could build their own LNG export facilities if they can make a good estimate of their natural gas resource, something that the US has done a very poor job of.

What is the source for

https://peakoilbarrel.com/wp-content/uploads/2025/07/blog250726w-768×446.png

I mean, what is the model, and where are the declining rates for that coming from?

Svaya,

The model s my own based on modelling of Permian basin, Bakken/Three Forks, Eagle Ford, DJ/Niobrara, and other tight oil plays. The decline comes from fewer completions as space in sweet spots decreases and average well productivity declines leading to less profitability. It is my best guess assuming oil and natural gas prices remain at $75/b or less and $4/MCF or less in 2024$. Mostly it is a reflection of a lower scenario for the Permian Basin as rig counts and average new well productivity normalized for lateral length continues to fall as sweet spots run out of room. Scenarios for 4 major tight oil plays and “other tight oil” in chart below.

A worst case, best case scenario would be interesting, fracking wells have notoriously steep decline rates. the curve you put reminds more of the convetional.

Svaya,

The model accounts for the steep decline of tight oil wells. The model matches fairly well with the data. You can just imagine something 20% lower and 20% higher to get a rough idea of the probable range (70% confidence interval). EIA data is red crosses, except Permian based on Novi data, PSM and RRC data for Permian basin.

Svaya,

Here is the Permian scenario with monthly completion rate on right vertical axis, the STEO has oil prices falling to $55/bo for WTI in 2026 so I assume the completion rate falls from about 460 wells per month in June 2025 to 364 wells per month in December 2026, the completion rate remains at this level until December 2030 and then decreases to zero by Feb 2027. Clearly this is a guess, but oversupply of oil seems to be the trend and eventually all tight oil plays will become unprofitable as resources deplete. average well productivity decreases and oil prices potentially remain low due to low demand relative to supply.

Alternative Permian scenario, obviously the future is unknown. For this scenario an extra 16500 Permian tight oil wells are completed and URR increases by about 6 Gb (from 37.5 to 43.5 Gb) for the alternative scenario.

Note that for both Permian scenarios the completion rate up to December 2025 is based on Permian horizontal oil rig counts up to June 2025 where I assume a 6 month delay between the start of drilling and first flow from the well, I also assume DUC count remains at the June 2025 level (no increase or decrease).

After December 2025 the scenarios diverge due to different assumptions about the future horizontal oil rig count after June 2025. The lower scenario assumes that the rig count continues to decline and the alternative scenario assumes that the horizontal oil rig count stabilizes at the June 2025 level until June 2028 with declining rig count after that date.

Using the alternative Permian scenario presented above, we get the following for US tight oil (other basins besides the Permian have the same scenarios as presented earlier). Note that the original US tight oil scenario presented in the post is 71 Gb rather than the 70 Gb on the chart (which was mislabelled, my apologies.)

Chart below shows other basins besides Permian summed up as “US tight less Permian” with “alternative” US tight oil model (URR=77 Gb).

For the Bakken/Three Forks URR=9.3 Gb, Eagle Ford URR=9.8 Gb, DJ/Niobrara URR=2.9 Gb, and Other tight oil output URR=11.4 Gb (this other tight oil group excludes Bakken, Eagle Ford, Niobrara, and Permian tight oil output).

“The U.S. oil rig count just suffered its fastest collapse since the pandemic.

From January to July 2025, rigs dropped 13.7%, the steepest 15-week plunge in five years.

This isn’t just about oil, it’s about inflation, jobs, energy security, and the global economy.

“

https://bsky.app/profile/investinq.bsky.social/post/3luy3xzhhbm2i

Interesting piece from EIA

https://www.eia.gov/todayinenergy/detail.php?id=65824

They predict an increase in Appalachian natural gas output of 8 TCF per year over the 2024 to 2050 period, that is about 22 BCF/d. This is a very optimistic estimate. For more reasonable estimates see

https://pubs.geoscienceworld.org/aapg/aapgbull/article/108/1/15/631779/Forecast-of-economic-gas-production-in-the

About 180 TCF for maecellus in paper above

and

https://www.sciencedirect.com/science/article/pii/S2949891024008613

this paper is quite optimistic with 157 TCF for core areas, though if condensate prices are not high enough, then it might only be about 120 TCF of URR for Utica (they use $80/b for NGL in their economic analysis which is likely 3 times too high).

The EIA’s AEO 2025 reference scenario has Appalachian output at about 52 BCF/d in 2050. A more realistic scenario has Appalachian output reaching about 40 BCF/d by 2029, in 2050 output will be about 6.2 BCF/d or about 46 BCF/d less than projected in the 2025 AEO. This scenario combines a Marcellus scenario with a Utica/Point Pleasant Scenario.

Also keep in mind that the rest of the US besides Appalachia will decline far more steeply than projected by the EIA, output of shale gas besides Appalachian falls by 50 BCF/d from 2030 to 2050. Total US Shale Gas falls from 96 BCF/d in 2030 to 17 BCF/d in 2050 (or by 79 BCF/d over 20 years).

D C,

The Marcellus-Utica gas production is not resources-limited, it is take-away & demand-limited, there has a been a glut of supply and price way depressed.

The solution now is to put AI data-center there, and hope to solve the demand limit.

The Utica Forecast paper (Patzek group) has metric “kTon” and MCF all together, and the less than 300kton for dry gas EUR means 10BCF EUR, this is even lower than Marcellus. Hope they were not confused as the Vaca Muerta gas report where they also confused with “BCM” with “BOE”.

The EIA obviously wants to please the Trump energy policy, they also add 7~8BCFPD for Haynesville EF which might be underestimated if EU and rest of the world eat up all the LNGs. Also, they should expect Gulf of America to decrease in gas when the deep low GOR part takes the major production increase.

The past decades old energy policy has now been reversed,

https://myemail.constantcontact.com/Killing-the-Endangerment-Finding.html?soid=1101509381788&aid=94wt5wchouw

https://www.energy.gov/sites/default/files/2025-07/DOE_Critical_Review_of_Impacts_of_GHG_Emissions_on_the_US_Climate_July_2025.pdf

“A Critical Review of Impacts of Greenhouse Gas Emissions on the U.S. Climate”

Report to U.S. Energy Secretary Christopher Wright

July 23, 2025

Climate Working Group:

John Christy, Ph.D.

Judith Curry, Ph.D.

Steven Koonin, Ph.D.

Ross McKitrick, Ph.D.

Roy Spencer, Ph.D.

The worst player in this group of worsts is likely Koonin, former bureaucrat in the DOE, who never mentions peak oil, depletion, or reserves in this report or the book he has written on climate change.

Hi Paul,

In the future please put this type of comment on the non-petroleum thread please.

Sorry, I was just providing the link to the actual gov’t paper that Sheng WU was referencing per the changed energy policy, not from some denier website.

IOW, see Nick below “Sheng Wu started it!” 😉

But Dad, Sheng Wu started it!

(muffled sounds from back seat)

You’re poking me. Stop POKING me!

(from front seat) Quiet down! Do you want me to turn this car around??

Sheng Wu,

We will see, the Marcellus Saputra paper looks very good. Patzek is a geophysicist, pretty sure the Marcellus estimate of 180 TCF is pretty solid, they used ktons because there is a mix of gas and NGL output in Utica. That estimate for the core areas is about 120 TCF which is probably pretty good, the non-core areas of the Utica/Point Pleasant play will not be profitable to produce unless natural gas prices and/or NGL prices are very high. The Utica paper uses and NGL price of $80/b which is about 3 times higher than reasonable (this is equivalent to about $240/bo for C plus C).

I use an average EUR of 11.8 BCF per well of natural gas for my Utica Model and and average EUR 14.9 BCF per well for my Marcellus model, based on a Hyperbolic fit to Novilabs data for each basin.

The Utica well profile is based on the average 2018 Utica well (last year with 24 months of data to make a decent estimate, 2019 looks very similar), the Marcellus well profile is based on Pennsylvannia data only in 2020 so may be a bit optimistic because the average W V well is not as prolific as those in PA.

D C,

The “ktons” unit might make others having a hard time to compare Utica to other shale gas basins, where “BCF” is often used. The mean more optimistic (without exterior input) EUR of 282 “ktons” dry gas is roughly only 11.5BCF, and this way lower than real core Utica wells which should deliver over 18BCF EUR with mean average.

The first obvious reason for the poor forecast is that there are 1-2 companies drilling in the northern-Middle PA area with non-core Utica, and they are drilling there because they have gas pipeline commitment/take away capacity to New England with good price, so they could drill in the non-core Utica. Also, this part of Utica has shallower depth and therefore D&C cost lower than the real Utica core part in the SWPA-WV-OH triangle area. This should not be inferred as or mix with core-Utica where the cost is higher but EUR is also way higher.

Similar economic/geological reasons for the Utica wells further west of the OH-WV border, and inside Ohio mixed with the wet gas/lean condensate area, here the shallower depth and lower pressure makes the original lean codensate/wet gas shale fluid fractionate into dry gas (non-core performance) and lean condensate liquid, and therefore they are confusing the operators who are just targeting liquid part.

In the end, the gas production is different from oil/liquid production here, it is like Marcellus shale gas production, the larger newer frac designs really lift not only the IP, but also the tail after 5 years. I believe this is also what Patzek forecast EUR deviation comes from.

Sheng wu,

My guess is that the Patzek analysis is fine, their analyses are very good for Permian and Marcellus and the only problem with their Utica analysis is the economic analysis which leads them to conclude that non-core areas will be profitable to produce, I doubt this is the case long term. A 120 TCF URR is probably reasonable (their drilling scenarios 1 and 2), the non-core areas will not be profitable. As far as I know there is no Appalachian Gas going to New England, no pipeline has been built.

There is not much evidence the tail is significantly different with new frac designs.

Also note that my model considers the Average Utica/Point Pleasant well and does not focus on core wells only. Note that the Arias-Ortiz et al 2025 Utica analysis does not separate the wells into core and non-core cohorts it simply creates two cohorts by time (2011-2017) and (2018-2024) with survival times of the newer wells expected to be shorter (about 6 years vs about 15 years for the older wells) and divides the wells into dry gas, wet gas, lean gas condensate, and rich gas condensate cohorts. So my estimate for the average 2018 Utica/Point Pleasant well matches the Arias-Ortiz estimate for the average 2018-2024 Utica/Point Peasant well fairly closely (11.8 BCF in each case). No estimate of “core wells” was done either by me or Arias-Ortiz. The non-core areas of that study are areas where very few wells have been drilled and that is likely to continue in the future in my opinion based on how poorly the wells perform in the lower producing counties.

Estimates by some such as Boswell take a county where 5 wells have been drilled and assume the entire county will be filled with wells in the future that all perform like the 5 that have been drilled to date. Such analyses are likely to be very far from the mark. So far the USGS analyses of mean TRR adjusted downward by about 60 to 65% to account for economics yields a far more reasonable estimate of URR.

Well profiles for PA Marcellus wells from Novi, note the increase from 2018 to 2020 followed by a decrease in 2021 and 2022 (wells from 2018 to 2022 are shown). I don’t have good data on Point Pleasant wells beyond 2018, the data for non-core Point pleasant wells is very sparse, but I am very skeptical of claims that such wells will be profitable. Probably the jump from 2019 to 2020 was high grading. The drop after 2020 may indicate that core areas may be nearly fully drilled and companies may be facing falling average well productivity as they begin to drill in less favorable areas. Link to chart below

https://public.tableau.com/shared/HT659DNFN?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

well profile for core counties of Point Pleasant formation

https://public.tableau.com/shared/6D7YB7DRG?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

core counties are Belmont, Jefferson(OH), Marshall (WV), Monroe (OH), and Westmoreland (PA). Cumulative is about 8.6 BCF at 36 months for these 4 counties for 2018-2021 average well profile.

Point pleasant 2018-2021 average wells from non-core counties in PA, OH, and WV (excludes the 5 core counties in previous chart).

https://public.tableau.com/shared/S6MG7NN5Q?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

At 36 months cumulative output for average non core well is about 3.7 BCF which is about 43% of the cumulative output from core counties. This is why I expect the non-core areas are not likely to be profitable for the Utica/Point Peasant formation and believe the URR will be 120 TCF or less.

For all of these charts just click on chart for larger view.

Also consider chart linked below which shows that longer term the Marcellus wells outperform the Point Pleasant wells after about 50 months for cumulative output for the average 2015 to 2017 wells.

https://public.tableau.com/shared/JN6YWTYRW?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

D C,

I agree that the REAL dry core parts of Utica (WV-SWPA and a small part of OH) have been barely drilled that any projection, i.e. by Boswell, has large uncertainties. Although, the successful wells are indeed spectacular. Probably the D&C cost for these core Utica parts is just too high to justify the the drilling, given there are already low cost prolific Marcellus wells on top in these areas.

But, it seems that Arias-Ortiz&Patzek (AOP) paper’s figure 1 obviously lumped all Dry Gas wells together and did not separately count the 5 wells that Boswell used to count the real core Dry Gas counties.

One of the reasons that the Utica is producing quite some gas right now is associated with liquid drilling, and the dry gas wells in this liquid-rich area is the result of PVT liquid and gas separation(most Dry wells in OH in figure 5a in AOP paper), and certainly not as good as original core real Dry Gas part, which are left in blank in figure 5a in AOP. This lumped average practice also discount the real potential TRR in the real Dry Gas Core counties.

About the Utica wells drilled in norther PA that has connection to New England (actually not direct), here is the info along with what Coffeeguyzz posted:

National Fuel Gas (NFG)’s primary natural gas pipeline infrastructure is located in New York and Pennsylvania, not New England. They own and operate nearly 2,800 miles of pipeline, providing access to markets in the Mid-Atlantic, Midwest, Northeast, and Canada. While National Fuel’s pipelines don’t directly serve New England, they connect with other interstate pipelines that do, allowing for gas transportation to the region.

This really demonstrates that what is preventing drilling in non-core area of Utica/Marcellus is not “non-core”, but rather take-away capacity that could deliver a reasonable price per MCF.

Finally back to Marcellus, the drop in 2022 curves is probably a combined result of exhaustion of “legacy tier1” or start test drilling into “tier2“ (led by Cotterra drilling into the upper Marcellus with shorter laterals), and more drilling into the lower IP wet gas SWPA. But, after 2022, the Marcellus type curve is again back to the highest level, probably a result of improved D&C and longer laterals, but certainly no obvious sign of deterioration.

see,https://thundersaidenergy.com/downloads/marcellus-shale-well-by-well-production-database/

Sheng Wu,

Longer laterals make the wells look more productive, but it does not create greater rock volume, it simply reduces costs a bit, the important metric is output per lateral foot as drilling longer lateral just uses up available rock volume.

You can’t pick 5 wells out of 500 and base the analysis on the best 5 wells, or if you do you will get an estimate that is 6 times higher than is realistic. Does the Boswell estimate look reasonable to you? I would say the mean TRR estimate in Boswell for the Appalachian (1400 TCF) is 3 to 4 times too high. Generally I have found using the average well profile from a play yields fairly good results. Note that when this is done the average well is heavily weighted towards the average core well productivity in any case because most of the producing wells are drilled in the core areas.

Notice on those type curves that the 2023 and 2024 curves cross the 2020 curve at around 10 months, so they have high IP, but look like they may not have very good cumulative production in the long run. A cumulative output curve is more useful in my view.

Sheng Wu,

In addition to the added cost of drilling Deep Utica wells versus Marcellus and the decade’s worth of Tier 1 Marcellus acreage remaining (Patzek’s figure), the SWPA operators stopped targeting the Utica due to the horrendous decline of the majority of the ~dozen Utica wells.

Results like the legendary Scott’s Run (72 MMcf 24 HR IP from a 3,200 foot lateral), the Gault and few others were not the norm. That is why the ongoing results from CNX are so intriguing as their work is consistently producing very high output Utica wells in SWPA.

Another interesting situation is the step out work of Seneca Resources up in Elk and Cameron counties … the very definition of Tier 3 acreage.

As their parent company – National Fuel Gas – guarantees purchase and transportation through their company-owned pipes and large customer base in the Buffalo/Western NY region – Seneca has been able to methodically, systematically learn best practices and locations without the normal financial pressures under which most operators toil.

The results are impressive.

Despite numerous ~10 year old Marcellus wells having produced over 4 Bcf cums – and STILL throwing off a half million cubic feet per day – virtually all the newer Utica wells are producing double the numbers of their Marcellus brethren in the same area.

This doubling coincides with CNX’s results as well as XTO’s single Utica well on its Trilogy pad.

For all these reasons – expansive (and expanding) footprint, ongoing lessons learned, demonstrated superior results from co-located Utica/Marcellus wells – many of us hydrocarbon boosters foresee the Utica ultimately surpassing its Little Brother several decades out.

D C,

I agree that longer laterals also deplete the TRR faster, but the cost-down also help make more 2nd tier more economical, and hence more TRR.

For the Boswell 1300TCF Appalachian TRR forecasts, I would put 80~95% confidence for the Marcellus and 50~70% for the Utica.

Similarly, I would put 30% confidence for the Marcellus TRR and 30~50% for the Utica TRR numbers by Patzek group. One technical note about Patzek model — it is actually based on conventional draining model, and not able to include the true original gas in place, i.e. OGIP, which is highly dependent on completion technique— like Coffeeguyzz discussed here.

The OGIP which still a myth, especially for the Marcellus SWPA and it continues to surprise in the upside for the past 6~8 years.

Sheng Wu,

So are you of the opinion that all og the recent USGS mean TRR estimates are too low by a factor of 2? USGS mean TRR estimates seem pretty reasonable for tight oil plays if reduced by about 2/3 to account for real world economics.

What is your explanation for why their estimates would be so far from the mark for natural gas?

Also note that many of the Boswell assumptions such as a 50 year well life with terminal declinecat 6% are not reasonable and at minimum their -30% scenario is somewhat more reasonable, though even this uses the 50 year well life but uses the more reasonable 10% terminal decline. A better model would assume a 20 or 30 year well life. No downhill repair at 500k will be done on a well over 15 years old, it won’t have high enough ROI to justify. Very few wells will produce beyond 20 years for this reason.

We need to look at both economics and physics to understand the reality of oil and gas production.

Using the Appalachian scenario with URR=338 TCF we get the following for US Shale gas where we assume natural gas prices remain under $4/MCF in 2024 $ and NGL less than $27/b. In 2050 for this scenario output is about 17 BCF/d with peak in 2029 at 100 BCF/d.

As far as I know, no pipeline to New England has ever been approved.

Maildog,

From the western direction, New England receives natty via the Algonquin, Iroquois, and Tennessee Gas Pipeline systems.

Not only does Marcellus gas flow through these pipes, the upstream company subsidiary of National Fuel Gas – Seneca Resources – is drilling Utica wells in Tioga county, PA, which might be sending its output farther northeast via NFG’s Empire Pipeline which hooks up to, I believe, the TGP pipes.

The New Englanders shot down 2 large greenfield pipes about a decade back, but incremental expansion capacity continues to fitfully be implented farther upstream which then allows the ‘end of the line’ folks in Dracut to stay warm during brutal winter cold snaps (albeit at very high cost).

Dennis,

So … EIA now speculates the AB will produce ~43 Bcfd in just a few years and go over 50 Bcfd down the road.

Hmmmm. Didn’t I read on this very site a week or so back someone else claiming almost those exact same numbers?

Oh yeah, it was Coffeeguyzz.

There may be little to be gained for you and I to go back and forth on what future natgas production will eventually emerge from the Appalachian Basin.

When super heavyweights like Engelder, USGS, UT-BEG, Patzek, NETL, et al have projections all over the map, we informed mortals are left with choosing in whom to believe.

Although I’ve spent way too much time on this the last couple of days, I will point out a randomly selected 8 well pad (from Range, Washington county) to show why – to me, anyway – I think Patzek is way, way off in his highly sophisticated analysis.

This Southwest cohort – according to Patzek – should have a ~13 year survivability rate. (I still do not understand his Equation #6 referring (?) to a~33% probability rate).

Anywhoo, the Breese Emma Jo pad came online in 2014 with 5 wells showing online production histories of ~10 years except for one (#8) which seems to be having operational issues.

Cums are 3.4, 3.8, 3.9, 5 and 6 Bfd. They presently flow from ~300 to ~500 thousand cubic feet per day which equates to roughly 30 to 50 thousand bucks per well per month gross revenue.

Some tens of thousands of barrels of condensate have been produced from each well, also.

Now, 3 new wells came online 20 months back.

Cums are 7.1, 7.6 and 7.8 Bcf with condensate production of 85,000, 109,000 and 114,000 barrels.

Big, BIG improvement in output.

Again, Dennis, you and I will – most likely – continue our long running stances of holding near 180 degree viewpoints on US hydrocarbon production.

However, should any of the more curious of your readers choose to ‘jump in’ and read the 44 page 2021 NETL report (author Boswell) and compare it to your linked Patzek report, I believe any and all would be highly impressed by the level of expertise that is displayed in both of these efforts.

Paraphrasing Mr. Patterson, Sir Francis Bacon, and many other wise sages throughout history, choose to believe that which you want to be true.

Coffeeguyzz,

The EIA often overestimates future production. In 2006 the EIA’s International energy outlook (IEO) had World liquids consumption at about 111 Mb/d in 2025 where the current STEO expects about 103.5 Mb/d in 2025. For Natural gas World consumption for the 2006 IEO was expected to be 165 TCF in 2025 where the 2023 IEO forecasts 153 TCF in 2025 (in 2024 World consumption of natural gas was 146 TCF.)

You have faith that the EIA is correct, but note that their recent AEO estimate for the Appalachian has 524 TCF produced through 2050. If we assume that’s the peak and cumulative output to tht point is 50% of URR this would imply a URR of 1048 TCF. This is consistent with Boswell if we assume about 68% of TRR is profitable to produce (Boswell TRR is 1400 TCF times 0.68=952 TCF.) To me the Patzek student’s estimates of 300 TCF for Appalachian shale gas are far more reasonable (Marcellus 180 TCF and Utica/Point Pleasant 120 TCF) and also consistent with the 2019 estimates by the USGS.

Well we also have the fact that the Saputra et al estimate for the Marcellus aligns with the USGS estimate. I would also note that usually Boswell has a number of other co-authors on his papers (much of his published work is on natural gas hydrates which is not closely related to shale gas geophysics) the paper you cite is Boswell alone, could he not find anyone who would sign on to that work?

https://scholar.google.com/citations?user=CpW5Jq4AAAAJ&hl=en

Three citations of the 2021 paper

https://scholar.google.com/citations?view_op=view_citation&hl=en&user=CpW5Jq4AAAAJ&cstart=100&pagesize=100&citation_for_view=CpW5Jq4AAAAJ:xGWFX6Gbr9MC

For USGS Marcellus there is this

https://pubs.usgs.gov/fs/2019/3050/fs20193050.pdf

For Utica USGS see link below

https://pubs.usgs.gov/fs/2019/3044/fs20193044.pdf

USGS Mean TRR for Marcellus when cumulative output to Dec 2018 and proved reserves at end of 2018 are added to mean undiscovered TRR is 273 TCF. For Utica/Point Pleasant the USGS mean TRR is 149 TCF when cumulative production to end of 2018 and proved reserves at end of 2018 are added to undiscovered mean TRR. Total TRR for Appalachian shale gas is 422 TCF and ERR is about 283 TCF if we assume that 67% of mean TRR is profitable to produce. Note that the 338 TCF Appalachian Scenario is 80% of USGS mean TRR and is quite optimistic (probably 55 TCF too high for URR).

D C,

couple of cents here about App gas,

1. Utica dry gas part (including so called 2nd/3rd tier where Seneca is improving fast) still way under-drilled to have confidence close to Marcellus. If well-head price goes up to $4/MCF, Utica could be extensively tested and the potential to give ~500TCF close to Boswell iss not totally mission impossible. One could use Seneca as example as Coffeeguyzz detailed, and you find the progresses Seneca made in Novi link, they are drilling in the non-core Marcellus and Utica and the progress is just spectacular. For now, it is still a wild guess without high confidence, same for AOP biased forecast using the liquid-drilling + Seneca non-core results.

2. Marcellus wet-gas part is indeed amazing as Boswell forecasted, and as we discussed before Saputra work was way too outdated to reflect results/progresses after 2019. The Dry gas core part (Coterra) had some down-side in their reserve when they try to add infill and see obviously lower EUR, but efforts to lower cost with longer lateral and larger frac really extends the core area in the NEPA, not just Coterra in Susqueshanna but also other 2nd Tier counties, and again Seneca is the good example, along with Expand(Chk and Southwestern).

3. USGS 2019 forecasts on Utica and Marcellus are for “Undiscovered” and again outdated, and their “Discovered” forecast numbers are even older and further more outdated than Saputra/Patzek.

4. EIA estimates back in 2006, I am surprised that the upside offset to today’s reality is not that huge, compared to other peaker’s 2011 forecast and particularly given the Covid which basically paused all increase by 5~7 years? I had thought the newly released EIA natty forecast in 2050 is a result of Trump and Chris Wright, but now I have to say they are optimistic with caution and solid facts.

Sheng Wu,

I think you are quite optimistic, the USGS estimates since 2013 have been quite good, just because lateral length increases by a factor of 2 or 3 and well EUR improves as a result, does not mean that play TRR changes, it simply results in fewer total wells drilled as the volume of rock that is productive is unchanged.

For Pennsylvannia wells from 2015 to 2021 here are the well profiles for Marcellus, Utica and Point Pleasant wells, point pleasant lowest and Marcellus highest

https://public.tableau.com/shared/5ZD52MMFP?:toolbar=n&:display_count=n&:origin=viz_share_link&:embed=y

I do agree that estimates for Utica/Point Pleasant are highly uncertain due to so few wells having been completed to date.

If we look at only the best 3 Ohio Counties (Belmont, Jefferson and Monroe) for Point Pleasant wells the well profile is excellent with cumulative output of 7290 MCF at 24 months for 403 wells that started producing in 2018 and 2019. For the other Ohio counties with Point Pleasant wells started in 2018 and 2019 (215 wells) cumulative output at 24 months is only 2975 MCF (41% of the best 3 counties). If these 3 counties were filled with wells (10k lateral on 1320 foot spacing) there could be about 3000 wells drilled. The EUR might be about 1.33 times the average well completed to date so if we increase the EUR from 12 BCF to 16 BCF that would cover these core counties with total EUR of 16 BCF times 3000 or 48 trillion cubic feet for URR, whether the non-core areas with average EUR of 6.6 BCF on average are likely to be fully drilled will depend on natural gas and NGL prices. I certainly think any assumption that these other counties besides the big 3 will be blanketed with point pleasant wells is far fetched.

So far for WV and PA the drilling in Point Pleasant has been very limited, some drilling of Utica in PA but also quite limited relative to Marcellus. The results from county to county have been highly variable and no doubt this is true within counties as well. The Patzek and students analysis for variuos shale gas and tight oil plays has been very good so fat and generally agree with the USGS assessments published since 2013 for Bakken, Permian, Haynesville/Bossier, Marcellus, and Utica/Point Pleasant.

The Boswell analysis seems problematic with very high EUR estimates (50 year well life with assumed terminal decline of 6% which does not match with reality).

COFFEEGUYZZ,

Just read Saputra 2024 paper on Marcellus and indeed there is the intriguing Equation 6, and the hard to believe 13 year survival rate for SouthWest cohorts, and the subs in figure 11 reads something more astonishing –=- “For instance, in the northeast core area,only 75% of wells completed in 2009 survived afte r11yr. The newer wells survive

less longer, so that the average survival probability is only 52%.

Finally, from a parabolic extrapolation, we obtain the maximum

time of well survival of 14 yr”.

Sheng Wu,

Yeah, I was so taken aback by the outlandish claim that Marcellus wells have a lifespan of 13/14 years that I was certain that I must be misinterpreting what Patzek was saying.

Consequently, I meticulously pored over every scrap of info that was presented, including footnotes, formulas, various definitions/stated parameters, yada yada.

While I was inclined (still am) to label the entire effort just ‘dressed up’, contrived bullshit, I decided to dig deeper and glean the actual production numbers/drilling histories of some NEPA and SWEPA counties to see how Patzek came to the absurd analysis that he presented regarding well survivability and lifespan.

Seems like he must have lumped in all the dry holes and drilled-but-never-producing wells along with the ‘normal’ producers we have today.

The degree of distortion that this ploy introduces to honest analysis is profound as Susquehannah county has over 100 plugged wells (mostly early vintage) with 69 being non producers and most of the remaining 32 being virtual dry holes (understandable in the early, wildcatting days).

Same for Washington county with 60 plugged total, 13 being non producers, all of the remaining 47 being dry holes.

Tioga county’s 171 P&A wells undoubtedly contain many of the older cohort that likely were included in the ‘drilled’ or ‘completed’ or ‘developed’ categories that can now be presented under the labels such as “wells from 2010” or some such.

Honest observers such as Dennis are susceptible to being misled by these types of (nefarious?) approaches.

FYI, Sheng Wu, the site Marcellusgas.org contains the complete drill/production/permitted histories of every Pennsylvania horizontal well dating back to the Renz 1. 20 bucks first year, 10 bucks annual thereafter.

Outstanding resource.

Coffeeguyzz,

An honest analysis looks at all of the drilling results, not just the above average wells. Note that the results you see in investor presentations drops the bad wells ond only considers the best wells. In the real world there are costs to failed wells and poorly performing wells, dropping them from the analysis gives a distorted perspective.

Dennis,

I am starting to wonder if you are just stringing me along here.

Of course all wells should be included in any analysis.

If the prior statement “~460 out of ~665 Marcellus 2010 are still producing” includes ONLY about 450 of what might be considered normal, productive wells, about 10 that were producing and then permanently shut in for whatever reason, and the remaining 215 were essentially dry holes and thence plugged … a HUGE difference in ‘analysis’ would be called for rather than making a sweeping generalization that “2010 Marcellus wells have a (fill-in-the-blank) lifespan” based on this cohort with an astronomically high level of non-producers.

Yes, include them all.

Yes, describe how ~20% were dry holes (precise numbers are accessible for anyone wanting to wade through them. This 20% figure roughly syncs with the ~200 Developed/Permitted pre-2012 Pennsylvania horizontal well profiles that I saw.)

Yes, ABSOLUTELY include the <5% that were producing and then plugged. If possible, determine the most plausible reason for the plugging. I found exactly 3 wells – out of ~200 – that were producing minimal amounts after years of respectable output and were thence permanently shut in.

If you – or anyone – thinks presenting the proposition that about 1 out of 3 'typical' Marcellus wells 'goes dark' after 13/14 years online is an accurate assessment, then you are either wildly delusional or – in the specific case of the author of this report – possibly motivated by some other factors beyond objectivity, accuracy and honesty.

This is my final post on this topic, Dennis.

Like many others, I appreciate the efforts of Ovi, Mr. Patterson , and yourself in keeping this site a'runnin'.

More attention on the Gas World might be of benefit to all as your whrleys are lookin' like they need some he'p keeping the lights on.

Should we understand that they reinvented the concept of “renewable” natural gas resources in the subsoil? The Soviets assumed that hydrocarbons are generated by abiotic processes (= eternal resources of oil and gas). Moreover, this prompted them to look for evidence of the existence of natural hydrogen emissions (no hydrogen, no production of hydrocarbons from CO2) on their territory and that, in fact, they found, even if it has no direct relation to hydrocarbons. In fact, it would seem that the flow of hydrogen in the crust participates in the maturation of oil. Hence the observation of the absence of hydrogen flow in the immediate environment of oil deposits.

haha, blame oil and gas for supression of Hydrogen in nature?

The hydrogen isotope of oil and gas are not supporting this idea of crust hydrogen participation of oil and gas maturation.

The initial guess of the giant Urengoy gas field (1/3 of the global gas reserved in the 1980s) is the result of abiotic or biogenic, but later carbon isotopes of C123 solved the mysteries — they are thermogenic decompositon of organics 100s of millions years ago.

Permian Basin fracking falling faster than expected

This fracking company is losing money.

Fracking in the Permian Basin is declining faster than expected due to tariff uncertainty and OPEC+ production hikes, ProPetro (NYSE:PUMP) CEO Sam Sledge said Wednesday, according to Bloomberg.

There are now ~70 hydraulic fracturing crews working in the world’s largest shale patch, down from as many as 100 at the start of this year, Sledge reportedly said on the company’s earnings conference call.

“The completions market in the Permian Basin continues to face challenges,” the CEO said on the call. “Increased market uncertainty driven by tariffs and rising OPEC+ production has resulted in more idle capacity than anticipated.”

ProPetro (NYSE:PUMP) -13.1% in Wednesday’s trading after reporting a surprise Q2 GAAP loss and a 9% Y/Y decline in revenues to $326M.

https://seekingalpha.com/news/4474549-permian-basin-fracking-falling-faster-than-expected-propetro-ceo-says

Ovi,

The steep decrease in Permian Basin horizontal oil rigs since March (roughly a monthly decrease of 8 HORs per month) is likely to result in a big drop in completions over the Sept 2025 to Jan 2026 period (assuming a 6 month lag between start of drilling and first flow from the well). This would translate to a drop of 36 completions over 3 month period and if the horizontal rigs continue this rate of decline for an entire year (annual rate is about 94 rigs per year) the completion rate would drop by about 162 from about 460 per month recently to 298 completions per month in Sept 2026. Not sure it will get that bad, but if oil prices drop as much as forecast in the July STEO it seems a possibility. Scenario for Permian with these assumptions below, completion rate constant from Sept 2026 to Dec 2035.

US May Oil Production at New High, Barely

US production up by 24 kb/d. GOM biggest gainer offset by biggest loser ND.

EROI

in simple terms EROI tells us how many man hours of work do we get out of a fuel that take one man hour to acquire.

In the 1950s the greatest return was achieved from oil, one man drilling for oil would produce the oil equivalent of 50/80 men working full time. An incredible source of power, which was used to build roads, homes, power for tractors and so much more.

Coal is just as great a source of power, one miner could dig an amount of coal which would do the work of 80 men or more. It powered the Industrial Revolution, enabling the manufacture of millions of tonnes of steel for rail, bridges and buildings.

Gas was the best, with an EROI of up to 100 to one.

https://jpt.spe.org/plummeting-energy-return-on-investment-of-oil-and-the-impact-on-global-energy-landscape

However EROI for all these wonderful fuels has been falling globally for decades. What took one man to produce enough oil to replace 80 labourers now take 4 or 5. This increase in effort required explains why oil prices have increased from lows of $12 a barrel to $70 and more.

The declining EROI has been hidden by ever increasing oil production, but that is coming to an end.

Analysis of declining energy return suggests that we are already at peak energy return for oil. The days of more and more energy slaves to help us are over.

The same can be found for coal, with a few exceptions, coal is becoming harder and more costly to mine. EROI from coal is down from 80:1 to around 20 or 30:1 and will continue to fall. When coal production peaks we will have to replace not just the declining tonnage but the falling EROI also.

Gas is the same, unfortunately this fact is hidden by reckless overproduction at the moment. This happy situation of lots of gas, low prices and massive amounts of money pouring in from exports will soon reverse.

Lower gas production, increasing costs poorer energy return will hit hard and faster than most people realise.

If this was not bad enough, droughts are rendering millions of hectares of land unproductive without irrigation and this adds considerable additional energy needs to farms all over the world.

Ridiculous statements such as energy requirements per GDP are falling fail to understand the basic needs are water and food. Both of which are needing more and more energy and chemical inputs to deliver. All with a global population that has increased by the equivalent of 70 SAN Francisco last year and the same this year.

This is why along with large increases in wind and solar, coal, gas and oil have increased greatly in the last 10 years.

With EROI peak and a continued increase in population we are now in a new reality of an ever shrinking pie.

Peak water and peak EROI are already impacting food prices and this will only get worse.

Intuition tells me that you are correct, sir.

what about nuclear power plant EROI?

Sheng Wu,

Any insights on what the EROEI for a nuclear power plant is? Chat GPT says 50-70 for light water reactors, does this seem reasonable?

DC,

my chatbot says 75:1 for nuclear power plant

from my AI source.

The energy return on investment (EROI) for nuclear power varies significantly depending on the study and methodology used, but generally falls within a range of 20 to 80. Some studies have found lower EROIs, even below 1, while others, particularly those focusing on centrifuge enrichment, estimate it to be as high as 40 to 60, according to the World Nuclear Association. This wide range is due to variations in how energy inputs (like mining, construction, and fuel enrichment) and outputs (including waste heat) are accounted for

Who’s making the huge profits from the 20-80/1 EROEI being reported by these AIs??

If a machine costs 1 to build and operate but returns say 50 times that amount, then someone is making a huge return on this, so who?

If the answer is no-one is making a huge profit, then the initial assumptions and methodology of working out the EROEI has to be incorrect.

There are several reasons why that argument doesn’t hold:

1st, E-ROI is very different from $-ROI. When you say “If a machine costs 1 to build and operate but returns say 50 times that amount,” you’re talking about $-ROI. Even with energy production, labor costs are more important than energy costs. So E-ROI doesn’t tell us very much about $-ROI.

2nd, someone is making money: the consumers. Wind and solar investments and production and pricing are far more competitive than fossil fuels. They’re manufactured and the manufacturing business is incredibly competitive and ruthless, especially in China where solar and wind producers are losing money hand over fist, just as early auto manufacturers lost money until most producers were forced out of business. So oil producers make money because they’re operating in a monopolistic environment where OPEC can restrict the supply and keep prices higher than they would be otherwise. Renewable manufactures don’t have that advantage, so their industry isn’t nearly as profitable.

Here’s the basic principle: in a monopolistic market reduced costs mostly benefit producers. In a highly competitive market reduced costs flow to consumers. This is, or course, why Adam Smith said that whenever producers in any industry get together, the first topic is how to eliminate competition.

3rd, EROEI is a very misleading ratio.

If EROEI goes from 100:1 to 50:1, that sounds very important, right? But it’s a change from one unit of input for a return of 100, to an input of two units.

Let’s take an example simplified for the sake of illustration: you’re drilling a well, and it takes 1 gallon of diesel to produce 100 gallons of oil. Let’s say diesel costs $2.50, oil sells for $60/barrel (or $1.50 per gallon), and it takes $30 of labor to produce a barrel of oil. That means that your cost is $31 (labor plus .42 gallons of diesel for your 42 gallons of oil). Now….EROEI goes to 50:1. What’s your new cost? It’s $32. Not a big change.

And…at 100:1 you start with one gallon and end with 99 gallons more. At 50:1 you start the day with 2 gallons, and at the end of the day you’re left with 98 gallons more. A 1% loss – not much. Certainly not a 2 to 1 change. The same logic applies to smaller changes: going from an EROEI of 50 to 15 sounds like a very big deal: it appears to be a 70% reduction! But it’s not: you go from 98% net energy to 93% net energy, which is a 5% reduction.

EROEI is not very useful. Cost is useful. Net energy is somewhat useful. But EROEI is mightily misleading.

Iver

Are you familiar with the two more recent pieces of work on EROI below? They are helpful in their use of consistent approach to analysis of boundaries to compare EROI. The work by Aramendia et. al. focuses on useful stage energy rather than the old ‘well head’ type of approach. Similarly, Murphy et al attempt to implement ‘methodological consistency’ to compare EROI at point-of-use.

https://www.mdpi.com/2071-1050/14/12/7098

https://www.nature.com/articles/s41560-024-01518-6

Comments on the 914:

Oil:

1. Overall, USA up slightly to new record at 13,488 thousand bopd. This is up 20 from last month. (Itself revised down 4 thousand bopd, if memory serves, did not check.)

2. Not sure what prices were like back then and shale is rather responsive. We are/were probably near a sort of equilibrium price. They just went up a few bucks, from tarriff/sanction jitters, but the long term outlook is more mid 60s.

3. FGOM up a fair amount, but it is very classic megaproject oil. Driven by long ago project timelines as well as hurricane up/downs. Definitely hanging in there a lot better than the naysayers (e.g. Kaplan) thought a decade ago. Still remember him laughing at EIA. Not just having a different outlook, but saying he couldn’t conceive how they differed from him. (Maybe he should figure out…might help any future work of his. Then again, peakers don’t actually rethink their methods/biases. Just shift the goalposts and pat themselves on the back for “adjusting to facts”, when they didn’t really adjust enough, didn’t consider the flaws of their approach itself. In his case, the detail-filled bottoms up field stacked area charts. Where I truly commend his knowledge, but criticize the lack of self reflection, when the EIA top down assessment did better than his bottoms up work.

4. ND down a fair amount. Prolly weather. Donno. Should be getting warmer, but maybe mud season? I anticipate a rough flatlining, with summer up and winter down. ND already kicked my ass last time and validated Ovi. [Hangs head in shame and bends over for wet noodle whipping.] I don’t think it will fall off a cliff (not a doomer). But it will sort of flatline for a long time. Ah well…we’ll always have those memories of the 2012 man camps! And Rune Red Queen. And Piccolo. (TOD writers.)

5. TX and NM almost flat.

6. Little MT passing LA. Mwahahahaha!

7. Oh…and look at OH! Another record. I love that App production!

————

Gas

1. Up slightly (0.1 BCFD), but almost flatline. If we look at lower 48, exclude the AK confounding, it is up 0.2. Still almost flat. Not bad for heading into summer though.

2. LA continues to increase. Very interesting. And amuses me with the David Hughes and Art Berman and Tad Patzek types who said 10-15 years, Haynesville was post peak and that shale gas was a mirage. Kaboom! Facts…crushing them.

3. Rest of the states not much interesting.

When do you think US oil production can get to 15,000 thousand bopd?

Never, at current prices.

At $100/bbl, 18 months.

P.s. https://www.youtube.com/watch?v=wRxHYHPzs7s

Something that is underappreciated about the GOM is the “staying power” of alot of the big, old legacy fields like Mars-Ursa (still over 140 kopd), Thunderhorse and Thunderhorse North (over 140 ), Tahiti-Caesar Tonga (around 110), Mad Dog (around 120), Jack-StMalo-Julia (around 120). If you look at GOM drilling activity, alot of the activity is in these fields- helping to maintain production.

The new projects like Anchor, Whale, Ballymore and Shenandoah also help arrest decline and lead to some increases.

Chart of production from those fields going back to 2020.

Thanks Bob,

I assume this is more than you expected in your mid-case scenario, am I correct?

Looking back on your update in 2022, perhaps this aligns better with your high case scenario.

Dennis,

The fields/field complexes that I highlighted above are maintaining production a little better than I thought they would 3 years ago. I thought Mad Dog would be higher now (because of Mad Dog 2, which has, in my opinion, underperformed a bit), but all the other fields have more than offset that.

In 2022 my estimated midcase EUR for the GOM was 36 billion (range from 31 to 42). Now, it’s 37 billion (range from 32 to 42). As time goes on, this range should narrow down, right!

In 2022 my projection for 2025 production was 1.7-1.8 mmbopd, which is pretty much in line with what we’ve seen so far in 2025.

Thanks Bob.

Hope all is well.

Amazing that majority of these deep water GOM fields have medium density oil (API 27~32deg), and GOR should also be lower ~300scf/bbl and yet they could have upside EUR.

NGL production continues to climb.

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=M_EPL2_FPF_NUS_MBBLD&f=M

1. New record at 7.4+ MM bopd.

2. There is some seasonality, but if you look at yty, it’s still up a little over 0.4 MM b(stuff)pd. This is normal…has been climbing 0.5 MM bopd/year for many many years now. Stronger growth than C&C, or dry gas, or wet gas!

3. Note that this is ALREADY a part of the 914 wet gas. However, of course, if you eschew looking at the 914 wet gas reports and look at dry marketed, than you need to look at NGL in addition. It’s actually more valuable than dry gas (and less than C&C). I guess you can also look at marketed, wet. I’ve never bothered…for one thing, you can’t look at state to state trends then.

That’s Great News.

– Ethane occupies the largest share of NGL field production. It is used almost exclusively to produce ethylene, which is then turned into plastics. https://www.eia.gov/todayinenergy/detail.php?id=5930

I couldn’t imagine a world without plastic and plastic bags, just imagine the expense of having to go back to biodegradable paper wrappings? We wouldn’t have the trees left to make them anyway. A polluted environment is a small price to pay.

I find most of the peak oil movement is driven by environmentalism bias. Look at how the Post Carbon has pivoted from being mostly about peak oil to mostly about reducing consumption.

It’s fine to be pro environment. But you should not let it affect a rational estimate of reserves. IOW, just because you hate it, doesn’t mean we are running out. (Look at coal for example!)

In theory, the peak oil fad was about people doing amateur reserves analysis, and just coming up with low numbers. But it really wasn’t some unbiased, scientific assessment. Instead it was driven by “wishcasting”.

That’s why I respect Monbiot who said “I was wrong…there’s enough to fry us all!”

Could you explain the rationale behind your estimate of reserves?

Humility? ;-0

I don’t set myself up as an oracle and am skeptical of those who do. I do value having people make estimates. Gives me something to critique and consume. But even then, I take it a lot better when the people doing so, have appropriate caveats about uncertainty and their level of expertise. And not just after making a bad call, but when making new ones. Unfortunately, there is a lot of demand for feeding the lowest common denominator readers…and that market wants red meat, not caveats and not Bayesian (even casually Bayesian) formulations.

Note: this is not just a peak oil issue. But applies in politics and political blogs/Twitter. It is a very well known thing called “wishcasting” that opinion writers of either left or right wing will generally make predictions that are biased in the direction of what they want to happen. (For the few that don’t, they are reviled and called doomers!)

You will see the same thing on Ukraine war blogs/chatter, with both sides having the less reflective writers and content consumers biasing their reporting and predictions in the direction of what they want to occur and the more reflective and objective writers being called doomers.

You see the same thing on sports blogs/Twitter. With fan writers and readers routinely overestimating the probable success of their teams. (In this case, the betting markets give a valuable external comparable.)

“It’s fine to be pro environment. But you should not let it affect a rational estimate of reserves. IOW, just because you hate it, doesn’t mean we are running out. (Look at coal for example!)”

Well anon, I’m not really pro environment, I was just pointing out where those hydrocarbons go and the consequences. NGL’s don’t go into transport fuel, so in that sense you can’t count them when you consider our peak oil dilemma. They are accounting smoke and mirrors, nothing more. Just because you hate the idea we are running out of transport fuels won’t stop them running out.

They are a co-product. Look at the classical economic study of chlorine production (with caustic being the co-product). Gas (and rich gas) is a co-product that (generally, assuming you have pipeline outlets) supports oil drilling.

I do agree that (mostly) NGLs are a petrochemical (“plastics”) feedstock. And of course natty is mostly going into heating and electrical production. I.e. both mostly not transport uses.

“Just because you hate the idea we are running out of transport fuels won’t stop them running out.”

Certainly…me “hating the idea we are running out” won’t change what will happen. Uh…greed! 🙂

Similarly, greenies loving the idea of oil scarcity won’t make it happen. That’s why I brought up the example of coal. You probably super hate the coal! But at least you realize that doesn’t stop there from being a lot of it. Remember Jimmy Carter saying the US was the Saudi Arabia of coal!?

It’s important to try to disaggregate what you want to happen from what you think will happen.

And to be sensitive to those (from whatever direction) who allow their biases to affect their forecasts. That goes double on commented blogs or forums or Twitter where there is a social dynamic and feedback from the various echo chambers of left/right bias.

many plastic bags now are bio-degradable

Actually you can look at state output of marketed natural gas and this is the number that reserves are based on.

see https://www.eia.gov/dnav/ng/ng_prod_sum_a_EPG0_VGM_mmcf_m.htm

and for reserves see table 3 at

https://www.eia.gov/naturalgas/crudeoilreserves/

Nice. Thanks.

D C,

Thanks for the links from EIA.

These are proved reserve numbers, and therefore much lower than TRR or URR numbers, i.e. Utica probably could give 100TCF forecast TRR by AOP paper, or USGS undiscovered nearly 100TCF P50 in Utica, but here only OH has about 30TCF proved reserves and almost all in Utica.

Amazing that the WV PA proved reserves is already ~150TCF (2022~2023), and most are Marcellus, and therefore,

1. with the already ~50TCF produced by 2023

2. the undiscovered P50, e.g. the 2019 USGS P50, and the already produced,

The TRR could easily close to 300TCF for Marcellus?

Sheng Wu,

For the 2019 USGS Asssessment we would use proved reserves and cumulative production as of Dec 31, 2018 and then add that to mean undiscovered TRR to arrive at a TRR estimate.

https://www.msn.com/en-us/money/markets/chevron-entry-to-guyana-oilfields-solves-companys-top-challenge/ar-AA1IRVDL

After Trump boots Chevron out of Venezuela

HOUSTON (Reuters) -Chevron’s imminent entry into Guyana’s rich offshore oilfields solves one of the biggest problems dogging the U.S. major: where its growth will come from beyond the next few years

US Natural gas has become wetter over the 2010 to 2024 period, perhaps due to increasing shale gas output. From Jan 1997 to Dec 2006 about 35 barrels of NGL were produced per million cubic feet of natural gas produced, in the most recent 12 months NGL output in b/MMcf of dry natural gas had increased to 68, nearly double the earlier period.

Nice chart. Agreed, you can see the associated gas effect, with a lot of rich gas, from 2010 forward, as the US went through an oil production boom. (Along with other effects like gas decaying faster than oil, so replacement drilling at 13ish MMbopd from 2019 to now, has still resulted in growing rich output gas, along with, perhaps LTO having more ass gas than medium/heavy crude, maybe also some rich fields on their own like the south Marcellus and Eagle Ford.)

Of course this means that marketed wet gas has become MORE valuable, not less. As generally NGLs are intermediate in value between dry gas and C&C. So, it’s actually more of a feature than a bug that the extracted gas is “full of NGLs”. (Not saying you don’t realize this…more for the hoi polloi.)

P.s. The other thing going on for NGL growth is not only has the “wetness” been increasing (NGL/dry), but dry itself has grown as well. So, the NGL growth has sort of compounded from these two effects. [And not saying you don’t realize this. Just my own realization, looking at the chart and wondering why it was less dramatic than the NGL absolute growth.] https://www.eia.gov/dnav/ng/hist/n9070us2a.htm

Nony,

Agreed, I created the chart because when I look at NGL growth it is even faster in percentage terms than the natural gas growth (which has been phenomenal since the tight oil and shale gas boom which started around 2007 or so.)

Nony and D C,

probably the faster NGL than dry gas is a combination several factors,

1. the shale oil production getting gassier, and this brought up more NGL, particularly the C4+

2. the prolific wet gas/condensate producers in WV+PA (Marcellus) and OH (Utica).

3. depressed dry gas price

Mike Wirth, Chevron Chairman and CEO states Chevron has reached plateau in the permian of a million barrels per day and can maintain it though the end of next decade with less than past prior investment and increased cash flow.

https://www.youtube.com/watch?v=bye__9Y5LXQ

Chevron Hess deal finally closed. While I had thought the synergies with Exxon were much higher, in both Guyana and the Bakken, it may be that XOM prefers to have an offshore partner and manage nationalization risk.

Not sure how CVX will approach the Bakken assets. It is not a premeir asset but is quite sizeable and is medium quality within the basin. E.g. divest, manage normally, or even aquire more. Any chatter here?

Nony,

Bruce Oksol just floated the idea of either Chord or Harold trying to buy Hess’ legacy assets (463,000 net acres).

Makes sense, especially if/when EOR starts to take hold.

1. So you are in the divest camp. CVX will keep the offshore assets and ditch the Bakken. Could be and makes sense. If so, they will just sell it to whoever pays the most. Little hard to predict that, but the two you mentioned would be possible buyers…definitely people that Goldman would send a prospectus to! 😉

2. It’s 2025. I been hearing about this shale EOR for 10-15 years now. When is it actually going to become something more meaningful that EOG PPT hype? 😉

Trump to fire BLS commissioner after bad jobs report

Is this a sign of what is to come as CPI gets worse and Oil production starts to drop?

https://thehill.com/homenews/administration/5432523-trump-fires-bls-commissioner/

Nothing new here. The right side of the political spectrum in the US is increasingly uncomfortable with math and science that does not conform to their ideological preferences.

https://www.nature.com/articles/s41562-025-02147-z

https://www.pewresearch.org/science/2024/11/14/public-trust-in-scientists-and-views-on-their-role-in-policymaking/#:~:text=Democrats%20continue%20to%20express%20more,making%20policy%20on%20scientific%20issues.

Yes, when oil production starts to drop it will (again) be blamed on environmentalists and regulators not letting industry drill.

T Hill,

When oil production or natural gas production drop, the Energy Secretary will be fired. Obviously nothing can be Trump’s fault

hope GOA oil and ABEH gas could help Chris Wright keep his job.

Oh, yeah. I voted Republican. I must not know how to do any math or science or engineering. I do stupid things like adding 10 plus 15 to get 25.

Oh well…I guess all the NPR-listening midwits can dazzle me with their science. Oh wait…that should be upper case “Science”. Need to venerate it, like a religion. A tribal religion. For the “Fresh Air” NPR listeners and Woordle-playing NYT readers.

[Not saying everything should be for me, just expressing a thought.]

I (and perhaps others) would have value for a “for dummies” explanation of GOM production. Not even the whole peak oil thing…but the explanation of areas and fields and operator and all that. With a reasonably long span of time and areal extent. Honest, it’s a blizzard of Wardogpighammer names, which I lack a feel for versus how I have a feel for different shale basins. Yes, I realize the FGOM experts know this stuff, but I bet most of the readers are, like me, in need of a dummies “who’ who in the zoo” primer first.

——–

And please…not the field by field stacked area charts! It’s a miserable format for actually conveying information. Dennis’s single line charts are much more beautiful and convey insight better. I do some investor/CEO MBA-ish style communications…and really stacked area charts are reviled. Maybe not quite as bad as 3-D columns, but…uck.

Stacked area charts are sort of show-offy in detail (many series, lots of time granularity), but the reader can usually only really read the top/total, unless there are three or even just two series. It’s also, often unclear (and unthoughtful) on how the series are ranked (e.g. largest on bottom). So you are really not conveying an illustration of a message. You’re blasting all kinds of detail, which the reader can’t actually parse (like what the middle series is doing over time). Like who really cares that we had a hurricane in JUL in 2008 and one in OCT in 2010? (Made up example.) Or even worse that the Manbearpig field recovered from the (made up) JUL08 ‘cane in AUG08, but the Umptifratz field didn’t recover until DEC08. It’s data overload, not relevant in retrospect, and not even readable given the stacking format.

You’d be better off with more separate charts/discussion rather than the all in one 20-color area chart with monthly data. Like honest…many individual charts (along with thoughtful discussion) rather than the omnibus area chart.

Line charts are generally more useful. If stacked charts must be done, the series should be kept to a small number (for example by grouping into categories) and the time granularity should be reduced to years (in which case, show stacked columns). Also consider to just show a line chart with several separate lines (as a separate and second chart, after the total over time).

Maybe my GOM summary from 2022 would help.

https://peakoilbarrel.com/2022/05/

The stacked field production chart above was to illustrate the point I made that the production from these fields/field complexes has remained pretty flat since 2020. The chart illustrates that pretty well – sorry if the field details are confusing, but, I suspect, if I hadn’t shown the field details, someone might have asked “What are the field details?”

At a quick look, the charts seem WAY more readable than Kaplan’s 20-color stacked chart things. Will take some time to read it.

Really…I think the primer is more needed for now than an “update” (emphasis on recent events) or a prediction. I’d also like some sort of super simple “getting arms around the basic” like TX/LA/FGOM categorization. Like operator 100% chart. Like 100% categorization by depth. (Current view would be fine here. Perhaps a time series makes it too complicated.)

Even for the “name blizzard” of fields some branching tree hierarchical organization/table would be helpful (probably with higher level plan view area as the controlling variable, not depth or strata or operator. After all the “where” on the map, sort of drives infrastructure.

Nony,

Search on Bob Meltz Peak Oil Barrel and SouthLAGeo Peak Oil Barrel, he has done at least 3 posts, maybe 4 and all have been excellent in my opinion.

Will do. And I guess, I could look at other resources (outside of this site) as well.

Nony,

Yes, just pointing you the sources here, there is also much info at BOEM, if you look at the comments for Bob’s posts there is some discussion about this and links to BOEM reports. No doubt there is more out there.

Regarding the EIA projections of APP gas growth, I think they are unreasonably high, but not for Dennis’s reasons.

The reason why growth has been limited for the last several years is that demand is constrained because of the difficulties piping gas out of the basin, along with the lack of growth of local demand. This is clear as day if you look at how low local prices are for gas in the App! It’s not flatlined because of lack of resource. It’s flatlined because the pipes are full and the Donks won’t let more get built. Look at the many large pipeline projects that the greenies were able to kill. Constitution, Atlantic Coast, etc. etc.

I think EIA is underestimating the future difficulties in getting those pipes permitted. Their process sort of assumes that if there is not a hard law against something that the infrastructure will get sorted out in time, driven by economics. But we already have 10 years of experience with the Northeast showing this is incorrect.

I do think their LNG growth/location projection is reasonable. (After all, there will be no more Atlantic LNG projects…and even if you COULD get one built in a blue/purple Midatlantic state, you couldn’t get the new pipes needed to supply it! But I think this Gulf Coast demand will be met more by production from TX/LA, perhaps with a slightly higher projected increase in Henry Hub. There’s a lot of local resource in the EF/H that comes on as the price goes up…it’s a resource pyramid.

We’ve had the discussion before about the App and I disagree with Dennis’s pessimism. Think the crazy high resource estimates are the correct ones. Patzek and USGS have a long history of underestimating shale. And analysis of App resource based on history of drilling density (essentially the implicit methodology of USGS, with a hidden economic variable) is very much confounded by the very low regional prices. So…App basin will grow slower than EIA predicts. But last longer than Dennis predicts.

IOW, sort of the opposite of the Roy phenomenon. A dimmer light, lasting a long time!

https://www.reddit.com/r/bladerunner/comments/g7qojz/the_light_that_burns_twice_as_bright_burns_half/

P.s. Neither do I think that local demand will grow that significantly either. Bitcoin is a Ponzi scheme and an environmental affront that is more wasteful than flaring!

Nony,

I agree demand may be the main problem currently, but I also think that as demand expands the gas production increases will be limited as the resource is more limited than Boswell’s paper projects (it uses unreasonably high EUR estimates). Welllife is assumed to be 50 years, not happening for a horizontal well with high cost downhill repairs knocking out any well over 15 years old.

The USGS prediction for the Bakken/Three Forks in 2013 was quite good and the Eagle Ford and 3 Permian assessments were also pretty good or perhaps too high. The EIA AEO 2025 has Appalachian natural gas output at about 700 TCF (assumes output goes to zero linearly to zero by 2070). My scenario is about half that based on my best guess for tight oil plays vs USGS estimates where ERR tend to be about 62% of TRR on average, You are wrong that the USGS usually underestimates, this only happens when they have very little production information.

Marcellus/Utica midstream companies can build pipelines to places other than the Northeast, to mid Atlantic coast, Midwest, etc, lots of Republican territory where the natural gas can go, The could Build a pipeline to the Gulf coast, though I tend to agree it may be hard to compete with Haynesville/Bossier.

Bottom line, since 2013 USGS assessments have been pretty good or perhaps a bit on the optimistic side (if one makes the incorrect assumption that 100% of TRR is a likely outcome.) So I am sticking to my guns here, the EIA is being too optimistic both on the supply and the demand side.

You were using USGS estimates as late as 2018 (even if done pre 2013), that ended up being dramatically wrong. The whole Permian fiasco of your science presentation having been just (a month before) doubled by a USGS revision, in 2018. Unless you have some process to prove when to trust a USGS estimate and when not to, I am skeptical of your idea that they are now OK. Certainly, it is fair to say that you relied on USGS at times when it did end up proving unreliable (despite being warned of the possibility of upward revisions). Maybe you’ve learned your lesson now, but a vague “they are good now” doesn’t give me a warm fuzzy, given your inability in the past to tell when they could be trusted and when not.

In particular, I think the issue is basically related to “maturity” (loosely defined). So, the Bakken was closer to maturity than the Permian was (hence the revision of the Permian, with the Bakken having a similar forecast). As the App has been pipeline constrained, I don’t think the USGS methodology, relying heavily on past density of drilling, is likely to be effective.

Even for the Permian, I would maintain some wide bars of uncertainty. For one, that area has very significant geologic complexity, with different strata and the like. For another, I don’t think (correct me if I’m wrong) that we’ve had the sort of “two in a row” estimates like we had for the Bakken, yet. So, how do you know we’ve really converged yet?

And while the App, I guess, has sort of had that “two in a row” estimate, I remain skeptical given how much their methodology relies on past drilling density/fairway considerations, given how much the basin is export capacity constrained. This is especially important for the Deep Utica which has much lower drilling history, still very early in its story, to define it’s ultimate fate. This is especially so as it is a formation that has a high cost and high return (so potentially very high extra capacity to come on, given price increases).

The approach that USGS uses is essentially to say “this is the expected EUR of a well” along with “this is the expected drilling density”. This approach has a lot of uncertainty when you are dealing with new provinces. And the Deep Utica (despite all the hype and article) has very low numbers of wells, for a resource play.