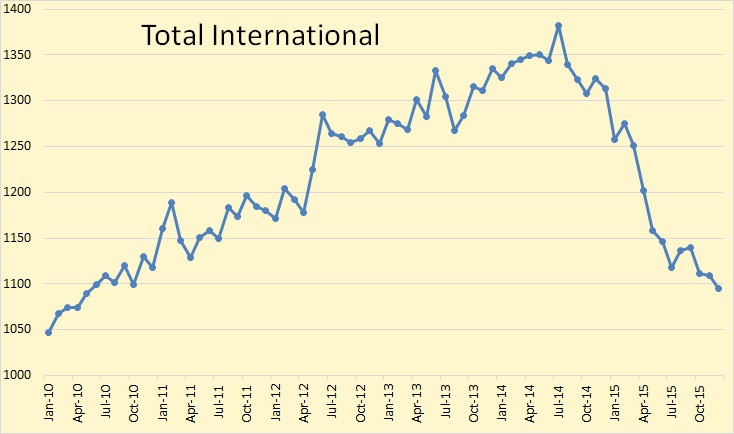

The monthly Baker Hughes International Rig Count came out a few days ago. Baker Hughes international rig counts do not include US, Canada, FSU countries or on shore China. All rig count data here is through December 2015 and includes all rigs, gas, oil and misc.

Total international rig count was down 14 rigs from November to December. From December 2014 to December 2015 rig count was down 218 rigs or 16.6 percent.

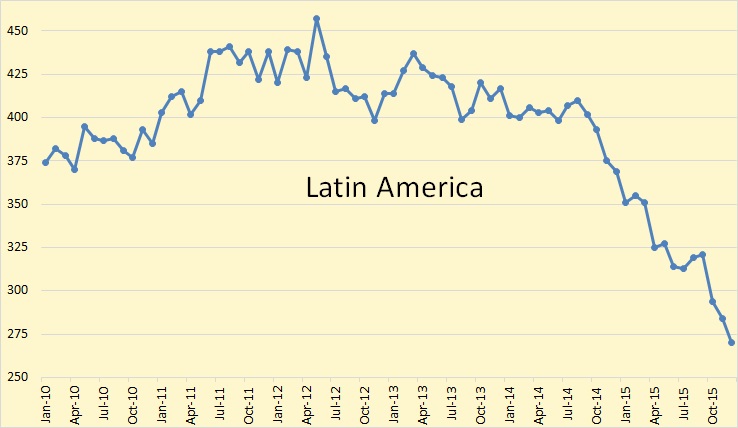

Latin America was down 14 rigs from November and down 99 rigs or 26.8 percent since December of 2014.

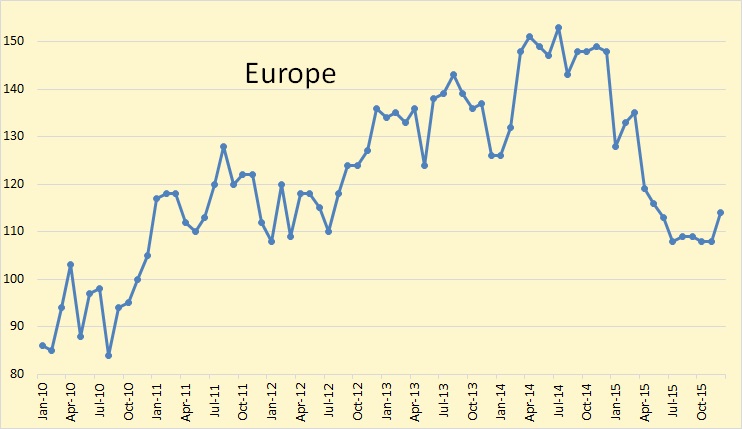

Europe was up 6 rigs in December but down 34 rigs from December or 23 percent from December 2014.

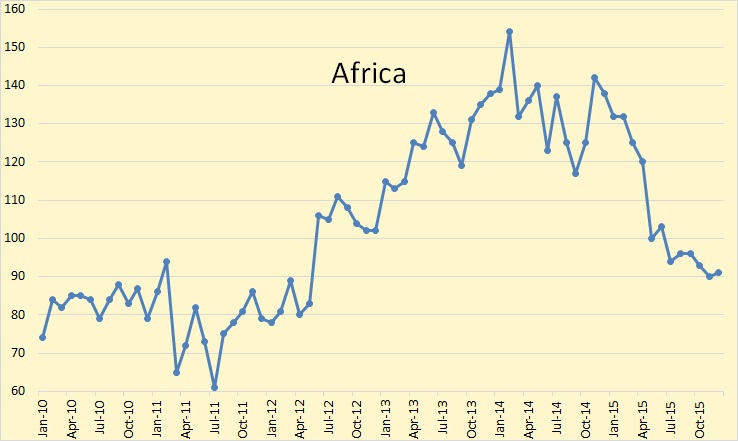

Africa was up 1 rig in December but down 47 rigs or 34.1 percent since December 2014.

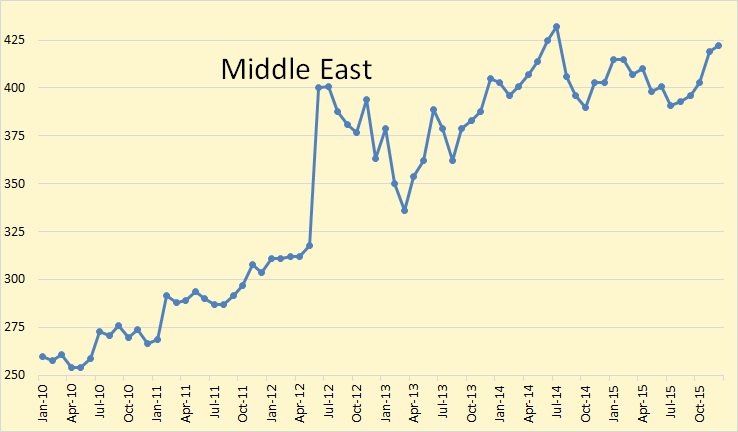

The Middle East was up 3 rigs in December and up 19 rigs or 19 percent since December 2014.

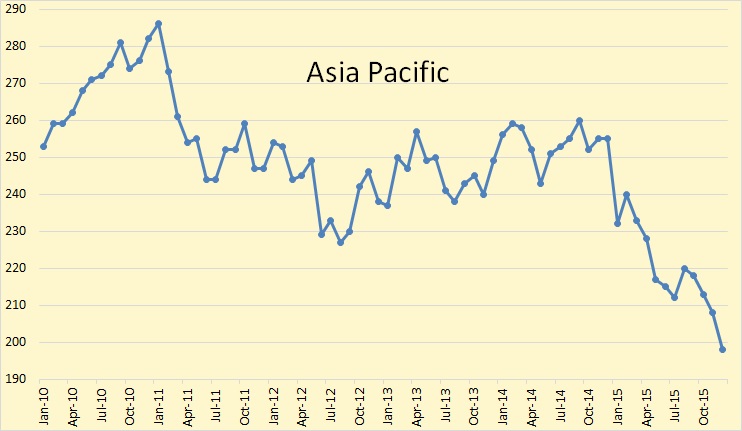

Asia Pacific was down 10 rigs in December and down 57 rigs or 22.4 percent since December 2014.

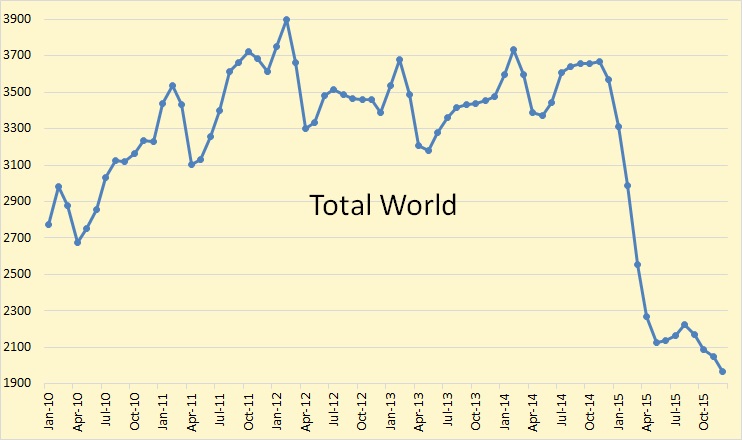

Baker Hughes Total World is just Total International plus the US and Canada. It still does not include any FSU nation or on shore China.

Total World rigs were down 78 rigs in December and down 1,601 rigs or 44.9 percent since December 2014.

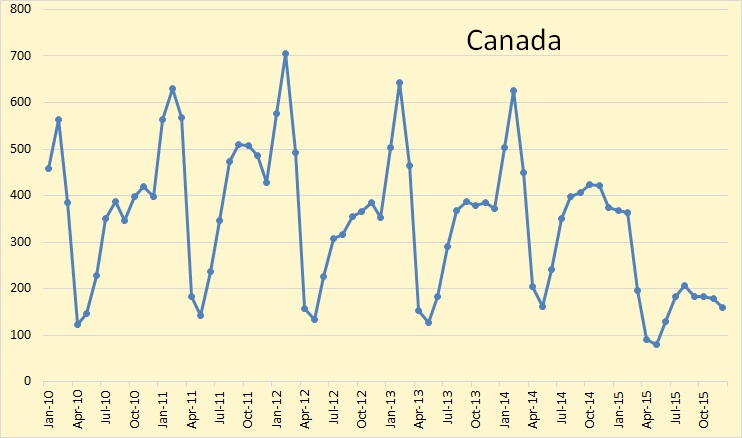

Canadian rigs were down 18 in December and down 215 rigs. or 57.3 percent since December 2014.

Total US rigs were down 46 in December and down 1168 or 62.1 percent since December 2014.

I had to include this chart. The 2016 average is only the average for the first 5 days of 2016. This is a very interesting chart. It shows that the price increase in 2008 was very short lived. Likewise the price crash of 2008 was also short lived. The price increase of 2011 lasted for four years. And the price crash of 2015 has already lasted just over a year. It is far deeper and already lasted far longer than the crash of 2008.

This is Brent premium over WTI. Normally WTI sells at a premium over Brent. What happened in 2011 to cause the sudden differential? And again in 2012 but began to decline in 2013. And now it’s gone.

This chart shows it a bit better. The price of WTI dropped below $80 a barrel in October of 2008 and broke $80 on the upside in October 2009. (Actually 1 year and 11 days later.) WTI broke $80 on the downside again on the 3 day of November 2014 and here 14 months later it shows no signs of broaching that number any time in the near future.

The point I am trying to make is this time it is different. After 4 years of very high oil prices it is quite possible, even likely, that we will have low oil prices lasting that long as well. That is because something other than the oil supply is in play here. Of course the oil supply is a very important part of it but demand just may be falling due to the state of the world economy. I think China is the wild card here.

From an Indian publication, bold mine.

Dark clouds over Chinese economy, world wide impact and what it means for India

Our largest and the most powerful neighbour China is causing tremors in India. The reason is not the Chinese military power. The cause for the worry is volatile Chinese stock market. The Chinese market is continuously crashing and its effects are already being felt all over the world. Will the Chinese markets stabilise? Will they affect the world economy in a big way? Or is it just a temporary phase which can end soon?

Even though the Chinese stock market is one of the largest in the world and the Chinese economy is the second largest in the world, it is not actually a transparent, first world market. In a single party Communist China, the markets are heavily regulated by the Communist government and the manipulation to suit the interests of the select few investors is rampant. Stock market scams are also quiet common in a very corrupt country like China.

It just may be that China is on the cusp of collapse. And if it does other economies around the world will likely go down with it.

_________________________________________________________

To receive an email notice of all new posts, post me at DarwinianOne at Gmail.com.

562 responses to “International Rig Counts Still Falling”

Hi all,

I am not posting often here, but read almost every day to learn.

Back on September 09, I made the prediction here on peakoilbarrel (sorry, I have only limited PC capabilities, so cannot post a direct link) that WTI would fall to $31. This forecast was actually made on August 27 (see attached graph with date and time stamp in lower left corner). The red targets are the most likely, so $35 was most likely to be just a short stopover. As we know now, $35 did not even hold for a week.

As you can see, I also gave three time zones when this would happen. The first two passed without touching one of the targets. So the third one had to be “it”.

What next? It all depends on the next 11 trading days (roughly half a month). If WTI manages to close above $40.99, then the Low is in. If not, $ 25 is the next target area. There are other criteria, but that would be beyond the scope of this post.

Why am I posting this? I am NOT trying to sell anything. I am trying to contribute to this forum and especially to the hands-on-contributors such as shallow sand who have been suffering for a long time now; to give them a heads-up.

How does it work? It is an old system of numerology to connect time and price.

How reliable is it? My experience over eight years is a success rate of approx. 80%. So there still is a 20% risk remaining.

So please take it foremost as another piece of information – and hopefully entertainment…

A bearish technical pattern projects the mid-$20s for WTI if the stop at $29 is taken out.

WTI $57 is currently the CPI- and US$-adjusted price basis 1973, the year the US$ was removed from gold and floated.

Basis the 1960s-1970, the CPI- and US$-adjusted WTI price would be $22-$25, which I suspect is where the price will eventually settle for the cycle, coincident with a global deflationary recession ahead.

My take on the situation is; the number of oil rigs dropping followed oil price dropping (which is still dropping slightly), and later when the over supply has been consumed, price will rise, followed by increasing number of rigs.

Sounds good. Do you think oversupply will be reduced by 2017? So oil price rise starts around then with rigs gradually rising starting mid 2017.

…still drinking that “demand-supply” and business as usual kool-aid” …huh, Dennis?!?!

Be well,

Petro

Hi Petro,

If BAU means constant change, then yes.

Demand and supply, also yes.

Society constantly changes, if you think this will no longer be the case, then we will no longer have BAU, but I think change is inevitable, always has been and always will be.

be well

Economics is simply a religious belief system, designed to compete with other religions and other economic religions such as Marxism and feudalism. That is why it is so difficult, if not impossible, to argue logically against it. It was never created based on logic but rather as a means to channel mans inner urgings and passions.

http://www.greattransition.org/publication/the-church-of-economism-and-its-discontents

Economists themselves have acknowledged the ultimately religious nature of their discipline. In 1932, Frank Knight, the most scholarly and broad-thinking of the founders of the influential market-oriented Chicago school of economics, literally argued that economics, at a fundamental level, had to be a religion, the basic tenets of which must be hidden from all but a few:

The point is that the “principles” by which a society or a group lives in tolerable harmony are essentially religious. The essential nature of a religious principle is that not merely is it immoral to oppose it, but to ask what it is, is morally identical with denial and attack.

There must be ultimates, and they must be religious, in economics as anywhere else, if one has anything to say touching conduct or social policy in a practical way. Man is a believing animal and to few, if any, is it given to criticize the foundations of belief “intelligently.”

To inquire into the ultimates behind accepted group values is obscene and sacrilegious: objective inquiry is an attempt to uncover the nakedness of man, his soul as well as his body, his deeds, his culture, and his very gods.

Certainly the large general [economics] courses should be prevented from raising any question about objectivity, but should assume the objectivity of the slogans they inculcate, as a sacred feature of the system.8

When I show students these passages in my lectures, they gasp, finally understanding why economics is taught so differently from the other social sciences, why it is presented so uncritically, as if it were a science when it obviously is not.

VK, well said.

Economics is politics. War is politics with other means. War is the business of empire. War is good business for imperialists. Therefore, economics is politics is the intellectual, amoral rationalization for the expansion of empire by way of large-scale state violence in order to expropriate resources, exploit cheap labor, co-opt foreign elites, and accept (encourage) genocide and ecocide in the process, all for fun and profit.

The job of eCONomists is that of imperial ministerial sophistry to rationalize the values, objectives, actions, and outcomes of imperial expansion, power, and control.

Same as it ever was . . .

Hey Mac, I saw this earlier today and thought you might be interested since, it might go some way towards answering questions I have heard you raise as to the effect renewables are having on the price of fossil fuels:

U.S. renewable energy mandates bring down fossil fuel use, power costs

29 states and Washington DC currently have RPS policies. These vary greatly in ambition, with Hawaii (100% by 2045) California (50% by 2030) and New York’s 50% by 2030 pledge leading the pack.

A new report by the U.S. Department of Energy’s National Renewable Energy Laboratories (NREL) and Berkeley Laboratory attempts to broadly quantify the impacts of these policies across a range of areas. These include reductions in fossil fuel use and avoided greenhouse gases, effects on wholesale electricity prices, reductions in water use, employment and cost to utilities and ratepayers.

A Retrospective Analysis of the Benefits and Impacts of U.S. Renewable Portfolio Standards finds that RPS- compliant systems made up 2.4% of nationwide electricity generation in 2013. This created 200,000 jobs, reduced wholesale electricity prices and reduced fossil fuel generation by 3.6%, resulting in 59 million metric tons fewer greenhouse gas emissions.

Thanks, Islandboy

This link certainly appears to support my argument that SOCIETY as a whole experiences a substantial net benefit as the result of supporting the renewables industries.

The sale of coal and gas are depressed, meaning their PRICES are also depressed, the environment is cleaner, there are more local jobs and jobs in more places, associated with the energy industries, etc.

The reduction in VOLUME purchases of gas and coal over time , combined with the savings on the PURCHASE PRICE of these depleting commodities, will be substantially greater than the cost of subsidies, so far as I can see.

WIN for every body except the people invested in the fossil fuel industries, or employed in these industries.

There is a time coming oil, gas, and coal supplies will be tight and questionable, and the prices of them will be UP sharply.

How long, I don’t know, but soon enough that we had best stay after scaling up renewables NOW so as not to get caught with our pants around our ankles later on.

The longer we can stretch out the one time endowment of oil and gas, the longer we have to adapt, both technologically and socially. Given time enough, we have a shot at coping with peak oil, and with peak gas as well, assuming supplies don’t crash too fast, and prices don’t spike too fast.

Personally I find the argument that the world cannot EVER support a present day price of oil of one hundred fifty bucks or more to be absurd. We would be in a hell of a lot of trouble if the price spiked that high in short order of course.

BUT in ten years we can, if we force the issue, get twice the bang out of a barrel of oil, and the world economy did not crash due to seventy five dollar oil.

Ships can slow down, and the bigger they get, the less fuel they use per ton of cargo. Air travel is a substantial contributor to the economy NOW, but we had a viable economy before air travel came of age, and we can have one again without it, given time to adapt. And aircraft probably eventually be made twice as fuel efficient as well.

Houses can certainly be built so as to be heated and cooled with half or less of the energy needed on average today, and for only a very little more in initial cost.

With a huge build out of wind and solar power farms, and lots of new long distance transmission lines, the gas we burn now to generate electricity can mostly be reserved to support generation when the wind and sun just don’t cooperate.

It is not our job to solve the problems of the twenty second century. Our job is to get thru the next few decades, as best we can, without fucking up the planet any more than necessary to survive.

I am not even an engineer but I know of dozens of ways ( mostly worked out by real engineers ) to reliably and afford-ably reduce energy consumption, while still living quite well. As energy prices increase, we will be putting these tricks to work one after another.

Will they enable us to continue to live ” life as we know it”?

NO- and nobody who understands the problem expects us to continue to live life as we know it today. But some of us have a pretty good shot at continuing to live a pretty decent life just the same, with all or most of the things we have come to take for granted still available to us.

A low and narrow fore and aft oriented two seat car can easily go a hundred miles on a rather modestly sized battery, especially if it is PROGRAMMED to never exceed let us say forty mph.

(And forty mph is still four times as fast as a fast horse, which can only run ten miles once in a day, and not very many days at all on a regular basis, and needs the other twenty three hours to recuperate. LOL)

Of course GS will be popping in to ridicule the idea that anybody will ever buy such a car, short of the nanny state holding a gun to his head, but anybody who really believes in peak oil will be a little more open minded about downsizing rather than WALKING.

Collapse may be inevitable. I personally believe it is, eventually, on the basis of chance alone, but that does NOT mean we have no choice but to go quietly into the night.

Some of us, most of us, are going to go kicking and gouging and biting and screaming, and shooting too, at least those of us wise enough to have weapons.

Anybody who believes a new sustainable, low energy, low impact way of life is TECHNICALLY IMPOSSIBLE is scientifically and technologically illiterate, it’s as simple as that.

Some of us have a fair shot at achieving it, and may be able to sustain it indefinitely.

Of course achieving such a society may be impossible, for many various reasons, until utter and absolute necessity forces the issue, and overshoot reduces the population substantially. Even then, it might never come to be, but impossible it is NOT.

oldfarmermac,

Since you invoked my name, I will gladly respond.

The study islandboy cited is a cost-benefit analysis.

This from the cost side of the study:

Question: The various entitites which comprise the United States government have not been very aggressive about forcing the production of renewable energy. But what if they had been? What if they had been as aggressive as, for instance, Spain, Italy, or Germany?

What do you believe would be the political fallout for US lawmakers if, instead of electricty costs increasing by a mere 2%, they had increased on the order of 50% or 100%, similar to what they have increased in countries like Spain, Italy and Germany, which have been more aggressive in forcing the production of renewables?

Glenn,

price per kWh is only half of the truth, you have to check the actual bill which is a product of ($/kWh) * consumption.Then you suddenly find that the monthly electricity bill of an US houshold is not lower than the monthly bill of a German household.

The second aspect you conveniently ignore is, that electricity was always very expensive in Germany or Denmark, to assume that the observed differences are a result of REs is nonsense, REs only contributed ~30%.

I’d like to add that my price for 2016 will be only 67% of the national average listed here.

Simply because I change the supplier every year and always get their discounts for being a new customer. This requires about 5 minutes of my time every year and saves me about 125 € compared to the national average (yes, we only use about 1.700 kWh per year, without any lack of modern comfort!).

Too lazy to invest 5 minutes for a return of 125€? You deserve to be fleeced!

Actually, checking my old bills right now I noticed that my electricity price has decreased from 0.26€/kWh in 2012 to 0.22€/kWh in 2016. Now, where does renewable energy cause higher prices?

If you want to know what electricity costs without the burden of taxes,…

http://www.eex.com/en/

PHELIX -> Germany and Austria

FRANCE -> obvious?

SWISSIX -> Switzerland

Want to know what electricity price to expect as an industrial customer?

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&plugin=1&language=en&pcode=ten00117

Compare the price history of France (with their “cheap” nuke power) to the price of Germany and tell me: Do you want your price to increase by 40% (France) or by 9% (Germany), while calculating the future prices you need to charge your customers for your goods and services?

Gerry,

Well that is certainly true. German industry has gotten a free ride when it comes to paying for Energiewende, since residential customers have been forced to pay the entire cost, then some.

Ulenspiegel says:

So let me get this straight.

American households can afford to pay close to 3x the kWh price for electricity, the same price as Germans do, in order to pay for the renewables “transformation.” All they have to do is cut their electricity usage by 2/3, to a level similar to that of German households?

I fully understand that this is part of Energiewende propaganda:

And maybe a majority of Germans do indeed believe they are doing God’s work, sacrificing to save the planet.

Nevertheless, try selling that to American households, and see how far you get.

As Samuel J. Best and Benajamin Radcliff documented in Polling America, very few US households are willing to pay even a very small additional cost for renewables when offered the choice to do so by their utility companies. The customer participation rates in the top 10 utility green-pricing programs have ranged from 3.9 to 11.1 percent.

Instead of making silly statements like “And maybe a majority of Germans do indeed believe they are doing God’s work, sacrificing to save the planet.” you shoulkd work a liottel bit harder to put your data in the correct context. You have failed.

Energy was and still is very expensive in Germany. This has consequences which you do obviously not understand. E.g. the German economy despite running a higher industrial production is at least 25% more emergy efiicien as the US economy.

The situation of German households is quite realaxed, as electricity is only the minor part of the energy bill. For SMEs electricity only contributes 2% of the costs, i.e. is menaingless.

To assume that the price increase of electric energy is a real issue is a littel bit naive, when at the same time wholesale prices DECREASED and as a result energy intensive industry improved their international position.

To use the USA situation to argue against German energywende is not useful.

Ulenspiegel,

Despite all the flowery rhetoric and professions of devotion that issue from the mouths of Merkel and Gabriel, pious declarations about how Energiewende “isn’t just for them, but all of mankind,” about how it is “irreversible” and how “I am convinced that if there’s one country that can master the Energiewende, it’s Germany,” Energiewende is facing some serious political challenges.

And while the political realities in Germany may be different than they are in the United States, the economic, physical and engineering realities are not:

Given that Germany is a country that must import oil and gas, and even good quality coal, Germans have sense enough to understand that their CONTINUED prosperity depends on their taking the lead in renewable energy.

Folks who are sensible are willing to consider the possibility that spending NOW can save many times the current expense LATER.

Consider this:

Countries such as Saudi Arabia that export oil are coming to understand that in is in their best interest to keep the oil at home, and export FINISHED PRODUCTS made from that oil, and are moving in that direction. A country that has little to export other than trees will come to understand that it is much better to export wooden furniture, or paper, or other products such as chemicals, made from wood.

What the FUCK is Germany going to export when the country can no longer IMPORT oil and gas, unless Germans generate their own energy supply?

That time is COMING, and the German people have sense enough to know it, and are sensible enough to prepare NOW for that time.

I doubt there are very many Germans as old as fifty who do not know ALL ABOUT WWII, from talking about it with family that lived thru it.

I doubt there are very many Russians of ANY age that have forgotten WWII in general, and the SIEGE OF STALINGRAD in particular.

Russians have long memories, and an authoritarian government.

Germans are not going to mention this very often, publicly, but you can bet your last can of beans that they are not going to FORGET it, at least not very soon.

OFM,

Judging from the comment by Ulrich Grillo, President of the German Federation of Industries, that I cited above, it looks like the German industrial class disagrees with you.

To wit:

“This places German industry at a serious competitive disadvantage that is only going to get worse,” said Ulrich Grillo, President of the German Federation of Industries, the country’s main industry lobby. “The electricity factor is a burden that endangers industry and therefore the livelihood of companies and their employees.”

OFM

“I doubt there are very many Russians of ANY age that have forgotten WWII in general, and the SIEGE OF STALINGRAD in particular.”

Small historical point.

I believe you are confusing the battle for Stalingrad with the siege of Leningrad.

Ulenspiegel,

Glen is not interested in facts such as this:

The situation of German households is quite realaxed, as electricity is only the minor part of the energy bill. For SMEs electricity only contributes 2% of the costs, i.e. is menaingless.

BTW, I have family in Germany. Both my brother and sister work for German companies are married to Germans and have raised families in Germany. I have been to visit on many occasions.

Nothing that Glen says about Germany or any other topic for that matter, has the slightest ring of truth about it. He is here only to make inflammatory remarks! He is not now, nor has he ever been, interested in any form of honest discussion.

He is best ignored! trying to engage him in a discussion is a total waste of time. He adds nothing of value. If I were Ron, I would permanently ban him from commenting here.

To be clear, before anyone suggests that I am in favor censoring opposing views, that is not at all what I propose. There are others on this site with whom I very strongly disagree on certain topics, however I have always gotten the impression they have arrived at their positions by honest means. I am more than willing to let them have their say and even when I disagree with them they always make me think and examine my own positions with more care.

Glen, on the other hand, seems only to be interested in obfuscation and sowing the seeds of discord.

Fred,

The reason Team Green takes such a keen interest in peak oil is because it believes its hallowed Green Utopia will arise from the death of carbon, just like the Phoenix arises from the ashes of its predecessor.

It’s the resurection theme, the ascenscion theme, taken right straight out of Greek and Christian theology.

“And my bible tells me that Good Friday comes before Easter,” the Reverend Martin Luther King intoned. “Before the crown we wear, there is the cross that we must bear.”

It is a veritably messianic political program, and like any messianic political program that succumbs to the utopian temptation, it does not take kindly to true difference.

Nevertheless, there is precious little factual, empirical evidence that demonstrates that “clean energy” can come anywhere close to replacing, or doing the heavy lifting of, carbon energy.

The only reason Team Green is interested in peak oil is because it believes its hallowed Green Utopia will arise from the death of carbon, just like the Phoenix rising from the ashes of its predecessor.

Team Green doesn’t exist except as your construct. It is a strawman pure and simple!

Strawman

You misrepresented someone’s argument to make it easier to attack. By exaggerating, misrepresenting, or just completely fabricating someone’s argument, it’s much easier to present your own position as being reasonable, but this kind of dishonesty serves to undermine honest rational debate.

https://yourlogicalfallacyis.com/strawman

Fred Magyar said:

Team Green doesn’t exist except as your construct.

Right. It doesn’t exist, except when the need arises to circle the wagons to defend its mythology.

I think Glenn is referring to Team CeeLo.

Hi Webhubbletelescope,

Glenn likes to create myths and then argue against those.

Much ado about nothing.

I has to look up CeeLo, as I didn’t get the reference, most old men probably are unfamiliar with Mr Green.

Ulenspiegel says:

Well again, this is part and parcel of Energiewende propaganda. But is it true?

Since the EEG renewable Feed-in Act took effect in 2000, it has been promised by green energy proponents time and again that the power price would fall in Germany. So what does the reality look like today?

Here are statistics from the Bundesnetzagentur (Federal Network Agency) on the latest power prices.

In 2000, when the Feed-in Act was introduced, Germans paid only 13.94 cents per kilowatt-hour, which at the time had hardly changed since German reunification in 1991. After the liberalization of the power market in 1998, the price of power even dropped some. Today, in 2014, the price is now 29.21 cents per kilowatt-hour, i.e. it has more than doubled in 14 years.

Hi Glenn,

It depends on where you start, on the curve and also where you end.

You like to point out that investment in renewables has declined since 2011, to follow your logic that the renewables are causing prices to increase, we would expect that the reduction in renewable investment would cause electricity prices to decrease. The reverse was the case.

In addition, you blame the price increase on renewables, natural gas prices have increased by a factor of 5 since 1998 in Europe.

This may be the main explanation for increased electricity prices in Germany along with shutting down nuclear power which most of the German population supports. Chart with natural gas prices uses BP data.

Dennis,

Only 11% of Germany’s electricity is generated from natural gas.

http://www.enerdata.net/enerdatauk/press-and-publication/energy-features/germany-increasing-power-generation.php

It takes about .01 MCF of gas to generate 1 kWh of electricity. So the cost of natural gas to generate a kWh of electricity has increased by about 8₡ since 2000.

http://michaelbluejay.com/electricity/fuel.html

But since only 11% of Germany’s electricity is generated from natural gas, this explains less than 1₡ of the more than 15₡ increase in the price of electricity.

Glenn,

The price is determined by the marginal cost of the most expensive electricity, so if your 8 eurocents is correct, that explains quite a lot of the price increase, it doesn’t matter if natural gas only produces 11% of the electricity, if that is the most expensive electricity produced it will determine the price.

Dennis,

Guess again.

The average feed-in tariff that German electric utilities were compelled to pay in 2014 was more than double their full costs for fossil-nuclear power production, and this in spite of all the operational problems forced upon them which greatly increase their fossil-nuclear costs.

Dennis,

Here is a link to a study, in German, which sets out the main factors which have caused electricity prices in Germany to skyrocket since Energiewende began:

http://www.science-skeptical.de/klimawandel/deutschland-strompreis-spitzenreiter-hinter-daenemark-in-der-eu-seit-einfuehrung-des-eeg-im-jahre-2000-hat-sich-der-strompreis-mehr-als-verdoppelt/0013133/

Here is a translation of some of it to English:

http://science-skeptical.de/ does not publish studies. They do propaganda.

Just read some of their stuff, it becomes obvious quite fast.

——————–

You also seem to be confused about the “EEG-Umlage”, thinking this is what’s being paid for electricity production from renewable sources.

It’s not, those 6.xct/kWh contain only 2.6ct/kWh which pays for renewable generation. The rest ist political bullshit and corruption designed to funnel money to those bribing politicians and to provide ammunition to propaganda people like you appear to be one.

http://strom-report.de/medien/eeg-umlage-boersenpreis-indutrierabatte.png

——————–

Seriously, are you trying some propaganda shit against a german native who actually reads details?

Or do you just bask in confirmation bias?

——————–

“American households can afford to pay close to 3x the kWh price for electricity, the same price as Germans do, in order to pay for the renewables “transformation.” All they have to do is cut their electricity usage by 2/3, to a level similar to that of German households?”

Of course they could. This is plain math. Actually, I guess this is about 5th or 6th grade math!

But of course, americans would never do this, as they do seem to think that wasting resources and energy is a god-(or cthulhu- or whatever stupid, invented figure)-given right that every american needs to excercise at any time.

——————–

And you definitively should use up to date sources.

Coal only provides 40% of electricity generation in 2015, not 47 as in 2012 (your source above).

Gas-powered prodution provides only 5% in 2015.

Please do not forget that 7.8% of production has been exported (a new all time record), even though nuclear proponents warned of blackouts due to the immediate shut down of several nuke plants in 2011. (1)

Export equals almost exactly one third of lignite based electricity production!

If our corrupt politicians would not protect coal fired power plants (2), we would already see a massive phase-out of coal plants.

https://www.energy-charts.de/energy_de.htm

(1)

Had coal production be shut down in times of high production of renewables, coal would have provided only 35% of total electricity production.

(2)

The population is quite indifferent to the problems associated with coal based power production, thus creating less incentive for politicians to shut them down.

Quite the opposite is true with nuke plants.

Annex 1:

Definition of “corrupt politician”:

Politicians are corrupt wheny they act to the benefit of themselves or very few people or corporations, despite a majority of the population requesting the exact opposite of that.

Hi Glenn,

It sounds like there is an oversupply of conventional power, do you think they should be subsidized?

Dennis,

You seemed to have missed this part:

…old power plants are being left on because the federal government has made it illegal to shut them down in attempt to keep the supply intact.

What would you say to the US government forcing an oil and gas operator in the US to continue producing a well that the operator wishes to shut in because he’s losing money by continuing to produce it?

Again, you do not analyse which part of the increase came actually from the FIT. We had different parallel developements which contributed to the current situation.

And again, the industry improved their relative competitiveness.

Ulenspiegel says:

And again, you continue to demonstrate that you live in a fact-free world, completely divorced from reality:

And what “had been promised”?

Jürgen Trittin, a former Green party environment minister, in 2004 declared that “subsidizing green energy wouldn’t cost the average German household more than one euro per month, or as much as a scoop of ice cream.”

And here’s more recent data on prices, a comparison of what various European countries pay for electricity.

The French in 2013 paid about half for electricity, on the average, as what Germans did.

BENEFITS

Most of the “benefits” that this study puts a dollar value on are those which are derived from reductions of highly politicized external costs: “GHG Emissions and Climate Change Damage Reductions” and “Air Pollution Emissions and Human Health and Environmental Benefits.”

The benefit you and islandboy singled out, however, is “natural gas price reduction impacts”. Quoting from the study:

The authors of the study of course have some very high falutin mathematical models which they use to justify their claims. But I have created the graph below, using EIA stats, to illustrate exactly what it is the authors are asking us to believe.

https://www.eia.gov/dnav/ng/hist/n9070us2A.htm

For 2013, the blue bar is actual natural gas production for that year. The brown bar is what natural gas production would need to be if it had not been reduced by RPS compliance.

Does it pass the common sense test to believe that such a tiny reduction in the use of natural gas for 2013 would cause a 5₡ to 14₡ reduction in the price of natural gas?

Another highly dubious “benefit” which the authors claim is this:

This harkens back to something which John Maynard Keynes said:

This sort of thinking has become axiomatic in orthodox economics circles, for as Richard Nixon proclaimed back in 1971, “We’re all Keynesians now.”

For instance, in an exchange on the CNN show “Fareed Zakaria GPS,” there’s the following exchange between an economist and the host:

This is one of the key roots of the problem with many mainstream economists. They believe the economy is about money. In reality, it’s about value produced.

After no one challenges Zakaria’s bizarro assertion that Boston’s Big Dig was just swell even though it cost ridiculous amounts of money for the value produced, my favorite economist from the Twilight Zone jumps in to pull out another favorite myth of the Keynesians and their friends.

These people honestly believe that money spent — no matter why it’s spent or the effects of the spending — is the same as creating growth. They don’t understand that if the spending produces nothing of value, the amount of overall value in the economy is lowered and that the average standard of living must go down.

The inestimable GS would make a hell of a fine lawyer, if you needed one to pound on the table, rather than THE facts, because he is extraordinarily adroit at making long pompous speeches about things that may be facts but are not RELEVANT to the argument.

Let me say first that anybody who is stupid enough to make an argument that externalized costs don’t matter is just plain and simple a fucking idiot. He does not QUITE go that far, but he insinuates it.

“Most of the “benefits” that this study puts a dollar value on are those which are derived from reductions of highly politicized external costs: “GHG Emissions and Climate Change Damage Reductions” and “Air Pollution Emissions and Human Health and Environmental Benefits.”

Now as it happens, I am a person who has made a LIFELONG CAREER out of not having a conventional career. I took my degree in agriculture, and my transcripts are heavy on the physical and life sciences. I have taken almost enough courses over the years to hold a couple more degrees, in order to keep up, or just for a change in the intellectual scenery. A few years back I nearly finished a program to earn a Registered Nurses license, but dropped out at the last minute, TWICE, to look after my parents.

So -I KNOW , from the professional study of managing crops and livestock, and managing the details involved in public health issues, that we are paying a HUGE HUGE HUGE penalty in external costs by using fossil fuels as if there were no tomorrow.

Incidentally GS apparently believes there is in effect ” no tomorrow” and that the world is going to hell in a hand basket and so we might as well “party hearty” and continue on our fossil fuel binge, because, hey , we are all dead in the long run anyway right?

Maybe the world IS headed to hell in a hand basket, but I know a few little boys and girls that brighten my heart, and I want them to live as well as they can, for as long as they can.

When responding to a comment posing the question, whether society ( USA society in this case ) derives a net benefit from subsidizing renewables, his total response is plainly and simply a case of misdirection, an attempt to switch the audience’s attention AWAY from the question, or at least from an open minded consideration of the question.

Fossil fuel shills want us to forget how many people die as the result of air pollution, they want us to forget how many resource wars have been and will be fought over access to fossil fuels, and above all they want us to forget that fossil fuels DEPLETE over time. They want us to forget the strip mines, and the mountains flattened and the buried streams, and the dead fish downstream.

His bag of diversionary arguments or tricks is apparently bottomless, but all of them, when you take a close look at them individually, are about as convincing as the car salesman with the oily manner and the mirrored sunglasses and the plastered on shark smile.

“Does it pass the common sense test to believe that such a tiny reduction in the use of natural gas for 2013 would cause a 5₡ to 14₡ reduction in the price of natural gas? ”

Well, now, obviously GS would have us believe that the people who do any studies contrary to his agenda are all idiots, or at least ethically challenged.

But ANY student of business and economics, or anybody with a brain at all, can tell you that a given factor ( in this specific case a reduction in gas consumption used to generate electricty in the USA ) reducing consumption of a given commodity has the effect of lowering the price of it.

Using LESS gas for any given purpose means cheaper gas. PERIOD. FOR EVERYBODY.

So – So far he has not been devious enough, or blatant enough, to claim that the study is altogether in error , and that we are using MORE gas and coal BECAUSE we are using wind and solar electricity now- but I have seen that argument made by other fossil fuel shills in other forums, although not recently.

I believe it is perfectly reasonable to use the figure given in this link to the effect that we used about a percent and a half less total gas, and about five percent less go generate electricity, as the result of deploying wind and solar power. The exact figure is not important, the point is that the reduction is real, that gas depletes, that it will not always be cheap, etc.

Now as to the MAGNITUDE of the price reduction that came about as the result of this lowered gas consumption is involved, anybody who is remotely acquainted with the concept of elasticity of demand understands that in the case of a commodity such as gas, a minor increase in supply, or a minor decrease in consumption, can result in a wild price swing.

His yakking about common sense is pure Koch brothers bullshit.

I have PERSONALLY hauled a truck load of SUPERB quality peaches around for a hundred miles, without being able to sell them to ANYBODY for any price, short of sitting on the side of the road selling them a pound at a time, and brought them home, and dumped them in a gully to rot. SUPPLY AND DEMAND MATTER when it comes to price.

And incidentally, what we have spent on subsidizing wind and solar farms will be having the SAME depressing effect on the price of coal and gas for the LIFETIME of this infrastructure, and hey guys, here is another thought about sustainability. Wind and solar farms are NEVER going to just WEAR OUT. They can be refurbished BETTER than new, piecemeal, as individual equipment fails, for a minor fraction of the cost of a from scratch new farm, because all the costs, except the actual cost of new machinery, is already covered, and will in most cases already be history, paid off.

Permits, surveys, environmental impact statements, access roads, interconnections to the grid, grading, etc, are ONE TIME expenses, they never have to be paid for AGAIN.

Now I have no idea what GS actually knows, but I suspect he knows more than he is able to admit, for fear of admitting his agenda.

But I HAVE personally spent a substantial amount of time in classrooms studying economics and business administration, taking probably more than a full academic years worth of such courses.

Any argument can be taken out of context, and used to make a person or a profession look like a fool, if the audience is gullible enough.

A long rant about digging holes and filling them up again to put people to work is an entirely bullshit diversion, in the first place, and in the second, it is presented as if it were put forward as a deliberate policy pronouncement, rather than a theoretical illustration.

A real economist, in real life, never argues that you should dig holes and fill them up again, as opposed to putting the workers doing something that is actually USEFUL.

Such policy proposals, when they are of the make work sort, are always after some fashion connected to reality, and instead of digging holes to kill time, the proposal is to dig a path for a sidewalk, or beautify a highway, or clear away trash, etc.

GS wants us to react to renewables without thinking, by pressing our hot buttons,and preventing us from thinking. This technique often works like a charm, if the perp is allowed to get away with it.

“Nobody ever went broke overestimating the stupidity of the public. ” I forget who said it , PT Barnum comes to mind.

“Hain’t we got all the fools in town on our side – ain’t that a big enough majority in any town?” Twain,probably off a bit, but close enough.

Fortunately, the audience here is more sophisticated, as a rule, but you never know who has not had the educational advantages of the regulars here, and might be lurking and so fall for his bullshit.

I am among other things a former professional educator, and habitually look out for ignorance and do what I can to stamp it out.I ENJOY stamping out ignorance.

And unlike GS, when I quote somebody, the quote is actually RELEVANT to my argument, rather than hot wind having little or nothing to do with the questions and issues under discussion.

Dressing his comments up with them no doubt impresses people so ignorant they cannot even make sense of them. Big words, and tailored suits, and lots of meaningless certificates on office walls have that effect on people not smart enough to know better.

The beer salesman NEVER allows you to focus on the headaches and the heartaches and the disasters associated with drinking beer, if it is within his power to prevent it. He stays on message, beer is fun, beer is cheap, beer makes you feel good, nothing wrong with beer, no siree, don’t pay no ‘tention to that fool preacher over there burying a couple of people killed day before yesterday by a drunk driver.

Almost everything he ever says is an attempt to divert attention away from relevant facts, and relevant questions, so as to protect and advance the fossil fuel agenda.

I won’t let him get away with it unchallenged.

It is GREAT FOR ME that he is gathering up all the counterarguments for me, where I will eventually be able to quote them, and ” rip them up like a chicken on a dry cow turd” in my book, which I will eventually finish and most likely publish free online.

(I don’t know who said THAT last one first, most likely nobody does, but the first person I ever heard say it was my dear long departed old country woman Momma. LOL She had only a grade school education, which is all most of her generation in this back woods got back when she was a kid during the DEPRESSION, but she had a BRAIN, and plenty of common sense. )

And one last thing-I have great sympathy for the guys who are working hands on in the oil and gas industries, and wish them all the best.

They need not worry themselves with renewable energy putting them out of work, because they will all be retired and most likely dead before we quit burning whatever oil and gas they can scrounge up.Their kids might do well to think about alternate careers though.

The best we can hope for is to get the renewables industries scaled up to the point that we can stretch out our fossil fuel endowment long enough to adapt to a low energy life style and economy as best we can.

Here is a little bit of FUTURE REALITY. The Saudis are going to eventually be building LOTS of BIG solar farms so as to have more oil to SELL, rather than burning it to air condition the desert, assuming of course that they are not politically gridlocked internally and can’t giterdone.

Mac, I found the above post in the trash file. Apparently WordPress software kicked it there because it was too long.

Mac, you just have to cut down on the size of your posts. They are way, way too long. Try to emulate Polonius.

Polonius:

My liege, and madam, to expostulate

What majesty should be, what duty is,

What day is day, night night, and time is time,

Were nothing but to waste night, day, and time;

Therefore, since brevity is the soul of wit,

And tediousness the limbs and outward flourishes,

I will be brief. Your noble son is mad. . . .

Hamlet Act 2, scene 2, 86–92

oldfarmermac,

I’m sorry, but the only way I could respond to that is with an equally long screed, so I’m not even going to try.

When it comes to desultory verbosity, you definitely take the prize.

Hi Ron,

Thank you for retrieving it.

I am trying to respond to GS posting half a dozen comments in a row, most of them with charts and lots of long quotes, with a single reply.

I will try to do better.

The problem with dealing with HIS long windedness is that it refuting a simple sounding, easy to swallow whole, partisan talking point that takes only a few words takes a couple of paragraphs AT LEAST to dismantle and expose for what it IS- in the case of GS, the Koch brother’s agenda.

I can break my comments up into smaller parts.

I thought you might find this last long one in spam, but composed another, just in case, in a word processor, so as to save it.

I am going to post it at the tail end of your last new post previous to this one.

Complicated issues simply cannot be debated in a few words, because the person using the fewest words can almost always get away with the biggest distortions of the actual facts, or outright lies.

In the future, I will try to remember to post much shorter comments, even if I must post two or three.

Thank you , Sir GS

I am immensely flattered to be recognized as an expert in your own league.

The biggest difference between us is that my long posts are mostly my own work, whereas yours are mostly bullshit fossil fuel industry talking points and long quotes by various philosophers or other folks- quotes that have very little, or NOTHING, actually to do with the issues under discussion.

Of course as Twain put it in Huck Finn,

“Hain’t we got all the fools in town on our side- and ain’t that a big enough majority in any town?” This Twain quote is from memory,and probably not exact.

You address the fools who are UNABLE to think, or would rather not be bothered. Such people are all to often easily led around by their perceived best short term interests, since they don’t know any better.

Unfortunately most people are very close to technically illiterate, in terms of the life sciences and other hard sciences, and so do not actually understand where their ACTUAL best interests lie.

I write for mostly for people who are willing to do a little thinking, and who have the necessary intellectual background to do so.

BUT I also take the time to explain as best I can to those who are willing to think, but not well enough informed to understand your bullshit, HOW you mislead them.

You write for the soundbite crowd for your obvious masters in the fossil fuel and “business as usual ” establishment.

Picking half truths apart necessarily takes MUCH more time than telling a half truth.

And for what it is worth-I believe people can actually make sense out of my rough and ready stories and homespun philosophy, whereas hardly anybody can see any serious connection between your long stuffed shirt QUOTED remarks and the questions under discussion.

If you have ever answered a direct question with anything other than the old politicians typical non answer, I cannot remember the occasion.

I am posting another reply on the last main open key post at the end, so as not to further hog the space on this one.

See you there, if you dare, I am enjoying myself. Your JOB writing the same old same old bullshit must be getting boring by now.

http://peakoilbarrel.com/confessions-of-a-doomer/#comment-555538

Mac,

I enjoy ur wisdom. I have learned heaps from u.

You now seem like u are arguing with yourself in the shower.

I hope everything is ok. I have been there mate!

Thank you Satan,

I was half asleep and half dreaming, as is often the case, given the situation in the house these days, when I wrote this response. I am also making sure I don’t overlook anything, and doing the best I can to make sure GS does not get the LAST word in.

( My old Daddy needs a LOT of attention some days recently.Uninterrupted sleep, etc, is mostly a luxury I vaguely remember from days gone by.

Given that I am an Honor Thy Mother and Thy Father BAPTIST by culture, even though I am a DARWINIST by intellectual training, I will NOT put him in a nursing home to die of heart break among strangers.

I would as soon as not SPIT on anybody who would do that to their PARENTS.

He will live out his days looking out his picture windows at the orchard and deer and birds, at home, where he is mostly happy.

oldfarmermac,

You always attempt to make the debate about me.

But it’s not about me. It’s about the facts, and the facts speak for themselves.

Only half true. You will only admit facts to the discussion if they make YOUR case.

So the debate will remain half about you, and the audience can decide who has the best mastery of the facts, and is most willing to acknowledge the facts for his position pro and con.

The audience will also decide who is actually making a FACTUAL argument.

I have not denied that renewables are expensive, and that economic transitions are expensive.

You otoh seldom if ever an indisputable fact contrary to your argument, and question the ethics and competence of virtually anybody who questions your ever so righteous pronouncements.

I am not at all PC, and I BELIEVE in being judgemental when judgement is called for.

My judgement is that you display all the proofmarks of a paid mouthpiece. This does not mean I believe you are personally unethical, or dishonest, in the usual sense.

My attorney is a highly ethical man, at the personal level, but he will tell you right quick that when it comes to representing a client, he will say “damned near anything he can get away with”.

That’s his JOB, it’s the way he pays his bills.

I will make sure the debate stays half about you to the best of my ability, because I believe you are a fossil fuel industry mouthpiece, meaning you are willing to say damned near anything you can get away with.

For my part, I am collecting data for a book, and passing the time, and I ENJOY poking sticks at holier than thou, self righteous people who imply every body else is ignorant, naive, or just plain stupid.

I make it a point to acknowledge both sides of arguments. I am for instance a big believer in electrifying personal transportation , but I often mention that I personally drive old conventional clunkers to save money, and that most of the driving public is going to continue driving conventional cars for a rather long time.

You claim or at least strongly imply the choice is between a conventional car, or shoe leather, with maybe a fortunate few being able to get along using mass transit.

My positions are all about acknowledging risks, catastrophes, and possible opportunities to avoid at least the worst of the catastrophes.

Your positions are all about denying any hope of affordable, practical positive solutions.

That makes you an obvious fossil fuel mouthpiece.

Hi Glenn,

Who decides what is valuable, you? When there is a depression and people need to eat, the choice is let people starve or find something “useful” for them to do.

This creates jobs and income and then entrepreneurs are more willing to invest because it creates some “hope”.

Are you arguing that Hoover had it right? Everyone should have just tightened their belts and the economy would have healed itself.

Also note that we can let the free market reign, but then you often have to wait for the long run to arrive before the economy rights itself. When the peak arrives and energy prices spike due to scarcity, we can hope that ingenuity can magically create more oil supply, there are many who believe that this is the case, I am not among them. Either we will have to use less energy ( and I agree that public transportation in urban areas will help) or find substitutes for fossil fuels, it will likely be both.

Spending on wind and solar may seem wasteful, but these industries will not develop adequately if we don’t create some demand through subsidies. The industry does not spring up full blown overnight. Waiting to develop these industries until peak fossil fuels is evident will make a transition exceedingly difficult, if not impossible.

If this is not clear to you, perhaps you believe there will be no peak in fossil fuel output. Is that the case? Explain what you think will occur when peak fossil fuels arrives (let’s assume all subsidies for renewables were eliminated tomorrow to please free market true believers). When do you think we will reach peak output in fossil fuels (if ever)?

Dennis,

So malinvestment in renewable energy can be justified, if we debauch Keynesian economic theory sufficiently?

Keynes must be rolling over in his grave with what is being done in his name.

Here are some more passages from the study in German I cited above, translated to English:

Hi Glenn,

Your premise is not sound. It is a good idea to invest in renewables such as wind and solar.

I noticed you did not answer the question about peak fossil fuels.

Is it your contention that peak fossil fuels will either never occur or will happen so far in the future (say after 2050) so as no investment in renewables is needed? Or is it that subsidies should be reserved for fossil fuels only (and maybe nuclear power as well)?

Dennis Coyne says:

So who is it now deciding what is valuable, you?

Hi Glenn,

Yes, me and others that recognize that energy will be needed when peak fossil fuels arrives.

I will assume because you do not answer the question, that you do not believe there will ever be a peak in fossil fuels. If that position were correct, then subsidizing fossil fuels would be a correct position.

You are wrong to think that renewable energy will not be needed.

I note that you seem to be a little shy about admitting your true position, as then you might be ignored.

This will be my last response to any of your comments.

Dennis Coyne said:

I will assume because you do not answer the question, that you do not believe there will ever be a peak in fossil fuels.

Dennis, since the acolytes of Team Green are fundamentalists at heart, and since fundamentalists generally try to stigmatize their opponents by depiciting them as apostates from the one true way, may I state for the record that I do not deny the existence, or the importance, of peak oil.

The disagreement between us is not about whether peak oil will occur or not.

There exists no doubt, on a finite planet, that peak oil will occur.

Everyone recognizes the existence of certain truths, that is, truths in which the predicate can be derived from an analysis of the subject. Such truths are a priori, because they do not require recourse to experience. The existence of peak oil is such an a priori truth.

The dispute between us is instead over the question: What will life be like in a post peak oil world?

My stance is, as I have stated numerous times on this blog, that when the carbon party is over, the party is over.

There exists no evidence that there can be a green-washed BAU in a post peak oil world. And in fact, there is a growing body of evidence that reveals the very opposite will be the case, that there will be no BAU in a post peak oil world.

Hi Glenn,

First we agree there will be no business as usual. This is also an a priori truth.

The only constant is change, the future is always different than the past, so if you believe that most others believe that there will be no changes in the future, you are mistaken.

So do you agree that fossil fuels will become more expensive when peak fossil fuels arrive? Do you also agree that the costs of wind and solar have been falling dramatically?

If the answer to both questions is yes, then it is pretty obvious that the relative cost of wind and solar will be lower than fossil fuels in the future.

The subsidies for renewables that you consider malinvestment help to drive the cost of wind and solar down as these industries develop.

Without such subsidies we would have an undeveloped wind and solar power industry when the time came that they were needed.

You seem to think the strategy of letting the free market direct this investment is best.

How is that working out in the LTO sector?

The free market is not perfect and neither is bureaucratic control of markets, we need to find a middle ground where investment in alternatives is encouraged or the party will indeed be over.

We can give up and party like its 1999, or we can get to work trying to solve the problems at hand.

°°°°Dennis Coyne says:

So do you agree that fossil fuels will become more expensive when peak fossil fuels arrive?

Yes.

°°°°Dennis Coyne says:

Do you also agree that the costs of wind and solar have been falling dramatically?

No.

This is where your magical thinking comes into play. It’s the same kind of magical thinking the shale guys and the Carbon Utopians use.

The cost of wind turbines, the only technology which comes remotely close to competing with power generated from $10 to $11 per MCF natural gas, are going up, not down.

Dennis,

But the real poison pill for wind and solar is the intermittency problem. There is no viable, scalable solution to the intermittency problem using existing technology (other than maybe in arid regions inside 35 degrees latitude north and south), other than having a parallel back-up fossil fuel or hydro system.

Grids always have some spare capacity beyond average peak load. This safety margin handles unexpected peaks, unplanned outages, and other random fluctuations. How much depends on a grid’s many specific details, but 10 – 20% reserve margins are typical.

For very small wind and solar generation proportions, the ‘normal’ reserve suffices. As the percentage of wind in the generation mix grows, it increasingly does not.

Increasing wind and solar to 10% of pre-existing grid capacity is the easy part. Anything over that and all hell breaks loose. That’s the predicament that Germany, and Texas, find themselves in now. (Germany generates about 13% of its electricity from wind and solar and Texas, on its ERCOT grid, 10.6% in 2014)

UK’s zero wind for three days in December, 2012 during its winter peak load season illustrates the National Grid’s need for wind backup. UK peak load is handled by flexing fossil fuel generation.

Glen says:

Do you also agree that the costs of wind and solar have been falling dramatically?

No.

Ok, that pretty much says it all! At least now I understand where Glen is coming from. Even though the facts absolutely contradict his opinion, he is certainly entitled to it.

Unfortunately it is not possible to have a meaningful discussion with someone who insists that white is actually black!

http://www.bloomberg.com/news/articles/2015-08-31/solar-wind-power-costs-drop-as-fossil-fuels-increase-iea-says

The cost of producing electricity from renewable sources such as solar and wind has dropped significantly over the past five years, narrowing the gap with power generated from fossil fuels and nuclear reactors, according to the International Energy Agency.

“The costs of renewable technologies — in particular solar photovoltaic — have declined significantly over the past five years,” the Paris-based IEA said in a report called Projected Costs of Generating Electricity. “These technologies are no longer cost outliers.”

I guess the IEA must be part of the renewables lobby…

Fred,

It is indeed a true statement that “The cost of producing electricity from…solar…has dropped significantly over the past five years, narrowing the gap with power generated from fossil fuels and nuclear reactors.”

But according to the Union of Concerned Scientists, the gap between power generated from natural gas and solar is still very large.

Why do you believe Germany finally got the message, drastically cutting its subsidies for solar, such that new installations for solar have all but ground to a halt?

That leaves wind.

Fred,

So with the cost of solar placing it completely out of the competition, that leaves wind.

Who do you believe has the sharpest pencil, Warren Buffet, who has invested $15 billion in wind, or the EIA?

The main US federal incentive for wind is the wind Production Tax Credit (PTC), created by the Energy Policy Act of 1992.

The PTC was renewed in December, 2015 and now stands at 2.3₡/kWh for the first ten years of generation.

When the PTC was created in 1992 it was intended to jumpstart the industry, so has expired via sunset provisions several times over the past 23 years. Each time, US wind investment promptly collapsed. Each time, Congress promptly renewed PTC at the same or higher incentive rates. Why?

At Berkshire Hathaway’s (BH) 2014 annual meeting Warren Buffet said:

I will do anything that is basically covered by the law to reduce Berkshire’s tax rate. For example, on wind energy, we get a tax credit if we build a lot of wind farms. That’s the only reason to build them. They don’t make sense without the tax credit.

Wind, and this is straight from the horse’s mouth, cannot currently compete with electricity generated from natural gas absent government subsidies.

And in addition to the PTC, Buffet also benefits from a smorgasborg of state subsidies for his wind investments.

But that still leaves the intermittency problem. When wind generation on Buffet’s grids grows to the point where it starts giving him headaches flexing fossil fuel generation, do you believe he will continue to invest in it?

Buffet is in it strictly for the money. He’s not out to save the planet, as he demonstrated very clearly last month in Nevada.

Hi Glenn,

Costs have come down since 2011, so look at more recent data for Wind. It is beating natural gas in good locations such as the Great plains (Iowa for example). Last I checked natural gas prices are pretty low in the US and this is unlikely to still be true in 10 years.

For intermittency see

http://www.sciencedirect.com/science/article/pii/S0378775312014759

Abstract

We model many combinations of renewable electricity sources (inland wind, offshore wind, and photovoltaics) with electrochemical storage (batteries and fuel cells), incorporated into a large grid system (72 GW). The purpose is twofold: 1) although a single renewable generator at one site produces intermittent power, we seek combinations of diverse renewables at diverse sites, with storage, that are not intermittent and satisfy need a given fraction of hours. And 2) we seek minimal cost, calculating true cost of electricity without subsidies and with inclusion of external costs. Our model evaluated over 28 billion combinations of renewables and storage, each tested over 35,040 h (four years) of load and weather data. We find that the least cost solutions yield seemingly-excessive generation capacity—at times, almost three times the electricity needed to meet electrical load. This is because diverse renewable generation and the excess capacity together meet electric load with less storage, lowering total system cost. At 2030 technology costs and with excess electricity displacing natural gas, we find that the electric system can be powered 90%–99.9% of hours entirely on renewable electricity, at costs comparable to today’s—but only if we optimize the mix of generation and storage technologies.

Your source is to a large extend nonsense. Electricity is only a small part of the typical energy bill of a German household. Real energy poverty is a result of high heating costs, i.e. not electricity.

Uncriticla Comparison with France are nonsense as the French electricity price is of course subsidized by the French government. Hint: EDF and Avreva are in interesting economic situation.

Or are you happy when the true costs of your energy is disguised?

Ulenspiegel,

You affluent elitists amaze me. You live in your own little bubble world, oblivous to how much of the rest of the world lives.

Obviously, you’ve never had any experience balancing the budget of a working-class household.

I have balanced the budget of a working class household most of my life, and so has most of my family.

The way you get ahead is that you sacrifice in the short term so as to invest in the long term. That is what we have all done, and we are all mostly “middle class” now with some family members earning top one percenter incomes.

We have for instance seldom taken the rent road, other than long enough to get a university degree, etc. Owning is more expensive up front, but generally FAR more economical long term.

I notice you REFUSE to answer Dennis’s question.

Just to make sure anybody paying attention does not forget that fact, I will ask it AGAIN.

Is it your contention that peak fossil fuels will either never occur or will happen so far in the future (say after 2050) so as no investment in renewables is needed? Or is it that subsidies should be reserved for fossil fuels only (and maybe nuclear power as well)?

You haven’t answered it , and I am confident that you will not, except with a politician’s non anwer about some other topic or question.

Dennis,

Who decides what is valuable?

In Germany, when it comes to electricity, it is the state which decides the value.

Back in 2000, when the EEG renewable Feed-in Act first took effect, a kWh of electricity generated by PV was valued at 50₡.

So not only did the German government mandate that the utility companies buy whatever power was offered by the owners of PV systems, but it also required them to pay the 50₡ per kWh price.

At that same time, the full cost of utility companies to generate that same kWh using fossil-nuclear was only 7₡.

So the electric utilities were compelled to pay more than a 700% premium to owners of PV systems over what they could generate the electricity themselves.

Now, 16 years later, that premium has been reduced to only about 220%, the result being that PV installations have all but ground to a halt.

Dennis,

Who decides what is valuable?

In Germany, when it comes to electricity, it is the state which decides what is valuable, and what the value is.

Back in 2000, when the EEG renewable Feed-in Act first took effect, a kWh of electricity generated by PV was valued at 50₡.

So not only did the German government mandate that the utility companies buy whatever power was offered by the owners of PV systems, but it also required them to pay the 50₡ per kWh price.

At that same time, the full cost of utility companies to generate that same kWh using fossil-nuclear was only 7₡.

So the electric utilities were compelled to pay more than a 700% premium to owners of PV systems over what they could generate the electricity themselves.

Dennis,

Who decides what is valuable?

In Germany, when it comes to electricity, it is the state which decides what is valuable, and what the value is.

Back in 2000 a kWh of electricity generated by PV was valued at 50₡.

The German government required the utility companies buy whatever power was offered to them by the owners of PV systems, and required them to pay the 50₡ per kWh price.

At that same time, the full cost of utility companies to generate that same kWh using fossil-nuclear was only 7₡.

Dennis,

Who decides what is valuable?

In Germany, when it comes to electricity, it is the state which decides what is valuable, and what the value is.

Back in 2000, when the EEG renewable Feed-in Act first took effect, a kWh of electricity generated by PV was valued at 50₡.

At that same time, the full cost for utility companies to generate that same kWh using fossil-nuclear was only 7₡.

That’s over a 700% premium the government forced the utilities to pay for PV electricity, over and above what they could generate it themselves.

That premium has now been reduced to about 220%, the result being that new PV installations have all but ground to a halt.

Hi Glenn,

As far as I understand the government of Germany is democratically elected. If the German people think this is a bad idea, they should elect different members to Parliament who will change the laws.

Dennis,

Just give them a little time. The German public is on a learning curve, and they’re getting there.

For instance, the feed-in tariff for newly installed rooftop PV has been reduced from 58₡ in 2004 to 14₡ in 2013, and then to 12₡ in 2015.

Installation of these systems has all but ground to a halt.

Yair . . . .

“the full cost for utility companies to generate that same kWh using fossil-nuclear was only 7₡.”

That’s probably more bullshit . . . . how are the costs calculated to store, transport and reprocess spent fuel and the costs of dismantling the plant and rehabilitating the site when the unit reaches the end of its use full life.

You’re saying those costs are included in the seven cents a unit?

Cheers.

scrub puller,

The 7₡ figure comes from the Fraunhofer-Institut für Solare Energiesysteme ISE chart I posted in my comment above.

http://peakoilbarrel.com/international-rig-counts-2/#comment-555455

Do you believe you have a better source? Then where is it?

You nailed it Dennis. It’s always ‘trimming the fat’ or a good idea to wait when it’s the ‘other guy’ making the sacrifice. Suggest readers watch PBS series “The Dust Bowl”. Sometimes, the right thing to do is help, and subsidize. Roosevelt had it right. Without his actions there would have been even more social upheavel and even revolution as far as I can tell.

I think many are just skipping Glenn’s comments these days.

Paulo,

Yep.

FFS Glenn, answer the actual question Dennis has asked you!

You are more slippery than slime.

Thanks for noticing Dave. Perhaps Glenn should run for political office, he is good at not answering questions, but still says a lot that might sound impressive to the common man.

needs more beating!

Not quite dead yet. 🙂

Dennis,

Oh I think it’s folks like you, ezrydermike, Dave, oldfarmermac, and Paulo who should run for political office.

I can see it now, you guys campaining to double or triple household electricity rates.

I’m sure you can convince folks to be proud that their country is in the forefront of fighting the pending global catastrophe that will result from the overproduction of that nasty, dirty, horrible carbon.

Higher electricity costs is a small price to pay for global adulation, and being mentioned as a shining example of what can be done by keeping one’s eyes focused solely on the glorious future, while ignoring yesterday’s and today’s catastrophes.

And while you’re at it, maybe you can treat your working class to a little bit of this employee compensation action too. I’m sure you, like Richard Nixon, will be able to convince them that it’s what John Maynard Keynes would have wanted:

Dennis asked you some simple questions but you avoided answering them, why?

I will now skip past your posts (and will recommend others do too) as you have shown you are full of hot air and behave like a Koch.

Actually people like Barack Obama have been and ARE running for office in even the somewhat backwards USA, and they are winning, quite often, and they are campaigning on going renewable and getting away from fossil fuels.

And even though I will always be a conservative ( playing by the Humpty Dumpty rules of linguistics and defining the word to suit myself ) I am GLAD environmentalists are making substantial progress politically in most parts of the world. Not ENOUGH progress, but still a substantial amount.

BUT our inestimable GS is as capable of looking the other way as the referee in a tag team pro wrestling match. As a matter of fact, if he were to apply for a pro wrestling referee’s job, his comments here in this blog would be AMPLE evidence he is fully qualified, he would be hired first opening.

OFM,

Folks like myself who are in the upstream oil and gas business actually stand to benefit from the new standards promulgated by the EPA last August.

The principle victim of the EPA ruling is coal (that is if the ruling manages to withstand the numerous court challenges it faces). But even though renewables may stand to benefit from the ruling, it is natural gas, and not renewables, that will pick up most of the slack created by the demise of coal.

Another thing Obama did that helped domestic oil producers was canceling the Keystone pipeline.

These issues are not nearly as black and white as your highly simplistic Manichean construct of the world leads you to believe.

In Germany, to cite another example, coal has done quite well as a result of Energiewende.

The German Energiewende has not resulted in less dependence on the burning of coal to generate electricity and will not do so anytime soon.

“That Man is the product of causes which had no prevision of the end they were achieving; that his origin, his growth, his hopes and fears, his loves and his beliefs, are but the outcome of accidental collocations of atoms; that no fire, no heroism, no intensity of thought and feeling, can preserve an individual life beyond the grave; that all the labours of all the ages, all the devotion, all the inspiration, all the noonday brightness of human genius, are destined to extinction in the vast death of the solar system, and that the whole temple of Man’s achievement must inevitably be buried beneath the debris of a universe in ruins – all these things, if not quite beyond dispute, are yet so nearly certain, that no philosophy which rejects them can hope to stand. Only within the scaffolding of these truths, only on the firm foundation of unyielding despair, can the soul’s habitation henceforth be safely built.”

Bertrand Russell.

In the end does it really matter if civilization collapses today or 5,000 years from now or if the biosphere collapses this century or is boiled to death by an expanding and dying sun a billion years hence? Because eventually every last trace of life and human existence will be snuffed out by the Universe itself. What is the struggle really for? It is all for nought. Nothing will exist, nothing will remain, nothing will be remembered. Just human delusion of self importance, a wishful longing for some meaning in an inherently cold world.

“What is the struggle really for? It is all for nought. Nothing will exist, nothing will remain, nothing will be remembered. Just human delusion of self importance, a wishful longing for some meaning in an inherently cold world.”

Again, well said. We inhabit a small, warm, wet rock orbiting a middle-aged, insignificant star far, far away from the center of the known/unknown universe/multiverse. It is conceivable that we are the only humanoid-like, higher-order lifeforms in the universe, which makes us unique but also highly selectively adapted, and thus highly vulnerable, to the uniqueness of our planet’s atmosphere. Odds are that our existence will last hardly a fraction of a fraction a fraction of the blink of time of the cosmic eyelid.

What is the struggle really for?