This post updates Non-OPEC production to February 2020. However we are now in late June 2020 and the effects of the plunge in the price of WTI which began on January 6 and ended in the negative low of $-37.63/bbl on April 20 is showing up in plunging production numbers in US and other oil producing countries that post more recent output numbers. However WTI has now recovered to close to $40/b and weekly US production numbers are indicating that output may have bottomed.

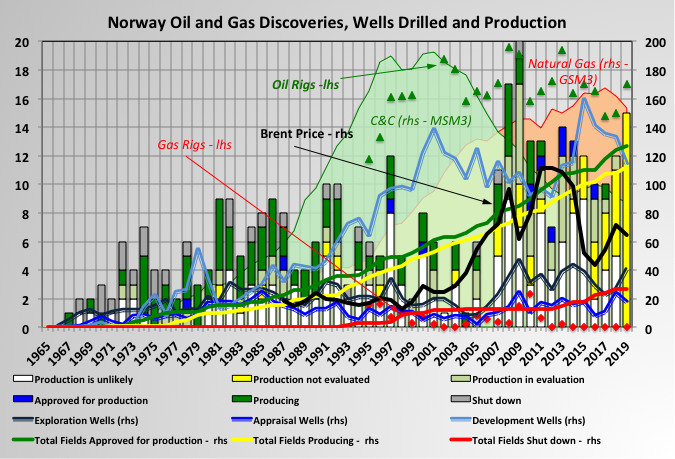

Drilling and development activity off shore Norway has been fairly steady through the life of the basin. This has been partly from government policy, through tax relief or direct action, but also through opening up of new areas as technology becomes available. It has moved from mainly producing oil to now being dominated by gas, although there is little direct gas exploration now (note that converting gas to o.e. is simple in S.I. units and is just a factor of 1000).

Drilling activity has been high in the 2000’s for development wells (including a lot of in fill drilling and some major redevelopments) and exploration (I think there is very favourable tax arrangements that encourage drilling in even fairly low prospective areas). Appraisal drilling has been more flat and there has been some reports that some discoveries have proved disappointing after start up, possibly because of insufficient drilling before development was approved.

There are twelve projects “approved for production” (i.e. in development) with average reserves of 26.5 MSm3 and average discovery year 2001; nineteen projects “production in clarification phase” (i.e. in FEED or pre-FEED) with average resources of 25 MSm3 and average discovery year also 2001; twenty nine projects “production likely but unclarified” (i.e. in conceptual design) with average resources of 10 MSm3 and average discovery year also 2003; and twenty eight projects “production not evaluated” with resources of 8.5 MSm3 and average discovery year also 2010.

The number of “hydrocarbon shows” has been large recently but they have mostly been small with “production unlikely” or “not yet evaluated” (and present prices mean most of these are likely to be deferred at best).

The number of development projects per year has, if anything, been increasing slightly, although the size has been generally decreasing. The number of shut down fields is increasing slowly but the have been a number that have had their life times extended beyond their original shut-down date (through improved reservoir performance and/or major redevelopments).

The oil price may have influenced activity but I can’t really see it much, maybe the effect of the current crash will be more obvious.

While this post updates Non-OPEC production to January 2020, we are now in late May and the direction for future production for the next few years is clear, LOWER than where it was in March 2020. OPEC, in response to the reduced worldwide demand, arranged for a production reduction through a Declaration of Cooperation (DoC) with OPEC and Non-OPEC countries. Also Canada and Norway have indicated they will be cutting production in response to world wide reduced demand. The OPEC + DoC reduction schedule and chart are shown and discussed at the end of this post.

All of the oil production data for the US states comes from the EIAʼs Petroleum Supply Monthly. In addition, information from other EIA offices is provided to project future US output. At the end, an analysis of a few different EIA reports is undertaken.

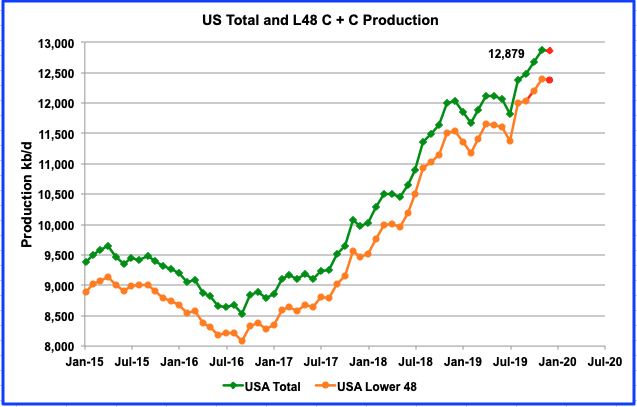

The charts below are updated to November 2019 for the 10 largest US oil producing states (>100 kb/d).

The latest data from the January EIA report shows that US production surged by 203 kb/d in November to reach a new high of 12,879 kb/d. Since June the US has increased output by an average of 164 kb/d/mth. Looking forward to December production, the January Monthly Energy Review (MER) estimates US production for December to be 12,861 kb/d, down 14 kb/d from November and shown in red as the last data point.

If the MER is correct for December at 12,861 kb/d, that means that the January 2020 STEO is too high in their output prediction. They estimate December output to be 12,967 kb/d, 106 kb/d too high.

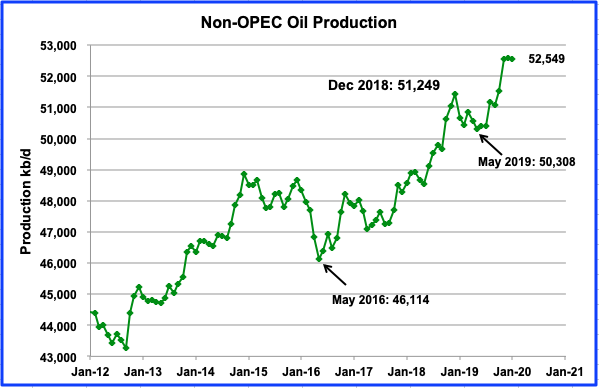

Below are a number of oil (C + C ) production charts for Non-OPEC countries created from data provided by the EIA’s International Energy Statistics and updated to September 2019. Information from other sources such as the IEA and OPEC is used to provide a short term outlook for future output and direction.

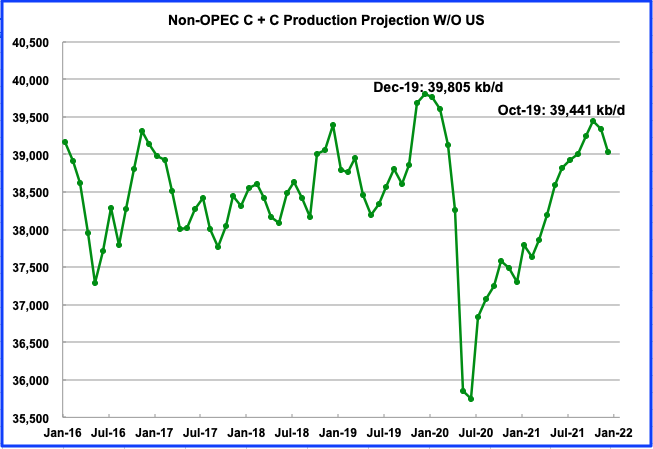

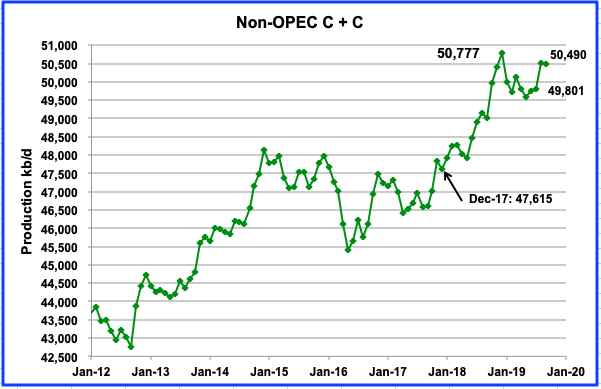

Non-OPEC production decreased by 22 kb/d from 50,512 kb/d in August to 50,490 kb/d in September. This is another output reduction month in 2019. In 2019 there have been 5 months of decline and 4 months of increases. For comparison purposes, in 2018, there were 9 monthly increases and 3 decreases. This is just another indicator of the increasing difficulty Non-OPEC countries will have boosting output going forward, now that US production growth has started to slow.

September production is just 287 kb/d short of the previous high of 50,777 kb/d reached in December 2018. Will new output from Norway and Brazil, along with small but increasing US output coming in the next few months raise Non-OPEC output beyond the previous December 2018 high?