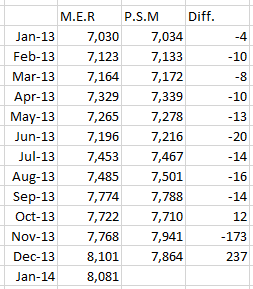

The EIA releases two monthly petroleum data sets for US oil production. The Monthly Energy Review which gives the US production and consumption of all forms of energy, oil, natural gas, coal and electricity. The other, the Petroleum Supply Monthly deals only with petroleum but gives every possible statistic, production, refining, export and import from every state and district.

Concerning total US crude oil production the two should agree but they don’t. From December 2011 back they have the exact same production numbers but the near months differ greatly. I have found that the latter, the Petroleum Supply Monthly is the most accurate. The Monthly Energy Review usually changes their numbers to match the Petroleum Supply Monthly but both revise their numbers as more accurate numbers come in. They both are published the last week of the month but the M.E.R is always a month ahead with their data.

Here are their the numbers in KB/d and the difference between the two.

Notice that the former had US production up by 333 kb/d in December while the latter had US production down by 77 kb/d in December. But both will be revised to match what each state or pad reports later on.

There is no uniform reporting strategy among different states. They all appear to do it differently and on a different time frame. For instance the PSM, which is the only one of the two that reports state by state production number, reports the exact same numbers for North Dakota that we get from North Dakota. But they get their Texas data from the Texas Rail Road Commission. And the Texas RRC is very delinquent with their reporting. They just report the numbers as they come in from the field and every month they change as more numbers come in, sometimes taking many months until all the numbers are in. So the EIA just guesses at Texas production numbers.

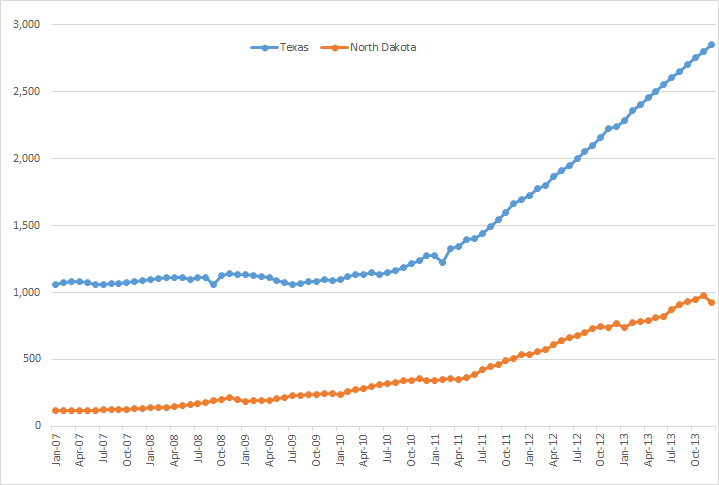

Texas and North Dakota daily C+C production in KB/D. The last data point is December 2013.

Notice the last nine months are extremely linear. In fact each month, April through December, Texas monthly crude production increased by exactly 50,000 barrels per day.

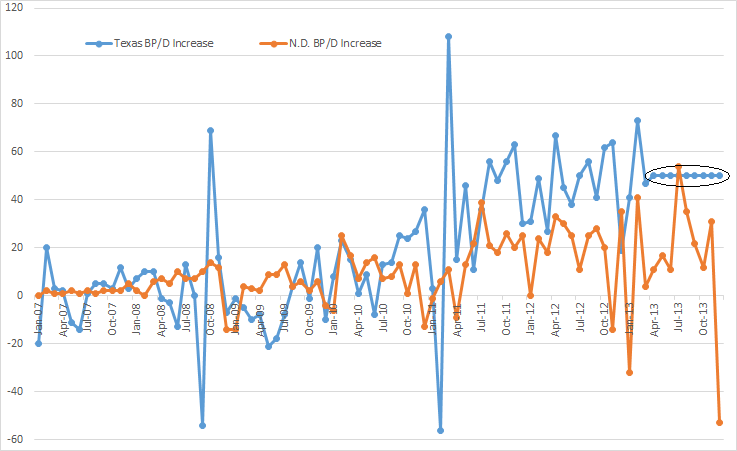

Here below is their production, along with North Dakota, plotted on as change per month. The December drop in North Dakota production is exactly what was reported by the State.

Notice the last nine months of Texas production increase. The EIA is guessing that Texas oil production will have increased by exactly 50,000 barrels per day every month from April through December 2013. The up and down spikes in 2008 and 2011 was just a reporting anomaly. Barrels not counted in one one month were counted the next month instead, causing a down spike one month and a corresponding up spike the next. But what this does tell us is that the EIA reports exactly what the Texas RRC reports, when they finally get around to reporting.

This also means that we don’t really get any good data for Eagle Ford and the Permian because the data we get from the EIA’s Drilling Productivity Report will reflect this same wild ass guess.

Basically this means we will not know when the US C+C peaks until several months after the fact. But we should get some hint when the EIA starts to lower their guessing numbers as to Texas Production.

I understand that perhaps half of Texas production is conventional oil, not shale oil but nevertheless this chart tells us that when US shale oil peaks, the US peaks… again.

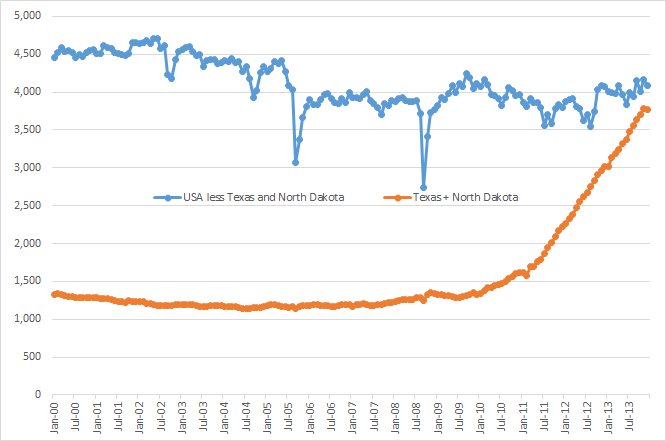

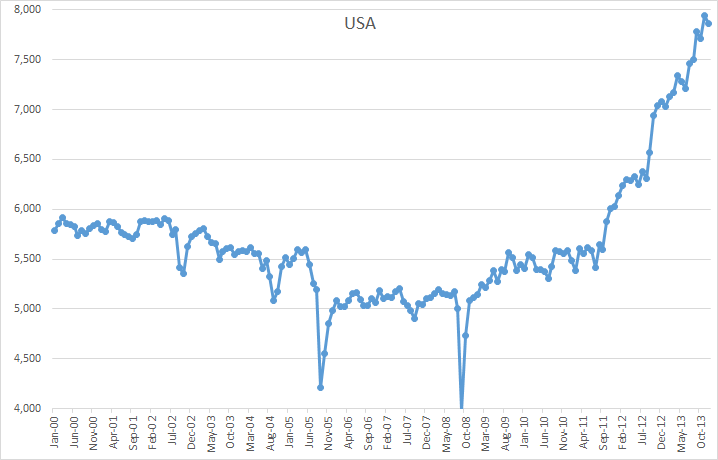

Here is the US C+C production using data from the EIA’s Petroleum Supply Monthly in kb/d. The last data point is December 2013.

Here you can see clearly that the US Shale or LTO production, beginning about two and one half years ago, has increased US production by 2.5 million barrels per day. This year will tell the story of whether that will continue or not. My bet is we will definitely see a slow down but just how big a slow down I can only guess.

News Jacking

In a way, the world’s major oil companies all suffer from some version of the same problem: They’re spending more money to produce less oil. The world’s cheap, easy-to-find reserves are basically gone; the low-hanging fruit was picked decades ago. Not only is the new stuff harder to find, but the older stuff is running out faster and faster.

EXCLUSIVE-North Dakota Jan oil output flat as winter chills drilling-data

Growth in the larger Eagle Ford shale in south Texas also ground to a halt at around 1.1 million bpd, according to the LCI data, which was made available to Reuters.

Parts of North Dakota had the third coldest December on record, so frigid, according to local papers, that diesel fuel froze in truck tanks. In January, it was the wind that forestalled the drilling and hydraulic fracturing operations that are necessary to keep output growing.

Still, it is likely to be a temporary lull in the otherwise upward trajectory of the Bakken region, whose bounty turned North Dakota into the country’s No. 2 oil-producing state. Regulators expect the backlog of wells waiting on completion, numbering 635 in December, to be up and running by May.

“In spite of the weather declines experienced in January, oil production from shale oil wells increased 30 percent from January 2013 after increasing almost 60 percent the year before,” said George Lippman, president of LCI.

Two things I take away from this. First the EIA will have to adjust their guess for Texas production for December because Eagle Ford also took a hit that month. Second if shale oil production increased by 60% in 2012 and 30% in 2013, we can clearly see a trend.

And how did I miss this one that came out about a week ago?

Expert: World could face oil shortage

Global demand for oil is about 90 million barrels a day. Factoring in production declines as well as new demand from emerging nations, in 10 years the world will need another 55 million barrels a day of oil, he said.

“I see a lot of forecasts for the future, but nobody is saying where the oil is going to come from,” Powers said.

319 responses to “EIA’s Petroleum Supply Monthly by State, Texas Reporting Problems”

US crude oil production growth declined in December 2013. See the graph comparing rigs in operation (in the oil sector, left scale) and the annual change in 12-month cumulative crude oil production (defined as the total production over the past 12 months less the total production over the previous 12 months, right scale).

The observed peak in crude oil production growth took place in September 2013, when the 12-month growth was 368 million barrels. By December 2013, this had declined to 346 million barrels. The declining rate is approximatley 7 million barrels per month. At this rate, it would take 49 months or about four years before the US oil production reaches the next peak.

In term of daily production, US crude oil production was 7864 thousand barrels per day in December, which was 785 thousand barrels per day higher than in December 2012. By comparison, the December 2012 production was 1051 thousand barrels per day higher than in December 2011.

You have to wonder if the ongoing overall decline in Bakken output persists for another month or two will drillers be able to ‘catch up’ with current decline rates.

Daily output oil per well is shrinking not just number of new wells …

https://www.dmr.nd.gov/oilgas/stats/historicalbakkenoilstats.pdf

That’s just because their were less new wells (and also over time, there will be more and more old wells even with constant addition of equal wells).

The main point is that Enno’s cum curves show wells are averaging the same (actually slightly better) productivity/well from 2008 to 2013.

You do realize new roads may have as much to do with improved per well output as geologic technique?

Interesting. How?

Trucks can carry more per day. More roads get them where they were going to load from an onsite tank faster, which means they can get to more onsite tanks per day, which means a well that had to stop because of a full onsite tank need no longer be stopped.

Go to the previous posted article, page 2 of the comments, there is a link entitled “long line of trucks”. The visual tells the story.

Thanks.

The guy in the article says 30% increase from Jan 2013 for Jan 2014. That would be a 14K bpd gain over Dec.

Consider the discrepancies between the weekly crude oil production data and the monthly data. Look at the graph below, showing the 52-week change in 52-week average weekly oil production.

The weekly data imply the US crude oil production in 2013 was 1.24 million barrels per day higher than in 2012. The monnly imply the growth from 2012 to 2013 was only 346 million barrels or 0.95 million barrels per day.

Ron:

Kudos on the plot of Texas numbers (must be models, should be so labeled) as well as the story on estimated JAN ND production.

For the other stuff (majors problems, an old oil exec saying we are running out), that’s been covered.

(must be models, should be so labeled)

I have no idea what you are talking about. The charts were all made with real data published by the EIA.

I mean that EIA is reporting modeled numbers and they should so label them. Nothing against you, against them. Ya done good.

Oh, you mean estimates! No, the EIA does not label them as estimates. Sometimes in their PDF tables they will put an “E” beside the total US data, or sometimes even an “RE” meaning a revised estimate. But they never label their Excel data as estimates.

However I thought I explained all that in the text. They must estimate the Texas data for the latest months because the Texas RRC simply takes months to report the actual production numbers.

I know what you said in your post. You just didn’t understand my comment. Now you do. 😉

Keep up the good work and don’t take any guff from the hoi polloi. 😉

http://theworldenergydilemma.com/about-the-author

An old exec saying we are running out. Head Petroleum Engineer for ARAMCO for 2 years, probably knows what he is talking about as it pertains to KSA. You don’t hear someone that previously worked for ARAMCO offer up much of anything.

Ron, you remember that old Yamani article I sent you where he said in (1980) that the world better get their act together in the next 30 years or it will be to late. Now Powers says KSA can produce for 30 more years.

Great stuff as always Ron. Thanks for your diligence.

Thanks Ed. No I don’t remember that Yamani article. Please send me the link if you still have it, or post it here. I think KSA can produce for 30 more years, just not very much. Did he say how much they could produce in 30 years?

Occasionally you do hear a Saudi official slip up and tell the truth.

U.S. Reliance on Oil From Saudi Arabia Is Growing Again

On page 2 of this New York Times article we get this:

“This is strictly, totally business,” said Sadad Al Husseini, a former executive at Saudi Aramco, the state oil company. “Saudi production is flat out. Where you send it is a matter of where you make the best profit.”

Bad news about the book… based on the Amazon preview and this review, it seems more like a memoir than a reasoned analysis. The reviewer recommends “Peeking at Peak Oil” as a superior study of the same issues.

http://www.amazon.com/review/R1C21EHA5HZ3RD/

US oil rises on Bakken supply rumours

http://www.upstreamonline.com/live/article1353885.ece

Crude oil loadings at a dozen major North Dakota rail terminals fell by more than 200,000 barrels on average in the past two days, data from industry intelligence provider Genscape showed on Friday according to Reuters.

Posted that a few hours ago on the previous post. Fleshing this out:

Boom.

http://www.reuters.com/article/2014/02/28/oil-bakken-rail-idUSL1N0LX1N720140228

“The Genscape data, made available to Reuters, showed that only 220,000 barrels were loaded at the terminals on Wednesday, the day after the DOT order, an exceptionally low rate.

On Thursday, seven of the 12 terminals monitored by Genscape loaded a total of 470,000 barrels; five terminals did not load at all, although two of those had been operating on Wednesday, according to the data.”

There is handwaving about a new DOT regulation that will “have government get in the way”, but it smells a lot like manufactured excuse.

btw the math . . . 200K barrels lost each day for 2 days is 400K barrels. / 28 (days in Feb) = 14285 bpd off of whatever number would would have seen in the month’s report we’ll see in April.

hmm or maybe not. We have presumed the measure is taken at the wellhead. There may be enough storage on site to keep the well operating even if there are few days of obstruction downstream, as it were.

The producers are paid upon/after delivery to their customers (refineries). Less oil transported means deferred cash flows for the companies.

Very good. True. But we won’t see that in the monthly output very soon.

Perhaps eventually, tho.

Rune: what happened with your 600-700 M bpd prediction? Why off and what learned?

My phrasing in http://www.theoildrum.com/node/9506 (back in Sep 2012) was:

“Now and based upon present observed trends for principally well productivity and crude oil futures (WTI), it is challenging to find support for the idea that total production of shale oil from the Bakken formation will move much above present levels of 0.6 – 0.7 Mb/d on an annual basis.”

(And I was referring to the Bakken formation in North Dakota, that is I did not include Montana)

For all of 2013 production from Bakken (ND) was an average of 794 kb/d.

1. So why were you wrong, low? It’s not just to hold you accountable, but what can you learn? Was it peaker bias? Poor model? Price crash? What assumption was off that drove it low?

2. You reiterated the prediction as late as JAN2013 (post was rerun). And the first calander year, your prediction was broken. Heck, I wonder if a 12 month period centered on JAN2013 would already break your prediction. Even with zero growth (unlikely), we will finish 2014 at about 900 k per month. Breaking your prediction even more.

3. Take a look at the image here (cum curves by year): http://peakoilbarrel.com/reverse-engineering-north-dakota-bakken-data/comment-page-2/#comment-9747

I mean 900 M/day. Lysdexic

A note on the Chart that Nony referenced above.

The 2007 cumulative curve is a combination of 2007 and some earlier wells (those that produced more than 1000 b/d as of Jan 2007) so that curve should probably be ignored. I found this out in an email conversation with Enno who has been a huge help (and very patient with my endless questions) after I had posted the chart.

I still think you ought to write an article on why/how you were wrong. Would be the straightforward thing to do. Was a lot of press on the dreaded Red Queen article, so fair thing to do would be to square that up.

In december the Bakken producing well count increased by 40. That means at least 40 new wells came on line. Nevertheless production per well decreased from 134 barrels per well per day to 126 barrels per well per day. That is a decrease on 6 percent in one month even when counting new well production. In December they could not run fast enough to stay in the same place.

That is the Red Queen in action!

I actually completely agree with you. It’s sort of like coal mining. If you shut down the extraction, production drops. And yeah, you definitely saw it in cold December 2013. Big time.

Still…we sure beat that 650 +/- k bpd of Rune’s post. The Red Queen is an evil bitch, but we kicked her ass in 2013. USA! (Eurocoms hate our pioneer spirit.)

650 +/- 50. Lysdexic. 🙁

Hi Nony,

Another thing in Rune’s model was that he used WTI for his oil price, which intuitively it seems that would be your choice as well (based on our conversations).

My thinking is that the marginal Bakken barrel goes to the East coast where refinery gate prices track Brent prices more closely than WTI, the WTI price would be correct if all of the Bakken oil was being sold to Midwest refineries, but in that case the $12/barrel transport cost in Rune’s model would be too high (because it is much less than that cost, perhaps $4/ barrel to transport to refineries in the Midwest.)

Based on WTI futures prices and $12/barrel transport costs, it looked as if Bakken oil would not remain profitable for very long back in Sept 2012. In addition well productivity was dropping slightly relative to 2011 wells, but this has changed in 2013.

For all of these reasons Rune’s scenario was a little on the pessimistic side, but personally I have learned a huge amount from Mr. Likvern and appreciate his work and his willingness to patiently share his knowledge with others.

Note that a big piece of his pessimism was a result of using WTI futures to predict 2013 and 2014 oil prices. Maybe Rune can comment on how good an estimate of future WTI prices the Sept 2012 futures price deck proved to be.

OK, thanks man

My thinking is that the marginal Bakken barrel goes to the East coast where refinery gate prices track Brent prices more closely than WTI,

Nope, the price the Bakken producer gets is actually about $20 a barrel below the WTI price.

Director’s Cut

Nov Sweet Crude Price = $71.42/barrel

Dec Sweet Crude Price = $73.47/barrel

Jan Sweet Crude Price = $74.20/barrel

Today Sweet Crude Price = $81.35/barrel

Are those the wellhead prices? Transport netted out?

I have no idea but I assume they are wellhead prices.

That is my impression as well, the listed NDIC prices are ND wellhead prices. What a company may do is to establish a trading company, selling the oil at the wellhead then paying the transport from the wellhead to the refinery and then pocketing the profit or……. loss.

Looking at todays price ($81/bbl, due to lower shipments??) a company could sell it for say $101/bbl, thus making $20/bbl and paying the transport of say $12/bbl, thus netting a profit of $8/bbl (that is post tax!)….which is a lot!

Exxon started as a transport company!

There are several things to keep in mind here.

Bakken oil (in general) has an API gravity of 36 – 44, which means it is very light (more like condensate) and thus have lower volumetric energy content than Brent oil (something like 5 – 8 % lower). What is being sold is energy and the ability to refine the “crude” into commercial products.

There is a limit to much LTO (Light Tight Oil) a refinery can allow into its feed.

The $12/bbl transport cost was from EIA that (at the time of writing) listed transport costs from Bakken to the refineries in the range of $12 – $15/bbl. (In other words I deliberately choose to go with the lower end to avoid being labeled as pessimistic).

As far as transport goes, pipelines is the most cost efficient way to move large volume oil over long distances, like oil from Bakken, for some reasons pipelines matching Bakken production growth have not happened.

Why? What is it the oil companies know that makes them not willing to commit to long term shipping rights (in pipelines) that would have increased their net back (and thus profits per barrel)?

The oil price has been in (steep) backwardation for some time (for what that is worth), and it is easy to use whatever future oil price for any scenario analyzed, however using futures gives everyone the same reference platform (this is about transparency).

I believe that the oil price in the short to medium term will move lower, simply because a growing number of consumers can not afford expensive oil.

I have several Bakken scenarios also some that are more optimistic.

Bakken oil is almost identical to LLS or WTI (closest to LLS). There is an overall glut of light sweet crude in the US because the refineries were changed over for heavy sour (remember 10 years ago when everyone thought any new sources would be crappy? HA! HA!) and because of export restrictions.

If you have some information that the oil is low quality

You have to compare apples to apples. Brent is priced in London, WTI at Cushing. If you price them both at a refinery, they are very comparable, with maybe a slight bias to the WTI.

Bakken is good quality oil with a very high yield of gasoline. At the door, it’s competitive with LLS or WTI. No crapping on my baby. Go Bakken, go!

http://g.foolcdn.com/editorial/images/6886/crude-quality_large.jpg

If you have information that the crude is considered low quality or trades at a deficit at the refiner door, let me know. I have things like EOG and CLR investor presentations that say the opposite. Maybe you don’t trust that (although companies could get in trouble for lying in such). But do you have any info of your own to say it’s not good oil?

Nony,

Perhaps you can explain to all readers why Bakken oil at the wellhead is fetching about $20/bbl below WTI and close to $30/bbl below Brent?

I think we covered this.

The comparison for kerosene and diesel Ron did and I think the yardstick was LLS (though that may have been the Eagleford), but the original heads up on the matter was from a presentation that compared to Nigerian oil, and it was woefully light in those two fractions vs Nigeria.

The point would be phrasing. “Good quality” doesn’t mean anything. If customers want diesel from a refinery, the refinery has a preference for conventional oil. The operative reality would be a matter of definition. “Good quality” should not be used. Diesel rich vs not diesel rich is more meaningful to a refinery, if that’s what their customers want. Diesel is selling at a substantial premium to gasoline.

1. “What is being sold is energy and the ability to refine the “crude” into commercial products.”

Correction: latter part of sentence is correct, earlier part is not.

2. WTI similar to Bakken: look at this comparison:

http://www.hydrocarbonprocessing.com/images/798/89779/Bryden-Tab-01.jpg

API: 42 versus 40

sulfur: 0.2 versus 0.33

3. North Dakota Petroleum Council:

“Question: What is the API gravity of Bakken crude oil? Explain its relative quality.

Answer: Bakken crude oil gravity ranges from 36 to 44 degrees API. The quality of this oil is excellent, almost identical to WTI. The benchmark crude oil is West Texas Intermediate, which is 40 degrees API sweet crude. It is the benchmark because it requires the least amount of processing in a modern refinery to make the most valuable products, unleaded gasoline and diesel fuel.”

http://www.ndoil.org/?id=78&offset=5&advancedmode=1&category=Bakken%20Basics

4. CLR official investor presentation:

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTM0OTQzfENoaWxkSUQ9MjIyOTAxfFR5cGU9MQ==&t=1

See pages 22-24 discussing refiner’s view of the oil. And while I can understand you being skeptical of a company presentation, this thing went through corporate legal and is not making projections about future growth or the like…they are talking time now. See in particular the footnotes at the bottom of pages 23 and 24.

5. EIA discussion of Bakken/WTI differentials. Note that they only discuss transport as a reason for difference, not quality.

http://www.eia.gov/todayinenergy/detail.cfm?id=10431

6. Another discussion of WTI (Cushing) versus Bakken (Clearbrook) differential:

http://marketrealist.com/2013/11/bakken-discount-wti-widest-point-since-early-2012-affecting-energy-names-earnings/

(Note that none of the discussion is about Bakken being worse than WTI. Transport is the rationale used for differentials.)

7. 10 dollar difference of WTI and Brent. WTI has traditionally been slightly better priced than Brent because it is lighter/sweeter and easier to process. The reason for the current difference is US shut in light crude and that Brent is priced in London, WTI in Cushing. Land the WTI in London or the Brent in Cushing and the price difference will evaporate.

http://www.caseyresearch.com/cdd/tricky-calculus-oil-price-differentials

7. “20 dollar difference of WTI and Bakken”: We don’t know what that NDIC price means. Is it net transport, net taxes? You’re jumping to conclusions.

Hi Rune,

This is a little off topic.

I was wondering about point forward vs. full cycle costs for Bakken oil. I believe you tend to use the point forward method (which seems to be what the oil companies also use in their investor presentations.)

Art Berman often points out that in the long term it is full cycle costs that are important if the oil production is going to be profitable. Have you ever attempted to estimate (at least roughly) the full cycle costs vs the point forward costs? For the average Bakken oil company would this add say $5/ barrel to overall costs ( obviously this would vary from company to company).

I sometimes forget that my scenarios may be overly optimistic because I am ignoring land costs and other general overhead when doing my NPV calculations. You often do a very detailed analysis of the financials (digging into annual reports and such) so your insights would be enlightening. Thanks.

Dennis

Dennis,

What I have presented are point forward estimates. I also have full life cycle costs for some companies, but these are not for publication.

Full life cycle costs brings the break even price higher and there are differences among companies.

Hi Rune,

How much higher would the breakeven price be using full cycle costs? 5, 10, 15 dollars? I am just trying to get a rough idea.

Can you give me an idea of the top 5 or 10 oil companies operating in the North Dakota bakken and what % of the total bakken oil those 5 or 10 companies produce as a group? (For example the top 5 companies produce x% of ND Bakken oil.)

Or maybe someone else knows of a website that tracks this stuff I have had little luck finding information.

I have seen assay information that suggests that the distillate yield is 10% lower….

I don’t have the links handy though….

Hi Rune,

Nony is in agreement with you that futures are the best way to estimate future prices, perhaps the EIA is too optimistic, but their reference scenario in 2013 had prices decreasing out to 2015 (which agrees with you) and then rising thereafter, which I believe that both you and Nony think is incorrect (I am more confident of Nony’s views because we have discussed this). The AEO 2013 low price scenario, which assumes real oil prices fall to about $75 (2013$) by 2015 and then remain at about that level out to 2040. I think the reference oil price case is more realistic.

It is also interesting that the low price case seems right to people with different views, you think it is correct because limited oil supply will cause a recession, I believe that Nony thinks that supply will be plentiful and keep prices low. I think supply will be limited and will drive up price, but not so fast that it crashes the economy. This knife edge scenario is probably not very realistic. Prices need to rise if we are to get to the other side, low prices will be bad in the long run IMO.

Dennis, Rune,

The price of oil is the most difficult thing to predict. That is because it all depends on the state of the economy. And the state of the economy depends, to no small extent, on the price of oil.

If the oil supply starts to drop off then one would think the price would skyrocket. Doubtful. If the price of oil starts to skyrocket then the economy goes in the tank, prices drops even as production collapses even further.

That is exactly what happened in 2008 so no one can claim that it cannot happen again. But if it happens again production is very unlikely to bounce back this time. The marginal barrel is now above $100. That was not the case in 2009.

So where will the price of oil be in a few years? I have no idea just as I have no idea as to what the state of the economy will be in a few years. But I am definitely not optimistic.

Ron,

By using the futures price one allows for a reference for anyone to check out. I have observed that the futures may be a poor indicator, but one has to use what is available.

I expect oil prices to soften over time and as you point out small changes in the supply/demand balance may have huge effects on the price.

That several big oil companies now are reducing CAPEX and exploration supports your view that it becomes harder for supply to bounce back post a (new) steep decline in the price.

Plus, I guess “price” is very relative, and does not say everything. The real important measure is “affordability”. Since I have been learning about oil and the economy I realized that while the price of oil could go down, it could at the same time become more unaffordable as well. Which feels somewhat counter intuative..

My intuition is that the economy is already pretty bad and we don’t have indicators of a looming recession, but more indicators of coming out of one. So I don’t think the markets are pricing in a general further economic decline, but rather increased supply (not just US LTO, but Iran, Iraq, Libya). Of course, the futures may be wrong, just like a point spread for a football game. But it’s sort of the best guess we have. And it could be wrong low or high. These things happen…

Must be Bakken production has a significant impact on oil prices. Less Bakken oil, higher price of oil. Demand outstrips supply.

In the final analysis, Bakken Oil will command higher prices and control the price.

It’s at the end of the 11/10/12 Patzek post:

http://patzek-lifeitself.blogspot.com/2012_11_04_archive.html

“I see a lot of forecasts for the future, but nobody is saying where the oil is going to come from,” Powers said.

This is pasted from the My San Antonio link Ron posted up thread.

I have posted a lot of links recently and pointed out that the authors of these links are dancing around and not mentioning the two dirty words ” peak oil ” even though it is perfectly obvious that the data they present point without question to those two dirty words.

This is because their editors are prim and proper old schoolmarm types and don’t allow dirty words in their publications because they will not be a party to offending the tender young ears of the children who run the companies that pay the bills via advertisements for every thing from beer to Lear Jets.

Any journalist working for a mainstream publication that even thinks about mentioning the dirty words ”peak oil” is probably put on notice in no uncertain terms that if he does so in public he will not only be looking for a new job but also that he will be blackballed by all the major media and that any writing he does in the future will be on his own time.

I am sure there must be a few exceptions to this unwritten rule but I haven’t been able to find them.

My guess is that ” My SanAntonio ” is a small outfit and doesn’t collect much in the line of ad revenue and can there fore fly under the big business black ball radar.

And even so the author of this article avoids the dirty words.

But someday within the next few years just about everybody with a byline in the entire country will be wringing their hands about how they were mislead by all those crooked oil guys or else telling us that they are breaking the story of the century.

Peak oil was in the media just plenty in the past. See this chart. There’s no black helicopters.

http://2.bp.blogspot.com/-hC819n9EoFM/UfkIFielYMI/AAAAAAAAAlw/wgwD7GDqfqQ/s1600/screenshot_12.jpg

Just look back to all the folderol with Matt Simmons on CNBC predicting $500/bbl oil and the like.

I do not disagree with Nony’s black helicopters comment.

I was following peak oil religiously when Simmons was still with us but that was some years back.

If I have one thing to contribute to this debate in general it is my rolling stone background because I have never claimed to be any more than a well informed layman with a few dozen relevant science courses on my transcripts when it comes to peak oil.

One rolling stone experience was finishing somewhat over half of a RN program which I was unable to complete because I wound up being the caretakers 24/7 for my bedridden Mom. So I went back and started again and be damned if I didn’t have to drop out again and now I am pretty close to 24/7 tied down looking after my almost ninety Daddy.

Nobody in my family on his side ever seems to die from anything except accidents, bullets, and dementia. There is no heart disease, to diabetes, no cancer, etc, to be detected in his family tree as far back as a hundred years or so.Hence I have read a dozen books about dementias, all of recent copyright and written by medical professionals because I am no doubt going to be dealing with my Dad until he dies and he is now showing all the early signs of Alzheimer’s.

The odds are depressingly high I will go that way myself.

Now my point in revealing this personal history is that anybody who knows sxxt (doo doo) from apple butter about dementias and who followed Matt Simmons will tell you that the odds are astronomically high that he was suffering near the end from some sort of dementia. It came on pretty fast so it wasn’t Alzheimer’s. It was probably related to stroke or a cancer or something of that nature.

Now as far as his predicting five hundred dollar oil I don’t see any reason why the price could not go that high for a very short period of time in the case of a panic.

The spot price of natural gas has peaked regionally in similar fashion on numerous occasions because of nothing more than the inability of the gas companies inability to get in to market in extreme cold snaps.

But I always interpreted such remarks as artistic license for the most parts. Simmons was a banker above all else and there can be no doubt that he understood that the economy cannot support five hundred dollar oil.

I may not have made in clear that my very recent comments here on publishers self censoring due to the issue of losing advertising revenue are intended to apply to the last few months.

The failure to sell ads to businesses vested in ” business as usual” is quite enough to break a publication or at the least get the editors fired.No helicopters needed. Beyond that the ownership and management of most major media these days is so intermixed with that of the ”business as usual ” dominant economic interests that there is hardly any risk at all of an editor who would seriously challenge business as usual ever getting hired.

Even NPR finds it necessary in my opinion to avoid addressing hot topic issues such as peak oil directly for fear of causing or contributing to an economic down turn brought about by disillusioning or panicking the public.

So they can talk about global warming -because there is no immediate risk of anything being done about it that will hurt Wall Street.

But peak oil would panic their listeners as well as the public in general and be a fist in the gut of the liberal coalition as well because bad economic news is always bad for the faction in control in Washington and right now the liberals have two out of three of the government and a chance of putting another justice or two on the Supreme Court as well if they can hold on long enough.

Peak oil news would be equally unwelcome if the repugicans and conservatives were in control of course and probably even worse.

This is one of the times when both political wings stand to gain or at least hold their ground by ignoring developing bad news.

The republicans cannot capitalize on the opportunity be cause they are the ones most heavily vested in business as usual and not in position to use peak oil as a club to bash the democrats.Doing so would be tantamount to and admission that the whale lovers and tree huggers and the global warming faction have been right all along.

hehe that’s nice, Peak “Peak Oil Talk” was in 2005 as well 🙂

Hello and FWIIW

Is that an “annual basis”? 😉 How many wells are waiting for fracking? How was the weather this year?

You want to put some serious money behind 2014 having annualized production less than 700 M bpd (your prediction)? I’m totally serious. I will take the bet.

I really expected better from you. Opinion is dropping. DC may be a doomer to my cornie, but he’s a truthseeker, which is what matters in the end.

Nony,

I think Rune’s work has been excellent and I have learned a huge amount from him.

Rune’s prediction was based on the productivity of the average well going forward being similar to the 2011 average well that he dug out of the NDIC data (he was the first one to do this, that I was aware of), he also very graciously shared that data with me which enabled me to get started on some of my modeling, which is simply an extension of the work that Rune started.

I think Rune also was using something like 1500 wells added per year for his projections because his financial analysis led him to believe that ramping up wells at a higher rate would not be profitable (I am guessing here, I do not think he ever wrote that). Anyway wells were added at a higher rate than 1500 wells per year and that is the sole reason his estimate was a little low, if you look at recent projections that take account of actual well additions his model is right on the money. Note that his 1800 well per year forecast comes out slightly below the actual production because 2013 wells were about 5 % more productive than 2011 wells See chart (taken from Rune likvern’s website Fractional Flow http://fractionalflow.com/2013/12/23/in-bakken-nd-it-is-now-mostly-about-mckenzie-county/#more-738 and also posted here at Peak Oil Barrel

You are a good guy, DC.

Nony,

I just wanted to give you and others a feel for the history. Another quick point on Rune’s scenarios. He was not predicting what would happen. It was a scenario where he said, lets assume wells in the future look like the average 2011 well and lets also assume that 1500 new wells are added each year in 2013 and 2014, what would the output be in that case, what would it look like if 1800 wells were added in 2013 and 2014? If he had included a scenario with 2000 wells added each year, that may have been a better guess for 2014 and maybe 1900 for 2013 and 2014 would prove correct, but scenarios created in Feb 2014 are much easier to get right for 2013 and 2014, than a scenario created in Sept 2012.

It got huge press. If he had been right, would we hear this “just a scenario”? I think he owes it to do a followup and eat some crow. Would be manly and honest.

Now Gail…but let’s not go there. 😉

DC,

When I presented my results back in Sep -12 it was based upon available hard data and it was chosen to go for how cumulative 12 month productivity had developed from the wells analyzed (this is a very reliable indicator). I did not use the average for all 2011, but the average for wells started as from June 2011 which was far better than the wells during the first half of 2011. I did not say anything about how well productivity would develop as the data showed that after a decline, the productivity at the time had improved somewhat.

There are several things to observe for developments of a trend like Bakken, number of added wells, the companies financial positions (that is how much more debt are they able to assume), developments of the oil price (which have been higher than what the futures suggested back in 2012), how the global supply/demand balance develops and also how financials develops.

How demand for LTO develops (there is a limit to how much LTO that the refineries can absorb), bottle necks in the value chain (like transport) that may affect the price of LTO. As Bakken is landlocked buyers would love a situation where they could get Bakken oil very cheap.

Where would the oil price be if all countries had to run a balanced budget?

Just a few.

EOG has lower D/E than they did before. See their stunning conference call. And if you say that is from E going up…well hello! Market is making a judgment.

I’m really trying not to tear into you, but I think you are making excuses. Those wells are profitable is why they are being drilled.

Hi Nony and every body else too,

Please remember that not all of us know all of the abbreviations and acronyms. There will be high school and college students as well as Joe Sixpack’s reading these comments in ever increasing numbers and attention spans are short under the best of circumstances.

”EOG has lower D/E than they did before. See their stunning conference call”.

I read this blog daily and several other sites covering energy but I haven’t the foggiest idea who EOG is and only a vague idea what D/E might be since it is given without context.

A couple of unfamiliar acronyms is all too often enough to cause people to just click on another site.Everybody can take this to be bank as solid gold fact based on real professional expertise.I have a copy of my (expired ) ”Collegiate Professional” teacher’s license issued by the Commonwealth of Virginia around here someplace.

I misspent seven years trying to explain reality to high school kids.

Mac, I couldn’t agree more. It really gets me when people throw those acronyms around and expect every reader to know what they stand for. For instance I just read this over on PeakOil.com:

“The FAO FPI has been under 210 for the last couple of years.”

People who write crap like that deserved to be stoned. 😉

Old man: OK. 🙂

EOG= Exxon Oil and Gas. They are the company that started the Eagle Ford shale exploitation and are the leader there. They are also big in the Bakken and have good acreage.

They have a reputation for being a good operator technically. They were spun off in 1999, couple years before Enron went bankrupt. Were a bastard stepchild in that company since they were real, had assets. They were skilfull at predicting and responding to the natural gas glut (shifted their acreage from US gas to US oil).

http://www.eogresources.com/home/index.html

D/E is debt to equity ratio. Both debt and equity are used to finance companies. Debt is optimal for tax purposes and for keeping managers noses to the grindstone. But too much of it can lead to cash crunches and bankruptcies and also makes a company unable to invest in growth. Finance theory shows that for different companies, there is an optimal blend that they should have. I actually think EOG should be running more debt, but they have lowered their debt to equity ratio and have an A bond rating (too “good” in my opinion, but the opposite of the doomer meme that Rune referred to, without analysis, or that Gail likes to spout off with.) Actually the ability to finance with some debt implies a less risky business (remember these guys are “mining coal” not running wildcats or gosh knows developing a biotech drug).

http://www.readyratios.com/reference/debt/debt_to_equity_ratio.html

Nony,

A slight typo on your behalf.

EOG Resources Inc. (formerly Enron Oil and Gas)

Not as you stated Exxon Oil & Gas, you had me confused for awhile. I know you went onto talk about Enron, rather than Exxon.

http://en.wikipedia.org/wiki/EOG_Resources

Thanks for fix.

Sorry about the formatting (no edit function)

Totals from NDIC daily reports

Hi Rune,

I assume most of these producing wells completed were in the Bakken/Three Forks? Or likely 95% or more of them were. Also I would assume that most of the plugged and abandoned wells (80% or more) were non-Bakken/Three Forks wells. Would that guess be fairly close.

DC,

I have not checked out all these wells by formation, but you may be close.

I checked one of the dry wells (in Feb) which was in Bakken/Three Forks.

Here is some info on the 6 dry holes:

http://themilliondollarway.blogspot.com/2014/02/eighteen-18-new-permits-williston-basin.html

I think the 4 dry holes are in the LodgePole formation and were drilled back in 2011, but status given now. (Not an assertion, just trying to figure it out.) See also here:

http://themilliondollarway.blogspot.com/2010/11/background-regarding-whiting-lodgepole.html

I think the Lodgepole is a layer just above the Bakken (based on google image). Not sure about the other two holes (are they in the Bakken or off in the Tyler or something)?

It’s actually news when there is a dry hole. Opposite of normal drilling. Supposedly all of 2012 had no dry holes.

http://themilliondollarway.blogspot.com/2013/06/the-geologic-column-in-north-dakota.html (scroll down)

A lot can be gleaned from the Bakken Blog Click on “ND drilling permits issued

week ending February 28 »” and get all permits, wells completed along with their barrels of oil per day and barrels of water per day. They even give the dry holes finished this week.

Dry hole

Renville ~ #16216 – Ballantyne Oil, LLC, Diepolder 11-1NENE 36-160N-84W TD: 5186

Stark ~ #19272 – Oil For America Exploration, LLC, Wolf 29-1SWSE 29-139N-95W TD: 9613

Stark ~ #19785 – Oil For America Exploration, LLC, Froelich 27-2NWSW 27-138N-97W TD: 9800

Stark ~ #20061 – Oil For America Exploration, LLC, Dohrmann 13-1SESW 13-140N-94W TD:9615

Stark ~ #20195 – Oil For America Exploration, LLC, Dohrmann 14-1NENE 14-140N-94W TD: 9680

Golden Valley ~ #21734 – Chesapeake Operating, Inc., Olson 12-139-104 A 1H SWSW 12-139N-104W TD: 18,844

Good info, man.

Yeah, looks like those holes are the same ones that were written about in 2011 and just now finally got officially called dry. (the numbers match)

The 4 Oil for America ones, that is. Don’t know about the other 2.

But how hilarious, that we are doing forensics on the less than 1% of total drilling population that was dry. 😉

Oh don’t underestimate that importance. It delineates boundaries in three dimensions.

Agreed. They are exploration holes and much more learning from them than a development hole.

My point is more that the bulk of the holes being drilled right now are very, very de-risked.

Is the number of dry wells an anomaly?

When I went through the detailed data I found that around 1 % of the wells were dry or very poor performers.

No, I think those dry holes were drilled some time ago. Their permit numbers were 5 to 6 thousand below those of the producing wells that were completed this week. They just finally got around to listing them. One of the 14 producing wells completed this week did produce 5 barrels per day however.

My model estimates it will take the net addition of around 115 new producing wells in Jan -14 to sustain the Dec -13 level of 863 kb/d from Bakken(ND).

For Jan -14 NDIC daily reports shows that 94 wells were completed (all ND).

Wells subject to weather related temporarily shut ins is expected to become higher.

Hi Rune,

Enno Peters has dug some data out of the NDIC monthly reports from 2008 to 2013, it shows that 2013 wells (for the first 11 months) were running about 5 % higher cumulative output than the 2011 wells, if that trend continues into 2014 (as in it does not decrease but remains 5 % higher than 2011 avg well), then possibly 110 wells would be enough to remain level. If you are interested in Mr. Peters data, let me know by e-mail.

I read Enno Peters post which I found to be excellent.

My model suggested that first 12 months production for more recent wells may have improved some, this by looking at differences relative to the 2011 reference well. The thing we have to watch for is how the cumulative develops.

In general I found that wells that had very good first 12 months total flows (above the reference well) also had steeper declines from year 1 to year 2 thus the cumulatives for these better wells versus the reference well converged with time.

What my model does not identify is wells being temporarily shut in for some reason (primarily weather) and there is no way to tell what wells are being shut in and where in there productive life (where on their depletion curve) they are.

During winter this makes new wells look poorer (than they really are), while during summer (as these wells are brought back to flow) new wells appears as better (than they really are).

Rune,

This is just a guess on my part, but I would think that it is the relatively low producing wells that would be temporarily shut in for the winter. I think that new wells that are brought online during the winter are unlikely to be shut down due to weather. The wells that produce the most will be plowed out first.

Note that when you look at all of North Dakota the percentage of idle wells stays pretty steady at around 9 to 10% (in 2013), back in 2011 it was around 12% so the % of idle wells has been decreasing perhaps because there is a higher percentage of newer wells that may require less maintenance/workovers.

DC,

I will give you some numbers to ponder,

From Nov-13 to Dec-13 the total number of idle wells increased with 168 (all ND).

The number of idle wells in the 4 counties with the biggest production (Dunn, McKenzie, Mountrail and Williams which mostly is Bakken/TF) increased by 133 (from Nov-13 to Dec-13).

Hi Rune,

This is mostly an increase in wells waiting to be fracked due to bad weather.

From the Feb Directors cut:

“We estimate that at the end of Dec there were about 635 wells waiting on completion services, an increase of 125.”

Most of the fracking services are occurring in those 4 counties you mention, the increase of 133 idle wells is mostly explained by the 125 wells mentioned in the quote above by Helms. Note the total number of idle wells in Dec was 1183 and 635 of these were waiting on fracking services. Also note that these 1183 idle wells are capable of producing and thus have been “completed”, but they remain idle because the production will be very low if they are not fracked. This is why the “wells completed” numbers that Helms mentions are not that important in determining production, many wells that are completed are not ready to produce, until they are fracked.

See https://www.dmr.nd.gov/oilgas/directorscut/directorscut-2011-10-12.pdf

Where Helms says:

“The idle well count dropped significantly again to 733 wells, but normal is 450, indicating a continuing backlog of almost 300 wells waiting on fracturing services.”

Also https://www.dmr.nd.gov/oilgas/mpr/2011_08.pdf

See page 2 of report above (state summary) to find the idle wells in Aug 2011 are indeed 733 wells. (The wells waiting on fracking is actually 733-450=283 wells.)

“My model suggested that first 12 months production for more recent wells may have improved some, this by looking at differences relative to the 2011 reference well. The thing we have to watch for is how the cumulative develops.”

FWIW: This could be attributed that the drillers have located a sweet spot that has better recovery than the areas they were drilling in 2011. If this is true than the peak date may be pushed out especially if even better areas are found.

What is the new sweet spot?

A moment of art, from death, aka trucks.

http://www.youtube.com/watch?v=M7FIvfx5J10

70 million views

Watcher: love that commercial, the music and all.

Just watched this one…scary too.

https://www.youtube.com/watch?v=1zXwOoeGzys

Peakoilbarrel seems more analytical than Peakoil. Also, I don’t see people commenting at both places. Are they rivals?

No of course not. I assume you are talking about PeakOil.com. I often comment on PeakOil.com. We are totally two different kinds of sites. PeakOil.com is a reposting site. That is they post stuff that has already been posted elsewhere. In fact this very blog was posted there today.

There may be more optimists that can be found at Peakoil.com.

A little Ukraine factoid. Way too much talk of the Russians losing leverage because it’s not winter and they can’t freeze them with a nat gas cutoff.

Saw this on ZH and fact checked it. Turns out 44% of Ukraine electric comes from nat gas, and they consume more than they produce. The remainder arrives from the Russian grid.

These people are screwed and probably don’t even realize it. Russia can do as they please, especially since Russia’s 6 million bpd export to Europe would be the source of NATO fuel.

Russia has a lot of power there, including from the Black Sea Fleet also. I have a feeling that West Ukraine will get cut off and this will be a shame. Much bigger country than Georgia and hard to say that they invaded Russia first.

Imagine if Russia started destabilizing Canada by causing civil unrest. What would the US do? You can bet your bottom dollar the US would be rolling in troops and tanks into Canada. The Ukraine is in Russia’s sphere of influence. To expect them to sit by and watch the US create the next Libya on their door step is beyond insane.

The EU wants the Ukraine to steal the Ukraine’s wealth, as happened to all of the other eastern European states that joined the EU. The US via NGOs (Non Gov’t Organizations) was financing the protests in the Ukraine to allow the EU to pillage it. The US involvement is likely because they want payback over Syria and to set up NATO bases in the Ukraine.

Tech Guy,

I couldn’t agree more with you. Dr. Paul Craig Roberts who was the former Assistant to Secretary of Treasury during the Regan Administration, was interviewed on King World News about the Russia/Ukraine situation.

It is very interesting as he discusses how the U.S. tried to destabilize Ukraine by funding riots and etc by financing the moderates. However, after the Coup, the hardcore nationalists from Western Ukraine stepped in with guns and forced the moderates to step aside.

Now it is a complete disaster because Washington and the EU did not get the desired outcome. Instead they have a historic pro-Nazi regime that actually supported Hitler during WW2 against Stalin who are trying to remove the Russian language as the official language in Ukraine. They also want any Russians stripped of their citizenship.

What a real mess. I highly recommend the interview below:

http://kingworldnews.com/kingworldnews/Broadcast/Entries/2014/3/1_Dr._Paul_Craig_Roberts.html

steve

I am not up on my internal history of the Soviets as well as I should be to stick my two cents in here but anti Stalin is not exactly the same thing as pro Nazi.

You take your allies where you are able to find them when you are dealing with a Stalin that has just recently starved millions of your fellow country men as Stalin did during the thirties and collectivization of the Ukraine.

AS Winston Churchill remarked at one point, if the devil were to come out against Hitler, then he would at least mention the devil favorably in Parliament .

I have never myself been able to decide whether Hitler, Stalin, or Mao was the worst man of recent times . Hitler started WWII of course but Stalin put him to shame in terms of terrorizing and murdering his own people even allowing for the Holocaust.

Ditto Mao with his Great Leap foolishness.

Of course there have been others just as depraved such as Idi Amin (spelling ?) but he was not able to fulfill his potential due to having control of a small country to small to give him free rein to exercise his talents.

The difference being that Ukraine strayed from Russia´s field of influence. Eastern Europe came in to play for others to try and exert their influence after Russia stumbled. Russia is once again establishing themselves and a clash is occuring where two (or more) significant players are trying to influence the same region.

It´s a dangerous game that all sides are playing but both sides have ideologies that dictate they play the game no matter the stakes.

Numbers, numbers, numbers. So many numbers. And how good are they? To paraphrase Colin Campbell, “It’s not an issue of whether my numbers are wrong. We know they are wrong. The question is how wrong.”

I love that Ron, Rune, Jean and others do their best with what they have to give us the best possible picture they can of what is to come. And if they are off by even five or even ten years (though I would bet real money they are not) that doesn’t change the importance of their message. We are headed for times unlike anything we or any previous civilization has seen, and very few people are taking it seriously. On the other hand, what difference would it make if they did?

Watching the numbers, looking at the graphs, reading the commentary — it all passes the time. And I will be more than a little interested to see whose predictions come closest to the mark. But that somewhat academic interest will be superseded by miles by my concern for my son and his future. He won’t care whose prediction was most accurate. He will have much weightier matters on his mind. And I will not blame him or others of his generation if they look back and curse my generation and my father’s generation for being so reckless and irresponsible.

Another way to characterize the situation is that we know we are depleting the remaining volume of economically recoverable hydrocarbons, the question is, what’s the depletion rate?

As I pointed out in the prior thread, by definition the remaining volume of post-2005 Top 33* CNE (Cumulative Net Exports) declined from 2005 to 2012. Again, the question is, what’s the depletion rate?

My estimate, based on the 2005 to 2012 rate of decline in the Top 33 ECI ratio (ratio of production to consumption) is that we may have already burned through about one-fifth of post-2005 Top 33 CNE in only seven years.

*Top 33 net oil exporters in 2005

Calhoun,

You’ve just provided us a concise, very well written description of reality. These are my own feelings, exactly. Good job man.

Doug

When your predictions are off, you should try to figure out why. Also, you should really watch out for your biases affecting your guesses/analyses. e.g. a peaker running a model that turns out a low/early peak.

It’s not just Rune. Look at Picollo/Gail in 2008 predicting 150-225,000 bpd peak and everyone in the comments section at TOD cheering that analysis on. Looks pretty flipping flawed now doesn’t it!

http://archive.is/Pc1uj

Rune’s post got a lot of real media attention. He owes it write up a crow version. I’m sure he would be shouting from the rooftops if he had been right. He was defensive about Filloon or others criticisms. But he still has not done the right thing when it turned out he was wrong. Being wrong does not annoy me as much as not being a truth seeker.

Nony,

You made your point fer pete sakes. Give it a rest dear sir.

The Titanic is sinking and people are bickering that it took a few more minutes longer for it to sink?

steve

OK. Will do.

Yeah, I second that motion. One can run anything in the ground.

Predictions? We are at peak oil right now. Or put it another way, we are well past peak oil for every importing nation. We importing nations are using less oil because there is less oil to use. Imports of all OECD nations combined has dropped by almost 7 million barrels per day since 2006.

End of story, peak oil has arrived. But apparently a few people just haven’t gotten the message.

12 Month Trailing Average of Combined OECD Imports

OECD Imports are dropping by one million barrels per day per year.

Predictions are right, predictions are wrong. It seems, though, the NET energy from oil extraction peaked a while ago. Yet there’s no data to prove that.

Ken Barrows Wrote:

“Predictions are right, predictions are wrong. It seems, though, the NET energy from oil extraction peaked a while ago. Yet there’s no data to prove that.”

Well there is data to support this. The price went way up. Pre-2005 the price of Oil was reasonable. Since 2005 the prices has been $80 or higher (except for a very brief dip of 2008\2009).

I think the Kopits presentation that compares capital expenditures to output also shows that net energy is long since in the rear view mirror.

Hey, if this is happening at or near the peak in world oil production, just imagine what it will be like when we start on the down slope.

Global riot epidemic due to demise of cheap fossil fuels

“If anyone had hoped that the Arab Spring and Occupy protests a few years back were one-off episodes that would soon give way to more stability, they have another thing coming. The hope was that ongoing economic recovery would return to pre-crash levels of growth, alleviating the grievances fueling the fires of civil unrest, stoked by years of recession.

But this hasn’t happened. And it won’t.”

It won’t happen because we are at peak oil, or so close that any increase in production will be marginal. We are at the end of growth. And the end of growth is the beginning of collapse.

Economists forecast the end of growth

“Future growth in real GDP per capita will be slower than in any extended period since the late 19th century.”…

“Our global economy, reckless in its use of all resources and natural systems, shows many of the indicators of potential failure that brought down so many civilisations before ours.”

A few days ago I said something to the effect of “absolutely nothing will happen at peak oil”. I take it all back. It looks like something is happening at peak oil after all.

Hi Ron,

The Guardian is number three on my list of bookmarked news sites and the only reason it isn’t number one is that I haven’t bothered to rearrange the icons.

I agree that ”something is happening” at peak oil and have long believed that we are in the early stages of collapse but that most people will not realize this because collapse will for the most part proceed piecemeal in the poorer parts of the world it it’s early stages at least. But it’s effects are perfectly clear to be seen even in this country if you happen to live in a depressed area where people have to drive a lot just to get to work. I live in such an area.

If the current total production plateau holds for few more years or if it doesn’t it is still (from a disinterested point of view ) obvious that the consequences of peak oil are already making themselves felt in very painful ways in countries that are energy poor.

Now as I see it in retrospect I think we have been focusing actual peak production too much and not enough on production per capita when it comes to getting the message across to the public.

Production per capita is the more important metric at least in the near term economic picture and peak oil per capita is in clearly in the rear view mirror.

Any honest fool with some background in agriculture acknowledges that oil prices and to a lesser extent natural gas prices determine food prices to a substantial extent and that the diversion of food crops or land and other capital diverted to biofuel production ( moonshine mostly here in the US) contributes heavily to rising food prices too.

Now this link you have put up is straight down the line the straight dope as I read it with maybe a couple of minor quibbles not worth mentioning.

But it is a blog published as a separate thing from the main part of the paper and not on the front page or in the business section of the paper or even in the main section of the environment.

Blogs are sort of letter to the editor thing.

The editors can run them without being accused of giving them the full-fledged stamp of approval of the paper itself.

Furthermore the Gaurdian is a non profit and as such not so much subject to pressure from advertisers as most papers.

THANK GOD (OR SKY DADDY for evolutionary pc types,lol) for the Gaurdian.

It is imo the best newspaper in the world right now and there is no doubt at all that it is the best one you may still read free on the net.

But even the Gaurdian does not yet dare to mention peak oil on the front page unless I have missed seeing it.

No other important paper that I know of is quite so close to acknowledging peak oil and I believe the Gaurdian will be the first major publication to put peak oil on the front page where it belongs.

Mac, the problem is we’re living a fantasy and what should matter is the world we leave for our children and the other wretched creatures trying to make a living here.

However, although I really hate to say it, Patrick (and Buddha) is right: the best thing we can do is accept Fate, tone down the stuff we do, and get on with life. Just because it pisses me off no one believes in global warming, Peak Oil or peak anything, that’s the way it is. And, ’twas ever thus.

I think the best way to improve response to both Climate Change and the fact of Peak Oil is to not discuss them at all with those who are resistant but to constantly discuss their effects. Transport poverty, rising energy cost, insurance cost rise, need for resilience in both energy supply and from unpredictable weather events. It’s crazy I know but I find that the conversation and resultant action on these issues is much easier to get going if we just pull back from raising their base causes. I am confident that soon enough we will be able to discuss base cause too, but right now it’s more productive to interest people in the direct economic and lifestyle benefits of improved transit, living and working with reduced car use, generating their own electricity and so on…

Things that you may not think will make any difference but when billions of people all make one small change it adds up to a big one. This is after all how we got into this oil addiction. And we have no choice. We may be condemned to a shark fin, or we may be able to flatten that out to a long tail, or somewhere in between, and the only way to find out is try.

To this end I am very keen on as gradual but continual price signal from crude as possible. This $100 plateau has been longer than I expected and is sure to break out north as soon as the Shale story gets more complicated (ie stops growing). A return to 2008 volatility is likely too but a lot more difficult to function in. All talk in the MSM then is about ‘shocks’, a way of avoiding discussing real supply/demand issues.

Patrick,

“Things that you may not think will make any difference but when billions of people all make one small change it adds up to a big one.” It’s exactly what my two daughters have been telling me for a very long time. Perhaps I’m hard wired for doom because it doesn’t seem like anyway near enough. That said, no peace of mind, or solutions, will come from a gloomy outlook either. So I concede, your view wins! I guess.

Doug

Gracious, Doug.

Canadian Urbanist Gordon Price likes to discuss change as being on a continuum between Utopian and Apocalyptic with Incremental in the middle. I guess the first is incredibly rare except in intention, the second all too common, but the last, Incremental, continual.

We can certainly find any number of ways that Catastrophic change is immanent but hasn’t the human experiment always really been in that state and only survived by seeking its reverse through the agency of Incremental acts.

However history is littered with the apocalyptic hastened by people promising the utopian. For me, now, the people offering the endless life at 20thC resource plunder are misguided Utopians. But then to many used to that world this is the very charge that is leveled at the Green movement. I detect it for example over on Euan Mearns’ site, where the UK energy predicament is being blamed on those urging transition from traditional sources and structures….

Also change is never synchronous. Different places will be forced to different states at different times. Very very interesting to watch!

Patrick Wrote:

“This $100 plateau has been longer than I expected and is sure to break out north as soon as the Shale story gets more complicated (ie stops growing).”

The price of oil probably not going to go too much higher. prices may go up $10 to $20 (except for Spikes from Geopolitical events) as the worlds economy can’t afford much higher prices. If they could then Oil majors would need to slash CapEx spending and the peak in shale could be delays as more money was able to fund expansion.

The 2008 spike happened because the world was in a housing bubble and banks were offering everyone easy loans. Instead of Oil prices resuming a trend higher, the global economy will shrink to the supply constraints. The next economic dip will get dicey for the west as unemployment is already too high. We are likely to see revolutions, civil war, as well as real war. The signs of this coming are very visible. We already have revolutions and civil war in the middle east. China/Japan cold war heading to a hot war, Trouble in the Ukraine, frequent riots in western nations with high unemployment.

Riots in the US may not be far off, now that California is out of water, and its farms will be cut off, we will almost certainly see some food inflation by the end of the year. Once food stamps can’t keep up, people will turn to violence.

“This is after all how we got into this oil addiction.”

Oil is the food for the modern economy. It not really an addiction because without it the economy will starve to death.

Oil prices cannot go much higher for a long period in inflation adjusted terms.

However, imagine this:

Russia invades Ukraine. tick

Western nations retaliate by selling Roubles and Russian stocks. tick

Russia retaliates by shutting gas and oil pipelines pipelines to Europe. No tick yet

Price spikes very rapidly (up $2 today so far )

Global recession within a couple of months.

All the important parties (i.e. not Ukraine) will pull back from the brink. Europe and the U.S don´t want to face the shock and Russia isn´t as resilient as it makes out. Ukraine will fracture and the various regions will have greater independence – all is well (barring Ukraine) until the next time.

These clashes are getting more frequent. Russia and the U.S came much closer to conflict than they have in a long time over Syria 6 months ago. Now we have Ukraine as a divisive issue – no suggestion of military action (not from the E.U and U.S anyway) but it´s a point of tension that won´t help in the long run.

As oil supplies tighten and prices inevitably rise (despite any offsetting economic decline), the cognitive dissonance experienced by the American population will be excruciating. After decades of real abundance and one decade of ersatz abundance (as touted by IEA, oil companies, govt, media), the reality that it is over will be too much to bear. Beyond the actual suffering that results from scarcity there will be the psychological damage from the realization that it is over. I can only expect the worst — but then, I’ve always been an optimist!

Calhoun,

I might add, the abundance we, and our parents generation, have taken for granted, in a very real sense, goes beyond anything witnessed in history, except perhaps by kings, queens, sultans, tsars, and the like. This is such an obviously unsustainable event that no one with any imagination could believe it will just could go on and on. Yet I meet people every day who honestly believe that it’s perfectly normal to own multiple luxury cars and yachts and be taking endless trips around the world. This phenomenon seems summed best by the phrase “sense of entitlement”. All this, naturally, financed by the riches of endless extremely cheap energy – and there’s the rub.

Good morning all.

Regarding the price of oil either by the barrel or by the gallon….

After we go over the cliff, I doubt most people will care if the price is rising or falling. Many people will have lost jobs, and for those still working, their wages will not keep pace with inflation.

If I cannot afford a car, but rather must ride a bike, or, a motor cycle or scooter, if I’m lucky, then the price of fuel at any price doesn’t matter much to me.

Even if fuel prices fall, they will still be higher, relative to all other prices.

On that note, I have four bikes in my household, as well as two bicycle cargo trailers. Next I’m looking to buy a scooter or motorbike.

Several bikes and several trailers in our household. Sold the scooters a while back, and the car a few years before that. And we rent out two rooms in our house to students. I think of this as the “new normal”, which seems like the “old normal”, which existed before my time. At least according to what I have read, and what older people have told me.

Pretty much only thing I use car for is to drive to get groceries, go to doctor/dentist, and occasional trips to a relative. Live in the city and lots of stuff is walkable. Even going to the gym, I bike rather than drive (transport becomes workout!) However, when working, I’m on the road with lots of flying and a rental car. Still, I stay at a hotel very close to the client site, so total drive is low. I don’t do it for $$ or environmental reasons, but for lower commute time.

I realize that everyone is different and if you have a wife pushing for a yard for the kids or exurb schools, etc….they are all choices. But my point is rather than just being planet-altruistic, try to find positive lifestyle reasons for “doing the right thing”. For example, low commute distance because it’s less time lost staring at the windshield and listening to Rush Limbaugh and sports talk. Biking or walking for errands because it’s tacit workout as well as just getting some outdoor time. If you’re a local foodie, than the joy of having absolutely fresh tomatoes rather than those rocks from Safeway. Etc. Etc.

The scooter or bike types with cargo carts behind them think they are preparing, but never seem to quite ask themselves how the groceries got onto the shelves to which they intend to bike when all others can’t drive.

I think that is sort of a bus versus car issue though. Think how much less gas it takes to go 10 miles as part of a busload as opposed to 10 miles as a single driver. Similarly, the semi truck with 30,000 pounds of groceries has way better economics per pound than me taking 50 pounds home in my 20 year old 2 seater sports car. 😉

Well of course, all generalizations are wrong …

It’s not so much “Preparing”, as just adapting and adjusting to various tends in modern day life, or, more accurately, what I THINK are the main trends in modern day life. I live in a place with a high walkability score, where riding a bicycle is very common. I couldn’t afford a car, even if I wanted one. Our main grocery store is very close, and is a local store that sells a lot of locally grown or produced food items.

I have no certainty of what the future holds, although I have many ideas (many of which are at odds with one another). Living locally, as much as possible, makes sense to me. It may turn out to be quite foolish, or just plain silly.

Unless things really go to hell in a hand basket the food will still get to the stores because fuel will be rationed to farmers and truckers hauling food with a priority right up there with the cops and rescue squad.

But the variety will fall of sharply and drumsticks will be the new ribeye and ribeye will be the new caviar.

I am not going so far as to say that industrial farming and delivery will collapse because I can’t see any SURE reasons why this should happen,at least not during the next couple decades.

But if the cards fall wrong —it could happen.

I am counting on Big Brother to prevent it though.By the time we are looking at collapse belly to belly and nose to nose Uncle Sam will literally know where each and every one of us sxxt last ( defecated in polite language) and the ration system will be ready on hard drives and backups at least.

I just hope the administration in charge when the time comes is competent in terms of actually administering a large undertaking.

This one will be the biggest ever and it is going to be one tough nut to manage. It will make Ocare look like a Sunday School picnic.

If there are any old commie administrators with top level experience still around from Soviet days they will be in big demand as consultants.;-)

“drumsticks will be the new ribeye and ribeye will be the new caviar.”

Which is why I’m eating a lot of steak now. Seriously.

Farmer Mac wrote:

“Unless things really go to hell in a hand basket the food will still get to the stores because fuel will be rationed to farmers and truckers hauling food with a priority right up there with the cops and rescue squad.”

Food stamps or EBTs are not keeping up. I think a lot of people will not have enough to eat anyway. Fewer workers means less tax revenue, and less money for wealthfare.

Another issue is that the majority of farmers in the US are at or near retirement age. As a farmer I think you realize the disaster would be if a bunch of city slickers attempted to work on farms.

Farmer Mac wrote:

“I just hope the administration in charge when the time comes is competent in terms of actually administering a large undertaking.”

I would consider that statement borderline “cornucopian” 🙂 Unfortunately things always get much worse before they get better.

For most of the reasons you listed is the reason why I am heading to a rural area and to become food self-reliant. I don’t want to end up getting fed soylent green if I remain where I am.

Based on thirty years of experience growing much of my food, and several years as a small commercial farmers–

There is no such thing as “food self-reliance.”

Just a short list of what one relies on to grow “one’s own” food:

tractor makers and repairers

fuel companies

seed companies

makers of chainsaws, implements, plastics, alloys

electrical infrastructures for such items as irrigation systems

tool makers

I’ve stopped fooling myself. I’ve stopped “preparing” for peak oil. Not only do we not know what to “prepare” for, there is no removing oneself from the system upon which one relies.

MikeB Wrote:

“I’ve stopped fooling myself. I’ve stopped “preparing” for peak oil. Not only do we not know what to “prepare” for, there is no removing oneself from the system upon which one relies.”