Guest Post by George Kaplan

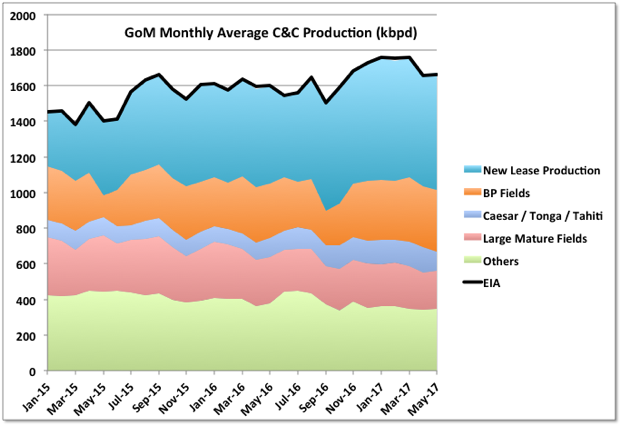

GoM Production

Production for May by BOEM was 1673 kbpd and by EIA 1661, compared with 1661 and 1658 kbpd, respectively in April.

March looks like the peak, at least near term, for the basin, especially with Hurricane Cindy impacting the coming June figures.

The combined new fields added from late 2014 look to be peaking as well. Great White came back on line but xxx and yyy declined. In previous data I had omitted one big producing lease in Mars, which included the new Deimos field. With this added the production growth through 2017 is higher (and as shown later the decline in mature fields faster) than previously shown. There may be more increase to come: the Mars leases had three rigs operating through June, one dedicated for Deimos, which has now gone. The two platforms on the field each have a dedicated platform rig, so they can continue with in-fill drilling and workovers as they wish. The Kaikias development will be tied into the Olympus TLP on the Mars field in 2019, but it’s a subsea tie-back so would need a separate drilling rig. The facility has nominal capacity of 100 kbpd, but that might be limited by the platform wells and manifolds rather than production trains – if not then Shell must be expecting some decline before Kaikias comes on line.

Stones start-up is still not looking good with an 8 kbpd fall – Shell are taking over the operation from SBM by buying the FPSO instead of leasing. Maybe this indicates poor operating performance (if so it’s something for ExxonMobil to be concerned with as they are following the same approach with SBM for Liza), or maybe just a convenient scapegoat. Julia, Cardamom, Stones, Jack and Lucius still have active drilling programs so may have opportunity for growth. Julia had plans for subsea multiphase pumping, I don’t know if that is operating or will be brought on as pressures fall.

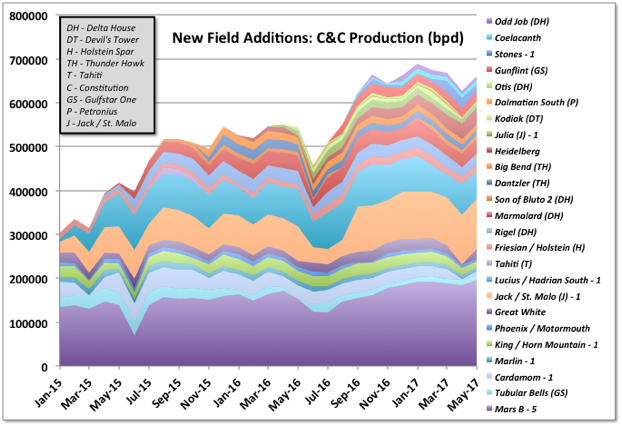

Production from the South Santa Cruz and Barataria fields started in mid June (actually part of Fourier and East Anstey fields by BOEM naming). The first Horn Mountain Deep well, for Anadarko, started production in April, a second well is due to be spudded this quarter. These are the only new fields announced for this year. Anadarko was the only company that had hinted they may develop something else (e.g. with Warrior and Phobos tie backs), but with them slashing budgets for 2017 after poor second quarter results that is now be unlikely: in their investor presentation they indicated they expected flat production out 3 to 5 years, and didn’t sound particularly confident of that to me, and with no mention of Shenandoah so that might be on the way to full cancellation. One new lease in the Marmalard field (the last there) for LLOG was started in late May.

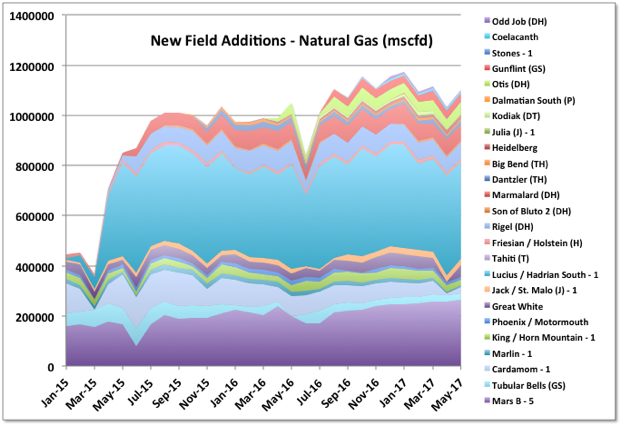

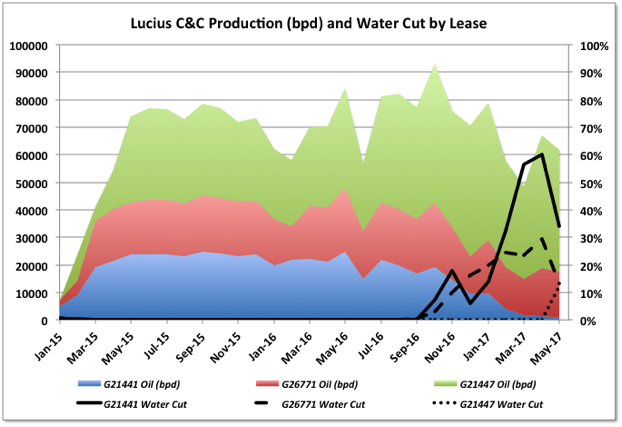

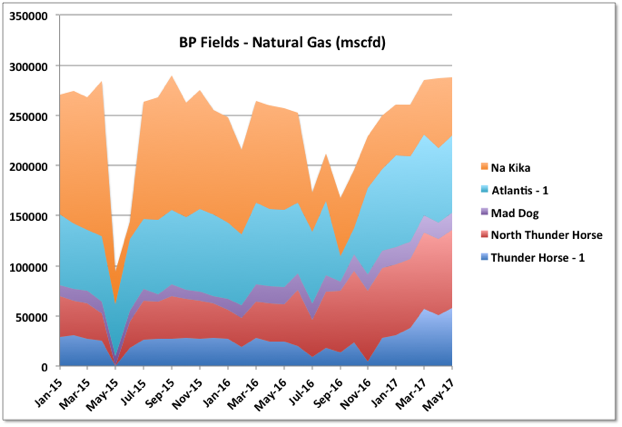

I’ve added natural gas production for the new fields here. Hadrian South and Otis are the only dedicated gas fields. Hadrian South production is a big proportion of the gas total from GoM now. It produces to the Lucius Spar, operated by Anadarko, and according to their investor presentation Hadrian South is supposed to finish by about 2021. I’m not sure if that can be correct, but if so it’s production should be declining significantly soon. Also on Lucius, it’s biggest producing lease, really part of Hadrian North field, started showing a sudden water cut increase in May, and dropped about 8% production (for some reason this does not show up in BOEMs list of qualified fields, but it is definitely tied in to Lucius). The first lease on the Lucius field has been killed in about two years with water break through; it’s not clear what their plans are for it (this is Anadarko as well).

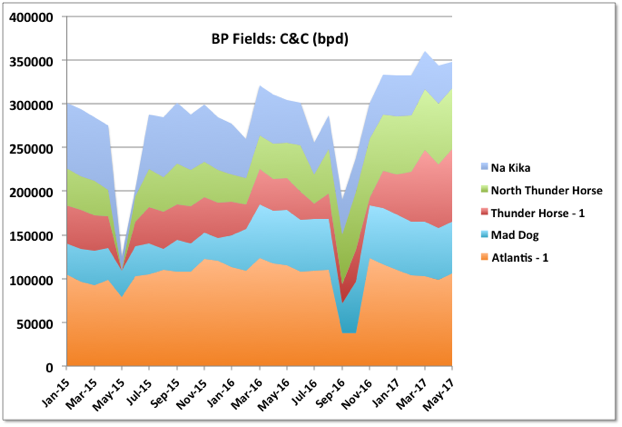

A couple of leases in Na Kika look like they have gone off line so production is down. Thunder Horse numbers were revised and now clearly show the impact from South Thunder Horse with about 35 kbpd increase. There have one rig still operating, but I think they will just maintain plateau now. Atlantis looks to be running about at nameplate capacity, so the coming North Atlantis development is likely only to be able to extend the plateau; there is one rig operating there now.

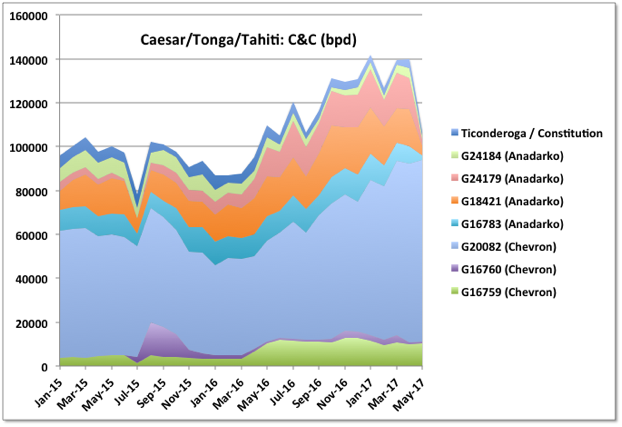

For the Caesar/Tonga/Tahiti fields the Anadarko facility (Constitution Spar) went off line taking off 40 kbpd production (Ticonderoga and Constitution fields go there too). The turn around was for 42 days so will reduce June figures too. The Constellation field is to be tied into the spar next year, the spar has nominal nameplate of 70 kbpd so another 25 or so (average) might be added to overall output.

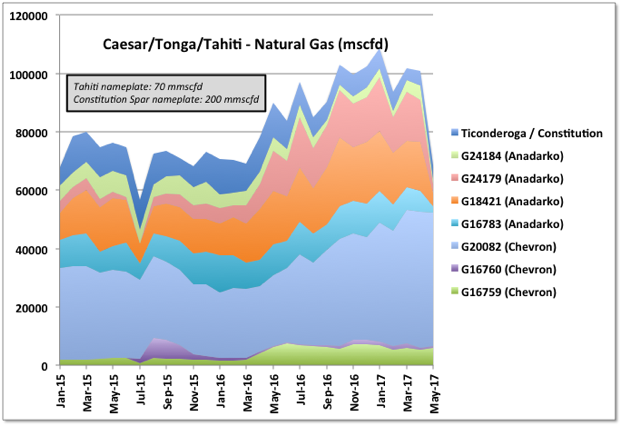

For the Chevron fields in these leases it looks like production is limited by the gas handling capacity on Tahiti platform, at 70 mmscfd, which is pretty low given it’s oil capacity of 125 kbpd.

After a bit of a plateau from some brownfield work and new tie backs the decline in the larger mature fields looks like starting up again; the drop in gas is particularly noticeable, but is mostly due to Baldpate turn around. Overall water cut looks like it might be rising as well. Thunder Hawk has two new rigs operating, but I haven’t seen any announcement for new developments there. The smaller mature fields (not included in the charts) seem to be holding up quite well, I will try to get some individual lease data for these next month.

For the GoM activity report from the last week in July, there were 28 rigs drilling, twelve running tools and two in plug and abandon operation. I think the report can mean there is dual activity on a single well (e.g. wire line and drilling). Two rigs are predrilling on Stampede, one on Appomattox and one on Mad Dog II. For the newer fields there is development drilling on Lucius, Cardamom, Mars (two rigs), Stones, Julia, Jack / St. Malo, plus new wells for recently added or due production on Horn Mountain Deep and South Santa Cruz/Barataria. Atlantis also has a new rig, which may be for development of the Atlantis North discovery – it’s noticeable how any reasonable discovery is immediately fast tracked, the North Sea is similar. The Dorado field (operator Anadarko, discovery in 2014) is also being drilled; I think it is one of the last of wells for small fields (King, Dorado, Holstien Deep) being tied back to Marlin, there’s probably one more for King and a couple of others possible. Only Phobos has appraisal drilling.

Five rigs are drilling on unnamed fields, so presumably exploration – four of these are in Green Canyon, which means they are near field, and probably smaller, prospects; the other one is for Shell, in Walker Ridge, and probably a frontier wildcat. With all the predrilling on new fields, most new fields reaching plateau or decline periods, and few exploration wells (and fewer still in frontier regions) it seems likely that the drilling numbers will tend to decline over the next few years as unused well slots and tie back locations on the facilities are exhausted, even with an increase in oil price.

In the past few months as production rose the EIA STEO showed a new production forecast which had the same shape but was just raised to start on the new production number. They didn’t do the reverse as the production fell but instead kept the June STEO forecast with a single dip down for April. The August STEO, showing May data, is due next week.

GoM Lease Sales

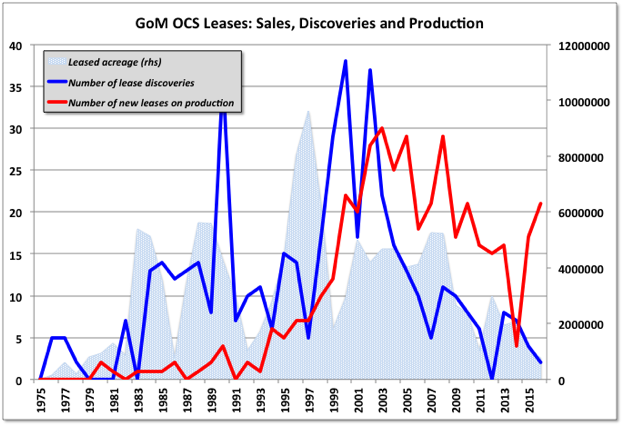

As further support that the current decline in exploration is not just a function of price, the chart below shows the acreage of GoM leases that have been successfully auctioned, plus the percentage of offerings that were taken up (charts are stacked according to BOEM designated production areas to the give total). The numbers before about 1976 are listed against states (FL, LA, TX) and I think are inshore shallow leases, although it might be they just changed naming convention. After about 1990 areas were split from just GOM to east, central and west. The percentage bought calculation only considers the area auctioned after 1990. It is marked how the amount bought and the percentage bought both peaked and rapidly dropped off, even in the high price years through to 2014. However there were obvious impacts from earlier price collapses in the late nineties and 2008.

It’s possible to read too much into these charts but generally it looks like, on average, discoveries follow three or four years behind the lease sales and production about the same length after that. But the recent production rise isn’t in that pattern – maybe disrupted by the 2008 recession and 2010 drilling hiatus, or maybe the high oil prices after 2011 allowed some difficult and expensive long term discoveries to become commercial.

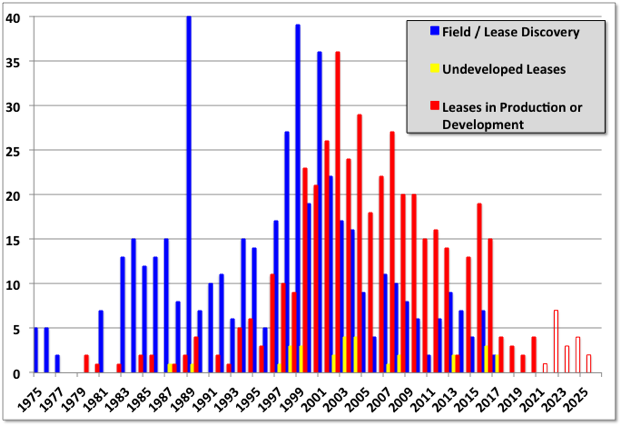

The number of open, undeveloped leases is relatively few, and declining. The chart below shows the number of leases discovered (and not terminated without development), producing or in development, and those still undeveloped. The open bars show my guesses for some larger fields that seem likely to be approved soon (e.g. Vito, Anchor). Most of the undeveloped leases (in yellow) are associated with existing, fairly recent, fields on production (e.g. St. Malo, Tubular Bells( and are likely to be poorer wells, waiting on surface facility capacity to become available before being tied in. There are two new field discoveries this year: Mormont and Khaleesi, by LLOG in Green Canyon (they have switched from Animal House to Game of Thrones naming convention) and are likely to be smaller reserves similar to their Delta House developments.

There is one area that might be expanding: deep shelf pre-salt. These are deep or ultra-deep wells but in shallow water (this is a rare combination and hence one problem is that there aren’t many rigs – jack-ups – that are suitable). W&T brought on Mahogany field this year, in an already producing lease (one well at 5000 boed with up to three others due, although the production data suggests it wasn’t as great as expected) and there may be more to come. The production is high pressure and high temperature, and in places can be too high for the available technology or commercial development, and mostly gas prone.

Again, thank you for the GOM update!

In the continued debate on US lower 48 shale, interesting developments with PXD. Stock at one point was off over $25 per share, but has recovered some. Will be interesting to see what happens to it in the next few weeks. Apparently GOR guidance was off, wells are producing too much gas?

Also, EOG earned 8 cents a share. Based on those earnings, EOG stock trading at a PE multiple of around 280. It’s stock is not down that much today.

Glenn – Regarding your comment to SS in the previous thread: “Have things changed that much with GAAP accounting rules? Back when I was still active in the oil business, impairments applied to depreciation and book value, not depletion.”

I have not analyzed SS assertion that PXD is understating depletion, thereby leaving a greater asset on its books after 5 years of production than it is worth.

With regard to your comment – no, GAAP has not changed. I think there is a communication gap. PXD, like all oil companies, capitalizes the entire cost of drilling a well for “book” purposes. The entire cost includes probably 95% “intangible” costs, such as paying for the rig and just digging a hole in the ground. About 5% of the cost is “tangible” equipment, including the steel casing, cement, pump jack (if needed) etc. [For tax purposes, only the tangible cost is capitalized, along with the leasehold cost.] For book purposes this entire drilling amount is capitalized [along with the original leasehold cost] and adds to PXD’s book value. This book value is reduced pro-rata when production starts, and the pro-rata reduction is called depletion.

SS point is, for example, let’s “assume that WE know” that the well is only going to produce 500,000 boe total. But, assume that PXD beleives that the well will produce 1,000,000 boe. After the $10 million of cost [assumption] is capitalized and 400,000 boe are produced, PXD will have deducted $400,000 of depletion, leaving $600,000 of book value. But, we know that the well is only going to produce 500,000 boe, so the book value should be only $200,000 [$10,000,000 minus 80%]. So, SS asserted that if this happens and PXD tries to sell the well [or even if it keeps it], at some point they will have to record an impairment and reduce the book value accordingly. So, SS is asserting that the impairment IS applying to book value.

as i understand tax issues relating to oil and gas production the “depletion allowance” is calculated at a rate of 15% of gross proceeds on an annual basis and has nothing to do with some EUR calculation. Depreciation on the other hand…

TT. You are referring to percentage depletion for income taxation purposes, which only applies to the first 1,000 BOEPD produced by any company. For income tax purposes, there is income depletion and cost depletion, and the producer is permitted to take the greater of the two, but as to percentage depletion, only as to the first 1,000 BOEPD.

I am referring to depletion for GAAP purposes, utilizing the units of production method. From what I understand, depreciation applies to the tangible equipment, such as casing, tubing, rods, pumpjack, downhole pump, gathering facilities, etc. Depletion refers to the intangible costs of the well, such as land, seismic, drilling the hole, completing the hole, etc.

Take a look at the website accountingtools.com, under depletion method. There is an overview which I think is fairly easy to understand.

I would very much like those with more knowledge than me to comment further on this issue, but I do realize this is a specialized accounting area.

My suspicion, which I have discussed with others, is that inflated EUR helps earnings in the near term, by causing less of an “expense” to be charged against earnings during the early years of the well. This, of course, will lead to reserve restatements/impairments, or impairments upon liquidation of the wells. However, as that is a problem 5+ years down the road, it is better to just kick that can a few years out rather than to keep recognizing losses now.

However, I think maybe recording small earnings is worse than losses. Losses can be excused for growth, new tech, Amazon and Tesla comparisons, etc. Small EPS results in 100+ P/E multiples, and suddenly some start to think, “are these companies overvalued trading at a forward P/E of 175?”

•••••shallow sand said:

I don’t think so. Tanglible drilling costs are capitalized in both tax basis and book value. I think clueless is correct in this.

There is book depletion used for SEC forms, and there is tax depletion used for federal income tax returns. They are two separate things. Here’s a brief explanation from an accounting firm:

•••••shallow sand said:

And so I will ask again what I asked on the other thread:

http://peakoilbarrel.com/brazil-reserves-and-production/#comment-610603

According to its SEC filings, Pioneer expects to invest $2.4 billion on its oil and gas properties in FY2017. If it takes $1.364 billion ($341 million x 4) in DD&A expense during the year, it will have taken a total of 56.8% of its total oil and gas capitalized cost in FY2017 in DD&A.

Do you believe taking 56.8% of total new oil and gas capitalized cost in DD&A expense during the first year to be “vastly understated”?

clueless said:

But the book value of an asset is the acquisition cost minus depreciation, not minus depletion.

If an asset is sold for less than its book value (acqusition cost minus accumulated depreciation), then sure, shallow sand’s assertion that “If PXD ever sells the well, huge impairment” is true.

But what does impairment or book value have to do with depletion? Absolutely nothing. Can you show me where depletion enters into the formula that is used to calculate book value?

You and shallow sand are using depletion and depreciation as if they were interchangeable, and I’m pretty sure they’re not, or at least they weren’t back when I was still active in the oil business. They weren’t the same for income tax purposes, and they weren’t the same according to GAAP accounting rules either.

Take this passage from Pioneer’s FY2016 annual report, for example:

Depletion and depreciation are not the same thing.

And so I will ask shallow sand again what I asked on the other thread:

http://peakoilbarrel.com/brazil-reserves-and-production/#comment-610603

According to its SEC filings, Pioneer expects to invest $2.4 billion on its oil and gas properties in FY2017. If it takes $1.364 billion ($341 million x 4) in DD&A during the year, it will have taken a total of 56.8% of its total oil and gas capitalized cost in FY2017 in DD&A.

Do you believe taking 56.8% of total new oil and gas capitalized cost in DD&A during the first year to be “vastly understaated”?

BBB-

Do you think they just imagine that credit rating?

Glenn.

I am looking at PXD earnings release for Q2, 2017. The expense for depletion, depreciation and amortization taken for Q2, 2017 is $341 million. So, annualized, this is the $1.364 billion that you are referring to. The DD&A for Q1, 2017 was $337 million. So it looks like the annualized number you use will be very close.

PXD plans on spending $2.4 billion on drilling and completion capital in 2017, plus $275 million in other capital for 2017, for a total of $2.675 billion in CAPEX in 2017. That is roughly double the amount of DD&A expense that will be taken in 2017.

On page 70 of the 2016 10K, and page 71 of the 2013 10K the actual DD&A numbers appear in the consolidated statement of operations for 2016, 2015, 2014, 2013, 2012 and 2011. Those number are:

2016:$1.480 billion

2015: $1.385 billion

2014: $1.047 billion

2013: $.907 billion

2012: $.708 billion

2011: $.490 billion

On page 73 of the 2016 10K, and on page 75 of the 2013 10K in the consolidated statements of cash flows for 2016, 2015, 2014, 2013, 2012 and 2011 are shown additions to oil and gas properties and additions to other assets and other property, plant and equipment. These numbers, (added together), are:

2016: $2.060 billion

2015: $2.393 billion

2014:$3.576 billion

2013: $2.876 billion

2012: $3.055 billion

2011:$2.290 billion

PXD DD&A expense 2011-2016: $6.017 billion

PXD additions to oil and gas properties and other PP&E 2011-2016: $16.250 billion.

This seems out of whack to me, considering how quickly PXD’s wells decline.

Glenn, are you arguing the estimated DD&A of $1.364 billion in 2017 would pertain to only 2017 CAPEX? I believe it would apply to all PXD wells, and other PP&E additions that have not been fully depleted, depreciated and amortized, and that have not been disposed of or abandoned by PXD for all years since the company came into existence. There could very well be 1990s assets still on DD&A, in the case of buildings and oil wells back to the late 1970s.

I do agree I did not figure in impairments in comparing 2011-2016 DD&A v. 2011-2016 CAPEX, but I do not see that PXD has taken impairments large enough to close a discrepancy of over $10 billion dollars over the course of six years.

It appears that much of the DD&A is being kicked far out in the future, but I would need to see the schedules carried out for the next 30+ years to confirm that, and I do not have access to that, of course.

Clueless, do you care to give your views on this? Am I looking at this incorrectly?

shallow sand,

I think Pioneer dug itself a heck of a hole back in 2012, 2013, 2014 and 2015.

The wells it drilled in those years, whether wolfberry or horizontal shale, will struggle to pay out with $50 oil. They were high cost, low performance wells in comparison to today’s wells. But a great deal of that sunk investment is still on the books. That’s why Pioneer’s DD&A per boe is so high. And that’s also why Pioneer’s DD&A to capital spend in 2017 is high. It’s like trying to swim (show positive earnings) with a lead anchor tied around your foot.

Should this DD&A expense be even greater than what Pionner is reporting? Has Pioneer engaged in some accounting tricks to make this DD&A less than what it should be? I don’t know.

As to a forward-looking analysis, it looks like Pioneer’s D&C cost per boe is too high in comparison to other peers like Diamondback and Encana.

With its “cube” strategy, Encana is nearing well manufacture mode where it stamps out 60 wells per section in five different stacked pay zones all at one time. It’s boilerplate at under $5 million per well. In its latest investor presentation, Encana argues that’s the only way drilling shale wells in the current oil price environment makes sense.

Pioneer has been, I can earnetly say, a pioneer in drilling shale wells in the Permian Basin, and is still playing that role, experimenting with longer and longer lateral lengths and more and more advanced completion techniques. Others can learn from its failures and successes.

In the long run, however, you may very well be correct when you said:

Time will tell, but there don’t seem to be any shortage of batters at the plate trying to eek out a profit from Permian shale, even at these depressed prices.

Glenn.

I have looked at Encana’s recent wells. I think we need a few more months to see how productive they will be.

I understand how drilling 60 wells as they are intending would cut down on costs per well. We will need to see how productive the wells are.

My initial reaction is that productivity per well is suffering, but it is too early to tell. By year end we should have a better idea.

FANG is a company that seems to have an edge, I haven’t had a chance to look at Q2 for them yet.

shallow sand,

In my view the underlying reason for the fast declining cash flow/DD&A ratio for PXD is the strongly rising depletion rate (see blow chart). As most analyst assumed the shale oil depletion rate (for Bakken, Eagle Ford and Permian combined) will be stable over the years, it actually rose to 91% for July. Although this is already an extreme depletion rate, it will very likely even rise further over the next months.

Bakken, Eagle Ford and the Permian spend cash on 5 mill bbl/d of annualized new production, yet get cash on just 0,5 mill bbl/d of net production growth. As this reduces cash flow considerably, it means also that drilling cost per net produced barrel are nearly ten times higher than for conventional production, despite much lower drilling costs per well.

As most investors probably cannot see the technical difference, it is now most obvious in financial numbers, which led to the crash of PXD (down 10.77% and spread triple breakdown on the point and figure chart). As PXD is the stallion of shale gas and oil production, it is a strong indicator of the future development and should give investors much concern about their shale oil and gas investments.

However, the strong decline of future US oil and gas production is an excellent indication for high oil and gas prices over the next few years.

clueless,

I was looking at Diamondback Energy’s 8-K that was filed this morning for 2Q2017.

What a difference between them and Pioneer.

• DD&A for FY2017 is almost 100% of capital spend for FY2017.

• DD&A is only $9.00 to $11.00 per boe, as opposed to $14.46 per boe for Pioneer (2Q2017).

• Budget to drill horizontal wells is estimated between $650 and $775 million

• For that you get between 115 and 135 wells

• That works out to an average of $5.7 million per well

http://files.shareholder.com/downloads/AMDA-1AK3IX/4882274790x0xS1539838-17-103/1539838/filing.pdf

Diamondback’s average lateral is only 7,500′, and Pioneer’s is closer to 10,000.

Pioneer is pushing the limit on lateral length, and that may prove to be a mistake. That extra 2,500′ seems to come at a very high initial cost, and with a lot more “operational problems,” as Pioneer called them, that slow down execution.

Diamondback is experimenting with a few of the long lateral wells. But they haven’t tried to make that their bread and butter the way Pioneer has. So maybe the Diamondback and the Encana strategy is the way to go. The stock market seems to be saying so.

Glenn – Believe me, people write entire books on various accounting words. So, when we talk here, we are not going to write a book.

I believe that I remember that Black’s Law Dictionary essentially defines an asset as anything of value. Anything of value that ends up on the asset side of a company’s balance sheet is called an asset AND EVERYTHING THAT ENDS UP THERE INCREASES THE COMANY’S “BOOK VALUE.” Everything that is a liability decreases book value, and the net of the two, whether positive or negative ends up being the “net book value” of the company. Purchased Goodwill is an asset. If you purchase CocaCola, the value of the formula would be an asset [billions of $’s] that would end up on the balance sheet and add to book value. If you bought General Motors, the value of their dealer network would be an asset [billions of $’s] and add to book value. If you purchased both with 100% borrowed money, well the debt would be an offsetting liability and the net book value of your company for these two items would be zero.

Assume that a comany uses its own employees to construct their own office building. All expenditures for employee labor, materials, even allocated interest costs, if the company has debt, are capitalized into an asset called office building. Generally, the building asset is depreciated, but at different rates for book and tax. They do not have to acquire the building from someone else. Same thing with an oil well. Only the asset ends up being put into two sub-categories – generally intangible costs, which are depleted and tangible assets which are depreciated.

You say: “But the book value of an asset is the acquisition cost minus depreciation, not minus depletion.” Like I say, you could write a book. But, for your information, the book value of an asset is the capitalized cost less ANY DEDUCTION. If you purchase a patent that is generating royalties, the deduction is called “amortization.” For tangible equipment or buildings, the deduction is called “depreciation.” For intangible drilling costs the deduction is called “depletion.” For accounts receivable assets, there is generally an offsetting reserve for “allowance for doubtful accounts.” For example accounts that are more than 6 months past due might be valued at 50%, and accounts in bankruptcy a zero. For other assets that are demostrably worth less than the book value computed normally, the deduction is called an “impairment.” [Once an impairment is recorded, it can never be reversed in GAAP, no matter how much the asset subsequently goes up in value. [But, you could write a book. For example, if a company has a net operating loss and it is doubtful that it will ever make enough money in the future to receive a tax benefit, the potential tax benefit (which would be an asset, which would increase book value) cannot be recorded on the books. However, if the comany’s profitablility does imporove such that it is reasonable that they will be able to use the benefit of the net operaing loss carryforward, then it can be added as an asset at that time – which increases book value.]

Glenn says: “Tanglible drilling costs are included in both tax basis and book value.” In oil and gas accounting, generaly there is no such thing as “tangible drilling cost.” Tangible items are classified as what they are – generally, depreciable equipment. And depreciation is not tied to production. I believe (but I am 30 years removed) that oil and gas equipent is depreciable over 5 years for tax, but most likely 5-10 years straight line for book purposes.

Glenn says: “You and shallow sand are using depletion and depreciation as if they were interchangeable.” No we are not. Depletion [generally recorded pro-rata over the expected total production] reduces the book value of an asset [generally intangible drilling costs and leasehold costs] and the net is the net book value of that asset. Depletion reduces the book value of an asset, eq1uipment, [for book purposes generally 5-10 years using a straight line method (same amount each year)] and the net is the net book value of those assets.

For general purposes, depletion, depreciation, amortization, valuation reserves and impairments are not recorded as liabilities, but rather as a direct reduction of the value of an asset. They are a reduction of the related asset’s book value. Assets have a book value, and the company as a whole has a book value. Liabilities affect the company as a whole.

clueless,

Well all I can do is speak from experience.

Back when I was participating as a working interest partner in the drilling of a well, in the first year:

1) I got to expense 100% of the Intanglible Drilling Cost.

2) I got to expense the first year’s depreciation, which was figured on a straight line basis (for instance, if it was 10 year property I could expense 10% of Tangible Drilling Cost).

3) I received a 10% investment tax credit, which was calculated by multiplying .10 times the Tanglible Drilling Cost.

4) I got to expense the depletion allowance, which for a little investor like myself amounted to 15% of the gross revenue generated by oil and gas sales.

At the end of the year, my tax basis would be the Tangible Drilling Cost less 10% deprecitation.

In the second year:

1) I got to expense the second year’s depreciation, or 10% of the Tanglible Drilling Cost.

2) I got to expense the depletion allowance, or 15% of the gross revenue generated by oil and gas sales.

At the end of the second year, my tax basis would be the Tangible Drilling Cost less the cumulative depreciation of 20% I had taken in two years.

Now let’s say I decided to sell my workng interest in year three. My capital gain (or loss) would be calculated as the sale price less sales expenses, minus the tax basis, which at that moment would be Tangible Drilling Cost less 20%.

Depletion in no way, shape or form entered into the calculation of tax basis. Depletion was a tax break that producers of oil, gas, other minerals and timber get to take.

Public corporations also got to expense Intangible Drilling Cost, got to take the investment tax credit, got to depreciate Tanglible Drilling Cost, and got to take the depletion allowance, even though depletion might have been figured on a cost basis rather than a percentage basis.

However, now you’re telling me that, for a public corporation, “the book value of an asset is the capitalized cost less ANY DEDUCTION,” and that “for intangible drilling costs the deduction is called ‘depletion.’ ”

You furthermore state that:

Well maybe that’s what depletion is according to current GAAP accounting rules and definitions. But if that is true, then what is depreciation according to GAAP rules and definitions?

Something tells me that the SEC is not nearly as imprecise as you are when it comes to stipulating its rules and definitions.

Glenn – You personnaly did all “tax accounting,” which has virtually nothing to do with GAAP accounting. But, with respect to depletion. There is depletion and “percentage depletion.” Well over 30 years ago, oil and gas companies lost virtually all percentage depletion for tax purposes [it never was used for book purposes], which was the 15% that you referred to. That used to be a tax break and used for tax purposes only. Now no taxpayer can use percentage depletion for tax purposes on more than 1,000 barrels per day. So, it it almost meaningless for public companies producing tens of thousands of barrels per day.

Obviously, what you refer to as “tangible drilling costs” is equipment costs. I cannot say that some operator did not produce a joint venture working interest statement you that said tangible drilling costs. However, I would beleive that most of them would have just said “tangible costs.”

With respect to depreciation, I should have proof read my comment. Your quote of my comment taken from the second to last paragraph – the first word of the last sentence should have been “depreciation” not a repeat of the word depletion used in the previous sentence. For some reason, I suspect that you recognized it as a typographical mistake.

Back in the investment tax credit days [1970’s?], I do know that there was accelerated tax depreciation allowed on most equipment. I would be surprised if you could not have used something that was essentially double declining balance over 5 years for oil and gas equipment depreciation. And section 1245 depreciation recapture was in effect, which may have required you to recapture depreciation at an ordinary income rate – if you sold equipment at a price that exceeded its tax basis.

clueless,

So then what you are saying is that, when it comes to GAAP accounting and the SEC’s rules and definitions, that tanglible costs are depreciated and intangible costs are depleted?

And furthermore, the only place where the IRS’s concept of a depletion allowance shows up on SEC forms is in the income tax line (in the form of lower taxes)?

Glenn – I would say in general, your first paragraph is correct. But, remember that the terms are more convention than radically different ideas. It’s like a musician produces music, and I produce noise. But, in both cases, the scientific result is noise. [Probably a crappy analogy, but I do not want to argue about it.]

With respect to IRS’s concept of depletion – I do not know how to answer. The IRS Code has % depletion, which is not in GAAP. So, you only see % depletion on tax returns. On the other hand, the IRS also does have normal depletion, just like GAAP. However, with respect to oil and gas, tax return depletion is generally much less than GAAP. That is because intangible drilling costs are expensed immediately for tax purposes, but are capitalized and depleted for GAAP purposes.

clueless,

That makes sense and seems to be consistent with the numbers that the O&G companies that operate in the Permian Basin are reporting on their SEC forms.

This discussion has helped me clarify some things. The fact that the IRS and SEC have completely different rules and definitions for “depletion” makes it quite confusing.

It sure is. And when we operate in other countries we have to keep three separate sets of books, all of them linked to ensure compliance, but which use different rules.

For example, in some nations there’s no difference between tangible and intangible costs. We also have different rules regarding what can be expensed versus capitalized. In some cases there’s a cap on capital recovery. In others, for example Angola, the net share of sales is adjusted according to the rate of return.

I’ve got so exasperated over stupid meetings with accountants to decide which portion of a well sidetrack is expensed and which is capitalized, I decided that if I ever get to design a system I won’t even have a difference between OPEX and CAPEX. I’ll simply say everything gets lumped and 33% of the total will be deducted from the gross income line each tax year.

clueless CORRECTION 4:25 pm comment- The first word of the last sentence in the 2nd to last paragraph should be “Depreciation” – not Depletion.

Thanks George—

My literacy on this is minimal.

Thanks again, George.

A few comments regarding your last paragraph on the shelf subsalt – there was a fair bit of interest in that play a few years ago after Freeport McMoran announced gas discoveries at Davey Jones and Blackbeard – nothing has come of them since except for an onshore gas development called Highlander. (Freeport spent a lot of money trying to produce one of the Davey Jones wells, but were, in the end, unsuccessful).

The W&T’s oil wells at Mahogany are actually a re-development of a subsalt discovery Phillips made in the mid 90s. Not sure if W&T is developing a different sand, or different fault blocks than Phillips.

In general, the shelf subsalt is thought to be a gas play, but, most of the prospective reservoirs are interpreted to be in a deep-water slope setting, rather than a basinal setting like the GOM deepwater subsalt. Being in a slope setting implies that reservoirs are going to be isolated to channels/channel systems. This suggests that unless your seismic data is good enough to identify these channels, and remember this is subsalt data, you are taking a big chance that reservoir is going to be present at any given prospect.

George – We have got to be from different generations. I am 76, and in the 1960’s did COBAL F programming for Bell Helicopter for a couple of years. So, I have been somewhat comfortable with computers.

But, I am just blown away by your charts and graphs and the huge volume of information that you put into a post. I have no clue where you get all of your information, nor how you are able to mass produce your graphs, etc. And, you have to be very good at it or else it would be consuming all of your spare time.

I have Windows 10, and I will be typing along and accidently hit some key [or combination, I have no idea what] and my entire comment will disappear. And I have no idea how to “find” it, and must start over. That could never happen to you because you would shoot yourself.

But, thank you for all that you do for us.

I guess I’m very good at it – LOL – not really. I’m a bit younger, but not much, my first programs were on tape and punch cards and on a main frame with men in white coats tending and sticky mats you had to walk over to keep the dirt out. I did Cobalt and Fortran and another beginning with B that I’ve completely forgotten (that was the tape one) then moved up to C, C++ and VBA and even Postscript, not sure if that’s used any more. It took a bit of time to set some of this up, but now the only time is with downloading the data from BOEM, and then only because it limits the number of leases that can be downloaded at once. Other than that I just run a couple of macros and use the SUMIFS function a lot (and with a lot of arguments) – I tried pivot tables, but not a fan really. I can handle interpretive languages these days, I’m not so sure how I’d do with the write-compile-correct-run cycles we had to go through, and my spelling and grammar get worse each day. Really I started looking in detail at GoM because the EIA forecasts didn’t make sense, overall it fills an hour or two most days.

I use a Mac, I hate Windows, I liked Unix the best – for some reason I think Mac operating systems might be based on it, long ago, but can’t remember why I think that.

Yes, Mac operating system is a Unix derivative, so is Android and Linux. And Chrome OS which runs my chromebook, my best laptop ever!

All but one release of Mac OS X (now macOS) has been certified as Unix by The Open Group, starting with 10.5:

10.12 (Sierra)

10.11 (El Capitan)

10.10 (Yosemite)

10.9 (Mavericks)

10.8 (Mountain Lion)

10.6 (Snow Leopard)

10.5 (Leopard)

Apple’s page on The Open Group site only lists the current version of macOS as I write this, but all of the links above were at one point found via that page.

OS X’s status as a certified Unix is called out in Apple’s Unix technology brief, which also has other good technical bits in it that will help you compare it to other UNIX® and Unix-like systems.

I did Cobalt and Fortran

Cobalt was the original precursor of today’s BLUE Screen of Death, in MS Windows’ Common Business Oriented applications… 😉

BTW, I did a lot of graphics and vaguely recall editing postscript code in text files for creating vector based images but then later Adobe evolved and I became a black belt bezier curve master with Illustrator and a mouse not having to worry about the underlying code.

I think I might have meant COBOL – did I? Whichever one was more for business and accountancy types in the 70s, with an attempt at natural language commands I think.

Yeah, I think the commerce types used COBOL while we (engineers) worked with FORTRAN. Not sure who used BASIC, I never did. The most time consuming job for me, and every other geophysicist, was doing the programming though by the time I came on the scene sub-routines were becoming available which helped a lot. Alas, punch cards.

Hi George

cobol is correct.

I can’t find the link now, but, I recently saw an EIA document about their projection for US production out through December, 2018. They projected that GOM production alone would have an increase of over 300 kbopd between June-2017 and December-2018. That would put GOM production at about 2 mmbopd or so by December-2018.

Between now and December-2018, the most notable new projects to come on line should be Big Foot and Stampede, which could add about 100 kbopd by December-2018. I can’t see where the rest is coming from.

We’ve established that EIA’s GOM projections are consistently too favorable, and here we see it again.

Probably STEO, which comes out around the middle of the month I think.

Found the link.

https://www.eia.gov/todayinenergy/detail.php?id=32192

The EIA identifies more than 2 projects to come on line between now and December-2018, but, I suspect most of them are tie-backs.

I think a lot of what they have is wrong: for this year and next they have Son of Bluto 2 – which came on last year; Otis, which is a gas field and came on last year; Atlantis North, which will come on but I think they don’t have capacity to increase production overall but only maintain plateau; Amethyst, which is gas field that came on last year and gave up after 4 months and I think has been abandoned; Horn Mountain Deep, which is on line but a small tie back; and then Stampede (I think 70 kbpd).

Last year they had a few that might increase in production especially Julia and Stones, but Heidelberg Phase II isn’t for a couple of years; Wide Berth is a small field that has been operating since 2012 (I think they actually meant Penn State); Thunder Horse South happened this year; I don’t know what Caesar/Tonga II is, I think they probably mean Constellation (maybe 30 kbpd next year). I think your 100 kbpd to come through 2018 is about right, Big Foot is not due until the end of the year, and then nothing planned for 2019 at the moment.

Hi George,

Did your analysis this month change your future projection from previous posts?

Seems you and SoLaGeo agree the EIA’s STEO for GOM in Dec 2018 is about 200 kb/d too high (or perhaps at least 200 kb/d too high).

If anything, with Anadarko cutting spending, I think maybe a slightly higher decline rate than I thought previously. I think EIA are predicting 300+ kbpd growth. I think it will be a decline from where we are now, unless there are a couple or more decent tie back discoveries in the next couple of months.

The BH GoM rig count dropped seven for last week, I expect some is just random variation and will come back, but as I said above it’s also likely that they are running out of planned development well targets, and possibly also near field exploration prospects; and opportunity in fill drilling for acceleration has been dead for three years now.

GoM rig count – I was looking to see if the -7 drop was seasonal but there is nothing much too see on the chart.

It looks like some was due to shut down for Tropical Storm Emily. This gives details of what’s happening, including non drilling workovers: https://www.bsee.gov/sites/bsee.gov/files/current-deepwater-activity.pdf

Thanks George.

EIA is too high on STEO by at least 200 kb/d (solageo’s estimate) and perhaps as much as 400 kb/d too high if GOM continues to decline.

Both the auto industry and US voters support increased fuel efficiency standards.

https://www.bloomberg.com/news/articles/2017-08-01/carmakers-say-trump-should-want-deal-to-boost-u-s-fuel-economy

http://cdn.exxonmobil.com/~/media/global/files/crude-oil-sales/crude_oil_thunder_horse_assay.pdf

ThunderHorse assay. 30% middle distillates. Right and proper oil.

George.

Which companies are still big players in GOM?

Did ConocoPhillips state they were soon out?

SS – This gives you an updated rank by oil production (CoP second bottom on first page, but they may have subsidiaries listed separately):

https://www.data.boem.gov/Production/Files/Rank%20File%20Oil%202017.pdf

and this by gas

https://www.data.boem.gov/Production/Files/Rank%20File%20Gas%202017.pdf

George. Thank you!

Is there any possibility that GOM wells that produced majority gas or solely gas have been economic in the past three years with gas prices under $3 per MCF?

Also, I had mentioned before looking at Energy XXI wells on an individual basis, and noted how many produce under 100 BOPD. Do you have any information as to how many oil wells in GOM produce under 100 BOPD at present?

I do not know much about GOM production, but suspect many wells have been operated at a loss since late 2014. I have heard there are concerns of many wells in GOM being abandoned and not plugged. Any truth to those concerns?

You are getting outside my comfort zone there, I mostly just look at the oil. First off I think you’d need to separate the associated gas from produced gas, and then shallow water from deep, and then new developments from legacy fields. Hadrian South and Otis (in charts above) are the only gas fields added recently. Baldpate is the only other largish deep water gas field operating. All the data you want is available but the download time is high if I haven’t kept the Excel files (or more likely can’t remember what the names mean). I’ll see what BOEM have and what I can easily extract.

SS – this shows the number of oil wells in the range shown (up to the maximum under the bar) in bpd for January this year. I calculated the flow as stream day (i.e. production divided by days on line) rather than monthly average. Don’t know if it helps. There are over 6000 wells that didn’t produce at all, and probably didn’t through the year, I haven’t managed to figure out if they are plugged yet, but might be able to.

This shows the number of gas wells (i.e. not associated gas) in the given flow range (again streamday, not average over the month). Does this mean anything – it might make more sense if I split it up by water depth?

Looks to me like there are likely a large percentage of both oil and gas wells in the GOM that are not economic on an operating basis, plus if those 6,000 wells are not plugged, wow!!

I have a hard time understanding how an offshore well making under 100 BOPD works in the world of sub $50 oil.

Energy XXI operates many of those and they long ago went BK, but I’d sure like to hear from someone in the know how to make stripper oil wells in GOM work. Not because I am interested in investing, but because I cannot see how it can work financially.

Many, or most, of those GOM wells currently producing at low rates (<100 bopd) now are shallow water wells that were drilled at a time when oil prices were much higher – so the wells may have actually been a good investment at the time, produced at higher rates during a year or years of high oil prices, and may have even paid out. Now, the operators are just milking them along for as long as they can.

Current shelf drilling activity is very low – maybe 3-4 drilling wells.

Current shelf oil production is probably around 150-200 kbopd.

I don’t know enough about shelf operating costs to know if an operator can afford to keep a platform with a bunch of 20-50 bopd wells.

SouthLaGeo.

I don’t know hardly anything about offshore operating costs either.

I would think offshore wells would need someone to periodically check them, which would mean taking a floating vessel with men and tools to them. I assume these wells quit flowing naturally, so need some type of artificial lift and I am trying to picture how those are powered if produced gas is not sufficient. Next, of course, would be disposal of salt water. How does that happen efficiently as the water cut rises? How about down hole chemical treatments? How about gathering for such small volumes. Finally, the abandonment costs have to be huge?

I’d sure like some information on this, if anyone out there is reading and knows the answers.

SLG beat me to it but below shows the split for deep and shallow. Almost all shallow wells are below 100 bpd. I’d imagine they are mostly on unmanned wellhead platforms, the water is mostly extremely shallow, I doubt there’s that much of a difference in operating costs with onshore wells, maybe a bigger one for new developments. Note I had something wrong above and included gas wells in the oil wells so had shown a lot of low producing condensate.

This shows the numbers for inactive wells, very few P&A fully, thousands inactive or temporarily abandoned (which probably means permanently abandoned but not yet fully P&A’d). With a caveat that this is new info. to me so I may have got something wrong somewhere along the line.

George. Thanks again for the GOM information.

I can’t help but think wells in very shallow water would still be much more expensive to operate than onshore wells.

For example, what all is involved to repair a tubing leak in a shallow offshore well?

Same with abandonment.

I do note many of these shallow offshore wells have produced over 1 million BO. But they have to really be hurting economically now, I suspect worse than most onshore stripper oil and gas wells.

Probably a bit more expensive, but I should think most of the wells are pretty simple and fairly short compared to horizontal wells on shore. I’ve seen a couple of shallow drilling rigs in yards and there’s not much to them compared to, say, a deep water DP drilling ship. Moving them around can’t be much of a problem, maybe easier than a fleet of trucks. But that’s all supposition.

As far as P&A goes it looks like they might have decided the best bet is not to bother. Although there have been activities listed as non-rig P&A on several deep water rigs each time I’ve looked at the BSEE activity list over the last six months or so.

George. If you have time, take a look at Energy XXI financials, on their website.

They also provide a good overview of their operations. They own some of the most prolific fields in shallow GOM. Some are Humble Oil discoveries from the late 1940s.

Unfortunately, production has fallen from 49K BOEPD to 41K BOEPD from Q1 2016 to Q1 2017. At $51 oil and $3.10 gas in Q1 2017, they only cleared $6 per BOE, before DD&A.

There is nothing left for new wells, very expensive to operate, more than our 1 BOPD shallow onshore stuff.

If they are wholly or mostly in GoM then they are going out of business within a few years I’d have thought.

They have 335 producing oil wells (but getting fewer each month by 2 or 3) averaging 85 bpd and falling slowly, and 88% water cut and rising, plus 250 inactive wells to be plugged.

For gas: 53 wells averaging 130 mscfd, but falling fairly quickly by the look of it (maybe 20 to 25% y-o-y decline), and 210 wells to be P&A’d.

SS asks an interesting question: “Do you have any information as to how many oil wells in GOM produce under 100 BOPD at present?”

I really have never even thought of such a thing. My guess is that would be like McDonalds operating a restaurant that sold less that 100 hamburgers a day. If any company has such wells, I think that I would be a seller.

Oh btw sportsfans re credit ratings. Fitch (one of the big three, if you don’t want to study Morningstar’s methodology) rates PXD as BBB.

They rate BP at A.

That’s BP. The company whose litigation expense from the spill has come in at the top end of estimates. The company dealing with $49 oil like everyone else. ANDDDDD the company with huge asset profiles inside Russia, which were seized in retaliation for England signing onto sanctions.

They are rated A. Compare and contrast.

TWIP has all stocks falling again, but by a total less than half each of the last couple of weeks: -1.5, -2.5 and -0.2 mmbbls for crude, gasoline and distillate respectively.

Hi George

Announced this morning.

The Stena Icemax encountered the Druid prospect in the porcupine basin and it is porous sandstone but water bearing they will now drill down to the lower Drombeg prospect.

No hydrocarbon show at all is not good news at all for the basin.

http://oilprice.com/Latest-Energy-News/World-News/Oil-And-Gas-Added-13-Trillion-To-The-US-Economy-In-2015.html

7% of all employment in the US is linked to the oil-and gas industry?

Does that include the US auto industry?

https://climatism.wordpress.com/2017/07/12/wind-turbines-are-neither-clean-nor-green-and-they-provide-zero-global-energy/

Few data points concerning wind power, electricity generation, and natgas …

World’s first floating offshore wind turbines being installed right now off Aberdeen by Norwegians. Project – called Hywind – incorporates amazing degree of engineering coupled with very high price.

South Australia wholesale electricity hit A$416/ Mwh a few hours ago, which is nearly 15 times New England’s (expensive for US) US$25/Mwh.

New England’s juice is 91% gas or nuclear sourced.

NE renewables right now provide 6% of total, 2% of that from wind. (Wood and refuse provide 92% of the overall 6% renewable category).

Range, along with EQT and Cabot, are now describing 4 Bcf of gas per 1,000 lateral foot from their wells to be the ‘new normal’.

They project thousands of these wells will be developed over the coming decades at lengths ranging from from 10,000′ to 15,000′ in length.

Do the math.

The folks who are expecting wind and solar to provide high amounts of electricity in the future are facing increasing challenges in seeing that implemented.

Hi Coffeeguyzz,

Like every other natural gas field, these fields will also peak and decline.

The shale gas also need to fill in supply from declining conventional natural gas, if it displaces coal fired power, great.

Eventually solar and wind will take over from natural gas as it depletes and becomes more expensive and as further technological improvements in solar power and batteries reduce the cost of solar power so that natural gas can only compete as backup power. This might take until 2040, hard to guess accurately. Wind power in good locations (Great Plains in US) is also very cheap, cheaper than new natural gas plants at current prices.

It takes 150 wind turbines to power one shopping mall. And there are over 47k shopping centers in America. It would over 25 million wind turbines to power just our shopping centers! And only when the wind was blowing heavily. BWWWAAAAAAA

https://www.physics.rutgers.edu/~matilsky/windmills/shopping.html

I think you should check your math: 25 million wind turbines, at 1.5MW each, would produce 37.5 terawatts when the wind was blowing heavily, while the US uses less than .5 terawatts.

Off by only a factor of 75.

Thus, if we now adopt this 10% effective capacity, each turbine provides 0.15 MW, and we need over 150 turbines just to provide the basic needs of ONE SHOPPING MALL!!

https://www.physics.rutgers.edu/~matilsky/windmills/shopping.html

It’s not 10% effective capacity, that’s around 33%.

The 10% figure is for something entirely different: statistical contribution to peak capacity. It’s a technical measurement used by utilities and grid operators – it doesn’t tell you how many kWhs are produced.

Did ruin your dreams of a brighter world? LOL You are a like a donkey Nick G. You will believe anything that Obomba and Musk and the MSM tell you. No questioning ever, No common sense. Just feed it to Nick and he will eat it!

I believe the math.

Just do the math!

There are about 1500 shopping malls in America, and 500 of them are dead. I notice you switched terms mid post.

https://www.oilandgas360.com/rambo-frac-delivers-new-marcellus-productivity-record-chesapeake/

61.8 MMcf/d from a single well

A – Robert Douglas Lawler: Okay, Charles, hold on to your sideboards of your desk there. So this well is a little bit more expensive than the wells we’ve drilled. This is a 10,500 foot lateral with a relatively aggressive frac on it, about $8.5 million. That’s the field estimate today. These are early numbers, of course, because we’ve been only been on for about six days or seven days, but we believe that we can get that cost down as we go forward.

Q – Charles A. Meade: Well, I tell you what, I’m out of my chair and on the floor, now.

A – Robert Douglas Lawler: Okay. Jason’s team has done a great job. I’d love Jason to put a little color on that as well.

A – Jason M. Pigott: Well, it’s funny. The team, again, they were trying to figure out how to get 60 million a day out of one of these wells, and they actually call it the Rambo frac because they needed to attack that formation like Rambo would a POW camp. So they increased the cluster efficiency and packed it with 32 million pounds of Hell on Earth. So we succeeded in setting the captive gas molecules free.

Lottsa significant info in that article. I believe that is the highest 24 hour IP from any Marcellus well of which I’m aware.

However,

To give some perspective on the vast, vast potential of the Utica …

Consol actually has 2 Utica wells, the Gaut and the GH 9 with 24 hour IPs at 61MMcf. (Casing pressure on the Gaut was a touch under 10,000 psi.

EQT’s Scotts Run – arguably the most successful unconventional well in the world – had a 24 hour IP of 72 MMcf, casing pressure st 10,000 psi, and a lateral only 3,200′ long. (Flowed 29 MMcfd for 8 months).

Appalachia Rising.

EQT’s upstream segment posted a net loss (non-GAAP) of $4.2 million in Q2, 2017.

EQT’s earnings of 24 cents per share in Q2 were the result of positive earnings in its gathering and transmission segments.

Once again, the Scott’s Run well cost $30mm. That well will lose $10mm+. The Scott’s Run was very unsuccessful.

The Scotts Run was in every sense of the word a ‘science project’ as it was EQT’s first Deep Utica well.

The $30 million dollar cost to drill and complete this well was partially due to the extraordinarily high pressure encountered. So high, in fact, that the original rig was replaced – after a several month delay – with a much larger rig with pumps able to handle the 10,000+ psi pressure.

Now, with 22 months’ production (665 days), the SR has surpassed 13 Bcf cum (13.038), and still flows over 8 MMcfd.

Using $3/mmbtu for rough evaluation, this well has generated almost $40 million in under 2 years.

EQT originally projected 12 to 19 Bcf cum over 30 years time for this well.

The only company seemingly still interested in Deep Utica wells in SWPA is Consol.

The expected D&C price of $14/15 million per well along with production results should increase available knowledge of this enormous resource’s potential.

This appears to be from Chesapeake’s CC.

Take a look at share price, $4.50. News reports out today say they are cutting back in NE Appalachia in a bid to increase the oil percentage of their production.

I assume the Marcellus and Utica companies will continue to over produce for years and sell their gas for $2.50 per MCF or less?

Fitch rates CHK paper B-, negative outlook.

OXY released Q2 2017 earnings.

OXY earned 66 cents per share, however only 15 cents per share was from continuing operations. The remaining 51 cents per share was a gain on the sale of assets.

OXY lost $300 million in Q2 on US upstream v a loss of $191 million in Q1 on domestic upstream.

OXY had positive earnings of $422 million in international upstream v earnings of $418 million in international upstream in Q1.

OXY had positive earnings of $230 million in chemical v positive earnings of $170 million in chemical in Q1.

OXY declared a dividend of 77 cents per share, which is a payout ratio of 513.3% of earnings per share from continuing operations.

OXY is the largest volume producer in the Permian Basin. OXY’s US upstream operations have been a large drag on earnings since 2015:

2015 – negative EPS of $704 million.

2016 – negative EPS of $1.658 billion

First 1/2 2017 – negative EPS of $491 billion.

So, from the above, OXY has had negative EPS of over $2.8 billion from its US upstream oil and gas operations since 1/1/2015.

It is noteworthy to look at OXY 2013 and 2014 US upstream EPS:

2013 – positive EPS of $2.545 billion.

2014 – positive EPS of $1.854 billion.

I think OXY is a very solid example of what low oil and natural gas prices from 2015-1/2 2017 have done to the economics of onshore lower 48 US upstream oil and gas.

The irony is that instead of saving the gas and oil industry, LTO may be hastening its decline.

First 1/2 2017 – negative EPS of $491 billion.

SS- Since I am the poster boy for typos and have been appropriately humbled, it is with no malice that I would note that in this case, the billions should be millions.

Clueless.

Thank you, my bad. I meant million. $491 million is still a lot of losses in just 181 days.

Clueless. I have a good example for how overvalued some shale stocks are.

PXD just cratered the last two days to about $135. It earned 21 cents a share for Q2.

Clorox just posted earnings today. It is also trading at about $135 per share. It earned $1.53 per share for the quarter, declared a per share dividend of 84 cents, and guided fiscal 2018 earnings of $5.25+.

“OXY declared a dividend of 77 cents per share, which is a payout ratio of 513.3% of earnings per share from continuing operations.”

RDS and BP both have this going on, but Shell has some downstream earnings so they are undercovered I think less than 100%.

But they can borrow. Credit ratings as . . . above? well last post. They don’t have to pay 8% for money.

OXY credit rating: A . . . on some 10 and 30 yr debenture issuance about 7 mos ago.

Compare and contrast with the shale credit zombies.

I put this in the older oil post. I meant to put it here.

The fight over water for drilling in Texas.

http://www.houstonchronicle.com/business/article/As-the-oil-patch-demands-more-water-West-Texas-11724100.phpI

I put this in the previous oil post in response to a comment about the Permian. But it is an article from yesterday so I want to post it here.

Here’s an article, plus a graphic showing sharp decline rates in the Permian, Bakke, Eagle Ford, and Niobrara.

https://www.bloomberg.com/news/articles/2017-08-03/how-the-wild-shale-race-may-be-harming-the-permian-s-oil-trove

This calls into question why drillers don’t drill outside of the core area where there wouldn’t be well interference. I monitored initial production figures for Bakken wells for 3-4 years and found that wells within the core area had a high probability of having initial production of >1000 b/d and often >2000 b/d. Outside of the core area, it was common for initial well production to be less than 100 b/d. The core area of Bakken is pretty well saturated. I personally don’t see production again reaching the level reached in Dec. 2014 even if the price of oil raises to over $100/barrel.

Investors are getting nervous.

https://www.bloomberg.com/gadfly/articles/2017-08-03/andy-god-hall-quits-oil-falls-crisis-of-faith

The “Self-Driving Car” is Only an Oxymoron

How are the potentially driverless cars doing in their testing? Awful. For example, in the first week of March, Uber’s 43 test cars in three states logged some 20,000 miles on public roads. Their drivers had to intervene and take control away from the software, an average of once every mile. Critical interventions, required to save lives and property, were counted separately; they occurred every 200 miles. Which makes your life expectancy, as a passenger in a truly autonomous car, approximately four hours.

Bottom line: “driverless cars” are not here, and not coming. Like artificial intelligence, virtual reality, genetic engineering and other “next-big-thing” oxymorons, what we’re really talking about here is a high-tech con, designed to separate real morons from their money.

http://www.dailyimpact.net/2017/08/03/the-self-driving-car-is-only-an-oxymoron/

I think they can build special highway lanes for cars equipped with autopilots. These can stay on course and react properly as long as the geometry is kept simple. I can also see use for small electric self driven vehicles limited to 35 mph (50 kmph). In this town where I live, that’s the top speed limit in 95% of streets and avenues. The slow speed and the enforced crosswalks make a serious accident almost impossible to have (I haven’t heard of a single deadly accident on city streets in years).

Such driverless vehicles would come in handy for older folk who mostly go to the market, to shopping centers, visit friends, the doctor, etc. They seldom log more than 30 km in one trip. So the battery range can be say 100 km. We really can’t use electric vehicles to go to a nearby city, the summers are hot and we have mountains to climb which really reduce battery life.

Limits to growth are not “predictions” they are scientific models based on computer simulations. They are used in physics, astrophysics, climatology, chemistry, biology, economics, psychology, social science, and engineering. (MIT Smithsonian Meadows 1972)

That’s exactly right – the Club of Rome LTG models were not predictions, they weren’t forecasts: they were *scenarios* that assumed limits to growth, and simply modeled the dynamics we’d see in the model outputs when the economy hits those limits. Basically, they modeled “overshoot” – what happens when there are lags, delays and positive feedback between between the points of hitting limits and seeing the results in the economy.

Most of all, they *assumed* limits to growth – they didn’t prove that those limits existed.

Sadly, Dennis Meadows has forgotten this basic fact, or chooses to not remember it, and is still going around talking as if those scenarios were in fact forecasts, and discussing how close they came to reality. In fact, the overshoot modeled in those scenarios has not been seen in any way – so far the world economy is pretty much simply growing in the same exponential way as before.

“Can anything be learned from such a highly aggregated model? Can its output be considered meaningful? In terms of exact redictions, the output is not meaningful.…The data we have to work with are certainly not sufficient for such forecasts, even if it were our purpose to make them” (Meadows et al. 1972, p. 94).”

http://wtf.tw/ref/costanza.pdf

The Club of Rome models did do us a service, by showing us what overshoot might look like, and showing us the impact of lags and delays. This appears to be relevant to Climate Change, though probably not relevant to Peak Fossil Fuels – the lags, delays and positive feedbacks that might impair mitigating the impact of PFF are much smaller and shorter.

Looked at Diamondback’s Q2 earnings release.

Diamondback’s gross revenue through the first six months of 2017 is $504 million. This is before any expenses.

Diamondback plans on spending between $900-$1,000 million in CAPEX in FY 2017. However, 2017 DD&A guidance is just $300 million.

IMO deferred depletion expense due to exaggerated EUR is the only reason why Diamondback has strong earnings. PXD DD&A/annual CAPEX ratio is around 50%, whereas FANG’s is around 30%.

shallow sand,

I agree that FANG’s DD&A/annual CAPEX ratio is around 30%. Where I said above that “DD&A for FY2017 is almost 100% of capital spend for FY2017,” that is mistaken. Your “around 30%” figure is the correct figure.

Diamondback has $12.5 billion of PP&E, with $2 billion of DD&A taken against said assets thus far.

49% of Diamondbacks’s horizontal wells produced under 3,000 BO in 4/17 and 95% of Diamondback’s vertical wells produced under 750 BO in 4/17.

IMO depletion expense for GAAP purposes is understated.

shallow sand,

Where do you get the $12.5 billion figure? According to Diamondback’s 2016 annual report, it had $3,390,857,000 net property and equipment on Dec. 31, 2016.

Diamondback took some very large impairments in 2015 and 2016.

Look at PP&E for Q2, 2017. Note FANG has elected not to schedule a little over $4 billion, which I assume must be land.

shallow sand,

I still don’t see where you’re coming up with the $12.5 billion.

If you add the $4,008,388 excluded to the $6,508,747 included, the total is $10,517,135.

But even that figure is erroneous, as is explained in detail lower in the Form 10-Q. The correct figure for net property and equipment on June 30, 2017, including the cost of recent acqusitions, is $6,508,747.

You are referring to net of DD & A. I am referring to gross, before DD & A, ($12 billion). However, you are correct, I did make an error and double counted the $4 billion not subject to depletion.

So, PP&E all categories is about $8.5 billion, and accumulated DD&A is about $2 billion, leaving about $6.5 billion of PP&E net of accumulated DD & A. Big error on my part. Sorry about that.

However, you do see where I indicate the percentage of horizontals below 100 BOPD and verticals below 25 BOPD? Shouldn’t depletion on those low volume wells have been mostly exhausted under the unit of production method, which FANG utilizes (see the note in the screenshot you posted)?

I agree, I am doing some educated guessing here. I would sure love to see the well by well schedules, and compare them to actual production histories. Given the sudden emergence of the “bubble point death” debate, I wonder if companies will possibly disclose this detail.

Interesting that PXD, who did acknowledge rapid pressure decreases and increasing GOR, is still being punished by Wall Street (low today of $131.08). Why wouldn’t this issue be relevant across the PB, and likely across all US shale basins? Aren’t companies drilling on very tight spacing, with longer laterals and larger fracs in all basins?

I also wonder over how many years tangible equipment is being depreciated. I assume 7 years, but that is also an educated guess on my part.

shallow sand,

On new years eve December 31, 2014, both Pioneer and Diamondback entered 2015 with a considerable number of wolfberry wells and horizontal shale wells. The shale wells were drilled during the experimental phase of the Permian shale play when oil was $100/barrel. And just like the wolfberry wells, these older shale wells were high cost wells with poor well productivity. More recent shale wells are much less expensive and have much higher well productivity.

The difference between Pioneer and Diamondback, however, is that the latter was very aggressive in 2015 and 2016 in realizing the necessary impairments to clean up its balance sheet. So, using impairments, Diamondback had reduced the book value of its oil and gas properties by 41% going into 2017.

Pioneer, on the other hand, had reduced the book value of its oil and gas properties using impairments by only 10%.

One end result of this is that in 2017 Pioneer is looking at about $14/boe in DD&A, whereas Diamondback is looking at about $10/boe in DD&A. That $4/boe difference counts directly against 2017 earnings.

Pioneer also experienced significant execution problems during 2Q2017, slowing it down and adding significantly to D&C costs.

Pioneer is also pushing the envelope on lateral length, far more so than Diamondback.

I suspect these factors have a lot more to do with why Pioneer’s stock price declined than the “bubble point death” debate.

Furthermore, Pioneer did not “acknowledge rapid pressure decreases.” Pioneer explained both in its slides and its conference call that the increase in GOR will enhance EUR, not diminish it. To date, it has had no effect on oil production whatsoever.

.

“increase in GOR will enhance EUR”

that explains in a nutshell why the scoop and stack play have some of the best economics of any LTO play. In simple terms the gas trapped in an over pressured tight formation is highly compressed and transports the liquids out of the pore spaces into the well bore and “lightens” the load of the liquids has it is brought to the surface. Higher pressure and more gas = more liquids where the formation contains oil, condensate or NGL’s.

texas tea,

It’s articles like the one linked below, written by someone who knows nothing about drilling and producing oil wells (his ignorance is obvious to anyone knowlegeable about drilling and production operations), that gives the shale bashers hope that the shale revolution will be a flash in the pan:

Rising Gas Output Drags Down Shares Of US Shale Leader Pioneer

https://www.reuters.com/article/us-pioneer-natl-rsc-hot-idUSKBN1AI2I6

What we’ve got is the blind leading the blind.

I listened to Pioneer’s 2Q2017 conference call, and the situation isn’t anything like the Reuter’s reporter says.

In the Midland Basin, it’s customary to set intermediate casing at about 5,000′. In one of the areas that Pioneer is operating in, it experienced an overcharged gas zone somewhere between 5,000′ and the top of the Sprayberry, so it had to mud up to keep this abnormally high-pressured zone under control. Then when Pioneer drilled into the depleted Wolfberry (conventional) zones, the mud was too heavy and they lost circulation.

These overcharged gas zones in the Midland Basin are exceedingly rare. For that reason it was totally unexpected and unplanned for. Nevertheless, the gas zone covered an area that affected about 30 wells that Pioneer was drilling.

Pioneer solved the problem by running a third string of casing to seal off the abnormally high-pressured zone. This extra string of casing cost them an extra $300,000 per well and many extra days of rig time per well. And, as I’m sure you’re aware, this could also completely screw up their well design, restricting bit and hole size below the extra string of casing and maybe causing a reduction in the size of production casing.

As Pioneer CEO Tim Dove called them, these were “train wreck wells.” And I’m sure they were.

So to conclude, here’s what the Reuter’s reporter wrote:

“The higher pressure, meanwhile, means Pioneer is producing more gas from the Permian than it anticipated.”

So here I am, saying to myself, “Lordy, lordy, save us from this ignorance.” The high-pressure zone is above the producing sprayberry and wolfcamp shales, completely sealed off behind an extra string of casing, and has nothing to do with the fact that Pioneer is producing more gas.

But something tells me that many oil and gas investors are no more knowledgeable about drilling and production operations than what the Reuters reporter is.

TT

And that is also the fundamental reason why EOG, being the very first significant player in the Eagle Ford, leased the hundreds of thousands of acres they did in the southwest to northeast narrow band they still operate.

It was at the point where high liquids were suspected go be along with high gas pressure with which to drive the oil out of formation, into wellbore, and assist in lift.

Their acreage is viewable on any of their presentations.

There is a very distinct difference in high initial GOR (as was found by GeoSouthern and Petrohawk in DeWitt County in the Eagle Ford play) and increasing GOR over the life cycle of a well in solution gas driven reservoirs like organic shales (Bakken/Eagle Ford) or shaley carbonates (Permian). Increasing GOR in solution gas (and/or gas expansion) driven mechanisms is natural; as hard as it is for shale oil cheerleaders to accept, its just life. Its the way reservoirs deplete. The party never lasts forever.

There are a host of SPE papers etc., that explain this phenomena http://wiki.aapg.org/Reservoir_drive_mechanisms. Better yet, there is a petroleum engineer among you that, in the interest of proper Society of Petroleum Engineers (SPE) ethics, should offer all of you an ‘unbiased, impartial’ explanation for what happens to oil recovery when GOR increases to below bubble point. Finding graphs and spin from investor presentations like those recently spewed by PDX does not count as unbiased. A shale oil company is never going to tell the truth about itself. As to the ethical requirements of an engineer, please see: http://www.spe.org/about/professional-code-of-conduct.php.

Truthfully the same thing happening in the Bakken and Eagle Ford may already be happening in some benches of the Permian and our friend Art Berman has already addressed this, here: http://www.artberman.com/the-beginning-of-the-end-for-the-bakken-shale-play/. The problem of increasing GOR in the Eagle Ford is so pronounced that EOG is now taking many of its wells off rod lift and placing them back on gas lift to recover more TF with much higher WOR.

“Increase (with a capital ‘I’) in GOR will enhance EUR,” is a wormy statement and not true. High initial GOR, yes, increasing GOR, no. Increasing GOR will ultimately have a negative effect on oil recovery. It did in the vertical Spraberry wells I drilled and every other reservoir I have ever drilled except those driven by water.

Increasing GOR does, however, ‘enhance’ BOE EUR because the increasing gas component in the production stream, multiplied times 600%, makes for huge EUR’s. I contend that increasing GOR is predicted in the type curves used for reporting EUR’s. It is part of the ploy.