The EIA’s latest Drilling Productivity Report is out. Not a lot of changes since we now know that the EIA just guesses at the production for the last five months, August through December, then plugs in their estimate for the next two months, January and February. In the case of the Bakken they say December production was 1,003,578 bp/d and January and February will be 1,025,634 and 1,050,521 bp/d respectively. For Eagle Ford December production, they say, was 1,221,576 bp/d and they expect January and February production to be 1,251,617 and 1,285,224 bp/d respectively.

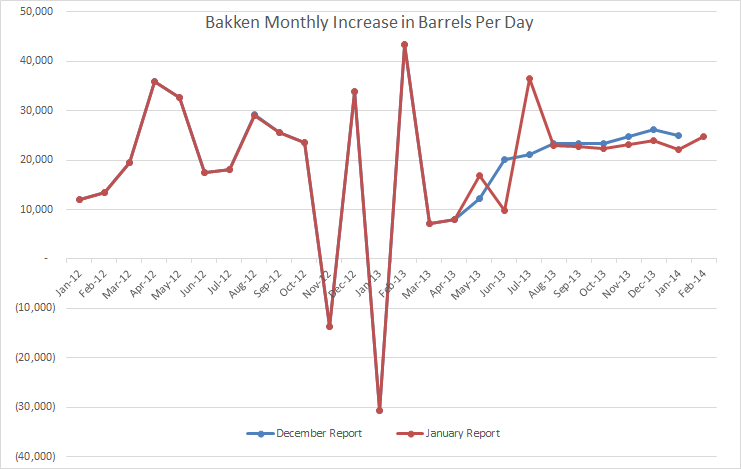

The below chart shows the Bakken production change from month to month. I have shortened the time displayed in order to better show the month to month change.

Notice the dramatic change in the January report for May, June and July. Obviously they looked at the real data and saw how different it was from what they had previously just plugged in, and made the necessary changes. They are saying that the Bakken had a really good December, slightly better than January, then things turn up again in February.

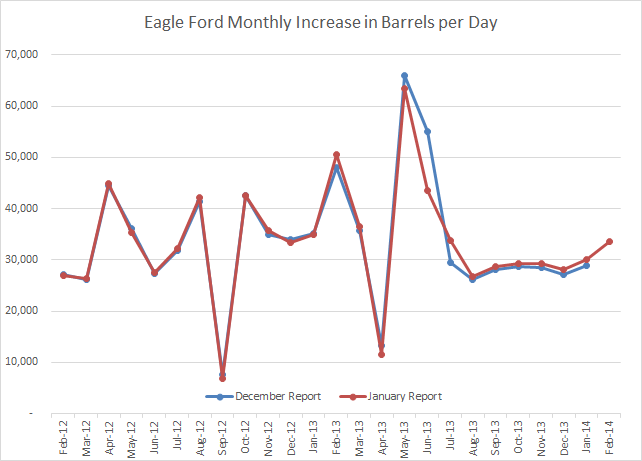

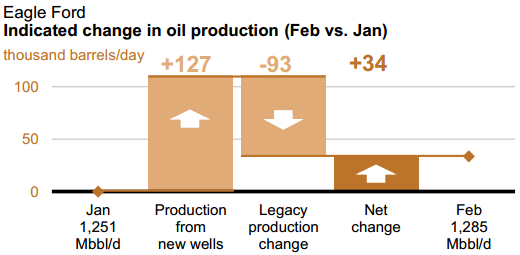

Here is the same chart for Eagle Ford.

Not such dramatic changes in the Eagle Ford production data. But notice they are expecting an upturn in January and December. We shall see.

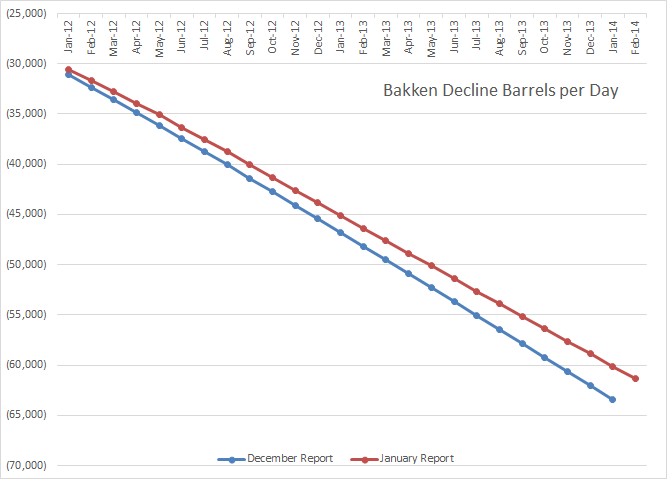

But what about the decline rate of all existing fields. Actually they give the decline amount instead of the rate. First the Bakken.

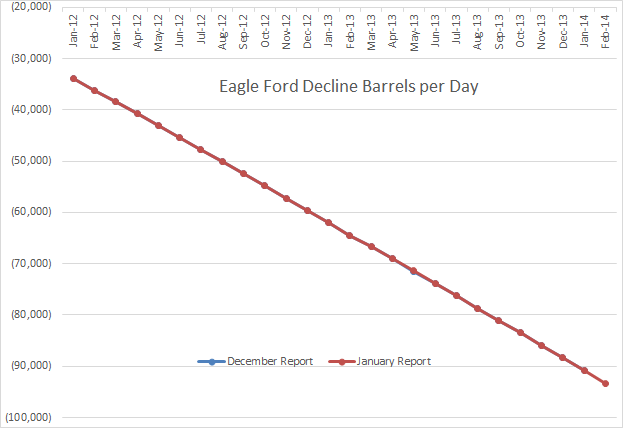

They have lowered their decline for the Bakken. They expect the Bakken to decline by 61,372 barrels per day in February. They originally had December declining by slightly more than that. But no such revisions in the Eagle Ford decline rate. The reason you don’t see the blue, or December decline rate below is because it is covered up by the January data.

There were virtually no changes is the amount they think Eagle Ford is declining. They say that, in February, existing wells in Eagle ford will decline by a whopping 93,374 barrels per day.

They expect 127 kb/d from new wells, a decline of 93 kb/d from old wells giving them an increase of 34 kb/d.

I have been getting emails every day for the last two weeks or so from Energy and Capital telling us about a miracle out in West Texas. They are pumping their newsletter “Oil and Gas Trader”, only $799 for a one year’s subscription, recently marked down from $999. And with a one year’s sbscription you will get a special report on the West Texas “Petroplex”. (That is also the name of an oil company based in Baton Rouge, La. but don’t let that confuse you.) This report is all about the source rock of West Texas not that oil company.

The below snippet is from my email but the snipping tool captured only the image, not the links. So the links don’t work but this one does: Oil and Gas Game Changer

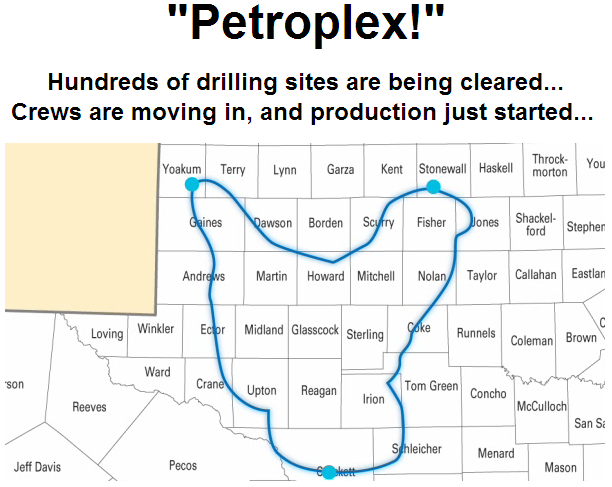

This is what they are talking about.

They claim, in this report that the Bakken and Eagle Ford will soon be producing more oil than Libya, Algeria, Kuwait, Nigeria and Venezuela combined. I did the math and that comes to over 9 million barrels per day. Really now? But this new source rock play will produce as much as 100 Eagle Fords or 140 Bakkens. Now folks that is a lot of oil.

Here is the logic. The Bakken and Eagle Ford is “Source Rock”, not reservoir rock. Source rock is where alga becomes kerogen and the kerogen, after many millions of years at coffee pot temperatures, is cooked into oil. But if the source rock is too tight the hydrocarbon strings cannot escape. So the oil companies fracture the rock allowing some of the hydrocarbon strings, or polymers, to escape. And even then only the very shortest polymer strings can escape.

What they get from the Bakken and Eagle Ford is natural gas and very light oil, it could almost be considered as condensate. But in the source rock that supplied West Texas oil fields is not tight at all. It is so porous that even the very long polymer strings could escape. Even the stuff that they make axel grease and asphalt from escaped, moved upward being replaced by water, until it hit rock so dense that it could go no further.

All source rocks are not equal. They are saying: “The Bakken and Eagle Ford is source rock, and there is a lot more source rock underneath the Petroplex, therefore we could get a lot more oil from there.” I really don’t think it works that way.

The Bakken and Eagle source rock is extremely tight while the Petroplex source rock is extremely porous and has already given up most of its oil. Now my question is this, will fracking the source rock where all that West Texas oil originally came from produce more oil than 100 Eagle Fords? I would like to hear from some oil people on this. Or perhaps a better question would be: Will fracking this extremely porous and already drained source rock produce even enough oil to pay for the effort of drilling and fracking?

Notice. The OPEC Monthly Oil Market Report will be out Thursday the 16th with the December production data for all OPEC countries. I will have a new post then along with an update of all the OPEC Charts.

Well now… I just listened to some of that sales pitch and I will say this for the guy making it.

He gets a couple of things right. He notes for instance that the Ghawar field is old and declining fast, and that Hubbert correctly predicted the American peak and a fewer other things.

Having said this for him just to bend over backwards to be fair, he sounds to me like a highly skilled classic come on artist. ‘Nuf said!

It occurs to me that anybody with a lick of sense and high school level level understanding of math would only need one serious look at the figures you have published recently to understand that the Bakken and the Eagle Ford aren’t going to be able to outrun the Red Queen too much longer because there aren’t enough available drilling rigs in the world to stay ahead of the gut wrenching decline rates.

I’d suggest that the issue is natural permeability.

My understanding is western Texas had pretty darn good permeability and that’s why conventional production was so good. So . . . a lot was recovered. I guess the theory somehow is that by revisiting these fields that had what, 30% recovery, and doing a permeability augmentation they can get 60% recovery.

This would be so in all fields globally. What doesn’t speak to me is how they would know what natural permeability pathways already drained. IOW, how does one know what direction to snake the horizontal drill? You could buy a 10 million dollar well that snakes into empty rock. There may be full rock there in which this could work, but is the imagery really good enough to know which is which?

I guess the theory somehow is that by revisiting these fields that had what, 30% recovery, and doing a permeability augmentation they can get 60% recovery.

No, that is not what they are talking about. This is not EOR from the old fields. They are talking about going way, way below the old fields into the original source rock. The oil was driven out of the source rock millions of years ago… by water. That is what they should find in the source rock… water.

This is a totally different animal than the Bakken or Eagle Ford. That source rock is so tight, (low permeability), that water cannot get in and the oil cannot get out, so they blow it apart. The Petroplex source rock has very high permeability. There gravity allowed the water to get in and the oil moved upward.

You’re right. Their text does say “under”. So they’re not revisiting the original fields to frack out what could not flow before. My bad.

Also fracking would gain you very little in already porous reservoir rock. You might get a few extra barrels but likely not enough to pay for the expense of fracking. And frackiing in a water injection field would cost a company far more than they could gain. Fractures allow a direct path to the well bore for the water to flow. Pressurized water takes the path of least resistance so instead of sweeping the oil to the well, fractures allow the water to pass directly to the well.

Ron – That’s so true. The reservoirs in Permian Basin (both source rock and non-source rock) have been the poster child of EOR. As pointed out fracturing a permeable reservoir is the last thing you want to do either early on or late in life. In fact one of the great failure points in water flooding occurs when the porosity and permeability is so high that the injected water bypasses the residual oil and “channels” directly from the injector to the producer. Inducing a fracture between an injectors to a producer would in effect create a super channel.

As far as source rocks being potential producing reservoirs I’ve never seen the complete tally but there are a great many source rocks in the Gulf Coast Basin alone. The Eagle Ford Shale represents just a very small percentage of the total volume. There are a total of 12 different source rocks in Gulf coast Texas alone with the EFS representing a rather small volume of the total. In fact many of those shale source rocks sit underneath leases current being developed in the EFS. When have you heard of the great Taylor Shale play? No you haven’t: though a significant source rock no one has figured out how to get any production out of it. The vast majority of those shale source rocks would be unfamiliar to almost everyone but a Gulf Coast geologist because they have yet to become big plays. Such as the Jackson, Wilcox, Taylor, Sligo, Bossier, etc., etc. Shales. Yet those are the source rocks that have created the hundreds of billions of bbls of oil produced from the region. And these represent just the Gulf Coast Basin…the Permian Basin contains a whole different population of source rocks. Same true for the various basins of the Rocky Mountains, west coast, mid-continent, Appalachian and Gulf of Mexico. The only reason the EFS stands out is its rather unique nature among source rocks to have some production potential. Which is why 80%+ of all unconventional reservoir production in the US comes from just two formations (Bakken and EFS) despite there being many dozens of shales that have acted as source rocks.

Here’s some more documented meat to chew on about sourfing and migration of oil. From http://www.geoexpro.com/article/Gulf_of_Mexico/958e8ee8.aspx

The petroleum system elements

Source Rocks

Many petroleum basins rely on only one or two principal source rock intervals to generate most of their contained hydrocarbons. The GOM contains multiple, thick, source rock intervals, including Upper Jurassic limestone and marl, Lower Cretaceous marl, lower Upper Cretaceous marl and mudstone and lower Tertiary mudstone. Cumulatively, these source rocks are dispersed throughout most of the basin’s area. Importantly, the bulk of the source rocks lie within the lower portion of the basin fill. The widespread accumulation of organic-rich sediment at multiple stratigraphic levels reflects the beneficial interplay of basin isolation and restricted circulation, tropical paleoclimate, development of a deep, often stratified and/or sediment-starved marine basin center, and high rates of terrestrial organic matter input.

Hydrocarbon Generation

The long depositional history and large size of the GOM has resulted in a great diversity of regional burial histories. Mesozoic source rocks of the landward basin margin were buried slowly by younger Cretaceous and relatively thin early Cenozoic sediments (Fig. 3); here petroleum generation progressed slowly in response to burial duration. Basinward, beneath the modern coastal plain and shelf, rapid burial of source rocks led to generation in the early to middle Cenozoic. Beneath the late Cenozoic outer shelf and continental slope depocenters, deep burial brought source rocks into oil and gas kitchens only within the last few million years. The overall pattern of basinward advancing deposition illustrated in the regional dip cross section (Fig. 3) created successive waves of maturation of source rocks. The result was multiple petroleum systems whose peak generation times spanned the 65 million years of the Cenozoic and continue today.

Migration

It has long been recognized that the principal GOM source rocks lie far beneath the center of mass of reservoired hydrocarbons. Large-scale upward migration of thousands of meters is commonly required, especially in the Cenozoic reservoirs that contain the bulk of the oil and gas. Here, structures created by the long history of gravity tectonics acting on the salt and overpressured mudstone have played a critical role. Faults, salt bodies, and welds created pathways that extend through source rocks many kilometers into overlying Cenozoic sediments . The long history of formation and reactivation of these growth structures provided condiuts that were ready and available when pulses of peak generation provided a charge of movable hydrocarbons.

Hey Rock Man,

Good to hear your voice again! Hope your well.

Rockman,

As always thank you for your insightful input. So in layman’s terms do you think the Petroplex has much potential? Or is it all hype?

Hey Rock Man,

Is that a name change from the old Rockman, or just fat finger syndrome? Good to see you have dropped into Ron’s site to throw in your insights.

I was over your way for a few weeks in July, Doing a few courses in LaPlace, Took the family made a holiday of it, and got to educate my god damn Yankee wife that Coonass is not a derogative word. You boys down south need to educate those Yankees better than that, lol.

I hope you hang around for awhile.

According to the EIA 2014 energy outlook by 2021 51% of US oil production will be coming from shale/tight oil (http://www.eia.gov/forecasts/aeo/er/pdf/0383er%282014%29.pdf):

In the AEO2014 Reference case, tight oil production increases from 2.3 MMbbl/d in 2012

(35% of total U.S. crude oil production) to 4.8 MMbbl/d in 2021 (51% of the total). As in

AEO2013 , tight oil production declines in AEO2014 after 2021, as more development moves into less-productive areas.

Meanwhile David Hughes in his November 19th presentation at the First Energy conference (http://legacy.firstenergy.com/UserFiles/HUGHES%20First%20Energy%20Nov%2019%202013.pdf) calculated the Bakken and Eagleford fields decline rates at 44% and 34% respectively.

In light of the above, if we were to apply those decline rates to US production by 2021, that estimated 4.8m barrels in production will be declining by a whopping 1.92m barrels at a 40% field decline rate. This is not counting the decline from the ex-shale production which if pegged at 10% would give us a total decline of 2.4m barrels per year. This is as much as the production of Kuwait or Venezuela! Or as much as the current production of the Bakken & Eagle Ford combined!. Yet, the EIA is only expecting a gentle total production decline between 2021 and 2040.

Where is the resource that will provide that oil abundance? Especially when we consider that 70% of shale production is coming from only two plays the Eagle Ford and the Bakken. Furthermore, 75% of the Eagle Ford production is coming from only 5 counties and 85% of Bakken production is coming from only 4 counties. Peak oil is being masked by a handful of counties that will soon run out of steam (at 2016 or 2017 latest). The EIA is truly living in fantasy land and dragging the world with it.

Regards,

Nawar

Nawar,

Today, the world is run by Governments & Central Banks that are completely FOS – Full of Sh*t. While that is a blunt statement, there is no better description. Because the global financial system is based on the greatest Ponzi scheme in history, the only thing keeping it alive is the notion that world oil production will continue to grow.

Why? Because…ENERGY = MONEY

Or rather the correct term is Fiat Currency. We don’t have money today. We have fancy pieces of monopoly paper that cost approximately 10 cents to produce each bill. The new $100 bill cost a bit more at 12.5 cents.

According to the World Gold Council the “All In Cost” for gold is now $1,250 an ounce. So, while the U.S. Treasury prints off $1,300 Dollars in $100 bills at a total cost of $1.63, the gold industry produces an ounce of gold.

The U.S. Dollar is a debt instrument as it has the words… FEDERAL RESERVE NOTE printed at the top. Furthermore, the U.S. Dollar is now backed by the total U.S. Treasury debt which stands at $17 trillion plus.

So as the Western Central Banks with the FED at the helm continue to print money, purchase Treasuries-Bonds and prop up the broader stock markets with continued market rigging through the Exchange Stabilization Fund, the EAST continues to exchange worthless Federal Reserve Notes for physical gold.

Not only did the Chinese import 2,200 metric tons of gold in 2013, each bar was assayed and then melted into new 1 kilogram bars with the Chinese Govt. stamp. The West has always traded the typical 400 oz gold bars between countries, but now as China consumes nearly all global gold production in one year, they are not letting any out of their country.

Again, the only way to keep the Dollar alive is to bamboozle the world into believing that the U.S. has all this untapped oil. Without a growing oil supply, the whole Fiat Monetary system comes crashing down.

I imagine when the Chinese acquire enough gold to their “Official Reserves” they are going to pull the plug on the U.S. Dollar. Not only have the Chinese purchased the largest Pig Farm in the United States, they also bought JP Morgan’s 6 commercial banking building complex in Manhattan… with the largest private gold vault in the world.

steve

Nawar,

As Toolpush pointed out…

To think that half of U.S. oil production will come from shales by the end of the decade (assuming that unrealistic scenario were true) should give us all pause given how much less diesel these Barely Crude Oil (BCO) grades yield.

The heavy lifting in our economies is done with diesel. Substitution will be difficult.

But Steve isn’t all money an abstraction? I agree that ENERGY = MONEY, but it doesn’t follow from that that gold = money. I have witnessed the transformation of energy [vast amounts of Diesel] into gold at a huge open cast mine in Central Otago, but that doesn’t mean that the resulting gold will ever power a truck again. Gold’s value is just as notional as a fiat currency surely. I have also witnessed the transformation of zillions of electrons into aluminium at a smelter, aluminium ingots are indeed but congealed electricity. Should we then back our currency with aluminium?

Aluminium might not be a bad idea really. maybe not thinking in anyones current lifetime, but in the long run once cheap electricity is gone the aluminium supply will likely be recycled and prized for a very long time. Making new aluminium will stop being profitable for a time line that is beyond my own powers of imagination.

Why will cheap electricity go? Renewables drive the marginal price to zero [though this brings its own problems of course]. Cheap oil has gone/is going; the electric age is just beginning.

The smelter I mentioned, at Bluff, NZ, is entirely powered by Hydro. Hydro that now delivers a more certain and constant flow of energy because it’s use is balanced by a growing portfolio of wind farms, enabling the operator to conserve water when wind is delivering power. And this is a windy [and pluvial] country, the wind turbines here are both unsubsidised and deliver at the top of the curve for land based systems globally.

Wanna see how we are actually selling windpower to the good ol’ USA?:

http://transportblog.co.nz/2013/02/05/magnetic-south-lessons-from-antarctica/

Patrick,

The idea that all money is an abstraction is one that many seem to believe. However, the Chinese would not be buying gold hand over fist if it was one of many money abstractions. Gold is the King of monetary metals.

The reason why gold and silver have been used as money for thousands of years is due to the fact that they store ECONOMIC ENERGY. Of course the gold does not give you back energy, but it stores ECONOMIC ENERGY in many forms that can be traded.

Analysts, especially many of the clowns on MSM call gold a barbarous Relic. They say that gold isn’t needed any more. If that is true why are we still eating the Barbarous relic called BREAD or cleaning with BROOMS. These too were used during the Ancient Roman times.

I am not going to get into the details of why gold is the king monetary metal because it takes a great deal of effort to produce the data. Furthermore, most people have their minds made up… so I don’t try to change them. I just like to share the information and news.

There is no secret why the Chinese and Russians have increased their domestic gold production significantly in the past several decades.

Annual Production figures 2013

1) China = 430 metric tons

2) Australia = 265 metric tons

3) Russia = 234 metric tons

4) USA = 230 metric tons

Again, the Elite Bankers know that Gold is the King monetary metal. They use Fiat Money to steal wealth from the public while the public is asleep by inflating the money supply. Gold and Silver make it harder for them to do so.

Kind of Ironic. The public actually believes that money can be anything so they unknowingly allow the Banking Elite to rob them of their hard earned money. This is nothing new… been going on for thousands of years.

steve

This is nothing new… been going on for thousands of years.

… and throughout most of that time sovereign currencies were minted with gold and silver.

It isn’t the volume of reserves (money or energy) that counts but the flow (energy production or spending/investment)

The trouble is whether money is spent or invested wisely, or whether energy is consumed efficiently for a useful purpose or squandered wastefully.

At the moment we choose to wastefully squander both capital and energy instead of using it to transition to a Post Carbon economy. And then all the gold in the world won’t fix the problems we are creating for ourselves.

You already see copper and aluminum becoming a sort-of currency, as new-age copper and aluminum thieves dismantle our power, air conditioning, and plumbing infrastructure whenever possible for the scrap value of the copper and aluminum inside.

Ron,

One small typo:

They had originally they had December declining

Keep up the good work!

I’d like to hear more about the other LTO formations. Niobarra etc.

ken.

Shell pulls back from North Sea as part of $15bn divestment drive

By Guy Chazan, Financial Times, January 14, 2014 1:05 pm

you are confusing increase with acceleration (top graph). all the months are over zero, thus increases.